More VA loan approvals and more closings

|

|

|

- Noel Robertson

- 8 years ago

- Views:

Transcription

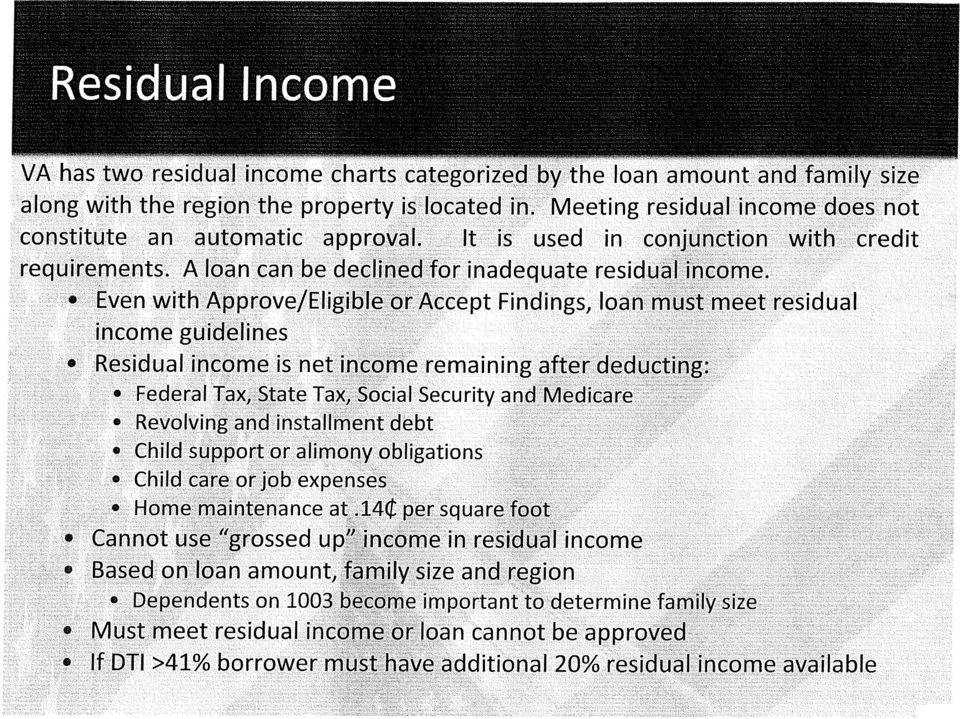

1 More VA loan approvals and more closings VA loans remain a very desirable and profitable product. As with most loan applications, a good submission equals a good approval. Here are some tips specific to VA loans Most commonly missed items on a VA application that hinder Underwriters abilities to formally approve a loan. 1. Dependents and their ages (size of veteran s family determines their residual income guideline) See charts provided for State and Family size & how to calculate residual income 2. Funding Fee this is determined by the Certificate of Eligibility This is a required document that MUST be in the file upon submission (due to the recent issues with Broker s and their ability to access the VA portal REMN can try to obtain as long as we have a signed application and a copy of the Veteran s DD214 or paystub if they are active military) Brokers can also fax the form to their Regional Loan Center) Paper forms of the Certificate of Eligibility are no longer Valid 3. Fully employment information a. Recently discharged Veterans if they are on the current civilian job less than 12 months from being discharged from the Service they MUST provide proof that the job the preformed for the US Military is in the same line of work as their Civilian job the Veteran needs to provide his DD214 (discharge papers) that will state what their duties where in the military and they MUST provide a signed LOX from the Veteran explaining how their training in the military prepared them for their civilian job. EXAMPLE: ACCEPTABLE: Veteran was an MP (military police) and is now a Police officer this is acceptable NOT ACCEPTABLE: Veteran worked in the Armory and is now and IT specialist for a private company. b. ETS Estimate Time of Separation for ACTIVE Military ONLY this is noted on the top of the Veteran s Paystub and it is also confirmed by the Commanding Officer Letter that is required in lieu of a Verbal VOE when a Veteran is going to be discharged from the Service within 12 months of the closing date the Veteran must provide one of the following: 1. Documentation that the Veteran has already re-enlisted or extended his/her period of active duty to a date beyond the 12 month period following the projected closing of the loan must provide new military orders supporting this 2. Verification that the Veteran has obtained Valid offer of local Civilian employment the Veteran must qualify on the income he will be earning on this new job not his military income and must also meet the recently discharged Veteran s rule listed above in #3a.

2 3. Statement from Veteran that he/she intends to re-enlist or extend his/her active duty and it MUST be confirmed by their Commanding Officer that such reenlistment or extension of active duty will be granted 4. MANUAL UNDERWRITTEN LOANS REFER ON DU many brokers do not read their DU findings it will state specifically what is needed on the loan for an underwriter to grant the approval. Please keep in mind this does not mean the lender will automatically approve a REFER on DU. Majority of the time the reason for the refer is bad credit whether recent or old, low fico scores and High DTI s. For the VA underwriter to approve a Manual underwritten loan we MUST have the following and then the file MUST go to upper management to approve the manual u/w a. 12 months cancelled rent checks on purchase deals if your Veteran does not have a history of making rental payments it is going to be very difficult for us to approve a refer DU 9 times out of 10 without proof we cannot proceed with the loan this is a MAJOR comp Factor b. Compensating factors please see chart provided if your Veteran has min. funds, lack of credit or bad credit, high DTI how are we approving the loan the broker must review the list provided and send in a statement as to what the compensating factors are on their loan (remember if you provide nothing you are leaving just the borrower s credit profile for us to Make a decision) COMMON ISSUES OR LACK OF COMMUNICATION THAT MAY DELAY A REVIEW OF YOUR LOAN Most common complaints by underwriters is the lack of communication regarding when VA appraisal are available. It is just as a much the broker s responsibility to inform their VA underwriter when a VA appraisal is available for review. Paid receipt for VA purchases do to the high volume of VA appraisers complaining that they are not paid in a timely manner on their services, REMN and many other lenders have taken the position that a PAID receipt prior to a CTC being issued PLEASE NOTE: BORROWERS CANNOT PAY FOR THE APPRAISAL DIRECTLY TO THE APPRAISER THIS IS NOT PERMITTED BY VA brokers must pay and then collect from the borrower VA IRRRL STREAMLINE REFINANCE The following is required upon submission of a VA IRRRL streamline refinance: 1. IRRRL case assignment pulled from the VA Portal it must reflect the Prior Loan information 2. Fully completed 1003, refinance section must be completed, listing employment, NO income, present housing expense, proposed housing expense, liabilities per the credit

