GOVERNANCE: Enhanced Controls Needed To Avoid Duplicate Payments

|

|

|

- Norah Harper

- 9 years ago

- Views:

Transcription

1 GOVERNANCE: Enhanced Controls Needed To Avoid Duplicate Payments Audit Report OIG-A September 20, 2013

2 NATIONAL RAILROAD PASSENGER CORPORATION Office of Inspector General REPORT HIGHLIGHTS Why We Did This Review From October 2005 through June 2013, the Amtrak Finance department processed 1.9 million transactions valued at $14.1 billion. Given the large value of transactions, sound payment processes are necessary to avoid duplicate invoice payments. A duplicate invoice payment occurs when a vendor is paid two or more times for the same goods and services. Our objective was to determine whether the Finance department was paying duplicate invoices and to assess the effectiveness of its internal controls to detect duplicate invoices and avoid unnecessary payments. GOVERNANCE: Enhanced Controls Needed To Avoid Duplicate Payments Audit Report OIG A , September 20, 2013 What We Found Using the results of our analysis, Finance department staff recovered or is in the process of recovering about $1.9 million in duplicate invoice payments and is reviewing another $4.8 million in potential duplicate invoices we identified. Private sector best practice organizations establish payment processes controls that prevent and detect duplicate invoices prior to payment. Duplicate payments have three major negative impacts on organizations: the direct loss from overpaying for goods and services, the cost of resources to attempt overpayment recoveries if duplicate payments are subsequently identified, and the unnecessary reductions in cash balances even if overpayments are recovered. We reviewed 25 duplicate invoice payments valued at $533,988 to determine why they occurred. We identified four major causes: (1) Accounts Payable personnel processed known duplicate payments despite system warnings, (2) the payment system included multiple codes for the same vendor that could not be detected by the automated controls, (3) Accounts Payable personnel did not ensure invoice numbers were accurate, and (4) the payment process allows vendors to submit invoices to Accounts Payable and other offices. Additionally, the corporation s policy for processing purchase order payments is out of date because it does not provide information on the current purchasing system. We will provide the testing tools we developed for this review to the Finance department for its use. Corrective Actions In summary, we recommend that the Acting Chief Financial Officer: Apply cost and benefit criteria in seeking recovery of potential duplicate payments valued at about $4.8 million. For further information, contact 3. Dave Warren, Assistant Inspector Direct the Amtrak Controls group to assess the adequacy of General for Audits (202) vendor payment process controls and take corrective actions as appropriate. For the full report, see 5. room The Finance Department agreed with our recommendations and is taking steps to address them.

3 NATIONALRAILROAD PASSENGER CORPORATION Memorandum Office of Inspector General To: From: Dan Black Acting Chief Financial Officer David R. Warren Assistant Inspector General, Audits Date: September 20, 2013 Subject: (Audit Report OIG A ) This report provides the results of our audit of the Finance department s controls and process to prevent the payment of duplicate invoices. A duplicate invoice payment occurs when a vendor is paid two or more times for the same goods and services. Private sector best practice organizations establish payment processes controls that prevent and detect duplicate invoices prior to payment. Duplicate payments have three major negative impacts on organizations: (1) the direct loss from overpaying for goods and services, (2) the cost of resources to attempt overpayment recoveries if duplicate payments are subsequently identified, and (3) the unnecessary reductions in cash balances even if overpayments are recovered. Our objective was to determine whether the Finance department was paying duplicate invoices and to assess the effectiveness of its internal controls to detect duplicate invoices and avoid unnecessary payments. After discussion with officials and staff in your department, we analyzed invoice payment data using Audit Command Language (ACL), a specialized data analysis software tool. By using this tool, we were able to analyze 100 percent of invoices for a selected timeframe to identify potential duplicate invoices. We will provide the testing tools we developed for this review to the Finance department for its use. Finance department officials stated that the ACL tool will be very useful to them and provide better capabilities for detecting and preventing duplicate payments than their existing processes. They expressed interest in using the tool to detect duplicate invoices before payment. For details on our scope and methodology, see Appendix I. 10 G Street, NE, 3W-300, Washington, DC (202) / Fraud Hotline (800)

4 2 DUPLICATE PAYMENTS HAVE OCCURRED, BUT THE AMOUNTS HAVE DECLINED OVER THE LAST YEAR To determine the potential for duplicate invoices, we analyzed 100 percent of the Finance department s invoice payment data from October 2005 through June We identified potential duplicate invoices of about $7.5 million. 2 The potential duplicates we identified contained some false positives. As part of our methodology during our work, we shared our results with personnel from Finance s Accounts Payable department (AP) to facilitate the identification of false positives and the recovery of overpayments. As of the date of this report, AP personnel recovered or are in the process of recovering about $1.9 million in duplicate invoice payments based on their review of about $2.7 million of potential duplicates. The remaining $4.8 million in potential duplicate invoices are being reviewed by AP. Data from October 2005 through June 2013 shows a significant increase in duplicate invoices leading up to, during, and after the June 2011 SAP implementation. 3 The data also showed that duplicate invoices are on the decline. The chart below shows the monthly dollar value of the potential duplicate invoices we identified. $700,000 $600,000 $500,000 $400,000 $300,000 $200,000 $100,000 $0 Chart: Monthly Potential Duplicate Invoice Totals Oct Dec Feb Apr Jun Aug Oct Dec Feb Apr Jun Aug Oct Dec Feb Apr Jun Aug Oct Dec Feb Apr Jun Aug Oct Dec Feb Apr Jun Aug Oct Dec Feb Apr Jun Aug Oct Dec Feb Apr Jun Aug Oct Dec Feb Apr Jun Source: Amtrak OIG analysis of Finance department invoice data. 1 Our analysis included invoices paid and invoices due for payment. 2 This total represents the upper limit of potential overpayments; the initial payments are not included. 3 Amtrak implemented the SAP system in June SAP software can process enterprise wide data from various business areas such as finance, procurement, payroll, and sales distribution.

5 3 We analyzed invoice data using four selected time periods, with the following results: From June 2011 through October 2012 (the first 17 months after SAP implementation) we identified potential duplicate invoices totaling $2.9 million (this total is 0.09 percent of all payment transactions in this period). We provided these results to AP on November 29, 2012 and January 24, Of the 1,075 potential duplicate invoices we identified, AP officials reviewed 76 potential duplicate invoices with a total value of $2.2 million. Their reviews confirmed that duplicate payments were made, and AP staff have initiated action to recover about $1.8 million related to those invoices. They determined that the remaining invoices totaling $0.4 million were not duplicates. From November 2012 through June 2013 we identified potential duplicate invoices totaling $526,000 (this total is 0.04 percent of all payment transactions in this period). We provided these results on a monthly basis to AP, starting in March AP has recovered or is in the process of recovering about $160,000 in overpayments based on its review of this data. They have determined that the remaining invoices totaling $366,000 were not duplicates. From October 2005 through May we identified potential duplicate invoices totaling $3.7 million that were processed using the corporation s former payment system Amtrak s Accounting, Materials, and Purchasing System (AAMPS). 5 We provided the detailed results of this analysis on June 12, 2013; AP personnel are reviewing this data for recoverable payments. From October 2005 through June 2013 we identified potential duplicate invoices totaling $420,000 for invoices processed in AAMPS (from October 2005 through May 2011) and then in SAP (from June 2011). These dates overlap the prior tests because this analysis looked at potential duplicate invoices where one invoice was paid in AAMPS and the potential duplicate invoice was paid in SAP. The AAMPS software had an automated duplicate invoice check feature to catch and stop invoices that were presented for payment a second time in SAP. Several of the potential duplicates we identified had also been identified by the AAMPS software feature as duplicates. These duplicate invoices should have been voided in SAP, but 4 We chose this 68 month time period because it represented 96.4 percent of transactions in this system. 5 AAMPS was Amtrak s legacy procurement system. Prior to implementing SAP in June 2011, Amtrak used AAMPS to request, order, and pay for materials, supplies, and services.

