Financial Management and Legislative Briefing

|

|

|

- Eric Daniels

- 10 years ago

- Views:

Transcription

1 MNDOT FINANCIAL MANAGEMENT AND LEGISLATIVE BRIEFING 2014 MARCH 2014 Financial Management and Legislative Briefing The Office of Financial Management prepared this financial management and legislative briefing to provide basic information on the Minnesota Department of Transportation s (MnDOT) finances. The first section describes MnDOT s capital and supplemental budget request for consideration by the 2014 Legislature, and a summary of MnDOT s proposed 2014 legislative policy initiatives. The second section provides a basic MnDOT financial overview. It includes information about how highway transportation is funded in Minnesota, and includes a history of significant revenue changes. The appendix includes fund statements for the six transportation funds, and financial data which include FY2013 overviews of MnDOT revenues and expenditures. Crews plow Hwy 28 west of Sauk Centre. Photo courtesy of District 3. Comments? This briefing was prepared by MnDOT s Office of Financial Management with writing, data, and analysis from Bruce Briese, Lynn Poirier, Kristi Schroedl, Robyn Rupp, Kim Kildal, Josh Knatterud-Hubinger and Maureen Newville. Please contact Lynn Poirier ([email protected]) with questions, comments, or suggestions. Contents Transportation Facts 2 SECTION 1 FY2014 Capital Budget 3 FY 2014 Supplemental Budget Direct Appropriations Summary Legislative Policy Initiatives 8 SECTION 2 MN Highway Finances 10 History of HUTD Revenue 13 APPENDIX 17 Fund Statements: Highway User Tax Distr. 2 Trunk Highway 1 Transit Assistance 2 State Airports 1 County State Aid Hwy. 1 Municipal State Aid St. 2 VMT and Fuel Trends 24 Transportation Funding 25 Revenue and Expenditures for transportation purposes, (Flowchart) FY Governor s Recommendation 2014 February Forecast

2 TRANSPORTATION FACTS MOTOR VEHICLE REGISTRATIONS: Minnesota s motor vehicle registrations totaled about 5.02 million in AERONAUTICS: Minnesota has 5,152 active registered aircraft and 135 public airports. 3) LICENSED DRIVERS: Minnesota had 4.04 million licensed drivers in SEAT BELT USAGE Minnesota s seat belt usage was 94% in VEHICLE MILES TRAVELED: Use of Minnesota s roads totaled an estimated 56.9 billion vehicle miles traveled in TRANSIT: Use of Minnesota transit systems totaled million transit trips in ) MnDOT Office of Transit RAIL SYSTEM: Minnesota s rail system consists of about 4,388 total miles of railroad, with 4,119 rail crossings. WATERWAYS: The Mississippi River System stretches over 222 miles in Minnesota. The five ports on this river plus four ports on Lake Superior transported a combined tonnage of 71.7 million tons. 4) In 2012, Minnesota shipped over 4.4 million tons of grain down the Mississippi. BICYCLE TRAILS: The State Trails system includes 1,323 developed state trail miles, of which 620 miles are paved for bicycling and other uses. 2) Unless otherwise noted; all facts are from 2012 Transportation Trivia, compiled by Office of Traffic Engineering at 1) MnDOT Office of Transit 2) 3) 4) DNR Division of Parks and Trails MnDOT Office of Aeronautics no longer includes antiques or registered non-flyables. MnDOT Ports and Waterways websitehttp:// Page 2

3 CAPITAL BUDGET GOVERNOR S RECOMMENDATIONS FOR THE 2014 LEGISLATIVE SESSION The Governor proposes a capital budget in even-numbered years. These typically involve requests for state bonding and non-bond funds for various infrastructure projects. State agencies and local governments submit requests to Minnesota Management and Budget (MMB), which advises the Governor and assists with deciding which projects are to be included in the Governor s recommendation. As part of this process, MnDOT submits its requests, which totaled approximately $344 million in 2014 for various building projects, local bridge bonding, local road improvement grants, railroad grade warning devices replacement, port development assistance, greater Minnesota transit facilities, and the safe routes to school program. The paragraphs below describe the projects approved by the Governor for MnDOT, as well as transportation-related projects for three local recommended projects where the funding will flow though MnDOT. Items described below have been introduced and are included in the Governor s bonding bill (House File 2490 and Senate File 2605). MNDOT CAPITAL PROJECTS LOCAL BRIDGE REPLACEMENT PROGRAM $30,000,000 General Obligation Bonds This request is for state funds to replace or rehabilitate deficient bridges owned by local governments throughout the state. State bridge replacement funds are used in two ways. The first is to leverage or supplement other types of bridge replacement funding such as federal aid, state aid, and township bridge funds. The second is to provide funds for bridges that have no other source of federal aid or state aid funds. improvement projects. This account provides funding for projects on county state-aid highways intended to reduce traffic crashes, deaths, injuries, and property damage. This funding would be administered in accordance with M.S MNDOT FACILITIES: LOCAL ROAD IMPROVEMENT PROGRAM $10,000,000 General Obligation Bonds This request is to provide additional funding assistance to local governments for construction, reconstruction, or reconditioning projects on local roads with statewide or regional significance. Also, it would assist in paying the costs of rural road safety capital WILLMAR DISTRICT HEADQUARTERS $4,370,000 Trunk Highway (TH) Cash This is to provide additional funding to complete the project originally authorized in the 2012 capital budget for $7,500,000. LITTLE FALLS TRUCK STATION $3,580,000 Trunk Highway (TH) Cash This is to provide additional funding to complete the project originally authorized in the 2010 capital budget for $3,300,000. Page 3

4 MODAL INVESTMENTS: GREATER MINNESOTA TRANSIT $1,130, 000 General Obligation Bonds This request is intended to fund the St. Cloud Metro Bus Operations Center, Vehicle Storage Addition, and Improvements. SAFE ROUTES TO SCHOOLS (SRTS) $2,000,000 General Obligation Bonds This request would provide grants to schools, in partnership with cities and counties, for infrastructure that improves safety or access for children walking and bicycling to school. would replace approximately 8 aging highway/rail grade crossing safety gate and signal warning systems. TOTAL MNDOT GOVERNOR S RECOMMENDATION: The total MnDOT amount for the projects described above is $53,480,000. The total recommended budget would be funded from the sources shown below: General Obligation Bonds $45,530,000 Trunk Highway Fund Cash $7,950,000 PORT DEVELOPMENT ASSISTANCE $400,000 General Obligation Bonds This request is to provide funding for the Heavy Lift Dock Capacity project in Winona. Non-MnDOT Transportation- Related Projects In addition to the amounts recommended for MnDOT, three other transportation projects would be appropriated to MnDOT as local capital projects. The Governor is recommending $36 million of funding, using General Obligation bonds for the transportation-related projects listed below: $5 million for the Iron Range Regional Airport $2 million for the Falls International Airport RAILROAD GRADE WARNING DEVICES REPLACEMENT $2,000,000 General Obligation Bonds This request is to provide additional funding assistance to MnDOT for replacing aging railroad highway grade crossings signals through a statewide life cycle planning process. This funding $29 million for Ramsey County Twin City Army Ammunition Plant (TCAAP) redevelopment project In addition the governor also recommended $5 million for the Department of Employment and Economic Development (DEED) for the Transportation Economic Development (TED) program, which is jointly administered by DEED and MnDOT. Page 4

5 Minnesota Department of Transportation FY 2014 Capital Budget - Projects Summary Project Funding Summary ($ in Thouands) Agency Request Governor's Rec Governor's Planning Estimates Project Title Agency Funding Priority Source Local Bridge Replacement Program 1 GO $ 75,000 $ 75,000 $ 75,000 $ 30,000 $ 30,000 $ 30,000 Local Road Improvement Fund Grants 3 GO 100, , ,000 10,000 10,000 10,000 Greater MN Transit Facilities 2 GO 1,130 5,000 5,000 1, Highway/Railroad Grade Crossing Warning Devices Replacement 4 GO 10,000 10,000 10,000 2,000 2,000 2,000 Willmar Headquarters Supplemental Funding 5 THF 4, , Little Falls Truck Station Supplemental Funding 6 THF 3,580 3,580 Safe Routes To School 7 GO 3,200 6,000 6,000 2,000 2,000 2,000 Rail Service Improvements 8 GO 10,000 10,000 10,000 - Port Development Assistance 9 GO 10,000 10,000 10, High Speed Corridor Match 10 GO 27,000 27,200 27,200 - Supplemental Funding For Turnbacks 11 GO 100, , ,000 - Total Project Funding General Fund General Obligation Bonds (GO) Trunk Highway Fund Cash (THF) $ 344,280 $ 343,200 $ 343,200 $ 53,480 $ 44,000 $ 44,000 $ 336,330 $ 343,200 $ 343,200 $ 45,530 $ 44,000 $ 44,000 $ 7,950 $ - $ - $ 7,950 $ - $ - Page 5

