April K Training CALL FHA. Servicing the American Homebuyer Since 1934

|

|

|

- Bruce Norman

- 7 years ago

- Views:

Transcription

1 April K Training 1

2 Presenters Thomas Baker Vaun Bateman Angela Escobedo Connie Schoenwald Linda Thompson 2

3 3

4 STREAMLINED (K) 4

5 Why 203(k)? Current owners stay in their homes and renovate Investors selling rentals that need repair Modifications for disabled individuals Ability to market properties that need updating Increasing a property s value One loan 5

6 STREAMLINED (k) Purchase or refinance transactions of properties needing minor repair or upgrading 6

7 STREAMLINED (k) Maximum loan amount is the lesser of: Purchase price (or as is value for refinances) plus rehabilitation costs, or 110% of after improved value Not to exceed maximum FHA loan limit for the area 7

8 STREAMLINED (k) Benefits Minor Repairs and Improvements (upgrades) Repair costs up to $35,000 (value permitting) No minimum repair cost threshold Repairs are completed after closing with loan proceeds Same down payment requirement for purchases (3.50%) No inspection required (If less than $15,000) 8

9 STREAMLINED (k) Benefits No 203 (k) Consultant No General Contractor Any FHA approved lender may originate a streamlined 203(k) mortgage 9

10 STREAMLINED (k) What can be included? Total cost of rehab Supplemental origination fee and discount points Contingency reserves (at lender s option) Inspection fees Building and other permits Title update costs 10

11 Eligible Work Items Repair/Replace/upgrade roofs, gutters and downspouts existing HVAC systems, plumbing, and electrical systems existing flooring Minor remodeling (non-structural) repairs Exterior and interior painting Weatherization STREAMLINED (k) Appliances (including free-standing ranges, refrigerators, washers/dryers, dishwashers and microwaves) Improvements for accessibility for persons with disabilities 11

12 STREAMLINED (k) Eligible Work Items Environmental mitigation Modifications involving disturbance of pre paint surfaces Lead based paint abatement Repair/Replace/add exterior decks, patios, porches Basement finishing and remodeling (not involving structural repairs) Basement water proofing Window and door replacements & exterior wall re-siding Septic system and/or well repair or replacement 12

13 STREAMLINED (k) Ineligible Work Items Major rehabilitation or remodeling ( such as the relocation of a load-bearing wall) New construction (including room additions) Repair of structural damage Repairs requiring detailed drawings or architectural exhibits Landscaping or similar site amenity improvements Any repair or improvements requiring more than 6 months to complete Rehabilitation activities that require more than two (2) payments per specialized contractor 13

14 STREAMLINED (k) Contractors and Rehabilitation Criteria Borrower must use licensed and bonded contractors Self-help is discouraged but acceptable IF the borrower can sufficiently demonstrate to the lender that he/she has the necessary expertise and experience to competently perform the work More information Mortgagee Letter

15 Eligible Properties HUD REO Properties New Properties Condominiums Refinance of existing Properties Free and Clear properties currently owned 1-4 units 15

16 Streamlined (k) Guidelines ML All repairs must comply with local codes All required permits must be obtained No minimum repair cost threshold Overall cost cannot exceed $35,000 16

17 Responsibilities Lender Examine bids(s) & work plan; review with Borrower and Contractor Ensure work meets program requirements and cost of repairs are reasonable/customary for area Assure all required permits obtained Complete HUD-92700, Maximum Mortgage Worksheet Determine if contingency reserve is needed; Determine if borrower meets requirements for self-help Contractor Must meet all jurisdictional licensing & bonding requirements Provide written cost estimate, provide licensing, bonding, reference information to lender. Only fixed prices acceptable (not time/material) Execute Homeowner/Contractor Agreement Obtain permits, if homeowner has not Maximum 2 draws per contractor 17

18 Responsibilities Homeowner Obtain necessary permits, if not obtained by the contractor Sign Homeowner/Contractor Agreement Select contractor (obtain cost estimates. submit to lender appraiser Must receive all cost estimates and list of work items Provide an after-improved value Perform final inspection to assure work completed as submitted 18

19 203K Streamline documents HUD B Conditional Commitment HUD 92900A Direct Endorsement Approval HUD LT FHA loan underwriting and transmittal summary HUD Maximum Mortgage Worksheet HUD 92700A Borrower s Acknowledgement Borrower s Identity of Interest Certification 19

20 203K Streamline documents Homeowner/Contractor Agreement Rehabilitation Self-Help Loan Agreement Rehabilitation Loan Agreement Rehabilitation Rider HUD Change Order Request (if needed) Mortgagor s Letter of Completion Contingency Release Letter Final Release Notice 20

21 203(k) vs. 203(k) Streamline 203(k) Repairs/Improvements Must be at least $5, (k) Streamline Facilitate Uncomplicated repairs/improvements Consultant Required No Consultant required Architectural Exhibits required Borrower can do repairs/ improvements if qualified No Architect required Borrower can do repairs/improvements if qualified Include up to $35,000 21

22 Major Rehabilitation and Repair 203(k) 22

23 Major Rehabilitation and Repair 203(k) Purpose of the 203(k) Loan: Primary Program for the rehabilitation and repair of single family housing Tool for community and neighborhood revitalization Expand Homeownership opportunities 23

24 Major Rehabilitation and Repair Program Details: Purchase or Refinance 203(k) Fixed or Adjustable Rate Mortgage Property must be 100% complete per Certificate of Occupancy or equivalent document, and must be over 1 year old Credit underwriting guidelines are the same as for any FHA loan A first mortgage that combines the purchase or refinance with renovation costs Loan is fully disbursed at closing 24

25 Major Rehabilitation and Repair Maximum Loan Amount: 203(k) Minimum $5,000 improvements Maximum loan amount is the lesser of: Maximum mortgage limit for area (base mortgage amount) Purchase price plus cost of rehabilitation 110% of After Improved value 25

26 Major Rehabilitation and Repair 203(k) How 203(k) Can Be Used : move a house onto existing foundation Refinance an existing loan Convert a 1-family dwelling to 2-4 units and vice versa Modernize or enlarge house Build a new house on an existing foundation Homes that have been demolished are eligible provided some of the existing foundation system remains in place 26

27 Major Rehabilitation and Repair Eligible Improvements : 203(k) eligible improvements include but are not limited to: Plumbing Floor treatments Electric Energy efficiency items Wells Storm Shelters Septic Heating/Cooling units Roofing Garage (attached or detached) Repairs to correct structural deficiencies A minimum of $5,000 of improvements which increase the marketability and value of the property Consultant write-up is required BEFORE the appraisal has been completed. 27

28 Major Rehabilitation and Repair Ineligible Improvements : 203(k) Luxury items that are not a permanent part of the real estate are not eligible as a cost of rehabilitation 28

29 Major Rehabilitation and Repair 203(k) Eligible Properties: 1-4 units Existing more than 1 year Condos Manufactured homes New construction on part of original foundation Existing house moved to new foundation Mixed use properties (% limitation of amount on commercial space) 29

30 203K documents HUD B Conditional Commitment HUD 92900A Direct Endorsement Approval HUD LT FHA loan underwriting and transmittal summary HUD Maximum Mortgage Worksheet HUD 92700A 203k Borrower s Acknowledgement HUD 9746-A Draw Request 203k Work Right-up (Completed by Consultant) checklist found in Appendix 1 of REV 2 30

31 203K documents Borrower s Identity of Interest Certification Homeowner/Contractor Agreement Rehabilitation Self-Help Loan Agreement Rehabilitation Loan Agreement Rehabilitation Rider HUD Change Order Request Mortgagor s Letter of Completion Contingency Release Letter Final Release Notice 31

32 Additional Programs available With the 203k product 32

, 203(k), Streamlined (k), etc Can be used on existing or newly constructed properties, on 1-4 unit properties & with any property type FHA - Serving Home Buyers")

33 Energy efficient mortgage Allows the financing of energy efficient features along with the purchase or refinance of the home Makes a home more comfortable, more affordable and more marketable Can be used with any FHA program 203(b), 203(k), Streamlined (k), etc Can be used on existing or newly constructed properties, on 1-4 unit properties & with any property type FHA - Serving Home Buyers 33

34 EEM continued EEM improvements (& weatherization items) can be added on top of the Streamlined (k) items Max FHA loan amount for area can be exceeded by the EEM amount Borrowers are qualified before the EEM amount is added to the final mortgage amount Cost of energy improvements & estimate of energy savings are determined by a HERS report Call FHA 34

