Accounting and. Business Services for Amoco Dealers. Your Logo Here (800)

|

|

|

- Jeffery Clark

- 8 years ago

- Views:

Transcription

1 Accounting and Your Logo Here Business Services for Amoco Dealers Franchise Franchise Business Business Systems Systems offers offers a a complete complete package package of of services services and and support support for for Amoco Amoco Dealers. Dealers. To To assist assist new new Dealers Dealers in in getting getting their their business business off off to to a a proper proper start start our our program program expands expands on on and and reinforces reinforces the the lessons lessons they they learn learn in in new new dealer dealer training. training. (800)

2 Services Offered! Monthly Accounting Service! Payroll Service! Tax Preparation & Planning! Business Plan Development! Pre Purchase Evaluation! Buyer Due Diligence Reviews! Retail Inventory Set-up! Merchandising Assistance! Incentive Plan Development! Audit Representation

3 Monthly Accounting Service Reports! Profit & Loss Statement! Balance Sheet! Departmental Sales, Cost of Sales & Gross Margin Report! Departmental Shrinkage Report! Gasoline Sales Graph! Gross Profit By Department Graph! W.A.M. ( Pool Margin) Report! Bank Reconciliation! Reconciliation of Daily Books & Daily Sales Analysis Report! Reconciliation of Accounts Payable, Accounts Receivable & Petty Cash! Complete Transaction Detail Reporting! Sales Tax Preparation! Quarterly Payroll Tax Returns

4 Monthly Accounting Service Also Includes! Free Custom Daily Books (Paper Books)! Free Daily Book Software & Support! Training on Completion of Daily Books! Training & Support for Retail Inventory System! Assistance With M.I.R. & D.I.R. When Necessary! Programming Ruby For Categories & Departments! Support For All Sales Tax Questions! Support For All Payroll Tax & Personnel Questions! Business Tax Planning! Assistance With Financing & Bank Paperwork! 1 Hour per Month Business Consulting Our basic monthly accounting standard fee is $ per month and covers the complete monthly accounting service. Amoco Dealers receive a 15% discount off our standard fee when referred by an S.O.M. To receive the discount, billing must be handled by EFT.

5 Monthly Accounting Service Setup There is a one time setup fee for all new Amoco monthly accounting service clients of $ This fee covers the following services.! Assistance with Amoco business plan! Pre closing meetings or telephone consultations! Review of purchase and asset allocations! Attendance at and assistance with closing! Conversion of retail inventory to cost for purchase! Programming of Ruby categories and reports! Initial training on daily books! Setup of accounting system

