TORCH Annual Conference and Trade Show

|

|

|

- Kristin Chambers

- 10 years ago

- Views:

Transcription

1 Photo: Rainbow Bridge by Blakemul via Wikimedia Creative Commons license Healthcare Environment in Transition: Opportunities for Rural Hospitals TORCH Annual Conference and Trade Show April 7-9, 2015 Hyatt Regency Dallas Eric K. Shell, CPA, MBA

2 The Healthcare Environment Has Changed! In the past 36 months, the healthcare field has experienced considerable changes with an increased number of rural-urban affiliations, physicians transitioning to hospital employment models, flattening volumes, CEO turnover, etc. Federal healthcare reform passed in March 2010 with sweeping changes to healthcare systems, payment models, and insurance benefits/programs Many of the more substantive changes will be implemented over the next two years State Medicaid programs are moving toward managed care models or reduced fee for service payments to balance State budgets Commercial insurers are steering patients to lower cost options Thus, providers face new financial uncertainty and challenges and will be required to adapt to the changing market INTRODUCTION 2

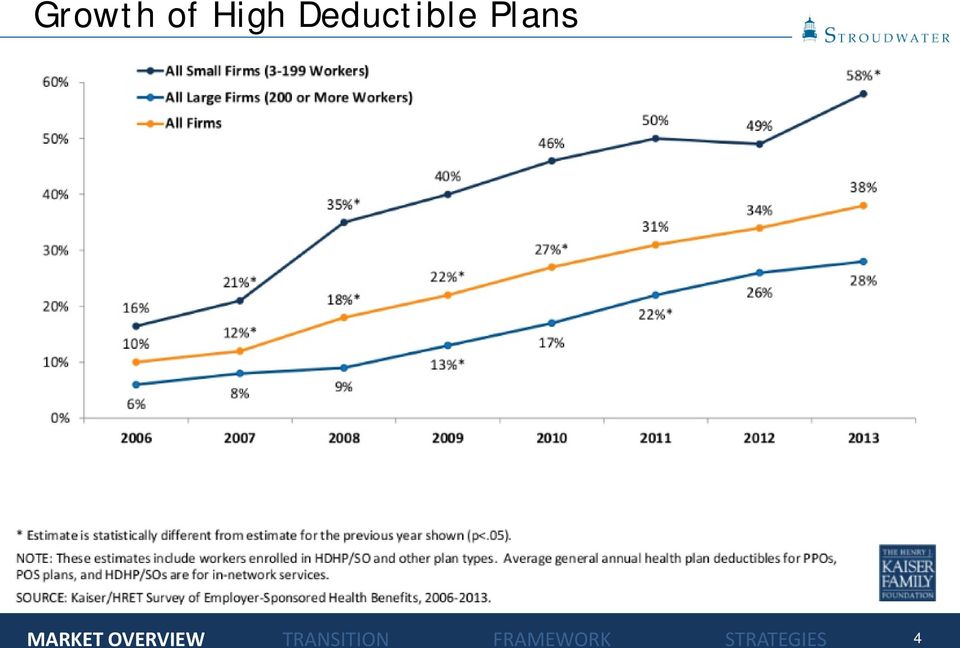

3 Market Overview State Budget Deficits Recovery Audit Contractors (RAC) Reduced Re-admissions 2-Midnight Rule Accelerating shift to outpatient care High Deductible Health Plans Non Healthcare CEO quote: We just renewed our High Deductible Plan going into our third year, and guess what...5% reduction in premium!!! Needless to say everyone is thrilled. Not sure what the average HSA balance is, but I think it is high. Doing what it is supposed to do, turning health care patients into consumers. 3/18/2013 WSJ Article 3

4 Growth of High Deductible Plans 4

5 Reduced Readmission Rates CMS: 2,610 PPS hospitals to receive penalties in 2015 Source: Centers for Medicare and Medicaid Services, Offices of Enterprise Management 5

6 Service Area Market Overview Results Declining Patient Volumes 115 Texas Hospital Admissions per 1000 Population Source: Kaiser State Health Facts, kff.org 6

7 Service Area Market Overview Healthcare Reform Coverage Expansion By 1/1/14, expand Medicaid to all non-medicare eligible individuals under age 65 with incomes up to 133% FPL based on modified AGI Currently, Medicaid covers only 45% of poor ( 100% FPL) 16 million new Medicaid beneficiaries; mostly traditional patients FMAP for newly eligible: 100% in ; 95% in 2017; 94% in 2018; 93% in 2019; 90% in Establishment of State-based Health Insurance Exchanges Subsidies for Health Insurance Coverage Individual and Employer Mandate Provider Implications Insurance coverage will be extended to 32 million additional Americans by 2019 Expansion of Medicaid is major vehicle for extending coverage May release pent-up demand and strain system capacity Traditionally underserved areas and populations will have increased provider competition Have insurance, will travel! 7

8 Service Area Market Overview Healthcare Reform Medicare and Medicaid Payment Policies Medicare Update Factor Reductions Annual updates will be reduced to reflect projected gains in productivity Medicare and Medicaid Disproportionate Share Hospital (DSH) Payment Reductions Medicare Hospital Wage Index Independent Payment Advisory Board (IPAB) Charged with figuring out how to reduce Medicare spending to targets with goal of $13B savings between 2014 and 2020 Summary Impact 8

9 Service Area Market Overview Healthcare Reform Medicare and Medicaid Payment Policies (continued) Provider Implications Payment changes will increase pressure on hospital margins and increase competition for patient volume Do more with less and then less with less Medicaid pays less than other insurers and will be forced to cut payments further 9

10 Service Area Market Overview Healthcare Reform Medicare and Medicaid Delivery System Reforms Expansion of Medicare and Medicaid Quality Reporting Programs Medicare and Medicaid Healthcare-Acquired Conditions (HAC) Payment Policy By Oct. 2014, the 25% of hospitals with the highest HAC rates will get a 1% overall payment penalty Medicare Readmission Payment Policy Hospitals with above expected risk-adjusted readmission rates will get reduced Medicare payments Value based purchasing Medicare will reduce DRG payments to create a pool of funds to pay for the VBPP 1% reduction in FFY 2013, Grows to 2% by FFY 2017 Bundled Payment Initiative Accountable Care Organizations Each ACO assigned at least 5,000 Medicare beneficiaries Providers continue to receive usual fee-for-service payments Compare expected and actual spend for specified time period If meet specified quality performance standards AND reduce costs, ACO receives portion of savings 10

11 Service Area Market Overview Healthcare Reform Medicare and Medicaid Delivery System Reforms (continued) Medicare Accountable Care Organizations (continued) 154 ACOs effective August, ACOs effective January, ACOs effective January, ACOs effective January 2015 More than half of the U.S. population now live in localities served by ACOs and almost 30 percent live in areas served by two or more 8 million Medicare beneficiaries, or about 21% of total Medicare feefor-service beneficiaries, now in Medicare ACOs

