Banking Regulation and Supervision Agency of Turkey (BRSA)

|

|

|

- Pearl Montgomery

- 8 years ago

- Views:

Transcription

1 Banking Regulation and Supervision Agency of Turkey (BRSA) Tuba GEÇER ER Senior Bank Examiner Başak ak YETİŞ İŞEN TEKER Banking Specialist Moscow, 28 September 2011

2 Who We Are Banking Regulation and Supervision Agency Independent Banking Authority Established in 2000 Regulation and supervision of the banking sector Its mission to provide safeness and soundness of financial markets in Turkey 1

3 Goals and Duties of BRSA The Fundemental Goals of BRSA are: To ensure the confidence and stability in financial markets, To provide effective operating of loan system and, To safeguard the rights and interests of depositors. The Fundemental Duties of BRSA are: To take necessary decisions and measures in order to protect the rights of depositors and ensure sound operating of the credit system and to implement them, To regulate, enforce and ensure the enforcement thereof, to monitor and supervise the implementation of establishment and activities, management and organizational structure, merger, disintegration, change of shares and liquidation of banks and financial holding companies as well as leasing, factoring and financing companies without prejudice to the provisions of other laws and related legislation. 2

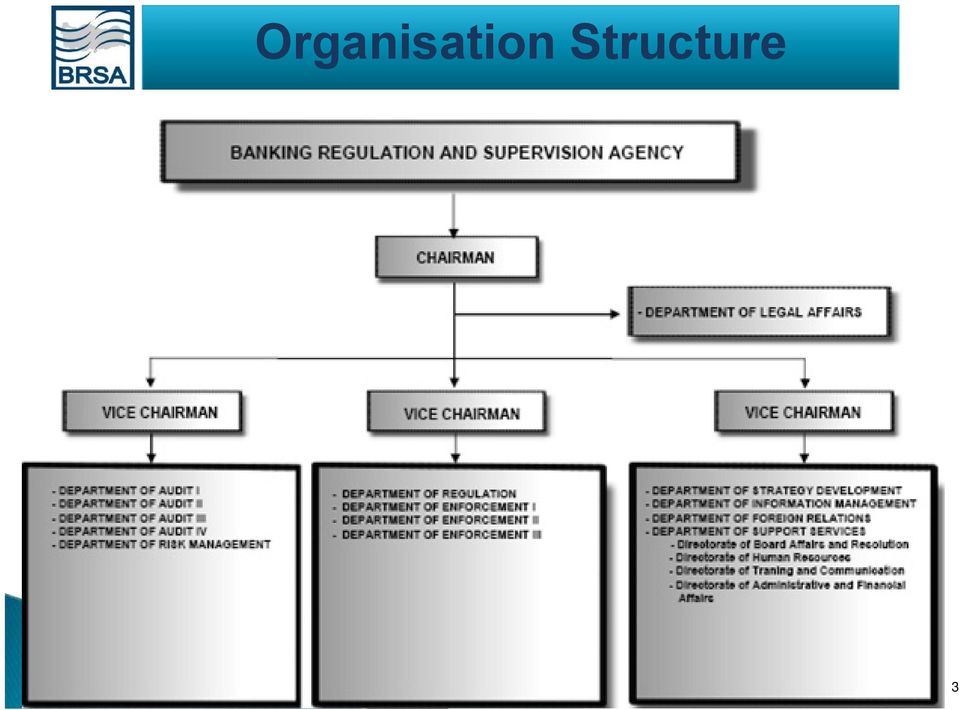

4 Organisation Structure 3

5 The Scope of Operations LICENSING AND ENFORCEMENT ACTIVITIES 4

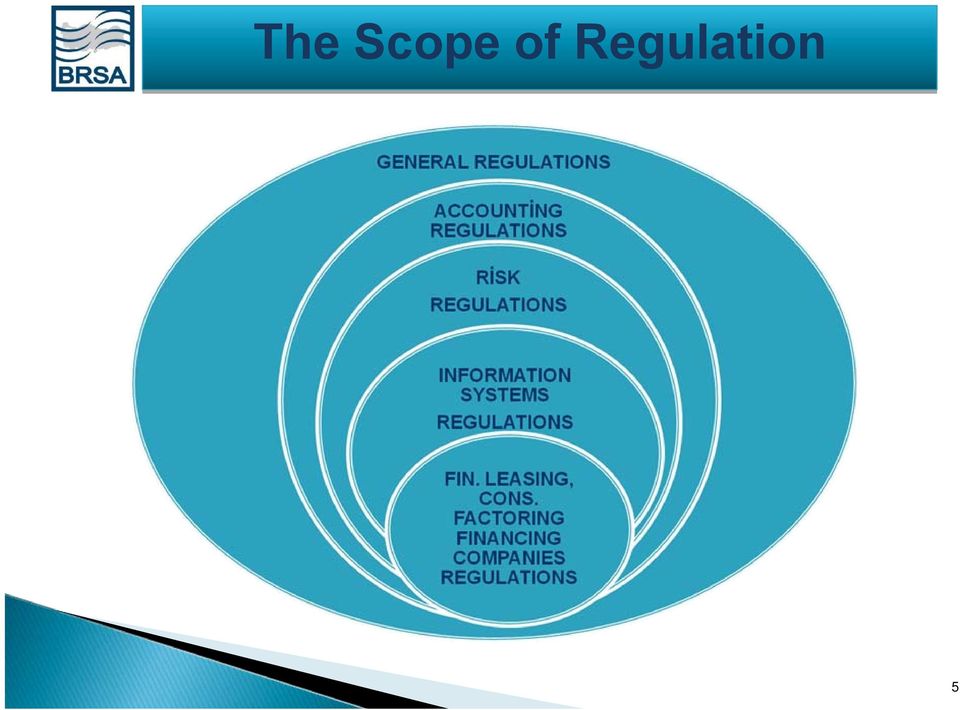

6 The Scope of Regulation 5

7 The Main Regulations (I) Banking Law No: 5411 (Banking Law 4389 is former one) Bank Cards and Credit Cards Law Fundamental sub-regulations: Regulation on own funds Regulation on credit operations Regulation on capital adequacy ratio (CAR) Regulation on liquidity Regulation on ratio of net foreign currency positions (FX regulation) 6

8 The Main Regulations (II) Fundamental sub-regulations: Regulation on the banks corparate management principles Regulation on rating agencies Regulation on classification and provisioning of loans and nonperforming loans (NPLs) Regulation on interest rate risk in the banking book Regulation on internal system of banks Regulation on financial holding companies 7

9 Integration to International Standards 8

10 Convergence to Best Practices Convergence Uniformity From our understanding, convergence means; moving closer to each other based on best practices but still being able to take into account national specificities! INTERNATIONAL PERSPECTIVE NATIONAL SPECIFICITIES important: Balance! 9

11 Basel-II Road Map PARALLEL RUN Only for Reporting Not any sanction THE COMMENCEMENT DATE of BASEL-II Only Standardised Approach for Credit and Operational Risk 10

12 The Risk Components of Basel II 11

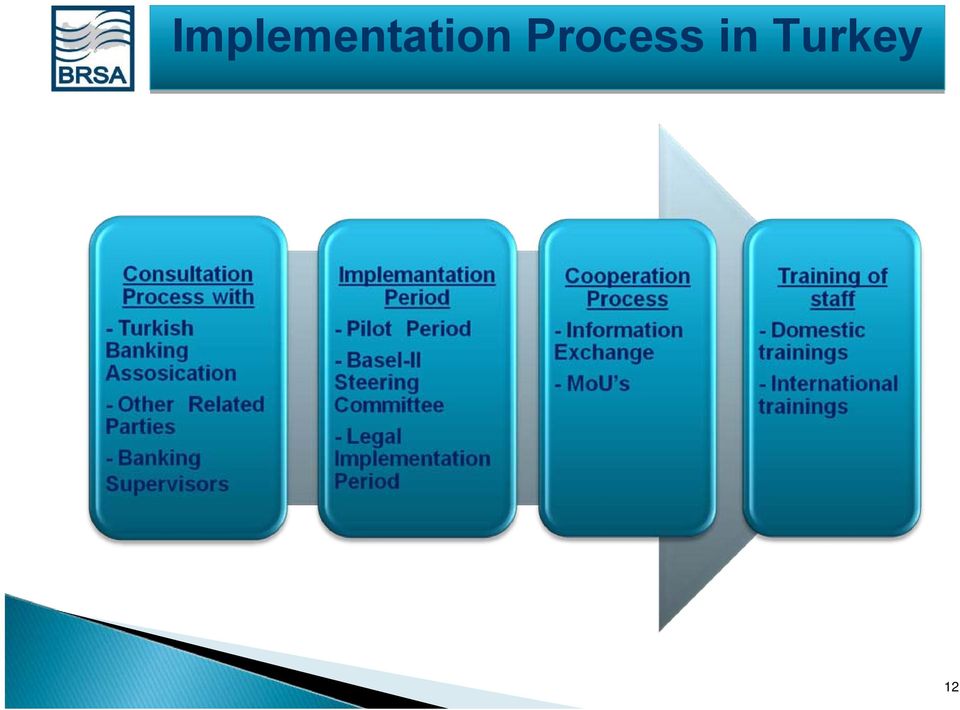

13 Implementation Process in Turkey 12

14 From The World From International Press: The Banker 30 June, 2011 Good regulation (and dose of good luck) in countries such as CANADA and TURKEY proved its worth during the last crisis Turkey s Renaissance: From Banking Crisis to Economic Revival From the IMF By Hugh Bredenkamp, Mats Josefsson, and Carl-Johan Lindgren 13

