VA Loan Guaranty Program Serve the mortgage lending needs of borrowers who serve our country

|

|

|

- Tiffany Porter

- 7 years ago

- Views:

Transcription

1 VA Loan Guaranty Program Serve the mortgage lending needs of borrowers who serve our country Jaime A Garcia NMLS DRE Desktop Underwriter is a registered trademark of Fannie Mae. Loan Prospector is a registered trademark of Freddie Mac. This presentation is a summary and is not complete. This information is for mortgage professionals only and should not be distributed to or used by consumers or other third-parties. Information is accurate as of the date shown below and is subject to change without notice. 05/15/2012 1

2 Underwriting Methods Underwriting Standards Other General Guidelines UNDERWRITING GUIDELINES Jaime A Garcia NMLS DRE

3 Underwriting Method UW follows standard VA guidelines and regulations Refer to VA Handbook Chapter 4. (DU & LP Automated Underwriting Engines incorporates VA s credit standards) Underwriting Method Eligible Acceptable AUS Result Manual (Program 07 only) Yes N/A Desktop Underwriter (DU ) Yes Approve/Eligible Loan Prospector (LP) NOT at FMC Not Applicable A finding of Approve/Eligible can reduce the amount of documentation requirements, and underwriting time of a loan file Absence of the above findings does not provide a basis for denying a loan application. Manual UW is permitted on Program 07 only. Jaime A Garcia NMLS DRE

4 Topic VA Home Loan Program Description Ratios, Residual, Reserves Max DTI 41% - VA uses a single ratio Ratios may be exceeded with: DU approval, or Manually underwritten loans May be stretched to 46% if veteran meets residual requirement with strong compensating factors (such as high residual income) Residual Income VA uses Residual Income veteran should have at least the minimum residual income remaining to qualify When the DTI > 41%, the residual income should be at least 20% over stated guideline. Otherwise, a 2 nd UW signature is required Residual Income is calculated based on the total number of dependents and the number of persons residing in the household Reserves NO RESERVES for loan amounts up to $417,000 2 Months PITI for loan amounts exceeding conforming limit it Jaime A Garcia NMLS DRE

5 UW: General Guidelines Topic Description Co-Borrowers Allowed only if co-borrower is a veteran Must consider all income and debt Non-married borrowers or 2 veterans / active service personnel borrowers must be UW by VA as a prior approval Non-Borrowing Spouse Acceptable on Purchases only. Community Prop State rules: Credit report ordered but don t consider credit history in analysis Debts are counted in ratio calculation Non Occupant Co-Borrower Allowed Co-Signers Permitted (Program 07 only) Resident Alien & Non Permanent Resident Alien Allowed as long as primary occupying applicant is a Veteran Borrower Contribution No Minimum Required Repairs Repairs required by VA generally performed by seller or veteran Not required for minor or cosmetic defects or normal wear & tear # of VA loans Limited only by amount of available entitlement (New loan - O/O) Jaime A Garcia NMLS DRE

Resident Alien & Non Permanent Resident Alien Allowed as long as primary occupying applicant is a Veteran Borrower Contribution No Minimum Required Repairs Repairs required by VA generally")

6 Topic VA Home Loan Program Description UW: General Guidelines Funds to Close Gift from relative: provide acceptable gift letter to evidence withdrawal from donor and transfer to borrower Seller Contribution If given by seller, realtor, builder, must be considered in 4% contribution calc Not allowed from non-profit agencies Funds from Seller Contribution Borrowers own funds On jumbo loan amounts where veteran has to come in with down payment on a purchase, it cannot be gifted funds Up to 4% of the lesser of sales price or appraised value and above any discount points paid by seller. May be contributed from an interested party (seller concession) to be applied towards closing costs and prepaid p items. Includes: VA funding Fee Prepayment of property taxes and insurance Buy-down funds temporary or extra point for permanent buy-down Payoff credit balances or judgments on behalf of the borrower Gifts such as TV, Lawnmower, Microwave, etc. Temporary Buy-downs Allowed on 30 Year Fixed product only Survey Requirements Required on all property types except condominiums In areas where surveys are not customary, the title insurance policy must insure over matters of survey Termite inspection Escrow Waivers Assumable Prepayments Required for all properties located in areas prone to termite infestation Not allowed all VA loans must have Impounds. Yes NONE 6

to be applied towards closing costs and prepaid p items.")

7 Topic Minimum Fico Scores VA Home Loan Program Description UW: Credit NO minimum with 07 Program See FMC rate sheet for program fico requirements Use FMC FHA Overlays as a guide for scores < 620 Bankruptcy (Chapter 7) Bankruptcy (Chapter 13) At least 2 years from discharge date; bankruptcy may be disregarded. Reason must be documented and not likely to reoccur. 1-2 Years from discharge date; Credit has been re-established for that period of time Was caused by circumstances beyond borrower s control and Evidence the applicants have demonstrated their ability to handle their credit affairs 1 Year seasoning with satisfactory payment performance Permission from court to enter into new obligation Foreclosures Treat same as Chapter 7 BK. If it was a VA loan, check if any amount of entitlement was forfeited Includes Deed in Lieu of Foreclosure and Short Sales, Collection Payoff is not required for approval Standard requirement is any individual amount up to $250 or cumulative of <$1,000 does not have to be paid prior to closing Any exception must be documented and approved by FMC UW Open collections are considered Recent Derogatory Items regardless of age No lates in last 12 months on manually UW loans or < 620 fico scores Obtain credit explanation even if not required by AUS Judgments Must be paid in full or A satisfactory payment plan is in effect at time of application with no late payments Consumer Credit Permitted with 12 months satisfactory repayments and administrator signs letter allowing applicant Counseling to seek financing Jaime A Garcia NMLS DRE

8 INCOME 1. Stable and Reliable 2. Anticipated to continue 3. Sufficient to support debt 4. Must be properly verified Jaime A Garcia NMLS DRE

9 UW: Income Topic Description Wages 2 year history. Less than 2 years considered on a case by case basis at UW discretion Overtime Income & 2 nd Job Income 2 year history. Less than 2 years considered on a case by case basis at UW discretion Commission Income 2 year history, unless previous related employment or specialized training 1040 s required (watch for 2106 expenses) Alimony/Child Support Must be verified and stable Non Taxable Income Allowed Does not apply to residual income Includes Disability, Public Assistance, Military Allowances, etc. Retirement Income Allowed Only non-taxable income may be grossed up for ratio Seasonal jobs and unemployment May be averaged 24 month history for both, if it is considered normal for the field the borrower is in Projected Income Generally not acceptable. Exceptions OK. Eg., Bonuses, Performance raises, etc. to begin within 60 days of closing and verified by employer New jobs with non-revocable contract if borrower can support PITI & other obligations during the interim period 9

10 Topic Rental Income VA Home Loan Program Description UW: Income Cont d Subject Property: Program 07 has no equity requirement on departing residence Multi-Unit Properties 6 months PITI required Must have prior experience managing properties Other Investment t Properties owned by Borrower Obtain individual tax returns for last 2 years showing rental income generated by the property 3 Months PITI reserves required Previous Owner Occupied Property See cash to close page Provide lease Minus 75% vacancy factor May be used to offset mortgage payment (of the other property) if qualify Cannot be used as income NO reserves required Self Employed 25% or greater ownership interest in a business Borrowers Must be self-employed for 2 years Income is averaged 24 months unless tax returns disclose questionable stability of income 1040 s required Other Income Other Income, Pension, Retirement, Disability, etc. must be verified. Document per AUS 10

11 UW: Income Cont d Active Military income consider base pay as stable & reliable unless applicant is within 12 months of release of active duty. Leave and Earnings Statement is required (LES) instead of a VOE and must be no more than 120 days old (180 for new construction). If re-enlisting, letter from commanding officer & the veteran stating may/will reenlist. Military quarters allowance and Basic Allowance Subsistence (BAS) can be considered income. Both non-taxable. Other Military allowances obtain verification of type and amount and length of receipt. Income from Reserves or National Guard can be considered if the length of total service indicates a strong probability of continuance. 11

can be considered income. Both non-taxable.")

12 UW: Income Tax Calculator Determine the appropriate deductions d for Federal income tax and Social Security/Medicare by using Employer s Tax Guide charts. Determine the appropriate deductions for state and local taxes. Social Security/Medicare is 7.65% of gross monthly income; OR Log on to and select Personal Calculators, then Paycheck Calculator to determine all types of taxes. Jaime A Garcia NMLS DRE

13 UW: Debts & Obligations Must verify alimony and child support. Student loans scheduled to begin within 12 months of the Note Date will be counted. Loans secured by deposited funds are not counted. Installment debts with less than 10 months remaining do not necessarily need to be included in credit qualifying. Large payments should be considered. Do not omit these debts in the AUS system. Always populate liabilities in AUS. 401(k) loans are not used against in debt calculation. Loan Pay advances (primarily seen on LES statement of in-service veterans) are used against and must be documented. Jaime A Garcia NMLS DRE

loans are not used against in debt calculation.")

