Assessing Controls Over the Utility Payment Process

|

|

|

- Kory Barrett

- 7 years ago

- Views:

Transcription

1 Audit Report Report Number SM-AR December 30, 2015 Assessing Controls Over the Utility Payment Process

2 In FY 2014, the Postal Service paid about through two systems. The U.S. Postal Service operates about 32,000 facilities that use various types of utilities. These utilities include electricity, natural gas, water, steam, sewerage, and regulated telecommunications. In fiscal year (FY) 2014, the Postal Service paid about $537 million for utilities through two systems. Over 196,000 invoices totaling $433.9 million were processed in the Utility Management System (UMS) and over 675,000 invoices totaling $102.9 million were processed in the ebuy2 system. A Postal Service contractor enters and processes utility bills in the UMS for about 5,500 larger Postal Service facilities. A system-generated is then sent to designated local officials to verify the accuracy of the processed invoices. In addition, the Postal Service uses an exception report to identify invoice anomalies, such as excessive billing amounts, on all invoices processed in the UMS. ebuy2 is designed for ordering goods and services that cost less than $10,000; however, it is also used for requesting payment for utilities such as electricity and water for Postal Service facilities the UMS does not manage. Unlike UMS, Postal Service employees input and review utility invoices in ebuy2 rather than a contractor. Also, ebuy2 does not have the capability to produce exception reports. $537 million for utilities Background In 2010, we issued a report addressing the certification process for electronic invoices, including utility invoices processed in the UMS. In that audit, we found Postal Service personnel responsible for reviewing invoices were unaware of their roles, and contact information in the UMS was inaccurate. In response, the Postal Service developed training videos that described personnel roles in the UMS invoice process and how to access and update reviewer contact information in the UMS. This report is a follow-up to the corrective actions taken to improve oversight of utility payments made through the UMS. We also reviewed the ebuy2 utility payment process. Our objective was to evaluate the Postal Service s controls over utility payments. What the OIG Found The Postal Service can improve controls over utility payments. Its processes for reviewing utility invoices in the UMS were overlapping and unclear. For example: Area and district personnel were responsible for resolving UMS invoice anomalies identified in the UMS exception report when designated local personnel were already tasked to review the invoices. For 49 of 55 (89 percent) sampled utility invoices analyzed, personnel designated to review, question, or approve invoices in UMS did not always do so because they were unaware of their roles and responsibilities. 1

and over 675,000 invoices totaling $102.9 million were processed in the ebuy2 system.")

3 Contact information for personnel designated to review and approve UMS invoices was inaccurate or incomplete for 35 of the 55 invoices we reviewed. Five of 39 district personnel we interviewed who were responsible for addressing invoice anomalies identified on the UMS exception report were not familiar with the exception reporting process. Without clear policy and procedures to help defend against improper payments and the difficult pay and chase aspects of recovering improper payments, it is more challenging for the Postal Service to detect such payments. What the OIG Recommended We recommended management develop comprehensive formal policies and procedures to help ensure utility payments are properly made through UMS and ebuy2. Further, based on our sample of 153 ebuy2 invoices, 85 employees who input invoice data and 95 employees who reviewed the data stated they did not receive guidance on their roles and responsibilities. For example, the Postal Service was not able to take advantage of a potential tax exemption in at least 14 cases where employees were not aware they could request exemptions from certain taxes and fees. We also referred an invoice to the U.S. Postal Service Office of Inspector General Office of Investigation because the invoice had a Post Office box as its return address for payment, and the local utility authority stated it had not issued it. These conditions existed because management had not established a comprehensive or cohesive formal policy to direct the utility payment process and help ensure proper payments through the UMS and ebuy2. Instead, management relied on piecemeal processes and informal guidance to mitigate potential risks associated with utility payments. For example, training videos about the UMS and ebuy2 utility payment processes were dated, and personnel were not always aware of the training videos existence. 2

4 Transmittal Letter December 30, 2015 MEMORANDUM FOR: SUSAN M. BROWNELL VICE PRESIDENT, SUPPLY MANAGEMENT THOMAS DAY CHIEF SUSTAINABILITY OFFICER E-Signed by John Cihota VERIFY authenticity with esign Desktop FROM: John E. Cihota Deputy Assistant Inspector General for Finance and Supply Management SUBJECT: Audit Report Assessing Controls Over the Utility Payment Process () This report presents the results of our audit of Assessing Controls Over the Utility Payment Process (Project Number 15BG008SM000). We appreciate the cooperation and courtesies provided by your staff. If you have any questions or need additional information, please contact Keshia L. Trafton, director, Supply Management and Facilities, or me at Attachment cc: Corporate Audit and Response Management 3

. We appreciate the cooperation and courtesies provided by your staff.")

5 Cover...1 Background...1 What the OIG Found...1 What the OIG Recommended...2 Transmittal Letter Introduction...5 Utility Management System...5 ebuy2...6 Summary...6 Processes for Reviewing Utility Management System Invoices...7 Personnel Knowledge of Reviewing Invoices...7 s...10 Management s Comments...10 Evaluation of Management s Comments Appendix A: Additional Information...13 Background...13 Objective, Scope, and Methodology...13 Prior Audit Coverage...14 Appendix B: Management s Comments...15 Contact Information

6 The Postal Service operates about 32,000 facilities that use various types of utilities, including electricity, natural gas, water, steam, sewerage, and regulated telecommunications governmental agencies or private enterprises. This report presents the results of our self-initiated audit on (Project Number 15BG008SM000). The objective of our review was to evaluate the U.S. Postal Service s controls over utility payments. See Appendix A for additional information about this audit. The Postal Service operates about 32,000 facilities that use various types of utilities, including electricity, natural gas, water, steam, sewerage, and regulated telecommunications services provided by governmental agencies or private enterprises. In fiscal year (FY) 2014, the Postal Service paid about $537 million for utilities through two systems the Utility Management System (UMS)1 and ebuy2.2 The UMS provides utility bill management services, such as capturing cost and consumption data, bill payment processes, database development, billing audits and corrections, utility data and reporting, and rate optimization. ebuy2 is a Postal Service tool designed for ordering goods and services that cost less than $10,000. It is also used to request payment for utilities. In FY 2014, the Postal Service processed about 196,000 invoices in the UMS totaling $433.9 million and over 675,000 invoices in ebuy2 totaling $102.9 million. We statistically sampled 208 utility invoices totaling $117,688 paid during FYs 2013 and Fifty-five invoices (26 percent) totaling $86,487 were paid through the UMS, and 153 invoices (74 percent) totaling $31,201 were paid using ebuy2. Utility Management System In 2007, the Postal Service awarded a contract to Energy United to capture, record, and analyze energy-related data and pay the associated utility invoices in the UMS on behalf of the Postal Service. Utility payments made through the UMS are for about 5,500 larger Postal Service facilities (like processing and distribution centers) that have high energy consumption. At each facility, primary and secondary contacts are responsible for reviewing UMS invoices for accuracy. The contractor notifies both contacts and reviewers via that an invoice has been entered into the UMS and is ready for review. The primary contact reviews the invoice for accuracy and the secondary contact reviews it if the primary contact is not available. The contractor pays utility invoices without verification from the reviewers. If an invoice discrepancy is noted, the reviewer should contact Energy United for resolution, which can occur after payment. District coordinators are responsible for ensuring there are two current contacts, or reviewers, for each facility in each district and maintaining their names in the UMS. However, reviewers are responsible for initially requesting access to the UMS to receive and review invoices. They are also responsible for notifying the district coordinator if they no longer perform UMS duties because they change positions or retire. services provided by Introduction The UMS produces an exception report to identify invoice anomalies, such as excessive amounts; improper bill dates; days out of billing cycle range; or overlapping, skipped, or missing billing periods. Any invoice that meets the pre-established exception criteria is highlighted for further review. Area and district coordinators are responsible for reviewing these invoices and resolving any discrepancies. 1 2 A contractor-developed and managed system designed to track energy consumption and pay utility bills. A commercial, off-the-shelf application used by the Postal Service to buy goods and services. The software was modified to pay utility bills. 5