15 The Pre-crisis Conditions of Turkish Banking Sector (Pre- 2001) Inadequate capital base Small and fragmented banking structure Dominance of state banks in total banking sector Weak asset quality (concentrated credits, group banking and concentrated risks, mismatch between loans and provisions) Extreme exposure and fragility towards market risk (maturity mismatch, FX open position) Inadequate internal control systems, risk management and corporate governance Lack of transparency 14

Inadequate internal control systems, risk management and corporate governance Lack of")

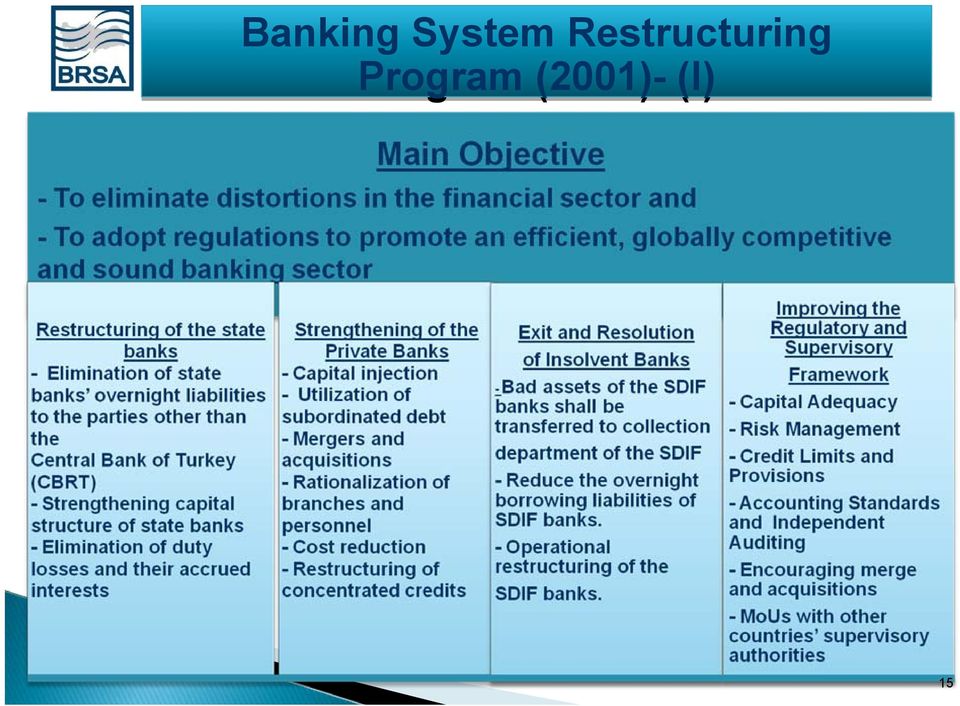

16 Banking System Restructuring Program (2001)- (I) 15

17 Banking System Restructuring Program (2001)- (II) BANKING SECTOR RESTRUCTURING PROGRAM State Bank Reform Strong Capital Base T.C Hazine İhracı YP Kamu Menkul Kıymetleri İçin Spesifik Risk Cost Efficiency Efficient Supervision Market Discipline and Transparency Sound Banking Strong Economy and Sustainabl e Growth Enviroment Corporate Restructuring Structural Reform Macroeconomic Stability Decline in Public Deficit 16

18 The Results of Restructuring Program Consolidation in the banking sector Increase in mergers and acquisitions Decline in the share of the State and the SDIF Banks Removal of distortionary effects of insolvent and state banks on interest rate Reduction of financial risks to manageable levels Strengthened the capital structure Improved transparency in financial statements Improved regulatory and supervisory framework 17

19 The Consolidation Process of Turkish Banking Sector Commercial Banks State Private Foreign SDIF Participation Banks Invest. & Dev. Banks TOTAL

20 What We Did For the Prudent Regulation 19

21 The Current Situation 12 March 2009 FSB Membership 25 May 2009 Basel Committee on Banking Supervision Supervision Committee Membership As a member country of G-20, BRSA undertakes the adopt Basel III reforms. 20

22 SUPERVISION Risk Based Supervision (is what we do) 21

23 Why Risk Based Supervision (RBS)? When and why we started RBS? (21 deposit banks failed from 1998 to 2003) 22

24 What is this thing called RBS? The focus of RBS is to identify, measure, control and monitor the risks arise from banking activities and to evaluate the adequacy of internal audit and risk management The aim of RBS is to ensure that banks are understanding and controlling levels and types of risks they face, not to prevent banks from taking risks. 23

25 So what are the risks? Credit Risk, Interest Rate Risk, Liquidity Risk, Market Risk, Foreign Exchange Risk, Operational Risk, Compliance Risk, Strategic Risk, Reputational Risk. These risks constitute the risk profile of the bank 24

26 Risk Based Supervision Scope, frequency and intensity of supervisory methods used in the audits are decided by not only taking into account bank s risk profile but also the quality of bank s internal control and risk management systems. (we check the checkers) 25

27 Risk Based Supervision is Proactive monitoring the risks, mitigating risks before the loss, taking precaution to increase the quality of risk management and internal audit Flexible supervision is tailored for each bank according to degree of reliability of the bank risk management and internal audit system, 26

28 Classical Supervision & Risk Based Supervision-1 Differences Classical Approach Risk Based Approach Focus of Supervision Confirming the accuracy of the financial statements and revaluation of the bank assets. Evaluation of Bank s internal control and risk management systems taking into account the risk profile of the bank Consistency Supervision bases on a certain date (balance sheet date). Supervision is consistent and dynamic. Communication Between Supervisors and Bank Management There is less communication with bank management. Supervisors communicate with bank management via formal/informal meetings, letters and audit reports. 27

29 Classical Supervision & Risk Based Supervision-2 Differences Classical Approach Risk Based Approach Investigation Procedure Focuses on the past. Determining the values of bank assets and determining the strength and reliability of bank at an exact time. Focuses on the future Evaluating the procedures used to manage existing and future risks. Organizational Area aims to investigate risk management applications in which the bank is licensed. focuses on basic activities of the bank, risks which are caused by mentioned activities and risk management systems. Monitoring of Bank Operations Monitoring and evaluations are exercised with the help of audit reports prepared annually and quarterly. Monitoring and evaluations are consistent. More interaction with staff Internal systems are consistently evaluated. 28

30 Classical Supervision & Risk Based Supervision-3 Differences Classical Approach Risk Based Approach Point of View Supervision Plan Bottom-up approach Aims to identify and quantify the results of the problems. Planning audit activities depends on the bank. Investigations are carried out according to the procedures provided from inspection guide. Top-down approach. Aims to determine the causes of the problems. Planning audit activities depends on the bank s main risk areas and risk profile. Allocation of Supervision Sources Audit teams are short-lived. Auditors usually don t have specific information about the organization of the bank. A stable audit team is formed. This team has information and experience about the organization of the bank 29

31 Classical Supervision & Risk Based Supervision-4 Differences Classical Approach Risk Based Approach Application Point of View Reactive Correction of the incorrect applications or compensation of the actual damages detected in supervisions. Proactive (reactive in case of necessity) Reduction of the incorrect application and the possible damages by eliminating the systemic or organizational problems may result in incorrect application. Focus of Application Correction of the results of the detected problems. Correction of the causes of actual or possible problems. 30

32 Classical Supervision & Risk Based Supervision-5 Differences Classical Approach Risk Based Approach Application Tools (Administrative) Application Tools (Administrative) Instructions. Administrative fine Judicial discipline. Meeting with bank management, Persuasion, Risk-reduction program, Action plan, Instruction. Increase minimum capital, Adequacy ratio, Increase deposit insurance premium, Restrict activities, Reduce risks, Restrict organization, Administrative fine, Judicial discipline. 31

33 How do we supervise? (our supervision cycle, rating system, CAMELS, reports and more) 32

34 Supervision Cycle How long it takes to supervise? Supervision consists of independent processes that are repeated in cycles and follow each other. Depends on bank's risk profile, size, diversity and complexity of activities on (We actually never leave the banks) 33

35 Who is to supervise? Audit Groups Bank Auditors and Assistants Banking Specialists and Assistants Headed by a Group Leader At least 5 years experience on-site supervision, Coordination of audit and execution of works, 3 years duration for accumulation of information on bank 34

36 How do we assess the risks? r s? Previous risk assessment report Meeting with previous audit team, Expectations and policies of the bank for the future, Meetings performed with upper and middle level managers, Surveillance reports, News in public and media, Independent audit reports Correspondence with BRSA and other public institutions, Board of directors & audit committee minutes. ( and come up with the risk profile of the bank ) 35

37 We have a plan Audit Plan Prepared by the group leaders, Approved by the upper management of BRSA The scope and the level of surveillance/audit are determined. 36

38 Execution of Audit BRSA audit system consist of two basic activities On-Site Supervision Off-Site Supervision which support and complement each other. 37

