Form 709: A Practicum. Monica Haven, EA, JD, LLM

|

|

|

- Emil Burns

- 9 years ago

- Views:

Transcription

1 Form 709: A Practicum Monica Haven, EA, JD, LLM

2 Text Page 1 What is a Gift Any transaction in which interest in property is gratuitously passed or conferred upon another Deemed complete when donor gives up control & cannot change disposition of property for own benefit or that of others

3 Text Page 2 Are these gifts? Interest-free family loan: YES Conveyance of economic benefit (use of money) without consideration (interest payments) Gift = interest income that should have been earned Loan guarantee: NO Incomplete gift if there is no certainty that payment will be required Inducement: YES Eager young man offers fiancé $150K to accept marriage proposal (marriage consideration) Divorce settlement: NO Surrender of marital rights as per divorce decree is not voluntary

4 Text Page 3 Elements of a Gift 1. Delivery Actual or implied (e.g. new car in driveway or give car keys) Directly or through 3 rd party 2. Donative intent [see Officer Peebles] Express or inferred At time of gift 3. Acceptance Donee takes unconditional possession (can disclaim in writing) Donor forfeits all rights

5 Text Page 3 Officer Peebles Uncovered wife s affair with doctor & blackmailed him Doctor delivered cash & said, This is not blackmail money; I just want to help you out [ Gift?] Peebles did not report gift but doctor s accountant issued 1099-MISC Court held that this was taxable income since it was not gifted with disinterested generosity

6 Text Page 4 Common Types of Gifts Below-market loan: Gift = Interest at Applicable Federal Rate Debt forgiveness: Gift = Unpaid balance Demand loan: treated as made on last day of calendar year Term loan: treated as gift on date funds are loaned De minimus exemption: $10,000 Below-market sale: Gift = FMV discounted sales price Transfer to an irrevocable trust: Gift = Value of assets transferred Joint annuity: Gift = Premium difference btw. joint & single-life annuity Corporate dissolution: Gift = Value of distribution shareholder s interest

7 Text Page 4 Gifts by Check Gift is considered complete if: donor intended to make gift delivery was unconditional deposit was made in year of gift & within reasonable time after issuance (even if not yet cleared) donor s bank did not reject the check and donor was alive when the donor s bank paid it

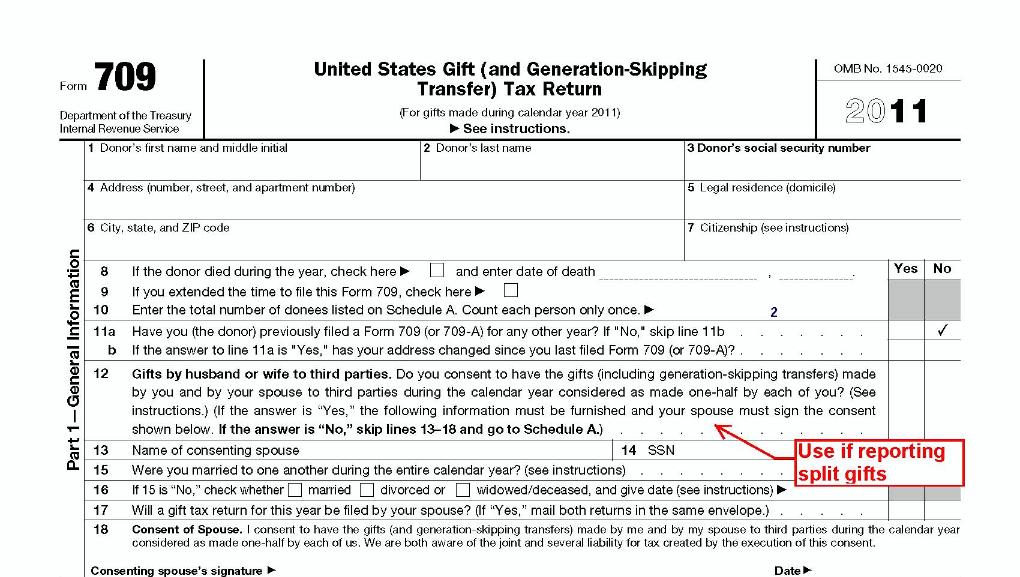

8 Text Page 4 Transfers into Joint Ownership State law governs when transfer is deemed complete generally: Real property, mutual funds, stocks & bonds upon re-titling Bank & brokerage accounts when donee makes withdrawal for own benefit Example: Mom re-titles condo to avoid probate [Gift # 1]; Son quit claims property back [Gift # 2] Strategy: Draft written agreement Neither party may sever joint tenancy without mutual consent Joint tenancy is for estate transfer purposes only, and Original owner will continue as sole owner until death or severance

9 Text Page 5 Partial Gifts Could result from sale for insufficient consideration & when donee (rather than donor) pays attendant gift tax Donor may deduct gift tax paid by donee from FMV of gift (a.k.a. net gift ), but must include gift tax in excess of property s basis as taxable income Example: Donor gifted stock (basis $50K) on condition that donee pays gift tax of $60K. Donor recognized taxable capital gain of $10K.

10 Text Page 6 Gift Tax Enacted in 1932 (16 years after Estate Tax) Imposed on donor Cumulative tax each successive gift is taxed at marginal rate of all gifts made (even if previously taxed)

11 Text Page 6 Exemptions Gifts to qualified charities Direct payments for another s medical expenses (incl. insurance premiums) Direct payments for another s tuition (no books, room & board, or supplies) No exemption for Qualified Tuition Programs (QTPs) But QTP eligible for aggregate of 5 years of annual exclusion (elect on Form 709, Schedule A) Support payments (if legally required)

12 Report 529 Plan Contributions

13 Text Page 8 Annual Exclusion $13K/year to each donee (indexed for inflation) Gift must be present interest & grant donee immediate right to use / possession (right to income & right to sell) UTMA accounts okay if funds immediately available for minor s benefit, minor will receive property by age 21, and property will pass to the minor s estate Convert gifts of future interest using Crummey power granting right to withdraw donated funds for limited time

14 Text Page 7 Exemption vs. Exclusion Grandpa sends $40K to University for grandson s tuition & sends $13K to grandson for books & supplies Neither payment is reportable: $40K was direct payment for tuition (exempt) $13K eligible for annual exclusion

15 Text Page 8 Gift-splitting Spouses may elect to jointly give $26K both spouses must be U.S. citizens / residents married at time of gift, and remain unmarried at year-end if separated after gift Elect on Form 709, Part I; each spouse must sign consent on Line 18 (NO joint return)

16 Text Page 8 Example of Gift-splitting H & W agree to split gifts H gave nephew $21K W gave niece $18K Each gift is treated as ½ from H and ½ from W H & W then viewed separately to determine if gifts > annual exclusion Each donor must file gift tax return to report gift-splitting (even if no taxable gift)

17 Report Gift-splitting Election

18 Text Page 9 Lifetime Exclusion Currently $5.12 million; $10.24 million MFJ 2012: exclusion equals Applicable Credit of $1,772,800 Gifts > annual exclusion must be reported on Form 709 No tax due unless cumulative gifts > lifetime exclusion Taxpayer entitled to only one lifetime exclusion for gifts and/or estates