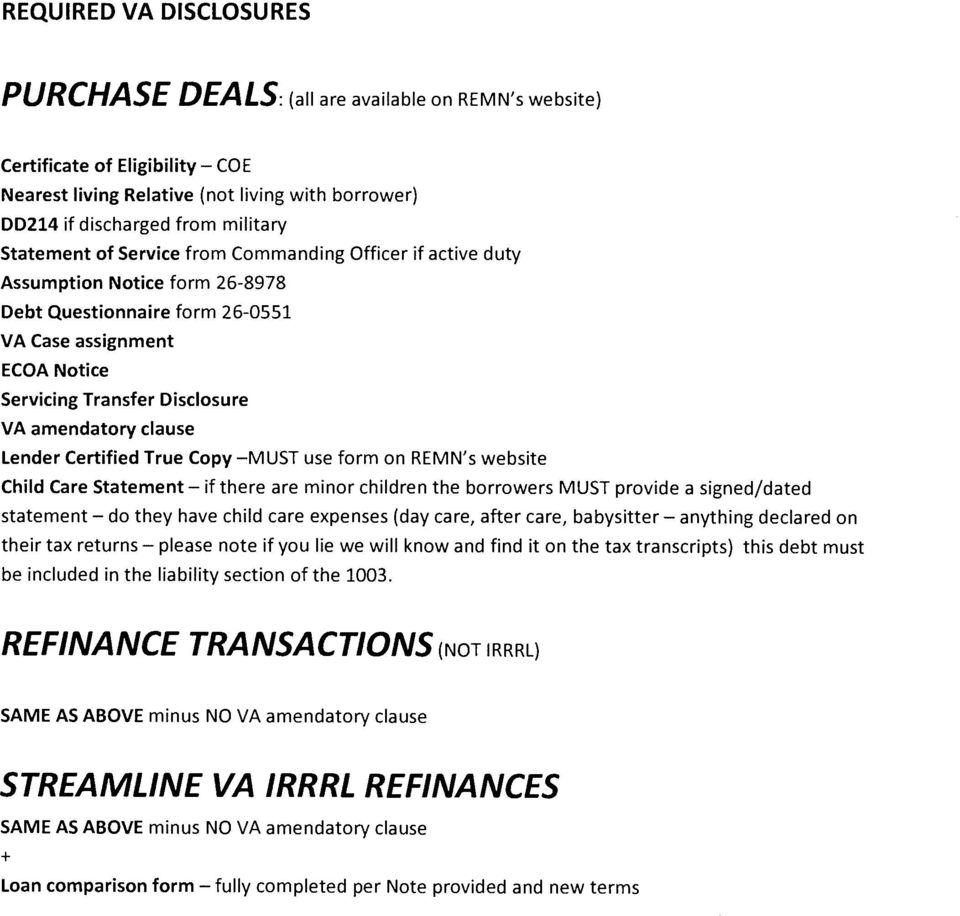

3 report provided (if mortgage only only list mortgage), REO section fully completed, declarations, details of transaction, government monitoring section believe it or not most of the time we get a half completed application which again causes us to not be able to see the whole picture. 3. Photo ID 4. Copy of SS card (these are no income loans we have no proof of their SS # without the card) 5. Pay off for mortgage 6. Loan Comparison form this MUST be fully completed per the Note provided and new terms of new loan and it MUST be signed by borrowers 7. Disclosures generic, state specific, and VA forms (see list provided for VA disclosures) 8. Calculation of loan amount the MAX loan amount that can be given is the total Pay off + closing costs/prepaid keep in mind you MUST subtract the broker credit towards closing costs prior to adding it to the total pay off. REQUIRED VA DISCLOSURES PURCHASE DEALS: (all are available on REMN s website) Certificate of Eligibility COE Nearest living Relative (not living with borrower) DD214 if discharged from military Statement of Service from Commanding Officer if active duty Assumption Notice form Debt Questionnaire form VA Case assignment ECOA Notice Servicing Transfer Disclosure VA amendatory clause Lender Certified True Copy MUST use form on REMN s website

8.")

4 Child Care Statement if there are minor children the borrowers MUST provide a signed/dated statement do they have child care expenses (day care, after care, babysitter anything declared on their tax returns please note if you lie we will know and find it on the tax transcripts) this debt must be included in the liability section of the REFINANCE TRANSACTIONS (NOT IRRRL) SAME AS ABOVE minus NO VA amendatory clause STREAMLINE VA IRRRL REFINANCES SAME AS ABOVE minus NO VA amendatory clause + Loan comparison form fully completed per Note provided and new terms

SAME AS ABOVE minus NO VA amendatory clause STREAMLINE VA IRRRL REFINANCES SAME AS ABOVE minus NO VA")

5

6

7

8

9

10

11

12

13

14

15

16

17

18

VA Lending Basic Training

VA Lending Basic Training Brought to you by: Quicken Loans Mortgage Services Q-University October 19, 2011 February 2014 1 What You will learn Today The Facts and Benefits Of VA Who is Eligible for VA

VA Lending Basic Training Brought to you by: Quicken Loans Mortgage Services Q-University October 19, 2011 February 2014 1 What You will learn Today The Facts and Benefits Of VA Who is Eligible for VA

Magnolia Bank VA Refinance Options

Interest Rate Reduction Refinance Loans (IRRRLS) Eligibility Cash Out Refinance 1. ELIGIBLE PRODUCTS VA Fixed Rate Product VA Hybrid ARMs VA High Balance Products VA Fixed Rate Product VA Hybrid ARMs VA

Interest Rate Reduction Refinance Loans (IRRRLS) Eligibility Cash Out Refinance 1. ELIGIBLE PRODUCTS VA Fixed Rate Product VA Hybrid ARMs VA High Balance Products VA Fixed Rate Product VA Hybrid ARMs VA

Lending Guide. Section 400 Loan Submission & Standards

General Brokers have the option to submit loans to Rushmore Home Loans, a division of Rushmore Loan Management Services LLC (Rushmore) for underwriting via e-mail, Rushmore s IQ2 System, or courier/mail

General Brokers have the option to submit loans to Rushmore Home Loans, a division of Rushmore Loan Management Services LLC (Rushmore) for underwriting via e-mail, Rushmore s IQ2 System, or courier/mail

FHA STREAMLINE REFINANCE PRODUCT PROFILE

Terms 30 Year Terms 15 Year Terms Maximum LTV/CLTV LTV/CLTV Score LTV/CLTV Score Non-Credit Qualifying N/A N/A Credit Qualifying 97.75% 97.75% Applies to Case Numbers assigned on or after January 26, 2015

Terms 30 Year Terms 15 Year Terms Maximum LTV/CLTV LTV/CLTV Score LTV/CLTV Score Non-Credit Qualifying N/A N/A Credit Qualifying 97.75% 97.75% Applies to Case Numbers assigned on or after January 26, 2015

VA IRRRL Offering 5/20/14

VA IRRRL Offering 5/20/14 What is an IRRRL? IRRRL stands for Interest Rate Reduction Refinance Loan An IRRRL is a VA guaranteed loan made to refinance an existing VA guaranteed loan, generally at a lower

VA IRRRL Offering 5/20/14 What is an IRRRL? IRRRL stands for Interest Rate Reduction Refinance Loan An IRRRL is a VA guaranteed loan made to refinance an existing VA guaranteed loan, generally at a lower

Get in the FAST LANE with WesLend Wholesale! VA Home Loan Guarantee Program Program Overview

VA Home Loan Guarantee Program Program Overview Eligible Borrowers All veterans are eligible for VA home loan benefits if they served in the Army, Navy, Air Force, Marine Corps, Coast Guard, Reserves or

VA Home Loan Guarantee Program Program Overview Eligible Borrowers All veterans are eligible for VA home loan benefits if they served in the Army, Navy, Air Force, Marine Corps, Coast Guard, Reserves or

E MORTGAGE MANAGEMENT, LLC 701 VA FIXED PRODUCT GUIDELINES

E MORTGAGE MANAGEMENT, LLC 70 VA FIXED PRODUCT GUIDELINES 2/24/205 Mortgage Eligibility Product Code Short Description Long Description Description VF5 VA 5 YR VF5 - VA FIXED 5 YEAR VF20 VA 20 YR VF20

E MORTGAGE MANAGEMENT, LLC 70 VA FIXED PRODUCT GUIDELINES 2/24/205 Mortgage Eligibility Product Code Short Description Long Description Description VF5 VA 5 YR VF5 - VA FIXED 5 YEAR VF20 VA 20 YR VF20

E MORTGAGE MANAGEMENT, LLC 702 VA ARMS PRODUCT GUIDELINES

E MORTGAGE MANAGEMENT, LLC 702 VA ARMS PRODUCT GUIDELINES 2/24/2015 Mortgage Eligibility Product Code Short Description Long Description Description VF31 VA 3 YR ARM VF31 - VA 3-1 ARM VF51 VA 5 YR ARM

E MORTGAGE MANAGEMENT, LLC 702 VA ARMS PRODUCT GUIDELINES 2/24/2015 Mortgage Eligibility Product Code Short Description Long Description Description VF31 VA 3 YR ARM VF31 - VA 3-1 ARM VF51 VA 5 YR ARM

File Retention Brokered and Mini Correspondent Loans

Berkshire Lending, LLC File Retention Brokered and Mini Correspondent Loans Your Branch Office must be in compliance for HUD audits and state license examinations. Audits are fairly routine and simple

Berkshire Lending, LLC File Retention Brokered and Mini Correspondent Loans Your Branch Office must be in compliance for HUD audits and state license examinations. Audits are fairly routine and simple

VA Homeowners Guide PRESENTED BY. www.lowvarates.com

VA Homeowners Guide PRESENTED BY www.lowvarates.com TABLE OF CONTENTS Introduction to LowVARates Why a VA Loan? VA Loan Eligibility What is a COE? Occupancy Requirements Credit/Income Requirements VA Funding