6 4 we found that they were paid. We provided the results of this analysis to AP on June 12, AP personnel are reviewing this data for recoverable amounts and to determine why the duplicate invoices were paid. CONTROLS AND PROCESSES TO PREVENT DUPLICATE PAYMENTS CAN BE FURTHER IMPROVED We reviewed 25 duplicate invoice payments valued at $533,988 for detailed review to determine why they occurred. We identified four major causes: 6 (1) AP personnel processed known duplicate payments despite system warnings, (2) the payment system included multiple codes for the same vendor that could not be detected by the automated controls, (3) AP personnel did not ensure SAP invoice numbers matched vendor invoices, and (4) the payment process allows vendors to submit invoices to AP and other offices. Those offices are allowed to submit invoices to AP, thus creating the potential for duplicate payments. Given the number of duplicate payments we identified, we recognize that there are likely other causes. Additionally, we noted that the corporation s policy for processing purchase order payments does not contain guidance on the current SAP system. Current Automated Controls and Causes of Duplicate Payments The Finance department identifies duplicate invoices by using the automated Vendor Invoice Management System a component of SAP. 7 When invoices are submitted, this system performs three analyses to identify potential duplicates. When the system identifies a potential duplicate invoice, it stops the payment process and sends a message alerting AP personnel. 8 AP managers and other company staff are responsible for researching these invoices to determine if payment should be made. We developed a flowchart of the corporation s payment process and have included it as Appendix II. Notwithstanding these controls, our review of 25 duplicate payments showed they occurred for the following reasons: 6 Some transactions had more than one cause. 7 AP uses the Vendor Invoice Management System to manage invoice processes and automate invoice routing and sorting. The System contains a feature that identifies duplicate invoices that are submitted for payment. 8 The system runs tests based on the exact match of invoice number, invoice date, invoice amount, and vendor number.

AP personnel processed known duplicate payments despite system warnings, (2) the payment system included multiple codes for the same vendor that could not be")

7 5 Personnel overrode system warnings. In 12 instances totaling $261,863, the duplicate payments occurred because personnel overrode system warnings and processed the duplicate payments. According to an AP official, these transactions were processed due to human error. When the payment system identifies a potential duplicate, it stops the payment processing and notifies AP personnel to check for suspected duplicate. This notification is routed to authorized personnel who are responsible for researching and resolving the warning. We identified several duplicate payments in which the invoice attributes demonstrated that they were duplicates. In these cases, all four attribute terms were consistent: the invoice number, invoice amount, invoice date, and vendor code. Authorized personnel overrode the system s stop payment features and approved these invoices for payment. Payment system includes multiple codes for the same vendor. In six instances totaling $127,371, the duplicate payments were made because the system contained duplicate vendor codes. The vendor master should contain a single code for each vendor. In December 2012, we determined that the vendor master file had 27,442 duplicate vendor codes. An AP official stated that duplicate vendor codes exist for a variety of reasons, such as personnel adding additional vendor codes because they could not find the original, and issues with the transition to the new financial system SAP. The duplicate codes allow duplicate invoices to go undetected by the system s automatic duplicate invoice detection tests. When the vendor code for a duplicate invoice is different, the system identifies it as a separate invoice and not a duplicate. In these instances, since the system did not send an alert, personnel approved these duplicate invoices for payment. In two of these six instances, the duplicate payment was made through a payment request. 9 Amtrak policy Request for Payment (October 6, 2010) establishes the requirements for payment requests and includes a section on preventing duplicate payments. 10 However, the prevention method relies on the Vendor Invoice Management System to identify duplicate payment requests. As noted above, this system contains duplicate codes for some vendors which could allow duplicate invoices to go undetected. This policy was updated on April 3, 2013, but the section on duplicate payment prevention was unchanged. 9 A payment request is a reimbursement tool for Amtrak obligations not covered by purchase order, employee business expense report reimbursements, or purchase card guidelines. Amtrak policy restricts the use of payment requests to non recurring purchases of goods and services under $5, While is the prior version of current Amtrak policy, this policy was in effect during the processing of the transactions we reviewed.

8 6 Personnel did not ensure SAP invoice numbers matched vendor invoices. In seven instances totaling $144,754, the duplicate payments occurred because the invoice number in SAP did not match the number on the vendor invoice. These vendor invoices had the identical invoice amount, invoice date, invoice number, and vendor code; however, personnel altered the invoice number during processing. Typically, such changes to the invoice number included or excluded non alphanumeric characters (for example, hyphens) or added additional characters to the invoice number. According to an AP official, its standard practice is to remove non alphanumeric characters from invoice Figure: Examples of Subtle Invoice Number Differences AMT vs. AMT A vs AMTK1400 vs AMT1400 Source: Amtrak s SAP Payment Processing System numbers when processing payments. This practice was carried over from the prior financial system, which was unable to recognize such characters. However, the new system recognizes such subtle differences and relies on the accuracy of the invoice number when conducting duplicate invoice detection tests. Therefore, when personnel altered the invoice number, the system s duplicate tests were defeated. Sources other than AP presented invoices for payment. In 14 cases totaling $265,440, the personnel who received the goods and services submitted duplicate invoices to AP for payment. These individuals received invoices directly from the vendor and submitted them to AP for payment. In these cases, AP also received a separate invoice for these same goods and services from the vendor. This caused the invoice to be entered into the payment processing system two or more times. Best practice organizations require vendors to submit invoices only to the accounts payable department. This practice ensures a single point of accountability for receiving, tracking, approving, and paying invoices. The corporation s practice of allowing vendors to submit invoices to offices other than AP and allowing those offices to submit them to AP has resulted in some duplicate payments. Policy Requires Updating. One of the corporation s policies for payment processing needs to be updated. Amtrak policy MM 5.13 Receipt of Amtrak Purchases covers payments for goods and services against a purchase order (19 of the 25 payments we reviewed were made in this manner). However, the policy applies to the former purchasing system AAMPS and has not been updated to reflect the new SAP system s processes. We also noted that the policy does not contain a section on preventing duplicate invoice payments.

or added additional characters to the invoice number.")

9 7 CONCLUSIONS AND RECOMMENDATIONS Weaknesses in the Finance department s payments control processes have, over time, allowed duplicate payments to be made to vendors. These payments have resulted in direct losses from overpayments, caused additional resources to be expended to recover them, and caused unnecessary reductions in cash balances. The amount of overpayments increased significantly leading up to, during, and after the SAP system implementation. Since July 2012, and as the SAP system has stabilized, to the Finance department s credit, the number of potential duplicate invoices has decreased. Also, overpayment recoveries have been made and others are being pursued. Continuation of these positive trends is paramount to detecting, preventing, and recovering duplicate payments. To help sustain those efforts, we recommend that the Acting Chief Financial Officer take the following actions: 1) Use cost and benefit criteria such as high dollar value payments and the length of time since the payments were made, in seeking recovery of the remaining $4.8 million in potential duplicate payments identified in this report. 2) Direct the Amtrak Controls group to assess the adequacy of vendor payment process controls and take corrective actions as appropriate. The group s assessment, at a minimum, should address issues related to: personnel overriding system warnings that identify duplicate payments duplicate vendor records in the vendor master file personnel altering invoice numbers when processing payments the practice of allowing invoices to be submitted to offices other than AP out of date payment policies and procedures for detecting, researching, and preventing duplicate payments routine monitoring of payment controls using data analytics similar to those developed for this review MANAGEMENT COMMENTS AND OIG ANALYSIS In his response to the draft report (see Appendix III), the Acting Chief Financial Officer agreed with our recommendations and provided corrective actions and implementation dates to address them. The proposed corrective actions address the intent of our recommendations.

