AGENDA: MANAGERIAL ACCOUNTING AND COST CONCEPTS

|

|

|

- James Elliott

- 7 years ago

- Views:

Transcription

1 TM 2-1 A. Cost classifications for: AGENDA: MANAGERIAL ACCOUNTING AND COST CONCEPTS 1. Financial statement preparation. 2. Predicting cost behavior. 3. Assigning costs to cost objects. 4. Making decisions B. Least-squares regression computations using Microsoft Excel. C. Cost of Quality.

2 TM 2-2 AN OVERVIEW OF COST CLASSIFICATIONS IN CHAPTER 2 Purpose of classification Preparing an income statement and balance sheet Predicting changes in cost due to changes in activity Assigning costs Making decisions Cost classifications Product costs Direct materials Direct labor Manufacturing overhead Period costs (nonmanufacturing costs) Selling costs Administrative costs Variable costs Fixed costs Mixed costs Direct costs Indirect costs Differential costs Sunk costs Opportunity costs

3 TM 2-3 MANUFACTURING COST CLASSIFICATIONS FOR EXTERNAL REPORTING COST CLASSIFICATIONS TO PREDICT COST BEHAVIOR To predict how costs react to changes in activity, costs are often classified as variable or fixed.

4 TM 2-4 VARIABLE COSTS Variable cost behavior can be summarized as follows: Variable Cost Behavior In Total Total variable cost increases and decreases in proportion to changes in activity. Per Unit Variable cost per unit is constant. EXAMPLE: A company manufactures microwave ovens. Each oven requires a timing device that costs $30. The cost per unit and the total cost of the timing device at various levels of activity (i.e., number of ovens produced) would be: Cost per Number of Total Variable Timing Ovens Cost Timing Device Produced Devices $30 1 $30 $30 10 $300 $ $3,000 $ $6,000

5 TM 2-5 FIXED COSTS Fixed cost behavior can be summarized as follows: Fixed Cost Behavior In Total Per Unit Total fixed cost is not affected Fixed cost per unit decreases by changes in activity (i.e., total as the activity level rises and fixed cost remains constant even increases as the activity level if activity changes). falls. EXAMPLE: Assume again that a company manufactures microwave ovens. The company pays $9,000 per month to rent its factory building. The total cost and the cost per unit of rent at various levels of activity would be: Number of Rent Cost Ovens Rent Cost per Month Produced per Oven $9,000 1 $9,000 $9, $900 $9, $90 $9, $45 TYPES OF FIXED COSTS Committed fixed costs relate to investment in plant, equipment, and basic administrative structure. It is difficult to reduce these fixed costs in the short-term. Examples include: Equipment depreciation. Real estate taxes. Salaries of key operating personnel. Discretionary fixed costs arise from annual decisions by management to spend in certain areas. These costs can often be reduced in the shortterm. Examples include: Advertising; public relations. Research; management development programs.

6 TM 2-6 A GRAPHIC VIEW OF COST BEHAVIOR $6,000 Total Variable Cost Total Fixed Cost $9,000 $3, Microwaves produced Microwaves produced RELEVANT RANGE If activity changes enough, fixed costs may change. For example, if microwave production were doubled, another factory building might have to be rented. The relevant range is the range of activity within which the assumptions that have been made about variable and fixed costs are valid. For example, the relevant range within which total fixed factory rent is $9,000 per month might be 1 to 200 microwaves produced per month.

7 TM 2-7 MIXED COSTS A mixed (or semi-variable) cost contains elements of both variable and fixed costs. Example: Lori Yang leases an automated photo developer for $2,500 per year plus 2 per photo developed. Equation of a straight line: Y = a + bx Y = $2,500 + $0.02X

8 TM 2-8 SCATTERGRAPH METHOD As the first step in the analysis of a mixed cost, cost and activity should be plotted on a scattergraph. This helps to quickly diagnose the nature of the relation between cost and activity. Example: Piedmont Wholesale Florists has maintained records of the number of orders and billing costs in each quarter over the past several years. Quarter Number of Orders Billing Costs Year 1 1st 1,500 $42,000 2nd 1,900 $46,000 3rd 1,000 $37,000 4th 1,300 $43,000 Year 2 1st 2,800 $54,000 2nd 1,700 $47,000 3rd 2,100 $51,000 4th 1,100 $42,000 Year 3 1st 2,000 $48,000 2nd 2,400 $53,000 3rd 2,300 $49,000 These data are plotted on the next page, with the activity (number of orders) on the horizontal X axis and the cost (billing costs) on the vertical Y axis.

9 TM 2-9 A COMPLETED SCATTERGRAPH Y $60,000 Regression Line $50,000 $48,000 Billing Costs $40,000 $30,000 $20,000 $10,000 $ ,000 1,500 2,000 2,500 3,000 Number of Orders X The relation between the number of orders and the billing cost is approximately linear. (A straight line that seems to reflect this basic relation was drawn with a ruler on the scattergraph.) Because a straight line seems to be a reasonable fit to the data, we can proceed to estimate the variable and fixed elements of the cost using one of the following methods. 1. High-low method. 2. Least-squares regression method.

Because a straight line seems to be a reasonable fit to the data, we can proceed to estimate the variable and fixed elements of the cost using one")

10 TM 2-10 ANALYSIS OF MIXED COSTS: HIGH-LOW METHOD EXAMPLE: Kohlson Company has incurred the following shipping costs over the past eight months: Units Sold Shipping Cost January... 6,000 $66,000 February... 5,000 $65,000 March... 7,000 $70,000 April... 9,000 $80,000 May... 8,000 $76,000 June... 10,000 $85,000 July... 12,000 $100, August... 11,000 $87,000 With the high-low method, only the periods in which the lowest activity and the highest activity occurred are used to estimate the variable and fixed components of the mixed cost. Units Sold Shipping Cost High activity level, July... 12,000 $100,000 Low activity level, February 5,000 65,000 Change... 7,000 $ 35,000 Change in cost $35,000 Variable cost= = =$5 per unit Change in activity 7,000 units Fixed cost = Total cost - Variable cost element = $100,000 - (12,000 units $5 per unit) = $40,000 The cost formula for shipping cost is: Y = $40,000 + $5X

11 TM 2-11 EVALUATION OF THE HIGH-LOW METHOD $100,000 Y high level of activity Shipping Costs $80,000 $60,000 $40,000 low level of activity Variable Cost $5/unit $20,000 Fixed Cost $40,000 $0 0 2,000 4,000 6,000 8,000 10,000 12,000 Units Sold X The high-low method suffers from two major defects: 1. It throws away all but two data points. 2. The periods with the highest and lowest volumes are often unusual.

12 TM 2-12 LEAST-SQUARES REGRESSION METHOD The least-squares regression method for analyzing mixed costs uses mathematical formulas to determine the regression line that minimizes the sum of the squared errors.

13 TM 2-13 TRADITIONAL VERSUS CONTRIBUTION INCOME STATEMENT

14 TM 2-14 COST CLASSIFICATIONS FOR ASSIGNING COSTS TO COST OBJECTS COST OBJECT A cost object is anything for which cost data are desired. Examples of cost objects: Products Customers Departments Jobs DIRECT COSTS A direct cost is a cost that can be easily and conveniently traced to a particular cost object. Examples of direct costs: The direct costs of a Ford SUV would include the cost of the steering wheel purchased by Ford from a supplier, the costs of direct labor workers, the costs of the tires, and so on. The direct costs of a hospital s radiology department would include X- ray film used in the department, the salaries of radiologists, and the costs of radiology lab equipment. INDIRECT COSTS An indirect cost is a cost that cannot be easily and conveniently traced to a particular cost object. Examples of indirect costs: Manufacturing overhead, such as the factory managers salary at a multi-product plant, is an indirect cost of any one product. General hospital administration costs are indirect costs of the radiology lab.