7 In 2010, the U.S. Postal Service Office of Inspector General (OIG) issued a report3 on the Postal Service s certification process for electronic payments. In that audit, we found designated Postal Service personnel responsible for reviewing invoices were unaware of their roles, and contact information in the UMS was inaccurate. In response, the Postal Service developed training videos that described personnel roles in the UMS invoice process and how to obtain access and update reviewer contact information in the UMS. ebuy2 Utility payments for smaller Postal Service facilities, primarily post offices, are paid through ebuy2, which was initially designed as a purchasing system. It was later modified to process utility invoice payments. Management stated that bringing the large number of smaller facilities into the UMS was too expensive. Paying utilities in ebuy2 is a two-step process. First, a Postal Service employee examines the utility bill, checks it for accuracy, and inputs the billing information into ebuy2. An approver then reviews the data and approves the invoice for payment, as appropriate. The Postal Service can improve controls over processes for reviewing utility invoices in the UMS were overlapping and unclear. utility payments. Its current Summary The Postal Service can improve controls over utility payments. Its current processes for reviewing utility invoices in the UMS were overlapping and unclear. For example, Postal Service area and district personnel were responsible for resolving identified UMS invoice discrepancies (as exceptions based on pre-established review criteria) through the exception reporting process when designated local Postal Service personnel were already tasked to review the invoices. In addition, Postal Service personnel designated to review, question, or approve invoices in the UMS did not always do so because they were unaware of their roles and responsibilities. Specifically, designated personnel did not review 49 of 55 (89 percent) utility invoices sampled in the UMS, and employees contact information in the system was inaccurate or incomplete for 35 of the 55 invoices we reviewed. Five of 39 employees responsible for addressing invoice anomalies identified on the UMS exception report were not familiar with the exception review process. We also found 12 invoices that included various taxes; seven of those invoices may have been eligible for exemption from the taxing authority. Further, based on our sample of 153 ebuy2 invoices, at least4 85 employees who input invoice data and 95 employees who reviewed the data stated they were not provided guidance on their roles and responsibilities. For example, for 21 invoices involving taxes and fees, personnel were not aware they could contact the Facility Services Category Management Center (CMC)5 in Windsor, CT, to determine whether the Postal Service could request an exemption from the taxes and fees included in the payment. At least 14 of the 21 may have been eligible for a tax exemption if the Postal Service had applied for it. These conditions occurred because management has not established a comprehensive or cohesive formal policy to direct the utility payment process and help ensure utility payments are properly paid through the UMS and ebuy2. Instead, management relied on piecemeal processes and informal guidance to mitigate potential risks associated with utility payments. For example, management created training videos about the UMS and ebuy2 utility payment processes; however, these videos were dated and the UMS video was hard to find. Although staff members were instructed to watch the videos, there was no mechanism in place to ensure staff complied with the directive Certification Process for Electronic Payments (Report Number CA-AR , dated September 30, 2010). For the 153 sampled invoices, we were not able to interview some relevant personnel because they retired, changed duties or facilities, or we could not locate them. This CMC oversees utility contracts. 6

8 Without clear guidance, the Postal Service is at risk of cost inefficiencies associated with duplicative effort. Processes for Reviewing Utility Management System Invoices Controls Over Utility Payment Processes The Postal Service s processes for reviewing utility invoices in the UMS were overlapping and unclear. In addition, based on our sample of ebuy2 invoices, not all personnel who input invoice data or those who reviewed the data stated they received guidance on their roles and responsibilities. The Postal Service s processes for reviewing utility invoices in the UMS were overlapping and unclear. Area and district coordinators were responsible for resolving UMS invoice anomalies identified in the exception report while primary and secondary contacts in the field were responsible for reviewing and approving these same invoices. Management had not addressed the necessity for all of these individuals to be involved in the invoice review process nor had they established policy to clearly define roles and responsibilities. By having multiple entities perform the same function without clear guidance, the Postal Service may, at a minimum, risk cost inefficiencies associated with duplicative efforts. The Postal Service needs to provide clear direction on how utility payments should be managed to ensure operational goals are met. Best practices state that management should define responsibilities, assign them to key personnel, and delegate authority to ensure control objectives are achieved. Doing so will enable the Postal Service to leverage its resources and maximize efficiencies in all operational areas, including utility payments. Personnel Knowledge of Reviewing Invoices Postal Service personnel designated to review, question, or approve invoices in the UMS did not always do so because they were unaware of their roles and responsibilities. We statistically sampled 208 utility invoices paid in FYs 2013 and Our analysis of the 55 UMS invoices revealed that: Click on the invoice to reveal information. 7

9 Thirty-four primary contacts and 29 secondary contacts did not have access to the UMS and, therefore, had not reviewed any invoices. The contacts had not requested UMS access nor were they aware of their responsibilities when they received an from the contractor indicating a bill would be paid on their behalf. Because of this audit, at least three sampled contacts requested UMS access in order to review utility invoices. Designated employees contact information in the UMS was inaccurate or incomplete for 35 of the 55 invoices we reviewed. For example, 14 primary contacts and 13 secondary contacts listed in the UMS were not the current designated official for the facility. Listed contacts had retired, left the Postal Service, or transferred to another facility. Energy United paid 12 invoices that included $470 in various taxes. The Postal Service might have been exempt from paying taxes (in the amount of $384) for at least seven of these invoices had it applied for an exemption from the local authorities. Energy United also paid one invoice with a $2.50 late fee. Personnel were not aware that they could contact the Postal Service Facility Services CMC to determine whether the Postal Service could apply for an exemption for taxes and fees included in the invoice. Also, five of 39 district employees we interviewed who were responsible for addressing invoice anomalies identified on the UMS exception report were not familiar with the exception reporting process. Of the 153 ebuy2 invoices we reviewed, 85 Postal Service employees designated to examine and input the utility invoices and 95 approvers stated they had not received any specific instructions on their job functions, or what taxes and fees to include when submitting or reviewing utility invoices in ebuy2. In addition, 11 employees inputting data and one approver stated that they did not check the accuracy of the invoices. Our analysis further revealed: Twenty-one ebuy2 invoices included state and local taxes totaling $270. For at least 14 of those invoices (with $225 in taxes) the Postal Service might have been exempt from paying taxes if it applied for an exemption from the local authority. For example, one transaction had state and franchise taxes of $93.31 and $22.79, respectively, totaling $ on an invoice totaling $1, The approver assumed the taxes needed to be paid and did not consult with the Facility Services CMC. Four ebuy2 invoices included late fees totaling $32. Click on the invoice to reveal information. In one district, an employee input utility bills in ebuy2 without review for at least 150 facilities within the district that were paid under one finance number. The district finance manager then approved the invoices without consulting with the local facilities to verify the accuracy of the billing information. One district employee responsible for approving at least 6,200 invoices stated that he approved them all without review. The Postal Service has taken corrective action by assigning one reviewer per invoice. 8

10 We were unable to obtain invoices for 12 sampled items. In many cases, the employees that input the invoice data or approved the invoice were no longer at the facilities, and the current personnel were not able to retrieve the invoices. We found an invoice from a local utility authority that used a Post Office box as its return address for payment. When asked, that local authority informed us it did not issue the invoice. We referred this invoice to the OIG s Office of Investigations. The Postal Service developed training videos to assist personnel involved in the utility payment process. The UMS training videos described the reviewer s (primary and secondary contacts) and coordinator s roles and responsibilities, explained how to run reports and update contact information in the system, and identified the process for resolving critical payment issues. Although the Postal Service developed these videos and staff members were instructed to watch them, there was no mechanism in place to ensure staff complied with the directive. Further, the videos were dated 2011 and not easily accessible in the Learning Management System.6 The Postal Service also developed ebuy2 training videos and published a user guide7 to assist personnel in the ebuy2 utility payment process. Although this online guidance provided instructions on how to input and approve invoice data, it did not establish roles and responsibilities for receiving, inputting, reviewing, and approving invoices, or updating the contact information in ebuy2. It also did not explain what taxes and fees were potentially eligible for an exemption from the taxing authority. These conditions occurred because management has not established a comprehensive or cohesive formal policy to direct the utility payment process and help ensure utility payments are correctly made through the UMS and ebuy2. Instead, management relied on piecemeal processes and informal guidance to mitigate potential risks associated with utility payments. In 2014, the Government Accountability Office (GAO) provided testimony to Congress on improper payments and strategies to reduce them. The GAO noted that designing and implementing strong preventive controls can help protect against improper payments, increasing public confidence, and avoiding the difficult pay and chase aspects of recovering improper payments. Without clear policy and procedures to govern and oversee the utility payment process, the Postal Service increases the risk that improper payments go undetected. Based on our analysis, $755,819,528 in payments made through the UMS in FYs 2013 and 2014 were at risk because they were not properly reviewed.8 This total amount does not represent an actual loss but was at risk because the Postal Service s processes were not followed The Postal Service s individual learning and training system designed to improve job performance. ebuy2 User Guide, dated August 30, Total utility payments made through UMS in FY 2013 and FY 2014 were $848,282,298. 9