14 UW: Compensating Factors Topic Compensating Factors Sample Compensating Factors Description Valid compensating factors should logically be able to compensate for the identified weakness in the loan. Should represent unusual strength rather than mere satisfaction of basic program requirements. Eg., Sufficient assets for closing or meets residual income guidelines is not a compensating factor. Eg., Significant liquid assets may compensate for a residual income shortfall whereas long term employment would not. Excellent credit history Conservative use of consumer credit Minimal consumer debt Long-term employment Significant liquid assets Sizable down payment Existence of equity in a refinance loan Military benefits High residual income Low DTI Tax credits for child care Tax benefits of home ownership Jaime A Garcia NMLS DRE

15 Appraisal Requirements for Loans Exceeding $417,000 ($625,000 in AK & HI) Loan Amount Appraisal Requirement $417,001 - $650,000 VA-required appraisal $650,001 - $1 million VA-required appraisal and LARA > $1 million FMC at this time VA-required appraisal and field review Appraisals are ordered via The Appraisal System (TAS) by the FMC Underwriting Department See FMC Bulletin for the most current guidelines for ordering VA Appraisals 15

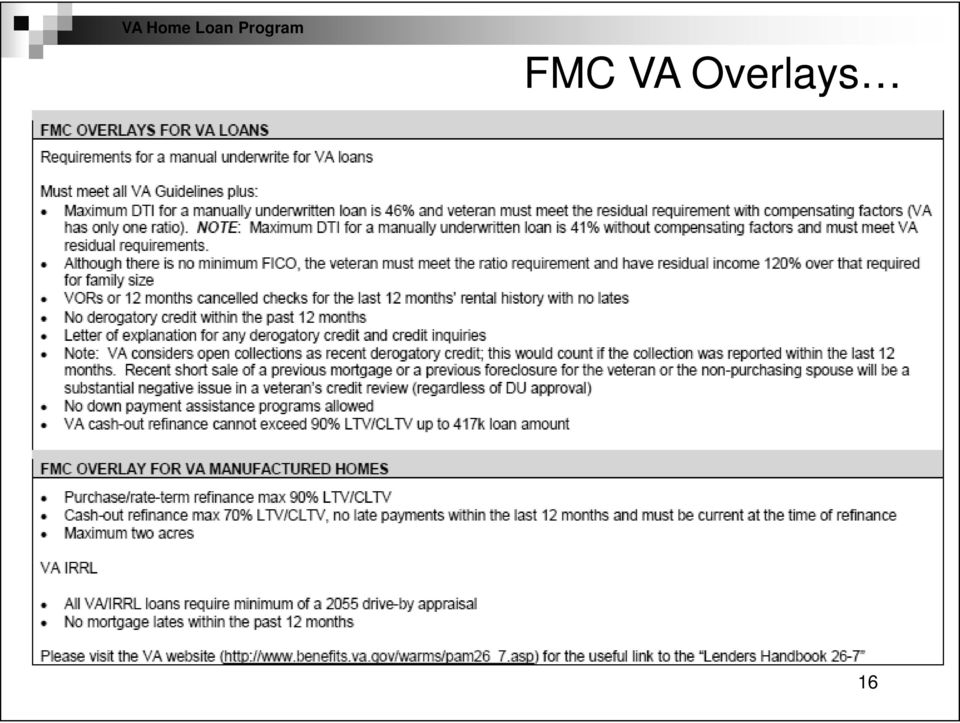

16 FMC VA Overlays 16

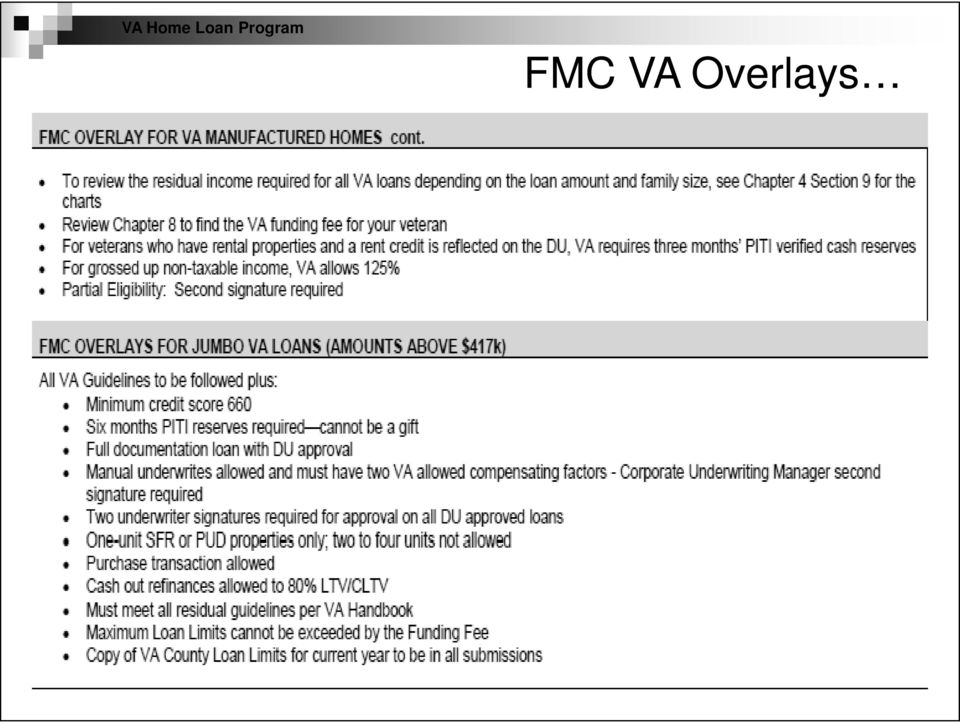

17 FMC VA Overlays 17

18 Borrower (Veteran) Allowable Fees & Charges VETERAN FEES & CHARGES Jaime A Garcia NMLS DRE

19 Topic Description Rates & Fees Interest Interest rate is fixed and the payment is fully amortized over the entire term of the loan. Rates For ARM loans, interest rate is fixed during the initial period and may change after the fixed period based on index, margin and caps. Available on page 2 of FMC Rate sheet Points (Origination i & Discount) Points are negotiated between LO and Veteran: 1% Max Origination Point Reasonable Discount Points (based on loan amount plus funding fee if financed) Points may be financed into the loan on refinances (IRRRLs caps 2% financed) Closing Costs Chapter 8.2 of VA Lender Handbook Those payable by the veteran are limited by regulation to a specific list of items plus a 1% flat fee charge by the lender (See Fee Section for more information) Reasonable & customary amounts for Itemized Fees and Charges Any other party, including seller, can pay any costs on behalf of the veteran. Closing costs cannot be financed in the loan except on certain refinancing loans Can be borrowed but must be included in DTI calculation 19

Points may be financed into the loan on refinances (IRRRLs caps 2% financed) Closing Costs Chapter 8.")

20 Veteran Fees & Charges Fees/Charges Veteran CAN pay Fees/Charges Veterans CANNOT pay 1% Origination Fee PLUS Escrow Reasonable Discount Points (Max 2% on IRRRL) Processing, Document, Underwriting Termite Report and Repairs, Appraisal, Recording, Credit Report, Flood Certification, and Survey Fee Prepaid Items, Taxes, Assessments, and Insurance Hazard Insurance Premium, Title Insurance Courier Fee on Refinances Tax Service Fees Notary Fees Appraisals requested by FMC or Seller for reconsideration of value Appraisals requested by parties other than FMC or the Veteran Attorneys Fees 1% Flat Lender Fee to cover all unreimbursable itemized fees & charges Brokerage Fees 20

21 Itemized Fees & Charges: FYI - Veteran Fees & Charges Veteran can pay any or all of the itemized fees and charges listed below in amounts that are reasonable and customary. If service is performed by a 3 rd party, Veteran cannot pay any amount that exceeds the actual charge by the 3 rd party. Appraisals, including 2 nd appraisals requested by the Veteran for reconsideration of value Recording fees and Recording Taxes or other charges incident id to recordation Credit report or on AUS-decisioned loans, up to $50 evaluation fee charged in lieu of credit report Prepaid items such as taxes, assessments, initial deposit for the tax and insurance account, etc. Hazard insurance premium including flood insurance, if required Flood Insurance Determination Survey Pest Inspection fees for refinances only Title Insurance & Title examination Special mailing fees such as fed-ex, express mail, etc. for refinance loans only 21

Name Account Executive. Contact Number E-Mail Address Website Address

VA Loan Information Name Account Executive Contact Number E-Mail Address Website Address Benefits of VA No Down Payment, 100% up to $417,000. No Monthly Mortgage Insurance Premiums. Leniency on Credit

VA Loan Information Name Account Executive Contact Number E-Mail Address Website Address Benefits of VA No Down Payment, 100% up to $417,000. No Monthly Mortgage Insurance Premiums. Leniency on Credit

