There is no difference when everyone is identical. All systems are equal

|

|

|

- Gregory Johnston

- 10 years ago

- Views:

Transcription

1 PART I: Short Answer 5 marks each 1) What is the difference between an ambient and emissions standard; and what are the enforcement issues with each? Ambient set an air/water quality level. It is the true objective of any enviro policy. Emissions standards limit the pollutants thought to lower ambient quality. The problem with emissions is that it is only a Proxy for ambient quality. It requires knowledge of how the emissions lowers the quality. Ambient Standards would be more desirable since they are the true goal. However, they are harder to enforce. The polluter may not be anywhere near the location of the damage or there may be multiple polluters damaging the same area. Very high transactions costs. 2) Emission taxes and transferable permits are both incentive based pollution controls. Give an explanation and example for a case when taxes are preferred to TEP s and when TEP s would be preferred to Taxes. TEP s require a competitive market. If there is not enough competition, then a tax is preferred. Since TEP s based on aggregate quantities of emissions and taxes are not, TEP s are preferred when there is economic growth. Taxes control the output per firm but not the number of firms, so economic growth will lead to an increase in total emissions under a tax 3) If all firms are identical with respect to their levels of emissions and MAC s, which is system would preferred by society: uniform standards or giving each firm the same number of transferable permits (equal to the standard)? There is no difference when everyone is identical. All systems are equal 4) What is the Coase Theorem and what are the necessary conditions to ensure that it would be an effective manner of dealing with pollution problems? Coase: It does not matter who is initially allocated the property right. As long as rights are well defined, there will be trade that allocates the rights to the most valued use; This will work as long as there is small numbers and the damage is limited to a clearly defined group and all parties have good knowledge of the relevant costs. PART II: True/False/Explain. 5 marks each (no marks without explanation) 5) Suppose, for a PUBLIC good, Skippy has MWTP 1 = 80 4Q and Myrtle has MWTP 2 = 40 2Q. If the marginal cost of the good is MC = 4Q, then, at the optimal quantity, the Fair price for each to pay is $24 (half the MC) which is equal to both Skippy and Myrtle s marginal willingness to pay for that many units. ANS: Add MWTP (vertically) Total MWTP = 120 6Q = MC =4Q Q* = 12 and MC(12) = 48 Skippy s MWTP for 12 = 32 Myrtle s MWTP for 12 = 16. FALSE 1 of 7

2 6) Suppose a chemical factory has MAC = 12 E and a laundry has MD = 2E. If the laundry initially has the right to zero pollution, then at the socially efficient level of emissions, a Lump-sum payment by the chemical factory that is greater than $16 and less than $40 will potentially make both parties better off. ANS: 12 E = 2E therefore E* = 4. At optimum total damages = (1/2)*MD(4)*(4) = (1/2)(8)(4) = 16 For Chemical Factory: TAC at E = 0 is (½)(12)(12) = 72 TAC at E = 4 is ½ (8)(8) = 32 Savings in TAC is 40 TRUE 7) Suppose 10 people each have the following demand for clean drinking water: Q = P (Litres Per Year). If they spend $1500 in the first year (t = 0) on a purifier they can have clean drinking water for the next three years at a price of P = 2. If the interest rate is 10% then a Benefit/Cost calculation says that this project has a net benefit of negative eight hundred dollars ( $800) 8) A regulator is uncertain about position of the MAC curve but knows that the MD curve is steep. In this case an emissions standard is preferred to an emissions tax. TRUE 2 of 7

*MD(4)*(4) = (1/2)(8)(4) = 16 For Chemical Factory: TAC at E = 0 is (½)(12)(12) = 72 TAC at E = 4 is ½ (8)(8) = 32 Savings in TAC is 40 TRUE 7) Suppose 10 people each")

3 PART III: Problems 10 marks each Problem 1: Suppose there are two firms with different MAC s. Firm 1: MAC 1 = 100 E 1 Firm 2: MAC 2 = E 2 Note that without any regulation, both firms will produce 100 units of emissions each (total = 200). The government wishes to reduce total emissions to 100. a) Suppose the government imposes a uniform standard equal to 50 units per firm. Calculate the total abatement cost to each firm and graph your result. Does this meet the equi-marginal principle. Firm 1: TAC= 50x50x0.5 = 1250 (area acg) MAC = 50 Firm 2: TAC = 50x75x0.5 = 1875 (area abg) MAC = 75 Total TAC = 3125 b) Now suppose the government wants to use an emissions tax. Find the tax rate that will reduce the total emissions by 100. What will be the emissions of each firm and what will be their total abatement cost under this system? Is abatement costs the firms only cost under this system? (Hint: find the aggregate MAC to find the optimal tax) Add E 1 + E 2 = (100 MAC) + (100 2/3MAC) = 200-5/3MAC Or MAC = 120 3/5E t set E t = 100 and MAC = 60 = tax Firm 1: E = 40 TAC = 1800 Firm 2: E = 60 TAC = 1200 Total TAC = 3000 (cheaper than standard) c) Which system would they prefer? Demonstrate your choice with numbers (costs). Even though it is more efficient with the tax, firm 1 pays $2400 in taxes plus $1800 in abatement. Firm 2 pays $3600 in taxes plus $1200 in abatement. They prefer Standards. 3 of 7

MAC = 50 Firm 2: TAC = 50x75x0.5 = 1875 (area abg) MAC = 75 Total TAC = 3125 b) Now suppose the government wants to use an emissions tax.")

4 d) Suppose each firm was allocated 50 permits. What would be the amount traded and what would be the NET private cost for each FIRM? Permit Trading would be the same outcome as the TAX. Firm 1 would have E1 = 40 (Abate 60) and sell 10 permits Firm 2 would have E2 = 60 (Abate 40) and buy 10 permits Permits would sell for 60 Private Net costs = TAC +/- permit revenue/cost Firm 1: TAC = 1800 Permit Revenue = 600 Net cost = 1200 Firm 2: TAC = 1200 Permit costs = 600, Net cost = of 7

and sell 10 permits Firm 2 would have E2 = 60 (Abate 40) and buy 10 permits Permits")

5 Problem 2: Suppose that the MD = 5E and with its current technology, the firm s MAC is given by MAC 1 = 200 5E. a) Determine the socially optimal level of emissions E E = 5E, therefore E = 20 b) Determine the emissions tax that would achieve the socially optimal level of emissions. Tax, t = MAC = 200-5E = 200 5(20) = 100 Now suppose the firm can adopt a new technology that changes is MAC to New MAC 2 = 160 4E Assuming no change to standard or tax rate after the change in technology, Calculate change in costs for the firm from adopting the new technology when: c) The government uses an emissions standard equal to your answer in (a) above If Standard set at E = 20, Old Technology has a TAC = $1000. New Technology has MAC = 80 and a TAC = 800. Savings from switching is $200. d) The government uses an emissions tax equal to your answer in (b) (Assume no change to standard or tax rate after the change in technology) With $100 tax Old: MAC1 = 200 5E = 100 tax E = 20 New: MAC2 = 160 4E = 100 tax E = 15 Tech 1 (old) Tech 2 (new) TAC 100 x 20 x (1/2) = x 100 x (1/2) = 1250 TAX Bill 100 x 20 = x 15 = 1500 $3000 $2750 Savings from switching is $250 5 of 7