10 8 Appendix I SCOPE AND METHODOLOGY This report provides the results of our audit to assess the corporation s controls and processes to prevent duplicate payments of invoices. Our objective was to assess the effectiveness of internal controls and business processes to identify duplicate invoices and unnecessary payments. We initiated data analysis work in June 2012 and field work in January This audit was performed by staff in our Washington, DC, and Philadelphia offices and concluded in August We conducted this performance audit in accordance with generally accepted government auditing standards. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions based on our audit objective. We believe that the evidence obtained provides a reasonable basis for our findings and conclusions based on our audit objectives. We requested documentation and interviewed staff members in the Audit Compliance Control, Procurement, and AP departments to understand business processes, key controls, and risk areas. Based on interviews with AP staff, we also created a flow chart of the invoice payment process to identify risk and control point weaknesses. The flowchart can be found in Appendix II. To Identify Potential Duplicate Invoices To identify potential duplicate invoices, we performed various data analytic tests on Amtrak s invoice data and analyzed the vendor master file. To perform this analysis, we employed ACL data analytics software. Duplicate Invoices We obtained all available invoice data from the prior and current corporate accounts payable systems, AAMPS and SAP. We imported that data into ACL and performed a series of data analytic tests to identify duplicate invoices.

11 9 Before June 2011, Amtrak used AAMPS for 1.3 million transactions totaling $9.2 billion. To identify duplicate invoices in AAMPS and also for invoices paid in AAMPS and then duplicated in SAP, we used the following test criteria: invoices that had the same computed invoice numbers 11, invoice dates, and invoice amounts We performed the following tests on invoices processed in SAP (invoices paid from June 2011 through June 2013: 552,000 transactions valued at $4.9 billion): invoices that had the same vendor numbers, computed invoice numbers, invoice dates, and invoice amounts invoices that had the same computed vendor numbers, computed invoice numbers, invoice dates, and invoice amounts invoices that had the same computed invoice numbers, invoice dates, and invoice amounts invoices that had the same bank account numbers, computed invoice numbers, invoice dates and invoice amounts We performed these tests in six increments: from June 2011 through October 2012, from November 2012 through February 2013, March 2013, April 2013, May 2013, and June Duplicate Vendor Records We also performed analysis on the vendor master file related to duplicate invoices. Our analysis included obtaining the vendor master data from SAP (42,978 vendors) as of December 31, 2012, and using the ACL tool to identify duplicate vendors who have the same computed vendor name 12, address, phone number, bank account numbers, tax identification number, or alternate payee identification number Computed invoice number is the vendor invoice number with just the numbers and no special characters or alphabets. 12 Computed vendor name is the standardized vendor name using the following transformations: (1) converting text to upper case, (2) removing leading and trailing blanks, and (3) replacing variations of words (for example, laboratory, laboratories, and labs) with a common standard. 13 Alternate payee identification number in SAP s vendor master record allows a payment to a vendor other than the one to which the invoice was posted.

: invoices that had the same vendor numbers, computed invoice numbers, invoice dates, and invoice amounts invoices that had the same computed vendor numbers, computed invoice numbers,")

12 10 To Identify Why Duplicate Payments Occurred To perform a detailed review, we used ACL to extract a random sample of duplicate transaction sets. These transactions were sampled from the June 2011 through October 2012 increment of potential duplicate invoices. We selected transactions with dollar values over $5,000 because they present the highest financial risk. From the random sample, we reviewed 25 potential duplicate invoice sets in detail 52 total transactions. 14 To review the transactions, we downloaded and analyzed SAP, Ariba, and bank reconciliation documents. We analyzed these documents to determine whether the transaction sets were duplicates and to verify invoice payment. We interviewed Amtrak personnel to determine the cause for the duplicate invoice payment. While this report identifies the causes for the transactions we reviewed, we recognize that other causes may be associated with the duplicate payment transactions we did not review. Internal Controls In conducting the audit, we assessed the adequacy of Amtrak s internal controls for detecting and preventing payments of duplicate invoices. We interviewed officials and staff from Audit Compliance Control, Procurement, and AP; reviewed written policies and procedures; traced accounts payable transactions; and obtained documentation to support these transactions. We also developed a flow chart of the payment process to identify and assess its control points it is included as Appendix II. This report identifies weaknesses in controls and business processes for which we have made recommendations. Use of Computer-Processed Data To achieve our objective, we used computer processed data contained in Amtrak s electronic records and accounts payable system, as previously described. We were unable to validate the AAMPS data because the system has been discontinued. To verify the accuracy of the SAP data, we downloaded and reviewed SAP, Ariba, and bank reconciliation documents used in support for our sampled transactions and found no exceptions. Based on our detailed analysis, we determined the data to be reliable. 14 One sampled duplicate invoice set contained four transactions.

13 11 Prior Reports We reviewed the following audit reports for potential relevance to our work: Amtrak OIG Report No , etrax Expense Reports FY 2003, 3/31/2005 identified a high degree of non compliance with Amtrak business travel policies and etrax instructions for the expense reports that were reviewed. The etrax system had been placed into production during fiscal year Amtrak OIG Report No , etrax Payment Requests FY 2003, 11/03/2004 found that payment requests were being used to procure services and rentals not permitted by corporate procedures, original supporting documentation was not being retained, and payment requests were improperly approved. The report cited the lack of a procedure defining the duties and responsibilities of the payment approver for reviewing a payment request prior to approval as an internal control weakness.

