The Genworth Outlook, A Review of the Q Investor Presentation

|

|

|

- Prosper Foster

- 7 years ago

- Views:

Transcription

1 In this quick note we look at the recent Genworth Australia disappointment adding color on how the process works down under, where the rise in defaults are being hidden, and what is likely to happen next. Mark Hanson Summary The Genworth presentation tries in vain to blame isolated geographic regions and other specific factors for a temporary poor performance when an analysis of the data clearly indicates a very poor outlook for Genworth and, therefore, the Australian financial system. Genworth s Siamese twin, QBE LMI, shares the same market and risk. Therefore, you can safely bet that the same situation is unfolding; although we suspect on the numbers above that QBE has a larger exposure proportionally in Victoria, which is a concern. There is one other factor which we would like to highlight. The capital requirements of both Genworth and QBE LMI are based primarily on their exposure relative to the LTV ratio of the mortgage being insured. As house prices decline, the Australian Prudential Regulatory Authority s (APRA) capital adequacy rules require that the LMIs must increase their minimum capital requirements because lower house prices significantly increases their risk exposure. With the information that APRA now has on performance, it is likely to significantly increased capital requirements well before the dramatic increases in LMI claims occur. The Genworth Outlook, A Review of the Q Investor Presentation by Leith van Onselen In this Update, we will dig a little deeper to see what the future might hold for the mortgage insurer, Genworth Australia, based on its Q Investor Presentation released last week. Firstly, let s remind ourselves what mortgage insurance actually entails in Australia. A mortgage insurer in Australia insures the lender under a mortgage for 100% of the balance of a loan for the life of the loan. Generally, the loan-to-value (LTV) ratio on insured loans is greater than 80% on settlement. Although the borrower pays the once-off premium at

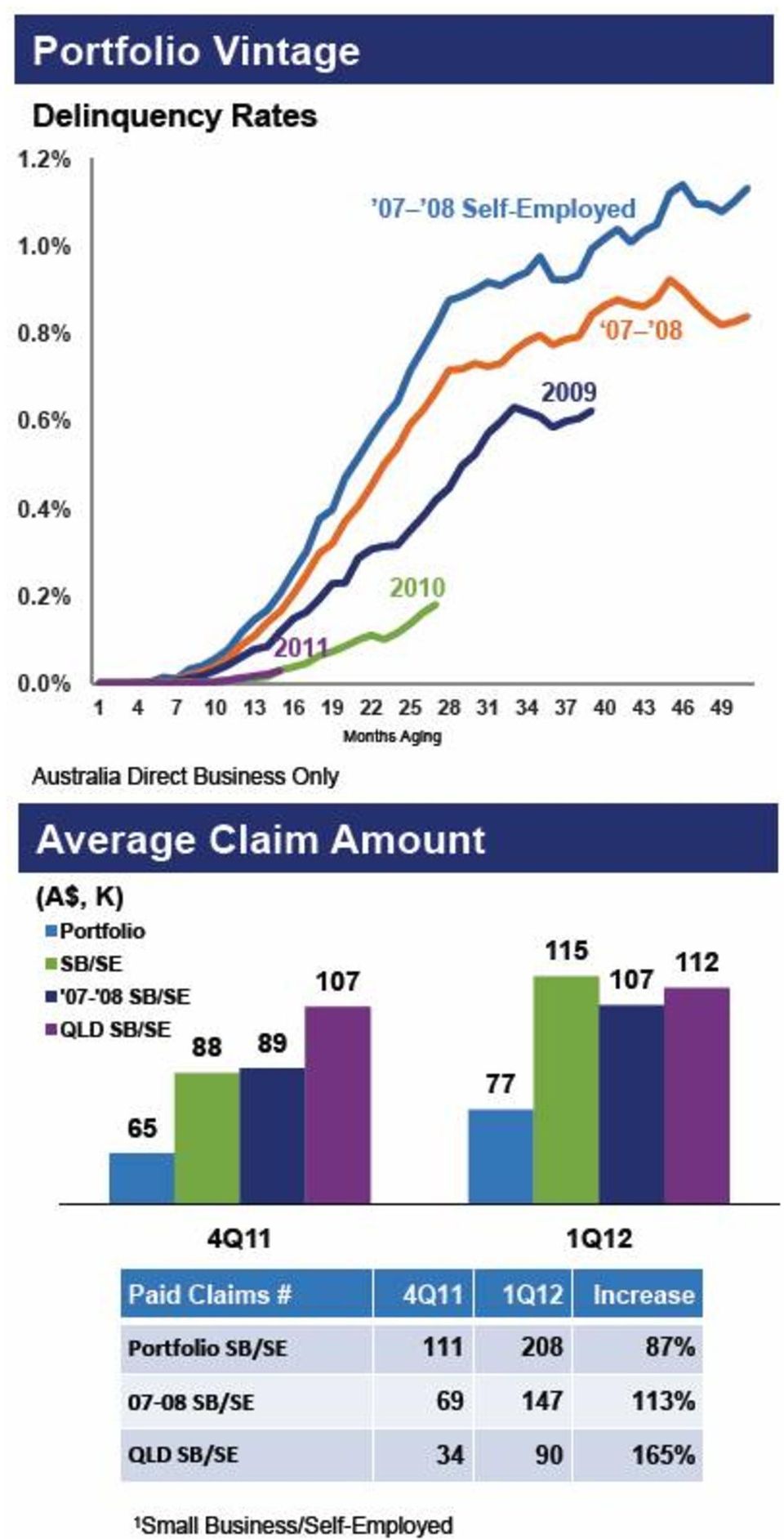

2 the time of entering the loan, the borrower receives no benefit from the insurance. Regardless of whether a lender successfully claims against the mortgage insurance, the borrower is still liable for repayment of the loan. Mortgage insurance is an unusual business because it is in essence a one way bet on house prices. You receive a premium up front, set your risk position and wait for the train to hit, as surely it will. If house prices are rising even modestly, it s generally a high cash generation business with low claim rates. However, when it turns, the reverse occurs, with no ability to re-price the risk in force to offset rising claims in both numbers and amounts. Genworth Australia has reported that their exposure or Risk-in-Force (RIF) in Australia is $100.5Bn. RIF is 35% of Genworth s total exposure because it believes that it would not lose more than 35% on any loan. The total balance of loans insured, therefore, is $287Bn. Against this risk, Genworth has a regulatory capital base of $2.3Bn or 0.8%. The capital ratio is a slight improvement from the previous 0.7% that we quoted previously [see December 15, 2011 note] due to the raising of Tier-2 subordinated debt and extra provisioning. In a stable market for mortgage exposure, this capital ratio, although thin, is sustainable especially with the size and diversity of exposure that Genworth holds in Australia. However, and as the Genworth report shows, stable mortgage exposure is not what is happening or being forecast. The Genworth Investor Presentation reports four reasons why they are strengthening their provisions (Presentation available fordownload here) 1) Coastal Queensland Economic Downturn. Queensland s (QLD) property market downturn has been underway for a number of years, with prices now back at 2007 levels. The most interesting development in the Genworth Presentation is the huge Q12012 uptick in claim size, especially in coastal QLD. Claim size has risen from around $90,000 to around $140,000 in the last 12 months (see below chart). Is coastal QLD, am outlier? We do not believe so. As explained previously, the Melbourne (Victorian) housing market is likely to be the

3 epicenter of the coming Australian housing bust, owing to its significant oversupply (both in terms of homes for sale and new home construction), over-inflated prices, and deteriorating economy. $66Bn of mortgage loans are insured by Genworth in Victoria, which is even higher than those insured in QLD. 2) Small Business/Self-Employed In Books. Genworth has an exposure of $43Bn to low doc loans taken out by Australian small businesses/self-employed persons (arguably Australia s version of sub-prime lending). As the domestic economy deteriorates even further, we expect that the number and amount of claims in this class will continue to rise.