VA Homeowners Guide PRESENTED BY www.lowvarates.com TABLE OF CONTENTS Introduction to LowVARates Why a VA Loan? VA Loan Eligibility What is a COE? Occupancy Requirements Credit/Income Requirements VA Funding

E MORTGAGE MANAGEMENT, LLC 703 VA HIGH BALANCE PRODUCT GUIDELINES

E MORTGAGE MANAGEMENT, LLC 703 VA HIGH BALANCE PRODUCT GUIDELINES 4/30/2014 Mortgage Eligibility Product Code Short Description Long Description Description VF30HB 30 YR VA HB VF30HB - 30 YR VA HIGH BALANCE

E MORTGAGE MANAGEMENT, LLC 703 VA HIGH BALANCE PRODUCT GUIDELINES 4/30/2014 Mortgage Eligibility Product Code Short Description Long Description Description VF30HB 30 YR VA HB VF30HB - 30 YR VA HIGH BALANCE

Name Account Executive. Contact Number E-Mail Address Website Address

VA Loan Information Name Account Executive Contact Number E-Mail Address Website Address Benefits of VA No Down Payment, 100% up to $417,000. No Monthly Mortgage Insurance Premiums. Leniency on Credit

VA Loan Information Name Account Executive Contact Number E-Mail Address Website Address Benefits of VA No Down Payment, 100% up to $417,000. No Monthly Mortgage Insurance Premiums. Leniency on Credit

IRRRL s. Interest Rate Reduction Refinance Loans. Helping Our Veterans While Helping Your Business

IRRRL s Interest Rate Reduction Refinance Loans Helping Our Veterans While Helping Your Business What is an IRRRL? An IRRRL is a VA guaranteed loan made to refinance an existing VA guaranteed loan, generally

IRRRL s Interest Rate Reduction Refinance Loans Helping Our Veterans While Helping Your Business What is an IRRRL? An IRRRL is a VA guaranteed loan made to refinance an existing VA guaranteed loan, generally

A Simplified Overview of FHA Loan Origination

Introduction to FHA Origination A Simplified Overview of FHA Loan Origination Topics of Discussion Introduction to FHA Fundamentals of Loan Origination FHA Loan Limits Borrower Eligibility Property Eligibility

Introduction to FHA Origination A Simplified Overview of FHA Loan Origination Topics of Discussion Introduction to FHA Fundamentals of Loan Origination FHA Loan Limits Borrower Eligibility Property Eligibility

VA Refinance IRRRL. VA Refinance IRRRL

This matrix is intended as an aid to help determine whether a property/loan qualifies for certain financing. It is not intended as a replacement for VA guidelines. Users are expected to know and comply

This matrix is intended as an aid to help determine whether a property/loan qualifies for certain financing. It is not intended as a replacement for VA guidelines. Users are expected to know and comply

VA Quick Reference Guides

Finance Type Occupancy Product Codes Purchase, Cash-Out and Rate & Term Refinance, Interest Rate Reduction Refinance Loan (IRRRL) Owner Occupied only, Second Homes not allowed, Investment properties not

Finance Type Occupancy Product Codes Purchase, Cash-Out and Rate & Term Refinance, Interest Rate Reduction Refinance Loan (IRRRL) Owner Occupied only, Second Homes not allowed, Investment properties not

VA Refinance Cash Out

VA Refinance Cash Out This matrix is intended as an aid to help determine whether a property/loan qualifies for certain financing. It is not intended as a replacement for VA guidelines. Users are expected

VA Refinance Cash Out This matrix is intended as an aid to help determine whether a property/loan qualifies for certain financing. It is not intended as a replacement for VA guidelines. Users are expected

VA Loan Training Overviews & Updates June 3, 2015

VA Loan Training Overviews & Updates June 3, 2015 Choose one of the following audio options: TO USE YOUR COMPUTER'S AUDIO: When the webinar begins, you will be connected to audio using your computer's

VA Loan Training Overviews & Updates June 3, 2015 Choose one of the following audio options: TO USE YOUR COMPUTER'S AUDIO: When the webinar begins, you will be connected to audio using your computer's

Your VA Home Benefit. Your VA Home Benefit. What We Will Cover in This Class. Basic Elements of VA Guarantee

Thank you for Joining Us We will begin Shortly A Complete Guide to What We Will Cover in This Class Basic Elements of VA Guaranteed Loan Rules for Eligibility Qualifying Basics - Getting Approved Overcoming

Thank you for Joining Us We will begin Shortly A Complete Guide to What We Will Cover in This Class Basic Elements of VA Guaranteed Loan Rules for Eligibility Qualifying Basics - Getting Approved Overcoming

VA IRRL 2. CURRENT FIRST MORTGAGE ELIGIBILITY

1. PRODUCT DESCRIPTION VA Fixed Rate and ARM Mortgages for Refinance Transactions Fixed Rate Mortgage 10 to 30 years in 5 year increments Fully amortizing Qualified Mortgage (QM) Safe Harbor loans are

1. PRODUCT DESCRIPTION VA Fixed Rate and ARM Mortgages for Refinance Transactions Fixed Rate Mortgage 10 to 30 years in 5 year increments Fully amortizing Qualified Mortgage (QM) Safe Harbor loans are

NOTE: This matrix includes overlays, which may be more restrictive than VA requirements. A thorough reading of this matrix is recommended.

VA Refinance IRRRL This matrix is intended as an aid to help determine whether a property/loan qualifies for certain financing. It is not intended as a replacement for VA guidelines. Users are expected

VA Refinance IRRRL This matrix is intended as an aid to help determine whether a property/loan qualifies for certain financing. It is not intended as a replacement for VA guidelines. Users are expected

FHA STREAMLINE GUIDELINES

Table of Contents LTV MATRIX... 4 PROGRAM OVERVIEW... 4 APPRAISALS & AVM... 4 AVM or 2055 Exterior... 4 Streamline with an Appraisal (1004 full FHA Appraisal)... 5 ASSETS... 5 Sourcing of Deposits... 5

Table of Contents LTV MATRIX... 4 PROGRAM OVERVIEW... 4 APPRAISALS & AVM... 4 AVM or 2055 Exterior... 4 Streamline with an Appraisal (1004 full FHA Appraisal)... 5 ASSETS... 5 Sourcing of Deposits... 5

VA LOAN Reference Guidance

VA LOAN Reference Guidance This guide offers a quick look at vital information you need in the process of buying or refinancing a home using your VA benefits. Through it, we intend to give you quick answers

VA LOAN Reference Guidance This guide offers a quick look at vital information you need in the process of buying or refinancing a home using your VA benefits. Through it, we intend to give you quick answers

Streamline VS FHA to FHA refinance

Streamline VS FHA to FHA refinance Streamline - Max loan amount is the borrower s unpaid principal balance plus up to 30 days of interest minus applicable UFMIP refund. Borrower will either need to bring

Streamline VS FHA to FHA refinance Streamline - Max loan amount is the borrower s unpaid principal balance plus up to 30 days of interest minus applicable UFMIP refund. Borrower will either need to bring

EFFECTIVE FOR FHA CASE NUMBER ASSIGNMENTS ON AND AFTER SEPTEMBER 14, 2015 OVERLAY MATRIX: GOVERNMENT

Appraisals Attached PUDs Automated Findings Condominiums Credit History VA: Form 2055 Appraisal dated prior to the Note Date required on IRRRLs if current VA loan is not serviced by BB&T. FHA: Property

Appraisals Attached PUDs Automated Findings Condominiums Credit History VA: Form 2055 Appraisal dated prior to the Note Date required on IRRRLs if current VA loan is not serviced by BB&T. FHA: Property

Purchasing a New Home using a VA Loan

Purchasing a New Home using a VA Loan Eligibility page 1 Benefits page 2 First-Time Home Buyers page Process page 4 Fees page 5 Documentation page 6 VA Loan Eligibility Service Length Eligibility Credit

Purchasing a New Home using a VA Loan Eligibility page 1 Benefits page 2 First-Time Home Buyers page Process page 4 Fees page 5 Documentation page 6 VA Loan Eligibility Service Length Eligibility Credit

