Regulatory reform banks and broker-dealers. Simon Morris, Ash Saluja, Paul Edmondson and Jean Price Mitre House 11 th November

|

|

|

- Blaise Alban Lamb

- 8 years ago

- Views:

Transcription

1

2 Regulatory reform banks and broker-dealers Simon Morris, Ash Saluja, Paul Edmondson and Jean Price Mitre House 11 th November

3 Outline Tougher supervision and enforcement (Simon) The new regulatory order the new authorities, their roles and macro-prudential regulation (Ash) Prudential regulation systemically significant firms and living wills, financial regulation update, risk management and governance (Paul) CoB -Tougher consumer protection mortgage market reform, cards and consumer finance (Jean)

CoB -Tougher consumer protection mortgage market reform, cards and")

4 Intrusive supervision and tough enforcement - banks and brokerdealers Simon Morris Partner CMS Cameron McKenna LLP

5 The new supervisory regime Intensive supervision/regulation More intrusive, challenging and systemic Increase in front line supervision Increase in specialist resources Shift in style and focus proactive rather reactive Expect challenge in new areas, previously out of FSA scope Competence of senior management and NEDs Accounting decisions Business model sustainability and strategy Products Firm failure and systemic/fscs impacts

6 And also More frequent meetings More frequent MI Closer engagement on projects Pushing the high-impact/non-relationship managed perimeter More interviews - when Approval ( Dear CEO on SIF approval process 172 interviews so far) ARROW All the time Probing Your competence, understanding and judgements Grasp of lessons from reverse stress tests

7 Five key messages to convey 1. I know my role 2. I know the strategy 3. I know the risks 4. I understand our governance 5. I understand the new order

8 The new enforcement regime Credible deterrence More high profile criminal action Fines (recent FSA consultation) More intelligent approach Higher (by a factor of 300% or more) 50/100 million possible? Conservatives say FSA enforcement has been very weak? new prosecutor to replace SFO BUT THE KEY POINT IS..

9 New emphasis on enforcement and fines against individuals personally An investigation will now normally include relevant individuals Chairman Chief executive More investigation and enforcement against senior management and NEDs personally even where not involved in front line breach and acted honestly FSA now making judgements on managements judgements

10 The new regulatory order for banks and broker-dealers Ash Saluja Partner, CMS Cameron McKenna LLP

11 The new order the different roles and objectives Macro-prudential (new/missing role) Regulating the system as whole In support of financial stability Firm regulation (micro-prudential) and supervision Covering individual firm requirements But also includes implementation of systemic requirements, so all gets mixed up

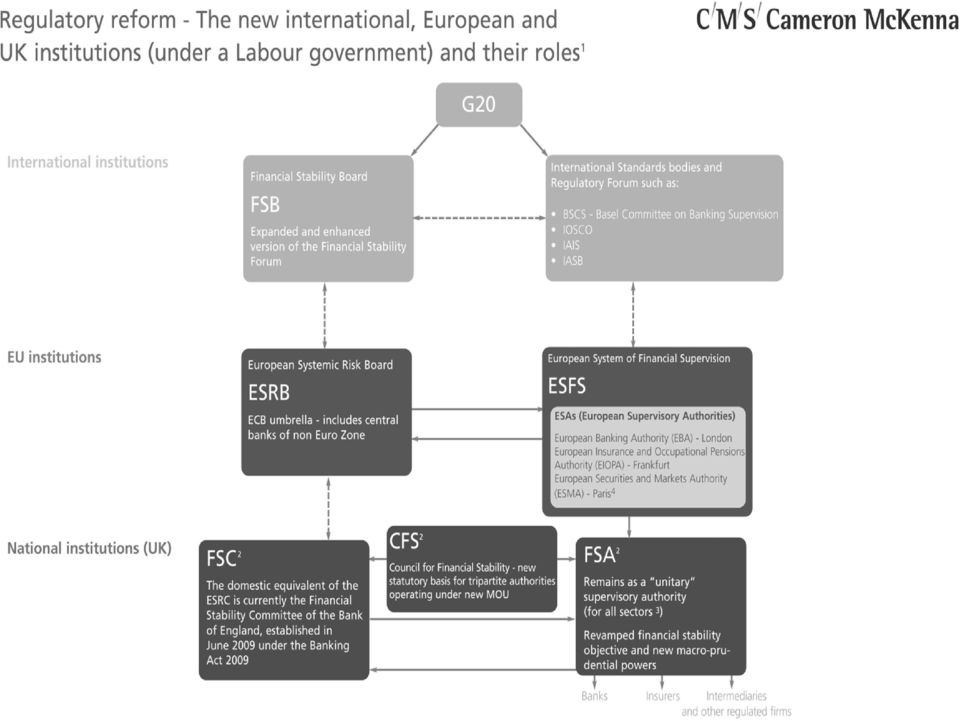

12 The new order the authorities developing the rules International European National

13

14 Regulation at the international level International - G20 lead (High level) policy driven Bank of International Settlements (BIS) hosted Financial Stability Board (FSB) beefed up and expanded 3 standing committees Basel Accords/Committee on Bank Supervision (BCBS) thinking again about its Basel II regime International Association of Deposit Insurers IMF, IOSCO, IASB etc

15 Regulation at the EU level the policy agenda EU regulatory regime needs to be More joined up (groups and home/host) More systemic, More consistent technical standards and supervision Enforced (getting tough with the national supervisors) European Systemic Risk Board - talking shop for central bankers?

European Systemic Risk Board - talking shop for")

16 European System of Financial Supervision (ESFS) Supervision to remain with domestic authorities European Banking Authority (EBA) and European Securities and Markets Authority (ESMA) but still a forum of regulators (acting by qualified/simple majority) More powerful authority to Set detailed technical standards ( e.g. conditions to permit IRB approach) Ensure common supervisory standards Promote colleges and resolve disputes between home/host/group supervisors (tie-breaker powers and appeals controversial in UK)

Ensure common supervisory standards Promote colleges and resolve disputes between")

17 Domestic reform - Labour Financial Services and Business Bill a rag bag following HMT white paper and BIS/BERR consumer consultations Keep FSA as combined financial/prudential and Conduct of Business regulator for all sectors Keep existing tripartite (BoE, FSA and HMT) Macro-prudential role (e.g. systemic issues and living wills) FSA Lobbying internationally Moving ahead of and beyond international consensus in some areas - bank liquidity, living wills and remuneration Big issues debated (yet again) in FS 09/3 and DP 09/4

FSA Lobbying internationally Moving ahead of and beyond international consensus in some areas -")

18 Domestic reform - the Conservatives Scrap FSA, the single regulator model and the tripartite system Bank of England Gets the entire macro-prudential role And main role in financial regulation of firms banks and broker-dealers New Consumer Protection Agency (CPA) takes on Conduct of Business/consumer protection Lots of issues being considered continental style Markets and Securities Authority (UKLA and market conduct -?plus Takeover Panel and Financial Reporting Council?)?RIE and MTF supervision?

?")

19

20 The new macro-prudential order key drivers Systemic impacts (e.g. of Lehmans collapse, money market fund withdrawals or a central counterparty failure) Rescue costs to save the system (e.g. Citi) Exposures and risks for The broader system e.g. Consumer confidence (Northern Rock, B&B) Wholesale markets (AIG) Real economy (RBS) Taxpayer (all of the above) Indirect exposures via deposit guarantee and FSCS

Exposures and risks for The broader system e.g.")

21 The new macro-prudential order options Still early days but lots to ponder Various international work underway Everyone has a view! Watch BoE dynamic stability and flexible risk weightings Tobin tax and macro-economic levers taking the punch bowl away The plumbing and wiring market infrastructure Regulating systemically significant firms Resolution and recovery

22 The new macro-prudential order protecting retail deposits Hard structural restrictions for retail banks Conservatives are keen but depends on international consensus? Or equivalent result by capital penalties Glass-Steagall indirectly? Lord Turner s preferred approach? The demise of the universal bank model and the funding of wholesale business with retail deposits? Barclays retail bank split announced last week?