15 TM 2-15 COST CLASSIFICATIONS FOR DECISION-MAKING DIFFERENTIAL COST Every decision involves choosing from among at least two alternatives. Any cost that differs between alternatives is a differential cost. Only the differential costs are relevant in making a decision. EXAMPLE: Bill is currently employed as a lifeguard, but he has been offered a job in an auto service center in the same town. When comparing the two jobs, the differential revenues and costs are: Auto Differential Life- Service costs and guard Center revenues Monthly salary... $1,200 $1,500 $300 Monthly expenses: Commuting Meals Apartment rent Uniform rental Sunscreen (10) Total monthly expenses Net monthly income... $ 560 $ 760 $200

16 TM 2-16 OPPORTUNITY COST An opportunity cost is the potential benefit given up when selecting one course of action over another. EXAMPLE: Linda has a job in the campus bookstore and is paid $65 per day. One of her friends is getting married and Linda would like to attend the wedding, but she would have to miss a day of work. If she attends the wedding, the $65 in lost wages will be an opportunity cost of attending the wedding. EXAMPLE: The reception for the wedding mentioned above will be held in the ballroom at the Lexington Club. The manager of the Lexington Club had to decide between accepting the booking for the wedding reception or accepting a booking for a corporate seminar. The hall could have been rented to the corporation for $600. The lost rental revenue of $600 is an opportunity cost of accepting the reservation for the wedding. SUNK COST A sunk cost is a cost that has already been incurred and that cannot be changed by any decision made now or in the future. Sunk costs are irrelevant and should be ignored in decisions. EXAMPLE: Linda has already purchased a ticket to a rock concert for $35. If she goes to the wedding, she will be unable to attend the concert. The $35 is a sunk cost that she should ignore when deciding whether or not to attend the wedding. [However, any amount she can get by reselling the ticket is NOT a sunk cost. And while she should ignore the $35 sunk cost, she should not ignore the enjoyment she would get if she were to attend the concert.]

17 TM 2-17 APPENDIX 2A: LEAST-SQUARES REGRESSION COMPUTATIONS Example: Montrose Hospital operates a cafeteria for employees. Management would like to know how cafeteria costs are affected by the number of meals served. Meals Served X Total Cost Y April... 4,000 $9,500 May... 1,000 $4,000 June... 3,000 $8,000 July... 5,000 $10,000 August... 10,000 $19,500 September.. 7,000 $14,000 Statistical software or a spreadsheet program can do the computations required by the least-squares method. The results in this case are: Intercept (fixed cost)... $2,433 Slope (variable cost)... $1.68 R The fixed cost is therefore $2,433 per month and the variable cost is $1.68 per meal served, or: where X is meals served. Y = $2,433 + $1.68X, R 2 is a measure of the goodness of fit of the regression line. In this case, it indicates that 99% of the variation in cafeteria costs is due to the number of meals served. This suggests an excellent fit.

... $2,433 Slope (variable cost)... $1.68 R 2... 0.99 The fixed cost is therefore $2,433 per month and the variable cost is $1.")

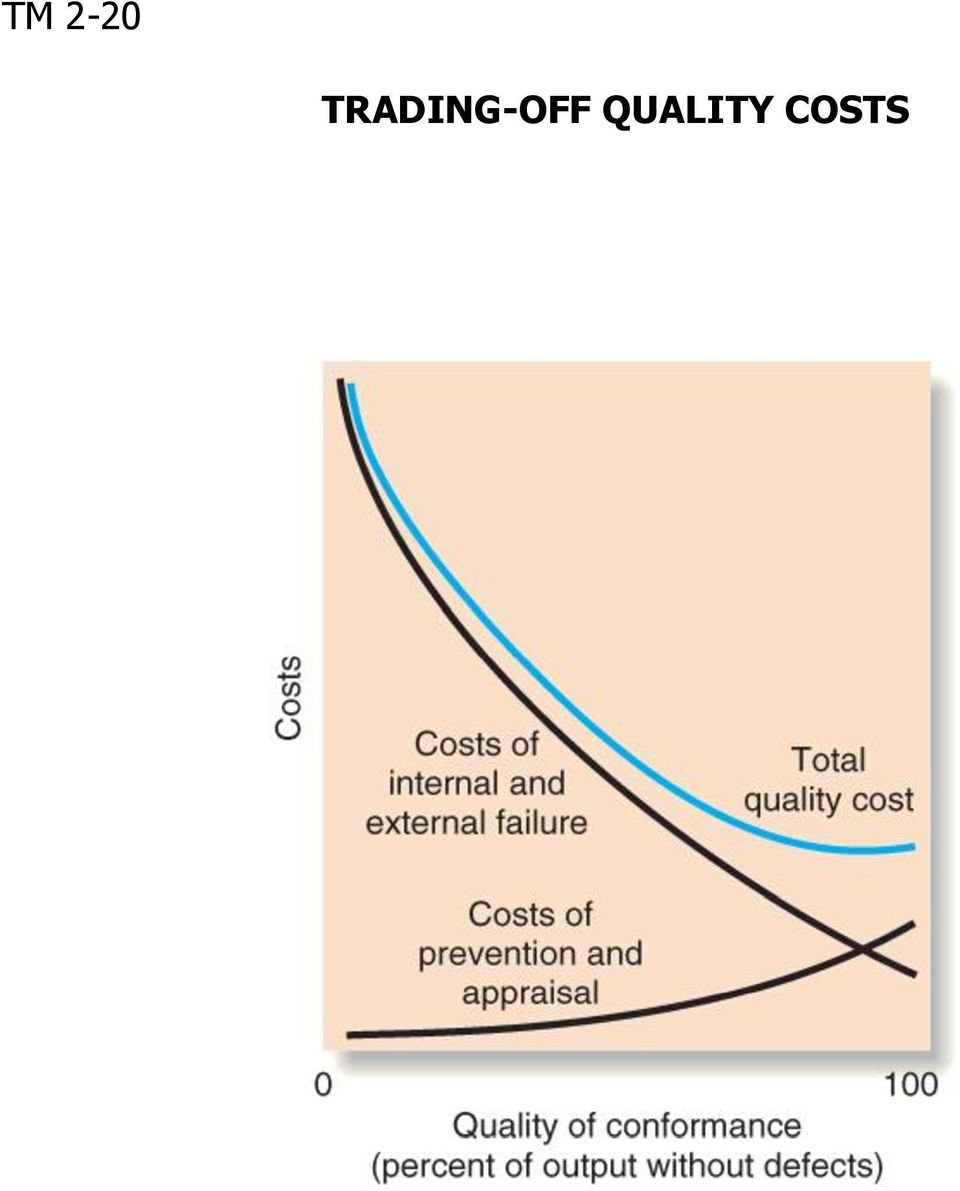

18 TM 2-18 APPENDIX 2B: QUALITY COSTS The costs of correcting defective units before they reach customers are called internal failure costs. Examples: Scrapped units. Rework of defective units. Costs that are incurred by releasing defective units to customers are called external failure costs. Examples: Costs of fixing products under warranty. Loss of sales due to a tarnished reputation. The costs of internal and external failures can be avoided by: Preventing defects. Finding defective units before they are released. The costs associated with these activities are called prevention costs and appraisal costs, respectively. Generally, prevention is the best policy. It is usually far easier and less expensive to prevent defects than to fix them.