VA Product Profile 05.01.2014

Maximum LTV / CLTV and FICO Requirements Purchase VA IRRRL / Rate & Term Cash-out Refinance Maximum LTV 1 / CLTV 1 Min FICO 2 Maximum LTV 1 / CLTV 1 Min FICO 2 Maximum LTV 1 / CLTV 1 Min FICO 2 100% 640

Maximum LTV / CLTV and FICO Requirements Purchase VA IRRRL / Rate & Term Cash-out Refinance Maximum LTV 1 / CLTV 1 Min FICO 2 Maximum LTV 1 / CLTV 1 Min FICO 2 Maximum LTV 1 / CLTV 1 Min FICO 2 100% 640

IRRRL s Interest Rate Reduction Refinance Loans. Allow REMN to Introduce You to IRRRL

IRRRL s Interest Rate Reduction Refinance Loans Allow REMN to Introduce You to IRRRL January 2013 Agenda Welcome What is IRRRL? Sales IRRRL Highlights Q&A Webinar Questions We will be collecting questions

IRRRL s Interest Rate Reduction Refinance Loans Allow REMN to Introduce You to IRRRL January 2013 Agenda Welcome What is IRRRL? Sales IRRRL Highlights Q&A Webinar Questions We will be collecting questions

FHA Fixed. FICO <580 Requirements: 1-4 580 (c) Varies by County (a) 97.75% 97.75% Per AUS (d) Sub 580 (560-579 FICO) FF30580SG FF15580SG

Varies by County (a) 97.75% 97.75% Per AUS (d) Sub 580 (560-579 FICO) FF30580SG FF15580SG") NOTES Primary Residence Units Minimum Credit Score SERIES G Max Loan Amount Continental US PURCHASE LTV CLTV Max Debt-to- Income Ratio 1-2 560 (e) Varies by County (a) 90% (e) 90% (e) 31/43% (e) 1-4 580

NOTES Primary Residence Units Minimum Credit Score SERIES G Max Loan Amount Continental US PURCHASE LTV CLTV Max Debt-to- Income Ratio 1-2 560 (e) Varies by County (a) 90% (e) 90% (e) 31/43% (e) 1-4 580

Appraisal requirements: No appraisal required. The original loan balance of the mortgage being refinanced is used as the appraised value.

PRODUCT: E3 CODES: PCM VA IRRRL VAS15W AND VAS30W Primary Capital Mortgage guidelines have been created to provide direction and consistency in determining a credit decision. The intention of these guidelines

PRODUCT: E3 CODES: PCM VA IRRRL VAS15W AND VAS30W Primary Capital Mortgage guidelines have been created to provide direction and consistency in determining a credit decision. The intention of these guidelines

VA FIXED RATE PROGRAM HIGHLIGHTS

Program Summary Loan Term & Program Category Entitlement These guidelines represent underwriting requirements for VA fixed rate mortgages. Also review the VA Lender s Handbook for any guidelines not specifically

Program Summary Loan Term & Program Category Entitlement These guidelines represent underwriting requirements for VA fixed rate mortgages. Also review the VA Lender s Handbook for any guidelines not specifically

FHA: Standard and Jumbo/High Balance Eligibility Matrix

FHA: Standard and Jumbo/High Balance Loan Purpose FICO Maximum LTV 1 Maximum CLTV Maximum DTI 3 >620 100.00% 2 45%/55% Purchase Rate and Term Refinance Cash-out Refinance 4 580-619 31%/43% 500-579 90.00%

FHA: Standard and Jumbo/High Balance Loan Purpose FICO Maximum LTV 1 Maximum CLTV Maximum DTI 3 >620 100.00% 2 45%/55% Purchase Rate and Term Refinance Cash-out Refinance 4 580-619 31%/43% 500-579 90.00%

FHA Streamline Training: Broker Edition. January 22, 2014

FHA Streamline Training: Broker Edition January 22, 2014 1 Jeff Walsh President of LDWholesale 2 What Is It? FHA Streamline refinance provides existing FHA borrower s an opportunity to lower monthly payments

FHA Streamline Training: Broker Edition January 22, 2014 1 Jeff Walsh President of LDWholesale 2 What Is It? FHA Streamline refinance provides existing FHA borrower s an opportunity to lower monthly payments

SUBMITTING AN ACCURATE GOOD FAITH ESTIMATE - INTRODUCTION... 1 ALL LOANS... 1 NAME OF ORIGINATOR... 1 BORROWER... 1 IMPORTANT DATES...

SUBMITTING AN ACCURATE GOOD FAITH ESTIMATE - INTRODUCTION... 1 ALL LOANS... 1 NAME OF ORIGINATOR... 1 BORROWER... 1 IMPORTANT DATES... 2 SUMMARY OF YOUR LOAN... 3 ESCROW ACCOUNT INFORMATION... 4 SUMMARY

SUBMITTING AN ACCURATE GOOD FAITH ESTIMATE - INTRODUCTION... 1 ALL LOANS... 1 NAME OF ORIGINATOR... 1 BORROWER... 1 IMPORTANT DATES... 2 SUMMARY OF YOUR LOAN... 3 ESCROW ACCOUNT INFORMATION... 4 SUMMARY

VA Product Guidelines

July 16, 2015 VA Product Guidelines Purchase Occupancy Units LTV CLTV Minimum Credit Score Primary 1-4 100 100 620 Rate/Term Refinance Occupancy Units LTV CLTV Minimum Credit Score Primary 1-4 90 90 620

July 16, 2015 VA Product Guidelines Purchase Occupancy Units LTV CLTV Minimum Credit Score Primary 1-4 100 100 620 Rate/Term Refinance Occupancy Units LTV CLTV Minimum Credit Score Primary 1-4 90 90 620

NON CREDIT QUALIFYING WITHOUT APPRAISAL, STANDARD & HIGH BALANCE, FIXED & ARM

NON CREDIT QUALIFYING WITHOUT APPRAISAL, STANDARD & HIGH BALANCE, FIXED & ARM Occupancy Maximum LTV/CLTV # of Units MAX Base Loan* High MIN Base* Min FICO Max Ratios Mortgage History** Primary 125% Non

NON CREDIT QUALIFYING WITHOUT APPRAISAL, STANDARD & HIGH BALANCE, FIXED & ARM Occupancy Maximum LTV/CLTV # of Units MAX Base Loan* High MIN Base* Min FICO Max Ratios Mortgage History** Primary 125% Non

VA IRRRL GUIDELINES. Table of Contents

Page 1 of 8 Table of Contents LTV MATRIX... 3 PROGRAM SUMMARY... 3 LOAN AMOUNTS... 3 LOAN PROGRAM CODES... 3 LOAN TERMS... 3 ADJUSTMENT RATE DETAILS... 3 ELIGIBLE PROPERTY TYPES... 3 INELIGIBLE PROPERTY

Page 1 of 8 Table of Contents LTV MATRIX... 3 PROGRAM SUMMARY... 3 LOAN AMOUNTS... 3 LOAN PROGRAM CODES... 3 LOAN TERMS... 3 ADJUSTMENT RATE DETAILS... 3 ELIGIBLE PROPERTY TYPES... 3 INELIGIBLE PROPERTY

Real Estate Professionals Selling to Veterans. St. Petersburg Regional Loan Center

Real Estate Professionals Selling to Veterans St. Petersburg Regional Loan Center Agenda Overview and History of VA Home Loan Program Understanding VA Home Loan Entitlement Occupancy Requirements Qualifying

Real Estate Professionals Selling to Veterans St. Petersburg Regional Loan Center Agenda Overview and History of VA Home Loan Program Understanding VA Home Loan Entitlement Occupancy Requirements Qualifying

VA Processing Checklist

VA Processing Checklist DU Findings Read DU Findings thoroughly and document accordingly! Provide documentation requested. Re: Paystubs/W-2 s, SS/Retirement earnings, bank statements, tax returns, do ratios

VA Processing Checklist DU Findings Read DU Findings thoroughly and document accordingly! Provide documentation requested. Re: Paystubs/W-2 s, SS/Retirement earnings, bank statements, tax returns, do ratios

E MORTGAGE MANAGEMENT, LLC 704 VA

E MORTGAGE MANAGEMENT, LLC 704 VA IRRRLs PRODUCT GUIDELINES 1/26/2015 Mortgage Eligibility Product Code Short Long Description Description Description VF15IRL VA 15 YR IRRRL VF15IRL - VA 15 YR IRRRL VF30IRL

