Massachusetts Dukakis Play or Pay Plan

|

|

|

- Alaina Hill

- 8 years ago

- Views:

Transcription

1 6 Massachusetts A proposed amendment to the Massachusetts state constitution, which would mandate that lawmakers provide medical insurance to all residents of the state, is the final stage in what critics have long warned would be a downward spiral for private health insurance caused by state over-regulation. The amendment proposal, reported by the Associated Press on April 6, 2004, would require the state Legislature to enact and implement such laws as will ensure that no Massachusetts resident lacks comprehensive, affordable, and equitably financed health insurance coverage for all medically necessary preventive, acute, and chronic health care and mental health care services, prescription drugs, and devices. Dukakis Play or Pay Plan The proposed constitutional amendment is an attempt to address the unintended consequences of two decades of manipulation and over-regulation by state government of Massachusetts insurance markets. The interference has left insurance rates high and consumers with only limited choices. In the late 1980s, Massachusetts aimed to become the first state to create a single-payer health care system. The Universal Entitlement Act of 1988 was passed during an especially partisan time when the state s three-term governor, Michael Dukakis, was running for president. Not unlike the Clinton administration s proposal to change the nation s health care system, the Dukakis plan tried to achieve universal coverage through an unfunded mandate on employers now called play or pay. It required all businesses with 25 employees or

2 DESTROYING INSURANCE MARKETS more to provide health insurance as a benefit, or pay $1,680 per employee to a state pool from which uncovered workers could receive insurance. The state s ambitious universal health care plan, however, was never put into place. Just as the Dukakis presidential bid was falling short, the state s economy was tanking. With state revenues plummeting and private employers battered by the economic downturn, there was neither the political will nor the financial wherewithal to put a health care-for-all plan into place. After repeated delays, the Universal Entitlement Act was officially repealed by the Legislature in Over-Regulation in the 1990s and 2000 In 1996, the Massachusetts Legislature passed the Non-Group Health Insurance Reform Act (Massachusetts calls individual insurance non-group ), which severely harmed the underwriting, pricing and marketing of individual and small group health insurance plans. Among the law s provisions:! Insurers serving the Massachusetts small group market and insuring at least 5,000 persons (employees and dependents) were required to guarantee issue at least one product in the non-group market;! The state division of insurance defined a standard individual insurance policy, specifying deductibles, premiums and coverage mandates for one HMO, one PPO and one indemnity-style plan. Insurers serving the individual insurance market were permitted to offer only the standardized plan in each category;! Approved plans were required to offer annual open enrollment periods;! Persons who were eligible for group coverage would not be eligible for non-group (individual) coverage;! Rates could be modified from the state-established community rate only for age and geography. Rate variation for age was -56-

3 MASSACHUSETTS extremely limited, ensuring that the young (with lower average incomes) subsidize the older population (with higher average incomes). Rates for plans with enhanced benefits could be adjusted to account for the benefit differences, but not for health risks; and! Insurance premiums would have to be approved by the insurance commissioner. The cumbersome process imposed by the Legislature tied the rates of the insurer to its competitors rates regardless of the experience of the carrier applying for the rate increase. This law was virtually identical to New Jersey s 1992 law. Massachusetts academics Katherine Swartz, professor of health policy and management at the Harvard School of Public Health, and Deborah Garnick, professor at the Heller School for Social Policy and Management at Brandeis University, were both strong supporters of these measures and had championed their adoption in New Jersey. New Jersey officials testified before the Massachusetts Legislature in support of both guaranteed issue and community rating. Legislation that passed in 2000 modified those rules in several ways. On the positive side, it allowed insurers to offer a second plan for individual insurance for HMO, PPO and indemnity-style coverage, subject to approval by the Division of Insurance. The rule that persons eligible for group coverage could not be eligible for individual coverage was repealed, and individual insurers were made to serve consumers eligible under HIPAA. A reinsurance pool (not a high-risk insurance pool) was established. On the negative side, at least for insurance companies trying to offer individual health insurance in the state, the 2000 legislation changed the open enrollment mandate from once a year to continuous, with pre-existing conditions excludable by insurers for only six months. If the insured had prior coverage within 63 days of his or her new coverage, there is full portability no pre-existing conditions could be excluded. -57-

4 DESTROYING INSURANCE MARKETS Individual Market Meltdown The new insurance regulations in Massachusetts had predictable results. Two years after the 1996 legislation was adopted, approximately 20 health insurers stopped marketing plans in Massachusetts, according to industry observer Daniel Heystek, owner of Gramercy Insurance Brokerage in Arlington. The new laws destroyed the individual insurance market. Among companies that left were such highly respected firms as Golden Rule Insurance Co., Travelers Insurance Companies, Mutual of Omaha, and Time Insurance Company. A few others did not leave but stopped underwriting individual policies. On October 20, 2003, the Boston Business Journal noted not all of the departures were due solely to the new law: Two big changes came after the Boston-based John Hancock Mutual Life Insurance Company sold its health plan to a California company, while Prudential Insurance Company auctioned off its insurance plan. But the new state law undoubtedly played a major role in forcing other players out of the market, industry observers say. The stated aim of the Non-Group Health Insurance Reform Act was to make sure no one in Massachusetts would go uninsured. That goal was not realized. According to a report published in the March 26, 2004 issue of the Boston Business Journal, Blue Cross Blue Shield statistics, based on state reports, reveal that the number of uninsured persons in the state has increased from 365,000 in 2000 to more than 500,000 today. High Insurance Premiums The 2000 Medical Expenditure Survey, conducted by the Agency for Healthcare Research and Quality, finds Massachusetts to have the highest average annual premiums in the nation for family coverage through small group policies: $8,468. New Jersey comes in second at $8,274. Individual insurance rates in the state are also high and, as a result, the share of persons insured in the state s individual insurance -58-