Product Product Code Loan Term 30-Year FRM FHA FHA30 30-years 15-Year FRM FHA FHA15 15-Years. Property Type Lowest Maximum (Floor)

") FHA Guidelines Product Description FHA Fixed Rate 15 and 30 Year Terms Fully Amortizing Product Codes Maximum s Product Product Code Loan Term 30-Year FRM FHA FHA30 30-years 15-Year FRM FHA FHA15 15-Years

FHA Guidelines Product Description FHA Fixed Rate 15 and 30 Year Terms Fully Amortizing Product Codes Maximum s Product Product Code Loan Term 30-Year FRM FHA FHA30 30-years 15-Year FRM FHA FHA15 15-Years

VA Product Guidelines

August 10, 2015 VA Product Guidelines Purchase Occupancy Units LTV CLTV Primary 1-4 100 100 620 Rate/Term Refinance Occupancy Units LTV CLTV Primary 1-4 100 100 620 IRRRL Occupancy Units LTV CLTV Primary

August 10, 2015 VA Product Guidelines Purchase Occupancy Units LTV CLTV Primary 1-4 100 100 620 Rate/Term Refinance Occupancy Units LTV CLTV Primary 1-4 100 100 620 IRRRL Occupancy Units LTV CLTV Primary

FHA STREAMLINE REFINANCE PRODUCT PROFILE

Terms 30 Year Terms 15 Year Terms Maximum LTV/CLTV LTV/CLTV Score LTV/CLTV Score Non-Credit Qualifying N/A N/A Credit Qualifying 97.75% 97.75% Applies to Case Numbers assigned on or after January 26, 2015

Terms 30 Year Terms 15 Year Terms Maximum LTV/CLTV LTV/CLTV Score LTV/CLTV Score Non-Credit Qualifying N/A N/A Credit Qualifying 97.75% 97.75% Applies to Case Numbers assigned on or after January 26, 2015

VA IRRRL GUIDELINES. Table of Contents

Page 1 of 8 Table of Contents LTV MATRIX... 3 PROGRAM SUMMARY... 3 LOAN AMOUNTS... 3 LOAN PROGRAM CODES... 3 LOAN TERMS... 3 ADJUSTMENT RATE DETAILS... 3 ELIGIBLE PROPERTY TYPES... 3 INELIGIBLE PROPERTY

Page 1 of 8 Table of Contents LTV MATRIX... 3 PROGRAM SUMMARY... 3 LOAN AMOUNTS... 3 LOAN PROGRAM CODES... 3 LOAN TERMS... 3 ADJUSTMENT RATE DETAILS... 3 ELIGIBLE PROPERTY TYPES... 3 INELIGIBLE PROPERTY

VA Product Guidelines

July 16, 2015 VA Product Guidelines Purchase Occupancy Units LTV CLTV Minimum Credit Score Primary 1-4 100 100 620 Rate/Term Refinance Occupancy Units LTV CLTV Minimum Credit Score Primary 1-4 90 90 620

July 16, 2015 VA Product Guidelines Purchase Occupancy Units LTV CLTV Minimum Credit Score Primary 1-4 100 100 620 Rate/Term Refinance Occupancy Units LTV CLTV Minimum Credit Score Primary 1-4 90 90 620

FHA Standard Refinance Cash Out

This matrix is intended as an aid to help determine whether a property/loan qualifies for certain financing. It is not intended as a replacement for FHA guidelines. Users are expected to know and comply

This matrix is intended as an aid to help determine whether a property/loan qualifies for certain financing. It is not intended as a replacement for FHA guidelines. Users are expected to know and comply

FHA 30, 15 Year Fixed Refinance Products 203b, 234c F30; F15; F30HPML Loan Amount and LTV Limitations

Units Length of Ownership 1 1-4 Units FHA 30, 15 Year Fixed Refinance Products 203b, 234c F30; F15; F30HPML Loan Amount and LTV Limitations < 1 year prior to application and the loan is not an existing

Units Length of Ownership 1 1-4 Units FHA 30, 15 Year Fixed Refinance Products 203b, 234c F30; F15; F30HPML Loan Amount and LTV Limitations < 1 year prior to application and the loan is not an existing

VA IRRL 2. CURRENT FIRST MORTGAGE ELIGIBILITY

1. PRODUCT DESCRIPTION VA Fixed Rate and ARM Mortgages for Refinance Transactions Fixed Rate Mortgage 10 to 30 years in 5 year increments Fully amortizing Qualified Mortgage (QM) Safe Harbor loans are

1. PRODUCT DESCRIPTION VA Fixed Rate and ARM Mortgages for Refinance Transactions Fixed Rate Mortgage 10 to 30 years in 5 year increments Fully amortizing Qualified Mortgage (QM) Safe Harbor loans are

EFFECTIVE SEP 14, 2015. FHA Rule Changes. www.greenpathfunding.com

EFFECTIVE SEP 14, 2015 FHA Rule Changes www.greenpathfunding.com FHA Changes: Assets 2015 1 Any single deposit that exceeds 25% of the total monthly qualifying income on the loan. Additionally, any questionable

EFFECTIVE SEP 14, 2015 FHA Rule Changes www.greenpathfunding.com FHA Changes: Assets 2015 1 Any single deposit that exceeds 25% of the total monthly qualifying income on the loan. Additionally, any questionable

Non-occupant co-borrowers are allowed. Borrowers to qualify at combined income and assets for standard FHA guidelines.

PRODUCT CHEAT SHEET-CA FHA $729,750 max loan amount in Orange County. If doing a loan in another county you can check max loan amount on the following link: https://entp.hud.gov/idapp/html/hicostlook.cfm

PRODUCT CHEAT SHEET-CA FHA $729,750 max loan amount in Orange County. If doing a loan in another county you can check max loan amount on the following link: https://entp.hud.gov/idapp/html/hicostlook.cfm

VA Guaranteed Home Loans Training

Serve the mortgage lending needs of borrowers who serve our country VA Guaranteed Home Loans Training OFFERED BY FIRST MORTGAGE CORPORATION NOVEMBER 21, 2014 Desktop Underwriter is a registered trademark

Serve the mortgage lending needs of borrowers who serve our country VA Guaranteed Home Loans Training OFFERED BY FIRST MORTGAGE CORPORATION NOVEMBER 21, 2014 Desktop Underwriter is a registered trademark

VA FIXED RATE PROGRAM HIGHLIGHTS

Program Summary Loan Term & Program Category Entitlement These guidelines represent underwriting requirements for VA fixed rate mortgages. Also review the VA Lender s Handbook for any guidelines not specifically

Program Summary Loan Term & Program Category Entitlement These guidelines represent underwriting requirements for VA fixed rate mortgages. Also review the VA Lender s Handbook for any guidelines not specifically

Max LTV/CLTV. Units. Max Debt Ratio Purchase or Refinance. 700 1 70% $1,500,000 40% Rate/Term Refinance Cash-Out N/A

Jumbo Series 3 Summary Product Types Minimum Loan Amount 5/1 and 7/1 ARMs $417,001 or Fannie/Freddie loan limits 5/1 ARM qualifies at the greater of the fully indexed rate or Note rate +2%. 7/1 ARM qualifies

Jumbo Series 3 Summary Product Types Minimum Loan Amount 5/1 and 7/1 ARMs $417,001 or Fannie/Freddie loan limits 5/1 ARM qualifies at the greater of the fully indexed rate or Note rate +2%. 7/1 ARM qualifies

ditech BUSINESS LENDING FREDDIE MAC ELIGIBLE FIXED RATE TEXAS HOME EQUITY PRODUCT

1. PRODUCT DESCRIPTION Conventional Conforming fixed rate mortgage Servicing retained 10 to 30 years in 5 year increments Fully amortizing Qualified Mortgage (QM) Safe Harbor loans are permitted Qualified

1. PRODUCT DESCRIPTION Conventional Conforming fixed rate mortgage Servicing retained 10 to 30 years in 5 year increments Fully amortizing Qualified Mortgage (QM) Safe Harbor loans are permitted Qualified

HARP DU REFI PLUS Training

HARP DU REFI PLUS Training Offered by FIRST MORTGAGE CORPORATION JUNE 14, 2013 Desktop Underwriter is a registered trademark of Fannie Mae. Loan Prospector is a registered trademark of Freddie Mac. This

HARP DU REFI PLUS Training Offered by FIRST MORTGAGE CORPORATION JUNE 14, 2013 Desktop Underwriter is a registered trademark of Fannie Mae. Loan Prospector is a registered trademark of Freddie Mac. This

A Simplified Overview of FHA Loan Origination

Introduction to FHA Origination A Simplified Overview of FHA Loan Origination Topics of Discussion Introduction to FHA Fundamentals of Loan Origination FHA Loan Limits Borrower Eligibility Property Eligibility

Introduction to FHA Origination A Simplified Overview of FHA Loan Origination Topics of Discussion Introduction to FHA Fundamentals of Loan Origination FHA Loan Limits Borrower Eligibility Property Eligibility