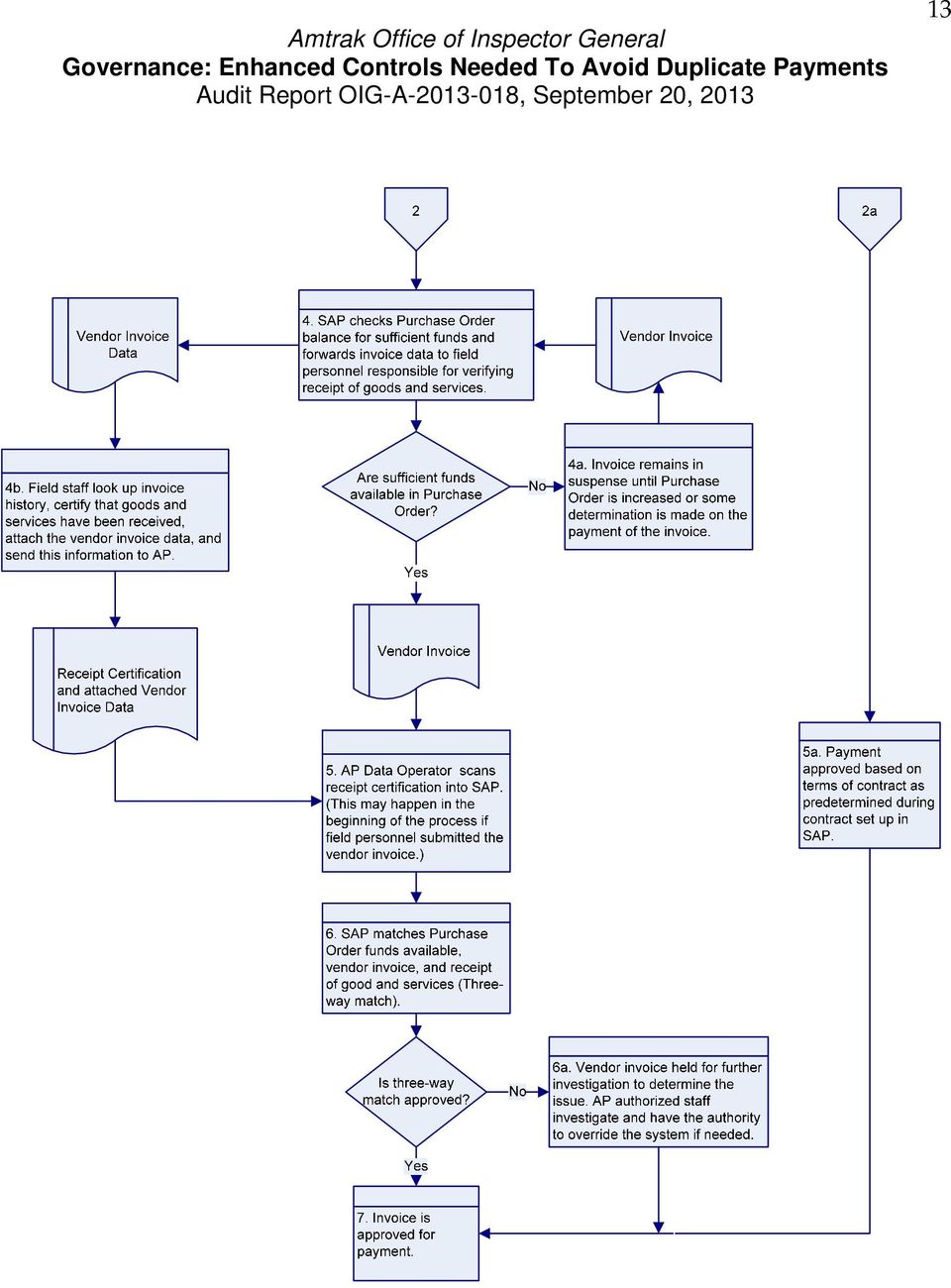

14 12 Appendix II FLOW CHART OF PAYMENT PROCESS

15 13

16 14 Appendix III

17 15

18 16 Appendix IV ABBREVIATIONS AAMPS ACL AP etrax Amtrak s Accounting, Materials, and Purchasing System Audit Command Language Accounts Payable Electronic Transaction Express

19 17 Appendix V OIG TEAM MEMBERS Vipul Doshi, Senior Director, Audits Matthew Simber, Senior Director, Audits Cheryl Chambers, Audit Manager Vijay Chheda, Audit Manager Ben Davani, Senior Auditor, IT John Flynn, Senior Auditor Mark Scheffler, Senior Auditor Asha Sriramulu, Senior Auditor, IT Ashish Tendulkar, Senior Auditor, IT Janene Haddix, Consultant Jim Tarantino, Consultant Kim Tolliver, Consultant

20 18 OIG MISSION AND CONTACT INFORMATION Amtrak OIG s Mission The Amtrak OIG s mission is to provide independent, objective oversight of Amtrak s programs and operations through audits, inspections, evaluations, and investigations focused on recommending improvements to Amtrak s economy, efficiency, and effectiveness; preventing and detecting fraud, waste, and abuse; and providing Congress, Amtrak management, and Amtrak s Board of Directors with timely information about problems and deficiencies relating to Amtrak s programs and operations. Obtaining Copies of OIG Reports and Testimony To Report Fraud, Waste, and Abuse Available at our website: Report suspicious or illegal activities to the OIG Hotline (you can remain anonymous): Web: Phone: (800) Congressional and Public Relations David R. Warren Assistant Inspector General, Audits Mail: Amtrak OIG 10 G Street, N.E., 3W-300 Washington, D.C Phone: (202) [email protected]

INFORMATION TECHNOLOGY: Reservation System Infrastructure Updated, but Future System Sustainability Remains an Issue

INFORMATION TECHNOLOGY: Reservation System Infrastructure Updated, but Future System Audit Report OIG-A-2015-010 May 19, 2015 This page intentionally left blank. NATIONAL RAILROAD PASSENGER CORPORATION

INFORMATION TECHNOLOGY: Reservation System Infrastructure Updated, but Future System Audit Report OIG-A-2015-010 May 19, 2015 This page intentionally left blank. NATIONAL RAILROAD PASSENGER CORPORATION

ACQUISITION AND PROCUREMENT: NEW JERSEY HIGH-SPEED RAIL IMPROVEMENT PROGRAM HAS COST AND SCHEDULE RISKS

ACQUISITION AND PROCUREMENT: NEW JERSEY HIGH-SPEED RAIL IMPROVEMENT PROGRAM HAS COST AND SCHEDULE RISKS Audit Report OIG-A-2015-012 June 17, 2015 DRAFT REPORT Page intentionally left blank NATIONAL RAILROAD

ACQUISITION AND PROCUREMENT: NEW JERSEY HIGH-SPEED RAIL IMPROVEMENT PROGRAM HAS COST AND SCHEDULE RISKS Audit Report OIG-A-2015-012 June 17, 2015 DRAFT REPORT Page intentionally left blank NATIONAL RAILROAD

REAL PROPERTY MANAGEMENT: Applying Best Practices Can Improve Real Property Inventory Management Information

REAL PROPERTY MANAGEMENT: Applying Best Practices Can Improve Real Property Inventory Management Information Report No. OIG-A-2013-015 June 12, 2013 NATIONAL RAILROAD PASSENGER CORPORATION The Inspector

REAL PROPERTY MANAGEMENT: Applying Best Practices Can Improve Real Property Inventory Management Information Report No. OIG-A-2013-015 June 12, 2013 NATIONAL RAILROAD PASSENGER CORPORATION The Inspector

SAFETY AND SECURITY: Opportunities to Improve Controls Over Police Department Workforce Planning

SAFETY AND SECURITY: Opportunities to Improve Controls Over Police Department Audit Report OIG-A-2015-006 February 12, 2015 2 OPPORTUNITIES EXIST TO IMPROVE WORKFORCE PLANNING PRACTICES AND RELATED SAFETY

SAFETY AND SECURITY: Opportunities to Improve Controls Over Police Department Audit Report OIG-A-2015-006 February 12, 2015 2 OPPORTUNITIES EXIST TO IMPROVE WORKFORCE PLANNING PRACTICES AND RELATED SAFETY

Navy s Contract/Vendor Pay Process Was Not Auditable

Inspector General U.S. Department of Defense Report No. DODIG-2015-142 JULY 1, 2015 Navy s Contract/Vendor Pay Process Was Not Auditable INTEGRITY EFFICIENCY ACCOUNTABILITY EXCELLENCE INTEGRITY EFFICIENCY

Inspector General U.S. Department of Defense Report No. DODIG-2015-142 JULY 1, 2015 Navy s Contract/Vendor Pay Process Was Not Auditable INTEGRITY EFFICIENCY ACCOUNTABILITY EXCELLENCE INTEGRITY EFFICIENCY

Department of Homeland Security Office of Inspector General. Audit of Application Controls for FEMA's Individual Assistance Payment Application

Department of Homeland Security Office of Inspector General Audit of Application Controls for FEMA's Individual Assistance Payment Application OIG-09-104 September 2009 Table of Contents Objectives,

Department of Homeland Security Office of Inspector General Audit of Application Controls for FEMA's Individual Assistance Payment Application OIG-09-104 September 2009 Table of Contents Objectives,

The Federal Railroad Retirement Board (RRB) and Data Analytics

and Data Analytics") Exploring Innovation Leads to Data Analytics Phase I February 14, 2013 OFFICE OF INSPECTOR GENERAL RAILROAD RETIREMENT BOARD INTRODUCTION In response to the Federal government s mandate to become more

Exploring Innovation Leads to Data Analytics Phase I February 14, 2013 OFFICE OF INSPECTOR GENERAL RAILROAD RETIREMENT BOARD INTRODUCTION In response to the Federal government s mandate to become more

Strategic Asset Management Program Controls Design Is Generally Sound, But Improvements Can Be Made. Final Audit Report No. 105-2010.