19 TM 2-19 EXAMPLES OF QUALITY COSTS

20 TM 2-20 TRADING-OFF QUALITY COSTS

21 TM 2-21 QUALITY COST REPORTS Quality cost reports summarize prevention costs, appraisal costs, internal failure costs, and external failure costs that would otherwise be hidden in general overhead. Managers are often surprised by how much defects cost. The report helps identify where the biggest quality problems lie. The report helps managers assess how resources should be distributed. If internal and external failure costs are high relative to prevention and appraisal costs, more should probably be spent on prevention and appraisal. Because quality cost reports are largely an attention-directing device, the costs do not have to be precise. Unfortunately, the cost of lost sales due to external failures is usually excluded from the reports due to measurement difficulties.

22 TM 2-22 SAMPLE QUALITY COST REPORT

y = a + bx Chapter 10: Horngren 13e The Dependent Variable: The cost that is being predicted The Independent Variable: The cost driver

Chapter 10: Dt Determining ii How Costs Behave Bh Horngren 13e 1 The Linear Cost Function y = a + bx The Dependent Variable: The cost that is being predicted The Independent Variable: The cost driver The

Chapter 10: Dt Determining ii How Costs Behave Bh Horngren 13e 1 The Linear Cost Function y = a + bx The Dependent Variable: The cost that is being predicted The Independent Variable: The cost driver The

Part Three. Cost Behavior Analysis

Part Three Cost Behavior Analysis Cost Behavior Cost behavior is the manner in which a cost changes as some related activity changes An understanding of cost behavior is necessary to plan and control costs

Part Three Cost Behavior Analysis Cost Behavior Cost behavior is the manner in which a cost changes as some related activity changes An understanding of cost behavior is necessary to plan and control costs

Management Accounting Theory of Cost Behavior

Management Accounting 63 Management Accounting Theory of Cost Behavior Management accounting contains a number of decision making tools that require the conversion of all operating costs and expenses into

Management Accounting 63 Management Accounting Theory of Cost Behavior Management accounting contains a number of decision making tools that require the conversion of all operating costs and expenses into

Custodial Guest- Days

Exercise 5-7 (30 minutes) 1. Custodial Guest- Days Supplies High activity level (July)... 12,000 $13,500 Low activity level (March)... 4,000 7,500 Change... 8,000 $ 6,000 Variable cost element: Change

Exercise 5-7 (30 minutes) 1. Custodial Guest- Days Supplies High activity level (July)... 12,000 $13,500 Low activity level (March)... 4,000 7,500 Change... 8,000 $ 6,000 Variable cost element: Change

Cost Behavior and. Types of Cost Behavior Patterns. Summary of VC and FC Behavior. Cost In Total Per Unit

Cost Behavior and Cost Estimation 1 Types of Cost Behavior Patterns Summary of VC and FC Behavior Cost In Total Per Unit Total VC is VC per unit remains VC proportional to the activity the same over wide

Cost Behavior and Cost Estimation 1 Types of Cost Behavior Patterns Summary of VC and FC Behavior Cost In Total Per Unit Total VC is VC per unit remains VC proportional to the activity the same over wide

Exam 1 Chapters 1-3 Key

Exam 1 Chapters 1-3 Key 1. Which of the following should NOT be included as part of manufacturing overhead at a company that makes office furniture? A. Sheet steel in a file cabinet made by the company.

Exam 1 Chapters 1-3 Key 1. Which of the following should NOT be included as part of manufacturing overhead at a company that makes office furniture? A. Sheet steel in a file cabinet made by the company.

House Published on www.jps-dir.com

I. Cost - Volume - Profit (Break - Even) Analysis A. Definitions 1. Cost - Volume - Profit (CVP) Analysis: is a means of predicting the relationships among revenues, variable costs, and fixed costs at

I. Cost - Volume - Profit (Break - Even) Analysis A. Definitions 1. Cost - Volume - Profit (CVP) Analysis: is a means of predicting the relationships among revenues, variable costs, and fixed costs at

C 5 - COST BEHAVIOR: ANALYSIS AND USE notes-c5.doc Written by Professor Gregory M. Burbage, MBA, CPA, CMA, CFM

C 5 - COST BEHAVIOR: ANALYSIS AND USE notes-c5.doc CHAPTER LEARNING OBJECTIVES: MAJOR: - Use the High-Low method to determine and calculate the structure of a cost. - Define, explain and use variable,

C 5 - COST BEHAVIOR: ANALYSIS AND USE notes-c5.doc CHAPTER LEARNING OBJECTIVES: MAJOR: - Use the High-Low method to determine and calculate the structure of a cost. - Define, explain and use variable,

Cost Behaviour. Concepts and definitions questions. 1.1 Distinguish between

1 ost ehaviour ost ehaviour 1 oncepts and definitions questions 1.1 istinguish between (iii) Financial accounting ost accounting Management accounting 1.2 State six different benefits of cost accounting.

1 ost ehaviour ost ehaviour 1 oncepts and definitions questions 1.1 istinguish between (iii) Financial accounting ost accounting Management accounting 1.2 State six different benefits of cost accounting.

Copyright 2015 Pearson Canada Inc. 1

1 Building Blocks of Managerial Accounting CHAPTER 2 2 Distinguish among service, merchandising, and manufacturing companies OBJECTIVE 1 3 Service Companies Provide an intangible service only Largest sector

1 Building Blocks of Managerial Accounting CHAPTER 2 2 Distinguish among service, merchandising, and manufacturing companies OBJECTIVE 1 3 Service Companies Provide an intangible service only Largest sector

You and your friends head out to a favorite restaurant

19 Cost-Volume-Profit Analysis Learning Objectives 1 Identify how changes in volume affect costs 2 Use CVP analysis to compute breakeven points 3 Use CVP analysis for profit planning, and graph the CVP

19 Cost-Volume-Profit Analysis Learning Objectives 1 Identify how changes in volume affect costs 2 Use CVP analysis to compute breakeven points 3 Use CVP analysis for profit planning, and graph the CVP

Cost Concepts and Behavior

Chapter 2 Cost Concepts and Behavior McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. Learning Objectives L.O. 1 Explain the basic concept of cost. L.O. 2 Explain

Chapter 2 Cost Concepts and Behavior McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. Learning Objectives L.O. 1 Explain the basic concept of cost. L.O. 2 Explain

In this chapter, you will learn to use cost-volume-profit analysis.

2.0 Chapter Introduction In this chapter, you will learn to use cost-volume-profit analysis. Assumptions. When you acquire supplies or services, you normally expect to pay a smaller price per unit as the

2.0 Chapter Introduction In this chapter, you will learn to use cost-volume-profit analysis. Assumptions. When you acquire supplies or services, you normally expect to pay a smaller price per unit as the

UG802: COST MEASUREMENT AND COST ANALYSIS

UG802: COST MEASUREMENT AND COST ANALYSIS April 6, 2014 Kanokporn Rienkhemaniyom, Ph.D. Managerial Accounting - Overview Definition: A profession that involves partnering in management decision making,

UG802: COST MEASUREMENT AND COST ANALYSIS April 6, 2014 Kanokporn Rienkhemaniyom, Ph.D. Managerial Accounting - Overview Definition: A profession that involves partnering in management decision making,

Helena Company reports the following total costs at two levels of production.

Chapter 22 Helena Company reports the following total costs at two levels of production. 10,000 Units 20,000 Units Direct materials $20,000 $40,000 Maintenance 8,000 10,000 Direct labor 17,000 34,000 Indirect

Chapter 22 Helena Company reports the following total costs at two levels of production. 10,000 Units 20,000 Units Direct materials $20,000 $40,000 Maintenance 8,000 10,000 Direct labor 17,000 34,000 Indirect

5-30. (25 min.) Methods of Estimating Costs High-Low: Adriana Corporation. a. High-low estimate

Methods of Estimating Costs High-Low: Adriana Corporation. a. High-low estimate") 5-30. (25 min.) Methods of Estimating Costs High-Low: Adriana Corporation. a. High-low estimate Machine- Hours Overhead Costs Highest activity (month 12)... 8,020 $564,210 Lowest activity (month 11)...

