Notice of Intent to Garnish

|

|

|

- Whitney Kennedy

- 8 years ago

- Views:

Transcription

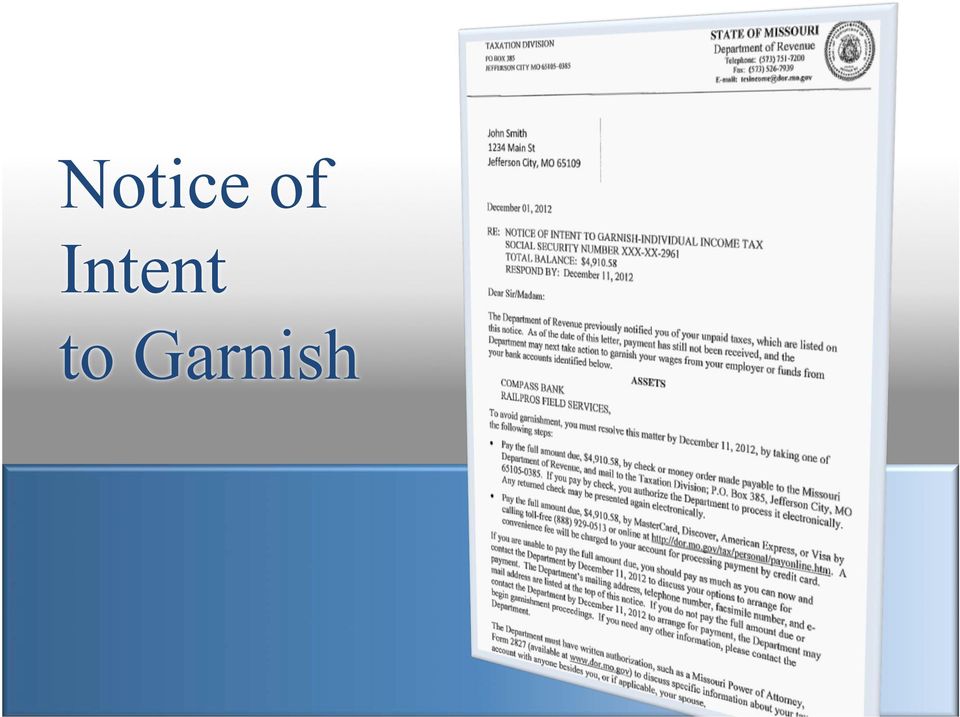

1 Notice of Intent to Garnish Missouri Department of Revenue MSATA Conference Presented by Cheryl Bosch August 2013

2 Notice of Intent to Garnish

3 Background Information Operating Process Receivables move through billing process in mainframe tax systems Corresponding collection cases in CACSG move through the state assignment process Debts may be: referred to outside collection agency; referred to participating prosecuting attorney; or Coded as difficult to collect

4 Background Information Operating Process Due to the high volumes of cases, inventory must be prioritized. Some taxpayers do not receive follow up letters or phone calls.

5 Background Information Operating Process August 2009, initiated garnishments of bank and wages assets, which resulted in increased collections. Obstacles: Time consuming Limited resources No administrative garnishment process in place

6 Timeline - March 2012 Contractor began working onsite: - Discuss current collection practices - Identify ways to increase collections

7 Timeline - March 2012 Brainstorming sessions outcome: - Send notices to taxpayers who have asset information stored in Department s data warehouse

8 Timeline April 2012 Decided to issue a Notice of Intent to Garnish to avoid the actual cost of filing a garnishment.

9 Timeline April 2012 Notice of Intent to Garnish criteria: Total receivable balance between $1,000 and $5,000 Lien on at least one or more of their outstanding periods Have a bank or wage asset Sources used - IRMF & IRS levy extract data - RemiFance processor - MO Dept of Labor & Industrial RelaKons

10 Timeline April 2012 Prepared business case: Number of potential taxpayers to receive letter Estimate response rate 20,304 taxpayers $47 million receivables AnKcipated 3% colleckons

11 Purpose of Notice Provide taxpayer with notification of outstanding balance Provide a detailed breakdown of liabilities Timeline - April 2012

12 Purpose of Notice Provide tear off voucher Timeline - April 2012

13 Purpose of Notice Minimize the amount of uncollectable debt prior to the conversion of the new system Timeline - April 2012

14 Outside Collection Agencies The Department sends difficult to collect debts to collection agencies: Delinquent out-of-state accounts Lower dollar debts Debts DOR attempted to collect without resolution Second placement debts previously with participating prosecuting The Department contracts with two outside colleckon agencies.

15 Prosecuting Attorney The Department sends difficult to collect debts to participating county prosecuting attorneys: Lower dollar Accounts with unsuccessful attempts to collect

16 Unsolicited Accounts Non-active accounts with collection agencies and Prosecuting Attorney s resulted in: Taxpayers not contacted No voluntary payments made Timeline - April 2012

17 Who to Contact Taxpayers with balance due of $1,000 to $5,000 Taxpayers who had asset information available Timeline - April 2012

18 Data Warehouses Storing wage information: December 2010 Missouri Department of Labor and Industrial Relations May INT October 2012 banking information

19 Coordination of Efforts Can the delinquent call center handle the increase in calls as result of this notice? Can we timely process: Additional correspondence Payments Return mail received Timeline - April 2012

20 Timeline May 2012 Approval for new process

21 Timeline May 2012 Notice of Intent to Garnish generated from CACSG

22 Timeline May 2012 Request funding for postage

23 Timeline - June 2012 Developed lead creation process and determined new routing rules to be set up within CACSG for tracking these leads.

24 Timeline - June 2012 IT staff created new routing rules and collection work flows for the new process in CACSG.

25 Timeline - July 2012 New process tested 100 letters sent per week; increased to 1,500 per week Expanded the program in June 2013 to include accounts with a balance due of $300 to $1,000.

26 Timeline - July 2012 Once taxpayers understand the Department will garnish wages they make agreements to pay their debt.

27 STATS Up-To-Date Letters and Collections

28 Stats Since July 20, 2012 Sent 51,446 Notices of Intent to Garnish Notices have generated 19,979 phone calls Resolve the debt on 1,596 accounts without payment Established 3,341 payment plans Collected $4.47 million as a result of this notice Originally anticipated a 3% collection rate. The actual collection rate is 9%.