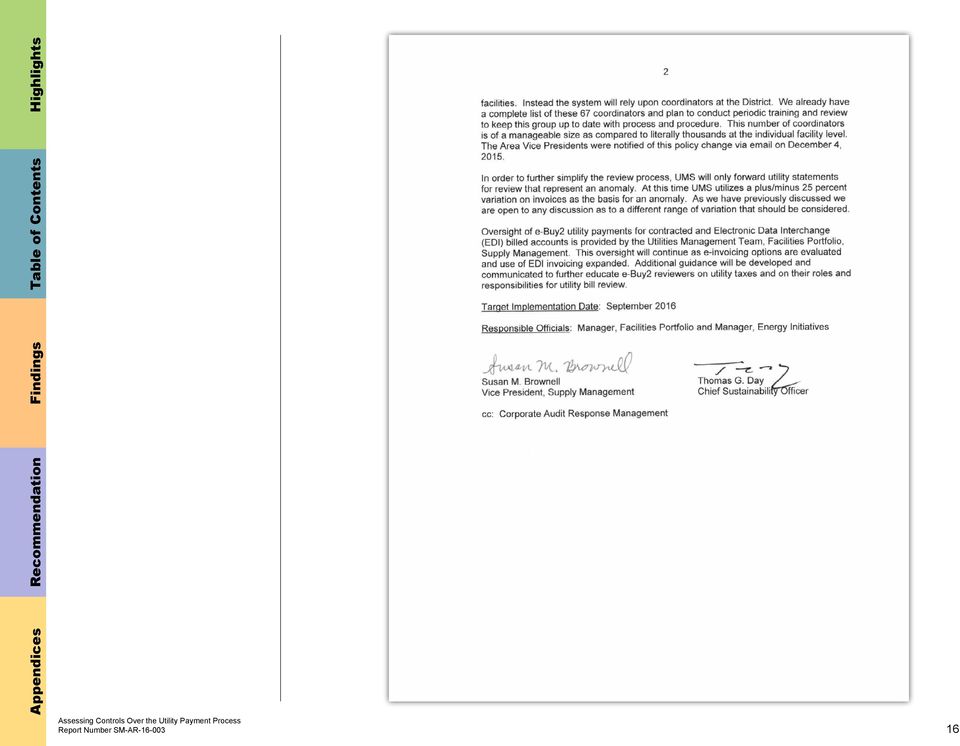

11 We recommend the vice president, Supply Management, in coordination with the chief sustainability officer: 1. Develop comprehensive formal policies and procedures to help ensure utility payments are properly made through the Utility Management System and ebuy2. Management s Comments Management agreed with the findings and recommendation but disagreed with the risk impact of $755,819,528. Regarding the recommendation, management agreed to develop additional guidance on the administration of utilities. Management stated they have modified the review process for UMS and there is no longer an invoice reviewer at each facility. Instead, the system will rely on 67 district coordinators. Management stated they plan to conduct periodic training and review to update this group with relevant processes and procedures. Management told us they notified area vice presidents in a December 4, 2015, . Management further stated the Supply Management Utilities Management Team, Facilities Portfolio, will continue overseeing ebuy2 utility payments for contracted and electronic data interchange (EDI) billed accounts as they evaluate e-invoicing options and expand use of EDI invoicing. Management will develop additional guidance and communicate it to educate ebuy2 reviewers on utility taxes and on their roles and responsibilities for utility bill review. The target implementation date is September 30, Regarding the impact risk, management stated the calculation was not correctly executed because it included the total value of utility invoices, when the audit findings indicated the risk was associated with a significantly small subset of fees and taxes. Management emphasized the Postal Service may be excluded from these payments and stated that a rough estimate indicates the risk as less than one hundredth of the amount the OIG calculated. Management further stated the Postal Service consumed the utilities and that timely payments were appropriate. Management stated that a higher level review process for UMS invoices begins with the bill management service that produces an exception report of anomalies. Management also pointed out that, based on a prior OIG report, the Postal Service implemented additional reviews this audit considered redundant. Further, while the report indicates these additional reviews were not always performed and is the basis for the impact, management disagreed with the calculation because of the extensive controls performed, up front, in the bill paying process. See Appendix B for management s comments in their entirety. Evaluation of Management s Comments The OIG considers management s comments responsive to the recommendation in the report. Regarding the disbursements at risk impact, we calculated this amount by totaling all utility invoices paid through UMS for FYs 2013 and 2014 and applying the percentage of invoices that were not reviewed based on our statistical sample for that period. This total amount does not represent an actual loss but was at risk because employees did not follow Postal Service processes. Management commented that they have controls such as an exception reporting process as part of the upfront controls in the bill payment process; however, as noted in our report, employees responsible for reviewing the exception reports, as well 10

12 as those reviewing invoices, were not always aware of their roles and responsibilities. Having multiple entities perform similar functions without clear guidance increases the risk of not detecting improper payments. All recommendations require OIG concurrence before closure. Consequently, the OIG requests written confirmation when corrective action is completed. 1 should not be closed in the Postal Service s follow-up tracking system until the OIG provides written confirmation that the recommendation can be closed. 11

13 to the right to navigate to the section content. Click on the appendix title Appendix A: Additional Information...13 Background...13 Objective, Scope, and Methodology...13 Prior Audit Coverage...14 Appendix B: Management s Comments

14 Background In FY 2014, the Postal Service paid about $537 million for utilities about $434 million through the UMS and about $103 million through ebuy2. The Postal Service requires vendors to submit utility invoices to a contractor for processing and payment in the UMS. For ebuy2, vendors may submit their invoices manually or via EDI to the Postal Service. Currently, a contractor pays utility invoices in UMS on behalf of the Postal Service for about 5,500 larger postal facilities. All invoices processed and paid through the UMS are received electronically. The time allotted to review utility invoices is 3 to 15 days, depending on the payment due date. The contractor s designated Postal Service officials when the invoice is ready for review. There are no read receipts to ensure the designated official reviews the information prior to paying the bill, and the official is not required to respond to the notification unless the invoice charges are incorrect. The contractor pays the utility invoice without reviewing results from the designated officials. If errors are found later with the invoice, the Postal Service must request a refund or adjustment. This process is often called a pay and chase arrangement. Appendix A: Additional Information This pay and chase process is critical as the Postal Service pays the invoice when it is electronically received from the supplier whether or not a designated Postal Service official has approved the invoice for payment. The UMS also has an exception process function to identify invoices with anomalies and reduce the number of refunds that would have to be chased. The exception process monitors invoices for anomalies such as excessive amounts, improper bill dates, days out of range, overlapping periods, and skipped/missing billing periods. In 2010, we conducted an audit of the certification process for electronic payments.9 That audit covered electronic payments made for highway contract routes, utilities, and communications. We found the Postal Service needed to improve oversight of electronic payments to ensure that payments to contractors are properly certified and that the agency has received goods and services before making payment. For utility payments, we recommended the Postal Service ensure that the designated official contact information in the UMS is accurate and the system required positive certification by the designated official before invoice payment. The Postal Service began updating contact information in 2013; however, it did not take action to ensure a positive certification was required by a designated official before invoice payment. The Postal Service provided evidence that invoice data it input into the system was validated for accuracy prior to payment and that invoice information was sent to the facility for review, but that process did not require positive certification of the invoiced amount by a designated Postal Service official before payment. Objective, Scope, and Methodology Our objective was to evaluate the Postal Service s controls over utility payments. To accomplish this objective we: Interviewed Postal Service Headquarters personnel to determine the process for receiving, certifying, and paying utility invoices managed and processed via the UMS and ebuy2. Interviewed personnel that oversee utility payments made via the UMS and ebuy2 to discuss the controls in place to ensure the accuracy of utility bills and payments. Identified policies and procedures that are applicable to the payment of utility expenses through the UMS and ebuy2. 9 Certification Process for Electronic Payments (Report Number CA-AR , dated September 30, 2010). 13

15 Statistically sampled 208 invoices from the UMS and ebuy2 and analyzed payment procedures/controls used in making the payment. We conducted this performance audit from January through December 2015, in accordance with generally accepted government auditing standards and included such tests of internal controls as we considered necessary under the circumstances. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions based on our audit objective. We believe that the evidence obtained provides a reasonable basis for our findings and conclusions based on our audit objective. We discussed our observations and conclusions with management on November 18, 2015, and included their comments where appropriate. We assessed the reliability of computer-generated data for the purposes of this report. We verified sampled electronic records in the UMS and ebuy2 system with source documentation. We determined that the data were sufficiently reliable for the purposes of this report. Prior Audit Coverage We did not identify any prior audits or reviews related to utility payments that were conducted in the last 3 years. However, we issued an audit report10 in 2010 on the certification process for electronic payments that addressed the certification of utility payments. The audit found that designated Postal Service officials were unaware of their roles and responsibilities for receiving and reviewing utility invoices from Energy United, the contractor responsible for processing the UMS payments. In addition, contact information in the UMS was inaccurate. The recommendations associated with this finding were considered significant and remained open until March The Postal Service began action to update contact information but never took action to ensure invoices were reviewed by a designated official prior to payment. 10 Certification Process for Electronic Payments (Report Number CA-AR , dated September 30, 2010). 14

16 Appendix B: Management s Comments 15

17 16

18 Contact us via our Hotline and FOIA forms, follow us on social networks, or call our Hotline at to report fraud, waste or abuse. Stay informed North Lynn Street Arlington, VA (703)

")

Oversight of Expense Purchase Cards

Oversight of Expense Purchase Cards Audit Report Report Number SM-AR-15-006 August 7, 2015 Background The expense purchase card is the most commonly used purchase card in the U.S. Postal Service. Postal

Oversight of Expense Purchase Cards Audit Report Report Number SM-AR-15-006 August 7, 2015 Background The expense purchase card is the most commonly used purchase card in the U.S. Postal Service. Postal

Professional Services Contract Rates

Professional Services Contract Rates Audit Report Report Number SM-AR-15-001 November 10, 2014 Highlights The Postal Service awarded one supplier an independent accounting services contract at individual

Professional Services Contract Rates Audit Report Report Number SM-AR-15-001 November 10, 2014 Highlights The Postal Service awarded one supplier an independent accounting services contract at individual

U.S. Postal Service s DRIVE 25 Improve Customer Experience

U.S. Postal Service s DRIVE 25 Improve Customer Experience Audit Report Report Number MI-AR-16-001 November 16, 2015 DRIVE Initiative 25 is suppose to increase customer satisfaction with how complaints

U.S. Postal Service s DRIVE 25 Improve Customer Experience Audit Report Report Number MI-AR-16-001 November 16, 2015 DRIVE Initiative 25 is suppose to increase customer satisfaction with how complaints

Management of Detail Assignments Follow-Up

Management of Detail Assignments Follow-Up Audit Report Report Number DP-AR-14-007 September 26, 2014 Highlights From June through December 2013 the Postal Service spent about $17.8 million on travel related

Management of Detail Assignments Follow-Up Audit Report Report Number DP-AR-14-007 September 26, 2014 Highlights From June through December 2013 the Postal Service spent about $17.8 million on travel related

Solution for Enterprise Asset. Management. System Vehicle Maintenance Facility Data. Management. Advisory Report. Report Number DR-MA-15-004