5-30. (25 min.) Methods of Estimating Costs High-Low: Adriana Corporation. a. High-low estimate Machine- Hours Overhead Costs Highest activity (month 12)... 8,020 $564,210 Lowest activity (month 11)...

Incremental Analysis and Decision-making Costs

Management Accounting 161 Incremental Analysis and Decision-making Costs Nature of Incremental Analysis Decision-making is essentially a process of selecting the best alternative given the available information

Management Accounting 161 Incremental Analysis and Decision-making Costs Nature of Incremental Analysis Decision-making is essentially a process of selecting the best alternative given the available information

CHAPTER 10 In-Class QUIZ

CHAPTER 10 In-Class QUIZ 1. A mixed cost function has a constant component of $20,000. If the total cost is $60,000 and the independent variable has the value 200, what is the value of the slope coefficient?

CHAPTER 10 In-Class QUIZ 1. A mixed cost function has a constant component of $20,000. If the total cost is $60,000 and the independent variable has the value 200, what is the value of the slope coefficient?

What is a cost? What is an expense?

What is a cost? What is an expense? A cost is a sacrifice of resources. An expense is a cost incurred in the process of generating revenues. Expenses are recorded at the same time that the associated revenues

What is a cost? What is an expense? A cost is a sacrifice of resources. An expense is a cost incurred in the process of generating revenues. Expenses are recorded at the same time that the associated revenues

Chapter 25 Cost-Volume-Profit Analysis Questions

Chapter 25 Cost-Volume-Profit Analysis Questions 1. Cost-volume-profit analysis is used to accomplish the first step in the planning phase for a business, which involves predicting the volume of activity,

Chapter 25 Cost-Volume-Profit Analysis Questions 1. Cost-volume-profit analysis is used to accomplish the first step in the planning phase for a business, which involves predicting the volume of activity,

1. The cost of a hard-drive installed in a computer: direct materials cost.

Brief Exercise 1-1 (15 minutes) 1. The cost of a hard-drive installed in a computer: direct materials cost. 2. The cost of advertising in the Puget Sound Computer User newspaper: selling cost. 3. The wages

Brief Exercise 1-1 (15 minutes) 1. The cost of a hard-drive installed in a computer: direct materials cost. 2. The cost of advertising in the Puget Sound Computer User newspaper: selling cost. 3. The wages

Module 4: Cost behaviour and cost-volume-profit analysis

Page 1 of 28 Module 4: Cost behaviour and cost-volume-profit analysis Required reading Chapter 5, pages 187-213 Chapter 6, pages 230-253 Appendix 6A, pages 256-258 Overview The way in which a cost responds

Page 1 of 28 Module 4: Cost behaviour and cost-volume-profit analysis Required reading Chapter 5, pages 187-213 Chapter 6, pages 230-253 Appendix 6A, pages 256-258 Overview The way in which a cost responds

AGENDA: JOB-ORDER COSTING

TM 3-1 AGENDA: JOB-ORDER COSTING A. The documents in a job-order costing system. 1. Materials requisition form. 2. Direct labor time ticket. 3. Job cost sheet. B. Applying overhead using a predetermined

TM 3-1 AGENDA: JOB-ORDER COSTING A. The documents in a job-order costing system. 1. Materials requisition form. 2. Direct labor time ticket. 3. Job cost sheet. B. Applying overhead using a predetermined

1 USING REGRESSION TO CALCULATE FIXED COST, CALCULATE THE VARIABLE RATE, CONSTRUCT A COST FORMULA AND DETERMINE BUDGETED COST

ESERCIZI 1 USING REGRESSION TO CALCULATE FIXED COST, CALCULATE THE VARIABLE RATE, CONSTRUCT A COST FORMULA AND DETERMINE BUDGETED COST Refer to the Pizza Vesuvio company information in Cornerstone Exercise

ESERCIZI 1 USING REGRESSION TO CALCULATE FIXED COST, CALCULATE THE VARIABLE RATE, CONSTRUCT A COST FORMULA AND DETERMINE BUDGETED COST Refer to the Pizza Vesuvio company information in Cornerstone Exercise

ICASL - Business School Programme

ICASL - Business School Programme Quantitative Techniques for Business (Module 3) Financial Mathematics TUTORIAL 2A This chapter deals with problems related to investing money or capital in a business

ICASL - Business School Programme Quantitative Techniques for Business (Module 3) Financial Mathematics TUTORIAL 2A This chapter deals with problems related to investing money or capital in a business

CHAPTER LEARNING OBJECTIVES. Identify common cost behavior patterns.

c04.qxd 6/2/06 2:53 PM Page 124 CHAPTER 4 LEARNING OBJECTIVES 1 2 3 4 5 6 Identify common cost behavior patterns. Estimate the relation between cost and activity using account analysis and the high-low

c04.qxd 6/2/06 2:53 PM Page 124 CHAPTER 4 LEARNING OBJECTIVES 1 2 3 4 5 6 Identify common cost behavior patterns. Estimate the relation between cost and activity using account analysis and the high-low

2. A direct cost is a cost that cannot be easily traced to the particular cost object under

Chapter 02 Managerial Accounting and Cost Concepts True / False Questions 1. Selling costs can be either direct or indirect costs. True False 2. A direct cost is a cost that cannot be easily traced to

Chapter 02 Managerial Accounting and Cost Concepts True / False Questions 1. Selling costs can be either direct or indirect costs. True False 2. A direct cost is a cost that cannot be easily traced to

Chapter 6 Cost-Volume-Profit Relationships

Chapter 6 Cost-Volume-Profit Relationships Solutions to Questions 6-1 The contribution margin (CM) ratio is the ratio of the total contribution margin to total sales revenue. It can be used in a variety

Chapter 6 Cost-Volume-Profit Relationships Solutions to Questions 6-1 The contribution margin (CM) ratio is the ratio of the total contribution margin to total sales revenue. It can be used in a variety

ACC 121 PRINCIPLES OF MANAGERIAL ACCOUNTING

PRINCIPLES OF MANAGERIAL ACCOUNTING COURSE DESCRIPTION: Prerequisites: ACC 120 Corequisites: None This course includes a greater emphasis on managerial and cost accounting skills. Emphasis is on managerial

PRINCIPLES OF MANAGERIAL ACCOUNTING COURSE DESCRIPTION: Prerequisites: ACC 120 Corequisites: None This course includes a greater emphasis on managerial and cost accounting skills. Emphasis is on managerial

Models of a Vending Machine Business

Math Models: Sample lesson Tom Hughes, 1999 Models of a Vending Machine Business Lesson Overview Students take on different roles in simulating starting a vending machine business in their school that

Math Models: Sample lesson Tom Hughes, 1999 Models of a Vending Machine Business Lesson Overview Students take on different roles in simulating starting a vending machine business in their school that

Management Accounting and Decision-Making

Management Accounting 15 Management Accounting and Decision-Making Management accounting writers tend to present management accounting as a loosely connected set of decision making tools. Although the

Management Accounting 15 Management Accounting and Decision-Making Management accounting writers tend to present management accounting as a loosely connected set of decision making tools. Although the

Section 1.5 Linear Models

Section 1.5 Linear Models Some real-life problems can be modeled using linear equations. Now that we know how to find the slope of a line, the equation of a line, and the point of intersection of two lines,

Section 1.5 Linear Models Some real-life problems can be modeled using linear equations. Now that we know how to find the slope of a line, the equation of a line, and the point of intersection of two lines,