6 2014 SUPPLEMENTAL BUDGET During even-numbered years state agencies are permitted to submit supplemental budget requests to address issues that have occurred since passage of the biennial budget enacted in the previous legislative session. These requests may result from funding changes, as indicated in the February forecast or funding needs previously unanticipated. MnDOT has proposed a number of initiatives in its supplemental budget request. The paragraphs below describe the supplemental funding requests approved by the Governor for MnDOT. These recommendations impact the Trunk Highway Fund, the County State Aid Highway Fund (an increase in transfer from Flexible Highway Account), and the State Airports Fund. The supplemental funding bill has not been introduced at the time of this publication. OPERATIONS AND MAINTENANCE INVESTMENTS The Governor recommends a $5 million trunk highway fund base increase in 2014 to accelerate the replacement of snow plow equipment from a 20 year average to a more appropriate 14 year average. A $16 million one-time trunk highway appropriation in 2015 is also recommended for snow and ice support equipment, LED lighting on trunk highways, enhanced patching methods, changeable message signs, detection devices, and enhanced project management practices. The total additional funding for this request for FY is $26 million of which $5 million is ongoing. This amount includes $3 million for enhanced project management which is technically funded within program planning & delivery, with the remaining $23 million for operations & maintenance. STILLWATER LIFT BRIDGE ENDOWMENT The Governor recommends transferring up to $6 million from the current trunk highway appropriation for State Road Construction to an endowment account for the operation and maintenance of the Stillwater lift bridge. This funding would establish an endowment, and only interest earnings would be spent. This maintenance account was part of the agreement to build the new St. Croix River Crossing. The maintenance costs will be shared with Wisconsin. This would technically not be an increase in expenditures, but would instead permit a transfer for an appropriation in the approved FY biennial budget. AERONAUTICS APPROPRIATION The Governor recommends an increase of $4 million ($1 million in FY 2014 and $3 million in FY 2015) from the state airports fund to provide the local match to federal grants, and to fund pavement maintenance and other improvements to the state s 135 airports. This proposal is made possible by the repayment by the General Fund of $15 million that was borrowed in 2008 to address a General Fund budget shortfall. HIGHWAY 14 TURNBACK SETTLEMENT The Governor recommends an increase of $14 million to the State Road Construction appropriation in the Trunk Highway Fund that would be used to upgrade a section of trunk highway 14 before turning it over to Steele and Waseca counties. An additional $21 million is recommended to be transferred from the Flexible Highway Account in the County State Aid Highway Fund to the Trunk Highway Fund in FY 2015 to provide additional funding for this project. This funding is proposed as a result of a legal settlement agreement and release executed between the state and Steele and Waseca Counties agreed to by MnDOT, Steele County, and Waseca County, dated January 7, Page 6

, and the State Airports Fund.")

7 FY Direct Appropriations, including Governor's Supplemental Recommendations Dollars in thousands FY Enacted Budget Chapter 117 FY Supplemental Recommendation FY Governor's Rec Program Name Budget Activity Name Fund Multimodal Systems Aeronautics Airports $ 18,934 $ 18,934 $ 1,000 $ 3,000 $ 19,934 $ 21,934 TH 1,100 1, ,100 1,100 Transit GF 16,451 16, ,451 16,470 TH Safe Routes to School GF State Roads Freight GF TH 4,897 4, ,897 4,897 Commuter & Passenger Rail GF Program Planning & Delivery TH 206, ,720-3, , ,720 HUTD State Road Construction TH 909, ,600 14, , ,600 Ecomomic Recovery Funds TH 1,000 1,000 1,000 1,000 Operations & Maintenance TH 262, ,395 5,000 18, , ,395 Electronic Communications GF TH 5,168 5, ,168 5,168 Local Roads Debt Service TH 158, , , ,821 - County State Aids CSAH 594, , , ,505 Municipal State Aids MSAS 152, , , ,060 Agency Management Agency Services Airports TH 41,972 41, ,972 41,972 Building Services GF TH 17,784 17, ,784 17,784 *Total Direct Appropriations 2,393,778 2,346,289 20,000 24,000 2,413,778 2,370,289 Totals by Fund: Trunk Highway (TH) 1,609,628 1,547,232 19,000 21,000 1,628,628 1,568,232 General (GF) 18,014 17, ,014 17,533 Airports 18,959 18,959 1,000 3,000 19,959 21,959 County State Aid Highway (CSAH) 594, , , ,505 Municipal State Aid Street (MSAS) 152, , , ,060 Highway User Tax Distribution (HUTD) $ 2,393,778 $ 2,346,289 $ 20,000 $ 24,000 $ 2,413,778 $ 2,370,289 *Does not include 2014 Governor's Capital Budget Recommendation for trunk highway fund cash capital building projects of $7.950 million or the transfer from the flexible highway account for $21 million. - - Page 7

8 MnDOT 2014 LEGISLATIVE POLICY INITIATIVES MnDOT proposed and the Governor approved a variety of initiatives for consideration during the 2014 legislative session. Those related to appropriations were included in the previous summary of supplemental budget recommendations recently announced by the Governor. Others are policy oriented. Unless otherwise noted the items described below have been introduced and are included in the MnDOT housekeeping bill (House File 2214 and Senate File 2154), which has had hearings in both the House and the Senate.. ROCHESTER MAINTENANCE FACILITY MnDOT received two appropriations for reconstruction of the Rochester Maintenance Facility, one in 2010 and the other in The unused portion ($1,493,000) of the 2010 appropriation would be transferred to the 2012 appropriation, which is being used for the second phase of this project and needs additional funding. PRODUCTS AND SERVICES MnDOT is revising its budgeting approach to one based on products and services. In conjunction with this initiative MnDOT is proposing legislation that would permit internal billing operations units for the costs of centrally managed products or services. This has not been included in the MnDOT housekeeping bill. It is anticipated that it will be included in the supplemental funding bill. TRANSPORTATION ECONOMIC DEVELOPMENT (TED) PROGRAM In previous sessions, MnDOT has received appropriations for the Transportation Economic Development Program (TED). Currently one active appropriation is only for the current biennium, while another is available until expended. MnDOT proposes having all TED appropriations be available until expended to accommodate the nature of this program. TED projects typically are multi-year projects, which may extend from one biennium to another. FLOOD BOND APPROPRIATION CANCELLATION CORRECTION MnDOT requested and the governor recommended correcting a 2007 trunk highway appropriation cancellation to reflect the actual balance that was available to be canceled. This is a technical correction that has no impact on expenditures or the fund balance. CONTRACTOR PAYMENTS MnDOT is proposing language to clarify when contractor payments need to be made and to clarify that contractors are not entitled to interest under two separate sections of statute. 60 DAY CURE PERIOD This proposal eliminates the 60 day period of time after a default by a MnDOT contractor that MnDOT currently has to wait before making alternate arrangements for the work. TRANSFER OF MNDOT OWNED RIGHT- OF-WAY This proposal would clarify the circumstances under which MnDOT would be allowed to dispose of right-of-way, taking into account the possible suitability for bicycle and pedestrian use. Page 8

9 ACCRUAL OF REVENUE FOR COUNTY STATE AID HIGHWAY FUND (CSAH) AND MUNICIPAL STATE AID STREET FUND (MSAS) REVENUE FOR USE IN APPORTIONMENT PROCESS This proposal is to change the number of months of actual revenue (currently five) that must be used in calculating the amount of revenue in a current fiscal year available for apportionment to counties and municipalities to the number of months at the time of the apportionment calculation. This would allow issuing the apportionments at a time earlier than what is currently done which is in January. REPAIR OF TOWNSHIP BRIDGES WHEN INSPECTION SHOWS DEFICIENCIES This proposal would clarify responsibilities between counties and townships when bridge inspections uncover deficiencies in township bridges. WIDE TURNS BY LARGE COMBINATION VEHICLES Due to their configuration, certain large vehicles are unable to make right turns and U-turns into the closest lane of the roadway. This proposal would allow these vehicles to use multiple lanes for turning, if the roadway has two or more lanes of traffic in the same direction. CONFORM AGRICULTURE VEHICLES PROVISION WITH MAP-21 MnDOT has proposed a number of revisions to state law as it relates to agricultural vehicles, in order to conform Minnesota law to the provisions of the recently passed federal MAP-21 (Moving Ahead For Progress in The 21 st Century) law. NON-MOTORIZED VEHICLE TASK FORCE MnDOT proposes extending the life of the Non-Motorized Vehicle Task Force by four years; the task force would expire in 2018 under this proposal. It is currently scheduled to expire this year. BLUE EARTH COUNTY TURNBACK This proposal is to amend the turnback passed by the 2013 legislature of a road in District 7. The amendment would facilitate having part of the road being turned back to the city of Mankato, rather than all of it being turned back to Blue Earth county. ROADWAY NEAR BRAINERD STATE HOSPITAL The Department of Administration has agreed to take over responsibility for a trunk highway near the old Brainerd State Hospital, so MnDOT is proposing that this highway be deleted from the list of statutory trunk highways contained in Minnesota Statutes Chapter 161. UNSESSION PROPOSALS Governor Dayton has directed state agencies to propose Minnesota state laws that are no longer needed and can be repealed. MnDOT has developed 86 proposals that would eliminate about 37 pages of statute for consideration by the legislature. These proposals have not been included in MnDOT s housekeeping bill. Two of these proposals combining two state aid rules advisory committees into one committee and abolishing the Commuter Rail Advisory Committee -- have been included in House File A variety of others have been incorporated into Senate File Page 9