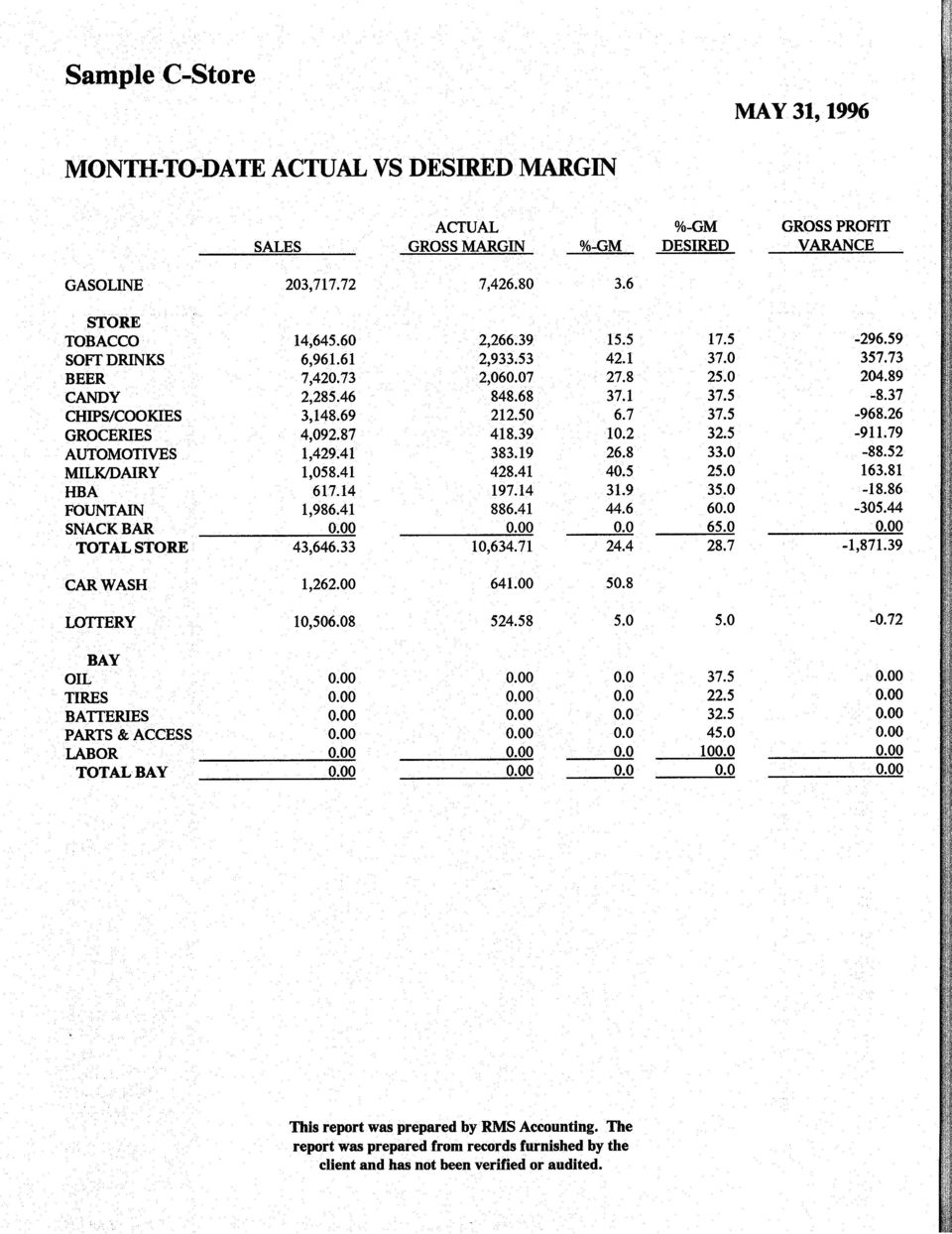

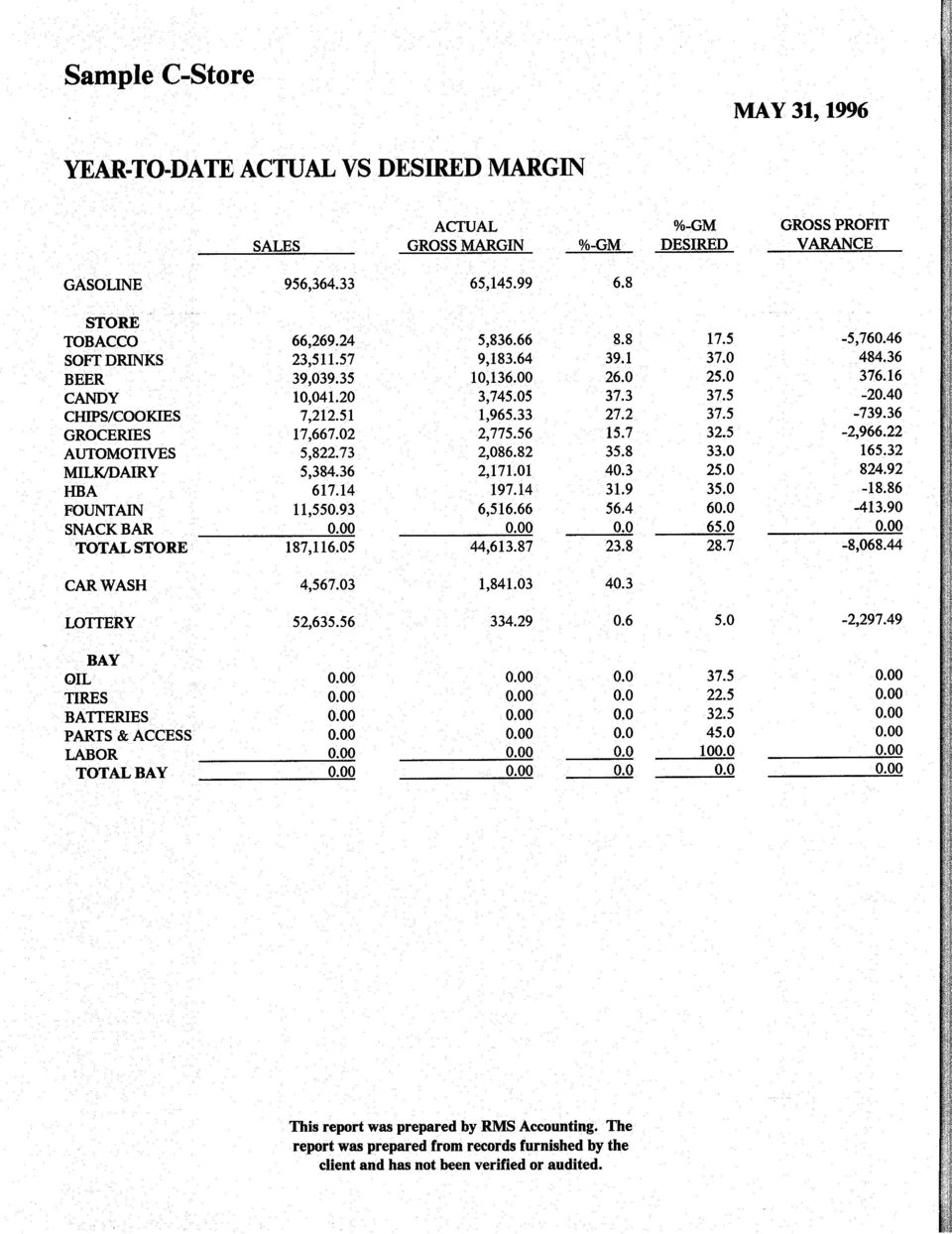

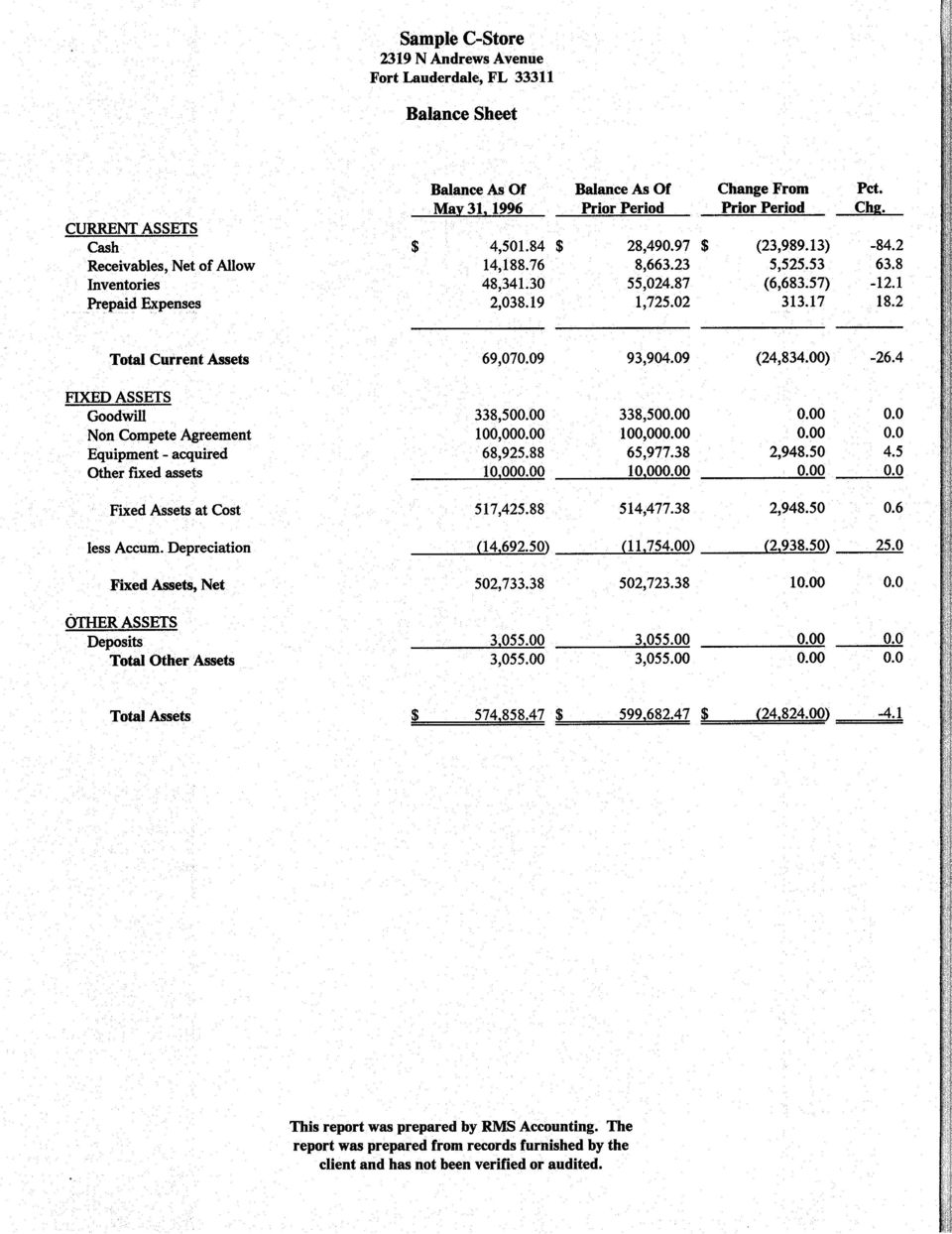

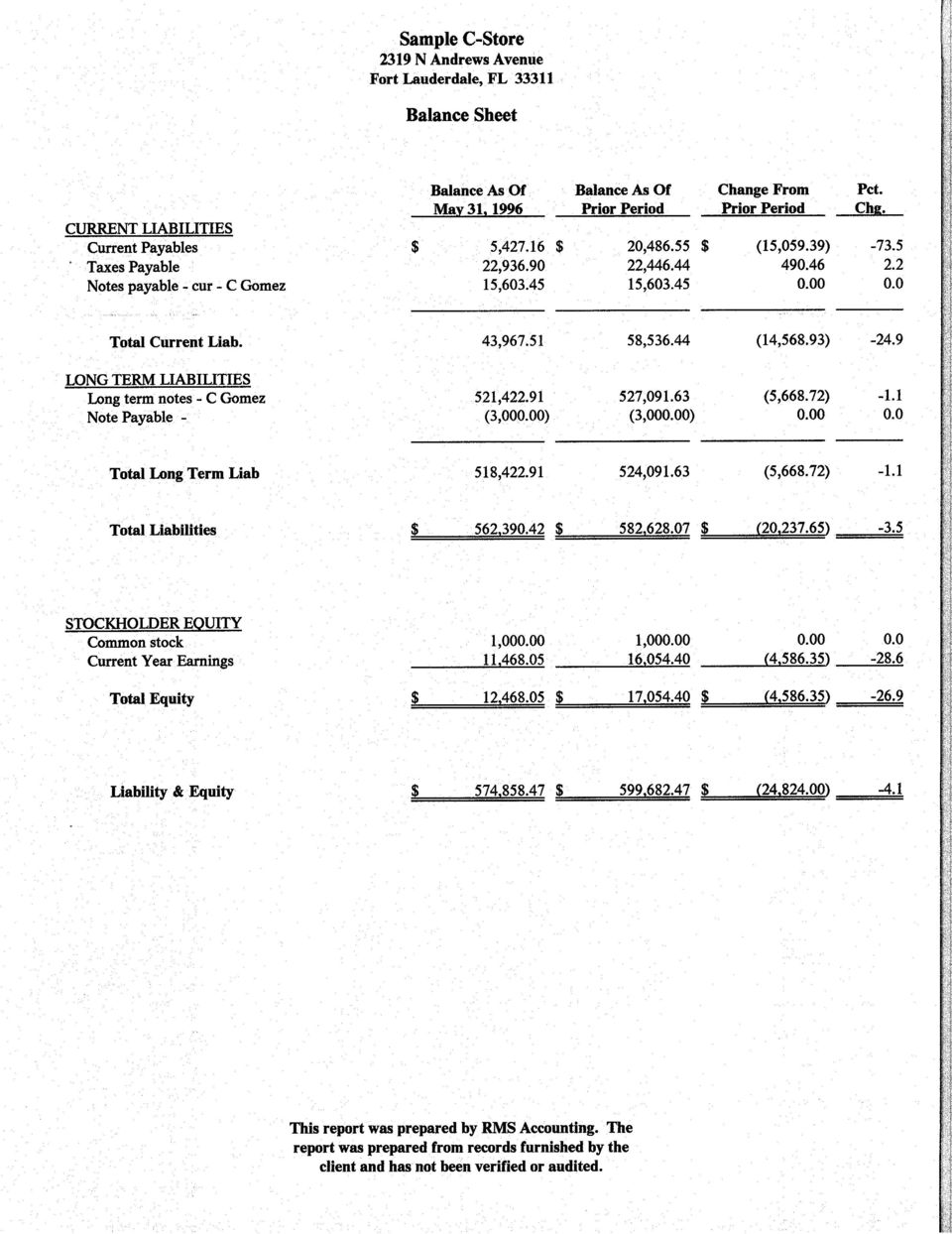

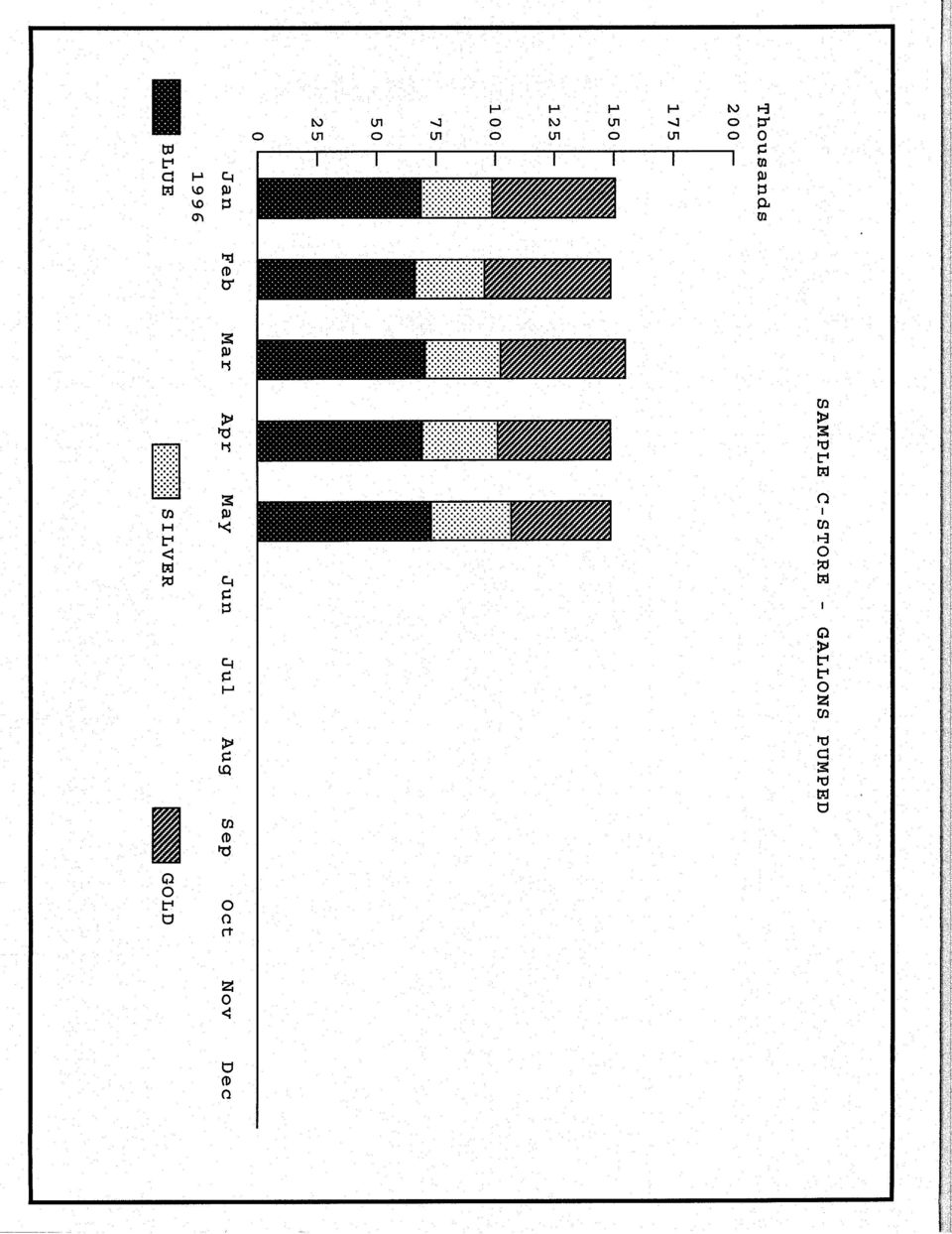

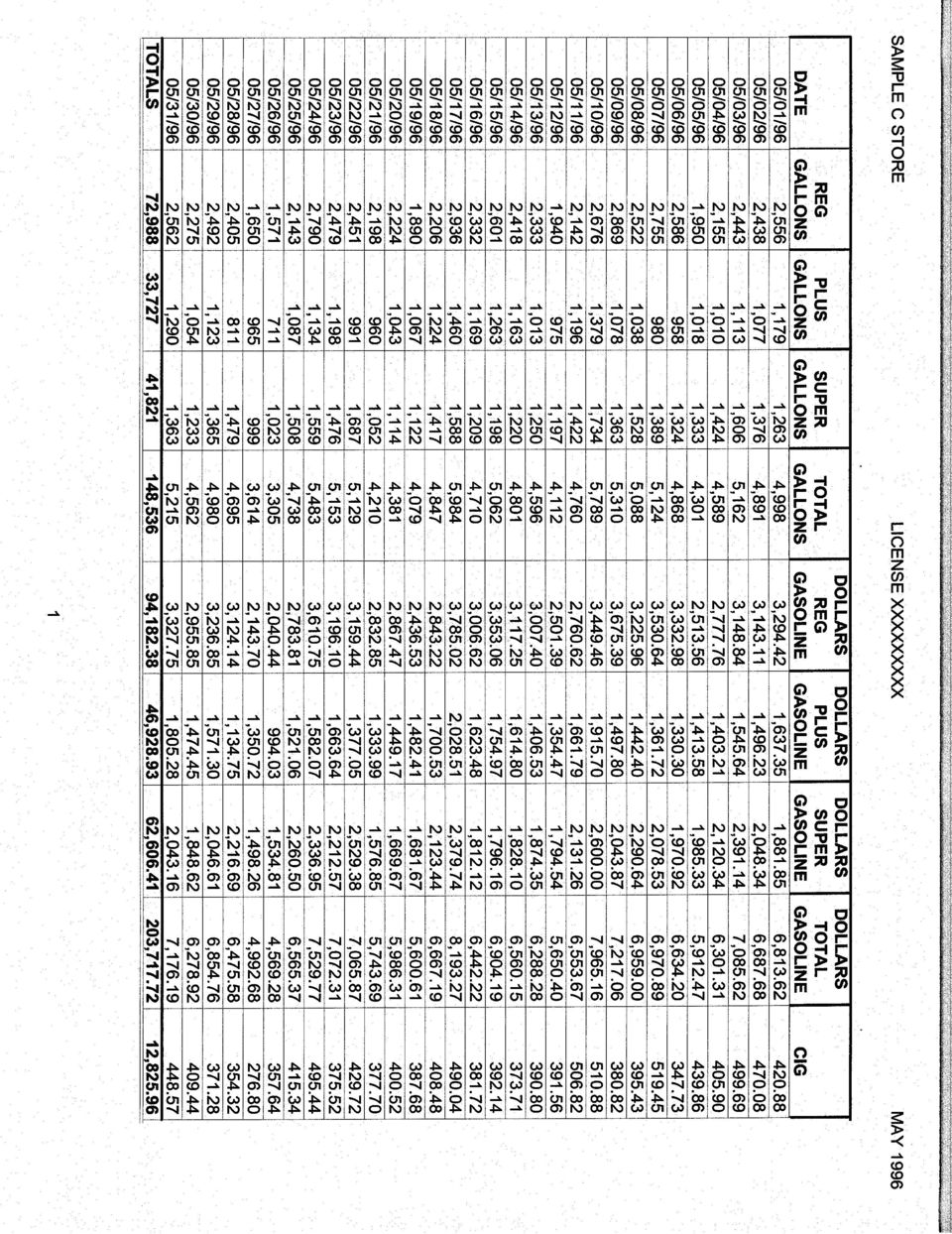

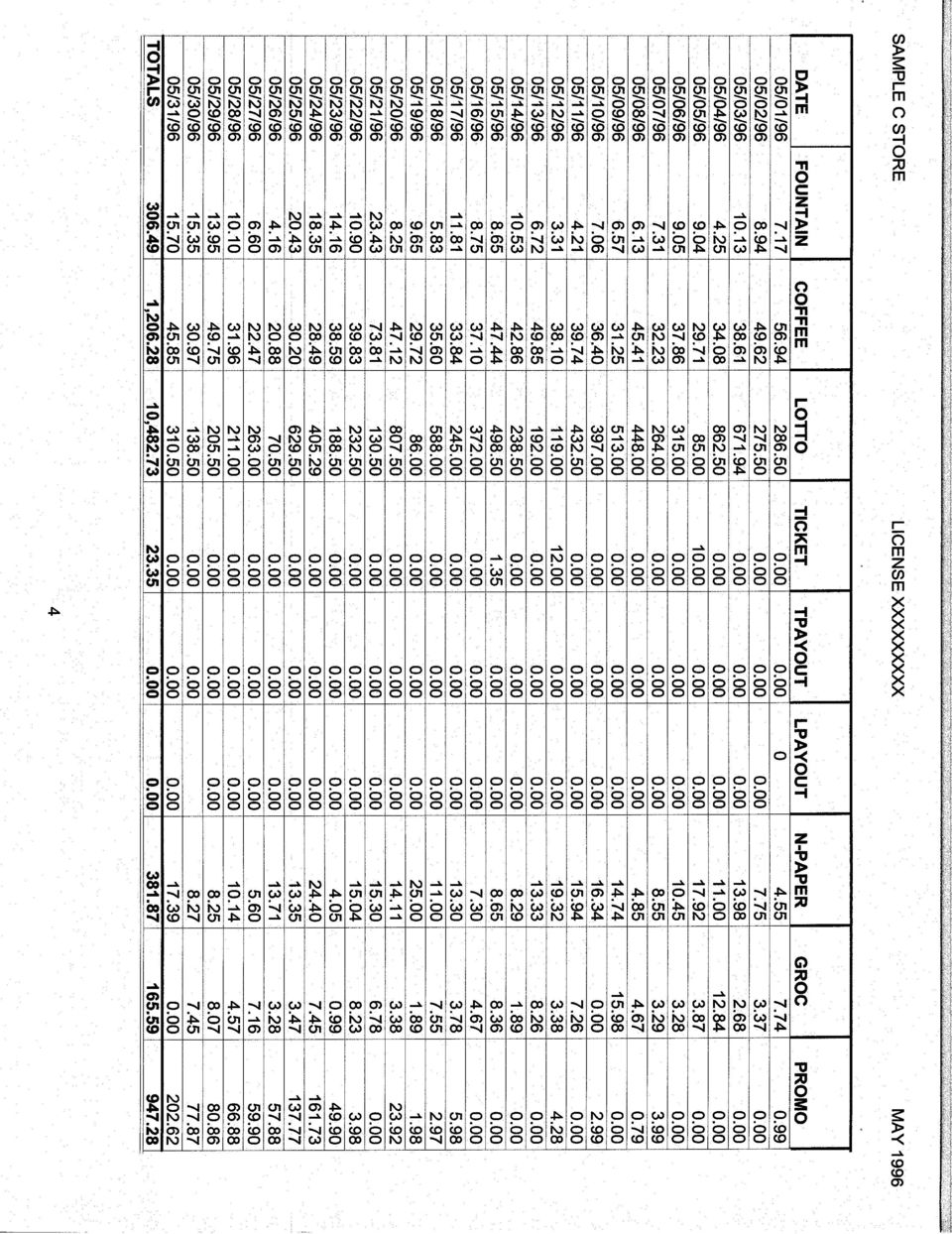

6 Sample Financial Statements For Retail Petroleum Dealers

7

8

9

10

11

12

13

14

15

16 Sample Daily Books Recap For Retail Petroleum Dealers

17

18

19

20

21

22

23

24 Payroll Services! Free set-up! Free checks! Free basic maintenance! Free new employee set-up! Free rehires! Free departmentalization! Fast payroll turnaround! We handle all payroll tax deposits! Personal service! Direct Deposit Available! Ready-to-sign Quarterly Tax Returns! We prepare reconciled W-2 s

25 Payroll Service Fees Number of Fee per Pay Period Employees Weekly Bi-Weekly Monthly Custom quotes available for 21 or more Fee of $5.00 per W-2 (minimum $10.00) at year end. Delivery/Postage at Cost

26 Tax Services! Our tax department provides complete tax preparation, tax planning, and audit representation services.! Because we specialize in helping retail petroleum, we keep up on all the latest tax matters that affect their business. We know what the IRS is looking for when they audit retail petroleum dealers, so we can help them avoid the tax traps that exist in their industry! We can help dealers comply with the complex sales tax rules for C-Store and Bay Operators.! Our year round tax planning, will help make sure you pay the lowest tax the law allows.! We can help you take advantage of the new Work Opportunity Tax Credit.

27 Sample Business Plan For Dealer School

28

29