19 Text Page 9 Apply Exclusions in Sequence In 2012, Taxpayer gifted: $8K car to son $25K cash to daughter for down-payment on house $15K paid college tuition of nephew 1. Apply educational (medical or charitable) exclusion gift to nephew is exempt 2. Apply annual exclusion entire gift to son & first $13K of gift to daughter are exempt 3. Apply lifetime exclusion remaining $12K of gift to daughter is taxable; tax totals $4,680 which will reduce available Unified Credit to $1,768,120 Taxpayer does not owe gift tax but must file Form 709 (even if he does not anticipate exceeding exclusion during lifetime)

20 Text Page 10 Non-Residents Subject to gift tax only on US-sited real or tangible personal property Mexican citizen gifts Arizona property to Mexican son taxable US citizen gifts Mexican property to daughter taxable (regardless of daughter s nationality) Eligible for annual exclusion; ineligible for lifetime exclusion Marital deduction limited to $139K in 2012

21

22 Text Page 11 Form 709 Due Date Due April 15 th of year following gift (or with Form 706 if donor has died since making gift) Automatically extended 6 months if Form 4868 filed to extend income tax return Use Form 8892 to extend 6 months if no income tax return due Extension does not extend time for payment

23 Text Page 11 Form 709 Filing Requirement Spouses must file separately Filing required even if no tax due Must file if: Gift > annual exclusion or annual limit to a non-citizen spouse Gift of future interest Gift-splitting elected Gift of jointly-held or community property by one spouse only Executor on behalf of deceased donor Individual is beneficiary, partner, or shareholder of donor entity

24 Text Page 12 Tax Calculation (Taxable Gifts during lifetime * Applicable Tax Rate) (Taxable Gifts in prior years * Applicable Tax Rate) = Tentative Tax Applicable Credit Amount = Tax Due Calculated at cumulative graduated rate

25 Text Page 12 Tax Rates (2012) Taxable Amount ($) Marginal Tax Rate (%) 0 10, ,001 20, ,001 40, ,001 60, ,001 80, , , , , , , , , > 500, The maximum tax rate will be automatically increased in 2013 to 55% if current legislation is not extended.

26 Text Page 13 Sample Calculation Facts 2003: $500K taxable gifts (after annual exclusion) 2006: $600K taxable gifts Value of estate at death (2006) = $2.9 million Step 1: Tax on previous gift(s) $500K in 2003 Tax = $155,800 But $0 paid since tax < lifetime credit available in 2003 $190K lifetime credit remaining ($345, ,800 )

27 Text Page 13 Sample Calculation (cont d) Step 2: Tentative tax on aggregate value of all gifts $1.1M cumulative gifts in 2006 Tentative tax = $386,800 Step 3: Gift Tax due in 2006 $386,800 Tentative tax 155,800 Tax previously paid on 2003 gift [see above] $231,000 Tax attributable to 2006 gift 190,000 Credit remaining after 2003 gift [see above] $ 41,000 Gift tax due in 2006

28 Text Page 13 Sample Calculation (cont d) Step 4: Tax base for Estate Tax $2.90M Value of estate in M Prior taxable gifts [see above] added back to estate $4.00M Tax base used to compute estate tax Step 5: Estate Tax due in 2006 $1,700,800 Tentative tax on $4 million tax base 41,000 Tax previously paid on gifts [see above] $1,659,800 Estate tax liability 780,800 Unified credit (based on $2M in 2006) $ 879,000 Estate tax 2006

29 Text Page 25 Clawback (in years when Unified Credit is rising) Should Unified Credit be amount as it existed under law in year of gift or in year of death? Taxpayer prefers NO clawback If Unified Credit low, previously paid Gift Tax will be higher Since Gift Tax is used as an offset, Estate Tax will be lower IRC states that tax rates in effect at death should be used infer that rule should require credit in year of death (= clawback) BUT gift tax is calculated on annual basis it would be logical to apply credit in year of gift (= no clawback) IRC 2001(b)(2) does not clarify!

30 Text Page 25 Looking forward ( to years when Unified Credit is dropping) Facts: 2012 gift of $5 million; 2013 death with estate of $1 million Unified exemption: $5 million in 2012; $1 million in 2013 Maximum estate tax rate: 35% in 2012; 55% in 2013 Use Date of Gift Use Date of Death Taxable estate 1,000,000 1,000,000 + Adjusted taxable gifts 5,000,000 5,000,000 = Unified amount 6,000,000 6,000,000 Tentative tax 2,940,800 2,940,800 - Deemed gift tax paid 660,000 2,045,000 = Gross estate tax 2,280, ,000

31 Text Page 13 Who is liable for gift tax? Donor Liability may shift to donee if donor is delinquent; must be assessed against transferee within 1 year after donor s statute expires Example: Title to family home transferred from father to son in exchange for care provided (= gift since state law does not mandate payment to child regardless of age or services performed). Dad was assessed gift tax on transfer Son assumed & held liable for Dad s previously unpaid income tax debts secured by IRS lien on home prior to transfer

32 Text Page 13 Famous Problem Nicolas Cage owes $624, in unpaid gift taxes to the IRS for $1.8 million paid to people between 2004 and 2009.

33 Text Page 14 Penalties 20% for substantial valuation misstatements; 40% for gross misstatements May be assessed against taxpayers as well as persons who knowingly aid/abet understatement of tax liability (e.g. attorney & appraiser) Preparer penalties previously applicable to income tax returns only were extended to include gift & estate returns in 2007

34 Text Page 14 Statute of Limitations 3 years (6 years if > 25% of items unreported) Gift tax valuations adequately disclosed on properly filed 709 cannot be challenged by IRS on 706 [TRA 1997] Example: Taxpayer gifts private company stock to daughter & values shares at $10K based on minority & marketability discounts. Since gift < annual exclusion, it is not reportable BUT file 709 anyway to explain valuation & prevent IRS from challenging future gifts & inheritances after statute on 709 expires.

35 Text Page 15 Valuation Valued at FMV when transfer is complete Value may be discounted for: Lack of marketability (e.g. restricted stock, limited partnerships) Lack of control (e.g. minority shares) Built-in gains on appreciation prior to donee ownership Frequently disputed by IRS

36 Text Page 17 Carry-over Basis GENERAL RULE: Donee s Basis = Donor s Basis + Gift tax attributable to accumulated appreciation Example: Donor gifts property ($100K basis; $120K basis) & pay $5K gift tax. Donee then sells property for $150K. 100,000 Donor s basis + 1,000 Allocated gift tax paid {(120K 100K) 100K} * 5K 101,000 Donee s basis

37 Text Page 18 Carryover Basis Exceptions Sell < FMV Sell btw FMV & D s Basis Sell > FMV Donor s Basis FMV at the time of gift Donee s Sales Price Donee s Basis or Donee s Capital Gain (Loss) (10) = = Donee s Basis equals The lower of FMV or Donor s Basis Basis for gain is 100, but no gain; basis for loss is 90, but no loss Donor s basis [GENERAL rule]

38 Text Page 19 Generation-skipping Transfers (GST) Imposed on direct skips to a relative 2 generations below GST tax rate = top Estate Tax rate in effect (currently 35%). No graduated rates! GST not imposed on direct payments for tuition and medical payments, nor on gifts < annual exclusion $5 million GST exemption (not portable)

39 Text Page 19 Transfers to Trusts No GST on gifts to trust if: Less than $13K, For the benefit of one skip person, and Trust will be includible in skip person s estate Example: Grandfather previously made annual gifts to 3 grandchildren (eligible for annual gift tax exclusion). Instead, creates trust for benefit of all 3 children & makes one lump-sum gift of $39K (ineligible for GST exclusion).