The government uses an emissions standard equal to your answer in (a) above If Standard set at E = 20, Old")

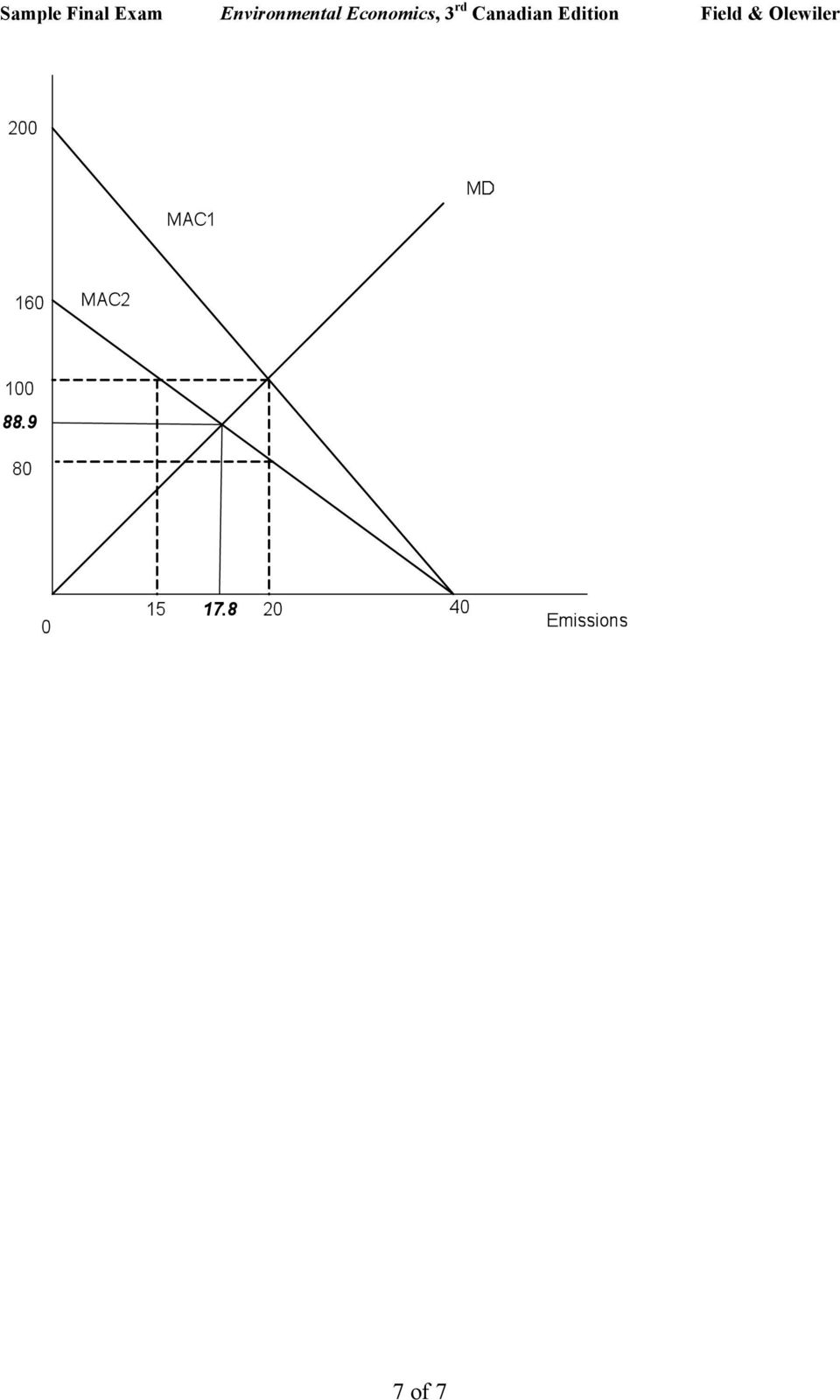

6 Now suppose the government adjusts the standard and/or the tax such that MD = New MAC. Calculate the change in total costs for the firm from adopting the new technology when: e) The government adjusts the standard, and f) The government adjusts the tax rate Under NEW technology: MAC2 = MD 160 4E = 5E E = 17.8 and MAC = 88.9 With a standard equal to 17.8 TAC = ( )(88.9)*(1/2) = Savings = = 13.2 Under Tax rate of t = 88.9, E = 17.8 Tax bill = (88.9)(17.8) = And TAC = TAC + Taxbill = Savings = = of 7

(88.9)*(1/2) = 986.8 Savings = 1000 986.8 = 13.2 Under Tax rate of t = 88.9, E = 17.8 Tax bill = (88.9)(17.8) =1582.")

7 7 of 7

6. Optimal Corrective Taxes

6. Optimal Corrective Taxes 6.1 Introduction The source of inefficiency associated with any externality is the absence of pricing. The external effect is external precisely because the source agent does

6. Optimal Corrective Taxes 6.1 Introduction The source of inefficiency associated with any externality is the absence of pricing. The external effect is external precisely because the source agent does

Unit 9: Utility, Externalities, and Factor Markets Lesson 4: Externalities

Unit 9: Utility, Externalities, and Factor Markets Lesson 4: Externalities Objectives: - Define externality - Draw negative and positive externality graphs. - Explain the remedies for positive and negative

Unit 9: Utility, Externalities, and Factor Markets Lesson 4: Externalities Objectives: - Define externality - Draw negative and positive externality graphs. - Explain the remedies for positive and negative

Fall 2007 Economics 431 Mid-Term Exam Prof. Hamilton

Fall 2007 Economics 431 Mid-Term Exam Prof. Hamilton Name: KEY Question 1A. (15 points) Externalities and Monopoly Markets Demonstrate on a diagram that the deadweight loss from a negative production externality

Fall 2007 Economics 431 Mid-Term Exam Prof. Hamilton Name: KEY Question 1A. (15 points) Externalities and Monopoly Markets Demonstrate on a diagram that the deadweight loss from a negative production externality

Name Eco200: Practice Test 2 Covering Chapters 10 through 15

Name Eco200: Practice Test 2 Covering Chapters 10 through 15 1. Four roommates are planning to spend the weekend in their dorm room watching old movies, and they are debating how many to watch. Here is

Name Eco200: Practice Test 2 Covering Chapters 10 through 15 1. Four roommates are planning to spend the weekend in their dorm room watching old movies, and they are debating how many to watch. Here is

Chapter 17. The Economics of Pollution Control

Chapter 17 The Economics of Pollution Control Economic Rationale for Regulating Pollution Pollution as an Externality -pollution problems are classic cases of a negative externality -the MSC of production

Chapter 17 The Economics of Pollution Control Economic Rationale for Regulating Pollution Pollution as an Externality -pollution problems are classic cases of a negative externality -the MSC of production

chapter >> Externalities Section 2: Policies Toward Pollution

chapter 19 >> Externalities Section 2: Policies Toward Pollution Before 1970, there were no rules governing the amount of sulfur dioxide power plants in the United States could emit which is why acid rain

chapter 19 >> Externalities Section 2: Policies Toward Pollution Before 1970, there were no rules governing the amount of sulfur dioxide power plants in the United States could emit which is why acid rain

Chapter 7: The Costs of Production QUESTIONS FOR REVIEW

HW #7: Solutions QUESTIONS FOR REVIEW 8. Assume the marginal cost of production is greater than the average variable cost. Can you determine whether the average variable cost is increasing or decreasing?