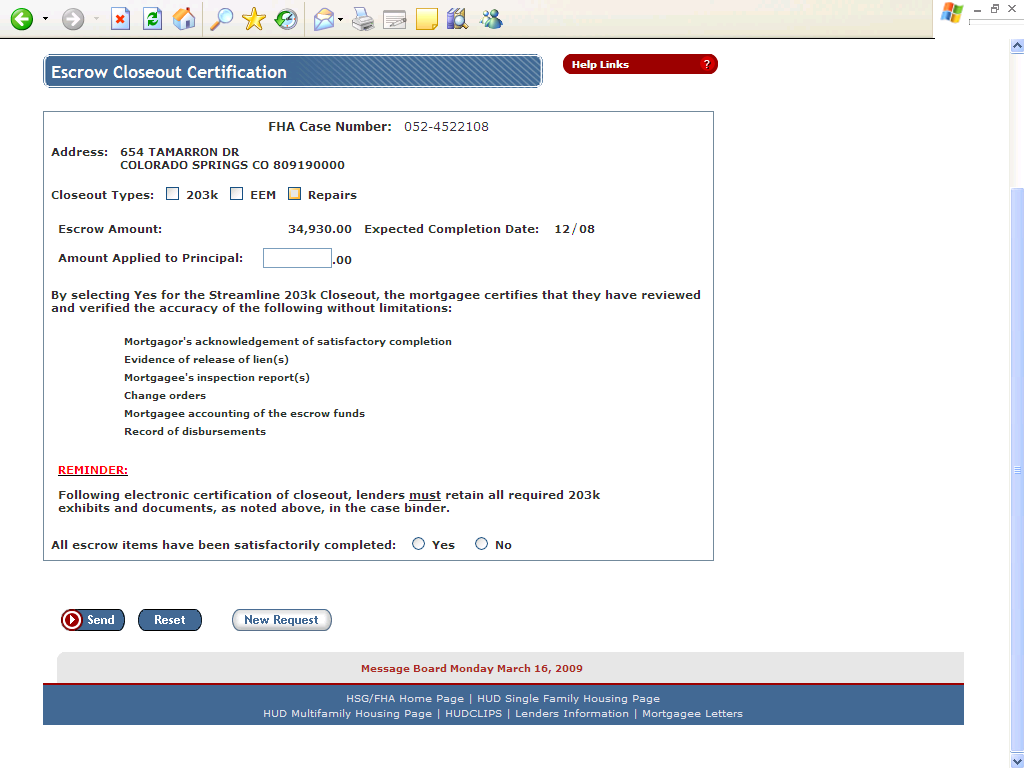

35 Real estate Owned Insurable with Escrow Uninsurable Sales Contract 35

36 REO Continued 36

37 Lead paint stabilization Clearance exam must be performed by state or epa certified lead-paint inspector, certified risk assessor or sampling examination If a HUD home, may receive a credit Credit not part of $35,000 streamlined (k) limit 37

38 case number assignment 38

39 CASE NUMBER ASSIGNMENT 39

40 CASE NUMBER ASSIGNMENT 40

41 Case number assignment 41

42 Case number assignment 42

43 Closeout requirements 43

44 Closeout requirements Proper close-out means the mortgagee has certified, reviewed and verified accuracy of the following: Mortgagor s acknowledgement of satisfactory completion Evidence of release of lien(s) inspection report(s) Change orders Mortgagee accounting of escrow funds and disbursements 44

45 Closeout requirements The mortgagee electronically certifies the closeout via FHA Connection Closeout documents are not required to be forwarded to FHA Documents must be retained by the mortgagee for 2 years following endorsement 45

46 46

47 HUD maximum mortgage worksheet 47

48 Streamlined (k) & 203(k) Worksheet Form HUD To be revised pdf Call FHA 48

49 HUD purchase Purchase price $150,000 After Improved Value $153,000 Closing costs and prepaids $ 3,500 Title up date fee $ 100 No Contingency reserve Proposed Improvements: Paint interior $ 1,500 Carpet $ 2,700 Linoleum $ 950 Trim $ 400 Total $ 5,550 49

50 HUD purchase 50

51 HUD purchase 51

52 Additional information 52

53 TO ACCESS INFORMATION FOR THE 203(k)and 203(ks) PROGRAM Visit the link referenced below: 53

54 54

55 resources ML : Streamlined (k) guidelines ML : EEM guidelines ML : For Non-Profit Purchasers Only ML : 203K Rehabilitation Mortgage program 55

56 RESOURCES ML Clarifications and modifications to 203(k) ML Revisions to 203(k) Rehab Mortgage Program ML Revisions to SF 203(k) Rehab Mortgage Program ML Expansion of the Energy Efficient Mortgage Program ML Using 203(k) Mortgage Ins. With Grant Programs ML Non-profit Agencies as Mortgagors ML Moratorium on Investor Loans in Conjunction with the 203(k) ML Revised Escrow commitment Procedure ML Combining EEM and 203 (k) ML Concerns about 203(k) Underwriting, Loan Processing ML Nonprofit Agency Participation in SF FHA Activities ML (k) Mortgage Program SF Loan Production ML Nonprofit Participation in FHA Single Family Activities New Requirements and Restrictions ML Enhancements to streamline K limited repair program 56

57 57

58 Frequently Asked Questions Can cost savings on the rehabilitation be given back to the borrower? Do I need 2 appraisals? Can Section 203(k) be used to improve a condominium unit? Can an investor use the 203(k) program? How do I find an FHA approved lender who participated in the 203(k) program 58

Enhancements to Streamlined (k) Limited Repair Program

Limited Repair Program") U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT WASHINGTON, DC 20410-8000 ASSISTANT SECRETARY FOR HOUSING- FEDERAL HOUSING COMMISSIONER December 29, 2005 MORTGAGEE LETTER 2005-50 TO: ALL APPROVED MORTGAGEES

U.S. DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT WASHINGTON, DC 20410-8000 ASSISTANT SECRETARY FOR HOUSING- FEDERAL HOUSING COMMISSIONER December 29, 2005 MORTGAGEE LETTER 2005-50 TO: ALL APPROVED MORTGAGEES

203K Loan Parameters

Full documentation only. 203K Loan Parameters AUS approval required, no manual underwriting permitted. Maximum DTI ratios of 31%/43% regardless of AUS findings. Both purchase or rate and term refinance

Full documentation only. 203K Loan Parameters AUS approval required, no manual underwriting permitted. Maximum DTI ratios of 31%/43% regardless of AUS findings. Both purchase or rate and term refinance

FHA 203k Inspections Changing climate in home buying markets: FHA 203k Inspections. FHA 203k Inspections. FHA 203k Inspections. FHA 203k Inspections

Changing climate in home buying markets: Mortgage qualifying still a challenge More people buying foreclosed/distressed properties Appraisals stricter Lower valuations of properties Increase in appraisal

Changing climate in home buying markets: Mortgage qualifying still a challenge More people buying foreclosed/distressed properties Appraisals stricter Lower valuations of properties Increase in appraisal

http://www.allregs.com/tpl/documentprint.aspx?did3=fbac4aa6751c4ea0b8e44256c659d9f...

Page 1 of 5 Lending Library / Correspondent Seller Guide / 500. Products / 508. HIP Full FHA 203(k) 508. HIP Full FHA 203(k) HIP Full FHA 203(k) Product Matrix/Guidelines The FHA 203(k) program (i.e. Full

Page 1 of 5 Lending Library / Correspondent Seller Guide / 500. Products / 508. HIP Full FHA 203(k) 508. HIP Full FHA 203(k) HIP Full FHA 203(k) Product Matrix/Guidelines The FHA 203(k) program (i.e. Full

FHA 203(k) Rehabilitation Mortgage Insurance Program

Rehabilitation Mortgage Insurance Program") FHA 203(k) Rehabilitation Mortgage Insurance Program This document is a reflection of current policy related to this topic. Its content is approved for use in FHA-related lender training. FHA 203(k) Rehabilitation

FHA 203(k) Rehabilitation Mortgage Insurance Program This document is a reflection of current policy related to this topic. Its content is approved for use in FHA-related lender training. FHA 203(k) Rehabilitation

FHA Streamline (K) Limited Repair Program

Limited Repair Program") Training Mortgage Professionals FHA Streamline (K) Limited Repair Program Facilitator: XXXXXXXXX The Streamline (K) Overview General Characteristics Eligible/Ineligible Improvements Documentation Requirements

Training Mortgage Professionals FHA Streamline (K) Limited Repair Program Facilitator: XXXXXXXXX The Streamline (K) Overview General Characteristics Eligible/Ineligible Improvements Documentation Requirements

FHA Streamline 203(k)

") Financing Provided by: Family Finance FHA Streamline 203(k) The Answer How many times have your customers said the following: 1. Needs carpet 2. Needs paint 3. Needs a new kitchen 4. Bathroom is ugly 5.