39 On-Site Supervision Analysis of the connections between Banks' assets, liabilities, equity, debt, profit and loss accounts, commitments and all other factors affecting the financial structure, Investigation of the adequacy and effectiveness of risk management and internal control systems, Determination of risk assessment and risk profile, Supervision of the financial tables and records according to accounting principles and auditing standards, Analysis of the adequacy and reliability of the information systems. 38

40 On-Site Supervision Supervision the activities compliance with the Banking Law No and in the other laws about the institutions under this Act. Consolidated supervision of financial holding company, bank subsidiaries and jointly controlled subsidiaries Assessing the quality of corporate management Supervision the activities of real and legal persons that provide services to organization, Investigation subjects relating to operation that are special, Consist of other on-site supervision activities. 39

41 On-Site Supervision Risk Assessment CAMELS, Branch Supervision, Compliance, Denunciation and Complaint Investigations, Investigation sent by the Prosecution, Anti-money Laundering Investigations 40

42 On-Site Supervision Sector Analysis, Factoring Supervision, Leasing Supervision, Consumer Finance Company Supervision, Asset Management Company Supervision, External Audit Company Supervision, 41

43 Our Rating System : CAMELS In the evaluation of Banks financial structure and competencies related to management and organization the CAMELS Rating System is used. CAMELS consist of 6 main evaluation criteria: C Capital Adequacy A Asset Quality M Managerial Ability E Earnings L Liquidity S Sensitivity to Market Risk 42

44 CAMELS-2 Each financial institution is given a compound (final) degree from 1 to 5 which result from evaluations of six components (C-A-M-E-L-S). 1 refers to maximum degree, strongest performance and risk management system, and minimum audit requirement; 5 refers to minimum degree, weakest performance and inadequate risk management, and consequently to the maximum audit requirement. (these degrees have an effect on deposit insurance premium) 43

45 CAMELS-3 Harmonizing with varying conditions and risks, and ability to manage new problems which may be encountered in new activity fields are important factors for the evaluation of general risk profile of financial institute. Therefore the management component should be paid special attention during compound marking. The managerial ability to define, measure, monitor, and control the risks arise from banking activities is also important when marking each component. (M is the most important letter of CAMELS) 44

46 Off-Site Supervision-1 Carried out by Audit Teams, Routine monitoring on solo and consolidated basis, Monitoring on the basis of high risk activities, Monitoring the results of the instructions given to the Banks, Analytical investigations from surveillance data, Monitoring of developments in credit, interest rate, foreign exchange and liquidity risk, Stress tests and scenario analysis, Monitoring and evaluation of financial structure and the process of change in performance with periodic reports. 45

47 Off-Site Supervision-2 Monitoring the development of rating grades by using the previous audit results and recent datas, Providing perception of change in financial structure and performance by early warning systems on time, Monitoring and analysis of financial developments on the basis of sector and organization. 46

48 Banking Data Transfer System Reports (Period) Daily, Weekly, Monthly, Quarterly, Annually Reports (Type) Solo, Consolidated Reports (Type) Bank, Islamic Bank, Independent Audit, Foreign Reporting (Associates, Subsidiaries, Jointly Controlled Companies), Non-Bank Financial Institutions(Factoring, Leasing, Consumer Finance) Asset Management Companies Financial Holding Companies (and numerous other reports we can produce) 47

49 Final Meeting Findings are shared with bank s senior management with coordination of the group leader in the final meeting and the report is submitted to the Audit Department. (of course some findings may be inconvenient to share with the bank) 48

50 What happens as a result of the reports? Implementation of the suggestions contained in reports Special warnings, precautions, fines to the Bank Sectoral warnings and precautions. ( what we all do is for the safety and soundness of the banks ) 49

51 THE END 50

THE EARLY WARNING SYSTEM PRESENTATION DEFINITION

THE EARLY WARNING SYSTEM PRESENTED BY: PETER GATERE MANGER, BANK SUPERVISION CENTRAL BANK OF KENYA 1 PRESENTATION Definition Background Objectives of an early warning system Role of qualitative information

THE EARLY WARNING SYSTEM PRESENTED BY: PETER GATERE MANGER, BANK SUPERVISION CENTRAL BANK OF KENYA 1 PRESENTATION Definition Background Objectives of an early warning system Role of qualitative information

Foreword 28. Introduction 30. Structure of the banking system 31. Why banking stability is important 33. Licensing requirements for banks 34

C ONTENTS Page Foreword 28 Introduction 30 Structure of the banking system 31 Why banking stability is important 33 Licensing requirements for banks 34 How the HKMA supervises banks 36 Conclusion 45 Frequently

C ONTENTS Page Foreword 28 Introduction 30 Structure of the banking system 31 Why banking stability is important 33 Licensing requirements for banks 34 How the HKMA supervises banks 36 Conclusion 45 Frequently

MISSION VALUES. The guide has been printed by:

www.cudgc.sk.ca MISSION We instill public confidence in Saskatchewan credit unions by guaranteeing deposits. As the primary prudential and solvency regulator, we promote responsible governance by credit

www.cudgc.sk.ca MISSION We instill public confidence in Saskatchewan credit unions by guaranteeing deposits. As the primary prudential and solvency regulator, we promote responsible governance by credit

Policy on the Management of Country Risk by Credit Institutions

2013 Policy on the Management of Country Risk by Credit Institutions 1 Policy on the Management of Country Risk by Credit Institutions Contents 1. Introduction and Application 2 1.1 Application of this

2013 Policy on the Management of Country Risk by Credit Institutions 1 Policy on the Management of Country Risk by Credit Institutions Contents 1. Introduction and Application 2 1.1 Application of this

LIQUIDITY RISK MANAGEMENT GUIDELINE

LIQUIDITY RISK MANAGEMENT GUIDELINE April 2009 Table of Contents Preamble... 3 Introduction... 4 Scope... 5 Coming into effect and updating... 6 1. Liquidity risk... 7 2. Sound and prudent liquidity risk

LIQUIDITY RISK MANAGEMENT GUIDELINE April 2009 Table of Contents Preamble... 3 Introduction... 4 Scope... 5 Coming into effect and updating... 6 1. Liquidity risk... 7 2. Sound and prudent liquidity risk

Capital Adequacy: Advanced Measurement Approaches to Operational Risk

Prudential Standard APS 115 Capital Adequacy: Advanced Measurement Approaches to Operational Risk Objective and key requirements of this Prudential Standard This Prudential Standard sets out the requirements

Prudential Standard APS 115 Capital Adequacy: Advanced Measurement Approaches to Operational Risk Objective and key requirements of this Prudential Standard This Prudential Standard sets out the requirements

Contents. About the author. Introduction

Contents About the author Introduction 1 Retail banks Overview: bank credit analysis and copulas Bank risks Bank risks and returns: the profitability, liquidity and solvency trade-off Credit risk Liquidity

Contents About the author Introduction 1 Retail banks Overview: bank credit analysis and copulas Bank risks Bank risks and returns: the profitability, liquidity and solvency trade-off Credit risk Liquidity

REPORT OF THE SUPERVISORY BOARD ON OPERATION IN 2013 AND ORIENTATION FOR 2014

JSC BANK FOR FOREIGN TRADE OF VIET NAM Address: 198 Tran Quang Khai St, Ha No Business Registration No. 0100112437 (8 th revision dated 1 st August, 2013) SOCIALIST REPUBLIC OF VIETNAM Independence - Freedom

JSC BANK FOR FOREIGN TRADE OF VIET NAM Address: 198 Tran Quang Khai St, Ha No Business Registration No. 0100112437 (8 th revision dated 1 st August, 2013) SOCIALIST REPUBLIC OF VIETNAM Independence - Freedom

GUIDELINES ON RISK MANAGEMENT AND INTERNAL CONTROLS FOR INSURANCE AND REINSURANCE COMPANIES

20 th February, 2013 To Insurance Companies Reinsurance Companies GUIDELINES ON RISK MANAGEMENT AND INTERNAL CONTROLS FOR INSURANCE AND REINSURANCE COMPANIES These guidelines on Risk Management and Internal

20 th February, 2013 To Insurance Companies Reinsurance Companies GUIDELINES ON RISK MANAGEMENT AND INTERNAL CONTROLS FOR INSURANCE AND REINSURANCE COMPANIES These guidelines on Risk Management and Internal

NEED OF FINANCIAL INSTITUTIONS SUPERVISION THROUGH AN SINGLE FRAMEWORK OF MACRO-PRUDENTIAL SUPERVISION

NEED OF FINANCIAL INSTITUTIONS SUPERVISION THROUGH AN SINGLE FRAMEWORK OF MACRO-PRUDENTIAL SUPERVISION MEDAR LUCIAN-ION, Professor PHD, CHIRTOC IRINA-ELENA, Assistant professor PHD, CONSTANTIN BRANCUSI

NEED OF FINANCIAL INSTITUTIONS SUPERVISION THROUGH AN SINGLE FRAMEWORK OF MACRO-PRUDENTIAL SUPERVISION MEDAR LUCIAN-ION, Professor PHD, CHIRTOC IRINA-ELENA, Assistant professor PHD, CONSTANTIN BRANCUSI

Basel II, Pillar 3 Disclosure for Sun Life Financial Trust Inc.