40 Text Page 20 GST Tax Computation GST Tax = all GST transfers during year * max. estate tax rate * inclusion ratio Inclusion ratio converts allocated portion of GST exemption into tax rate deduction Example: Taxpayer transfers $2 million to trust for son & grandson & allocates $500K of her GST exemption to the transfer. When son dies, there is taxable termination of trust now valued at $3 million. Inclusion Ratio = 1 (500,000 2,000,000) = 75% GST Tax = $3 million * 35% * 75% = $795,000

41 Text Page 20 GST Tax Reporting Lifetime transfers reported on Form 709, Schedule A, Part 2 Transfers at death reported on Form 706, Schedule R Liability for GST Tax: Transferor if direct skip Trustee if taxable termination of trust Transferee if distribution from trust

42 Text Page 21 Gift & Estate Tax Combo Lifetime gifts are added back to bump decedent s estate into higher marginal bracket Gift tax previously paid is deducted against estate tax liability no double taxation, BUT gift always taxed at highest possible bracket

43 Text Page 21 Gift vs. Estate Tax Gift tax is tax-exclusive (assessed only on assets transferred); estate tax is inclusive (assessed on assets transferred + assets used to pay tax) Example: Assume gift & estate tax rates are flat 50% & all unified credit has been used Gift: Donor transfers $2 million gift to donee & pays $1 million tax from other moneys Donee pockets ⅔ Estate: Decedent leaves $3 million estate; executor must use $1.5 million to pay tax Heir receives ½

44 Text Page 21 Deathbed Transfers Certain last-minute (within 3 years) transfers intended to reduce taxable estate are added back to gross estate Example: Dad gifts personal residence valued at $5,263,000 to Son in 2011, retaining the right to live in the home rent-free Dad pays gift tax of $87.5K Dad dies in 2012 Value of gift & gift tax paid are added back to estate (now $5,350,500); estate tax due will be reduced by amount of gift tax previously paid Affected gifts: Retained life estates, revocable transfers, life insurance proceeds

45

46 Text Page 22 Comprehensive Example Facts: Single Taxpayer gifted $200K to Son reportable $100K to Church reportable $13K each to 5 grandchildren not reportable (exempted by annual exclusion)

47

48 Text Page 24 Step 1: Use Schedule A, Part 1 to report gifts to Son and Church report gifted amounts in full (attach statement & provide as much detail as possible).

49 Text Page 23 Step 2: Do not report gifts to grandchildren in Part 2 or 3 since they are exempt under the annual exclusion.

to determine taxable")

50 Text Page 24 Step 3: Carry totals from Part 1 to Part 4 (on Page 3) deduct annual exclusion & non-taxable charitable deduction (net of its exclusion) to determine taxable gifts.

51 Text Page 23 Step 4: Carry total of taxable gifts on Line 11 of Schedule A, Part 4 to Line 1 of Form 709, Page 1 and complete tax computation using tax rate schedule provided with Form 709 Instructions; then subtract available Unified Credit to determine tax due.

52 Text Page 24 Disclosure is Crucial

53

54

55 Text Page 25 Gift Tax History Years Max. Tax Rates Annual Exclusion Lifetime Exclusion Marital Deduction ,000 N/A N/A 52.5 (1936) ,400 (1942); N/A 50% (1949) $3, $3,000 $30,000 50% $47,000 (1981) ( ); $10,000 62, % 55 $675,000 (2001) % (2002) $11,000 ( ); 1,000, % 45% (2007) $12,000 ( ) $13,000 5,000, % 5,120,000 (2012) 2013 (?) 55 Indexed 1,000, % Joulfaian, The Federal Gift Tax: History, Law, and Economics, US Department of the Treasury OTA Paper 100, November 2007.

56 Text Page 26 Proposed Changes Obama introduced legislation in February 2012: $3.5 million lifetime exclusion ($1 million on GST); 45% maximum rate Arguments in favor of tax: Provides progressivity Provides backstop to income tax Targets inheritances rather than earnings Arguments against tax: Discourages savings & economic growth Burdens small businesses & family farms Assessed at inopportune time

57 Text Page 26 Any guesses? The year of the big gift Paul L. Caron as posted

58 Call or Monica Haven, E.A., J.D. (310) PHONE (310) FAX The information contained herein is for educational use only and should not be construed as tax, financial, or legal advice. Each individual s situation is unique and may require specialized treatment. It is, therefore, imperative that you consult with tax and legal professionals prior to implementation of any strategies discussed.

U.S. GIFT (AND GENERATION-SKIPPING TRANSFER) TAX RETURN CHECKLIST 2013- FORM 709 (For Gifts Made During Calendar Year 2013)

TAX RETURN CHECKLIST 2013- FORM 709 (For Gifts Made During Calendar Year 2013)") U.S. GIFT (AND GENERATION-SKIPPING TRANSFER) TAX RETURN CHECKLIST 2013- FORM 709 (For Gifts Made During Calendar Year 2013) ClientName: Client Number: Prepared by: Date: Reviewed by: Date: 100) GENERAL

U.S. GIFT (AND GENERATION-SKIPPING TRANSFER) TAX RETURN CHECKLIST 2013- FORM 709 (For Gifts Made During Calendar Year 2013) ClientName: Client Number: Prepared by: Date: Reviewed by: Date: 100) GENERAL

Gifting: A Property Transfer Tool of Estate Planning

Gifting: A Property Transfer Tool of Estate Planning by Marsha A. Goetting, Ph.D., CFP, CFCS, Professor and Extension Family Economics Specialist; and Joel Schumacher, Extension Economics Associate Economics

Gifting: A Property Transfer Tool of Estate Planning by Marsha A. Goetting, Ph.D., CFP, CFCS, Professor and Extension Family Economics Specialist; and Joel Schumacher, Extension Economics Associate Economics

Gifting: A Property Transfer Tool of Estate Planning

MontGuide Gifting: A Property Transfer Tool of Estate Planning by Marsha A. Goetting, Ph.D., CFP, CFCS, Professor and Extension Family Economics Specialist; and Joel Schumacher, Extension Economics Associate

MontGuide Gifting: A Property Transfer Tool of Estate Planning by Marsha A. Goetting, Ph.D., CFP, CFCS, Professor and Extension Family Economics Specialist; and Joel Schumacher, Extension Economics Associate

Presentations also allow you to add an introductory note specifically for the client receiving the presentation.

