NONPROFIT HEALTH INSURERS:

|

|

|

- Randell Carr

- 8 years ago

- Views:

Transcription

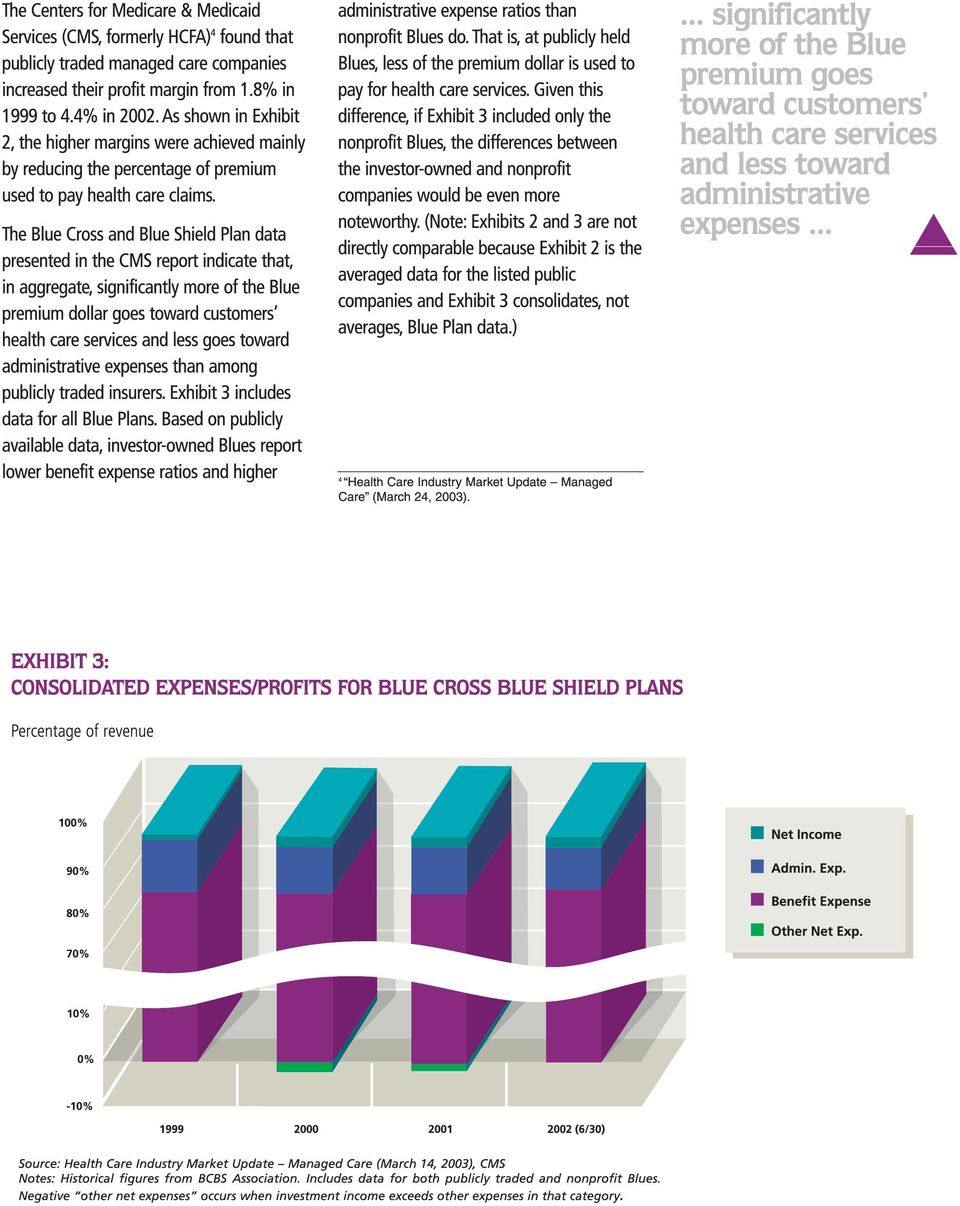

1 EXECUTIVE SUMMARY For several years,wall Street investment firms have campaigned for conversion of not-for-profit health insurers to investor ownership, arguing that an infusion of equity capital is critical to insurers survival. However, closer examination of the financial performance and capital position of not-for-profit health plans shows that: NONPROFIT HEALTH INSURERS: The Financial Story Wall Street Doesn t Tell. Susan R. Barrish The lower operating margins reported by not-for-profit health very likely reflect the organizations corporate missions to serve their communities by minimizing the cost of coverage and their ability to invest all gains back into the company for the future benefit of their customers.their investor-owned counterparts must generate higher margins to give shareholders a return on their investment. Compared with investor-owned insurers, not-for-profit health plans use a significantly higher percentage of the customers premium dollar to pay health care claims.a lower percentage goes for administrative expenses. Over the past ten years, not-for-profit health plans have succeeded in using operational and investment gains to build and retain a strong capital position - stronger than that of investor-owned companies - while investing heavily in infrastructure, product development, and market growth.

2 nonprofit HEALTH INSURERS: THE FINANCIAL STORY WALL STREET DOESN T TELL INTRODUCTION Wall Street... has been championing health carrier conversion to investor ownership both as a source of fees for themselves and as a requirement for company survival when you go beyond Wall Street reports, you find that nonprofit health insurers continue to be a robust, vital component of the health care financing industry. For decades, community-based nonprofit organizations 1 were the chief source of health insurance coverage.the recent wave of highly publicized initial public offerings of health insurers, including a number of Blue Cross and Blue Shield Plans, has led some to conclude that the nonprofit health insurer is an endangered species on the brink of extinction. Wall Street (and investor-owned companies) has been championing health carrier conversion to investor ownership both as a source of fees for themselves and as a requirement for company survival, bringing access to capital for investments in technology and market growth, an avenue to economies of scale, and a bottom-line orientation. However,when you go beyond Wall Street reports, you find that nonprofit health insurers continue to be a robust, vital component of the health care financing industry.these companies do not necessarily require equity capital to fund the future.their investments in service delivery, product development, and growth can continue to be funded through a combination of gains from operations and investment portfolios, accumulated reserves, access to alternative capital sources, and intercompany alliances that share development and/or operational costs. This paper offers an overview of the financial position and performance of nonprofit health plans. It presents related issues to consider by organizations contemplating conversion to investor ownership and by regulators who have to approve the conversion. 1 In this paper, the terms not-for-profit and nonprofit include all non-investor-owned organizations, such as mutual insurance companies.

3 EXHIBIT 1: NET MARGIN AS A PERCENTAGE OF REVENUE FOR NONPROFIT BLUES, PUBLIC BLUES AND PUBLIC NONBLUES Source: PULSE, published by Sherlock Company (2000 from June 2002 issue, from June 2003 issue) STRONG PERFORMANCE IS? Recent investment analyst reports on the health insurance industry have taken a consistent position: nonprofit health plans under-perform compared with publicly held ones, and without access to the capital markets, nonprofits will lack sufficient resources to make the critical investments in technology and product development necessary to remain competitive. However, these reports tend to rely on a limited set of financial statistics, such as earnings per share, net margins,medical loss ratio, and market growth. They overlook the effects of a corporation s market and financial position, strategy, and business philosophy on its operating results. When the analysis is broadened to relate quarterly/annual operating results with corporate strategy and mission, it appears that many nonprofit health insurers are well positioned to fund the accomplishment of long-term business plans, including necessary infrastructure investments, without requiring access to the capital markets. Historically, the health insurance industry was considered a low-margin business.a health insurer that averaged 1-2% annual gain over time was considered a good performer. Margins have grown since the late 1990s, fueled by the rising number of publicly traded insurers (as well as companies planning to convert) and extraordinary investment portfolio performance. Over the past three years, investor-owned, or public, health insurers have reported increasingly larger net margins. As Exhibit 1 shows, by December 31, 2002, the publicly traded health plans tracked by Sherlock Company reported an average net margin of 3.7%, almost double the 2.0% reported by nonprofit Blue Cross and Blue Shield Plans many nonprofit health insurers are well-positioned to fund... long-term business plans... without requiring access to the capital markets. 2 Blue Cross and Blue Shield system data are used as a proxy for the nonprofit health plan segment, in view of the size of the system (42 enterprises covering the United States and Puerto Rico, generating annual revenue of $163 billion in 2002, and serving 85 million customers) and the availability of aggregate, systemwide data.