Financing Provided by: Family Finance FHA Streamline 203(k) The Answer How many times have your customers said the following: 1. Needs carpet 2. Needs paint 3. Needs a new kitchen 4. Bathroom is ugly 5.

PRMI 203K Streamline Loan. FHA Renovation Loan

PRMI 203K Streamline Loan FHA Renovation Loan Put the finishing touches on your borrowers Dream home. Purchase or Refinances Help you to sell more homes, and represent more buyers. Work with contractors

PRMI 203K Streamline Loan FHA Renovation Loan Put the finishing touches on your borrowers Dream home. Purchase or Refinances Help you to sell more homes, and represent more buyers. Work with contractors

Financing Options to support Energy Efficiency & Contractors

Financing Options to support Energy Efficiency & Contractors Renovation Loan Overview Renovation Loans offer a buyer the opportunity to buy a property and close as-is, financing both the purchase and repair

Financing Options to support Energy Efficiency & Contractors Renovation Loan Overview Renovation Loans offer a buyer the opportunity to buy a property and close as-is, financing both the purchase and repair

FHA Streamlined 203(k) Loan Program

Loan Program") FHA Streamlined 203(k) Loan Program 8/7/14 Overview FHA Streamlined 203(k) Program Through the Federal Housing Administration s (FHA) Streamlined 203(k) program, Borrowers can purchase or refinance their

FHA Streamlined 203(k) Loan Program 8/7/14 Overview FHA Streamlined 203(k) Program Through the Federal Housing Administration s (FHA) Streamlined 203(k) program, Borrowers can purchase or refinance their

All contents copyright 2009 2011 by 203KMortgageLender.com. All rights reserved. No part of this document or the related files may be republished to

All contents copyright 2009 2011 by 203KMortgageLender.com. All rights reserved. No part of this document or the related files may be republished to any website, blog, ebook etc. without prior wri en permission.

All contents copyright 2009 2011 by 203KMortgageLender.com. All rights reserved. No part of this document or the related files may be republished to any website, blog, ebook etc. without prior wri en permission.

SECTION 4 REHABILITATION MORTGAGES 203(k) Standard & 203(k) Limited

Standard & 203(k) Limited") SECTION 4 REHABILITATION MORTGAGES 203(k) Standard & 203(k) Limited 4.1 Program Descriptions 4.2 Borrower Eligibility 4.3 Property Eligibility 4.4 Principal Residence Requirement 4.5 Rehabilitation Loan

SECTION 4 REHABILITATION MORTGAGES 203(k) Standard & 203(k) Limited 4.1 Program Descriptions 4.2 Borrower Eligibility 4.3 Property Eligibility 4.4 Principal Residence Requirement 4.5 Rehabilitation Loan

SLIDE 1 OUT OF 42. THE BASICS: 203(k) FHA Standard 203(k) Andrew Allen COPYRIGHT 2013 AMERICAN FINANCIAL RESOURCES, INC. ALL RIGHTS RESERVED

FHA Standard 203(k) Andrew Allen COPYRIGHT 2013 AMERICAN FINANCIAL RESOURCES, INC. ALL RIGHTS RESERVED") SLIDE 1 OUT OF 42 R THE BASICS: 203(k) FHA Standard 203(k) Andrew Allen SLIDE 2 OUT OF 42 FHA 203K Questions 203k Explained What is the FHA 203(k) Loan Program? What are the program guidelines? What types

SLIDE 1 OUT OF 42 R THE BASICS: 203(k) FHA Standard 203(k) Andrew Allen SLIDE 2 OUT OF 42 FHA 203K Questions 203k Explained What is the FHA 203(k) Loan Program? What are the program guidelines? What types

Presents. FHA Streamlined(K) & 203(k) Training. July 20, 2011 7/18/2011. FHA Streamlined(k) Rehab Program

& 203(k) Training. July 20, 2011 7/18/2011. FHA Streamlined(k) Rehab Program") Presents FHA Streamlined(K) & 203(k) Training July 20, 2011 FHA Streamlined(k) Rehab Program Enables borrowers to finance both the purchase or refinance of a home and the cost of its rehabilitation through

Presents FHA Streamlined(K) & 203(k) Training July 20, 2011 FHA Streamlined(k) Rehab Program Enables borrowers to finance both the purchase or refinance of a home and the cost of its rehabilitation through

THE BASICS: 203(k) Limited. FHA Limited 203(k) ssss. Andrew Allen Updated 10/20/15

Limited. FHA Limited 203(k) ssss. Andrew Allen Updated 10/20/15") SLIDE 1 R THE BASICS: Limited 203(k) ssss FHA Limited 203(k) Andrew Allen Updated 10/20/15 SLIDE 2 FHA Limited 203(k) Questions Limited 203(k) Explained What is the FHA Limited 203(k)s Loan Program? What

SLIDE 1 R THE BASICS: Limited 203(k) ssss FHA Limited 203(k) Andrew Allen Updated 10/20/15 SLIDE 2 FHA Limited 203(k) Questions Limited 203(k) Explained What is the FHA Limited 203(k)s Loan Program? What

203K Streamline. Help qualified borrowers purchase or refinance AND renovate..with a single loan!

203K Streamline Help qualified borrowers purchase or refinance AND renovate..with a single loan! Why FHA 203K Streamline Offers a solution that helps borrowers obtain financing that covers both the acquisition

203K Streamline Help qualified borrowers purchase or refinance AND renovate..with a single loan! Why FHA 203K Streamline Offers a solution that helps borrowers obtain financing that covers both the acquisition

More than 35 Mortgage Loan Officers who live and work in your neighborhood. Lending in MA, NH, RI, ME, CT & FL

Founded in 1855 More than 35 Mortgage Loan Officers who live and work in your neighborhood. Lending in MA, NH, RI, ME, CT & FL Largest servicer of mortgage loans headquartered in New England. Finances

Founded in 1855 More than 35 Mortgage Loan Officers who live and work in your neighborhood. Lending in MA, NH, RI, ME, CT & FL Largest servicer of mortgage loans headquartered in New England. Finances

HUD REO M & M III. FHA Webinar on HUD REO 203-K Standard 203-K Streamline. HUD REO (Real Estate Owned) 203(k) Streamline.

203(k) Streamline.") FHA Webinar on HUD REO 203-K Standard 203-K Streamline HUD REO (Real Estate Owned) 203(k) Streamline 203-K Standard National Servicing Center (NSC) is responsible for direct oversight of the MCM contractor:

FHA Webinar on HUD REO 203-K Standard 203-K Streamline HUD REO (Real Estate Owned) 203(k) Streamline 203-K Standard National Servicing Center (NSC) is responsible for direct oversight of the MCM contractor:

NMLS ID: 110139 AmeriFirst Home Mortgage 800.466.5626

How do you turn a fixer upper into your dream home? The Solution the FHA 203(k) Loan! The purchase of a house that needs repair is often a catch-22 situation, because the bank won't lend the money to buy

How do you turn a fixer upper into your dream home? The Solution the FHA 203(k) Loan! The purchase of a house that needs repair is often a catch-22 situation, because the bank won't lend the money to buy

Purchase and rate/terms only. Streamline Standard (aka full consultant) Cash out to borrowers is not allowed

Cash out to borrowers is not allowed") February 2014 The FHA 203K program is HUD s primary program for the rehabilitation and repair of residential properties There are 2 different 203(k) programs offered: Streamline Standard (aka full consultant)

February 2014 The FHA 203K program is HUD s primary program for the rehabilitation and repair of residential properties There are 2 different 203(k) programs offered: Streamline Standard (aka full consultant)

Introduction to the Fannie Mae HomeStyle Renovation Mortgage. Presented by Damon Richardson, Program Specialist - American Financial Resources, Inc.