Firm Name Team Name (if one) CPA Planner Name, Credentials Title Street Address City, NY 13160 Phone number xext # Alternate phone # [email protected] website URL Estate Tax Presentations also allow you

Firm Name Team Name (if one) CPA Planner Name, Credentials Title Street Address City, NY 13160 Phone number xext # Alternate phone # [email protected] website URL Estate Tax Presentations also allow you

Estate Planning. Farm Credit East, ACA Stephen Makarevich

Estate Planning Farm Credit East, ACA Stephen Makarevich Farm Business Consultant 9 County Road 618 Lebanon, NJ 08833 1.800.787.3276 [email protected] 1 What is Estate Planning? 2 Estate

Estate Planning Farm Credit East, ACA Stephen Makarevich Farm Business Consultant 9 County Road 618 Lebanon, NJ 08833 1.800.787.3276 [email protected] 1 What is Estate Planning? 2 Estate

Chapter 18 GENERATION-SKIPPING TRANSFER TAX

Chapter 18 GENERATION-SKIPPING TRANSFER TAX WHAT IS IT? This chapter discusses the generation-skipping transfer tax and planning with generation-skipping transfers, including the use of generation-skipping

Chapter 18 GENERATION-SKIPPING TRANSFER TAX WHAT IS IT? This chapter discusses the generation-skipping transfer tax and planning with generation-skipping transfers, including the use of generation-skipping

Form 709: A Practicum

Form 709: A Practicum Monica Haven 042412 Summary Oft ignored by the unwitting taxpayer and overlooked by the practitioner, gift tax returns are left unfiled. Find out when these returns are due and how

Form 709: A Practicum Monica Haven 042412 Summary Oft ignored by the unwitting taxpayer and overlooked by the practitioner, gift tax returns are left unfiled. Find out when these returns are due and how

LIFE INSURANCE TRUSTS

LIFE INSURANCE TRUSTS Robert M. Mendell, JD, CPA* Robert M. Mendell, Attorney at Law, P.C. 908 Town & Country Blvd. Suite 120 Houston, Texas 77024 (713) 888-0700 Fax: (713) 888-0800 Email: [email protected]

LIFE INSURANCE TRUSTS Robert M. Mendell, JD, CPA* Robert M. Mendell, Attorney at Law, P.C. 908 Town & Country Blvd. Suite 120 Houston, Texas 77024 (713) 888-0700 Fax: (713) 888-0800 Email: [email protected]

Form CT-706 NT Instructions Connecticut Estate Tax Return (for Nontaxable Estates)

") (Rev. 05/14) Form CT-706 NT Instructions Connecticut Estate Tax Return (for Nontaxable Estates) General Information For decedents dying during 2014, the Connecticut estate tax exemption amount is $2 million.

(Rev. 05/14) Form CT-706 NT Instructions Connecticut Estate Tax Return (for Nontaxable Estates) General Information For decedents dying during 2014, the Connecticut estate tax exemption amount is $2 million.

GIFTS: THE KEY TO ESTATE TAX SAVINGS

GIFTS: THE KEY TO ESTATE TAX SAVINGS THE LAW FIRM OF ELLEN M. WINKLER 58 Atlantic Avenue Marblehead, MA 01945 Tel. 781-631-6404 Fax 781-631-7338 www.emwinklerlaw.com Estate taxes can take a significant

GIFTS: THE KEY TO ESTATE TAX SAVINGS THE LAW FIRM OF ELLEN M. WINKLER 58 Atlantic Avenue Marblehead, MA 01945 Tel. 781-631-6404 Fax 781-631-7338 www.emwinklerlaw.com Estate taxes can take a significant

Estate Planning For Everyone

Estate Planning For Everyone Boston College Shaw Society Boston College Alumni Association November 20, 2013 Michael J. Puzo, Esq. Hemenway & Barnes LLP 60 State Street Boston, Massachusetts 02109 617-557-9721

Estate Planning For Everyone Boston College Shaw Society Boston College Alumni Association November 20, 2013 Michael J. Puzo, Esq. Hemenway & Barnes LLP 60 State Street Boston, Massachusetts 02109 617-557-9721

CHAPTER 13 Generation Skipping Transfers

CHAPTER 13 Generation Skipping Transfers DISCUSSION QUESTIONS 1. Define skip person. A natural person two or more generations younger than the transferor is a skip person. A trust is a skip person if all

CHAPTER 13 Generation Skipping Transfers DISCUSSION QUESTIONS 1. Define skip person. A natural person two or more generations younger than the transferor is a skip person. A trust is a skip person if all

U.S. Tax and Estate Planning Issues for Canadians with U.S. Assets or U.S. Citizenship

U.S. Tax and Estate Planning Issues for Canadians with U.S. Assets or U.S. Citizenship May 28, 2014 Cheyenne J.H. Reese Christine M. Muckle Legacy Tax + Trust Lawyers Smythe Ratcliffe U.S. Residency Issues

U.S. Tax and Estate Planning Issues for Canadians with U.S. Assets or U.S. Citizenship May 28, 2014 Cheyenne J.H. Reese Christine M. Muckle Legacy Tax + Trust Lawyers Smythe Ratcliffe U.S. Residency Issues

Estate Planning Basics. An Overview of the Estate Planning Process

Estate Planning Basics An Overview of the Estate Planning Process What Is an Estate Plan? An estate plan is a map This map reflects the way you want your personal and financial affairs to be handled in

Estate Planning Basics An Overview of the Estate Planning Process What Is an Estate Plan? An estate plan is a map This map reflects the way you want your personal and financial affairs to be handled in

Review Questions & Answers. Estate Planning

Review Questions & Answers Estate Planning 2003 2015, College for Financial Planning, all rights reserved. This publication may not be duplicated in any way without the express written consent of the publisher.

Review Questions & Answers Estate Planning 2003 2015, College for Financial Planning, all rights reserved. This publication may not be duplicated in any way without the express written consent of the publisher.

Charitable Giving. 2012 Page 1 of 7, see disclaimer on final page

Charitable Giving 2012 Page 1 of 7, see disclaimer on final page By leaving money to charity when you die, the full amount of your charitable gift may be deducted from the value of your taxable estate.

Charitable Giving 2012 Page 1 of 7, see disclaimer on final page By leaving money to charity when you die, the full amount of your charitable gift may be deducted from the value of your taxable estate.

Federal and State Gift and Estate Taxes

E s t a t e P l a n n i n g I N N O R T H C A R O L I N A Federal and State Gift and Estate Taxes Learn about federal gift and estate taxes what they are, how they are calculated, and how they may be avoided

E s t a t e P l a n n i n g I N N O R T H C A R O L I N A Federal and State Gift and Estate Taxes Learn about federal gift and estate taxes what they are, how they are calculated, and how they may be avoided

IRREVOCABLE TRUST CAUTION: The purposes of this memorandum are to assist you and the trustee of your irrevocable trust in:

CHERRY CREEK CORPORATE CENTER 4500 CHERRY CREEK DRIVE SOUTH #600 DENVER, CO 80246-1500 303.322.8943 WWW.WADEASH.COM DISCLAIMER Material presented on the Wade Ash Woods Hill & Farley, P.C., website is intended

CHERRY CREEK CORPORATE CENTER 4500 CHERRY CREEK DRIVE SOUTH #600 DENVER, CO 80246-1500 303.322.8943 WWW.WADEASH.COM DISCLAIMER Material presented on the Wade Ash Woods Hill & Farley, P.C., website is intended

Wealthiest Families Know: 2013 & Beyond

What the Wealthiest Families Know: 2013 & Beyond Determine How Estate Planning Strategies and Life Insurance May Help You Turn Your Goals into a Wealth Legacy Whether you acquired it or inherited it, wealth

What the Wealthiest Families Know: 2013 & Beyond Determine How Estate Planning Strategies and Life Insurance May Help You Turn Your Goals into a Wealth Legacy Whether you acquired it or inherited it, wealth

20. Income Tax Consequences at Death

20. Income Tax Consequences at Death When you die, your income tax situation changes: your estate becomes a separate taxpayer and your tax situation is more complicated. However, the situation also presents

20. Income Tax Consequences at Death When you die, your income tax situation changes: your estate becomes a separate taxpayer and your tax situation is more complicated. However, the situation also presents

Administrator. Any person to whom letters of administration have been issued to administer an intestate estate.