12 ACO Growth

13 ACO Growth

14 Where Are Medicare ACOs Forming? Source: CMS 1/20/15- Mapped from address of parent ACO 14

15 ACOs in Texas In 2014, a Leavitt Partners survey for ModernHealthcare listed 43 ACOs in Texas covering more than a million lives. In this survey, TX ranked third in the nation for number of ACOs. As of November 2014, 17 Texas ACOs were participating in the Medicare Shared Savings Program. Example: Accountable Care Coalition of Texas., a MSSP ACO. Numerous participants include Northwest Diagnostic Clinic, Golden Triangle Physician Alliance, Memorial Clinical Associates, Village Family Practice, Heritage Physician Networks Sources: ModernHealthcare, Harris County Medical Society, Beckers Hospital Review, 15

16 ACOs Results and Projections 2014 Results from Pioneer ACOs (Source: Brookings.edu blog post, 10/13/14) In September 2014, CMS announced that the Pioneer Program was able to yield total program savings of $96 million in its second year and resulted in ACOs sharing in savings of $68 million CMS also reported that the Pioneers were able to improve mean quality scores by 19 percent and increased performance on 28 of 33 measures between performance year one and performance year two 16

17 Fee-For-Service Financial Model Assumptions Utilization Inpatient and Outpatient Impact of ACA Impact of Blue Cross steerage initiatives Revenue Third party price increases Cost based Medicare revenue DSH payments (Zeroed out in 2014) Bad debt % of patient service revenue (75% reduction in 2014) Impact of ACA Meaningful use incentive payments Other operating revenue Non-operating gains and Expenses Salaries, wages and benefits Productivity Supplies and other 17

18 18

19 Fee-For-Service Financial Model Results When operating income becomes negative in 2016, cash reserves start to decline Millions $4 $2 $- $(2) $(4) $(6) $(8) $(10) $(12) $(14) $(16) $(18) Operating income (Consolidated) Operational improvement and shared service economies of scale are insufficient to combat declining utilization Can t cut your way to sustainability 19

20 Service Area Market Overview Healthcare Reform Medicare and Medicaid Delivery System Reforms (continued) Provider Implications Hospitals are taking the lead in forming Accountable Care Organizations with physician groups that will share in Medicare savings Value based purchasing program will shift payments from low performing hospitals to high performing hospitals Acute care hospitals with higher than expected risk-adjusted readmission rates and HAC will receive reduced Medicare payments for every discharge Physician payments will be modified based on performance against quality and cost indicators There are significant opportunities for demonstration project funding 20

21 Market Overview Results Service Area Stability and US Healthcare Spending Source: The Wall Street Journal, January 6,

22 Closed Hospitals Since the Beginning of 2013 Source: Reuters Graphics 22

23 2013 Health Spending 23

24 How Do Real and Projected Spending Compare? Chart source: The New York Times Data source: CBO 24

25 Challenges Affecting Rural Hospitals Factors that will have a significant impact on rural hospitals over the next 5-10 years Difficulty with recruitment of providers and aging of current medical staff Struggle to pay market rates Increasing competition from other hospitals and physician providers for limited revenue opportunities Small hospital governance members without sophisticated understanding of small hospital strategies, finances, and operations Consumer perception that bigger is better Severe limitations on access to capital for necessary investments in infrastructure and provider recruitment Facilities historically built around IP model of care Increased burden of remaining current on onslaught of regulatory changes Regulatory Friction / Overload Payment systems transitioning from volume based to value based Increased emphasis of quality as payment and market differentiator Reduced payments that are Real this time 3rd party steerage (surgery, lab, and Imaging), RAC audits 25

26 We Have Moved into a New Environment! Subset of most recent challenges Payment systems transitioning from volume based to value based Increased emphasis as quality as payment and market differentiator Reduced payments that are Real this time New environmental challenges are the TRIPLE AIM!!! Market Competition on economic driver of healthcare: PATIENT VALUE 26

27 Future Hospital Financial Value Equation Definitions Patient Value Accountable Care: Patient Value Quality Cost A mechanism for providers to monetize the value derived from increasing quality and reducing costs Accountable care includes many models including bundled payments, value-based payment program, provider selfinsured health plans, Medicare defined ACO, capitated provider sponsored healthcare, etc. Different this time Providers monetize value New information systems to manage costs and quality Agreed upon evidence-based protocols Going back is not an option 27

28 Future Hospital Financial Value Equation ACO Relationship to Small and Rural Hospitals Revenue stream of future tied to Primary Care Physicians (PCP) and their patients Small and rural hospitals bring value / negotiating power to affiliation relationships as generally PCP based Smaller community hospitals and rural hospitals have value through alignment with revenue drivers (PCPs) rather than cost drivers but must position themselves for new market: Alignment with PCPs in local service area Develop a position of strength by becoming highly efficient Demonstrate high quality through monitoring and actively pursuing quality goals 28

29 Future Hospital Financial Value Equation Economics As payment systems transition away from volume based payment, the current economic model of increasing volume to reduce unit costs and generate profit is no longer relevant New economic models based on patient value must be developed by hospitals but not before the payment systems have converted Economic Model: FFS Rev and Exp VS. Budget Based Payment Rev and Exp Revenue Dollars Profit Zone Cost Loss Zone Service Volumes 29

30 Future Hospital Financial Value Equation Value in Rural Hospitals Lower Per Beneficiary Costs Revenue centers of the future PCP based delivery system CAH cost-based reimbursement Incremental volume drives down unit costs Once commitment to community Emergency Room, system incentives to drive low acuity volume to CAH MedPAC Confusion Limited Incentives to manage costs??? 30

31 The Challenge: Crossing the Shaky Bridge Fee for Service Payment System Population Based Payment System

32 The Challenge Shaky Bridge Concern of task force members is that transitioning of the delivery system functions must coincide with transitioning payment system of rural hospitals, without adequate reserves, will be a financial risk Stepping onto the shaky bridge analogy Necessary for hospitals to survive the gap between pay-for-volume and payfor-performance Delivery system has to remain aligned with current payment system while seeking to implement programs / processes that will allow flexibility to new payment system Delivery system must be ready to jump when new payment systems roll out 32

33 The Premise Finance Function Form Macro-economic Payment System Government Payers Changing from F-F-S to PBPS Private Payers Follow Government payers Steerage to lower cost providers Provider Imperatives F-F-S Management of price, utilization, and costs PBPS Management of care for defined population (under PBPS) Providers assume insurance risk Provider organization Evolution from Independent organizations competing with each other for market share based on volume to Aligned organizations competing with other aligned organizations for covered lives based on quality and value Network and care management organization New competencies required Network development Care management Risk contracting Risk management 33