23 Market infrastructure reform policy International G20 summits (April/September 2009) Standardized OTC derivative contracts to be traded on exchange or e-platform (organised trading venues) and cleared through Central Counterparty (CCP) by end 2012 European Commission consultation (July-October 2009) Increase standardization for OTC derivatives Use central data repository Strengthen use of CCPs Increase use of organised trading venues International (especially US)/European approach to be co-ordinated before proposals become concrete at National level

24 Market infrastructure reform implications Scope unclear but most standardised OTC derivatives to avoid regulatory arbitrage Reduction of risk CCP prevents domino effect of counterparty collapse through multilateral (rather than bilateral) netting CCP requires margin (initial and variation) and takes guarantee funds from clearing members CCPs (implicitly) will not be allowed to fail Exceptions non-standard OTC derivatives, may be cleared bilaterally but potentially subject to Increased margin requirements (initial and variation) Higher capital charges and greater transparency on positions for regulated firms

25 Regulating groups and cross border businesses Bringing unauthorised holding companies into direct regulation Intra-group relationships work Groups level regulation versus local survivability Higher capital for group level or A constellation of local ring fenced banks EU passport UK still wants more host state powers Better cross-border supervision - colleges of supervisors EU and international (G20 says 30 now in operation) and the ESFS

26 Winding down banks and broker-dealers paying for resolution International work on deposit insurance/ collective and individual resolution funds Revised EU deposit guarantee legislation Should there be one EU wide scheme? Move to pre-funded schemes Avoid post-event levy with interim government funding With risk based premium (BoE view) Avoid cross subsidisation

27 Reforming the prudential regulation of banks and brokerdealers Paul Edmondson Partner CMS Cameron McKenna LLP

28 Macro-prudential impacts Regulating systemically significant banks and broker-dealers - Authorities must ensure that groups providing economically critical functions are capable of being supervised and resolved Banks should not be too big or complex Simpler, more transparent legal structures that are capable of being supervised and resolved

29 Defining systemically significant firms A few (based on impact of failure in good times) or Lots (based on impact of failure in bad times eg all Irish banks or a herd ) What criteria? Size? Infrastructure providers Or a graduated response? regulatory standards calibrated to firms contribution to systemic risk Even small deposit takers being treated as systemically significant First international work delivered to G20 St Andrews meeting DP09/4 also considers

30 Principles emerging for banks and broker-dealers.firms must Be capable of being supervised effectively Understand what would cause them to fail have reduced that risk by reverse engineering Have resources available for recovery (as a going concern) But also be capable of resolution (a gone concern winddown) without tax payer support Unacceptable consequences for the system or consumers And have detailed systems in operation to ensure this

31 In light of their Legal and corporate structure Intra-group relationships Current FSA/international thematic Size, international structure and complexity etc Business mix Recovery facilities available Resolution insurance coverage (currently only limited FSCS capacity)

32 Living wills FSA s requirements for recovery and resolution plans Recovery as a going concern (plan 1) Eg contingent capital/liquidity De-risk and contagion control plan Resolution/wind down (plan 2) Detailed plan for use of different SRR tools Demonstrate ability to unplug from the system without systemic impact protect consumers from available resolution insurance Produce data

33 Living wills - scope FSA intends to apply to All UK banks and building societies And other systemically important firms (insurers and broker-dealers etc) FSB/international Top 25 banks and broker-dealers Already working on plans International dimension different perspectives at group level and home/host state

34 Preparing for the new order and living wills do you have? An intelligible and reliable mapping of Group corporate structure legal entity and regulatory status (FSA worried directors do not understand) Contractual, operational and branding overlay Intra-group relationships finance, security, guarantees, collateral, cross default, capital/liquidity/cash management Structured relationships (tax or capital driven) Group Treasury arrangements Client asset and stock lending Analysis of how this legal structure plays out under stress (for plan 1) and SRR/failure/insolvency (for plan 2).

35 Living wills potential impact on firms Huge cost in Set up Maintaining plans/data/contingency arrangements (for ever) Provides FSA with over-arching mechanism to deal with many of the themes from financial crisis reform? Not just areas where detailed requirements are being imposed (such as reverse stress testing and single customer view) Huge power to FSA to unpick, restructure and restrain your business? Plans must be negotiated with regulator Reverse engineering/stress testing Onus on firm - not FSA or its rules Fate hangs on subjective value judgements by FSA

36 Financial regulation of banks and brokerdealers Detail and timing of reforms in the RegZone Complex mix of international/basel and EU legislation Quick fixes (wave 1) and fundamental reform (wave 2) Liquidity Capital Higher requirements Common equity Internal models Higher for systemically important banks and brokerdealers (macro-prudential add-ons) Accounting

37 Walker and governance Big bank focus but extended to BAOFI including broker-dealers but muddled on read-across Draft proposals focus on developing the Combined Code for listed companies Comply or explain may not be enough for HMG/FSA Non-listed groups outside scope? FSA to respond/consult on its rules Remuneration and shareholder engagement debate

38 Walker on risk for banks and brokerdealers Separate board risk committee NED chair NED majority Independent enterprise risk management function Independent Chief Risk Officer Risk report

39 Non-executives at banks and brokerdealers FSA New APER guidance on NED role Original ideas more radical than Walker? Walker proposes.

40 Non-executives at banks and brokerdealers the Walker consultation No liability cap (Walker considered a cap) More time but not full time (non-exec chairman at least 2/3rds of his time) Better understanding of business model, risks and legal structure More challenge of executives and more independent but not dual level boards More training and expertise/qualifications More support/resources for independent role Greater overall responsibility for risk management and remuneration

41 Remuneration - update More internal/external transparency - Walker recommends public disclosure of high end non-board remuneration (above board median) Even FSA admit remuneration is not the cause or cure but huge political focus FSA s new Remuneration rule and code currently only applies to 26 banks and broker-dealers FSA to announce decision on broader application And review next year FSA and Conservatives against direct regulation of quantum

42 Tougher consumer protection banks and broker-dealers in retail markets Jean Price Head of retail banking CMS Cameron McKenna LLP

43 Current issues - FSA Retail Investments Retail Distribution Review Banking: Conduct of Business Payment Services Regulations Mortgage Market Review

44 Current Issues other OFT Consultation Guidance on Irresponsible Lending Consumer Credit Directive Consultation of Store and Credit Cards The Lending Code

45 What are the current targets? Mortgages Credit and store cards Secured and unsecured lending

46 What are the key themes? Suitability Affordability ability of borrower to repay Customers in financial difficulty Arrears handling

47 How are the regulators intending to protect consumers? Transparency Better qualified and more accountable advisers Banning products Greater responsibility on lenders More rules Increased scope for FSA Wider Implications More enforcement action Class actions as another route to redress

48 Current consultations Mortgage Market Review - Discussion paper closes 20 January 2010 Review of Regulations of Credit and Store Cards: Consultation closes 19 January 2010

49 What else is on the horizon? OFT Possible removal as key regulator for certain products Conservatives will move to new CPA Europe Integration of EU Mortgage Credit Markets Responsible lending and borrowing PRIPS Single Euro Payments Area

50 How we can help Living wills legal and regulatory input Scoping the legal mapping All areas Governance and systems benchmarking Training Board briefing Strategic impacts Lobbying And

51

52 Regulatory change - keeping track of What is proposed by international forum, EU, labour government, the Conservatives, FSA, BoE etc etc Stream of publications 100s of pages a day, mostly with heavy political spin/twist Difficult to gauge what the readacross/impact/timing will be for the insurance market Only bite sized chunks today but all the detail is in the RegZone..