Strategic Asset Management Program Controls Design Is Generally Sound, But Final Audit January 14, 2011 Audit Report Issued By: NATIONAL RAILROAD PASSENGER CORPORATION OFFICE OF INSPECTOR GENERAL 10 G

Strategic Asset Management Program Controls Design Is Generally Sound, But Final Audit January 14, 2011 Audit Report Issued By: NATIONAL RAILROAD PASSENGER CORPORATION OFFICE OF INSPECTOR GENERAL 10 G

AGA Kansas City Chapter Data Analytics & Continuous Monitoring

AGA Kansas City Chapter Data Analytics & Continuous Monitoring Agenda Market Overview & Drivers for Change Key challenges that organizations face Data Analytics What is data analytics and how can it help

AGA Kansas City Chapter Data Analytics & Continuous Monitoring Agenda Market Overview & Drivers for Change Key challenges that organizations face Data Analytics What is data analytics and how can it help

Performance Audit City s Payment Process

Performance Audit City s Payment Process January 2013 City Auditor s Office City of Kansas City, Missouri 18-2011 Office of the City Auditor 21 st Floor, City Hall 414 East 12 th Street (816) 513-3300

Performance Audit City s Payment Process January 2013 City Auditor s Office City of Kansas City, Missouri 18-2011 Office of the City Auditor 21 st Floor, City Hall 414 East 12 th Street (816) 513-3300

U.S. Chemical Safety and Hazard Investigation Board Should Determine the Cost Effectiveness of Performing Improper Payment Recovery Audits

U.S. ENVIRONMENTAL PROTECTION AGENCY OFFICE OF INSPECTOR GENERAL U.S. Chemical Safety and Hazard Investigation Board Should Determine the Cost Effectiveness of Performing Improper Payment Recovery Audits

U.S. ENVIRONMENTAL PROTECTION AGENCY OFFICE OF INSPECTOR GENERAL U.S. Chemical Safety and Hazard Investigation Board Should Determine the Cost Effectiveness of Performing Improper Payment Recovery Audits

Table of Contents. Transmittal Letter... 1. Executive Summary... 2-3. Background... 4-5. Objectives and Approach... 6. Issues Matrix...

Internal Audit Committee of Brevard County, Florida Internal Audit Review of Accounts Payable Prepared By: Internal Auditors of Brevard County September 22, 2010 Table of Contents Transmittal Letter...

Internal Audit Committee of Brevard County, Florida Internal Audit Review of Accounts Payable Prepared By: Internal Auditors of Brevard County September 22, 2010 Table of Contents Transmittal Letter...

City of Berkeley. Accounts Payable Audit

City of Berkeley Accounts Payable Audit Prepared by: Ann-Marie Hogan, City Auditor, CIA, CGAP Teresa Berkeley-Simmons, Audit Manager, CIA, CGAP Frank Marietti, Senior Auditor, CIA, CGAP Presented to Council

City of Berkeley Accounts Payable Audit Prepared by: Ann-Marie Hogan, City Auditor, CIA, CGAP Teresa Berkeley-Simmons, Audit Manager, CIA, CGAP Frank Marietti, Senior Auditor, CIA, CGAP Presented to Council

a GAO-02-635 GAO DOD CONTRACT MANAGEMENT Overpayments Continue and Management and Accounting Issues Remain

GAO United States General Accounting Office Report to the Chairman, Committee on Government Reform, House of Representatives May 2002 DOD CONTRACT MANAGEMENT Overpayments Continue and Management and Accounting

GAO United States General Accounting Office Report to the Chairman, Committee on Government Reform, House of Representatives May 2002 DOD CONTRACT MANAGEMENT Overpayments Continue and Management and Accounting

ASSESSMENT REPORT 09 14 GPO WORKERS COMPENSATION PROGRAM. September 30, 2009

ASSESSMENT REPORT 09 14 GPO WORKERS COMPENSATION PROGRAM September 30, 2009 Date September 30, 2009 To Chief Management Officer Chief, Office of Workers Compensation From Assistant Inspector General for

ASSESSMENT REPORT 09 14 GPO WORKERS COMPENSATION PROGRAM September 30, 2009 Date September 30, 2009 To Chief Management Officer Chief, Office of Workers Compensation From Assistant Inspector General for

THE FRAUD PREVENTION SYSTEM IDENTIFIED MILLIONS IN MEDICARE SAVINGS, BUT THE DEPARTMENT COULD STRENGTHEN SAVINGS DATA

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL THE FRAUD PREVENTION SYSTEM IDENTIFIED MILLIONS IN MEDICARE SAVINGS, BUT THE DEPARTMENT COULD STRENGTHEN SAVINGS DATA BY IMPROVING ITS

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL THE FRAUD PREVENTION SYSTEM IDENTIFIED MILLIONS IN MEDICARE SAVINGS, BUT THE DEPARTMENT COULD STRENGTHEN SAVINGS DATA BY IMPROVING ITS

DoD Methodologies to Identify Improper Payments in the Military Health Benefits and Commercial Pay Programs Need Improvement

Report No. DODIG-2015-068 I nspec tor Ge ne ral U.S. Department of Defense JA N UA RY 1 4, 2 0 1 5 DoD Methodologies to Identify Improper Payments in the Military Health Benefits and Commercial Pay Programs

Report No. DODIG-2015-068 I nspec tor Ge ne ral U.S. Department of Defense JA N UA RY 1 4, 2 0 1 5 DoD Methodologies to Identify Improper Payments in the Military Health Benefits and Commercial Pay Programs

Status of Enterprise Resource Planning Systems Cost, Schedule, and Management Actions Taken to Address Prior Recommendations

Report No. DODIG-2013-111 I nspec tor Ge ne ral Department of Defense AUGUST 1, 2013 Status of Enterprise Resource Planning Systems Cost, Schedule, and Management Actions Taken to Address Prior s I N T

Report No. DODIG-2013-111 I nspec tor Ge ne ral Department of Defense AUGUST 1, 2013 Status of Enterprise Resource Planning Systems Cost, Schedule, and Management Actions Taken to Address Prior s I N T

ACCOUNTS PAYABLE AUDIT RECOVERING LOST DOLLARS AT NO COST

ACCOUNTS PAYABLE AUDIT RECOVERING LOST DOLLARS AT NO COST 1 Our Objective To assist organizations in finding lost thousands of dollars in profits through duplicate payments, duplicate billings, overpayments,