Classification of Manufacturing Costs and Expenses

Management Accounting 51 Classification of Manufacturing Costs and Expenses Introduction Management accounting, as previously explained, consists primarily of planning, performance evaluation, and decision

Management Accounting 51 Classification of Manufacturing Costs and Expenses Introduction Management accounting, as previously explained, consists primarily of planning, performance evaluation, and decision

WEB APPENDIX. Calculating Beta Coefficients. b Beta Rise Run Y 7.1 1 8.92 X 10.0 0.0 16.0 10.0 1.6

WEB APPENDIX 8A Calculating Beta Coefficients The CAPM is an ex ante model, which means that all of the variables represent before-thefact, expected values. In particular, the beta coefficient used in

WEB APPENDIX 8A Calculating Beta Coefficients The CAPM is an ex ante model, which means that all of the variables represent before-thefact, expected values. In particular, the beta coefficient used in

COST & BREAKEVEN ANALYSIS

COST & BREAKEVEN ANALYSIS http://www.tutorialspoint.com/managerial_economics/cost_and_breakeven_analysis.htm Copyright tutorialspoint.com In managerial economics another area which is of great importance

COST & BREAKEVEN ANALYSIS http://www.tutorialspoint.com/managerial_economics/cost_and_breakeven_analysis.htm Copyright tutorialspoint.com In managerial economics another area which is of great importance

How to Forecast Your Revenue and Sales A Step by Step Guide to Revenue and Sales Forecasting in a Small Business

How to Forecast Your Revenue and Sales A Step by Step Guide to Revenue and Sales Forecasting in a Small Business By BizMove Management Training Institute Other free books by BizMove that may interest you:

How to Forecast Your Revenue and Sales A Step by Step Guide to Revenue and Sales Forecasting in a Small Business By BizMove Management Training Institute Other free books by BizMove that may interest you:

Assessing the Cost of Poor Quality

Assessing the Cost of Poor Quality Convincing OEMs to invest in preventive actions may be as simple as showing them the numbers. The key is to understand the costs associated with a poor quality system.

Assessing the Cost of Poor Quality Convincing OEMs to invest in preventive actions may be as simple as showing them the numbers. The key is to understand the costs associated with a poor quality system.

COST CLASSIFICATION AND COST BEHAVIOR INTRODUCTION

COST CLASSIFICATION AND COST BEHAVIOR INTRODUCTION LESSON# 1 Cost Accounting Cost Accounting is an expanded phase of financial accounting which provides management promptly with the cost of producing and/or

COST CLASSIFICATION AND COST BEHAVIOR INTRODUCTION LESSON# 1 Cost Accounting Cost Accounting is an expanded phase of financial accounting which provides management promptly with the cost of producing and/or

Paper F2. Management Accounting. Fundamentals Pilot Paper Knowledge module. The Association of Chartered Certified Accountants. Time allowed: 2 hours

Fundamentals Pilot Paper Knowledge module Management ccounting Time allowed: 2 hours LL FIFTY questions are compulsory and MUST be attempted. Paper F2 o NOT open this paper until instructed by the supervisor.

Fundamentals Pilot Paper Knowledge module Management ccounting Time allowed: 2 hours LL FIFTY questions are compulsory and MUST be attempted. Paper F2 o NOT open this paper until instructed by the supervisor.

Financial Analysis, Modeling, and Forecasting Techniques

Financial Analysis, Modeling, and Forecasting Techniques Course #5710A/QAS-5710A Course Material Financial Analysis, Modeling, and Forecasting Techniques (Course #5710A/QAS-5710A) Table of Contents PART

Financial Analysis, Modeling, and Forecasting Techniques Course #5710A/QAS-5710A Course Material Financial Analysis, Modeling, and Forecasting Techniques (Course #5710A/QAS-5710A) Table of Contents PART

Accounting Building Business Skills. Learning Objectives: Learning Objectives: Paul D. Kimmel. Chapter Fourteen: Cost-volume-profit Relationships

Accounting Building Business Skills Paul D. Kimmel Chapter Fourteen: Cost-volume-profit Relationships PowerPoint presentation by Kate Wynn-Williams University of Otago, Dunedin 2003 John Wiley & Sons Australia,

Accounting Building Business Skills Paul D. Kimmel Chapter Fourteen: Cost-volume-profit Relationships PowerPoint presentation by Kate Wynn-Williams University of Otago, Dunedin 2003 John Wiley & Sons Australia,

1. Managerial accounting: A. is governed by generally accepted accounting principles. B. places emphasis on special-purpose information.

1. Managerial accounting: A. is governed by generally accepted accounting principles. B. places emphasis on special-purpose information. C. pertains to the entity as a whole and is highly aggregated. D.

1. Managerial accounting: A. is governed by generally accepted accounting principles. B. places emphasis on special-purpose information. C. pertains to the entity as a whole and is highly aggregated. D.

Chapter 10 Revenue, costs and break-even analysis

Chapter 10, costs and break-even analysis, costs and break-even analysis is the money a business makes from sales. In other words, it is the value of the sales and is also referred to as turnover. The

Chapter 10, costs and break-even analysis, costs and break-even analysis is the money a business makes from sales. In other words, it is the value of the sales and is also referred to as turnover. The

Budgetary Planning. Managerial Accounting Fifth Edition Weygandt Kimmel Kieso. Page 9-2

9-1 Budgetary Planning Managerial Accounting Fifth Edition Weygandt Kimmel Kieso 9-2 study objectives 1. Indicate the benefits of budgeting. 2. State the essentials of effective budgeting. 3. Identify

9-1 Budgetary Planning Managerial Accounting Fifth Edition Weygandt Kimmel Kieso 9-2 study objectives 1. Indicate the benefits of budgeting. 2. State the essentials of effective budgeting. 3. Identify

Part II Management Accounting Decision-Making Tools

Part II Management Accounting Decision-Making Tools Chapter 7 Chapter 8 Chapter 9 Cost-Volume-Profit Analysis Comprehensive Business Budgeting Incremental Analysis and Decision-making Costs Chapter 10

Part II Management Accounting Decision-Making Tools Chapter 7 Chapter 8 Chapter 9 Cost-Volume-Profit Analysis Comprehensive Business Budgeting Incremental Analysis and Decision-making Costs Chapter 10

Review of Fundamental Mathematics

Review of Fundamental Mathematics As explained in the Preface and in Chapter 1 of your textbook, managerial economics applies microeconomic theory to business decision making. The decision-making tools

Review of Fundamental Mathematics As explained in the Preface and in Chapter 1 of your textbook, managerial economics applies microeconomic theory to business decision making. The decision-making tools

Solutions to Homework Problems for Basic Cost Behavior by David Albrecht

Solutions to Homework Problems for Basic Cost Behavior by David Albrecht Solution to Problem #11 This problem focuses on being able to work with both total cost and average per unit cost. As a brief review,

Solutions to Homework Problems for Basic Cost Behavior by David Albrecht Solution to Problem #11 This problem focuses on being able to work with both total cost and average per unit cost. As a brief review,

Assumptions of CVP Analysis. Objective 1: Contribution Margin Income Statement. Assumptions of CVP Analysis. Contribution Margin Example

Assumptions of CVP Analysis Cost-Volume-Profit Analysis Expenses can be classified as either variable or fixed. CVP relationships are linear over a wide range of production and sales. Sales prices, unit

Assumptions of CVP Analysis Cost-Volume-Profit Analysis Expenses can be classified as either variable or fixed. CVP relationships are linear over a wide range of production and sales. Sales prices, unit