30 New Dealer Setup Outline First Meeting or Consultation Prospective Dealer Consultation 1) Review accounting needs and services available 2) Review choice of business entity 3) Supply prospective dealer with industry standards 4) Review areas of due dilligence Second Meeting or Consultation Dealer Approved By Amoco (Pre dealer school) 1) Complete accounting services agreement 2) Assist with completion of Amoco business plan 3) Assist with due diligence as requested Pre Closing Meeting or Consultation 1) Complete sales tax application 2) Complete application for temporary alcohol and tobacco license 3) Complete DBA paperwork 4) Setup payroll service & payroll information

31 New Dealer Setup Outline At Closing 1) Assist with inventory calculations 2) Program Ruby categories and reports 3) Provide shift report forms 4) Provide payroll setup for new employees 5) Review store layout and procedures with new dealer. 5 Days After Closing 1) Train new dealer on completion of daily books 2) Assist as necessary with accounting and accounting procedures 3) Obtain copies of closing statements and purchase documents 7-10 Days After End of First Month 1) Contact new dealer for monthly work 15th-19th Day After Month End 1) Sales tax sent to dealer After End Month Work Received 1) Financial statements sent to dealer

32 Closing Check List 10 Days Before Closing Review sellers sales tax records for successor liabilities Arrange for closing inventory to be taken Apply for sales tax number Apply for alcohol and tobacco licenses Obtain copies of sellers commercial personal property tax returns Apply for DBA as Amoco Set allocation of purchase price for assets, goodwill and non-compete with seller Arrange for transfer of existing phone number with seller 1 Day Before Closing Transfer funds for closing to your attorney s