Introduction to the Fannie Mae HomeStyle Renovation Mortgage Presented by Damon Richardson, Program Specialist - American Financial Resources, Inc. About the Presenter With 12 years of mortgage industry

Introduction to the Fannie Mae HomeStyle Renovation Mortgage Presented by Damon Richardson, Program Specialist - American Financial Resources, Inc. About the Presenter With 12 years of mortgage industry

FHA 203(k) Information Package

Information Package") PO Box 2395 Birmingham, MI 48012-2395 Office: 248 644 8798 Fax: 248 644 8947 Email: PropInspEngineer@aol.com Web: http://www.propertyinspectionengineers.biz FHA 203(k) Information Package Program Overview:

PO Box 2395 Birmingham, MI 48012-2395 Office: 248 644 8798 Fax: 248 644 8947 Email: PropInspEngineer@aol.com Web: http://www.propertyinspectionengineers.biz FHA 203(k) Information Package Program Overview:

FHA Streamline 203(k) Guide. Effective as of April 2, 2015 Primary Capital Mortgage

Guide. Effective as of April 2, 2015 Primary Capital Mortgage") FHA Streamline 203(k) Guide Effective as of April 2, 2015 Primary Capital Mortgage Contents 1. Overview... 2 2. Documentation... 2 2.1 Allowable Age of Credit Documents... 2 2.2 Allowable Age of Federal

FHA Streamline 203(k) Guide Effective as of April 2, 2015 Primary Capital Mortgage Contents 1. Overview... 2 2. Documentation... 2 2.1 Allowable Age of Credit Documents... 2 2.2 Allowable Age of Federal

Understanding The Standard FHA 203(k) Standard Rehab Loan Program

Standard Rehab Loan Program") Understanding The Standard FHA 203(k) Standard Rehab Loan Program FHA s 203K Rehab Program The FHA 203(k) program is HUD s primary program for the rehabilitation and repair of residential properties This

Understanding The Standard FHA 203(k) Standard Rehab Loan Program FHA s 203K Rehab Program The FHA 203(k) program is HUD s primary program for the rehabilitation and repair of residential properties This

Renovating and Rebuilding America - One Home at a Time NMLS# 338923. Everything You Need To Know. 203K Manual

Renovating and Rebuilding America - One Home at a Time Everything You Need To Know 203K Manual Everything YOU Need to Know FHA 203K Manual You just found the deal of a lifetime! With improvements to this

Renovating and Rebuilding America - One Home at a Time Everything You Need To Know 203K Manual Everything YOU Need to Know FHA 203K Manual You just found the deal of a lifetime! With improvements to this

THE BASICS: Andrew Allen Updated 3/24/2015 COPYRIGHT 2013 AMERICAN FINANCIAL RESOURCES, INC. ALL RIGHTS RESERVED

R THE BASICS: Andrew Allen Updated 3/24/2015 The Formula for Success = AFR s Wholesale division is the #1 203(k) lender in the country for sponsored originations. HomeStyle Questions HomeStyle Explained

R THE BASICS: Andrew Allen Updated 3/24/2015 The Formula for Success = AFR s Wholesale division is the #1 203(k) lender in the country for sponsored originations. HomeStyle Questions HomeStyle Explained

Renovation. Your Guide Through the Process

Renovation Your Guide Through the Process Renovation Financing: An Investment in the Future TABLE OF CONTENTS An Investment in the Future.......... 1 An Opportunity for Everyone......... 2 Who can benefit

Renovation Your Guide Through the Process Renovation Financing: An Investment in the Future TABLE OF CONTENTS An Investment in the Future.......... 1 An Opportunity for Everyone......... 2 Who can benefit

HUD Real Estate Owned (REO) Loan Program Guide

Loan Program Guide") Table of Contents HUD Real Estate Owned (REO) Loan Program Guide Wholesale Lending January 9, 2014 Program Guide... 2 Pacific Union Financial Credit Philosophy... 2 Ability to Repay and Qualified Mortgages...

Table of Contents HUD Real Estate Owned (REO) Loan Program Guide Wholesale Lending January 9, 2014 Program Guide... 2 Pacific Union Financial Credit Philosophy... 2 Ability to Repay and Qualified Mortgages...

Home Purchase Rehabilitation Pilot Program Procedures Manual

Home Purchase Rehabilitation Pilot Program Procedures Manual Department of Housing and Community Development Home Purchase Assistance Program (HPAP) Residential and Community Services Division 1800 Martin

Home Purchase Rehabilitation Pilot Program Procedures Manual Department of Housing and Community Development Home Purchase Assistance Program (HPAP) Residential and Community Services Division 1800 Martin

Understanding the benefits and process of a Residential Renovation Loan for Realtors

Understanding the benefits and process of a Residential Renovation Loan for Realtors What is a Renovation loan and how does it work? Why do you need to know about Renovation loans? How will Renovation

Understanding the benefits and process of a Residential Renovation Loan for Realtors What is a Renovation loan and how does it work? Why do you need to know about Renovation loans? How will Renovation

FHA 203K ACQUISITION & REHABILITATION LOANS FOR HOMESTEADS & 1 4 APARTMENTS

FHA 203K ACQUISITION & REHABILITATION LOANS FOR HOMESTEADS & 1 4 APARTMENTS Rehab a Home w/hud's 203(k) The Federal Housing Administration (FHA), which is part of the Department of Housing and Urban Development

FHA 203K ACQUISITION & REHABILITATION LOANS FOR HOMESTEADS & 1 4 APARTMENTS Rehab a Home w/hud's 203(k) The Federal Housing Administration (FHA), which is part of the Department of Housing and Urban Development

HUD REPOS. SecurityNational Mortgage Company

HUD REPOS SecurityNational Mortgage Company Appraisal Requirements Appraisals are ordered by the M&M contractor from an FHA appraiser. Utilities should be on at the time the appraisal is conducted. If

HUD REPOS SecurityNational Mortgage Company Appraisal Requirements Appraisals are ordered by the M&M contractor from an FHA appraiser. Utilities should be on at the time the appraisal is conducted. If

The Ultimate. Improvement Loans

The Ultimate Guide to Home Improvement Loans Page 2 THE ULTIMATE GUIDE TO HOME IMPROVEMENT LOANS Section 1: What is a Renovation Mortgage? Page 4.What is a Renovation Mortgage? Section 2: Home Improvement

The Ultimate Guide to Home Improvement Loans Page 2 THE ULTIMATE GUIDE TO HOME IMPROVEMENT LOANS Section 1: What is a Renovation Mortgage? Page 4.What is a Renovation Mortgage? Section 2: Home Improvement

Renovation Financing 1

Renovation Financing 1 Renovation Financing The Win, Win, Win Scenario Presented By Lisa Marra The Marra Mortgage Group 2 What is a Renovation Loan? A renovation loan allows a borrower to secure financing

Renovation Financing 1 Renovation Financing The Win, Win, Win Scenario Presented By Lisa Marra The Marra Mortgage Group 2 What is a Renovation Loan? A renovation loan allows a borrower to secure financing

Renovation. Your Guide Through the Process

Renovation Your Guide Through the Process Renovation Financing: An Investment in the Future TABLE OF CONTENTS An Investment in the Future.......... 1 An Opportunity for Everyone......... 2 Who can benefit

Renovation Your Guide Through the Process Renovation Financing: An Investment in the Future TABLE OF CONTENTS An Investment in the Future.......... 1 An Opportunity for Everyone......... 2 Who can benefit

FHA 203K Rehab Remodel Repair

1 FHA 203K Rehab Remodel Repair What is an FHA 203K? FHA stands for Federal Housing Administration (FHA) and is part of the Department of Housing and Urban Development (HUD). FHA administers a number of

1 FHA 203K Rehab Remodel Repair What is an FHA 203K? FHA stands for Federal Housing Administration (FHA) and is part of the Department of Housing and Urban Development (HUD). FHA administers a number of

FHA 203k Rehab Loans. How to Use a 203k Rehab Loan to Move Your Listings and Put Buyers into Homes!

