How to Successfully Apply for a Business Loan

|

|

|

- Emerald Bennett

- 8 years ago

- Views:

Transcription

1 How to Successfully Apply for a Business Loan

2 Presenter Marc Rand 20 years lending experience, including nonprofits Micro lending to large multinational corporate lending. Lender, donor, foundation, and board member perspectives 2

3 Overview of the Session Definitions Why should I look for a loan? Underwriting process Suggestions on how best to prepare How to evaluate your bank and how your bank will evaluate your organization Resources 3

4 A loan is a loan, is a loan Line of credit Acquisition loan Equipment loan Construction loan Permanent loan/mortgage 4

5 We have plenty of cash, why apply for a loan? Cash flow seasonality, contract reimbursable, fundraisers, late funders Equipment Building acquisition Stamp of approval 5

6 Know your rights, and know your terms Collateral, security Interest rate fixed, variable Prepayment Covenants Revolver Balloon Bullet Prime, Libor Liquidity Leverage 6

7 What does a bank underwriting process look like? Gather information Financials, history, cash flow, purpose Collateral Experience borrowing Evaluation of information Goal is to determine what the risks and mitigating factors are How does your organization compare to others in the industry? Review Credit officer and relationship manager Documentation and closing Loan agreement, promissory note, deed of trust, environmental, UCC 1 Timeline 2 3 months Monitoring 7

8 How will the bank review my application? Banks are evaluating two principle ideas: What are the risks and mitigating factors, and what are the primary and secondary sources of repayment? Risk and return pricing Debt service coverage ratio 1.2x or more Loan to value 80% or less 10+ weeks of cash reserves Covenants/restrictions/requirements clean up period, no additional bank debt, move bank accounts, financial reporting What is the financial sophistication of the organization? 8

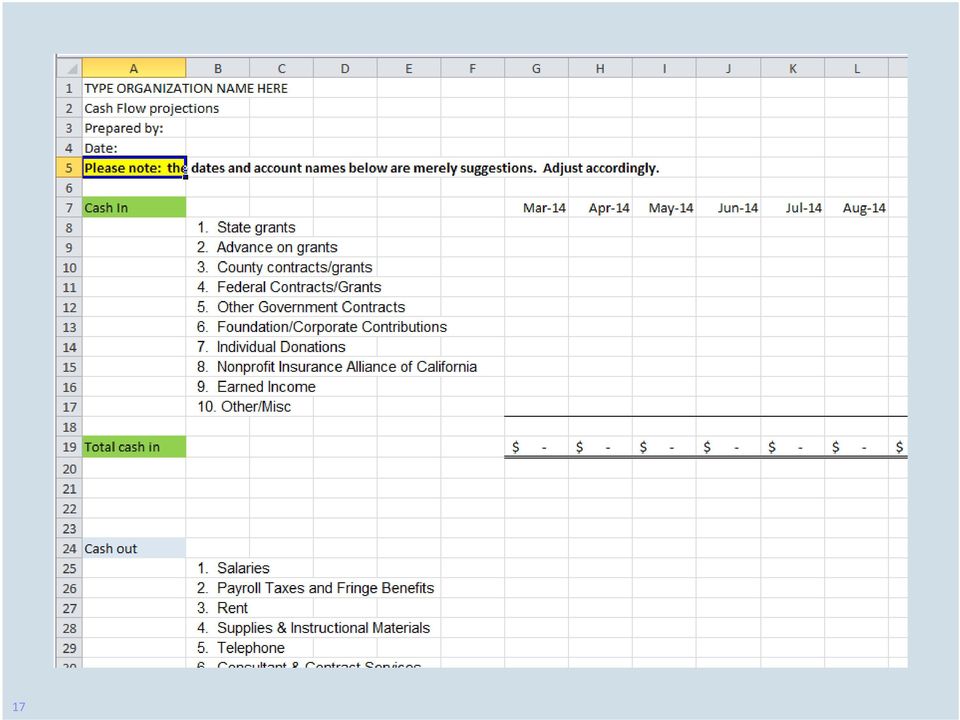

9 How can you prepare for a successful loan application? Be prepared! Provide a loan package/application that includes the following information: 4 years of financials (audits, 990s) Any financial summary report explanation of variations Cash flow projections for the life of the loan Any funder references Sector analysis Strategic plan Bios of key management Proof of insurance property, directors and officers, etc. 9

10 Where do things go awry? Loan closing Pricing Restrictions moving bank accounts Some bankers may not understand nonprofits Collateral requirements Guarantees 10

11 Suggestions and Discussion Topics The more prepared you are, the easier, quicker and more likely your loan will be approved. The best time to apply for a loan is when you do not need it. Is it time to move your banking relationship? What are the organization s long term needs? What are the purposes and restrictions for the loan? 11

12 Banking Relationships What are the long term benefits of working with this institution? What is the pricing? Are there hidden fees? (closing costs, title insurance, application fee, commitment fee) Are you happy with the service? What is their value add? Does the bank understand your business? Can they offer advice versus just credit and checking? What other services do they offer? Fraud, wires, online services, direct deposit? 12

13 How will others look at our organization now that we have debt? Foundations Board of Directors Funders and donors Banks Government 13

14 Who lends to nonprofits? Nonprofit Finance Fund Northern California Grantsmakers arts organizations NIAC 12 month loans Low Income Investment Fund housing, childcare Community Foundations 14

15 NIAC Loan Fund Loans up to $50,000 6% interest fixed Unsecured, no board guarantee required 1 month turnaround time 12 month term Application fee of $250 (loans up to $25,000) Application fee of $500 (loans up to $50,000) 15

Application fee of $500 (loans up")

16 16

17 17

18 18

19 If you have questions or need additional information, contact: Marc Rand

Use this section to learn more about business loans and specific financial products that might be right for your company.

Types of Financing Use this section to learn more about business loans and specific financial products that might be right for your company. Revolving Line Of Credit Revolving lines of credit are the most

Types of Financing Use this section to learn more about business loans and specific financial products that might be right for your company. Revolving Line Of Credit Revolving lines of credit are the most

The Corporate Finance Shift to Asset- Based Loans PART I

The Corporate Finance Shift to Asset- Based Loans PART I Realistic Business Owners Look Beyond Bank Cash Flow Loans 1 Brian Ballo Corporate Finance Associates The Good News 1 Financing is currently available

The Corporate Finance Shift to Asset- Based Loans PART I Realistic Business Owners Look Beyond Bank Cash Flow Loans 1 Brian Ballo Corporate Finance Associates The Good News 1 Financing is currently available

SAFE Credit Underwriting Guidelines for Non-Profit Lending. Organization Type: NON-PROFIT ORGANIZATIONS. Bridge Loan Guidelines.