29 Up-to-Date Implement outbound call campaign Work with RSI to develop a Business Case for sending a Notice of Intent to Garnish to delinquent businesses for sales and employer s withholding tax debts

30 Up-to-Date Develop a Statement of Account letter to include: Each tax period and outstanding debt Tear off voucher The Department s website and call center phone number Plain talk language

31 Up-to-Date Calculated the amount of Missouri taxpayers that do not file/pay their income tax in a timely manner Determined that 94% of Missouri taxpayers pay and file on time

32 Stats 18,588 taxpayers with $96,712,875 in receivables eligible to receive the Statement of Account letter (3% response rate to the notice, this program would generate $2.9 million)

33 Stats July 30, 2013 Began issuing the Statement of Account letter

34 Notice of Intent to Garnish Missouri Department Of Revenue MSATA Conference Presented by Cheryl Bosch August 2013

Report on Compliance Programs, Activities, Trends and Targets Prepared in Accordance with Act 50, Sec. E. 111 (b) of 2013

of 2013") Report on Compliance Programs, Activities, Trends and Targets Prepared in Accordance with Act 50, Sec. E. 111 (b) of 2013 January 15, 2014 Vermont Department of Taxes: Report on Compliance Programs, Activities,

Report on Compliance Programs, Activities, Trends and Targets Prepared in Accordance with Act 50, Sec. E. 111 (b) of 2013 January 15, 2014 Vermont Department of Taxes: Report on Compliance Programs, Activities,

Accounts Receivable Report

Accounts Receivable Report For the Fiscal Year Ended June 30, 2004 Colorado Department of Personnel & Administration Division of Finance and Procurement Office of the State Controller Leslie M. Shenefelt,

Accounts Receivable Report For the Fiscal Year Ended June 30, 2004 Colorado Department of Personnel & Administration Division of Finance and Procurement Office of the State Controller Leslie M. Shenefelt,

>A favorable payment opportunity for taxpayers financially impacted by a weakened economy to pay current outstanding individual income tax debts.

Individual Income Tax Debt Payment Program >A favorable payment opportunity for taxpayers financially impacted by a weakened economy to pay current outstanding individual income tax debts. >Taxpayers can

Individual Income Tax Debt Payment Program >A favorable payment opportunity for taxpayers financially impacted by a weakened economy to pay current outstanding individual income tax debts. >Taxpayers can

The state's collection procedures are detailed in the State Administrative Manual. Collection steps may include some or all of the following:

This report is submitted to meet the provisions of Government Code (GC) Section 13292.5, requiring annual reporting by the Department of Finance to the Legislature on the status of delinquent receivables

This report is submitted to meet the provisions of Government Code (GC) Section 13292.5, requiring annual reporting by the Department of Finance to the Legislature on the status of delinquent receivables

Wisconsin TAX BULLETIN

Number 108 June 1998 Wisconsin TAX BULLETIN Tax Amnesty Program Created The Wisconsin Legislature created a tax amnesty program in its extraordinary session which ended May 13, 1998. The amnesty program

Number 108 June 1998 Wisconsin TAX BULLETIN Tax Amnesty Program Created The Wisconsin Legislature created a tax amnesty program in its extraordinary session which ended May 13, 1998. The amnesty program

Employment Development Department Accounts Receivables for State's Employment Tax Program

Employment Development Department Accounts Receivables for State's Employment Tax Program Introduction As one of the nation s largest tax collection agencies, the Employment Development Department (EDD)

Employment Development Department Accounts Receivables for State's Employment Tax Program Introduction As one of the nation s largest tax collection agencies, the Employment Development Department (EDD)

BILLING AND COLLECTIONS POLICY

1st Effective 10-23-2015 BILLING AND COLLECTIONS POLICY Potomac Valley Hospital, Inc. is a not-for profit hospital committed to providing emergency and medically necessary, high quality healthcare services

1st Effective 10-23-2015 BILLING AND COLLECTIONS POLICY Potomac Valley Hospital, Inc. is a not-for profit hospital committed to providing emergency and medically necessary, high quality healthcare services

GAO TAX DEBT COLLECTION. IRS Has a Complex Process to Attempt to Collect Billions of Dollars in Unpaid Tax Debts

GAO United States Government Accountability Office Report to the Committee on Finance, U.S. Senate June 2008 TAX DEBT COLLECTION IRS Has a Complex Process to Attempt to Collect Billions of Dollars in Unpaid

GAO United States Government Accountability Office Report to the Committee on Finance, U.S. Senate June 2008 TAX DEBT COLLECTION IRS Has a Complex Process to Attempt to Collect Billions of Dollars in Unpaid

IRS PRIVATE DEBT COLLECTION

IRS PRIVATE DEBT COLLECTION Executive Summary Introduction Cost Effectiveness Study March 2009 Approach Results Analysis & Findings Appendices TABLE OF CONTENTS Executive Summary 3 I. Introduction 5 II.

IRS PRIVATE DEBT COLLECTION Executive Summary Introduction Cost Effectiveness Study March 2009 Approach Results Analysis & Findings Appendices TABLE OF CONTENTS Executive Summary 3 I. Introduction 5 II.

North Carolina Department of Revenue. 2012 2013 Collection Strategy

North Carolina Department of Revenue 2012 2013 Collection Strategy 2 0 1 2-1 3 C o l l e c t i o n S t r a t e g y P a g e 2 Table of Contents Table of Contents... 2 Overview... 3 Trends... 3 Account Stratification...

North Carolina Department of Revenue 2012 2013 Collection Strategy 2 0 1 2-1 3 C o l l e c t i o n S t r a t e g y P a g e 2 Table of Contents Table of Contents... 2 Overview... 3 Trends... 3 Account Stratification...

The IRS Resolution Guide for Owner-Operators

The IRS Resolution Guide for Owner-Operators Learn ways to avoid penalties, how the IRS deals with unpaid taxes, the resolution options available, and how to take action to resolve your debt. PRESENTED

The IRS Resolution Guide for Owner-Operators Learn ways to avoid penalties, how the IRS deals with unpaid taxes, the resolution options available, and how to take action to resolve your debt. PRESENTED

Combining Financial Management and Collections to Increase Revenue and Efficiency

Experience the commitment SOLUTION BRIEF FOR CGI ADVANTAGE ERP CLIENTS Combining Financial Management and Collections to Increase Revenue and Efficiency CGI Advantage ERP clients have a unique opportunity

Experience the commitment SOLUTION BRIEF FOR CGI ADVANTAGE ERP CLIENTS Combining Financial Management and Collections to Increase Revenue and Efficiency CGI Advantage ERP clients have a unique opportunity

Governmental Entity Collection Programs Guide Setoff Debt and Government Entity Accounts Receivable (GEAR) SOUTH CAROLINA DEPARTMENT OF REVENUE

SOUTH CAROLINA DEPARTMENT OF REVENUE") Governmental Entity Collection Programs Guide Setoff Debt and Government Entity Accounts Receivable (GEAR) SOUTH CAROLINA DEPARTMENT OF REVENUE MAY 2015 TABLE OF CONTENTS INTRODUCTION... 2 South Carolina

Governmental Entity Collection Programs Guide Setoff Debt and Government Entity Accounts Receivable (GEAR) SOUTH CAROLINA DEPARTMENT OF REVENUE MAY 2015 TABLE OF CONTENTS INTRODUCTION... 2 South Carolina

FEMA Debt Resolution Process: In Summary

FEMA Debt Resolution Process: In Summary After every disaster, FEMA is required to audit disaster assistance payments to ensure taxpayer dollars were properly spent. Those audits often show a small percentage

FEMA Debt Resolution Process: In Summary After every disaster, FEMA is required to audit disaster assistance payments to ensure taxpayer dollars were properly spent. Those audits often show a small percentage

Employment Development Department Accounts Receivable for Benefit Overpayments

Employment Development Department Accounts Receivable for Benefit Overpayments Introduction In addition to collections of the State's employment tax program, the Employment Development Department (EDD

Employment Development Department Accounts Receivable for Benefit Overpayments Introduction In addition to collections of the State's employment tax program, the Employment Development Department (EDD

DET710. A Guide to Tax Resolution: Solving IRS Problems - 12 Hours

DET710 A Guide to Tax Resolution: Solving IRS Problems - 12 Hours Course Objectives and Outline Chapter 1 - IRS Overview and Taxpayer Rights 1. List the mission of the IRS. 2. State the role of Taxpayer

DET710 A Guide to Tax Resolution: Solving IRS Problems - 12 Hours Course Objectives and Outline Chapter 1 - IRS Overview and Taxpayer Rights 1. List the mission of the IRS. 2. State the role of Taxpayer

PRO FAQ. General Overview. Who is Eligible?

