V. DEVELOPING SUSTAINABLE MICROFINANCE SYSTEMS

|

|

|

- Jeremy Reed

- 9 years ago

- Views:

Transcription

1 V. DEVELOPING SUSTAINABLE MICROFINANCE SYSTEMS Introduction Ashok Sharma Senior Financial Economist Asian Development Bank While many factors contribute to poverty, its most obvious manifestation is insufficient household income. Both the extent of income-generating opportunities and ability to respond to such opportunities are determined to a great degree by access to affordable financial services. Increasing the access of poor households to microfinance 1 is therefore being actively pursued worldwide. Once almost exclusively the domain of donors and experimental projects, microfinance has evolved during the last decade with prospects for viability, offering a broader range of services and significant opportunities for expansion. Development practitioners, policy makers, and multilateral and bilateral lenders, recognize that providing efficient microfinance services is important for a variety of reasons. Improved access to microfinance services can enable the poor to smoothout their consumption, manage their risks better, build their assets, develop their microenterprises, enhance their income-earning capacity, and enjoy an improved quality of life. Microfinance services have a significant positive impact on the depth (severity) of poverty and on specific socio-economic variables such as children s schooling, household nutrition status, and women s empowerment. Despite this, about 95 per cent of some 180 million poor households in the Asian and Pacific region still have little access to affordable institutional microfinance services. Significant resources are required to meet the potential demand. This chapter argues that on the supply side there is a need to build microfinance systems that can grow and provide microfinance services on a permanent basis to an increasing number of the poor through domestic resource mobilization. On the demand side, there is a need to invest in social intermediation 2 to enable the poor to optimally utilize microfinance services. The chapter analyses the status of microfinance in Asia and the Pacific, discusses means to develop microfinance systems capable of financing 1 Microfinance is the provision of a range of financial services such as deposits, loans, payment services, money transfers, and insurance to poor and low-income households and their microenterprises. Microfinance institutions (rural banks, cooperatives, NGOs etc.) are defined as institutions whose major business is the provision of microfinance services. 2 Improving the condition for the excluded to access finance, for example, through grass-roots training in group formation and vocational and financial skills. 123

2 their growth for sustainable expansion, and provides an overview of the microfinance activities supported by the Asian Development Bank (ADB). A. MICROFINANCE IN THE ASIAN AND PACIFIC REGION Over 900 million people in about 180 million households in the region are poor, earning less than one dollar a day. More than 670 million poor people live in rural areas. Reliance on secondary occupations in rural areas is increasing as agriculture can no longer meet the income needs of the growing rural population. These occupations include paid employment, micro-enterprises, and services such as carpenters and weavers. The urban poor are engaged in self-employed businesses such as food stalls, tailoring and shoe repair. Women, who are a significant proportion of the poor and suffer disproportionately from poverty, operate many of these microenterprises. Corresponding to the higher rural poverty incidence, most of the microfinance institutions have a rural bias. However, the supply of microfinance to the urban poor has also markedly increased in recent years. In comparison with rural areas, microfinance service delivery in urban areas involves lower costs owing to higher population density as well as better infrastructure and economic opportunities. 1. Demand for microfinance services The poor and low-income households as well as the micro-enterprises they undertake differ greatly in Asia and the Pacific. The collective demand of these groups for financial services is large and the types of services they demand vary across households and micro-enterprises. This large demand and the heterogeneity of services needed across households and micro-enterprises and over time have created scope for commercial financial intermediation. Savings. Poor and low-income households and their micro-enterprises have a large demand for safe and convenient deposit services. The poor households have the capacity and willingness to save for emergencies, investment, consumption, social obligations, education of their children and other purposes. Savings are important for micro-enterprises and provide them with a major source of investment funds. Extensive use of informal savings arrangements by poor households is another indicator of their demand for savings facilities. The demand for deposit services is particularly strong among poor women in the Asian and Pacific region. Microcredit. Demand for microcredit that originates both from households and micro-enterprises is also large. Poor households require microcredit to finance livelihood activities, for consumption smoothening, and to finance non-food expenses for purposes such as education, housing improvements and migration. Many countries in the region have numerous small farms and their operators also require microfinance services. The other source of demand is non-farm micro-enterprises, which cover a 124

3 wide array of activities such as food preparation and processing, weaving, pottery, furniture making and petty trading. Others. The poor are the most vulnerable to economic and physical downturns. As a result, they forego potentially viable income-generating opportunities because of risk aversion. Therefore, the demand for insurance services among the poor is vast. For instance, micro-insurance products offered by microfinance institutions in Nepal have been subscribed to by most of the clients. This shows that the supply of such services creates its own demand because the real demand remains hidden in the absence of suitable products. 2. Supply of microfinance services The microfinance market structure varies significantly across countries depending on their stage of financial development, level of economic development and policy environment. Most commercial banks do not serve the poor because of perceived high risks, high costs involved in small transactions, perceived low relative profitability, and inability of the poor to provide physical collateral. Thus, a segment of the poor households that has viable investment opportunities persists in poverty for lack of access to credit at reasonable cost. Most of the poor households also find it difficult to accumulate financial savings without easy access to safe institutions that provide deposit services. Informal. The supply of microfinance services is dominated by informal sources. Their collective outreach, both breadth and depth, is vast in most countries. They supply mainly short-term credit and charge higher interest rates than semi-formal and formal sources. Because of the relatively greater bargaining power enjoyed by the informal suppliers in general, the terms and conditions under which services are provided do not enable the clients to fully harness economic opportunities. The informal sources operate in highly localized areas. Therefore, their contribution to financial intermediation and improvement of resource allocation is also limited. Semi-formal. Semi-formal sources mainly comprise the NGOs. In virtually all countries NGOs have become important microfinance providers. Their involvement is important because their clients in general are poorer than those reached by many formal institutions, their services are targeted in most countries to serve poor women and services are provided largely on the basis of social collateral. The small average loan sizes of NGOs, which usually range from about $30 to $150 per loan account, suggest that their clients include the poorest. NGOs in some countries are trying to organize themselves into coalitions to improve microfinance standards and self-regulation. Some NGOs plan to graduate into formal financial institutions, illustrating the potential value of the NGO modality for expanding the services to a large number of poor households. Formal. Formal refers to an organized, registered and regulated system of institutions providing microfinance services. The involvement of formal sources in microfinance has increased during the last two decades. This greater involvement has 125

4 stemmed from (a) the expansion of the scope of formal institutions into microfinance through downscaling (for example, Government Savings Bank, Thailand); (b) establishment of linkage programmes with semi-formal sources of different types (Self-help Group-Bank Linkage Programme, India); (c) the emergence of formal institutions focused on microfinance (for example, Grameen Bank of Bangladesh and Khushhalibank in Pakistan); (d) reforms of state-owned financial institutions (for example, unit desas of Bank Rakyat Indonesia); (e) the introduction of microfinance programmes by the governments through non-financial institutions (for example, Viet Nam Womens Union); and (f) entry of private sector institutions (for example, Badan kredit-desas owned by Indonesian villagers). Cooperatives are also playing a significant role as financial intermediaries in the region, particularly in India, Sri Lanka, Thailand and Viet Nam. However, the formal operations concentrate mostly on providing credit facilities, and savings mobilization has yet to receive adequate attention, with few exceptions. 3. Major achievements in microfinance The microfinance institutions and other microfinance providers have expanded their outreach from a few thousand clients in the 1970s to over 10 million in the late 1990s. The developments in microfinance in Asia and the Pacific have set in motion a process of change from an activity that was entirely subsidy dependent to one that can be a viable business. (a) The myth that poor households cannot and do not save has been shattered. Savings can be successfully mobilized from poor households. (b) Poor, especially poor women, have emerged as creditworthy clients, enabling microfinance service delivery at low transaction costs without relying on physical collateral. (c) Microfinance services have strengthened the social and human capital of the poor, particularly women, at the household, enterprise and community level. (d) Sustainable delivery of microfinance services on a large scale in some countries has generated positive developments in microfinance policies, practices and institutions. (e) Microfinance services have triggered a process toward the broadening and deepening of rural financial markets. 4. Major challenges The achievement in microfinance in the region has been impressive relative to the status in the 1970s. However, a number of major problems remain. (a) Policy environment Despite general improvement in the policy environment for financial sector programmes, the policy environment for microfinance in many countries remains unfavourable for sustainable growth in microfinance operations. For example, in countries such as Viet Nam and China, ceilings on interest rates limit the ability of microfinance institutions to expand and diversify. Governments continue to intervene in 126

; and (f) entry of private sector institutions (for example, Badan kredit-desas owned by Indonesian villagers).")