Introduction The Credit Underwriting Guidelines (CUG) manual is designed for use with products delivered to faith-based and non-profit organizations. The guidelines herein govern the granting of credit

Introduction The Credit Underwriting Guidelines (CUG) manual is designed for use with products delivered to faith-based and non-profit organizations. The guidelines herein govern the granting of credit

3. Seasonal or cyclical working capital to finance the temporary cash shortfalls due to the nature of the firm s normal business cycle.

11.437 Financing Community Economic Development Class 5: Working Capital Financing I. Three different meanings of term working capital 1. Excess of current assets over current liabilities 2. Firm's investment

11.437 Financing Community Economic Development Class 5: Working Capital Financing I. Three different meanings of term working capital 1. Excess of current assets over current liabilities 2. Firm's investment

Neighborhood Lending Partners, Inc. Florida Minority Affordable Housing Development Fund Presentation Florida Housing Coalition September 9, 2014

Neighborhood Lending Partners, Inc. Florida Minority Affordable Housing Development Fund Presentation Florida Housing Coalition September 9, 2014 Overview Neighborhood Lending Partners Certified as a CDFI-providing

Neighborhood Lending Partners, Inc. Florida Minority Affordable Housing Development Fund Presentation Florida Housing Coalition September 9, 2014 Overview Neighborhood Lending Partners Certified as a CDFI-providing

NOTE ON LOAN CAPITAL MARKETS

The structure and use of loan products Most businesses use one or more loan products. A company may have a syndicated loan, backstop, line of credit, standby letter of credit, bridge loan, mortgage, or

The structure and use of loan products Most businesses use one or more loan products. A company may have a syndicated loan, backstop, line of credit, standby letter of credit, bridge loan, mortgage, or

How Bankers Think. Build a sound financial base to support your company for future growth

How Bankers Think Build a sound financial base to support your company for future growth Presented by: Lisa Chapman Business Planning, Social Media Marketing & SEO 615-477-8412 Questions to Consider First

How Bankers Think Build a sound financial base to support your company for future growth Presented by: Lisa Chapman Business Planning, Social Media Marketing & SEO 615-477-8412 Questions to Consider First

SBA 504 Non Bank Business Model. Presented by Sok Cordell

SBA 504 Non Bank Business Model Presented by Sok Cordell CH Capital Partners LLC (SBA Non Bank Lending Program) The information contained in this presentation has been obtained from sources believed to

SBA 504 Non Bank Business Model Presented by Sok Cordell CH Capital Partners LLC (SBA Non Bank Lending Program) The information contained in this presentation has been obtained from sources believed to

GrowFL and SunTrust Bank Present: How To Utilize The SBA Loan Programs To Improve Cash Flow And Grow Your Business

GrowFL and SunTrust Bank Present: How To Utilize The SBA Loan Programs To Improve Cash Flow And Grow Your Business GrowFL Webinar Series Date: March 5, 2012 Presented by: Hetal Engineer, SunTrust VP hetal.engineer@suntrust.com

GrowFL and SunTrust Bank Present: How To Utilize The SBA Loan Programs To Improve Cash Flow And Grow Your Business GrowFL Webinar Series Date: March 5, 2012 Presented by: Hetal Engineer, SunTrust VP hetal.engineer@suntrust.com

MRRA Revolving Loan Program for Tenant Leasehold Improvements and Working Capital. Lending Policies and Procedures

MRRA Revolving Loan Program for Tenant Leasehold Improvements and Working Capital Lending Policies and Procedures Midcoast Regional Redevelopment Authority Mission Statement MRRA was established by the

MRRA Revolving Loan Program for Tenant Leasehold Improvements and Working Capital Lending Policies and Procedures Midcoast Regional Redevelopment Authority Mission Statement MRRA was established by the

Nonprofit Finance Fund. Accessing and Managing Credit Webinar. Presented by. Stephanie DeVane Associate Director, Financial Services

Nonprofit Finance Fund Accessing and Managing Credit Webinar Presented by Stephanie DeVane Associate Director, Financial Services Jessica LaBarbera Associate Director, Northeast Region Released the week

Nonprofit Finance Fund Accessing and Managing Credit Webinar Presented by Stephanie DeVane Associate Director, Financial Services Jessica LaBarbera Associate Director, Northeast Region Released the week

SBA MICROLOAN PROGRAM. Session: Loan Side Basics

SBA MICROLOAN PROGRAM Session: Loan Side Basics Microloan Program Purpose The Microloan Program assists women, low income, veteran, and minority entrepreneurs, and other small businesses in need of financing

SBA MICROLOAN PROGRAM Session: Loan Side Basics Microloan Program Purpose The Microloan Program assists women, low income, veteran, and minority entrepreneurs, and other small businesses in need of financing

Overview of Financial Solutions

Overview of Financial Solutions The Etra Advisory Group provides solutions to businesses for growth, expansion, cash flow, refinance and acquisition. We cover the world of business financing that banks

Overview of Financial Solutions The Etra Advisory Group provides solutions to businesses for growth, expansion, cash flow, refinance and acquisition. We cover the world of business financing that banks

Part II: Understanding the Lender s Perspective Evaluation of the franchise Variables in decision making How to enhance the funding package

Financial Summit Part II: Understanding the Lender s Perspective Evaluation of the franchise Variables in decision making How to enhance the funding package Moderator: Brad Fishman, CFE, CEO, Fishman Public

Financial Summit Part II: Understanding the Lender s Perspective Evaluation of the franchise Variables in decision making How to enhance the funding package Moderator: Brad Fishman, CFE, CEO, Fishman Public

Financing for Community Development

Financing for Community Development Introduction The attached sheets describe the financing LISC provides for an array of activities carried out by community development corporations (CDCs) and other community-based

Financing for Community Development Introduction The attached sheets describe the financing LISC provides for an array of activities carried out by community development corporations (CDCs) and other community-based

NONPROFITS ASSISTANCE FUND FINANCIAL STATEMENTS YEARS ENDED MARCH 31, 2015 AND 2014

FINANCIAL STATEMENTS YEARS ENDED TABLE OF CONTENTS YEARS ENDED INDEPENDENT AUDITORS' REPORT 1 FINANCIAL STATEMENTS STATEMENTS OF FINANCIAL POSITION 3 STATEMENTS OF ACTIVITIES 5 STATEMENTS OF CASH FLOWS

FINANCIAL STATEMENTS YEARS ENDED TABLE OF CONTENTS YEARS ENDED INDEPENDENT AUDITORS' REPORT 1 FINANCIAL STATEMENTS STATEMENTS OF FINANCIAL POSITION 3 STATEMENTS OF ACTIVITIES 5 STATEMENTS OF CASH FLOWS

Real Estate Principles Chapter 12 Quiz

Real Estate Principles Chapter 12 Quiz 1. A prudent lender who is deciding whether or not to make a real estate loan to a prospective borrower will ensure that: A. the market value of the property is greater

Real Estate Principles Chapter 12 Quiz 1. A prudent lender who is deciding whether or not to make a real estate loan to a prospective borrower will ensure that: A. the market value of the property is greater

WHAT IS PREMIUM HOW DOES PREMIUM FINANCING? FINANCING WORK?