An Estate Planning Glossary The estate planning process is a complex one. During the course of your research into the firm to choose to handle your needs in administering your assets you will hear numerous

An Estate Planning Glossary The estate planning process is a complex one. During the course of your research into the firm to choose to handle your needs in administering your assets you will hear numerous

Tax Effective Cross-Border Will Planning

Tax Effective Cross-Border Will Planning Martin Rochwerg Partner Federated Press Cross-Border Personal Tax Planning February 27-28, 2012 DISCLAIMER 1. We are not U.S. lawyers or tax advisors. 2. This presentation

Tax Effective Cross-Border Will Planning Martin Rochwerg Partner Federated Press Cross-Border Personal Tax Planning February 27-28, 2012 DISCLAIMER 1. We are not U.S. lawyers or tax advisors. 2. This presentation

Form CT-706 NT Instructions Connecticut Estate Tax Return (for Nontaxable Estates)

") (Rev. 06/11) Form CT-706 NT Instructions Connecticut Estate Tax Return (for Nontaxable Estates) General Information For decedents dying on or after January 1, 2011, the Connecticut estate tax exemption

(Rev. 06/11) Form CT-706 NT Instructions Connecticut Estate Tax Return (for Nontaxable Estates) General Information For decedents dying on or after January 1, 2011, the Connecticut estate tax exemption

CHAPTER 6 Estate Tax

CHAPTER 6 Estate Tax DISCUSSION QUESTIONS 1. List six assets included in a decedent s gross estate. 1. Cash. 2. Stocks and bonds. 3. Annuities. 4. Retirement accounts. 5. Notes receivable. 6. Residences.

CHAPTER 6 Estate Tax DISCUSSION QUESTIONS 1. List six assets included in a decedent s gross estate. 1. Cash. 2. Stocks and bonds. 3. Annuities. 4. Retirement accounts. 5. Notes receivable. 6. Residences.

IRREVOCABLE LIFE INSURANCE TRUST CAUTION:

CHERRY CREEK CORPORATE CENTER 4500 CHERRY CREEK DRIVE SOUTH #600 DENVER, CO 80246-1500 303.322.8943 WWW.WADEASH.COM DISCLAIMER Material presented on the Wade Ash Woods Hill & Farley, P.C., website is intended

CHERRY CREEK CORPORATE CENTER 4500 CHERRY CREEK DRIVE SOUTH #600 DENVER, CO 80246-1500 303.322.8943 WWW.WADEASH.COM DISCLAIMER Material presented on the Wade Ash Woods Hill & Farley, P.C., website is intended

By Edward L. Perkins, JD, LLM. CPE CREDIT - 1.0 Hour of Interactive Self-Study

Estate Planning After the Tax Relief Act of 2010 What to Do? By Edward L. Perkins, JD, LLM CPE CREDIT - 1.0 Hour of Interactive Self-Study FIELD OF STUDY - Taxation PROGRAM LEVEL - Intermediate PREREQUISITE

Estate Planning After the Tax Relief Act of 2010 What to Do? By Edward L. Perkins, JD, LLM CPE CREDIT - 1.0 Hour of Interactive Self-Study FIELD OF STUDY - Taxation PROGRAM LEVEL - Intermediate PREREQUISITE

Wealth Transfer Planning Considerations for 2011 and 2012

THE CENTER FOR WEALTH PLANNING Wealth Transfer Planning Considerations for 2011 and 2012 March 2011 The Center for Wealth Planning is part of Credit Suisse s Private Banking USA and does not provide tax

THE CENTER FOR WEALTH PLANNING Wealth Transfer Planning Considerations for 2011 and 2012 March 2011 The Center for Wealth Planning is part of Credit Suisse s Private Banking USA and does not provide tax

Robert J. Ross 1622 W. Colonial Parkway, Suite 201 (847) 358-5757 Inverness, Illinois 60067 Fax (847) 358-7088 [email protected]

358-5757 Inverness, Illinois 60067 Fax (847) 358-7088 Bob@RobertJRoss.com") Law Offices of Robert J. Ross 1622 W. Colonial Parkway, Suite 201 (847) 358-5757 Inverness, Illinois 60067 Fax (847) 358-7088 [email protected] ESTATE PLANNING Estate planning is more than simply signing

Law Offices of Robert J. Ross 1622 W. Colonial Parkway, Suite 201 (847) 358-5757 Inverness, Illinois 60067 Fax (847) 358-7088 [email protected] ESTATE PLANNING Estate planning is more than simply signing

Divorce and Life Insurance. in brief

Divorce and Life Insurance in brief Divorce and Life Insurance Introduction In a divorce, property is divided between the spouses. In addition, a divorce decree may require that one spouse pay alimony

Divorce and Life Insurance in brief Divorce and Life Insurance Introduction In a divorce, property is divided between the spouses. In addition, a divorce decree may require that one spouse pay alimony

HERMENZE & MARCANTONIO LLC ADVANCED ESTATE PLANNING TECHNIQUES - 2015

HERMENZE & MARCANTONIO LLC ADVANCED ESTATE PLANNING TECHNIQUES - 2015 I. Overview of federal, Connecticut, and New York estate and gift taxes. A. Federal 1. 40% tax rate. 2. Unlimited estate and gift tax

HERMENZE & MARCANTONIO LLC ADVANCED ESTATE PLANNING TECHNIQUES - 2015 I. Overview of federal, Connecticut, and New York estate and gift taxes. A. Federal 1. 40% tax rate. 2. Unlimited estate and gift tax

Estate Tax Overview. Emphasis on Generation Skipping Transfers

Estate Tax Overview Emphasis on Generation Skipping Transfers 1 A Brief History - 1916 The Revenue Act of 1916 (39 Stat. 756) created a tax on the transfer of wealth from an estate to its beneficiaries,

Estate Tax Overview Emphasis on Generation Skipping Transfers 1 A Brief History - 1916 The Revenue Act of 1916 (39 Stat. 756) created a tax on the transfer of wealth from an estate to its beneficiaries,

Final Affairs: (Estate) Planning is a Good Thing

Planning is a Good Thing") Final Affairs: (Estate) Planning is a Good Thing Senior Ministries of the Episcopal Diocese of Newark St. Luke s Episcopal Church Montclair, NJ March 14, 2015 Lance T. Eisenberg, Esq. Berkowitz, Lichtstein,

Final Affairs: (Estate) Planning is a Good Thing Senior Ministries of the Episcopal Diocese of Newark St. Luke s Episcopal Church Montclair, NJ March 14, 2015 Lance T. Eisenberg, Esq. Berkowitz, Lichtstein,

Sales Strategy Sale to a Grantor Trust (SAGT)

") Estate planners have been using the Irrevocable Life Insurance Trust (ILIT) for many years, to increase wealth and liquidity outside the taxable estate. 1 However, transfers to ILITs One effective technique

Estate planners have been using the Irrevocable Life Insurance Trust (ILIT) for many years, to increase wealth and liquidity outside the taxable estate. 1 However, transfers to ILITs One effective technique

The New Era of Wealth Transfer Planning #1. American Taxpayer Relief Act Boosts Life Insurance. For agent use only. Not for public distribution.