4

5 3) Lender Servicing/Forbearance Impact. Australia operates a range of programs (loosely known as Borrower Assist ), which are a potential sleeper risk that could suddenly accelerate the spiral down. In effect, borrowers in Australia have been given rights to delay foreclosure processes in order to allow themselves more time to become current on their mortgage payments (see here for details). The process is either by agreement with certain lenders or through a government sanctioned process. Our understanding is that most mortgage lenders allow for up to 12 months payment deferral (i.e. capitalization) for hardship, which is not usually classified as arrears. Genworth has shown the dramatic increase in the time taken from 13 months to 21 months - for a claim to be made from delinquency has dramatically increased the size of Genworth s claims. Anyone wondering why Australian mortgage delinquencies have not risen more quickly, Borrower Assist is your smoking gun.the stretching of lender forbearance, most likely via the Borrower Assist programs that all banks are required to run, operate like purgatory buckets from which the banks can delay and then drip feed delinquencies onto the market. While Borrower Assist is not necessarily a bad policy, it does lead to an understatement of the true level of stress (and risks) in the Australian mortgage market, particularly when house prices are falling as is the case currently. Lenders have not consistently reported the numbers and exposure to borrowers in all forms of Borrower Assist; therefore it is not currently possible to ascertain the extent of their exposures. We would hazard a guess that most distressed borrowers go into Borrower Assist programs first, and not straight into foreclosure. As such, there are likely to be a significant number of delinquent mortgages floating underneath the surface. 4) Paid Claims. Genworth reports an increase in the number of claims paid in the quarter of 76% - i.e. from 483 to 852 (see below charts). Is this a one off event, or the start of a trend? Time will tell. It is significant, however, that Genworth were not able to predict this dramatic increase in claims and both provide for it and disclose it. With

6 house prices falling across most of Australia, and the domestic economy deteriorating, it is hard to not come to the conclusion that the claims against Genworth mortgage insurance will continue at elevated levels. In summary, the Genworth presentation tries in vain to blame isolated geographic regions and other specific factors for a temporary poor performance when an analysis of the data clearly indicates a very poor outlook for Genworth and, therefore, the Australian financial system. Genworth s Siamese twin, QBE LMI, shares the same market and risk. Therefore, you can safely bet that the same situation is unfolding; although we suspect on the numbers above that QBE has a larger exposure proportionally in Victoria, which is a concern. There is one other factor which we would like to highlight. The capital requirements of both Genworth and QBE LMI are based primarily on their exposure relative to the LTV ratio of the mortgage being insured. As house

7 prices decline, the Australian Prudential Regulatory Authority s (APRA) capital adequacy rules require that the LMIs must increase their minimum capital requirements because lower house prices significantly increases their risk exposure. With the information that APRA now has on performance, it is likely to significantly increased capital requirements well before the dramatic increases in LMI claims occur. Best Regards, Leith van Onselen Mark Hanson DISCLAIMER: This message and attachments are for the sole use of the addressee and are privileged, confidential and exempt from disclosure. If you are not the addressee, copying, dissemination, or distribution of this communication is strictly prohibited. You must delete the e mail and destroy any copies. In publishing research, Hanson Advisors, JCLMH LLC, and MAHA, Inc (the Company) is not soliciting any action based upon it. The Company's publications contain material based upon publicly available information, obtained from sources that we consider reliable. However, the Company does not represent that it is accurate and it should not be relied on as such. Opinions expressed are current opinions as of the date appearing in the Company's publications only. All forecasts and statements about the future, even if presented as fact, should be treated as judgments, and neither the Company nor its partners can be held responsible for any failure of those judgments to prove accurate. It should be assumed that, from time to time, the Company and its partners will hold investments in securities and other positions, in equity, bond, currency and commodities markets, from which they will benefit if the forecasts and judgments about the future presented in this document do prove to be accurate. The Company is not liable for any loss or damage resulting from the use of its product. The Company is CA Corp registered in the state of CA.

In my opinion, the following data do not bode well for increasing home improvement/rehab spend...

Home Improvement/Rehab Trade is Tired... It remains my opinion on home improvement that with... foreclosure completions at an artificial and transitory 5-year low for the election cycle leading to significantly

Home Improvement/Rehab Trade is Tired... It remains my opinion on home improvement that with... foreclosure completions at an artificial and transitory 5-year low for the election cycle leading to significantly

CCPA misses the boat: Huge jump in low ratio insurance during GFC hints at REAL bailout

Good Morning, CMHC cheap, bulk portfolio insurance provided a mechanism that allowed banks to roll risky low ratio loans to Canadian taxpayers. Knowing the risky loan securitization "eject" button was

Good Morning, CMHC cheap, bulk portfolio insurance provided a mechanism that allowed banks to roll risky low ratio loans to Canadian taxpayers. Knowing the risky loan securitization "eject" button was

FIIG ESSENTIALS GUIDE. Residential Mortgage Backed Securities

FIIG ESSENTIALS GUIDE Residential Mortgage Backed Securities Introduction Residential Mortgage Backed Securities (RMBS) are debt securities that are secured by a pool of home loans. RMBS are a subset

FIIG ESSENTIALS GUIDE Residential Mortgage Backed Securities Introduction Residential Mortgage Backed Securities (RMBS) are debt securities that are secured by a pool of home loans. RMBS are a subset

Australian RMBS Index Report Q3 2014: Housing Loan Arrears Hit Eight-Year Low

Australian RMBS Index Report Q3 2014: Housing Loan Arrears Hit Eight-Year Low Primary Credit Analyst: Erin Kitson, Melbourne (61) 3-9631-2166; erin.kitson@standardandpoors.com Secondary Contacts: Kate

Australian RMBS Index Report Q3 2014: Housing Loan Arrears Hit Eight-Year Low Primary Credit Analyst: Erin Kitson, Melbourne (61) 3-9631-2166; erin.kitson@standardandpoors.com Secondary Contacts: Kate

Please find attached an announcement and supplementary information for release to the market.

QBE INSURANCE GROUP LIMITED ABN 28 008 485 014 Head Office 82 Pitt Street Sydney NSW 2000 AUSTRALIA 14 August 2008 The Manager Company Announcements ASX Limited Level 6 Exchange Centre 20 Bridge Street

QBE INSURANCE GROUP LIMITED ABN 28 008 485 014 Head Office 82 Pitt Street Sydney NSW 2000 AUSTRALIA 14 August 2008 The Manager Company Announcements ASX Limited Level 6 Exchange Centre 20 Bridge Street

Third Quarter 2012. Australia Mortgage Insurance & U.S. Mortgage Insurance Investor Materials October 30, 2012

Third Quarter 2012 Australia Mortgage Insurance & U.S. Mortgage Insurance Investor Materials October 30, 2012 2012 Genworth Financial, Inc. All rights reserved. Cautionary Note Regarding Forward-Looking

Third Quarter 2012 Australia Mortgage Insurance & U.S. Mortgage Insurance Investor Materials October 30, 2012 2012 Genworth Financial, Inc. All rights reserved. Cautionary Note Regarding Forward-Looking

Interest-Only Loans Could Destabilize Denmark's Mortgage Market

STRUCTURED FINANCE RESEARCH Interest-Only Loans Could Destabilize Denmark's Mortgage Market Primary Credit Analyst: Casper R Andersen, London (44) 20-7176-6757; casper_andersen@standardandpoors.com Table

STRUCTURED FINANCE RESEARCH Interest-Only Loans Could Destabilize Denmark's Mortgage Market Primary Credit Analyst: Casper R Andersen, London (44) 20-7176-6757; casper_andersen@standardandpoors.com Table

CARDMEMBER AGREEMENT AND DISCLOSURE STATEMENT

CARDMEMBER AGREEMENT AND DISCLOSURE STATEMENT Part 1 of 2: Agreement About this Agreement Part 1 and 2 together make your Cardmember Agreement and Disclosure Statement ( Agreement ) and govern your Credit

CARDMEMBER AGREEMENT AND DISCLOSURE STATEMENT Part 1 of 2: Agreement About this Agreement Part 1 and 2 together make your Cardmember Agreement and Disclosure Statement ( Agreement ) and govern your Credit

IMF Country Report No. 11/365

The mortgage finance system in Canada is quite strong, as evidenced by its performance during the recent financial crisis. Home buyers who cannot make a 20 percent down-payment are required to insure their

The mortgage finance system in Canada is quite strong, as evidenced by its performance during the recent financial crisis. Home buyers who cannot make a 20 percent down-payment are required to insure their

"Sales down? Weak performance?? Say what?!? The headlines don't say anything about a slump! What about the 40 people lined up on every offer?