Life Insurance Premium Financing 1 of 5 WHAT IS PREMIUM FINANCING? Premium financing allows individuals who have a life insurance need to defer using their liquid assets to fund a life insurance policy.

Life Insurance Premium Financing 1 of 5 WHAT IS PREMIUM FINANCING? Premium financing allows individuals who have a life insurance need to defer using their liquid assets to fund a life insurance policy.

Understanding Your credit risk

www.unitedfinance.com Personal Loans 101: Understanding Your credit risk AFSA Education Foundation 919 Eighteenth Street, NW Washington, DC 20006-5517 Phone: 888-400-7577 Email: personalloans101@afsaef.org

www.unitedfinance.com Personal Loans 101: Understanding Your credit risk AFSA Education Foundation 919 Eighteenth Street, NW Washington, DC 20006-5517 Phone: 888-400-7577 Email: personalloans101@afsaef.org

Personal Loans 101: Understanding Your credit risk

Personal Loans 101: Understanding Your credit risk Loans have some risk for both the borrower and the lender. The borrower takes on the responsibilities and terms of paying back the loan. The lender s

Personal Loans 101: Understanding Your credit risk Loans have some risk for both the borrower and the lender. The borrower takes on the responsibilities and terms of paying back the loan. The lender s

Small Business Finance Thinking Strategically

Small Business Finance Thinking Strategically Copyright 2007 by AbdulJaami, PLLC. All Rights Reserved. This publication is intended as a general guide only. It does not contain a general legal analysis

Small Business Finance Thinking Strategically Copyright 2007 by AbdulJaami, PLLC. All Rights Reserved. This publication is intended as a general guide only. It does not contain a general legal analysis

Page 1 of 9 MICROLOAN RULES AND REGULATIONS

Page 1 of 9 MICROLOAN RULES AND REGULATIONS Micro Loans will be made available to small businesses located in or locating in, the City of Darlington. The Darlington Downtown Revitalization Association

Page 1 of 9 MICROLOAN RULES AND REGULATIONS Micro Loans will be made available to small businesses located in or locating in, the City of Darlington. The Darlington Downtown Revitalization Association

Commercial Loan Pricing Variables for Consideration

Commercial Loan Pricing Variables for Consideration OFN Small Business Finance Forum June 18, 2012 HOPE Colorado Enterprise Fund Commercial Loan Pricing Variables for Consideration HOPE The Primary Driver

Commercial Loan Pricing Variables for Consideration OFN Small Business Finance Forum June 18, 2012 HOPE Colorado Enterprise Fund Commercial Loan Pricing Variables for Consideration HOPE The Primary Driver

ECONOMIC DEVELOPMENT EQUIPMENT REVOLVING LOAN FUND

ECONOMIC DEVELOPMENT EQUIPMENT REVOLVING LOAN FUND APPLICATION Return Application To: Hutchinson Economic Development Authority 111 Hassan Street SE Hutchinson MN 55350 Email: edadirector@ci.hutchinson.mn.us

ECONOMIC DEVELOPMENT EQUIPMENT REVOLVING LOAN FUND APPLICATION Return Application To: Hutchinson Economic Development Authority 111 Hassan Street SE Hutchinson MN 55350 Email: edadirector@ci.hutchinson.mn.us

Non-traded financial contracts

11-1 Introduction Financial contracts are made between lenders and borrowers Non-traded financial contracts are tailor-made to fit the characteristics of the borrower In business financing, the differences

11-1 Introduction Financial contracts are made between lenders and borrowers Non-traded financial contracts are tailor-made to fit the characteristics of the borrower In business financing, the differences

www.development.ohio.gov

Minority Business Development Division Joseph Brooks (614) 466-5065 joseph.brooks@development.ohio.gov www.development.ohio.gov The State of Ohio is an Equal Opportunity Employer and Provider of ADA Services

Minority Business Development Division Joseph Brooks (614) 466-5065 joseph.brooks@development.ohio.gov www.development.ohio.gov The State of Ohio is an Equal Opportunity Employer and Provider of ADA Services

Contract Financing for the Contractor

a Contract Financing for the Contractor SBA s Contract CAPLines Program A Presentation For The Contractor SBA has a Loan Guaranty Program To help Contractors Obtain Financing for Contract Work Its Called

a Contract Financing for the Contractor SBA s Contract CAPLines Program A Presentation For The Contractor SBA has a Loan Guaranty Program To help Contractors Obtain Financing for Contract Work Its Called

747 Market Street, Room 900 * Tacoma, WA. 98402-3793 * (253) 591-5221 * Fax (253) 591-5180 * www.cityoftacoma.org

591-5221 * Fax (253) 591-5180 * www.cityoftacoma.org") 747 Market Street, Room 900 * Tacoma, WA. 98402-3793 * (253) 591-5221 * Fax (253) 591-5180 * www.cityoftacoma.org February 13, 2015 RESPONSES DUE BY 5:00 PM FRIDAY, MARCH 13, 2015 REQUEST FOR PROPOSALS

747 Market Street, Room 900 * Tacoma, WA. 98402-3793 * (253) 591-5221 * Fax (253) 591-5180 * www.cityoftacoma.org February 13, 2015 RESPONSES DUE BY 5:00 PM FRIDAY, MARCH 13, 2015 REQUEST FOR PROPOSALS

USDA Business & Industry (B&I) Guaranteed Loan Program

Guaranteed Loan Program") USDA Business & Industry (B&I) Guaranteed Loan Program B&I Program To Create And Maintain Employment And Improve Economic And Environmental Climate In Rural Communities Administered By The Rural Business

USDA Business & Industry (B&I) Guaranteed Loan Program B&I Program To Create And Maintain Employment And Improve Economic And Environmental Climate In Rural Communities Administered By The Rural Business

Multi-family Affordable. Becky Christoffersen, Midwest Housing Development Fund, Inc.