Solution for Enterprise Asset Management System Vehicle Maintenance Facility Data Management Advisory Report Report Number DR-MA-15-004 September 18, 2015 Highlights This management advisory discusses

Solution for Enterprise Asset Management System Vehicle Maintenance Facility Data Management Advisory Report Report Number DR-MA-15-004 September 18, 2015 Highlights This management advisory discusses

Cloud Computing Contract Clauses

Cloud Computing Contract Clauses Management Advisory Report Report Number SM-MA-14-005-DR April 30, 2014 Highlights The 13 cloud computing contracts did not address information accessibility and data security

Cloud Computing Contract Clauses Management Advisory Report Report Number SM-MA-14-005-DR April 30, 2014 Highlights The 13 cloud computing contracts did not address information accessibility and data security

Misclassified Training Expenses

Misclassified Training Expenses Management Advisory Report Report Number DP-MA-14-003 September 16, 2014 Highlights The Postal Service overstated the general ledger expense account balances for "Training

Misclassified Training Expenses Management Advisory Report Report Number DP-MA-14-003 September 16, 2014 Highlights The Postal Service overstated the general ledger expense account balances for "Training

INSPECTOR GENERAL. Contracting of Real Estate Management Services. Audit Report. June 12, 2013. Report Number SM-AR-13-001 OFFICE OF

OFFICE OF INSPECTOR GENERAL UNITED STATES POSTAL SERVICE Contracting of Real Estate Management Services Audit Report June 12, 2013 Report Number June 12, 2013 Contracting of Real Estate Management Services

OFFICE OF INSPECTOR GENERAL UNITED STATES POSTAL SERVICE Contracting of Real Estate Management Services Audit Report June 12, 2013 Report Number June 12, 2013 Contracting of Real Estate Management Services

Information Security Awareness Training and Phishing

Information Security Awareness Training and Phishing Audit Report Report Number IT-AR-16-001 October 5, 2015 Highlights The Postal Service s information security awareness training related to phishing

Information Security Awareness Training and Phishing Audit Report Report Number IT-AR-16-001 October 5, 2015 Highlights The Postal Service s information security awareness training related to phishing

Software Change Management for Engineering Systems

Audit Report Report Number IT-AR-16-007 June 13, 2016 Software Change Management for Engineering Systems Our objective was to evaluate the effectiveness of the software change management process for Engineering

Audit Report Report Number IT-AR-16-007 June 13, 2016 Software Change Management for Engineering Systems Our objective was to evaluate the effectiveness of the software change management process for Engineering

Monitoring of Government Travel Card Transactions

Monitoring of Government Travel Card Transactions Management Advisory Report Report Number DP-MA-14-002 June 25, 2014 Highlights The Postal Service has eliminated use of the travel card for cash advances

Monitoring of Government Travel Card Transactions Management Advisory Report Report Number DP-MA-14-002 June 25, 2014 Highlights The Postal Service has eliminated use of the travel card for cash advances

Software Contract and Compliance Review

Audit Report Report Number IT-AR-15-009 September 18, 2015 Software Contract and Compliance Review The software contract did not comply with all applicable standards and management did not ensure the supplier

Audit Report Report Number IT-AR-15-009 September 18, 2015 Software Contract and Compliance Review The software contract did not comply with all applicable standards and management did not ensure the supplier

Undeliverable as Addressed Mail

Undeliverable as Addressed Mail Audit Report Report Number MS-AR-14-006 July 14, 2014 Highlights The Postal Service has taken action to reduce and recover UAA mail costs by testing whether business mailers

Undeliverable as Addressed Mail Audit Report Report Number MS-AR-14-006 July 14, 2014 Highlights The Postal Service has taken action to reduce and recover UAA mail costs by testing whether business mailers

Hardware Inventory Management Greater Boston District

Hardware Inventory Management Greater Boston District Audit Report Report Number IT-AR-15-004 March 25, 2015 Highlights Management does not have an accurate inventory of hardware assets connected to the

Hardware Inventory Management Greater Boston District Audit Report Report Number IT-AR-15-004 March 25, 2015 Highlights Management does not have an accurate inventory of hardware assets connected to the

Retail Systems Software Deployment and Functionality

Retail Systems Software Deployment and Functionality Audit Report Report Number MI-AR-15-002 March 13, 2015 Highlights Background The U.S. Postal Service Office of Inspector General (OIG) conducted a self-initiated

Retail Systems Software Deployment and Functionality Audit Report Report Number MI-AR-15-002 March 13, 2015 Highlights Background The U.S. Postal Service Office of Inspector General (OIG) conducted a self-initiated

Review of Selected Active Directory Domains

Audit Report Report Number IT-AR-16-006 February 10, 2016 Review of Selected Active Directory Domains Postal Service management did not appropriately configure and manage the five domains we reviewed on

Audit Report Report Number IT-AR-16-006 February 10, 2016 Review of Selected Active Directory Domains Postal Service management did not appropriately configure and manage the five domains we reviewed on

Geo-Fence Technology in Delivery Operations

Geo-Fence Technology in Delivery Operations Management Advisory Report Report Number DR-MA-14-006 August 14, 2014 Highlights The Postal Service s planned use of geo-fence technology in the delivery environment

Geo-Fence Technology in Delivery Operations Management Advisory Report Report Number DR-MA-14-006 August 14, 2014 Highlights The Postal Service s planned use of geo-fence technology in the delivery environment

Utilization of Marketing and Sales Data for Executives

Utilization of Marketing and Sales Data for Executives Audit Report Report Number MS-AR-15-002 March 4, 2015 Highlights The CMSO effectively uses available data to manage business activities and mitigate

Utilization of Marketing and Sales Data for Executives Audit Report Report Number MS-AR-15-002 March 4, 2015 Highlights The CMSO effectively uses available data to manage business activities and mitigate

INSPECTOR GENERAL UNITED STATES POSTAL SERVICE

OFFICE OF INSPECTOR GENERAL UNITED STATES POSTAL SERVICE Trends and Systemic Issues in Defense Contract Audit Agency Audit Work for Fiscal Years 2009-2012 Management Advisory Report Report Number March

OFFICE OF INSPECTOR GENERAL UNITED STATES POSTAL SERVICE Trends and Systemic Issues in Defense Contract Audit Agency Audit Work for Fiscal Years 2009-2012 Management Advisory Report Report Number March

April 27, 2011 SUSAN M. BROWNELL VICE PRESIDENT, SUPPLY MANAGEMENT. SUBJECT: Audit Report Contract Management Data (Report Number CA-AR-11-002)

") April 27, 2011 SUSAN M. BROWNELL VICE PRESIDENT, SUPPLY MANAGEMENT SUBJECT: Audit Report Contract Management Data (Report Number ) This report presents the results of our self-initiated audit of contract

April 27, 2011 SUSAN M. BROWNELL VICE PRESIDENT, SUPPLY MANAGEMENT SUBJECT: Audit Report Contract Management Data (Report Number ) This report presents the results of our self-initiated audit of contract

Customer Service Operations Efficiency Chicago District

Customer Service Operations Efficiency Chicago District Audit Report Report Number MS-AR-15-005 April 28, 2015 Highlights During FY 2014, 12 of 13 facilities had actual workhours in excess of estimated

Customer Service Operations Efficiency Chicago District Audit Report Report Number MS-AR-15-005 April 28, 2015 Highlights During FY 2014, 12 of 13 facilities had actual workhours in excess of estimated

Software Development Processes

Software Development Processes Audit Report Report Number IT-AR-15-006 July 13, 2015 Highlights The Postal Service does not consistently manage software development risk. Background Organizations spend

Software Development Processes Audit Report Report Number IT-AR-15-006 July 13, 2015 Highlights The Postal Service does not consistently manage software development risk. Background Organizations spend

Customer Retention. Audit Report. Report Number MS-AR-14-008. September 25, 2014

Customer Retention Audit Report Report Number MS-AR-14-008 September 25, 2014 Background The U.S. Postal Service has a significant customer base, ranging from residential customers to large commercial

Customer Retention Audit Report Report Number MS-AR-14-008 September 25, 2014 Background The U.S. Postal Service has a significant customer base, ranging from residential customers to large commercial

Customer Care Centers

Customer Care Centers Audit Report Report Number MS-AR-15-006 June 11, 2015 Highlights Residential and business customers contact the U.S. Postal Service through various toll-free telephone numbers for

Customer Care Centers Audit Report Report Number MS-AR-15-006 June 11, 2015 Highlights Residential and business customers contact the U.S. Postal Service through various toll-free telephone numbers for

Capital District Vulnerability Assessment

Capital District Vulnerability Assessment Audit Report Report Number IT-AR-15-1 December 12, 214 These vulnerabilities expose the infrastructure to unauthorized remote access by potential attackers who

Capital District Vulnerability Assessment Audit Report Report Number IT-AR-15-1 December 12, 214 These vulnerabilities expose the infrastructure to unauthorized remote access by potential attackers who

Voyager Card Program Capping Report

Voyager Card Program Capping Report Management Advisory Report Report Number NO-MA-14-007 September 30, 2014 Highlights The HCR Voyager Card Program implemented by the Postal Service in 2005 is not effective

Voyager Card Program Capping Report Management Advisory Report Report Number NO-MA-14-007 September 30, 2014 Highlights The HCR Voyager Card Program implemented by the Postal Service in 2005 is not effective

U.S. Postal Service s Delivering Results, Innovation, Value, and Efficiency Initiative 30 Achieve 100 Percent Customer and Revenue Visibility