Section 1: Loan Characteristics

Home Flex Quick Reference: Program Summary The following is an outline of the underwriting and closing requirements of New Hampshire Housing Home Flex program, which is available to lenders who have signed

Home Flex Quick Reference: Program Summary The following is an outline of the underwriting and closing requirements of New Hampshire Housing Home Flex program, which is available to lenders who have signed

PORTFOLIO ARM CLOSED END 2 ND TD. Table of Contents

Table of Contents 1. Program Codes...2 2. Product Overview...2 3. Product Summary...2 4. Documentation...2 5. Underwriting...2 6. Qualifying Rate...2 7. Borrower Eligibility...2 8. Appraisal...3 9. Appraised

Table of Contents 1. Program Codes...2 2. Product Overview...2 3. Product Summary...2 4. Documentation...2 5. Underwriting...2 6. Qualifying Rate...2 7. Borrower Eligibility...2 8. Appraisal...3 9. Appraised

QUICK MORTGAGE GUIDE

QUICK MORTGAGE GUIDE TABLE OF CONTENTS FNMA CONVENTIONAL LOANS - Page 3 FHA LOANS - Page 7 VA LOANS - Page 11 ADJUSTABLE RATE MORTGAGES - Page 15 CONTACT INFORMATION - Page 16 FNMA CONVENTIONAL LOANS The

QUICK MORTGAGE GUIDE TABLE OF CONTENTS FNMA CONVENTIONAL LOANS - Page 3 FHA LOANS - Page 7 VA LOANS - Page 11 ADJUSTABLE RATE MORTGAGES - Page 15 CONTACT INFORMATION - Page 16 FNMA CONVENTIONAL LOANS The

VA Quick Reference Guides

Finance Type Occupancy Product Codes Purchase, Cash-Out and Rate & Term Refinance, Interest Rate Reduction Refinance Loan (IRRRL) Owner Occupied only, Second Homes not allowed, Investment properties not

Finance Type Occupancy Product Codes Purchase, Cash-Out and Rate & Term Refinance, Interest Rate Reduction Refinance Loan (IRRRL) Owner Occupied only, Second Homes not allowed, Investment properties not

Contents. VA Credit Overlays

Contents... 1 Introduction... 3 Links... 3 Transaction Types... 3 Purchase Transactions... 3 Refinance Transaction Regular Refinance... 3 Refinance Transaction Interest Rate Reduction Refinance Loan/IRRRL...

Contents... 1 Introduction... 3 Links... 3 Transaction Types... 3 Purchase Transactions... 3 Refinance Transaction Regular Refinance... 3 Refinance Transaction Interest Rate Reduction Refinance Loan/IRRRL...

VA Refinance IRRRL. VA Refinance IRRRL

This matrix is intended as an aid to help determine whether a property/loan qualifies for certain financing. It is not intended as a replacement for VA guidelines. Users are expected to know and comply

This matrix is intended as an aid to help determine whether a property/loan qualifies for certain financing. It is not intended as a replacement for VA guidelines. Users are expected to know and comply

VA Lending Basic Training

VA Lending Basic Training Brought to you by: Quicken Loans Mortgage Services Q-University October 19, 2011 February 2014 1 What You will learn Today The Facts and Benefits Of VA Who is Eligible for VA

VA Lending Basic Training Brought to you by: Quicken Loans Mortgage Services Q-University October 19, 2011 February 2014 1 What You will learn Today The Facts and Benefits Of VA Who is Eligible for VA

ditech BUSINESS LENDING FREDDIE MAC ELIGIBLE ARM PRODUCT CORRESPONDENT ONLY

1. PRODUCT DESCRIPTION Conventional Conforming five year/one year adjustable rate mortgage Servicing retained 30-year term Fully amortizing Non-convertible ARM Plan ID 2725 Manufactured homes not eligible

1. PRODUCT DESCRIPTION Conventional Conforming five year/one year adjustable rate mortgage Servicing retained 30-year term Fully amortizing Non-convertible ARM Plan ID 2725 Manufactured homes not eligible

Choice Jumbo Mortgage

Finance Type Purchase/Rate and Term Refinance Property Type Primary Residence Second Home Investment Max Loan Max LTV Min FICO Max LTV Min FICO Max LTV Min FICO $1,000,000 80% 70% 80% N/A N/A SFR/PUD/

Finance Type Purchase/Rate and Term Refinance Property Type Primary Residence Second Home Investment Max Loan Max LTV Min FICO Max LTV Min FICO Max LTV Min FICO $1,000,000 80% 70% 80% N/A N/A SFR/PUD/

RATE/TERM REFINANCE AND CASH-OUT - FIXED RATE

RATE/TERM REFINANCE AND CASH-OUT - FIXED RATE Occupancy Max Loan Amount Maximum LTV Maximum CLTV Min FICO Max Ratios Minimum Cash Investments Mortgage/Rental History Reserves Primary 1 Unit $417,000 80%

RATE/TERM REFINANCE AND CASH-OUT - FIXED RATE Occupancy Max Loan Amount Maximum LTV Maximum CLTV Min FICO Max Ratios Minimum Cash Investments Mortgage/Rental History Reserves Primary 1 Unit $417,000 80%

Magnolia Bank VA Refinance Options

Interest Rate Reduction Refinance Loans (IRRRLS) Eligibility Cash Out Refinance 1. ELIGIBLE PRODUCTS VA Fixed Rate Product VA Hybrid ARMs VA High Balance Products VA Fixed Rate Product VA Hybrid ARMs VA

Interest Rate Reduction Refinance Loans (IRRRLS) Eligibility Cash Out Refinance 1. ELIGIBLE PRODUCTS VA Fixed Rate Product VA Hybrid ARMs VA High Balance Products VA Fixed Rate Product VA Hybrid ARMs VA

Sponsored by: EQUITY. Sid Shah Director, Mortgage Origination SShah@callequity.net 614-571-3893 RESOURCES, INC. mortgages

Sponsored by: EQUITY RESOURCES, INC. mortgages Sid Shah Director, Mortgage Origination SShah@callequity.net 614-571-3893 Exempt from Qualified Mortgage rule/law Any Veteran can refinance their Conventional,

Sponsored by: EQUITY RESOURCES, INC. mortgages Sid Shah Director, Mortgage Origination SShah@callequity.net 614-571-3893 Exempt from Qualified Mortgage rule/law Any Veteran can refinance their Conventional,

BankSouth Mortgage Direct VA Fixed Rate and Adjustable Rate Guidelines

BankSouth Mortgage Direct VA Fixed Rate and Adjustable Rate Guidelines BSM Direct guidelines have been created to provide guidance and consistency in determining credit decisions. The guides are not all

BankSouth Mortgage Direct VA Fixed Rate and Adjustable Rate Guidelines BSM Direct guidelines have been created to provide guidance and consistency in determining credit decisions. The guides are not all

11.1 INTRODUCTION 11.2 THE RATIOS

0BCHAPTER 11: RATIO ANALYSIS 11.1 INTRODUCTION Ratios are used to determine whether the borrower s repayment income can reasonably be expected to meet the anticipated monthly housing expense and total

0BCHAPTER 11: RATIO ANALYSIS 11.1 INTRODUCTION Ratios are used to determine whether the borrower s repayment income can reasonably be expected to meet the anticipated monthly housing expense and total

FHA Streamline (Full Credit and Non-Credit Qualifying)

") . This matrix is intended as an aid to help determine whether a property/loan qualifies for certain financing. It is not intended as a replacement for FHA guidelines. Users are expected to know and comply

. This matrix is intended as an aid to help determine whether a property/loan qualifies for certain financing. It is not intended as a replacement for FHA guidelines. Users are expected to know and comply

PRODUCT MATRIX 7/25/2012

PRODUCT MATRIX 7/25/2012 For general underwriting questions and scenarios or product guideline interpretation, call the Underwriting Help Line at (866) 807-6049 For status, pricing, registration and closing

PRODUCT MATRIX 7/25/2012 For general underwriting questions and scenarios or product guideline interpretation, call the Underwriting Help Line at (866) 807-6049 For status, pricing, registration and closing

`2 TERMS AND CONDITIONS

`2 TERMS AND CONDITIONS Each House Key Program Mortgage Loan must satisfy the following terms and conditions: LOAN TYPES Fixed rate FHA 203(b), 234 (c), HUD 184, VA, USDA Rural Development, and Conventional

`2 TERMS AND CONDITIONS Each House Key Program Mortgage Loan must satisfy the following terms and conditions: LOAN TYPES Fixed rate FHA 203(b), 234 (c), HUD 184, VA, USDA Rural Development, and Conventional

CALHOME MORTGAGE ASSISTANCE PROGRAM GUIDELINES

PLANNING AND DEVELOPMENT DEPARTMENT HOUSING AND COMMUNITY DEVELOPMENT DIVISION CALHOME MORTGAGE ASSISTANCE PROGRAM GUIDELINES PROGRAM OVERVIEW The CalHome Mortgage Assistance Program is a program funded