Sacramento Housing Update...Jan 2013. Weak sales performance mirrors Las Vegas, Phoenix, Silicon Valley and a host of other first-mover, 2012 short squeeze regions that are now seizing up. "Sales down?

Sacramento Housing Update...Jan 2013. Weak sales performance mirrors Las Vegas, Phoenix, Silicon Valley and a host of other first-mover, 2012 short squeeze regions that are now seizing up. "Sales down?

FSP SOP 94-6-a PROPOSED FASB STAFF POSITION. No. SOP 94-6-a. Title: Nontraditional Loan Products. Comment Deadline: November 11, 2005.

PROPOSED FASB STAFF POSITION No. SOP 94-6-a Title: Nontraditional Loan Products Comment Deadline: November 11, 2005 Introduction 1. This FASB Staff Position (FSP) is in response to inquiries from constituents

PROPOSED FASB STAFF POSITION No. SOP 94-6-a Title: Nontraditional Loan Products Comment Deadline: November 11, 2005 Introduction 1. This FASB Staff Position (FSP) is in response to inquiries from constituents

Investing in mortgage schemes?

Investing in mortgage schemes? Independent guide for investors about unlisted mortgage schemes This guide is for you, whether you re an experienced investor or just starting out. Key tips from ASIC about

Investing in mortgage schemes? Independent guide for investors about unlisted mortgage schemes This guide is for you, whether you re an experienced investor or just starting out. Key tips from ASIC about

INVESTING IN MORTGAGE FUNDS?

INVESTING IN MORTGAGE FUNDS? Independent guide for investors about unlisted mortgage funds Mortgage funds can also be called mortgage trusts or mortgage schemes. About ASIC The Australian Securities and

INVESTING IN MORTGAGE FUNDS? Independent guide for investors about unlisted mortgage funds Mortgage funds can also be called mortgage trusts or mortgage schemes. About ASIC The Australian Securities and

Australian Perspective on Developments in US Subprime Mortgage Market

International Structured Finance Australia Special Comment Australian Perspective on Developments in US Subprime Mortgage Market Author Nicola O Brien Vice President Senior Analyst +61 2 9270-8112 Nicola.Obrien@moodys.com

International Structured Finance Australia Special Comment Australian Perspective on Developments in US Subprime Mortgage Market Author Nicola O Brien Vice President Senior Analyst +61 2 9270-8112 Nicola.Obrien@moodys.com

MEASUREMENTS OF FAIR VALUE IN ILLIQUID (OR LESS LIQUID) MARKETS

MARKETS") MEASUREMENTS OF FAIR VALUE IN ILLIQUID (OR LESS LIQUID) MARKETS Objective The objective of this paper is to discuss issues associated with the measurement of fair value under existing generally accepted

MEASUREMENTS OF FAIR VALUE IN ILLIQUID (OR LESS LIQUID) MARKETS Objective The objective of this paper is to discuss issues associated with the measurement of fair value under existing generally accepted

Fees we charge for consumer mortgage lending products

s we charge for consumer mortgage lending products Effective February 2016 Section 1: Understanding fees and charges When we may charge fees The Commonwealth Bank charges fees for administering your account

s we charge for consumer mortgage lending products Effective February 2016 Section 1: Understanding fees and charges When we may charge fees The Commonwealth Bank charges fees for administering your account

CONSULTATION PAPER P016-2006 October 2006. Proposed Regulatory Framework on Mortgage Insurance Business

CONSULTATION PAPER P016-2006 October 2006 Proposed Regulatory Framework on Mortgage Insurance Business PREFACE 1 Mortgage insurance protects residential mortgage lenders against losses on mortgage loans

CONSULTATION PAPER P016-2006 October 2006 Proposed Regulatory Framework on Mortgage Insurance Business PREFACE 1 Mortgage insurance protects residential mortgage lenders against losses on mortgage loans

Standard Mortgage Terms

Page 1 of 45 Standard Mortgage Terms Filed By: Canadian Imperial Bank of Commerce Filing Number: MT160006 Filing Date: March 17, 2016 The following set of standard mortgage terms shall be deemed to be

Page 1 of 45 Standard Mortgage Terms Filed By: Canadian Imperial Bank of Commerce Filing Number: MT160006 Filing Date: March 17, 2016 The following set of standard mortgage terms shall be deemed to be

Conclusion. Below are the key takeaways as I see them. 1) The Stimulus-Driven, Thin and Volatile Dash-to-Trash in SoCal

The Stimulus-Driven, Thin and Volatile Dash-to-Trash in SoCal") Conclusion After reviewing the DataQuick Feb SoCal house sales internals I have never been more confident that this megaregion is not in a "recovery"; rather benefiting from a sudden, unprecedented interest

Conclusion After reviewing the DataQuick Feb SoCal house sales internals I have never been more confident that this megaregion is not in a "recovery"; rather benefiting from a sudden, unprecedented interest

Central Bank of Ireland Macro-prudential policy for residential mortgage lending Consultation Paper CP87

Central Bank of Ireland Macro-prudential policy for residential mortgage lending Consultation Paper CP87 An initial assessment from Genworth Financial The Central Bank ( CB ) published a consultation paper

Central Bank of Ireland Macro-prudential policy for residential mortgage lending Consultation Paper CP87 An initial assessment from Genworth Financial The Central Bank ( CB ) published a consultation paper

Investing in unlisted property schemes?

Investing in unlisted property schemes? Independent guide for investors about unlisted property schemes This guide is for you, whether you re an experienced investor or just starting out. Key tips from

Investing in unlisted property schemes? Independent guide for investors about unlisted property schemes This guide is for you, whether you re an experienced investor or just starting out. Key tips from

Licensed by the California Department of Corporations as an Investment Advisor

Licensed by the California Department of Corporations as an Investment Advisor The Impact of the Alternative Minimum Tax (AMT) on Leverage Benefits My associate Matthias Schoener has pointed out to me

Licensed by the California Department of Corporations as an Investment Advisor The Impact of the Alternative Minimum Tax (AMT) on Leverage Benefits My associate Matthias Schoener has pointed out to me

Fees we charge for consumer mortgage lending products

s we charge for consumer mortgage lending products Effective July 2015 Section 1: Understanding fees and charges When we may charge fees The Commonwealth Bank charges fees for administering your account

s we charge for consumer mortgage lending products Effective July 2015 Section 1: Understanding fees and charges When we may charge fees The Commonwealth Bank charges fees for administering your account

HOME EQUITY LINES OF CREDIT

HOME EQUITY LINES OF CREDIT WHAT YOU SHOULD KNOW ABOUT HOME EQUITY LINES OF CREDIT: More and more lenders are offering home equity lines of credit. By using the equity in your home, you may qualify for