E MORTGAGE MANAGEMENT, LLC 704 VA IRRRLs PRODUCT GUIDELINES 1/26/2015 Mortgage Eligibility Product Code Short Long Description Description Description VF15IRL VA 15 YR IRRRL VF15IRL - VA 15 YR IRRRL VF30IRL

Product Product Code Loan Term 30-Year FRM FHA FHA30 30-years 15-Year FRM FHA FHA15 15-Years. Property Type Lowest Maximum (Floor)

") FHA Guidelines Product Description FHA Fixed Rate 15 and 30 Year Terms Fully Amortizing Product Codes Maximum s Product Product Code Loan Term 30-Year FRM FHA FHA30 30-years 15-Year FRM FHA FHA15 15-Years

FHA Guidelines Product Description FHA Fixed Rate 15 and 30 Year Terms Fully Amortizing Product Codes Maximum s Product Product Code Loan Term 30-Year FRM FHA FHA30 30-years 15-Year FRM FHA FHA15 15-Years

It s easier than you think! Phoenix Regional Loan Center

It s easier than you think! Phoenix Regional Loan Center Why VA Loans? Help veterans Fast and easy to process Flexible underwriting standards Potential Income--- Over 18.6 Billion Loans Totaling $1,027,282,752,622!

It s easier than you think! Phoenix Regional Loan Center Why VA Loans? Help veterans Fast and easy to process Flexible underwriting standards Potential Income--- Over 18.6 Billion Loans Totaling $1,027,282,752,622!

Sierra Lending Group LLC Document Check List

Sierra Lending Group LLC Document Check List The following documents will be needed for full credit approval: Application 1. Fully completed and signed initial 1003. Please make sure to provide all assets

Sierra Lending Group LLC Document Check List The following documents will be needed for full credit approval: Application 1. Fully completed and signed initial 1003. Please make sure to provide all assets

Next Home Government Program Term Sheet Effective December 1, 2015

Next Home Government Program Term Sheet Effective December 1, 2015 This Program Term Sheet ( Program Term Sheet as referenced in the Master Origination and Sale Agreement, HFA Guidelines as expressed in

Next Home Government Program Term Sheet Effective December 1, 2015 This Program Term Sheet ( Program Term Sheet as referenced in the Master Origination and Sale Agreement, HFA Guidelines as expressed in

WHOLESALE VA IRRRL NO APPRAISAL PRODUCT PROFILE

Maximum LTV/CLTV and Credit Score Requirements VA IRRRL No Appraisal 1 WHOLESALE VA IRRRL NO APPRAISAL Program Code(s): VF30IRRRLNA = 30 year VF15IRRRLNA= 15 year Occupancy LTV/CLTV 3 Min Credit Score

Maximum LTV/CLTV and Credit Score Requirements VA IRRRL No Appraisal 1 WHOLESALE VA IRRRL NO APPRAISAL Program Code(s): VF30IRRRLNA = 30 year VF15IRRRLNA= 15 year Occupancy LTV/CLTV 3 Min Credit Score

VA Product Guidelines

August 10, 2015 VA Product Guidelines Purchase Occupancy Units LTV CLTV Primary 1-4 100 100 620 Rate/Term Refinance Occupancy Units LTV CLTV Primary 1-4 100 100 620 IRRRL Occupancy Units LTV CLTV Primary

August 10, 2015 VA Product Guidelines Purchase Occupancy Units LTV CLTV Primary 1-4 100 100 620 Rate/Term Refinance Occupancy Units LTV CLTV Primary 1-4 100 100 620 IRRRL Occupancy Units LTV CLTV Primary

VA Home Loans 101 An Easy Reference Guide

VA Home Loans 101 An Easy Reference Guide Website: Email: www.valoans.com assistance@valoans.com Congratulations on Starting Your Journey to Home Ownership This guide offers a quick look at vital information

VA Home Loans 101 An Easy Reference Guide Website: Email: www.valoans.com assistance@valoans.com Congratulations on Starting Your Journey to Home Ownership This guide offers a quick look at vital information

Single Family Bond Program Lender Training PROGRAM OVERVIEW

Single Family Bond Program Lender Training PROGRAM OVERVIEW What this program ISN T NOT A DOWN PAYMENT ASSISTANCE PROGRAM NOT FOR BUYERS WITH POOR CREDIT DOES NOT PROVIDE A SUBPRIME PRODUCT NOT FOR LOW

Single Family Bond Program Lender Training PROGRAM OVERVIEW What this program ISN T NOT A DOWN PAYMENT ASSISTANCE PROGRAM NOT FOR BUYERS WITH POOR CREDIT DOES NOT PROVIDE A SUBPRIME PRODUCT NOT FOR LOW

Loan Product Guide (Matrix)

") Loan Product Guide (Matrix) 1 FHA Page 2 FNMA 3 USDA 4 VA 1.1 Streamline...2 1.2 Purchase 203 (B)...3 1.3 Refinance 203 (B)...4 2.1 Purchase...5 2.2 Refinance...6 3.1 Purchase...7 3.2 Refinance/Streamline...8

Loan Product Guide (Matrix) 1 FHA Page 2 FNMA 3 USDA 4 VA 1.1 Streamline...2 1.2 Purchase 203 (B)...3 1.3 Refinance 203 (B)...4 2.1 Purchase...5 2.2 Refinance...6 3.1 Purchase...7 3.2 Refinance/Streamline...8

VA RATE REDUCTION REFINANCE (VAFX)

") ELIGIBLE MORTGAGE VA to VA Refinance PRODUCT-EXISTING LOAN ELIGIBLE MORTGAGE Fixed Rate 30 year PRODUCT-NEW LOAN MAXIMUM LOAN AMOUNT 620 FICO Maximum loan amount including VA Funding Fee (VAFF) is $417,000

ELIGIBLE MORTGAGE VA to VA Refinance PRODUCT-EXISTING LOAN ELIGIBLE MORTGAGE Fixed Rate 30 year PRODUCT-NEW LOAN MAXIMUM LOAN AMOUNT 620 FICO Maximum loan amount including VA Funding Fee (VAFF) is $417,000

Standards for Determining Monthly Debt and Income Appendix Q

Standards for Determining Monthly Debt and Income Appendix Q October 2014 2012 Genworth Financial, Inc. All rights reserved. Agenda What we will cover General Income Requirements Documentation Requirements

Standards for Determining Monthly Debt and Income Appendix Q October 2014 2012 Genworth Financial, Inc. All rights reserved. Agenda What we will cover General Income Requirements Documentation Requirements

RETAIL VA IRRRL NO APPRAISAL PRODUCT PROFILE

Maximum LTV/CLTV and Credit Score Requirements VA IRRRL No Appraisal 1 Program Code(s): VF30IRRRLNA = 30 year VF15IRRRLNA= 15 year Occupancy LTV/CLTV 3 Min Credit Score 5 NYLX Codes O/O 1 Unit 100% 580-599

Maximum LTV/CLTV and Credit Score Requirements VA IRRRL No Appraisal 1 Program Code(s): VF30IRRRLNA = 30 year VF15IRRRLNA= 15 year Occupancy LTV/CLTV 3 Min Credit Score 5 NYLX Codes O/O 1 Unit 100% 580-599

VA and VA IRRRL Programs

VA and VA IRRRL Programs 12/12/14 VA Program Benefits VA loan programs offer exceptional financing options for active duty military personnel, veterans and their families. 100% financing on purchase and

VA and VA IRRRL Programs 12/12/14 VA Program Benefits VA loan programs offer exceptional financing options for active duty military personnel, veterans and their families. 100% financing on purchase and

COMPENSATING FACTORS FOR FHA

COMPENSATING FACTORS FOR FHA Key Points Credit Only allowed for Case numbers assigned on or after 4/1/13 for borrowers with FICO s at 620 or less with Debt to Income (DTI ) ratios above 43%. Even if broker

COMPENSATING FACTORS FOR FHA Key Points Credit Only allowed for Case numbers assigned on or after 4/1/13 for borrowers with FICO s at 620 or less with Debt to Income (DTI ) ratios above 43%. Even if broker

AMX / Land Home Financial Services Wholesale Lending Division

SECTION: 1 PAGE: 1 of 13 VA MORTGAGE LIMITS FOR ALL AREAS: http://www.benefits.va.gov/homeloans/purchaseco_loan_limits.asp Regardless of loan amount, the VA guaranty plus cash/equity must be equal to at

SECTION: 1 PAGE: 1 of 13 VA MORTGAGE LIMITS FOR ALL AREAS: http://www.benefits.va.gov/homeloans/purchaseco_loan_limits.asp Regardless of loan amount, the VA guaranty plus cash/equity must be equal to at

Contents. VA Credit Overlays

Contents... 1 Introduction... 3 Links... 3 Transaction Types... 3 Purchase Transactions... 3 Refinance Transaction Regular Refinance... 3 Refinance Transaction Interest Rate Reduction Refinance Loan/IRRRL...