PRO FAQ General Overview What is PRO? PRO, or Pay Right OK, is a limited-time opportunity for individuals and businesses to pay past-due tax free of penalty, interest, collection fees and costs without

PRO FAQ General Overview What is PRO? PRO, or Pay Right OK, is a limited-time opportunity for individuals and businesses to pay past-due tax free of penalty, interest, collection fees and costs without

Garnishments Overview. Audio for this session will play through your computer

Garnishments Overview Audio for this session will play through your computer Objective This session is designed to provide an overview of the different types of garnishments that can be assessed against

Garnishments Overview Audio for this session will play through your computer Objective This session is designed to provide an overview of the different types of garnishments that can be assessed against

STATE OF NEW JERSEY DEPARTMENT OF THE TREASURY DIVISION OF TAXATION REQUEST FOR INFORMATION ON TAX DEBT ADMINISTRATION AND RESOLUTION

STATE OF NEW JERSEY DEPARTMENT OF THE TREASURY DIVISION OF TAXATION REQUEST FOR INFORMATION ON TAX DEBT ADMINISTRATION AND RESOLUTION Purpose The Department of the Treasury, Division of Taxation (Taxation)

STATE OF NEW JERSEY DEPARTMENT OF THE TREASURY DIVISION OF TAXATION REQUEST FOR INFORMATION ON TAX DEBT ADMINISTRATION AND RESOLUTION Purpose The Department of the Treasury, Division of Taxation (Taxation)

North Carolina Department of Revenue

Michael F. Easley Governor MEMORANDUM North Carolina Department of Revenue Reginald S. Hinton Secretary TO: The Honorable Marc Basnight Senator John H. Kerr, III President Pro Tempore Revenue Laws Study

Michael F. Easley Governor MEMORANDUM North Carolina Department of Revenue Reginald S. Hinton Secretary TO: The Honorable Marc Basnight Senator John H. Kerr, III President Pro Tempore Revenue Laws Study

DESCRIPTION OF THE CHAIRMAN S MARK OF A PROPOSAL TO CREATE A MILITARY SPOUSE JOB CONTINUITY CREDIT

DESCRIPTION OF THE CHAIRMAN S MARK OF A PROPOSAL TO CREATE A MILITARY SPOUSE JOB CONTINUITY CREDIT Scheduled for Markup by the SENATE COMMITTEE ON FINANCE on February 11, 2015 Prepared by the Staff of

DESCRIPTION OF THE CHAIRMAN S MARK OF A PROPOSAL TO CREATE A MILITARY SPOUSE JOB CONTINUITY CREDIT Scheduled for Markup by the SENATE COMMITTEE ON FINANCE on February 11, 2015 Prepared by the Staff of

Garnishments BEYOND Child Support

Garnishments BEYOND Child Support Agenda Involuntary nta Deductions Federal Tax Levy State Tax Levy Student Loan Creditor Garnishment Bankruptcy 1 Involuntary Deductions Involuntary deductions Neither

Garnishments BEYOND Child Support Agenda Involuntary nta Deductions Federal Tax Levy State Tax Levy Student Loan Creditor Garnishment Bankruptcy 1 Involuntary Deductions Involuntary deductions Neither

Tax Resolution Underwriting Worksheet

Tax Resolution Underwriting Worksheet Office: Tax Consultant: Date: Personal Information Spouse info Taxpayer's name DOB SSN Filing Status (SINGLE, JOINTLY, SEPARATELY) Address Home Phone Number Cell Phone

Tax Resolution Underwriting Worksheet Office: Tax Consultant: Date: Personal Information Spouse info Taxpayer's name DOB SSN Filing Status (SINGLE, JOINTLY, SEPARATELY) Address Home Phone Number Cell Phone

Frequently Asked Questions about Taxes and SSA Disability Benefit Programs

Frequently Asked Questions about Taxes and SSA Disability Benefit Programs January 2010 QUESTION: I have been getting services from my local Work Incentives Planning and Assistance (WIPA) project can my

Frequently Asked Questions about Taxes and SSA Disability Benefit Programs January 2010 QUESTION: I have been getting services from my local Work Incentives Planning and Assistance (WIPA) project can my

Cleveland County Emergency Medical Services. PO Box 1210. Shelby, NC 28151 704-484-4984. Request for Proposal. For. Debt Collection Agency Services

Cleveland County Emergency Medical Services PO Box 1210 Shelby, NC 28151 704-484-4984 Request for Proposal For Debt Collection Agency Services Proposals Must Be Submitted by July 16, 2013 Issue Date: June

Cleveland County Emergency Medical Services PO Box 1210 Shelby, NC 28151 704-484-4984 Request for Proposal For Debt Collection Agency Services Proposals Must Be Submitted by July 16, 2013 Issue Date: June

Mr. Chairman, Senator Levin, and Members of the Subcommittee: Thank you for inviting me to discuss the role of the Financial Management Service

Statement of Commissioner Richard L. Gregg Financial Management Service U.S. Department of the Treasury Before the Permanent Subcommittee on Investigations Senate Committee on Governmental Affairs February

Statement of Commissioner Richard L. Gregg Financial Management Service U.S. Department of the Treasury Before the Permanent Subcommittee on Investigations Senate Committee on Governmental Affairs February

The attached instructions are for employers who have employees that are subject to wage garnishment in connection with the Federal Student Loan

The attached instructions are for employers who have employees that are subject to wage garnishment in connection with the Federal Student Loan Program. 1 THE STUDENT LOAN PROGRAM PROGRAM OVERVIEW The

The attached instructions are for employers who have employees that are subject to wage garnishment in connection with the Federal Student Loan Program. 1 THE STUDENT LOAN PROGRAM PROGRAM OVERVIEW The

North Carolina Department of Revenue

Beverly Eaves Purdue Governor MEMORANDUM North Carolina Department of Revenue Kenneth R. Lay Secretary TO: The Honorable Marc Basnight Senator John H. Kerr, III President Pro Tempore Revenue Laws Study

Beverly Eaves Purdue Governor MEMORANDUM North Carolina Department of Revenue Kenneth R. Lay Secretary TO: The Honorable Marc Basnight Senator John H. Kerr, III President Pro Tempore Revenue Laws Study

Judicial Branch Strategies for Fee and Debt Collections. Legislative Fiscal Committee September 14, 2011

Judicial Branch Strategies for Fee and Debt Collections Legislative Fiscal Committee September 14, 2011 Debt Collection Tools Centralized Collections Unit (CCU) under Iowa Code 602.8107(3) County Attorney