PLANNING AND DEVELOPMENT DEPARTMENT HOUSING AND COMMUNITY DEVELOPMENT DIVISION CALHOME MORTGAGE ASSISTANCE PROGRAM GUIDELINES PROGRAM OVERVIEW The CalHome Mortgage Assistance Program is a program funded

E MORTGAGE MANAGEMENT, LLC 702 VA ARMS PRODUCT GUIDELINES

E MORTGAGE MANAGEMENT, LLC 702 VA ARMS PRODUCT GUIDELINES 2/24/2015 Mortgage Eligibility Product Code Short Description Long Description Description VF31 VA 3 YR ARM VF31 - VA 3-1 ARM VF51 VA 5 YR ARM

E MORTGAGE MANAGEMENT, LLC 702 VA ARMS PRODUCT GUIDELINES 2/24/2015 Mortgage Eligibility Product Code Short Description Long Description Description VF31 VA 3 YR ARM VF31 - VA 3-1 ARM VF51 VA 5 YR ARM

VA FIXED RATE PRODUCT

Primary 1 Unit Max Loan Amount Max Loan Amount Max Loan Amount See VA County Limits LTV CLTV Min FICO Max Ratios 96.50% 96.50% 55% 600 100% 100% 50% LTV CLTV Min FICO Max Ratios Minimum Cash Investments

Primary 1 Unit Max Loan Amount Max Loan Amount Max Loan Amount See VA County Limits LTV CLTV Min FICO Max Ratios 96.50% 96.50% 55% 600 100% 100% 50% LTV CLTV Min FICO Max Ratios Minimum Cash Investments

Conventional DU Refi Plus

Endeavor America Loan Services Conventional DU Refi Plus Guidelines Conventional Guidelines... 3 Matrix... 3 Overview... 3 Program Expiration... 3 Loan Purpose... 4 Maximum LTV, CLTV, and HCLTV Ratios

Endeavor America Loan Services Conventional DU Refi Plus Guidelines Conventional Guidelines... 3 Matrix... 3 Overview... 3 Program Expiration... 3 Loan Purpose... 4 Maximum LTV, CLTV, and HCLTV Ratios

CITY OF SAN DIEGO 3% INTEREST DEFERRED LOAN PROGRAM GUIDELINES

CITY OF SAN DIEGO 3% INTEREST DEFERRED LOAN PROGRAM GUIDELINES Program Overview: BUYERS EARNING 100% OR LESS OF AREA MEDIAN INCOME (AMI) The 3% Interest Deferred Loan Program is a homeownership program

CITY OF SAN DIEGO 3% INTEREST DEFERRED LOAN PROGRAM GUIDELINES Program Overview: BUYERS EARNING 100% OR LESS OF AREA MEDIAN INCOME (AMI) The 3% Interest Deferred Loan Program is a homeownership program

PURCHASE AND RATE TERM REFINANCE 1. Occupancy Units FICO LTV/CLTV Loan Amount

EXPRESS JUMBO FIXED RATE AND ARM PROGRAM MATRIX: PURCHASE AND RATE TERM REFINANCE 1 Occupancy Units FICO LTV/CLTV Loan Amount 80/80 $1,500,000 Primary Residence 1 720 75/75 $1,750,000 70/70 $2,000,000

EXPRESS JUMBO FIXED RATE AND ARM PROGRAM MATRIX: PURCHASE AND RATE TERM REFINANCE 1 Occupancy Units FICO LTV/CLTV Loan Amount 80/80 $1,500,000 Primary Residence 1 720 75/75 $1,750,000 70/70 $2,000,000

E MORTGAGE MANAGEMENT, LLC 701 VA FIXED PRODUCT GUIDELINES

E MORTGAGE MANAGEMENT, LLC 70 VA FIXED PRODUCT GUIDELINES 2/24/205 Mortgage Eligibility Product Code Short Description Long Description Description VF5 VA 5 YR VF5 - VA FIXED 5 YEAR VF20 VA 20 YR VF20

E MORTGAGE MANAGEMENT, LLC 70 VA FIXED PRODUCT GUIDELINES 2/24/205 Mortgage Eligibility Product Code Short Description Long Description Description VF5 VA 5 YR VF5 - VA FIXED 5 YEAR VF20 VA 20 YR VF20

It s easier than you think! Phoenix Regional Loan Center

It s easier than you think! Phoenix Regional Loan Center Why VA Loans? Help veterans Fast and easy to process Flexible underwriting standards Potential Income--- Over 18.6 Billion Loans Totaling $1,027,282,752,622!

It s easier than you think! Phoenix Regional Loan Center Why VA Loans? Help veterans Fast and easy to process Flexible underwriting standards Potential Income--- Over 18.6 Billion Loans Totaling $1,027,282,752,622!

Page 1 of 9 Table of Contents

Page 1 of 9 Table of Contents LTV MATRIX... 2 PROGRAM SUMMARY... 3 LOAN AMOUNTS... 3 Conforming... 3 High Balance... 3 LOAN PROGRAM CODES... 3 LOAN TERMS... 3 ADJUSTMENT RATE DETAILS... 4 ELIGIBLE PROPERTY

Page 1 of 9 Table of Contents LTV MATRIX... 2 PROGRAM SUMMARY... 3 LOAN AMOUNTS... 3 Conforming... 3 High Balance... 3 LOAN PROGRAM CODES... 3 LOAN TERMS... 3 ADJUSTMENT RATE DETAILS... 4 ELIGIBLE PROPERTY

VA Product Profile 05.01.2014

Maximum LTV / CLTV and FICO Requirements Purchase VA IRRRL / Rate & Term Cash-out Refinance Maximum LTV 1 / CLTV 1 Min FICO 2 Maximum LTV 1 / CLTV 1 Min FICO 2 Maximum LTV 1 / CLTV 1 Min FICO 2 100% 640

Maximum LTV / CLTV and FICO Requirements Purchase VA IRRRL / Rate & Term Cash-out Refinance Maximum LTV 1 / CLTV 1 Min FICO 2 Maximum LTV 1 / CLTV 1 Min FICO 2 Maximum LTV 1 / CLTV 1 Min FICO 2 100% 640

E MORTGAGE MANAGEMENT, LLC 704 VA

E MORTGAGE MANAGEMENT, LLC 704 VA IRRRLs PRODUCT GUIDELINES 1/26/2015 Mortgage Eligibility Product Code Short Long Description Description Description VF15IRL VA 15 YR IRRRL VF15IRL - VA 15 YR IRRRL VF30IRL

E MORTGAGE MANAGEMENT, LLC 704 VA IRRRLs PRODUCT GUIDELINES 1/26/2015 Mortgage Eligibility Product Code Short Long Description Description Description VF15IRL VA 15 YR IRRRL VF15IRL - VA 15 YR IRRRL VF30IRL

Financing Residential Real Estate

Financing Residential Real Estate Chapter 1: Finance and Investment Borrowing Money to Buy a Home Investments and Returns Types of Investments Ownership Investments Debt Investments Securities Investment

Financing Residential Real Estate Chapter 1: Finance and Investment Borrowing Money to Buy a Home Investments and Returns Types of Investments Ownership Investments Debt Investments Securities Investment

FHA LOAN PROGRAM Conforming and High Balance Loan Amounts

FHA PRODUCT MATRIX Purchase Rate and Term Cash Out Units LTV/CLTV Fico* Units LTV/CLTV Fico Units LTV/CLTV Fico 1 4 96.5/105 620 1 4 97.75/97.75 620 1 4 85/85 620 FYIs: Complete HUD guidelines can be referenced

FHA PRODUCT MATRIX Purchase Rate and Term Cash Out Units LTV/CLTV Fico* Units LTV/CLTV Fico Units LTV/CLTV Fico 1 4 96.5/105 620 1 4 97.75/97.75 620 1 4 85/85 620 FYIs: Complete HUD guidelines can be referenced

Conventional Jumbo seven year/one year adjustable rate mortgage 30 year term Fully amortizing

1. PRODUCT DESCRIPTION Conventional Jumbo fixed rate mortgage 15 and 30 year terms Fully amortizing Conventional Jumbo five year/one year adjustable rate mortgage 30 year term Fully amortizing Conventional

1. PRODUCT DESCRIPTION Conventional Jumbo fixed rate mortgage 15 and 30 year terms Fully amortizing Conventional Jumbo five year/one year adjustable rate mortgage 30 year term Fully amortizing Conventional

VA FIXED RATE PRODUCT

Primary Primary Primary Age of Documents Borrower Eligibility 1 to 4 Units 1 to 2 Units 1 Unit Max Loan See VA County Limits Max Loan See VA County Limits Max Loan See VA County Limits LTV CLTV Min FICO

Primary Primary Primary Age of Documents Borrower Eligibility 1 to 4 Units 1 to 2 Units 1 Unit Max Loan See VA County Limits Max Loan See VA County Limits Max Loan See VA County Limits LTV CLTV Min FICO

Appraisal requirements: No appraisal required. The original loan balance of the mortgage being refinanced is used as the appraised value.

