Well-Performing Portfolios and Well-Disguised Insolvency. Patrick J. Collins, Steven M. Fast & Laura A. Schuyler

|

|

|

- Austen Matthews

- 8 years ago

- Views:

Transcription

1 Well-Performing Portfolios and Well-Disguised Insolvency Patrick J. Collins, Steven M. Fast & Laura A. Schuyler

2 The Secret to Life According to Charles Dickens: Annual income 20 pounds, annual expenditure 19 pounds, 19 and 6, result happiness. Annual income 20 pounds, annual expenditure 20 pounds ought and 6, result misery. Page 2

3 The Secret to a Successful Trust Portfolio Trust Assets > Trust Liabilities... Result = Happiness Trust Assets < Trust Liabilities... Result = Misery Page 3

4 Trust Liabilities: Distributions to Current Beneficiaries Capital Preservation/Growth for Remainder Beneficiaries Page 4

5 Key Duties of a Trustee: Monitor the trust portfolio and inform the beneficiaries in a meaningful way. Page 5

6 Key Duties of a Trustee: Monitor the trust portfolio and inform the beneficiaries in a meaningful way. How is the trust portfolio doing relative to its liabilities? NOT how the trust portfolio is doing in relation to the S&P Page 6

7 Key Duties of a Trustee: Monitor the trust portfolio and inform the beneficiaries in a meaningful way. How is the trust portfolio doing relative to its liabilities? Are there enough assets to distribute amounts to the current beneficiary and preserve capital for the remainder beneficiaries? Sequence Risk Feeding the Bear Page 7