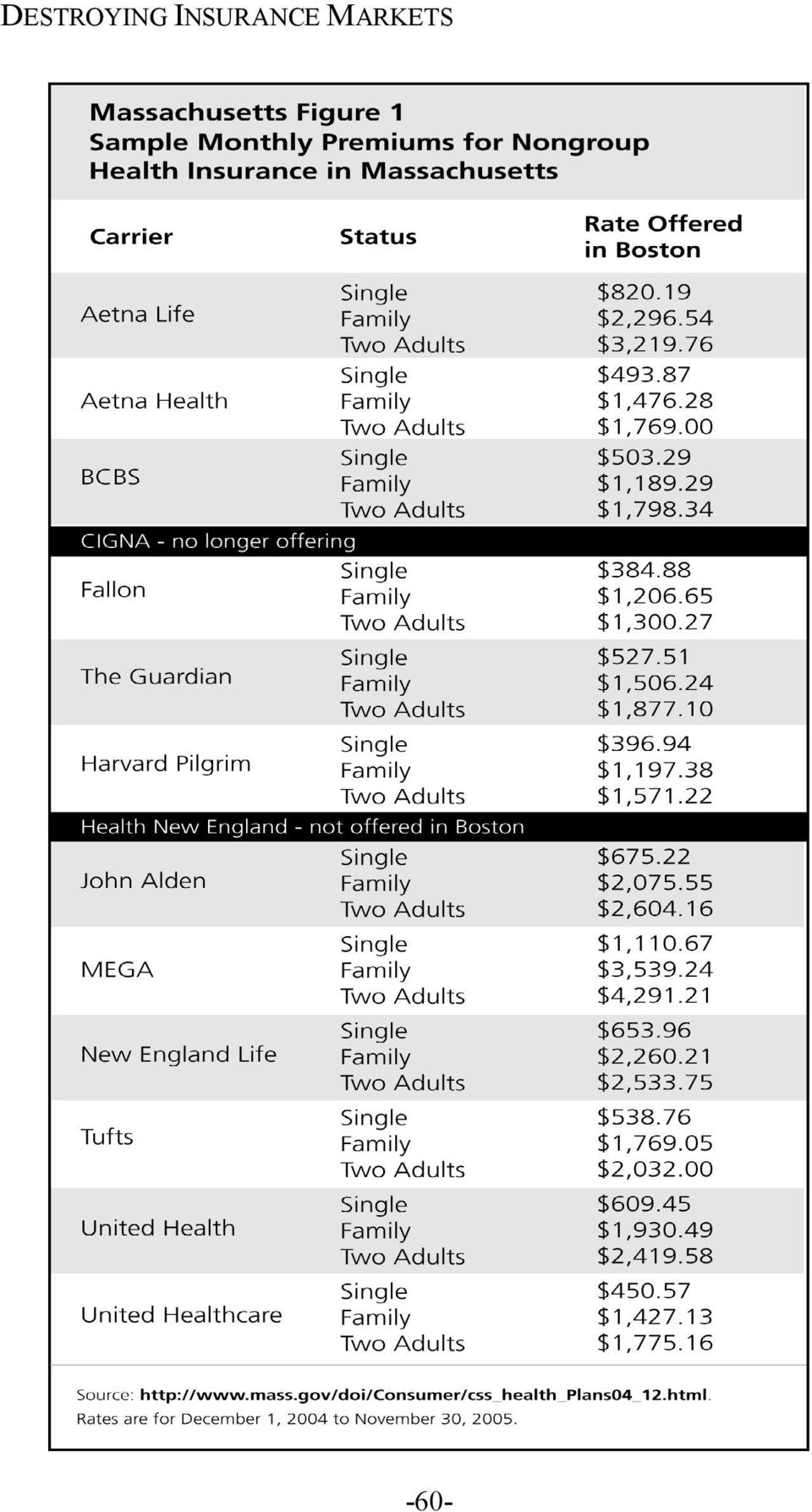

5 MASSACHUSETTS market fell from 10.8 percent in 1994 to 8.3 percent in As of June 2005, monthly premiums in the state s non-group market ranged from $384 for a 25-year-old individual ($4,618 per year), offered by Fallon Community Health Plan Inc., to as high as $4,291 for the two-adult plan ($51,494 a year) offered by The MEGA Life Insurance Company. (See Massachusetts Figure 1.) Those rates are substantially higher than the national average annual premiums reported in the January/February 2004 issue of Healthplan magazine: $2,070 for single coverage and $4,009 for family coverage. In an April 6, 2004 newswire report by the Associated Press, insurance broker Heystek said prior to the enactment of guaranteed issue and community rating he could have lined up coverage for a single 25-year-old at rates starting at $25 a month. Premiums under many individual plans have since skyrocketed, said Heystek, rising to more than $600 a month or more. It differs from company to company. For an individual to spend less than $180 a month is now the exception. It [guaranteed issue and community rating] has limited the choice. The high cost of health insurance is the reason most often given by those who are uninsured. Yet Massachusetts policymakers, claiming to be concerned about the state s uninsured rate, nevertheless continue to support laws that increase the price of insurance. Health Insurance for All? With so much evidence available showing the failure of past attempts to regulate the state s private insurance market, what should Massachusetts elected officials do? According to a coalition of liberal advocacy groups called the Health Care for Massachusetts Campaign, the solution is... even more regulation! The group is the force behind the Health Care Insurance for Massachusetts Constitutional Initiative. That proposal will be presented to the state s voters only if approved by the current Legislature and again by the new, two-year -59-

Those rates are substantially higher than the national average annual premiums reported in the January/February 2004 issue of Healthplan magazine: $2,070 for single coverage and $4,009 for family")

6 DESTROYING INSURANCE MARKETS -60-

7 MASSACHUSETTS Legislature that will take office in January The soonest the question could appear on the ballot, then, is November The amendment s supporters say it will force lawmakers to come to grips with the state s health care crisis. Dr. Peter Slavin, president of Massachusetts General Hospital, told the Associated Press, Some say we cannot afford the cost of covering the uninsured, but we are already paying for the much higher costs of failing to provide health care to those who need it. Critics say the amendment would just extend to ridiculous and expensive extremes the failed policies of the past. Eileen McAnneny, vice president of government affairs for Associated Industries of Massachusetts, says the amendment could cost the state s taxpayers as much as $3 billion. Said Bill Vernon of the Massachusetts National Federation of Independent Business, this amendment is not necessary. It is a statement of a goal that we all share... but it doesn t get us any closer to that goal. State Rep. William Galvin (D-Canton) warns, If this becomes part of our constitution, the Legislature will be forced to come up with some solution and when they do, it s going to be taken to the SJC [Supreme Judicial Court] and the SJC is going to mandate it. Punting to the judiciary the difficult decisions about how to define, finance and deliver a major new public entitlement is hardly good public policy. Better Alternatives Other states have been more successful than Massachusetts in keeping health insurance premiums affordable, the uninsured rate low and the quality of health care services high. Policies they have adopted include:! Establishing a high-risk health insurance pool for the medically uninsurable;! Repealing guaranteed issue and community rating requirements, which would encourage insurers to re-enter the state by -61-

8 DESTROYING INSURANCE MARKETS discouraging behavior that leads to higher rates for everyone, but especially for younger and healthy consumers. The high-risk pool then acts as a safety net for those who cannot qualify for insurance;! Repealing the cumbersome rate approval process that discourages price competition and offering consumers more choices;! Allowing health insurers to offer mandate-free insurance polices to individuals and to small group plan sponsors; and! Encouraging the use of Health Savings Accounts by giving public employees the option to choose them and providing state income tax deductions for deposits made to the accounts. Conclusion By now, state policymakers should know better than to propose more regulation as the solution to the state s health insurance woes. Rules and regulations already on the books have driven up prices and reduced consumer choices. More of the same kind of regulation will produce only more of the same results. Much more promising than the constitutional initiative is a reform agenda that allows Massachusetts to take advantage of the trend toward consumer-directed health care. Competition among insurers and providers can lower prices and rationalize services; giving consumers choices can help them find the combination of price, service and financial risk that is best for them. Massachusetts needs to overcome its fear of markets if it ever hopes to achieve the goal of access to quality health care for all. -62-

MHA Comparison of Michigan Legislative Health Insurance Reform Proposals

Overall approach to expanding health care coverage Amends the Insurance Code to create Health Care Affordability Fund within Treasury. These funds are used to: expand MIChild to 300% of poverty level Subsidize

Overall approach to expanding health care coverage Amends the Insurance Code to create Health Care Affordability Fund within Treasury. These funds are used to: expand MIChild to 300% of poverty level Subsidize

Health Insurance Exchanges and Market Design

Health Insurance Exchanges and Market Design: An Introduction Presentation to Oregon Health Fund Board November 6, 2007 1 Important Questions Can an exchange solve the problems of cost, quality and/or

Health Insurance Exchanges and Market Design: An Introduction Presentation to Oregon Health Fund Board November 6, 2007 1 Important Questions Can an exchange solve the problems of cost, quality and/or

TESTIMONY OF. Joel Ario Acting Commissioner of Insurance Commonwealth of Pennsylvania

TESTIMONY OF Joel Ario Acting Commissioner of Insurance Commonwealth of Pennsylvania Testifying on Behalf of the NATIONAL ASSOCIATION OF INSURANCE COMMISSIONERS BEFORE THE SENATE COMMITTEE ON FINANCE on

TESTIMONY OF Joel Ario Acting Commissioner of Insurance Commonwealth of Pennsylvania Testifying on Behalf of the NATIONAL ASSOCIATION OF INSURANCE COMMISSIONERS BEFORE THE SENATE COMMITTEE ON FINANCE on

Small Group Health Insurance Reform In New Hampshire

Small Group Health Insurance Reform In New Hampshire Report to Joint Committee on Health Care Oversight February 2006 Christopher F. Koller Health Insurance Commissioner REPORT TO THE LEGISLATURE FROM

Small Group Health Insurance Reform In New Hampshire Report to Joint Committee on Health Care Oversight February 2006 Christopher F. Koller Health Insurance Commissioner REPORT TO THE LEGISLATURE FROM

or vertical applications)