4

5

6 nonprofit HEALTH INSURERS: THE FINANCIAL STORY WALL STREET DOESN T TELL The higher a company s riskbased capital ratio, the more financial flexibility it has to invest in new initiatives and technologies and in customer growth.... as a not-for-profit company does not distribute earnings to stockholders, it retains all financial gains ( profit ) for future internal investments. The adequacy of a company s operating margin should also be analyzed in light of the entity s capital position, a perspective typically neglected by Wall Street when evaluating health insurers. In 1998 the National Association of Insurance Commissioners (NAIC) adopted a risk-based capital formula for managed care organizations, MCO-RBC. This formula measures the adequacy of a health plan s capital position in relation to the risks associated with issuing insurance contracts, investment portfolio, and other business contingencies.the higher a company s riskbased capital ratio, the more financial flexibility it has to invest in new initiatives and technologies and in customer growth. It is also better able to weather financial losses associated with unfavorable underwriting results (financial losses incurred when claims and related administrative expenses exceed premiums collected). The NAIC has established a minimum RBC level that triggers regulatory action: 200% of the Authorized Control Level, or ACL, is the first step in an early warning process; at 70% of ACL, state regulators are mandated to assume control of the entity. However, the formula does not establish a target or a maximum level of reserves.an individual health plan must determine how much capital it should accumulate above regulatory action levels to ensure that its long-term business strategy can be supported. For Blue Plans, unlike the rest of the industry, the capital requirement generated by the MCO-RBC formula was not a new concept 5.The Blue Cross and Blue Shield Association had adopted a similar approach for all its domestic licensees in the early 1990s that encouraged Blue Plans to be well capitalized. By year end 2002,as shown in Exhibit 4, the average Blue Plan risk-based capital ratio was 623%; the average for nonprofit Blue Plans was 17% higher,at 727%. These figures indicate that most 6 of the Blue nonprofits have been quite successful in implementing a capital-building and retention strategy - without access to the capital market - while adding 3.8 million new customers,a 7.7% increase in three years 7, and making significant infrastructure and product investments critical to maintaining market leadership. The higher RBC position may also partially explain the lower operating margins reported by nonprofits.a strong capital position means less need to generate capital through operations, resulting in less margin built into premium levels. 5 The Blue Cross and Blue Shield Association s minimum licensure requirement is 200%. 6 RBC-MCO ratios for not-for-profit Blue Plans ranged from 257% % as of December 31, Per BCBS Association enrollment reports.

adopted a risk-based capital formula for managed care organizations, MCO-RBC.")

7 SUMMARY When considering the appropriateness of converting a nonprofit health insurer to investor ownership, it is critical that all decision makers develop a full understanding of a health plan s financial performance and position beyond just operating-margin statistics.a thorough review includes answering the following questions: How does the company s actual performance (e.g., underwriting margin, net margin, premium levels, administrative and medical loss ratios) compare with forecasted performance? Does the company have the discipline to achieve its forecast? What is the company s mission, and how well aligned are its business practices, pricing policies, and performance results to ensure that the mission is achieved? What changes in pricing policies, product design, and business practices would be required to increase operating margins? How would key stakeholders (e.g., customers, potential customers, the medical and hospital communities, state regulators and legislators, competitors) respond? What is the company s MCO-RBC position? Will the company be able to generate sufficient capital from operations and its investment portfolio to fund the future? If not, what are the options to reduce the cost of the strategy and/or raise the capital shortfall?... it is critical that all decision makers develop a full understanding of a health plan s financial performance and position beyond just operating margin statistics. EXHIBIT 4: YEAR-END MCO-RBC RATIOS RBC percentage Source: BCBS Association * Includes data for all nonprofit and mutual plans that were not pursuing conversion as of year end 2002 and permit BCBSA to publish results.

8 SUSAN R. BARRISH Ms. Barrish is a consultant to the health insurance industry, advising executive management on the development and execution of strategic initiatives. Previously she was a Senior Vice President at the Blue Cross and Blue Shield Association, the central coordinating body for Blue Cross Blue Shield Plans. As the architect of the Association s brand protection program, she guided the establishment and implementation of consistent, high standards for the 200 independent Blue Cross Blue Shield licensees that generate annual revenue in excess of $162 billion and serve 85 million customers. She also led the Association s financial, actuarial and federal tax services and related policy and advocacy efforts at the National Association of Insurance Commissioners (NAIC), the IRS and the U.S. Treasury Department. Prior to joining the Association, Susan was in hospital financial management at several large, urban teaching hospitals. Ms. Barrish holds a Bachelor of Science in Accounting from American International College (Springfield, Massachusetts) and a Masters of Business Administration from Cornell University (Ithaca, New York). Learn more about the Alliance. Visit us at: Or by at: info@nonprofithealthcare.org Alliance for Advancing Nonprofit HealthCare 165 Court Street Rochester, NY (877)

The Role of Nonprofit Healthcare Organizations in Controlling Costs and Improving Quality for Retirees

The Role of Nonprofit Healthcare Organizations in Controlling Costs and Improving Quality for Retirees Employee Benefits Research Institute Education and Research Fund Policy Forum # 56 Washington, DC

The Role of Nonprofit Healthcare Organizations in Controlling Costs and Improving Quality for Retirees Employee Benefits Research Institute Education and Research Fund Policy Forum # 56 Washington, DC

From the Publisher* Costs, Commitment and Locality: A Comparison of For-Profit and Not-for-Profit Health Plans. Treo Solutions

From the Publisher* Treo Solutions Costs, Commitment and Locality: A Comparison of For-Profit and Not-for-Profit Health Plans Following on the heels of the first national study demonstrating differences

From the Publisher* Treo Solutions Costs, Commitment and Locality: A Comparison of For-Profit and Not-for-Profit Health Plans Following on the heels of the first national study demonstrating differences

Webinar Transcript: Key Components of the Health Insurance Rating Process.

Webinar Transcript: Key Components of the Health Insurance Rating Process. Ken Frino Group Vice President, JOHN WEBER: I m John Weber with the A.M. Best Company. Welcome to our webinar, Key Components

Webinar Transcript: Key Components of the Health Insurance Rating Process. Ken Frino Group Vice President, JOHN WEBER: I m John Weber with the A.M. Best Company. Welcome to our webinar, Key Components

Five Best Practice Strategies for Maintaining Excellence in Workers Compensation Self-Insured Groups

Five Best Practice Strategies for Maintaining Excellence in Workers Compensation Self-Insured Groups Safety National is the market leader for providing excess workers compensation coverage for self-insured

Five Best Practice Strategies for Maintaining Excellence in Workers Compensation Self-Insured Groups Safety National is the market leader for providing excess workers compensation coverage for self-insured

How To Control Surplus In Health Insurance

How Much Is Too Much: Have Nonprofit Blue Cross Blue Shield Plans Amassed Excessive Amounts of Surplus? EXECUTIVE SUMMARY In the last decade, nonprofit Blue Cross and Blue Shield (BCBS) plans have set

How Much Is Too Much: Have Nonprofit Blue Cross Blue Shield Plans Amassed Excessive Amounts of Surplus? EXECUTIVE SUMMARY In the last decade, nonprofit Blue Cross and Blue Shield (BCBS) plans have set

Legislation-in-Brief The Standard Valuation Law and Principle-based Reserves

1 Legislation-in-Brief The Standard Valuation Law and Principle-based Reserves The American Academy of Actuaries is an 18,000+ member professional association whose mission is to serve the public and the

1 Legislation-in-Brief The Standard Valuation Law and Principle-based Reserves The American Academy of Actuaries is an 18,000+ member professional association whose mission is to serve the public and the