Judicial Branch Strategies for Fee and Debt Collections Legislative Fiscal Committee September 14, 2011 Debt Collection Tools Centralized Collections Unit (CCU) under Iowa Code 602.8107(3) County Attorney

Accounts Receivable Report

Accounts Receivable Report For the Fiscal Year Ended June 30, 2002 Colorado Department of Personnel & Administration Division of Finance and Procurement Office of the State Controller Arthur L. Barnhart,

Accounts Receivable Report For the Fiscal Year Ended June 30, 2002 Colorado Department of Personnel & Administration Division of Finance and Procurement Office of the State Controller Arthur L. Barnhart,

CLIENT SERVICES: Tax Problem Resolution Services

CLIENT SERVICES: Tax Problem Resolution Services Dear Client: Are you having problems with the IRS? We re here to help you resolve your tax problems and put an end to the misery that the IRS can put you

CLIENT SERVICES: Tax Problem Resolution Services Dear Client: Are you having problems with the IRS? We re here to help you resolve your tax problems and put an end to the misery that the IRS can put you

Keep the IRS from Taking Your Paycheck: Guide to Wage Garnishment and How to Stop It 1.866.866.1555. www.toptaxdefenders.com

Keep the IRS from Taking Your Paycheck: Guide to Wage Garnishment and How to Stop It 1.866.866.1555 www.toptaxdefenders.com What You Need to Know about IRS Wage Garnishment When you fall behind on your

Keep the IRS from Taking Your Paycheck: Guide to Wage Garnishment and How to Stop It 1.866.866.1555 www.toptaxdefenders.com What You Need to Know about IRS Wage Garnishment When you fall behind on your

The Announcement provides an overview of the IRS s use of private collection agencies (PCAs) in 2006

in 2006") Part IV- Items of General Interest The Announcement provides an overview of the IRS s use of private collection agencies (PCAs) in 2006 ANNOUNCEMENT 2006-63 Section 881 of the American Jobs Creation Act,

Part IV- Items of General Interest The Announcement provides an overview of the IRS s use of private collection agencies (PCAs) in 2006 ANNOUNCEMENT 2006-63 Section 881 of the American Jobs Creation Act,

PERSONAL INCOME TAXES

Report of the Vermont State Auditor April 18, 2016 PERSONAL INCOME TAXES Department of Taxes Collected About Half of 2013 and 2014 Delinquent PIT, but was Unable to Assess the Effectiveness of Its Collection

Report of the Vermont State Auditor April 18, 2016 PERSONAL INCOME TAXES Department of Taxes Collected About Half of 2013 and 2014 Delinquent PIT, but was Unable to Assess the Effectiveness of Its Collection

Chapter 25 - Payroll. 25.60 Garnishments and Wage Assignments

Chapter 25 - Payroll 25.60 Garnishments and Wage Assignments 25.60.10 Garnishments and levies March 18, 2005 25.60.20 Child Support March 18, 2005 25.60.30 Wage Assignments March 18, 2005 25.60.40 Other

Chapter 25 - Payroll 25.60 Garnishments and Wage Assignments 25.60.10 Garnishments and levies March 18, 2005 25.60.20 Child Support March 18, 2005 25.60.30 Wage Assignments March 18, 2005 25.60.40 Other

This test letter is NOT to be sent to a taxpayer. This text does not appear on production letters.

Letter This test letter is NOT to be sent to a taxpayer. This text does not appear on production letters. Subject: Demand for payment and intent to levy wages This letter is to notify you of a debt referred

Letter This test letter is NOT to be sent to a taxpayer. This text does not appear on production letters. Subject: Demand for payment and intent to levy wages This letter is to notify you of a debt referred

Commissioner. Wage & Investment. Collection Strategy

Commissioner Services & Enforcement Operations Support Small Business- Self Employed Wage & Investment Campus & Call Site Operations Campus & Call Site Operations Field Collection Enterprise Collection

Commissioner Services & Enforcement Operations Support Small Business- Self Employed Wage & Investment Campus & Call Site Operations Campus & Call Site Operations Field Collection Enterprise Collection

SSM Health Policy System Administrative

SSM Health Policy System Administrative TITLE: Billing and Collecting Patient Liabilities OUTCOME STATEMENT: The purpose of this policy is to provide guidelines within SSM Health for billing and collecting

SSM Health Policy System Administrative TITLE: Billing and Collecting Patient Liabilities OUTCOME STATEMENT: The purpose of this policy is to provide guidelines within SSM Health for billing and collecting

Frequently Asked Questions about Taxes and SSA Disability Benefit Programs

Frequently Asked Questions about Taxes and SSA Disability Benefit Programs February 2012 Contributing Authors and Editors: Jim Huston, CPA (Venture Mentors, LLC) and Lucy Miller QUESTION: I have been getting

Frequently Asked Questions about Taxes and SSA Disability Benefit Programs February 2012 Contributing Authors and Editors: Jim Huston, CPA (Venture Mentors, LLC) and Lucy Miller QUESTION: I have been getting

Reporting Requirements & Deadlines for Payroll. Discussions: 9/9/2014. New Hire Reporting. Presented by: Carrie Johnson & Duane Tarrant

Reporting Requirements & Deadlines for Payroll Presented by: Carrie Johnson & Duane Tarrant Discussions: New Hire Reporting Levies & Garnishments Standard Deductions & Voluntary Deductions Direct Deposit

Reporting Requirements & Deadlines for Payroll Presented by: Carrie Johnson & Duane Tarrant Discussions: New Hire Reporting Levies & Garnishments Standard Deductions & Voluntary Deductions Direct Deposit

U.S. Government Receivables and Debt Collection Activities of Federal Agencies

FISCAL YEAR 2011 REPORT TO THE CONGRESS U.S. Government Receivables and Debt Collection Activities of Federal Agencies Department of the Treasury June 2012 department of the treasury washington, dc office

FISCAL YEAR 2011 REPORT TO THE CONGRESS U.S. Government Receivables and Debt Collection Activities of Federal Agencies Department of the Treasury June 2012 department of the treasury washington, dc office

Table of Contents 2016-17 Biennial Budget Revenue, Department of

Table of Contents 2016-17 Biennial Budget Revenue, Department of Agency Profile Revenue, Department of... 1 Tax System Management... 3 Debt Collection... 6 Minnesota Department of Revenue www.revenue.state.mn.us

Table of Contents 2016-17 Biennial Budget Revenue, Department of Agency Profile Revenue, Department of... 1 Tax System Management... 3 Debt Collection... 6 Minnesota Department of Revenue www.revenue.state.mn.us

Don't go it alone* The IRS collection process. pwc. *connectedthinking. Introduction. IRS emphasis on increasing tax collection.