") or vertical applications) Health care reform is on many of our minds. After all, the Affordable Care Act (ACA), will be in full swing by January 2014. But many people still have questions about what the

or vertical applications) Health care reform is on many of our minds. After all, the Affordable Care Act (ACA), will be in full swing by January 2014. But many people still have questions about what the

Health Care Reform: What s in the Law

Health Care Reform: What s in the Law Professor Sidney D. Watson March 2013 On June 28, 2012, the United States Supreme Court upheld the Affordable Care Act, also known as ObamaCare. The Supreme Court

Health Care Reform: What s in the Law Professor Sidney D. Watson March 2013 On June 28, 2012, the United States Supreme Court upheld the Affordable Care Act, also known as ObamaCare. The Supreme Court

The Policy Debate on Government Sponsored Health Care Reinsurance Mechanisms Colorado s Proposal and a Look at the New York and Arizona Models

The Policy Debate on Government Sponsored Health Care Reinsurance Mechanisms Colorado s Proposal and a Look at the New York and Arizona Models Robert M. Ferm, Esq. 303.628.3380 Introduction Recently many

The Policy Debate on Government Sponsored Health Care Reinsurance Mechanisms Colorado s Proposal and a Look at the New York and Arizona Models Robert M. Ferm, Esq. 303.628.3380 Introduction Recently many

Arizona Health Care Cost Containment System Issue Paper on High-Risk Pools

Arizona Health Care Cost Containment System Issue Paper on High-Risk Pools Prepared by: T. Scott Bentley, A.S.A. Associate Actuary David F. Ogden, F.S.A. Consulting Actuary August 27, 2001 Arizona Health

Arizona Health Care Cost Containment System Issue Paper on High-Risk Pools Prepared by: T. Scott Bentley, A.S.A. Associate Actuary David F. Ogden, F.S.A. Consulting Actuary August 27, 2001 Arizona Health

Nevada Health Plan Project

Nevada Health Plan Project Health Plan Basics Health Savings Accounts A Threat - The Fair Share Act New Trends - Wellness Programs Opportunity - High Risk Pools 1 Who is NAHU? Larry S. Harrison, President

Nevada Health Plan Project Health Plan Basics Health Savings Accounts A Threat - The Fair Share Act New Trends - Wellness Programs Opportunity - High Risk Pools 1 Who is NAHU? Larry S. Harrison, President

INDIVIDUAL (NON-GROUP) POLICIES

POLICIES") CHAPTER 3 INDIVIDUAL (NON-GROUP) POLICIES What are they? Who are they for? How to obtain coverage INTRODUCTION An individual health insurance policy is one that is purchased outside a group setting. (Most

CHAPTER 3 INDIVIDUAL (NON-GROUP) POLICIES What are they? Who are they for? How to obtain coverage INTRODUCTION An individual health insurance policy is one that is purchased outside a group setting. (Most

Report to the Health Care Access Bureau Within the Massachusetts Division of Insurance

June 2010 Report to the Health Care Access Bureau Within the Massachusetts Division of Insurance Analysis of Individual Health Coverage In Massachusetts Before and After the July 1, 2007 Merger of the

June 2010 Report to the Health Care Access Bureau Within the Massachusetts Division of Insurance Analysis of Individual Health Coverage In Massachusetts Before and After the July 1, 2007 Merger of the

Impact of Merging the Massachusetts Non-Group and Small Group Health Insurance Markets

Prepared for the Massachusetts Division of Insurance and Market Merger Special Commission December 26, 2006 Gorman Actuarial, LLC 210 Robert Road Marlborough MA 01752 DeWeese Consulting, Inc. 263 Wright

Prepared for the Massachusetts Division of Insurance and Market Merger Special Commission December 26, 2006 Gorman Actuarial, LLC 210 Robert Road Marlborough MA 01752 DeWeese Consulting, Inc. 263 Wright

What an employer should know about Health Care Reform

What an employer should know about Health Presented By David L. Fear, Sr. RHU NAHU Education Foundation Sponsored by PPACA - history Signed into law in March, 2010 2,700 page rough draft became the law

What an employer should know about Health Presented By David L. Fear, Sr. RHU NAHU Education Foundation Sponsored by PPACA - history Signed into law in March, 2010 2,700 page rough draft became the law

UNDERSTANDING INDIVIDUAL HEALTH INSURANCE

UNDERSTANDING INDIVIDUAL HEALTH INSURANCE Continuing Education Provider #S10725 Imperial Training Services, Inc. Post Office Box 8 Garner, North Carolina 27529 Instructor: Cliff Davis MBA, CLU Phone: (919)

UNDERSTANDING INDIVIDUAL HEALTH INSURANCE Continuing Education Provider #S10725 Imperial Training Services, Inc. Post Office Box 8 Garner, North Carolina 27529 Instructor: Cliff Davis MBA, CLU Phone: (919)

Insurance Agents: Ignored Players In Health Insurance Reform

Insurance Agents: Ignored Players In Health Insurance Reform After reforms, insurance agents in New Jersey still exert a good deal of influence in the individual health insurance market. b y D e b o r

Insurance Agents: Ignored Players In Health Insurance Reform After reforms, insurance agents in New Jersey still exert a good deal of influence in the individual health insurance market. b y D e b o r

HEALTH CARE REFORM DOCUMENT FROM THE WEBSITE OF BLUE CROSS BLUE SHIELD OF NORTH DAKOTA

HEALTH CARE REFORM DOCUMENT FROM THE WEBSITE OF BLUE CROSS BLUE SHIELD OF NORTH DAKOTA Frequently Asked Questions I ve heard the federal government launched a new website called Healthcare.gov. How can

HEALTH CARE REFORM DOCUMENT FROM THE WEBSITE OF BLUE CROSS BLUE SHIELD OF NORTH DAKOTA Frequently Asked Questions I ve heard the federal government launched a new website called Healthcare.gov. How can

Presented to: 2007 Kansas Legislature. February 1, 2007

MARCIA J. NIELSEN, PhD, MPH Executive Director ANDREW ALLISON, PhD Deputy Director SCOTT BRUNNER Chief Financial Officer Report on: Massachusetts Commonwealth Health Insurance Connector Program Presented

MARCIA J. NIELSEN, PhD, MPH Executive Director ANDREW ALLISON, PhD Deputy Director SCOTT BRUNNER Chief Financial Officer Report on: Massachusetts Commonwealth Health Insurance Connector Program Presented

Health Insurance Exchange Study

Health Insurance Exchange Study Minnesota Department of Health February, 2008 Division of Health Policy Health Economics Program PO Box 64882 St. Paul, MN 55164-0882 (651) 201-3550 www.health.state.mn.us

Health Insurance Exchange Study Minnesota Department of Health February, 2008 Division of Health Policy Health Economics Program PO Box 64882 St. Paul, MN 55164-0882 (651) 201-3550 www.health.state.mn.us

Review of Florida s Health Insurance Laws Relating to Rates and Access to Coverage

Review of Florida s Health Insurance Laws Relating to Rates and Access to Coverage Report Number 2000-04 August 1999 Prepared for The Florida Senate by Committee on Banking and Insurance Summary... separate

Review of Florida s Health Insurance Laws Relating to Rates and Access to Coverage Report Number 2000-04 August 1999 Prepared for The Florida Senate by Committee on Banking and Insurance Summary... separate

The Health Benefit Exchange and the Commercial Insurance Market

The Health Benefit Exchange and the Commercial Insurance Market Overview The federal health care reform law directs states to set up health insurance marketplaces, called Health Benefit Exchanges, that

The Health Benefit Exchange and the Commercial Insurance Market Overview The federal health care reform law directs states to set up health insurance marketplaces, called Health Benefit Exchanges, that

U.S. Senate Finance Committee Hearing on Health Insurance Market Reform

U.S. Senate Finance Committee Hearing on Health Insurance Market Reform Testimony of Pam MacEwan Executive Vice President, Public Affairs and Governance Group Health Cooperative September 23, 2008 Washington,