FHA 203k Rehab Loans How to Use a 203k Rehab Loan to Move Your Listings and Put Buyers into Homes! Today s s Agenda 203k Loan Overview How to Use the Program as a Tool to Market Your Properties How to

FHA 203k Rehab Loans How to Use a 203k Rehab Loan to Move Your Listings and Put Buyers into Homes! Today s s Agenda 203k Loan Overview How to Use the Program as a Tool to Market Your Properties How to

HOMESTYLE RENOVATION. Look at the possibilities

HOMESTYLE RENOVATION Look at the possibilities HOMESTREET: WHO ARE WE? Based in the Northwest, HomeStreet Bank if one of the largest community banks in the Northwest and Hawaii. HomeStreet began in 1921

HOMESTYLE RENOVATION Look at the possibilities HOMESTREET: WHO ARE WE? Based in the Northwest, HomeStreet Bank if one of the largest community banks in the Northwest and Hawaii. HomeStreet began in 1921

Welcome to the world of Renovation loans

Welcome to the world of Renovation loans What is a 203K loan? How can a 203K loan be used? Advantages of 203K loans The process of obtaining a 203K loan Why we are the experts A 203K is FHA s Rehabilitation

Welcome to the world of Renovation loans What is a 203K loan? How can a 203K loan be used? Advantages of 203K loans The process of obtaining a 203K loan Why we are the experts A 203K is FHA s Rehabilitation

FNMA HomeStyle Renovation

Product Types 10-30 year fixed Sales Focus HomeStyle enables homebuyers and homeowners to finance either the purchase or a refinance of a house and the cost of its rehabilitation through a single mortgage.

Product Types 10-30 year fixed Sales Focus HomeStyle enables homebuyers and homeowners to finance either the purchase or a refinance of a house and the cost of its rehabilitation through a single mortgage.

Understanding 203k Loans 2 Hour Continuing Education Course Outline

1. Course overview and requirements. a. Course length of 2 hours with a 10 minute break each hour on the hour. b. Making sure all attendees have a course outline. c. There will be a 10 question test at

1. Course overview and requirements. a. Course length of 2 hours with a 10 minute break each hour on the hour. b. Making sure all attendees have a course outline. c. There will be a 10 question test at

Disclosure Specialist Responsibilities. Lock Procedures. Processor Responsibilities. Appraisal Ordering

FHA 203K Streamline - Policies & Procedures FHA 203K Streamline will now be underwritten and funded in house. These applications should be originated in Mortgage Builder under the FHA203K-SR program code.

FHA 203K Streamline - Policies & Procedures FHA 203K Streamline will now be underwritten and funded in house. These applications should be originated in Mortgage Builder under the FHA203K-SR program code.

Renovate your home your way. The FHA 203(k) Renovation Loan

Renovation Loan") Renovate your home your way The FHA 203(k) Renovation Loan Agenda What is an FHA 203(k) Renovation Loan? Advantages of an FHA 203(k) Renovation Loan FHA 203(k) Renovation Loan: Standard vs. Streamline

Renovate your home your way The FHA 203(k) Renovation Loan Agenda What is an FHA 203(k) Renovation Loan? Advantages of an FHA 203(k) Renovation Loan FHA 203(k) Renovation Loan: Standard vs. Streamline

HUD Marketing Approaches Each HUD REO property will be offered for sale using one of the approaches listed below.

HUD REOs Overview Through the Property Disposition Insured Sales Program, HUD offers its Real Estate Owned (REO) properties for sale with FHA-insured financing available. Properties must meet the intent

HUD REOs Overview Through the Property Disposition Insured Sales Program, HUD offers its Real Estate Owned (REO) properties for sale with FHA-insured financing available. Properties must meet the intent

FHA: Standard and Jumbo/High Balance Eligibility Matrix

FHA: Standard and Jumbo/High Balance Loan Purpose FICO Maximum LTV 1 Maximum CLTV Maximum DTI 3 >620 100.00% 2 45%/55% Purchase Rate and Term Refinance Cash-out Refinance 4 580-619 31%/43% 500-579 90.00%

FHA: Standard and Jumbo/High Balance Loan Purpose FICO Maximum LTV 1 Maximum CLTV Maximum DTI 3 >620 100.00% 2 45%/55% Purchase Rate and Term Refinance Cash-out Refinance 4 580-619 31%/43% 500-579 90.00%

FHA 203(k) Streamline Training

Streamline Training") FHA 203(k) Streamline Training Guidelines Forms Point MyKey 12/11 FHA 203(k) Streamline Help qualified borrowers purchase and renovate a primary residence all with a single loan Allows Loan Officers to

FHA 203(k) Streamline Training Guidelines Forms Point MyKey 12/11 FHA 203(k) Streamline Help qualified borrowers purchase and renovate a primary residence all with a single loan Allows Loan Officers to

PRODUCT GUIDELINES FHA 203K STREAMLINE PROGRAM CODES: F30F203K, H30F203K

Maximum LTV 90.00%* 96.5%* 96.5%* LTV Maximum LTV Max Loan Amount.. REFINANCE OF RECENTLY ACQUIRED FREE & CLEAR PROPERTY* Max Loan Amount PURCHASE Max Ratios MINIMUM FICO 550 43% Regardless of AUS Maximum

Maximum LTV 90.00%* 96.5%* 96.5%* LTV Maximum LTV Max Loan Amount.. REFINANCE OF RECENTLY ACQUIRED FREE & CLEAR PROPERTY* Max Loan Amount PURCHASE Max Ratios MINIMUM FICO 550 43% Regardless of AUS Maximum

PRODUCT GUIDELINES FHA 203K LIMITED PROGRAM CODES: F30F203K, H30F203K

Maximum LTV 90.00%* 96.5%* 96.5%* Max Loan Amount...... PURCHASE Max Ratios MINIMUM FICO 550 43% MINIMUM FICO 580 Mortgage/Rental History 0 X 30 past 12 months *The maximum LTV on a Purchase transaction

Maximum LTV 90.00%* 96.5%* 96.5%* Max Loan Amount...... PURCHASE Max Ratios MINIMUM FICO 550 43% MINIMUM FICO 580 Mortgage/Rental History 0 X 30 past 12 months *The maximum LTV on a Purchase transaction

FHA Office of Single Family Housing. Energy Efficient Mortgage (EEM)

") Energy Efficient Mortgage (EEM) 1 Energy Efficient Mortgage (EEM) Program Allows the Mortgagee to offer financing for cost-effective, energy efficient improvements to an existing property at the time of

Energy Efficient Mortgage (EEM) 1 Energy Efficient Mortgage (EEM) Program Allows the Mortgagee to offer financing for cost-effective, energy efficient improvements to an existing property at the time of

renovation loans for REALTORS LEARN HOW renovation loans CAN BUILD YOUR BUSINESS STEP BY STEP INSTRUCTIONS COMPARISON OF PRODUCTS SIDE BY SIDE

renovation loans for REALTORS LEARN HOW renovation loans CAN BUILD YOUR BUSINESS COMPARISON OF PRODUCTS SIDE BY SIDE STEP BY STEP INSTRUCTIONS table of CONTENTS 3 4 5 6 7 8 9 10 11 12-13 14 15-16 17 Introduction

renovation loans for REALTORS LEARN HOW renovation loans CAN BUILD YOUR BUSINESS COMPARISON OF PRODUCTS SIDE BY SIDE STEP BY STEP INSTRUCTIONS table of CONTENTS 3 4 5 6 7 8 9 10 11 12-13 14 15-16 17 Introduction

A Guide To An FHA 203(k) Loan

Loan") A Guide To An FHA 203(k) Loan US Mortgage Corporation (NMLS ID#3901). Corporate Office is located at 201 Old Country Road, Suite 140, Melville, NY 11747; 631-580-2600 or (800) 562-6715 (LOANS15). Licensed

A Guide To An FHA 203(k) Loan US Mortgage Corporation (NMLS ID#3901). Corporate Office is located at 201 Old Country Road, Suite 140, Melville, NY 11747; 631-580-2600 or (800) 562-6715 (LOANS15). Licensed

CITY OF MOBILE COMMUNITY PLANNING & DEVELOPMENT DEPARTMENT

CITY OF MOBILE COMMUNITY PLANNING & DEVELOPMENT DEPARTMENT HOMEOWNER REHAB LOAN PROGRAM FOR ELIGIBLE RESIDENTS CITY WIDE Are You Having Problems with Your Plumbing? Do You Need a New Roof? Are Your Windows

CITY OF MOBILE COMMUNITY PLANNING & DEVELOPMENT DEPARTMENT HOMEOWNER REHAB LOAN PROGRAM FOR ELIGIBLE RESIDENTS CITY WIDE Are You Having Problems with Your Plumbing? Do You Need a New Roof? Are Your Windows