8 1. Use Risk Models Judiciously. Page 8

9 Page 9 Simple, 2-Asset Class Portfolio

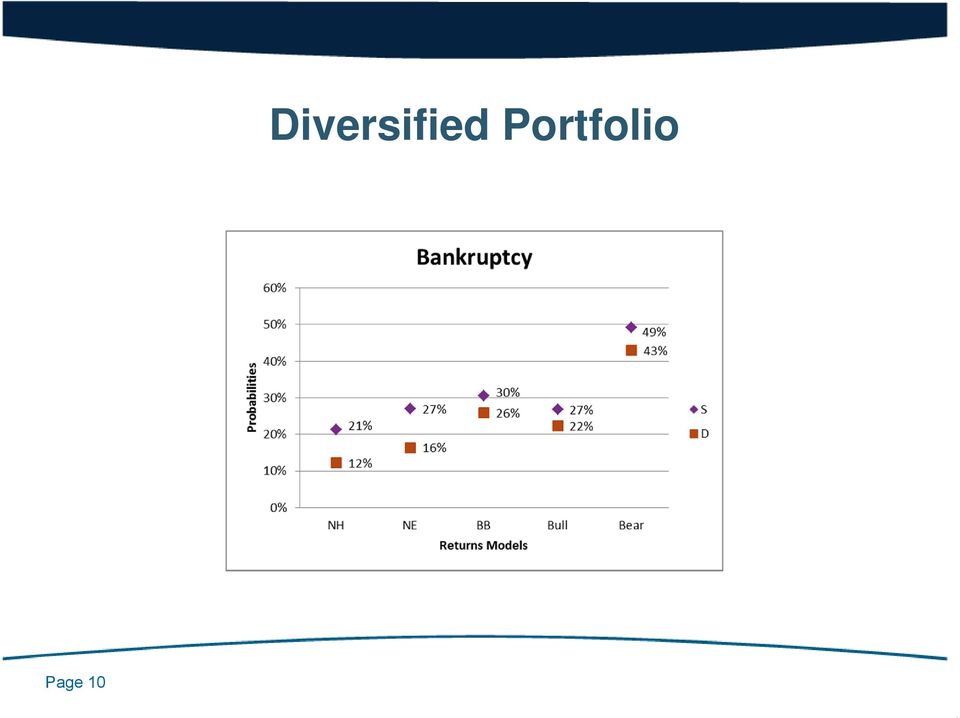

10 Page 10 Diversified Portfolio

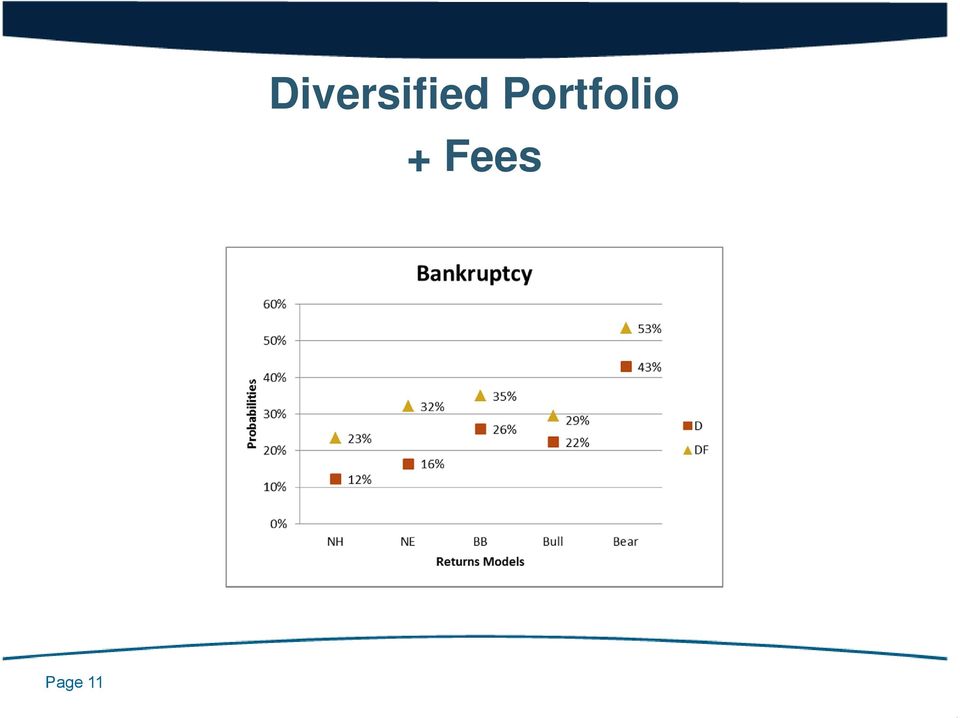

11 Diversified Portfolio + Fees Page 11

12 Diversified Portfolio + Fees + Longevity Page 12

13 Diversified Portfolio + Fees + Longevity + Taxes Page 13

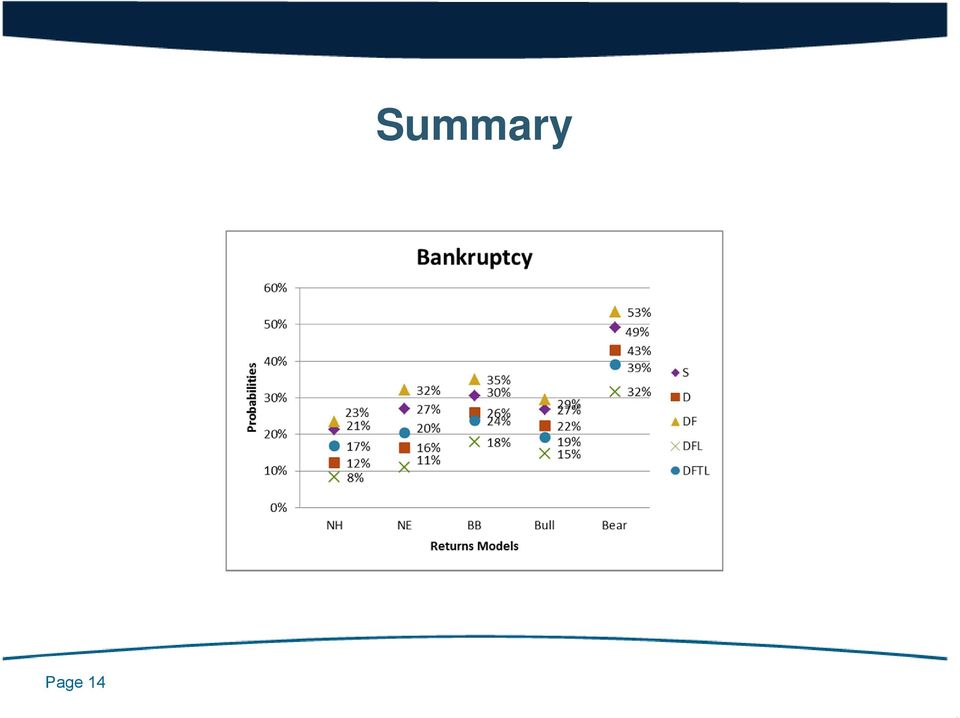

14 Page 14 Summary

15 Summary: Model Risk Results range from an 8% risk of bankruptcy to a 53% risk of bankruptcy. Page 15

16 Summary: Model Risk Results range from an 8% risk of bankruptcy to a 53% risk of bankruptcy. The NH model (simple Monte Carlo model) produces the most optimistic results in each case, perhaps underestimating risk. Page 16

17 Summary: Model Risk Results range from an 8% risk of bankruptcy to a 53% risk of bankruptcy. The NH model (simple Monte Carlo model) produces the most optimistic results in each case, perhaps underestimating risk. The Bear model (regime-switching model, assuming initial bear market) produces the most pessimistic results in each case, perhaps overstating risk. Page 17

produces the most")

18 2. Locate the Free Boundary. Page 18

19 The Free Boundary Free Boundary Line Unfeasible Feasible Region $0 Wealth Deficit Wealth Surplus Page 19

20 The Free Boundary Present Value of Trust Assets [Stochastic Present Value of Distributions to the Current Beneficiary + Stochastic Present Value of Capital Preserved for Remainder Beneficiaries + Stochastic Present Value of Fees and Investment Expenses.] Page 20

21 The Free Boundary Present Value of Trust Assets [Cost of an Annuity for the Current Beneficiary + Stochastic Present Value of Capital Preserved for Remainder Beneficiaries + Stochastic Present Value of Fees and Investment Expenses.] Page 21

22 The Free Boundary Wealth to Annuity Cost Ratio (WACR) = The Ratio of the Trust s Value to the Cost of Purchasing an Annuity for the Current Beneficiary and Returning Capital to the Remainder Beneficiaries Page 22

23 Example 1: Bob & Joanna Assumptions: Bob s Goal: Provide for his wife Joanna for her lifetime. Initial Trust Value = $1 million Joanna is 70 years old. Joanna needs distributions of $61,800 per year. Page 23

24 Example 1: Bob & Joanna Is Bob s goal feasible? Page 24

25 Example 1: Bob & Joanna Is Bob s goal feasible? Page 25

26 Example 1: Bob & Joanna 5 Years Later... Is Bob s goal feasible? Page 26

27 Example 2: Bob, Joanna & Children Assumptions: Bob s Goals: (1) Provide for his wife Joanna for her lifetime and (2) preserve the original principal (as adjusted for inflation) for his children. Initial Trust Value = $1 million Joanna is 50 years old. Joanna needs distributions of $42,000 per year. Page 27

28 Example 2: Bob, Joanna & Children Are Bob s goals feasible? Page 28

29 Example 2: Bob, Joanna & Children 20 Years Later... Are Bob s goals feasible? Page 29

30 Free Boundary: Summary If the only goal is to provide for the current beneficiary, the free boundary is located at a WACR of 1. Page 30

31 Free Boundary: Summary If the only goal is to provide for the current beneficiary, the free boundary is located at a WACR of 1. If there are dual goals of providing for the current beneficiary and preserving capital for the remainder beneficiaries, a higher WACR is necessary because the portfolio must grow to sustain the remainder beneficiaries interest on a constant dollar basis. Page 31

32 What Are My Options? Based on your analysis of the risk models and the location of the free boundary, you know you re in trouble. Page 32

33 What Are My Options? Based on your analysis of the risk models and the location of the free boundary, you know you re in trouble. 1. Stay the course? Page 33

34 What Are My Options? Based on your analysis of the risk models and the location of the free boundary, you know you re in trouble. 1. Stay the course? 2. Change the asset allocation? Page 34

35 What Are My Options? Based on your analysis of the risk models and the location of the free boundary, you know you re in trouble. 1. Stay the course? 2. Change the asset allocation? 3. Reduce distributions to the current beneficiary? Page 35

36 What Are My Options? Based on your analysis of the risk models and the location of the free boundary, you know you re in trouble. 1. Stay the course? 2. Change the asset allocation? 3. Reduce distributions to the current beneficiary? 4. Divide the portfolio into two funds? Page 36

37 What Are My Options? Based on your analysis of the risk models and the location of the free boundary, you know you re in trouble. 1. Stay the course? 2. Change the asset allocation? 3. Reduce distributions to the current beneficiary? 4. Divide the portfolio into two funds? 5. Buy an annuity and invest the balance? Page 37

38 Summary Monitor the trust portfolio and inform the beneficiaries in a meaningful way. Use Risk Models Judiciously. Locate the Free Boundary. Review Options. Page 38

Retirement Income Adequacy With Immediate and Longevity Annuities

May 2011 No. 357 Retirement Income Adequacy With Immediate and Longevity Annuities By Youngkyun Park, Employee Benefit Research Institute UPDATING EARLIER EBRI ANALYSIS: This Issue Brief updates with recent

May 2011 No. 357 Retirement Income Adequacy With Immediate and Longevity Annuities By Youngkyun Park, Employee Benefit Research Institute UPDATING EARLIER EBRI ANALYSIS: This Issue Brief updates with recent

Your model to successful individual retirement investment plans

Your model to successful individual retirement investment plans Tim Noonan Managing Director, Capital Markets Insights Russell Investments WWW.RISYMPOSIUM.COM Presented by: Important Information Please

Your model to successful individual retirement investment plans Tim Noonan Managing Director, Capital Markets Insights Russell Investments WWW.RISYMPOSIUM.COM Presented by: Important Information Please

Meeting the Global Challenge of Funding Retirement:

Meeting the Global Challenge of Funding Retirement: A Case Study of Financial Engineering in the Design and Implementation of a Solution Robert C. Merton School of Management Distinguished Professor of

Meeting the Global Challenge of Funding Retirement: A Case Study of Financial Engineering in the Design and Implementation of a Solution Robert C. Merton School of Management Distinguished Professor of

Maximize Retirement Income and Preserve Accumulated Wealth

Maximize Retirement Income and Preserve Accumulated Wealth Welcome! Steven M. Dalton, CFP 40 South River Road, Unit 15 Bedford, NH 03110 603-668-2303 Securities offered through Comprehensive Asset Management

Maximize Retirement Income and Preserve Accumulated Wealth Welcome! Steven M. Dalton, CFP 40 South River Road, Unit 15 Bedford, NH 03110 603-668-2303 Securities offered through Comprehensive Asset Management

The 2004 Report of the Social Security Trustees: Social Security Shortfalls, Social Security Reform and Higher Education

POLICY BRIEF Visit us at: www.tiaa-crefinstitute.org. September 2004 The 2004 Report of the Social Security Trustees: Social Security Shortfalls, Social Security Reform and Higher Education The 2004 Social