HW #7: Solutions QUESTIONS FOR REVIEW 8. Assume the marginal cost of production is greater than the average variable cost. Can you determine whether the average variable cost is increasing or decreasing?

Figure 1. Quantity (tons of medicine) b. What is represented by the vertical distance between the two supply curves?

b. What is represented by the vertical distance between the two supply curves?") Price per ton Practice Homework Pollution & Environment Economics 101 The Economic Way of Thinking 1. Suppose that the production of pharmaceuticals generates pollution of the Columbia River, which is

Price per ton Practice Homework Pollution & Environment Economics 101 The Economic Way of Thinking 1. Suppose that the production of pharmaceuticals generates pollution of the Columbia River, which is

Problem Set #1 14.41 Public Economics

Problem Set #1 14.41 Public Economics DUE: September 24, 2010 1 Question One For each of the examples below, please answer the following: 1. Does an externality exist? If so, classify the externality as

Problem Set #1 14.41 Public Economics DUE: September 24, 2010 1 Question One For each of the examples below, please answer the following: 1. Does an externality exist? If so, classify the externality as

AGEC 105 Spring 2016 Homework 7. 1. Consider a monopolist that faces the demand curve given in the following table.

AGEC 105 Spring 2016 Homework 7 1. Consider a monopolist that faces the demand curve given in the following table. a. Fill in the table by calculating total revenue and marginal revenue at each price.

AGEC 105 Spring 2016 Homework 7 1. Consider a monopolist that faces the demand curve given in the following table. a. Fill in the table by calculating total revenue and marginal revenue at each price.

Externalities: Problems and Solutions. 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley

Externalities: Problems and Solutions 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley 1 OUTLINE Chapter 5 5.1 Externality Theory 5.2 Private-Sector Solutions to Negative Externalities 5.3

Externalities: Problems and Solutions 131 Undergraduate Public Economics Emmanuel Saez UC Berkeley 1 OUTLINE Chapter 5 5.1 Externality Theory 5.2 Private-Sector Solutions to Negative Externalities 5.3

COMM 220: Ch 17 and 18 Multiple Choice Questions Figure 18.1

COMM 220: Ch 17 and 18 Multiple Choice Questions 1) When sellers have more information about products than buyers do, we would expect A) sellers to get higher prices for their goods than they could otherwise.

COMM 220: Ch 17 and 18 Multiple Choice Questions 1) When sellers have more information about products than buyers do, we would expect A) sellers to get higher prices for their goods than they could otherwise.

Exam Prep Questions and Answers

Exam Prep Questions and Answers Instructions: You will have 75 minutes for the exam. Do not cheat. Raise your hand if you have a question, but continue to work on the exam while waiting for your question

Exam Prep Questions and Answers Instructions: You will have 75 minutes for the exam. Do not cheat. Raise your hand if you have a question, but continue to work on the exam while waiting for your question

Public Goods & Externalities

Market Failure Public Goods & Externalities Spring 09 UC Berkeley Traeger 2 Efficiency 26 Climate change as a market failure Environmental economics is for a large part about market failures: goods (or

Market Failure Public Goods & Externalities Spring 09 UC Berkeley Traeger 2 Efficiency 26 Climate change as a market failure Environmental economics is for a large part about market failures: goods (or

Solution to Exercise 7 on Multisource Pollution

Peter J. Wilcoxen Economics 437 The Maxwell School Syracuse University Solution to Exercise 7 on Multisource Pollution 1 Finding the Efficient Amounts of Abatement There are two ways to find the efficient

Peter J. Wilcoxen Economics 437 The Maxwell School Syracuse University Solution to Exercise 7 on Multisource Pollution 1 Finding the Efficient Amounts of Abatement There are two ways to find the efficient

Chapter 7 Externalities

Chapter 7 Externalities Reading Essential reading Hindriks, J and G.D. Myles Intermediate Public Economics. (Cambridge: MIT Press, 2006) Chapter 7. Further reading Bator, F.M. (1958) The anatomy of market

Chapter 7 Externalities Reading Essential reading Hindriks, J and G.D. Myles Intermediate Public Economics. (Cambridge: MIT Press, 2006) Chapter 7. Further reading Bator, F.M. (1958) The anatomy of market

c. Given your answer in part (b), what do you anticipate will happen in this market in the long-run?

, what do you anticipate will happen in this market in the long-run?") Perfect Competition Questions Question 1 Suppose there is a perfectly competitive industry where all the firms are identical with identical cost curves. Furthermore, suppose that a representative firm

Perfect Competition Questions Question 1 Suppose there is a perfectly competitive industry where all the firms are identical with identical cost curves. Furthermore, suppose that a representative firm

Name Eco200: Practice Test 1 Covering Chapters 10 through 15

Name Eco200: Practice Test 1 Covering Chapters 10 through 15 1. Many observers believe that the levels of pollution in our society are too high. a. If society wishes to reduce overall pollution by a certain

Name Eco200: Practice Test 1 Covering Chapters 10 through 15 1. Many observers believe that the levels of pollution in our society are too high. a. If society wishes to reduce overall pollution by a certain

Common in European countries government runs telephone, water, electric companies.

Public ownership Common in European countries government runs telephone, water, electric companies. US: Postal service. Because delivery of mail seems to be natural monopoly. Private ownership incentive

Public ownership Common in European countries government runs telephone, water, electric companies. US: Postal service. Because delivery of mail seems to be natural monopoly. Private ownership incentive

PART A: For each worker, determine that worker's marginal product of labor.