10 MINNESOTA S HIGHWAY FINANCES This section describes Minnesota s highway financing, followed by historical revenue trends since MOTOR FUEL TAX The state motor fuel tax is a major source of revenue for highways in Minnesota. Each one cent of gas tax yields about $30 million per year to the Highway User Tax Distribution (HUTD) Fund and thus about $17 million in revenues to the Trunk Highway (TH) Fund. The current tax yielded $860 million in FY 2013 after refunds, but before collection costs and transfers to the Department of Natural Resources (DNR). Approximately eighty percent of motor fuel tax revenues are generated from gasoline sales. The remainder comes mostly from diesel and special fuel sales. State law requires transfers of non-highway use gasoline tax revenues (e.g., from fuel used in boats and snowmobiles) to accounts managed by the DNR. About 3% of gasoline tax revenues, or approximately $22 million in FY 2013, were termed unrefunded and were transferred from the HUTD Fund to DNR accounts. Based on information supplied by the American Petroleum Institute (as of January 2014), seven states have gasoline tax rates higher than Minnesota. Some states have local option gas taxes and/or levy a statewide sales tax or other statewide tax (e.g., an oil franchise tax in Pennsylvania) on gasoline sales. If these additional taxes are taken into account, nineteen states have higher gas tax rates than Minnesota. MOTOR VEHICLE REGISTRATION TAXES In FY 2013, motor vehicle registration taxes, after refunds, but before collection costs, yielded $623 million. Passenger class and pickup truck vehicles generated approximately 80% of total motor vehicle registration tax revenues. MOTOR VEHICLE SALES TAX The motor vehicle sales tax, a 6.5% tax on the sale of new and used motor vehicles, is constitutionally dedicated to transportation, with 40% allocated to transit and 60% allocated to highways by state statute. In FY 2013, this amounted to $359 million to the HUTD and $239 million to transit. FEDERAL HIGHWAY FUNDS The level of federal funding is a critical issue for MnDOT and for local governments across the state, because federal funds make up a substantial portion of transportation spending. For the TH Fund, which is the principal funding source for MnDOT and which also provides significant funding for the Department of Public Safety, $551 million of federal aid agreements were entered into in FY 2013; this is about 33% of total revenue. In addition, a substantial amount of federal revenue is made available for local government projects. In FY 2013 $195 million was received for local government use. The February 2014 forecast for federal agreements revenue has not changed, since forecast made in November This forecast is for lower amounts of revenue in FY 2016 and 2017, compared with FY 2014 and 2015, which in turn are lower than the amount received in FY However, it should be noted that there is a high level of uncertainty about forecasts for years beyond FY This is due both to the expiration of the current federal authorization law (Moving Ahead for Progress in the 21st Century, or MAP-21) on September 30, 2014, and to the deteriorating ability of the federal highway trust fund (funded primarily by the federal motor fuel taxes) to fully fund the various federal transportation programs. HIGHWAY USER TAX DISTRIBUTIONS The Minnesota Constitution provides that 95% of HUTD Fund revenues are distributed as follows: Trunk Highway (TH) fund - 62%; County State Aid Highway (CSAH) fund - 29%; and Municipal State Aid Streets (MSAS) fund - 9%. The remaining 5%, referred to as the five percent set-aside, is distributed in accordance with a formula established by the Legislature. Page 10

.")

11 This formula may only be changed once every six years, and was most recently changed by the 1998 Legislature. Since July 1, 1999, the five percent set-aside revenues, $90 million in FY 2013, have been deposited in the CSAH Fund, where they have been further allocated to the Township Roads Account (30.5%), Township Bridges Account (16%), and Flexible Highway Account (53.5%). FLEXIBLE HIGHWAY ACCOUNT The Flexible Highway Account was created by the 1998 Legislature by combining money from the five percent set-aside that was previously allocated to the Trunk Highway Fund, the county turnback account in the CSAH Fund, and the municipal turnback account in the MSAS Fund. According to changes made by the 2008 Legislature, the commissioner of transportation must recommend allocation of money in the Flexible Highway Account to the CSAH Fund, which includes allocations to metropolitan counties (except that the shares allocated to Hennepin and Ramsey counties do not include the population of the cities of the first class Minneapolis and St. Paul) from the excess sum, the county turnback account, the safety improvement account, and the routes of regional significance account; the MSAS Fund (municipal turnback account); and the Trunk Highway Fund (for trunk highways that will be restored and subsequently turned back by agreement to local governments) for each upcoming two-year period as part of the biennial budget proposal. Since the distribution of money in the Flexible Highway Account is subject to decisions made in the biennial budget process, the relative amounts in the following table could be different in future biennia. The following table describes allocations of the five percent set-aside for FY 2012 through The amounts for the town road and town bridge accounts are based on percentages contained in statute. The allocations of the Flexible Highway Account are based on: FY2012 and 2013 actual transfers; and FY 2014 and recommendations included in the biennial budget request. CSAH FUND AND MSAS FUND SPENDING Money in these funds is allocated to all counties and to municipalities with populations greater than 5,000, based on statutorily defined apportionment formulas. The 2008 Legislature changed the process for allocation (formally termed apportionment) of this money to the CSAH Fund. Revenues derived from increases provided by the 2008 Legislature (e.g., increased gas tax rates) plus increased revenue from the percentages allocated to the Highway User Tax Distribution fund above 32% due to the phase-in of motor vehicle sales tax revenue as a constitutionally dedicated transportation revenue source are apportioned 60% based on money needs and 40% based on relative shares of the number of motor vehicle registrations in each county. For revenues not derived from increases provided by the 2008 Legislature, the apportionment is based on monetary needs (50%), relative shares of lane miles of roads (30%), relative shares of the number of motor vehicle registrations (10%), and equal shares to each of the 87 counties (10%). The allocation of money for the MSAS Fund was unchanged by the 2008 legislature; the municipalities respective shares are based on monetary needs (50%) and population (50%). As a result of each decennial census, or as a result of the annual state demographer s estimate, additional municipalities may qualify for funding because their population grew beyond 5,000. At each census, some municipalities may stop qualifying for funding because their population fell below 5,000. As the decade progresses, additional municipalities may qualify for funding due to incorporation, Page 11

12 consolidation, or by state demographer s estimate. Municipalities may also appeal their census counts. Of the 147 cities that qualify for funding, 5 are below 5,000 in population, but will remain eligible for funding through 2015 due to legislation passed in sales in the future. The current estimate of these transfers is from the February 2014 forecast: BONDING As of October 2013, the principal amount of outstanding trunk highway bonds totaled approximately $1,025 million, of which $641 million were authorized by Chapter 152 and the remainder by other laws. Approximately $527 million of interest must be paid on these bonds. When refunding bonds are included, the total of outstanding debt service is approximately $1,936 million. The total amount of trunk highway bond authorizations provided by the Legislature since 2003 is $2.8 billion. From these authorizations, $1.8 billion of bonds have been issued. The most recent bond authorizations occurred when the 2013 Legislature approved $300.3 million of trunk highway bonds for a Corridor of Commerce program. If MnDOT did not sell any additional bonds in the future, principal and interest on the outstanding trunk highway bonds for upcoming fiscal years are: This total repayment is reduced each fiscal year by the interest earned on the balances in the trunk highway account in the state debt service fund. The total estimated debt service transfers from the Trunk Highway Fund is based on the currently known debt service (see above) plus estimates that are developed for planned bond The reason the estimated debt service expenditures are higher than the amounts shown in the Minnesota Management and Budget s official statement is that the fund statement reflects MnDOT s plans to sell significant amounts of additional bonds from the authorizations provided by the Legislatures. As estimates of cash flow expenditures from the additional bonding authorizations are refined, these estimates of debt service will change. Debt service is higher in the earlier years of repayment because the repayment schedules are based on retiring onetwentieth of the principal each year, unlike repayment requirements for a home mortgage, which are a fixed annual sum for combined principal and interest, with the amount of principal being repaid increasing each year. ADVANCE CONSTRUCTION MnDOT utilizes a type of federal financing called advance construction (AC). In general, this technique permits recognizing federal revenues in the current year that are scheduled to be received in future years. This results in a number of benefits. Even though the budgetary revenue is recognized, actual reimbursement (receipt of cash from FHWA) does not begin until the year the advanced construction agreements are converted to regular federal funds (the year the federal funds are actually made available through a federal appropriations act). The cash balance in the trunk highway fund may sometimes be used to pay contractors before the project is converted and federal reimbursement received. Careful management of the use of AC has been adopted to avoid potential cash flow issues. MnDOT has developed and continues to refine advance construction and cash management techniques and policies. Page 12

13 HISTORY OF MnDOT REVENUE CHANGES MOTOR FUEL TAX RATES PER GALLON: MINNESOTA Year Description 1975 Increased from 7 to 9 cents per gallon to 11 cents to 13 cents to 16 cents (for eight months) and then to 17 cents beginning January 1, to 20 cents 1994 Phased out 2-cent gasohol credit over 4 years 2008 Chapter 152 authorized a number of changes to the fuel tax rates from 2008 to 2012; including a general rate increase of 5 cents phased in by October 1, 2008, and a debt service surcharge that increases to 3.5 cents by April 1 20 cents to 22.0 cents (2 cent general increase) 2008 Aug cents to 22.5 cents (debt service surcharge) 2008 Oct cents to 25.5 cents (3 cent general increase) 2009 Jul cents to 27.1 cents (debt service surcharge) 2010 Jul cents to 27.5 cents (debt service surcharge) 2011 Jul cents to 28 cents (debt service surcharge) 2012 Jul cents to 28.5 cents (debt service surcharge) MOTOR FUEL TAX RATES PER GALLON: FEDERAL, MINNESOTA, AND NEIGHBORING STATES, JANUARY 2014 Cents per gallon Federal MN WI SD IA ND Gasoline Diesel Gasohol (10% blend) MOTOR VEHICLE REGISTRATION TAXES Year Description 1981 Increased passenger vehicle registration taxes by phasing in an increased minimum tax 1986 Increased truck registration taxes for heavier trucks 1989 Adjusted schedule for reduction of taxes paid for passenger vehicles as they become older, such that citizens pay more over the life of the vehicle 2000 Retained the same policy for calculating the tax for passenger vehicles, but provided a maximum tax of $189 for the first renewal and a maximum tax of $99 for the second and subsequent renewals 2008 Modified registration tax policy for passenger vehicles to institute a process similar to what existed prior to 2000, by eliminating caps and changing the depreciation schedule; these provisions are phased-in by virtue of a provision that provides that for currently registered vehicles, no one s tax will be higher in a current year than it was in the previous year. Page 13

2008 Aug 1 22.0 cents to 22.5 cents (debt service surcharge) 2008 Oct 1 22.5 cents to 25.5 cents (3 cent general increase) 2009 Jul 1 25.5 cents to 27.")