POLICY BRIEF Visit us at: www.tiaa-crefinstitute.org. September 2004 The 2004 Report of the Social Security Trustees: Social Security Shortfalls, Social Security Reform and Higher Education The 2004 Social

4.0% 2.0% 0.0% -2.0% -4.0% 1/1/1930 1/1/1940 1/1/1950 1/1/1960 1/1/1970 1/1/1980 1/1/1990 1/1/2000 1/1/2010 Period end date

I am still looking at issues around statistics of how lump sum investing behaves relative to periodic investing () which most of us do. In particular, most arguments, growth of $10,00 charts, and statistics

I am still looking at issues around statistics of how lump sum investing behaves relative to periodic investing () which most of us do. In particular, most arguments, growth of $10,00 charts, and statistics

Managing Retirement Security with an Income Advantage

Managing Retirement Security with an Income Advantage The VantageTrust Retirement IncomeAdvantage Fund 0186480-00001-00 How can you make sure that you have the tools necessary to achieve your desired standard

Managing Retirement Security with an Income Advantage The VantageTrust Retirement IncomeAdvantage Fund 0186480-00001-00 How can you make sure that you have the tools necessary to achieve your desired standard

http://www.fpanet.org/journal/articles/2004_issues/jfp1004-art6.cfm?renderforprint=1

Page 1 of 10 You are here: FPA Net > FPA Journal > Past Issues & Articles > 2004 Issues > 2004 October Issue - Article 6 Return to normal view Contributions Decision Rules and Portfolio Management for

Page 1 of 10 You are here: FPA Net > FPA Journal > Past Issues & Articles > 2004 Issues > 2004 October Issue - Article 6 Return to normal view Contributions Decision Rules and Portfolio Management for

Planning a prosperous retirement

Planning a prosperous retirement Towry s Guide to Retirement Planning About Towry We are one of the UK s leading Wealth Advisers and specialise in providing high quality, expert financial advice to private

Planning a prosperous retirement Towry s Guide to Retirement Planning About Towry We are one of the UK s leading Wealth Advisers and specialise in providing high quality, expert financial advice to private

What Is the Funding Status of Corporate Defined-Benefit Pension Plans in Canada?

Financial System Review What Is the Funding Status of Corporate Defined-Benefit Pension Plans in Canada? Jim Armstrong Chart 1 Participation in Pension Plans Number of Plans Number of Members Thousands

Financial System Review What Is the Funding Status of Corporate Defined-Benefit Pension Plans in Canada? Jim Armstrong Chart 1 Participation in Pension Plans Number of Plans Number of Members Thousands

Pension Plan for Employees of Ontario College of Art & Design University [Ontario Registration Number 0284455] September 30, 2011

![Pension Plan for Employees of Ontario College of Art & Design University [Ontario Registration Number 0284455] September 30, 2011](/thumbs/25/6733260.jpg "Pension Plan for Employees of Ontario College of Art & Design University [Ontario Registration Number 0284455] September 30, 2011") Financial Statements Pension Plan for Employees of Ontario College of Art & Design University [Ontario Registration Number 0284455] INDEPENDENT AUDITORS' REPORT To the Pension Committee of the Pension

Financial Statements Pension Plan for Employees of Ontario College of Art & Design University [Ontario Registration Number 0284455] INDEPENDENT AUDITORS' REPORT To the Pension Committee of the Pension

Retirement plans should target income as the outcome

Retirement plans should target income as the outcome Forward-thinking plan sponsors are committed to helping their employees reach a secure retirement, and in recent years, they have made great strides

Retirement plans should target income as the outcome Forward-thinking plan sponsors are committed to helping their employees reach a secure retirement, and in recent years, they have made great strides

Retirement Planning Software and Post-Retirement Risks: Highlights Report

Retirement Planning Software and Post-Retirement Risks: Highlights Report DECEMBER 2009 SPONSORED BY PREPARED BY John A. Turner Pension Policy Center Hazel A. Witte, JD This report provides a summary of

Retirement Planning Software and Post-Retirement Risks: Highlights Report DECEMBER 2009 SPONSORED BY PREPARED BY John A. Turner Pension Policy Center Hazel A. Witte, JD This report provides a summary of

Simple solution for retirement. Freedom to choose the best retirement solution when your client needs income. New improved compensation

1 Key points for you Simple solution for retirement Income guaranteed FORLIFE Freedom to choose the best retirement solution when your client needs income New improved compensation 2 Key points for your

1 Key points for you Simple solution for retirement Income guaranteed FORLIFE Freedom to choose the best retirement solution when your client needs income New improved compensation 2 Key points for your

How To Calculate Bequest Volatility

Do Annuities Reduce Bequest Values? May 21, 2013 by Joe Tomlinson The widely held view that annuities reduce bequest values is too narrow. Adjustments can be made in retirement portfolios to reduce retirement

Do Annuities Reduce Bequest Values? May 21, 2013 by Joe Tomlinson The widely held view that annuities reduce bequest values is too narrow. Adjustments can be made in retirement portfolios to reduce retirement

Investment opportunities Locking the potential of future benefits

Investment opportunities Locking the potential of future benefits Ivo van der Veen Senior Manager Risk Services Deloitte Sjoerd Kampen Junior Manager Risk Services Deloitte 72 The last couple of years

Investment opportunities Locking the potential of future benefits Ivo van der Veen Senior Manager Risk Services Deloitte Sjoerd Kampen Junior Manager Risk Services Deloitte 72 The last couple of years

New Research: Reverse Mortgages, SPIAs and Retirement Income

New Research: Reverse Mortgages, SPIAs and Retirement Income April 14, 2015 by Joe Tomlinson Retirees need longevity protection and additional funds. Annuities and reverse mortgages can meet those needs.

New Research: Reverse Mortgages, SPIAs and Retirement Income April 14, 2015 by Joe Tomlinson Retirees need longevity protection and additional funds. Annuities and reverse mortgages can meet those needs.

Understand the relationship between financial plans and statements.

#2 Budget Development Your Financial Statements and Plans Learning Goals Understand the relationship between financial plans and statements. Prepare a personal balance sheet. Generate a personal income

#2 Budget Development Your Financial Statements and Plans Learning Goals Understand the relationship between financial plans and statements. Prepare a personal balance sheet. Generate a personal income

A GUIDE TO INVESTING IN ANNUITIES

A GUIDE TO INVESTING IN ANNUITIES What Benefits Do Annuities Offer in Planning for Retirement? Oppenheimer Life Agency, Ltd. Oppenheimer Life Agency, Ltd., a wholly owned subsidiary of Oppenheimer & Co.

A GUIDE TO INVESTING IN ANNUITIES What Benefits Do Annuities Offer in Planning for Retirement? Oppenheimer Life Agency, Ltd. Oppenheimer Life Agency, Ltd., a wholly owned subsidiary of Oppenheimer & Co.

Our distinctive approach is based on our commitment to combining sound financial advice with exceptional service and a well-executed investment plan.

Joggers on the Buffalo Bayou trail are treated to a dramatic view of Downtown Houston s distincive, stunning skyline. ith over 90 years of combined financial services experience, we established MDT Financial

Joggers on the Buffalo Bayou trail are treated to a dramatic view of Downtown Houston s distincive, stunning skyline. ith over 90 years of combined financial services experience, we established MDT Financial

Are Managed-Payout Funds Better than Annuities?