FHA Purchase and Refinance Loans

FHA Purchase & Refinance Loans Also known as a "government loan," an FHA loan is guaranteed by the Federal Housing Administration (FHA). The FHA provides mortgage insurance on loans made by FHA-approved

FHA Purchase & Refinance Loans Also known as a "government loan," an FHA loan is guaranteed by the Federal Housing Administration (FHA). The FHA provides mortgage insurance on loans made by FHA-approved

Underwriting Memo 1.2013

06/13/13 Underwriting Memo 1.2013 Attention: SNMC Underwriters Branch Managers and Quality Control Subject: FHA 203K Streamlines SNMC will no longer underwrite FHA 203K Streamlines in-house or offer the

06/13/13 Underwriting Memo 1.2013 Attention: SNMC Underwriters Branch Managers and Quality Control Subject: FHA 203K Streamlines SNMC will no longer underwrite FHA 203K Streamlines in-house or offer the

FHA 203(k) Rehabilitation Loans

Rehabilitation Loans") Everything You Need to Know About FHA 203(k) Rehabilitation Loans Presented April 10, 2009 Senior Loan Officer, FHA Consultant Bill@YourFhaGuru.com http://www.yourfhaguru.com FHA/VA Since 1970 CLASS TOPICS

Everything You Need to Know About FHA 203(k) Rehabilitation Loans Presented April 10, 2009 Senior Loan Officer, FHA Consultant Bill@YourFhaGuru.com http://www.yourfhaguru.com FHA/VA Since 1970 CLASS TOPICS

PROGRAM DESCRIPTION HOMEOWNER REHABILITATION LOAN FOR INCOME ELIGIBLE CITY OF MOBILE HOMEOWNERS

CITY OF MOBILE COMMUNITY PLANNING & DEVELOPMENT CITYWIDE III HOMEOWNER REHAB PROGRAM HOMEOWNER REHABILITATION LOAN PROGRAM DESCRIPTION FOR INCOME ELIGIBLE CITY OF MOBILE HOMEOWNERS Our Home Rehab Program

CITY OF MOBILE COMMUNITY PLANNING & DEVELOPMENT CITYWIDE III HOMEOWNER REHAB PROGRAM HOMEOWNER REHABILITATION LOAN PROGRAM DESCRIPTION FOR INCOME ELIGIBLE CITY OF MOBILE HOMEOWNERS Our Home Rehab Program

Full A Service. Construction Company. Quality. Bradley Construction. is non-negotiable.

Full A Service Construction Company Quality When is non-negotiable. Bradley Construction Location and Contact Information Office Address: Bradley Construction LLC 112 Clair Drive Piedmont, SC 29673 Mailing

Full A Service Construction Company Quality When is non-negotiable. Bradley Construction Location and Contact Information Office Address: Bradley Construction LLC 112 Clair Drive Piedmont, SC 29673 Mailing

Fannie Mae HomeStyle: LifeStyle Home Improvement Loan 8/29/14

Fannie Mae HomeStyle: LifeStyle Home Improvement Loan 8/29/14 What is a Fannie Mae LifeStyle Home Improvement Loan? Offers a solution to help Borrowers obtain financing that covers both the acquisition

Fannie Mae HomeStyle: LifeStyle Home Improvement Loan 8/29/14 What is a Fannie Mae LifeStyle Home Improvement Loan? Offers a solution to help Borrowers obtain financing that covers both the acquisition

Buy a home, plus make improvements, with just one loan

Homebuyer guide to a mortgage with built-in renovation financing Buy a home, plus make improvements, with just one loan Learn how Are you thinking of buying a home that needs work? Well Fargo is here to

Homebuyer guide to a mortgage with built-in renovation financing Buy a home, plus make improvements, with just one loan Learn how Are you thinking of buying a home that needs work? Well Fargo is here to

APMC CORRESPONDENT LENDING FREQUENTLY ASKED QUESTIONS

FHA 203(k) and Streamlined 203(k) Loan Programs 1. If the loan is approved by Desktop Underwriter (DU ) or Loan Prospector (LP), can it exceed guidelines? Except for the minimum credit score requirement,

FHA 203(k) and Streamlined 203(k) Loan Programs 1. If the loan is approved by Desktop Underwriter (DU ) or Loan Prospector (LP), can it exceed guidelines? Except for the minimum credit score requirement,

THE BASICS: FHA STANDARD 203(k) COPYRIGHT 2015 AMERICAN FINANCIAL RESOURCES, INC. ALL RIGHTS RESERVED

COPYRIGHT 2015 AMERICAN FINANCIAL RESOURCES, INC. ALL RIGHTS RESERVED") THE BASICS: FHA STANDARD 203(k) Last Revised 12/8/2015 DISCLAIMER These materials are intended for informational use only. This is neither legal advice nor a substitute for Agency Guidelines. Please do

THE BASICS: FHA STANDARD 203(k) Last Revised 12/8/2015 DISCLAIMER These materials are intended for informational use only. This is neither legal advice nor a substitute for Agency Guidelines. Please do

Dream It. FInance It. BuIlD It.

Dream It. FInance It. BuIlD It. Construction loans designed to your specifications You ve got You ve US! got US! Banking Loans Investments Tax & Payroll Insurance CONSTRUCTION/PERMANENT MORTGAGE PROGRAM

Dream It. FInance It. BuIlD It. Construction loans designed to your specifications You ve got You ve US! got US! Banking Loans Investments Tax & Payroll Insurance CONSTRUCTION/PERMANENT MORTGAGE PROGRAM

CONDOMINIUM PROCESSING Q&A s

CONDOMINIUM PROCESSING Q&A s 1 P age FAQ s-ml 2009-46B Condominium Processing Contents Page/s General Processing for DELRAP & HRAP. 3-6 DELRAP Processing. 6-8 HRAP Processing.. 8 Project Recertification.

CONDOMINIUM PROCESSING Q&A s 1 P age FAQ s-ml 2009-46B Condominium Processing Contents Page/s General Processing for DELRAP & HRAP. 3-6 DELRAP Processing. 6-8 HRAP Processing.. 8 Project Recertification.

203K CONTRACTOR DOC REQUIREMENTS

203K CONTRACTOR DOC REQUIREMENTS CONTRACTOR REQUIREMENTS: Contractor's Resume/Contractor Profile Report Copy of Contractor Liability Insurance Evidence of Contractor License & Contractor Bonding(if required

203K CONTRACTOR DOC REQUIREMENTS CONTRACTOR REQUIREMENTS: Contractor's Resume/Contractor Profile Report Copy of Contractor Liability Insurance Evidence of Contractor License & Contractor Bonding(if required

MINNESOTA HOUSING Mortgage Revenue Bond Program

MINNESOTA HOUSING Mortgage Revenue Bond Program Lou Caresani Sheryl Krocek 2009 Disclaimer This presentation is for basic informational purposes only. It does not modify or replace the information provided

MINNESOTA HOUSING Mortgage Revenue Bond Program Lou Caresani Sheryl Krocek 2009 Disclaimer This presentation is for basic informational purposes only. It does not modify or replace the information provided

April 2010. FHA FAQs/HOT TOPICS. www.hud.gov 1-800-CALL FHA. Servicing the American Homebuyer Since 1934

April 2010 FHA FAQs/HOT TOPICS 1 Presenters CONNIE SCHOENWALD LAURA ARUNDEL LINDA THOMPSON PAVLINA KUSNIERZ 2 AGENDA Occupancy Income/employment Credit Miscellaneous Property FHA Connection Refinances

April 2010 FHA FAQs/HOT TOPICS 1 Presenters CONNIE SCHOENWALD LAURA ARUNDEL LINDA THOMPSON PAVLINA KUSNIERZ 2 AGENDA Occupancy Income/employment Credit Miscellaneous Property FHA Connection Refinances

FHA REPAIR ESCROW GUIDELINES

FHA REPAIR ESCROW GUIDELINES Introduction Escrow holdbacks are used to facilitate loan closings for properties that require no more than $5000 of repairs to meet FHA s minimum property requirements. The

FHA REPAIR ESCROW GUIDELINES Introduction Escrow holdbacks are used to facilitate loan closings for properties that require no more than $5000 of repairs to meet FHA s minimum property requirements. The