ACCOUNTS PAYABLE AUDIT RECOVERING LOST DOLLARS AT NO COST 1 Our Objective To assist organizations in finding lost thousands of dollars in profits through duplicate payments, duplicate billings, overpayments,

Allegations of the Defense Contract Management Agency s Performance in Administrating Selected Weapon Systems Contracts (D-2004-054)

") February 23, 2004 Acquisition Allegations of the Defense Contract Management Agency s Performance in Administrating Selected Weapon Systems Contracts (D-2004-054) This special version of the report has

February 23, 2004 Acquisition Allegations of the Defense Contract Management Agency s Performance in Administrating Selected Weapon Systems Contracts (D-2004-054) This special version of the report has

Five-Year Strategic Plan

U.S. Department of Education Office of Inspector General Five-Year Strategic Plan Fiscal Years 2014 2018 Promoting the efficiency, effectiveness, and integrity of the Department s programs and operations

U.S. Department of Education Office of Inspector General Five-Year Strategic Plan Fiscal Years 2014 2018 Promoting the efficiency, effectiveness, and integrity of the Department s programs and operations

Evaluation of Defense Contract Management Agency Actions on Reported DoD Contractor Business System Deficiencies

Inspector General U.S. Department of Defense Report No. DODIG-2016-001 OCTOBER 1, 2015 Evaluation of Defense Contract Management Agency Actions on Reported DoD Contractor Business System Deficiencies INTEGRITY

Inspector General U.S. Department of Defense Report No. DODIG-2016-001 OCTOBER 1, 2015 Evaluation of Defense Contract Management Agency Actions on Reported DoD Contractor Business System Deficiencies INTEGRITY

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION Direct Debit Installment Agreement Procedures Addressing Taxpayer Defaults Can Be Improved February 5, 2016 Reference Number: 2016-30-011 This report has

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION Direct Debit Installment Agreement Procedures Addressing Taxpayer Defaults Can Be Improved February 5, 2016 Reference Number: 2016-30-011 This report has

U.S. Department of Energy Office of Inspector General Office of Audits and Inspections

U.S. Department of Energy Office of Inspector General Office of Audits and Inspections Audit Report The Department of Energy's Weatherization Assistance Program Funded under the American Recovery and Reinvestment

U.S. Department of Energy Office of Inspector General Office of Audits and Inspections Audit Report The Department of Energy's Weatherization Assistance Program Funded under the American Recovery and Reinvestment

AUDIT REPORT 12-1 8. Audit of Controls over GPO s Fleet Credit Card Program. September 28, 2012

AUDIT REPORT 12-1 8 Audit of Controls over GPO s Fleet Credit Card Program September 28, 2012 Date September 28, 2012 To Director, Acquisition Services From Inspector General Subject Audit Report Audit

AUDIT REPORT 12-1 8 Audit of Controls over GPO s Fleet Credit Card Program September 28, 2012 Date September 28, 2012 To Director, Acquisition Services From Inspector General Subject Audit Report Audit

Funding Invoices to Expedite the Closure of Contracts Before Transitioning to a New DoD Payment System (D-2002-076)

") March 29, 2002 Financial Management Funding Invoices to Expedite the Closure of Contracts Before Transitioning to a New DoD Payment System (D-2002-076) Department of Defense Office of the Inspector General

March 29, 2002 Financial Management Funding Invoices to Expedite the Closure of Contracts Before Transitioning to a New DoD Payment System (D-2002-076) Department of Defense Office of the Inspector General

Department of Homeland Security. U.S. Coast Guard s Maritime Patrol Aircraft

Department of Homeland Security OIG-12-73 (Revised) August 2012 August 31, 2012 Office of Inspector General U.S. Department of Homeland Security Washington, DC 20528 August 31, 2012 Preface The Department

Department of Homeland Security OIG-12-73 (Revised) August 2012 August 31, 2012 Office of Inspector General U.S. Department of Homeland Security Washington, DC 20528 August 31, 2012 Preface The Department

Audit of the Administrative and Loan Accounting Center, Austin, Texas

Department of Veterans Affairs Office of Inspector General Audit of the Administrative and Loan Accounting Center, Austin, Texas The Administrative and Loan Accounting Center needed to strengthen certain

Department of Veterans Affairs Office of Inspector General Audit of the Administrative and Loan Accounting Center, Austin, Texas The Administrative and Loan Accounting Center needed to strengthen certain

AUDIT REPORT INTERNAL AUDIT DIVISION. Invoice Processing in UNAMID. Internal controls over invoice processing were inadequate and ineffective

INTERNAL AUDIT DIVISION AUDIT REPORT Invoice Processing in UNAMID Internal controls over invoice processing were inadequate and ineffective 1 June 2010 Assignment No. AP2009/634/18 INTERNAL AUDIT DIVISION

INTERNAL AUDIT DIVISION AUDIT REPORT Invoice Processing in UNAMID Internal controls over invoice processing were inadequate and ineffective 1 June 2010 Assignment No. AP2009/634/18 INTERNAL AUDIT DIVISION

United States Secret Service's Management Letter for DHS' FY 2014 Financial Statements Audit

United States Secret Service's Management Letter for DHS' FY 2014 Financial Statements Audit April 8, 2015 OIG-15-58 HIGHLIGHTS United States Secret Service s Management Letter for DHS FY 2014 Financial

United States Secret Service's Management Letter for DHS' FY 2014 Financial Statements Audit April 8, 2015 OIG-15-58 HIGHLIGHTS United States Secret Service s Management Letter for DHS FY 2014 Financial

U.S. Department of Labor. Office of Inspector General Office of Audit RECOVERY ACT: EFFECTIVENESS OF NEW YORK

U.S. Department of Labor Office of Inspector General Office of Audit REPORT TO EMPLOYMENT AND TRAINING ADMINISTRATION RECOVERY ACT: EFFECTIVENESS OF NEW YORK IN DETECTING AND REDUCING UNEMPLOYMENT INSURANCE

U.S. Department of Labor Office of Inspector General Office of Audit REPORT TO EMPLOYMENT AND TRAINING ADMINISTRATION RECOVERY ACT: EFFECTIVENESS OF NEW YORK IN DETECTING AND REDUCING UNEMPLOYMENT INSURANCE

Informational Notice

Pat Quinn, Governor Julie Hamos, Director 201 South Grand Avenue East Telephone: 1-877-782-5565 Springfield, Illinois 62763-0002 TTY: (800) 526-5812 Informational Notice Date: March 7, 2013 To: Re: Participating

Pat Quinn, Governor Julie Hamos, Director 201 South Grand Avenue East Telephone: 1-877-782-5565 Springfield, Illinois 62763-0002 TTY: (800) 526-5812 Informational Notice Date: March 7, 2013 To: Re: Participating

The Transportation Security Administration Does Not Properly Manage Its Airport Screening Equipment Maintenance Program

The Transportation Security Administration Does Not Properly Manage Its Airport Screening Equipment Maintenance Program May 6, 2015 OIG-15-86 HIGHLIGHTS The Transportation Security Administration Does

The Transportation Security Administration Does Not Properly Manage Its Airport Screening Equipment Maintenance Program May 6, 2015 OIG-15-86 HIGHLIGHTS The Transportation Security Administration Does

Department of Homeland Security

FEMA Public Assistance Grant Funds Awarded to South Florida Water Management District Under Hurricane Charley DA-12-23 August 2012 Washington, DC 20528 / www.oig.dhs.gov AUG 2 7 2012 MEMORANDUM FOR: agement