IRS Service Team Don't go it alone* The IRS collection process Introduction Taxpayers periodically request assistance with IRS collection matters. IRS collection contacts can appear intimidating, and taxpayers

IRS Service Team Don't go it alone* The IRS collection process Introduction Taxpayers periodically request assistance with IRS collection matters. IRS collection contacts can appear intimidating, and taxpayers

WAGE WITHHOLDING FOR DEFAULTED STUDENT LOANS A HANDBOOK FOR EMPLOYERS

WAGE WITHHOLDING FOR DEFAULTED STUDENT LOANS A HANDBOOK FOR EMPLOYERS TABLE of CONTENTS A Letter to Employers.3 The Student Loan Program...4 Collection Authority...4 The Basic Steps Employers Follow for

WAGE WITHHOLDING FOR DEFAULTED STUDENT LOANS A HANDBOOK FOR EMPLOYERS TABLE of CONTENTS A Letter to Employers.3 The Student Loan Program...4 Collection Authority...4 The Basic Steps Employers Follow for

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION More Management Information Is Needed to Improve Oversight of Automated Collection System Outbound Calls April 28, 2010 Reference Number: 2010-30-046 This

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION More Management Information Is Needed to Improve Oversight of Automated Collection System Outbound Calls April 28, 2010 Reference Number: 2010-30-046 This

78th OREGON LEGISLATIVE ASSEMBLY--2015 Regular Session. Enrolled. House Bill 2089

78th OREGON LEGISLATIVE ASSEMBLY--2015 Regular Session Enrolled House Bill 2089 Introduced and printed pursuant to House Rule 12.00. Presession filed (at the request of House Interim Committee on Revenue)

78th OREGON LEGISLATIVE ASSEMBLY--2015 Regular Session Enrolled House Bill 2089 Introduced and printed pursuant to House Rule 12.00. Presession filed (at the request of House Interim Committee on Revenue)

GAO. TAX DEBT COLLECTION Measuring Taxpayer Opinions Regarding Private Collection Agencies

GAO United States Government Accountability Office Testimony Before the Committee on Ways and Means, House of Representatives For Release on Delivery Expected at 10:00 a.m. EDT Wednesday, May 23, 2007

GAO United States Government Accountability Office Testimony Before the Committee on Ways and Means, House of Representatives For Release on Delivery Expected at 10:00 a.m. EDT Wednesday, May 23, 2007

The Case for Centralized Collections

Experience the commitment ISSUE PAPER The Case for Centralized Collections This paper reviews the key drivers, considerations and benefits of centralizing the debt collection function at the national,

Experience the commitment ISSUE PAPER The Case for Centralized Collections This paper reviews the key drivers, considerations and benefits of centralizing the debt collection function at the national,

Version Date: 10/16/2013

2004094 Accounting Documents (ADVANTAGE Financial System Input) This record series is used to input information into the ADVANTAGE Financial System. The files may contain, but are not limited to: copies

2004094 Accounting Documents (ADVANTAGE Financial System Input) This record series is used to input information into the ADVANTAGE Financial System. The files may contain, but are not limited to: copies

PURPOSE: SCOPE: DEFINITIONS:

PURPOSE: To establish procedures regarding collection of patient accounts including external collection agencies and potential legal actions balancing the need for financial stewardship with needs of individual

PURPOSE: To establish procedures regarding collection of patient accounts including external collection agencies and potential legal actions balancing the need for financial stewardship with needs of individual

Matthew Von Schuch. Tax Attorney and CPA

Matthew Von Schuch Tax Attorney and CPA 7 METHODS TO RESOLVE IRS TAX DEBT Offer in Compromise Settling tax debt for less than owed Installment Agreement A payment plan for tax debts Non- Collectable Status

Matthew Von Schuch Tax Attorney and CPA 7 METHODS TO RESOLVE IRS TAX DEBT Offer in Compromise Settling tax debt for less than owed Installment Agreement A payment plan for tax debts Non- Collectable Status

Legal Aid Society of Orange County Low Income Taxpayer Clinic

Legal Aid Society of Orange County Low Income Taxpayer Clinic Presented by: Renato L. Izquieta, Esq. Legal Aid Society of Orange County Presented by: Richard Silva, Paralegal Legal Aid Society of Orange

Legal Aid Society of Orange County Low Income Taxpayer Clinic Presented by: Renato L. Izquieta, Esq. Legal Aid Society of Orange County Presented by: Richard Silva, Paralegal Legal Aid Society of Orange

St. Elizabeth Healthcare - Billing and Collection Policy

St. Elizabeth Healthcare - Billing and Collection Policy Policy After our patients have received services, it is the policy of St. Elizabeth Healthcare to bill patients and applicable payers accurately

St. Elizabeth Healthcare - Billing and Collection Policy Policy After our patients have received services, it is the policy of St. Elizabeth Healthcare to bill patients and applicable payers accurately

DESCRIPTION OF THE CHAIRMAN S MARK RELATING TO MODIFICATIONS TO ALTERNATIVE TAX FOR CERTAIN SMALL INSURANCE COMPANIES

DESCRIPTION OF THE CHAIRMAN S MARK RELATING TO MODIFICATIONS TO ALTERNATIVE TAX FOR CERTAIN SMALL INSURANCE COMPANIES Scheduled for Markup by the SENATE COMMITTEE ON FINANCE on February 11, 2015 Prepared

DESCRIPTION OF THE CHAIRMAN S MARK RELATING TO MODIFICATIONS TO ALTERNATIVE TAX FOR CERTAIN SMALL INSURANCE COMPANIES Scheduled for Markup by the SENATE COMMITTEE ON FINANCE on February 11, 2015 Prepared

Representing Clients in Collection Due Process Hearings

Representing Clients in Collection Due Process Hearings Prepared by The Community Tax Law Project 2006 A substantial number of the Community Tax Law Project s cases involve collection activity by the IRS

Representing Clients in Collection Due Process Hearings Prepared by The Community Tax Law Project 2006 A substantial number of the Community Tax Law Project s cases involve collection activity by the IRS

New. INHS will make best efforts to obtain cost reimbursement for any portion of uncollectible bad debt attributable to Medicare beneficiaries.

Subject: Collection Policy & Assignment Department: Revenue Cycle Executive Sponsor: Helen Andrus, CFO Approved by: INHS Leadership Policy Number: INHS-PFS-001 New Date: 12/01/2015 Revised Reviewed Policy

Subject: Collection Policy & Assignment Department: Revenue Cycle Executive Sponsor: Helen Andrus, CFO Approved by: INHS Leadership Policy Number: INHS-PFS-001 New Date: 12/01/2015 Revised Reviewed Policy

State of Iowa Offset Program. Department of Administrative Services State Accounting Enterprise

State of Iowa Offset Program Department of Administrative Services State Accounting Enterprise Offset Program City Participation -Overview -Participation -Vendor Offsets -Tax Offsets -Questions 2 Function

State of Iowa Offset Program Department of Administrative Services State Accounting Enterprise Offset Program City Participation -Overview -Participation -Vendor Offsets -Tax Offsets -Questions 2 Function

NASA Financial Management Requirements Volume 11, Chapter 7 Effective: September 2008 Expiration: September 2013

CHAPTER 7. WITHHOLDING DEDUCTIONS FROM GROSS PAY TABLE OF CONTENTS 7.1 POLICY....7-1 7.2 AUTHORIZATION...7-1 7.3 TYPES OF DEDUCTIONS...7-1 7.4 ORDER OF WITHHOLDING PREFERENCE FOR DEDUCTIONS...7-2 7.5 OTHER