Are Managed-Payout Funds Better than Annuities? July 28, 2015 by Joe Tomlinson Managed-payout funds promise to meet retirees need for sustainable lifetime income without relying on annuities. To see whether

Are Managed-Payout Funds Better than Annuities? July 28, 2015 by Joe Tomlinson Managed-payout funds promise to meet retirees need for sustainable lifetime income without relying on annuities. To see whether

Senator Tom Harkin chaired the U.S. Senate

Variable Annuity Pension Plans an Emerging Retirement Plan Design Variable annuity pension plans (VAPPs) are not new but may deserve a second look by plan sponsors seeking a more secure retirement plan

Variable Annuity Pension Plans an Emerging Retirement Plan Design Variable annuity pension plans (VAPPs) are not new but may deserve a second look by plan sponsors seeking a more secure retirement plan

Wealth Structuring and Estate Planning. Your vision and your legacy. Life s better when we re connected

Wealth Structuring and Estate Planning Your vision and your legacy Life s better when we re connected Inside 1 Helping you shape the future 2 The elements of wealth structuring 4 The power and flexibility

Wealth Structuring and Estate Planning Your vision and your legacy Life s better when we re connected Inside 1 Helping you shape the future 2 The elements of wealth structuring 4 The power and flexibility

Planning Retirement in a Rising Tax Environment

Planning Retirement in a Rising Tax Environment (Based on the published article written in the 2014 semi-annual edition of Wealth Channel Magazine) By Francis J. Lojewski, MSFS, ChFC, CLU, LUTCF, AEP One-sentence

Planning Retirement in a Rising Tax Environment (Based on the published article written in the 2014 semi-annual edition of Wealth Channel Magazine) By Francis J. Lojewski, MSFS, ChFC, CLU, LUTCF, AEP One-sentence

Estimating the True Cost of Retirement

Estimating the True Cost of Retirement David Blanchett, CFA, CFP Head of Retirement Research Morningstar Investment Management 2013 Morningstar. All Rights Reserved. These materials are for information

Estimating the True Cost of Retirement David Blanchett, CFA, CFP Head of Retirement Research Morningstar Investment Management 2013 Morningstar. All Rights Reserved. These materials are for information

Embedded Value Report

Embedded Value Report 2012 ACHMEA EMBEDDED VALUE REPORT 2012 Contents Management summary 3 Introduction 4 Embedded Value Results 5 Value Added by New Business 6 Analysis of Change 7 Sensitivities 9 Impact

Embedded Value Report 2012 ACHMEA EMBEDDED VALUE REPORT 2012 Contents Management summary 3 Introduction 4 Embedded Value Results 5 Value Added by New Business 6 Analysis of Change 7 Sensitivities 9 Impact

SOCIAL SECURITY WON T BE ENOUGH:

SOCIAL SECURITY WON T BE ENOUGH: 6 REASONS TO CONSIDER AN INCOME ANNUITY How long before you retire? For some of us it s 20 to 30 years away, and for others it s closer to 5 or 0 years. The key here is

SOCIAL SECURITY WON T BE ENOUGH: 6 REASONS TO CONSIDER AN INCOME ANNUITY How long before you retire? For some of us it s 20 to 30 years away, and for others it s closer to 5 or 0 years. The key here is

College of Business Administration Savannah State University Personal Finance (BUSA 3000) Quiz 1 Fall 2011 Dr. William A. Dowling.

Quiz 1 Fall 2011 Dr. William A. Dowling.") College of Business Administration Savannah State University Personal Finance (BUSA 3000) Quiz 1 Fall 2011 Dr. William A. Dowling Exam Key Instructions: You are to answer each of the following. If the

College of Business Administration Savannah State University Personal Finance (BUSA 3000) Quiz 1 Fall 2011 Dr. William A. Dowling Exam Key Instructions: You are to answer each of the following. If the

MANAGING YOUR BENEFITS AT RETIREMENT AT NORMAL RETIREMENT AGE OR EARLIER

MANAGING YOUR BENEFITS AT RETIREMENT AT NORMAL RETIREMENT AGE OR EARLIER Managing your benefits at retirement If you retire at your normal retirement age, or earlier A step-by-step guide to retiring from

MANAGING YOUR BENEFITS AT RETIREMENT AT NORMAL RETIREMENT AGE OR EARLIER Managing your benefits at retirement If you retire at your normal retirement age, or earlier A step-by-step guide to retiring from

Pricing and Risk Management of Variable Annuity Guaranteed Benefits by Analytical Methods Longevity 10, September 3, 2014

Pricing and Risk Management of Variable Annuity Guaranteed Benefits by Analytical Methods Longevity 1, September 3, 214 Runhuan Feng, University of Illinois at Urbana-Champaign Joint work with Hans W.

Pricing and Risk Management of Variable Annuity Guaranteed Benefits by Analytical Methods Longevity 1, September 3, 214 Runhuan Feng, University of Illinois at Urbana-Champaign Joint work with Hans W.

Retirement Benefits in Hong Kong

Retirement Benefits in Hong Kong Introduction In Hong Kong, there are several types of retirement benefits sponsored by different parties as shown below. Government-sponsor - Old Age Allowances from the

Retirement Benefits in Hong Kong Introduction In Hong Kong, there are several types of retirement benefits sponsored by different parties as shown below. Government-sponsor - Old Age Allowances from the

Standby Reverse Mortgages: A Risk Management Tool for Retirement Distributions

Standby Reverse Mortgages: A Risk Management Tool for Retirement Distributions John Salter, PhD, CFP, AIFA Associate Professor, Texas Tech University Vice-President, Wealth Manager, Evensky & Katz Wealth

Standby Reverse Mortgages: A Risk Management Tool for Retirement Distributions John Salter, PhD, CFP, AIFA Associate Professor, Texas Tech University Vice-President, Wealth Manager, Evensky & Katz Wealth

PRIVATE WEALTH MANAGEMENT

CFA LEVEL 3 STUDY SESSION 4 PRIVATE WEALTH MANAGEMENT a. Risk tolerance affected by Sources of wealth Active wealth creation (by entrepreneurial activity) Passive wealth creation, acquired Through inheritance

CFA LEVEL 3 STUDY SESSION 4 PRIVATE WEALTH MANAGEMENT a. Risk tolerance affected by Sources of wealth Active wealth creation (by entrepreneurial activity) Passive wealth creation, acquired Through inheritance

EXCELSIOR INVESTMENTS. Post-Retirement

Your financial planning does not retire when you do Your retirement has finally arrived and a long-awaited chapter in your life begins. By now you should have built up an adequate capital base to provide

Your financial planning does not retire when you do Your retirement has finally arrived and a long-awaited chapter in your life begins. By now you should have built up an adequate capital base to provide

Early Retirement Account

Early Retirement Account As the representative voice of 1.2 million mature Americans and senior citizens, AMAC is deeply concerned with the solvency of Federal legacy programs such as Medicare and Social

Early Retirement Account As the representative voice of 1.2 million mature Americans and senior citizens, AMAC is deeply concerned with the solvency of Federal legacy programs such as Medicare and Social

BS2551 Money Banking and Finance. Institutional Investors

BS2551 Money Banking and Finance Institutional Investors Institutional investors pension funds, mutual funds and life insurance companies are the main players in securities markets in both the USA and

BS2551 Money Banking and Finance Institutional Investors Institutional investors pension funds, mutual funds and life insurance companies are the main players in securities markets in both the USA and

New Research: Reverse Mortgages, SPIAs and Retirement Income

New Research: Reverse Mortgages, SPIAs and Retirement Income April 14, 2015 by Joe Tomlinson Retirees need longevity protection and additional funds. Annuities and reverse mortgages can meet those needs.

New Research: Reverse Mortgages, SPIAs and Retirement Income April 14, 2015 by Joe Tomlinson Retirees need longevity protection and additional funds. Annuities and reverse mortgages can meet those needs.