Multi-family Affordable Housing Capital Solutions Becky Christoffersen, Midwest Housing Development Fund, Inc. Midwest Housing Development Fund, Inc. CDFI since 2000 Revolving loan fund Affordable Housing

Multi-family Affordable Housing Capital Solutions Becky Christoffersen, Midwest Housing Development Fund, Inc. Midwest Housing Development Fund, Inc. CDFI since 2000 Revolving loan fund Affordable Housing

Federal Reserve Bank of Atlanta. A Guide for Specialized Credit Activities

Federal Reserve Bank of Atlanta A Guide for Specialized Credit Activities CONSUMER LENDING According to the Federal Reserve Board of Governors, seasonally adjusted consumer credit outstanding including

Federal Reserve Bank of Atlanta A Guide for Specialized Credit Activities CONSUMER LENDING According to the Federal Reserve Board of Governors, seasonally adjusted consumer credit outstanding including

Financing for the Car Wash Industry. WHITE PAPER: An Overview of SBA 7(a) Financing

Financing") Financing for the Car Wash Industry WHITE PAPER: An Overview of SBA 7(a) Financing INTRODUCTION If you are looking to purchase, build, upgrade, or refinance a car wash you already own, you may be surprised

Financing for the Car Wash Industry WHITE PAPER: An Overview of SBA 7(a) Financing INTRODUCTION If you are looking to purchase, build, upgrade, or refinance a car wash you already own, you may be surprised

Q4. How should institutions determine if they may exclude asset-based loans (ABL) from their definition of leveraged loans?

from their definition of leveraged loans?") Board of Governors of the Federal Reserve System Federal Deposit Insurance Corporation Office of the Comptroller of the Currency Frequently Asked Questions (FAQ) for Implementing March 2013 Interagency

Board of Governors of the Federal Reserve System Federal Deposit Insurance Corporation Office of the Comptroller of the Currency Frequently Asked Questions (FAQ) for Implementing March 2013 Interagency

11.437 Financing Community Economic Development Class 6: Fixed Asset Financing

11.437 Financing Community Economic Development Class 6: Fixed Asset Financing I. Purpose of asset financing Fixed asset financing refers to the financing for real estate and equipment needs of a business.

11.437 Financing Community Economic Development Class 6: Fixed Asset Financing I. Purpose of asset financing Fixed asset financing refers to the financing for real estate and equipment needs of a business.

MICROCREDIT ENTERPRISES. Financial Statements For the Year Ended December 31, 2013

Financial Statements Table of Contents Independent Auditor s Report 1-2 Financial Statements: Statement of Financial Position 3 Statement of Activities 4 Statement of Cash Flows 5 6-18 Page 10900 NE 4th

Financial Statements Table of Contents Independent Auditor s Report 1-2 Financial Statements: Statement of Financial Position 3 Statement of Activities 4 Statement of Cash Flows 5 6-18 Page 10900 NE 4th

NAVIGATING TODAY S CREDIT JUNGLE ALTERNATIVES

NAVIGATING TODAY S CREDIT JUNGLE AN OVERVIEW OF SBA FINANCING ALTERNATIVES November, 2011 Timothy D. Dixon Head of Small Business Administration (W) 216-514-5431 timothy.dixon@citizensbanking.com 1 Discussion

NAVIGATING TODAY S CREDIT JUNGLE AN OVERVIEW OF SBA FINANCING ALTERNATIVES November, 2011 Timothy D. Dixon Head of Small Business Administration (W) 216-514-5431 timothy.dixon@citizensbanking.com 1 Discussion

Working Capital and Contract Caplines Program. Caplines 2.0: New and Improved

Working Capital and Contract Caplines Program Caplines 2.0: New and Improved Topics for Today s Discussion Structural Changes Key Features for Working Capital Caplines Key Features for Contract Caplines

Working Capital and Contract Caplines Program Caplines 2.0: New and Improved Topics for Today s Discussion Structural Changes Key Features for Working Capital Caplines Key Features for Contract Caplines

Understanding Loans and Other Programs Available for Certified Minority Business Enterprises

Understanding Loans and Other Programs Available for Certified Minority Business Enterprises Presented by Allen McConnell, Manager Minority Business Development Division Slide 1 Access to Financial Assistance

Understanding Loans and Other Programs Available for Certified Minority Business Enterprises Presented by Allen McConnell, Manager Minority Business Development Division Slide 1 Access to Financial Assistance

Handout for Rule-making meeting on May 20, 2016

Compare sections of Chapter 208-460 to 12 CFR 723 (2016). Handout for Rule-making meeting on May 20, 2016 Section of Existing State Rule WAC 208-460-040 WAC 208-460-040 How do you implement a member business

Compare sections of Chapter 208-460 to 12 CFR 723 (2016). Handout for Rule-making meeting on May 20, 2016 Section of Existing State Rule WAC 208-460-040 WAC 208-460-040 How do you implement a member business

Borrowing 101. Resources. Are you ready to Borrow?

Borrowing 101 The BDC wants your business to succeed and in turn pay the BDC back. Our programs are revolving loan funds that require loans to be repaid so that we can lend our dollars to other businesses

Borrowing 101 The BDC wants your business to succeed and in turn pay the BDC back. Our programs are revolving loan funds that require loans to be repaid so that we can lend our dollars to other businesses

Business Financing. An Article by Michael L. Messer and Thomas L. Hofstetter SCHENCK, PRICE, SMITH & KING, LLP

Business Financing An Article by Michael L. Messer and Thomas L. Hofstetter SCHENCK, PRICE, SMITH & KING, LLP Even in these challenging economic times, businesses still have a need to grow and to obtain

Business Financing An Article by Michael L. Messer and Thomas L. Hofstetter SCHENCK, PRICE, SMITH & KING, LLP Even in these challenging economic times, businesses still have a need to grow and to obtain

Growing Your Loan Portfolio Through SBA Lending

Growing Your Loan Portfolio Through SBA Lending Presented By: U.S. Small Business Administration Tennessee District Office 2 International Plaza, Suite 500 Nashville, TN 37217 Today s SBA: Smart, Bold,

Growing Your Loan Portfolio Through SBA Lending Presented By: U.S. Small Business Administration Tennessee District Office 2 International Plaza, Suite 500 Nashville, TN 37217 Today s SBA: Smart, Bold,

Form. Account Disclosure Document for Licensed Corporation

Form (Made for the purposes of compliance with the requirements of section 156(1) of the Securities and Futures Ordinance (Cap.571) as amplified in section 3(1) of the Securities and Futures (Accounts

Form (Made for the purposes of compliance with the requirements of section 156(1) of the Securities and Futures Ordinance (Cap.571) as amplified in section 3(1) of the Securities and Futures (Accounts

HOUSING FINANCE AUTHORITY OF PINELLAS COUNTY AFFORDABLE MULTIFAMILY RENTAL DEVELOPMENT LOAN PROCEDURES

HOUSING FINANCE AUTHORITY OF PINELLAS COUNTY AFFORDABLE MULTIFAMILY RENTAL DEVELOPMENT LOAN PROCEDURES LENDING PHILOSOPHY The Housing Finance Authority of Pinellas County (HFA) follows Pinellas County

HOUSING FINANCE AUTHORITY OF PINELLAS COUNTY AFFORDABLE MULTIFAMILY RENTAL DEVELOPMENT LOAN PROCEDURES LENDING PHILOSOPHY The Housing Finance Authority of Pinellas County (HFA) follows Pinellas County

USDA Guarantee + NMTC Equity = Facility Financing for a Start Up Charter School

USDA Guarantee + NMTC Equity = Facility Financing for a Start Up Charter School Berkshire Arts & Technology Public Charter School Adams, MA The BArT Charter School opened its doors in the fall of 2004

USDA Guarantee + NMTC Equity = Facility Financing for a Start Up Charter School Berkshire Arts & Technology Public Charter School Adams, MA The BArT Charter School opened its doors in the fall of 2004

Non Profit Social Financing. What do you need to know?