Introduction to Renovation Lending. Presented by: Jane King Freedom Mortgage

Introduction to Renovation Lending Presented by: Jane King Freedom Mortgage Agenda Renovation Lending Overview of renovation products Identifying the right borrower Identifying the right property Evaluating

Introduction to Renovation Lending Presented by: Jane King Freedom Mortgage Agenda Renovation Lending Overview of renovation products Identifying the right borrower Identifying the right property Evaluating

Vacant Properties Rehabilitation Program

City of Columbus Department of Development Housing Division Vacant Properties Rehabilitation Program Redevelopment for Homeownership/ Lease-Purchase Guidelines Old Oaks City of Columbus Department of Development

City of Columbus Department of Development Housing Division Vacant Properties Rehabilitation Program Redevelopment for Homeownership/ Lease-Purchase Guidelines Old Oaks City of Columbus Department of Development

Construction Conversion and Renovation Mortgages

Conversion and Renovation Mortgages Use this summary of requirements to help you process, underwrite and deliver Conversion and Renovation Mortgages. For complete information on Conversion and Renovation

Conversion and Renovation Mortgages Use this summary of requirements to help you process, underwrite and deliver Conversion and Renovation Mortgages. For complete information on Conversion and Renovation

U.S. Department of Housing and Urban Development H O U S I N G

U.S. Department of Housing and Urban Development H O U S I N G Special Attention of: Transmittal Handbook No.: DIRECTORS, HOUSING DEVELOPMENT DIVISION AND HOUSING MANAGEMENT DIVISION; FIELD OFFICE MANAGERS

U.S. Department of Housing and Urban Development H O U S I N G Special Attention of: Transmittal Handbook No.: DIRECTORS, HOUSING DEVELOPMENT DIVISION AND HOUSING MANAGEMENT DIVISION; FIELD OFFICE MANAGERS

Energy Efficient Mortgages & HERS Ratings. Peter V. Vargo Nu-Tech Energy Solutions, Co LLC

Energy Efficient Mortgages & HERS Ratings Peter V. Vargo Nu-Tech Energy Solutions, Co LLC PA Housing & Land Development Conference February 20, 2013 Energy Efficient Mortgages & HERS Ratings Peter V. Vargo

Energy Efficient Mortgages & HERS Ratings Peter V. Vargo Nu-Tech Energy Solutions, Co LLC PA Housing & Land Development Conference February 20, 2013 Energy Efficient Mortgages & HERS Ratings Peter V. Vargo

Review of FHA s Policies

Review of FHA s Policies January 16, 2014 Presented by Arlene Nunes 1 Agenda HUD s Qualified Mortgage Rule 2014 FHA Loan Limits (ML 2013 43) Manual Underwriting Final Notice Single Family Housing Policy

Review of FHA s Policies January 16, 2014 Presented by Arlene Nunes 1 Agenda HUD s Qualified Mortgage Rule 2014 FHA Loan Limits (ML 2013 43) Manual Underwriting Final Notice Single Family Housing Policy

PURCHASE/REHABILITATION PROGRAM PROGRAM OUTLINE

PURCHASE/REHABILITATION PROGRAM PROGRAM OUTLINE PROGRAM STRUCTURE The improvement/rehabilitation portion of the first mortgage loan will be limited to a minimum of $2,000 and not to exceed a maximum of

PURCHASE/REHABILITATION PROGRAM PROGRAM OUTLINE PROGRAM STRUCTURE The improvement/rehabilitation portion of the first mortgage loan will be limited to a minimum of $2,000 and not to exceed a maximum of

HUD Mortgage Insurance Program Section 232 LEAN

HUD Mortgage Insurance Program Section 232 LEAN Skilled Nursing, Intermediate Care, Assisted Living, Board & Care Benefits: The LEAN program offers more efficient processing through a centralized application,

HUD Mortgage Insurance Program Section 232 LEAN Skilled Nursing, Intermediate Care, Assisted Living, Board & Care Benefits: The LEAN program offers more efficient processing through a centralized application,

Homeownership Division

Michigan Credit Union League & Affiliates Annual Convention and Exposition Helping Credit Unions Serve, Grow and Remain Strong #mculace MSHDA s Homeownership Programs Delivering the Dream to Michigan Families

Michigan Credit Union League & Affiliates Annual Convention and Exposition Helping Credit Unions Serve, Grow and Remain Strong #mculace MSHDA s Homeownership Programs Delivering the Dream to Michigan Families

Frequently Asked Questions Valuation Protocol Overview

Frequently Asked Questions Valuation Protocol Overview Contents This publication contains the following topics: Topic New Construction Wood Destroying Insects/Termites Utilities Well and Septic Inspections

Frequently Asked Questions Valuation Protocol Overview Contents This publication contains the following topics: Topic New Construction Wood Destroying Insects/Termites Utilities Well and Septic Inspections

Vacant Properties Rehabilitation Program

City of Columbus Department of Development Housing Division Vacant Properties Rehabilitation Program Redevelopment for Homeownership/ Lease-Purchase Guidelines Capital Bond Funds Home Funds NSP 1, 2, 3

City of Columbus Department of Development Housing Division Vacant Properties Rehabilitation Program Redevelopment for Homeownership/ Lease-Purchase Guidelines Capital Bond Funds Home Funds NSP 1, 2, 3

HOUSING ASSISTANCE REHABILITATION PROGRAM (HARP)

") HOUSING ASSISTANCE REHABILITATION PROGRAM (HARP) PURPOSE The Housing Assistance Rehabilitation Program (HARP) provides loans and assistance for the rehabilitation and reconstruction of substandard and

HOUSING ASSISTANCE REHABILITATION PROGRAM (HARP) PURPOSE The Housing Assistance Rehabilitation Program (HARP) provides loans and assistance for the rehabilitation and reconstruction of substandard and

MUNICIPAL HOUSING REHABILITATION PROGRAM HANDBOOK

MUNICIPAL HOUSING REHABILITATION PROGRAM HANDBOOK For further information or inquiries please write or call your municipality s Small Cities Consultants: Lisa Low & Associates 293 Riggs Street Oxford,

MUNICIPAL HOUSING REHABILITATION PROGRAM HANDBOOK For further information or inquiries please write or call your municipality s Small Cities Consultants: Lisa Low & Associates 293 Riggs Street Oxford,

COEUR D ALENE TRIBAL HOUSING AUTHORITY HOUSING REHABILITATION POLICY (CDTHA REHAB)

") COEUR D ALENE TRIBAL HOUSING AUTHORITY HOUSING REHABILITATION POLICY (CDTHA REHAB) Adopted by the Housing Board May 25, 2005 CDTHA HOUSING REHAB POLICY Programs Available... 3 Reconstruction... 3 Relocation/Displacement...

COEUR D ALENE TRIBAL HOUSING AUTHORITY HOUSING REHABILITATION POLICY (CDTHA REHAB) Adopted by the Housing Board May 25, 2005 CDTHA HOUSING REHAB POLICY Programs Available... 3 Reconstruction... 3 Relocation/Displacement...

10.08 New ConstructionError! Bookmark not defined.

10.08 New Error! Bookmark not defined. Definition Exhibits and Inspections To be eligible for appraisal as new construction, the property must be fully completed or completed except for customer preference

10.08 New Error! Bookmark not defined. Definition Exhibits and Inspections To be eligible for appraisal as new construction, the property must be fully completed or completed except for customer preference

FHA 203K MATRIX. Second Appraisal Requirements

FHA 203K MATRIX Self Help Allowed NO NO ELIGIBLE PROPERTIES 1-4 Family including HUD REOs 1-4 FAMILY INCLUDING HUD REOs ALLOWS RELATIVES/EMPLOYERS TO COMPLETE WORK NO NO MIXED USE ACCEPTABLE ONLY UNDER

FHA 203K MATRIX Self Help Allowed NO NO ELIGIBLE PROPERTIES 1-4 Family including HUD REOs 1-4 FAMILY INCLUDING HUD REOs ALLOWS RELATIVES/EMPLOYERS TO COMPLETE WORK NO NO MIXED USE ACCEPTABLE ONLY UNDER

506 Loan Terms The Loan amount is $14,000.00 and will be a second mortgage lien closed with a DCA-approved Lender s first mortgage.