ECON 3310 Homework #4 - Solutions 1: Suppose the following indicates how many units of output y you can produce per hour with different levels of labor input (given your current factory capacity): PART

ECON 3310 Homework #4 - Solutions 1: Suppose the following indicates how many units of output y you can produce per hour with different levels of labor input (given your current factory capacity): PART

Marginal cost. Average cost. Marginal revenue 10 20 40

Economics 101 Fall 2011 Homework #6 Due: 12/13/2010 in lecture Directions: The homework will be collected in a box before the lecture. Please place your name, TA name and section number on top of the homework

Economics 101 Fall 2011 Homework #6 Due: 12/13/2010 in lecture Directions: The homework will be collected in a box before the lecture. Please place your name, TA name and section number on top of the homework

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

MBA 640 Survey of Microeconomics Fall 2006, Quiz 6 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) A monopoly is best defined as a firm that

MBA 640 Survey of Microeconomics Fall 2006, Quiz 6 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) A monopoly is best defined as a firm that

LAW OF MARKET EQUILIBRIUM A free market, if out of equilibrium, tends toward equilibrium.

LAW OF MARKET EQUILIBRIUM A free market, if out of equilibrium, tends toward equilibrium. Free market = one in which prices and quantities are set by bargaining between fully informed buyers and sellers

LAW OF MARKET EQUILIBRIUM A free market, if out of equilibrium, tends toward equilibrium. Free market = one in which prices and quantities are set by bargaining between fully informed buyers and sellers

First degree price discrimination ECON 171

First degree price discrimination Introduction Annual subscriptions generally cost less in total than one-off purchases Buying in bulk usually offers a price discount these are price discrimination reflecting

First degree price discrimination Introduction Annual subscriptions generally cost less in total than one-off purchases Buying in bulk usually offers a price discount these are price discrimination reflecting

Economics 201 Fall 2010 Introduction to Economic Analysis

Economics 201 Fall 2010 Introduction to Economic Analysis Jeffrey Parker Problem Set #5 Solutions Instructions: This problem set is due in class on Wednesday, October 13. If you get stuck, you are encouraged

Economics 201 Fall 2010 Introduction to Economic Analysis Jeffrey Parker Problem Set #5 Solutions Instructions: This problem set is due in class on Wednesday, October 13. If you get stuck, you are encouraged

Assessment Schedule 2014 Economics: Demonstrate understanding of macro-economic influences on the New Zealand economy (91403)

") NCEA Level 3 Economics (91403) 2014 page 1 of 10 Assessment Schedule 2014 Economics: Demonstrate understanding of macro-economic influences on the New Zealand economy (91403) Assessment criteria with Merit

NCEA Level 3 Economics (91403) 2014 page 1 of 10 Assessment Schedule 2014 Economics: Demonstrate understanding of macro-economic influences on the New Zealand economy (91403) Assessment criteria with Merit

Practice Problems on Current Account

Practice Problems on Current Account 1- List de categories of credit items and debit items that appear in a country s current account. What is the current account balance? What is the relationship between

Practice Problems on Current Account 1- List de categories of credit items and debit items that appear in a country s current account. What is the current account balance? What is the relationship between

A. a change in demand. B. a change in quantity demanded. C. a change in quantity supplied. D. unit elasticity. E. a change in average variable cost.

1. The supply of gasoline changes, causing the price of gasoline to change. The resulting movement from one point to another along the demand curve for gasoline is called A. a change in demand. B. a change

1. The supply of gasoline changes, causing the price of gasoline to change. The resulting movement from one point to another along the demand curve for gasoline is called A. a change in demand. B. a change

Midterm Exam #1 - Answers

Page 1 of 9 Midterm Exam #1 Answers Instructions: Answer all questions directly on these sheets. Points for each part of each question are indicated, and there are 1 points total. Budget your time. 1.

Page 1 of 9 Midterm Exam #1 Answers Instructions: Answer all questions directly on these sheets. Points for each part of each question are indicated, and there are 1 points total. Budget your time. 1.

Profit maximization in different market structures

Profit maximization in different market structures In the cappuccino problem as well in your team project, demand is clearly downward sloping if the store wants to sell more drink, it has to lower the

Profit maximization in different market structures In the cappuccino problem as well in your team project, demand is clearly downward sloping if the store wants to sell more drink, it has to lower the

Problem Set #1 14.41 Public Economics

Problem Set # 4.4 Public Economics DUE: September 24, 200 Question One F each of the examples below, please answer the following:. Does an externality exist? If so, classify the externality as positive/negative

Problem Set # 4.4 Public Economics DUE: September 24, 200 Question One F each of the examples below, please answer the following:. Does an externality exist? If so, classify the externality as positive/negative

How To Calculate Profit Maximization In A Competitive Dairy Firm

Microeconomic FRQ s 2005 1. Bestmilk, a typical profit-maximizing dairy firm, is operating in a constant-cost, perfectly competitive industry that is in long-run equilibrium. a. Draw correctly-labeled

Microeconomic FRQ s 2005 1. Bestmilk, a typical profit-maximizing dairy firm, is operating in a constant-cost, perfectly competitive industry that is in long-run equilibrium. a. Draw correctly-labeled

1 Economic Application of Derivatives

1 Economic Application of Derivatives deriv-applic.te and.pdf April 5, 2007 In earlier notes, we have already considered marginal cost as the derivative of the cost function. That is mc() = c 0 () How

1 Economic Application of Derivatives deriv-applic.te and.pdf April 5, 2007 In earlier notes, we have already considered marginal cost as the derivative of the cost function. That is mc() = c 0 () How

11 PERFECT COMPETITION. Chapter. Competition

Chapter 11 PERFECT COMPETITION Competition Topic: Perfect Competition 1) Perfect competition is an industry with A) a few firms producing identical goods B) a few firms producing goods that differ somewhat

Chapter 11 PERFECT COMPETITION Competition Topic: Perfect Competition 1) Perfect competition is an industry with A) a few firms producing identical goods B) a few firms producing goods that differ somewhat

Economics 181: International Trade Homework # 4 Solutions

Economics 181: International Trade Homework # 4 Solutions Ricardo Cavazos and Robert Santillano University of California, Berkeley Due: November 1, 006 1. The nation of Bermuda is small and assumed to

Economics 181: International Trade Homework # 4 Solutions Ricardo Cavazos and Robert Santillano University of California, Berkeley Due: November 1, 006 1. The nation of Bermuda is small and assumed to

Q D = 100 - (5)(5) = 75 Q S = 50 + (5)(5) = 75.

(5) = 75 Q S = 50 + (5)(5) = 75.") 4. The rent control agency of New York City has found that aggregate demand is Q D = 100-5P. Quantity is measured in tens of thousands of apartments. Price, the average monthly rental rate, is measured

4. The rent control agency of New York City has found that aggregate demand is Q D = 100-5P. Quantity is measured in tens of thousands of apartments. Price, the average monthly rental rate, is measured

2 Applications to Business and Economics

2 Applications to Business and Economics APPLYING THE DEFINITE INTEGRAL 442 Chapter 6 Further Topics in Integration In Section 6.1, you saw that area can be expressed as the limit of a sum, then evaluated

2 Applications to Business and Economics APPLYING THE DEFINITE INTEGRAL 442 Chapter 6 Further Topics in Integration In Section 6.1, you saw that area can be expressed as the limit of a sum, then evaluated

Notes - Gruber, Public Finance Section 12.1 Social Insurance What is insurance? Individuals pay money to an insurer (private firm or gov).