trust account (any excess funds will be returned at closing) Purchase change bank for opening Be sure transfer letters will be provided for pay phones, and other vending income sources Day of Closing Check inventory to be purchased for out of date items or items that are not in sellable condition

Accounting and Business Services for Alphagraphics

Accounting and Business Services for Alphagraphics Franchise Franchise Business Business Services, Services, Inc. Inc. Offers Offers a a Complete Complete Package Package of of Services Services and and

Accounting and Business Services for Alphagraphics Franchise Franchise Business Business Services, Services, Inc. Inc. Offers Offers a a Complete Complete Package Package of of Services Services and and

Accounting and Business Services for Planet Smoothie

Accounting and Business Services for Planet Smoothie Franchise Franchise Business Business Systems Systems Offers Offers a a Complete Complete Package Package of of Services Services and and Support Support

Accounting and Business Services for Planet Smoothie Franchise Franchise Business Business Systems Systems Offers Offers a a Complete Complete Package Package of of Services Services and and Support Support

MOUNTAIN VIEW SCHOOL DISTRICT

MOUNTAIN VIEW SCHOOL DISTRICT COMPUTERIZED ACCOUNTING I Curriculum Content Frameworks 0 Curriculum Content Frameworks COMPUTERIZED ACCOUNTING I Grade Levels: 0,, Course Code: 900 Prerequisite: Tech Prep

MOUNTAIN VIEW SCHOOL DISTRICT COMPUTERIZED ACCOUNTING I Curriculum Content Frameworks 0 Curriculum Content Frameworks COMPUTERIZED ACCOUNTING I Grade Levels: 0,, Course Code: 900 Prerequisite: Tech Prep

Chapter 5. Accounting for merchandising operations. Appendix 5A: Periodic inventory system