Chapter 5 Georgia Dream NSP Purchase Program 501 Georgia Dream NSP Purchase Program The Georgia Dream NSP Purchase Program is funded with proceeds from an allocation of federal funds from the Housing and

Chapter 5 Georgia Dream NSP Purchase Program 501 Georgia Dream NSP Purchase Program The Georgia Dream NSP Purchase Program is funded with proceeds from an allocation of federal funds from the Housing and

203kLender.com. The 10 Step Quick Start Guide. What s Included: Types of 203k Loans. 10 Quick Steps To Get You Started

203kLender.com The 10 Step Quick Start Guide What s Included: & Types of 203k Loans 10 Quick Steps To Get You Started The FHA 203K Loan 10 Step Quick Start Guide If there was a way to create your dream

203kLender.com The 10 Step Quick Start Guide What s Included: & Types of 203k Loans 10 Quick Steps To Get You Started The FHA 203K Loan 10 Step Quick Start Guide If there was a way to create your dream

The Rehab Inspector and LBP

The Rehab Inspector and LBP 2013 Housing Conference OCD/OCCD Sawmill Creek Resort and Conference Center November 20-22, 2013 GH Runevitch- Presenter The Rehab Inspector and LBP The Rehab Specialist has

The Rehab Inspector and LBP 2013 Housing Conference OCD/OCCD Sawmill Creek Resort and Conference Center November 20-22, 2013 GH Runevitch- Presenter The Rehab Inspector and LBP The Rehab Specialist has

Quick Reference Program Summary. The following is an outline of the underwriting and closing requirements of New Hampshire Housing.

Quick Reference Program Summary The following is an outline of the underwriting and closing requirements of New Hampshire Housing. Specific Program Rules are attached to this reference. A reservation cannot

Quick Reference Program Summary The following is an outline of the underwriting and closing requirements of New Hampshire Housing. Specific Program Rules are attached to this reference. A reservation cannot

Village of Oak Park Community Services Department Single-Family Rehabilitation Loan Program Oak Park, Illinois POLICY GUIDELINES

Village of Oak Park Community Services Department Single-Family Rehabilitation Loan Program Oak Park, Illinois POLICY GUIDELINES A. ELIGIBLE PROPERTY OWNERS 1. Benefit to Very Low- and Low- Income Owner-Occupants.

Village of Oak Park Community Services Department Single-Family Rehabilitation Loan Program Oak Park, Illinois POLICY GUIDELINES A. ELIGIBLE PROPERTY OWNERS 1. Benefit to Very Low- and Low- Income Owner-Occupants.

NON CREDIT QUALIFYING WITHOUT APPRAISAL, STANDARD & HIGH BALANCE, FIXED & ARM

NON CREDIT QUALIFYING WITHOUT APPRAISAL, STANDARD & HIGH BALANCE, FIXED & ARM Occupancy Maximum LTV/CLTV # of Units MAX Base Loan* High MIN Base* Min FICO Max Ratios Mortgage History** Primary 125% Non

NON CREDIT QUALIFYING WITHOUT APPRAISAL, STANDARD & HIGH BALANCE, FIXED & ARM Occupancy Maximum LTV/CLTV # of Units MAX Base Loan* High MIN Base* Min FICO Max Ratios Mortgage History** Primary 125% Non

A Little TLC Goes. A Long Way! FHA 203k. Home Loan. Compliments of Certified Mortgage Advisor. Kevin Walton

! FHA 203k Compliments of Certified Mortgage Advisor Kevin Walton Buying a fixer-upper? Buying an as-is condition property? Having problems obtaining lender approval due to an undesirable property? Purchase

! FHA 203k Compliments of Certified Mortgage Advisor Kevin Walton Buying a fixer-upper? Buying an as-is condition property? Having problems obtaining lender approval due to an undesirable property? Purchase

Construction-to-Perm FHA One Time Close. Construction Financing for Today's Market

Construction-to-Perm FHA One Time Close Construction Financing for Today's Market AGENDA Overview Construction-to-Perm Guidelines Eligibility Requirements Documentation Requirements (Closing and Endorsement)

Construction-to-Perm FHA One Time Close Construction Financing for Today's Market AGENDA Overview Construction-to-Perm Guidelines Eligibility Requirements Documentation Requirements (Closing and Endorsement)

The 10 Step Quick Start Guide

Renovating and Rebuilding America - One Home at a Time & The 10 Step Quick Start Guide What s Included: Types of 203K Loans 10 Quick Steps To Get You Started The FHA 203K Loan 10 Step Quick Start Guide

Renovating and Rebuilding America - One Home at a Time & The 10 Step Quick Start Guide What s Included: Types of 203K Loans 10 Quick Steps To Get You Started The FHA 203K Loan 10 Step Quick Start Guide

Lending Guide Investor Rehab Loan Program

Program Description The Rehab loan program is an asset-based financing option designed for borrowers who wish to acquire, rehabilitate, and sell residential real estate. This program is well suited for

Program Description The Rehab loan program is an asset-based financing option designed for borrowers who wish to acquire, rehabilitate, and sell residential real estate. This program is well suited for

SPECIAL REPORT: How to Use the 203K Loan Program to Profit From the Foreclosure Crisis

SPECIAL REPORT: How to Use the 203K Loan Program to Profit From the Foreclosure Crisis Presented By: RGR Construction, Ltd. 1-877-289-7231 Welcome, and thank you for ordering this report from RGR Construction

SPECIAL REPORT: How to Use the 203K Loan Program to Profit From the Foreclosure Crisis Presented By: RGR Construction, Ltd. 1-877-289-7231 Welcome, and thank you for ordering this report from RGR Construction

EFFECTIVE FOR FHA CASE NUMBER ASSIGNMENTS ON AND AFTER SEPTEMBER 14, 2015 OVERLAY MATRIX: GOVERNMENT

Appraisals Attached PUDs Automated Findings Condominiums Credit History VA: Form 2055 Appraisal dated prior to the Note Date required on IRRRLs if current VA loan is not serviced by BB&T. FHA: Property

Appraisals Attached PUDs Automated Findings Condominiums Credit History VA: Form 2055 Appraisal dated prior to the Note Date required on IRRRLs if current VA loan is not serviced by BB&T. FHA: Property

CITY OF BAY VILLAGE DEPARTMENT OF COMMUNITY SERVICES DOWN PAYMENT ASSISTANCE PROGRAMS

CITY OF BAY VILLAGE DEPARTMENT OF COMMUNITY SERVICES DOWN PAYMENT ASSISTANCE PROGRAMS Cuyahoga County Loan and Grant Programs for Residents For application forms or more information on the programs below,

CITY OF BAY VILLAGE DEPARTMENT OF COMMUNITY SERVICES DOWN PAYMENT ASSISTANCE PROGRAMS Cuyahoga County Loan and Grant Programs for Residents For application forms or more information on the programs below,

Important Information for Owners of Buildings in Flood Zones

Important Information for Owners of Buildings in Flood Zones Rebuilding your home after the storm? Adding on, renovating, or remodeling your home? Here is information YOU need to know about the 50 percent

Important Information for Owners of Buildings in Flood Zones Rebuilding your home after the storm? Adding on, renovating, or remodeling your home? Here is information YOU need to know about the 50 percent

MARS DISCLOSURE FOR CONSUMER SPECIFIC COMMERCIAL COMMUNICATION

MARS DISCLOSURE FOR CONSUMER SPECIFIC COMMERCIAL COMMUNICATION The disclosure below is required by 16 C.F.R. 322.4(b) in every consumer-specific commercial communication for any mortgage assistance relief

MARS DISCLOSURE FOR CONSUMER SPECIFIC COMMERCIAL COMMUNICATION The disclosure below is required by 16 C.F.R. 322.4(b) in every consumer-specific commercial communication for any mortgage assistance relief

Affordable, fixed rate mortgages

First Home Program Affordable, fixed rate mortgages Dear Future Homeowner, MaineHousing s First Home Program makes it easier and more affordable to buy a home of your own. There are many reasons to consider

First Home Program Affordable, fixed rate mortgages Dear Future Homeowner, MaineHousing s First Home Program makes it easier and more affordable to buy a home of your own. There are many reasons to consider

A consumer guide to construction financing.

A consumer guide to construction financing. Single Close Construction Loans Are you building a custom home? This guide is a valuable resource for anyone planning to build a custom home. It provides information

A consumer guide to construction financing. Single Close Construction Loans Are you building a custom home? This guide is a valuable resource for anyone planning to build a custom home. It provides information