5 microfinance to address the perceived market failure through channelling microcredit to target groups that are considered to have been underserved by the existing institutions. Furthermore, government programmes with subsidized interest rates and poor loan collection rates undermine sustainable development of microfinance. As a result, most countries are crowded with poorly performing government microfinance programmes that distort the market, discourage private sector institutions from entering the industry, and affects the integration of microfinance into the financial sector. (b) Inadequate financial infrastructure Inadequate financial infrastructure (legal, information, and supervision and regulation) is another major problem. Most governments have focused on creating institutions or special programmes to disburse funds to the poor with little attention to building the financial infrastructure that supports, strengthens and ensures their sustainability. Lack of a legal framework conducive for the emergence and sustainable growth of small-scale microfinance institutions and corresponding supervisory and regulatory systems have impeded the expansion of market-based microfinance services by limiting their access to commercial sources of funding. (c) Limited retail level institutional capacity Most retail level institutions do not have adequate capacity to expand the scope and outreach of sustainable microfinance services. Many institutions lack the capacity to leverage funds, including public deposits, in commercial markets and are unable to provide a range of products and services compatible with client characteristics. In the absence of an adequate network and delivery mechanisms, many microfinance institutions are unable to cost-effectively reach the poorest of the poor, particularly those concentrated in resource-poor areas and areas with low population densities. (d) Inadequate emphasis on financial viability Inadequate emphasis on financial viability is the most serious problem of microfinance institutions in the region. This prevails among many NGOs, governmentdirected microcredit programmes, state-owned banks, and cooperatives providing microfinance services. As a result, only a few microfinance institutions are sustainable; most are not moving toward sustainability nor reducing subsidy dependence. Viability is important from an equity perspective because only viable institutions can leverage funds in the market to serve a significant number of clients. (e) Inadequate investment in agriculture and rural development Agricultural growth, which underpins much of the growth in the rural non-farm subsector, significantly influences rural financial market development. Inadequate investment in the sector is a major constraint on the development of sustainable microfinance services. The insufficient investments in physical infrastructure (especially irrigation; roads; electricity; and support services for marketing, business development and extension) continue to increase the risk and cost of microfinance and particularly discourage private investments in the provision of microfinance services on 127