MML Bay State Life Insurance Company Management s Discussion and Analysis Of the 2005 Financial Condition and Results of Operations

MML Bay State Life Insurance Company Management s Discussion and Analysis Of the 2005 Financial Condition and Results of Operations General Management s Discussion and Analysis of Financial Condition and

MML Bay State Life Insurance Company Management s Discussion and Analysis Of the 2005 Financial Condition and Results of Operations General Management s Discussion and Analysis of Financial Condition and

FOCUS PROASSURANCE 2005 ANNUAL REPORT

FOCUS PROASSURANCE 2005 ANNUAL REPORT THE FOCUS OF PROASSURANCE CORPORATION We are a specialty insurer focused on writing medical professional liability insurance and developing insurance solutions which

FOCUS PROASSURANCE 2005 ANNUAL REPORT THE FOCUS OF PROASSURANCE CORPORATION We are a specialty insurer focused on writing medical professional liability insurance and developing insurance solutions which

Department of State. Bureau of Securities Regulation

Department of State Bureau of Securities Regulation RECOMMENDATIONS CONCERNING THE LIMITATION OF RESERVES AND THE LIMITATION ON ADMINISTRATIVE EXPENSES AS A PERCENT AGE OF CLAIMS OF POOLED RISK MANAGEMENT

Department of State Bureau of Securities Regulation RECOMMENDATIONS CONCERNING THE LIMITATION OF RESERVES AND THE LIMITATION ON ADMINISTRATIVE EXPENSES AS A PERCENT AGE OF CLAIMS OF POOLED RISK MANAGEMENT

Looking back on 2014, we:

Aetna Inc. Fourth Quarter 2014 Earnings Conference Call Hartford, CT Tuesday February 3, 2015, 8:00 A.M. ET Prepared Remarks Tom Cowhey, Vice President Investor Relations Good morning and thank you for

Aetna Inc. Fourth Quarter 2014 Earnings Conference Call Hartford, CT Tuesday February 3, 2015, 8:00 A.M. ET Prepared Remarks Tom Cowhey, Vice President Investor Relations Good morning and thank you for

Financial Review. 16 Selected Financial Data 18 Management s Discussion and Analysis of Financial Condition and Results of Operations

2011 Financial Review 16 Selected Financial Data 18 Management s Discussion and Analysis of Financial Condition and Results of Operations 82 Quantitative and Qualitative Disclosures About Market Risk 90

2011 Financial Review 16 Selected Financial Data 18 Management s Discussion and Analysis of Financial Condition and Results of Operations 82 Quantitative and Qualitative Disclosures About Market Risk 90

The Medical Malpractice Industry - Highlights and Insights*

The Medical Malpractice Industry - Highlights and Insights* By Robert L. Sanders, FCAS, MAAA and Kevin J. Atinsky, FCAS, MAAA Milliman As has been extensively chronicled, the marketplace for medical malpractice

The Medical Malpractice Industry - Highlights and Insights* By Robert L. Sanders, FCAS, MAAA and Kevin J. Atinsky, FCAS, MAAA Milliman As has been extensively chronicled, the marketplace for medical malpractice

Group to Individual Trend - How Health Plans Can Optimize Retention

Get Smart. Get Covered. Get Going. Group to Individual Trend - How Health Plans Can Optimize Retention Wellthie s Retail Ready White Paper Series What is the group to individual trend? Small group employers

Get Smart. Get Covered. Get Going. Group to Individual Trend - How Health Plans Can Optimize Retention Wellthie s Retail Ready White Paper Series What is the group to individual trend? Small group employers

Information. Canada s Life and Health Insurers. Canada s Financial Services Sector. Overview

Information Canada s Life and Health Insurers Canada s Financial Services Sector September 2002 Overview Canada s life and health insurance industry comprises 120 firms, down from 163 companies in 1990,

Information Canada s Life and Health Insurers Canada s Financial Services Sector September 2002 Overview Canada s life and health insurance industry comprises 120 firms, down from 163 companies in 1990,

Credit & Risk Management. Lawrence Marsiello Vice Chairman and Chief Lending Officer

Credit & Risk Management Lawrence Marsiello Vice Chairman and Chief Lending Officer 2006 Progress and 2007 Expectations Well-positioned to perform through the cycle Robust and consistent credit grading

Credit & Risk Management Lawrence Marsiello Vice Chairman and Chief Lending Officer 2006 Progress and 2007 Expectations Well-positioned to perform through the cycle Robust and consistent credit grading

Plan to Transfer. to Independent Trust. August 11, 2008

Plan to Transfer Conseco Senior Health Insurance Company to Independent Trust August 11, 2008 Forward Looking Statements Cautionary Statement Regarding Forward-Looking Statements. Our statements, trend

Plan to Transfer Conseco Senior Health Insurance Company to Independent Trust August 11, 2008 Forward Looking Statements Cautionary Statement Regarding Forward-Looking Statements. Our statements, trend

Massachusetts Dukakis Play or Pay Plan

6 Massachusetts A proposed amendment to the Massachusetts state constitution, which would mandate that lawmakers provide medical insurance to all residents of the state, is the final stage in what critics

6 Massachusetts A proposed amendment to the Massachusetts state constitution, which would mandate that lawmakers provide medical insurance to all residents of the state, is the final stage in what critics

Request for Comment #1 How common is the use of stop-loss insurance in connection with self-insured arrangements?

U.S. Department of Labor Office of Health Plan Standards and Compliance Assistance Employee Benefits Security Administration Room N-5653 200 Constitution Avenue, NW Washington, DC 20210 Re: Request for

U.S. Department of Labor Office of Health Plan Standards and Compliance Assistance Employee Benefits Security Administration Room N-5653 200 Constitution Avenue, NW Washington, DC 20210 Re: Request for

Investment in Life Settlements: Certainty in Uncertain Times

Investment in Life Settlements: Certainty in Uncertain Times November 30, 2010 by J. Mark Goode Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent

Investment in Life Settlements: Certainty in Uncertain Times November 30, 2010 by J. Mark Goode Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent

Life Insurance Corporation (Singapore)Pte Ltd UEN 201210695E MANAGEMENT REPORT 31/12/2014

Pte Ltd UEN 201210695E MANAGEMENT REPORT 31/12/2014") Life Insurance Corporation (Singapore)Pte Ltd UEN 201210695E MANAGEMENT REPORT 31/12/2014 LIFE INSURANCE CORPORATION (SINGAPORE) PTE. LTD. For the financial year from 1 January 2014 to 31 December 2014

Life Insurance Corporation (Singapore)Pte Ltd UEN 201210695E MANAGEMENT REPORT 31/12/2014 LIFE INSURANCE CORPORATION (SINGAPORE) PTE. LTD. For the financial year from 1 January 2014 to 31 December 2014

2014-15 Property and Liability Insurance Program

A&I 12/18/15 2014-15 Property and Liability Insurance Program The Risk Management department coordinates the University s comprehensive risk financing program which includes the purchase of commercial

A&I 12/18/15 2014-15 Property and Liability Insurance Program The Risk Management department coordinates the University s comprehensive risk financing program which includes the purchase of commercial

STANCORP FINANCIAL GROUP, INC. (Exact name of registrant as specified in its charter)

") UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. FORM 10-K ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 1999

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. FORM 10-K ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 1999

FINANCIAL REVIEW. 18 Selected Financial Data 20 Management s Discussion and Analysis of Financial Condition and Results of Operations

2012 FINANCIAL REVIEW 18 Selected Financial Data 20 Management s Discussion and Analysis of Financial Condition and Results of Operations 82 Quantitative and Qualitative Disclosures About Market Risk 88

2012 FINANCIAL REVIEW 18 Selected Financial Data 20 Management s Discussion and Analysis of Financial Condition and Results of Operations 82 Quantitative and Qualitative Disclosures About Market Risk 88

2010 Commercial Health Insurance Market:

Prepared by: FSA, MAAA 2010 Commercial Health Insurance Market: New Financial and Enrollment Data Available from the Supplemental Exhibit is among the world s largest independent actuarial and consulting