34 Implementation Framework What Is It? A strategic framework for assisting organizations transition from a payment system dominated by the FFS payment model to one dominated by population based payment models Delivery system side addresses strategic imperatives for providers Provider side addresses strategies for providers to influence the evolution of the payment system in their market Requires creation of an integrating vehicle so that providers can contract for covered lives, create value through active care management and monetize the creation of that value Strategic imperatives drive the initiatives that must be designed and timely implemented to successfully make the transition Each initiative is developed in phases that correspond to the evolution of the payment models Work on each initiative needs to begin now so they will be ready to implement when required 34

35 Implementation Framework What Is It? 35

36 Initiative I Operating Efficiencies, Patient Safety and Quality Hospitals not operating at efficient levels are currently, or will be, struggling financially Efficient is defined as Appropriate patient volumes meeting needs of their service area Revenue cycle practices operating with best practice processes Expenses managed aggressively Physician practices managed effectively Effective organizational design Graphic: National Patient Safety Foundation 36

37 Initiative I Operating Efficiencies, Patient Safety and Quality Focus on Quality and Patient Safety As a strategic imperative As a competitive advantage U.S. HHS Hospital Compare Measures Hospital Acquired Conditions National Avg. New York Avg. Lewis County General Carthage Area Hospital Samaritan Medical Center Rome Memorial Hospital E.J. Noble Hospital Clifton- Fine Hospital Falls and Injuries 0.53 N/A N/A 5 N/A 5 Infection from a Urinary Catheter 0.36 N/A N/A 5 N/A 5 The River Hospital Patient Satisfaction (HCAHPS) 71% 66% 74% 69% 69% 66% 57% 84% 1,2 85% 6 Nurses "Always" communicated well 78% 73% 76% 72% 76% 76% 63% 96% 90% Doctors "Always" communicated well 81% 77% 87% 77% 80% 77% 76% 97% 91% "Always" received help when wanted 66% 59% 70% 61% 64% 62% 53% 93% 90% Pain "Always" well controlled 70% 66% 70% 66% 68% 68% 53% 87% 87% Staff "Always" explained med's before administering 63% 58% 67% 61% 61% 58% 49% 72% 78% Room and bathroom "Always" clean 73% 68% 76% 78% 82% 72% 66% 89% 86% Area around room "Always" quiet at night 60% 49% 60% 55% 54% 49% 42% 55% 78% YES, given at home recovery information 84% 81% 84% 87% 84% 84% 83% 81% 83% Gave hospital rating of 9 or 10 (0-10 scale) 69% 61% 72% 64% 62% 61% 47% 86% 78% YES, definitely recommend the hospital 70% 64% 75% 66% 61% 57% 41% 87% 88% Note: footnotes [detailed below ] may not apply to all data points w ithin the selected hospital compare measure (data source: w w w.hospitalcompare.hhs.gov) Hospital Acquired Condition rates are per 1,000 discharges 1 The number of cases is too small to reliably tell how w ell a hospital is performing. 2 The hospital indicated that the data submitted for this measure w ere based on a sample of cases. 5 No data are available from the hospital for this measure. 6 Few er than 100 patients completed the HCAHPS survey. Use these scores w ith caution, as the number of surveys may be too low to reliably assess hospital performance. 37

38 Initiative II Primary Care Alignment Understand that revenue streams of the future will be tied to primary care physicians, which often comprise a majority of the rural and small hospital healthcare delivery network Thus small and rural hospitals, through alignment with PCPs, will have extraordinary value relative to costs Physician Relationships Hospital align with employed and independent providers to enable interdependence with medical staff and support clinical integration efforts Contract (e.g., employ, management agreements) Functional (share medical records, joint development of evidence based protocols) Governance (Board, executive leadership, planning committees, etc.) 38

39 Initiative III Rationalize Service Network Develop system integration strategy Evaluate wide range of affiliation options ranging from network relationships, to interdependence models, to full asset ownership models Interdependence models through alignment on contractual, functional, and governance levels, may be option for rural hospitals that want to remain independent Explore / Seek to establish interdependent relationships among small and rural hospitals understanding their unique value relative to future revenue streams Identify the number of providers needed in the service area based on population and the impact of an integrated regional healthcare system Conduct focused analysis of procedures leaving the market Understand real value to hospitals Under F-F-S Under PBPS (Cost of out of network claims) 39

40 Payment System Initiatives Initiative I: Develop self-funded employer health plan Hospital is already 100% at risk for medical claims Change benefits to encourage greater consumerism Begin creation of care management infrastructure Begin to move up the learning curve Cost reduction opportunity for the delivery system Initiative II: Begin implementation planning for transitional payment models Transitional payment models include: FFS against capitation benchmark w/ shared savings Shared savings model Medicare ACOs Shared savings models with other governmental and commercial insurers Partial capitation and sub-capitation options with shared savings Prioritize insurance market opportunities Take the initiative with insurers to gauge interest and opportunities for collaborating on transitional payment models Explore direct contracting opportunities with self-funded employers Initiative III: Develop strategy for full risk capitated plans 40

41 Initiative IV Population Based Payment System A narrow rural/urban provider network focused on patient value Aggregates multiple rural/cah populations for critical mass Restricted to payers willing to commit to population health and payment On CCO s terms NOT for existing fee-for-service or cost contracts Legal entity with corporate powers Governance structure for setting strategy, policy, accountability Actively secures and manages risk/reward-based payer contracts Supports PCP-focused quality & care coordination across the network Retains local hospital independence, but with contractual accountability Houses care management infrastructure 41

42 Community Care Organizations (CCO) Initiatives Phase I: Develop care management building blocks Goal: Infrastructure to manage self insured lives Initiatives: PCMH Develop claims analysis capabilities/infrastructure Develop evidenced based protocols Phase II: Develop Strategy for full population health management Goal: Infrastructure to manage transitional payment models Initiatives: Develop capability to contract with third party payers including actuarial expertise Acquire and analyze third party payer claims targeting high cost users Develop payment/measurement system to attribute value and distribute shared savings PCMHs are provided tools to better manage patient care to improve outcomes and patient health 42

43 CCO Initiatives Phase III and IV Phase III: Implementation plan for full risk-based population contracts Goal: Infrastructure to manage care for a defined population within a budget Initiatives: Risk management capability (e.g., re-insurance) Enhanced third-party payer partnerships (e.g., plan design, joint marketing, etc.) Capability to support value-based credentialing Phase IV: Implementation of Integrated delivery and payment system Goal: Implement full provider-based health plan 43

44 Implementation Framework In review 44

45 Conclusions/Recommendations For decades, rural hospitals have dealt with many challenges including low volumes, declining populations, difficulties with provider recruitment, limited capital constraining necessary investments, etc. The current environment driven by healthcare reform and market realities now offers a new set of challenges. Many rural healthcare providers have not yet considered either the magnitude of the changes or the required strategies to appropriately address the changes Core set of new challenges represents the Triple Aim being played on in the market Locally delivered healthcare (including rural and small community hospitals) has high value in the emerging delivery system Shaky Bridge crossing will required planned, proactive approach Finance will lead function and form Maintain alignment between delivery system models and payment systems building flexibility into the delivery system model for the changing payment system CONCLUSIONS / RECOMMENDATIONS 45