1 Chapter 5 Accounting for merchandising operations Appendix 5A: Periodic inventory system 2 Learning objectives 1. Record purchase and sales transactions under the periodic inventory system 2. Prepare

1 Chapter 5 Accounting for merchandising operations Appendix 5A: Periodic inventory system 2 Learning objectives 1. Record purchase and sales transactions under the periodic inventory system 2. Prepare

JOB READY ASSESSMENT BLUEPRINT ACCOUNTING-BASIC - PILOT. Test Code: 4100 Version: 01

JOB READY ASSESSMENT BLUEPRINT ACCOUNTING-BASIC - PILOT Test Code: 4100 Version: 01 Specific Competencies and Skills Tested in this Assessment: Journalizing Apply the accounting equation to journalize

JOB READY ASSESSMENT BLUEPRINT ACCOUNTING-BASIC - PILOT Test Code: 4100 Version: 01 Specific Competencies and Skills Tested in this Assessment: Journalizing Apply the accounting equation to journalize

Job Ready Assessment Blueprint. Accounting-Advanced. Test Code: 3900 / Version: 01

Job Ready Assessment Blueprint Accounting-Advanced Test Code: 3900 / Version: 01 Measuring What Matters Specific Competencies and Skills Tested in this Assessment: Journalizing Journalize an opening entry

Job Ready Assessment Blueprint Accounting-Advanced Test Code: 3900 / Version: 01 Measuring What Matters Specific Competencies and Skills Tested in this Assessment: Journalizing Journalize an opening entry

M-48A Franchise Financial Summary

Overview These guidelines have been designed to help you understand the information contained in the Franchise Income / (Expense) Statement. It is comprised of the following reports: 1) Financial Summary

Overview These guidelines have been designed to help you understand the information contained in the Franchise Income / (Expense) Statement. It is comprised of the following reports: 1) Financial Summary

Self-test Comprehensive Problems II 综 合 自 测 题 II

Self-test Comprehensive Problems II 综 合 自 测 题 II Part One (30%) 1. Give the Chinese/English of the following terms: (5%) subsidiary ledger 统 制 账 户 purchase requisition 现 金 溢 缺 petty cash fund 永 续 盘 存 制

Self-test Comprehensive Problems II 综 合 自 测 题 II Part One (30%) 1. Give the Chinese/English of the following terms: (5%) subsidiary ledger 统 制 账 户 purchase requisition 现 金 溢 缺 petty cash fund 永 续 盘 存 制

COMPUTERIZED ACCOUNTING I Curriculum Content Frameworks

COMPUTERIZED ACCOUNTING I Curriculum Content Frameworks Please note: All assessment questions will be taken from the knowledge portion of these frameworks. Prepared by Loretta Burgess, Greenbrier High

COMPUTERIZED ACCOUNTING I Curriculum Content Frameworks Please note: All assessment questions will be taken from the knowledge portion of these frameworks. Prepared by Loretta Burgess, Greenbrier High

Accounting Notes. Purchasing Merchandise under the Perpetual Inventory system:

Systems: Perpetual VS Periodic " Keeps running record of all goods " Does not keep a running record bought and sold " is counted once a year " is counted at least once a year " Used for all types of goods

Systems: Perpetual VS Periodic " Keeps running record of all goods " Does not keep a running record bought and sold " is counted once a year " is counted at least once a year " Used for all types of goods

1. A set of procedures for controlling cash payments by preparing and approving vouchers before payments are made is known as a voucher system.

Accounting II True/False Indicate whether the sentence or statement is true or false. 1. A set of procedures for controlling cash payments by preparing and approving vouchers before payments are made is

Accounting II True/False Indicate whether the sentence or statement is true or false. 1. A set of procedures for controlling cash payments by preparing and approving vouchers before payments are made is

SOLUTIONS. Learning Goal 22 LG 22-1. LG 22-2.

S1 Learning Goal 22 Multiple Choice 1. b 2. d A purchase discount is recorded when payment is made. 3. a The payment is within the discount period, so $5,000.02 = $100. 4. b The discount is ($1,000/.98)

S1 Learning Goal 22 Multiple Choice 1. b 2. d A purchase discount is recorded when payment is made. 3. a The payment is within the discount period, so $5,000.02 = $100. 4. b The discount is ($1,000/.98)

Cash in bank checking account $22,500 U.S. treasury bills 5,000 Cash on hand 1,350 Undeposited customer checks 1,840 Total $30,690 Requirement 2

Chapter 7 Solutions EXERCISES Exercise 7 2 Cash and cash equivalents includes: Cash in bank checking account $22,500 U.S. treasury bills 5,000 Cash on hand 1,350 Undeposited customer checks 1,840 Total

Chapter 7 Solutions EXERCISES Exercise 7 2 Cash and cash equivalents includes: Cash in bank checking account $22,500 U.S. treasury bills 5,000 Cash on hand 1,350 Undeposited customer checks 1,840 Total

2. A service company earns net income by buying and selling merchandise. Ans: False

Chapter 6: Accounting For Merchandising Activities True/False 1. Merchandise consists of products that a company acquires for the purpose of reselling them to customers. 2. A service company earns net

Chapter 6: Accounting For Merchandising Activities True/False 1. Merchandise consists of products that a company acquires for the purpose of reselling them to customers. 2. A service company earns net

1. Analyze the following T-account in the ledger of Moxy Pool Supply Company

Name: Date: 1. Analyze the following T-account in the ledger of Moxy Pool Supply Company Mdse. Inventory 5,000 400 If $5,000 in the Inventory account represents merchandise purchased from a supplier, we

Name: Date: 1. Analyze the following T-account in the ledger of Moxy Pool Supply Company Mdse. Inventory 5,000 400 If $5,000 in the Inventory account represents merchandise purchased from a supplier, we

Job Ready Assessment Blueprint. Accounting-Basic. Test Code: 4000 / Version: 01. Copyright 2012. All Rights Reserved.

Job Ready Assessment Blueprint Accounting-Basic Test Code: 4000 / Version: 01 Copyright 2012. All Rights Reserved. General Assessment Information Blueprint Contents General Assessment Information Written

Job Ready Assessment Blueprint Accounting-Basic Test Code: 4000 / Version: 01 Copyright 2012. All Rights Reserved. General Assessment Information Blueprint Contents General Assessment Information Written

Accounting 303 Exam 3, Chapters 7-9 Fall 2011 Section Row

Accounting 303 Name Exam 3, Chapters 7-9 Fall 2011 Section Row I. Multiple Choice Questions. (2 points each, 34 points in total) Read each question carefully and indicate your answer by circling the letter

Accounting 303 Name Exam 3, Chapters 7-9 Fall 2011 Section Row I. Multiple Choice Questions. (2 points each, 34 points in total) Read each question carefully and indicate your answer by circling the letter

Bookkeeping Quiz = + For each account listed below, indicate whether it normally has a debit or a credit balance: III.

ookkeeping Quiz I. Match the account titles with the appropriate financial statement classification: A Current Assets Sales Property, Plant and Equipment Cash in Checking C Other Assets Accumulated Depreciation

ookkeeping Quiz I. Match the account titles with the appropriate financial statement classification: A Current Assets Sales Property, Plant and Equipment Cash in Checking C Other Assets Accumulated Depreciation

Dutchess Community College ACC 104 Financial Accounting Quiz Prep Chapter 5

Dutchess Community College ACC 104 Financial Accounting Quiz Prep Chapter 5 Merchandising Operations Peter Rivera October 2009 Disclaimer This Quiz Prep is provided as an outline of the key concepts from

Dutchess Community College ACC 104 Financial Accounting Quiz Prep Chapter 5 Merchandising Operations Peter Rivera October 2009 Disclaimer This Quiz Prep is provided as an outline of the key concepts from

Sample Test for entrance into Acct 3110 and Acct 3310

Sample Test for entrance into Acct 3110 and Acct 3310 1. Which of the following financial statements could properly have the following in the date line: For the Year Ended December 31, 2010"? a. Balance

Sample Test for entrance into Acct 3110 and Acct 3310 1. Which of the following financial statements could properly have the following in the date line: For the Year Ended December 31, 2010"? a. Balance

Chapter 04 - Accounting for Merchandising Operations. Chapter Outline

I. Merchandising Activities Products that a company acquires to resell to customers are referred to as merchandise (also called goods). A merchandiser earns net income by buying and selling merchandise.

I. Merchandising Activities Products that a company acquires to resell to customers are referred to as merchandise (also called goods). A merchandiser earns net income by buying and selling merchandise.