Contents... 1 Introduction... 3 Links... 3 Transaction Types... 3 Purchase Transactions... 3 Refinance Transaction Regular Refinance... 3 Refinance Transaction Interest Rate Reduction Refinance Loan/IRRRL...

Conventional DU Refi Plus

Endeavor America Loan Services Conventional DU Refi Plus Guidelines Conventional Guidelines... 3 Matrix... 3 Overview... 3 Program Expiration... 3 Loan Purpose... 4 Maximum LTV, CLTV, and HCLTV Ratios

Endeavor America Loan Services Conventional DU Refi Plus Guidelines Conventional Guidelines... 3 Matrix... 3 Overview... 3 Program Expiration... 3 Loan Purpose... 4 Maximum LTV, CLTV, and HCLTV Ratios

FHA STREAMLINE REFINANCE GUIDELINES

Table of Contents FHA STREAMLINE REFINANCE GUIDELINES Maximum Mortgage Amount Calculations... 1 Streamline With Appraisal... 1 Streamline Without Appraisal... 2 Underwriting and Eligibility Criteria...

Table of Contents FHA STREAMLINE REFINANCE GUIDELINES Maximum Mortgage Amount Calculations... 1 Streamline With Appraisal... 1 Streamline Without Appraisal... 2 Underwriting and Eligibility Criteria...

FHA Streamline Refi. Max Loan Amount Hawaii. LTV w/o Sec Fin STREAMLINE REFINANCE WITHOUT AN APPRAISAL

Primary Residence Units Minimum Credit Score SERIES 3 Continental US Hawaii LTV w/o STREAMLINE REFINANCE WITHOUT AN APPRAISAL CLTV w/ Max Debtto-Income Ratio 1-4 700 (f) Varies by County (a) Varies by

Primary Residence Units Minimum Credit Score SERIES 3 Continental US Hawaii LTV w/o STREAMLINE REFINANCE WITHOUT AN APPRAISAL CLTV w/ Max Debtto-Income Ratio 1-4 700 (f) Varies by County (a) Varies by

Affiliated Mortgage Company

Affiliated Mortgage Company Investor Tips: Conforming Max Debt Ratios -45%, regardless of AUS recommendation MI Companies Allowed : Genworth, MGIC, UG and Essent Minimum 720 credit score for LTV/CLTV/HCLTV

Affiliated Mortgage Company Investor Tips: Conforming Max Debt Ratios -45%, regardless of AUS recommendation MI Companies Allowed : Genworth, MGIC, UG and Essent Minimum 720 credit score for LTV/CLTV/HCLTV

VA PROGRAMS PRODUCT MATRIX

OCCUPANCY LTV UNITS CLTV STANDARD PORTFOLIO Purchase O/O 100% 1-4 100% 620 Cash Out O/O 100% 1-4 100% 620 O/O IRRRL 1,2 2 nd Home 3 130% 1-4 130% 4 620 N/O/O Conforming Balance: 580 FICO High Balance:

OCCUPANCY LTV UNITS CLTV STANDARD PORTFOLIO Purchase O/O 100% 1-4 100% 620 Cash Out O/O 100% 1-4 100% 620 O/O IRRRL 1,2 2 nd Home 3 130% 1-4 130% 4 620 N/O/O Conforming Balance: 580 FICO High Balance:

The FHA & VA Client Opportunity

The FHA & VA Client Opportunity October 2014 MEET THE SPEAKERS Bobbi Macpherson QL Senior Product Manager, Capital Markets Geno Yoscovits QL Product Manager, Capital Markets Stacey Burlison QL Senior Team

The FHA & VA Client Opportunity October 2014 MEET THE SPEAKERS Bobbi Macpherson QL Senior Product Manager, Capital Markets Geno Yoscovits QL Product Manager, Capital Markets Stacey Burlison QL Senior Team

U.S. Bank Home Mortgage

U.S. Bank Home Mortgage VA Presentation This material is not to be reproduced without the approval of U.S. Bank Corporate Compliance. The information is provided to assist Mortgage Brokers and is not intended

U.S. Bank Home Mortgage VA Presentation This material is not to be reproduced without the approval of U.S. Bank Corporate Compliance. The information is provided to assist Mortgage Brokers and is not intended

FHA LOAN PROGRAM Conforming and High Balance Loan Amounts

FHA PRODUCT MATRIX Purchase Rate and Term Cash Out Units LTV/CLTV Fico* Units LTV/CLTV Fico Units LTV/CLTV Fico 1 4 96.5/105 620 1 4 97.75/97.75 620 1 4 85/85 620 FYIs: Complete HUD guidelines can be referenced

FHA PRODUCT MATRIX Purchase Rate and Term Cash Out Units LTV/CLTV Fico* Units LTV/CLTV Fico Units LTV/CLTV Fico 1 4 96.5/105 620 1 4 97.75/97.75 620 1 4 85/85 620 FYIs: Complete HUD guidelines can be referenced

Chapter 5. How to Process VA Loans and Submit Them to VA Overview

Chapter 5. How to Process VA Loans and Submit Them to VA Overview In this Chapter This chapter contains the following topics. Topic Topic name See Page 1 Refinancing Loans 5-2 2 Processing Procedures 5-3

Chapter 5. How to Process VA Loans and Submit Them to VA Overview In this Chapter This chapter contains the following topics. Topic Topic name See Page 1 Refinancing Loans 5-2 2 Processing Procedures 5-3

FHA Streamline Refi. LTV w/o Sec Fin. CLTV w/ Sec Fin. Varies by County (a) None (b) 125 (b,d) 31/43 (c)

None (b) 125 (b,d) 31/43 (c)") SERIES 3 Primary Residence Units Minimum Credit Score Max Loan Amount Continental US 1-4 680 (f) Varies by County (a) 1-4 680 (f) Varies by County (a) Max Loan Amount Hawaii LTV w/o Sec Fin STREAMLINE

SERIES 3 Primary Residence Units Minimum Credit Score Max Loan Amount Continental US 1-4 680 (f) Varies by County (a) 1-4 680 (f) Varies by County (a) Max Loan Amount Hawaii LTV w/o Sec Fin STREAMLINE

Underwriting Guidelines VA Interest Rate Reduction Refinancing Loans (IRRRL)

") VA Interest Rate Reduction Refinancing Loans (IRRRL) OVERVIEW Purpose The following document describes the responsibilities and requirements of the Carrington Mortgage Services, LLC (CMS) Underwriter (Underwriter)

VA Interest Rate Reduction Refinancing Loans (IRRRL) OVERVIEW Purpose The following document describes the responsibilities and requirements of the Carrington Mortgage Services, LLC (CMS) Underwriter (Underwriter)

Understand the VA Loan Program. Serve the mortgage lending needs of borrowers who serve our country

Understand the VA Loan Program Serve the mortgage lending needs of borrowers who serve our country Eligible Borrowers A veteran is eligible for VA home loan benefits if he or she served in the Army, Navy,

Understand the VA Loan Program Serve the mortgage lending needs of borrowers who serve our country Eligible Borrowers A veteran is eligible for VA home loan benefits if he or she served in the Army, Navy,

Please be sure to only initial below the description of the category of how you would like to do business with AFR.