53 RegZone and the roadmap On-line free to view without passwords! Up to date Roadmap report 40 areas of regulatory change Overview, status/timing and impact More detailed chronology with hyperlinks Charts and visuals Other tools by topic ( Handling a regulatory crisis tool), by type of publication (Articles and press quotes), by sector (insurance specific section coming soon )

54

55

56

57

58

59

60

61

62

Living wills the new regulatory regime for financial institutions

Living wills the new regulatory regime for financial institutions FAQs about the new requirements - - To manage for the firm s own failure, for example, through the preparation and operation of Recovery

Living wills the new regulatory regime for financial institutions FAQs about the new requirements - - To manage for the firm s own failure, for example, through the preparation and operation of Recovery

OTC derivatives reforming EU market structures. Ash Saluja, Partner CMS Cameron McKenna LLP

OTC derivatives reforming EU market structures Ash Saluja, Partner CMS Cameron McKenna LLP The OTC derivatives market - a brief reminder. Scope $605 trillion notional amount / $25 trillion gross market

OTC derivatives reforming EU market structures Ash Saluja, Partner CMS Cameron McKenna LLP The OTC derivatives market - a brief reminder. Scope $605 trillion notional amount / $25 trillion gross market

FSA: Regulatory Reform.

FSA: Regulatory Reform. FSA: Regulatory Reform Introduction Largely as a result of the FSA s failing performance during the financial crisis in 2008, it was announced in June 2010 that the FSA would be

FSA: Regulatory Reform. FSA: Regulatory Reform Introduction Largely as a result of the FSA s failing performance during the financial crisis in 2008, it was announced in June 2010 that the FSA would be

Reducing the moral hazard posed by systemically important financial institutions. FSB Recommendations and Time Lines

Reducing the moral hazard posed by systemically important financial institutions FSB Recommendations and Time Lines 20 October 2010 Table of Contents I. Overall policy framework to reduce moral hazard

Reducing the moral hazard posed by systemically important financial institutions FSB Recommendations and Time Lines 20 October 2010 Table of Contents I. Overall policy framework to reduce moral hazard

DECLARATION ON STRENGTHENING THE FINANCIAL SYSTEM LONDON SUMMIT, 2 APRIL 2009

DECLARATION ON STRENGTHENING THE FINANCIAL SYSTEM LONDON SUMMIT, 2 APRIL 2009 We, the Leaders of the G20, have taken, and will continue to take, action to strengthen regulation and supervision in line

DECLARATION ON STRENGTHENING THE FINANCIAL SYSTEM LONDON SUMMIT, 2 APRIL 2009 We, the Leaders of the G20, have taken, and will continue to take, action to strengthen regulation and supervision in line

Implementing OTC Derivatives Market Reforms

Implementing OTC Derivatives Market Reforms 25 October 2010 Foreword In September 2009, G-20 Leaders agreed in Pittsburgh that: All standardised OTC derivative contracts should be traded on exchanges

Implementing OTC Derivatives Market Reforms 25 October 2010 Foreword In September 2009, G-20 Leaders agreed in Pittsburgh that: All standardised OTC derivative contracts should be traded on exchanges

Memorandum of Understanding between the Financial Conduct Authority and the Bank of England, including the Prudential Regulation Authority

Memorandum of Understanding between the Financial Conduct Authority and the Bank of England, including the Prudential Regulation Authority Purpose and scope 1. This Memorandum of Understanding (MoU) sets

Memorandum of Understanding between the Financial Conduct Authority and the Bank of England, including the Prudential Regulation Authority Purpose and scope 1. This Memorandum of Understanding (MoU) sets

EBA Work Programme 2015

30 September 2014 EBA Work Programme 2015 1. In accordance with Regulation (EU) No 1093/2010 1 of the European Parliament and of the Council of 24 November 2010 establishing the European Banking Authority

30 September 2014 EBA Work Programme 2015 1. In accordance with Regulation (EU) No 1093/2010 1 of the European Parliament and of the Council of 24 November 2010 establishing the European Banking Authority

How do we get banks to better serve the real economy: ethics, incentives, and the role of supervisors

How do we get banks to better serve the real economy: ethics, incentives, and the role of supervisors Washington, June 3, 2015 1. The financial crisis highlighted severe weaknesses and excesses in the

How do we get banks to better serve the real economy: ethics, incentives, and the role of supervisors Washington, June 3, 2015 1. The financial crisis highlighted severe weaknesses and excesses in the

Settlement Agreement between the Central Bank of Ireland (the Central Bank ) and Irish Nationwide Building Society ( INBS )

and Irish Nationwide Building Society ( INBS )") Settlement Agreement between the Central Bank of Ireland (the Central Bank ) and Irish Nationwide Building Society ( INBS ) Following Central Bank Investigation INBS admits widespread breaches INBS has

Settlement Agreement between the Central Bank of Ireland (the Central Bank ) and Irish Nationwide Building Society ( INBS ) Following Central Bank Investigation INBS admits widespread breaches INBS has

September 2014. The CSD Regulation A guide for clients

September 2014 The CSD Regulation A guide for clients 1 Contents Introduction 3 About this guide 3 Background 3 Provisions for securities settlement (Title II) 4 Provision of banking-type ancillary services

September 2014 The CSD Regulation A guide for clients 1 Contents Introduction 3 About this guide 3 Background 3 Provisions for securities settlement (Title II) 4 Provision of banking-type ancillary services

Operational continuity in recovery and resolution planning Exploring the Service Company structure

Operational continuity in recovery and resolution planning Exploring the Service Company structure Contents The requirement for operational continuity 1 in recovery and resolution planning Operational

Operational continuity in recovery and resolution planning Exploring the Service Company structure Contents The requirement for operational continuity 1 in recovery and resolution planning Operational

OTC Derivatives Market Reforms - Focusing on International Discussion-

OTC Derivatives Market Reforms - Focusing on International Discussion- June 12, 2015 Shunsuke Shirakawa Financial Services Agency Government of Japan * This presentation represents the presenter s own

OTC Derivatives Market Reforms - Focusing on International Discussion- June 12, 2015 Shunsuke Shirakawa Financial Services Agency Government of Japan * This presentation represents the presenter s own

Net Stable Funding Ratio

Net Stable Funding Ratio Aims to establish a minimum acceptable amount of stable funding based on the liquidity characteristics of an institution s assets and activities over a one year horizon. The amount

Net Stable Funding Ratio Aims to establish a minimum acceptable amount of stable funding based on the liquidity characteristics of an institution s assets and activities over a one year horizon. The amount

Deutsche Bank UK Banks Conference 07 April 2011 Chris Lucas, Group Finance Director

Deutsche Bank UK Banks Conference 07 April 2011 Chris Lucas, Group Finance Director Slide: Name Slide Thanks very much, it s a great pleasure to be here today and I d like to thank our hosts Deutsche Bank

Deutsche Bank UK Banks Conference 07 April 2011 Chris Lucas, Group Finance Director Slide: Name Slide Thanks very much, it s a great pleasure to be here today and I d like to thank our hosts Deutsche Bank

Gaps and Duplicative Requirements, August 30, 2013, available at http://www.cftc.gov/ucm/groups/public/@newsroom/documents/file/odrgreport.pdf.