14 MOTOR VEHICLE SALES TAX AS A TRANSPORTATION REVENUE SOURCE The Motor Vehicle Sales Tax (MVST) was previously known as the Motor Vehicle Excise Tax (MVET) Year Description Numerous changes were made, which first statutorily dedicated this revenue to transportation on a phase-in basis, began the phase-in, delayed the phase-in, and ultimately eliminated this as a transportation revenue source Allocation of this revenue for highways and transit began. For highways the allocation was intended to offset the reduced revenues from the change in tax policy for passenger motor vehicles made by the 2000 legislature. For transit the allocation was intended to offset a 2001 reduction in local government property taxes due to the law being changed prohibiting levying taxes for transit operations A constitutional amendment was passed, providing that by FY 2012 all revenue would be dedicated to transportation as follows: (1) not more than 60% to be deposited in the Highway User Tax Distribution Fund; and (2) not less than 40% to be dedicated to transit. A five-year phase-in schedule is provided in the amendment Voters approved the proposed constitutional amendment in the general election held in November The legislature provided a statutory allocation of revenues, consistent with the constitutional amendment, which is shown below The percentages were changed for FYs 2010 and 2011 to address operating deficits in transit. For FY 2012 and beyond, the allocation percentages are the same as in the legislation passed in Statutory allocation of motor vehicle sales tax revenues Enacted by the 2007 Legislature Consistent with the constitutional amendment passed by the voters in November 2006 Fiscal Year Highway user tax distribution fund 38.25% 44.25% 50.25% 56.25% 60% Metropolitan transit 24.00% 27.75% 30.00% 33.75% 36% Greater Minnesota transit 1.50% 1.75% 3.50% 3.75% 4% Total to transportation 63.75% 73.75% 83.75% 93.75% 100% Statutory allocation of motor vehicle sales tax revenues Fiscal Years 2010 and 2011 shift to transit Enacted by the 2009 Legislature Fiscal Year Highway user tax distribution fund 38.25% 44.25% 47.50% 54.50% 60% Metropolitan transit 24.00% 27.75% 31.50% 35.25% 36% Greater Minnesota transit 1.50% 1.75% 4.75% 4% 4% Total to transportation 63.75% 73.75% 83.75% 93.75% 100% Page 14

15 HISTORICAL TRENDS IN HIGHWAY REVENUE TO THE HUTD, 1980 TO 2013 AND FORECAST TO 2017 The following page shows the history of the major state highway revenue sources in Minnesota and the February 2014 forecast for the period of FY Please note that this chart shows the three major funding sources of gas tax, tab fees and motor vehicle sales tax. Small additional amounts of revenue are also deposited in the Highway User Tax Distribution fund (HUTD), and are shown in the fund statement in the appendix. Page 15

, and are shown in the")