FEMA Public Assistance Grant Funds Awarded to South Florida Water Management District Under Hurricane Charley DA-12-23 August 2012 Washington, DC 20528 / www.oig.dhs.gov AUG 2 7 2012 MEMORANDUM FOR: agement

Weaknesses in the Smithsonian Tropical Research Institute s Financial Management Require Prompt Attention

Weaknesses in the Smithsonian Tropical Research Institute s Financial Management Require Prompt Attention Office of the Inspector General Report Number A-13-01 October 29, 2013 INTRODUCTION This report

Weaknesses in the Smithsonian Tropical Research Institute s Financial Management Require Prompt Attention Office of the Inspector General Report Number A-13-01 October 29, 2013 INTRODUCTION This report

STATE OF NORTH CAROLINA

STATE OF NORTH CAROLINA PERFORMANCE AUDIT STATE HEALTH PLAN RISK ASSESSMENT SEPTEMBER 2011 OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA STATE AUDITOR PERFORMANCE AUDIT STATE HEALTH PLAN RISK ASSESSMENT

STATE OF NORTH CAROLINA PERFORMANCE AUDIT STATE HEALTH PLAN RISK ASSESSMENT SEPTEMBER 2011 OFFICE OF THE STATE AUDITOR BETH A. WOOD, CPA STATE AUDITOR PERFORMANCE AUDIT STATE HEALTH PLAN RISK ASSESSMENT

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION The Internal Revenue Service September 14, 2010 Reference Number: 2010-10-115 This report has cleared the Treasury Inspector General for Tax Administration

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION The Internal Revenue Service September 14, 2010 Reference Number: 2010-10-115 This report has cleared the Treasury Inspector General for Tax Administration

Office of Inspector General

DEPARTMENT OF HOMELAND SECURITY Office of Inspector General INFORMATION TECHNOLOGY: Final Obstacles Removed To Eliminate Customs Disaster Recovery Material Weakness Office of Information Technology OIG-IT-03-01

DEPARTMENT OF HOMELAND SECURITY Office of Inspector General INFORMATION TECHNOLOGY: Final Obstacles Removed To Eliminate Customs Disaster Recovery Material Weakness Office of Information Technology OIG-IT-03-01

DODIG-2013-105 July 18, 2013. Navy Did Not Develop Processes in the Navy Enterprise Resource Planning System to Account for Military Equipment Assets

DODIG-2013-105 July 18, 2013 Navy Did Not Develop Processes in the Navy Enterprise Resource Planning System to Account for Military Equipment Assets Additional Copies To obtain additional copies of this

DODIG-2013-105 July 18, 2013 Navy Did Not Develop Processes in the Navy Enterprise Resource Planning System to Account for Military Equipment Assets Additional Copies To obtain additional copies of this

PROCUREMENT. Actions Needed to Enhance Training and Certification Requirements for Contracting Officer Representatives OIG-12-3

PROCUREMENT Actions Needed to Enhance Training and Certification Requirements for Contracting Officer Representatives OIG-12-3 Office of Inspector General U.S. Government Accountability Office Report Highlights

PROCUREMENT Actions Needed to Enhance Training and Certification Requirements for Contracting Officer Representatives OIG-12-3 Office of Inspector General U.S. Government Accountability Office Report Highlights

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION Management Oversight of the Small Business/Self-Employed Division s Fuel Compliance Fleet Card Program Should Be Strengthened September 27, 2011 Reference

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION Management Oversight of the Small Business/Self-Employed Division s Fuel Compliance Fleet Card Program Should Be Strengthened September 27, 2011 Reference

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION Accounting and Controls Need to Be Improved for Excess Collections December 15, 2015 Reference Number: 2016-30-005 This report has cleared the Treasury

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION Accounting and Controls Need to Be Improved for Excess Collections December 15, 2015 Reference Number: 2016-30-005 This report has cleared the Treasury

How To Reduce Disruption Risk In An Amtrak Program

Strategic Asset Management Program: Further Actions Should Be Taken To Reduce Business Disruption Risk Audit Report No. 001-2011 June 2, 2011 Audit Report Issued By: NATIONAL RAILROAD PASSENGER CORPORATION

Strategic Asset Management Program: Further Actions Should Be Taken To Reduce Business Disruption Risk Audit Report No. 001-2011 June 2, 2011 Audit Report Issued By: NATIONAL RAILROAD PASSENGER CORPORATION

Department of Homeland Security Office of Inspector General

Department of Homeland Security Office of Inspector General Special Review of the Science and Technology Directorate s Contracts with a Small Business (Summary) OIG-10-103 July 2010 Office of Inspector

Department of Homeland Security Office of Inspector General Special Review of the Science and Technology Directorate s Contracts with a Small Business (Summary) OIG-10-103 July 2010 Office of Inspector

FEMA Faces Challenges in Verifying Applicants' Insurance Policies for the Individuals and Households Program

FEMA Faces Challenges in Verifying Applicants' Insurance Policies for the Individuals and Households Program October 6, 2015 OIG-16-01-D DHS OIG HIGHLIGHTS FEMA Faces Challenges in Verifying Applicants

FEMA Faces Challenges in Verifying Applicants' Insurance Policies for the Individuals and Households Program October 6, 2015 OIG-16-01-D DHS OIG HIGHLIGHTS FEMA Faces Challenges in Verifying Applicants

Department of Homeland Security

U.S. Citizenship and Immigration Services Tracking and Monitoring of Potentially Fraudulent Petitions and Applications for Family-Based Immigration Benefits OIG-13-97 June 2013 Washington, DC 20528 / www.oig.dhs.gov

U.S. Citizenship and Immigration Services Tracking and Monitoring of Potentially Fraudulent Petitions and Applications for Family-Based Immigration Benefits OIG-13-97 June 2013 Washington, DC 20528 / www.oig.dhs.gov

VA Office of Inspector General

VA Office of Inspector General OFFICE OF AUDITS & EVALUATIONS Veterans Health Administration Review of Fraud Management for the Non-VA Fee Care Program June 08, 2010 10-00004-166 ACRONYMS AND ABBREVIATIONS

VA Office of Inspector General OFFICE OF AUDITS & EVALUATIONS Veterans Health Administration Review of Fraud Management for the Non-VA Fee Care Program June 08, 2010 10-00004-166 ACRONYMS AND ABBREVIATIONS

Office of the City Auditor. Audit Report. AUDIT OF ACCOUNTS PAYABLE APPLICATION CONTROLS (Report No. A10-003) October 2, 2009.