Prepared by: FSA, MAAA 2010 Commercial Health Insurance Market: New Financial and Enrollment Data Available from the Supplemental Exhibit is among the world s largest independent actuarial and consulting

Oregon Health Insurance Rates

Kate Brown, Secretary of State Gary Blackmer, Director, Audits Division Oregon Secretary of State 1 Oregon Health Insurance Rates Introduction We conducted preliminary work on the Oregon Insurance Division

Kate Brown, Secretary of State Gary Blackmer, Director, Audits Division Oregon Secretary of State 1 Oregon Health Insurance Rates Introduction We conducted preliminary work on the Oregon Insurance Division

Risk-Based Capital. Overview

Risk-Based Capital Definition: Risk-based capital (RBC) represents an amount of capital based on an assessment of risks that a company should hold to protect customers against adverse developments. Overview

Risk-Based Capital Definition: Risk-based capital (RBC) represents an amount of capital based on an assessment of risks that a company should hold to protect customers against adverse developments. Overview

Valuation Actuary Symposium September 23-24, 2013 Indianapolis, IN. 29 PD, New Health Care Receivables Exhibit. Moderator: F Kevin Russell FSA,MAAA

Valuation Actuary Symposium September 23-24, 2013 Indianapolis, IN 29 PD, New Health Care Receivables Exhibit Moderator: F Kevin Russell FSA,MAAA Presenters: Susan Lynn Mateja FSA,MAAA,FCA Session 29PD

Valuation Actuary Symposium September 23-24, 2013 Indianapolis, IN 29 PD, New Health Care Receivables Exhibit Moderator: F Kevin Russell FSA,MAAA Presenters: Susan Lynn Mateja FSA,MAAA,FCA Session 29PD

AIG Management Proposal and Reserve Strengthening February 5, 2016

AIG Management Proposal and Reserve Strengthening February 5, 2016 On January 26, AIG announced a series of strategic measures to create a leaner, more profitable and focused insurer. This new plan was

AIG Management Proposal and Reserve Strengthening February 5, 2016 On January 26, AIG announced a series of strategic measures to create a leaner, more profitable and focused insurer. This new plan was

How To Divide Life Insurance Assets Into Two Accounts

2ASSETS Assets held by life insurers back the companies life, annuity, and health liabilities. Accumulating these assets via the collection of premiums from policyholders and earnings on investments provides

2ASSETS Assets held by life insurers back the companies life, annuity, and health liabilities. Accumulating these assets via the collection of premiums from policyholders and earnings on investments provides

Organizational Structure: Vision, Mission and Values: BCBSF COMPANY FACTS

Headquarters: Jacksonville, Florida Founded: In 1944, the Florida Hospital Service Corporation, the forerunner of Blue Cross of Florida, began operations in Jacksonville with a staff of four. In 1946,

Headquarters: Jacksonville, Florida Founded: In 1944, the Florida Hospital Service Corporation, the forerunner of Blue Cross of Florida, began operations in Jacksonville with a staff of four. In 1946,

Surveying Commercial Insurance

Surveying Commercial Insurance Pricing and Profitability 2013 Q3 Update 2013 Towers Watson. All rights reserved. Now more than ever, price monitoring is key Exposure Uncertainty How are prices affected

Surveying Commercial Insurance Pricing and Profitability 2013 Q3 Update 2013 Towers Watson. All rights reserved. Now more than ever, price monitoring is key Exposure Uncertainty How are prices affected

Health Care Receivables Follow-up Study

Health Annual Statement New Exhibit 3A Health Care Receivables Follow-up Study F. Kevin Russell, FSA, MAAA Chairperson, Health Care Receivables Factors Work Group Susan Mateja, FSA, MAAA Member, Health

Health Annual Statement New Exhibit 3A Health Care Receivables Follow-up Study F. Kevin Russell, FSA, MAAA Chairperson, Health Care Receivables Factors Work Group Susan Mateja, FSA, MAAA Member, Health

Kansas Health Care Stabilization Fund General Information (As of July 1, 2014)

") Kansas Health Care Stabilization Fund General Information (As of July 1, 2014) The HCSF Board of Governors The Health Care Stabilization Fund Board of Governors is a state agency governed by an eleven

Kansas Health Care Stabilization Fund General Information (As of July 1, 2014) The HCSF Board of Governors The Health Care Stabilization Fund Board of Governors is a state agency governed by an eleven

How To Write An Insurance Profile Summary

EXHIBIT H INSURER PROFILE SUMMARY TEMPLATE Introductory Guidance An Insurer Profile Summary should be developed by the domestic state for each domestic insurer. The Insurer Profile Summary should be updated

EXHIBIT H INSURER PROFILE SUMMARY TEMPLATE Introductory Guidance An Insurer Profile Summary should be developed by the domestic state for each domestic insurer. The Insurer Profile Summary should be updated

How to Choose a Life Insurance Company *YP½PPMRK 4VSQMWIW A 2014 GUIDE THROUGH RELEVANT INDUSTRY INFORMATION

How to Choose a Life Insurance Company *YP½PPMRK 4VSQMWIW A 2014 GUIDE THROUGH RELEVANT INDUSTRY INFORMATION Because the most important people in your life will car, or computer, most people are completely

How to Choose a Life Insurance Company *YP½PPMRK 4VSQMWIW A 2014 GUIDE THROUGH RELEVANT INDUSTRY INFORMATION Because the most important people in your life will car, or computer, most people are completely

Arizona Chamber Foundation Unveils Study on the Impact of the Hidden Healthcare Tax on Businesses & Consumers

Release: March 12, 2009 Contacts: Suzanne Taylor, Executive Director, Arizona Chamber Foundation, 602-248-9172, ext. 125, staylor@azchamber.com Bridget O Gara, Vice President of Communications, Arizona

Release: March 12, 2009 Contacts: Suzanne Taylor, Executive Director, Arizona Chamber Foundation, 602-248-9172, ext. 125, staylor@azchamber.com Bridget O Gara, Vice President of Communications, Arizona

Business Value Drivers

Business Value Drivers by Kurt Havnaer, CFA, Business Analyst white paper A Series of Reports on Quality Growth Investing jenseninvestment.com Price is what you pay, value is what you get. 1 Introduction

Business Value Drivers by Kurt Havnaer, CFA, Business Analyst white paper A Series of Reports on Quality Growth Investing jenseninvestment.com Price is what you pay, value is what you get. 1 Introduction

Self Funded Health Insurance To be or not to be?

Self Funded Health Insurance To be or not to be? Janet S. Spencer A.S.A, M.A.A.A., C.P.A. Self Funded Insurance To be or not to be? BlueCross BlueShield of SC (BCBSSC) Self Funded To be or not to be? Important

Self Funded Health Insurance To be or not to be? Janet S. Spencer A.S.A, M.A.A.A., C.P.A. Self Funded Insurance To be or not to be? BlueCross BlueShield of SC (BCBSSC) Self Funded To be or not to be? Important

China Pacific Insurance (Group) Co., Ltd. Issue of 2010 Interim Results

Co., Ltd. Issue of 2010 Interim Results") China Pacific Insurance (Group) Co., Ltd. Issue of 2010 Interim Results Strong Growth of Insurance Business and Significant Increase in Operating Profit Shanghai, Hong Kong, 30 August 2010 China Pacific

China Pacific Insurance (Group) Co., Ltd. Issue of 2010 Interim Results Strong Growth of Insurance Business and Significant Increase in Operating Profit Shanghai, Hong Kong, 30 August 2010 China Pacific

Treasure Trove The Rising Role of Treasury in Accounts Payable

Treasury and Trade Solutions North America July 30, 2015 Treasure Trove The Rising Role of Treasury in Accounts Payable 2015 Citibank, N.A. All rights reserved Today s Speakers Andrew Bartolini Chief Research

Treasury and Trade Solutions North America July 30, 2015 Treasure Trove The Rising Role of Treasury in Accounts Payable 2015 Citibank, N.A. All rights reserved Today s Speakers Andrew Bartolini Chief Research