CHAPTER 7. WITHHOLDING DEDUCTIONS FROM GROSS PAY TABLE OF CONTENTS 7.1 POLICY....7-1 7.2 AUTHORIZATION...7-1 7.3 TYPES OF DEDUCTIONS...7-1 7.4 ORDER OF WITHHOLDING PREFERENCE FOR DEDUCTIONS...7-2 7.5 OTHER

Revenue en e Solutions, Inc. Top Ten Compliance Programs to Drive Revenue

Revenue en e Solutions, Inc. Top Ten Compliance Programs to Drive Revenue Presentation for: Federation of Tax Administrators Solution Track Series June 2009 Introductions Paul Panariello Co-founder of

Revenue en e Solutions, Inc. Top Ten Compliance Programs to Drive Revenue Presentation for: Federation of Tax Administrators Solution Track Series June 2009 Introductions Paul Panariello Co-founder of

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION Reducing the Processing Time Between Balance Due Notices Could Increase Collections September 26, 2011 Reference Number: 2011-30-112 This report has cleared

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION Reducing the Processing Time Between Balance Due Notices Could Increase Collections September 26, 2011 Reference Number: 2011-30-112 This report has cleared

IRS Tax Resolution. Course #5730B/QAS5730B Exam Packet

IRS Tax Resolution Course #5730B/QAS5730B Exam Packet IRS TAX RESOLUTION (COURSE #5730B/QAS5730B) COURSE DESCRIPTION AND INTRODUCTION Tax resolution means providing solutions to businesses and individuals

IRS Tax Resolution Course #5730B/QAS5730B Exam Packet IRS TAX RESOLUTION (COURSE #5730B/QAS5730B) COURSE DESCRIPTION AND INTRODUCTION Tax resolution means providing solutions to businesses and individuals

Appendix to CGI s A proven path to improving government debt collection issue paper

Appendix to CGI s A proven path to improving government debt collection issue paper SAMPLE COLLECTION STATUTES This appendix contains the following sample collection statutes: Kentucky Financial Institution

Appendix to CGI s A proven path to improving government debt collection issue paper SAMPLE COLLECTION STATUTES This appendix contains the following sample collection statutes: Kentucky Financial Institution

TOPIC NO. 50405 TOPIC Court-Ordered Withholdings Table of Contents

Table of Contents Overview... 3 Introduction... 3 Disclaimer... 3 Definitions... 4 Applicable Laws... 5 Honoring the Garnishment... 6 Garnishments on Work Study Payments... 7 Garnishment Fee... 7 Deduction

Table of Contents Overview... 3 Introduction... 3 Disclaimer... 3 Definitions... 4 Applicable Laws... 5 Honoring the Garnishment... 6 Garnishments on Work Study Payments... 7 Garnishment Fee... 7 Deduction

DEPARTMENT OF DEFENSE DEFENSE OFFICE OF HEARINGS AND APPEALS

DEPARTMENT OF DEFENSE DEFENSE OFFICE OF HEARINGS AND APPEALS In the matter of: ) ) ------------------------ ) ISCR Case No. 07-02458 SSN: ----------- ) ) Applicant for Security Clearance ) Appearances

DEPARTMENT OF DEFENSE DEFENSE OFFICE OF HEARINGS AND APPEALS In the matter of: ) ) ------------------------ ) ISCR Case No. 07-02458 SSN: ----------- ) ) Applicant for Security Clearance ) Appearances

Mechanic s Liens. Colorado Revised Statutes, Section 38-22-101

This handout is intended as general information only, and not as legal advice for any specific situation. If you have a legal problem, you may want to check with an attorney. What is a Mechanic s Lien?

This handout is intended as general information only, and not as legal advice for any specific situation. If you have a legal problem, you may want to check with an attorney. What is a Mechanic s Lien?

PATIENT COLLECTION. Account An account receivable based on services furnished by Aurora.

Policy No: 245 Effective Date: 01/01/14 (all encounters from that date forward) Revision Dates: 12/15 1. Purpose 2. Scope PATIENT COLLECTION Aurora Health Care, Inc. and its affiliates (collectively Aurora

Policy No: 245 Effective Date: 01/01/14 (all encounters from that date forward) Revision Dates: 12/15 1. Purpose 2. Scope PATIENT COLLECTION Aurora Health Care, Inc. and its affiliates (collectively Aurora

GAO TAX ADMINISTRATION. Federal Payment Levy Program Measures, Performance, and Equity Can Be Improved. Report to Congressional Requesters

GAO United States General Accounting Office Report to Congressional Requesters March 2003 TAX ADMINISTRATION Federal Payment Levy Program Measures, Performance, and Equity Can Be Improved GAO-03-356 March

GAO United States General Accounting Office Report to Congressional Requesters March 2003 TAX ADMINISTRATION Federal Payment Levy Program Measures, Performance, and Equity Can Be Improved GAO-03-356 March

UAN File (Or other software vendor) 3/12/2015. How to Organize Your Files. Not requirements Other methods may be used

3/12/2015. How to Organize Your Files. Not requirements Other methods may be used") How to Organize Your Files Presented by: Trina Martin UAN Project Accountant Tips For Organization Not requirements Other methods may be used 2 UAN File (Or other software vendor) UAN User Agreement Correspondence

How to Organize Your Files Presented by: Trina Martin UAN Project Accountant Tips For Organization Not requirements Other methods may be used 2 UAN File (Or other software vendor) UAN User Agreement Correspondence

Collection Technology and Automation

Collection Technology and Automation Field Collection 2 Western Area Collection Alaska Washington Idaho Montana Oregon Wyoming Northern California Nevada Utah Colorado International 3 Predictive Analytics

Collection Technology and Automation Field Collection 2 Western Area Collection Alaska Washington Idaho Montana Oregon Wyoming Northern California Nevada Utah Colorado International 3 Predictive Analytics

A proven path for improving government debt collection

Experience the commitment ISSUE PAPER A proven path for improving government debt collection This issue paper describes a proven path to maximizing revenue collection using modern tools and techniques,

Experience the commitment ISSUE PAPER A proven path for improving government debt collection This issue paper describes a proven path to maximizing revenue collection using modern tools and techniques,

The Johns Hopkins Health System Policy & Procedure. SELF-PAY COLLECTIONS Revised 2/25/08 POLICY

Page 1 of 8 POLICY This policy applies to The Johns Hopkins Health System Corporation (JHHS) and the following affiliated entities: The Johns Hopkins Hospital (JHH), Johns Hopkins Bayview Medical Center,

Page 1 of 8 POLICY This policy applies to The Johns Hopkins Health System Corporation (JHHS) and the following affiliated entities: The Johns Hopkins Hospital (JHH), Johns Hopkins Bayview Medical Center,

U.S. Department of Treasury Offset Program (TOP)

") U.S. Department of Treasury Offset Program (TOP) The Treasury Offset Program (TOP) enables the U.S. Department of Treasury to reduce or withhold any of your eligible federal income tax refund by the amount

U.S. Department of Treasury Offset Program (TOP) The Treasury Offset Program (TOP) enables the U.S. Department of Treasury to reduce or withhold any of your eligible federal income tax refund by the amount