Basel II, Pillar 3 Disclosure for Sun Life Financial Trust Inc. Introduction Basel II is an international framework on capital that applies to deposit taking institutions in many countries, including Canada.

Basel II, Pillar 3 Disclosure for Sun Life Financial Trust Inc. Introduction Basel II is an international framework on capital that applies to deposit taking institutions in many countries, including Canada.

GUIDELINES ON CORPORATE GOVERNANCE FOR LABUAN BANKS

GUIDELINES ON CORPORATE GOVERNANCE FOR LABUAN BANKS 1.0 Introduction 1.1 Good corporate governance practice improves safety and soundness through effective risk management and creates the ability to execute

GUIDELINES ON CORPORATE GOVERNANCE FOR LABUAN BANKS 1.0 Introduction 1.1 Good corporate governance practice improves safety and soundness through effective risk management and creates the ability to execute

ZAG BANK BASEL II & III PILLAR 3 DISCLOSURES. December 31, 2014

ZAG BANK BASEL II & III PILLAR 3 DISCLOSURES December 31, 2014 Zag Bank (the Bank ) is required to make certain disclosures to meet the requirements of the Office of the Superintendent of Financial Institutions

ZAG BANK BASEL II & III PILLAR 3 DISCLOSURES December 31, 2014 Zag Bank (the Bank ) is required to make certain disclosures to meet the requirements of the Office of the Superintendent of Financial Institutions

Financial Architecture and Banking Systems

Financial Architecture and Banking Systems Financial and Private Sector Development Financial Systems Practice The World Bank Group Our Mission The Financial Architecture and Banking Systems Service Line

Financial Architecture and Banking Systems Financial and Private Sector Development Financial Systems Practice The World Bank Group Our Mission The Financial Architecture and Banking Systems Service Line

Risk Management. Credit Risk Management

Risk Management In response to market changes, the Bank intensified proactive risk management to improve the Group s overall risk control capability. Credit Risk Management The Bank made deeper adjustments

Risk Management In response to market changes, the Bank intensified proactive risk management to improve the Group s overall risk control capability. Credit Risk Management The Bank made deeper adjustments

Strategic Planning and Organizational Structure Standard

Table of contents Strategic Planning and Organizational Structure Standard 1. General provisions Grounds for application of the Standard Provisions of the Standard 2. Contents of the Standard 3. Corporate

Table of contents Strategic Planning and Organizational Structure Standard 1. General provisions Grounds for application of the Standard Provisions of the Standard 2. Contents of the Standard 3. Corporate

Guidelines. ADI Authorisation Guidelines. www.apra.gov.au Australian Prudential Regulation Authority. April 2008

Guidelines ADI Authorisation Guidelines April 2008 www.apra.gov.au Australian Prudential Regulation Authority Disclaimer and copyright These guidelines are not legal advice and users are encouraged to

Guidelines ADI Authorisation Guidelines April 2008 www.apra.gov.au Australian Prudential Regulation Authority Disclaimer and copyright These guidelines are not legal advice and users are encouraged to

Key matters in examining Liquidity Risk Management at Large Complex Financial Groups

Key matters in examining Liquidity Risk Management at Large Complex Financial Groups (1) Governance of liquidity risk management Senior management of a large complex financial group (hereinafter referred

Key matters in examining Liquidity Risk Management at Large Complex Financial Groups (1) Governance of liquidity risk management Senior management of a large complex financial group (hereinafter referred

Basel Committee on Banking Supervision

Basel Committee on Banking Supervision Liquidity coverage ratio disclosure standards January 2014 (rev. March 2014) This publication is available on the BIS website (www.bis.org). Bank for International

Basel Committee on Banking Supervision Liquidity coverage ratio disclosure standards January 2014 (rev. March 2014) This publication is available on the BIS website (www.bis.org). Bank for International

News Release January 28, 2016. Performance Review: Quarter ended December 31, 2015

News Release January 28, 2016 Performance Review: Quarter ended December 31, 20% year-on-year growth in total domestic advances; 24% year-on-year growth in retail advances 18% year-on-year growth in current

News Release January 28, 2016 Performance Review: Quarter ended December 31, 20% year-on-year growth in total domestic advances; 24% year-on-year growth in retail advances 18% year-on-year growth in current

Statement of Principles

Statement of Principles Bank Registration and Supervision Prudential Supervision Department Document Issued: 2 TABLE OF CONTENTS Subject Page A. INTRODUCTION... 3 B. PURPOSES OF BANK REGISTRATION AND SUPERVISION...

Statement of Principles Bank Registration and Supervision Prudential Supervision Department Document Issued: 2 TABLE OF CONTENTS Subject Page A. INTRODUCTION... 3 B. PURPOSES OF BANK REGISTRATION AND SUPERVISION...

Risk Management Programme Guidelines

Risk Management Programme Guidelines Submissions are invited on these draft Reserve Bank risk management programme guidelines for non-bank deposit takers. Submissions should be made by 29 June 2009 and

Risk Management Programme Guidelines Submissions are invited on these draft Reserve Bank risk management programme guidelines for non-bank deposit takers. Submissions should be made by 29 June 2009 and

Principles for An. Effective Risk Appetite Framework

Principles for An Effective Risk Appetite Framework 18 November 2013 Table of Contents Page I. Introduction... 1 II. Key definitions... 2 III. Principles... 3 1. Risk appetite framework... 3 1.1 An effective

Principles for An Effective Risk Appetite Framework 18 November 2013 Table of Contents Page I. Introduction... 1 II. Key definitions... 2 III. Principles... 3 1. Risk appetite framework... 3 1.1 An effective

Eighth UNCTAD Debt Management Conference

Eighth UNCTAD Debt Management Conference Geneva, 14-16 November 2011 Debt Resolution Mechanisms: Should there be a Statutory Mechanism for Resolving Debt Crises? by Mr. Hakan Tokaç Deputy Director General

Eighth UNCTAD Debt Management Conference Geneva, 14-16 November 2011 Debt Resolution Mechanisms: Should there be a Statutory Mechanism for Resolving Debt Crises? by Mr. Hakan Tokaç Deputy Director General

EASTERN CARIBBEAN CENTRAL BANK

EASTERN CARIBBEAN CENTRAL BANK GUIDELINES ON CREDIT RISK MANAGEMENT FOR INSTITUTIONS LICENSED TO CONDUCT BANKING BUSINESS UNDER THE BANKING ACT Prepared by the BANK SUPERVISION DEPARTMENT May 2009 TABLE

EASTERN CARIBBEAN CENTRAL BANK GUIDELINES ON CREDIT RISK MANAGEMENT FOR INSTITUTIONS LICENSED TO CONDUCT BANKING BUSINESS UNDER THE BANKING ACT Prepared by the BANK SUPERVISION DEPARTMENT May 2009 TABLE

Saxo Capital Markets CY Limited

Saxo Capital Markets CY Limited DISCLOSURES IN ACCORDANCE WITH THE REGULATION FOR THE CAPITAL REQUIREMENTS OF INVESTMENT FIRMS FOR THE YEAR ENDED 31 DECEMBER 2014 MAY 2015 CONTENTS 1. GENERAL INFORMATION

Saxo Capital Markets CY Limited DISCLOSURES IN ACCORDANCE WITH THE REGULATION FOR THE CAPITAL REQUIREMENTS OF INVESTMENT FIRMS FOR THE YEAR ENDED 31 DECEMBER 2014 MAY 2015 CONTENTS 1. GENERAL INFORMATION

T.C. ZIRAAT BANKASI A.S. 2014 US Resolution Plan. Public Section. December 2014

T.C. ZIRAAT BANKASI A.S. 2014 US Resolution Plan Public Section December 2014 1 Introduction This is the public section of the tailored resolution plan for the U.S. operations of T.C. Ziraat Bankasi A.S.

T.C. ZIRAAT BANKASI A.S. 2014 US Resolution Plan Public Section December 2014 1 Introduction This is the public section of the tailored resolution plan for the U.S. operations of T.C. Ziraat Bankasi A.S.