Report of the OTC Derivatives Regulators Group (ODRG) 1 on Cross-Border Implementation Issues March 2014 At the St. Petersburg summit in September 2013, the G20 leaders welcomed the set of understandings

Report of the OTC Derivatives Regulators Group (ODRG) 1 on Cross-Border Implementation Issues March 2014 At the St. Petersburg summit in September 2013, the G20 leaders welcomed the set of understandings

Recovery and Resolution of CCPs: let s bring the lifeboats in place

Date: 24 June 2016 ESMA/2016/1002 Recovery and Resolution of CCPs: let s bring the lifeboats in place Banque de France s policy conference on Recovery and Resolution of CCPs Paris, 24 June 2016 Steven

Date: 24 June 2016 ESMA/2016/1002 Recovery and Resolution of CCPs: let s bring the lifeboats in place Banque de France s policy conference on Recovery and Resolution of CCPs Paris, 24 June 2016 Steven

Financial Conduct Authority. The FCA s response to the Parliamentary Commission on Banking Standards

Financial Conduct Authority The s to the Parliamentary Commission on Banking Standards October 2013 Contents Introduction 3 1 Holding individuals to account 5 2 Governance and culture 9 3 Securing better

Financial Conduct Authority The s to the Parliamentary Commission on Banking Standards October 2013 Contents Introduction 3 1 Holding individuals to account 5 2 Governance and culture 9 3 Securing better

InVest. In this issue:

May 2010 InVest This month's roundup of developments affecting banks, wealth managers, brokers and funds sees the Financial Services Bill and the Bribery Bill receiving royal assent, the FSA fining former

May 2010 InVest This month's roundup of developments affecting banks, wealth managers, brokers and funds sees the Financial Services Bill and the Bribery Bill receiving royal assent, the FSA fining former

The Mortgage Market Review and Non-bank mortgage lenders is enhanced Prudential Supervision on the way?

JULY 2010 The Mortgage Market Review and Non-bank mortgage lenders is enhanced Prudential Supervision on the way? Introduction Since the publication of the FSA's latest Mortgage Market Review consultation

JULY 2010 The Mortgage Market Review and Non-bank mortgage lenders is enhanced Prudential Supervision on the way? Introduction Since the publication of the FSA's latest Mortgage Market Review consultation

THE IMPACT OF EMIR ON FINANCIAL COUNTERPARTIES

March 15, 2013 THE IMPACT OF EMIR ON FINANCIAL COUNTERPARTIES To Our Clients and Friends: On 16 August 2012, The European Market Infrastructure Regulation ( EMIR ) 1 came into force with immediate and

March 15, 2013 THE IMPACT OF EMIR ON FINANCIAL COUNTERPARTIES To Our Clients and Friends: On 16 August 2012, The European Market Infrastructure Regulation ( EMIR ) 1 came into force with immediate and

Hong Kong Proposes Margin and Risk Mitigation Standards for Non-Centrally Cleared OTC Derivatives

30 December 2015 Hong Kong Proposes Margin and Risk Mitigation Standards for Non-Centrally Cleared OTC Derivatives Introduction On 3 December 2015, the Hong Kong Monetary Authority ( HKMA ) issued a consultation

30 December 2015 Hong Kong Proposes Margin and Risk Mitigation Standards for Non-Centrally Cleared OTC Derivatives Introduction On 3 December 2015, the Hong Kong Monetary Authority ( HKMA ) issued a consultation

Consultation Paper. Proposed rules for recognised clearing houses and approved operators

Consultation Paper Proposed rules for recognised clearing houses and approved operators February 2013 Consultation Paper Proposed rules for recognised clearing houses and approved operators February 2013

Consultation Paper Proposed rules for recognised clearing houses and approved operators February 2013 Consultation Paper Proposed rules for recognised clearing houses and approved operators February 2013

Core Principles for Effective Banking Supervision: New Edition Released

News Bulletin September 17, 2012 Core Principles for Effective Banking Supervision: New Edition Released Last Friday, September 14, 2012, the Basel Committee on Banking Supervision published a new set

News Bulletin September 17, 2012 Core Principles for Effective Banking Supervision: New Edition Released Last Friday, September 14, 2012, the Basel Committee on Banking Supervision published a new set

Q3 INTERIM MANAGEMENT STATEMENT Presentation to analysts and investors. 28 October 2014

INTERIM MANAGEMENT STATEMENT Presentation to analysts and investors 28 October HIGHLIGHTS FOR THE FIRST NINE MONTHS OF Continued successful execution of our strategy and further improvement in financial

INTERIM MANAGEMENT STATEMENT Presentation to analysts and investors 28 October HIGHLIGHTS FOR THE FIRST NINE MONTHS OF Continued successful execution of our strategy and further improvement in financial

Regulation and the future of the insurance industry

1 Regulation and the future of the insurance industry Speech given by Paul Fisher, Deputy Head of the Prudential Regulation Authority and Executive Director, Insurance Supervision At the Westminster Business

1 Regulation and the future of the insurance industry Speech given by Paul Fisher, Deputy Head of the Prudential Regulation Authority and Executive Director, Insurance Supervision At the Westminster Business

05.11.2013. Closing Speech by the Governor of the Banco de España 6th Santander International Banking Conference Luis M.

05.11.2013 Closing Speech by the Governor of the Banco de España 6th Santander International Banking Conference Luis M. Linde Governor I would like first to give my thanks to Banco de Santander for inviting

05.11.2013 Closing Speech by the Governor of the Banco de España 6th Santander International Banking Conference Luis M. Linde Governor I would like first to give my thanks to Banco de Santander for inviting

European Union Green Paper on Mortgage Credit in the EU. Response from Prudential plc

1 General Comments European Union Green Paper on Mortgage Credit in the EU Response from Prudential plc 1.1 We welcome the opportunity to respond to the Commission s Green Paper on Mortgage Credit in the

1 General Comments European Union Green Paper on Mortgage Credit in the EU Response from Prudential plc 1.1 We welcome the opportunity to respond to the Commission s Green Paper on Mortgage Credit in the

Regulated Mortgages. March 2012

Regulated Mortgages March 2012 1 Introduction Since 31 October 2004, Regulated Mortgage Contracts have been subject to statutory control, supervised by the Financial Services Authority ("FSA"). Under Section

Regulated Mortgages March 2012 1 Introduction Since 31 October 2004, Regulated Mortgage Contracts have been subject to statutory control, supervised by the Financial Services Authority ("FSA"). Under Section

Banking Organizations Subject to the Advanced Approaches Risk- Based Capital Rule

February 17, 2015 Mr. Robert DeV. Frierson Secretary Board of Governors of the Federal Reserve System 20th Street and Constitution Avenue, NW Washington, DC 20551 RIN 7100- AE 24 Regulation Q; Docket No.

February 17, 2015 Mr. Robert DeV. Frierson Secretary Board of Governors of the Federal Reserve System 20th Street and Constitution Avenue, NW Washington, DC 20551 RIN 7100- AE 24 Regulation Q; Docket No.

The challenge of liquidity and collateral management in the new regulatory landscape

The challenge of liquidity and collateral management in the new regulatory landscape ICMA Professional Repo and Collateral Management Course 2012 Agenda 1. Background: The repo product under pressure 2.

The challenge of liquidity and collateral management in the new regulatory landscape ICMA Professional Repo and Collateral Management Course 2012 Agenda 1. Background: The repo product under pressure 2.