DESCRIPTION OF THE CHAIRMAN S MARK OF A PROPOSAL TO CLARIFY SPECIAL RULE FOR CERTAIN GOVERNMENTAL PLANS

DESCRIPTION OF THE CHAIRMAN S MARK OF A PROPOSAL TO CLARIFY SPECIAL RULE FOR CERTAIN GOVERNMENTAL PLANS Scheduled for Markup by the SENATE COMMITTEE ON FINANCE on February 11, 2015 Prepared by the Staff

DESCRIPTION OF THE CHAIRMAN S MARK OF A PROPOSAL TO CLARIFY SPECIAL RULE FOR CERTAIN GOVERNMENTAL PLANS Scheduled for Markup by the SENATE COMMITTEE ON FINANCE on February 11, 2015 Prepared by the Staff

This Offer in Compromise package includes: Information you need to know before submitting an offer in compromise

www.irs.gov Form 656 (Rev. 5-2001) Catalog Number 16728N Form 656 Offer in Compromise This Offer in Compromise package includes: Information you need to know before submitting an offer in compromise Instructions

www.irs.gov Form 656 (Rev. 5-2001) Catalog Number 16728N Form 656 Offer in Compromise This Offer in Compromise package includes: Information you need to know before submitting an offer in compromise Instructions

Procedure for Completing IRS Form 2159 Payroll Deduction Agreement

Updated 06.19.13 IRS Form 2159 PAYROLL JOB AID COMPLETING IRS FORM 2159 PAYROLL DEDUCTION AGREEMENT FOR STATE OF NC EMPLOYEES/EMPLOYERS General Information PROCESS TITLE: Procedure for Completing IRS Form

Updated 06.19.13 IRS Form 2159 PAYROLL JOB AID COMPLETING IRS FORM 2159 PAYROLL DEDUCTION AGREEMENT FOR STATE OF NC EMPLOYEES/EMPLOYERS General Information PROCESS TITLE: Procedure for Completing IRS Form

ACCOUNTING POLICY AND PROCEDURES (APP) MANUAL. TOPIC: Section 4 Receivables 2.0 EFFECTIVE DATE: 12/05/1994

MANUAL. TOPIC: Section 4 Receivables 2.0 EFFECTIVE DATE: 12/05/1994") STATE OF WISCONSIN DEPARTMENT OF HEALTH SERVICES DIVISION OF ENTERPRISE SERVICES BUREAU OF FISCAL SERVICES ACCOUNTING POLICY AND PROCEDURES (APP) MANUAL TOPIC: Section 4 Receivables 2.0 EFFECTIVE DATE:

STATE OF WISCONSIN DEPARTMENT OF HEALTH SERVICES DIVISION OF ENTERPRISE SERVICES BUREAU OF FISCAL SERVICES ACCOUNTING POLICY AND PROCEDURES (APP) MANUAL TOPIC: Section 4 Receivables 2.0 EFFECTIVE DATE:

The IRS Private Debt Collection Program A Comparison of Private Sector and IRS Collections While Working Private Collection Agency Inventory

The IRS Private Debt Program A Comparison of Private Sector and IRS s While Working Private Agency Inventory SECTION SIX Penalties and Private Debt The IRS Private Debt Program A Comparison of Private

The IRS Private Debt Program A Comparison of Private Sector and IRS s While Working Private Agency Inventory SECTION SIX Penalties and Private Debt The IRS Private Debt Program A Comparison of Private

DESCRIPTION OF THE CHAIRMAN S MARK OF A PROPOSAL FOR A WASTE-HEAT-TO-POWER INVESTMENT TAX CREDIT

DESCRIPTION OF THE CHAIRMAN S MARK OF A PROPOSAL FOR A WASTE-HEAT-TO-POWER INVESTMENT TAX CREDIT Scheduled for Markup by the SENATE COMMITTEE ON FINANCE on February 11, 2015 Prepared by the Staff of the

DESCRIPTION OF THE CHAIRMAN S MARK OF A PROPOSAL FOR A WASTE-HEAT-TO-POWER INVESTMENT TAX CREDIT Scheduled for Markup by the SENATE COMMITTEE ON FINANCE on February 11, 2015 Prepared by the Staff of the

Inside the SC DOR Data Warehouse Project

Inside the SC DOR Data Warehouse Project Presented by: Terry Garber, New Applications Manager, South Carolina DOR Paul Morris, Director, Revenue Solutions, Inc. (RSI) Agenda Introduction Project Overview

Inside the SC DOR Data Warehouse Project Presented by: Terry Garber, New Applications Manager, South Carolina DOR Paul Morris, Director, Revenue Solutions, Inc. (RSI) Agenda Introduction Project Overview

KENTUCKY DEPARTMENT OF REVENUE OFFER IN SETTLEMENT APPLICATION CHECKLIST. Form 12A018 (08/12)

") CHECKLIST I. BEFORE COMPLETING THE APPLICATION, PLEASE VERIFY THAT YOU ARE ELIGIBLE TO SUBMIT AN OFFER IN SETTLEMENT! Check (a) or (b) to each question below. If you check (a), you may proceed to the next

CHECKLIST I. BEFORE COMPLETING THE APPLICATION, PLEASE VERIFY THAT YOU ARE ELIGIBLE TO SUBMIT AN OFFER IN SETTLEMENT! Check (a) or (b) to each question below. If you check (a), you may proceed to the next

A Assets and Other Debits: Code and Definitions 2-A-1. B Liabilities and Other Credits: Code and Definitions 2-B-1

Section: Chapter Contents Date: June 006 Section Page A Assets and Other Debits: Code and Definitions -A-1 B Liabilities and Other Credits: Code and Definitions -B-1 NOTE 1: In order to maintain uniformity

Section: Chapter Contents Date: June 006 Section Page A Assets and Other Debits: Code and Definitions -A-1 B Liabilities and Other Credits: Code and Definitions -B-1 NOTE 1: In order to maintain uniformity

Don t get discouraged if you are in default on your federal student loan.

visited on Page 1 of 7 Menu Home» How to Repay Your Loans» Understanding Default» Getting out of Default Don t get discouraged if you are in default on your federal student loan. Options for getting out

visited on Page 1 of 7 Menu Home» How to Repay Your Loans» Understanding Default» Getting out of Default Don t get discouraged if you are in default on your federal student loan. Options for getting out

Garnishments A-Z: An In-depth Look at Federal and Illinois Garnishment Law

Garnishments A-Z: An In-depth Look at Federal and Illinois Garnishment Law Chicago Chapter of American Payroll Association June 14, 2013 Presented By: Robert McCabe James D. Rock Ancel, Glink, Diamond,

Garnishments A-Z: An In-depth Look at Federal and Illinois Garnishment Law Chicago Chapter of American Payroll Association June 14, 2013 Presented By: Robert McCabe James D. Rock Ancel, Glink, Diamond,

The Next Generation of Government Debt Collection Practices

Experience the commitment ISSUE PAPER The Next Generation of Government Debt Collection Practices This issue paper provides an overview of current and emerging best practices in government debt collections.

Experience the commitment ISSUE PAPER The Next Generation of Government Debt Collection Practices This issue paper provides an overview of current and emerging best practices in government debt collections.