Dear Lending Partner, It is our pleasure to introduce the different ways you can do business with American Financial Resources Wholesale and Correspondent Lending Divisions. To better serve you, you will

Dear Lending Partner, It is our pleasure to introduce the different ways you can do business with American Financial Resources Wholesale and Correspondent Lending Divisions. To better serve you, you will

SONYMA FHA Plus Correspondent Term Sheet

Product Type 30 Year Fixed Rate Mortgages Sales Focus This program provides the flexibility offered by FHA s 203(b) or 234(c) mortgages along with SONYMA s Down Payment Assistance Loan (DPAL). HUD Mortgagee

Product Type 30 Year Fixed Rate Mortgages Sales Focus This program provides the flexibility offered by FHA s 203(b) or 234(c) mortgages along with SONYMA s Down Payment Assistance Loan (DPAL). HUD Mortgagee

VA Borrower Fees and Charges

VA Borrower Fees and OVERVIEW Purpose The VA home loan program involves a veteran s benefit. VA policy has evolved around the objective of helping the veteran to use his/her home loan benefit. Therefore,

VA Borrower Fees and OVERVIEW Purpose The VA home loan program involves a veteran s benefit. VA policy has evolved around the objective of helping the veteran to use his/her home loan benefit. Therefore,

Document source of funds if amount exceeds 1% of sales price OR appears excessive based on borrower's savings history.

ASSETS Earnest Money Document source of funds if amount exceeds 2% of sales price OR appears excessive based on borrower's savings history. Document source of funds if amount exceeds 1% of sales price

ASSETS Earnest Money Document source of funds if amount exceeds 2% of sales price OR appears excessive based on borrower's savings history. Document source of funds if amount exceeds 1% of sales price

Guide to FHA Streamline Refinances. By J.J. Sawicki, CMP AVP Third Party Lending/Merrimack Mortgage

Guide to FHA Streamline Refinances By J.J. Sawicki, CMP AVP Third Party Lending/Merrimack Mortgage What is a streamline refinance? The FHA streamline refinance has become an increasingly attractive option

Guide to FHA Streamline Refinances By J.J. Sawicki, CMP AVP Third Party Lending/Merrimack Mortgage What is a streamline refinance? The FHA streamline refinance has become an increasingly attractive option

Housing Trust Silicon Valley ( HTSV ) Mortgage Assistance Program (MAP)

Mortgage Assistance Program (MAP)") Housing Trust Silicon Valley ( HTSV ) Mortgage Assistance Program (MAP) Program Description: Housing Trust Silicon Valley s Mortgage Assistance Program (MAP) is an amortizing second loan that is now available

Housing Trust Silicon Valley ( HTSV ) Mortgage Assistance Program (MAP) Program Description: Housing Trust Silicon Valley s Mortgage Assistance Program (MAP) is an amortizing second loan that is now available

FMC Product and Credit Guidance for Wholesale Divisions

FMC Product and Credit Guidance for Divisions Ineligible Product Programs and Properties FMC does not accept Loan Prospector AUS for Conventional, FHA or VA loans The Negative Equity FHA (MHA) loan program

FMC Product and Credit Guidance for Divisions Ineligible Product Programs and Properties FMC does not accept Loan Prospector AUS for Conventional, FHA or VA loans The Negative Equity FHA (MHA) loan program

Section 1: Loan Characteristics

Home Flex Quick Reference: Program Summary The following is an outline of the underwriting and closing requirements of New Hampshire Housing Home Flex program, which is available to lenders who have signed

Home Flex Quick Reference: Program Summary The following is an outline of the underwriting and closing requirements of New Hampshire Housing Home Flex program, which is available to lenders who have signed

VA Loan Guaranty Program Serve the mortgage lending needs of borrowers who serve our country

VA Loan Guaranty Program Serve the mortgage lending needs of borrowers who serve our country Jaime A Garcia 626.768.0700 NMLS 290316 DRE 01148553 Desktop Underwriter is a registered trademark of Fannie

VA Loan Guaranty Program Serve the mortgage lending needs of borrowers who serve our country Jaime A Garcia 626.768.0700 NMLS 290316 DRE 01148553 Desktop Underwriter is a registered trademark of Fannie

FHA STREAMLINE REFINANCE GUIDELINES

Table of Contents FHA STREAMLINE REFINANCE GUIDELINES Maximum Mortgage Amount Calculations... 1 Underwriting and Eligibility Criteria... 2 Documentation Requirements... 4 Appraisal Requirements... 5 Maximum

Table of Contents FHA STREAMLINE REFINANCE GUIDELINES Maximum Mortgage Amount Calculations... 1 Underwriting and Eligibility Criteria... 2 Documentation Requirements... 4 Appraisal Requirements... 5 Maximum

FHA FIXED RATE AND ADJUSTABLE RATE

FHA FIXED RATE AND ADJUSTABLE RATE Product Description FHA Conforming Fixed and ARM FHA15 = FHA 15 Year Fixed FHA30 = FHA 30 Year Fixed Program Numbers FHA5/1 = FHA 5/1 ARM FHASTREAM15 = FHA 15 Year Fixed

FHA FIXED RATE AND ADJUSTABLE RATE Product Description FHA Conforming Fixed and ARM FHA15 = FHA 15 Year Fixed FHA30 = FHA 30 Year Fixed Program Numbers FHA5/1 = FHA 5/1 ARM FHASTREAM15 = FHA 15 Year Fixed

PORTFOLIO ARM CLOSED END 2 ND TD. Table of Contents

Table of Contents 1. Program Codes...2 2. Product Overview...2 3. Product Summary...2 4. Documentation...2 5. Underwriting...2 6. Qualifying Rate...2 7. Borrower Eligibility...2 8. Appraisal...3 9. Appraised

Table of Contents 1. Program Codes...2 2. Product Overview...2 3. Product Summary...2 4. Documentation...2 5. Underwriting...2 6. Qualifying Rate...2 7. Borrower Eligibility...2 8. Appraisal...3 9. Appraised

Disclosure Specialist Responsibilities. Lock Procedures. Processor Responsibilities. Appraisal Ordering

FHA 203K Streamline - Policies & Procedures FHA 203K Streamline will now be underwritten and funded in house. These applications should be originated in Mortgage Builder under the FHA203K-SR program code.

FHA 203K Streamline - Policies & Procedures FHA 203K Streamline will now be underwritten and funded in house. These applications should be originated in Mortgage Builder under the FHA203K-SR program code.

QUICK MORTGAGE GUIDE

QUICK MORTGAGE GUIDE TABLE OF CONTENTS FNMA CONVENTIONAL LOANS - Page 3 FHA LOANS - Page 7 VA LOANS - Page 11 ADJUSTABLE RATE MORTGAGES - Page 15 CONTACT INFORMATION - Page 16 FNMA CONVENTIONAL LOANS The

QUICK MORTGAGE GUIDE TABLE OF CONTENTS FNMA CONVENTIONAL LOANS - Page 3 FHA LOANS - Page 7 VA LOANS - Page 11 ADJUSTABLE RATE MORTGAGES - Page 15 CONTACT INFORMATION - Page 16 FNMA CONVENTIONAL LOANS The

FAQ s in general VA Loans

Oscar Castillo - REALTOR - Broker Associate (858) 775-1057 CalBRE lic# 01140298 www.oscarsellshomes.com FAQ s in general VA Loans General questions regarding the VA Loan program. What is the History of

Oscar Castillo - REALTOR - Broker Associate (858) 775-1057 CalBRE lic# 01140298 www.oscarsellshomes.com FAQ s in general VA Loans General questions regarding the VA Loan program. What is the History of

Sponsored by: EQUITY. Sid Shah Director, Mortgage Origination SShah@callequity.net 614-571-3893 RESOURCES, INC. mortgages

Sponsored by: EQUITY RESOURCES, INC. mortgages Sid Shah Director, Mortgage Origination SShah@callequity.net 614-571-3893 Exempt from Qualified Mortgage rule/law Any Veteran can refinance their Conventional,

Sponsored by: EQUITY RESOURCES, INC. mortgages Sid Shah Director, Mortgage Origination SShah@callequity.net 614-571-3893 Exempt from Qualified Mortgage rule/law Any Veteran can refinance their Conventional,

WHOLESALE VA IRRRL WITH APPRAISAL

Program Code(s): WHOLESALE VA IRRRL WITH APPRAISAL Maximum LTV/CLTV and Credit Score Requirements VF30 = 30 year VF15 = 15 year VA IRRRL With Appraisal 1 Occupancy LTV/CLTV 4 Min Credit Score 5 Investor

Program Code(s): WHOLESALE VA IRRRL WITH APPRAISAL Maximum LTV/CLTV and Credit Score Requirements VF30 = 30 year VF15 = 15 year VA IRRRL With Appraisal 1 Occupancy LTV/CLTV 4 Min Credit Score 5 Investor

Foreign National Lender Programs & Guidelines

Foreign National Lender Programs & Guidelines Lender Names, Contact Information & Phone Numbers First Choice Loan Services Mortgage Consultant: Frank Fisher Email: Frank@frankfisher.net Phone: Cell (407)

Foreign National Lender Programs & Guidelines Lender Names, Contact Information & Phone Numbers First Choice Loan Services Mortgage Consultant: Frank Fisher Email: Frank@frankfisher.net Phone: Cell (407)

Loan Estimate. Loan Terms. Projected Payments. Costs at Closing. Save this Loan Estimate to compare with your Closing Disclosure.