Finansinspektionen's Regulations

Finansinspektionen's Regulations Publisher: Gent Jansson, Finansinspektionen, Box 6750, 113 85 Stockholm. Ordering address: Thomson Fakta AB, Box 6430, 113 82 Stockholm. Tel +46 8-587 671 00, Fax +46 8-587

Finansinspektionen's Regulations Publisher: Gent Jansson, Finansinspektionen, Box 6750, 113 85 Stockholm. Ordering address: Thomson Fakta AB, Box 6430, 113 82 Stockholm. Tel +46 8-587 671 00, Fax +46 8-587

SAMPLE AUDIT REPORT. Sample Credit Union. Report on Operations. As of Audit Date

Sample Credit Union Report on Operations As of Audit Date GENERAL OVERVIEW Overall, the Credit Union appeared to be well managed and continuing to maintain its financial stability. During the twelve months

Sample Credit Union Report on Operations As of Audit Date GENERAL OVERVIEW Overall, the Credit Union appeared to be well managed and continuing to maintain its financial stability. During the twelve months

Basel Committee on Banking Supervision. Consolidated KYC Risk Management

Basel Committee on Banking Supervision Consolidated KYC Risk Management October 2004 Table of contents Introduction...4 Global process for managing KYC risks...5 Risk management...5 Customer acceptance

Basel Committee on Banking Supervision Consolidated KYC Risk Management October 2004 Table of contents Introduction...4 Global process for managing KYC risks...5 Risk management...5 Customer acceptance

Chart I.1. Difference between Primary Surplus (PS) and Bond Yield Spreads in Selected EU 1 Countries

and Bond Yield Spreads in Selected EU 1 Countries") LIST OF CHARTS Chart I.1. Difference between Primary Surplus (PS) and Bond Yield Spreads in Selected EU 1 Countries Chart I.2. Gross Debt Stock and Budget Deficits of Selected Countries as of 2010 1 Chart

LIST OF CHARTS Chart I.1. Difference between Primary Surplus (PS) and Bond Yield Spreads in Selected EU 1 Countries Chart I.2. Gross Debt Stock and Budget Deficits of Selected Countries as of 2010 1 Chart

Federal Reserve Bank Surveillance and Early Warning System

Federal Reserve Bank Surveillance and Early Warning System Kevin Bertsch Deputy Associate Director Surveillance, Financial Trends & Analysis Section Division of Banking Supervision & Regulation Board of

Federal Reserve Bank Surveillance and Early Warning System Kevin Bertsch Deputy Associate Director Surveillance, Financial Trends & Analysis Section Division of Banking Supervision & Regulation Board of

The Philippine banking industry: competition, consolidation and systemic stability

The Philippine banking industry: competition, consolidation and systemic stability Alberto Reyes 1 1. Introduction Despite the generally difficult regional conditions which prevailed as a result of the

The Philippine banking industry: competition, consolidation and systemic stability Alberto Reyes 1 1. Introduction Despite the generally difficult regional conditions which prevailed as a result of the

Loi M Bakani: Effective compliance, risk mitigation and control

Loi M Bakani: Effective compliance, risk mitigation and control Speech by Mr Loi M Bakani, Governor of the Bank of Papua New Guinea, at the Institute of Banking and Business Management (IBBM) seminar on

Loi M Bakani: Effective compliance, risk mitigation and control Speech by Mr Loi M Bakani, Governor of the Bank of Papua New Guinea, at the Institute of Banking and Business Management (IBBM) seminar on

Regulatory Examination Process

Regulatory Examination Process 1 Objective To provide general examination-related concepts and terms used by regulators 2 Regulators Most common regulatory agencies that will interact with your bank: FDIC

Regulatory Examination Process 1 Objective To provide general examination-related concepts and terms used by regulators 2 Regulators Most common regulatory agencies that will interact with your bank: FDIC

CHALLENGES FOR BASEL II IMPLEMENTATION IN CHILE

DIALOGUE ON BASEL II IMPLEMENTATION ABAC - SBIF - ABIF CHALLENGES FOR BASEL II IMPLEMENTATION IN CHILE ENRIQUE MARSHALL SUPERINTENDENT OF BANKS AND FINANCIAL INSTITUTIONS SEPTEMBER 2004 EVALUATION OF THE

DIALOGUE ON BASEL II IMPLEMENTATION ABAC - SBIF - ABIF CHALLENGES FOR BASEL II IMPLEMENTATION IN CHILE ENRIQUE MARSHALL SUPERINTENDENT OF BANKS AND FINANCIAL INSTITUTIONS SEPTEMBER 2004 EVALUATION OF THE

Session 5, Part 2 Managing Banking Risks in Australian and Chinese Banking Systems: Credit Risk Management

Session 5, Part 2 Managing Banking Risks in Australian and Chinese Banking Systems: Credit Risk Management Ms Cui Hui (Susan) Risk Management, Industrial and Commercial Bank of China, Sydney Branch Abstract

Session 5, Part 2 Managing Banking Risks in Australian and Chinese Banking Systems: Credit Risk Management Ms Cui Hui (Susan) Risk Management, Industrial and Commercial Bank of China, Sydney Branch Abstract

YEARENDED31DECEMBER2013 RISKMANAGEMENTDISCLOSURES

RISKMANAGEMENTDISCLOSURES 2015 YEARENDED31DECEMBER2013 ACCORDINGTOCHAPTER7(PAR.34-38)OFPARTCANDANNEXXIOFTHECYPRUSSECURITIES ANDEXCHANGECOMMISSIONDIRECTIVEDI144-2007-05FORTHECAPITALREQUIREMENTSOF INVESTMENTFIRMS

RISKMANAGEMENTDISCLOSURES 2015 YEARENDED31DECEMBER2013 ACCORDINGTOCHAPTER7(PAR.34-38)OFPARTCANDANNEXXIOFTHECYPRUSSECURITIES ANDEXCHANGECOMMISSIONDIRECTIVEDI144-2007-05FORTHECAPITALREQUIREMENTSOF INVESTMENTFIRMS

Act on Investment Firms 26.7.1996/579

Please note: This is an unofficial translation. Amendments up to 135/2007 included, May 2007. Act on Investment Firms 26.7.1996/579 CHAPTER 1 General provisions Section 1 Scope of application This Act

Please note: This is an unofficial translation. Amendments up to 135/2007 included, May 2007. Act on Investment Firms 26.7.1996/579 CHAPTER 1 General provisions Section 1 Scope of application This Act

Application for a Banking Authority Foreign Bank Branches Prudential Statement J2

Application for a Banking Authority Foreign Bank Branches Prudential Statement J2 PS J2 Introduction 1. A foreign bank wishing to operate as a branch in Australia must obtain a banking authority issued

Application for a Banking Authority Foreign Bank Branches Prudential Statement J2 PS J2 Introduction 1. A foreign bank wishing to operate as a branch in Australia must obtain a banking authority issued

Pursuant to Article 95, item 3 of the Constitution of Montenegro I hereby pass the ENACTMENT PROCLAIMING THE LAW ON BANKS

Pursuant to Article 95, item 3 of the Constitution of Montenegro I hereby pass the ENACTMENT PROCLAIMING THE LAW ON BANKS I hereby proclaim the Law on Banks, adopted by the Parliament of Montenegro at

Pursuant to Article 95, item 3 of the Constitution of Montenegro I hereby pass the ENACTMENT PROCLAIMING THE LAW ON BANKS I hereby proclaim the Law on Banks, adopted by the Parliament of Montenegro at

Guidelines on preparation for and management of a financial crisis

CEIOPS-DOC-15/09 26 March 2009 Guidelines on preparation for and management of a financial crisis in the Context of Supplementary Supervision as defined by the Insurance Groups Directive (98/78/EC) and

CEIOPS-DOC-15/09 26 March 2009 Guidelines on preparation for and management of a financial crisis in the Context of Supplementary Supervision as defined by the Insurance Groups Directive (98/78/EC) and

REINSURANCE RISK MANAGEMENT GUIDELINE

REINSURANCE RISK MANAGEMENT GUIDELINE Initial publication: April 2010 Update: July 2013 Table of Contents Preamble... 2 Introduction... 3 Scope... 5 Coming into effect and updating... 6 1. Reinsurance

REINSURANCE RISK MANAGEMENT GUIDELINE Initial publication: April 2010 Update: July 2013 Table of Contents Preamble... 2 Introduction... 3 Scope... 5 Coming into effect and updating... 6 1. Reinsurance

Central Bank of The Bahamas Consultation Paper PU42-0408 Draft Guidelines for the Management of Interest Rate Risk

Central Bank of The Bahamas Consultation Paper PU42-0408 Draft Guidelines for the Management of Interest Rate Risk Policy Unit Bank Supervision Department April16 th 2008 Consultation Paper Draft Guidelines

Central Bank of The Bahamas Consultation Paper PU42-0408 Draft Guidelines for the Management of Interest Rate Risk Policy Unit Bank Supervision Department April16 th 2008 Consultation Paper Draft Guidelines

How To Understand And Understand The Financial Sector In Turkish Finance Companies

FEBRUARY 14, 2013 BANKING SECTOR COMMENT Turkish Finance Companies: New legislation on Financial Leasing, Factoring and Financing Institutions Is Credit Positive Table of Contents: SUMMARY OPINION 1 OVERVIEW

FEBRUARY 14, 2013 BANKING SECTOR COMMENT Turkish Finance Companies: New legislation on Financial Leasing, Factoring and Financing Institutions Is Credit Positive Table of Contents: SUMMARY OPINION 1 OVERVIEW

SECTOR ASSESSMENT (SUMMARY): FINANCE 1. 1. Sector Performance, Problems, and Opportunities

: FINANCE 1. 1. Sector Performance, Problems, and Opportunities") Country Partnership Strategy: Bangladesh, 2011 2015 SECTOR ASSESSMENT (SUMMARY): FINANCE 1 Sector Road Map 1. Sector Performance, Problems, and Opportunities 1. The finance sector in Bangladesh is diverse,

Country Partnership Strategy: Bangladesh, 2011 2015 SECTOR ASSESSMENT (SUMMARY): FINANCE 1 Sector Road Map 1. Sector Performance, Problems, and Opportunities 1. The finance sector in Bangladesh is diverse,

6/8/2016 OVERVIEW. Page 1 of 9

OVERVIEW Attachment Supervisory Guidance for Assessing Risk Management at Supervised Institutions with Total Consolidated Assets Less than $50 Billion [Fotnote1 6/8/2016 Managing risks is fundamental to

OVERVIEW Attachment Supervisory Guidance for Assessing Risk Management at Supervised Institutions with Total Consolidated Assets Less than $50 Billion [Fotnote1 6/8/2016 Managing risks is fundamental to

Supervisory Policy Manual

This module should be read in conjunction with the Introduction and with the Glossary, which contains an explanation of abbreviations and other terms used in this Manual. If reading on-line, click on blue

This module should be read in conjunction with the Introduction and with the Glossary, which contains an explanation of abbreviations and other terms used in this Manual. If reading on-line, click on blue

An Overview of Basel II s Pillar 2

An Overview of Basel II s Pillar 2 Seminar for Senior Bank Supervisors from Emerging Economies Washington, DC 23 October 2008 Elizabeth Roberts Director, FSI Topics to be covered Why does Pillar 2 exist?