Client(s): Luke Affluent. Jen Affluent. Advisor:

: Luke Affluent. Jen Affluent. Advisor:") Table of Contents Table of Contents... 1 Disclaimer... 2 Basics of Life Insurance... 4 Survivor Costs... 5 Survivor Costs vs. Resources... 8 Survivor Portfolio... 11 Survivor Costs vs. Resources w/ Add'l

Table of Contents Table of Contents... 1 Disclaimer... 2 Basics of Life Insurance... 4 Survivor Costs... 5 Survivor Costs vs. Resources... 8 Survivor Portfolio... 11 Survivor Costs vs. Resources w/ Add'l

Company Pension Plans in Canada

Company Pension Plans in Canada This article provides an introduction to company pension plans as well as a discussion of several issues currently facing company pension plans in Canada. Company pension

Company Pension Plans in Canada This article provides an introduction to company pension plans as well as a discussion of several issues currently facing company pension plans in Canada. Company pension

Annuity Principles and Concepts Session Five Lesson Two. Annuity (Benefit) Payment Options

Payment Options") Annuity Principles and Concepts Session Five Lesson Two Annuity (Benefit) Payment Options Life Contingency Options - How Income Payments Can Be Made To The Annuitant. Pure Life versus Life with Guaranteed

Annuity Principles and Concepts Session Five Lesson Two Annuity (Benefit) Payment Options Life Contingency Options - How Income Payments Can Be Made To The Annuitant. Pure Life versus Life with Guaranteed

FAMILY LIMITED LIABILITY COMPANY

FAMILY LIMITED LIABILITY COMPANY INTRODUCTION A limited liability company is a business entity that insulates its owners from the liabilities of the entity like a corporation but is taxed for income tax

FAMILY LIMITED LIABILITY COMPANY INTRODUCTION A limited liability company is a business entity that insulates its owners from the liabilities of the entity like a corporation but is taxed for income tax

Variable Annuity Pension Plans: A Balanced Approach to Retirement Risk

Variable Annuity Pension Plans: A Balanced Approach to Retirement Kelly Coffing, EA, FSA, MAAA Principal and Consulting Actuary Milliman, Seattle, Washington Grant Camp, EA, FSA, MAAA, Consulting Actuary

Variable Annuity Pension Plans: A Balanced Approach to Retirement Kelly Coffing, EA, FSA, MAAA Principal and Consulting Actuary Milliman, Seattle, Washington Grant Camp, EA, FSA, MAAA, Consulting Actuary

Corporate asset efficiency

Life insurance solutions Corporate asset efficiency Manage. Access. Preserve. A smart solution for professionals permanent life insurance, a unique asset that can offer tax-advantaged growth. Consider

Life insurance solutions Corporate asset efficiency Manage. Access. Preserve. A smart solution for professionals permanent life insurance, a unique asset that can offer tax-advantaged growth. Consider

Best Practices in Retirement Planning

Best Practices in Retirement Planning Wade D. Pfau, Ph.D., CFA The American College instream Solutions McLean Asset Management Retirement Researcher blog (www.retirementresearcher.com/blog) Retirement

Best Practices in Retirement Planning Wade D. Pfau, Ph.D., CFA The American College instream Solutions McLean Asset Management Retirement Researcher blog (www.retirementresearcher.com/blog) Retirement

How To Fund Retirement

Challenges and Solutions in Retirement Funding and Post-Retirement Payout Robert C. Merton School of Management Distinguished Professor of Finance MIT Sloan School of Management MIT Sloan School Reunion

Challenges and Solutions in Retirement Funding and Post-Retirement Payout Robert C. Merton School of Management Distinguished Professor of Finance MIT Sloan School of Management MIT Sloan School Reunion

How To Reduce Income Taxes In 2014

T A C I T A strategy for reducing income taxes in 2014 Tax deduction for you Avoid capital gains Charitable contribution Income for life or Tax-free passing of assets to your heirs Prepared by Elliot Goldberg

T A C I T A strategy for reducing income taxes in 2014 Tax deduction for you Avoid capital gains Charitable contribution Income for life or Tax-free passing of assets to your heirs Prepared by Elliot Goldberg

Strategies for a more secure retirement

Investment insight February 2013 Jerome Bodisco Investment Research Strategist ThreeSixty As retirement approaches, protecting investments becomes more important than ever. One of the main financial risks

Investment insight February 2013 Jerome Bodisco Investment Research Strategist ThreeSixty As retirement approaches, protecting investments becomes more important than ever. One of the main financial risks

RETIREMENT FUND MEMBER INFORMATION

RETIREMENT FUND MEMBER INFORMATION OPTIONS ON RESIGNATION, RETRENCHMENT OR DISMISSAL If you resign, or are retrenched or dismissed, your membership of your retirement fund will come to an end. The fund

RETIREMENT FUND MEMBER INFORMATION OPTIONS ON RESIGNATION, RETRENCHMENT OR DISMISSAL If you resign, or are retrenched or dismissed, your membership of your retirement fund will come to an end. The fund

Financial Planning in a Low Interest Rate Environment: The Good, the Bad and the Potentially Ugly

Financial Planning in a Low Interest Rate Environment: The Good, the Bad and the Potentially Ugly In June of 2012, the 10 year Treasury note hit its lowest rate level in history when it fell to 1.62%.

Financial Planning in a Low Interest Rate Environment: The Good, the Bad and the Potentially Ugly In June of 2012, the 10 year Treasury note hit its lowest rate level in history when it fell to 1.62%.

May 27, 2015. Most Public Policy Efforts to Date Have Been Focused on the Front End -- Getting People to Participate in Plans

Written Statement of Bradford P. Campbell Before the Advisory Council on Employee Welfare and Pension Benefit Plan s Working Group on Model Notices and Plan Sponsor Education on Lifetime Plan Participation

Written Statement of Bradford P. Campbell Before the Advisory Council on Employee Welfare and Pension Benefit Plan s Working Group on Model Notices and Plan Sponsor Education on Lifetime Plan Participation

What to Consider When Faced With the Pension Election Decision

PENSION ELECTION Key Information About Your Pension (Optional Forms of Benefits) Pension Math and Factors to Consider Pension Maximization What Happens if Your Company Files for Bankruptcy and Your Company

PENSION ELECTION Key Information About Your Pension (Optional Forms of Benefits) Pension Math and Factors to Consider Pension Maximization What Happens if Your Company Files for Bankruptcy and Your Company

[because] administrative charges / investment expenses / [and] asset management fees

![[because] administrative charges / investment expenses / [and] asset management fees](/thumbs/39/19024164.jpg "[because] administrative charges / investment expenses / [and] asset management fees") 11 Simple 401k Learn How to Increase Your Company's 401k Account Values by as Much as 30% to 40% The fees and expenses charged within your company's 401k plan could be costing your employees as much as

11 Simple 401k Learn How to Increase Your Company's 401k Account Values by as Much as 30% to 40% The fees and expenses charged within your company's 401k plan could be costing your employees as much as

Delay Social Security: Funding the Income Gap with a Reverse Mortgage

Thomas C. B. Davison, MA, PhD, CFP NAPFA Registered Financial Advisor Partner Emeritus, Summit Financial Strategies, Inc. toolsforretirementplanning.com tcbdavison@gmail.com Update: June 22, 2014 slightly

Thomas C. B. Davison, MA, PhD, CFP NAPFA Registered Financial Advisor Partner Emeritus, Summit Financial Strategies, Inc. toolsforretirementplanning.com tcbdavison@gmail.com Update: June 22, 2014 slightly

Life Insurance Review Using Legacy Advantage SUL Insurance Policy

Using Legacy Advantage SUL Insurance Policy Supplemental Illustration Prepared by: MetLife Agent 200 Park Ave. New York, NY 10166 Insurance Products: Not A Deposit Not FDIC-Insured Not Insured By Any Federal

Using Legacy Advantage SUL Insurance Policy Supplemental Illustration Prepared by: MetLife Agent 200 Park Ave. New York, NY 10166 Insurance Products: Not A Deposit Not FDIC-Insured Not Insured By Any Federal

HOW A LONG TERM CARE INSURANCE TRUST CAN INCREASE THE VALUE OF ONE S ESTATE

HOW A LONG TERM CARE INSURANCE TRUST CAN INCREASE THE VALUE OF ONE S ESTATE By Anthony C. Stratidis CLTC LTCP, Karen M. Mellon CLTC Achieving the top strata of net worth has its advantages and its challenges.