U.S. Senate Finance Committee Hearing on Health Insurance Market Reform Testimony of Pam MacEwan Executive Vice President, Public Affairs and Governance Group Health Cooperative September 23, 2008 Washington,

Romneycare Versus Obamacare

Romneycare Versus Obamacare Two Names; Same Model Maura Calsyn July 2012 Introduction Mitt Romney, the Republican Party candidate for president, says he abhors Obamacare. The Center for American Progress

Romneycare Versus Obamacare Two Names; Same Model Maura Calsyn July 2012 Introduction Mitt Romney, the Republican Party candidate for president, says he abhors Obamacare. The Center for American Progress

Breakout Session: Transition to the Market

Investing in Texas: Financing Health Coverage Expansion Conference Proceedings Breakout Session: Transition to the Market Although many Texans have been able to obtain health care through public programs

Investing in Texas: Financing Health Coverage Expansion Conference Proceedings Breakout Session: Transition to the Market Although many Texans have been able to obtain health care through public programs

to Health Care Reform

The Employer s Guide to Health Care Reform What you need to know now to: Consider your choices Decide what s best for you Follow the rules 2013-2014 Health care reform is the law of the land. Some don

The Employer s Guide to Health Care Reform What you need to know now to: Consider your choices Decide what s best for you Follow the rules 2013-2014 Health care reform is the law of the land. Some don

SOMETHING OLD, SOMETHING NEW: TEXAS TWO HIGH-RISK POOLS

July 19, 2010 Contact: Stacey Pogue, pogue@cppp.org SOMETHING OLD, SOMETHING NEW: TEXAS TWO HIGH-RISK POOLS Thanks to national health reform, Texas now has two separate high-risk pools that offer health

July 19, 2010 Contact: Stacey Pogue, pogue@cppp.org SOMETHING OLD, SOMETHING NEW: TEXAS TWO HIGH-RISK POOLS Thanks to national health reform, Texas now has two separate high-risk pools that offer health

Wisconsin typically ranks among the states with the highest level of health

Health Insurance Marketplace in Wisconsin by Wisconsin Office of the Commissioner of Insurance Staff Wisconsin typically ranks among the states with the highest level of health care coverage for its citizens.

Health Insurance Marketplace in Wisconsin by Wisconsin Office of the Commissioner of Insurance Staff Wisconsin typically ranks among the states with the highest level of health care coverage for its citizens.

The New and Temporary Federal High-Risk Insurance Pool

The New and Temporary Federal High-Risk Insurance Pool By Craig A. Conway, J.D., LL.M. (Health Law) caconway@central.uh.edu The Patient Protection and Affordable Care Act (PPACA), 1 includes several measures

The New and Temporary Federal High-Risk Insurance Pool By Craig A. Conway, J.D., LL.M. (Health Law) caconway@central.uh.edu The Patient Protection and Affordable Care Act (PPACA), 1 includes several measures

L. IRC 501(c)(15) - SMALL INSURANCE COMPANIES OR ASSOCIATIONS

(15) - SMALL INSURANCE COMPANIES OR ASSOCIATIONS") L. IRC 501(c)(15) - SMALL INSURANCE COMPANIES OR ASSOCIATIONS 1. Introduction The purpose of this section is to provide some background and an update in the area of IRC 501(c)(15) insurance companies or

L. IRC 501(c)(15) - SMALL INSURANCE COMPANIES OR ASSOCIATIONS 1. Introduction The purpose of this section is to provide some background and an update in the area of IRC 501(c)(15) insurance companies or

NEW JERSEY SMALL EMPLOYER HEALTH BENEFITS PROGRAM FIELD RESEARCH REPORT

NEW JERSEY SMALL EMPLOYER HEALTH BENEFITS PROGRAM FIELD RESEARCH REPORT I. CONTEXT Overview of Trends in New Jersey s Health Insurance Markets In 2005, New Jersey s 8.7 million residents fell into one

NEW JERSEY SMALL EMPLOYER HEALTH BENEFITS PROGRAM FIELD RESEARCH REPORT I. CONTEXT Overview of Trends in New Jersey s Health Insurance Markets In 2005, New Jersey s 8.7 million residents fell into one

Preliminary Health Insurance Landscape Analysis

Preliminary Health Insurance Landscape Analysis Prior to addressing some of the issues listed under Section 3.1 3.5 of the HRSA State Planning Grant report template, here is some of the information available

Preliminary Health Insurance Landscape Analysis Prior to addressing some of the issues listed under Section 3.1 3.5 of the HRSA State Planning Grant report template, here is some of the information available

Medigap Coverage for Prescription Drugs. Statement of Deborah J. Chollet, Senior Fellow Mathematica Policy Research, Inc.

Medigap Coverage for Prescription Drugs Statement of Deborah J. Chollet, Senior Fellow Mathematica Policy Research, Inc. Washington, DC Testimony before the U.S. Senate Committee on Finance Finding the

Medigap Coverage for Prescription Drugs Statement of Deborah J. Chollet, Senior Fellow Mathematica Policy Research, Inc. Washington, DC Testimony before the U.S. Senate Committee on Finance Finding the

Health Care Reform Frequently Asked Questions (FAQ) Consumers Employers

Consumers Employers") This page provides answers to frequently asked questions (FAQ) regarding The Patient Protection and Affordable Care Act (PPACA; P.L. 111-148) and the Health Care and Education Reconciliation Act of 2010

This page provides answers to frequently asked questions (FAQ) regarding The Patient Protection and Affordable Care Act (PPACA; P.L. 111-148) and the Health Care and Education Reconciliation Act of 2010

Exchanges and the ACA What You Need to Know for 2014

Exchanges and the ACA What You Need to Know for 2014 How the Affordable Care Act affects the Individual Health Insurance Market This presentation is for informational purposes only and does not constitute

Exchanges and the ACA What You Need to Know for 2014 How the Affordable Care Act affects the Individual Health Insurance Market This presentation is for informational purposes only and does not constitute

MANDATING HEALTH INSURANCE: WOULD THE MASSACHUSETTS PLAN WORK FOR MARYLAND?

MANDATING HEALTH INSURANCE: WOULD THE MASSACHUSETTS PLAN WORK FOR MARYLAND? MARC KILMER Recent surveys indicate roughly 16 percent of Maryland s population has no health insurance. Only 22 states have

MANDATING HEALTH INSURANCE: WOULD THE MASSACHUSETTS PLAN WORK FOR MARYLAND? MARC KILMER Recent surveys indicate roughly 16 percent of Maryland s population has no health insurance. Only 22 states have

CERTIFICATION OF ENROLLMENT ENGROSSED SUBSTITUTE SENATE BILL 6333. 60th Legislature 2008 Regular Session

CERTIFICATION OF ENROLLMENT ENGROSSED SUBSTITUTE SENATE BILL 6333 60th Legislature 2008 Regular Session Passed by the Senate March 10, 2008 YEAS 28 NAYS 18 President of the Senate Passed by the House March

CERTIFICATION OF ENROLLMENT ENGROSSED SUBSTITUTE SENATE BILL 6333 60th Legislature 2008 Regular Session Passed by the Senate March 10, 2008 YEAS 28 NAYS 18 President of the Senate Passed by the House March

Healthcare Reform Preparedness for Small Businesses

Healthcare Reform Preparedness for Small Businesses Blue KC on Wheels Community awareness initiative Health screenings Wellness information Seminars on healthcare reform, health insurance and wellness

Healthcare Reform Preparedness for Small Businesses Blue KC on Wheels Community awareness initiative Health screenings Wellness information Seminars on healthcare reform, health insurance and wellness

Comparison of Major Health Care Reform Proposals Using League of Women Voters of California Evaluation Criteria September 9, 2007

Comparison of Major Health Care Reform Proposals Using League of Women Voters of California Evaluation Criteria September 9, 2007 Section I: Elements Supported by the LWVC Elements SB 840 (Kuehl) AB 8