CMU and a review of the regulatory initiatives affecting the international securities markets ICMA/NCMF Bond Market Seminar, Helsinki Martin Scheck,

CMU and a review of the regulatory initiatives affecting the international securities markets ICMA/NCMF Bond Market Seminar, Helsinki Martin Scheck, 22 January 2015 Contents Introduction current status

CMU and a review of the regulatory initiatives affecting the international securities markets ICMA/NCMF Bond Market Seminar, Helsinki Martin Scheck, 22 January 2015 Contents Introduction current status

UK Proposals for Bank Levies under the June 2010 Emergency Budget

News Bulletin June 30, 2010 UK Proposals for Bank Levies under the June 2010 Emergency Budget On 22 June 2010, the UK Chancellor, George Osborne MP, of the Conservative-led UK government (the Govt. ),

News Bulletin June 30, 2010 UK Proposals for Bank Levies under the June 2010 Emergency Budget On 22 June 2010, the UK Chancellor, George Osborne MP, of the Conservative-led UK government (the Govt. ),

Northern Rock plc: Half Year Results 2011

Press Release 3 August 2011 Northern Rock plc: Half Year Results 2011 Northern Rock has continued to build momentum during the first half of the year and considerably improved its position over 2010 The

Press Release 3 August 2011 Northern Rock plc: Half Year Results 2011 Northern Rock has continued to build momentum during the first half of the year and considerably improved its position over 2010 The

Arnout H. E. M. Wellink. President, De Nederlandsche Bank Chairman, Basel Committee on Banking Supervision

President, De Nederlandsche Bank Chairman, Basel Committee on Banking Supervision 118 27. Mai 2008 Banking Supervision in Europe: Developments and Challenges 1. The banking system has gone through major

President, De Nederlandsche Bank Chairman, Basel Committee on Banking Supervision 118 27. Mai 2008 Banking Supervision in Europe: Developments and Challenges 1. The banking system has gone through major

CCP RISK MANAGEMENT, RECOVERY & RESOLUTION. An LCH.Clearnet White Paper

CCP RISK MANAGEMENT, RECOVERY & RESOLUTION An LCH.Clearnet White Paper Table of Contents Executive Summary 1. Risk Management 2. Recovery Tools 3. Resolution Plans Recommendations Introduction Chapter

CCP RISK MANAGEMENT, RECOVERY & RESOLUTION An LCH.Clearnet White Paper Table of Contents Executive Summary 1. Risk Management 2. Recovery Tools 3. Resolution Plans Recommendations Introduction Chapter

Financial Conduct Authority. Business Plan 2014/15

Financial Conduct Authority Business Plan 2014/15 Business Plan 2014/15 Financial Conduct Authority 2014 25 The North Colonnade Canary Wharf London E14 5HS Telephone: +44 (0)20 7066 1000 Website: www.fca.org.uk

Financial Conduct Authority Business Plan 2014/15 Business Plan 2014/15 Financial Conduct Authority 2014 25 The North Colonnade Canary Wharf London E14 5HS Telephone: +44 (0)20 7066 1000 Website: www.fca.org.uk

Discussion Paper DP1/14. Ensuring operational continuity in resolution

Discussion Paper DP1/14 Ensuring operational continuity in resolution October 2014 Prudential Regulation Authority 20 Moorgate London EC2R 6DA Prudential Regulation Authority, registered office: 8 Lothbury,

Discussion Paper DP1/14 Ensuring operational continuity in resolution October 2014 Prudential Regulation Authority 20 Moorgate London EC2R 6DA Prudential Regulation Authority, registered office: 8 Lothbury,

Basel Committee on Banking Supervision. Consultative Document. Net Stable Funding Ratio disclosure standards. Issued for comment by 6 March 2015

Basel Committee on Banking Supervision Consultative Document Net Stable Funding Ratio disclosure standards Issued for comment by 6 March 2015 December 2014 This publication is available on the BIS website

Basel Committee on Banking Supervision Consultative Document Net Stable Funding Ratio disclosure standards Issued for comment by 6 March 2015 December 2014 This publication is available on the BIS website

The Independent Commission on Banking s Report and Recommendations

The Independent Commission on Banking s Report and Recommendations The Independent Commission on Banking (ICB) chaired by Sir John Vickers was established in June 2010 to consider structural and related

The Independent Commission on Banking s Report and Recommendations The Independent Commission on Banking (ICB) chaired by Sir John Vickers was established in June 2010 to consider structural and related

List of legislative acts

List of legislative acts BRRd : d irective 2014/59/EU of the European Parliament and of the Council of 15 May 2014 establishing a framework for the recovery and resolution of credit institutions and investment

List of legislative acts BRRd : d irective 2014/59/EU of the European Parliament and of the Council of 15 May 2014 establishing a framework for the recovery and resolution of credit institutions and investment

An effective recovery and resolution regime for CCPs

An effective recovery and resolution regime for CCPs December 2014 1. Summary...3 2. Why are CCPs important for the stability of the financial system?...4 3. Why are CCPs resilient institutions?...5 4.

An effective recovery and resolution regime for CCPs December 2014 1. Summary...3 2. Why are CCPs important for the stability of the financial system?...4 3. Why are CCPs resilient institutions?...5 4.

IOSCO BN01-11 Consultative Report

IOSCO BN01-11 10 March 2011 Cover note to the consultative report 1 Overview of the report The consultative report on Principles for Financial Market Infrastructures (consultative report) was prepared

IOSCO BN01-11 10 March 2011 Cover note to the consultative report 1 Overview of the report The consultative report on Principles for Financial Market Infrastructures (consultative report) was prepared

Agathe Côté: Toward a stronger financial market infrastructure for Canada taking stock

Agathe Côté: Toward a stronger financial market infrastructure for Canada taking stock Remarks by Ms Agathe Côté, Deputy Governor of the Bank of Canada, to the Association for Financial Professionals of

Agathe Côté: Toward a stronger financial market infrastructure for Canada taking stock Remarks by Ms Agathe Côté, Deputy Governor of the Bank of Canada, to the Association for Financial Professionals of

To G20 Finance Ministers and Central Bank Governors. Financial Reforms Finishing the Post-Crisis Agenda and Moving Forward

THE CHAIRMAN 4 February 2015 To G20 Finance Ministers and Central Bank Governors Financial Reforms Finishing the Post-Crisis Agenda and Moving Forward In Brisbane, G20 Leaders welcomed the progress we

THE CHAIRMAN 4 February 2015 To G20 Finance Ministers and Central Bank Governors Financial Reforms Finishing the Post-Crisis Agenda and Moving Forward In Brisbane, G20 Leaders welcomed the progress we

Principles for the supervision of financial conglomerates

THE JOINT FORUM BASEL COMMITTEE ON BANKING SUPERVISION INTERNATIONAL ORGANIZATION OF SECURITIES COMMISSIONS INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS C/O BANK FOR INTERNATIONAL SETTLEMENTS CH-4002

THE JOINT FORUM BASEL COMMITTEE ON BANKING SUPERVISION INTERNATIONAL ORGANIZATION OF SECURITIES COMMISSIONS INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS C/O BANK FOR INTERNATIONAL SETTLEMENTS CH-4002

VI. Structural and regulatory developments

Serge Jeanneau (+41 61) 280 8416 serge.jeanneau@bis.org VI. Structural and regulatory developments Initiatives and reports concerning financial institutions July The Supervision (BCBS) released a consultative

Serge Jeanneau (+41 61) 280 8416 serge.jeanneau@bis.org VI. Structural and regulatory developments Initiatives and reports concerning financial institutions July The Supervision (BCBS) released a consultative

CPSS-IOSCO Principles for Financial Market Infrastructures*

CSS-IOSCO rinciples for Financial Market Infrastructures* Workshop on ayments Systems Oversight Banco de Guatemala Guatemala, Guatemala, October 16-18, 2013 Klaus Löber CSS Secretariat Bank for International

CSS-IOSCO rinciples for Financial Market Infrastructures* Workshop on ayments Systems Oversight Banco de Guatemala Guatemala, Guatemala, October 16-18, 2013 Klaus Löber CSS Secretariat Bank for International

EVOLUTION OF FINANCIAL REGULATION AT BCBS AND FSB

EVOLUTION OF FINANCIAL REGULATION AT BCBS AND FSB SINCE 2008 Christoph Baumann* THE FINANCIAL STABILITY BOARD AND THE BASEL COMMITTEE ON BANKING SUPERVISION International financial regulation has been

EVOLUTION OF FINANCIAL REGULATION AT BCBS AND FSB SINCE 2008 Christoph Baumann* THE FINANCIAL STABILITY BOARD AND THE BASEL COMMITTEE ON BANKING SUPERVISION International financial regulation has been

The Role of Mortgage Insurance under the New Global Regulatory Frameworks

The Role of Mortgage Insurance under the New Global Regulatory Frameworks By Anna Whittingham Regulatory Analyst, Genworth Financial Mortgage Insurance Europe Summary and Overview The introduction of fundamental

The Role of Mortgage Insurance under the New Global Regulatory Frameworks By Anna Whittingham Regulatory Analyst, Genworth Financial Mortgage Insurance Europe Summary and Overview The introduction of fundamental

FSI-IADI Seminar on Bank Resolution, Crisis Management and Deposit Insurance Issues. Coordination of safety net players: Role of DIA.