An Overview of Basel II s Pillar 2 Seminar for Senior Bank Supervisors from Emerging Economies Washington, DC 23 October 2008 Elizabeth Roberts Director, FSI Topics to be covered Why does Pillar 2 exist?

RISK FACTORS AND RISK MANAGEMENT

Bangkok Bank Public Company Limited 044 RISK FACTORS AND RISK MANAGEMENT Bangkok Bank recognizes that effective risk management is fundamental to good banking practice. Accordingly, the Bank has established

Bangkok Bank Public Company Limited 044 RISK FACTORS AND RISK MANAGEMENT Bangkok Bank recognizes that effective risk management is fundamental to good banking practice. Accordingly, the Bank has established

International Monetary Fund Washington, D.C.

2009 International Monetary Fund May 2009 IMF Country Report No. 09/167 Cyprus: Financial Sector Assessment Program Update Technical Note Factual Update on Basel Core Principles for Effective Banking Supervision

2009 International Monetary Fund May 2009 IMF Country Report No. 09/167 Cyprus: Financial Sector Assessment Program Update Technical Note Factual Update on Basel Core Principles for Effective Banking Supervision

BY G. A. OGUNLEYE, OFR MANAGING/DIRECTOR/CEO NIGERIA DEPOSIT INSURANCE CORPORATION

THE ROLE OF DEPOSIT INSURANCE IN ENSURING FINANCIAL SYSTEM STABILITY IN NIGERIA BY G. A. OGUNLEYE, OFR MANAGING/DIRECTOR/CEO NIGERIA DEPOSIT INSURANCE CORPORATION 1 PAPER OUTLINE INTRODUCTION FUNCTIONS

THE ROLE OF DEPOSIT INSURANCE IN ENSURING FINANCIAL SYSTEM STABILITY IN NIGERIA BY G. A. OGUNLEYE, OFR MANAGING/DIRECTOR/CEO NIGERIA DEPOSIT INSURANCE CORPORATION 1 PAPER OUTLINE INTRODUCTION FUNCTIONS

mr. M.G.F.M.V. Janssen Secretary to the Managing Board T: +31 20 557 52 30 I: www.kasbank.com

Date: 27 August 2015 For information: mr. M.G.F.M.V. Janssen Secretary to the Managing Board T: +31 20 557 52 30 I: www.kasbank.com Growth of 20% in net result, excluding non-recurring items, to EUR 8.3

Date: 27 August 2015 For information: mr. M.G.F.M.V. Janssen Secretary to the Managing Board T: +31 20 557 52 30 I: www.kasbank.com Growth of 20% in net result, excluding non-recurring items, to EUR 8.3

School of Accounting Finance and Economics

School of Accounting Finance and Economics MSc BANKING AND FINANCE PROGRAMME DOCUMENT VERSION 3.1 CODE July 2013 University of Technology, Mauritius La Tour Koenig, Pointe aux Sables, Mauritius Tel: (230)

School of Accounting Finance and Economics MSc BANKING AND FINANCE PROGRAMME DOCUMENT VERSION 3.1 CODE July 2013 University of Technology, Mauritius La Tour Koenig, Pointe aux Sables, Mauritius Tel: (230)

BOARD OF GOVERNORS FEDERAL RESERVE SYSTEM

BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM WASHINGTON, D.C. 20551 DIVISION OF BANKING SUPERVISION AND REGULATION DIVISION OF CONSUMER AND COMMUNITY AFFAIRS SR 12-17 CA 12-14 December 17, 2012 TO

BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM WASHINGTON, D.C. 20551 DIVISION OF BANKING SUPERVISION AND REGULATION DIVISION OF CONSUMER AND COMMUNITY AFFAIRS SR 12-17 CA 12-14 December 17, 2012 TO

Basel Committee on Banking Supervision. Consultative Document. Net Stable Funding Ratio disclosure standards. Issued for comment by 6 March 2015

Basel Committee on Banking Supervision Consultative Document Net Stable Funding Ratio disclosure standards Issued for comment by 6 March 2015 December 2014 This publication is available on the BIS website

Basel Committee on Banking Supervision Consultative Document Net Stable Funding Ratio disclosure standards Issued for comment by 6 March 2015 December 2014 This publication is available on the BIS website

Annual Disclosures (Banks, Foreign Bank Branches, Federally Regulated Trust and Loan Companies, and Cooperative Credit Associations)

") Guideline Subject: (Banks, Foreign Bank Branches, Federally Regulated Trust and Loan Companies, and Cooperative Credit Associations) Category: Accounting No: D-1 Date: July 1997 Revised: July 2010 Introduction

Guideline Subject: (Banks, Foreign Bank Branches, Federally Regulated Trust and Loan Companies, and Cooperative Credit Associations) Category: Accounting No: D-1 Date: July 1997 Revised: July 2010 Introduction

Core Principles for Effective Banking Supervision: New Edition Released

News Bulletin September 17, 2012 Core Principles for Effective Banking Supervision: New Edition Released Last Friday, September 14, 2012, the Basel Committee on Banking Supervision published a new set

News Bulletin September 17, 2012 Core Principles for Effective Banking Supervision: New Edition Released Last Friday, September 14, 2012, the Basel Committee on Banking Supervision published a new set

We endeavor to maximize returns.

We endeavor to maximize returns. Ayşegül Özel Yapı Kredi Bankası Private Banking Portfolio Manager Erdoğan Yücel Yapı Kredi Emeklilik Sales Manager FInance 4 th largest private bank (asset size) Leader

We endeavor to maximize returns. Ayşegül Özel Yapı Kredi Bankası Private Banking Portfolio Manager Erdoğan Yücel Yapı Kredi Emeklilik Sales Manager FInance 4 th largest private bank (asset size) Leader

Risk Management Guidelines For Co-operative Financial Institutions

Risk Management Guidelines For Co-operative Financial Institutions Table of Contents 1 PREAMBLE... 5 2 INTERNAL CONTROL ENVIRONMENT WITHIN A CFI... 6 2.1 Introduction... 6 2.2 Internal Control Environment...

Risk Management Guidelines For Co-operative Financial Institutions Table of Contents 1 PREAMBLE... 5 2 INTERNAL CONTROL ENVIRONMENT WITHIN A CFI... 6 2.1 Introduction... 6 2.2 Internal Control Environment...

DEVELOPMENTS IN 1990 s

MACROECONOMIC MANAGEMENT WITH OPEN CAPITAL ACCOUNTS: THE TURKISH CASE FAIK OZTRAK Director TUSIAD-Koc University, Economic Research Forum HIGH LEVEL SEMINAR ON CRISIS PREVENTION, SINGAPORE, JULY 1, 26

MACROECONOMIC MANAGEMENT WITH OPEN CAPITAL ACCOUNTS: THE TURKISH CASE FAIK OZTRAK Director TUSIAD-Koc University, Economic Research Forum HIGH LEVEL SEMINAR ON CRISIS PREVENTION, SINGAPORE, JULY 1, 26

BANK EXAMINERS MANUAL FOR AML/CFT RBS EXAMINATION

BANK EXAMINERS MANUAL FOR AML/CFT RBS EXAMINATION 1 Contents 1. EXAMINATION PROCEDURES ON SCOPING AND PLANNING 1..1 2. EXAMINATION PROCEDURES OF AML/CFT COMPLIANCE PROGRAM...3.. 3 3. OVERVIEW OF AML/CFT

BANK EXAMINERS MANUAL FOR AML/CFT RBS EXAMINATION 1 Contents 1. EXAMINATION PROCEDURES ON SCOPING AND PLANNING 1..1 2. EXAMINATION PROCEDURES OF AML/CFT COMPLIANCE PROGRAM...3.. 3 3. OVERVIEW OF AML/CFT

Funds Transfer Pricing A gateway to enhanced business performance

Funds Transfer Pricing A gateway to enhanced business performance Jean-Philippe Peters Partner Governance, Risk & Compliance Deloitte Luxembourg Arnaud Duchesne Senior Manager Governance, Risk & Compliance

Funds Transfer Pricing A gateway to enhanced business performance Jean-Philippe Peters Partner Governance, Risk & Compliance Deloitte Luxembourg Arnaud Duchesne Senior Manager Governance, Risk & Compliance

Administration of the Act

Administration of the Act Administration of the Act Legislation The insurance industry in Malaysia is governed by the Insurance Act 1996 (Act) which came into force on 1 January 1997. The Act is supplemented

Administration of the Act Administration of the Act Legislation The insurance industry in Malaysia is governed by the Insurance Act 1996 (Act) which came into force on 1 January 1997. The Act is supplemented

FEDERAL RESERVE SYSTEM. Banco Financiera Comercial Hondurena, S.A. Tegucigalpa, Honduras. Order Approving Establishment of a Representative Office

1 FEDERAL RESERVE SYSTEM Banco Financiera Comercial Hondurena, S.A. Tegucigalpa, Honduras Order Approving Establishment of a Representative Office Banco Financiera Comercial Hondurena, S.A. ( Bank ), Tegucigalpa,

1 FEDERAL RESERVE SYSTEM Banco Financiera Comercial Hondurena, S.A. Tegucigalpa, Honduras Order Approving Establishment of a Representative Office Banco Financiera Comercial Hondurena, S.A. ( Bank ), Tegucigalpa,

The Northern Trust Company, Canada Basel III Pillar lll Disclosure as at December 31, 2015

The Northern Trust Company, Canada Basel III Pillar lll Disclosure as at December 31, 2015 Subject to Board Approval Posting date: January 29, 2016 Contents NORTHERN TRUST OVERVIEW AND SCOPE OF APPPLICATION.