Management Accounting Fundamentals

Management Accounting Fundamentals Module 4 Cost behaviour and cost-volume-profit analysis Lectures and handouts by: Shirley Mauger, HB Comm, CGA Part 1 2 3 Module 4 - Table of Contents Content 4.1 Variable

Management Accounting Fundamentals Module 4 Cost behaviour and cost-volume-profit analysis Lectures and handouts by: Shirley Mauger, HB Comm, CGA Part 1 2 3 Module 4 - Table of Contents Content 4.1 Variable

Module 3: Correlation and Covariance

Using Statistical Data to Make Decisions Module 3: Correlation and Covariance Tom Ilvento Dr. Mugdim Pašiƒ University of Delaware Sarajevo Graduate School of Business O ften our interest in data analysis

Using Statistical Data to Make Decisions Module 3: Correlation and Covariance Tom Ilvento Dr. Mugdim Pašiƒ University of Delaware Sarajevo Graduate School of Business O ften our interest in data analysis

1.1 Introduction. Chapter 1: Feasibility Studies: An Overview

Chapter 1: Introduction 1.1 Introduction Every long term decision the firm makes is a capital budgeting decision whenever it changes the company s cash flows. Consider launching a new product. This involves

Chapter 1: Introduction 1.1 Introduction Every long term decision the firm makes is a capital budgeting decision whenever it changes the company s cash flows. Consider launching a new product. This involves

Management Accounting 303 Segmental Profitability Analysis and Evaluation

Management Accounting 303 Segmental Profitability Analysis and Evaluation Unless a business is a not-for-profit business, all businesses have as a primary goal the earning of profit. In the long run, sustained

Management Accounting 303 Segmental Profitability Analysis and Evaluation Unless a business is a not-for-profit business, all businesses have as a primary goal the earning of profit. In the long run, sustained

10.SHORT-TERM DECISIONS & CAPITAL INVESTMENT APPRAISAL

INDUSTRIAL UNIVERSITY OF HO CHI MINH CITY AUDITING ACCOUNTING FACULTY 10.SHORT-TERM DECISIONS & CAPITAL INVESTMENT APPRAISAL 4 Topic List INDUSTRIAL UNIVERSITY OF HO CHI MINH CITY AUDITING ACCOUNTING FACULTY

INDUSTRIAL UNIVERSITY OF HO CHI MINH CITY AUDITING ACCOUNTING FACULTY 10.SHORT-TERM DECISIONS & CAPITAL INVESTMENT APPRAISAL 4 Topic List INDUSTRIAL UNIVERSITY OF HO CHI MINH CITY AUDITING ACCOUNTING FACULTY

CHAPTER19. Acct202. Managerial Accounting 19-1

CHAPTER19 Managerial Accounting Acct202 19-1 PreviewofCHAPTER19 19-2 Managerial Accounting Basics Managerial accounting, a field of accounting that provides economic and financial information for managers

CHAPTER19 Managerial Accounting Acct202 19-1 PreviewofCHAPTER19 19-2 Managerial Accounting Basics Managerial accounting, a field of accounting that provides economic and financial information for managers

Costs and Decision Making

139 Part 2 Costs and Decision Making Chapter 5 Chapter 6 Chapter 7 Chapter 8 Cost Behavior and Relevant Costs Cost-Volume-Profit Analysis and Variable Costing Short-Term Tactical Decision Making Long-Term

139 Part 2 Costs and Decision Making Chapter 5 Chapter 6 Chapter 7 Chapter 8 Cost Behavior and Relevant Costs Cost-Volume-Profit Analysis and Variable Costing Short-Term Tactical Decision Making Long-Term

Practical Business Application of Break Even Analysis in Graduate Construction Education

Journal of Construction Education Spring 1999, Vol. 4, No. 1, pp. 26-37 Copyright 1999 by the Associated Schools of Construction 1522-8150/99/$3.00/Educational Practice Manuscript Practical Business Application

Journal of Construction Education Spring 1999, Vol. 4, No. 1, pp. 26-37 Copyright 1999 by the Associated Schools of Construction 1522-8150/99/$3.00/Educational Practice Manuscript Practical Business Application

Chapter 3: Cost-Volume-Profit Analysis and Planning

Chapter 3: Cost-Volume-Profit Analysis and Planning Agenda Direct Materials, Direct Labor, and Overhead Traditional vs. Contribution Margin Income Statements Cost-Volume-Profit (CVP) Analysis Profit Planning

Chapter 3: Cost-Volume-Profit Analysis and Planning Agenda Direct Materials, Direct Labor, and Overhead Traditional vs. Contribution Margin Income Statements Cost-Volume-Profit (CVP) Analysis Profit Planning

Management Accounting 243 Pricing Decision Analysis

Management Accounting 243 Pricing Decision Analysis The setting of a price for a product is one of the most important decisions and certainly one of the more complex. A change in price not only directly

Management Accounting 243 Pricing Decision Analysis The setting of a price for a product is one of the most important decisions and certainly one of the more complex. A change in price not only directly

Part 1 : 07/27/10 21:30:31

Question 1 - CIA 593 III-64 - Forecasting Techniques What coefficient of correlation results from the following data? X Y 1 10 2 8 3 6 4 4 5 2 A. 0 B. 1 C. Cannot be determined from the data given. D.

Question 1 - CIA 593 III-64 - Forecasting Techniques What coefficient of correlation results from the following data? X Y 1 10 2 8 3 6 4 4 5 2 A. 0 B. 1 C. Cannot be determined from the data given. D.

Marginal and. this chapter covers...

7 Marginal and absorption costing this chapter covers... This chapter focuses on the costing methods of marginal and absorption costing and compares the profit made by a business under each method. The

7 Marginal and absorption costing this chapter covers... This chapter focuses on the costing methods of marginal and absorption costing and compares the profit made by a business under each method. The

Variable Costs. Breakeven Analysis. Examples of Variable Costs. Variable Costs. Mixed

Breakeven Analysis Variable Vary directly in proportion to activity: Example: if sales increase by 5%, then the Variable will increase by 5% Remain the same, regardless of the activity level Mixed Combines

Breakeven Analysis Variable Vary directly in proportion to activity: Example: if sales increase by 5%, then the Variable will increase by 5% Remain the same, regardless of the activity level Mixed Combines

The Cost of Production

The Cost of Production 1. Opportunity Costs 2. Economic Costs versus Accounting Costs 3. All Sorts of Different Kinds of Costs 4. Cost in the Short Run 5. Cost in the Long Run 6. Cost Minimization 7. The

The Cost of Production 1. Opportunity Costs 2. Economic Costs versus Accounting Costs 3. All Sorts of Different Kinds of Costs 4. Cost in the Short Run 5. Cost in the Long Run 6. Cost Minimization 7. The

Mc Graw Hill Education

Managerial Accounting for Managers F o u r t h Edition Eric W. Noreen, Ph.D., CMA Professor Emeritus University of Washington Peter C. Brewer, Ph.D. Wake Forest University Ray H. Garrison, D.B.A., CPA

Managerial Accounting for Managers F o u r t h Edition Eric W. Noreen, Ph.D., CMA Professor Emeritus University of Washington Peter C. Brewer, Ph.D. Wake Forest University Ray H. Garrison, D.B.A., CPA

Exercise 17-1 (15 minutes)

") Exercise 17-1 (15 minutes) 1. 2002 2001 Sales... 100.0% 100.0 % Less cost of goods sold... 63.2 60.0 Gross margin... 36.8 40.0 Selling expenses... 18.0 17.5 Administrative expenses... 13.6 14.6 Total expenses...

Exercise 17-1 (15 minutes) 1. 2002 2001 Sales... 100.0% 100.0 % Less cost of goods sold... 63.2 60.0 Gross margin... 36.8 40.0 Selling expenses... 18.0 17.5 Administrative expenses... 13.6 14.6 Total expenses...