FSI-IADI Seminar on Bank Resolution, Crisis Management and Deposit Insurance Issues Coordination of safety net players: Role of DIA Jerzy Pruski IADI President and Chair of the Executive Council President

FSI-IADI Seminar on Bank Resolution, Crisis Management and Deposit Insurance Issues Coordination of safety net players: Role of DIA Jerzy Pruski IADI President and Chair of the Executive Council President

European Securities Forum

European Securities Forum Submission to the Basel Committee on Banking Supervision The New Basel Capital Accord The European Securities Forum (ESF) is an organisation established by the major users of

European Securities Forum Submission to the Basel Committee on Banking Supervision The New Basel Capital Accord The European Securities Forum (ESF) is an organisation established by the major users of

Chapter 4: Comparison with other arrangements

Chapter 4: Comparison with other arrangements This chapter outlines the compensation arrangements for consumers in some other countries in relation to their dealings with financial intermediaries. It also

Chapter 4: Comparison with other arrangements This chapter outlines the compensation arrangements for consumers in some other countries in relation to their dealings with financial intermediaries. It also

International Monetary Fund Washington, D.C.

2013 International Monetary Fund March 2013 IMF Country Report No. 13/72 January 22, 2013 January 29, 2001 January 29, 2001 January 29, 2001 January 29, 2001 European Union: Publication of Financial Sector

2013 International Monetary Fund March 2013 IMF Country Report No. 13/72 January 22, 2013 January 29, 2001 January 29, 2001 January 29, 2001 January 29, 2001 European Union: Publication of Financial Sector

RegZone www.law-now.com/regzone

RegZone www.law-now.com/regzone MiFID and MAD round two - an overview London and Edinburgh 1 CMS Cameron McKenna CMS Cameron McKenna is an international commercial law firm advising businesses, financial

RegZone www.law-now.com/regzone MiFID and MAD round two - an overview London and Edinburgh 1 CMS Cameron McKenna CMS Cameron McKenna is an international commercial law firm advising businesses, financial

Glossary & Definitions

Glossary & Definitions SEB Glossary & Definitions December 2014 Asset quality... 3 Credit loss level... 3 Gross level of impaired loans... 3 Net level of impaired loans... 3 Specific reserve ratio for

Glossary & Definitions SEB Glossary & Definitions December 2014 Asset quality... 3 Credit loss level... 3 Gross level of impaired loans... 3 Net level of impaired loans... 3 Specific reserve ratio for

Financial stability, systemic risk & macroprudential supervision: an actuarial perspective

Financial stability, systemic risk & macroprudential supervision: an actuarial perspective Paul Thornton International Actuarial Association Presentation to OECD Insurance and Pensions Committee June 2010

Financial stability, systemic risk & macroprudential supervision: an actuarial perspective Paul Thornton International Actuarial Association Presentation to OECD Insurance and Pensions Committee June 2010

Impact of the financial crisis and bank failure

Impact of the financial crisis and bank failure Professor Julian Franks London Business School July 2009 Introduction Some questions and issues which will affect the future of the financial services industry.

Impact of the financial crisis and bank failure Professor Julian Franks London Business School July 2009 Introduction Some questions and issues which will affect the future of the financial services industry.

FSB launches peer review on deposit insurance systems and invites feedback from stakeholders

Press release Press enquiries: Basel +41 61 280 8037 Press.service@bis.org Ref no: 26/2011 1 July 2011 FSB launches peer review on deposit insurance systems and invites feedback from stakeholders The Financial

Press release Press enquiries: Basel +41 61 280 8037 Press.service@bis.org Ref no: 26/2011 1 July 2011 FSB launches peer review on deposit insurance systems and invites feedback from stakeholders The Financial

Financial Regulation: An overview of the FCA s proposal of the new Consumer Credit regime October 2013

Financial Regulation: An overview of the FCA s proposal of the new Consumer Credit regime October 2013 Consultation Paper 13/10: Detailed Proposals for the FCA regime for Consumer Credit In early October

Financial Regulation: An overview of the FCA s proposal of the new Consumer Credit regime October 2013 Consultation Paper 13/10: Detailed Proposals for the FCA regime for Consumer Credit In early October

approach To regulation

THE Financial Conduct Authority Approach to Regulation JUNE 2011 Contents Introduction 2 ONE Overview 4 TWO Scope 10 THREE Objectives and powers 14 1 FOUR Regulatory approach 22 FIVE Regulatory activities

THE Financial Conduct Authority Approach to Regulation JUNE 2011 Contents Introduction 2 ONE Overview 4 TWO Scope 10 THREE Objectives and powers 14 1 FOUR Regulatory approach 22 FIVE Regulatory activities

Implications of the SSM for the Nordic banking sector. Stefan Ingves, June 5 2014

Implications of the SSM for the Nordic banking sector Stefan Ingves, June 5 2014 Financial trilemma Financial stability Financial integration National supervision Arrangements for cross-border cooperation

Implications of the SSM for the Nordic banking sector Stefan Ingves, June 5 2014 Financial trilemma Financial stability Financial integration National supervision Arrangements for cross-border cooperation

EBA final draft Regulatory Technical Standards

EBA/RTS/2014/11 18 July 2014 EBA final draft Regulatory Technical Standards on the content of recovery plans under Article 5(10) of Directive 2014/59/EU establishing a framework for the recovery and resolution

EBA/RTS/2014/11 18 July 2014 EBA final draft Regulatory Technical Standards on the content of recovery plans under Article 5(10) of Directive 2014/59/EU establishing a framework for the recovery and resolution

Vítor Constâncio: A European solution for crisis management and bank resolution

Vítor Constâncio: A European solution for crisis management and bank resolution Speech by Mr Vítor Constâncio, Vice-President of the European Central Bank, at Sveriges Riksbank and ECB Conference on Bank

Vítor Constâncio: A European solution for crisis management and bank resolution Speech by Mr Vítor Constâncio, Vice-President of the European Central Bank, at Sveriges Riksbank and ECB Conference on Bank

3 F i n a n c i a l stability

3 F i n a n c i a l stability The world economy was hit by a global credit shock in mid-2007. Since then, global financial markets have suffered a sustained period of stress and instability. The intensification

3 F i n a n c i a l stability The world economy was hit by a global credit shock in mid-2007. Since then, global financial markets have suffered a sustained period of stress and instability. The intensification

SUBMISSION BY THE AUSTRALIAN SECURITIES AND INVESTMENTS COMMISSION

SUBMISSION BY THE AUSTRALIAN SECURITIES AND INVESTMENTS COMMISSION Executive Summary ASIC has responsibility for the regulation of securities and some derivatives markets in Australia. These markets are

SUBMISSION BY THE AUSTRALIAN SECURITIES AND INVESTMENTS COMMISSION Executive Summary ASIC has responsibility for the regulation of securities and some derivatives markets in Australia. These markets are

DETAILED TABLE OF CONTENTS

DETAILED TABLE OF CONTENTS Table of Cases Table of Legislation List of Abbreviations xxii xxv lxi I. Introduction 1 1.1 EU Securities and Markets Regulation 1 1.2 Securities and Markets Regulation and

DETAILED TABLE OF CONTENTS Table of Cases Table of Legislation List of Abbreviations xxii xxv lxi I. Introduction 1 1.1 EU Securities and Markets Regulation 1 1.2 Securities and Markets Regulation and