The Northern Trust Company, Canada Basel III Pillar lll Disclosure as at December 31, 2015 Subject to Board Approval Posting date: January 29, 2016 Contents NORTHERN TRUST OVERVIEW AND SCOPE OF APPPLICATION.

Capital adequacy ratios for banks - simplified explanation and

Page 1 of 9 Capital adequacy ratios for banks - simplified explanation and example of calculation Summary Capital adequacy ratios are a measure of the amount of a bank's capital expressed as a percentage

Page 1 of 9 Capital adequacy ratios for banks - simplified explanation and example of calculation Summary Capital adequacy ratios are a measure of the amount of a bank's capital expressed as a percentage

Close Brothers Group plc

Close Brothers Group plc Pillar 3 disclosures for the year ended 31 July 2008 Close Brothers Group plc Pillar 3 disclosures for the year ended 31 July 2008 Contents 1. Overview 2. Risk management objectives

Close Brothers Group plc Pillar 3 disclosures for the year ended 31 July 2008 Close Brothers Group plc Pillar 3 disclosures for the year ended 31 July 2008 Contents 1. Overview 2. Risk management objectives

Who should submit the application

Operational risk: Application to use an Advanced Measurement Approach February 2007 1 Contents This document contains Finansinspektionen s requirements regarding the content and structure of an application

Operational risk: Application to use an Advanced Measurement Approach February 2007 1 Contents This document contains Finansinspektionen s requirements regarding the content and structure of an application

The Western Hemisphere Credit & Loan Reporting Initiative (WHCRI)

") The Western Hemisphere Credit & Loan Reporting Initiative (WHCRI) Public Credit Registries as a Tool for Bank Regulation and Supervision Matías Gutierrez Girault & Jane Hwang III Evaluation Workshop Mexico

The Western Hemisphere Credit & Loan Reporting Initiative (WHCRI) Public Credit Registries as a Tool for Bank Regulation and Supervision Matías Gutierrez Girault & Jane Hwang III Evaluation Workshop Mexico

NOTICE 158 OF 2014 FINANCIAL SERVICES BOARD REGISTRAR OF LONG-TERM INSURANCE AND SHORT-TERM INSURANCE

STAATSKOERANT, 19 DESEMBER 2014 No. 38357 3 BOARD NOTICE NOTICE 158 OF 2014 FINANCIAL SERVICES BOARD REGISTRAR OF LONG-TERM INSURANCE AND SHORT-TERM INSURANCE LONG-TERM INSURANCE ACT, 1998 (ACT NO. 52

STAATSKOERANT, 19 DESEMBER 2014 No. 38357 3 BOARD NOTICE NOTICE 158 OF 2014 FINANCIAL SERVICES BOARD REGISTRAR OF LONG-TERM INSURANCE AND SHORT-TERM INSURANCE LONG-TERM INSURANCE ACT, 1998 (ACT NO. 52

Report on Internal Control

Annex to letter from the General Secretary of the Autorité de contrôle prudentiel to the Director General of the French Association of Credit Institutions and Investment Firms Report on Internal Control

Annex to letter from the General Secretary of the Autorité de contrôle prudentiel to the Director General of the French Association of Credit Institutions and Investment Firms Report on Internal Control

[Investment Company Act Release No. 29332; 812-13752] Korea Finance Corporation; Notice of Application

![[Investment Company Act Release No. 29332; 812-13752] Korea Finance Corporation; Notice of Application](/thumbs/26/7429171.jpg "[Investment Company Act Release No. 29332; 812-13752] Korea Finance Corporation; Notice of Application") SECURITIES AND EXCHANGE COMMISSION [Investment Company Act Release No. 29332; 812-13752] Korea Finance Corporation; Notice of Application June 25, 2010 Agency: Securities and Exchange Commission (the Commission

SECURITIES AND EXCHANGE COMMISSION [Investment Company Act Release No. 29332; 812-13752] Korea Finance Corporation; Notice of Application June 25, 2010 Agency: Securities and Exchange Commission (the Commission

Market and Liquidity Risk Assessment Overview. Federal Reserve System

Market and Liquidity Risk Assessment Overview Federal Reserve System Overview Inherent Risk Risk Management Composite Risk Trend 2 Market and Liquidity Risk: Inherent Risk Definition Identification Quantification

Market and Liquidity Risk Assessment Overview Federal Reserve System Overview Inherent Risk Risk Management Composite Risk Trend 2 Market and Liquidity Risk: Inherent Risk Definition Identification Quantification

CANADIAN TIRE BANK. BASEL PILLAR 3 DISCLOSURES December 31, 2014 (unaudited)

") (unaudited) 1. SCOPE OF APPLICATION Basis of preparation This document represents the Basel Pillar 3 disclosures for Canadian Tire Bank ( the Bank ) and is unaudited. The Basel Pillar 3 disclosures included

(unaudited) 1. SCOPE OF APPLICATION Basis of preparation This document represents the Basel Pillar 3 disclosures for Canadian Tire Bank ( the Bank ) and is unaudited. The Basel Pillar 3 disclosures included

APPENDIX A NCUA S CAMEL RATING SYSTEM (CAMEL) 1

1") APPENDIX A NCUA S CAMEL RATING SYSTEM (CAMEL) 1 The CAMEL rating system is based upon an evaluation of five critical elements of a credit union's operations: Capital Adequacy, Asset Quality, Management,

APPENDIX A NCUA S CAMEL RATING SYSTEM (CAMEL) 1 The CAMEL rating system is based upon an evaluation of five critical elements of a credit union's operations: Capital Adequacy, Asset Quality, Management,

Course Syllabus For Banking and Financial Management Department

For Banking and Financial Management Department School Year First Year First year Second year Third year Fifth year Fifth year Fifth year Fifth year Name of course Financial Accounting principles Intermediate

For Banking and Financial Management Department School Year First Year First year Second year Third year Fifth year Fifth year Fifth year Fifth year Name of course Financial Accounting principles Intermediate

As of July 1, 2013. Risk Management and Administration

Risk Management Risk Control The ORIX Group allocates management resources by taking into account Group-wide risk preference based on management strategies and the strategy of individual business units.

Risk Management Risk Control The ORIX Group allocates management resources by taking into account Group-wide risk preference based on management strategies and the strategy of individual business units.

RISK MANAGEMENT REPORT (for the Financial Year Ended 31 March 2012)

") RISK MANAGEMENT REPORT (for the Financial Year Ended 31 March 2012) Integrated Risk Management Framework The Group s Integrated Risk Management Framework (IRMF) sets the fundamental elements to manage

RISK MANAGEMENT REPORT (for the Financial Year Ended 31 March 2012) Integrated Risk Management Framework The Group s Integrated Risk Management Framework (IRMF) sets the fundamental elements to manage

COMPUTERSHARE TRUST COMPANY OF CANADA BASEL III PILLAR 3 DISCLOSURES

COMPUTERSHARE TRUST COMPANY OF CANADA BASEL III PILLAR 3 DISCLOSURES December 31, 2013 Table of Contents Scope of Application... 3 Capital Structure... 3 Capital Adequacy... 3 Credit Risk... 4 Market Risk...

COMPUTERSHARE TRUST COMPANY OF CANADA BASEL III PILLAR 3 DISCLOSURES December 31, 2013 Table of Contents Scope of Application... 3 Capital Structure... 3 Capital Adequacy... 3 Credit Risk... 4 Market Risk...