HOW A LONG TERM CARE INSURANCE TRUST CAN INCREASE THE VALUE OF ONE S ESTATE By Anthony C. Stratidis CLTC LTCP, Karen M. Mellon CLTC Achieving the top strata of net worth has its advantages and its challenges.

The Classic Swiss Franc Annuities

An Invitation from GONTHIER GROUP SA The Classic Swiss Franc Annuities Retirement Income You Can Count On Pierre-André Gonthier International English edition Preserving your Purchasing Power with a Swiss

An Invitation from GONTHIER GROUP SA The Classic Swiss Franc Annuities Retirement Income You Can Count On Pierre-André Gonthier International English edition Preserving your Purchasing Power with a Swiss

THE ITC BUY OUT BOND BROCHURE. www.independent-trustee.com

THE ITC BUY OUT BOND BROCHURE www.independent-trustee.com If you were the member of an occupational pension scheme, leaving or have left employment, or your pension scheme is being wound up, it is time

THE ITC BUY OUT BOND BROCHURE www.independent-trustee.com If you were the member of an occupational pension scheme, leaving or have left employment, or your pension scheme is being wound up, it is time

The Fiducia Guide to Retirement Planning

The Fiducia Guide to Retirement Planning September 2012 Fiducia Wealth Management Limited Dedham Hall Business Centre, Brook Street Colchester, Essex, CO7 6AD Fiducia Wealth Management Limited is authorised

The Fiducia Guide to Retirement Planning September 2012 Fiducia Wealth Management Limited Dedham Hall Business Centre, Brook Street Colchester, Essex, CO7 6AD Fiducia Wealth Management Limited is authorised

This document introduces the principles behind LDI, how LDI strategies work and how to decide on an appropriate approach for your pension scheme.

for professional clients only. NOT TO BE DISTRIBUTED TO RETAIL CLIENTS. An introduction TO Liability driven INVESTMENT HELPING PENSION SCHEMES ACHIEVE THEIR ULTIMATE GOAL Every defined benefit pension

for professional clients only. NOT TO BE DISTRIBUTED TO RETAIL CLIENTS. An introduction TO Liability driven INVESTMENT HELPING PENSION SCHEMES ACHIEVE THEIR ULTIMATE GOAL Every defined benefit pension

On Simulation Method of Small Life Insurance Portfolios By Shamita Dutta Gupta Department of Mathematics Pace University New York, NY 10038

On Simulation Method of Small Life Insurance Portfolios By Shamita Dutta Gupta Department of Mathematics Pace University New York, NY 10038 Abstract A new simulation method is developed for actuarial applications

On Simulation Method of Small Life Insurance Portfolios By Shamita Dutta Gupta Department of Mathematics Pace University New York, NY 10038 Abstract A new simulation method is developed for actuarial applications

ThoughtCapital. Investment Strength and Flexibility

Investment Strength and Flexibility Principal Trust SM Target Date Funds The Principal Trust SM Target Date Funds (Target Date Funds) are designed to capitalize on the growing popularity of Do-It-For-Me

Investment Strength and Flexibility Principal Trust SM Target Date Funds The Principal Trust SM Target Date Funds (Target Date Funds) are designed to capitalize on the growing popularity of Do-It-For-Me

Life Insurance Gifts: Planning Considerations

Life Insurance Gifts: Planning Considerations Gifts of life insurance are an additional option for charitable giving. While life insurance is not the answer to every financial planning and estate planning

Life Insurance Gifts: Planning Considerations Gifts of life insurance are an additional option for charitable giving. While life insurance is not the answer to every financial planning and estate planning

National Committee to Preserve Social Security and Medicare. Social Security Reform. Presented to: Commission to Save Social Security.

National Committee to Preserve Social Security and Medicare Presented to: Commission to Save Social Security Regarding Social Security Reform September 6, 2001 The Social Security system contributes to

National Committee to Preserve Social Security and Medicare Presented to: Commission to Save Social Security Regarding Social Security Reform September 6, 2001 The Social Security system contributes to

Should You Take a Lump Sum Payment from Your Pension Plan? A Trap for the Unwary! By Steve Vernon, FSA

Should You Take a Lump Sum Payment from Your Pension Plan? A Trap for the Unwary! By Steve Vernon, FSA Steve recently published Recession-Proof Your Retirement Years, which describes ten steps to survive

Should You Take a Lump Sum Payment from Your Pension Plan? A Trap for the Unwary! By Steve Vernon, FSA Steve recently published Recession-Proof Your Retirement Years, which describes ten steps to survive

10 MISTAKES PEOPLE MAKE IN RETIREMENT

10 MISTAKES PEOPLE MAKE IN RETIREMENT by Bill Elson, CFP 3705 Grand Avenue Des Moines, IA 50312 (515) 255-3306 or (800) 616-4392 belson@vsrfin.com KEYWORDS: RETIREMENT PLANNING, RETIREMENT INCOME, RETIREMENT

10 MISTAKES PEOPLE MAKE IN RETIREMENT by Bill Elson, CFP 3705 Grand Avenue Des Moines, IA 50312 (515) 255-3306 or (800) 616-4392 belson@vsrfin.com KEYWORDS: RETIREMENT PLANNING, RETIREMENT INCOME, RETIREMENT

Total Asset, Life Cycle, Wealth Management

Total Asset, Life Cycle, Wealth Management Total Asset, Life Cycle, Wealth Management is the management of total financial needs and total financial assets over an individual s lifetime. All financial

Total Asset, Life Cycle, Wealth Management Total Asset, Life Cycle, Wealth Management is the management of total financial needs and total financial assets over an individual s lifetime. All financial

Report for Charles & Jennifer [CS7] (prepared in August 2012 in tax year ending 05-April-2013)

![Report for Charles & Jennifer [CS7] (prepared in August 2012 in tax year ending 05-April-2013)](/thumbs/25/4701127.jpg "Report for Charles & Jennifer [CS7] (prepared in August 2012 in tax year ending 05-April-2013)") Report for Charles & Jennifer [CS7] (prepared in August 2012 in tax year ending 05-April-2013) Objectives Jennifer has recently inherited 50,000 and you would like advice on how to use this to meet the

Report for Charles & Jennifer [CS7] (prepared in August 2012 in tax year ending 05-April-2013) Objectives Jennifer has recently inherited 50,000 and you would like advice on how to use this to meet the

Estate Maximization THE USE OF INSURANCE

Estate Maximization Estate maximization is just what the name implies, the process of maximizing the estate that will be passed on to your heirs. You should first determine if maximizing your estate is

Estate Maximization Estate maximization is just what the name implies, the process of maximizing the estate that will be passed on to your heirs. You should first determine if maximizing your estate is