The New Era of Wealth Transfer Planning #1 American Taxpayer Relief Act Boosts Life Insurance For agent use only. Not for public distribution. In January 2013 Congress stepped back from the fiscal cliff

The New Era of Wealth Transfer Planning #1 American Taxpayer Relief Act Boosts Life Insurance For agent use only. Not for public distribution. In January 2013 Congress stepped back from the fiscal cliff

United States Estate (and Generation-Skipping Transfer) Tax Return

Tax Return") Form 706 (Rev. August 2013) Department of the Treasury Internal Revenue Service United States Estate (and Generation-Skipping Transfer) Tax Return Estate of a citizen or resident of the United States (see

Form 706 (Rev. August 2013) Department of the Treasury Internal Revenue Service United States Estate (and Generation-Skipping Transfer) Tax Return Estate of a citizen or resident of the United States (see

Wealth transfer and gifting strategies. A guide to lifetime gifts. Life s better when we re connected

Wealth transfer and gifting strategies A guide to lifetime gifts Life s better when we re connected Index 3 Introduction 4 Transfer tax basics 5 An overview of the federal gift tax system 6 Outright gifts

Wealth transfer and gifting strategies A guide to lifetime gifts Life s better when we re connected Index 3 Introduction 4 Transfer tax basics 5 An overview of the federal gift tax system 6 Outright gifts

2016 Tax Planning & Reference Guide

2016 Tax Planning & Reference Guide The 2016 Tax Planning & Reference Guide is designed as a reference and is not intended to function as tax advice. Please consult your professional accounting advisor

2016 Tax Planning & Reference Guide The 2016 Tax Planning & Reference Guide is designed as a reference and is not intended to function as tax advice. Please consult your professional accounting advisor

KURT D. PANOUSES, P.A. ATTORNEYS AND COUNSELORS AT LAW 310 Fifth Avenue Indialantic, FL 32903 (321) 729-9455 FAX: (321) 768-2655

729-9455 FAX: (321) 768-2655") KURT D. PANOUSES, P.A. ATTORNEYS AND COUNSELORS AT LAW 310 Fifth Avenue Indialantic, FL 32903 (321) 729-9455 FAX: (321) 768-2655 Kurt D. Panouses is Board Certified by the Florida Bar as a Specialist in

KURT D. PANOUSES, P.A. ATTORNEYS AND COUNSELORS AT LAW 310 Fifth Avenue Indialantic, FL 32903 (321) 729-9455 FAX: (321) 768-2655 Kurt D. Panouses is Board Certified by the Florida Bar as a Specialist in

A Sole Proprietor Insured Buy-Sell Plan

A Sole Proprietor Insured Buy-Sell Plan At a sole proprietor s death, the business is dissolved and all business assets and liabilities become part of the sole proprietor's personal estate. Have you evaluated

A Sole Proprietor Insured Buy-Sell Plan At a sole proprietor s death, the business is dissolved and all business assets and liabilities become part of the sole proprietor's personal estate. Have you evaluated

Preparing a Federal Estate Tax Return Form 706, By Yahne Miorini, LL.M.

You must attach to the return a certified copy There are 5 parts in the Form 706, 9 schedules to determine the gross estate, and 7 schedules for deductions. It is a good practice to include all of the

You must attach to the return a certified copy There are 5 parts in the Form 706, 9 schedules to determine the gross estate, and 7 schedules for deductions. It is a good practice to include all of the

DIVORCE AND LIFE INSURANCE, QUALIFIED PLANS AND IRAS 2013-2015

DIVORCE AND LIFE INSURANCE, QUALIFIED PLANS AND IRAS 2013-2015 I. INTRODUCTION In a divorce, property is generally divided between the spouses. Generally, all assets of the spouses, whether individual,

DIVORCE AND LIFE INSURANCE, QUALIFIED PLANS AND IRAS 2013-2015 I. INTRODUCTION In a divorce, property is generally divided between the spouses. Generally, all assets of the spouses, whether individual,

Planning your estate

Planning your estate A general guide to estate planning Policies issued by: American General Life Insurance Company The United States Life Insurance Company in the City of New York What is estate planning?

Planning your estate A general guide to estate planning Policies issued by: American General Life Insurance Company The United States Life Insurance Company in the City of New York What is estate planning?

Estate Tax Concepts. for Edward and Tina Collins

Estate Tax Concepts for Edward and Tina Collins Joseph Davis, CLU, ChFC 215 Broad Street Charlotte, North Carolina 26292 Phone: 704-927-5555 Mobile Phone: 704-549-5555 Fax: 704-549-6666 Email: [email protected]

Estate Tax Concepts for Edward and Tina Collins Joseph Davis, CLU, ChFC 215 Broad Street Charlotte, North Carolina 26292 Phone: 704-927-5555 Mobile Phone: 704-549-5555 Fax: 704-549-6666 Email: [email protected]

Sales Strategy Estate Planning for Non-Citizens in the United States

Sales Strategy Estate Planning for Non-Citizens in the United States SINGLE LIFE SPOUSAL ACCESS TRUST: A LIFE INSURANCE ALTERNATIVE As large numbers of people from other countries settle in the United

Sales Strategy Estate Planning for Non-Citizens in the United States SINGLE LIFE SPOUSAL ACCESS TRUST: A LIFE INSURANCE ALTERNATIVE As large numbers of people from other countries settle in the United

IRREVOCABLE TRUSTS Memorandum to the Settlor and the Trustee

Memorandum to the Settlor and the Trustee by Layne T. Rushforth 1. GENERALLY This memorandum is for the settlor (creator) and the trustee (manager) of an irrevocable trust. There is a section for each

Memorandum to the Settlor and the Trustee by Layne T. Rushforth 1. GENERALLY This memorandum is for the settlor (creator) and the trustee (manager) of an irrevocable trust. There is a section for each

CLIENT GUIDE. Advanced Markets. Estate Planning Client Guide

CLIENT GUIDE Advanced Markets Estate Planning Client Guide TABLE OF CONTENTS Why Create an Estate Plan?........................ 1 Basic Estate Planning Tools......................... 2 Funding an Irrevocable

CLIENT GUIDE Advanced Markets Estate Planning Client Guide TABLE OF CONTENTS Why Create an Estate Plan?........................ 1 Basic Estate Planning Tools......................... 2 Funding an Irrevocable

IN THIS ISSUE: July, 2011 j Income Tax Planning Concepts in Estate Planning

IN THIS ISSUE: Goals of Income Tax Planning Basic Estate Planning Has No Income Tax Impact Advanced Estate Planning Can Have Income Tax Implications Taxation of Corporations, LLCs, Partnerships and Non-

IN THIS ISSUE: Goals of Income Tax Planning Basic Estate Planning Has No Income Tax Impact Advanced Estate Planning Can Have Income Tax Implications Taxation of Corporations, LLCs, Partnerships and Non-

The. Estate Planner. The GRAT: A limited time offer? International relations. Avoid probate to keep your estate private

The Estate Planner September/October 2013 The GRAT: A limited time offer? International relations Estate planning for noncitizens Avoid probate to keep your estate private Estate Planning Red Flag You

The Estate Planner September/October 2013 The GRAT: A limited time offer? International relations Estate planning for noncitizens Avoid probate to keep your estate private Estate Planning Red Flag You

How are trusts and estates taxed for income tax purposes?

Income Taxation of Trusts and Estates How are trusts and estates taxed for income tax purposes? What are the general income tax rules for trusts? What are the general income tax rules for estates? What

Income Taxation of Trusts and Estates How are trusts and estates taxed for income tax purposes? What are the general income tax rules for trusts? What are the general income tax rules for estates? What

HERMENZE & MARCANTONIO LLC ESTATE PLANNING PRIMER FOR MARRIED COUPLES 2015 (New York)

") HERMENZE & MARCANTONIO LLC ESTATE PLANNING PRIMER FOR MARRIED COUPLES 2015 (New York) I. Purposes of Estate Planning. II. A. Providing for the distribution and management of your assets after your death.