U.S. Postal Service s Delivering Results, Innovation, Value, and Efficiency Initiative 30 Achieve 100 Percent Customer and Revenue Visibility Audit Report Report Number MI-AR-15-004 June 12, 2015 Highlights

U.S. Postal Service s Delivering Results, Innovation, Value, and Efficiency Initiative 30 Achieve 100 Percent Customer and Revenue Visibility Audit Report Report Number MI-AR-15-004 June 12, 2015 Highlights

Seamless Acceptance Implementation

Seamless Acceptance Implementation Audit Report Report Number MS-AR-15-004 April 7, 2015 Highlights Background Commercial mail accounted for most of the U.S. Postal Service s revenue 70 percent ($47 billion)

Seamless Acceptance Implementation Audit Report Report Number MS-AR-15-004 April 7, 2015 Highlights Background Commercial mail accounted for most of the U.S. Postal Service s revenue 70 percent ($47 billion)

Software Inventory Management Greater Boston District

Software Inventory Management Greater Boston District Audit Report Report Number IT-AR-15-007 July 13, 2015 Highlights Effective software management practices are not in place to adequately protect and

Software Inventory Management Greater Boston District Audit Report Report Number IT-AR-15-007 July 13, 2015 Highlights Effective software management practices are not in place to adequately protect and

SUBJECT: Management Advisory Retirement for U.S. Postal Service Employees on Workers Compensation (Report Number HR-MA-11-001)

") April 22, 2011 DEBORAH M. GIANNONI-JACKSON VICE PRESIDENT, EMPLOYEE RESOURCE MANAGEMENT SUBJECT: Management Advisory Retirement for U.S. Postal Service Employees on Workers Compensation (Report Number

April 22, 2011 DEBORAH M. GIANNONI-JACKSON VICE PRESIDENT, EMPLOYEE RESOURCE MANAGEMENT SUBJECT: Management Advisory Retirement for U.S. Postal Service Employees on Workers Compensation (Report Number

VICE PRESIDENT, ENTERPRISE ANALYTICS. Deputy Assistant Inspector General for Finance and Supply Management

September 11, 2015 MEMORANDUM FOR: ROBERT CINTRON VICE PRESIDENT, ENTERPRISE ANALYTICS E-Signed by Lorie Nelson ERIFY authenticity with esign Deskto FROM: SUBJECT: for John Cihota Deputy Assistant Inspector

September 11, 2015 MEMORANDUM FOR: ROBERT CINTRON VICE PRESIDENT, ENTERPRISE ANALYTICS E-Signed by Lorie Nelson ERIFY authenticity with esign Deskto FROM: SUBJECT: for John Cihota Deputy Assistant Inspector

How To Improve The Business Service Network

Business Service Network Customer Service Audit Report July 9, 2014 Highlights Background The U.S. Postal Service s (BSN) of 300 employees supports nearly 23,000 large customers for service issues, information,

Business Service Network Customer Service Audit Report July 9, 2014 Highlights Background The U.S. Postal Service s (BSN) of 300 employees supports nearly 23,000 large customers for service issues, information,

SUBJECT: Audit Report Contract Payment Terms (Report Number CA-AR-10-004)

") May 27, 2010 SUSAN M. BROWNELL VICE PRESIDENT, SUPPLY MANAGEMENT SUBJECT: Audit Report Contract Payment Terms (Report Number ) This report presents the results of our audit of contract payment terms (Project

May 27, 2010 SUSAN M. BROWNELL VICE PRESIDENT, SUPPLY MANAGEMENT SUBJECT: Audit Report Contract Payment Terms (Report Number ) This report presents the results of our audit of contract payment terms (Project

INSPECTOR GENERAL UNITED STATES POSTAL SERVICE

OFFICE OF INSPECTOR GENERAL UNITED STATES POSTAL SERVICE Corporate Succession Planning Program Management Advisory Report April 23, 2014 Report Number April 23, 2014 Corporate Succession Planning Program

OFFICE OF INSPECTOR GENERAL UNITED STATES POSTAL SERVICE Corporate Succession Planning Program Management Advisory Report April 23, 2014 Report Number April 23, 2014 Corporate Succession Planning Program

Management Advisory Postal Service Transformation Plan (Report Number OE-MA-03-001)

") October 29, 2002 RALPH J. MODEN VICE PRESIDENT, STRATEGIC PLANNING SUBJECT: Management Advisory Postal Service Transformation Plan (Report Number ) This management advisory presents the results of our

October 29, 2002 RALPH J. MODEN VICE PRESIDENT, STRATEGIC PLANNING SUBJECT: Management Advisory Postal Service Transformation Plan (Report Number ) This management advisory presents the results of our

SUBJECT: Audit Report Electronic Data Systems Contract Invoice Approval Procedures (Report Number CA-AR-05-002)

") Office of Inspector General May 13, 2005 KEITH STRANGE VICE PRESIDENT, SUPPLY MANAGEMENT SUBJECT: Audit Report Electronic Data Systems Contract Invoice Approval Procedures (Report Number ) This report

Office of Inspector General May 13, 2005 KEITH STRANGE VICE PRESIDENT, SUPPLY MANAGEMENT SUBJECT: Audit Report Electronic Data Systems Contract Invoice Approval Procedures (Report Number ) This report

Report No. D-2010-058 May 14, 2010. Selected Controls for Information Assurance at the Defense Threat Reduction Agency

Report No. D-2010-058 May 14, 2010 Selected Controls for Information Assurance at the Defense Threat Reduction Agency Additional Copies To obtain additional copies of this report, visit the Web site of

Report No. D-2010-058 May 14, 2010 Selected Controls for Information Assurance at the Defense Threat Reduction Agency Additional Copies To obtain additional copies of this report, visit the Web site of

Management Advisory Review of Decontamination Activities at the Pentagon Station (Report Number LH-MA-02-003)

") March 12, 2002 PATRICK R. DONAHOE CHIEF OPERATING OFFICER AND EXECUTIVE VICE PRESIDENT KEITH STRANGE VICE PRESIDENT, PURCHASING AND MATERIALS SUBJECT: Management Advisory Review of Decontamination Activities

March 12, 2002 PATRICK R. DONAHOE CHIEF OPERATING OFFICER AND EXECUTIVE VICE PRESIDENT KEITH STRANGE VICE PRESIDENT, PURCHASING AND MATERIALS SUBJECT: Management Advisory Review of Decontamination Activities

Parcel Readiness Product Tracking and Reporting System Controls

Parcel Readiness Product Tracking and Reporting System Controls Audit Report Report Number IT-AR-5-002 December 6, 204 The Postal Service needs to improve its process for managing and securing the PTR

Parcel Readiness Product Tracking and Reporting System Controls Audit Report Report Number IT-AR-5-002 December 6, 204 The Postal Service needs to improve its process for managing and securing the PTR

Workers Compensation Compound Drug Costs. Management Advisory. Report Number HR-MA-16-003. March 14, 2016

Management Advisory Report Number HR-MA-16-003 March 14, 2016 Workers Compensation Compound Drug Costs In CBY 2015, the total number of Postal Service employees with compound drug prescriptions increased

Management Advisory Report Number HR-MA-16-003 March 14, 2016 Workers Compensation Compound Drug Costs In CBY 2015, the total number of Postal Service employees with compound drug prescriptions increased

CHIEF POSTAL INSPECTOR. Management Alert Watch Desk Notifications (Report Number HR-MA-14-005)

") February 27, 2014 MEMORANDUM FOR: GUY J. COTTRELL CHIEF POSTAL INSPECTOR FROM: SUBJECT: Michael A. Magalski Deputy Assistant Inspector General for Support Operations Management Alert Watch Desk Notifications

February 27, 2014 MEMORANDUM FOR: GUY J. COTTRELL CHIEF POSTAL INSPECTOR FROM: SUBJECT: Michael A. Magalski Deputy Assistant Inspector General for Support Operations Management Alert Watch Desk Notifications

Objectives, Scope, and Methodology

March 20, 2007 LYNN MALCOLM VICE PRESIDENT, CONTROLLER SUBJECT: Audit Report Employee Accounts Receivable Follow-Up (Report Number ) This report presents the results of our self-initiated audit of Employee

March 20, 2007 LYNN MALCOLM VICE PRESIDENT, CONTROLLER SUBJECT: Audit Report Employee Accounts Receivable Follow-Up (Report Number ) This report presents the results of our self-initiated audit of Employee

AUDIT REPORT 12-1 8. Audit of Controls over GPO s Fleet Credit Card Program. September 28, 2012

AUDIT REPORT 12-1 8 Audit of Controls over GPO s Fleet Credit Card Program September 28, 2012 Date September 28, 2012 To Director, Acquisition Services From Inspector General Subject Audit Report Audit

AUDIT REPORT 12-1 8 Audit of Controls over GPO s Fleet Credit Card Program September 28, 2012 Date September 28, 2012 To Director, Acquisition Services From Inspector General Subject Audit Report Audit

SUBJECT: Audit Report Compliance with Occupational Safety and Health Administration Recordkeeping Requirements (Report Number HR-AR-11-004)

") May 27, 2011 DEBORAH M. GIANNONI-JACKSON VICE PRESIDENT, EMPLOYEE RESOURCE MANAGEMENT SUBJECT: Audit Report Compliance with Occupational Safety and Health (Report Number ) This report presents the results

May 27, 2011 DEBORAH M. GIANNONI-JACKSON VICE PRESIDENT, EMPLOYEE RESOURCE MANAGEMENT SUBJECT: Audit Report Compliance with Occupational Safety and Health (Report Number ) This report presents the results