PRODUCT: E3 CODES: PCM VA IRRRL VAS15W AND VAS30W Primary Capital Mortgage guidelines have been created to provide direction and consistency in determining a credit decision. The intention of these guidelines

PRODUCT: E3 CODES: PCM VA IRRRL VAS15W AND VAS30W Primary Capital Mortgage guidelines have been created to provide direction and consistency in determining a credit decision. The intention of these guidelines

VA Refinance Cash Out

VA Refinance Cash Out This matrix is intended as an aid to help determine whether a property/loan qualifies for certain financing. It is not intended as a replacement for VA guidelines. Users are expected

VA Refinance Cash Out This matrix is intended as an aid to help determine whether a property/loan qualifies for certain financing. It is not intended as a replacement for VA guidelines. Users are expected

Standards for Determining Monthly Debt and Income Appendix Q

Standards for Determining Monthly Debt and Income Appendix Q October 2014 2012 Genworth Financial, Inc. All rights reserved. Agenda What we will cover General Income Requirements Documentation Requirements

Standards for Determining Monthly Debt and Income Appendix Q October 2014 2012 Genworth Financial, Inc. All rights reserved. Agenda What we will cover General Income Requirements Documentation Requirements

NOTE: This matrix includes overlays, which may be more restrictive than VA requirements. A thorough reading of this matrix is recommended.

VA Refinance IRRRL This matrix is intended as an aid to help determine whether a property/loan qualifies for certain financing. It is not intended as a replacement for VA guidelines. Users are expected

VA Refinance IRRRL This matrix is intended as an aid to help determine whether a property/loan qualifies for certain financing. It is not intended as a replacement for VA guidelines. Users are expected

ditech BUSINESS LENDING VA PURCHASE PRODUCTS DELEGATED CLIENTS ONLY

1. PRODUCT DESCRIPTION VA Fixed Rate Mortgage 10 to 30 years in 5 year increments Fully amortizing Servicing retained All transactions are considered Qualified Mortgage (QM) Safe Harbor loans ditech BUSINESS

1. PRODUCT DESCRIPTION VA Fixed Rate Mortgage 10 to 30 years in 5 year increments Fully amortizing Servicing retained All transactions are considered Qualified Mortgage (QM) Safe Harbor loans ditech BUSINESS

The Chase Guaranteed Rural Housing Refinance Program Features

PROGRAM ELIGIBILITY Borrower Eligibility In order to be eligible for a Rural Development guaranteed loan, the Borrowers adjusted household income cannot exceed the maximum allowable income limit set forth

PROGRAM ELIGIBILITY Borrower Eligibility In order to be eligible for a Rural Development guaranteed loan, the Borrowers adjusted household income cannot exceed the maximum allowable income limit set forth

VA INTEREST RATE REDCUTION REFINANCE PRODUCTS VA 30 Year Fixed Jumbo Full Appraisal

Program Overview An Interest Rate Reduction Refinancing Loan (IRRRL) is a VA-guaranteed loan made to refinance an existing VA-guaranteed loan, generally at a lower interest rate than the existing VA loan,

Program Overview An Interest Rate Reduction Refinancing Loan (IRRRL) is a VA-guaranteed loan made to refinance an existing VA-guaranteed loan, generally at a lower interest rate than the existing VA loan,

Real Estate Professionals Selling to Veterans. St. Petersburg Regional Loan Center

Real Estate Professionals Selling to Veterans St. Petersburg Regional Loan Center Agenda Overview and History of VA Home Loan Program Understanding VA Home Loan Entitlement Occupancy Requirements Qualifying

Real Estate Professionals Selling to Veterans St. Petersburg Regional Loan Center Agenda Overview and History of VA Home Loan Program Understanding VA Home Loan Entitlement Occupancy Requirements Qualifying

1030HARP DU REFI PLUS (6/8/12)

") 1030HARP DU REFI PLUS (6/8/12) DESCRIPTION REQUIRED BORROWER BENEFIT DU Refi Plus is a limited cash-out refinance program that allows for expanded eligibility criteria, as well as reduced documentation

1030HARP DU REFI PLUS (6/8/12) DESCRIPTION REQUIRED BORROWER BENEFIT DU Refi Plus is a limited cash-out refinance program that allows for expanded eligibility criteria, as well as reduced documentation

6176 VA IRRRL. DW0114 Page 1 of 8

6176 VA IRRRL Interest Rate The loan must be to reduce the interest rate. If refinancing an adjustable rate mortgage (ARM) loan to a fixed rate loan, an exception is made allowing the new interest rate

6176 VA IRRRL Interest Rate The loan must be to reduce the interest rate. If refinancing an adjustable rate mortgage (ARM) loan to a fixed rate loan, an exception is made allowing the new interest rate

Borrower Fees and Charges and the VA Funding Fee

VA Pamphlet 26-7, Revised Chapter 8: Borrower Fees and Charges and the VA Funding Fee Chapter 8 Borrower Fees and Charges and the VA Funding Fee Overview Introduction This chapter contains information

VA Pamphlet 26-7, Revised Chapter 8: Borrower Fees and Charges and the VA Funding Fee Chapter 8 Borrower Fees and Charges and the VA Funding Fee Overview Introduction This chapter contains information

How To Understand The Veteran Loan Policy

Chapter 8. Borrower Fees and Charges and the VA Funding Fee Overview In this Chapter This chapter contains the following topics. Topic Topic Name See Page 1 VA Policy on Fees and Charges Paid by the Veteran-Borrower

Chapter 8. Borrower Fees and Charges and the VA Funding Fee Overview In this Chapter This chapter contains the following topics. Topic Topic Name See Page 1 VA Policy on Fees and Charges Paid by the Veteran-Borrower

VA IRRRL Offering 5/20/14

VA IRRRL Offering 5/20/14 What is an IRRRL? IRRRL stands for Interest Rate Reduction Refinance Loan An IRRRL is a VA guaranteed loan made to refinance an existing VA guaranteed loan, generally at a lower

VA IRRRL Offering 5/20/14 What is an IRRRL? IRRRL stands for Interest Rate Reduction Refinance Loan An IRRRL is a VA guaranteed loan made to refinance an existing VA guaranteed loan, generally at a lower

VA Loan Training Overviews & Updates June 3, 2015

VA Loan Training Overviews & Updates June 3, 2015 Choose one of the following audio options: TO USE YOUR COMPUTER'S AUDIO: When the webinar begins, you will be connected to audio using your computer's

VA Loan Training Overviews & Updates June 3, 2015 Choose one of the following audio options: TO USE YOUR COMPUTER'S AUDIO: When the webinar begins, you will be connected to audio using your computer's

Quick Reference Program Summary. The following is an outline of the underwriting and closing requirements of New Hampshire Housing.

Quick Reference Program Summary The following is an outline of the underwriting and closing requirements of New Hampshire Housing. Specific Program Rules are attached to this reference. A reservation cannot

Quick Reference Program Summary The following is an outline of the underwriting and closing requirements of New Hampshire Housing. Specific Program Rules are attached to this reference. A reservation cannot

FHA Guideline Changes Effective for Case Numbers Assigned On or After Sept 14, 2015

Topic Current FHA Guideline New FHA Guideline Assets Gift Funds as Reserves Manual Underwriting: Not allowed as reserves Manual underwriting: Not allowed as reserves TOTAL Scorecard: Not allowed as reserves

Topic Current FHA Guideline New FHA Guideline Assets Gift Funds as Reserves Manual Underwriting: Not allowed as reserves Manual underwriting: Not allowed as reserves TOTAL Scorecard: Not allowed as reserves

E MORTGAGE MANAGEMENT LLC 303 DU REFI PLUS

E MORTGAGE MANAGEMENT LLC 303 DU REFI PLUS PRODUCT GUIDELINES 12/8/2014 MORTGAGE ELIGIBILITY Product Description and Product Codes Code Short Description Long Description CF30RP 30 YR REFI PLUS CF30RP

E MORTGAGE MANAGEMENT LLC 303 DU REFI PLUS PRODUCT GUIDELINES 12/8/2014 MORTGAGE ELIGIBILITY Product Description and Product Codes Code Short Description Long Description CF30RP 30 YR REFI PLUS CF30RP

FHA STREAMLINE GUIDELINES

Table of Contents LTV MATRIX... 4 PROGRAM OVERVIEW... 4 APPRAISALS & AVM... 4 AVM or 2055 Exterior... 4 Streamline with an Appraisal (1004 full FHA Appraisal)... 5 ASSETS... 5 Sourcing of Deposits... 5

Table of Contents LTV MATRIX... 4 PROGRAM OVERVIEW... 4 APPRAISALS & AVM... 4 AVM or 2055 Exterior... 4 Streamline with an Appraisal (1004 full FHA Appraisal)... 5 ASSETS... 5 Sourcing of Deposits... 5

Section 2.08 - Jumbo Solution Second Mortgage

- In This Product Description This product description contains the following topics: Overview... 2 Related Bulletins... 3 Loan Terms... 4 Assumptions... 4 Eligible First and Second Mortgage Products...