46 Conclusions/Recommendations (continued) Important strategies for providers to consider include: Increase leadership awareness of new environment realities Improve operational efficiency of provider organizations Adapt effective quality measurement and improvement systems as a strategic priority Align/partner with medical staff members contractually, functionally, and through governance where appropriate Seek interdependent relationships with developing regional systems CONCLUSIONS / RECOMMENDATIONS 46

47 Eric K. Shell, CPA, MBA 50 Sewall Street, Suite 102 Portland, Maine (207)

The Affordable Care Act

The Affordable Care Act What does it mean for internists? Joshua Becker MD 10/14/2015 VII. 2015 Reforms and Beyond Payment Penalties under Medicare s Pay-for-Reporting Program Value-Based Payment Modifier

The Affordable Care Act What does it mean for internists? Joshua Becker MD 10/14/2015 VII. 2015 Reforms and Beyond Payment Penalties under Medicare s Pay-for-Reporting Program Value-Based Payment Modifier

Westchester Medical Center. 2012 Operating Budget

Westchester Medical Center 2012 Operating Budget December 7, 2011 WESTCHESTER COUNTY HEALTH CARE CORPORATION Overview Westchester Medical Center s (WMC) 2012 Operating Budget reflects significant reductions

Westchester Medical Center 2012 Operating Budget December 7, 2011 WESTCHESTER COUNTY HEALTH CARE CORPORATION Overview Westchester Medical Center s (WMC) 2012 Operating Budget reflects significant reductions

HCAHPS and Value-Based Purchasing Methods and Measurement. Deb Stargardt, Improvement Services Darrel Shanbour, Consulting Services

HCAHPS and Value-Based Purchasing Methods and Measurement Deb Stargardt, Improvement Services Darrel Shanbour, Consulting Services Today s Learning Objectives Acquire new knowledge pertaining to: A. Hospital

HCAHPS and Value-Based Purchasing Methods and Measurement Deb Stargardt, Improvement Services Darrel Shanbour, Consulting Services Today s Learning Objectives Acquire new knowledge pertaining to: A. Hospital

THE FUTURE OF QUALITY HEALTHCARE: ACO S?????

THE FUTURE OF QUALITY HEALTHCARE: ACO S????? ARKANSAS LEADERSHIP FORUM Lance W. Keilers, MBA, CAPPM September 15, 2015 Learning Objectives Recognize current changes in rural hospital delivery systems Identify

THE FUTURE OF QUALITY HEALTHCARE: ACO S????? ARKANSAS LEADERSHIP FORUM Lance W. Keilers, MBA, CAPPM September 15, 2015 Learning Objectives Recognize current changes in rural hospital delivery systems Identify

Federal Health Care Reform: Implications for Hospital and Physician partnerships. Walter Kopp Medical Management Services

Federal Health Care Reform: Implications for Hospital and Physician partnerships Walter Kopp Medical Management Services Outline Overview of federal health reform legislation Implications for Care delivery

Federal Health Care Reform: Implications for Hospital and Physician partnerships Walter Kopp Medical Management Services Outline Overview of federal health reform legislation Implications for Care delivery

Westchester Medical Center. 2014 Operating Budget

Westchester Medical Center 2014 Operating Budget December 4, 2013 WESTCHESTER COUNTY HEALTH CARE CORPORATION Operating Budget 2014 Table of Contents Page Executive Summary 1 Detailed Discussion of Revenue

Westchester Medical Center 2014 Operating Budget December 4, 2013 WESTCHESTER COUNTY HEALTH CARE CORPORATION Operating Budget 2014 Table of Contents Page Executive Summary 1 Detailed Discussion of Revenue

What is an Accountable Care Organization. Amit Rastogi, MD President/CEO PriMed

What is an Accountable Care Organization Amit Rastogi, MD President/CEO PriMed Goals Why is U.S. healthcare undergoing dramatic change How reimbursement structures are likely to change What is the timeline

What is an Accountable Care Organization Amit Rastogi, MD President/CEO PriMed Goals Why is U.S. healthcare undergoing dramatic change How reimbursement structures are likely to change What is the timeline

Enterprise Analytics Strategic Planning

Enterprise Analytics Strategic Planning June 5, 2013 1 "The first question a data driven organization needs to ask itself is not "what do we think?" but rather "what do we know? Big Data: The Management

Enterprise Analytics Strategic Planning June 5, 2013 1 "The first question a data driven organization needs to ask itself is not "what do we think?" but rather "what do we know? Big Data: The Management

Value-Based Purchasing Program Overview. Maida Soghikian, MD Grand Rounds Scripps Green Hospital November 28, 2012

Value-Based Purchasing Program Overview Maida Soghikian, MD Grand Rounds Scripps Green Hospital November 28, 2012 Presentation Overview Background and Introduction Inpatient Quality Reporting Program Value-Based

Value-Based Purchasing Program Overview Maida Soghikian, MD Grand Rounds Scripps Green Hospital November 28, 2012 Presentation Overview Background and Introduction Inpatient Quality Reporting Program Value-Based

Payor Perspectives on Provider Realignment and ACOs

Payor Perspectives on Provider Realignment and ACOs Joel L. Michaels March 15, 2011 Overview Issues to be addressed Medicare Shared Savings Program overview ACO organization options Health care reform

Payor Perspectives on Provider Realignment and ACOs Joel L. Michaels March 15, 2011 Overview Issues to be addressed Medicare Shared Savings Program overview ACO organization options Health care reform

Accountable Care Communities 101. Jennifer M. Flynn, Esq. Senior Director, State Affairs Premier healthcare alliance January 30, 2014

Accountable Care Communities 101 Jennifer M. Flynn, Esq. Senior Director, State Affairs Premier healthcare alliance January 30, 2014 Premier is the largest healthcare alliance in the U.S. Our Mission:

Accountable Care Communities 101 Jennifer M. Flynn, Esq. Senior Director, State Affairs Premier healthcare alliance January 30, 2014 Premier is the largest healthcare alliance in the U.S. Our Mission:

Westchester Medical Center. 2015 Operating Budget

Westchester Medical Center 2015 Operating Budget December 3, 2014 WESTCHESTER COUNTY HEALTH CARE CORPORATION Operating Budget 2015 Table of Contents Page Executive Summary 1 Detailed Discussion of Revenue

Westchester Medical Center 2015 Operating Budget December 3, 2014 WESTCHESTER COUNTY HEALTH CARE CORPORATION Operating Budget 2015 Table of Contents Page Executive Summary 1 Detailed Discussion of Revenue

The Impact of Healthcare Reform on Pharmacy Practice. Disclosure

The Impact of Healthcare Reform on Pharmacy Practice Thomas Buckley, MPH, RPh Assistant Clinical Professor University of Connecticut School of Pharmacy Disclosure Thomas Buckley has nothing to disclose