16 Page 16

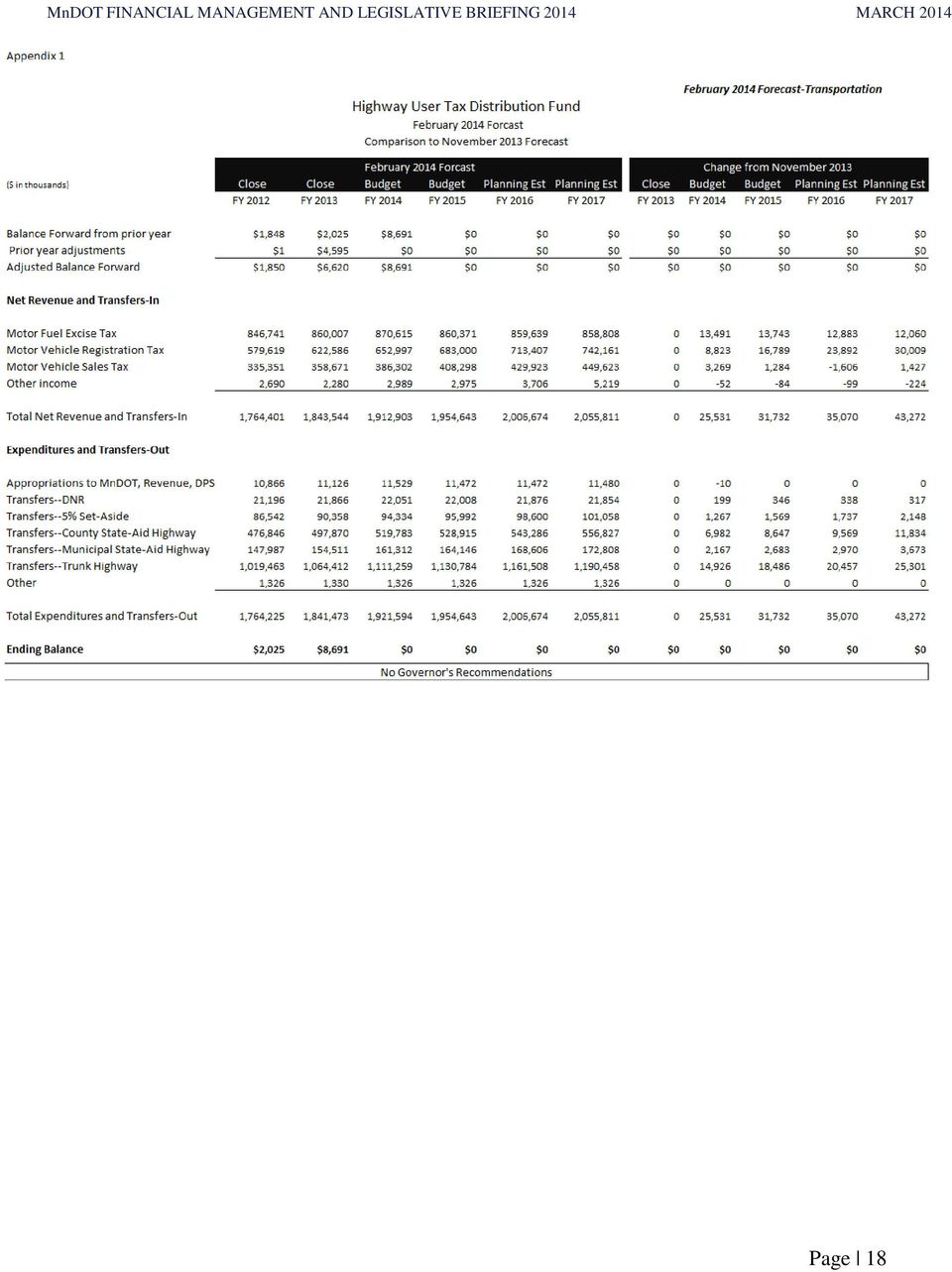

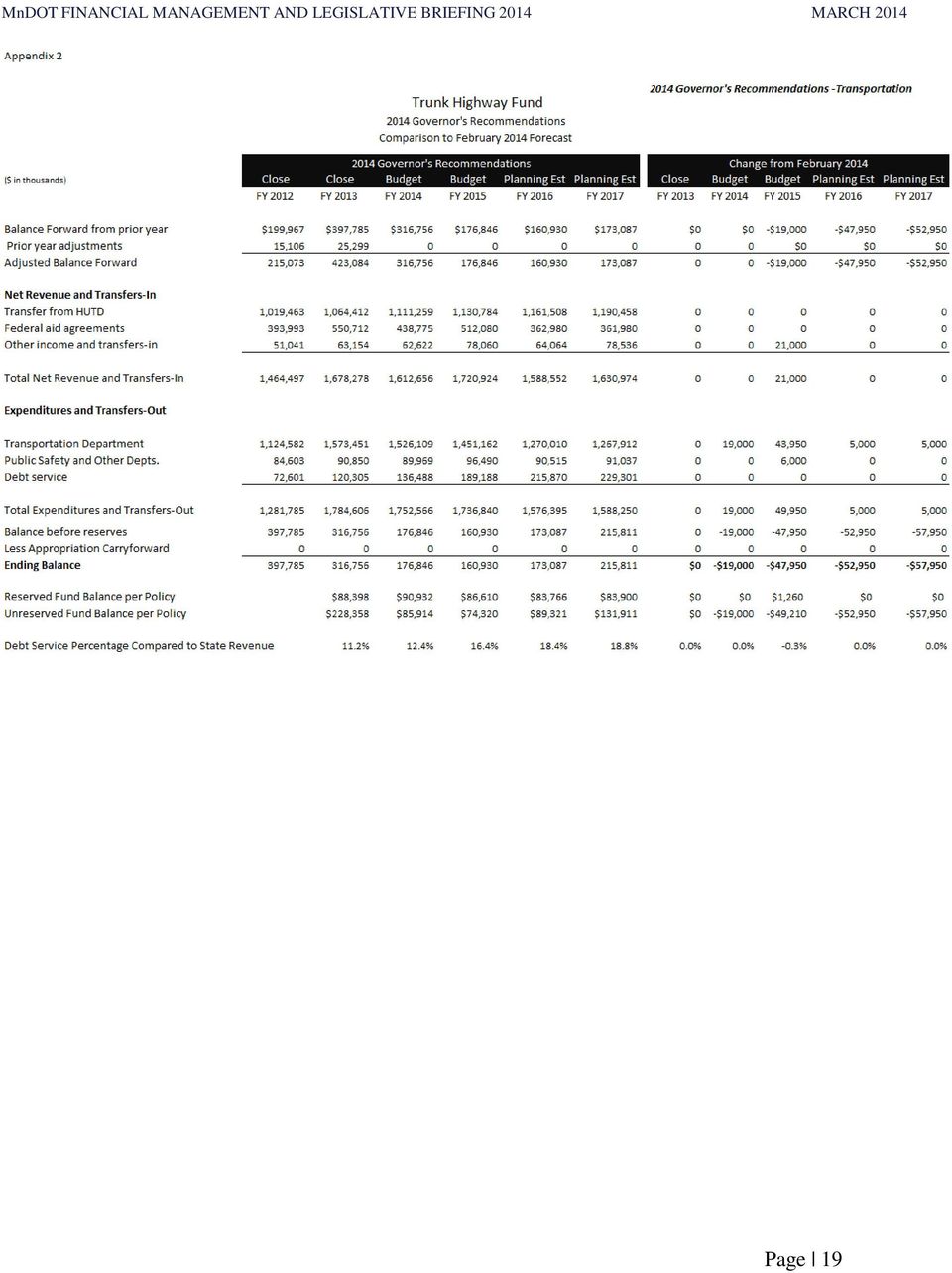

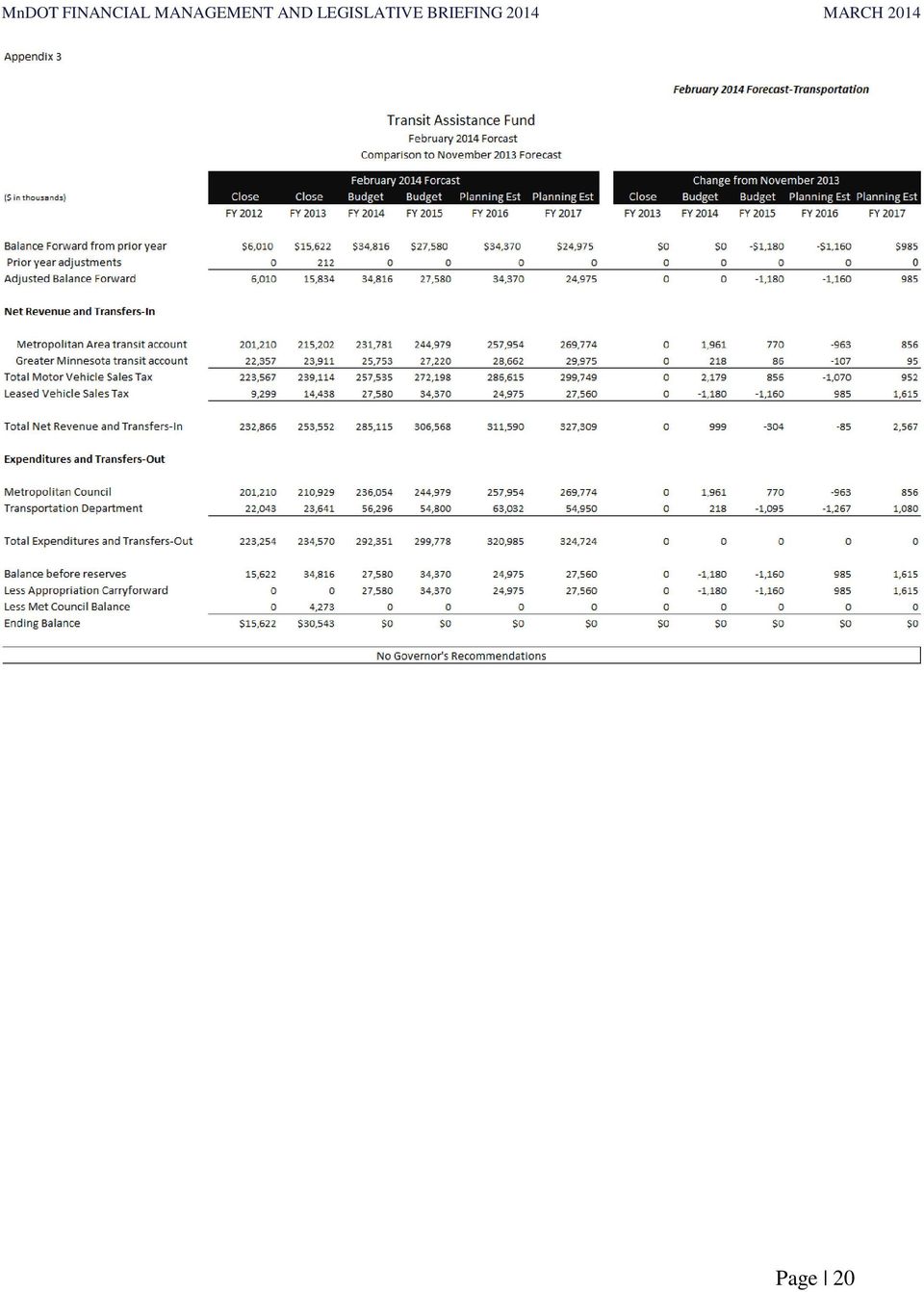

17 Appendix This section includes a range of additional detailed or background information: Current forecast fund statements for the major state transportation funds: o Highway User Tax Distribution fund statement, February 2014 forecast; o Trunk Highway fund statement, 2014 Governor s Recommendation; o Transit Assistance fund statement, February 2014 forecast; o State Airports fund statement, 2014 Governor s Recommendation; o County State Aid fund statement, 2014 Governor s Recommendation; o Municipal State Aid Streets fund statement, February 2014 forecast; Vehicles Miles Traveled (VMT) and Motor Fuel Consumption from 1975 to the present, together with implied overall fleet efficiency (VMT per gallon of fuel); Transportation Funding, Fiscal Year where it comes from and where it goes; Revenue and expenditures for transportation purposes, all sources of funds, FY 2013 final (budgetary basis), on the last page. Note: The Governor s FY Supplemental Budget Recommendations are available at the following link: Page 17

; Transportation Funding, Fiscal Year 2013 - where it comes from and where")

18 Page 18

19 Page 19

20 Page 20

21 Page 21

22 Page 22

23 Page 23

24 Page 24

25 Transportation Funding, Fiscal Year 2013 Where it comes from and where it goes $3.14 billion About 80 percent of MnDOT funds are appropriated by the legislature and 20 percent are statutorily appropriated. Sources of legislative appropriations include state motor fuel taxes, motor vehicle registration fees, motor vehicle sales taxes (MVST), and federal motor fuel tax grants. Mn/DOT is a multi-modal agency. Its activities include transit, aeronautics, freight and commercial vehicles, construction, maintenance, and operation of 12,000 miles of state highways. Approximately 30% of MnDOT s appropriations are state aid to local governments for road and bridge projects and other activities. Note 1: Revenues and expenditures of the Metropolitan Airports Commission (MAC) and Metro Transit are not included. Note 2: Data from the State of Minnesota Revenue and Expenditures for Transportation Purposes flowchart (budgetary basis). Includes bond expenditures. Total of Sources: differs from Uses due to fund balance changes. Page 25

26 Page 26

Transportation Funds Forecast. February 2013. Transportation Funds Forecast. Released March 1, 2013. February 2013 Forecast Executive Summary

Transportation Funds Forecast The purpose of this document is to serve as the official guide to the Minnesota Department of Transportation (MnDOT) forecast for the six transportation funds: Highway User

Transportation Funds Forecast The purpose of this document is to serve as the official guide to the Minnesota Department of Transportation (MnDOT) forecast for the six transportation funds: Highway User

Transportation Funds Forecast

Transportation Funds Forecast February 2015 Released March 2, 2015 February 2015 Forecast Executive Summary Revenues up 14 million in Highway User Tax Distribution (HUTD) Fund in FY 2014-15 The February

Transportation Funds Forecast February 2015 Released March 2, 2015 February 2015 Forecast Executive Summary Revenues up 14 million in Highway User Tax Distribution (HUTD) Fund in FY 2014-15 The February

CHAPTER 20 COUNTY PERMISSIVE MOTOR VEHICLE LICENSE TAX

CHAPTER 20 COUNTY PERMISSIVE MOTOR VEHICLE LICENSE TAX Latest Revision March, 2013 20.01 INTRODUCTION In 1967 the General Assembly granted counties the authority to enact a permissive motor vehicle license

CHAPTER 20 COUNTY PERMISSIVE MOTOR VEHICLE LICENSE TAX Latest Revision March, 2013 20.01 INTRODUCTION In 1967 the General Assembly granted counties the authority to enact a permissive motor vehicle license

Analysis of the Obama Administration s FY 2017 Budget Proposal for Transportation

Analysis of the Obama Administration s FY 2017 Budget Proposal for Transportation FY 2017 Budget Summary The Obama s Administration s proposed budget for FY 2017, which was submitted to Congress February

Analysis of the Obama Administration s FY 2017 Budget Proposal for Transportation FY 2017 Budget Summary The Obama s Administration s proposed budget for FY 2017, which was submitted to Congress February

Technical Memorandum REVENUE FORECASTS. Prepared for: Prepared by:

Technical Memorandum REVENUE FORECASTS Prepared for: Prepared by: April 2014 TABLE OF CONTENTS 1 Introduction... 1 1.1 Inflation Indices... 2 1.2 Previous Studies... 3 2 Highway Revenue Baseline Forecast...

Technical Memorandum REVENUE FORECASTS Prepared for: Prepared by: April 2014 TABLE OF CONTENTS 1 Introduction... 1 1.1 Inflation Indices... 2 1.2 Previous Studies... 3 2 Highway Revenue Baseline Forecast...

Primer Highway Trust Fund. Federal Highway Administration Office of Policy Development

Primer Highway Trust Fund Federal Highway Administration Office of Policy Development November 1998 Highway Trust Fund Primer Summary This Highway Trust Fund Primer is designed to provide basic information

Primer Highway Trust Fund Federal Highway Administration Office of Policy Development November 1998 Highway Trust Fund Primer Summary This Highway Trust Fund Primer is designed to provide basic information

Montana Legislative Fiscal Division. September 19, 2000. Prepared by Greg DeWitt, Senior Fiscal Analyst

Montana Legislative Fiscal Division Highway State Special Revenue Account: Working Capital Update September 19, 2000 Prepared by Greg DeWitt, Senior Fiscal Analyst Highway State Special Revenue Account:

Montana Legislative Fiscal Division Highway State Special Revenue Account: Working Capital Update September 19, 2000 Prepared by Greg DeWitt, Senior Fiscal Analyst Highway State Special Revenue Account:

Chapter 5 Financial Plan

The Safe, Accountable, Flexible, Efficient Transportation Equity Act: A Legacy for Users (SAFETEA_LU) requires that the MTP incorporate a financial plan for the planning period. The MTP is required to

The Safe, Accountable, Flexible, Efficient Transportation Equity Act: A Legacy for Users (SAFETEA_LU) requires that the MTP incorporate a financial plan for the planning period. The MTP is required to

Wayne Sandberg, Washington County Public Works Abbey Bryduck, Association of MN Counties

Wayne Sandberg, Washington County Public Works Abbey Bryduck, Association of MN Counties County Wheelage Tax What is it? Experiences What to expect in 2014 City Options Local Option Sales Tax What is it?