HOME EQUITY LINES OF CREDIT WHAT YOU SHOULD KNOW ABOUT HOME EQUITY LINES OF CREDIT: More and more lenders are offering home equity lines of credit. By using the equity in your home, you may qualify for

Statistics. Quarterly Authorised Deposit-taking Institution Property Exposures. March 2014 (released 27 May 2014)

") Statistics Quarterly Authorised Deposit-taking Institution Property Exposures March 2014 (released 27 May 2014) www.apra.gov.au Australian Prudential Regulation Authority Copyright Australian Prudential

Statistics Quarterly Authorised Deposit-taking Institution Property Exposures March 2014 (released 27 May 2014) www.apra.gov.au Australian Prudential Regulation Authority Copyright Australian Prudential

HOME AFFORDABLE MODIFICATION PROGRAM BASE NET PRESENT VALUE (NPV) MODEL SPECIFICATIONS

MODEL SPECIFICATIONS") Overview HOME AFFORDABLE MODIFICATION PROGRAM BASE NET PRESENT VALUE (NPV) MODEL SPECIFICATIONS As a part of the Making Home Affordable Program, we are providing standardized guidance and a base net present

Overview HOME AFFORDABLE MODIFICATION PROGRAM BASE NET PRESENT VALUE (NPV) MODEL SPECIFICATIONS As a part of the Making Home Affordable Program, we are providing standardized guidance and a base net present

Real Estate Investment Newsletter July 2004

The Case for Selling Real Estate in California This month I am writing the newsletter for those investors who currently own rental properties 1 in California. In any type of investing, be it real estate,

The Case for Selling Real Estate in California This month I am writing the newsletter for those investors who currently own rental properties 1 in California. In any type of investing, be it real estate,

CMHC Mortgage Loan Insurance Overview

CMHC Mortgage Loan Insurance view Mortgage loan insurance is typically required when homebuyers make a down payment of less than 2% of the purchase price. Mortgage loan insurance helps protect lenders

CMHC Mortgage Loan Insurance view Mortgage loan insurance is typically required when homebuyers make a down payment of less than 2% of the purchase price. Mortgage loan insurance helps protect lenders

CALL DEBT. Talk to an Aussie Who Cares

A Complete complete Guide Guide to to Debt Relief Debt Relief Solutions in Australia in Australia CALL 1800 00 3328 DEBT Talk to an Aussie Who Cares Contents Introduction... 3 About Debt Rescue... 4 The

A Complete complete Guide Guide to to Debt Relief Debt Relief Solutions in Australia in Australia CALL 1800 00 3328 DEBT Talk to an Aussie Who Cares Contents Introduction... 3 About Debt Rescue... 4 The

Privacy Policy. Effective Date 1 October 2015

Privacy Policy Effective Date 1 October 2015 The Rock - A division of MyState Bank Limited (MyState) ABN 89 067 729 195 AFSL 240896 Australian Credit Licence Number 240896 A wholly owned subsidiary of

Privacy Policy Effective Date 1 October 2015 The Rock - A division of MyState Bank Limited (MyState) ABN 89 067 729 195 AFSL 240896 Australian Credit Licence Number 240896 A wholly owned subsidiary of

SBERBANK GROUP S IFRS RESULTS. March 2015

SBERBANK GROUP S IFRS RESULTS 2014 March 2015 SUMMARY OF PERFORMANCE FOR 2014 STATEMENT OF PROFIT OR LOSS Net profit reached RUB 290.3bn (or RUB 13.45 per ordinary share), compared to RUB 362.0bn (or RUB

SBERBANK GROUP S IFRS RESULTS 2014 March 2015 SUMMARY OF PERFORMANCE FOR 2014 STATEMENT OF PROFIT OR LOSS Net profit reached RUB 290.3bn (or RUB 13.45 per ordinary share), compared to RUB 362.0bn (or RUB

Chapter 7. Mortgage Insurance Premiums (MIPs) Table of Contents

Table of Contents") HUD 4155.2 Chapter 7, Table of Contents Chapter 7. Mortgage Insurance Premiums (MIPs) Table of Contents Chapter 7. Mortgage Insurance Premiums (MIPs) 1. Types of MIPs... 7-1 2. Up Front Mortgage Insurance

HUD 4155.2 Chapter 7, Table of Contents Chapter 7. Mortgage Insurance Premiums (MIPs) Table of Contents Chapter 7. Mortgage Insurance Premiums (MIPs) 1. Types of MIPs... 7-1 2. Up Front Mortgage Insurance

SSAP 24 STATEMENT OF STANDARD ACCOUNTING PRACTICE 24 ACCOUNTING FOR INVESTMENTS IN SECURITIES

SSAP 24 STATEMENT OF STANDARD ACCOUNTING PRACTICE 24 ACCOUNTING FOR INVESTMENTS IN SECURITIES (Issued April 1999) The standards, which have been set in bold italic type, should be read in the context of

SSAP 24 STATEMENT OF STANDARD ACCOUNTING PRACTICE 24 ACCOUNTING FOR INVESTMENTS IN SECURITIES (Issued April 1999) The standards, which have been set in bold italic type, should be read in the context of

Supervisor of Banks: Proper Conduct of Banking Business [9] (4/13) Sound Credit Risk Assessment and Valuation for Loans Page 314-1

![Supervisor of Banks: Proper Conduct of Banking Business [9] (4/13) Sound Credit Risk Assessment and Valuation for Loans Page 314-1](/thumbs/39/20028146.jpg "Supervisor of Banks: Proper Conduct of Banking Business [9] (4/13) Sound Credit Risk Assessment and Valuation for Loans Page 314-1") Sound Credit Risk Assessment and Valuation for Loans Page 314-1 SOUND CREDIT RISK ASSESSMENT AND VALUATION FOR LOANS Principles for sound credit risk assessment and valuation for loans: 1. A banking corporation

Sound Credit Risk Assessment and Valuation for Loans Page 314-1 SOUND CREDIT RISK ASSESSMENT AND VALUATION FOR LOANS Principles for sound credit risk assessment and valuation for loans: 1. A banking corporation

SafeGuard Capital partners

SafeGuard Capital partners Private Lending: Mortgages & Trust Deeds 900 Washington St, Suite 800 Vancouver, WA 98660 877-280-5771 Private Mortgage Lending (Also Known as Trust Deed Investing) Most investors

SafeGuard Capital partners Private Lending: Mortgages & Trust Deeds 900 Washington St, Suite 800 Vancouver, WA 98660 877-280-5771 Private Mortgage Lending (Also Known as Trust Deed Investing) Most investors

Financial Plan for Your 30s

Financial Plan for Your 30s 0 5 10 15 20 25 30 35 40 Number of years 40 years 30 years 35 years 25 years CIR116014 Getting Started In their 30s, many workers have an established job and cash flow. With

Financial Plan for Your 30s 0 5 10 15 20 25 30 35 40 Number of years 40 years 30 years 35 years 25 years CIR116014 Getting Started In their 30s, many workers have an established job and cash flow. With

Standard Charge Terms Land Registration Reform Act

Page 1 of 32 Standard Charge Terms Land Registration Reform Act Filed By: Canadian Imperial Bank of Commerce Filing Number: 201610 Filing Date: March 29, 2016 The following set of standard charge terms

Page 1 of 32 Standard Charge Terms Land Registration Reform Act Filed By: Canadian Imperial Bank of Commerce Filing Number: 201610 Filing Date: March 29, 2016 The following set of standard charge terms

Household debt in Australia

Household debt in Australia Michael Davies 1 Introduction Over the past two decades, Australian households debt levels have increased noticeably and are now fairly high by international standards. The