Non Profit Social Financing What do you need to know? What is CAIC? A social finance fund providing mortgages, construction financing & loans to groups, organizations & cooperatives with a project of social

Non Profit Social Financing What do you need to know? What is CAIC? A social finance fund providing mortgages, construction financing & loans to groups, organizations & cooperatives with a project of social

WHAT IS BUSINESS CREDIT?

1 WHAT IS BUSINESS CREDIT? Why Do I Need Credit? Establishing a good credit rating is an important financial priority for every business. Having good business credit means that owners of businesses can

1 WHAT IS BUSINESS CREDIT? Why Do I Need Credit? Establishing a good credit rating is an important financial priority for every business. Having good business credit means that owners of businesses can

MICROCREDIT ENTERPRISES. (A California Not-For-Profit Organization) FINANCIAL STATEMENTS DECEMBER 31, 2007

FINANCIAL STATEMENTS DECEMBER 31, 2007") (A California Not-For-Profit Organization) FINANCIAL STATEMENTS DECEMBER 31, 2007 TABLE OF CONTENTS Independent auditors' report Page 2 Statement of financial position - December 31, 2007 Statement of

(A California Not-For-Profit Organization) FINANCIAL STATEMENTS DECEMBER 31, 2007 TABLE OF CONTENTS Independent auditors' report Page 2 Statement of financial position - December 31, 2007 Statement of

OPIC Finance Program FAQs

OPIC Finance Program FAQs Q: What products does OPIC s Finance Program offer? OPIC s Finance Program offers three basic products: 1) Direct Loans, 2) Investment Guaranties Funded by OPIC Certificates of

OPIC Finance Program FAQs Q: What products does OPIC s Finance Program offer? OPIC s Finance Program offers three basic products: 1) Direct Loans, 2) Investment Guaranties Funded by OPIC Certificates of

SMALL BUSINESS REVOLVING LOAN FUND GUIDELINES

SMALL BUSINESS REVOLVING LOAN FUND GUIDELINES 1.0 INTRODUCTION Fay-Penn Economic Development Council has established a Small Business Loan Fund. The Small Business Loan Fund Program is designed to stimulate

SMALL BUSINESS REVOLVING LOAN FUND GUIDELINES 1.0 INTRODUCTION Fay-Penn Economic Development Council has established a Small Business Loan Fund. The Small Business Loan Fund Program is designed to stimulate

BANKERS GUIDE TO SECURE LENDING

BANKERS GUIDE TO SECURE LENDING WAREHOUSE RECEIPTS, ORDER OR STRAIGHT BILLS OF LADING, OTHER NEGOTIABLE AND NON-NEGOTIABLE DOCUMENTS OF TITLE, INCLUDING WAREHOUSE AND BAILEE OR DOCK RECEIPTS Lending Rationale

BANKERS GUIDE TO SECURE LENDING WAREHOUSE RECEIPTS, ORDER OR STRAIGHT BILLS OF LADING, OTHER NEGOTIABLE AND NON-NEGOTIABLE DOCUMENTS OF TITLE, INCLUDING WAREHOUSE AND BAILEE OR DOCK RECEIPTS Lending Rationale

EMERGING BANKER PROGRAM

NATTYMAC EMERGING BANKER PROGRAM A WHOLLY-OWNED WAREHOUSE BANKING SUBSIDIARY OF STONEGATE MORTGAGE CORPORATION (NYSE: SGM) Effective 6.23.2015 NATTYMAC: FASTER, SMARTER, FRIENDLIER Mortgage banking firms,

NATTYMAC EMERGING BANKER PROGRAM A WHOLLY-OWNED WAREHOUSE BANKING SUBSIDIARY OF STONEGATE MORTGAGE CORPORATION (NYSE: SGM) Effective 6.23.2015 NATTYMAC: FASTER, SMARTER, FRIENDLIER Mortgage banking firms,

North Carolina Community Federal Credit Union Policy Number 1400 2401 East Ash Street Goldsboro, NC 27534 Revised and Approved 06/22/04 Page 1 of 12

Page 1 of 12 1400 BUSINESS LOAN POLICY I400.1 General. It is the policy of NORTH CAROLINA COMMUNITY FEDERAL CREDIT UNION (NCCFCU) to make loans that represent a desirable and profitable means of investing

Page 1 of 12 1400 BUSINESS LOAN POLICY I400.1 General. It is the policy of NORTH CAROLINA COMMUNITY FEDERAL CREDIT UNION (NCCFCU) to make loans that represent a desirable and profitable means of investing

New Project Finance Structures for Worldwide Renewable Energy Development. Cindy Thyfault, CEO & Founder Westar Trade Resources May 23, 2012

New Project Finance Structures for Worldwide Renewable Energy Development Cindy Thyfault, CEO & Founder Westar Trade Resources May 23, 2012 Presentation Outline Overview of Westar History & Services Challenges

New Project Finance Structures for Worldwide Renewable Energy Development Cindy Thyfault, CEO & Founder Westar Trade Resources May 23, 2012 Presentation Outline Overview of Westar History & Services Challenges

Ethiopian Institute of Financial Studies (EIFS) PROJECT FINANCE

PROJECT FINANCE") PROJECT FINANCE With the growth in the economy and the revival in the industrial sector coupled with the increasing role of private players in the field of infrastructure, more and more Ethiopian banks

PROJECT FINANCE With the growth in the economy and the revival in the industrial sector coupled with the increasing role of private players in the field of infrastructure, more and more Ethiopian banks

A fresh perspective on Asset Based Lending (ABL)

") A fresh perspective on Asset Based Lending (ABL) While asset-based lending may often be considered last-resort funding, commercial borrowers of all types and sizes are using this flexible, cost-effective

A fresh perspective on Asset Based Lending (ABL) While asset-based lending may often be considered last-resort funding, commercial borrowers of all types and sizes are using this flexible, cost-effective

Wright County Enterprise Loan Fund Policies and Procedures

Wright County Enterprise Loan Fund Policies and Procedures Established 1993 Revised December 1998 Revised December 2002 Revised in 2004 & approved by commissioners January 2005 1 I. OVERVIEW The purpose

Wright County Enterprise Loan Fund Policies and Procedures Established 1993 Revised December 1998 Revised December 2002 Revised in 2004 & approved by commissioners January 2005 1 I. OVERVIEW The purpose

SBA 7(a) Government. Guaranteed Loan Program

Government. Guaranteed Loan Program") SBA 7(a) Government Guaranteed Loan Program SBA Overview The U.S. Small Business Administration (SBA) Was Created By Congress In 1953 To Assist And Counsel Small Business Growth And Prosperity, Thereby

SBA 7(a) Government Guaranteed Loan Program SBA Overview The U.S. Small Business Administration (SBA) Was Created By Congress In 1953 To Assist And Counsel Small Business Growth And Prosperity, Thereby

How Do I Qualify for a loan?