Wayne Sandberg, Washington County Public Works Abbey Bryduck, Association of MN Counties County Wheelage Tax What is it? Experiences What to expect in 2014 City Options Local Option Sales Tax What is it?

S.B. NO. JAN 2 2 2016

THE SENATE TWENTY-EIGHTH LEGISLATURE, 0 STATE OF HAWAII S.B. NO. JAN 0 A BILL FOR AN ACT RELATING TO STATEWIDE INFRASTRUCTURE CAPACITY BUILDING CONSTRUCTION FINANCING. BE IT ENACTED BY THE LEGISLATURE

THE SENATE TWENTY-EIGHTH LEGISLATURE, 0 STATE OF HAWAII S.B. NO. JAN 0 A BILL FOR AN ACT RELATING TO STATEWIDE INFRASTRUCTURE CAPACITY BUILDING CONSTRUCTION FINANCING. BE IT ENACTED BY THE LEGISLATURE

New Jersey Transportation Trust Fund Authority Fiscal Year 2016 Financial Plan

New Jersey Transportation Trust Fund Authority Fiscal Year 2016 Financial Plan Plan for Financing Anticipated NJDOT/NJT Capital Program Outlays for Fiscal Year 2016 NEW JERSEY TRANSPORTATION TRUST FUND

New Jersey Transportation Trust Fund Authority Fiscal Year 2016 Financial Plan Plan for Financing Anticipated NJDOT/NJT Capital Program Outlays for Fiscal Year 2016 NEW JERSEY TRANSPORTATION TRUST FUND

Program guidance that details the eligibility, criteria and application process. Ferry Boat Program. Ohio Department of Transportation

Program guidance that details the eligibility, criteria and application process. Ferry Boat Program Ohio Department of Transportation TABLE OF CONTENTS Program Overview Program Administration.........2

Program guidance that details the eligibility, criteria and application process. Ferry Boat Program Ohio Department of Transportation TABLE OF CONTENTS Program Overview Program Administration.........2

2035 FINANCIAL RESOURCES FORECAST

2035 FINANCIAL RESOURCES FORECAST AKRON METROPOLITAN AREA TRANSPORTATION STUDY 806 CITICENTER BUILDING 146 SOUTH HIGH STREET AKRON, OHIO 44308 December 2012 This report was prepared by the Akron Metropolitan

2035 FINANCIAL RESOURCES FORECAST AKRON METROPOLITAN AREA TRANSPORTATION STUDY 806 CITICENTER BUILDING 146 SOUTH HIGH STREET AKRON, OHIO 44308 December 2012 This report was prepared by the Akron Metropolitan

Cost and Financial Analysis

Chapter 19: Cost and Financial Analysis A. INTRODUCTION The purpose of this chapter is to present examples of financial resources available to the Metropolitan Transportation Authority (MTA), which may

Chapter 19: Cost and Financial Analysis A. INTRODUCTION The purpose of this chapter is to present examples of financial resources available to the Metropolitan Transportation Authority (MTA), which may

The Roads to Recovery. Facts About Transportation Funding and Spending

The Roads to Recovery Facts About Transportation Funding and Spending How Pima County spends transportation money (F.Y. 2014-15 Transportation Budget) 1 Debt Service (1997 bonds): $19.1 million In 1997,

The Roads to Recovery Facts About Transportation Funding and Spending How Pima County spends transportation money (F.Y. 2014-15 Transportation Budget) 1 Debt Service (1997 bonds): $19.1 million In 1997,

State Cashflow Management

Informational Paper 77 State Cashflow Management Wisconsin Legislative Fiscal Bureau January, 2009 State Cashflow Management Prepared by Dave Loppnow Wisconsin Legislative Fiscal Bureau One East Main,

Informational Paper 77 State Cashflow Management Wisconsin Legislative Fiscal Bureau January, 2009 State Cashflow Management Prepared by Dave Loppnow Wisconsin Legislative Fiscal Bureau One East Main,

A Legislative Briefing prepared by Volume 7, Number 1 February 2001

fiscal forum A Legislative Briefing prepared by Volume 7, Number 1 February 2001 Mitchell E. Bean, Director P. O. Box 30014, Lansing, MI 48909-7514 517-373-8080! FAX 517-373-5874! www.house.state.mi.us/hfa

fiscal forum A Legislative Briefing prepared by Volume 7, Number 1 February 2001 Mitchell E. Bean, Director P. O. Box 30014, Lansing, MI 48909-7514 517-373-8080! FAX 517-373-5874! www.house.state.mi.us/hfa

Operating Budget Data

J00A04 Debt Service Requirements Maryland Department of Transportation Operating Budget Data ($ in Thousands) FY 14 FY 15 FY 16 FY 15-16 % Change Actual Working Allowance Change Prior Year Special Fund

J00A04 Debt Service Requirements Maryland Department of Transportation Operating Budget Data ($ in Thousands) FY 14 FY 15 FY 16 FY 15-16 % Change Actual Working Allowance Change Prior Year Special Fund

Chapter 8 Funding Considerations

Chapter 8 Funding Considerations Expanding transit services into El Dorado Hills under any of the service alternatives has associated operating and capital costs. This chapter considers the funding sources

Chapter 8 Funding Considerations Expanding transit services into El Dorado Hills under any of the service alternatives has associated operating and capital costs. This chapter considers the funding sources

Pedestrian & Bicycle Plan

RAMSEY COMMUNITIES COUNTYWIDE Pedestrian & Bicycle Plan PRIMER: LEGAL FRAMEWORK PRIMER: LEGAL FRAMEWORK Walking and Biking for All e 2 CHAPTER 2: Walking and Biking for All This page intentionally left

RAMSEY COMMUNITIES COUNTYWIDE Pedestrian & Bicycle Plan PRIMER: LEGAL FRAMEWORK PRIMER: LEGAL FRAMEWORK Walking and Biking for All e 2 CHAPTER 2: Walking and Biking for All This page intentionally left

Lynn M. Suter and Associates

3 Lynn M. Suter and Associates Government Relations GM Memo No. 05-181 August 5, 2005 TO: Joe Wallace, President, and Members of the AC Transit Board of Directors Jim Gleich, DGM FR: RE: Lynn M. Suter

3 Lynn M. Suter and Associates Government Relations GM Memo No. 05-181 August 5, 2005 TO: Joe Wallace, President, and Members of the AC Transit Board of Directors Jim Gleich, DGM FR: RE: Lynn M. Suter

Examples of Transportation Plan Goals, Objectives and Performance Measures

Examples of Transportation Plan Goals, Objectives and Performance Measures The next step in the Long Range Transportation Plan (LRTP) process is to develop goals, objectives, and performance measures.

Examples of Transportation Plan Goals, Objectives and Performance Measures The next step in the Long Range Transportation Plan (LRTP) process is to develop goals, objectives, and performance measures.

Summary of MAP-21 Matrix

Summary of MAP-21 Matrix Overview On July 6, 2012, President Obama signed into law P.L. 112-141, the Moving Ahead for Progress in the 21st Century Act (MAP-21). Funding surface transportation programs

Summary of MAP-21 Matrix Overview On July 6, 2012, President Obama signed into law P.L. 112-141, the Moving Ahead for Progress in the 21st Century Act (MAP-21). Funding surface transportation programs

State of North Carolina Department of State Treasurer

RICHARD H. MOORE TREASURER State of North Carolina Department of State Treasurer State and Local Government Finance Division and the Local Government Commission T. VANCE HOLLOMAN DEPUTY TREASURER Memorandum

RICHARD H. MOORE TREASURER State of North Carolina Department of State Treasurer State and Local Government Finance Division and the Local Government Commission T. VANCE HOLLOMAN DEPUTY TREASURER Memorandum

E2SHB 2569 - S COMM AMD By Committee on Energy, Environment & Telecommunications

2569-S2.E AMS EET S4774.1 E2SHB 2569 - S COMM AMD By Committee on Energy, Environment & Telecommunications ADOPTED 03/06/2014 1 Strike everything after the enacting clause and insert the 2 following: 3

2569-S2.E AMS EET S4774.1 E2SHB 2569 - S COMM AMD By Committee on Energy, Environment & Telecommunications ADOPTED 03/06/2014 1 Strike everything after the enacting clause and insert the 2 following: 3

Federal Guidelines for STP-U Funding

MPC 5.f Attachment 1 STP-U Eligibility Guidelines Page 1 of 5 Federal Guidelines for STP-U Funding SURFACE TRANSPORTATION PROGRAM (STP) ELIGIBLE EXPENDITURES PERIOD AVAILABLE: FY + 3 Years FUND: Highway

MPC 5.f Attachment 1 STP-U Eligibility Guidelines Page 1 of 5 Federal Guidelines for STP-U Funding SURFACE TRANSPORTATION PROGRAM (STP) ELIGIBLE EXPENDITURES PERIOD AVAILABLE: FY + 3 Years FUND: Highway

General fund revenues expected to show moderate growth over the forecast horizon

A-13 REVENUE FORECAST The Commonwealth's total revenue consists of two types of resources: the general fund and nongeneral funds. About half of state revenues are "nongeneral funds," or funds earmarked

A-13 REVENUE FORECAST The Commonwealth's total revenue consists of two types of resources: the general fund and nongeneral funds. About half of state revenues are "nongeneral funds," or funds earmarked

HOUSE BILL 2587 AN ACT

Senate Engrossed House Bill State of Arizona House of Representatives Fifty-second Legislature First Regular Session 2015 HOUSE BILL 2587 AN ACT AMENDING SECTIONS 35-142 AND 35-315, ARIZONA REVISED STATUTES;

Senate Engrossed House Bill State of Arizona House of Representatives Fifty-second Legislature First Regular Session 2015 HOUSE BILL 2587 AN ACT AMENDING SECTIONS 35-142 AND 35-315, ARIZONA REVISED STATUTES;

Regional Surface Transportation Program Policy and Allocation

FY 2014-15 Regional Surface Transportation Program Policy and Allocation August 2015 Humboldt County Association of Governments 611 I Street, Suite B Eureka, CA 95501 Phone: 707.444.8208 www.hcaog.net

FY 2014-15 Regional Surface Transportation Program Policy and Allocation August 2015 Humboldt County Association of Governments 611 I Street, Suite B Eureka, CA 95501 Phone: 707.444.8208 www.hcaog.net

Arizona 1. Dependent Public School Systems (14) Arizona ranks 39th among the states in number of local governments, with 639 as of June 2002.