.") Notes - Gruber, Public Finance Section 12.1 Social Insurance What is insurance? Individuals pay money to an insurer (private firm or gov). These payments are called premiums. Insurer promises to make a

Notes - Gruber, Public Finance Section 12.1 Social Insurance What is insurance? Individuals pay money to an insurer (private firm or gov). These payments are called premiums. Insurer promises to make a

13 EXPENDITURE MULTIPLIERS: THE KEYNESIAN MODEL* Chapter. Key Concepts

Chapter 3 EXPENDITURE MULTIPLIERS: THE KEYNESIAN MODEL* Key Concepts Fixed Prices and Expenditure Plans In the very short run, firms do not change their prices and they sell the amount that is demanded.

Chapter 3 EXPENDITURE MULTIPLIERS: THE KEYNESIAN MODEL* Key Concepts Fixed Prices and Expenditure Plans In the very short run, firms do not change their prices and they sell the amount that is demanded.

Why is Insurance Good? An Example Jon Bakija, Williams College (Revised October 2013)

") Why is Insurance Good? An Example Jon Bakija, Williams College (Revised October 2013) Introduction The United States government is, to a rough approximation, an insurance company with an army. 1 That is

Why is Insurance Good? An Example Jon Bakija, Williams College (Revised October 2013) Introduction The United States government is, to a rough approximation, an insurance company with an army. 1 That is

Economics 201 Fall 2010 Introduction to Economic Analysis Problem Set #6 Due: Wednesday, November 3

Economics 201 Fall 2010 Introduction to Economic Analysis Jeffrey Parker Problem Set #6 Due: Wednesday, November 3 1. Cournot Duopoly. Bartels and Jaymes are two individuals who one day discover a stream

Economics 201 Fall 2010 Introduction to Economic Analysis Jeffrey Parker Problem Set #6 Due: Wednesday, November 3 1. Cournot Duopoly. Bartels and Jaymes are two individuals who one day discover a stream

MONEY, INTEREST, REAL GDP, AND THE PRICE LEVEL*

Chapter 11 MONEY, INTEREST, REAL GDP, AND THE PRICE LEVEL* The Demand for Topic: Influences on Holding 1) The quantity of money that people choose to hold depends on which of the following? I. The price

Chapter 11 MONEY, INTEREST, REAL GDP, AND THE PRICE LEVEL* The Demand for Topic: Influences on Holding 1) The quantity of money that people choose to hold depends on which of the following? I. The price

3. George W. Bush is the current U.S. President. This is an example of a: A. Normative statement B. Positive statement

Econ 3144 Fall 2006 Test 1 Dr. Rupp Name Sign Pledge I have neither given nor received aid on this exam Multiple Choice Questions (3 points each) 1. What you give up to obtain an item is called your A.

Econ 3144 Fall 2006 Test 1 Dr. Rupp Name Sign Pledge I have neither given nor received aid on this exam Multiple Choice Questions (3 points each) 1. What you give up to obtain an item is called your A.

Law of Demand: Other things equal, price and the quantity demanded are inversely related.

SUPPLY AND DEMAND Law of Demand: Other things equal, price and the quantity demanded are inversely related. Every term is important -- 1. Other things equal means that other factors that affect demand

SUPPLY AND DEMAND Law of Demand: Other things equal, price and the quantity demanded are inversely related. Every term is important -- 1. Other things equal means that other factors that affect demand

AP Microeconomics 2002 Scoring Guidelines

AP Microeconomics 2002 Scoring Guidelines The materials included in these files are intended for use by AP teachers for course and exam preparation in the classroom; permission for any other use must be

AP Microeconomics 2002 Scoring Guidelines The materials included in these files are intended for use by AP teachers for course and exam preparation in the classroom; permission for any other use must be

Review Question - Chapter 7. MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Review Question - Chapter 7 MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) International trade arises from A) the advantage of execution. B) absolute

Review Question - Chapter 7 MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) International trade arises from A) the advantage of execution. B) absolute

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Chapter 11 Monopoly practice Davidson spring2007 MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) A monopoly industry is characterized by 1) A)

Chapter 11 Monopoly practice Davidson spring2007 MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) A monopoly industry is characterized by 1) A)

The Efficiency of Markets. What is the best quantity to be produced from society s standpoint, in the sense of maximizing the net benefit to society?

The Efficiency of Markets What is the best quantity to be produced from society s standpoint, in the sense of maximizing the net benefit to society? We need to look at the benefits to consumers and producers.

The Efficiency of Markets What is the best quantity to be produced from society s standpoint, in the sense of maximizing the net benefit to society? We need to look at the benefits to consumers and producers.

7. Which of the following is not an important stock exchange in the United States? a. New York Stock Exchange

Econ 20B- Additional Problem Set 4 I. MULTIPLE CHOICES. Choose the one alternative that best completes the statement to answer the question. 1. Institutions in the economy that help to match one person's

Econ 20B- Additional Problem Set 4 I. MULTIPLE CHOICES. Choose the one alternative that best completes the statement to answer the question. 1. Institutions in the economy that help to match one person's

Figure 1. D S (private) S' (social) Quantity (tons of medicine)

S' (social) Quantity (tons of medicine)") Price per ton Practice Homework Pollution & Environment Economics 101 The Economic Way of Thinking 1. Suppose that the production of pharmaceuticals generates pollution of the Columbia River, which is

Price per ton Practice Homework Pollution & Environment Economics 101 The Economic Way of Thinking 1. Suppose that the production of pharmaceuticals generates pollution of the Columbia River, which is

13. If Y = AK 0.5 L 0.5 and A, K, and L are all 100, the marginal product of capital is: A) 50. B) 100. C) 200. D) 1,000.

50. B) 100. C) 200. D) 1,000.") Name: Date: 1. In the long run, the level of national income in an economy is determined by its: A) factors of production and production function. B) real and nominal interest rate. C) government budget

Name: Date: 1. In the long run, the level of national income in an economy is determined by its: A) factors of production and production function. B) real and nominal interest rate. C) government budget

Practice Questions Week 6 Day 1

Practice Questions Week 6 Day 1 Multiple Choice Identify the choice that best completes the statement or answers the question. 1. Economists assume that the goal of the firm is to a. maximize total revenue

Practice Questions Week 6 Day 1 Multiple Choice Identify the choice that best completes the statement or answers the question. 1. Economists assume that the goal of the firm is to a. maximize total revenue

2.If actual investment is greater than planned investment, inventories increase more than planned. TRUE.

Macro final exam study guide True/False questions - Solutions Case, Fair, Oster Chapter 8 Aggregate Expenditure and Equilibrium Output 1.Firms react to unplanned inventory investment by reducing output.