Financial ratio analysis

Financial ratio analysis A reading prepared by Pamela Peterson Drake O U T L I N E 1. Introduction 2. Liquidity ratios 3. Profitability ratios and activity ratios 4. Financial leverage ratios 5. Shareholder

Financial ratio analysis A reading prepared by Pamela Peterson Drake O U T L I N E 1. Introduction 2. Liquidity ratios 3. Profitability ratios and activity ratios 4. Financial leverage ratios 5. Shareholder

VALIDUS ANNOUNCES 2015 FULL YEAR NET INCOME OF $374.9 MILLION 2015 NET OPERATING RETURN ON AVERAGE EQUITY OF 11.3%

VALIDUS ANNOUNCES 2015 FULL YEAR NET INCOME OF $374.9 MILLION 2015 NET OPERATING RETURN ON AVERAGE EQUITY OF 11.3% BOOK VALUE PER DILUTED COMMON SHARE OF $42.33 AT DECEMBER 31, 2015 Pembroke, Bermuda,

VALIDUS ANNOUNCES 2015 FULL YEAR NET INCOME OF $374.9 MILLION 2015 NET OPERATING RETURN ON AVERAGE EQUITY OF 11.3% BOOK VALUE PER DILUTED COMMON SHARE OF $42.33 AT DECEMBER 31, 2015 Pembroke, Bermuda,

Unum s Business Rules Journey

Unum s Business Rules Journey A Case Study Oct 2012 Table of Contents u About Unum Group u BEFORE formal rule management > AFTER formal rule management u How we got here u Strategy steps to managing business

Unum s Business Rules Journey A Case Study Oct 2012 Table of Contents u About Unum Group u BEFORE formal rule management > AFTER formal rule management u How we got here u Strategy steps to managing business

The New Florida Insurance Bill SB 130

BILL: SB 130 The Florida Senate BILL ANALYSIS AND FISCAL IMPACT STATEMENT (This document is based on the provisions contained in the legislation as of the latest date listed below.) Prepared By: The Professional

BILL: SB 130 The Florida Senate BILL ANALYSIS AND FISCAL IMPACT STATEMENT (This document is based on the provisions contained in the legislation as of the latest date listed below.) Prepared By: The Professional

Transition risk: Rethinking investing for retirement By Tim Friederich, David Karim and Dr. Wolfgang Mader

Allianz Global Investors white paper series Transition risk: Rethinking investing for retirement By Tim Friederich, David Karim and Dr. Wolfgang Mader Executive summary Are millions of Americans, retirement-plan

Allianz Global Investors white paper series Transition risk: Rethinking investing for retirement By Tim Friederich, David Karim and Dr. Wolfgang Mader Executive summary Are millions of Americans, retirement-plan

(Unofficial Translation) Acquisition of Protective Life Corporation Conference Call for Institutional Investors and Analysts Q&A Summary

Acquisition of Protective Life Corporation Conference Call for Institutional Investors and Analysts Q&A Summary") (Unofficial Translation) Acquisition of Protective Life Corporation Conference Call for Institutional Investors and Analysts Q&A Summary Date: June 4, 2014 16:00-17:00 Respondent: Seiji Inagaki, Executive

(Unofficial Translation) Acquisition of Protective Life Corporation Conference Call for Institutional Investors and Analysts Q&A Summary Date: June 4, 2014 16:00-17:00 Respondent: Seiji Inagaki, Executive

The BrightScope/ICI Defined Contribution Plan Profile: A Close Look at 401(k) Plans

Plans") The BrightScope/ICI Defined Contribution Plan Profile: A Close Look at 401(k) Plans DECEMBER 2014 The BrightScope/ICI Defined Contribution Plan Profile: A Close Look at 401(k) Plans 1 THE BRIGHTSCOPE/ICI

The BrightScope/ICI Defined Contribution Plan Profile: A Close Look at 401(k) Plans DECEMBER 2014 The BrightScope/ICI Defined Contribution Plan Profile: A Close Look at 401(k) Plans 1 THE BRIGHTSCOPE/ICI

WCIRB REPORT ON THE STATE OF THE CALIFORNIA WORKERS COMPENSATION INSURANCE SYSTEM

STATE OF THE SYSTEM WCIRB REPORT ON THE STATE OF THE CALIFORNIA WORKERS COMPENSATION INSURANCE SYSTEM Introduction The workers compensation insurance system in California is over 100 years old. It provides

STATE OF THE SYSTEM WCIRB REPORT ON THE STATE OF THE CALIFORNIA WORKERS COMPENSATION INSURANCE SYSTEM Introduction The workers compensation insurance system in California is over 100 years old. It provides

Process of Establishing a Surplus Policy for the New Jersey School Boards Insurance Group

1 Process of Establishing a Surplus Policy for the New Jersey School Boards Insurance Group Background In 2010 the Board of Trustees of the New Jersey School Boards Insurance Group (NJSBAIG) developed

1 Process of Establishing a Surplus Policy for the New Jersey School Boards Insurance Group Background In 2010 the Board of Trustees of the New Jersey School Boards Insurance Group (NJSBAIG) developed

A Technical Guide for Individuals. The Whole Story. Understanding the features and benefits of whole life insurance. Insurance Strategies

A Technical Guide for Individuals The Whole Story Understanding the features and benefits of whole life insurance Insurance Strategies Contents 1 Insurance for Your Lifetime 3 How Does Whole Life Insurance

A Technical Guide for Individuals The Whole Story Understanding the features and benefits of whole life insurance Insurance Strategies Contents 1 Insurance for Your Lifetime 3 How Does Whole Life Insurance

Administrative Expenses of Health Plans

Administrative Expenses of Health Plans Douglas B. Sherlock, CFA S h e r l o c k C om pa n y 2009 Prepared for the Blue Cross and Blue Shield Association An Association of Independent Blue Cross and Blue

Administrative Expenses of Health Plans Douglas B. Sherlock, CFA S h e r l o c k C om pa n y 2009 Prepared for the Blue Cross and Blue Shield Association An Association of Independent Blue Cross and Blue

Life Insurance Corporation (Singapore)Pte Ltd UEN 201210695E MANAGEMENT REPORT 31/12/2013

Pte Ltd UEN 201210695E MANAGEMENT REPORT 31/12/2013") Life Insurance Corporation (Singapore)Pte Ltd UEN 201210695E MANAGEMENT REPORT 31/12/2013 LIFE INSURANCE CORPORATION (SINGAPORE) PTE. LTD. For the financial period from 1 January 2013 to 31 December 2013

Life Insurance Corporation (Singapore)Pte Ltd UEN 201210695E MANAGEMENT REPORT 31/12/2013 LIFE INSURANCE CORPORATION (SINGAPORE) PTE. LTD. For the financial period from 1 January 2013 to 31 December 2013

United Fire & Casualty Company Reports Record Quarterly Earnings

FOR IMMEDIATE RELEASE For: United Fire & Casualty Company 118 Second Avenue SE, PO Box 73909 Cedar Rapids, Iowa 52407-3909 Contact: John A. Rife, President/CEO, 319-399-5700 United Fire & Casualty Company

FOR IMMEDIATE RELEASE For: United Fire & Casualty Company 118 Second Avenue SE, PO Box 73909 Cedar Rapids, Iowa 52407-3909 Contact: John A. Rife, President/CEO, 319-399-5700 United Fire & Casualty Company

EMPLOYER SHARED RESPONSIBILITY:

EMPLOYER SHARED RESPONSIBILITY: PLAY OR PAY DISCUSSION GUIDE WHY THE MATH DOESN T WORK TO DROP COVERAGE 1 EVERYONE IS REQUIRED TO MAINTAIN HEALTH COVERAGE The Affordable Care Act (ACA) is ushering in

EMPLOYER SHARED RESPONSIBILITY: PLAY OR PAY DISCUSSION GUIDE WHY THE MATH DOESN T WORK TO DROP COVERAGE 1 EVERYONE IS REQUIRED TO MAINTAIN HEALTH COVERAGE The Affordable Care Act (ACA) is ushering in