How Do I Qualify for a loan? Borrowing money is one of the most common sources of funding for a small business, but obtaining a loan isn't always easy. Before you approach your banker for a loan, it is

How Do I Qualify for a loan? Borrowing money is one of the most common sources of funding for a small business, but obtaining a loan isn't always easy. Before you approach your banker for a loan, it is

Glossary of Lending Terms

Glossary of Lending Terms Adjustable Rate Loan or Adjustable Rate Mortgage (ARM) A loan with an interest rate that changes during the term of the loan. The payments generally increase or decrease with

Glossary of Lending Terms Adjustable Rate Loan or Adjustable Rate Mortgage (ARM) A loan with an interest rate that changes during the term of the loan. The payments generally increase or decrease with

Elements of a Successful MBL Program. Creating And Sustaining Your MBL Competitive Advantage

Creating And Sustaining Your MBL Competitive Advantage Jim Devine, CEO, Hipereon, Inc. Let s Define Some of The Strategic Concerns For Member Business Lending Where are we Now? There are 2,000+ Credit

Creating And Sustaining Your MBL Competitive Advantage Jim Devine, CEO, Hipereon, Inc. Let s Define Some of The Strategic Concerns For Member Business Lending Where are we Now? There are 2,000+ Credit

The Business Case For SBA 7a Lending For Community Banks

The Business Case For SBA 7a Lending For Community Banks How Community Banks Can Prudently Make Loans to Small Business By: Joanne Thompson SBA OneSource, LLC This paper examines the business reasons for

The Business Case For SBA 7a Lending For Community Banks How Community Banks Can Prudently Make Loans to Small Business By: Joanne Thompson SBA OneSource, LLC This paper examines the business reasons for

National Association of. Professionals Presents: The Power of Leverage

National Association of Accredited Advanced Insurance Markets Professionals Presents: The Power of Leverage David Gordon Vice President NAAIP Tel: (800)770-0492 Email: david (at) naaip.org I. Introduction

National Association of Accredited Advanced Insurance Markets Professionals Presents: The Power of Leverage David Gordon Vice President NAAIP Tel: (800)770-0492 Email: david (at) naaip.org I. Introduction

RMA Commercial & Business Banking

RMA Commercial & Business Banking The Commercial Real Estate Lending Decision Process The Commercial Real Estate Lending Decision Process, authored by The Risk Management Association and brought to you

RMA Commercial & Business Banking The Commercial Real Estate Lending Decision Process The Commercial Real Estate Lending Decision Process, authored by The Risk Management Association and brought to you

SCORE. Counselors to America s Small Business SMALL BUSINESS START-UP FINANCING OVERVIEW

SCORE Counselors to America s Small Business SMALL BUSINESS START-UP FINANCING OVERVIEW One key to a successful business start-up and expansion is your ability to obtain and secure appropriate financing.

SCORE Counselors to America s Small Business SMALL BUSINESS START-UP FINANCING OVERVIEW One key to a successful business start-up and expansion is your ability to obtain and secure appropriate financing.

Applying for a Business Loan A Cardinal Bank Lender s View. Components of an Application Package

Applying for a Business Loan A Cardinal Bank Lender s View By James N. Estep, AVP, Business Lending Contents Loan Interview Expectations Types of Business Loans Preferred Business Attributes Components

Applying for a Business Loan A Cardinal Bank Lender s View By James N. Estep, AVP, Business Lending Contents Loan Interview Expectations Types of Business Loans Preferred Business Attributes Components

4/20/2010. SBA Lending 2010. Jean M. Nelson. Bremer Bank, NA Regional SBA Manager Direct: 612-782-2821 jmnelson1@bremer.com

4/20/2010 SBA Lending 2010 Jean M. Nelson Bremer Bank, NA Regional SBA Manager Direct: 612-782-2821 jmnelson1@bremer.com Outline Background Role of the SBA What is a Small Business? Programs Available

4/20/2010 SBA Lending 2010 Jean M. Nelson Bremer Bank, NA Regional SBA Manager Direct: 612-782-2821 jmnelson1@bremer.com Outline Background Role of the SBA What is a Small Business? Programs Available

Doing Business. A Practical Guide. casselsbrock.com. Canada. Dispute Resolution. Foreign Investment. Aboriginal. Securities and Corporate Finance

About Canada Dispute Resolution Forms of Business Organization Aboriginal Law Competition Law Real Estate Securities and Corporate Finance Foreign Investment Public- Private Partnerships Restructuring

About Canada Dispute Resolution Forms of Business Organization Aboriginal Law Competition Law Real Estate Securities and Corporate Finance Foreign Investment Public- Private Partnerships Restructuring

Minority Business Development Division Allen McConnell, Manger (614) 752-4833 Allen.McConnell@development.ohio.gov www.development.ohio.

752-4833 Allen.McConnell@development.ohio.gov www.development.ohio.") Minority Business Development Division Allen McConnell, Manger (614) 752-4833 Allen.McConnell@development.ohio.gov www.development.ohio.gov The State of Ohio is an Equal Opportunity Employer and Provider

Minority Business Development Division Allen McConnell, Manger (614) 752-4833 Allen.McConnell@development.ohio.gov www.development.ohio.gov The State of Ohio is an Equal Opportunity Employer and Provider

5 Ways of Financing Your Growth

5 Ways of Financing Your Growth Kwesi Rogers President & CEO Federal National Commercial Credit In this whitepaper, you will learn five ways of financing your growth. It will show the opportunity and challenges

5 Ways of Financing Your Growth Kwesi Rogers President & CEO Federal National Commercial Credit In this whitepaper, you will learn five ways of financing your growth. It will show the opportunity and challenges

Underwriting Commercial Loans

Underwriting Commercial Loans T he objective of this study is to understand the basic principles of underwriting for multifamily housing and commercial real estate loans. As a mortgage broker, real estate