Comparison of Major Health Care Reform Proposals Using League of Women Voters of California Evaluation Criteria September 9, 2007 Section I: Elements Supported by the LWVC Elements SB 840 (Kuehl) AB 8

Here in Oklahoma we have an interesting story to tell. Our economy is growing through sectors

HEALTH CARE It goes without saying that health care reform remains the focus of a great deal of debate and attention even after all the years since the Patient Protection and Affordable Care Act, or Obamacare,

HEALTH CARE It goes without saying that health care reform remains the focus of a great deal of debate and attention even after all the years since the Patient Protection and Affordable Care Act, or Obamacare,

HEALTH CARE REFORM FREQUENTLY ASKED QUESTIONS

HEALTH CARE REFORM FREQUENTLY ASKED QUESTIONS Consumers When will the health care reform law take effect? The health insurance reforms adopted as part of the Patient Protection and Affordable Care Act

HEALTH CARE REFORM FREQUENTLY ASKED QUESTIONS Consumers When will the health care reform law take effect? The health insurance reforms adopted as part of the Patient Protection and Affordable Care Act

Private Insurance Fundamentals: Health Insurance Coverage, the Market, and Insurance Regulation. Bernadette Fernandez February 25, 2011

Private Insurance Fundamentals: Health Insurance Coverage, the Market, and Insurance Regulation Bernadette Fernandez February 25, 2011 Health Insurance Insurance provides protection from economic loss

Private Insurance Fundamentals: Health Insurance Coverage, the Market, and Insurance Regulation Bernadette Fernandez February 25, 2011 Health Insurance Insurance provides protection from economic loss

THE MASSACHUSETTS HEALTH CARE REFORM ACT: WHAT MUST EMPLOYERS DO?

JULY 11, 2007 VOLUME 3, NUMBER 5 Employers nationwide need to understand what is happening in Massachusetts. THE MASSACHUSETTS HEALTH CARE REFORM ACT: WHAT MUST EMPLOYERS DO? by Katherine J. Utz* kutz@utzmiller.com

JULY 11, 2007 VOLUME 3, NUMBER 5 Employers nationwide need to understand what is happening in Massachusetts. THE MASSACHUSETTS HEALTH CARE REFORM ACT: WHAT MUST EMPLOYERS DO? by Katherine J. Utz* kutz@utzmiller.com

Ronald Riner, MD. The Riner Group, Inc. 5811 Pelican Bay Blvd., Suite 210 Naples, FL 34108 800.965.8485 www.rinergroup.com

Impact of Healthcare Reform on Small Business January 12, 2011 Ronald Riner, MD The Riner Group, Inc. 5811 Pelican Bay Blvd., Suite 210 Naples, FL 34108 800.965.8485 www.rinergroup.com Healthcare Reform

Impact of Healthcare Reform on Small Business January 12, 2011 Ronald Riner, MD The Riner Group, Inc. 5811 Pelican Bay Blvd., Suite 210 Naples, FL 34108 800.965.8485 www.rinergroup.com Healthcare Reform

What Can We Learn About Federal ERISA Law from Maryland s Court Decision?

What Can We Learn About Federal ERISA Law from Maryland s Court Decision? Patricia A. Butler, JD, Dr.P.H. Family Impact Seminar January 24, 2007 Presentation Overview Background on ERISA preemption provisions

What Can We Learn About Federal ERISA Law from Maryland s Court Decision? Patricia A. Butler, JD, Dr.P.H. Family Impact Seminar January 24, 2007 Presentation Overview Background on ERISA preemption provisions

GENDER RATING IN HEALTH INSURANCE

GENDER RATING IN HEALTH INSURANCE Colorado Health Care Task Force August 10, 2009 By Richard Cauchi Program Director, Health Program - Denver National Conference of State Legislatures rev. 8/9/09 1 What

GENDER RATING IN HEALTH INSURANCE Colorado Health Care Task Force August 10, 2009 By Richard Cauchi Program Director, Health Program - Denver National Conference of State Legislatures rev. 8/9/09 1 What

WHAT COULD YOU DO WITH $70 BILLION DOLLARS? HR 676: Healthcare Savings for Healthier Cities

WHAT COULD YOU DO WITH $70 BILLION DOLLARS? HR 676: Healthcare Savings for Healthier Cities The ABCs of Improved Medicare-for-All A Primer for the Kingston City School District Here s an example of how

WHAT COULD YOU DO WITH $70 BILLION DOLLARS? HR 676: Healthcare Savings for Healthier Cities The ABCs of Improved Medicare-for-All A Primer for the Kingston City School District Here s an example of how

In preparing the February 2014 baseline budget

APPENDIX B Updated Estimates of the Insurance Coverage Provisions of the Affordable Care Act In preparing the February 2014 baseline budget projections, the Congressional Budget Office () and the staff

APPENDIX B Updated Estimates of the Insurance Coverage Provisions of the Affordable Care Act In preparing the February 2014 baseline budget projections, the Congressional Budget Office () and the staff

Coinsurance A percentage of a health care provider's charge for which the patient is financially responsible under the terms of the policy.

Glossary of Health Insurance Terms On March 23, 2010, President Obama signed the Patient Protection and Affordable Care Act (PPACA) into law. When making decisions about health coverage, consumers should

Glossary of Health Insurance Terms On March 23, 2010, President Obama signed the Patient Protection and Affordable Care Act (PPACA) into law. When making decisions about health coverage, consumers should

Arizona State Senate Issue Brief June 22, 2010 SMALL BUSINESS HEALTH INSURANCE. Overview. What is a Small Business? Note to Reader: INTRODUCTION

Arizona State Senate Issue Brief June 22, 2010 Note to Reader: The Senate Research Staff provides nonpartisan, objective legislative research, policy analysis and related assistance to the members of the

Arizona State Senate Issue Brief June 22, 2010 Note to Reader: The Senate Research Staff provides nonpartisan, objective legislative research, policy analysis and related assistance to the members of the

Countdown to Healthcare Reform

Newtek Insurance Agency & Town of North Hempstead Business & Tourism Development Corp Countdown to Healthcare Reform Presented by: Kyle Sloane Senior Vice President Newtek Insurance Agency Newtek Insurance

Newtek Insurance Agency & Town of North Hempstead Business & Tourism Development Corp Countdown to Healthcare Reform Presented by: Kyle Sloane Senior Vice President Newtek Insurance Agency Newtek Insurance

The Massachusetts Health Reform Law: Public Opinion and Perception

The Massachusetts Health Reform Law: Public Opinion and Perception A REPORT FOR THE BLUE CROSS BLUE SHIELD OF MASSACHUSETTS FOUNDATION November 2006 Robert J. Blendon Tami Buhr Channtal Fleischfresser

The Massachusetts Health Reform Law: Public Opinion and Perception A REPORT FOR THE BLUE CROSS BLUE SHIELD OF MASSACHUSETTS FOUNDATION November 2006 Robert J. Blendon Tami Buhr Channtal Fleischfresser

Summary. Main features of the current US health system. Changes brought by the Obama reform. Effects on the Insurance market.