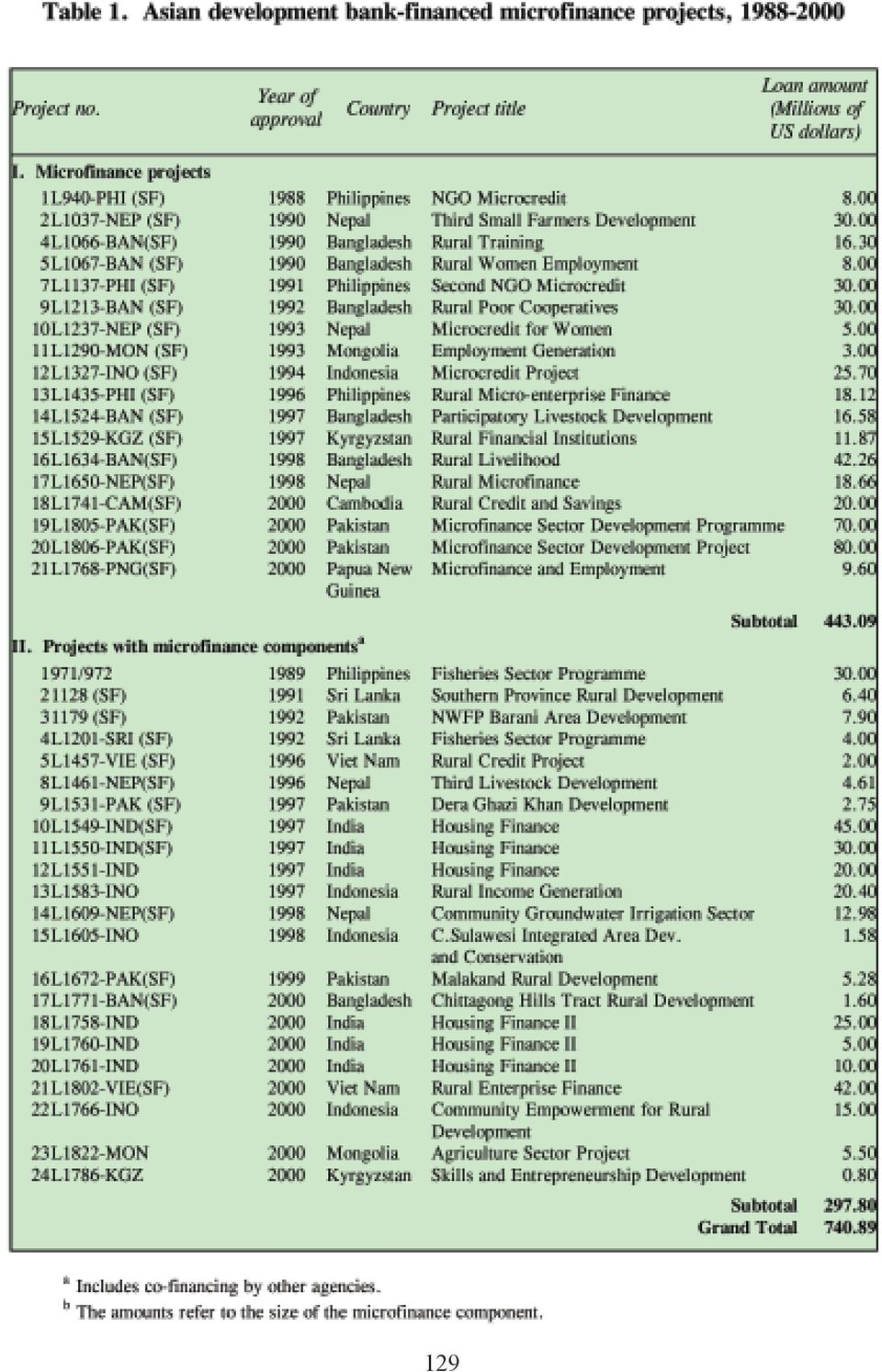

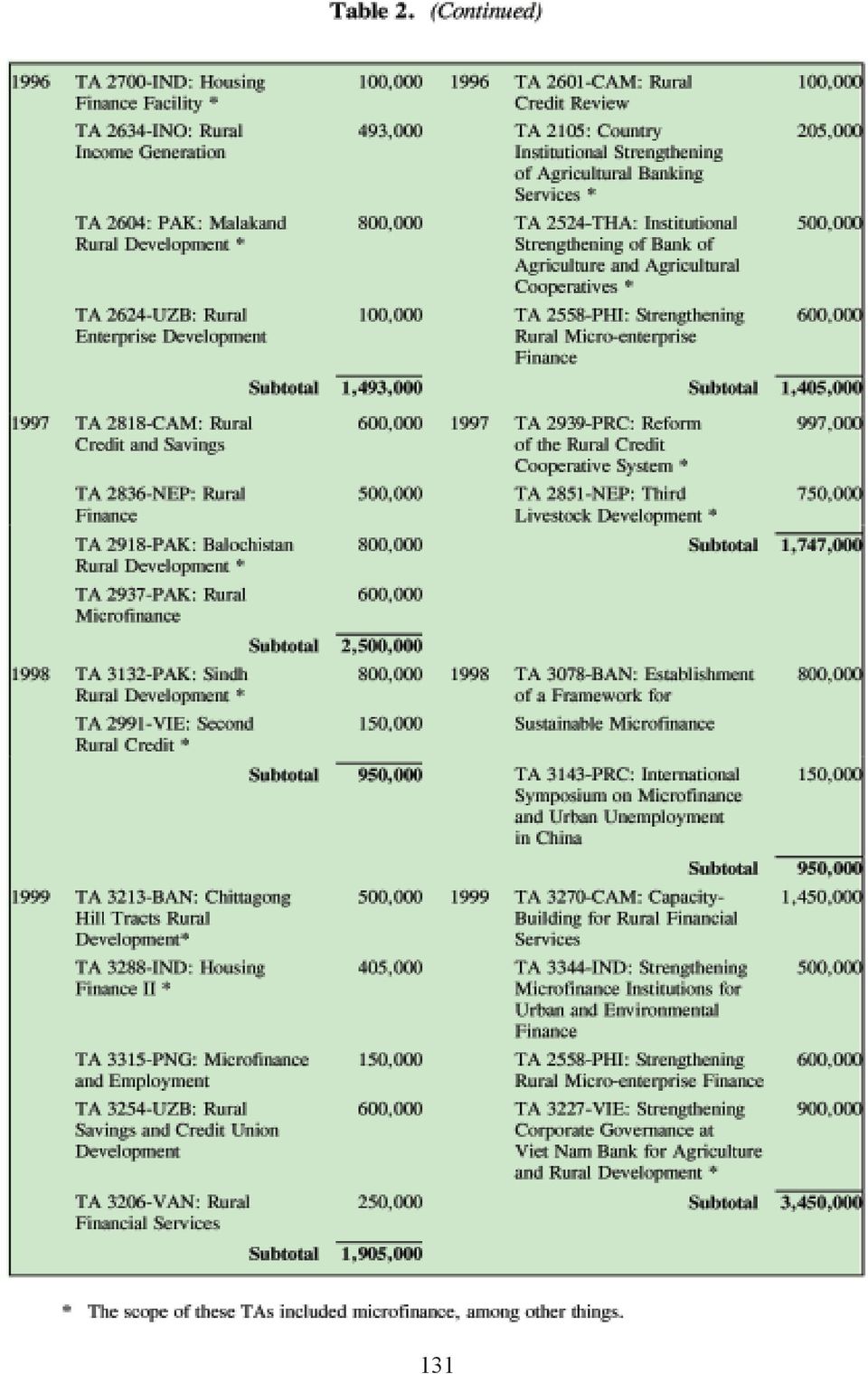

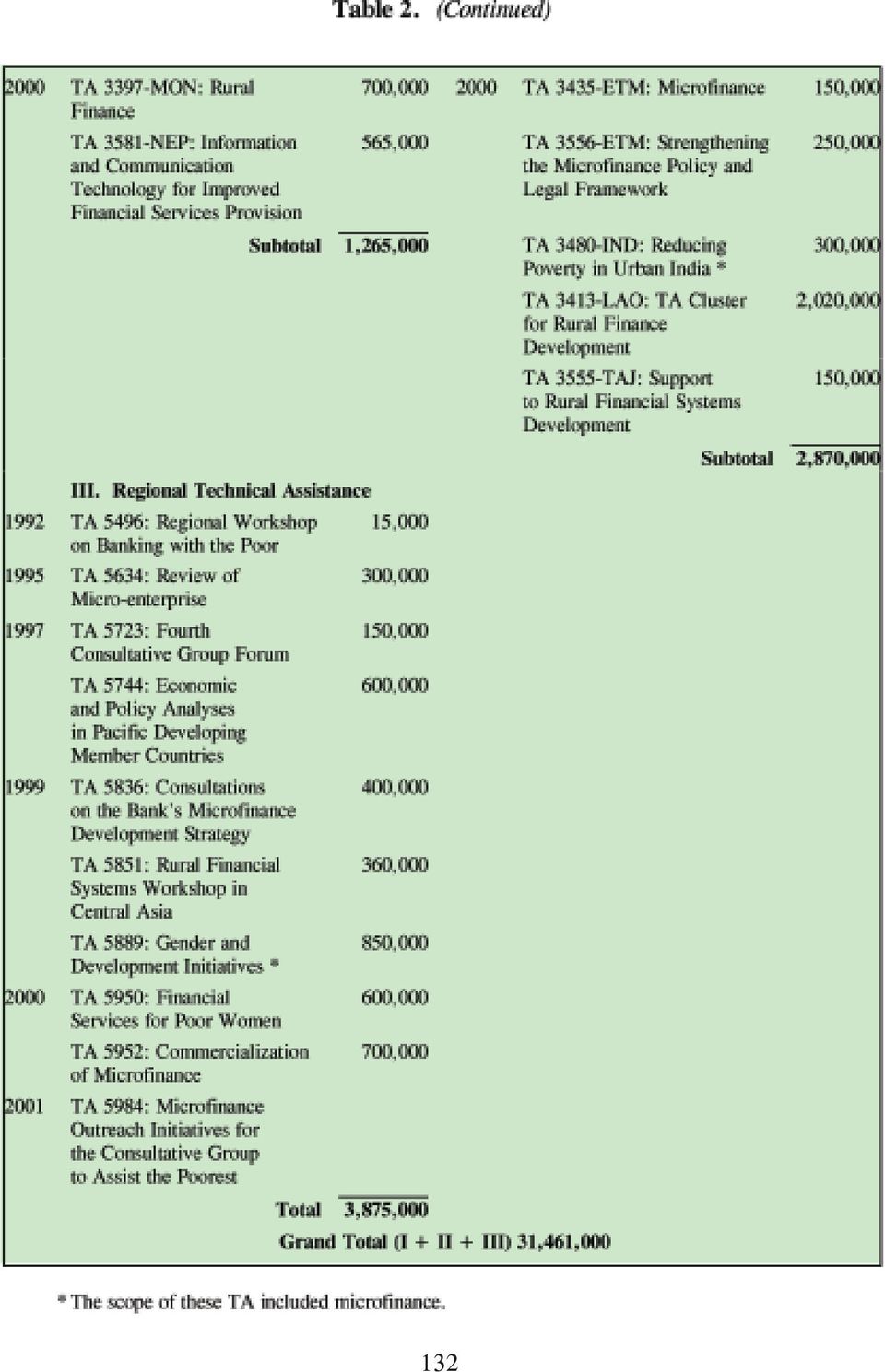

6 a significant scale. In addition, in the absence of economic opportunities created by growth-inducing processes, microfinance cannot be expected to play a significant role in poverty reduction. (f) Inadequate investment in social intermediation The low level of social development, a distinctive characteristic of the poor in Asia and the Pacific is another major constraint. This is particularly true with respect to the poorest, women in poor households, the poor in resource-poor and remote areas, and ethnic minorities. The development of sustainable microfinance to reach a large segment of the potential market requires supporting social intermediation on a large scale. Private sector investments in social intermediation are unlikely in view of the externalities associated with such investments. 5. Lessons learned Microfinance is a critical element of the overarching poverty reduction objective of ADB. During the period , ADB approved 21 microfinance projects and 24 projects with microfinance components totalling $741 million (table 1). Over the same period, 60 technical assistance projects totalling $31 million were also approved for social mobilization, training of clients, and institutional strengthening (table 2). Increasing attention is being given by ADB to sector analysis and policy dialogue for establishing self-financing microfinance systems, as resources required to serve the potential market are far beyond what funding agencies and governments can provide. In general, the early microfinance projects did not make a significant poverty reduction impact because of their limited outreach. There was no mechanism to sustain the positive impact on a small number of clients beyond the project period. Poor infrastructure, sluggish agricultural growth, and limited markets imposed serious limitations on the potential for broad-based growth in rural areas and access to credit could contribute little to permanent improvements in income for clients of microfinance projects under such conditions. Thus, to maximize their development impact, it is essential to integrate microfinance services with other critical measures aimed at reducing poverty. Other lessons learned include: (a) (b) (c) Microfinance is an effective way to assist and empower poor women, who make up a significant proportion of the poor and suffer disproportionately from poverty; Microfinance clients are more concerned about access to services that are compatible with their requirements than about the cost of the services; Social mobilization is necessary to introduce the poor to a market-oriented institutional environment. This is particularly true for poor women and the poorest of the poor. It is important, however, to distinguish between financial intermediation and social intermediation in designing support programmes; 128

7 129

8 (d) (e) (f) Given the diversity of demand for financial services, a broad range of institutional types is required to expand outreach; Expansion of the outreach of savings services can have a potentially significant impact on both institutional sustainability and poverty reduction; Adoption of financial system development is the key to achieving sustainable results and to maximizing development impact. This approach emphasizes an enabling policy environment, financial infrastructure, and the development 130

9 131

10 132

11 (g) (h) of viable microfinance institutions that can provide a variety of financial services, not just credit; Strong retail institutions committed to outreach and sustainability are essential for extending the permanent reach of financial services and for a significant impact on poverty reduction. Thus, building the capacity of institutions with a commitment to reach the poor is vital; Microfinance can contribute to the development of the overall financial system through the integration of financial markets. The collective experience of ADB and other funding agencies confirms that microfinance can play an important role in poverty reduction, and the economic and social benefits can be large. The challenge is to mainstream good practice in microfinance operations and increase outreach to the poor on a sustainable basis. Experience also indicates the importance of integrating microfinance operations with the broader financial system to sustain outreach. B. TOWARDS A SUSTAINABLE MICROFINANCE SYSTEM To realize the poverty reduction potential of microfinance, substantial continuing resources are required to provide institutional microfinance services to the potential clients who are currently outside formal finance in the Asian and Pacific region. Efficient institutional and market mechanisms are needed whereby funds can be sourced and allocated efficiently through appropriately designed and priced services to the poor for profitable investment in agriculture and micro-enterprises. Hence, there is a need to catalyse the growth in supply of sustainable microfinance services and strengthen the capacity of the potential clients to access the services. This can be facilitated through support for the following mutually reinforcing areas: Creating a conducive policy environment Developing critical financial infrastructure Developing viable microfinance institutions Pro-poor innovations in financial technology Social intermediation 1. Policy environment In many countries, the lack of an enabling policy environment for microfinance continues to be a major constraint. Relevant policy reforms include undertaking interest rate reforms for microcredit and savings, creating an environment sufficiently flexible to accommodate a wide array of microfinance service providers to meet the diverse demand, and redefining the role of the state and the central banks in microfinance development to facilitate the participation of private sector financial institutions. Given that non-financial policies such as agricultural pricing and taxation of micro-enterprises also have a critical role in the sustainable development of microfinance, the policy 133

12 reforms need to be extended to address such issues where they constitute significant constraints. 2. Financial infrastructure Microfinance institutions can develop sustainable commercial services on a permanent basis and expand their scope of operations and outreach only if they operate within an appropriate financial infrastructure, such as information systems and training facilities. The legal framework and supervision and regulation of microfinance institutions, including self-regulation and performance standards need to be established to facilitate sound growth and improve the capacity of microfinance institutions to leverage funds in the market and provide competition. However, legal and regulatory systems should not discourage financial innovations, stunt institutional growth, and prevent the emergence of a diverse set of dynamic institutions. Legal barriers preventing banks from establishing business relationships with informal or semiformal bodies, such as community-based organizations or self-help groups, will need to be removed. 3. Developing viable microfinance institutions Viability is critical for expanding the outreach of microfinance institutions to achieve the primary objective of poverty reduction. The institutional development support for viability needs to encompass (a) ownership and governance, (b) diversified products and services, (c) management information systems and accounting policies and practices, (d) management of portfolio quality and growth, (e) systems, procedures and financial technology for reducing transaction costs, and (f) training facilities. In countries where state-owned agricultural and rural development banks continue to undermine the development of sustainable microfinance operations, reform of such banks is necessary. In some circumstances, especially in transitional economies that lack appropriate institutions to efficiently provide microfinance, new institutions may be needed. 4. Pro-poor innovations Those in resource-poor and low-population density areas, the poorest of the poor, and ethnic minorities often tend to be excluded by financial institutions because of risk-return considerations, although the social returns to reaching these clients may be high. Therefore, it is important to support microfinance institutions and other financial institutions to expand the services to these categories through innovative programmes, the development of financial technology that contribute to breaking these barriers through pilot projects and other measures that aim at establishing linkages between formal financial institutions and informal service providers. 5. Social intermediation Investment in social intermediation is necessary to increase the capacity of the poor to access and productively use microfinance services. Such investments, among other things, should support (a) awareness-building programmes on a broad range of microfinance services; (b) information dissemination on service providers; (c) basic 134