Broker. Owning, Managing and Supervising a Real Estate Office. Chapter 3. Copyright Gold Coast Schools 1

Broker Chapter 3 Owning, Managing and Supervising a Real Estate Office 1 Learning Objectives List at least 6 categories of costs required when establishing a brokerage office List the 3 factors a broker

Broker Chapter 3 Owning, Managing and Supervising a Real Estate Office 1 Learning Objectives List at least 6 categories of costs required when establishing a brokerage office List the 3 factors a broker

Baseline Assessment. Date Accounting 1

Name Baseline Assessment Date Accounting 1 Part 1: Instructions: Place a check mark under the column for each account to determine which Financial the accounts belongs on. Financial Information 1. Cash

Name Baseline Assessment Date Accounting 1 Part 1: Instructions: Place a check mark under the column for each account to determine which Financial the accounts belongs on. Financial Information 1. Cash

BEDFORD PUBLIC SCHOOLS BUSINESS OFFICE PROCEDURES MANUAL

BEDFORD PUBLIC SCHOOLS BUSINESS OFFICE PROCEDURES MANUAL Revised 3-27-2014 TABLE OF CONTENTS Section 1: Section 2: Section 3: Section 4: Section 5: Section 6: Section 7: Section 8: Section 9: Cash Management

BEDFORD PUBLIC SCHOOLS BUSINESS OFFICE PROCEDURES MANUAL Revised 3-27-2014 TABLE OF CONTENTS Section 1: Section 2: Section 3: Section 4: Section 5: Section 6: Section 7: Section 8: Section 9: Cash Management

FINANCIAL AND PURCHASING RECORDS. Includes records showing a summary of receipts, disbursements and other activity against each account.

FINANCIAL AND PURCHASING RECORDS FN-1 Account Distribution Summaries (Treasurer s Report) Includes records showing a summary of receipts, disbursements and other activity against each account. Weekly/Monthly-

FINANCIAL AND PURCHASING RECORDS FN-1 Account Distribution Summaries (Treasurer s Report) Includes records showing a summary of receipts, disbursements and other activity against each account. Weekly/Monthly-

CENTURY 21 ACCOUNTING, 8e General Journal Chapter Objectives

CENTURY 21 ACCOUNTING, 8e General Journal Chapter Objectives Chapter 1 Starting A Proprietorship: Changes that Affect the Accounting Equation After studying Chapter 1, you will be able to: 1. Define accounting

CENTURY 21 ACCOUNTING, 8e General Journal Chapter Objectives Chapter 1 Starting A Proprietorship: Changes that Affect the Accounting Equation After studying Chapter 1, you will be able to: 1. Define accounting

Accounting 303 Exam 3, Chapters 7-9 Fall 2013 Section Row

Accounting 303 Name Exam 3, Chapters 7-9 Fall 2013 Section Row I. Multiple Choice Questions. (2 points each, 28 points in total) Read each question carefully and indicate your answer by circling the letter

Accounting 303 Name Exam 3, Chapters 7-9 Fall 2013 Section Row I. Multiple Choice Questions. (2 points each, 28 points in total) Read each question carefully and indicate your answer by circling the letter

Accounting 303 Exam 3, Chapters 7-9 Fall 2012 Section Row

Accounting 303 Name Exam 3, Chapters 7-9 Fall 2012 Section Row I. Multiple Choice Questions. (2 points each, 34 points in total) Read each question carefully and indicate your answer by circling the letter

Accounting 303 Name Exam 3, Chapters 7-9 Fall 2012 Section Row I. Multiple Choice Questions. (2 points each, 34 points in total) Read each question carefully and indicate your answer by circling the letter

Example: Spencer Company has the following information available as of April 30, 2002.

CASH AND CASH EQUIVALENTS on hand, demand deposits and other bank accounts are considered cash. equivalents are short-term investments (90 days or less) that can be converted into cash without any significant

CASH AND CASH EQUIVALENTS on hand, demand deposits and other bank accounts are considered cash. equivalents are short-term investments (90 days or less) that can be converted into cash without any significant

Merchandise Accounts. Chapter 7 - Unit 14

Merchandise Accounts Chapter 7 - Unit 14 Merchandising... Merchandising... There are many types of companies out there Merchandising... There are many types of companies out there Service company - sells

Merchandise Accounts Chapter 7 - Unit 14 Merchandising... Merchandising... There are many types of companies out there Merchandising... There are many types of companies out there Service company - sells

EXPENSE CONTROL A Profit Enhancing Opportunity

EXPENSE CONTROL A Profit Enhancing Opportunity General: Do you have a budget for all expenses? Do you review each expense category monthly? Do you know precisely what % of sales goes to expenses? Do you

EXPENSE CONTROL A Profit Enhancing Opportunity General: Do you have a budget for all expenses? Do you review each expense category monthly? Do you know precisely what % of sales goes to expenses? Do you

BUSINESS BOOKS. Accounting SIXTH EDITION. Peter J. Eisen Assistant Principal Retired Accounting & Business Practice N.YC. Department of Education

BUSINESS BOOKS Accounting SIXTH EDITION Peter J. Eisen Assistant Principal Retired Accounting & Business Practice N.YC. Department of Education BARRON'S CONTENTS Preface ix 1 THE ACCOUNTING EQUATION I

BUSINESS BOOKS Accounting SIXTH EDITION Peter J. Eisen Assistant Principal Retired Accounting & Business Practice N.YC. Department of Education BARRON'S CONTENTS Preface ix 1 THE ACCOUNTING EQUATION I

In the event of a tie, the score on the last ten questions will be used as a tie-breaker.

NEW YORK STATE ASSOCIATION FUTURE BUSINESS LEADERS OF AMERICA SPRING DISTRICT MEETING ACCOUNTING I 2010 TEST DIRECTIONS 1. Complete the information requested on the answer sheet. PRINT your name on the

NEW YORK STATE ASSOCIATION FUTURE BUSINESS LEADERS OF AMERICA SPRING DISTRICT MEETING ACCOUNTING I 2010 TEST DIRECTIONS 1. Complete the information requested on the answer sheet. PRINT your name on the

2012-2016 Business Plan Summary

Owner: 2012-2016 Business Plan Summary Program Corporate, Operational & Council Services Service grouping Corporate Services Service Type Internal Service Julie Kovacs, Manager Systems and Development,

Owner: 2012-2016 Business Plan Summary Program Corporate, Operational & Council Services Service grouping Corporate Services Service Type Internal Service Julie Kovacs, Manager Systems and Development,

CONTENTS 1.1 Information Needed 1.2 Other Considerations 1.3 Specific Businesses 1.4 Franchises

1.0 BUSINESS PURCHASE OR SALE CONTENTS 1.1 Information Needed 1.2 Other Considerations 1.3 Specific Businesses 1.4 Franchises 1.1 Checklist Of Information Needed In Evaluation (Due Diligence): Profit and

1.0 BUSINESS PURCHASE OR SALE CONTENTS 1.1 Information Needed 1.2 Other Considerations 1.3 Specific Businesses 1.4 Franchises 1.1 Checklist Of Information Needed In Evaluation (Due Diligence): Profit and

FINANCIAL POLICIES INDEX

FINANCIAL POLICIES INDEX Page Accounts Payable 2 Cash Receipts 6 Credit Cards 9 General Ledger Adjustments 10 Fixed Asset 11 Payroll Tax Reporting 13 Travel Reimbursement 14 Handling Mail 15 1 Accounts

FINANCIAL POLICIES INDEX Page Accounts Payable 2 Cash Receipts 6 Credit Cards 9 General Ledger Adjustments 10 Fixed Asset 11 Payroll Tax Reporting 13 Travel Reimbursement 14 Handling Mail 15 1 Accounts

Records Retention Guidelines

Records Retention Guidelines There are no hard and fast rules regarding the amount of time taxpayers should keep important legal and financial documents. However, the following list of guidelines aims

Records Retention Guidelines There are no hard and fast rules regarding the amount of time taxpayers should keep important legal and financial documents. However, the following list of guidelines aims

Accounting and financial services are among the first type of services to be outsourced by business owners.