Loan Estimate DATE ISSUED APPLICANTS PROPERTY SALE PRICE Loan Terms Save this Loan Estimate to compare with your Closing Disclosure. LOAN TERM 30 years PURPOSE Purchase PRODUCT 5 Year Interest Only, 5/3

Loan Estimate DATE ISSUED APPLICANTS PROPERTY SALE PRICE Loan Terms Save this Loan Estimate to compare with your Closing Disclosure. LOAN TERM 30 years PURPOSE Purchase PRODUCT 5 Year Interest Only, 5/3

Conventional Fixed Rate Conforming Product Guidelines

Loan Parameters Loan Purpose Allowed Minimum Credit Score Maximum LTV/CLTV Owner Occupied & Second Home Maximum LTV/CLTV Non-Owner Occupants Max. Loan Amount Subordinate Financing Maximum Ratios Max. No.

Loan Parameters Loan Purpose Allowed Minimum Credit Score Maximum LTV/CLTV Owner Occupied & Second Home Maximum LTV/CLTV Non-Owner Occupants Max. Loan Amount Subordinate Financing Maximum Ratios Max. No.

DU User s Guide for VA Loans

DU User s Guide for VA Loans 1999, 2005 Fannie Mae. All rights reserved. Desktop Originator and Desktop Underwriter are registered trademarks of Fannie Mae. DO, DU, and GUS are trademarks of Fannie Mae.

DU User s Guide for VA Loans 1999, 2005 Fannie Mae. All rights reserved. Desktop Originator and Desktop Underwriter are registered trademarks of Fannie Mae. DO, DU, and GUS are trademarks of Fannie Mae.

Your home financing process checklist

Your home financing process checklist As you prepare to purchase a home or refinance your loan, it s important to know what to expect along the way. Here, we ve outlined some of the general steps in the

Your home financing process checklist As you prepare to purchase a home or refinance your loan, it s important to know what to expect along the way. Here, we ve outlined some of the general steps in the

HARP DU REFI PLUS Training

HARP DU REFI PLUS Training Offered by FIRST MORTGAGE CORPORATION JUNE 14, 2013 Desktop Underwriter is a registered trademark of Fannie Mae. Loan Prospector is a registered trademark of Freddie Mac. This

HARP DU REFI PLUS Training Offered by FIRST MORTGAGE CORPORATION JUNE 14, 2013 Desktop Underwriter is a registered trademark of Fannie Mae. Loan Prospector is a registered trademark of Freddie Mac. This

Corporate. Overview. Rate Locks. Wholesale Rate Lock Policy

Corporate Lock Desk Wholesale Rate Lock Policy Overview The Lock Desk Department will issue the daily rate sheets via e-mail as well as upload to www.famwholesale.com site every morning M-F. Sometimes

Corporate Lock Desk Wholesale Rate Lock Policy Overview The Lock Desk Department will issue the daily rate sheets via e-mail as well as upload to www.famwholesale.com site every morning M-F. Sometimes

1030HARP DU REFI PLUS (6/8/12)

") 1030HARP DU REFI PLUS (6/8/12) DESCRIPTION REQUIRED BORROWER BENEFIT DU Refi Plus is a limited cash-out refinance program that allows for expanded eligibility criteria, as well as reduced documentation

1030HARP DU REFI PLUS (6/8/12) DESCRIPTION REQUIRED BORROWER BENEFIT DU Refi Plus is a limited cash-out refinance program that allows for expanded eligibility criteria, as well as reduced documentation

Non-occupant co-borrowers are allowed. Borrowers to qualify at combined income and assets for standard FHA guidelines.

PRODUCT CHEAT SHEET-CA FHA $729,750 max loan amount in Orange County. If doing a loan in another county you can check max loan amount on the following link: https://entp.hud.gov/idapp/html/hicostlook.cfm

PRODUCT CHEAT SHEET-CA FHA $729,750 max loan amount in Orange County. If doing a loan in another county you can check max loan amount on the following link: https://entp.hud.gov/idapp/html/hicostlook.cfm

CalStar Mortgage Inc. For All Your Financing Needs

CalStar Mortgage Inc. For All Your Financing Needs Jasmen Vartanian Tel: 818-952-2701 Email: Jasmen@calstarinc.com www.calstarmortgage.com Excellent Service since 1987 1033 Foothill Blvd. La Canada Flintridge,

CalStar Mortgage Inc. For All Your Financing Needs Jasmen Vartanian Tel: 818-952-2701 Email: Jasmen@calstarinc.com www.calstarmortgage.com Excellent Service since 1987 1033 Foothill Blvd. La Canada Flintridge,

Appendix B: VA Forms and Their Uses

VA Pamphlet 26-7, Revised How to Use this Appendix This appendix lists and describes the forms most frequently used by lenders and other program participants in connection with the processing, closing,

VA Pamphlet 26-7, Revised How to Use this Appendix This appendix lists and describes the forms most frequently used by lenders and other program participants in connection with the processing, closing,

City of Miami Department of Community Development Florida Homebuyer Opportunity Program

City of Miami Department of Community Development Florida Homebuyer Opportunity Program The City s Florida Homebuyer Opportunity Program (FLHOP) provides assistance of up to $8,000 to income eligible homebuyers.

City of Miami Department of Community Development Florida Homebuyer Opportunity Program The City s Florida Homebuyer Opportunity Program (FLHOP) provides assistance of up to $8,000 to income eligible homebuyers.

PRE-CLOSING AUDIT WORKSHEET

1 PRE-CLOSING AUDIT WORKSHEET Performed by: Date: BORROWER LOAN# LOAN TYPE TRANSACTION TYPE ORIGINATION DATE STAGE LOAN IS IN LOAN ORIGINATOR PROCESSOR UNDERWRITER Loan Officer Rating: Acceptable Minor

1 PRE-CLOSING AUDIT WORKSHEET Performed by: Date: BORROWER LOAN# LOAN TYPE TRANSACTION TYPE ORIGINATION DATE STAGE LOAN IS IN LOAN ORIGINATOR PROCESSOR UNDERWRITER Loan Officer Rating: Acceptable Minor

RATE/TERM REFINANCE AND CASH-OUT - FIXED RATE

RATE/TERM REFINANCE AND CASH-OUT - FIXED RATE Occupancy Max Loan Amount Maximum LTV Maximum CLTV Min FICO Max Ratios Minimum Cash Investments Mortgage/Rental History Reserves Primary 1 Unit $417,000 80%

RATE/TERM REFINANCE AND CASH-OUT - FIXED RATE Occupancy Max Loan Amount Maximum LTV Maximum CLTV Min FICO Max Ratios Minimum Cash Investments Mortgage/Rental History Reserves Primary 1 Unit $417,000 80%

Lender Company Name 2.3 Street Address, City, State, ZIP 23.2.1 Save this Loan Estimate to compare with your Closing Disclosure. Loan Estimate 0.1 DATE ISSUED 1.1 APPLICANTS 2.1 123 Anywhere Street Anytown,

Lender Company Name 2.3 Street Address, City, State, ZIP 23.2.1 Save this Loan Estimate to compare with your Closing Disclosure. Loan Estimate 0.1 DATE ISSUED 1.1 APPLICANTS 2.1 123 Anywhere Street Anytown,