VA Office of Inspector General

w VA Office of Inspector General OFFICE OF AUDITS AND EVALUATIONS Veterans Health Administration Audit of Support Service Contracts November 19, 2014 12-02576-30 ACRONYMS AND ABBREVIATIONS A&A COR ecms

w VA Office of Inspector General OFFICE OF AUDITS AND EVALUATIONS Veterans Health Administration Audit of Support Service Contracts November 19, 2014 12-02576-30 ACRONYMS AND ABBREVIATIONS A&A COR ecms

Management of Cloud Computing Contracts and Environment

Management of Cloud Computing Contracts and Environment Audit Report Report Number IT-AR-14-009 September 4, 2014 Cloud computing contracts did not comply with Postal Service standards. Background The

Management of Cloud Computing Contracts and Environment Audit Report Report Number IT-AR-14-009 September 4, 2014 Cloud computing contracts did not comply with Postal Service standards. Background The

ROSS PHILO EXECUTIVE VICE PRESIDENT AND CHIEF INFORMATION OFFICER

July 22, 2010 ROSS PHILO EXECUTIVE VICE PRESIDENT AND CHIEF INFORMATION OFFICER DEBORAH J. JUDY DIRECTOR, INFORMATION TECHNOLOGY OPERATIONS CHARLES L. MCGANN, JR. MANAGER, CORPORATE INFORMATION SECURITY

July 22, 2010 ROSS PHILO EXECUTIVE VICE PRESIDENT AND CHIEF INFORMATION OFFICER DEBORAH J. JUDY DIRECTOR, INFORMATION TECHNOLOGY OPERATIONS CHARLES L. MCGANN, JR. MANAGER, CORPORATE INFORMATION SECURITY

THOMAS G. DAY SENIOR VICE PRESIDENT, INTELLIGENT MAIL AND ADDRESS QUALITY PRITHA N. MEHRA VICE PRESIDENT, BUSINESS MAIL ENTRY AND PAYMENT TECHNOLOGIES

March 31, 2009 THOMAS G. DAY SENIOR VICE PRESIDENT, INTELLIGENT MAIL AND ADDRESS QUALITY PRITHA N. MEHRA VICE PRESIDENT, BUSINESS MAIL ENTRY AND PAYMENT TECHNOLOGIES GEORGE W. WRIGHT VICE PRESIDENT, INFORMATION

March 31, 2009 THOMAS G. DAY SENIOR VICE PRESIDENT, INTELLIGENT MAIL AND ADDRESS QUALITY PRITHA N. MEHRA VICE PRESIDENT, BUSINESS MAIL ENTRY AND PAYMENT TECHNOLOGIES GEORGE W. WRIGHT VICE PRESIDENT, INFORMATION

How To Check For Errors In International Mail Volume Data

Office of Inspector General March 22, 2006 AYODEJI O. SANYAOLU PLANT MANAGER - J.T. WEEKER (CHICAGO) INTERNATIONAL SERVICE CENTER SUBJECT: Audit Report J.T. Weeker (Chicago) International Service Center

Office of Inspector General March 22, 2006 AYODEJI O. SANYAOLU PLANT MANAGER - J.T. WEEKER (CHICAGO) INTERNATIONAL SERVICE CENTER SUBJECT: Audit Report J.T. Weeker (Chicago) International Service Center

January 20, 2009 GEORGE W. WRIGHT VICE PRESIDENT, INFORMATION TECHNOLOGY OPERATIONS

January 20, 2009 GEORGE W. WRIGHT VICE PRESIDENT, INFORMATION TECHNOLOGY OPERATIONS SUBJECT: Audit Report Service Continuity at the Information Technology and (Report Number ) This report presents the

January 20, 2009 GEORGE W. WRIGHT VICE PRESIDENT, INFORMATION TECHNOLOGY OPERATIONS SUBJECT: Audit Report Service Continuity at the Information Technology and (Report Number ) This report presents the

Postal Service Management of CBRE Real Estate Transactions

Postal Service Management of CBRE Real Estate Transactions Audit Report Report Number SM-AR-15-003 April 22, 2015 Background Under a June 2011 contract, CBRE Group, Inc. (CBRE) is the sole provider of

Postal Service Management of CBRE Real Estate Transactions Audit Report Report Number SM-AR-15-003 April 22, 2015 Background Under a June 2011 contract, CBRE Group, Inc. (CBRE) is the sole provider of

NATIONAL OCEANIC AND ATMOSPHERIC ADMINISTRATION. Opportunities to Strengthen Internal Controls Over Improper Payments PUBLIC RELEASE

U.S. DEPARTMENT OF COMMERCE Office of Inspector General NATIONAL OCEANIC AND ATMOSPHERIC ADMINISTRATION Opportunities to Strengthen Internal Controls Over Improper Payments Final Report No.BSD-16186-0001/July

U.S. DEPARTMENT OF COMMERCE Office of Inspector General NATIONAL OCEANIC AND ATMOSPHERIC ADMINISTRATION Opportunities to Strengthen Internal Controls Over Improper Payments Final Report No.BSD-16186-0001/July

PROCUREMENT. Actions Needed to Enhance Training and Certification Requirements for Contracting Officer Representatives OIG-12-3

PROCUREMENT Actions Needed to Enhance Training and Certification Requirements for Contracting Officer Representatives OIG-12-3 Office of Inspector General U.S. Government Accountability Office Report Highlights

PROCUREMENT Actions Needed to Enhance Training and Certification Requirements for Contracting Officer Representatives OIG-12-3 Office of Inspector General U.S. Government Accountability Office Report Highlights

Postal Service Management of Closed Post Office Boxes. Audit Report. Report Number DP-AR-13-007

Postal Service Management of Closed Post Office Boxes Audit Report Report Number June 18, 2013 June 18, 2013 Postal Service Management of Closed Post Office Boxes Report Number BACKGROUND: Post Office

Postal Service Management of Closed Post Office Boxes Audit Report Report Number June 18, 2013 June 18, 2013 Postal Service Management of Closed Post Office Boxes Report Number BACKGROUND: Post Office

US Postal Service - Effective Security Policies and Controls For Wireless Networks

Wireless Local Area Network Deployment and Security Practices Audit Report Report Number IT-AR-14-005-DR April 24, 2014 Highlights Our objectives were to determine whether the Postal Service has effective

Wireless Local Area Network Deployment and Security Practices Audit Report Report Number IT-AR-14-005-DR April 24, 2014 Highlights Our objectives were to determine whether the Postal Service has effective

DoD Methodologies to Identify Improper Payments in the Military Health Benefits and Commercial Pay Programs Need Improvement

Report No. DODIG-2015-068 I nspec tor Ge ne ral U.S. Department of Defense JA N UA RY 1 4, 2 0 1 5 DoD Methodologies to Identify Improper Payments in the Military Health Benefits and Commercial Pay Programs

Report No. DODIG-2015-068 I nspec tor Ge ne ral U.S. Department of Defense JA N UA RY 1 4, 2 0 1 5 DoD Methodologies to Identify Improper Payments in the Military Health Benefits and Commercial Pay Programs

INSPECTOR GENERAL UNITED STATES POSTAL SERVICE

OFFICE OF INSPECTOR GENERAL UNITED STATES POSTAL SERVICE Bad Check Prevention and Collection Audit Report January 10, 2012 Report Number January 10, 2012 Bad Check Prevention and Collection Report Number

OFFICE OF INSPECTOR GENERAL UNITED STATES POSTAL SERVICE Bad Check Prevention and Collection Audit Report January 10, 2012 Report Number January 10, 2012 Bad Check Prevention and Collection Report Number

INSPECTOR GENERAL. Funnel Management Program. Management Advisory Report. March 20, 2013. Report Number MS-MA-13-001 OFFICE OF

OFFICE OF INSPECTOR GENERAL UNITED STATES POSTAL SERVICE Funnel Management Program Management Advisory Report March 20, 2013 Report Number March 20, 2013 Funnel Management Program Report Number BACKGROUND:

OFFICE OF INSPECTOR GENERAL UNITED STATES POSTAL SERVICE Funnel Management Program Management Advisory Report March 20, 2013 Report Number March 20, 2013 Funnel Management Program Report Number BACKGROUND:

INSPECTOR GENERAL UNITED STATES POSTAL SERVICE

OFFICE OF INSPECTOR GENERAL UNITED STATES POSTAL SERVICE Metro Post Same Day Delivery Pilot Management Advisory Report Report Number February 5, 2014 February 5, 2014 Metro Post Same Day Delivery Pilot

OFFICE OF INSPECTOR GENERAL UNITED STATES POSTAL SERVICE Metro Post Same Day Delivery Pilot Management Advisory Report Report Number February 5, 2014 February 5, 2014 Metro Post Same Day Delivery Pilot

AUDIT REPORT REPORT NUMBER 14 08. Information Technology Professional Services Oracle Software March 25, 2014

AUDIT REPORT REPORT NUMBER 14 08 Information Technology Professional Services Oracle Software March 25, 2014 Date March 25, 2014 To Chief Information Officer Director, Acquisition Services From Inspector

AUDIT REPORT REPORT NUMBER 14 08 Information Technology Professional Services Oracle Software March 25, 2014 Date March 25, 2014 To Chief Information Officer Director, Acquisition Services From Inspector

FOR PUBLIC RELEASE. Office of the Secretary. Commerce Should Strengthen Accountability and Internal Controls in Its Motor Pool Operations