00.05. Health Reform US Health CareUS Reform 00.05. Summary Main features of the current US health system Changes brought by the Obama reform Effects on the Insurance market Challenges ahead 00.05. US

00.05. Health Reform US Health CareUS Reform 00.05. Summary Main features of the current US health system Changes brought by the Obama reform Effects on the Insurance market Challenges ahead 00.05. US

The Impact of Guaranteed Issue and Community Rating Reforms on States Individual Insurance Markets

The Impact of Guaranteed Issue and Community Rating Reforms on States Individual Insurance Markets prepared for America s Health Insurance Plans March 2012 By: Leigh Wachenheim, FSA, MAAA Principal & Consulting

The Impact of Guaranteed Issue and Community Rating Reforms on States Individual Insurance Markets prepared for America s Health Insurance Plans March 2012 By: Leigh Wachenheim, FSA, MAAA Principal & Consulting

How To Pass The Health Care Bill

Timeline/Summary of Tax s in the Health Reform Laws Effective Date Retrospective to Enactment Health professionals State loan repayment tax relief. Excludes from gross income payments made under any State

Timeline/Summary of Tax s in the Health Reform Laws Effective Date Retrospective to Enactment Health professionals State loan repayment tax relief. Excludes from gross income payments made under any State

A Consumer Guide to Creating a Health Insurance Connector

A Consumer Guide to Creating a Health Insurance Connector July 2007 Christine Barber and Michael Miller State Consumer Health Advocacy Program Community Catalyst, Inc. 30 Winter St. 10 th Floor Boston,

A Consumer Guide to Creating a Health Insurance Connector July 2007 Christine Barber and Michael Miller State Consumer Health Advocacy Program Community Catalyst, Inc. 30 Winter St. 10 th Floor Boston,

Comparison of California Health Coverage Expansion Proposals

Note: A comparison of the Senate Republican proposal for the special session, CalCare Plus will be available shortly. Californians to Be Covered 1 Consumers/ Individuals Treatment of Self-Employed Employers

Note: A comparison of the Senate Republican proposal for the special session, CalCare Plus will be available shortly. Californians to Be Covered 1 Consumers/ Individuals Treatment of Self-Employed Employers

ADVERSE SELECTION ISSUES AND HEALTH INSURANCE EXCHANGES UNDER THE AFFORDABLE CARE ACT

Draft: 6/22/11 Reflects revisions to the June 17 draft as discussed during the Health Insurance and Managed Care (B) Committee conference call June 22, 2011 Background ADVERSE SELECTION ISSUES AND HEALTH

Draft: 6/22/11 Reflects revisions to the June 17 draft as discussed during the Health Insurance and Managed Care (B) Committee conference call June 22, 2011 Background ADVERSE SELECTION ISSUES AND HEALTH

The Role of Insurance Agents and Brokers Under Health Care Reform

T HE J AECKLE A LERT HEALTH CARE PRACTICE GROUP ATTORNEY ADVERTISING The Role of Insurance Agents and Brokers Under Health Care Reform The New York Health Benefit Exchange, the health insurance exchange

T HE J AECKLE A LERT HEALTH CARE PRACTICE GROUP ATTORNEY ADVERTISING The Role of Insurance Agents and Brokers Under Health Care Reform The New York Health Benefit Exchange, the health insurance exchange

America s Health Insurance Plans. Guaranteeing Access. to Coverage for All Americans

America s Health Insurance Plans Guaranteeing Access to Coverage for All Americans Our Commitment The members of (AHIP) believe that all Americans regardless of health status or income should have access

America s Health Insurance Plans Guaranteeing Access to Coverage for All Americans Our Commitment The members of (AHIP) believe that all Americans regardless of health status or income should have access

CAHI Policy Brief: Is There Really An Uninsured Children s Epidemic? Council for Affordable Health Insurance. Introduction

CAHI Policy Brief: Council for Affordable Health Insurance Is There Really An Uninsured Children s Epidemic? Volume 1, Number 1 April 1, 1997 112 S. West Street Suite 400 Alexandria, VA 22314 Phone: (703)

CAHI Policy Brief: Council for Affordable Health Insurance Is There Really An Uninsured Children s Epidemic? Volume 1, Number 1 April 1, 1997 112 S. West Street Suite 400 Alexandria, VA 22314 Phone: (703)

March 9, 2016. Update on the Affordable Care Act and Student Insurance

March 9, 2016 Update on the Affordable Care Act and Student Insurance Agenda 2 Background ACA Impact to Student Health Plan Student Health Options UNC Student Health Insurance Offerings Legislative and

March 9, 2016 Update on the Affordable Care Act and Student Insurance Agenda 2 Background ACA Impact to Student Health Plan Student Health Options UNC Student Health Insurance Offerings Legislative and

What the Health Care Reform Bill Means to Employers

What the Health Care Reform Bill Means to Employers No doubt you have heard the news that on Tuesday, March 23, 2010, President Obama signed into law sweeping health care overhaul legislation. This followed

What the Health Care Reform Bill Means to Employers No doubt you have heard the news that on Tuesday, March 23, 2010, President Obama signed into law sweeping health care overhaul legislation. This followed

Health Care Reform: Policy Implications for the Future

Health Care Reform: Policy Implications for the Future Michigan Primary Care Association Douglas M. Paterson, MPA Director of State Policy Promoting, supporting, and developing comprehensive, accessible,

Health Care Reform: Policy Implications for the Future Michigan Primary Care Association Douglas M. Paterson, MPA Director of State Policy Promoting, supporting, and developing comprehensive, accessible,

INSURING THE HEALTHY OR INSURING THE SICK? THE DILEMMA OF REGULATING THE INDIVIDUAL HEALTH INSURANCE MARKET

INSURING THE HEALTHY OR INSURING THE SICK? THE DILEMMA OF REGULATING THE INDIVIDUAL HEALTH INSURANCE MARKET FINDINGS FROM A STUDY OF SEVEN STATES Nancy C. Turnbull and Nancy M. Kane Harvard School of Public

INSURING THE HEALTHY OR INSURING THE SICK? THE DILEMMA OF REGULATING THE INDIVIDUAL HEALTH INSURANCE MARKET FINDINGS FROM A STUDY OF SEVEN STATES Nancy C. Turnbull and Nancy M. Kane Harvard School of Public

The New Bipartisan Consensus for an Individual Mandate

HEALTH POLICY CENTER The New Bipartisan Consensus for an Individual Mandate Linda J. Blumberg and John Holahan April 2015 In Brief The individual responsibility requirement, most often referred to as the

HEALTH POLICY CENTER The New Bipartisan Consensus for an Individual Mandate Linda J. Blumberg and John Holahan April 2015 In Brief The individual responsibility requirement, most often referred to as the

Health Insurance Options for Small Business Employers

Health Insurance Options for Small Business Employers April 2, 2008 Insure the Uninsured Project Rebecca Pizzitola and Lucien Wulsin, Jr. www.itup.org Funded by: L.A. Care Health Plan The California Endowment

Health Insurance Options for Small Business Employers April 2, 2008 Insure the Uninsured Project Rebecca Pizzitola and Lucien Wulsin, Jr. www.itup.org Funded by: L.A. Care Health Plan The California Endowment

Kansas Health Policy Authority Small Business Health Insurance Steering Committee

How Health Coverage Works: Coverage Delivery, Risk Assessment, and Regulation The following summarizes the document How Private Health Coverage Works: A Primer 2008 Update published by the Kaiser Family

How Health Coverage Works: Coverage Delivery, Risk Assessment, and Regulation The following summarizes the document How Private Health Coverage Works: A Primer 2008 Update published by the Kaiser Family

California Health Benefits Exchange Backgrounder January 2012

California Health Benefits Exchange Backgrounder January 2012 The implementation of the California Health Benefits Exchange, California s place for health care providers to compete for customers, is expected

California Health Benefits Exchange Backgrounder January 2012 The implementation of the California Health Benefits Exchange, California s place for health care providers to compete for customers, is expected

Joint Select Committee on Health Care Reform

LD 1611 An Act To Provide Affordable Health Insurance to Small Businesses and Individuals and To Control Health Care Costs PUBLIC 469 Sponsor(s) Committee Report Amendments Adopted O'NEIL OTP-AM H-565

LD 1611 An Act To Provide Affordable Health Insurance to Small Businesses and Individuals and To Control Health Care Costs PUBLIC 469 Sponsor(s) Committee Report Amendments Adopted O'NEIL OTP-AM H-565

Medical Insurance for Retirees: Basics You Need to Know Last update: June 3, 2014

Summary Medical Insurance for Retirees: Basics You Need to Know Last update: June 3, 2014 For most of us, medical insurance is important because it guards us against catastrophic financial losses if we

Summary Medical Insurance for Retirees: Basics You Need to Know Last update: June 3, 2014 For most of us, medical insurance is important because it guards us against catastrophic financial losses if we

Health insurance Marketplace. What to expect in 2014

Health insurance Marketplace What to expect in 2014 Overview The Affordable Care Act (ACA) includes several provisions geared to extend greater access to health insurance benefits to more people. Beginning