Arizona ranks 39th among the states in number of local governments, with 639 as of June 2002.") Arizona Arizona ranks 39th among the states in number of local governments, with 639 as of June 2002. COUNTY GOVERNMENTS (15) There are no areas in Arizona lacking county government. The county governing

Arizona Arizona ranks 39th among the states in number of local governments, with 639 as of June 2002. COUNTY GOVERNMENTS (15) There are no areas in Arizona lacking county government. The county governing

CHAPTER 4 SURFACE TRANSPORTATION PROGRAM (STP)

") Local Assistance Program Guidelines Chapter 4 CHAPTER 4 SURFACE TRANSPORTATION PROGRAM (STP) CONTENTS Section Subject Page Number 4.1 INTRODUCTION... 4-1 4.2 ELIGIBILITY CRITERIA... 4-1 General... 4-1

Local Assistance Program Guidelines Chapter 4 CHAPTER 4 SURFACE TRANSPORTATION PROGRAM (STP) CONTENTS Section Subject Page Number 4.1 INTRODUCTION... 4-1 4.2 ELIGIBILITY CRITERIA... 4-1 General... 4-1

Legislative Fiscal Bureau One East Main, Suite 301 Madison, WI 53703 (608) 266-3847 Fax: (608) 267-6873

266-3847 Fax: (608) 267-6873") Legislative Fiscal Bureau One East Main, Suite 301 Madison, WI 53703 (608) 266-3847 Fax: (608) 267-6873 February 16, 2010 TO: FROM: Members Joint Committee on Finance Bob Lang, Director SUBJECT: Governor's

Legislative Fiscal Bureau One East Main, Suite 301 Madison, WI 53703 (608) 266-3847 Fax: (608) 267-6873 February 16, 2010 TO: FROM: Members Joint Committee on Finance Bob Lang, Director SUBJECT: Governor's

SCOPE OF WORK for High Speed Rail and Intercity Passenger Rail Program Federal Grant Application Development

Draft 06162009 SCOPE OF WORK for High Speed Rail and Intercity Passenger Rail Program Federal Grant Application Development The Minnesota Department of Transportation (Mn/DOT) requires the services of

Draft 06162009 SCOPE OF WORK for High Speed Rail and Intercity Passenger Rail Program Federal Grant Application Development The Minnesota Department of Transportation (Mn/DOT) requires the services of

Legislative Fiscal Bureau One East Main, Suite 301 Madison, WI 53703 (608) 266-3847 Fax: (608) 267-6873

266-3847 Fax: (608) 267-6873") Legislative Fiscal Bureau One East Main, Suite 301 Madison, WI 53703 (608) 266-3847 Fax: (608) 267-6873 December 7, 2011 TO: FROM: Members Joint Committee on Finance Bob Lang, Director SUBJECT: Military

Legislative Fiscal Bureau One East Main, Suite 301 Madison, WI 53703 (608) 266-3847 Fax: (608) 267-6873 December 7, 2011 TO: FROM: Members Joint Committee on Finance Bob Lang, Director SUBJECT: Military

DEPARTMENT OF TRANSPORTATION

DEPARTMENT OF TRANSPORTATION UNITED STATES OF AMERICA DEPARTMENT OF TRANSPORTATION Funding Highlights: Invests a total of $74 billion in discretionary and mandatory budgetary resources for the Department

DEPARTMENT OF TRANSPORTATION UNITED STATES OF AMERICA DEPARTMENT OF TRANSPORTATION Funding Highlights: Invests a total of $74 billion in discretionary and mandatory budgetary resources for the Department

AN ACT...; relating to: the budget.

2013 2014 LEGISLATURE DOA:...Byrnes, BB0358 Expand flood damage aids appropriation to cover other disasters FOR 2013 2015 BUDGET NOT READY FOR INTRODUCTION AN ACT...; relating to: the budget. Analysis

2013 2014 LEGISLATURE DOA:...Byrnes, BB0358 Expand flood damage aids appropriation to cover other disasters FOR 2013 2015 BUDGET NOT READY FOR INTRODUCTION AN ACT...; relating to: the budget. Analysis

Matt Burress, Legislative Analyst Rebecca Pirius, Legislative Analyst Updated: September 2012. Traffic Citations

INFORMATION BRIEF Research Department Minnesota House of Representatives 600 State Office Building St. Paul, MN 55155 Matt Burress, Legislative Analyst Rebecca Pirius, Legislative Analyst Updated: September

INFORMATION BRIEF Research Department Minnesota House of Representatives 600 State Office Building St. Paul, MN 55155 Matt Burress, Legislative Analyst Rebecca Pirius, Legislative Analyst Updated: September

2005 SCHOOL FINANCE LEGISLATION Funding and Distribution

2005 SCHOOL FINANCE LEGISLATION Funding and Distribution RESEARCH REPORT # 3-05 Legislative Revenue Office State Capitol Building 900 Court Street NE, H-197 Salem, Oregon 97301 (503) 986-1266 http://www.leg.state.or.us/comm/lro/home.htm

2005 SCHOOL FINANCE LEGISLATION Funding and Distribution RESEARCH REPORT # 3-05 Legislative Revenue Office State Capitol Building 900 Court Street NE, H-197 Salem, Oregon 97301 (503) 986-1266 http://www.leg.state.or.us/comm/lro/home.htm

Federal Highway Administration 1200 New Jersey Avenue, SE Washington, DC 20590 202-366-4000

1 of 8 12/27/2013 8:21 AM U.S. Department of Transportation Federal Highway Administration 1200 New Jersey Avenue, SE Washington, DC 20590 202-366-4000 MAP-21 - Moving Ahead for Progress in the 21st Century

1 of 8 12/27/2013 8:21 AM U.S. Department of Transportation Federal Highway Administration 1200 New Jersey Avenue, SE Washington, DC 20590 202-366-4000 MAP-21 - Moving Ahead for Progress in the 21st Century

A JOINT RESOLUTION OF THE SENATE AND THE HOUSE OF REPRESENTATIVES OF THE STATE OF MONTANA REVISING THE OFFICIAL

SJ00.0 SENATE JOINT RESOLUTION NO. INTRODUCED BY B. TUTVEDT A JOINT RESOLUTION OF THE SENATE AND THE HOUSE OF REPRESENTATIVES OF THE STATE OF MONTANA REVISING THE OFFICIAL ESTIMATE OF THE STATE'S GENERAL

SJ00.0 SENATE JOINT RESOLUTION NO. INTRODUCED BY B. TUTVEDT A JOINT RESOLUTION OF THE SENATE AND THE HOUSE OF REPRESENTATIVES OF THE STATE OF MONTANA REVISING THE OFFICIAL ESTIMATE OF THE STATE'S GENERAL

State Debt Management Presentation February 2013. Kristin A. Hanson, Assistant Commissioner, Treasury

State Debt Management Presentation February 2013 Kristin A. Hanson, Assistant Commissioner, Treasury What is a Bond? Municipal bonds are debt securities issued by states, cities, counties and other governmental

State Debt Management Presentation February 2013 Kristin A. Hanson, Assistant Commissioner, Treasury What is a Bond? Municipal bonds are debt securities issued by states, cities, counties and other governmental

FINANCIAL PLAN. Any future earmarks are assumed to carry their own limitation and not reduce the regular limitation identified in these calculations.

VII. FINANCIAL PLAN FHWA Funds The Federal Highway Administration (FHWA) funds are appropriated by Congress. FHWA funding levels are identified in the six-year Transportation Act. Each year, a federal

VII. FINANCIAL PLAN FHWA Funds The Federal Highway Administration (FHWA) funds are appropriated by Congress. FHWA funding levels are identified in the six-year Transportation Act. Each year, a federal

The 2016-17 Budget: The Governor s Proposition 2 Debt Proposal

The 2016-17 Budget: The Governor s Proposition 2 Debt Proposal MAC TAYLOR LEGISLATIVE ANALYST FEBRUARY 2016 Summary Proposition 2 requires the state to pay down a minimum annual amount of state debts.

The 2016-17 Budget: The Governor s Proposition 2 Debt Proposal MAC TAYLOR LEGISLATIVE ANALYST FEBRUARY 2016 Summary Proposition 2 requires the state to pay down a minimum annual amount of state debts.

Airport and Aviation Funding Programs

Chapter 7 Airport and Aviation Funding Programs Airports and aviation projects across the nation benefit from many funding sources including the federal, state, and local units of government. Some improvement

Chapter 7 Airport and Aviation Funding Programs Airports and aviation projects across the nation benefit from many funding sources including the federal, state, and local units of government. Some improvement

RPA 14/ATURA Surface Transportation Program (STP) APPLICATION FOR FUNDS

APPLICATION FOR FUNDS") RPA 14/ATURA Surface Transportation Program (STP) APPLICATION FOR FUNDS Please provide the following information when applying to RPA 14/ATURA for Surface Transportation Program (STP) funding for projects

RPA 14/ATURA Surface Transportation Program (STP) APPLICATION FOR FUNDS Please provide the following information when applying to RPA 14/ATURA for Surface Transportation Program (STP) funding for projects

2012-2013 Transition from SAFETEA-LU to the new MAP-21 Federal Transportation Act

C h a p t e r 9 - F i n a n c i a l P l a n a n d R e c o m m e n d a t i o n s f o r T r a n s p o r t a t i o n S y s t e m I m p r o v e m e n t P r o j e c t s A major component of the Plan (T2040)

C h a p t e r 9 - F i n a n c i a l P l a n a n d R e c o m m e n d a t i o n s f o r T r a n s p o r t a t i o n S y s t e m I m p r o v e m e n t P r o j e c t s A major component of the Plan (T2040)

The financial plan was prepared in conjunction with the Technical Working Group. Refer to Table 3-1: Funding and Implementation Plan.