HERMENZE & MARCANTONIO LLC ESTATE PLANNING PRIMER FOR MARRIED COUPLES 2015 (New York) I. Purposes of Estate Planning. II. A. Providing for the distribution and management of your assets after your death.

Estate planning strategies using life insurance in a trust Options for handling distributions, rollovers and conversions

Estate planning strategies using life insurance in a trust Options for handling distributions, rollovers and conversions Life s better when we re connected Table of contents Find your questions review

Estate planning strategies using life insurance in a trust Options for handling distributions, rollovers and conversions Life s better when we re connected Table of contents Find your questions review

ESTATE PLANNING QUESTIONNAIRE

ESTATE PLANNING QUESTIONNAIRE Please complete this form to the best of your ability and bring it with you to our initial meeting. Your cooperation in this regard will make your appointment more productive

ESTATE PLANNING QUESTIONNAIRE Please complete this form to the best of your ability and bring it with you to our initial meeting. Your cooperation in this regard will make your appointment more productive

TAX RELIEF ACT UPDATED DECEMBER 29, 2010

2010 TAX RELIEF ACT UPDATED DECEMBER 29, 2010 TAX RELIEF, UNEMPLOYMENT INSURANCE RE-AUTHORIZATION, AND JOB CREATION ACT OF 2010 INTRODUCTION On December 17, 2010, President Obama signed the much-anticipated

2010 TAX RELIEF ACT UPDATED DECEMBER 29, 2010 TAX RELIEF, UNEMPLOYMENT INSURANCE RE-AUTHORIZATION, AND JOB CREATION ACT OF 2010 INTRODUCTION On December 17, 2010, President Obama signed the much-anticipated

RETIREMENT PLANNING FOR THE SMALL BUSINESS

RETIREMENT PLANNING FOR THE SMALL BUSINESS PI-1157595 v1 0950000-0102 II. INCOME AND TRANSFER TAX CONSIDERATIONS A. During Participant s Lifetime 1. Prior to Distribution Income tax on earnings on plan

RETIREMENT PLANNING FOR THE SMALL BUSINESS PI-1157595 v1 0950000-0102 II. INCOME AND TRANSFER TAX CONSIDERATIONS A. During Participant s Lifetime 1. Prior to Distribution Income tax on earnings on plan

THE FUTURE OF ESTATE PLANNING - 2012 AND BEYOND

THE FUTURE OF ESTATE PLANNING - 2012 AND BEYOND By Edward L. Perkins, JD, LLM (Tax), CPA I. The New Estate Planning Reality A. The Return of the Federal Estate Tax, et al. 1. The Estate Tax Returns After

THE FUTURE OF ESTATE PLANNING - 2012 AND BEYOND By Edward L. Perkins, JD, LLM (Tax), CPA I. The New Estate Planning Reality A. The Return of the Federal Estate Tax, et al. 1. The Estate Tax Returns After

Generation Skipping Transfer Tax

Generation Skipping Transfer Tax Producer Guide For agent use only. Not for public distribution. Generation Skipping Transfer Tax Summary The generation skipping transfer (GST) tax is a complex tax. This

Generation Skipping Transfer Tax Producer Guide For agent use only. Not for public distribution. Generation Skipping Transfer Tax Summary The generation skipping transfer (GST) tax is a complex tax. This

Minimum Distributions & Beneficiary Designations: Planning Opportunities

28 $ $ $ RETIREMENT PLANS The rules regarding distributions and designated beneficiaries are complex, but there are strategies that will help minimize income and estate taxes. Minimum Distributions & Beneficiary

28 $ $ $ RETIREMENT PLANS The rules regarding distributions and designated beneficiaries are complex, but there are strategies that will help minimize income and estate taxes. Minimum Distributions & Beneficiary

T he transfer of assets upon death by residents of Puerto Rico ( PR ) may be subject to estate taxes imposed by the United

may be subject to estate taxes imposed by the United") US and PR Estate Tax considerations for Puerto Rico Residents Born in PR or Who Acquired US Citizenship Solely by Residency in PR (PR Persons) By: Ricardo Muñiz, Esq. T he transfer of assets upon death

US and PR Estate Tax considerations for Puerto Rico Residents Born in PR or Who Acquired US Citizenship Solely by Residency in PR (PR Persons) By: Ricardo Muñiz, Esq. T he transfer of assets upon death

REVOCABLE LIVING TRUST

CHERRY CREEK CORPORATE CENTER 4500 CHERRY CREEK DRIVE SOUTH, SUITE 600 DENVER, CO 80246-1500 303.322.8943 WWW.WADEASH.COM DISCLAIMER Material presented on the Wade Ash Woods Hill & Farley, P.C., website

CHERRY CREEK CORPORATE CENTER 4500 CHERRY CREEK DRIVE SOUTH, SUITE 600 DENVER, CO 80246-1500 303.322.8943 WWW.WADEASH.COM DISCLAIMER Material presented on the Wade Ash Woods Hill & Farley, P.C., website

Estate & Gift Tax Treatment for Non-Citizens

ADVANCED MARKETS Estate & Gift Tax Treatment for Non-Citizens It goes without saying that the laws governing the U.S. estate and gift tax system are complex. When you then consider the additional complexities

ADVANCED MARKETS Estate & Gift Tax Treatment for Non-Citizens It goes without saying that the laws governing the U.S. estate and gift tax system are complex. When you then consider the additional complexities

IRREVOCABLE LIFE INSURANCE TRUSTS

IRREVOCABLE LIFE INSURANCE TRUSTS March 9, 2016 H. Wes Taylor Foley & Lardner LLP 150 E. Gilman St. Madison, Wisconsin 53703 (608) 258-4213 [email protected] A. Irrevocable Trusts a. In General. i. Irrevocable

IRREVOCABLE LIFE INSURANCE TRUSTS March 9, 2016 H. Wes Taylor Foley & Lardner LLP 150 E. Gilman St. Madison, Wisconsin 53703 (608) 258-4213 [email protected] A. Irrevocable Trusts a. In General. i. Irrevocable

Advanced Estate Planning

Advanced Estate Planning October 7, 2014 Presented by Gregory E. Lambourne, Esq. Brown & Streza LLP Irvine, CA Review of Basic Estate Planning Health Care Directives Powers of Attorney The Probate Process

Advanced Estate Planning October 7, 2014 Presented by Gregory E. Lambourne, Esq. Brown & Streza LLP Irvine, CA Review of Basic Estate Planning Health Care Directives Powers of Attorney The Probate Process

Prepared For: The Client Family

Annuity Maximization Estate Planning and Deferred Annuities - Annuitization Prepared For: The Client Family Insurance products are issued by: John Hancock Life Insurance Company (U.S.A.), Boston, MA and

Annuity Maximization Estate Planning and Deferred Annuities - Annuitization Prepared For: The Client Family Insurance products are issued by: John Hancock Life Insurance Company (U.S.A.), Boston, MA and

Hot Topic!!!! Funding Trust-Owned Life Insurance - Selecting the Best Option.