The Impact of Healthcare Reform on Pharmacy Practice Thomas Buckley, MPH, RPh Assistant Clinical Professor University of Connecticut School of Pharmacy Disclosure Thomas Buckley has nothing to disclose

6 Critical Impact Factors of Health Reform on Revenue Cycle Management Pyramid Healthcare Solutions Thought Leadership Series

6 Critical Impact Factors of Health Reform on Revenue Cycle Management Pyramid Healthcare Solutions Thought Leadership Series The healthcare industry is undergoing significant change in the face of the

6 Critical Impact Factors of Health Reform on Revenue Cycle Management Pyramid Healthcare Solutions Thought Leadership Series The healthcare industry is undergoing significant change in the face of the

Managing and Coordinating Non-Acute Care in an ACO Environment

Managing and Coordinating Non-Acute Care in an ACO Environment By Glen Roebuck, Vice President of Business Development, Health Dimensions Group Hospital and health care systems across the country are engaging

Managing and Coordinating Non-Acute Care in an ACO Environment By Glen Roebuck, Vice President of Business Development, Health Dimensions Group Hospital and health care systems across the country are engaging

33rd Annual J.P. Morgan Healthcare Conference

33rd Annual J.P. Morgan Healthcare Conference January 12, 2015 Disclosures / Forward-looking Statements This presentation includes forward-looking statements. Such forward-looking statements are based

33rd Annual J.P. Morgan Healthcare Conference January 12, 2015 Disclosures / Forward-looking Statements This presentation includes forward-looking statements. Such forward-looking statements are based

Accountable Care and Value Based Payments 101: Government Programs Update

1 Accountable Care and Value Based Payments 101: Government Programs Update June 24 th, 2014 Dave Neiman, FSA, MAAA Senior Consulting Actuary [email protected] (720) 226-9806 2 Caveats Opinions expressed

1 Accountable Care and Value Based Payments 101: Government Programs Update June 24 th, 2014 Dave Neiman, FSA, MAAA Senior Consulting Actuary [email protected] (720) 226-9806 2 Caveats Opinions expressed

ACO s as Private Label Insurance Products

ACO s as Private Label Insurance Products Creating Value for Plan Sponsors Continuing Education: November 19, 2013 Clarence Williams Vice President Client Strategy Accountable Care Solutions Today s discussion

ACO s as Private Label Insurance Products Creating Value for Plan Sponsors Continuing Education: November 19, 2013 Clarence Williams Vice President Client Strategy Accountable Care Solutions Today s discussion

EHR Incentive Payments For Rural Hospitals and Eligible Providers. April, 2011. Tommy Barnhart, Dixon Hughes Goodman LLP

EHR Incentive Payments For Rural Hospitals and Eligible Providers April, 2011 Tommy Barnhart, Dixon Hughes Goodman LLP Objectives Health Information Technology (HIT) and Electronic Health Record (EHR)

EHR Incentive Payments For Rural Hospitals and Eligible Providers April, 2011 Tommy Barnhart, Dixon Hughes Goodman LLP Objectives Health Information Technology (HIT) and Electronic Health Record (EHR)

6 Critical Impact Factors of Health Reform on Revenue Cycle Management

6 Critical Impact Factors of Health Reform on Revenue Cycle Management Pyramid Healthcare Solutions Thought Leadership Series The healthcare industry is undergoing significant change in the face of the

6 Critical Impact Factors of Health Reform on Revenue Cycle Management Pyramid Healthcare Solutions Thought Leadership Series The healthcare industry is undergoing significant change in the face of the

Clinically Integrated Networks and Accountable Care Organizations

Clinically Integrated Networks and Accountable Care Organizations 1 Do Nothing 2 Become Someone s Employee 3 Join a Network Provider The wake up call is for POPULATION health management managing clinical

Clinically Integrated Networks and Accountable Care Organizations 1 Do Nothing 2 Become Someone s Employee 3 Join a Network Provider The wake up call is for POPULATION health management managing clinical

Healthcare Reform (ACA) Update Greater Magnolia Chamber of Commerce

Update Greater Magnolia Chamber of Commerce") Healthcare Reform (ACA) Update Greater Magnolia Chamber of Commerce FREDDY WARNER System Executive, Public Policy & Government Relations Memorial Hermann Health System March 27, 2014 PRESENTATION OUTLINE

Healthcare Reform (ACA) Update Greater Magnolia Chamber of Commerce FREDDY WARNER System Executive, Public Policy & Government Relations Memorial Hermann Health System March 27, 2014 PRESENTATION OUTLINE

Analytic-Driven Quality Keys Success in Risk-Based Contracts. Ross Gustafson, Vice President Allina Performance Resources, Health Catalyst

Analytic-Driven Quality Keys Success in Risk-Based Contracts March 2 nd, 2016 Ross Gustafson, Vice President Allina Performance Resources, Health Catalyst Brian Rice, Vice President Network/ACO Integration,

Analytic-Driven Quality Keys Success in Risk-Based Contracts March 2 nd, 2016 Ross Gustafson, Vice President Allina Performance Resources, Health Catalyst Brian Rice, Vice President Network/ACO Integration,

HEALTHCARE REFORM CARE DELIVERY AND REIMBURSEMENT MODELS. April 10, 2014

HEALTHCARE REFORM CARE DELIVERY AND REIMBURSEMENT MODELS April 10, 2014 1 MARKETPLACE UPDATE 2 MARKETPLACE - ESSENTIAL HEALTH BENEFITS 3 MARKETPLACE - METAL LEVELS 4 WHAT IS THE HEALTH INSURANCE MARKETPLACE

HEALTHCARE REFORM CARE DELIVERY AND REIMBURSEMENT MODELS April 10, 2014 1 MARKETPLACE UPDATE 2 MARKETPLACE - ESSENTIAL HEALTH BENEFITS 3 MARKETPLACE - METAL LEVELS 4 WHAT IS THE HEALTH INSURANCE MARKETPLACE

Quality Accountable Care Population Health: The Journey Continues

Quality Accountable Care Population Health: The Journey Continues Health Insights April 10, 2014 Doug Hastings 2001 Institute of Medicine 2 An Agenda For Crossing The Chasm Between the health care we have

Quality Accountable Care Population Health: The Journey Continues Health Insights April 10, 2014 Doug Hastings 2001 Institute of Medicine 2 An Agenda For Crossing The Chasm Between the health care we have

HEALTHCARE REFORM OCTOBER 2012

HEALTHCARE REFORM Tracking ACO Growth Nationally OCTOBER 2012 The enclosed slides are intended to provide you with a snapshot of how private sector accountable care organizations (ACOs) have formed since

HEALTHCARE REFORM Tracking ACO Growth Nationally OCTOBER 2012 The enclosed slides are intended to provide you with a snapshot of how private sector accountable care organizations (ACOs) have formed since

Accountable Care Organizations: Reality or Myth?