Briefing Paper Individual Health Insurance Markets Grow and Are Transformed: Results for Four States Allan Baumgarten, 2014

Briefing Paper Individual Health Insurance s Grow and Are Transformed: Results for Four States As implementation of the Affordable Care Act (ACA) continues, the market for individual health insurance has

Briefing Paper Individual Health Insurance s Grow and Are Transformed: Results for Four States As implementation of the Affordable Care Act (ACA) continues, the market for individual health insurance has

CFA Institute Contingency Reserves Investment Policy Effective 8 February 2012

CFA Institute Contingency Reserves Investment Policy Effective 8 February 2012 Purpose This policy statement provides guidance to CFA Institute management and Board regarding the CFA Institute Reserves

CFA Institute Contingency Reserves Investment Policy Effective 8 February 2012 Purpose This policy statement provides guidance to CFA Institute management and Board regarding the CFA Institute Reserves

STEVEN HALL & PARTNERS. NEW YORK 650 Fifth Avenue 33rd Floor New York NY 10019. Phone: 212.488.5400 shp@shallpartners.com

STEVEN HALL & PARTNERS E X E C U T I V E C O M P E N S AT I O N C O N S U LTA N T S NEW YORK 650 Fifth Avenue 33rd Floor New York NY 10019 Phone: 212.488.5400 shp@shallpartners.com ABOUT US Steven Hall

STEVEN HALL & PARTNERS E X E C U T I V E C O M P E N S AT I O N C O N S U LTA N T S NEW YORK 650 Fifth Avenue 33rd Floor New York NY 10019 Phone: 212.488.5400 shp@shallpartners.com ABOUT US Steven Hall

Department of Labor Hearing on the Definition of Fiduciary Proposed Regulation. Testimony on behalf of. America s Health Insurance Plans and

August 10, 2015 Department of Labor Hearing on the Definition of Fiduciary Proposed Regulation Testimony on behalf of America s Health Insurance Plans and Blue Cross Blue Shield Association By Jon Breyfogle

August 10, 2015 Department of Labor Hearing on the Definition of Fiduciary Proposed Regulation Testimony on behalf of America s Health Insurance Plans and Blue Cross Blue Shield Association By Jon Breyfogle

Ultimate Parent: Highmark Health HM LIFE INSURANCE COMPANY OF NEW YORK. New York, New York

New York, New York A- Ultimate Parent: Highmark Health HM LIFE INSURANCE COMPANY OF NEW YORK Mail: 420 Fifth Avenue, 3rd Floor, New York, NY 10018 Web: www.hmig.com Tel: 800-328-5433 Fax: 717-260-7261

New York, New York A- Ultimate Parent: Highmark Health HM LIFE INSURANCE COMPANY OF NEW YORK Mail: 420 Fifth Avenue, 3rd Floor, New York, NY 10018 Web: www.hmig.com Tel: 800-328-5433 Fax: 717-260-7261

Patrick M. Avitabile Managing Director Citibank, N.A. 111 Wall Street New York, New York 10005

SECURITIES LENDING AND INVESTOR PROTECTION CONCERNS: CASH COLLATERAL REINVESTMENT; BORROWER DEFAULT; LENDING AGENT COMPENSATION AND FEE SPLITS; AND PROXY VOTING Patrick M. Avitabile Managing Director Citibank,

SECURITIES LENDING AND INVESTOR PROTECTION CONCERNS: CASH COLLATERAL REINVESTMENT; BORROWER DEFAULT; LENDING AGENT COMPENSATION AND FEE SPLITS; AND PROXY VOTING Patrick M. Avitabile Managing Director Citibank,

EMC Insurance Group Inc. Reports 2014 Fourth Quarter and Year-End Results and 2015 Operating Income Guidance

FOR IMMEDIATE RELEASE Contact: Steve Walsh (Investors) 515-345-2515 Lisa Hamilton (Media) 515-345-7589 EMC Insurance Group Inc. Reports 2014 Fourth Quarter and Year-End Results and 2015 Operating Income

FOR IMMEDIATE RELEASE Contact: Steve Walsh (Investors) 515-345-2515 Lisa Hamilton (Media) 515-345-7589 EMC Insurance Group Inc. Reports 2014 Fourth Quarter and Year-End Results and 2015 Operating Income

Community Benefit Provided by Nonprofit Health Plans

Community Benefit Provided by Nonprofit Health Plans Minnesota Department of Health January, 2009 Division of Health Policy Health Economics Program PO Box 64882 St. Paul, MN 55164-0882 (651) 201-3550

Community Benefit Provided by Nonprofit Health Plans Minnesota Department of Health January, 2009 Division of Health Policy Health Economics Program PO Box 64882 St. Paul, MN 55164-0882 (651) 201-3550

Index Growth Annuities

Index Growth Annuities 5 And 7 A Rewarding Combination Of Safety, Tax Deferral And Choice Standard Insurance Company Index Growth Annuities A Deferred Annuity Is An Insurance Contract A deferred annuity

Index Growth Annuities 5 And 7 A Rewarding Combination Of Safety, Tax Deferral And Choice Standard Insurance Company Index Growth Annuities A Deferred Annuity Is An Insurance Contract A deferred annuity

2013 Health Insurance Industry Analysis Report

2013 Health Insurance Industry Analysis Report Health Industry at a Glance Table 1 below provides a snapshot of the U.S. health insurance industry s aggregate financial results for health entities who

2013 Health Insurance Industry Analysis Report Health Industry at a Glance Table 1 below provides a snapshot of the U.S. health insurance industry s aggregate financial results for health entities who

to Health Care Reform

The Employer s Guide to Health Care Reform What you need to know now to: Consider your choices Decide what s best for you Follow the rules 2013-2014 Health care reform is the law of the land. Some don

The Employer s Guide to Health Care Reform What you need to know now to: Consider your choices Decide what s best for you Follow the rules 2013-2014 Health care reform is the law of the land. Some don

Each year, millions of Californians pursue degrees and certificates or enroll in courses

Higher Education Each year, millions of Californians pursue degrees and certificates or enroll in courses to improve their knowledge and skills at the state s higher education institutions. More are connected

Higher Education Each year, millions of Californians pursue degrees and certificates or enroll in courses to improve their knowledge and skills at the state s higher education institutions. More are connected

Protect your business, your family, and your legacy.

An Educational Guide for Business Owners Protect your business, your family, and your legacy. Take a closer look at buy-sell agreements. Needs-based Strategies Your business is probably your single largest

An Educational Guide for Business Owners Protect your business, your family, and your legacy. Take a closer look at buy-sell agreements. Needs-based Strategies Your business is probably your single largest

Rising Health Care Costs What Factors are Driving Increases?

Rising Health Care Costs What Factors are Driving Increases? Rising health care costs and access to affordable coverage are prominent issues for Washington employers, health care providers, purchasers,

Rising Health Care Costs What Factors are Driving Increases? Rising health care costs and access to affordable coverage are prominent issues for Washington employers, health care providers, purchasers,

Enhancements to the Massachusetts Health Insurance Rate Review Practice: Promoting Transparency and Protecting Massachusetts Consumers

Page 1 of 9 Enhancements to the Massachusetts Health Insurance Rate Review Practice: Promoting Transparency and Protecting Massachusetts Consumers a) Current Health Insurance Rate Review Capacity and Process

Page 1 of 9 Enhancements to the Massachusetts Health Insurance Rate Review Practice: Promoting Transparency and Protecting Massachusetts Consumers a) Current Health Insurance Rate Review Capacity and Process

TESTIMONY OF. Joel Ario Acting Commissioner of Insurance Commonwealth of Pennsylvania

TESTIMONY OF Joel Ario Acting Commissioner of Insurance Commonwealth of Pennsylvania Testifying on Behalf of the NATIONAL ASSOCIATION OF INSURANCE COMMISSIONERS BEFORE THE SENATE COMMITTEE ON FINANCE on