Executive Capital Resources 5550 W Touhy Ave. Suite 304 Skokie, Illinois 60077 847-673-2677 www.ecrllc.com [email protected] Washimgton Report 13-12 Hot Topic!!!! Funding Trust-Owned Life Insurance -

Executive Capital Resources 5550 W Touhy Ave. Suite 304 Skokie, Illinois 60077 847-673-2677 www.ecrllc.com [email protected] Washimgton Report 13-12 Hot Topic!!!! Funding Trust-Owned Life Insurance -

HOW TO MAKE CHARITABLE GIFTS FROM YOUR IRA DONOR S GUIDE

HOW TO MAKE CHARITABLE GIFTS FROM YOUR IRA DONOR S GUIDE H OW TO M AKE C HARITABLE G IFTS F ROM Y OUR IRA Thanks to the success of tax-deferred investments within qualified retirement plans, many people

HOW TO MAKE CHARITABLE GIFTS FROM YOUR IRA DONOR S GUIDE H OW TO M AKE C HARITABLE G IFTS F ROM Y OUR IRA Thanks to the success of tax-deferred investments within qualified retirement plans, many people

The Basics of Estate Planning

The Basics of Estate Planning Introduction The process of estate planning can be a daunting prospect. Often individuals will avoid the process altogether. Obviously, this is not the best approach since

The Basics of Estate Planning Introduction The process of estate planning can be a daunting prospect. Often individuals will avoid the process altogether. Obviously, this is not the best approach since

U.S. Taxes for Canadians with U.S. assets

U.S. Taxes for Canadians with U.S. assets December 2014 U.S. Gift, Estate and Generation Skipping Transfer Tax can affect Canadians who don t even live in the United States. This article examines how these

U.S. Taxes for Canadians with U.S. assets December 2014 U.S. Gift, Estate and Generation Skipping Transfer Tax can affect Canadians who don t even live in the United States. This article examines how these

ESTATE TAX RETURN ORGANIZER FORM 706

ESTATE TAX RETURN ORGANIZER FORM 706 This organizer is designed to assist you, the personal representative, in gathering the information required for preparation of the appropriate estate and inheritance

ESTATE TAX RETURN ORGANIZER FORM 706 This organizer is designed to assist you, the personal representative, in gathering the information required for preparation of the appropriate estate and inheritance

Advanced Markets Estate Planning for Non-Citizens in the United States

Estate Planning for Non-Citizens in the United States SINGLE LIFE SPOUSAL ACCESS TRUSTS: A LIFE INSURANCE ALTERNATIVE As large numbers of people from other countries settle in the United States (U.S.),

Estate Planning for Non-Citizens in the United States SINGLE LIFE SPOUSAL ACCESS TRUSTS: A LIFE INSURANCE ALTERNATIVE As large numbers of people from other countries settle in the United States (U.S.),

Effective Planning with Life Insurance

Effective Planning with Life Insurance The Tax Considerations... Ken Knox, CLU, ChFC Regional Director The Penn Mutual Life Insurance Company 1304529TM_Sept17 Retirement Planning Case Scenario #1... Client

Effective Planning with Life Insurance The Tax Considerations... Ken Knox, CLU, ChFC Regional Director The Penn Mutual Life Insurance Company 1304529TM_Sept17 Retirement Planning Case Scenario #1... Client

Preserve and protect your legacy. UBS Trust Company, N.A.

Preserve and protect your legacy UBS Trust Company, N.A. Contents Common trust and estate planning documents.... 2 Will... 2 Living or revocable trust.... 2 Living will and health care proxy... 2 Financial

Preserve and protect your legacy UBS Trust Company, N.A. Contents Common trust and estate planning documents.... 2 Will... 2 Living or revocable trust.... 2 Living will and health care proxy... 2 Financial

IN THIS ISSUE: March, 2011 j Planning with the $5 Million Gift Tax Exemption

IN THIS ISSUE: Federal Gift, Estate and GST Exemptions and Tax Rates New York State Gift & Estate Tax March, 2011 j Planning with the $5 Million Gift Tax Exemption By: Louis W. Pierro, Esq., Philip A.

IN THIS ISSUE: Federal Gift, Estate and GST Exemptions and Tax Rates New York State Gift & Estate Tax March, 2011 j Planning with the $5 Million Gift Tax Exemption By: Louis W. Pierro, Esq., Philip A.

Custodial accounts 3. Kiddie tax 4. Estimated tax payments 4. Retirement plans 6. 2015 individual income tax rates 10. Charitable contributions 12

a b 2015 tax planning guide The confidence to pursue all your life goals begins with a plan. Advice. Beyond investing. Your financial life encompasses much more than the current markets. It includes your

a b 2015 tax planning guide The confidence to pursue all your life goals begins with a plan. Advice. Beyond investing. Your financial life encompasses much more than the current markets. It includes your

Instructions for Completing Indiana Inheritance Tax Return

Instructions for Completing Indiana Return This form does not need to be completed for those individuals dying after Dec. 31, 2012. For those individuals dying before Jan. 1, 2013, this form may need to

Instructions for Completing Indiana Return This form does not need to be completed for those individuals dying after Dec. 31, 2012. For those individuals dying before Jan. 1, 2013, this form may need to

Gift and estate planning: Opportunities abound

Gift and estate planning: Opportunities abound Vanguard research July 2013 Executive summary. Under federal gift and estate tax rules, individuals can potentially make significant gifts that are exempt

Gift and estate planning: Opportunities abound Vanguard research July 2013 Executive summary. Under federal gift and estate tax rules, individuals can potentially make significant gifts that are exempt

How To Get A Life Insurance Policy From A Trust

THE KUGLER SYSTEM ESTATE CONCEPTS TECHNIQUE BOOK TABLE OF CONTENTS Review of Important Terms and Concepts Chapter I: The Proposed Estate Strategy Simple Will Arrangement (assuming Mr. Kugler Predeceases

THE KUGLER SYSTEM ESTATE CONCEPTS TECHNIQUE BOOK TABLE OF CONTENTS Review of Important Terms and Concepts Chapter I: The Proposed Estate Strategy Simple Will Arrangement (assuming Mr. Kugler Predeceases

THE INCOME TAXATION OF ESTATES & TRUSTS

The income taxation of estates and trusts can be complex because, as with partnerships, estates and trusts are a hybrid entity for income tax purposes. Trusts and estates are treated as an entity for certain

The income taxation of estates and trusts can be complex because, as with partnerships, estates and trusts are a hybrid entity for income tax purposes. Trusts and estates are treated as an entity for certain

ESTATE PLANNING BOOKLET

ESTATE PLANNING BOOKLET (Information about Wills, Trusts, Estate Taxes, and more...) P P P SUSSMAN+PARKHURST ATTORNEYS AT LAW ROSS A. SUSSMAN (612) 465-0099 CAMERON M. PARKHURST (612) 465-0097 222 NORTH

ESTATE PLANNING BOOKLET (Information about Wills, Trusts, Estate Taxes, and more...) P P P SUSSMAN+PARKHURST ATTORNEYS AT LAW ROSS A. SUSSMAN (612) 465-0099 CAMERON M. PARKHURST (612) 465-0097 222 NORTH

First-Time Home Buyer Savings Account Guidelines

Introduction During the 2014 Session, the Virginia General Assembly enacted House Bill 331 (2014 Acts of Assembly, Chapter 729), which allows an individual to designate an account at a financial institution

Introduction During the 2014 Session, the Virginia General Assembly enacted House Bill 331 (2014 Acts of Assembly, Chapter 729), which allows an individual to designate an account at a financial institution