Underwriting Commercial Loans T he objective of this study is to understand the basic principles of underwriting for multifamily housing and commercial real estate loans. As a mortgage broker, real estate

MEDC Capital Services Team. Leveraging Private Capital to Increase Lending Activity in Michigan

MEDC Capital Services Team Leveraging Private Capital to Increase Lending Activity in Michigan MBGF Program Michigan Business Growth Fund Helping diversify and strengthen Michigan businesses Two programs,

MEDC Capital Services Team Leveraging Private Capital to Increase Lending Activity in Michigan MBGF Program Michigan Business Growth Fund Helping diversify and strengthen Michigan businesses Two programs,

Syndicated Revenue Loans. Secured Lines of Credit

Syndicated Revenue Loans. Syndicated Revenue Loans are Revenue loans grouped together through a syndicate. Typically these loans are given while a revenue loan is still outstanding, but the business owner

Syndicated Revenue Loans. Syndicated Revenue Loans are Revenue loans grouped together through a syndicate. Typically these loans are given while a revenue loan is still outstanding, but the business owner

Financing Technology: Trends in debt & equity termsheets

Financing Technology: Trends in debt & equity termsheets Dan Allred Silicon Valley Bank dallred@svb.com Twitter: @dgallred http://danallred.tumblr.com Technology Risk vs. Market Risk Funding sources: the

Financing Technology: Trends in debt & equity termsheets Dan Allred Silicon Valley Bank dallred@svb.com Twitter: @dgallred http://danallred.tumblr.com Technology Risk vs. Market Risk Funding sources: the

Real Estate & Mortgage Investment Specialists

Your Real Estate & Mortgage Investment Specialists Private Lending FAQ s 1. Why Should I Invest In A Mortgage? A mortgage is a loan in which real estate or property is used as collateral. When an individual

Your Real Estate & Mortgage Investment Specialists Private Lending FAQ s 1. Why Should I Invest In A Mortgage? A mortgage is a loan in which real estate or property is used as collateral. When an individual

CDA BLF LOAN APPLICATION

CDA BLF LOAN APPLICATION Name of of Business (Legal Name): Address: City, State, Zip: Business Phone // Fax: Federal Tax ID#: Principals Principal 1 Principal 2 Name: Address: City, State, Zip: Phone:

CDA BLF LOAN APPLICATION Name of of Business (Legal Name): Address: City, State, Zip: Business Phone // Fax: Federal Tax ID#: Principals Principal 1 Principal 2 Name: Address: City, State, Zip: Phone:

Asset Creation Planning

Asset Creation Planning Innovative Solutions For Seniors Now Seniors have the opportunity to improve their financial situation through the creation of a Life Insurance Asset, often without any out of pocket

Asset Creation Planning Innovative Solutions For Seniors Now Seniors have the opportunity to improve their financial situation through the creation of a Life Insurance Asset, often without any out of pocket

Financing and Liquidity Strategies

Financing and Liquidity Strategies A Morgan Stanley offers you a comprehensive approach to financing and liquidity delivering customized solutions for you that complement your overall investment strategy

Financing and Liquidity Strategies A Morgan Stanley offers you a comprehensive approach to financing and liquidity delivering customized solutions for you that complement your overall investment strategy

CHAPTER 9: BANKING DOING BUSINESS IN GREATER PHOENIX, U.S.A. 9.1: THE U.S. BANKING SYSTEM 9.2: ESTABLISHING A U.S. BANK ACCOUNT

CHAPTER 9: BANKING 9.1: THE U.S. BANKING SYSTEM Unlike banks in many countries, U.S. banks are not government-owned and managed. They provide deposit facilities for the general public, provide loans for

CHAPTER 9: BANKING 9.1: THE U.S. BANKING SYSTEM Unlike banks in many countries, U.S. banks are not government-owned and managed. They provide deposit facilities for the general public, provide loans for

Vermont Employee Ownership Center. Sixth Annual Employee Ownership Conference. Financing an ESOP. Burlington, VT June 6, 2008

Vermont Employee Ownership Center Sixth Annual Employee Ownership Conference Financing an ESOP Burlington, VT June 6, 2008 Copyright 2008 by SES Advisors, Inc. All rights reserved. Program Agenda Basic

Vermont Employee Ownership Center Sixth Annual Employee Ownership Conference Financing an ESOP Burlington, VT June 6, 2008 Copyright 2008 by SES Advisors, Inc. All rights reserved. Program Agenda Basic

Borrowing Money for Your Business

Borrowing Money for Your Business After you have developed a cash flow analysis and determined when your business will make profit, you may decide you need additional funding. Borrowing money is one of

Borrowing Money for Your Business After you have developed a cash flow analysis and determined when your business will make profit, you may decide you need additional funding. Borrowing money is one of

Building Your Pipeline. July 1, 2015. Pathway Lending

Building Your Pipeline July 1, 2015 1 Pathway Lending Mission: Providing underserved small businesses with lending solutions and educational services that result in job creation and economic development.

Building Your Pipeline July 1, 2015 1 Pathway Lending Mission: Providing underserved small businesses with lending solutions and educational services that result in job creation and economic development.

FDIC Liquidity Management. Tony Olbrich Regional President U.S. Bank

FDIC Liquidity Management Tony Olbrich Regional President U.S. Bank 0 Commercial Banks Checking and savings deposit accounts Consumer loans Business & Commercial Loans Payment Services Trust or fiduciary

FDIC Liquidity Management Tony Olbrich Regional President U.S. Bank 0 Commercial Banks Checking and savings deposit accounts Consumer loans Business & Commercial Loans Payment Services Trust or fiduciary

Key Points to Borrowing Money

Key Points to Borrowing Money Borrowing money is one of the most common sources of funding for a small business, but obtaining a loan isn't always easy. Before you approach your banker for a loan, it is

Key Points to Borrowing Money Borrowing money is one of the most common sources of funding for a small business, but obtaining a loan isn't always easy. Before you approach your banker for a loan, it is

Sources of Finance. Andy South Business Partner Clydesdale Bank. Steve Merchant Head of Asset Based Lending Services Baker Tilly

Sources of Finance Andy South Business Partner Clydesdale Bank Steve Merchant Head of Asset Based Lending Services Baker Tilly Angus Rooms Invoice Finance Partner Clydesdale Bank What we will be covering?

Sources of Finance Andy South Business Partner Clydesdale Bank Steve Merchant Head of Asset Based Lending Services Baker Tilly Angus Rooms Invoice Finance Partner Clydesdale Bank What we will be covering?