TESTIMONY OF Joel Ario Acting Commissioner of Insurance Commonwealth of Pennsylvania Testifying on Behalf of the NATIONAL ASSOCIATION OF INSURANCE COMMISSIONERS BEFORE THE SENATE COMMITTEE ON FINANCE on

VARIABLE PORTFOLIO HOLLAND LARGE CAP GROWTH FUND 50606 Ameriprise Financial Center Minneapolis, MN 55474

VARIABLE PORTFOLIO HOLLAND LARGE CAP GROWTH FUND 50606 Ameriprise Financial Center Minneapolis, MN 55474 INFORMATION STATEMENT NOTICE REGARDING SUBADVISER This information statement mailed on or about

VARIABLE PORTFOLIO HOLLAND LARGE CAP GROWTH FUND 50606 Ameriprise Financial Center Minneapolis, MN 55474 INFORMATION STATEMENT NOTICE REGARDING SUBADVISER This information statement mailed on or about

The BrightScope/ICI Defined Contribution Plan Profile: A Close Look at 401(k) Plans

Plans") The BrightScope/ICI Defined Contribution Plan Profile: A Close Look at 401(k) Plans DECEMBER 2014 The BrightScope/ICI Defined Contribution Plan Profile: A Close Look at 401(k) Plans 1 THE BRIGHTSCOPE/ICI

The BrightScope/ICI Defined Contribution Plan Profile: A Close Look at 401(k) Plans DECEMBER 2014 The BrightScope/ICI Defined Contribution Plan Profile: A Close Look at 401(k) Plans 1 THE BRIGHTSCOPE/ICI

Student Health Program Academic Year 2009-2010 Annual Report

Student Health Program Academic Year 29-21 Annual Report August 211 Deval Patrick, Governor Commonwealth of Massachusetts Timothy P. Murray Lieutenant Governor JudyAnn Bigby, M.D., Secretary Executive

Student Health Program Academic Year 29-21 Annual Report August 211 Deval Patrick, Governor Commonwealth of Massachusetts Timothy P. Murray Lieutenant Governor JudyAnn Bigby, M.D., Secretary Executive

NASDAQ: FNHC. Joint Venture to Form an Insurance Company July 2014

Joint Venture to Form an Insurance Company July 2014 1 SAFE HARBOR STATEMENT Safe harbor statement under the Private Securities Litigation Reform Act of 1995: Statements that are not historical fact are

Joint Venture to Form an Insurance Company July 2014 1 SAFE HARBOR STATEMENT Safe harbor statement under the Private Securities Litigation Reform Act of 1995: Statements that are not historical fact are

No Basis for High Insurance Rates:

No Basis for High Insurance Rates: An Analysis of the 15 Largest Medical Malpractice Insurers 2006 Financial Statements Jay Angoff Of Counsel Roger Brown & Associates 216 E. McCarty Street Jefferson City,

No Basis for High Insurance Rates: An Analysis of the 15 Largest Medical Malpractice Insurers 2006 Financial Statements Jay Angoff Of Counsel Roger Brown & Associates 216 E. McCarty Street Jefferson City,

The Implications of Reform on the US Health Insurance Industry

WHITE PAPER The Implications of Reform on the US Health Insurance Industry Key Research Findings Table of Contents Executive Summary...1 Research Synopsis...2 Strategic Themes Driving Change...3 1. Shift

WHITE PAPER The Implications of Reform on the US Health Insurance Industry Key Research Findings Table of Contents Executive Summary...1 Research Synopsis...2 Strategic Themes Driving Change...3 1. Shift

GE Financial Assurance Holdings, Inc. (Exact name of registrant as specified in its charter)

") UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 10-Q QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 10-Q QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the quarterly period ended

Report of Examination of. Harleysville Insurance Company of Ohio Columbus, Ohio. As of December 31, 2009

Report of Examination of Harleysville Insurance Company of Ohio Columbus, Ohio As of December 31, 2009 Table of Contents Subject Page Salutation... 1 Description of Company... 1 Scope of Examination...

Report of Examination of Harleysville Insurance Company of Ohio Columbus, Ohio As of December 31, 2009 Table of Contents Subject Page Salutation... 1 Description of Company... 1 Scope of Examination...

Milliman Response to. Actuarial Risk Management Report of August 31, 2009 Titled Excessive Surplus Assessment Report of GHMSI, Inc.

Milliman Response to Actuarial Risk Management Report of August 31, 2009 Titled Excessive Surplus Assessment Report of GHMSI, Inc. Surplus Position November 2, 2009 Robert H. Dobson, FSA, MAAA Phyllis

Milliman Response to Actuarial Risk Management Report of August 31, 2009 Titled Excessive Surplus Assessment Report of GHMSI, Inc. Surplus Position November 2, 2009 Robert H. Dobson, FSA, MAAA Phyllis

How to Choose a Life Insurance Company

How to Choose a Life Insurance Company A Guide through Financial Data and Industry Information The Guardian Life Insurance Company of America New York, NY 10004-4025 Table of Contents Page 1. Mutuality...

How to Choose a Life Insurance Company A Guide through Financial Data and Industry Information The Guardian Life Insurance Company of America New York, NY 10004-4025 Table of Contents Page 1. Mutuality...

How to choose the right insurance carrier for your business

How to choose the right insurance carrier for your business Risk managers and insurance buyers often rely on the expertise of their brokers when choosing insurance carriers. While brokers provide valuable

How to choose the right insurance carrier for your business Risk managers and insurance buyers often rely on the expertise of their brokers when choosing insurance carriers. While brokers provide valuable

Economical Insurance reports financial results for First Quarter 2015

NEWS RELEASE Economical Insurance reports financial results for First Quarter 2015 Increased gross written premiums by 2.0% over first quarter 2014 Recorded a combined ratio of 105.7% for the quarter Generated

NEWS RELEASE Economical Insurance reports financial results for First Quarter 2015 Increased gross written premiums by 2.0% over first quarter 2014 Recorded a combined ratio of 105.7% for the quarter Generated

ORGANIZATIONAL EXAMINATION DL REINSURANCE COMPANY AS OF DECEMBER 10, 2014

ORGANIZATIONAL EXAMINATION OF DL REINSURANCE COMPANY AS OF DECEMBER 10, 2014 TABLE OF CONTENTS SALUTATION... 1 SCOPE OF EXAMINATION... 2 HISTORY... 2 MANAGEMENT AND CONTROL... 2 HOLDING COMPANY SYSTEM...

ORGANIZATIONAL EXAMINATION OF DL REINSURANCE COMPANY AS OF DECEMBER 10, 2014 TABLE OF CONTENTS SALUTATION... 1 SCOPE OF EXAMINATION... 2 HISTORY... 2 MANAGEMENT AND CONTROL... 2 HOLDING COMPANY SYSTEM...

Prospectus Socially Responsible Funds

Prospectus Socially Responsible Funds Calvert Social Investment Fund (CSIF) Balanced Portfolio Equity Portfolio Enhanced Equity Portfolio Bond Portfolio Money Market Portfolio Calvert Social Index Fund

Prospectus Socially Responsible Funds Calvert Social Investment Fund (CSIF) Balanced Portfolio Equity Portfolio Enhanced Equity Portfolio Bond Portfolio Money Market Portfolio Calvert Social Index Fund

CareFirst, Inc. Group Hospitalization and Medical Services, Inc. Need for Statutory Surplus and Development of Optimal Surplus Target Range

CareFirst, Inc. Group Hospitalization and Medical Services, Inc. Need for Statutory Surplus and Development of Optimal Surplus Target Range March 22, 2005 Robert H. Dobson, F.S.A. Phyllis A. Doran, F.S.A.

CareFirst, Inc. Group Hospitalization and Medical Services, Inc. Need for Statutory Surplus and Development of Optimal Surplus Target Range March 22, 2005 Robert H. Dobson, F.S.A. Phyllis A. Doran, F.S.A.