Chapter 5 Business Expenses

Chapter 5 Business Expenses Key Concepts Trade or business expenses must be ordinary, necessary, and reasonable in amount to be deductible. Accrual-basis taxpayers deduct their expenses when the all-events

Chapter 5 Business Expenses Key Concepts Trade or business expenses must be ordinary, necessary, and reasonable in amount to be deductible. Accrual-basis taxpayers deduct their expenses when the all-events

Identifying Relevant Costs

Relevant Costs for Decision Making Identifying Relevant Costs A relevant cost is a cost that differs between alternatives. An avoidable cost can be eliminated, in whole or in part, by choosing one alternative

Relevant Costs for Decision Making Identifying Relevant Costs A relevant cost is a cost that differs between alternatives. An avoidable cost can be eliminated, in whole or in part, by choosing one alternative

Review of Production and Cost Concepts

Sloan School of Management 15.010/15.011 Massachusetts Institute of Technology RECITATION NOTES #3 Review of Production and Cost Concepts Thursday - September 23, 2004 OUTLINE OF TODAY S RECITATION 1.

Sloan School of Management 15.010/15.011 Massachusetts Institute of Technology RECITATION NOTES #3 Review of Production and Cost Concepts Thursday - September 23, 2004 OUTLINE OF TODAY S RECITATION 1.

FULL COST METHODOLOGY MODEL

FULL COST METHODOLOGY MODEL This cost methodology model was developed using concepts from two State Auditor's Office (SAO) reports, Guide To Implement the Competitive Cost Review Program, October 1992

FULL COST METHODOLOGY MODEL This cost methodology model was developed using concepts from two State Auditor's Office (SAO) reports, Guide To Implement the Competitive Cost Review Program, October 1992

Chapter 6 Cost Allocation and Activity-Based Costing

Chapter 6 Cost Allocation and Activity-Based Costing QUESTIONS 1. Indirect costs are allocated to (1) provide information for decision making, (2) reduce frivolous use of common resources, (3) encourage

Chapter 6 Cost Allocation and Activity-Based Costing QUESTIONS 1. Indirect costs are allocated to (1) provide information for decision making, (2) reduce frivolous use of common resources, (3) encourage

Introduction To Cost Accounting

Page 1 Introduction To Cost Accounting 15.501/516 Accounting Spring 2004 Professor S. Roychowdhury Sloan School of Management Massachusetts Institute of Technology April 28, 2004 6 Outline Overview of

Page 1 Introduction To Cost Accounting 15.501/516 Accounting Spring 2004 Professor S. Roychowdhury Sloan School of Management Massachusetts Institute of Technology April 28, 2004 6 Outline Overview of

There are two basic types of cost accounting systems:

CHAPTER 2 JOB ORDER COSTING Managerial Accounting, Fourth Edition 2-1 Cost Accounting Systems There are two basic types of cost accounting systems: 2-2 LO 1: Explain the characteristics and purposes of

CHAPTER 2 JOB ORDER COSTING Managerial Accounting, Fourth Edition 2-1 Cost Accounting Systems There are two basic types of cost accounting systems: 2-2 LO 1: Explain the characteristics and purposes of

n System Design Job Order Costing n What is Product Costing n Types of Product Costing n When and how to use Job-Order Costing McGraw-Hill /Irwin

2-1 Today s Lecture Management Accounting Lecture 7 (Chapter 2) Systems Design: n System Design Job Order Costing n What is Product Costing n Types of Product Costing n When and how to use n Journal entries

2-1 Today s Lecture Management Accounting Lecture 7 (Chapter 2) Systems Design: n System Design Job Order Costing n What is Product Costing n Types of Product Costing n When and how to use n Journal entries

Discretionary Owner Earnings (%) Firms Analyzed 2011 2,736 2012 2,982 2013 2,979 2014 2,814 2015 2,392

Firms Analyzed 2011 2,736 2012 2,982 2013 2,979 2014 2,814 2015 2,392") Industry Financial Report release date: June 216 ALL US [23822] Plumbing, Heating, and Air-Conditioning Contractors Sector: Construction Sales Class: $5m - $9.99m Contents Income-Expense statement - dollar-based

Industry Financial Report release date: June 216 ALL US [23822] Plumbing, Heating, and Air-Conditioning Contractors Sector: Construction Sales Class: $5m - $9.99m Contents Income-Expense statement - dollar-based

Business and Economic Applications

Appendi F Business and Economic Applications F1 F Business and Economic Applications Understand basic business terms and formulas, determine marginal revenues, costs and profits, find demand functions,

Appendi F Business and Economic Applications F1 F Business and Economic Applications Understand basic business terms and formulas, determine marginal revenues, costs and profits, find demand functions,

how to prepare a profit and loss (income) statement

statement") business builder 3 how to prepare a profit and loss (income) statement amegy bank business resource center how to prepare a profit and loss (income) statement 2 how to prepare a profit and loss (income)

business builder 3 how to prepare a profit and loss (income) statement amegy bank business resource center how to prepare a profit and loss (income) statement 2 how to prepare a profit and loss (income)

BUSINESS BUILDER 3 HOW TO PREPARE A PROFIT AND LOSS (INCOME) STATEMENT

STATEMENT") BUSINESS BUILDER 3 HOW TO PREPARE A PROFIT AND LOSS (INCOME) STATEMENT zions business resource center 2 how to prepare a profit and loss (income) statement A Profit and Loss (P&L) or income statement measures

BUSINESS BUILDER 3 HOW TO PREPARE A PROFIT AND LOSS (INCOME) STATEMENT zions business resource center 2 how to prepare a profit and loss (income) statement A Profit and Loss (P&L) or income statement measures

Inventory Decision-Making

Management Accounting 195 Inventory Decision-Making To be successful, most businesses other than service businesses are required to carry inventory. In these businesses, good management of inventory is

Management Accounting 195 Inventory Decision-Making To be successful, most businesses other than service businesses are required to carry inventory. In these businesses, good management of inventory is

Financial Statements for Manufacturing Businesses

Management Accounting 31 Financial Statements for Manufacturing Businesses Importance of Financial Statements Accounting plays a critical role in decision-making. Accounting provides the financial framework

Management Accounting 31 Financial Statements for Manufacturing Businesses Importance of Financial Statements Accounting plays a critical role in decision-making. Accounting provides the financial framework

Accounting 2910, Summer 2002 Practice Exam 4. 1. The cost of materials entering directly into the manufacturing process is classified as:

Accounting 2910, Summer 2002 Practice Exam 4 1. The cost of materials entering directly into the manufacturing process is classified as: a. direct labor cost b. factory overhead cost c. burden cost d.

Accounting 2910, Summer 2002 Practice Exam 4 1. The cost of materials entering directly into the manufacturing process is classified as: a. direct labor cost b. factory overhead cost c. burden cost d.