Accounting and financial services are among the first type of services to be outsourced by business owners. By outsourcing, business owners are able to realize consistent results, increased efficiency

Accounting and financial services are among the first type of services to be outsourced by business owners. By outsourcing, business owners are able to realize consistent results, increased efficiency

BUS 207 ACCOUNTING INFORMATION SYSTEMS SYLLABUS LECTURE HOURS/CREDITS: 2 LECTURE HOURS, 2 LAB HOURS/3 CREDITS

BUS 207 ACCOUNTING INFORMATION SYSTEMS SYLLABUS LECTURE HOURS/CREDITS: 2 LECTURE HOURS, 2 LAB HOURS/3 CREDITS CATALOG DESCRIPTION Prerequisites: BUS 102 Accounting I CIS 102 Introduction to Computers This

BUS 207 ACCOUNTING INFORMATION SYSTEMS SYLLABUS LECTURE HOURS/CREDITS: 2 LECTURE HOURS, 2 LAB HOURS/3 CREDITS CATALOG DESCRIPTION Prerequisites: BUS 102 Accounting I CIS 102 Introduction to Computers This

Financial Accounting: Assets FA 2 Module 6. Handouts. Current financial assets And current liabilities. Presented by: Laura Dallas, CGA

Accounting: Assets FA 2 Module 6 Handouts Current financial assets And current liabilities Presented by: Laura Dallas, CGA Note: this information is prepared from the best information I have available

Accounting: Assets FA 2 Module 6 Handouts Current financial assets And current liabilities Presented by: Laura Dallas, CGA Note: this information is prepared from the best information I have available

Century 21 Accounting, 8e General Journal Chapter Outlines

Century 21 Accounting, 8e General Journal Chapter Outlines PART 1 Chapter 1 ACCOUNTING FOR A SERVICE BUSINESS ORGANIZED AS A PROPRIETORSHIP Starting A Proprietorship: Changes that Affect the Accounting

Century 21 Accounting, 8e General Journal Chapter Outlines PART 1 Chapter 1 ACCOUNTING FOR A SERVICE BUSINESS ORGANIZED AS A PROPRIETORSHIP Starting A Proprietorship: Changes that Affect the Accounting

EMERSON AND SUBSIDIARIES CONSOLIDATED OPERATING RESULTS (AMOUNTS IN MILLIONS EXCEPT PER SHARE, UNAUDITED)

") CONSOLIDATED OPERATING RESULTS (AMOUNTS IN MILLIONS EXCEPT PER SHARE, UNAUDITED) TABLE 1 Quarter Ended March 31, Percent Change Net Sales $ 5,854 $ 5,919 1% Costs and expenses: Cost of sales 3,548 3,583

CONSOLIDATED OPERATING RESULTS (AMOUNTS IN MILLIONS EXCEPT PER SHARE, UNAUDITED) TABLE 1 Quarter Ended March 31, Percent Change Net Sales $ 5,854 $ 5,919 1% Costs and expenses: Cost of sales 3,548 3,583

February 2, 2016 Consolidated Financial Results for the Third Quarter of Fiscal Year 2015 (From April 1, 2015 to December 31, 2015) [Japan GAAP]

![February 2, 2016 Consolidated Financial Results for the Third Quarter of Fiscal Year 2015 (From April 1, 2015 to December 31, 2015) [Japan GAAP]](/thumbs/34/17006729.jpg "February 2, 2016 Consolidated Financial Results for the Third Quarter of Fiscal Year 2015 (From April 1, 2015 to December 31, 2015) [Japan GAAP]") February 2, 2016 Consolidated Financial Results for the Third Quarter of Fiscal Year 2015 (From April 1, 2015 to December 31, 2015) [Japan GAAP] Company Name: Idemitsu Kosan Co.,Ltd. (URL http://www.idemitsu.com)

February 2, 2016 Consolidated Financial Results for the Third Quarter of Fiscal Year 2015 (From April 1, 2015 to December 31, 2015) [Japan GAAP] Company Name: Idemitsu Kosan Co.,Ltd. (URL http://www.idemitsu.com)

November 4, 2015 Consolidated Financial Results for the Second Quarter of Fiscal Year 2015 (From April 1, 2015 to September 30, 2015) [Japan GAAP]

![November 4, 2015 Consolidated Financial Results for the Second Quarter of Fiscal Year 2015 (From April 1, 2015 to September 30, 2015) [Japan GAAP]](/thumbs/25/6762882.jpg "November 4, 2015 Consolidated Financial Results for the Second Quarter of Fiscal Year 2015 (From April 1, 2015 to September 30, 2015) [Japan GAAP]") November 4, 2015 Consolidated Financial Results for the Second Quarter of Fiscal Year 2015 (From April 1, 2015 to September 30, 2015) [Japan GAAP] Company Name: Idemitsu Kosan Co., Ltd. (URL http://www.idemitsu.com)

November 4, 2015 Consolidated Financial Results for the Second Quarter of Fiscal Year 2015 (From April 1, 2015 to September 30, 2015) [Japan GAAP] Company Name: Idemitsu Kosan Co., Ltd. (URL http://www.idemitsu.com)

2014-2015 High School Accounting II Curriculum Map

2014-2015 High School Accounting II Curriculum Map Rev. 6/16/2014 Harrison School District Two Curriculum Map Pacing Guide The curriculum map is a paced guide to the curriculum. It is a planning tool to

2014-2015 High School Accounting II Curriculum Map Rev. 6/16/2014 Harrison School District Two Curriculum Map Pacing Guide The curriculum map is a paced guide to the curriculum. It is a planning tool to

STATE BOARD OF ACCOUNTS 302 West Washington Street Room E418 INDIANAPOLIS, INDIANA 46204-2765

STATE BOARD OF ACCOUNTS 302 West Washington Street Room E418 INDIANAPOLIS, INDIANA 46204-2765 REVIEW REPORT OF INDIANA PROFESSIONAL LICENSING AGENCY March 1, 2002 to April 30, 2005 TABLE OF CONTENTS Description

STATE BOARD OF ACCOUNTS 302 West Washington Street Room E418 INDIANAPOLIS, INDIANA 46204-2765 REVIEW REPORT OF INDIANA PROFESSIONAL LICENSING AGENCY March 1, 2002 to April 30, 2005 TABLE OF CONTENTS Description

2 Under a perpetual inventory system merchandise is purchased for cash. Which is the correct journal entry to record this purchase?

KRUG PRACTICE TEST ACCTG 1 - CHAP 5,6 PRACTICE TEST -- The following is a practice test for Accounting 1, Chapters 5 and 6 It is only a representation of wha the test could be like. It is not a guarantee

KRUG PRACTICE TEST ACCTG 1 - CHAP 5,6 PRACTICE TEST -- The following is a practice test for Accounting 1, Chapters 5 and 6 It is only a representation of wha the test could be like. It is not a guarantee

How to set up a people based. accounting system that makes your. small business work for you. Thomas G. Post. Certified Public Accountant 281-351-2688

How to set up a people based accounting system that makes your small business work for you. By Thomas G. Post Certified Public Accountant 281-351-2688 www.texastaxman.com 1 Title How to set up a people

How to set up a people based accounting system that makes your small business work for you. By Thomas G. Post Certified Public Accountant 281-351-2688 www.texastaxman.com 1 Title How to set up a people

Advanced Accounting (02)

") 10 Pages Contestant Number Time Rank Advanced Accounting (02) Regional 2009 Multiple Choice (15 @ 3 points each) Short Answer (10 @ 3 points each) Matching (10 @ 2 points each) Production Portion Problem

10 Pages Contestant Number Time Rank Advanced Accounting (02) Regional 2009 Multiple Choice (15 @ 3 points each) Short Answer (10 @ 3 points each) Matching (10 @ 2 points each) Production Portion Problem

PROFESSOR S NAME ACC 255 FALL 2011 COVER SHEET FOR COMPREHENSIVE PROBLEM 2 (CHAPTERS 2, 5-8)

") COMPREHENSIVE PROBLEM 2 (CHAPTERS 2, 5-8) Page 137 NAME ANSWER KEY PROFESSOR S NAME SECTION SCORE ACC 255 FALL 2011 COVER SHEET FOR COMPREHENSIVE PROBLEM 2 (CHAPTERS 2, 5-8) INSTRUCTIONS: COMPLETE ALL

COMPREHENSIVE PROBLEM 2 (CHAPTERS 2, 5-8) Page 137 NAME ANSWER KEY PROFESSOR S NAME SECTION SCORE ACC 255 FALL 2011 COVER SHEET FOR COMPREHENSIVE PROBLEM 2 (CHAPTERS 2, 5-8) INSTRUCTIONS: COMPLETE ALL