- In This Product Description This product description contains the following topics: Overview... 2 Related Bulletins... 3 Loan Terms... 4 Assumptions... 4 Eligible First and Second Mortgage Products...

MSHDA's Down Payment Assistance and Mortgage Credit Certificate. May 21, 2010 (3:30 5:00 p.m.) Facilitated by: Carol Brito (MSHDA) Sponsored by:

Facilitated by: Carol Brito (MSHDA) Sponsored by:") MSHDA's Down Payment Assistance and Mortgage Credit Certificate May 21, 2010 (3:30 5:00 p.m.) Facilitated by: Carol Brito (MSHDA) Sponsored by: CREDIT UNIONS A DRIVING FORCE OF COMMUNITIES MSHDA Overview

MSHDA's Down Payment Assistance and Mortgage Credit Certificate May 21, 2010 (3:30 5:00 p.m.) Facilitated by: Carol Brito (MSHDA) Sponsored by: CREDIT UNIONS A DRIVING FORCE OF COMMUNITIES MSHDA Overview

EFFECTIVE FOR FHA CASE NUMBER ASSIGNMENTS ON AND AFTER SEPTEMBER 14, 2015 OVERLAY MATRIX: GOVERNMENT

Appraisals Attached PUDs Automated Findings Condominiums Credit History VA: Form 2055 Appraisal dated prior to the Note Date required on IRRRLs if current VA loan is not serviced by BB&T. FHA: Property

Appraisals Attached PUDs Automated Findings Condominiums Credit History VA: Form 2055 Appraisal dated prior to the Note Date required on IRRRLs if current VA loan is not serviced by BB&T. FHA: Property

FHA Changes 4000.1 Effective With Case Numbers assigned on or after 9/14/15. Skyline / New Leaf

FHA Changes 4000.1 Effective With Case Numbers assigned on or after 9/14/15 Skyline / New Leaf Manual downgrade regardless of a Total Scorecard Approval When the date of the Borrower s bankruptcy discharge

FHA Changes 4000.1 Effective With Case Numbers assigned on or after 9/14/15 Skyline / New Leaf Manual downgrade regardless of a Total Scorecard Approval When the date of the Borrower s bankruptcy discharge

VA and VA IRRRL Programs

VA and VA IRRRL Programs 12/12/14 VA Program Benefits VA loan programs offer exceptional financing options for active duty military personnel, veterans and their families. 100% financing on purchase and

VA and VA IRRRL Programs 12/12/14 VA Program Benefits VA loan programs offer exceptional financing options for active duty military personnel, veterans and their families. 100% financing on purchase and

GETTING STARTED WITH Southern Home Loans A Division of Goldwater Bank NMLS# 452955

2016 GETTING STARTED WITH Southern Home Loans A Division of Goldwater Bank NMLS# 452955 YOUR PLAY-BY-PLAY GUIDE TO RESPONSIBLE NON-PRIME LENDING Highlights No Seasoning on Foreclosure, BK or Short Sale

2016 GETTING STARTED WITH Southern Home Loans A Division of Goldwater Bank NMLS# 452955 YOUR PLAY-BY-PLAY GUIDE TO RESPONSIBLE NON-PRIME LENDING Highlights No Seasoning on Foreclosure, BK or Short Sale

Loan Product Guide (Matrix)

") Loan Product Guide (Matrix) 1 FHA Page 2 FNMA 3 USDA 4 VA 1.1 Streamline...2 1.2 Purchase 203 (B)...3 1.3 Refinance 203 (B)...4 2.1 Purchase...5 2.2 Refinance...6 3.1 Purchase...7 3.2 Refinance/Streamline...8

Loan Product Guide (Matrix) 1 FHA Page 2 FNMA 3 USDA 4 VA 1.1 Streamline...2 1.2 Purchase 203 (B)...3 1.3 Refinance 203 (B)...4 2.1 Purchase...5 2.2 Refinance...6 3.1 Purchase...7 3.2 Refinance/Streamline...8

Program Matrix for VA IRRRL Black Programs:

Program Matrix for VA IRRRL Black Programs: Primary Residence 1 to 4 Unit, Condo, PUD none** 600 Second Home* 1 Unit, Condo, PUD none** 600 Investment Property* 1 to 4 Unit, Condo, PUD none** 600 * For

Program Matrix for VA IRRRL Black Programs: Primary Residence 1 to 4 Unit, Condo, PUD none** 600 Second Home* 1 Unit, Condo, PUD none** 600 Investment Property* 1 to 4 Unit, Condo, PUD none** 600 * For

Federal Housing Administration [FHA] and Veterans Administration [VA] Loan Programs A. LOAN PROGRAMS OF THE FEDERAL HOUSING ADMINISTRATION (FHA)

![Federal Housing Administration [FHA] and Veterans Administration [VA] Loan Programs A. LOAN PROGRAMS OF THE FEDERAL HOUSING ADMINISTRATION (FHA)](/thumbs/25/5268134.jpg "Federal Housing Administration [FHA] and Veterans Administration [VA] Loan Programs A. LOAN PROGRAMS OF THE FEDERAL HOUSING ADMINISTRATION (FHA)") Chapter 42 Federal Housing Administration [FHA] and Veterans Administration [VA] Loan Programs A. LOAN PROGRAMS OF THE FEDERAL HOUSING ADMINISTRATION (FHA) INTRODUCTION Besides conventional loans discussed

Chapter 42 Federal Housing Administration [FHA] and Veterans Administration [VA] Loan Programs A. LOAN PROGRAMS OF THE FEDERAL HOUSING ADMINISTRATION (FHA) INTRODUCTION Besides conventional loans discussed

FMC Product and Credit Guidance for Wholesale Divisions

FMC Product and Credit Guidance for Divisions Ineligible Product Programs and Properties FMC does not accept Loan Prospector AUS for Conventional, FHA or VA loans The Negative Equity FHA (MHA) loan program

FMC Product and Credit Guidance for Divisions Ineligible Product Programs and Properties FMC does not accept Loan Prospector AUS for Conventional, FHA or VA loans The Negative Equity FHA (MHA) loan program

FHA HIGH BALANCE FIXED PROGRAM HIGHLIGHTS

Product Summary These guidelines represent underwriting requirements for FHA fixed rate and ARM mortgages with increased loan size limits with a minimum floor of greater than $417,000. These guidelines

Product Summary These guidelines represent underwriting requirements for FHA fixed rate and ARM mortgages with increased loan size limits with a minimum floor of greater than $417,000. These guidelines

What s s New With FHA?

What s s New With FHA? Presented By: Bill Ladewig 866.204.9733 http://www.mortgage- FHA Calculator Calculates everything needed to quote or qualify FHA loans Click to Open: http://www.themtgmentor.com/fha_mortgage_calculator.html

What s s New With FHA? Presented By: Bill Ladewig 866.204.9733 http://www.mortgage- FHA Calculator Calculates everything needed to quote or qualify FHA loans Click to Open: http://www.themtgmentor.com/fha_mortgage_calculator.html

Dr. Debra Sherrill Central Piedmont Community College

Dr. Debra Sherrill Central Piedmont Community College 1 2 Describe the benefits and pitfalls of renting versus owning a home. List the steps required to obtain a mortgage loan. Identify mortgage options

Dr. Debra Sherrill Central Piedmont Community College 1 2 Describe the benefits and pitfalls of renting versus owning a home. List the steps required to obtain a mortgage loan. Identify mortgage options

COMPENSATING FACTORS FOR FHA

COMPENSATING FACTORS FOR FHA Key Points Credit Only allowed for Case numbers assigned on or after 4/1/13 for borrowers with FICO s at 620 or less with Debt to Income (DTI ) ratios above 43%. Even if broker

COMPENSATING FACTORS FOR FHA Key Points Credit Only allowed for Case numbers assigned on or after 4/1/13 for borrowers with FICO s at 620 or less with Debt to Income (DTI ) ratios above 43%. Even if broker

AMX / Land Home Financial Services Wholesale Lending Division

SECTION: 1 PAGE: 1 of 13 VA MORTGAGE LIMITS FOR ALL AREAS: http://www.benefits.va.gov/homeloans/purchaseco_loan_limits.asp Regardless of loan amount, the VA guaranty plus cash/equity must be equal to at

SECTION: 1 PAGE: 1 of 13 VA MORTGAGE LIMITS FOR ALL AREAS: http://www.benefits.va.gov/homeloans/purchaseco_loan_limits.asp Regardless of loan amount, the VA guaranty plus cash/equity must be equal to at

VA Home Loan Program. Wholesale Lending

VA Home Loan Program Wholesale Lending November, 2009 The VA Loan Guaranty program is a benefit Throughout the history of our country, it has been a priority of the government and the citizens to support