Written by: Ty Meyer Accountable Care Organizations: Reality or Myth? Introduction According to Steven Gerst, VP of Medical Affairs at MedCurrent Corporation, The Patient Protection and Affordable Care

Written by: Ty Meyer Accountable Care Organizations: Reality or Myth? Introduction According to Steven Gerst, VP of Medical Affairs at MedCurrent Corporation, The Patient Protection and Affordable Care

Strengthening Community Health Centers. Provides funds to build new and expand existing community health centers. Effective Fiscal Year 2011.

Implementation Timeline Reflecting the Affordable Care Act 2010 Access to Insurance for Uninsured Americans with a Pre-Existing Condition. Provides uninsured Americans with pre-existing conditions access

Implementation Timeline Reflecting the Affordable Care Act 2010 Access to Insurance for Uninsured Americans with a Pre-Existing Condition. Provides uninsured Americans with pre-existing conditions access

Home Health Care Today: Higher Acuity Level of Patients Highly skilled Professionals Costeffective Uses of Technology Innovative Care Techniques

Comprehensive EHR Infrastructure Across the Health Care System The goal of the Administration and the Department of Health and Human Services to achieve an infrastructure for interoperable electronic health

Comprehensive EHR Infrastructure Across the Health Care System The goal of the Administration and the Department of Health and Human Services to achieve an infrastructure for interoperable electronic health

Reforming and restructuring the health care delivery system

Reforming and restructuring the health care delivery system Are Accountable Care Organizations and bundling the solution? Prepared by: Dan Head, Principal, RSM US LLP [email protected], +1 703 336 6536

Reforming and restructuring the health care delivery system Are Accountable Care Organizations and bundling the solution? Prepared by: Dan Head, Principal, RSM US LLP [email protected], +1 703 336 6536

Accountable Care Organizations: An old idea with new potential. Stephen E. Whitney, MD, MBA Testimony to Senate State Affairs September 22, 2010

Accountable Care Organizations: An old idea with new potential Stephen E. Whitney, MD, MBA Testimony to Senate State Affairs September 22, 2010 Impetus for ACO Formation Increased health care cost From

Accountable Care Organizations: An old idea with new potential Stephen E. Whitney, MD, MBA Testimony to Senate State Affairs September 22, 2010 Impetus for ACO Formation Increased health care cost From

Affordable Care Act at 3: Strengthening Medicare

Affordable Care Act at 3: Strengthening Medicare ISSUE BRIEF Fifth in a series May 22, 2013 Kyle Brown Senior Health Policy Analyst 789 Sherman St. Suite 300 Denver, CO 80203 www.cclponline.org 303-573-5669

Affordable Care Act at 3: Strengthening Medicare ISSUE BRIEF Fifth in a series May 22, 2013 Kyle Brown Senior Health Policy Analyst 789 Sherman St. Suite 300 Denver, CO 80203 www.cclponline.org 303-573-5669

Southwestern Vermont Medical Center Operating Budget Fiscal Year 2016

Southwestern Vermont Medical Center Operating Budget Fiscal Year 2016 Southwestern Vermont Medical Center s (hereafter SVMC or Medical Center ) Operating Budget for Fiscal Year (hereafter FY ) 2016 has

Southwestern Vermont Medical Center Operating Budget Fiscal Year 2016 Southwestern Vermont Medical Center s (hereafter SVMC or Medical Center ) Operating Budget for Fiscal Year (hereafter FY ) 2016 has

6 Critical Impact Factors of Health Reform on Revenue Cycle Management

6 Critical Impact Factors of Health Reform on Revenue Cycle Management Pyramid Healthcare Solutions Thought Leadership Series The healthcare industry is undergoing significant change in the face of the

6 Critical Impact Factors of Health Reform on Revenue Cycle Management Pyramid Healthcare Solutions Thought Leadership Series The healthcare industry is undergoing significant change in the face of the

UNIVERSITY OF ILLINOIS HOSPITAL & HEALTH SCIENCES SYSTEM: FINANCIAL REPORT AND SYSTEM DASHBOARDS May 29, 2013

UNIVERSITY OF ILLINOIS HOSPITAL & HEALTH SCIENCES SYSTEM: FINANCIAL REPORT AND SYSTEM DASHBOARDS May 29, 2013 Office of the Vice President for Health Affairs Board of Trustees Spring Chicago Meeting UI

UNIVERSITY OF ILLINOIS HOSPITAL & HEALTH SCIENCES SYSTEM: FINANCIAL REPORT AND SYSTEM DASHBOARDS May 29, 2013 Office of the Vice President for Health Affairs Board of Trustees Spring Chicago Meeting UI

Using Partial Capitation as an Alternative to Shared Savings to Support Accountable Care Organizations in Medicare

December 2010 Using Partial Capitation as an Alternative to Shared Savings to Support Accountable Care Organizations in Medicare CONTENTS Background... 2 Problems with the Shared Savings Model... 2 How

December 2010 Using Partial Capitation as an Alternative to Shared Savings to Support Accountable Care Organizations in Medicare CONTENTS Background... 2 Problems with the Shared Savings Model... 2 How

Clinical Integration in Practice Case Study Allina Health

Clinical Integration in Practice Case Study Allina ealth The Second of Six Conference Calls for VA, Inc. Leading Constructive Change Boston Cleveland Dallas Denver Miami San Francisco Washington, D.C.

Clinical Integration in Practice Case Study Allina ealth The Second of Six Conference Calls for VA, Inc. Leading Constructive Change Boston Cleveland Dallas Denver Miami San Francisco Washington, D.C.

How Health Reform Will Affect Health Care Quality and the Delivery of Services

Fact Sheet AARP Public Policy Institute How Health Reform Will Affect Health Care Quality and the Delivery of Services The recently enacted Affordable Care Act contains provisions to improve health care

Fact Sheet AARP Public Policy Institute How Health Reform Will Affect Health Care Quality and the Delivery of Services The recently enacted Affordable Care Act contains provisions to improve health care

Georgia Society for Healthcare Materials Management. The status of ACO s in the market and how they impact materials management.