Your Guide To. Planned Giving. An Overview Of 6 Types of Charitable Planned Gifts

Your Guide To Planned Giving An Overview Of 6 Types of Charitable Planned Gifts Interesting Ideas in Estate Planning 2 Welcome Are you looking for ways to save on your taxes this year through charitable

Your Guide To Planned Giving An Overview Of 6 Types of Charitable Planned Gifts Interesting Ideas in Estate Planning 2 Welcome Are you looking for ways to save on your taxes this year through charitable

TOUCHSTONE FINANCIAL PLANNING OBSERVATIONS & INDUSTRY NEWS

Featuring: Michael A. Dubis, CFP, President Date: November 2004 Happy Election Day! What a day to send out my newsletter. Hopefully this will get to you before the exit polls do so you can actually read

Featuring: Michael A. Dubis, CFP, President Date: November 2004 Happy Election Day! What a day to send out my newsletter. Hopefully this will get to you before the exit polls do so you can actually read

retirement income solutions *Advisor Design guide for Life s brighter under the sun What s inside Retirement income solutions advisor guide USE ONLY

Retirement income solutions advisor guide *Advisor USE ONLY Design guide for retirement income solutions What s inside Discussing retirement needs with clients Retirement income product comparison Creating

Retirement income solutions advisor guide *Advisor USE ONLY Design guide for retirement income solutions What s inside Discussing retirement needs with clients Retirement income product comparison Creating

Is Your Financial Plan Worth the Paper It s Printed On?

T e c h n o l o g y & P l a n n i n g Is Your Financial Plan Worth the Paper It s Printed On? By Patrick Sullivan and Dr. David Lazenby, PhD www.scenarionow.com 2002-2005 ScenarioNow Inc. All Rights Reserved.

T e c h n o l o g y & P l a n n i n g Is Your Financial Plan Worth the Paper It s Printed On? By Patrick Sullivan and Dr. David Lazenby, PhD www.scenarionow.com 2002-2005 ScenarioNow Inc. All Rights Reserved.

Withdrawal Strategies to Make Your Nest Egg Last Longer

Withdrawal Strategies to Make Your Nest Egg Last Longer Ibbotson Associates/IFID Centre Retirement Income Products Executive Symposium William Reichenstein, PhD, CFA Baylor University 1 Presentation based

Withdrawal Strategies to Make Your Nest Egg Last Longer Ibbotson Associates/IFID Centre Retirement Income Products Executive Symposium William Reichenstein, PhD, CFA Baylor University 1 Presentation based

Chaper 3 -- Analyzing Suitability

Chaper 3 -- Analyzing Suitability Multiple Choice Identify the choice that best completes the statement or answers the question. When you have answered all of the questions, click the Check Your Work button

Chaper 3 -- Analyzing Suitability Multiple Choice Identify the choice that best completes the statement or answers the question. When you have answered all of the questions, click the Check Your Work button

Preserving, protecting and expanding your wealth with a holistic integrated wealth planning strategy.

Preserving, protecting and expanding your wealth with a holistic integrated wealth planning strategy. Small & Medium-Size Enterprise Conference INNOVATION BEYOND FINANCE DeGroote School of Business, Burlington,

Preserving, protecting and expanding your wealth with a holistic integrated wealth planning strategy. Small & Medium-Size Enterprise Conference INNOVATION BEYOND FINANCE DeGroote School of Business, Burlington,

IncomeSource. Issuers: Integrity Life Insurance Company National Integrity Life Insurance Company. Single Premium Immediate Annuity

IncomeSource Single Premium Immediate Annuity RISK MANAGEMENT FINANCIAL SOLUTIONS Issuers: Integrity Life Insurance Company National Integrity Life Insurance Company CF-10-29000-1209 Create Retirement

IncomeSource Single Premium Immediate Annuity RISK MANAGEMENT FINANCIAL SOLUTIONS Issuers: Integrity Life Insurance Company National Integrity Life Insurance Company CF-10-29000-1209 Create Retirement

Are Defined Benefit Funds still Beneficial?

Are Defined Benefit Funds still Beneficial? Prepared by Greg Einfeld Presented to the Actuaries Institute Financial Services Forum 30 April 1 May 2012 Melbourne This paper has been prepared for Actuaries

Are Defined Benefit Funds still Beneficial? Prepared by Greg Einfeld Presented to the Actuaries Institute Financial Services Forum 30 April 1 May 2012 Melbourne This paper has been prepared for Actuaries

Our managed funds products are issued by

Our managed funds products are issued by 1 According to the Investment and Financial Services Association 1, Australia s first managed funds were introduced in 1954. Since then the industry has grown substantially

Our managed funds products are issued by 1 According to the Investment and Financial Services Association 1, Australia s first managed funds were introduced in 1954. Since then the industry has grown substantially

SPRINGWATER C APITAL

SPRINGWATER C APITAL RETHINK REVERSE increase portfolio longevity with a reverse mortgage LEARN HOW UTILIZING HOME EQUITY CAN BETTER YOUR CLIENT S FINANCIAL POSITION BY: Eliminating monthly mortgage payments

SPRINGWATER C APITAL RETHINK REVERSE increase portfolio longevity with a reverse mortgage LEARN HOW UTILIZING HOME EQUITY CAN BETTER YOUR CLIENT S FINANCIAL POSITION BY: Eliminating monthly mortgage payments

Federal Income Taxes and Investment Strategy

Federal Income Taxes and Investment Strategy By Sholom Feldblum, FCAS, FSA, MAAA June 2007 CAS Study Note EXAM 7 STUDY NOTE: FEDERAL INCOME TAXES AND INVESTMENT STRATEGY This reading explains tax influences

Federal Income Taxes and Investment Strategy By Sholom Feldblum, FCAS, FSA, MAAA June 2007 CAS Study Note EXAM 7 STUDY NOTE: FEDERAL INCOME TAXES AND INVESTMENT STRATEGY This reading explains tax influences

Predictive Modeling. Age. Sex. Y.o.B. Expected mortality. Model. Married Amount. etc. SOA/CAS Spring Meeting

watsonwyatt.com SOA/CAS Spring Meeting Application of Predictive Modeling in Life Insurance Jean-Felix Huet, ASA June 18, 28 Predictive Modeling Statistical model that relates an event (death) with a number

watsonwyatt.com SOA/CAS Spring Meeting Application of Predictive Modeling in Life Insurance Jean-Felix Huet, ASA June 18, 28 Predictive Modeling Statistical model that relates an event (death) with a number

How To Buy A Structured Settlement

Structured Settlements: A Buyer s Guide for Investors Learn more about court ordered structured settlement transfers, why they are viewed as safe investments, and how they can help you reach your financial

Structured Settlements: A Buyer s Guide for Investors Learn more about court ordered structured settlement transfers, why they are viewed as safe investments, and how they can help you reach your financial

WITH-PROFIT ANNUITIES

WITH-PROFIT ANNUITIES BONUS DECLARATION 2014 Contents 1. INTRODUCTION 3 2. SUMMARY OF BONUS DECLARATION 3 3. ECONOMIC OVERVIEW 5 4. WITH-PROFIT ANNUITY OVERVIEW 7 5. INVESTMENTS 9 6. EXPECTED LONG-TERM

WITH-PROFIT ANNUITIES BONUS DECLARATION 2014 Contents 1. INTRODUCTION 3 2. SUMMARY OF BONUS DECLARATION 3 3. ECONOMIC OVERVIEW 5 4. WITH-PROFIT ANNUITY OVERVIEW 7 5. INVESTMENTS 9 6. EXPECTED LONG-TERM

ability to accumulate retirement resources while increasing their retirement needs; and