VA Home Loan Program Wholesale Lending November, 2009 The VA Loan Guaranty program is a benefit Throughout the history of our country, it has been a priority of the government and the citizens to support

VA Borrower Fees and Charges

VA Borrower Fees and OVERVIEW Purpose The VA home loan program involves a veteran s benefit. VA policy has evolved around the objective of helping the veteran to use his/her home loan benefit. Therefore,

VA Borrower Fees and OVERVIEW Purpose The VA home loan program involves a veteran s benefit. VA policy has evolved around the objective of helping the veteran to use his/her home loan benefit. Therefore,

The City of MIDWEST CITY GRANTS MANAGEMENT DEPARTMENT Terri L. Craft, Grants Manager. MIDWEST CITY Homebuyer Assistance Program

The City of MIDWEST CITY GRANTS MANAGEMENT DEPARTMENT Terri L. Craft, Grants Manager Grant Amount: $5,000.00 MIDWEST CITY Homebuyer Assistance Program The Homebuyer Assistance Program promotes homeownership

The City of MIDWEST CITY GRANTS MANAGEMENT DEPARTMENT Terri L. Craft, Grants Manager Grant Amount: $5,000.00 MIDWEST CITY Homebuyer Assistance Program The Homebuyer Assistance Program promotes homeownership

Single Family Housing Guaranteed Loan Program Underwriting and Loan Closing Documentation Matrix

Single Family Housing Guaranteed Loan Program Underwriting and Loan Closing Matrix Origination Matrix (January 2013) Table of Contents Matrix Origination... 1 Underwriting... 1 Credit... 7 Employment/Income...

Single Family Housing Guaranteed Loan Program Underwriting and Loan Closing Matrix Origination Matrix (January 2013) Table of Contents Matrix Origination... 1 Underwriting... 1 Credit... 7 Employment/Income...

PRODUCT GUIDELINES CONVENTIONAL NON-CONFORMING FIXED 15-20-30 YEAR HEF

Several states and local municipalities have enacted legislation that define High Cost loans based on APR and fee thresholds which may or may not relate to the HOEPA thresholds. These types of loans typically

Several states and local municipalities have enacted legislation that define High Cost loans based on APR and fee thresholds which may or may not relate to the HOEPA thresholds. These types of loans typically

Financing Residential Real Estate. Lesson 12: VA-Guaranteed Loans

Financing Residential Real Estate Lesson 12: VA-Guaranteed Loans Introduction In this lesson we will cover: characteristics of VA loans, eligibility requirements, VA guaranty, VA loan amounts, and underwriting

Financing Residential Real Estate Lesson 12: VA-Guaranteed Loans Introduction In this lesson we will cover: characteristics of VA loans, eligibility requirements, VA guaranty, VA loan amounts, and underwriting

Understand the VA Loan Program. Serve the mortgage lending needs of borrowers who serve our country

Understand the VA Loan Program Serve the mortgage lending needs of borrowers who serve our country Eligible Borrowers A veteran is eligible for VA home loan benefits if he or she served in the Army, Navy,

Understand the VA Loan Program Serve the mortgage lending needs of borrowers who serve our country Eligible Borrowers A veteran is eligible for VA home loan benefits if he or she served in the Army, Navy,

Program Type Occupancy Units LTV/CLTV * Purchase Owner-occupied 1-4 100%

Maximum DTI: 41% Maximum Loan Amount: 1-unit $417,000 2-units $533,850 DU Approve/ 3-units $645,300 4-units $801,850 Minimum Loan Amount: $75,000 Maximums LTVs Purchase 100% LTV Rate/term & Cash-out 90%

Maximum DTI: 41% Maximum Loan Amount: 1-unit $417,000 2-units $533,850 DU Approve/ 3-units $645,300 4-units $801,850 Minimum Loan Amount: $75,000 Maximums LTVs Purchase 100% LTV Rate/term & Cash-out 90%

How To Get An Fha Loan

FHA Financing - All You Need to Know 2 Hour Continuing Education Course Presentation by: Ashley Brint Patrick Axford Date: August 22, 2012 2012 Regions Bank. Member FDIC. Regions is a registered service

FHA Financing - All You Need to Know 2 Hour Continuing Education Course Presentation by: Ashley Brint Patrick Axford Date: August 22, 2012 2012 Regions Bank. Member FDIC. Regions is a registered service

Conventional Fixed Rate Conforming Product Guidelines

Loan Parameters Loan Purpose Allowed Minimum Credit Score Maximum LTV/CLTV Owner Occupied & Second Home Maximum LTV/CLTV Non-Owner Occupants Max. Loan Amount Subordinate Financing Maximum Ratios Max. No.

Loan Parameters Loan Purpose Allowed Minimum Credit Score Maximum LTV/CLTV Owner Occupied & Second Home Maximum LTV/CLTV Non-Owner Occupants Max. Loan Amount Subordinate Financing Maximum Ratios Max. No.

File Retention Brokered and Mini Correspondent Loans

Berkshire Lending, LLC File Retention Brokered and Mini Correspondent Loans Your Branch Office must be in compliance for HUD audits and state license examinations. Audits are fairly routine and simple

Berkshire Lending, LLC File Retention Brokered and Mini Correspondent Loans Your Branch Office must be in compliance for HUD audits and state license examinations. Audits are fairly routine and simple

E MORTGAGE MANAGEMENT, LLC 703 VA HIGH BALANCE PRODUCT GUIDELINES

E MORTGAGE MANAGEMENT, LLC 703 VA HIGH BALANCE PRODUCT GUIDELINES 4/30/2014 Mortgage Eligibility Product Code Short Description Long Description Description VF30HB 30 YR VA HB VF30HB - 30 YR VA HIGH BALANCE

E MORTGAGE MANAGEMENT, LLC 703 VA HIGH BALANCE PRODUCT GUIDELINES 4/30/2014 Mortgage Eligibility Product Code Short Description Long Description Description VF30HB 30 YR VA HB VF30HB - 30 YR VA HIGH BALANCE

Housing Trust Silicon Valley ( HTSV ) Mortgage Assistance Program (MAP)

Mortgage Assistance Program (MAP)") Housing Trust Silicon Valley ( HTSV ) Mortgage Assistance Program (MAP) Program Description: Housing Trust Silicon Valley s Mortgage Assistance Program (MAP) is an amortizing second loan that is now available

Housing Trust Silicon Valley ( HTSV ) Mortgage Assistance Program (MAP) Program Description: Housing Trust Silicon Valley s Mortgage Assistance Program (MAP) is an amortizing second loan that is now available

DU User s Guide for VA Loans

DU User s Guide for VA Loans 1999 2008 Fannie Mae. All rights reserved. Desktop Originator, DO, Desktop Underwriter, and DU, are registered trademarks of Fannie Mae. pmiaura is a service mark of PMI Mortgage

DU User s Guide for VA Loans 1999 2008 Fannie Mae. All rights reserved. Desktop Originator, DO, Desktop Underwriter, and DU, are registered trademarks of Fannie Mae. pmiaura is a service mark of PMI Mortgage

The SAPPHIRE. Program Training. Offered through FIRST MORTGAGE CORPORATION

The SAPPHIRE Program Training Offered through FIRST MORTGAGE CORPORATION Desktop Underwriter is a registered trademark of Fannie Mae. Loan Prospector is a registered trademark of Freddie Mac. This presentation

The SAPPHIRE Program Training Offered through FIRST MORTGAGE CORPORATION Desktop Underwriter is a registered trademark of Fannie Mae. Loan Prospector is a registered trademark of Freddie Mac. This presentation

SONYMA FHA Plus Correspondent Term Sheet

Product Type 30 Year Fixed Rate Mortgages Sales Focus This program provides the flexibility offered by FHA s 203(b) or 234(c) mortgages along with SONYMA s Down Payment Assistance Loan (DPAL). HUD Mortgagee

Product Type 30 Year Fixed Rate Mortgages Sales Focus This program provides the flexibility offered by FHA s 203(b) or 234(c) mortgages along with SONYMA s Down Payment Assistance Loan (DPAL). HUD Mortgagee

Revolving Debt & Other Agency Guideline Revisions Note: SunTrust specific overlays are underlined.

Assets Section 2.04 DU Refi Plus Loan Program DU Refi Plus STM to STM Transactions Asset Documentation Requirements Assets must be documented in accordance with DU Refi Plus eligible DU Findings report.

Assets Section 2.04 DU Refi Plus Loan Program DU Refi Plus STM to STM Transactions Asset Documentation Requirements Assets must be documented in accordance with DU Refi Plus eligible DU Findings report.

Credit. 3.3-A General Requirements_. 3.3-B Credit Analysis. Section 3.3: Credit

Credit 3.3-A General Requirements_ Obtain at least one, preferably two or three, credit scores for each borrower; all available scores must be obtained. The scores must be obtained from all major repositories

Credit 3.3-A General Requirements_ Obtain at least one, preferably two or three, credit scores for each borrower; all available scores must be obtained. The scores must be obtained from all major repositories