The EMU and the debt crisis

The EMU and the debt crisis MONETARY POLICY REPORT FEBRUARY 212 43 The debt crisis in Europe is not only of concern to the individual debt-ridden countries; it has also developed into a crisis for the

The EMU and the debt crisis MONETARY POLICY REPORT FEBRUARY 212 43 The debt crisis in Europe is not only of concern to the individual debt-ridden countries; it has also developed into a crisis for the

FinfraG / EMIR. Your partner to navigate the challenges in investment and risk management. Current Status What you need to know. 23 rd September 2014

Your partner to navigate the challenges in investment and risk management. FinfraG / EMIR ROSENWEG 3 GARTENSTRASSE 19 CH-6340 BAAR/ZUG CH-8002 ZURICH SWITZERLAND SWITZERLAND INFO@INCUBEGROUP.COM INCUBEGROUP.COM

Your partner to navigate the challenges in investment and risk management. FinfraG / EMIR ROSENWEG 3 GARTENSTRASSE 19 CH-6340 BAAR/ZUG CH-8002 ZURICH SWITZERLAND SWITZERLAND INFO@INCUBEGROUP.COM INCUBEGROUP.COM

Consultation Paper. Draft Regulatory Technical Standards on the content of resolution plans and the assessment of resolvability EBA/CP/2014/16

EBA/CP/2014/16 9 July 2014 Consultation Paper Draft Regulatory Technical Standards on the content of resolution plans and the assessment of resolvability Contents 1. Responding to this Consultation 3 2.

EBA/CP/2014/16 9 July 2014 Consultation Paper Draft Regulatory Technical Standards on the content of resolution plans and the assessment of resolvability Contents 1. Responding to this Consultation 3 2.

How to improve financial stability and resilience of systemically important financial institutions after the crisis?

How to improve financial stability and resilience of systemically important financial institutions after the crisis? EBA Policy Research Workshop How to regulate and resolve systemically important banks

How to improve financial stability and resilience of systemically important financial institutions after the crisis? EBA Policy Research Workshop How to regulate and resolve systemically important banks

Accounting and Reporting Policy FRS 102. Staff Education Note 14 Credit unions - Illustrative financial statements

Accounting and Reporting Policy FRS 102 Staff Education Note 14 Credit unions - Illustrative financial statements Disclaimer This Education Note has been prepared by FRC staff for the convenience of users

Accounting and Reporting Policy FRS 102 Staff Education Note 14 Credit unions - Illustrative financial statements Disclaimer This Education Note has been prepared by FRC staff for the convenience of users

CPSS IOSCO Principles for financial market infrastructures: vectors of international convergence

CPSS IOSCO Principles for financial market infrastructures: vectors of international convergence Daniela RUSSO Director General of the Directorate General Payments and Market Infrastructure European Central

CPSS IOSCO Principles for financial market infrastructures: vectors of international convergence Daniela RUSSO Director General of the Directorate General Payments and Market Infrastructure European Central

Financial Conduct Authority The FCA s approach to advancing its objectives

Financial Conduct Authority The FCA s approach to advancing its objectives July 2013 Glossary helping to explain financial terms As with many industries, the financial marketplace uses terminology that

Financial Conduct Authority The FCA s approach to advancing its objectives July 2013 Glossary helping to explain financial terms As with many industries, the financial marketplace uses terminology that

Regional workshop BCCL-METAC Operational functioning of supervisory Colleges BEYROUTH, April 25 th, 2012

Regional workshop BCCL-METAC Operational functioning of supervisory Colleges BEYROUTH, April 25 th, 2012 INTRODUCTION SUPERVISORY COLLEGES ARE A FUNDAMENTAL TOOL OF COOPERATION : At the light of the crisis,

Regional workshop BCCL-METAC Operational functioning of supervisory Colleges BEYROUTH, April 25 th, 2012 INTRODUCTION SUPERVISORY COLLEGES ARE A FUNDAMENTAL TOOL OF COOPERATION : At the light of the crisis,

March 2014. Guide to the regulation of workplace defined contribution pensions

March 2014 Guide to the regulation of workplace defined contribution pensions The Financial Conduct Authority (FCA) and The Pensions Regulator have jointly developed this guide to provide an overview of

March 2014 Guide to the regulation of workplace defined contribution pensions The Financial Conduct Authority (FCA) and The Pensions Regulator have jointly developed this guide to provide an overview of

Directors remuneration

Briefing A review of the Government s June 2012 proposals for a binding shareholder vote on directors pay and new pay disclosures Summary This briefing looks at the detailed proposals for the new regime

Briefing A review of the Government s June 2012 proposals for a binding shareholder vote on directors pay and new pay disclosures Summary This briefing looks at the detailed proposals for the new regime

Guidelines on preparation for and management of a financial crisis

CEIOPS-DOC-15/09 26 March 2009 Guidelines on preparation for and management of a financial crisis in the Context of Supplementary Supervision as defined by the Insurance Groups Directive (98/78/EC) and

CEIOPS-DOC-15/09 26 March 2009 Guidelines on preparation for and management of a financial crisis in the Context of Supplementary Supervision as defined by the Insurance Groups Directive (98/78/EC) and

Financial Services Authority (FSA)

") FCA Approach Financial Services Authority 25 The North Colonnade Canary Wharf London E14 5HS E-mail: fcaapproach@fsa.gov.uk 12 December 2012 Financial Services Authority (FSA) Journey to the FCA Chapters

FCA Approach Financial Services Authority 25 The North Colonnade Canary Wharf London E14 5HS E-mail: fcaapproach@fsa.gov.uk 12 December 2012 Financial Services Authority (FSA) Journey to the FCA Chapters

What is new in Basel 3:

Camera dei Deputati 17 Indagine conoscitiva 4 ALLEGATO What is new in Basel 3: How it will influence market participants Krishnan Ramadurai Managing Director Camera dei Deputati 18 Indagine conoscitiva

Camera dei Deputati 17 Indagine conoscitiva 4 ALLEGATO What is new in Basel 3: How it will influence market participants Krishnan Ramadurai Managing Director Camera dei Deputati 18 Indagine conoscitiva

DG FISMA CONSULTATION PAPER ON FURTHER CONSIDERATIONS FOR THE IMPLEMENTATION OF THE NSFR IN THE EU

EUROPEAN COMMISSION Directorate-General for Financial Stability, Financial Services and Capital Markets Union DG FISMA CONSULTATION PAPER ON FURTHER CONSIDERATIONS FOR THE IMPLEMENTATION OF THE NSFR IN

EUROPEAN COMMISSION Directorate-General for Financial Stability, Financial Services and Capital Markets Union DG FISMA CONSULTATION PAPER ON FURTHER CONSIDERATIONS FOR THE IMPLEMENTATION OF THE NSFR IN

COMMISSION STAFF WORKING PAPER EXECUTIVE SUMMARY OF THE IMPACT ASSESSMENT. Accompanying the document. Proposal for a

EUROPEAN COMMISSION Brussels, XXX SEC(2011) 1227 COMMISSION STAFF WORKING PAPER EXECUTIVE SUMMARY OF THE IMPACT ASSESSMENT Accompanying the document Proposal for a DIRECTIVE OF THE EUROPEAN PARLIAMENT

EUROPEAN COMMISSION Brussels, XXX SEC(2011) 1227 COMMISSION STAFF WORKING PAPER EXECUTIVE SUMMARY OF THE IMPACT ASSESSMENT Accompanying the document Proposal for a DIRECTIVE OF THE EUROPEAN PARLIAMENT

Independent Commission on Banking. Investment Management Association response to Interim Report

Independent Commission on Banking Investment Management Association response to Interim Report The IMA represents the investment management industry in the UK. Its members managed a total of 3.9 trillion