Household debt in Australia Michael Davies 1 Introduction Over the past two decades, Australian households debt levels have increased noticeably and are now fairly high by international standards. The

Bank of Queensland Limited

APRA 30 April 2012 The Basel II Capital Accord principles took effect in Australia on 1 January 2008. The framework for the application of Basel II in Australia is comprised of three pillars: Pillar 1:

APRA 30 April 2012 The Basel II Capital Accord principles took effect in Australia on 1 January 2008. The framework for the application of Basel II in Australia is comprised of three pillars: Pillar 1:

Investor pre-close briefing

Investor preclose briefing 18 September Proviso Please note that matters discussed in today s presentation may contain forward looking statements which are subject to various risks and uncertainties and

Investor preclose briefing 18 September Proviso Please note that matters discussed in today s presentation may contain forward looking statements which are subject to various risks and uncertainties and

The Effects of Funding Costs and Risk on Banks Lending Rates

The Effects of Funding Costs and Risk on Banks Lending Rates Daniel Fabbro and Mark Hack* After falling for over a decade, the major banks net interest margins appear to have stabilised in a relatively

The Effects of Funding Costs and Risk on Banks Lending Rates Daniel Fabbro and Mark Hack* After falling for over a decade, the major banks net interest margins appear to have stabilised in a relatively

The Westpac Group third quarter 2011 sound core earnings growth

Media Release 16 August 2011 The Westpac Group third quarter 2011 sound core earnings growth Third quarter 2011 highlights (compared to results for the average of 1Q and 2Q 2011) 1 Cash earnings of approximately

Media Release 16 August 2011 The Westpac Group third quarter 2011 sound core earnings growth Third quarter 2011 highlights (compared to results for the average of 1Q and 2Q 2011) 1 Cash earnings of approximately

Catalyst/Princeton Floating Rate Income Fund Class A: CFRAX Class C: CFRCX Class I: CFRIX SUMMARY PROSPECTUS NOVEMBER 1, 2015

Catalyst/Princeton Floating Rate Income Fund Class A: CFRAX Class C: CFRCX Class I: CFRIX SUMMARY PROSPECTUS NOVEMBER 1, 2015 Before you invest, you may want to review the Fund s complete prospectus, which

Catalyst/Princeton Floating Rate Income Fund Class A: CFRAX Class C: CFRCX Class I: CFRIX SUMMARY PROSPECTUS NOVEMBER 1, 2015 Before you invest, you may want to review the Fund s complete prospectus, which

RE: Genworth Response to Final Report of the Financial System Inquiry

Senior Advisor Financial System and Services Division The Treasury Langton Crescent Parkes ACT 2600 Level 26 101 Miller Street North Sydney NSW 2060 Australia Tel 1300 655 422 Fax 1300 662 228 genworth.com.au

Senior Advisor Financial System and Services Division The Treasury Langton Crescent Parkes ACT 2600 Level 26 101 Miller Street North Sydney NSW 2060 Australia Tel 1300 655 422 Fax 1300 662 228 genworth.com.au

Ocwen Loan Servicing, LLC HELPING HOMEOWNERS IS WHAT WE DO! WWW.OCWEN.COM

12/20/11 Paula Bachaman (203) 548-9046 paula@propertychoicesllc.com Property Address: 1024 Lindley Street, Bridgeport, CT 06606 Borrower Name: Jacqueline Muniz Antonio Muniz RE: Short Sale Request Package

12/20/11 Paula Bachaman (203) 548-9046 paula@propertychoicesllc.com Property Address: 1024 Lindley Street, Bridgeport, CT 06606 Borrower Name: Jacqueline Muniz Antonio Muniz RE: Short Sale Request Package

NEED TO KNOW. IFRS 9 Financial Instruments Impairment of Financial Assets

NEED TO KNOW IFRS 9 Financial Instruments Impairment of Financial Assets 2 IFRS 9 FINANCIAL INSTRUMENTS IMPAIRMENT OF FINANCIAL ASSETS IFRS 9 FINANCIAL INSTRUMENTS IMPAIRMENT OF FINANCIAL ASSETS 3 TABLE

NEED TO KNOW IFRS 9 Financial Instruments Impairment of Financial Assets 2 IFRS 9 FINANCIAL INSTRUMENTS IMPAIRMENT OF FINANCIAL ASSETS IFRS 9 FINANCIAL INSTRUMENTS IMPAIRMENT OF FINANCIAL ASSETS 3 TABLE

Nationwide Building Society

Nationwide Building Society Interim Management Statement Q1 2016/17 Underlying profit Statutory profit before tax has been adjusted for a number of items, consistent with prior periods, to derive an underlying

Nationwide Building Society Interim Management Statement Q1 2016/17 Underlying profit Statutory profit before tax has been adjusted for a number of items, consistent with prior periods, to derive an underlying

Introduction to Australian Real Estate Debt Securities

1 Introduction Introduction to Australian Real Estate Debt Securities Superannuation fund investors and managers have for a long time invested in real estate as part of their asset allocation in the belief

1 Introduction Introduction to Australian Real Estate Debt Securities Superannuation fund investors and managers have for a long time invested in real estate as part of their asset allocation in the belief

The Role of Mortgage Insurance under the New Global Regulatory Frameworks

The Role of Mortgage Insurance under the New Global Regulatory Frameworks By Anna Whittingham Regulatory Analyst, Genworth Financial Mortgage Insurance Europe Summary and Overview The introduction of fundamental

The Role of Mortgage Insurance under the New Global Regulatory Frameworks By Anna Whittingham Regulatory Analyst, Genworth Financial Mortgage Insurance Europe Summary and Overview The introduction of fundamental

Significant Mark-To-Market Losses On Credit Derivatives Not Expected To Affect Bond Insurer Ratings

October 31, 2007 Significant Mark-To-Market Losses On Credit Derivatives Not Expected To Affect Bond Insurer Ratings Primary Credit Analyst: Dick P Smith, New York (1) 212-438-2095; dick_smith@standardandpoors.com

October 31, 2007 Significant Mark-To-Market Losses On Credit Derivatives Not Expected To Affect Bond Insurer Ratings Primary Credit Analyst: Dick P Smith, New York (1) 212-438-2095; dick_smith@standardandpoors.com

How To Get A Better Home Loan Rate In Australia

AUSTRALIA S TOP 30 HOME LOAN MYTHS BUSTED Australia s Top 30 Home Loan Myths BUSTED! Fairer home loans for Australians Hi, I m Mark Bouris from Yellow Brick Road. Australia, it s time for a fairer deal

AUSTRALIA S TOP 30 HOME LOAN MYTHS BUSTED Australia s Top 30 Home Loan Myths BUSTED! Fairer home loans for Australians Hi, I m Mark Bouris from Yellow Brick Road. Australia, it s time for a fairer deal

The Adam Lee Team 480-331-3501 Info@theadamleeteam.com. Alternatives to Foreclosure & REASONS WHY SHORT SALES ARE THE BETTER SOLUTION!