13 literacy, numeracy and skills training for women, ethnic minorities, and other disadvantaged groups; and (d) social mobilization for the formation of community-based organizations and solidarity groups to actively participate in microfinance markets. C. CONCLUSIONS The landscape of microfinance is changing as a result of increasing understanding of how the poor use money and their diverse demands for financial services. Correspondingly, the microfinance industry is evolving into an increasingly commercial operation to serve a larger segment of the potential market. A number of challenges need to be overcome to facilitate and accelerate this process to realize the vast potential of microfinance. This calls for a comprehensive approach, as outlined above, that takes cognizance of the diversity of microfinance development issues across countries. ADB interventions in support of microfinance pursue this approach to catalyse the development of sustainable microfinance systems in the region. With a view to leveraging its support, ADB is coordinating with other funding agencies involved in microfinance and enhancing the involvement of its private sector operations in microfinance. 135

14 136

Finance for the Poor: Microfinance Development Strategy

Finance for the Poor: Microfinance Development Strategy Finance for the Poor: Microfinance Development Strategy 2000 Contents Introduction 1 Need for a development strategy for microfinance 7 Microfinance

Finance for the Poor: Microfinance Development Strategy Finance for the Poor: Microfinance Development Strategy 2000 Contents Introduction 1 Need for a development strategy for microfinance 7 Microfinance

Understanding and Dealing with High Interest Rates on Microcredit

Understanding and Dealing with High Interest Rates on Microcredit A Note to Policy Makers in the Asia and Pacific Region Nimal A. Fernando Understanding and Dealing with High Interest Rates on Microcredit

Understanding and Dealing with High Interest Rates on Microcredit A Note to Policy Makers in the Asia and Pacific Region Nimal A. Fernando Understanding and Dealing with High Interest Rates on Microcredit

SECTOR ASSESSMENT (SUMMARY): FINANCE

: FINANCE") Microfinance Expansion Project (RRP PNG 44304) Sector Road Map SECTOR ASSESSMENT (SUMMARY): FINANCE 1. Sector Performance, Problems, and Opportunities 1. During 2000 2006, the growth in population in Papua

Microfinance Expansion Project (RRP PNG 44304) Sector Road Map SECTOR ASSESSMENT (SUMMARY): FINANCE 1. Sector Performance, Problems, and Opportunities 1. During 2000 2006, the growth in population in Papua

FINANCING SMALL AND MICRO ENTERPRISES IN AFRICA 2. THE CHARACTERISTICS OF MICROFINANCE ARRANGEMENTS IN AFRICA

FINANCING SMALL AND MICRO ENTERPRISES IN AFRICA 1. THE ISSUES There is the perception that the demand for finance by small enterprises far exceeds the supply, but recent research in 4 countries shows that

FINANCING SMALL AND MICRO ENTERPRISES IN AFRICA 1. THE ISSUES There is the perception that the demand for finance by small enterprises far exceeds the supply, but recent research in 4 countries shows that

MICROFINANCE. Orrick, Herrington & Sutcliffe. Legal guide. Type: Published: Last Updated: Keywords: Microfinance; lending; development.

MICROFINANCE Orrick, Herrington & Sutcliffe Type: Published: Last Updated: Keywords: Legal guide Microfinance; lending; development. This document provides general information and comments on the subject

MICROFINANCE Orrick, Herrington & Sutcliffe Type: Published: Last Updated: Keywords: Legal guide Microfinance; lending; development. This document provides general information and comments on the subject

VALUE CHAIN DEVELOPMENT Training activities & Tools

VALUE CHAIN DEVELOPMENT Training activities & Tools VALUE CHAIN DEVELOPMENT Overview The question is thus not if, but how to integrate in value chains in a way that allows for incorporation of a growing

VALUE CHAIN DEVELOPMENT Training activities & Tools VALUE CHAIN DEVELOPMENT Overview The question is thus not if, but how to integrate in value chains in a way that allows for incorporation of a growing

ACCESS TO FINANCIAL SERVICES IN MALAWI: POLICIES AND CHALLENGES

UNITED NATIONS CONFERENCE ON TRADE AND DEVELOPMENT Expert Meeting on THE IMPACT OF ACCESS TO FINANCIAL SERVICES, INCLUDING BY HIGHLIGHTING THE IMPACT ON REMITTANCES ON DEVELOPMENT: ECONOMIC EMPOWERMENT

UNITED NATIONS CONFERENCE ON TRADE AND DEVELOPMENT Expert Meeting on THE IMPACT OF ACCESS TO FINANCIAL SERVICES, INCLUDING BY HIGHLIGHTING THE IMPACT ON REMITTANCES ON DEVELOPMENT: ECONOMIC EMPOWERMENT

SECTOR ASSESSMENT (SUMMARY): MICRO, SMALL AND MEDIUM-SIZED ENTERPRISE DEVELOPMENT 1 Sector Road Map 1. Sector Performance, Problems, and Opportunities

: MICRO, SMALL AND MEDIUM-SIZED ENTERPRISE DEVELOPMENT 1 Sector Road Map 1. Sector Performance, Problems, and Opportunities") Small Business and Entrepreneurship Development Project (RRP UZB 42007-014) SECTOR ASSESSMENT (SUMMARY): MICRO, SMALL AND MEDIUM-SIZED ENTERPRISE DEVELOPMENT 1 Sector Road Map 1. Sector Performance, Problems,

Small Business and Entrepreneurship Development Project (RRP UZB 42007-014) SECTOR ASSESSMENT (SUMMARY): MICRO, SMALL AND MEDIUM-SIZED ENTERPRISE DEVELOPMENT 1 Sector Road Map 1. Sector Performance, Problems,

Financial inclusion and poverty reduction: the role of financial inclusion in achieving the Millennium Development Goals.

Financial inclusion and poverty reduction: the role of financial inclusion in achieving the Millennium Development Goals. 1. It is indeed a source of deep concern that the number of people living in extreme

Financial inclusion and poverty reduction: the role of financial inclusion in achieving the Millennium Development Goals. 1. It is indeed a source of deep concern that the number of people living in extreme

Facilitating Remittances to Help Families and Small Businesses

G8 ACTION PLAN: APPLYING THE POWER OF ENTREPRENEURSHIP TO THE ERADICATION OF POVERTY The UN Commission on the Private Sector and Development has stressed that poverty alleviation requires a strong private

G8 ACTION PLAN: APPLYING THE POWER OF ENTREPRENEURSHIP TO THE ERADICATION OF POVERTY The UN Commission on the Private Sector and Development has stressed that poverty alleviation requires a strong private

micronote #23 Leasing: A Potential Solution for SME Expansion and Rural Financial Sector Deepening

micronote #23 Leasing: A Potential Solution for SME Expansion and Rural Financial Sector Deepening A Case Study of Russia An animal fodder production company leases equipment (photo above) outside Krasnodar,

micronote #23 Leasing: A Potential Solution for SME Expansion and Rural Financial Sector Deepening A Case Study of Russia An animal fodder production company leases equipment (photo above) outside Krasnodar,

Current challenges in delivering social security health insurance

International Social Security Association Afric ISSA Meeting of Directors of Social Security Organizations in Asia and the Pacific Seoul, Republic of Korea, 9-11 November 2005 Current challenges in delivering

International Social Security Association Afric ISSA Meeting of Directors of Social Security Organizations in Asia and the Pacific Seoul, Republic of Korea, 9-11 November 2005 Current challenges in delivering

Annex I ROLE OF THE INFORMAL SECTOR

Annex I ROLE OF THE INFORMAL SECTOR A. Background 1. Role and challenges of the informal sector during economic downturns Chapter I discusses in detail the increase in unemployment as a direct result of

Annex I ROLE OF THE INFORMAL SECTOR A. Background 1. Role and challenges of the informal sector during economic downturns Chapter I discusses in detail the increase in unemployment as a direct result of

SECTOR ASSESSMENT (SUMMARY): EDUCATION 1

: EDUCATION 1") Country Partnership Strategy: Bangladesh, 2011 2015 SECTOR ASSESSMENT (SUMMARY): EDUCATION 1 Sector Road Map 1. Sector Performance, Problems, and Opportunities 1. Bangladesh has made considerable progress

Country Partnership Strategy: Bangladesh, 2011 2015 SECTOR ASSESSMENT (SUMMARY): EDUCATION 1 Sector Road Map 1. Sector Performance, Problems, and Opportunities 1. Bangladesh has made considerable progress

Village banks: the new generation. How IFAD helped FINCA set its village banking programmes on the road to commercialization

Village banks: the new generation How IFAD helped FINCA set its village banking programmes on the road to commercialization What is FINCA? FINCA International, Inc. provides financial services to the world

Village banks: the new generation How IFAD helped FINCA set its village banking programmes on the road to commercialization What is FINCA? FINCA International, Inc. provides financial services to the world

SECTOR ASSESSMENT (SUMMARY): FINANCE 1. 1. Sector Performance, Problems, and Opportunities

: FINANCE 1. 1. Sector Performance, Problems, and Opportunities") Country Partnership Strategy: Bangladesh, 2011 2015 SECTOR ASSESSMENT (SUMMARY): FINANCE 1 Sector Road Map 1. Sector Performance, Problems, and Opportunities 1. The finance sector in Bangladesh is diverse,