How to Assess Your Financial Planning and Loan Proposals By BizMove Management Training Institute

How to Assess Your Financial Planning and Loan Proposals By BizMove Management Training Institute Other free books by BizMove that may interest you: Free starting a business books Free management skills

How to Assess Your Financial Planning and Loan Proposals By BizMove Management Training Institute Other free books by BizMove that may interest you: Free starting a business books Free management skills

GrowFL and SunTrust Bank Present: Business Acquisitions and Partner Buyouts How SBA Loans can be leveraged to help

GrowFL and SunTrust Bank Present: Business Acquisitions and Partner Buyouts How SBA Loans can be leveraged to help GrowFL Webinar Series Date: September 4, 2012 Presented by: Hetal Engineer, SunTrust VP

GrowFL and SunTrust Bank Present: Business Acquisitions and Partner Buyouts How SBA Loans can be leveraged to help GrowFL Webinar Series Date: September 4, 2012 Presented by: Hetal Engineer, SunTrust VP

TAKING THE MYSTERY OUT OF FINANCE

TAKING THE MYSTERY OUT OF FINANCE Presented By: Eva Brown, Director of Access to Capital 312 853 3477 x 560 OBJECTIVES Determine how much money you need to start/expand your business. Determine your ability

TAKING THE MYSTERY OUT OF FINANCE Presented By: Eva Brown, Director of Access to Capital 312 853 3477 x 560 OBJECTIVES Determine how much money you need to start/expand your business. Determine your ability

AUSTIN STONE COMMUNITY CHURCH FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS' REPORT JULY 31, 2014 AND 2013

FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS' REPORT C O N T E N T S Page Independent Auditors' Report 1 Financial Statements Statements of Financial Position 3 Statements of Activities 4 Statements of

FINANCIAL STATEMENTS AND INDEPENDENT AUDITORS' REPORT C O N T E N T S Page Independent Auditors' Report 1 Financial Statements Statements of Financial Position 3 Statements of Activities 4 Statements of

Nonprofit Finance Fund. Preparing Your Organization to Apply for a Loan. Anne Dyjak Chief Credit Officer & Vice President Nonprofit Finance Fund

Nonprofit Finance Fund Preparing Your Organization to Apply for a Loan Anne Dyjak Chief Credit Officer & Vice President Nonprofit Finance Fund June 2010 Agenda Introductions Considering a Loan? What types

Nonprofit Finance Fund Preparing Your Organization to Apply for a Loan Anne Dyjak Chief Credit Officer & Vice President Nonprofit Finance Fund June 2010 Agenda Introductions Considering a Loan? What types

Wealth Creation Planning

Wealth Creation Planning A better way to own Life Insurance! Life insurance is the most effective way to protect against the financial risk and strain of a premature death. However, large or long term

Wealth Creation Planning A better way to own Life Insurance! Life insurance is the most effective way to protect against the financial risk and strain of a premature death. However, large or long term

4/20/2015. Dodd Frank Sections 1411 and 1412. Defines pretty specifically the terms and dimensions of each. On this one, you can't blame the CFPB

Ability To Repay and Qualified Mortgages Presented by: TriComply, a Temenos Product Presenter: Blair Rugh, Compliance Director Florida Banker's Association, Annual Consumer Compliance Seminar April 29

Ability To Repay and Qualified Mortgages Presented by: TriComply, a Temenos Product Presenter: Blair Rugh, Compliance Director Florida Banker's Association, Annual Consumer Compliance Seminar April 29

Small Business Administration

Financing the SBA Way Wayne Bell District Director Wichita District Office June 6, 2012 1 Agency History SBA What it is Federal Agency Created in 1953 Purpose To help potential and current small business

Financing the SBA Way Wayne Bell District Director Wichita District Office June 6, 2012 1 Agency History SBA What it is Federal Agency Created in 1953 Purpose To help potential and current small business

HEALTHCARE EXPANSION LOAN PROGRAM II (HELP II)

") CALIFORNIA HEALTH FACILITIES FINANCING AUTHORITY HEALTHCARE EXPANSION LOAN PROGRAM II (HELP II) OVERVIEW LOW FIXED INTEREST RATE LOANS FOR CALIFORNIA S NON-PROFIT SMALL AND RURAL HEALTH FACILITIES 915

CALIFORNIA HEALTH FACILITIES FINANCING AUTHORITY HEALTHCARE EXPANSION LOAN PROGRAM II (HELP II) OVERVIEW LOW FIXED INTEREST RATE LOANS FOR CALIFORNIA S NON-PROFIT SMALL AND RURAL HEALTH FACILITIES 915

ARC LOAN PROGRAM. Office of Small Business & Entrepreneurship and SBA

ARC LOAN PROGRAM Office of Small Business & Entrepreneurship and SBA 1 Timeline June 8 th : Regulation, Procedural Guidance and Forms Released Week of June 8 th : Lender Training June 15 th : SBA Begins

ARC LOAN PROGRAM Office of Small Business & Entrepreneurship and SBA 1 Timeline June 8 th : Regulation, Procedural Guidance and Forms Released Week of June 8 th : Lender Training June 15 th : SBA Begins

Chapter 13: Residential and Commercial Property Financing

Chapter 13 Outline / Page 1 Chapter 13: Residential and Commercial Property Financing Understanding the Mortgage Concept - secured vs. unsecured debt - mortgage pledge of property to secure a debt (See

Chapter 13 Outline / Page 1 Chapter 13: Residential and Commercial Property Financing Understanding the Mortgage Concept - secured vs. unsecured debt - mortgage pledge of property to secure a debt (See

Entrepreneur Academy: SBA 504 & 7(a) Loan Programs & Updates

Loan Programs & Updates") Entrepreneur Academy: SBA 504 & 7(a) Loan Programs & Updates Wendy J. Jeffers Sr. Lending Officer: SBA Programs wjeffers@sbacsav.com Mobile: 912.398.3090 or 888.287.2137 In full operation since September

Entrepreneur Academy: SBA 504 & 7(a) Loan Programs & Updates Wendy J. Jeffers Sr. Lending Officer: SBA Programs wjeffers@sbacsav.com Mobile: 912.398.3090 or 888.287.2137 In full operation since September

MONTGOMERY COUNTY LOAN PROGRAM. Serviced by the Montgomery County Development Corporation

MONTGOMERY COUNTY LOAN PROGRAM Serviced by the Montgomery County Development Corporation Thank you for your interest in the Montgomery County Loan Program. We are excited to be able to offer opportunities

MONTGOMERY COUNTY LOAN PROGRAM Serviced by the Montgomery County Development Corporation Thank you for your interest in the Montgomery County Loan Program. We are excited to be able to offer opportunities

Understanding the (GFE) Good Faith Estimate

Good Faith Estimate") A good faith estimate is a document that estimates the total costs to get a loan when you are buying or refinancing a home. The good faith estimate details costs you will incur on all loan related fees

A good faith estimate is a document that estimates the total costs to get a loan when you are buying or refinancing a home. The good faith estimate details costs you will incur on all loan related fees