Independent Commission on Banking Investment Management Association response to Interim Report The IMA represents the investment management industry in the UK. Its members managed a total of 3.9 trillion

Definition of Capital

Definition of Capital Capital serves as a buffer to absorb unexpected losses as well as to fund ongoing activities of the firm. A number of substantial changes have been made to the minimum level of capital

Definition of Capital Capital serves as a buffer to absorb unexpected losses as well as to fund ongoing activities of the firm. A number of substantial changes have been made to the minimum level of capital

THOMSON REUTERS ACCELUS. The FCA: A Game Changer

THOMSON REUTERS ACCELUS The FCA: A Game Changer for Company Training Statement of intent This whitepaper, brought to you by Thomson Reuters, discusses the implications of the new financial regulatory framework

THOMSON REUTERS ACCELUS The FCA: A Game Changer for Company Training Statement of intent This whitepaper, brought to you by Thomson Reuters, discusses the implications of the new financial regulatory framework

Product Intervention in the UK and the New FCA

News Bulletin July 5, 2011 Product Intervention in the UK and the New FCA Background As we have previously discussed, 1 the UK Financial Services Authority (the FSA ) signalled a sea change in the way

News Bulletin July 5, 2011 Product Intervention in the UK and the New FCA Background As we have previously discussed, 1 the UK Financial Services Authority (the FSA ) signalled a sea change in the way

Policy on the Management of Country Risk by Credit Institutions

2013 Policy on the Management of Country Risk by Credit Institutions 1 Policy on the Management of Country Risk by Credit Institutions Contents 1. Introduction and Application 2 1.1 Application of this

2013 Policy on the Management of Country Risk by Credit Institutions 1 Policy on the Management of Country Risk by Credit Institutions Contents 1. Introduction and Application 2 1.1 Application of this

October 2014. Guide to the Financial Market Infrastructure Act

October 2014 Guide to the Financial Market Infrastructure Act 1. Executive Summary The Financial Market Infrastructure Act (FMIA) (Bundesgesetz über die Finanzmarktinfrastrukturen und das Marktverhalten

October 2014 Guide to the Financial Market Infrastructure Act 1. Executive Summary The Financial Market Infrastructure Act (FMIA) (Bundesgesetz über die Finanzmarktinfrastrukturen und das Marktverhalten

Regulatory Practice Letter November 2014 RPL 14-20

Regulatory Practice Letter November 2014 RPL 14-20 BCBS Issues Final Net Stable Funding Ratio Standard Executive Summary The Basel Committee on Banking Supervision ( BCBS or Basel Committee ) issued its

Regulatory Practice Letter November 2014 RPL 14-20 BCBS Issues Final Net Stable Funding Ratio Standard Executive Summary The Basel Committee on Banking Supervision ( BCBS or Basel Committee ) issued its

by William A. Scott, Stikeman Elliott LLP

Recent regulatory developments in the Canadian OTC derivatives market by William A. Scott, Stikeman Elliott LLP As the Canadian federal government seemingly never tires of reminding us, the Canadian financial

Recent regulatory developments in the Canadian OTC derivatives market by William A. Scott, Stikeman Elliott LLP As the Canadian federal government seemingly never tires of reminding us, the Canadian financial

Basel Committee on Banking Supervision. Net Stable Funding Ratio disclosure standards

Basel Committee on Banking Supervision Net Stable Funding Ratio disclosure standards June 2015 This publication is available on the BIS website (www.bis.org). Bank for International Settlements 2015. All

Basel Committee on Banking Supervision Net Stable Funding Ratio disclosure standards June 2015 This publication is available on the BIS website (www.bis.org). Bank for International Settlements 2015. All

Financial Reforms Achieving and Sustaining Resilience for All

T H E C H A I R M A N 9 November 2015 To G20 Leaders Financial Reforms Achieving and Sustaining Resilience for All Over the past seven years, the G20 has fundamentally reformed the global financial system

T H E C H A I R M A N 9 November 2015 To G20 Leaders Financial Reforms Achieving and Sustaining Resilience for All Over the past seven years, the G20 has fundamentally reformed the global financial system

THE REGULATORY LANDSCAPE IS CHANGING, ARE YOU READY? RECENT UPDATES TO PRA AND TLAC STANDARDS

THE REGULATORY LANDSCAPE IS CHANGING, ARE YOU READY? RECENT UPDATES TO PRA AND TLAC STANDARDS PRA OPERATIONAL CONTINUITY REQUIREMENTS FURTHER ENHANCEMENTS BUT GREATER COSTS 15 October saw the release of

THE REGULATORY LANDSCAPE IS CHANGING, ARE YOU READY? RECENT UPDATES TO PRA AND TLAC STANDARDS PRA OPERATIONAL CONTINUITY REQUIREMENTS FURTHER ENHANCEMENTS BUT GREATER COSTS 15 October saw the release of

Credit Rating Agencies Reducing reliance and strengthening oversight

29 August 2013 Credit Rating Agencies Reducing reliance and strengthening oversight Progress report to the St Petersburg G20 Summit Authorities need to accelerate work to end the mechanistic reliance of

29 August 2013 Credit Rating Agencies Reducing reliance and strengthening oversight Progress report to the St Petersburg G20 Summit Authorities need to accelerate work to end the mechanistic reliance of

G20 Financial Regulatory Reforms and Australia

G20 Financial Regulatory Reforms and Australia Carl Schwartz* The global financial crisis prompted a comprehensive international regulatory response, directed through the Group of Twenty (G20). The Reserve

G20 Financial Regulatory Reforms and Australia Carl Schwartz* The global financial crisis prompted a comprehensive international regulatory response, directed through the Group of Twenty (G20). The Reserve

Liquidity Coverage Ratio

Liquidity Coverage Ratio Aims to ensure banks maintain adequate levels of unencumbered high quality assets (numerator) against net cash outflows (denominator) over a 30 day significant stress period. High

Liquidity Coverage Ratio Aims to ensure banks maintain adequate levels of unencumbered high quality assets (numerator) against net cash outflows (denominator) over a 30 day significant stress period. High

Governance and the role of Boards

1 Governance and the role of Boards Speech given by Andrew Bailey, Deputy Governor, Prudential Regulation and Chief Executive Officer, Prudential Regulation Authority Westminster Business Forum, London

1 Governance and the role of Boards Speech given by Andrew Bailey, Deputy Governor, Prudential Regulation and Chief Executive Officer, Prudential Regulation Authority Westminster Business Forum, London

CEO Overview - Corporate Governance and Reporting in the UK

Financial Reporting Council Plan & Budget 2011/12 Financial Reporting Council Council Plan & Budget 2011/12 Plan & Budget 2011/12 April 2011 Contents Section 1: CEO Overview 3 Section 2: Major activities

Financial Reporting Council Plan & Budget 2011/12 Financial Reporting Council Council Plan & Budget 2011/12 Plan & Budget 2011/12 April 2011 Contents Section 1: CEO Overview 3 Section 2: Major activities

MiFID/MiFIR: The OTF and SI regime for OTC derivatives

MiFID/MiFIR: The OTF and SI regime for OTC derivatives The International Swaps and Derivatives Association (ISDA) would like to take this opportunity to set out its views on the elements of European Commission

MiFID/MiFIR: The OTF and SI regime for OTC derivatives The International Swaps and Derivatives Association (ISDA) would like to take this opportunity to set out its views on the elements of European Commission

Flash News. European Parliament adopts MiFID II. 1. Background. 2. MiFID II for banks, investment firms and asset managers

www.pwc.lu/regulatory-compliance Flash News European Parliament adopts MiFID II 23 April 2014 Following the political agreement reached on 14 January 2014 by the European Parliament, the Council and the

www.pwc.lu/regulatory-compliance Flash News European Parliament adopts MiFID II 23 April 2014 Following the political agreement reached on 14 January 2014 by the European Parliament, the Council and the