Country Partnership Strategy: Bangladesh, 2011 2015 SECTOR ASSESSMENT (SUMMARY): FINANCE 1 Sector Road Map 1. Sector Performance, Problems, and Opportunities 1. The finance sector in Bangladesh is diverse,

Banco Santander HOUSING MICROFINANCE WITH CONSTRUCTION TECHNICAL ASSISTANCE CASE STUDY:

A woman in front of her improved house. HOUSING MICROFINANCE WITH CONSTRUCTION TECHNICAL ASSISTANCE CASE STUDY: Banco Santander HFHI/LAC Executive summary This case study presents key lessons that emerged

A woman in front of her improved house. HOUSING MICROFINANCE WITH CONSTRUCTION TECHNICAL ASSISTANCE CASE STUDY: Banco Santander HFHI/LAC Executive summary This case study presents key lessons that emerged

Community Investing in Canada. Written by: Susannah Cameron, Executive Director Canadian Community Investment Network Cooperative Canada

Community Investing in Canada Written by: Susannah Cameron, Executive Director Canadian Community Investment Network Cooperative Canada TABLE OF CONTENTS Introduction... 1 Describing the community investing

Community Investing in Canada Written by: Susannah Cameron, Executive Director Canadian Community Investment Network Cooperative Canada TABLE OF CONTENTS Introduction... 1 Describing the community investing

Towards 2017 Better Work Phase III Strategy

Towards 2017 Better Work Phase III Strategy Towards 2017 Better Work Phase III Strategy Promoting Good Working Conditions Across the International Garment Industry Problem Analysis Sixty million workers

Towards 2017 Better Work Phase III Strategy Towards 2017 Better Work Phase III Strategy Promoting Good Working Conditions Across the International Garment Industry Problem Analysis Sixty million workers

SECTOR ASSESSMENT: MICROFINANCE

Microfinance Development Program Cluster (Subprogram 1) (RRP VIE 42235-01) A. Overall Sector Context SECTOR ASSESSMENT: MICROFINANCE 1. Poverty Reduction Objectives and Measures. About 72% of the population

Microfinance Development Program Cluster (Subprogram 1) (RRP VIE 42235-01) A. Overall Sector Context SECTOR ASSESSMENT: MICROFINANCE 1. Poverty Reduction Objectives and Measures. About 72% of the population

REMARKS BY H.E. MARTHA POBEE ON WOMEN AND YOUTH ENTREPRENEURSHIP IN AFRICA: THE IMPACT OF ENTREPRENEURIAL EDUCATION ON DEVELOPMENT

REMARKS BY H.E. MARTHA POBEE ON WOMEN AND YOUTH ENTREPRENEURSHIP IN AFRICA: THE IMPACT OF ENTREPRENEURIAL EDUCATION ON DEVELOPMENT UNITED NATIONS, NEW YORK, 13TM JUNE, 2016 I thank the co-sponsors for

REMARKS BY H.E. MARTHA POBEE ON WOMEN AND YOUTH ENTREPRENEURSHIP IN AFRICA: THE IMPACT OF ENTREPRENEURIAL EDUCATION ON DEVELOPMENT UNITED NATIONS, NEW YORK, 13TM JUNE, 2016 I thank the co-sponsors for

The Effective Use of Remittances in Promoting Economic Development. by Gloria Moreno-Fontes Chammartin [email protected]

The Effective Use of Remittances in Promoting Economic Development by Gloria Moreno-Fontes Chammartin [email protected] Positive Effect on the Economies and Development Prospects of Countries of Origin 1.

The Effective Use of Remittances in Promoting Economic Development by Gloria Moreno-Fontes Chammartin [email protected] Positive Effect on the Economies and Development Prospects of Countries of Origin 1.

Capacity Statement Youth Enterprise and Vocational Training 1

Capacity Statement Youth Enterprise and Vocational Training 1 Nearly 90% of today s youth, those aged 15 to 24, live in developing countries 2, and these youth represent more than 40% of the world s unemployed

Capacity Statement Youth Enterprise and Vocational Training 1 Nearly 90% of today s youth, those aged 15 to 24, live in developing countries 2, and these youth represent more than 40% of the world s unemployed

FEED THE FUTURE LEARNING AGENDA

FEED THE FUTURE LEARNING AGENDA OBJECTIVE OF THE LEARNING AGENDA USAID s Bureau of Food Security will develop Feed the Future s (FTF) Learning Agenda, which includes key evaluation questions related to

FEED THE FUTURE LEARNING AGENDA OBJECTIVE OF THE LEARNING AGENDA USAID s Bureau of Food Security will develop Feed the Future s (FTF) Learning Agenda, which includes key evaluation questions related to

Chapter 1. What is Poverty and Why Measure it?

Chapter 1. What is Poverty and Why Measure it? Summary Poverty is pronounced deprivation in well-being. The conventional view links well-being primarily to command over commodities, so the poor are those

Chapter 1. What is Poverty and Why Measure it? Summary Poverty is pronounced deprivation in well-being. The conventional view links well-being primarily to command over commodities, so the poor are those

5. Industrial and sector strategies

5. Industrial and sector strategies 5.1 Issues identified by the Accelerated and Shared Growth Initiative for South Africa (AsgiSA) Industrial policy has three core aims, namely: creation and smaller enterprises.

5. Industrial and sector strategies 5.1 Issues identified by the Accelerated and Shared Growth Initiative for South Africa (AsgiSA) Industrial policy has three core aims, namely: creation and smaller enterprises.

As of 2010, an estimated 61 million students of primary school age 9% of the world total - are out of school vi.

YOUTH AND EDUCATION HIGHLIGHTS 10.6% of the world s youth (15-24 years old) are non-literate i. Data from 2011 indicates that in developing countries, the percentage of non-literate youth is 12.1%, with

YOUTH AND EDUCATION HIGHLIGHTS 10.6% of the world s youth (15-24 years old) are non-literate i. Data from 2011 indicates that in developing countries, the percentage of non-literate youth is 12.1%, with

Health Promotion, Prevention, Medical care, Rehabilitation under the CBR Matrix heading of "Health

Health Promotion, Prevention, Medical care, Rehabilitation under the CBR Matrix heading of "Health Dr Deepthi N Shanbhag Assistant Professor Department of Community Health St. John s Medical College Bangalore

Health Promotion, Prevention, Medical care, Rehabilitation under the CBR Matrix heading of "Health Dr Deepthi N Shanbhag Assistant Professor Department of Community Health St. John s Medical College Bangalore

Investing in rural people in Indonesia

IFAD/Roger Arnold Investing in rural people in Indonesia Rural poverty in Indonesia Indonesia is the largest economy in South-East Asia and has progressed rapidly over the past decade into a dynamic, highly

IFAD/Roger Arnold Investing in rural people in Indonesia Rural poverty in Indonesia Indonesia is the largest economy in South-East Asia and has progressed rapidly over the past decade into a dynamic, highly

The Impact of Interest Rate Ceilings on Microfinance Industry

The Impact of Interest Rate Ceilings on Microfinance Industry Ali Saleh Alshebami School of Commerce & Management Science, SRTM University, India E-mail: [email protected] Prof. D. M. Khandare School

The Impact of Interest Rate Ceilings on Microfinance Industry Ali Saleh Alshebami School of Commerce & Management Science, SRTM University, India E-mail: [email protected] Prof. D. M. Khandare School

iii. Vision: promoting Decent Work for Afghan workers (men and women) overseas and regulating foreign workers in Afghanistan.

overseas and regulating foreign workers in Afghanistan.") WORKING GROUP PAPER ON ECONOMIC DEVELOPMENT (LABOR MIGRATION) 1 Table of Contents 1- Introduction... 3 2- Importance of regional Cooperation... 3 3- Five priority areas for regional cooperation (inc recommendations...

WORKING GROUP PAPER ON ECONOMIC DEVELOPMENT (LABOR MIGRATION) 1 Table of Contents 1- Introduction... 3 2- Importance of regional Cooperation... 3 3- Five priority areas for regional cooperation (inc recommendations...

Fact Sheet: Youth and Education

Fact Sheet: Youth and Education 11% of the world s youth (15-24 years old) are non-literate. Data from 2005-2008 indicates that in developing countries, the percentage of nonliterate youth is 13%, with

Fact Sheet: Youth and Education 11% of the world s youth (15-24 years old) are non-literate. Data from 2005-2008 indicates that in developing countries, the percentage of nonliterate youth is 13%, with

Education for All An Achievable Vision

Education for All An Achievable Vision Education for All Education is a fundamental human right. It provides children, youth and adults with the power to reflect, make choices and enjoy a better life.

Education for All An Achievable Vision Education for All Education is a fundamental human right. It provides children, youth and adults with the power to reflect, make choices and enjoy a better life.