Sure and Secure IRS Resolution Services

Sure and Secure IRS Resolution Services Enrolled Agent - Representation What is an Enrolled Agent? An Enrolled Agent (EA) is a federally-authorized tax practitioner who has technical expertise in the field

Sure and Secure IRS Resolution Services Enrolled Agent - Representation What is an Enrolled Agent? An Enrolled Agent (EA) is a federally-authorized tax practitioner who has technical expertise in the field

CACalifornia Taxpayers Bill of Rights

CACalifornia Taxpayers Bill of Rights Inside 01 Taxpayers Bill of Rights legislation enacted 1988 02 Taxpayers Bill of Rights legislation enacted 1997 Information for Taxpayers» 03 California Taxpayers

CACalifornia Taxpayers Bill of Rights Inside 01 Taxpayers Bill of Rights legislation enacted 1988 02 Taxpayers Bill of Rights legislation enacted 1997 Information for Taxpayers» 03 California Taxpayers

WAGE WITHHOLDING FOR DEFAULTED STUDENT LOANS A HANDBOOK FOR EMPLOYERS. Revised June 18, 2008

WAGE WITHHOLDING FOR DEFAULTED STUDENT LOANS A HANDBOOK FOR EMPLOYERS Revised June 18, 2008 TABLE of CONTENTS A Letter to Employers..3 The Student Loan Program.4-5 The Basic Steps Employers Follow for

WAGE WITHHOLDING FOR DEFAULTED STUDENT LOANS A HANDBOOK FOR EMPLOYERS Revised June 18, 2008 TABLE of CONTENTS A Letter to Employers..3 The Student Loan Program.4-5 The Basic Steps Employers Follow for

GAO TAX COMPLIANCE. Businesses Owe Billions in Federal Payroll Taxes. Report to Congressional Committees

GAO United States Government Accountability Office Report to Congressional Committees July 2008 TAX COMPLIANCE Businesses Owe Billions in Federal Payroll Taxes On December 19, 2008, the PDF file was revised

GAO United States Government Accountability Office Report to Congressional Committees July 2008 TAX COMPLIANCE Businesses Owe Billions in Federal Payroll Taxes On December 19, 2008, the PDF file was revised

Title 35 Mississippi State Tax Commission. Part I Administrative

1 Title 35 Mississippi State Tax Commission Formatted Part I Administrative Chapter 05: Collection Procedures for Levy of Monies 100 Purpose This regulation is promulgated to established a uniform method

1 Title 35 Mississippi State Tax Commission Formatted Part I Administrative Chapter 05: Collection Procedures for Levy of Monies 100 Purpose This regulation is promulgated to established a uniform method

Report to the General Assembly on the Enhanced Revenue Collection Account June 1, 2015

Report to the General Assembly on the Enhanced Revenue Collection Account June 1, 2015 Pennsylvania Department of Revenue Bureau of Research Introduction and Background Act 46 of 2010 created the Enhanced

Report to the General Assembly on the Enhanced Revenue Collection Account June 1, 2015 Pennsylvania Department of Revenue Bureau of Research Introduction and Background Act 46 of 2010 created the Enhanced

PRESENT LAW AND BACKGROUND RELATING TO PERMITTING PRIVATE SECTOR DEBT COLLECTION COMPANIES TO COLLECT TAX DEBTS

Joint Committee on Taxation May 12, 2003 JCX-49-03 PRESENT LAW AND BACKGROUND RELATING TO PERMITTING PRIVATE SECTOR DEBT COLLECTION COMPANIES TO COLLECT TAX DEBTS Scheduled for a Public Hearing Before

Joint Committee on Taxation May 12, 2003 JCX-49-03 PRESENT LAW AND BACKGROUND RELATING TO PERMITTING PRIVATE SECTOR DEBT COLLECTION COMPANIES TO COLLECT TAX DEBTS Scheduled for a Public Hearing Before

RULE 90 GARNISHMENTS AND SEQUESTRATION. (c) A "garnishee" is the person summoned as garnishee in the writ of garnishment or

A garnishee is the person summoned as garnishee in the writ of garnishment or") RULE 90 GARNISHMENTS AND SEQUESTRATION 90.01 DEFINITIONS In this Rule 90: (a) A "garnishor" is a judgment creditor; (b) A "debtor" is a judgment debtor; (c) A "garnishee" is the person summoned as garnishee

RULE 90 GARNISHMENTS AND SEQUESTRATION 90.01 DEFINITIONS In this Rule 90: (a) A "garnishor" is a judgment creditor; (b) A "debtor" is a judgment debtor; (c) A "garnishee" is the person summoned as garnishee

Statement of National Treasury Employees Union

Statement of National Treasury Employees Union On Examining potential reforms to ensure federal employees and contractors satisfy in good faith their financial obligations, including federal taxes Presented

Statement of National Treasury Employees Union On Examining potential reforms to ensure federal employees and contractors satisfy in good faith their financial obligations, including federal taxes Presented

Federal Stafford Loan Counseling Checklist

Student s Name (Please Print) Social Security Number You are receiving a Federal Stafford loan to help you cover the costs of your education. You must repay this loan. Before you receive your Stafford

Student s Name (Please Print) Social Security Number You are receiving a Federal Stafford loan to help you cover the costs of your education. You must repay this loan. Before you receive your Stafford

IRS FULL SERVICE COLLECTION

4DM 585 1 of 7 IRS FULL SERVICE COLLECTION REGULATION Definition Enforcement Tool Request IRS Full Service Collection is a method of collection which uses the full powers of the Internal Revenue Service

4DM 585 1 of 7 IRS FULL SERVICE COLLECTION REGULATION Definition Enforcement Tool Request IRS Full Service Collection is a method of collection which uses the full powers of the Internal Revenue Service

A. We will automatically withhold the following taxes from these supplemental payments:

Frequently Asked Questions on Pay-Related Aspects of Your Voluntary Separation incentive Payment (VSIP/Buyout) Prepared by the GSA National Payroll Center, Kansas City, MO. Q-1. The Human Resources Office

Frequently Asked Questions on Pay-Related Aspects of Your Voluntary Separation incentive Payment (VSIP/Buyout) Prepared by the GSA National Payroll Center, Kansas City, MO. Q-1. The Human Resources Office

OPERATIONS MEMO For Public Release

State Board of Equalization OPERATIONS MEMO For Public Release No. : 1170 Date : February 22, 2011 SUBJECT: Procedures for Releasing or Modifying a Notice of Levy I. PURPOSE The following are guidelines

State Board of Equalization OPERATIONS MEMO For Public Release No. : 1170 Date : February 22, 2011 SUBJECT: Procedures for Releasing or Modifying a Notice of Levy I. PURPOSE The following are guidelines

Your tax return can be filed electronically so you will get your refund in 7 10 business days.

Tax Services Tax Preparation Preparing your own income tax return can be a task that leaves you with more questions than answers. According to a study released by the US Government's General Accounting

Tax Services Tax Preparation Preparing your own income tax return can be a task that leaves you with more questions than answers. According to a study released by the US Government's General Accounting

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION Revenue Officers Took Appropriate Levy Actions but Face Challenges and Delays Bringing Taxpayers Into Compliance November 21, 2011 Reference Number: 2012-30-007

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION Revenue Officers Took Appropriate Levy Actions but Face Challenges and Delays Bringing Taxpayers Into Compliance November 21, 2011 Reference Number: 2012-30-007