Table of Contents. Introduction... 1. Definition of Loss Ratio... 2. Notes on Using the Results...2. How Rates are Regulated... 4

Report of 2013 Loss Ratio Experience in the Individual and Small Employer Markets for: Insurance Companies Nonprofit Health Service Plan Corporations and Health Maintenance Organizations June, 2014 Table

Report of 2013 Loss Ratio Experience in the Individual and Small Employer Markets for: Insurance Companies Nonprofit Health Service Plan Corporations and Health Maintenance Organizations June, 2014 Table

You work hard for your clients every day. That s why we re working hard for you.

2015 BROKER GUIDE You work hard for your clients every day. That s why we re working hard for you. Excellus BlueCross BlueShield dedicated to making your job easier. A nonprofit independent licensee of

2015 BROKER GUIDE You work hard for your clients every day. That s why we re working hard for you. Excellus BlueCross BlueShield dedicated to making your job easier. A nonprofit independent licensee of

Economical Insurance reports financial results for Second Quarter and Year-todate

NEWS RELEASE Economical Insurance reports financial results for Second Quarter and Year-todate 2015 Increased gross written premiums by 3.0% over second quarter 2014 Recorded a combined ratio of 95.9%

NEWS RELEASE Economical Insurance reports financial results for Second Quarter and Year-todate 2015 Increased gross written premiums by 3.0% over second quarter 2014 Recorded a combined ratio of 95.9%

OREGON S WORKERS COMPENSATION INSURANCE MARKET

LEGISLATIVE REVENUE OFFICE State Capitol Building 900 Court Street NE, H-197 Salem, Oregon 97301 (503) 986-1266 http://www.leg.state.or.us/comm/lro/home.htm Research Report Number 10-00 September 7, 2000

LEGISLATIVE REVENUE OFFICE State Capitol Building 900 Court Street NE, H-197 Salem, Oregon 97301 (503) 986-1266 http://www.leg.state.or.us/comm/lro/home.htm Research Report Number 10-00 September 7, 2000

Tax Exemption for Credit Unions: An Unjustifiable $10 Billion Tax Expenditure

Tax Exemption for Credit Unions: An Unjustifiable $10 Billion Tax Expenditure By Kenneth J. Kies and Bert Ely Unlike other financial institutions like banks and thrifts, credit unions do not pay corporate

Tax Exemption for Credit Unions: An Unjustifiable $10 Billion Tax Expenditure By Kenneth J. Kies and Bert Ely Unlike other financial institutions like banks and thrifts, credit unions do not pay corporate

FREE MARKET U.S. EQUITY FUND FREE MARKET INTERNATIONAL EQUITY FUND FREE MARKET FIXED INCOME FUND of THE RBB FUND, INC. PROSPECTUS.

FREE MARKET U.S. EQUITY FUND FREE MARKET INTERNATIONAL EQUITY FUND FREE MARKET FIXED INCOME FUND of THE RBB FUND, INC. PROSPECTUS December 31, 2014 Investment Adviser: MATSON MONEY, INC. 5955 Deerfield

FREE MARKET U.S. EQUITY FUND FREE MARKET INTERNATIONAL EQUITY FUND FREE MARKET FIXED INCOME FUND of THE RBB FUND, INC. PROSPECTUS December 31, 2014 Investment Adviser: MATSON MONEY, INC. 5955 Deerfield

The Use of Captives in the Life Insurance Industry

AUCTORIS Architects of Wealth Preservation Strategies 5350 S. Roslyn Street, Suite 310 Greenwood Village, CO 80111 Phone: 303-740-8001 Website: www.auctoris.com Prepared and Researched by July 2013 On

AUCTORIS Architects of Wealth Preservation Strategies 5350 S. Roslyn Street, Suite 310 Greenwood Village, CO 80111 Phone: 303-740-8001 Website: www.auctoris.com Prepared and Researched by July 2013 On

THE ROLE OF THE ACTUARY IN AN INSURANCE BROKERAGE FIRM. Edgar W. Davenport

THE ROLE OF THE ACTUARY IN AN INSURANCE BROKERAGE FIRM Edgar W. Davenport 209 THE ROLE OF THE ACTUARY IN AN INSURANCE BROKERAGE FIRM BY EDGAR W. DAVENPORT BIOGRAPHY: ABSTRACT: Mr. Davenport is Vice President

THE ROLE OF THE ACTUARY IN AN INSURANCE BROKERAGE FIRM Edgar W. Davenport 209 THE ROLE OF THE ACTUARY IN AN INSURANCE BROKERAGE FIRM BY EDGAR W. DAVENPORT BIOGRAPHY: ABSTRACT: Mr. Davenport is Vice President

Discussion Board Articles Ratio Analysis

Excellence in Financial Management Discussion Board Articles Ratio Analysis Written by: Matt H. Evans, CPA, CMA, CFM All articles can be viewed on the internet at www.exinfm.com/board Ratio Analysis Cash

Excellence in Financial Management Discussion Board Articles Ratio Analysis Written by: Matt H. Evans, CPA, CMA, CFM All articles can be viewed on the internet at www.exinfm.com/board Ratio Analysis Cash

Presented to the National Association of Insurance Commissioners Life Risk-Based Capital Working Group March 2001 Nashville, TN

Comments from the American Academy of Actuaries Life-Risk Based Capital Committee on a Letter Commenting Upon the Proposed Change to the Treatment of Common Stock in the Life Risk-Based Capital Formula

Comments from the American Academy of Actuaries Life-Risk Based Capital Committee on a Letter Commenting Upon the Proposed Change to the Treatment of Common Stock in the Life Risk-Based Capital Formula

Getting More From Your Actuarial Loss Reserve Analysis. For Property/Casualty Insurance and Reinsurance Companies

Getting More From Your Actuarial Loss Reserve Analysis For Property/Casualty Insurance and Reinsurance Companies Introduction Many property/casualty insurance and reinsurance companies retain the services

Getting More From Your Actuarial Loss Reserve Analysis For Property/Casualty Insurance and Reinsurance Companies Introduction Many property/casualty insurance and reinsurance companies retain the services

Spring 2003 Notes for SoA Course 6 exam, Copyright 2003 by Krzysztof Ostaszewski - 479 -

Risk-Based Capital for Insurers in the United States (The following notes are partly based on the work of Michael Barth, Life Risk-Based Capital: The U.S. Experience, presented at the World Bank s Contractual

Risk-Based Capital for Insurers in the United States (The following notes are partly based on the work of Michael Barth, Life Risk-Based Capital: The U.S. Experience, presented at the World Bank s Contractual

BNY Mellon Third Quarter 2015 Financial Highlights

BNY Mellon Third Quarter 205 Financial Highlights October 20, 205 Cautionary Statement A number of statements in our presentations, the accompanying slides and the responses to your questions are forward-looking

BNY Mellon Third Quarter 205 Financial Highlights October 20, 205 Cautionary Statement A number of statements in our presentations, the accompanying slides and the responses to your questions are forward-looking

THE HARTFORD DIRECTORS, OFFICERS AND ENTITY LIABILITY INSURANCE APPLICATION (FINANCIAL INSTITUTIONS/FINANCIAL SERVICES) NEW YORK

NEW YORK") , a stock insurance company, herein called the Insurer THE HARTFORD DIRECTORS, OFFICERS AND ENTITY LIABILITY INSURANCE APPLICATION (FINANCIAL INSTITUTIONS/FINANCIAL SERVICES) NEW YORK NOTICE: THIS IS A

, a stock insurance company, herein called the Insurer THE HARTFORD DIRECTORS, OFFICERS AND ENTITY LIABILITY INSURANCE APPLICATION (FINANCIAL INSTITUTIONS/FINANCIAL SERVICES) NEW YORK NOTICE: THIS IS A

An Overview of Trade Credit Insurance. Author: Joe Ketzner Executive Vice President, Commercial Euler Hermes

An Overview of Trade Credit Insurance Author: Joe Ketzner Executive Vice President, Commercial Euler Hermes Table of Contents Introduction...3 More about Trade Credit Insurance...4 Philosophy of Trade

An Overview of Trade Credit Insurance Author: Joe Ketzner Executive Vice President, Commercial Euler Hermes Table of Contents Introduction...3 More about Trade Credit Insurance...4 Philosophy of Trade