Health insurance Marketplace What to expect in 2014 Overview The Affordable Care Act (ACA) includes several provisions geared to extend greater access to health insurance benefits to more people. Beginning

ACA Premium Impact Variability of Individual Market Premium Rate Changes Robert M. Damler, FSA, MAAA Paul R. Houchens, FSA, MAAA

ACA Premium Impact Variability of Individual Market Premium Rate Changes Robert M. Damler, FSA, MAAA Paul R. Houchens, FSA, MAAA BACKGROUND The Patient Protection and Affordable Care Act (ACA) introduces

ACA Premium Impact Variability of Individual Market Premium Rate Changes Robert M. Damler, FSA, MAAA Paul R. Houchens, FSA, MAAA BACKGROUND The Patient Protection and Affordable Care Act (ACA) introduces

State Health Insurance Reform: Experience With Community Rating And Guaranteed Issue In The Small Group And Individual Markets

State Health Insurance Reform: Experience With Community Rating And Guaranteed Issue In The Small Group And Individual Markets Prepared By The Technical Committee of The Council for Affordable Health Insurance

State Health Insurance Reform: Experience With Community Rating And Guaranteed Issue In The Small Group And Individual Markets Prepared By The Technical Committee of The Council for Affordable Health Insurance

State of Wisconsin / OFFICE OF THE COMMISSIONER OF INSURANCE

State of Wisconsin / OFFICE OF THE COMMISSIONER OF INSURANCE Scott Walker, Governor Theodore K. Nickel, Commissioner Wisconsin.gov 125 South Webster Street P.O. Box 7873 Madison, Wisconsin 53707-7873 Phone:

State of Wisconsin / OFFICE OF THE COMMISSIONER OF INSURANCE Scott Walker, Governor Theodore K. Nickel, Commissioner Wisconsin.gov 125 South Webster Street P.O. Box 7873 Madison, Wisconsin 53707-7873 Phone:

Your Bo'om Line: What Health Reform Means For Illinois Small Businesses

Your Bo'om Line: What Health Reform Means For Illinois Small Businesses Jessica Stone and Rhett Buttle, Small Business Majority Jim Duffett, Campaign for Better Health Care Lina Choudhry Rashid, U.S. Department

Your Bo'om Line: What Health Reform Means For Illinois Small Businesses Jessica Stone and Rhett Buttle, Small Business Majority Jim Duffett, Campaign for Better Health Care Lina Choudhry Rashid, U.S. Department

Briefing Paper. Cape Cod Municipal Health Group

Briefing Paper for the Cape Cod Municipal Health Group Parts of Medicare Medicare Supplement Plans Medicare Advantage Plans Medicare Part D Plans, Employer Group Waiver Plans (EGWPs) Medicare Secondary

Briefing Paper for the Cape Cod Municipal Health Group Parts of Medicare Medicare Supplement Plans Medicare Advantage Plans Medicare Part D Plans, Employer Group Waiver Plans (EGWPs) Medicare Secondary

Update. Director of Policy and National Health Care Reform Coordinator. Roni Mansur Chief Operating Officer. Board of Directors Meeting March 8, 2012

National Health Care Reform Update Kaitlyn Kenney Director of Policy and National Health Care Reform Coordinator Roni Mansur Chief Operating Officer Board of Directors Meeting March 8, 2012 Agenda Update

National Health Care Reform Update Kaitlyn Kenney Director of Policy and National Health Care Reform Coordinator Roni Mansur Chief Operating Officer Board of Directors Meeting March 8, 2012 Agenda Update

www.thinkhr.com 877-225-1101 Employer Health Reform Checklist

www.thinkhr.com 877-225-1101 Employer Health ThinkHR grants the reader non-exclusive, non-transferable, and limited permission to use this document. The reader may not sell or otherwise use this document

www.thinkhr.com 877-225-1101 Employer Health ThinkHR grants the reader non-exclusive, non-transferable, and limited permission to use this document. The reader may not sell or otherwise use this document

Health Insurance 101. A brief overview of health insurance 10/15/09

Health Insurance 101 A brief overview of health insurance 10/15/09 Health Care vs. Health Insurance Health Care is Provision of Medical Services by Private Physicians and Hospitals (private pay or insurance)

Health Insurance 101 A brief overview of health insurance 10/15/09 Health Care vs. Health Insurance Health Care is Provision of Medical Services by Private Physicians and Hospitals (private pay or insurance)

Medicare Explained (For the rest of us!) A plain English version

A plain English version") Produced by & Not affiliated with any Government Agency A Brief History of Medicare Medicare is a national social insurance program, administered by the U.S. federal government since 1965, that guarantees

Produced by & Not affiliated with any Government Agency A Brief History of Medicare Medicare is a national social insurance program, administered by the U.S. federal government since 1965, that guarantees

WILL HEALTH CARE REFORM CAUSE EMPLOYERS TO DROP THEIR EMPLOYEE HEALTH CARE PLANS?

WILL HEALTH CARE REFORM CAUSE EMPLOYERS TO DROP THEIR EMPLOYEE HEALTH CARE PLANS? In the wake of the passage of the Patient Protection and Affordable Care Act and the Health Care Education and Reconciliation

WILL HEALTH CARE REFORM CAUSE EMPLOYERS TO DROP THEIR EMPLOYEE HEALTH CARE PLANS? In the wake of the passage of the Patient Protection and Affordable Care Act and the Health Care Education and Reconciliation

Health Insurance Buyers Guide. What You Need to Know to Get Started

Health Insurance Buyers Guide What You Need to Know to Get Started Time to Enroll The Affordable Care Act has changed the way that many people get health insurance. You may have more options and more ways

Health Insurance Buyers Guide What You Need to Know to Get Started Time to Enroll The Affordable Care Act has changed the way that many people get health insurance. You may have more options and more ways

Squaring the Circle? Reforming the U.S. Health Care System Karen Davenport 1

FOKUS AMERIKA Almut Wieland-Karimi 1023 15 th Street NW, # 801 Washington, DC 20005 USA Tel.: +1 202 408 5444 Fax: +1 202 408 5537 fesdc@fesdc.org www.fesdc.org Nr. 2 / 2009 Squaring the Circle? Reforming

FOKUS AMERIKA Almut Wieland-Karimi 1023 15 th Street NW, # 801 Washington, DC 20005 USA Tel.: +1 202 408 5444 Fax: +1 202 408 5537 fesdc@fesdc.org www.fesdc.org Nr. 2 / 2009 Squaring the Circle? Reforming

Kansas Insurance Department

Kansas Insurance Department A Kansas Guide to Health Insurance Changes Public Policy Session Panel Discussion KAMU Annual Conference Sept. 26, 2013 Sandy Praeger, Commissioner of Insurance 2014 Affordable

Kansas Insurance Department A Kansas Guide to Health Insurance Changes Public Policy Session Panel Discussion KAMU Annual Conference Sept. 26, 2013 Sandy Praeger, Commissioner of Insurance 2014 Affordable

Updated Estimates for the Insurance Coverage Provisions of the Affordable Care Act

MARCH 2012 Updated Estimates for the Insurance Coverage Provisions of the Affordable Care Act In preparing the March 2012 baseline budget projections, the Congressional Budget Office (CBO) and the staff

MARCH 2012 Updated Estimates for the Insurance Coverage Provisions of the Affordable Care Act In preparing the March 2012 baseline budget projections, the Congressional Budget Office (CBO) and the staff

Exchange 101. August 2013

Exchange 101 August 2013 455430 27517 Penalties for individuals 2017 and beyond: Annual adjustments 2016: Greater of $695 or 2.5% of taxable income 2015: Greater of $325 or 2% of taxable income 2014: Greater

Exchange 101 August 2013 455430 27517 Penalties for individuals 2017 and beyond: Annual adjustments 2016: Greater of $695 or 2.5% of taxable income 2015: Greater of $325 or 2% of taxable income 2014: Greater