The Global Banking Crisis: an African banker's response

Sir Patrick Gillam Lecture The Global Banking Crisis: an African banker's response Mallam Sanusi Lamido Sanusi Governor, Central Bank of Nigeria Professor Judith Rees Chair, LSE Suggested hashtag for Twitter

Sir Patrick Gillam Lecture The Global Banking Crisis: an African banker's response Mallam Sanusi Lamido Sanusi Governor, Central Bank of Nigeria Professor Judith Rees Chair, LSE Suggested hashtag for Twitter

Navigate the regulatory maze

www.pwc.com.cy Navigate the regulatory maze Delivering Regulatory Compliance services to the Financial Services industry September 2014 As at July 2014 there were more than 40 licensed banking institutions

www.pwc.com.cy Navigate the regulatory maze Delivering Regulatory Compliance services to the Financial Services industry September 2014 As at July 2014 there were more than 40 licensed banking institutions

Assessing Credit Risk

Assessing Credit Risk Objectives Discuss the following: Inherent Risk Quality of Risk Management Residual or Composite Risk Risk Trend 2 Inherent Risk Define the risk Identify sources of risk Quantify

Assessing Credit Risk Objectives Discuss the following: Inherent Risk Quality of Risk Management Residual or Composite Risk Risk Trend 2 Inherent Risk Define the risk Identify sources of risk Quantify

REGULATION ON DEPOSITS AND PARTICIPATION FUNDS SUBJECT TO INSURANCE AND PREMIUMS COLLECTED BY SAVING DEPOSITS INSURANCE FUND

() () REGULATION ON DEPOSITS AND PARTICIPATION FUNDS SUBJECT TO INSURANCE AND PREMIUMS COLLECTED BY SAVING DEPOSITS INSURANCE FUND Published in issue 226339 of the Official Gazette dated November 7, 2006

() () REGULATION ON DEPOSITS AND PARTICIPATION FUNDS SUBJECT TO INSURANCE AND PREMIUMS COLLECTED BY SAVING DEPOSITS INSURANCE FUND Published in issue 226339 of the Official Gazette dated November 7, 2006

Chairman s Statement. Contents & Introduction. Introduction

Business Plan 2016 Contents Chairman s & Introduction Statement Introduction Chairman s Statement About the Commission Our major priorities for 2016 Facilitating market access & other benefits to industry

Business Plan 2016 Contents Chairman s & Introduction Statement Introduction Chairman s Statement About the Commission Our major priorities for 2016 Facilitating market access & other benefits to industry

Colleen Johnston Group Head Finance & CFO TD Bank Financial Group. Citi Financial Services Conference

Colleen Johnston Group Head Finance & CFO TD Bank Financial Group Citi Financial Services Conference January 28, 2009 Caution regarding forward-looking statements From time to time, the Bank makes written

Colleen Johnston Group Head Finance & CFO TD Bank Financial Group Citi Financial Services Conference January 28, 2009 Caution regarding forward-looking statements From time to time, the Bank makes written

SCREENING CHAPTER 18 STATISTICS FINANCIAL ACCOUNTS

1 SCREENING CHAPTER 18 FINANCIAL ACCOUNTS Country Session: CONTENT Overview Responsible Institutions and Stakeholders Legal Framework Classifications Data Sources Future Plans 2 Overview The Central Bank

1 SCREENING CHAPTER 18 FINANCIAL ACCOUNTS Country Session: CONTENT Overview Responsible Institutions and Stakeholders Legal Framework Classifications Data Sources Future Plans 2 Overview The Central Bank

Financial Services Regulatory Commission Antigua and Barbuda Division of Gaming Customer Due Diligence Guidelines for

Division of Gaming Customer Due Diligence Guidelines for Interactive Gaming & Interactive Wagering Companies November 2005 Customer Due Diligence for Interactive Gaming & Interactive Wagering Companies

Division of Gaming Customer Due Diligence Guidelines for Interactive Gaming & Interactive Wagering Companies November 2005 Customer Due Diligence for Interactive Gaming & Interactive Wagering Companies

Asset Liability Management

e-learning and reference solutions for the global finance professional Asset Liability Management A comprehensive e-learning product covering Global Best Practices, Strategic, Operational and Analytical

e-learning and reference solutions for the global finance professional Asset Liability Management A comprehensive e-learning product covering Global Best Practices, Strategic, Operational and Analytical

Advisory Guidelines of the Financial Supervisory Authority. Requirements regarding the arrangement of operational risk management

Advisory Guidelines of the Financial Supervisory Authority Requirements regarding the arrangement of operational risk management These Advisory Guidelines have established by resolution no. 63 of the Management

Advisory Guidelines of the Financial Supervisory Authority Requirements regarding the arrangement of operational risk management These Advisory Guidelines have established by resolution no. 63 of the Management

FSB launches peer review on deposit insurance systems and invites feedback from stakeholders

Press release Press enquiries: Basel +41 61 280 8037 Press.service@bis.org Ref no: 26/2011 1 July 2011 FSB launches peer review on deposit insurance systems and invites feedback from stakeholders The Financial

Press release Press enquiries: Basel +41 61 280 8037 Press.service@bis.org Ref no: 26/2011 1 July 2011 FSB launches peer review on deposit insurance systems and invites feedback from stakeholders The Financial

Financial Risk Management Courses

Financial Risk Management Courses The training was great, the materials were informative and the instructor was very knowledgeable. The course covered real scenarios that were well put together and delivered.

Financial Risk Management Courses The training was great, the materials were informative and the instructor was very knowledgeable. The course covered real scenarios that were well put together and delivered.

GUIDANCE NOTE FOR DEPOSIT-TAKERS. Operational Risk Management. March 2012

GUIDANCE NOTE FOR DEPOSIT-TAKERS Operational Risk Management March 2012 Version 1.0 Contents Page No 1 Introduction 2 2 Overview 3 Operational risk - fundamental principles and governance 3 Fundamental

GUIDANCE NOTE FOR DEPOSIT-TAKERS Operational Risk Management March 2012 Version 1.0 Contents Page No 1 Introduction 2 2 Overview 3 Operational risk - fundamental principles and governance 3 Fundamental

Sample Financial institution Risk Management Policy 2011

Sample Financial institution Risk Management Policy 2011 1 Contents Risk Management Program...2 Internal Control and Risk Management Diagram... 2 General Control Environment... 2 Specific Internal Control

Sample Financial institution Risk Management Policy 2011 1 Contents Risk Management Program...2 Internal Control and Risk Management Diagram... 2 General Control Environment... 2 Specific Internal Control

Memorandum of Understanding on Maintenance of Financial Stability

Unofficial translation Memorandum of Understanding on Maintenance of Financial Stability Purpose and organization of participating institutions activity 1. The Government of the Republic of Moldova (Government),

Unofficial translation Memorandum of Understanding on Maintenance of Financial Stability Purpose and organization of participating institutions activity 1. The Government of the Republic of Moldova (Government),

HOCH CAPITAL LTD PILLAR 3 DISCLOSURES As at 1 February 2015

HOCH CAPITAL LTD PILLAR 3 DISCLOSURES As at 1 February 2015 TABLE OF CONTENTS 1. Overview / Background 1.1 Introduction 1.2 Frequency of disclosure 1.3 Location and verification of disclosure 1.4 Scope

HOCH CAPITAL LTD PILLAR 3 DISCLOSURES As at 1 February 2015 TABLE OF CONTENTS 1. Overview / Background 1.1 Introduction 1.2 Frequency of disclosure 1.3 Location and verification of disclosure 1.4 Scope

2015 DFAST Annual Stress Test Disclosure For Synchrony Bank, a Wholly-Owned Subsidiary of Synchrony Financial. June 26, 2015

2015 DFAST Annual Stress Test Disclosure For Synchrony Bank, a Wholly-Owned Subsidiary of Synchrony Financial June 26, 2015 Disclaimers Cautionary Statement Regarding Forward-Looking Statements This presentation

2015 DFAST Annual Stress Test Disclosure For Synchrony Bank, a Wholly-Owned Subsidiary of Synchrony Financial June 26, 2015 Disclaimers Cautionary Statement Regarding Forward-Looking Statements This presentation

Capital Requirements Directive Pillar 3 Disclosure. December 2015

Capital Requirements Directive Pillar 3 Disclosure December 2015 1. Background The purpose of this document is to outline the Pillar 3 disclosures for BlueBay Asset Management LLP ( BlueBay ). BlueBay

Capital Requirements Directive Pillar 3 Disclosure December 2015 1. Background The purpose of this document is to outline the Pillar 3 disclosures for BlueBay Asset Management LLP ( BlueBay ). BlueBay

Disclosure 17 OffV (Credit Risk Mitigation Techniques)

") Disclosure 17 OffV (Credit Risk Mitigation Techniques) The Austrian Financial Market Authority (FMA) and the Oesterreichsiche Nationalbank (OeNB) have assessed UniCredit Bank Austria AG for the use of

Disclosure 17 OffV (Credit Risk Mitigation Techniques) The Austrian Financial Market Authority (FMA) and the Oesterreichsiche Nationalbank (OeNB) have assessed UniCredit Bank Austria AG for the use of

LAW ON PAYMENT AND SECURITY SETTLEMENT SYSTEMS, PAYMENT SERVICES AND ELECTRONIC MONEY INSTITUTIONS. Law No. 6493 Date of Enactment: 20/6/2013

27 June 2013 THURSDAY Official Gazette Issue Nr: 28690 LAW ON PAYMENT AND SECURITY SETTLEMENT SYSTEMS, PAYMENT SERVICES AND ELECTRONIC MONEY INSTITUTIONS Law No. 6493 Date of Enactment: 20/6/2013 SECTION

27 June 2013 THURSDAY Official Gazette Issue Nr: 28690 LAW ON PAYMENT AND SECURITY SETTLEMENT SYSTEMS, PAYMENT SERVICES AND ELECTRONIC MONEY INSTITUTIONS Law No. 6493 Date of Enactment: 20/6/2013 SECTION