Georgia Society for Healthcare Materials Management The status of ACO s in the market and how they impact materials management October 25, 2013 A Highly Volatile And Complex Industry Key Trends Impacting

Georgia Society for Healthcare Materials Management The status of ACO s in the market and how they impact materials management October 25, 2013 A Highly Volatile And Complex Industry Key Trends Impacting

Value Based Care and Healthcare Reform

Value Based Care and Healthcare Reform Dimensions in Cardiac Care November, 2014 Jacqueline Matthews, RN, MS Senior Director, Quality Reporting & Reform Quality and Patient Safety Institute Cleveland Clinic

Value Based Care and Healthcare Reform Dimensions in Cardiac Care November, 2014 Jacqueline Matthews, RN, MS Senior Director, Quality Reporting & Reform Quality and Patient Safety Institute Cleveland Clinic

PL 111-148 and Amendments: Impact on Post-Acute Care for Health Care Systems

PL 111-148 and Amendments: Impact on Post-Acute Care for Health Care Systems By Kathleen M. Griffin, PhD. There are three key provisions of the law that will have direct impact on post-acute care needs

PL 111-148 and Amendments: Impact on Post-Acute Care for Health Care Systems By Kathleen M. Griffin, PhD. There are three key provisions of the law that will have direct impact on post-acute care needs

Summary of the Final Medicaid Redesign Team (MRT) Report A Plan to Transform The Empire State s Medicaid Program

Report A Plan to Transform The Empire State s Medicaid Program") Summary of the Final Medicaid Redesign Team (MRT) Report A Plan to Transform The Empire State s Medicaid Program May 2012 This document summarizes the key points contained in the MRT final report, A Plan

Summary of the Final Medicaid Redesign Team (MRT) Report A Plan to Transform The Empire State s Medicaid Program May 2012 This document summarizes the key points contained in the MRT final report, A Plan

The meeting was called to order at 5:27 by the Chairman of the Executive Committee, Joseph Szot, M.D.

Minutes Carver College of Medicine Fall Faculty Forum: Health Care Reform Legislation - Its Implementation and Impact on UI Health Care Tuesday, October 26, 2010 Presenters: Vice-President Jean Robillard,

Minutes Carver College of Medicine Fall Faculty Forum: Health Care Reform Legislation - Its Implementation and Impact on UI Health Care Tuesday, October 26, 2010 Presenters: Vice-President Jean Robillard,

Leveraging Predictive Analytic and Artificial Intelligence Technology for Financial and Clinical Performance

Leveraging Predictive Analytic and Artificial Intelligence Technology for Financial and Clinical Performance Matt Seefeld CEO & Co-Founder [email protected] www.interpointpartners.com (404)446-0051

Leveraging Predictive Analytic and Artificial Intelligence Technology for Financial and Clinical Performance Matt Seefeld CEO & Co-Founder [email protected] www.interpointpartners.com (404)446-0051

The Cornerstones of Accountable Care ACO

The Cornerstones of Accountable Care Clinical Integration Care Coordination ACO Information Technology Financial Management The Accountable Care Organization is emerging as an important care delivery and

The Cornerstones of Accountable Care Clinical Integration Care Coordination ACO Information Technology Financial Management The Accountable Care Organization is emerging as an important care delivery and

Applying ACO Principles to a Pediatric Population UH Rainbow Care Connection: Transforming Pediatric Ambulatory Care with a Physician Extension Team

Applying ACO Principles to a Pediatric Population UH Rainbow Care Connection: Transforming Pediatric Ambulatory Care with a Physician Extension Team Ethan Chernin, MBA Director 1 Objectives Understand

Applying ACO Principles to a Pediatric Population UH Rainbow Care Connection: Transforming Pediatric Ambulatory Care with a Physician Extension Team Ethan Chernin, MBA Director 1 Objectives Understand

Critical Access Hospitals and

Critical Access Hospitals and Health Care Reform What s in it for you? Patient Protection and Affordable Care Act (ACA) Fundamental changes Moving Medicare from payment for services to payment for outcomes

Critical Access Hospitals and Health Care Reform What s in it for you? Patient Protection and Affordable Care Act (ACA) Fundamental changes Moving Medicare from payment for services to payment for outcomes

The Patient Protection and Affordable Care Act. Implementation Timeline

The Patient Protection and Affordable Care Act Implementation Timeline 2009 Credit to Encourage Investment in New Therapies: A two year temporary credit subject to an overall cap of $1 billion to encourage

The Patient Protection and Affordable Care Act Implementation Timeline 2009 Credit to Encourage Investment in New Therapies: A two year temporary credit subject to an overall cap of $1 billion to encourage

Strengthening Medicare: Better Health, Better Care, Lower Costs Efforts Will Save Nearly $120 Billion for Medicare Over Five Years.

Strengthening Medicare: Better Health, Better Care, Lower Costs Efforts Will Save Nearly $120 Billion for Medicare Over Five Years Introduction The Centers for Medicare and Medicaid Services (CMS) and

Strengthening Medicare: Better Health, Better Care, Lower Costs Efforts Will Save Nearly $120 Billion for Medicare Over Five Years Introduction The Centers for Medicare and Medicaid Services (CMS) and

The Patient Protection & Affordable Care Act: Next Steps in Maine. February 8, 2013 1

The Patient Protection & Affordable Care Act: Next Steps in Maine February 8, 2013 1 Maine Medical Association Voluntary membership association of over 3,600 Maine physicians, residents, and medical students

The Patient Protection & Affordable Care Act: Next Steps in Maine February 8, 2013 1 Maine Medical Association Voluntary membership association of over 3,600 Maine physicians, residents, and medical students

Prescription drugs are a critical component of health care. Because of the role of drugs in treating conditions, it is important that Medicare ensures that its beneficiaries have access to appropriate

Prescription drugs are a critical component of health care. Because of the role of drugs in treating conditions, it is important that Medicare ensures that its beneficiaries have access to appropriate

Nuts and Bolts Accountable Care Organizations: A New Care Delivery Model for New Expectations

Nuts and Bolts Accountable Care Organizations: A New Care Delivery Model for New Expectations Presented to The American College of Cardiology October 27, 2012 1 Franciscan Alliance Overview Franciscan

Nuts and Bolts Accountable Care Organizations: A New Care Delivery Model for New Expectations Presented to The American College of Cardiology October 27, 2012 1 Franciscan Alliance Overview Franciscan

Proven Innovations in Primary Care Practice

Proven Innovations in Primary Care Practice October 14, 2014 The opinions expressed are those of the presenter and do not necessarily state or reflect the views of SHSMD or the AHA. 2014 Society for Healthcare

Proven Innovations in Primary Care Practice October 14, 2014 The opinions expressed are those of the presenter and do not necessarily state or reflect the views of SHSMD or the AHA. 2014 Society for Healthcare

Repeal the Sustainable Growth Rate (SGR), avoiding annual double digit payment cuts;

, avoiding annual double digit payment cuts;") Background Summary of H.R. 2: The Medicare Access and CHIP Reauthorization Act of 2015 SGR Reform Law Enacts Payment Reforms to Improve Quality, Outcomes, and Cost On April 16, 2015, the President signed

Background Summary of H.R. 2: The Medicare Access and CHIP Reauthorization Act of 2015 SGR Reform Law Enacts Payment Reforms to Improve Quality, Outcomes, and Cost On April 16, 2015, the President signed

Accountable Care Organization Workgroup Glossary

Accountable Care Organization Workgroup Glossary Accountable care organization (ACO) a group of coordinated health care providers that care for all or some of the health care needs of a defined population.

Accountable Care Organization Workgroup Glossary Accountable care organization (ACO) a group of coordinated health care providers that care for all or some of the health care needs of a defined population.