The Adam Lee Team 480-331-3501 Info@ Alternatives to Foreclosure & REASONS WHY SHORT SALES ARE THE BETTER SOLUTION! Options When Facing Foreclosure 1. Do Nothing: If you choose to do nothing, you will

The Adam Lee Team 480-331-3501 Info@ Alternatives to Foreclosure & REASONS WHY SHORT SALES ARE THE BETTER SOLUTION! Options When Facing Foreclosure 1. Do Nothing: If you choose to do nothing, you will

Additional Terms and Conditions

Page 1 of 35 Additional Terms and Conditions The following set of additional terms and conditions is attached as Schedule B to Canadian Imperial Bank of Commerce Residential Mortgages in Newfoundland and

Page 1 of 35 Additional Terms and Conditions The following set of additional terms and conditions is attached as Schedule B to Canadian Imperial Bank of Commerce Residential Mortgages in Newfoundland and

Walshs Financial Planning Financial Services + Credit Guide Version 03.2016

Walshs Financial Planning Financial Services + Credit Guide Version 03.2016 The purpose of this guide is to give you information about: The services we or our advisers are authorised to provide How we

Walshs Financial Planning Financial Services + Credit Guide Version 03.2016 The purpose of this guide is to give you information about: The services we or our advisers are authorised to provide How we

Atrium Mortgage Investment Corporation (TSX: AI) Record Year / Shares at Attractive Entry Levels. Sector/Industry: Mortgage Investment Corporation

Record Year / Shares at Attractive Entry Levels. Sector/Industry: Mortgage Investment Corporation") Siddharth Rajeev, B.Tech, MBA, CFA Analyst February 17, 2016 Atrium Mortgage Investment Corporation (TSX: AI) Record Year / Shares at Attractive Entry Levels Sector/Industry: Mortgage Investment Corporation

Siddharth Rajeev, B.Tech, MBA, CFA Analyst February 17, 2016 Atrium Mortgage Investment Corporation (TSX: AI) Record Year / Shares at Attractive Entry Levels Sector/Industry: Mortgage Investment Corporation

Mortgage Terms. Accrued interest Interest that is earned but not paid, adding to the amount owed.

Mortgage Terms Accrued interest Interest that is earned but not paid, adding to the amount owed. Negative amortization A rise in the loan balance when the mortgage payment is less than the interest due.

Mortgage Terms Accrued interest Interest that is earned but not paid, adding to the amount owed. Negative amortization A rise in the loan balance when the mortgage payment is less than the interest due.

MORTGAGE TERMS. Assignment of Mortgage A document used to transfer ownership of a mortgage from one party to another.

MORTGAGE TERMS Acceleration Clause This is a clause used in a mortgage that can be enforced to make the entire amount of the loan and any interest due immediately. This is usually stipulated if you default

MORTGAGE TERMS Acceleration Clause This is a clause used in a mortgage that can be enforced to make the entire amount of the loan and any interest due immediately. This is usually stipulated if you default

Standard Chartered today releases its Interim Management Statement for the third quarter of 2015.

Standard Chartered PLC Interim Management Statement 3 November 2015 Standard Chartered today releases its Interim Management Statement for the third quarter of 2015. Bill Winters, Group Chief Executive,

Standard Chartered PLC Interim Management Statement 3 November 2015 Standard Chartered today releases its Interim Management Statement for the third quarter of 2015. Bill Winters, Group Chief Executive,

Macquarie Prime Loan Facility

Macquarie Prime Loan Facility Product Disclosure Statement Contents Section 1 - About Macquarie Bank Limited and the Macquarie Prime Loan Facility 1 Section 2 - Benefits of a Macquarie Prime Loan Facility

Macquarie Prime Loan Facility Product Disclosure Statement Contents Section 1 - About Macquarie Bank Limited and the Macquarie Prime Loan Facility 1 Section 2 - Benefits of a Macquarie Prime Loan Facility

What You Should Know About Home Equity Lines of Credit and Important Terms of FlexEquity SM

What You Should Know About Home Equity Lines of Credit and Important Terms of FlexEquity SM Effective March 1, 2008 The Housing Financial Discrimination Act of 1977 Fair Lending Notice It is illegal to

What You Should Know About Home Equity Lines of Credit and Important Terms of FlexEquity SM Effective March 1, 2008 The Housing Financial Discrimination Act of 1977 Fair Lending Notice It is illegal to

Section C. Maximum Mortgage Amounts on Streamline Refinances Overview

Section C. Maximum Mortgage Amounts on Overview In This Section This section contains the topics listed in the table below. Topic Topic Name See Page 1 General Information on 3-C-2 2 Without an Appraisal

Section C. Maximum Mortgage Amounts on Overview In This Section This section contains the topics listed in the table below. Topic Topic Name See Page 1 General Information on 3-C-2 2 Without an Appraisal

How Mortgage Insurance Works A GUIDE FOR LENDERS

How Mortgage Insurance Works A GUIDE FOR LENDERS 2 What Is Mortgage Insurance? It s a financial guaranty that reduces the loss to the lender or investor in the event the borrowers do not repay their mortgage

How Mortgage Insurance Works A GUIDE FOR LENDERS 2 What Is Mortgage Insurance? It s a financial guaranty that reduces the loss to the lender or investor in the event the borrowers do not repay their mortgage

TILA Escrow Requirements for High Priced Mortgage Loans (12 CFR 1026.35)

") TILA Escrow Requirements for High Priced Mortgage Loans (12 CFR 1026.35) The Consumer Financial Protection Bureau s (CFPB) mortgage rules include new escrow account requirements for higher-priced mortgage

TILA Escrow Requirements for High Priced Mortgage Loans (12 CFR 1026.35) The Consumer Financial Protection Bureau s (CFPB) mortgage rules include new escrow account requirements for higher-priced mortgage

EASY FOREX TRADING LTD DISCLOSURE AND MARKET DISCIPLINE IN ACCORDANCE WITH CAPITAL ADEQUACY AND THE REQUIREMENTS ON RISK MANAGEMENT

EASY FOREX TRADING LTD DISCLOSURE AND MARKET DISCIPLINE IN ACCORDANCE WITH CAPITAL ADEQUACY AND THE REQUIREMENTS ON RISK MANAGEMENT 31 st December 2012 Introduction For the purposes of Directive DI144-2007-05

EASY FOREX TRADING LTD DISCLOSURE AND MARKET DISCIPLINE IN ACCORDANCE WITH CAPITAL ADEQUACY AND THE REQUIREMENTS ON RISK MANAGEMENT 31 st December 2012 Introduction For the purposes of Directive DI144-2007-05

Banks. Commonwealth Bank of Australia. Australia Credit Analysis. Rating Rationale. Key Rating Drivers. Profile

Australia Credit Analysis Ratings Foreign Currency Long Term IDR AA Short Term IDR F1+ Individual Rating A/B Support Rating 1 Support Rating Floor A Sovereign Risk Foreign Currency Long Term IDR Local

Australia Credit Analysis Ratings Foreign Currency Long Term IDR AA Short Term IDR F1+ Individual Rating A/B Support Rating 1 Support Rating Floor A Sovereign Risk Foreign Currency Long Term IDR Local

Basel Committee on Banking Supervision

Basel Committee on Banking Supervision Frequently asked questions on the Basel III leverage ratio framework April 2016 (update of FAQs published in July 2015) This publication is available on the BIS website

Basel Committee on Banking Supervision Frequently asked questions on the Basel III leverage ratio framework April 2016 (update of FAQs published in July 2015) This publication is available on the BIS website

Assurance and accounting A Guide to Financial Instruments for Private

june 2011 www.bdo.ca Assurance and accounting A Guide to Financial Instruments for Private Enterprises and Private Sector t-for-profit Organizations For many entities adopting the Accounting Standards

june 2011 www.bdo.ca Assurance and accounting A Guide to Financial Instruments for Private Enterprises and Private Sector t-for-profit Organizations For many entities adopting the Accounting Standards

Sberbank Group s IFRS Results for 6 Months 2013. August 2013

Sberbank Group s IFRS Results for 6 Months 2013 August 2013 Summary of 6 Months 2013 performance: Income Statement Net profit reached RUB 174.5 bn (or RUB 7.95 per ordinary share), a 0.5% decrease on RUB

Sberbank Group s IFRS Results for 6 Months 2013 August 2013 Summary of 6 Months 2013 performance: Income Statement Net profit reached RUB 174.5 bn (or RUB 7.95 per ordinary share), a 0.5% decrease on RUB

Causes of mortgage defaults and repossessions

4 Causes of mortgage defaults and repossessions 4.1 The RBA estimates that there are 5.3 million housing loans outstanding in Australia. Of these, it estimates 11,800, or 0.22 per cent, are in arrears

4 Causes of mortgage defaults and repossessions 4.1 The RBA estimates that there are 5.3 million housing loans outstanding in Australia. Of these, it estimates 11,800, or 0.22 per cent, are in arrears

HOUSE BILL 2242 AN ACT AMENDING TITLE 6, ARIZONA REVISED STATUTES, BY ADDING CHAPTER 16; RELATING TO REVERSE MORTGAGES.