Paper 7 Management Accounting

Technician Level Paper 7 Management Accounting Extended Syllabus INTRODUCTION Extended Syllabuses are part of a comprehensive package of support materials offered by SIAT. This package includes past question

Technician Level Paper 7 Management Accounting Extended Syllabus INTRODUCTION Extended Syllabuses are part of a comprehensive package of support materials offered by SIAT. This package includes past question

Acquisition Lesson Plan for the Concept, Topic or Skill---Not for the Day

Acquisition Lesson Plan Concept: Linear Systems Author Name(s): High-School Delaware Math Cadre Committee Grade: Ninth Grade Time Frame: Two 45 minute periods Pre-requisite(s): Write algebraic expressions

Acquisition Lesson Plan Concept: Linear Systems Author Name(s): High-School Delaware Math Cadre Committee Grade: Ninth Grade Time Frame: Two 45 minute periods Pre-requisite(s): Write algebraic expressions

11.3 BREAK-EVEN ANALYSIS. Fixed and Variable Costs

385 356 PART FOUR Capital Budgeting a large number of NPV estimates that we summarize by calculating the average value and some measure of how spread out the different possibilities are. For example, it

385 356 PART FOUR Capital Budgeting a large number of NPV estimates that we summarize by calculating the average value and some measure of how spread out the different possibilities are. For example, it

Understanding Financial Statements. For Your Business

Understanding Financial Statements For Your Business Disclaimer The information provided is for informational purposes only, does not constitute legal advice or create an attorney-client relationship,

Understanding Financial Statements For Your Business Disclaimer The information provided is for informational purposes only, does not constitute legal advice or create an attorney-client relationship,

Professional Development Programme on Enriching Knowledge of the Business, Accounting and Financial Studies (BAFS) Curriculum

Curriculum") Professional Development Programme on Enriching Knowledge of the Business, Accounting and Financial Studies (BAFS) Curriculum Course 1 : Contemporary Perspectives on Accounting Unit 7 : Marginal and Absorption

Professional Development Programme on Enriching Knowledge of the Business, Accounting and Financial Studies (BAFS) Curriculum Course 1 : Contemporary Perspectives on Accounting Unit 7 : Marginal and Absorption

BASIC CONCEPTS AND FORMULAE

12 Marginal Costing BASIC CONCEPTS AND FORMULAE Basic Concepts 1. Absorption Costing: a method of costing by which all direct cost and applicable overheads are charged to products or cost centers for finding

12 Marginal Costing BASIC CONCEPTS AND FORMULAE Basic Concepts 1. Absorption Costing: a method of costing by which all direct cost and applicable overheads are charged to products or cost centers for finding

Replacement Heifers Costs and Return Calculation Decision Aids

Replacement Heifers Costs and Return Calculation Decision Aids The purpose of these replacement heifer cost decision aids is to calculate total production costs and return on investment (ROI) to evaluate

Replacement Heifers Costs and Return Calculation Decision Aids The purpose of these replacement heifer cost decision aids is to calculate total production costs and return on investment (ROI) to evaluate

Blended Value Business Plan Pro Forma Income Statement User Guide

Blended Value Business Plan Pro Forma Income Statement User Guide OVERVIEW A business plan goes beyond the forecasting of a Feasibility Study. It provides details on the multiple factors required to develop

Blended Value Business Plan Pro Forma Income Statement User Guide OVERVIEW A business plan goes beyond the forecasting of a Feasibility Study. It provides details on the multiple factors required to develop

Demand, Supply, and Market Equilibrium

3 Demand, Supply, and Market Equilibrium The price of vanilla is bouncing. A kilogram (2.2 pounds) of vanilla beans sold for $50 in 2000, but by 2003 the price had risen to $500 per kilogram. The price

3 Demand, Supply, and Market Equilibrium The price of vanilla is bouncing. A kilogram (2.2 pounds) of vanilla beans sold for $50 in 2000, but by 2003 the price had risen to $500 per kilogram. The price

Module 2: Job-order costing

Module 2: Job-order costing Required reading Overview Chapter 3, pages 69-99 This module introduces the distinctions between two methods of determining unit costs of production joborder costing and process

Module 2: Job-order costing Required reading Overview Chapter 3, pages 69-99 This module introduces the distinctions between two methods of determining unit costs of production joborder costing and process

Workbook 2 Overheads

Contents Highlights... 2 Quick Practice Session on Overheads... 2 Financial Quiz 2 - Overheads... 3 Learning Zone Overheads... 3 Fixed and Variable costs and Break-even analysis explained... 3 Fixed Costs...

Contents Highlights... 2 Quick Practice Session on Overheads... 2 Financial Quiz 2 - Overheads... 3 Learning Zone Overheads... 3 Fixed and Variable costs and Break-even analysis explained... 3 Fixed Costs...

4. The accountant s product costing art

4. The accountant s product costing art How to move from cost pools to product costs Define an appropriate number of cost pools Each cost pool aggregates costs associated with some set of activities Estimate

4. The accountant s product costing art How to move from cost pools to product costs Define an appropriate number of cost pools Each cost pool aggregates costs associated with some set of activities Estimate

APPENDIX. Interest Concepts of Future and Present Value. Concept of Interest TIME VALUE OF MONEY BASIC INTEREST CONCEPTS

CHAPTER 8 Current Monetary Balances 395 APPENDIX Interest Concepts of Future and Present Value TIME VALUE OF MONEY In general business terms, interest is defined as the cost of using money over time. Economists

CHAPTER 8 Current Monetary Balances 395 APPENDIX Interest Concepts of Future and Present Value TIME VALUE OF MONEY In general business terms, interest is defined as the cost of using money over time. Economists

Chapter 3 Notes Page 1

Chapter 3 Notes Page 1 Job-Order System There are basically two approaches to assign manufacturing costs to products produced or services rendered: Job-Order Costing and Process Costing. The approach that

Chapter 3 Notes Page 1 Job-Order System There are basically two approaches to assign manufacturing costs to products produced or services rendered: Job-Order Costing and Process Costing. The approach that

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

Module 7 Test Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. You are given information about a straight line. Use two points to graph the equation.

Module 7 Test Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. You are given information about a straight line. Use two points to graph the equation.

Chapter 2 Cost Terms, Concepts, and Classifications

Chapter 2 Cost Terms, Concepts, and Classifications Solutions to Questions 2-1 The three major elements of product costs in a manufacturing company are direct materials, direct labour, and manufacturing

Chapter 2 Cost Terms, Concepts, and Classifications Solutions to Questions 2-1 The three major elements of product costs in a manufacturing company are direct materials, direct labour, and manufacturing

The Business Plan and You

The Business Plan and You BUSINESS START-UP For more information, contact: The Business Link Edmonton: 100 10237 104 Street NW Edmonton, Alberta T5J 1B1 Calgary: 250 639 5 Avenue SW Calgary, Alberta T2P

The Business Plan and You BUSINESS START-UP For more information, contact: The Business Link Edmonton: 100 10237 104 Street NW Edmonton, Alberta T5J 1B1 Calgary: 250 639 5 Avenue SW Calgary, Alberta T2P

Marginal Costing and Absorption Costing

Marginal Costing and Absorption Costing Learning Objectives To understand the meanings of marginal cost and marginal costing To distinguish between marginal costing and absorption costing To ascertain

Marginal Costing and Absorption Costing Learning Objectives To understand the meanings of marginal cost and marginal costing To distinguish between marginal costing and absorption costing To ascertain

Discretionary Owner Earnings (%) Firms Analyzed 2011 45 2012 42 2013 41 2014 43 2015 39

Firms Analyzed 2011 45 2012 42 2013 41 2014 43 2015 39") Industry Financial Report release date: June 216 Harrisburg, PA Metro Area [23822] Plumbing, Heating, and Air-Conditioning Contractors Sector: Construction Sales Class: $1m - $2.49m Contents Income-Expense

Industry Financial Report release date: June 216 Harrisburg, PA Metro Area [23822] Plumbing, Heating, and Air-Conditioning Contractors Sector: Construction Sales Class: $1m - $2.49m Contents Income-Expense

Preparing cash budgets

3 Preparing cash budgets this chapter covers... In this chapter we will examine in detail how a cash budget is prepared. This is an important part of your studies, and you will need to be able to prepare

3 Preparing cash budgets this chapter covers... In this chapter we will examine in detail how a cash budget is prepared. This is an important part of your studies, and you will need to be able to prepare