Health Care Financing: ACC/ ACO s, beyond the hype hope. Brian Seppi, MD, President, Washington State Medical Assn.

: ACC/ ACO s, beyond the hype hope Brian Seppi, MD, President, Washington State Medical Assn. Washington State Medical Association Health Care Financing Our vision Make Washington the best place to practice

: ACC/ ACO s, beyond the hype hope Brian Seppi, MD, President, Washington State Medical Assn. Washington State Medical Association Health Care Financing Our vision Make Washington the best place to practice

Healthcare Reform: An Analysis of the Impact on Healthcare Providers

Healthcare Reform: An Analysis of the Impact on Healthcare Providers Background The financial impact from the Affordable Care Act on providers from changes in Medicare reimbursement have been well documented

Healthcare Reform: An Analysis of the Impact on Healthcare Providers Background The financial impact from the Affordable Care Act on providers from changes in Medicare reimbursement have been well documented

Urgent Care. A Brief Overview of Urgent Care and Opportunities in an Era of Health Care Reform. Presented at NCSL, August 2014 A SNAPSHOT

Urgent Care A Brief Overview of Urgent Care and Opportunities in an Era of Health Care Reform Presented at NCSL, August 2014 A SNAPSHOT 1 What Is Urgent Care? Health care provided on a walk in, no appointment

Urgent Care A Brief Overview of Urgent Care and Opportunities in an Era of Health Care Reform Presented at NCSL, August 2014 A SNAPSHOT 1 What Is Urgent Care? Health care provided on a walk in, no appointment

Banner Health Network Pioneer ACO - Physician Toolkit

& The Banner Health Network, an AIP and Banner Health partnership, present the Banner Health Network Pioneer ACO - Physician Toolkit This BHN Pioneer ACO Physician Toolkit has been developed to provide

& The Banner Health Network, an AIP and Banner Health partnership, present the Banner Health Network Pioneer ACO - Physician Toolkit This BHN Pioneer ACO Physician Toolkit has been developed to provide

Summary of Major Provisions in Final House Reform Package

SPECIAL BULLETIN Monday, March 22, 2010 This summary is five pages. Summary of Major Provisions in Final House Reform Package The U.S. House of Representatives late yesterday voted to pass landmark health

SPECIAL BULLETIN Monday, March 22, 2010 This summary is five pages. Summary of Major Provisions in Final House Reform Package The U.S. House of Representatives late yesterday voted to pass landmark health

ACOs: Six Things Specialty Practices Should Know

ACOs: Six Things Specialty Practices Should Know =TOS Newsletter, July/August 2014= Authors: John P. Schmitt, Ph.D. and J. Garrett Schmitt, MBA, PCMH CCE INTRODUCTION Do you remember the analogy of four

ACOs: Six Things Specialty Practices Should Know =TOS Newsletter, July/August 2014= Authors: John P. Schmitt, Ph.D. and J. Garrett Schmitt, MBA, PCMH CCE INTRODUCTION Do you remember the analogy of four

Helping You Achieve Better Clinical and Financial Health

McKesson Business Performance Services Accountable Care Services Helping You Achieve Better Clinical and Financial Health 1 We recognized that fee-for-service would decrease and value-based care would

McKesson Business Performance Services Accountable Care Services Helping You Achieve Better Clinical and Financial Health 1 We recognized that fee-for-service would decrease and value-based care would

Accountable Care Platform

The shift toward increased collaboration, outcome-based payment and new benefit design is transforming how we pay for health care and how health care is delivered. UnitedHealthcare is taking an industry

The shift toward increased collaboration, outcome-based payment and new benefit design is transforming how we pay for health care and how health care is delivered. UnitedHealthcare is taking an industry

Adding Value to. Provider Compensation. June 13, 2016. Healthcare Strategy Group OHA Presentation 2016. Adding Value to. Physician Compensation

Provider Compensation June 13, 2016 1 Who are We? About (HSG) Hospital-physician integration specialists since 1999 Strategic, best practice approach to employed physician networks and independent physician

Provider Compensation June 13, 2016 1 Who are We? About (HSG) Hospital-physician integration specialists since 1999 Strategic, best practice approach to employed physician networks and independent physician

Health Care Reform Update January 2012 MG76120 0212 LILLY USA, LLC. ALL RIGHTS RESERVED

Health Care Reform Update January 2012 Disclaimer This presentation is for educational purposes only. It is not a complete analysis of the material contained herein. Before taking any action on the issues

Health Care Reform Update January 2012 Disclaimer This presentation is for educational purposes only. It is not a complete analysis of the material contained herein. Before taking any action on the issues

Accountable Care Organization Refinement Brief

Accountable Care Organization Refinement Brief The participants in the Medicare Shared Savings Program (MSSP), the Physician Group Practice Transition Demonstration (PGP-TD), and the Pioneer Accountable

Accountable Care Organization Refinement Brief The participants in the Medicare Shared Savings Program (MSSP), the Physician Group Practice Transition Demonstration (PGP-TD), and the Pioneer Accountable

Healthcare Payment Reform: Transition from Volume-Based to Value-Based Payments. October 6, 2014

Healthcare Payment Reform: Transition from Volume-Based to Value-Based Payments October 6, 2014 1 Healthcare Payment Reform: From Volume to Value-Based Payments Healthcare Reform Overview National Trends

Healthcare Payment Reform: Transition from Volume-Based to Value-Based Payments October 6, 2014 1 Healthcare Payment Reform: From Volume to Value-Based Payments Healthcare Reform Overview National Trends

Hospital Financing Overview

Texas Hospital Association 1108 Lavaca, Suite 700, Austin, TX, 78701-2180 www.tha.org Hospital Financing Overview Under federal law, hospitals are required to provide care to anyone who seeks it in their

Texas Hospital Association 1108 Lavaca, Suite 700, Austin, TX, 78701-2180 www.tha.org Hospital Financing Overview Under federal law, hospitals are required to provide care to anyone who seeks it in their

April 17, 2014. Re: Evolution of ACO initiatives at CMS. Dear Dr. Conway:

Patrick Conway, M.D. Acting Director of the Innovation Center Centers for Medicare & Medicaid Services Hubert H. Humphrey Building 200 Independence Avenue, S.W. Room 445-G Washington, DC 20201 Re: Evolution

Patrick Conway, M.D. Acting Director of the Innovation Center Centers for Medicare & Medicaid Services Hubert H. Humphrey Building 200 Independence Avenue, S.W. Room 445-G Washington, DC 20201 Re: Evolution

Concept Paper: Texas Nursing Facility Transformation Program

QAPI Version Concept Paper: Texas Nursing Facility Transformation Program Introduction This concept paper presents a proposal to establish a Nursing Facility (NF) Transformation Program beginning in DY

QAPI Version Concept Paper: Texas Nursing Facility Transformation Program Introduction This concept paper presents a proposal to establish a Nursing Facility (NF) Transformation Program beginning in DY