WORLD HEALTH ORGANIZATION

WORLD HEALTH ORGANIZATION FIFTY-SIXTH WORLD HEALTH ASSEMBLY A56/27 Provisional agenda item 14.18 24 April 2003 International Conference on Primary Health Care, Alma-Ata: twenty-fifth anniversary Report

WORLD HEALTH ORGANIZATION FIFTY-SIXTH WORLD HEALTH ASSEMBLY A56/27 Provisional agenda item 14.18 24 April 2003 International Conference on Primary Health Care, Alma-Ata: twenty-fifth anniversary Report

SECTOR ASSESMENT (SUMMARY): EDUCATION 1

: EDUCATION 1") Country Partnership Strategy: Viet Nam, 2012 2015 SECTOR ASSESMENT (SUMMARY): EDUCATION 1 Sector Road Map 1. Sector Performance, Problems, and Opportunities 1. Country context. In Viet Nam, education is

Country Partnership Strategy: Viet Nam, 2012 2015 SECTOR ASSESMENT (SUMMARY): EDUCATION 1 Sector Road Map 1. Sector Performance, Problems, and Opportunities 1. Country context. In Viet Nam, education is

Business Opportunities Fair

Business Opportunities Fair Increasing Consulting Capability in ADB s Developing Member Countries March 2-3 2011 Hamid Sharif Principal Director Central Operations Services Office Asian Development Bank

Business Opportunities Fair Increasing Consulting Capability in ADB s Developing Member Countries March 2-3 2011 Hamid Sharif Principal Director Central Operations Services Office Asian Development Bank

Arab Republic of Egypt: Commercial Microfinance The National Bank for Development

Arab Republic of Egypt: Commercial Microfinance The National Bank for Development There is a large unmet demand for microfinance services among the entrepreneurial poor in Egypt. It is estimated that Egypt

Arab Republic of Egypt: Commercial Microfinance The National Bank for Development There is a large unmet demand for microfinance services among the entrepreneurial poor in Egypt. It is estimated that Egypt

Kyrgyz Republic: Women s Entrepreneurship Development Project

Kyrgyz Republic: Women s Entrepreneurship Development Project Project Name Project Number 46010-001 Country Project Status Project Type / Modality of Assistance Source of Funding / Amount Women s Entrepreneurship

Kyrgyz Republic: Women s Entrepreneurship Development Project Project Name Project Number 46010-001 Country Project Status Project Type / Modality of Assistance Source of Funding / Amount Women s Entrepreneurship

CONCLUSIONS AND IMPLICATIONS. 1. Jobs, an urgent challenge. 2. Opportunities for job creation

CHAPTER 11 CONCLUSIONS AND IMPLICATIONS 1. Jobs, an urgent challenge The world is facing an enormous jobs challenge, a challenge that is twofold. First, 600 million jobs must be created by 2020. Second,

CHAPTER 11 CONCLUSIONS AND IMPLICATIONS 1. Jobs, an urgent challenge The world is facing an enormous jobs challenge, a challenge that is twofold. First, 600 million jobs must be created by 2020. Second,

Typology of Microfinance Service Providers Version 1.3 1

Page 1 of 5 Typology of Microfinance Service Providers Version 1.3 1 Formal financial institutions (FFIs) 1a. Private commercial bank Usually has corporate shareholding structure Regulated and supervised

Page 1 of 5 Typology of Microfinance Service Providers Version 1.3 1 Formal financial institutions (FFIs) 1a. Private commercial bank Usually has corporate shareholding structure Regulated and supervised

LEARNING CASE 9: GENDER AND RURAL INFORMATION AND COMMUNICATIONS TECHNOLOGY 1

LEARNING CASE 9: GENDER AND RURAL INFORMATION AND COMMUNICATIONS TECHNOLOGY 1 1. An Information and Communications Technology (ICT) project in Jordan was launched to create an enabling environment that:

LEARNING CASE 9: GENDER AND RURAL INFORMATION AND COMMUNICATIONS TECHNOLOGY 1 1. An Information and Communications Technology (ICT) project in Jordan was launched to create an enabling environment that:

Remittances, Microfinance and Technology

Remittances, Microfinance and Technology C P Abeywickrema, Deputy General Manager Hatton National Bank, Sri Lanka This paper discusses migrant remittances in the Sri Lankan context, specifically in relation

Remittances, Microfinance and Technology C P Abeywickrema, Deputy General Manager Hatton National Bank, Sri Lanka This paper discusses migrant remittances in the Sri Lankan context, specifically in relation

FUNDAMENTALS OF MICROFINANCE BANKING

FUNDAMENTALS OF MICROFINANCE BANKING GENERAL COMMENTS The questions were standard, simple and within the syllabus. A total of 913 candidates attempted this paper, 379 candidates (42%) passed, which include

FUNDAMENTALS OF MICROFINANCE BANKING GENERAL COMMENTS The questions were standard, simple and within the syllabus. A total of 913 candidates attempted this paper, 379 candidates (42%) passed, which include

Loan guarantee funds. Inclusive rural financial services. Introduction

Loan guarantee funds Inclusive rural financial services Introduction For more than seven decades, loan guarantee funds (LGFs) have been used extensively internationally in different market segments and

Loan guarantee funds Inclusive rural financial services Introduction For more than seven decades, loan guarantee funds (LGFs) have been used extensively internationally in different market segments and

The role of Agricultural cooperatives in accessing input and output markets An overview of experiences of SRFCF, SNNPR, Ethiopia

The role of Agricultural cooperatives in accessing input and output markets An overview of experiences of SRFCF, SNNPR, Ethiopia By Yehulashet A.Argaw Managing director, Southern Region Farmers Cooperative

The role of Agricultural cooperatives in accessing input and output markets An overview of experiences of SRFCF, SNNPR, Ethiopia By Yehulashet A.Argaw Managing director, Southern Region Farmers Cooperative

Shaping national health financing systems: can micro-banking contribute?

Shaping national health financing systems: can micro-banking contribute? Varatharajan Durairaj, Sidhartha R. Sinha, David B. Evans and Guy Carrin World Health Report (2010) Background Paper, 22 HEALTH

Shaping national health financing systems: can micro-banking contribute? Varatharajan Durairaj, Sidhartha R. Sinha, David B. Evans and Guy Carrin World Health Report (2010) Background Paper, 22 HEALTH

World Health Organization 2009

World Health Organization 2009 This document is not a formal publication of the World Health Organization (WHO), and all rights are reserved by the Organization. The document may, however, be freely reviewed,

World Health Organization 2009 This document is not a formal publication of the World Health Organization (WHO), and all rights are reserved by the Organization. The document may, however, be freely reviewed,

RURAL AND AGRICULTURE FINANCE Prof. Puneetha Palakurthi School of Community Economic Development Sothern New Hampshire University

RURAL AND AGRICULTURE FINANCE Prof. Puneetha Palakurthi School of Community Economic Development Sothern New Hampshire University DRIVERS OF RURAL DEVELOPMENT High overall economic growth Effective land

RURAL AND AGRICULTURE FINANCE Prof. Puneetha Palakurthi School of Community Economic Development Sothern New Hampshire University DRIVERS OF RURAL DEVELOPMENT High overall economic growth Effective land

Immigrants/ethnic minorities

Immigrants/ethnic minorities Microcredit Foundation Horizonti Innovative approaches for providing sustainable financial services to the Roma community - Republic of Macedonia Objective: provide sustainable

Immigrants/ethnic minorities Microcredit Foundation Horizonti Innovative approaches for providing sustainable financial services to the Roma community - Republic of Macedonia Objective: provide sustainable

Microinsurance NOTE 1 What is Microinsurance?

Microinsurance NOTE 1 What is Microinsurance? Because most low-income people in developing countries are selfemployed or employed in small firms, they have not had access to insurance products that fit

Microinsurance NOTE 1 What is Microinsurance? Because most low-income people in developing countries are selfemployed or employed in small firms, they have not had access to insurance products that fit

FINANCIAL INCLUSION OF YOUTH

FINANCIAL INCLUSION OF YOUTH HIGHLIGHTS 2.5 billion - more than half of the world s working adults- are excluded from financial services. This is most acute among low-income populations in emerging and

FINANCIAL INCLUSION OF YOUTH HIGHLIGHTS 2.5 billion - more than half of the world s working adults- are excluded from financial services. This is most acute among low-income populations in emerging and

ENTERPRISE DEVELOPMENT STRATEGY Small- and Medium-Sized Enterprises. I. Introduction

ENTERPRISE DEVELOPMENT STRATEGY Small- and Medium-Sized Enterprises I. Introduction I.1 Current Challenge: Most countries in the region are undergoing reforms that are opening their economies to greater

ENTERPRISE DEVELOPMENT STRATEGY Small- and Medium-Sized Enterprises I. Introduction I.1 Current Challenge: Most countries in the region are undergoing reforms that are opening their economies to greater

Hong Kong Declaration on Sustainable Development for Cities

Hong Kong Declaration on Sustainable Development for Cities 1. We, the representatives of national and local governments, community groups, the scientific community, professional institutions, business,

Hong Kong Declaration on Sustainable Development for Cities 1. We, the representatives of national and local governments, community groups, the scientific community, professional institutions, business,

The Global Findex Database. Adults with an account at a formal financial institution (%) OTHER BRICS ECONOMIES REST OF DEVELOPING WORLD

OTHER BRICS ECONOMIES REST OF DEVELOPING WORLD") 08 NOTE NUMBER FEBRUARY 2013 FINDEX NOTES Asli Demirguc-Kunt Leora Klapper Douglas Randall The Global Findex Database Financial Inclusion in India In India 35 percent of adults have a formal account and

08 NOTE NUMBER FEBRUARY 2013 FINDEX NOTES Asli Demirguc-Kunt Leora Klapper Douglas Randall The Global Findex Database Financial Inclusion in India In India 35 percent of adults have a formal account and

CONSUMERLAB. Mobile COMMERCE IN EMERGING MARKETS

CONSUMERLAB Mobile COMMERCE IN EMERGING MARKETS An Ericsson ConsumerLab Insight Summary Report January 2015 contents EXAMINING ATTITUDES 3 GROWING URBANIZATION 4 A CASH ECONOMY 6 PERCEPTION IS KEY 7 ECONOMIC

CONSUMERLAB Mobile COMMERCE IN EMERGING MARKETS An Ericsson ConsumerLab Insight Summary Report January 2015 contents EXAMINING ATTITUDES 3 GROWING URBANIZATION 4 A CASH ECONOMY 6 PERCEPTION IS KEY 7 ECONOMIC

What is MicroInsurance?