3 Financial Plan The purpose of the financial plan is to identify funding options that would be likely sources of money to advance recommendations made by this study. The Capitol Region Transportation

3 Financial Plan The purpose of the financial plan is to identify funding options that would be likely sources of money to advance recommendations made by this study. The Capitol Region Transportation

(1) Bases the computations for steps 1, 2 and 5 on net enrollment only, eliminating the adjusted enrollment limits;

Bases the computations for steps 1, 2 and 5 on net enrollment only, eliminating the adjusted enrollment limits;") STATE OF WEST VIRGINIA EXECUTIVE SUMMARY OF THE PUBLIC SCHOOL SUPPORT PROGRAM BASED ON THE FINAL COMPUTATIONS FOR THE 2011-12 YEAR The Public School Support Program (PSSP) is a plan of financial support

STATE OF WEST VIRGINIA EXECUTIVE SUMMARY OF THE PUBLIC SCHOOL SUPPORT PROGRAM BASED ON THE FINAL COMPUTATIONS FOR THE 2011-12 YEAR The Public School Support Program (PSSP) is a plan of financial support

Property Type. Minnesota Property Tax Class Rates Payable in 2010

Property Taxes Property Taxes Property tax revenues account for 33% of general fund revenue. In any given year several factors affect how much an individual property owner pays in city property taxes,

Property Taxes Property Taxes Property tax revenues account for 33% of general fund revenue. In any given year several factors affect how much an individual property owner pays in city property taxes,

Table of Contents 2016-17 Biennial Budget Revenue, Department of

Table of Contents 2016-17 Biennial Budget Revenue, Department of Agency Profile Revenue, Department of... 1 Tax System Management... 3 Debt Collection... 6 Minnesota Department of Revenue www.revenue.state.mn.us

Table of Contents 2016-17 Biennial Budget Revenue, Department of Agency Profile Revenue, Department of... 1 Tax System Management... 3 Debt Collection... 6 Minnesota Department of Revenue www.revenue.state.mn.us

ORANGE COUNTY TRANSPORTATION AUTHORITY. Final Long-Range Transportation Plan - Destination 2035. Attachment A

ORANGE COUNTY TRANSPORTATION AUTHORITY Final Long-Range Transportation Plan - Destination 2035 Attachment A DESTINATION 2035 DESTINATION 2035 EXECUTIVE SUMMARY ATTACHMENT A Moving Toward a Greener Tomorrow

ORANGE COUNTY TRANSPORTATION AUTHORITY Final Long-Range Transportation Plan - Destination 2035 Attachment A DESTINATION 2035 DESTINATION 2035 EXECUTIVE SUMMARY ATTACHMENT A Moving Toward a Greener Tomorrow

administrative subdivisions of the counties and are not counted as separate governments in census statistics on governments. IOWA

IOWA Iowa ranks 17th among the states in number of local governments with 1,954 as of October 2007. COUNTY GOVERNMENTS (99) There are no areas in Iowa lacking county government. The county governing body

IOWA Iowa ranks 17th among the states in number of local governments with 1,954 as of October 2007. COUNTY GOVERNMENTS (99) There are no areas in Iowa lacking county government. The county governing body

Operating Budget. MARIN TRANSIT 2016 2025 SHORT RANGE TRANSIT PLAN Chapter 5: Financial Plan

Operating Budget Marin Transit forecasts revenues and expenses for the 10-year period based on current contract rates, annual escalations, historical trends, and partner agencies revenue projections. Marin

Operating Budget Marin Transit forecasts revenues and expenses for the 10-year period based on current contract rates, annual escalations, historical trends, and partner agencies revenue projections. Marin

GENERAL. This manual addresses five local programs that are funded under the current Highway Act:

OVERVIEW The Local Public Agency Manual published by the Missouri Department of Transportation (MoDOT) is intended to be used as a guide for cities and counties that sponsor projects utilizing federal

OVERVIEW The Local Public Agency Manual published by the Missouri Department of Transportation (MoDOT) is intended to be used as a guide for cities and counties that sponsor projects utilizing federal

CONNECTICUT S TOP TRANSPORTATION ISSUES:

CONNECTICUT S TOP TRANSPORTATION ISSUES: Meeting the State s Need for Safe, Smooth and Efficient Mobility NOVEMBER 2015 202-466-6706 tripnet.org Founded in 1971, TRIP of Washington, DC, is a nonprofit

CONNECTICUT S TOP TRANSPORTATION ISSUES: Meeting the State s Need for Safe, Smooth and Efficient Mobility NOVEMBER 2015 202-466-6706 tripnet.org Founded in 1971, TRIP of Washington, DC, is a nonprofit

JAN 2 2 2016. amended by adding a new section to be appropriately designated. costs of construction and operation incurred by a contractor

THE SENATE WENTY-EIGHTH LEGISLATURE, 0 STATE OF HAWAII JAN 0 S.B. NO. - A BILL FOR AN ACT RELATING TO TAXATION BE IT ENACTED BY THE LEGISLATURE OF THE STATE OF HAWAII: SECTION. Chapter, Hawaii Revised

THE SENATE WENTY-EIGHTH LEGISLATURE, 0 STATE OF HAWAII JAN 0 S.B. NO. - A BILL FOR AN ACT RELATING TO TAXATION BE IT ENACTED BY THE LEGISLATURE OF THE STATE OF HAWAII: SECTION. Chapter, Hawaii Revised

SECTION D CAPITAL PROGRAM CAPITAL PROGRAM 1999 2013 D 1 FEDERAL TAX LAW D 2 STATUTORY DEBT LIMIT D 2 FINANCING SUMMARY D 3 AGENCY DETAIL D 4

SECTION D CAPITAL PROGRAM CAPITAL PROGRAM 1999 2013 D 1 FEDERAL TAX LAW D 2 STATUTORY DEBT LIMIT D 2 FINANCING SUMMARY D 3 AGENCY DETAIL D 4 Capital Budget CAPITAL BUDGET 1999 2013 RECOMMENDED EXECUTIVE

SECTION D CAPITAL PROGRAM CAPITAL PROGRAM 1999 2013 D 1 FEDERAL TAX LAW D 2 STATUTORY DEBT LIMIT D 2 FINANCING SUMMARY D 3 AGENCY DETAIL D 4 Capital Budget CAPITAL BUDGET 1999 2013 RECOMMENDED EXECUTIVE

Explaining Federal, State and Local Government Responsibilities in Virginia

Explaining Federal, State and Local Government Responsibilities in Virginia System of Federalism We all benefit from the services of government every day. Each layer of government federal, state and local

Explaining Federal, State and Local Government Responsibilities in Virginia System of Federalism We all benefit from the services of government every day. Each layer of government federal, state and local

the sixth class. Eighth class--fewer than 20,000 inhabitants PENNSYLVANIA

PENNSYLVANIA Pennsylvania ranks 2nd among the states in number of local governments, with 4,871 as of October 2007. COUNTY GOVERNMENTS (66) The entire area of the state is encompassed by county government

PENNSYLVANIA Pennsylvania ranks 2nd among the states in number of local governments, with 4,871 as of October 2007. COUNTY GOVERNMENTS (66) The entire area of the state is encompassed by county government

NEW JERSEY. New Jersey ranks 24th among the states in number of local governments, with 1,383 as of October 2007. COUNTY GOVERNMENTS (21)

") NEW JERSEY New Jersey ranks 24th among the states in number of local governments, with 1,383 as of October 2007. COUNTY GOVERNMENTS (21) There are no areas in New Jersey lacking county government. The

NEW JERSEY New Jersey ranks 24th among the states in number of local governments, with 1,383 as of October 2007. COUNTY GOVERNMENTS (21) There are no areas in New Jersey lacking county government. The

2014 County Ballot Issues Results General Election November 4th

Moving Alachua County Forward One Percent Transportation Sales Surtax Tourist Development Tax Valorem Tax Exemptions for New Businesses and Expansions of Existing Businesses One-half Cent Sales Surtax

Moving Alachua County Forward One Percent Transportation Sales Surtax Tourist Development Tax Valorem Tax Exemptions for New Businesses and Expansions of Existing Businesses One-half Cent Sales Surtax

SURFACE TRANSPORTATION PROGRAM (STP) PROCEDURES FOR THE OKLAHOMA CITY URBANIZED AREA FUNDS

PROCEDURES FOR THE OKLAHOMA CITY URBANIZED AREA FUNDS") SURFACE TRANSPORTATION PROGRAM (STP) PROCEDURES FOR THE OKLAHOMA CITY URBANIZED AREA FUNDS October 2015 Background The Surface Transportation Program (STP) was originally established as Section 133 of

SURFACE TRANSPORTATION PROGRAM (STP) PROCEDURES FOR THE OKLAHOMA CITY URBANIZED AREA FUNDS October 2015 Background The Surface Transportation Program (STP) was originally established as Section 133 of

State Property Tax Credits (School Levy, First Dollar, and Lottery and Gaming Credits)

") State Property Tax Credits (School Levy, First Dollar, and Lottery and Gaming Credits) Informational Paper 21 Wisconsin Legislative Fiscal Bureau January, 2013 Wisconsin Legislative Fiscal Bureau January,

State Property Tax Credits (School Levy, First Dollar, and Lottery and Gaming Credits) Informational Paper 21 Wisconsin Legislative Fiscal Bureau January, 2013 Wisconsin Legislative Fiscal Bureau January,