U.S. DEPARTMENT OF COMMERCE Office of the Secretary Commerce Should Strengthen Accountability and Internal Controls in Its Motor Pool Operations FOR PUBLIC RELEASE Office of Audit and Evaluation UNITED

U.S. DEPARTMENT OF COMMERCE Office of the Secretary Commerce Should Strengthen Accountability and Internal Controls in Its Motor Pool Operations FOR PUBLIC RELEASE Office of Audit and Evaluation UNITED

ODIG-AUD (ATTN: Audit Suggestions) Department of Defense Inspector General 400 Army Navy Drive (Room 801) Arlington, VA 22202-4704

Department of Defense Inspector General 400 Army Navy Drive (Room 801) Arlington, VA 22202-4704") Additional Copies To obtain additional copies of this report, visit the Web site of the Department of Defense Inspector General at http://www.dodig.mil/audit/reports or contact the Secondary Reports Distribution

Additional Copies To obtain additional copies of this report, visit the Web site of the Department of Defense Inspector General at http://www.dodig.mil/audit/reports or contact the Secondary Reports Distribution

Audit of Management of the Government Purchase Card Program, Number A-13-04

Audit of Management of the Government Purchase Card Program, Number A-13-04 Smithsonian Needs to Improve Preventative Controls for the Purchase Card Program Office of the Inspector General Report Number

Audit of Management of the Government Purchase Card Program, Number A-13-04 Smithsonian Needs to Improve Preventative Controls for the Purchase Card Program Office of the Inspector General Report Number

State and District Monitoring of School Improvement Grant Contractors in California FINAL AUDIT REPORT

State and District Monitoring of School Improvement Grant Contractors in California FINAL AUDIT REPORT ED-OIG/A09O0009 March 2016 Our mission is to promote the efficiency, effectiveness, and integrity

State and District Monitoring of School Improvement Grant Contractors in California FINAL AUDIT REPORT ED-OIG/A09O0009 March 2016 Our mission is to promote the efficiency, effectiveness, and integrity

The Transportation Security Administration Does Not Properly Manage Its Airport Screening Equipment Maintenance Program

The Transportation Security Administration Does Not Properly Manage Its Airport Screening Equipment Maintenance Program May 6, 2015 OIG-15-86 HIGHLIGHTS The Transportation Security Administration Does

The Transportation Security Administration Does Not Properly Manage Its Airport Screening Equipment Maintenance Program May 6, 2015 OIG-15-86 HIGHLIGHTS The Transportation Security Administration Does

SUBJECT: Audit Report Disaster Recovery Capabilities of the Enterprise Payment Switch (Report Number IS-AR-09-009)

") July 30, 2009 ROSS PHILO VICE PRESIDENT, CHIEF INFORMATION OFFICER ROBERT J. PEDERSEN TREASURER SUBJECT: Audit Report Disaster Recovery Capabilities of the (Report Number ) This report presents the results

July 30, 2009 ROSS PHILO VICE PRESIDENT, CHIEF INFORMATION OFFICER ROBERT J. PEDERSEN TREASURER SUBJECT: Audit Report Disaster Recovery Capabilities of the (Report Number ) This report presents the results

SUBJECT: Audit Report Access Controls in the Enterprise Data Warehouse (Report Number IS-AR-09-004)

") February 20, 2009 GEORGE W. WRIGHT VICE PRESIDENT, INFORMATION TECHNOLOGY OPERATIONS SUBJECT: Audit Report Access Controls in the Enterprise Data Warehouse (Report Number ) This report presents the results

February 20, 2009 GEORGE W. WRIGHT VICE PRESIDENT, INFORMATION TECHNOLOGY OPERATIONS SUBJECT: Audit Report Access Controls in the Enterprise Data Warehouse (Report Number ) This report presents the results

Office of Inspector General Office of Audit

OFFICE OF WORKERS' COMPENSATION PROGRAMS Office of Inspector General Office of Audit OWCP'S EFFORTS TO DETECT AND PREVENT FECA IMPROPER PAYMENTS HAVE NOT ADDRESSED KNOWN WEAKNESSES Date Issued: February

OFFICE OF WORKERS' COMPENSATION PROGRAMS Office of Inspector General Office of Audit OWCP'S EFFORTS TO DETECT AND PREVENT FECA IMPROPER PAYMENTS HAVE NOT ADDRESSED KNOWN WEAKNESSES Date Issued: February

September 27, 2002 THOMAS G. DAY VICE PRESIDENT, ENGINEERING CHARLES E. BRAVO SENIOR VICE PRESIDENT, CHIEF TECHNOLOGY OFFICER

September 27, 2002 THOMAS G. DAY VICE PRESIDENT, ENGINEERING CHARLES E. BRAVO SENIOR VICE PRESIDENT, CHIEF TECHNOLOGY OFFICER JOHN A. RAPP SENIOR VICE PRESIDENT, OPERATIONS SUBJECT: Audit Report Integrated

September 27, 2002 THOMAS G. DAY VICE PRESIDENT, ENGINEERING CHARLES E. BRAVO SENIOR VICE PRESIDENT, CHIEF TECHNOLOGY OFFICER JOHN A. RAPP SENIOR VICE PRESIDENT, OPERATIONS SUBJECT: Audit Report Integrated

Office of Inspector General Evaluation of the Consumer Financial Protection Bureau s Consumer Response Unit

Office of Inspector General Evaluation of the Consumer Financial Protection Bureau s Consumer Response Unit Consumer Financial Protection Bureau September 2012 September 28, 2012 MEMORANDUM TO: FROM: SUBJECT:

Office of Inspector General Evaluation of the Consumer Financial Protection Bureau s Consumer Response Unit Consumer Financial Protection Bureau September 2012 September 28, 2012 MEMORANDUM TO: FROM: SUBJECT:

U.S. Chemical Safety and Hazard Investigation Board Should Determine the Cost Effectiveness of Performing Improper Payment Recovery Audits

U.S. ENVIRONMENTAL PROTECTION AGENCY OFFICE OF INSPECTOR GENERAL U.S. Chemical Safety and Hazard Investigation Board Should Determine the Cost Effectiveness of Performing Improper Payment Recovery Audits

U.S. ENVIRONMENTAL PROTECTION AGENCY OFFICE OF INSPECTOR GENERAL U.S. Chemical Safety and Hazard Investigation Board Should Determine the Cost Effectiveness of Performing Improper Payment Recovery Audits

MORE INCURRED-COST AUDITS OF DOT PROCUREMENT CONTRACTS SHOULD BE OBTAINED

MORE INCURRED-COST AUDITS OF DOT PROCUREMENT CONTRACTS SHOULD BE OBTAINED Office of the Secretary Report Number: FI-2007-064 Date Issued: August 29, 2007 U.S. Department of Transportation Office of the

MORE INCURRED-COST AUDITS OF DOT PROCUREMENT CONTRACTS SHOULD BE OBTAINED Office of the Secretary Report Number: FI-2007-064 Date Issued: August 29, 2007 U.S. Department of Transportation Office of the

GOVERNANCE: Enhanced Controls Needed To Avoid Duplicate Payments

GOVERNANCE: Enhanced Controls Needed To Avoid Duplicate Payments Audit Report OIG-A-2013-018 September 20, 2013 NATIONAL RAILROAD PASSENGER CORPORATION Office of Inspector General REPORT HIGHLIGHTS Why

GOVERNANCE: Enhanced Controls Needed To Avoid Duplicate Payments Audit Report OIG-A-2013-018 September 20, 2013 NATIONAL RAILROAD PASSENGER CORPORATION Office of Inspector General REPORT HIGHLIGHTS Why

Final Evaluation Report

U.S. OFFICE OF PERSONNEL MANAGEMENT OFFICE OF THE INSPECTOR GENERAL OFFICE OF EVALUATIONS AND INSPECTIONS Final Evaluation Report EVALUATION OF THE U.S. OFFICE OF PERSONNEL MANAGEMENT S OVERSIGHT OF THE

U.S. OFFICE OF PERSONNEL MANAGEMENT OFFICE OF THE INSPECTOR GENERAL OFFICE OF EVALUATIONS AND INSPECTIONS Final Evaluation Report EVALUATION OF THE U.S. OFFICE OF PERSONNEL MANAGEMENT S OVERSIGHT OF THE

Hotline Complaint Regarding the Defense Contract Audit Agency Examination of a Contractor s Subcontract Costs

Inspector General U.S. Department of Defense Report No. DODIG-2015-061 DECEMBER 23, 2014 Hotline Complaint Regarding the Defense Contract Audit Agency Examination of a Contractor s Subcontract Costs INTEGRITY

Inspector General U.S. Department of Defense Report No. DODIG-2015-061 DECEMBER 23, 2014 Hotline Complaint Regarding the Defense Contract Audit Agency Examination of a Contractor s Subcontract Costs INTEGRITY

March 2010 Report No. 10-025

John Keel, CPA State Auditor An Audit Report on The Department of Criminal Justice s Oversight of Selected Providers That Deliver Residential Services and Substance Abuse Treatment Programs Report No.

John Keel, CPA State Auditor An Audit Report on The Department of Criminal Justice s Oversight of Selected Providers That Deliver Residential Services and Substance Abuse Treatment Programs Report No.