Senate Engrossed House Bill State of Arizona House of Representatives Forty-ninth Legislature Second Regular Session HOUSE BILL AN ACT AMENDING TITLE, ARIZONA REVISED STATUTES, BY ADDING CHAPTER ; RELATING

Senate Engrossed House Bill State of Arizona House of Representatives Forty-ninth Legislature Second Regular Session HOUSE BILL AN ACT AMENDING TITLE, ARIZONA REVISED STATUTES, BY ADDING CHAPTER ; RELATING

Retail and Business Banking Financial Services Guide, Credit Guide and Privacy Statement

Retail and Business Banking Financial Services Guide, Credit Guide and Privacy Statement Preparation Date: 31 July 2015 St.George Bank - A Division of Westpac Banking Corporation ABN 33 007 457 141 AFSL

Retail and Business Banking Financial Services Guide, Credit Guide and Privacy Statement Preparation Date: 31 July 2015 St.George Bank - A Division of Westpac Banking Corporation ABN 33 007 457 141 AFSL

lending Lending Advice.much more than just a Mortgage Broker

lending Lending Advice.much more than just a Mortgage Broker Notes: living a life well planned General Advice Warning: Any advice in this publication is of a general nature only and has not been tailored

lending Lending Advice.much more than just a Mortgage Broker Notes: living a life well planned General Advice Warning: Any advice in this publication is of a general nature only and has not been tailored

Recent Developments in the Housing Market and its Financing

Recent Developments in the Housing Market and its Financing Luci Ellis Head of Financial Stability Department Financial Review Residential Property Conference 2010 Sydney - 18 May 2010 I d like to thank

Recent Developments in the Housing Market and its Financing Luci Ellis Head of Financial Stability Department Financial Review Residential Property Conference 2010 Sydney - 18 May 2010 I d like to thank

Transaction Update: Swedbank Mortgage AB's Covered Bond Program

Transaction Update: Swedbank Mortgage AB's Covered Bond Program Primary Credit Analyst: Casper R Andersen, London (44) 20-7176-6757; casper.andersen@standardandpoors.com Secondary Contact: Judit O Woelk,

Transaction Update: Swedbank Mortgage AB's Covered Bond Program Primary Credit Analyst: Casper R Andersen, London (44) 20-7176-6757; casper.andersen@standardandpoors.com Secondary Contact: Judit O Woelk,

13 May 2015. 1Q2015 Financial Results

13 May 2015 1Q2015 Financial Results Forward Looking Statements Important information All information contained in this presentation should be regarded as preliminary and based on company data available

13 May 2015 1Q2015 Financial Results Forward Looking Statements Important information All information contained in this presentation should be regarded as preliminary and based on company data available

PRIVACY NOTICE AND CONSENT

Australian Credit Licence Number 387406 PRIVACY NOTICE AND CONSENT This privacy notice and consent relates to an application (the application) you make to a mortgage manager for a loan (your loan) or in

Australian Credit Licence Number 387406 PRIVACY NOTICE AND CONSENT This privacy notice and consent relates to an application (the application) you make to a mortgage manager for a loan (your loan) or in

INVESTMENT. Understanding your investment in super doesn t have to be hard. You don t need to be a financial whiz to make it work for you!

1 Understanding your investment in super doesn t have to be hard. You don t need to be a financial whiz to make it work for you! You just need to understand your options and how you can make the most of

1 Understanding your investment in super doesn t have to be hard. You don t need to be a financial whiz to make it work for you! You just need to understand your options and how you can make the most of

Commerzbank: Strategy successful net profit of over 1 billion euros and dividend

IR release 12 February 2016 Commerzbank: Strategy successful net profit of over 1 billion euros and dividend Operating profit in 2015 more than doubled to EUR 1,909 m (2014: EUR 689 m) Operating profit

IR release 12 February 2016 Commerzbank: Strategy successful net profit of over 1 billion euros and dividend Operating profit in 2015 more than doubled to EUR 1,909 m (2014: EUR 689 m) Operating profit

Reclassification of financial assets

Issue 34 / March 2009 Supplement to IFRS outlook Reclassification of financial assets This publication summarises all the recent amendments to IAS 39 Financial Instruments: Recognition and Measurement

Issue 34 / March 2009 Supplement to IFRS outlook Reclassification of financial assets This publication summarises all the recent amendments to IAS 39 Financial Instruments: Recognition and Measurement

Genworth Australia - Mortgage Insurance

Genworth Australia - Mortgage Insurance September 26, 2011 2011 Genworth Financial, Inc. All rights reserved. Forward-Looking Statements This presentation contains certain forward-looking statements within

Genworth Australia - Mortgage Insurance September 26, 2011 2011 Genworth Financial, Inc. All rights reserved. Forward-Looking Statements This presentation contains certain forward-looking statements within

Guidelines for Extra-Judicial Restructuring of Mortgage Loans

Guidelines for Extra-Judicial Restructuring of Mortgage Loans Helping lenders to manage better risks and consumers to make more informed decisions Friedemann Roy The World Bank, Washington DC 2 Objectives

Guidelines for Extra-Judicial Restructuring of Mortgage Loans Helping lenders to manage better risks and consumers to make more informed decisions Friedemann Roy The World Bank, Washington DC 2 Objectives

JOINT RBA-APRA SUBMISSION TO THE INQUIRY INTO HOME LENDING PRACTICES AND PROCESSES

JOINT RBA-APRA SUBMISSION TO THE INQUIRY INTO HOME LENDING PRACTICES AND PROCESSES Introduction This submission brings together the factual material available to the Reserve Bank of Australia and APRA

JOINT RBA-APRA SUBMISSION TO THE INQUIRY INTO HOME LENDING PRACTICES AND PROCESSES Introduction This submission brings together the factual material available to the Reserve Bank of Australia and APRA

GOLDMAN SACHS VARIABLE INSURANCE TRUST

GOLDMAN SACHS VARIABLE INSURANCE TRUST Institutional and Service Shares of the Goldman Sachs Money Market Fund (the Fund ) Supplement dated July 29, 2015 to the Prospectuses and Summary Prospectuses, each

GOLDMAN SACHS VARIABLE INSURANCE TRUST Institutional and Service Shares of the Goldman Sachs Money Market Fund (the Fund ) Supplement dated July 29, 2015 to the Prospectuses and Summary Prospectuses, each

Introduction. The new rules and forms take effect October 3 rd, 2015 for all loan applications submitted on or after that date.