Consulting Retirement Consulting Talent & Rewards The Real Deal 2012 Retirement Income Adequacy at Large Companies RETIREMENT YOU ARE HERE About This Report This study assesses whether employees of large

Consulting Retirement Consulting Talent & Rewards The Real Deal 2012 Retirement Income Adequacy at Large Companies RETIREMENT YOU ARE HERE About This Report This study assesses whether employees of large

Solutions for the New Retirement Reality

Solutions for the New Retirement Reality Fernando Suarez CFP, CLU, ChFC Managing Director - Wealth Management Advisor May 8 th, 2012 29-5184-02 (10-11) Disclosure The Northwestern Mutual Life Insurance

Solutions for the New Retirement Reality Fernando Suarez CFP, CLU, ChFC Managing Director - Wealth Management Advisor May 8 th, 2012 29-5184-02 (10-11) Disclosure The Northwestern Mutual Life Insurance

Gifts of Life Insurance

Gifts of Life Insurance Effective Ways to Make Them If you have a desire to make a major contribution to support our good works, life insurance can be an excellent tool for helping you accomplish your

Gifts of Life Insurance Effective Ways to Make Them If you have a desire to make a major contribution to support our good works, life insurance can be an excellent tool for helping you accomplish your

RE 7: Second Level Regulatory Examination: Long Term Insurance Category B, Long Term Insurance Category C And Retail Pension Funds

COMPLIANCE MONITORING SYSTEMS CC RE 7: Second Level Regulatory Examination: Long Term Insurance Category B, Long Term Insurance Category C And Retail Pension Funds Alan Holton December 2009 All representatives

COMPLIANCE MONITORING SYSTEMS CC RE 7: Second Level Regulatory Examination: Long Term Insurance Category B, Long Term Insurance Category C And Retail Pension Funds Alan Holton December 2009 All representatives

It s Time to Save for Retirement. The Benefit of Saving Early and the Cost of Delay

It s Time to Save for Retirement The Benefit of Saving Early and the Cost of Delay November 2014 About the Insured Retirement Institute: The Insured Retirement Institute (IRI) is the leading association

It s Time to Save for Retirement The Benefit of Saving Early and the Cost of Delay November 2014 About the Insured Retirement Institute: The Insured Retirement Institute (IRI) is the leading association

Personal Financial Plan. John and Mary Sample

For January 1, 2014 Prepared by Allen Adviser 2430 NW Professional Dr. Corvallis, OR 97330 541.754.3701 Twelve lines of custom report cover text can be entered. This presentation provides a general overview

For January 1, 2014 Prepared by Allen Adviser 2430 NW Professional Dr. Corvallis, OR 97330 541.754.3701 Twelve lines of custom report cover text can be entered. This presentation provides a general overview

8th Bowles Symposium and 2nd International Longevity Risk and Capital Market Solutions Symposium

8th Bowles Symposium and 2nd International Longevity Risk and Capital Market Solutions Symposium Annuitization lessons from the UK Money-Back annuities and other developments Tom Boardman UK Policy Development

8th Bowles Symposium and 2nd International Longevity Risk and Capital Market Solutions Symposium Annuitization lessons from the UK Money-Back annuities and other developments Tom Boardman UK Policy Development

Collectibles, such as art, antiques and classic cars

feature: estate planning & taxation By K. Eli Akhavan Brushstrokes of Art Planning A primer on tax strategies Collectibles, such as art, antiques and classic cars often have significant emotional and economic

feature: estate planning & taxation By K. Eli Akhavan Brushstrokes of Art Planning A primer on tax strategies Collectibles, such as art, antiques and classic cars often have significant emotional and economic

Joseph A. Tomlinson, FSA, CFP Tomlinson Financial Planning, LLC PO Box 1349, Greenville, ME 04441 1349 207 333 7600 joetmail@aol.

Joseph A. Tomlinson, FSA, CFP Tomlinson Financial Planning, LLC PO Box 1349, Greenville, ME 04441 1349 207 333 7600 joetmail@aol.com April 22, 2010 To: Employee Benefits Security Administration, Department

Joseph A. Tomlinson, FSA, CFP Tomlinson Financial Planning, LLC PO Box 1349, Greenville, ME 04441 1349 207 333 7600 joetmail@aol.com April 22, 2010 To: Employee Benefits Security Administration, Department

Understanding annuities

ab Wealth Management Americas Understanding annuities Rethinking the role they play in retirement income planning Protecting your retirement income security from life s uncertainties. The retirement landscape

ab Wealth Management Americas Understanding annuities Rethinking the role they play in retirement income planning Protecting your retirement income security from life s uncertainties. The retirement landscape

MPP Decision Guide 15 01. MPP Dairy Financial Stress test Calculator: A User s Guide

MPP Decision Guide 15 01 MPP Dairy Financial Stress test Calculator: A User s Guide Christopher Wolf and Marin Bozic Michigan State University and the University of Minnesota A financial stress test calculator

MPP Decision Guide 15 01 MPP Dairy Financial Stress test Calculator: A User s Guide Christopher Wolf and Marin Bozic Michigan State University and the University of Minnesota A financial stress test calculator

READING 14: LIFETIME FINANCIAL ADVICE: HUMAN CAPITAL, ASSET ALLOCATION, AND INSURANCE

READING 14: LIFETIME FINANCIAL ADVICE: HUMAN CAPITAL, ASSET ALLOCATION, AND INSURANCE Introduction (optional) The education and skills that we build over this first stage of our lives not only determine

READING 14: LIFETIME FINANCIAL ADVICE: HUMAN CAPITAL, ASSET ALLOCATION, AND INSURANCE Introduction (optional) The education and skills that we build over this first stage of our lives not only determine

Session # R1 The Use of Life Annuities in an Optimal Retirement Portfolio

Investment Symposium March 13-14, 2014 New York, NY Session # R1 The Use of Life Annuities in an Optimal Retirement Portfolio Moderators Martin Belanger, FSA, FCIA Brett Dutton, FSA, MAAA, EA Presenter

Investment Symposium March 13-14, 2014 New York, NY Session # R1 The Use of Life Annuities in an Optimal Retirement Portfolio Moderators Martin Belanger, FSA, FCIA Brett Dutton, FSA, MAAA, EA Presenter

Managing Life Insurer Risk and Profitability: Annuity Market Development using Natural Hedging Strategies

Managing Life Insurer Risk and Profitability: Annuity Market Development using Natural Hedging Strategies 1st CEPAR International Conference Analysing Population Ageing: Multidisciplinary perspectives

Managing Life Insurer Risk and Profitability: Annuity Market Development using Natural Hedging Strategies 1st CEPAR International Conference Analysing Population Ageing: Multidisciplinary perspectives

Case Study. Retirement Planning Needs are Evolving

Case Study Retirement Planning Based on Stochastic Financial Analysis Fiserv Helps Investment Professionals Improve Their Retirement Planning Practices Many personal financial planning solutions rely on

Case Study Retirement Planning Based on Stochastic Financial Analysis Fiserv Helps Investment Professionals Improve Their Retirement Planning Practices Many personal financial planning solutions rely on

ENDOWMENT GIVING ESSENTIALS

ENDOWMENT GIVING ESSENTIALS Long Beach, CA 8 November 2014 Don Hill Don Hill Consulting Lynne Hansen United Church Funds Our Mission Our mission Invest responsibly. Strengthen ministry. United Church Funds

ENDOWMENT GIVING ESSENTIALS Long Beach, CA 8 November 2014 Don Hill Don Hill Consulting Lynne Hansen United Church Funds Our Mission Our mission Invest responsibly. Strengthen ministry. United Church Funds