October 2, 2009.") CITY OF DALLAS Dallas City Council Office of the City Auditor Audit Report Mayor Tom Leppert Mayor Pro Tem Dwaine Caraway Deputy Mayor Pro Tem Pauline Medrano Council Members Jerry R. Allen Tennell Atkins

CITY OF DALLAS Dallas City Council Office of the City Auditor Audit Report Mayor Tom Leppert Mayor Pro Tem Dwaine Caraway Deputy Mayor Pro Tem Pauline Medrano Council Members Jerry R. Allen Tennell Atkins

Using Technology to Automate Fraud Detection Within Key Business Process Areas

Using Technology to Automate Fraud Detection Within Key Business Process Areas 2013 ACFE Canadian Fraud Conference September 10, 2013 John Verver, CA, CISA, CMA Vice President, Strategy ACL Services Ltd

Using Technology to Automate Fraud Detection Within Key Business Process Areas 2013 ACFE Canadian Fraud Conference September 10, 2013 John Verver, CA, CISA, CMA Vice President, Strategy ACL Services Ltd

Internal Audit Practice Guide

Internal Audit Practice Guide Continuous Auditing Office of the Comptroller General, Internal Audit Sector May 2010 Table of Contents Purpose...1 Background...1 Definitions...2 Continuous Auditing Professional

Internal Audit Practice Guide Continuous Auditing Office of the Comptroller General, Internal Audit Sector May 2010 Table of Contents Purpose...1 Background...1 Definitions...2 Continuous Auditing Professional

GAO FEDERAL STUDENT LOAN PROGRAMS. Opportunities Exist to Improve Audit Requirements and Oversight Procedures. Report to Congressional Committees

GAO United States Government Accountability Office Report to Congressional Committees July 2010 FEDERAL STUDENT LOAN PROGRAMS Opportunities Exist to Improve Audit Requirements and Oversight Procedures

GAO United States Government Accountability Office Report to Congressional Committees July 2010 FEDERAL STUDENT LOAN PROGRAMS Opportunities Exist to Improve Audit Requirements and Oversight Procedures

Independent Evaluation of NRC s Implementation of the Federal Information Security Modernization Act of 2014 for Fiscal Year 2015

Independent Evaluation of NRC s Implementation of the Federal Information Security Modernization Act of 2014 for Fiscal Year 2015 OIG-16-A-03 November 12, 2015 All publicly available OIG reports (including

Independent Evaluation of NRC s Implementation of the Federal Information Security Modernization Act of 2014 for Fiscal Year 2015 OIG-16-A-03 November 12, 2015 All publicly available OIG reports (including

NATIONAL OCEANIC AND ATMOSPHERIC ADMINISTRATION. Opportunities to Strengthen Internal Controls Over Improper Payments PUBLIC RELEASE

U.S. DEPARTMENT OF COMMERCE Office of Inspector General NATIONAL OCEANIC AND ATMOSPHERIC ADMINISTRATION Opportunities to Strengthen Internal Controls Over Improper Payments Final Report No.BSD-16186-0001/July

U.S. DEPARTMENT OF COMMERCE Office of Inspector General NATIONAL OCEANIC AND ATMOSPHERIC ADMINISTRATION Opportunities to Strengthen Internal Controls Over Improper Payments Final Report No.BSD-16186-0001/July

Accounts Payable Outsourcing Audit April 2014

Accounts Payable Outsourcing Audit April 2014 Craig Terrell, Interim City Auditor Lee Hagelstein, Internal Auditor Accounts Payable Outsourcing Audit Table of Contents Page Executive Summary...1 Audit

Accounts Payable Outsourcing Audit April 2014 Craig Terrell, Interim City Auditor Lee Hagelstein, Internal Auditor Accounts Payable Outsourcing Audit Table of Contents Page Executive Summary...1 Audit

NOT ALL COMMUNITY SERVICES BLOCK GRANT RECOVERY ACT COSTS CLAIMED

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL NOT ALL COMMUNITY SERVICES BLOCK GRANT RECOVERY ACT COSTS CLAIMED ON BEHALF OF THE COMMUNITY ACTION PARTNERSHIP OF NATRONA COUNTY FOR

Department of Health and Human Services OFFICE OF INSPECTOR GENERAL NOT ALL COMMUNITY SERVICES BLOCK GRANT RECOVERY ACT COSTS CLAIMED ON BEHALF OF THE COMMUNITY ACTION PARTNERSHIP OF NATRONA COUNTY FOR

William D. Tamburrino, Director, Baltimore Public Housing Program Hub, 3BPH

Issue Date December 19, 2007 Audit Report Number 2008-PH-1004 TO: William D. Tamburrino, Director, Baltimore Public Housing Program Hub, 3BPH FROM: SUBJECT: John P. Buck, Regional Inspector General for

Issue Date December 19, 2007 Audit Report Number 2008-PH-1004 TO: William D. Tamburrino, Director, Baltimore Public Housing Program Hub, 3BPH FROM: SUBJECT: John P. Buck, Regional Inspector General for

Department of Homeland Security Office of Inspector General

Department of Homeland Security Office of Inspector General Final Letter Report: Potential Duplicate Benefits Between FEMA s National Flood Insurance Program and Housing Assistance Programs OIG-09-102

Department of Homeland Security Office of Inspector General Final Letter Report: Potential Duplicate Benefits Between FEMA s National Flood Insurance Program and Housing Assistance Programs OIG-09-102

Controls Over EPA s Compass Financial System Need to Be Improved

U.S. ENVIRONMENTAL PROTECTION AGENCY OFFICE OF INSPECTOR GENERAL Controls Over EPA s Compass Financial System Need to Be Improved Report No. 13-P-0359 August 23, 2013 Scan this mobile code to learn more

U.S. ENVIRONMENTAL PROTECTION AGENCY OFFICE OF INSPECTOR GENERAL Controls Over EPA s Compass Financial System Need to Be Improved Report No. 13-P-0359 August 23, 2013 Scan this mobile code to learn more

INSPECTOR GENERAL. Fiscal Year 2013 Postal Service Financial Statements Audit St. Louis Accounting Services. Audit Report.

OFFICE OF INSPECTOR GENERAL UNITED STATES POSTAL SERVICE Fiscal Year 2013 Postal Service Financial Statements Audit Audit Report March 20, 2014 Report Number March 20, 2014 Fiscal Year 2013 Postal Service

OFFICE OF INSPECTOR GENERAL UNITED STATES POSTAL SERVICE Fiscal Year 2013 Postal Service Financial Statements Audit Audit Report March 20, 2014 Report Number March 20, 2014 Fiscal Year 2013 Postal Service

Chairwoman Foxx, Ranking Member Hinojosa, and members of the Subcommittee, thank you

Testimony of Kathleen S. Tighe, Inspector General U.S. Department of Education Before the Education and the Workforce Committee Subcommittee on Higher Education and Workforce Training U.S. House of Representatives

Testimony of Kathleen S. Tighe, Inspector General U.S. Department of Education Before the Education and the Workforce Committee Subcommittee on Higher Education and Workforce Training U.S. House of Representatives

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION The External Leads Program Results in the Recovery of Erroneously Issued Tax Refunds; However, Improvements Are Needed to Ensure That Leads Are Timely

TREASURY INSPECTOR GENERAL FOR TAX ADMINISTRATION The External Leads Program Results in the Recovery of Erroneously Issued Tax Refunds; However, Improvements Are Needed to Ensure That Leads Are Timely

Review of U.S. Coast Guard's FY 2014 Drug Control Performance Summary Report

Review of U.S. Coast Guard's FY 2014 Drug Control Performance Summary Report January 26, 2015 OIG-15-27 HIGHLIGHTS Review of U.S. Coast Guard s FY 2014 Drug Control Performance Summary Report January 26,

Review of U.S. Coast Guard's FY 2014 Drug Control Performance Summary Report January 26, 2015 OIG-15-27 HIGHLIGHTS Review of U.S. Coast Guard s FY 2014 Drug Control Performance Summary Report January 26,

Security Concerns with Federal Emergency Management Agency's egrants Grant Management System

Security Concerns with Federal Emergency Management Agency's egrants Grant Management System November 19, 2015 OIG-16-11 DHS OIG HIGHLIGHTS Security Concerns with Federal Emergency Management Agency s

Security Concerns with Federal Emergency Management Agency's egrants Grant Management System November 19, 2015 OIG-16-11 DHS OIG HIGHLIGHTS Security Concerns with Federal Emergency Management Agency s