Macro final exam study guide True/False questions - Solutions Case, Fair, Oster Chapter 8 Aggregate Expenditure and Equilibrium Output 1.Firms react to unplanned inventory investment by reducing output.

Theoretical Tools of Public Economics. Part-2

Theoretical Tools of Public Economics Part-2 Previous Lecture Definitions and Properties Utility functions Marginal utility: positive (negative) if x is a good ( bad ) Diminishing marginal utility Indifferences

Theoretical Tools of Public Economics Part-2 Previous Lecture Definitions and Properties Utility functions Marginal utility: positive (negative) if x is a good ( bad ) Diminishing marginal utility Indifferences

Pricing decisions and profitability analysis

Pricing decisions and profitability analysis Solutions to Chapter 11 questions Question 11.24 (a) (b) Computation of full costs and budgeted cost-plus selling price EXE WYE Stores Maintenance Admin ( m)

Pricing decisions and profitability analysis Solutions to Chapter 11 questions Question 11.24 (a) (b) Computation of full costs and budgeted cost-plus selling price EXE WYE Stores Maintenance Admin ( m)

Monopolistic Competition

Monopolistic Chapter 17 Copyright 2001 by Harcourt, Inc. All rights reserved. Requests for permission to make copies of any part of the work should be mailed to: Permissions Department, Harcourt College

Monopolistic Chapter 17 Copyright 2001 by Harcourt, Inc. All rights reserved. Requests for permission to make copies of any part of the work should be mailed to: Permissions Department, Harcourt College

Chapter. Perfect Competition CHAPTER IN PERSPECTIVE

Perfect Competition Chapter 10 CHAPTER IN PERSPECTIVE In Chapter 10 we study perfect competition, the market that arises when the demand for a product is large relative to the output of a single producer.

Perfect Competition Chapter 10 CHAPTER IN PERSPECTIVE In Chapter 10 we study perfect competition, the market that arises when the demand for a product is large relative to the output of a single producer.

A Detailed Price Discrimination Example

A Detailed Price Discrimination Example Suppose that there are two different types of customers for a monopolist s product. Customers of type 1 have demand curves as follows. These demand curves include

A Detailed Price Discrimination Example Suppose that there are two different types of customers for a monopolist s product. Customers of type 1 have demand curves as follows. These demand curves include

Chapter 12. Aggregate Expenditure and Output in the Short Run

Chapter 12. Aggregate Expenditure and Output in the Short Run Instructor: JINKOOK LEE Department of Economics / Texas A&M University ECON 203 502 Principles of Macroeconomics Aggregate Expenditure (AE)

Chapter 12. Aggregate Expenditure and Output in the Short Run Instructor: JINKOOK LEE Department of Economics / Texas A&M University ECON 203 502 Principles of Macroeconomics Aggregate Expenditure (AE)

Chapter 6 Economic Growth

Chapter 6 Economic Growth 1 The Basics of Economic Growth 1) The best definition for economic growth is A) a sustained expansion of production possibilities measured as the increase in real GDP over a

Chapter 6 Economic Growth 1 The Basics of Economic Growth 1) The best definition for economic growth is A) a sustained expansion of production possibilities measured as the increase in real GDP over a

, to its new position, ATC 2

S171-S184_Krugman2e_PS_Ch12.qxp 9/16/08 9:22 PM Page S-171 Behind the Supply Curve: Inputs and Costs chapter: 12 1. Changes in the prices of key commodities can have a significant impact on a company s

S171-S184_Krugman2e_PS_Ch12.qxp 9/16/08 9:22 PM Page S-171 Behind the Supply Curve: Inputs and Costs chapter: 12 1. Changes in the prices of key commodities can have a significant impact on a company s

Chapter 22 The Cost of Production Extra Multiple Choice Questions for Review

Chapter 22 The Cost of Production Extra Multiple Choice Questions for Review 1. Implicit costs are: A) equal to total fixed costs. B) comprised entirely of variable costs. C) "payments" for self-employed

Chapter 22 The Cost of Production Extra Multiple Choice Questions for Review 1. Implicit costs are: A) equal to total fixed costs. B) comprised entirely of variable costs. C) "payments" for self-employed

In following this handout, sketch appropriate graphs in the space provided.

Dr. McGahagan Graphs and microeconomics You will see a remarkable number of graphs on the blackboard and in the text in this course. You will see a fair number on examinations as well, and many exam questions,

Dr. McGahagan Graphs and microeconomics You will see a remarkable number of graphs on the blackboard and in the text in this course. You will see a fair number on examinations as well, and many exam questions,

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Economics 103 Spring 2012: Multiple choice review questions for final exam. Exam will cover chapters on perfect competition, monopoly, monopolistic competition and oligopoly up to the Nash equilibrium

Economics 103 Spring 2012: Multiple choice review questions for final exam. Exam will cover chapters on perfect competition, monopoly, monopolistic competition and oligopoly up to the Nash equilibrium

(1) A reduction in the lump sum tax (2) A rise in the marginal propensity to import (3) A decrease in the marginal propensity to consume

A reduction in the lump sum tax (2) A rise in the marginal propensity to import (3) A decrease in the marginal propensity to consume") S.7 Economics On 3 & 4-Sector Simple Keynesian Models S.7 Economics/3 & 4-sector Keynesian Models/p.1 95 #4 Which of the following would reduce the multiplier effect of investment on national income? (1)

S.7 Economics On 3 & 4-Sector Simple Keynesian Models S.7 Economics/3 & 4-sector Keynesian Models/p.1 95 #4 Which of the following would reduce the multiplier effect of investment on national income? (1)

Public Goods and Common Resources

Public Goods and Common Resources chapter: 17 1. The government is involved in providing many goods and services. For each of the goods or services listed, determine whether it is rival or nonrival in

Public Goods and Common Resources chapter: 17 1. The government is involved in providing many goods and services. For each of the goods or services listed, determine whether it is rival or nonrival in

Answers to Text Questions and Problems. Chapter 22. Answers to Review Questions

Answers to Text Questions and Problems Chapter 22 Answers to Review Questions 3. In general, producers of durable goods are affected most by recessions while producers of nondurables (like food) and services

Answers to Text Questions and Problems Chapter 22 Answers to Review Questions 3. In general, producers of durable goods are affected most by recessions while producers of nondurables (like food) and services

Solution to Homework Set 7

Solution to Homework Set 7 Managerial Economics Fall 011 1. An industry consists of five firms with sales of $00 000, $500 000, $400 000, $300 000, and $100 000. a) points) Calculate the Herfindahl-Hirschman

Solution to Homework Set 7 Managerial Economics Fall 011 1. An industry consists of five firms with sales of $00 000, $500 000, $400 000, $300 000, and $100 000. a) points) Calculate the Herfindahl-Hirschman