What is MicroInsurance? Craig Thorburn Senior Insurance Specialist, The World Bank Policy Advisory Consultant, CGAP [email protected] +1 202 473 4932 or +1 202 470 6012 Skype: craig_thorburn MicroInsurance

What is MicroInsurance? Craig Thorburn Senior Insurance Specialist, The World Bank Policy Advisory Consultant, CGAP [email protected] +1 202 473 4932 or +1 202 470 6012 Skype: craig_thorburn MicroInsurance

SNV s value chain development approach

SNV s value chain development approach Introduction In order to identify the best entry points for capacity development, SNV has under the BOAM 1 program adopted the value chain approach. A value chain

SNV s value chain development approach Introduction In order to identify the best entry points for capacity development, SNV has under the BOAM 1 program adopted the value chain approach. A value chain

United Nations Programme on Youth. Interagency Expert Group Meeting on. Goals and Targets for Monitoring the Progress of Youth in the Global Economy

BACKGROUND PAPER United Nations Programme on Youth Interagency Expert Group Meeting on Goals and Targets for Monitoring the Progress of Youth in the Global Economy New York, 30-31 May 2007 INTRODUCTION

BACKGROUND PAPER United Nations Programme on Youth Interagency Expert Group Meeting on Goals and Targets for Monitoring the Progress of Youth in the Global Economy New York, 30-31 May 2007 INTRODUCTION

Eliminating child labour in agriculture

Eliminating child labour in agriculture Gender, Equity and Rural Employment Division Economic and Social Development Department Food and Agriculture Organization of the United Nations May 2010 The following

Eliminating child labour in agriculture Gender, Equity and Rural Employment Division Economic and Social Development Department Food and Agriculture Organization of the United Nations May 2010 The following

Expanding the Financial Services Frontier: Lessons From Mobile Phone Banking in Kenya

Expanding the Financial Services Frontier: Lessons From Mobile Phone Banking in Kenya Mwangi S. Kimenyi Senior Fellow, Africa Growth Initiative at Brookings Njuguna S. Ndung u Governor, Central Bank of

Expanding the Financial Services Frontier: Lessons From Mobile Phone Banking in Kenya Mwangi S. Kimenyi Senior Fellow, Africa Growth Initiative at Brookings Njuguna S. Ndung u Governor, Central Bank of

Emerging Face of Micro-Finance in India--A Review

Emerging Face of Micro-Finance in India--A Review ABSTRACT Meenu Shahi 1 Assistant Professor in Department of Commerce Government College for Girls (Gcg-14) Panchkula Anu Kumari 2 Assistant Professor in

Emerging Face of Micro-Finance in India--A Review ABSTRACT Meenu Shahi 1 Assistant Professor in Department of Commerce Government College for Girls (Gcg-14) Panchkula Anu Kumari 2 Assistant Professor in

G20 DEVELOPMENT WORKING GROUP G20 INCLUSIVE BUSINESS FRAMEWORK

G20 DEVELOPMENT WORKING GROUP G20 INCLUSIVE BUSINESS FRAMEWORK G20 INCLUSIVE BUSINESS FRAMEWORK A framework that defines inclusive business, sets out recommendations to enable inclusive business, and proposes

G20 DEVELOPMENT WORKING GROUP G20 INCLUSIVE BUSINESS FRAMEWORK G20 INCLUSIVE BUSINESS FRAMEWORK A framework that defines inclusive business, sets out recommendations to enable inclusive business, and proposes

VIETNAM FORUM ON LIFELONG LEARNING: BUILDING A LEARNING SOCIETY. ILO Director Ms. Rie Vejs-Kjeldgaard Hanoi, 6-8 December 2010

VIETNAM FORUM ON LIFELONG LEARNING: BUILDING A LEARNING SOCIETY ILO Director Ms. Rie Vejs-Kjeldgaard Hanoi, 6-8 December 2010 Deputy Prime Minister Nguyen Thien Nhan, cum Chairman of the National Steering

VIETNAM FORUM ON LIFELONG LEARNING: BUILDING A LEARNING SOCIETY ILO Director Ms. Rie Vejs-Kjeldgaard Hanoi, 6-8 December 2010 Deputy Prime Minister Nguyen Thien Nhan, cum Chairman of the National Steering

Allianz Reducing the risks of the poor through microinsurance

DEDICATED TO MAKING A DIFFERENCE World Business Council for Sustainable Development Case Study 2009 Allianz Reducing the risks of the poor through microinsurance The business case The Allianz Group has

DEDICATED TO MAKING A DIFFERENCE World Business Council for Sustainable Development Case Study 2009 Allianz Reducing the risks of the poor through microinsurance The business case The Allianz Group has

EFFECTIVE STRATEGIES FOR PROMOTING GENDER EQUALITY

EFFECTIVE STRATEGIES FOR PROMOTING GENDER EQUALITY How can we increase the likelihood of women benefiting equally from development activities? What strategies have proven to be effective in the field?

EFFECTIVE STRATEGIES FOR PROMOTING GENDER EQUALITY How can we increase the likelihood of women benefiting equally from development activities? What strategies have proven to be effective in the field?

Making financial markets work for the poor: From theory to praxis

Making financial markets work for the poor: From theory to praxis BDS Seminar 2005 Turin David Ferrand FSD Kenya Making financial markets work in Kenya 1. Conceptual issues 2. Understanding the market

Making financial markets work for the poor: From theory to praxis BDS Seminar 2005 Turin David Ferrand FSD Kenya Making financial markets work in Kenya 1. Conceptual issues 2. Understanding the market

SOCIAL PROTECTION BRIEFING NOTE SERIES NUMBER 4. Social protection and economic growth in poor countries

A DFID practice paper Briefing SOCIAL PROTECTION BRIEFING NOTE SERIES NUMBER 4 Social protection and economic growth in poor countries Summary Introduction DFID s framework for pro-poor growth sets out

A DFID practice paper Briefing SOCIAL PROTECTION BRIEFING NOTE SERIES NUMBER 4 Social protection and economic growth in poor countries Summary Introduction DFID s framework for pro-poor growth sets out

GLOBAL ALLIANCE FOR CLIMATE-SMART AGRICULTURE (GACSA)

") GLOBAL ALLIANCE FOR CLIMATE-SMART AGRICULTURE (GACSA) FRAMEWORK DOCUMENT Version 01 :: 1 September 2014 I Vision 1. In today s world there is enough food produced for all to be well-fed, but one person

GLOBAL ALLIANCE FOR CLIMATE-SMART AGRICULTURE (GACSA) FRAMEWORK DOCUMENT Version 01 :: 1 September 2014 I Vision 1. In today s world there is enough food produced for all to be well-fed, but one person

THE MULTILATERAL INVESTMENT FUND DEPLOYING VALUE CHAINS FOR DEVELOPMENT. Nancy Lee General Manager MULTILATERAL INVESTMENT FUND

THE MULTILATERAL INVESTMENT FUND DEPLOYING VALUE CHAINS FOR DEVELOPMENT Nancy Lee General Manager MULTILATERAL INVESTMENT FUND 2. TABLE OF CONTENTS Introduction to the Multilateral Investment Fund Evolution

THE MULTILATERAL INVESTMENT FUND DEPLOYING VALUE CHAINS FOR DEVELOPMENT Nancy Lee General Manager MULTILATERAL INVESTMENT FUND 2. TABLE OF CONTENTS Introduction to the Multilateral Investment Fund Evolution

What Is Poverty and Why Measure It?

Chapter What Is Poverty and Why Measure It? Summary Poverty is pronounced deprivation in well-being. The conventional view links wellbeing primarily to command over commodities, so the poor are those who

Chapter What Is Poverty and Why Measure It? Summary Poverty is pronounced deprivation in well-being. The conventional view links wellbeing primarily to command over commodities, so the poor are those who

SECTOR ASSESSMENT (SUMMARY): TECHNICAL EDUCATION AND VOCATIONAL TRAINING SUBSECTOR

: TECHNICAL EDUCATION AND VOCATIONAL TRAINING SUBSECTOR") Skills Development Project (RRP NEP 38176) SECTOR ASSESSMENT (SUMMARY): TECHNICAL EDUCATION AND VOCATIONAL TRAINING SUBSECTOR Sector Road Map A. Sector Performance, Problems, and Opportunities 1. After

Skills Development Project (RRP NEP 38176) SECTOR ASSESSMENT (SUMMARY): TECHNICAL EDUCATION AND VOCATIONAL TRAINING SUBSECTOR Sector Road Map A. Sector Performance, Problems, and Opportunities 1. After

Applying the Value Chain Framework to the Health Sector. Concept Note

Applying the Value Chain Framework to the Health Sector Concept Note I) Definition of value chain analysis Value chain analysis is an economic development strategy to reduce poverty by better integrating

Applying the Value Chain Framework to the Health Sector Concept Note I) Definition of value chain analysis Value chain analysis is an economic development strategy to reduce poverty by better integrating

Microfinance Expert, CEO of YOSEFO Finance Chairman of the Board of Directors of Mbinga Community Bank