Health Care Reform Management Alert Series Roadmap of Plan Changes Needed For Upcoming Plan Years

Health Care Reform Management Alert Series Roadmap of Plan Changes Needed For Upcoming Plan Years Seyfarth Shaw has generously given permission to Lawyers Alliance for New York to circulate this chart

Health Care Reform Management Alert Series Roadmap of Plan Changes Needed For Upcoming Plan Years Seyfarth Shaw has generously given permission to Lawyers Alliance for New York to circulate this chart

TESTIMONY OF JUDITH SOLOMON HOUSE BILL 700, THE PENNSYLVANIA HEALTH CARE REFORM ACT HOUSE INSURANCE COMMITTEE MAY 3, 2007

820 First Street NE Suite 510 Washington DC 20002 (202)408-1080 fax (202)408-1056 center@cbpp.org www.cbpp.org TESTIMONY OF JUDITH SOLOMON HOUSE BILL 700, THE PENNSYLVANIA HEALTH CARE REFORM ACT HOUSE

820 First Street NE Suite 510 Washington DC 20002 (202)408-1080 fax (202)408-1056 center@cbpp.org www.cbpp.org TESTIMONY OF JUDITH SOLOMON HOUSE BILL 700, THE PENNSYLVANIA HEALTH CARE REFORM ACT HOUSE

Health Care Reform How it Will Affect Employers and their Group Health Plans. Benecon Comments and Observations

Health Care Reform How it Will Affect Employers and their Group Health Plans This Health Care Reform Summary applies to all employers (including government and church plans) that provide health coverage

Health Care Reform How it Will Affect Employers and their Group Health Plans This Health Care Reform Summary applies to all employers (including government and church plans) that provide health coverage

Putting the 'Insurance' Back in Health Insurance - Forbes

Avik Roy, Contributor The Apothecary is a blog about health-care and entitlement reform. PHARMA & HEALTHCARE 5/21/2012 @ 12:55AM 28,608 views Putting the 'Insurance' Back in Health Insurance We understand

Avik Roy, Contributor The Apothecary is a blog about health-care and entitlement reform. PHARMA & HEALTHCARE 5/21/2012 @ 12:55AM 28,608 views Putting the 'Insurance' Back in Health Insurance We understand

Massachusetts Health Care Reform and Cancer Care. Therese Mulvey, MD Southcoast Centers for Cancer Care February 2010

Massachusetts Health Care Reform and Cancer Care Therese Mulvey, MD Southcoast Centers for Cancer Care February 2010 Southcoast Health System in Massachusetts Southcoast Primary and Secondary Markets An

Massachusetts Health Care Reform and Cancer Care Therese Mulvey, MD Southcoast Centers for Cancer Care February 2010 Southcoast Health System in Massachusetts Southcoast Primary and Secondary Markets An

Affordable Care Act FAQs

Note: This material is not intended to serve as legal advice and only constitutes Delta Dental s opinion on the subject matter contained herein based on its own review of available guidance. Delta Dental

Note: This material is not intended to serve as legal advice and only constitutes Delta Dental s opinion on the subject matter contained herein based on its own review of available guidance. Delta Dental

POLICYBRIEF. By John Garen, Ph.D.

POLICYBRIEF By John Garen, Ph.D. Recently, the creation of health insurance exchanges in Kentucky has come to the forefront. The Patient Protection and Affordable Care Act (PPACA) often called Obamacare

POLICYBRIEF By John Garen, Ph.D. Recently, the creation of health insurance exchanges in Kentucky has come to the forefront. The Patient Protection and Affordable Care Act (PPACA) often called Obamacare

Universal Health Care

Universal Health Care By John Steen (written August 2005) Consultant in Health Planning, Health Regulation, and Public Health The last attempt to formulate a national plan for universal health care ended

Universal Health Care By John Steen (written August 2005) Consultant in Health Planning, Health Regulation, and Public Health The last attempt to formulate a national plan for universal health care ended

Presentation for Licensed Producers The Affordable Care Act

Presentation for Licensed Producers The Affordable Care Act Bruce Donaldson, CHC Producer & Stakeholder Specialist Arkansas Insurance Department Affordable Care Act The ACA was passed by Congress and signed

Presentation for Licensed Producers The Affordable Care Act Bruce Donaldson, CHC Producer & Stakeholder Specialist Arkansas Insurance Department Affordable Care Act The ACA was passed by Congress and signed

A HEALTH INSURANCE EXCHANGE FOR MARYLAND? Comparing Massachusetts and Maryland

Maryland Association of Health Underwriters National Association of Insurance and Financial Advisors of Maryland A HEALTH INSURANCE EXCHANGE FOR MARYLAND? Comparing Massachusetts and Maryland Robert L.

Maryland Association of Health Underwriters National Association of Insurance and Financial Advisors of Maryland A HEALTH INSURANCE EXCHANGE FOR MARYLAND? Comparing Massachusetts and Maryland Robert L.

State Health Insurance Index 2006: A 50-State Comparison of the Nation s Health Insurance Market

State Health Insurance Index 2006: A 50-State Comparison of the Nation s Health Insurance Market Merrill Matthews, Ph.D., Director Victoria Craig Bunce, Director of Research and Policy JP Wieske, Director

State Health Insurance Index 2006: A 50-State Comparison of the Nation s Health Insurance Market Merrill Matthews, Ph.D., Director Victoria Craig Bunce, Director of Research and Policy JP Wieske, Director

KANSAS HEALTH POLICY AUTHORITY LEGISLATIVE COORDINATING COUNCIL STUDIES #13 Young Adult Policy Options and #15 Small Business Health Reform Options

KANSAS HEALTH POLICY AUTHORITY LEGISLATIVE COORDINATING COUNCIL STUDIES #13 Young Adult Policy Options and #15 Small Business Health Reform Options INTRODUCTION In 2008, the Kansas Legislature s Joint

KANSAS HEALTH POLICY AUTHORITY LEGISLATIVE COORDINATING COUNCIL STUDIES #13 Young Adult Policy Options and #15 Small Business Health Reform Options INTRODUCTION In 2008, the Kansas Legislature s Joint

LWVSD UNIT PRESENTATION, SEPTEMBER, 2009 "HEALTHCARE: HELPING YOU FOLLOW THE DEBATE"

LWVSD UNIT PRESENTATION, SEPTEMBER, 2009 "HEALTHCARE: HELPING YOU FOLLOW THE DEBATE" Luncheons a) Tuesday, September 22nd - Retired State Senator Sheila Kuehl, "What's So Great About Single Payer Healthcare".

LWVSD UNIT PRESENTATION, SEPTEMBER, 2009 "HEALTHCARE: HELPING YOU FOLLOW THE DEBATE" Luncheons a) Tuesday, September 22nd - Retired State Senator Sheila Kuehl, "What's So Great About Single Payer Healthcare".

STUDY OF STATE CONTRIBUTIONS TO STATE EMPLOYEE HEALTH INSURANCE PREMIUMS - BACKGROUND MEMORANDUM

17.9025.01000 Prepared for the Government Finance Committee STUDY OF STATE CONTRIBUTIONS TO STATE EMPLOYEE HEALTH INSURANCE PREMIUMS - BACKGROUND MEMORANDUM STUDY RESPONSIBILITIES House Concurrent Resolution

17.9025.01000 Prepared for the Government Finance Committee STUDY OF STATE CONTRIBUTIONS TO STATE EMPLOYEE HEALTH INSURANCE PREMIUMS - BACKGROUND MEMORANDUM STUDY RESPONSIBILITIES House Concurrent Resolution

Health Insurance Reform in Kansas - A Model For Success

Draft Health Reform Plan Roadmap 1. Goals for June 20 th KHPA Board Meeting Review demographics of Kansas uninsured Review of 2005 Mercer health insurance study (in reference section) Determine overarching

Draft Health Reform Plan Roadmap 1. Goals for June 20 th KHPA Board Meeting Review demographics of Kansas uninsured Review of 2005 Mercer health insurance study (in reference section) Determine overarching