Economics 431 Fall 2003 1st midterm Answer Key

Economics 431 Fall 003 1st midterm Answer Key 1) (7 points) Consider an industry that consists of a large number of identical firms. In the long run competitive equilibrium, a firm s marginal cost must

Economics 431 Fall 003 1st midterm Answer Key 1) (7 points) Consider an industry that consists of a large number of identical firms. In the long run competitive equilibrium, a firm s marginal cost must

AGGREGATE DEMAND AND AGGREGATE SUPPLY The Influence of Monetary and Fiscal Policy on Aggregate Demand

AGGREGATE DEMAND AND AGGREGATE SUPPLY The Influence of Monetary and Fiscal Policy on Aggregate Demand Suppose that the economy is undergoing a recession because of a fall in aggregate demand. a. Using

AGGREGATE DEMAND AND AGGREGATE SUPPLY The Influence of Monetary and Fiscal Policy on Aggregate Demand Suppose that the economy is undergoing a recession because of a fall in aggregate demand. a. Using

SECOND-DEGREE PRICE DISCRIMINATION

SECOND-DEGREE PRICE DISCRIMINATION FIRST Degree: The firm knows that it faces different individuals with different demand functions and furthermore the firm can tell who is who. In this case the firm extracts

SECOND-DEGREE PRICE DISCRIMINATION FIRST Degree: The firm knows that it faces different individuals with different demand functions and furthermore the firm can tell who is who. In this case the firm extracts

Problem Set 1 Solutions

Health Economics Economics 156 Prof. Jay Bhattacharya Problem Set 1 Solutions A. Risk Aversion Consider a risk averse consumer with probability p of becoming sick. Let I s be the consumer s income if he

Health Economics Economics 156 Prof. Jay Bhattacharya Problem Set 1 Solutions A. Risk Aversion Consider a risk averse consumer with probability p of becoming sick. Let I s be the consumer s income if he

N. Gregory Mankiw Principles of Economics. Chapter 15. MONOPOLY

N. Gregory Mankiw Principles of Economics Chapter 15. MONOPOLY Solutions to Problems and Applications 1. The following table shows revenue, costs, and profits, where quantities are in thousands, and total

N. Gregory Mankiw Principles of Economics Chapter 15. MONOPOLY Solutions to Problems and Applications 1. The following table shows revenue, costs, and profits, where quantities are in thousands, and total

1. The value today of a payment you will receive ten years from now is the of the payment.

CHAPTER 14 MARKETS FOR OTHER RESOURCES Microeconomics in Context (Goodwin, et al.), 2 nd Edition Chapter Summary Having learned about the market for labor, in this chapter you will look at the markets

CHAPTER 14 MARKETS FOR OTHER RESOURCES Microeconomics in Context (Goodwin, et al.), 2 nd Edition Chapter Summary Having learned about the market for labor, in this chapter you will look at the markets

Managerial Economics & Business Strategy Chapter 9. Basic Oligopoly Models

Managerial Economics & Business Strategy Chapter 9 Basic Oligopoly Models Overview I. Conditions for Oligopoly? II. Role of Strategic Interdependence III. Profit Maximization in Four Oligopoly Settings

Managerial Economics & Business Strategy Chapter 9 Basic Oligopoly Models Overview I. Conditions for Oligopoly? II. Role of Strategic Interdependence III. Profit Maximization in Four Oligopoly Settings

These are some practice questions for CHAPTER 23. Each question should have a single answer. But be careful. There may be errors in the answer key!

These are some practice questions for CHAPTER 23. Each question should have a single answer. But be careful. There may be errors in the answer key! 67. Public saving is equal to a. net tax revenues minus

These are some practice questions for CHAPTER 23. Each question should have a single answer. But be careful. There may be errors in the answer key! 67. Public saving is equal to a. net tax revenues minus

Lecture 5: Review Investment decisions and break even analysis

Lecture 5: Review Investment decisions and break even analysis 2 Summary Investments imply willingness to trade dollars in the present for dollars in the future. Wealth-creating transactions occur when

Lecture 5: Review Investment decisions and break even analysis 2 Summary Investments imply willingness to trade dollars in the present for dollars in the future. Wealth-creating transactions occur when

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Multiple choice review questions for Midterm 2 MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) A consumption point inside the budget line A) is

Multiple choice review questions for Midterm 2 MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) A consumption point inside the budget line A) is

Part A: Use the income identities to find what U.S. private business investment, I, was in 2004. Show your work.

Exercise 1 Due: Preliminary figures (in billions of dollars) for 2004 taken from the 2005 Economic Report of the President showed that: Y = 11,728.0, C = 8,231.1, EX = 1,170.2, IM = 1,779.6, G = 2,183.8

Exercise 1 Due: Preliminary figures (in billions of dollars) for 2004 taken from the 2005 Economic Report of the President showed that: Y = 11,728.0, C = 8,231.1, EX = 1,170.2, IM = 1,779.6, G = 2,183.8

Cosumnes River College Principles of Macroeconomics Problem Set 11 Will Not Be Collected

Name: Solutions Cosumnes River College Principles of Macroeconomics Problem Set 11 Will Not Be Collected Fall 2015 Prof. Dowell Instructions: This problem set will not be collected. You should still work

Name: Solutions Cosumnes River College Principles of Macroeconomics Problem Set 11 Will Not Be Collected Fall 2015 Prof. Dowell Instructions: This problem set will not be collected. You should still work

22 COMPETITIVE MARKETS IN THE LONG-RUN

22 COMPETITIVE MARKETS IN THE LONG-RUN Purpose: To illustrate price determination in the long-run in a competitive market. Computer file: lrmkt198.xls Instructions and background information: You are a

22 COMPETITIVE MARKETS IN THE LONG-RUN Purpose: To illustrate price determination in the long-run in a competitive market. Computer file: lrmkt198.xls Instructions and background information: You are a

Midterm exam, Health economics, Spring 2007 Answer key

Midterm exam, Health economics, Spring 2007 Answer key Instructions: All points on true/false and multiple choice questions will be given for the explanation. Note that you can choose which questions to

Midterm exam, Health economics, Spring 2007 Answer key Instructions: All points on true/false and multiple choice questions will be given for the explanation. Note that you can choose which questions to

Practice Questions Week 2 Day 1 Multiple Choice

Practice Questions Week 2 Day 1 Multiple Choice 1. When individuals come together to buy and sell goods and services, they form a(n) a. economy b. market c. production possibilities frontier d. supply

Practice Questions Week 2 Day 1 Multiple Choice 1. When individuals come together to buy and sell goods and services, they form a(n) a. economy b. market c. production possibilities frontier d. supply

Economics 380: International Economics Fall 2000 Exam #2 100 Points

Economics 380: International Economics Fall 2000 Exam #2 100 Points Name (ID) YOU SHOULD HAVE 7 PAGES FOR THIS EXAM. EXAM WILL END AT 1:50. MAKE SURE YOUR NAME IS ON THE FIRST AND LAST PAGE OF THE EXAM.