A CLKnet FORUM PRESENTATION BY ALTEMIUS MILLINGA Microfinance Expert, CEO of YOSEFO Finance Chairman of the Board of Directors of Mbinga Community Bank 11 th April, 2012 1 Tanzania s Financial Sector Landscape

A CLKnet FORUM PRESENTATION BY ALTEMIUS MILLINGA Microfinance Expert, CEO of YOSEFO Finance Chairman of the Board of Directors of Mbinga Community Bank 11 th April, 2012 1 Tanzania s Financial Sector Landscape

E/CN.6/2011/CRP.7. Gender equality and sustainable development

18 March 2011 Original: English Commission on the Status of Women Fifty-fifth session 22 February-4 March 2011 Agenda item 3 (b) Follow-up to the Fourth World Conference on Women and to the twenty-third

18 March 2011 Original: English Commission on the Status of Women Fifty-fifth session 22 February-4 March 2011 Agenda item 3 (b) Follow-up to the Fourth World Conference on Women and to the twenty-third

Financial Inclusion in the Philippines

Financial Inclusion in the Philippines Issue No. 3 Third Quarter 2013 What is Microcredit? Brief History of Microcredit in the Philippines Unique Features of Microcredit BSP Regulations on Microcredit

Financial Inclusion in the Philippines Issue No. 3 Third Quarter 2013 What is Microcredit? Brief History of Microcredit in the Philippines Unique Features of Microcredit BSP Regulations on Microcredit

The IBIS Education for Change strategy states the overall objective

CONCEPT PAPER: YOUTH EDUCATION & TRAINING 1 Concept Paper youth education & training Photo: Ricardo Ramirez The IBIS Education for Change strategy states the overall objective of IBIS work with education

CONCEPT PAPER: YOUTH EDUCATION & TRAINING 1 Concept Paper youth education & training Photo: Ricardo Ramirez The IBIS Education for Change strategy states the overall objective of IBIS work with education

Indonesia Solar Loan (ISL) Programme: Lessons learned for Solar PV project development

Programme: Lessons learned for Solar PV project development") Lessons learned for Solar PV project development Marjan Stojiljkovic FS-UNEP Collaborating Centre for Climate and Sustainable Energy Finance GIZ Workshop, March 7th, 2012 Berlin, Germany F r a n k f u

Lessons learned for Solar PV project development Marjan Stojiljkovic FS-UNEP Collaborating Centre for Climate and Sustainable Energy Finance GIZ Workshop, March 7th, 2012 Berlin, Germany F r a n k f u

Microinsurance as a social protection instrument

Microinsurance as a social protection instrument Protection from major risks for little money The lives of the poor in developing countries are characterized by constant economic insecurity. Most of them

Microinsurance as a social protection instrument Protection from major risks for little money The lives of the poor in developing countries are characterized by constant economic insecurity. Most of them

Trade Finance : SMEs Emerging Needs

ASIA-PACIFIC TRADE FACILITATION FORUM 2013 [Session 2: Integrating SMEs into international supply chains through trade finance] Beijing, China, 10-11 September 2013 Trade Finance : SMEs Emerging Needs

ASIA-PACIFIC TRADE FACILITATION FORUM 2013 [Session 2: Integrating SMEs into international supply chains through trade finance] Beijing, China, 10-11 September 2013 Trade Finance : SMEs Emerging Needs

Having undertaken a general discussion on the basis of Report IV, Small and medium-sized enterprises and decent and productive employment creation,

International Labour Conference Provisional Record 104th Session, Geneva, June 2015 11-1 Fourth item on the agenda: Small and medium-sized enterprises and decent and productive employment creation Reports

International Labour Conference Provisional Record 104th Session, Geneva, June 2015 11-1 Fourth item on the agenda: Small and medium-sized enterprises and decent and productive employment creation Reports

Central African Republic Country Profile 2011

Central African Republic Country Profile 2011 Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Region: Sub-Saharan Africa Income Group:

Central African Republic Country Profile 2011 Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Region: Sub-Saharan Africa Income Group:

are country driven and in conformity with, and supportive of, national development priorities;

OPERATIONAL PROGRAM NUMBER 6 PROMOTING THE ADOPTION OF RENEWABLE ENERGY BY REMOVING BARRIERS AND REDUCING IMPLEMENTATION COSTS 6.1 The United Nations Framework Convention on Climate Change (UNFCCC) seeks

OPERATIONAL PROGRAM NUMBER 6 PROMOTING THE ADOPTION OF RENEWABLE ENERGY BY REMOVING BARRIERS AND REDUCING IMPLEMENTATION COSTS 6.1 The United Nations Framework Convention on Climate Change (UNFCCC) seeks

FINAL. World Education Forum. The Dakar Framework for Action. Education For All: Meeting our Collective Commitments. Revised Final Draft

28/04/2000, 3 P.m. FINAL The Dakar Framework for Action Education For All: Meeting our Collective Commitments Revised Final Draft World Education Forum Dakar, Senegal, 26-28 April 2000 1 1 The Dakar Framework

28/04/2000, 3 P.m. FINAL The Dakar Framework for Action Education For All: Meeting our Collective Commitments Revised Final Draft World Education Forum Dakar, Senegal, 26-28 April 2000 1 1 The Dakar Framework

Agricultural Growth Is the Key to Poverty Alleviation in Low-Income Developing Countries

International Food Policy Research Institute 2020 Brief 15, April 1995 Agricultural Growth Is the Key to Poverty Alleviation in Low-Income Developing Countries by Per Pinstrup-Andersen and Rajul Pandya-Lorch

International Food Policy Research Institute 2020 Brief 15, April 1995 Agricultural Growth Is the Key to Poverty Alleviation in Low-Income Developing Countries by Per Pinstrup-Andersen and Rajul Pandya-Lorch

Micro, Small and Medium Enterprises Financing in India - Issues and Concerns

Micro, Small and Medium Enterprises Financing in India - Issues and Concerns Dr. C.S. Prasad* Micro, Small and Medium enterprises (MSME) constitute the dominant form of business organisation worldwide.

Micro, Small and Medium Enterprises Financing in India - Issues and Concerns Dr. C.S. Prasad* Micro, Small and Medium enterprises (MSME) constitute the dominant form of business organisation worldwide.

Submission to the Productivity Commission Childcare and Early Childhood Learning February 2014. Background. The Montessori Australia Foundation (MAF)

") Submission to the Productivity Commission Childcare and Early Childhood Learning February 2014 Background The Montessori sector is unique, diverse and significant in Australian education, particularly

Submission to the Productivity Commission Childcare and Early Childhood Learning February 2014 Background The Montessori sector is unique, diverse and significant in Australian education, particularly

Social protection, agriculture and the PtoP project

Social protection, agriculture and the PtoP project Benjamin Davis Workshop on the Protection to Production project September 24-25, 2013 Rome What do we mean by social protection and agriculture? Small

Social protection, agriculture and the PtoP project Benjamin Davis Workshop on the Protection to Production project September 24-25, 2013 Rome What do we mean by social protection and agriculture? Small

5. SOCIAL PERFORMANCE MANAGEMENT IN MICROFINANCE 1

5. SOCIAL PERFORMANCE MANAGEMENT IN MICROFINANCE 1 INTRODUCTION TO SOCIAL PERFORMANCE MANAGEMENT Achieving Social and Financial Performance In the microfinance arena, performance has long been associated

5. SOCIAL PERFORMANCE MANAGEMENT IN MICROFINANCE 1 INTRODUCTION TO SOCIAL PERFORMANCE MANAGEMENT Achieving Social and Financial Performance In the microfinance arena, performance has long been associated

Mainstreaming Disaster Risk Reduction into National and Sectoral Development Process

Mainstreaming Disaster Risk Reduction into National and Sectoral Development Process Safer Training Health Course Facilities Regional Consultative Committee on Disaster Management (RCC) Training Course

Mainstreaming Disaster Risk Reduction into National and Sectoral Development Process Safer Training Health Course Facilities Regional Consultative Committee on Disaster Management (RCC) Training Course

IOE PERSPECTIVES ON THE POST 2015 DEVELOPMENT AGENDA JANUARY 2013

IOE PERSPECTIVES ON THE POST 2015 DEVELOPMENT AGENDA JANUARY 2013 INTERNATIONAL ORGANISATION OF EMPLOYERS Disclaimer Articles posted on the website are made available by the UNCTAD secretariat in the form

IOE PERSPECTIVES ON THE POST 2015 DEVELOPMENT AGENDA JANUARY 2013 INTERNATIONAL ORGANISATION OF EMPLOYERS Disclaimer Articles posted on the website are made available by the UNCTAD secretariat in the form

TRAINING CATALOGUE ON IMPACT INSURANCE. Building practitioner skills in providing valuable and viable insurance products

TRAINING CATALOGUE ON IMPACT INSURANCE Building practitioner skills in providing valuable and viable insurance products 2016 List of training courses Introduction to microinsurance and its business case...

TRAINING CATALOGUE ON IMPACT INSURANCE Building practitioner skills in providing valuable and viable insurance products 2016 List of training courses Introduction to microinsurance and its business case...

Youth access to rural finance

TEASER Youth access to rural finance Inclusive rural financial services IFAD/Guy Stubbs Swaziland Rural Finance and Enterprise Development Programme Introduction As a specialized agency of the United Nations,

TEASER Youth access to rural finance Inclusive rural financial services IFAD/Guy Stubbs Swaziland Rural Finance and Enterprise Development Programme Introduction As a specialized agency of the United Nations,