Improvements Needed for Triannual Review Process at Norfolk Ship Support Activity

Report No. DODIG-2014-070 I nspec tor Ge ne ral U.S. Department of Defense M AY 6, 2 0 1 4 Improvements Needed for Triannual Review Process at Norfolk Ship Support Activity I N T E G R I T Y E F F I C

Report No. DODIG-2014-070 I nspec tor Ge ne ral U.S. Department of Defense M AY 6, 2 0 1 4 Improvements Needed for Triannual Review Process at Norfolk Ship Support Activity I N T E G R I T Y E F F I C

Audit Report. The Social Security Administration s Fiscal Year 2014 Government Purchase Card Program

Audit Report The Social Security Administration s Fiscal Year 2014 Government Purchase Card Program A-13-15-50038 May 2016 MEMORANDUM Date: May 10, 2016 Refer To: To: From: The Commissioner Inspector General

Audit Report The Social Security Administration s Fiscal Year 2014 Government Purchase Card Program A-13-15-50038 May 2016 MEMORANDUM Date: May 10, 2016 Refer To: To: From: The Commissioner Inspector General

U.S. SMALL BUSINESS ADMINISTRATION OFFICE OF INSPECTOR GENERAL WASHINGTON, D.C. 20416

U.S. SMALL BUSINESS ADMINISTRATION OFFICE OF INSPECTOR GENERAL WASHINGTON, D.C. 20416 AUDIT REPORT Issue Date: December 27, 2000 Number: 1-02 To: Robert J. Moffitt Associate Administrator, Office of Surety

U.S. SMALL BUSINESS ADMINISTRATION OFFICE OF INSPECTOR GENERAL WASHINGTON, D.C. 20416 AUDIT REPORT Issue Date: December 27, 2000 Number: 1-02 To: Robert J. Moffitt Associate Administrator, Office of Surety

ASSESSMENT REPORT 09 14 GPO WORKERS COMPENSATION PROGRAM. September 30, 2009

ASSESSMENT REPORT 09 14 GPO WORKERS COMPENSATION PROGRAM September 30, 2009 Date September 30, 2009 To Chief Management Officer Chief, Office of Workers Compensation From Assistant Inspector General for

ASSESSMENT REPORT 09 14 GPO WORKERS COMPENSATION PROGRAM September 30, 2009 Date September 30, 2009 To Chief Management Officer Chief, Office of Workers Compensation From Assistant Inspector General for

INSPECTOR GENERAL. Availability of Critical Applications. Audit Report. September 25, 2013. Report Number IT-AR-13-008 OFFICE OF

OFFICE OF INSPECTOR GENERAL UNITED STATES POSTAL SERVICE Availability of Critical Applications Audit Report September 25, 2013 Report Number September 25, 2013 Availability of Critical Applications Report

OFFICE OF INSPECTOR GENERAL UNITED STATES POSTAL SERVICE Availability of Critical Applications Audit Report September 25, 2013 Report Number September 25, 2013 Availability of Critical Applications Report

Allegations of the Defense Contract Management Agency s Performance in Administrating Selected Weapon Systems Contracts (D-2004-054)

") February 23, 2004 Acquisition Allegations of the Defense Contract Management Agency s Performance in Administrating Selected Weapon Systems Contracts (D-2004-054) This special version of the report has

February 23, 2004 Acquisition Allegations of the Defense Contract Management Agency s Performance in Administrating Selected Weapon Systems Contracts (D-2004-054) This special version of the report has

Office of Inspector General Pension Benefit Guaranty Corporation

Office of Inspector General Pension Benefit Guaranty Corporation RISK ADVISORY February 19, 2016 To: From: Subject: W. Thomas Reeder, Jr. Director Robert A. Westbrooks Inspector General Monitoring and

Office of Inspector General Pension Benefit Guaranty Corporation RISK ADVISORY February 19, 2016 To: From: Subject: W. Thomas Reeder, Jr. Director Robert A. Westbrooks Inspector General Monitoring and

Evaluation Report. The Social Security Administration s Cloud Computing Environment

Evaluation Report The Social Security Administration s Cloud Computing Environment A-14-14-24081 December 2014 MEMORANDUM Date: December 17, 2014 Refer To: To: From: The Commissioner Inspector General

Evaluation Report The Social Security Administration s Cloud Computing Environment A-14-14-24081 December 2014 MEMORANDUM Date: December 17, 2014 Refer To: To: From: The Commissioner Inspector General

VA Office of Inspector General

VA Office of Inspector General OFFICE OF AUDITS AND EVALUATIONS Veterans Benefits Administration Audit of Fiduciary Program s Management of Field Examinations June 1, 2015 14-01883-371 ACRONYMS BFFS CY

VA Office of Inspector General OFFICE OF AUDITS AND EVALUATIONS Veterans Benefits Administration Audit of Fiduciary Program s Management of Field Examinations June 1, 2015 14-01883-371 ACRONYMS BFFS CY

Audit of the Administrative and Loan Accounting Center, Austin, Texas

Department of Veterans Affairs Office of Inspector General Audit of the Administrative and Loan Accounting Center, Austin, Texas The Administrative and Loan Accounting Center needed to strengthen certain

Department of Veterans Affairs Office of Inspector General Audit of the Administrative and Loan Accounting Center, Austin, Texas The Administrative and Loan Accounting Center needed to strengthen certain

UNITED STATES DEPARTMENT OF EDUCATION OFFICE OF INSPECTOR GENERAL. December 10, 2015

UNITED STATES DEPARTMENT OF EDUCATION OFFICE OF INSPECTOR GENERAL AUDIT SERVICES Sacramento Audit Region Joe Xavier Director California Department of Rehabilitation 721 Capitol Mall Sacramento, CA 95814

UNITED STATES DEPARTMENT OF EDUCATION OFFICE OF INSPECTOR GENERAL AUDIT SERVICES Sacramento Audit Region Joe Xavier Director California Department of Rehabilitation 721 Capitol Mall Sacramento, CA 95814

GAO FEDERAL STUDENT LOAN PROGRAMS. Opportunities Exist to Improve Audit Requirements and Oversight Procedures. Report to Congressional Committees

GAO United States Government Accountability Office Report to Congressional Committees July 2010 FEDERAL STUDENT LOAN PROGRAMS Opportunities Exist to Improve Audit Requirements and Oversight Procedures

GAO United States Government Accountability Office Report to Congressional Committees July 2010 FEDERAL STUDENT LOAN PROGRAMS Opportunities Exist to Improve Audit Requirements and Oversight Procedures

Internal Control Review of the Government Purchase Card Program

Internal Control Review of the Government Purchase Card Program September 18, 2008 Report No. 440 UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 OFFICE OF INSPECTOR GENERAL September

Internal Control Review of the Government Purchase Card Program September 18, 2008 Report No. 440 UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 OFFICE OF INSPECTOR GENERAL September

How To Check If Nasa Can Protect Itself From Hackers

SEPTEMBER 16, 2010 AUDIT REPORT OFFICE OF AUDITS REVIEW OF NASA S MANAGEMENT AND OVERSIGHT OF ITS INFORMATION TECHNOLOGY SECURITY PROGRAM OFFICE OF INSPECTOR GENERAL National Aeronautics and Space Administration

SEPTEMBER 16, 2010 AUDIT REPORT OFFICE OF AUDITS REVIEW OF NASA S MANAGEMENT AND OVERSIGHT OF ITS INFORMATION TECHNOLOGY SECURITY PROGRAM OFFICE OF INSPECTOR GENERAL National Aeronautics and Space Administration

Status of Enterprise Resource Planning Systems Cost, Schedule, and Management Actions Taken to Address Prior Recommendations

Report No. DODIG-2013-111 I nspec tor Ge ne ral Department of Defense AUGUST 1, 2013 Status of Enterprise Resource Planning Systems Cost, Schedule, and Management Actions Taken to Address Prior s I N T

Report No. DODIG-2013-111 I nspec tor Ge ne ral Department of Defense AUGUST 1, 2013 Status of Enterprise Resource Planning Systems Cost, Schedule, and Management Actions Taken to Address Prior s I N T

OFFICE OF THE SECRETARY Internal Controls for Purchase Card Transactions Need to Be Strengthened

OFFICE OF THE SECRETARY Internal Controls for Purchase Card Transactions Need to Be Strengthened FINAL REPORT NO. OIG-13-025-A MAY 2, 2013 U.S. Department of Commerce Office of Inspector General Office

OFFICE OF THE SECRETARY Internal Controls for Purchase Card Transactions Need to Be Strengthened FINAL REPORT NO. OIG-13-025-A MAY 2, 2013 U.S. Department of Commerce Office of Inspector General Office

MEDICARE RECOVERY AUDIT CONTRACTORS AND CMS S ACTIONS TO ADDRESS IMPROPER PAYMENTS, REFERRALS OF POTENTIAL FRAUD, AND PERFORMANCE

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL MEDICARE RECOVERY AUDIT CONTRACTORS AND CMS S ACTIONS TO ADDRESS IMPROPER PAYMENTS, REFERRALS OF POTENTIAL FRAUD, AND PERFORMANCE Daniel

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL MEDICARE RECOVERY AUDIT CONTRACTORS AND CMS S ACTIONS TO ADDRESS IMPROPER PAYMENTS, REFERRALS OF POTENTIAL FRAUD, AND PERFORMANCE Daniel

Acquisition. Controls for the DoD Aviation Into-Plane Reimbursement Card (D-2003-003) October 3, 2002

October 3, 2002") October 3, 2002 Acquisition Controls for the DoD Aviation Into-Plane Reimbursement Card (D-2003-003) Department of Defense Office of the Inspector General Quality Integrity Accountability Report Documentation