Economics 380: International Economics Fall 2000 Exam #2 100 Points Name (ID) YOU SHOULD HAVE 7 PAGES FOR THIS EXAM. EXAM WILL END AT 1:50. MAKE SURE YOUR NAME IS ON THE FIRST AND LAST PAGE OF THE EXAM.

Chapter 7. a. Plot Lauren Landlord's willingness to pay in Exhibit 1. Exhibit 1. Answer: See Exhibit 6. Exhibit 6

Chapter 7 1. The following information describes the value Lauren Landlord places on having her five houses repainted. She values the repainting of each house at a different amount depending on how badly

Chapter 7 1. The following information describes the value Lauren Landlord places on having her five houses repainted. She values the repainting of each house at a different amount depending on how badly

I. Introduction to Aggregate Demand/Aggregate Supply Model

University of California-Davis Economics 1B-Intro to Macro Handout 8 TA: Jason Lee Email: [email protected] I. Introduction to Aggregate Demand/Aggregate Supply Model In this chapter we develop a model

University of California-Davis Economics 1B-Intro to Macro Handout 8 TA: Jason Lee Email: [email protected] I. Introduction to Aggregate Demand/Aggregate Supply Model In this chapter we develop a model

Chapter 13 Oligopoly 1

Chapter 13 Oligopoly 1 4. Oligopoly A market structure with a small number of firms (usually big) Oligopolists know each other: Strategic interaction: actions of one firm will trigger re-actions of others

Chapter 13 Oligopoly 1 4. Oligopoly A market structure with a small number of firms (usually big) Oligopolists know each other: Strategic interaction: actions of one firm will trigger re-actions of others

Math 1314 Lesson 8 Business Applications: Break Even Analysis, Equilibrium Quantity/Price

Math 1314 Lesson 8 Business Applications: Break Even Analysis, Equilibrium Quantity/Price Three functions of importance in business are cost functions, revenue functions and profit functions. Cost functions

Math 1314 Lesson 8 Business Applications: Break Even Analysis, Equilibrium Quantity/Price Three functions of importance in business are cost functions, revenue functions and profit functions. Cost functions

a. What is the total revenue Joe can earn in a year? b. What are the explicit costs Joe incurs while producing ten boats?

Chapter 13 1. Joe runs a small boat factory. He can make ten boats per year and sell them for 25,000 each. It costs Joe 150,000 for the raw materials (fibreglass, wood, paint, and so on) to build the ten

Chapter 13 1. Joe runs a small boat factory. He can make ten boats per year and sell them for 25,000 each. It costs Joe 150,000 for the raw materials (fibreglass, wood, paint, and so on) to build the ten

Exercises Lecture 8: Trade policies

Exercises Lecture 8: Trade policies Exercise 1, from KOM 1. Home s demand and supply curves for wheat are: D = 100 0 S = 0 + 0 Derive and graph Home s import demand schedule. What would the price of wheat

Exercises Lecture 8: Trade policies Exercise 1, from KOM 1. Home s demand and supply curves for wheat are: D = 100 0 S = 0 + 0 Derive and graph Home s import demand schedule. What would the price of wheat

Week 4 Tutorial Question Solutions (Ch2 & 3)

") Chapter 2: Q1: Macroeconomics P.52 Numerical Problems #3 part (a) Q2: Macroeconomics P.52 Numerical Problems #5 Chapter 3: Q3: Macroeconomics P.101 Numerical Problems #5 Q4: Macroeconomics P102 Analytical

Chapter 2: Q1: Macroeconomics P.52 Numerical Problems #3 part (a) Q2: Macroeconomics P.52 Numerical Problems #5 Chapter 3: Q3: Macroeconomics P.101 Numerical Problems #5 Q4: Macroeconomics P102 Analytical

Aggressive Advertisement. Normal Advertisement Aggressive Advertisement. Normal Advertisement

Professor Scholz Posted: 11/10/2009 Economics 101, Problem Set #9, brief answers Due: 11/17/2009 Oligopoly and Monopolistic Competition Please SHOW your work and, if you have room, do the assignment on

Professor Scholz Posted: 11/10/2009 Economics 101, Problem Set #9, brief answers Due: 11/17/2009 Oligopoly and Monopolistic Competition Please SHOW your work and, if you have room, do the assignment on

Chapter 9 Basic Oligopoly Models

Managerial Economics & Business Strategy Chapter 9 Basic Oligopoly Models McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All rights reserved. Overview I. Conditions for Oligopoly?

Managerial Economics & Business Strategy Chapter 9 Basic Oligopoly Models McGraw-Hill/Irwin Copyright 2010 by the McGraw-Hill Companies, Inc. All rights reserved. Overview I. Conditions for Oligopoly?

b. Cost of Any Action is measure in foregone opportunities c.,marginal costs and benefits in decision making

1 Economics 130-Windward Community College Review Sheet for the Final Exam This final exam is comprehensive in nature and in scope. The test will be divided into two parts: a multiple-choice section and

1 Economics 130-Windward Community College Review Sheet for the Final Exam This final exam is comprehensive in nature and in scope. The test will be divided into two parts: a multiple-choice section and

Thus MR(Q) = P (Q) Q P (Q 1) (Q 1) < P (Q) Q P (Q) (Q 1) = P (Q), since P (Q 1) > P (Q).

= P (Q) Q P (Q 1) (Q 1) < P (Q) Q P (Q) (Q 1) = P (Q), since P (Q 1) > P (Q).") A monopolist s marginal revenue is always less than or equal to the price of the good. Marginal revenue is the amount of revenue the firm receives for each additional unit of output. It is the difference

A monopolist s marginal revenue is always less than or equal to the price of the good. Marginal revenue is the amount of revenue the firm receives for each additional unit of output. It is the difference

In the Herb Business, Part III Factoring and Quadratic Equations

74 In the Herb Business, Part III Factoring and Quadratic Equations In the herbal medicine business, you and your partner sold 120 bottles of your best herbal medicine each week when you sold at your original

74 In the Herb Business, Part III Factoring and Quadratic Equations In the herbal medicine business, you and your partner sold 120 bottles of your best herbal medicine each week when you sold at your original

Practiced Questions. Chapter 20

Practiced Questions Chapter 20 1. The model of aggregate demand and aggregate supply a. is different from the model of supply and demand for a particular market, in that we cannot focus on the substitution

Practiced Questions Chapter 20 1. The model of aggregate demand and aggregate supply a. is different from the model of supply and demand for a particular market, in that we cannot focus on the substitution

Econ Wizard User s Manual

1 Econ Wizard User s Manual Kevin Binns Matt Friedrichsen Purpose: This program is intended to be used by students enrolled in introductory economics classes. The program is meant to help these students

1 Econ Wizard User s Manual Kevin Binns Matt Friedrichsen Purpose: This program is intended to be used by students enrolled in introductory economics classes. The program is meant to help these students