Introduction The new rules and forms take effect October 3 rd, 2015 for all loan applications submitted on or after that date. Phased-in approach: Continue to close out loans in the lender s pipeline using

Introduction The new rules and forms take effect October 3 rd, 2015 for all loan applications submitted on or after that date. Phased-in approach: Continue to close out loans in the lender s pipeline using

MORTGAGE FOCUS with Kelly Wealth Lending Services and Acceptance Finance

July/August 2015 MORTGAGE FOCUS with Kelly Wealth Lending Services and Acceptance Finance Happy New Financial Year! We hope that tax time is not proving to be too tedious for you and you re looking forward

July/August 2015 MORTGAGE FOCUS with Kelly Wealth Lending Services and Acceptance Finance Happy New Financial Year! We hope that tax time is not proving to be too tedious for you and you re looking forward

A CONSUMER'S GUIDE TO. from YOUR North Carolina Department of Insurance CONSUMER'SGUIDE

A CONSUMER'S GUIDE TO from YOUR North Carolina Department of Insurance CONSUMER'SGUIDE A MESSAGE FROM YOUR INSURANCE COMMISSIONER Greetings, The North Carolina Department of Insurance recognizes that insurance

A CONSUMER'S GUIDE TO from YOUR North Carolina Department of Insurance CONSUMER'SGUIDE A MESSAGE FROM YOUR INSURANCE COMMISSIONER Greetings, The North Carolina Department of Insurance recognizes that insurance

Chief Executive Officers of National Banks, Department and Division Heads, and All Examining Personnel

OCC 2003-1 OCC BULLETIN Comptroller of the Currency Administrator of National Banks Subject: Credit Card Lending Description: Account Management and Loss Allowance Guidance TO: Chief Executive Officers

OCC 2003-1 OCC BULLETIN Comptroller of the Currency Administrator of National Banks Subject: Credit Card Lending Description: Account Management and Loss Allowance Guidance TO: Chief Executive Officers

Basel II, Pillar 3 Disclosure for Sun Life Financial Trust Inc.

Basel II, Pillar 3 Disclosure for Sun Life Financial Trust Inc. Introduction Basel II is an international framework on capital that applies to deposit taking institutions in many countries, including Canada.

Basel II, Pillar 3 Disclosure for Sun Life Financial Trust Inc. Introduction Basel II is an international framework on capital that applies to deposit taking institutions in many countries, including Canada.

CREDIT CARD AGREEMENT AND DISCLOSURE STATEMENT

CREDIT CARD AGREEMENT AND DISCLOSURE STATEMENT THIS IS YOUR CREDIT CARD AGREEMENT AND IT INCLUDES NECESSARY FEDERAL TRUTH-IN- LENDING DISCLOSURE STATEMENTS, WORLD MASTERCARD, MASTERCARD PLATINUM, MASTERCARD

CREDIT CARD AGREEMENT AND DISCLOSURE STATEMENT THIS IS YOUR CREDIT CARD AGREEMENT AND IT INCLUDES NECESSARY FEDERAL TRUTH-IN- LENDING DISCLOSURE STATEMENTS, WORLD MASTERCARD, MASTERCARD PLATINUM, MASTERCARD

Our Ref.: B4/1C. 14 September 2012. The Chief Executive All Authorized Institutions. Dear Sir/Madam, Prudential Measures for Property Mortgage Loans

Our Ref.: B4/1C 14 September 2012 The Chief Executive All Authorized Institutions Dear Sir/Madam, Prudential Measures for Property Mortgage Loans The Hong Kong Monetary Authority (HKMA) notices that there

Our Ref.: B4/1C 14 September 2012 The Chief Executive All Authorized Institutions Dear Sir/Madam, Prudential Measures for Property Mortgage Loans The Hong Kong Monetary Authority (HKMA) notices that there

FHA Home Loans 101 An Easy Reference Guide

FHA Home Loans 101 An Easy Reference Guide Updated for loans on or after June 3, 2013 Congratulations on Starting Your Journey to Home Ownership This guide offers a quick look at vital information you

FHA Home Loans 101 An Easy Reference Guide Updated for loans on or after June 3, 2013 Congratulations on Starting Your Journey to Home Ownership This guide offers a quick look at vital information you

lending Lending Advice.much more than just a Mortgage Broker

lending Lending Advice.much more than just a Mortgage Broker living a life well planned We rebate trail commissions it s our gift to you. We are very well known for our pioneering rebating of trail commission

lending Lending Advice.much more than just a Mortgage Broker living a life well planned We rebate trail commissions it s our gift to you. We are very well known for our pioneering rebating of trail commission

Predatory Lending : Predatory Lending Practices

Predatory Lending : Predatory Lending Practices Taken and abbreviated from ACORN website: http://www.acorn.org/acorn10/predatorylending/practices.htm The reach and effect of abusive practices by predatory

Predatory Lending : Predatory Lending Practices Taken and abbreviated from ACORN website: http://www.acorn.org/acorn10/predatorylending/practices.htm The reach and effect of abusive practices by predatory

Discussion Paper. Maximum Event Retention for Lenders Mortgage Insurers. www.apra.gov.au Australian Prudential Regulation Authority.

Discussion Paper Maximum Event Retention for Lenders Mortgage Insurers September 2008 www.apra.gov.au Australian Prudential Regulation Authority Disclaimer and copyright This prudential practice guide

Discussion Paper Maximum Event Retention for Lenders Mortgage Insurers September 2008 www.apra.gov.au Australian Prudential Regulation Authority Disclaimer and copyright This prudential practice guide

WESTPAC DELIVERS SOUND RESULT IN CHALLENGING CONDITIONS

Media Release 2 May 2016 WESTPAC DELIVERS SOUND RESULT IN CHALLENGING CONDITIONS Westpac Group today announced First Half 2016 statutory net profit of $3,701 million, up 3% over the prior corresponding

Media Release 2 May 2016 WESTPAC DELIVERS SOUND RESULT IN CHALLENGING CONDITIONS Westpac Group today announced First Half 2016 statutory net profit of $3,701 million, up 3% over the prior corresponding

The Aftermath of the Housing Bubble

The Aftermath of the Housing Bubble James Bullard President and CEO, FRB-St. Louis Housing in America: Innovative Solutions to Address the Needs of Tomorrow 5 June 2012 The Bipartisan Policy Center St.

The Aftermath of the Housing Bubble James Bullard President and CEO, FRB-St. Louis Housing in America: Innovative Solutions to Address the Needs of Tomorrow 5 June 2012 The Bipartisan Policy Center St.

COMPREHENSIVE LOAN MODIFICATION PROGRAM

I. Definitions. COMPREHENSIVE LOAN MODIFICATION PROGRAM a) Residential mortgage loan shall mean any loan primarily for personal, family, or household use that is secured by a mortgage, deed of trust, or

I. Definitions. COMPREHENSIVE LOAN MODIFICATION PROGRAM a) Residential mortgage loan shall mean any loan primarily for personal, family, or household use that is secured by a mortgage, deed of trust, or

EC 341 Monetary and Banking Institutions, Boston University Summer 2, 2012 Homework 3 Due date: Tuesday, July 31, 6:00 PM.

EC 341 Monetary and Banking Institutions, Boston University Summer 2, 2012 Homework 3 Due date: Tuesday, July 31, 6:00 PM. Problem 1 Questions 1, 4, 6, 8, 12, 13, 16, 18, 22, and 23 from Chapter 8. Solutions:

EC 341 Monetary and Banking Institutions, Boston University Summer 2, 2012 Homework 3 Due date: Tuesday, July 31, 6:00 PM. Problem 1 Questions 1, 4, 6, 8, 12, 13, 16, 18, 22, and 23 from Chapter 8. Solutions:

GRF_116_1 Probable Maximum Loss for LMIs - Standard Loans

GRF_116_1 Probable Maximum Loss for LMIs - Standard Loans These instructions must be read in conjunction with the general instruction guide. Explanatory notes Standard loan A standard loan is one which

GRF_116_1 Probable Maximum Loss for LMIs - Standard Loans These instructions must be read in conjunction with the general instruction guide. Explanatory notes Standard loan A standard loan is one which