Objective Evidence. Unit of Measurement. Accounting Period Cycle. Business Entity. Going Concern. Adequate Disclosure. Matching Expenses with Revenue

Accounting Concept: A source document is prepared for each transaction Objective Evidence Accounting Concept: Business transactions are stated in numbers that have common values; that is, using a common

Accounting Concept: A source document is prepared for each transaction Objective Evidence Accounting Concept: Business transactions are stated in numbers that have common values; that is, using a common

Bookkeeping Proficiency

Bookkeeping Proficiency (Exam) Your AccountingCoach PRO membership includes lifetime access to all of our materials. Take a quick tour by visiting www.accountingcoach.com/quicktour. Table of Contents (click

Bookkeeping Proficiency (Exam) Your AccountingCoach PRO membership includes lifetime access to all of our materials. Take a quick tour by visiting www.accountingcoach.com/quicktour. Table of Contents (click

INVENTORY. Merchandising Firms COST OF GOODS SOLD. Traditional bookkeeping uses separate accounts for different types of transactions

Merchandising Firms Principles of Accounting Created 2005 By Michael Worthington Elizabeth City State University INVENTORY Traditional bookkeeping uses separate accounts for different types of transactions

Merchandising Firms Principles of Accounting Created 2005 By Michael Worthington Elizabeth City State University INVENTORY Traditional bookkeeping uses separate accounts for different types of transactions

COMPUTERIZED ACCOUNTING II Curriculum Content Frameworks

COMPUTERIZED ACCOUNTING II Curriculum Content Frameworks Please note: All assessment questions will be taken from the knowledge portion of these frameworks. Prepared by Loretta Burgess, Greenbrier High

COMPUTERIZED ACCOUNTING II Curriculum Content Frameworks Please note: All assessment questions will be taken from the knowledge portion of these frameworks. Prepared by Loretta Burgess, Greenbrier High

ACCOUNTING FOR MERCHANDISING OPERATIONS

Chapter 5 ACCOUNTING FOR MERCHANDISING OPERATIONS PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA Winston

Chapter 5 ACCOUNTING FOR MERCHANDISING OPERATIONS PowerPoint Authors: Susan Coomer Galbreath, Ph.D., CPA Charles W. Caldwell, D.B.A., CMA Jon A. Booker, Ph.D., CPA, CIA Cynthia J. Rooney, Ph.D., CPA Winston

ACC207 Computerized Accounting Administration Outline

ACC207 Computerized Accounting Administration Outline Course Information Organization Mercer County Community College Course Number ACC 207 Credits 3 Description Introduction to general ledger accounting

ACC207 Computerized Accounting Administration Outline Course Information Organization Mercer County Community College Course Number ACC 207 Credits 3 Description Introduction to general ledger accounting

QuickBooks. Reports List 2013. Enterprise Solutions 14.0

QuickBooks Reports List 2013 Enterprise Solutions 14.0 Table of Contents Complete List of Reports... 5 Company & Financial Reports... 6 Profit & Loss... 6 Income & Expenses... 7 Balance Sheet & Net Worth...

QuickBooks Reports List 2013 Enterprise Solutions 14.0 Table of Contents Complete List of Reports... 5 Company & Financial Reports... 6 Profit & Loss... 6 Income & Expenses... 7 Balance Sheet & Net Worth...

NONPROFIT FINANCIAL MANAGEMENT SELF ASSESSMENT TOOL

NONPROFIT FINANCIAL MANAGEMENT SELF ASSESSMENT TOOL I. Financial Planning/Budget Systems 1. Organization has a comprehensive annual budget which includes all sources and uses of funds for all aspects of

NONPROFIT FINANCIAL MANAGEMENT SELF ASSESSMENT TOOL I. Financial Planning/Budget Systems 1. Organization has a comprehensive annual budget which includes all sources and uses of funds for all aspects of

Selling a Small Business. and Succession Planning FOR A SMALL BUSINESS

Selling a Small Business and Succession Planning FOR A SMALL BUSINESS Welcome 1. Agenda 2. Ground Rules 3. Introductions 2 Objectives Change ownership of a business through selling, closing, or handing

Selling a Small Business and Succession Planning FOR A SMALL BUSINESS Welcome 1. Agenda 2. Ground Rules 3. Introductions 2 Objectives Change ownership of a business through selling, closing, or handing

Exam 1 chapters 1-4 Needles 10ed

Exam 1 chapters 1-4 Needles 10ed Multiple Choice Identify the choice that best completes the statement or answers the question. 1. Which of the following is the most appropriate definition of accounting?

Exam 1 chapters 1-4 Needles 10ed Multiple Choice Identify the choice that best completes the statement or answers the question. 1. Which of the following is the most appropriate definition of accounting?

BUSINESS BOOKKEEPING & ACCOUNTS Designed to produce bookkeeping and accounts personnel trained in the

INTERNATIONAL DIPLOMA PROGRAM ON BUSINESS BOOKKEEPING & ACCOUNTS Designed to produce bookkeeping and accounts personnel trained in the MODERN PRACTICAL METHODS OF ACCOUNTING Trained and competent bookkeeping

INTERNATIONAL DIPLOMA PROGRAM ON BUSINESS BOOKKEEPING & ACCOUNTS Designed to produce bookkeeping and accounts personnel trained in the MODERN PRACTICAL METHODS OF ACCOUNTING Trained and competent bookkeeping

Fiscal Procedure Sequence page number

Table of Contents Fiscal Procedure Sequence page number Treasurer Responsibilities Maintenance of General Ledger Financial Statements Financial Signature/Review Policy Insurance Protection Payroll Procedures

Table of Contents Fiscal Procedure Sequence page number Treasurer Responsibilities Maintenance of General Ledger Financial Statements Financial Signature/Review Policy Insurance Protection Payroll Procedures

Intuit QuickBooks Enterprise Solutions 10.0 Complete List of Reports

Intuit QuickBooks Enterprise Solutions 10.0 Complete List of Reports Intuit QuickBooks Enterprise Solutions, for growing businesses, is the most powerful QuickBooks product. It has the capabilities and

Intuit QuickBooks Enterprise Solutions 10.0 Complete List of Reports Intuit QuickBooks Enterprise Solutions, for growing businesses, is the most powerful QuickBooks product. It has the capabilities and

Accounting 201 Comprehensive Practice Exam 2C Page 1

Accounting 201 Comprehensive Practice Exam 2C Page 1 1. A business organized as a corporation a. is not a separate legal entity in most states. b. requires that stockholders be personally liable for the

Accounting 201 Comprehensive Practice Exam 2C Page 1 1. A business organized as a corporation a. is not a separate legal entity in most states. b. requires that stockholders be personally liable for the

1. Merchandising company VS Service company V.S Manufacturing company

Chapter 6 Mechandising Activities 1. Merchandising company VS Service company V.S Manufacturing company Manufacturing companies use raw materials to make the inventory they sell. Their operating cycles

Chapter 6 Mechandising Activities 1. Merchandising company VS Service company V.S Manufacturing company Manufacturing companies use raw materials to make the inventory they sell. Their operating cycles

COURSE GUIDELINE--Accounting

COURSE GUIDELINE--Accounting Grade: 9- (Elective Course, offered one semester at a time) SUBJECT: Accounting TEACHER: Reimer STANDARD QTR. RESOURCES STRATEGIES ASSESSMENTS. Define accounting and explain

COURSE GUIDELINE--Accounting Grade: 9- (Elective Course, offered one semester at a time) SUBJECT: Accounting TEACHER: Reimer STANDARD QTR. RESOURCES STRATEGIES ASSESSMENTS. Define accounting and explain

Financial Accounting. (Exam)

") Financial Accounting (Exam) Your AccountingCoach PRO membership includes lifetime access to all of our materials Take a quick tour by visiting wwwaccountingcoachcom/quicktour Table of Contents (click to

Financial Accounting (Exam) Your AccountingCoach PRO membership includes lifetime access to all of our materials Take a quick tour by visiting wwwaccountingcoachcom/quicktour Table of Contents (click to

ACCOUNTING 105 CONCEPTS REVIEW

ACCOUNTING 105 CONCEPTS REVIEW A note from the tutors: This handout is designed to help you review important information as you study for your cumulative final exam. While it does cover many important

ACCOUNTING 105 CONCEPTS REVIEW A note from the tutors: This handout is designed to help you review important information as you study for your cumulative final exam. While it does cover many important

Selling a Small Business and Succession Planning for a Small Business

Table of Contents Welcome... 3 What Do You Know? Selling a Small Business and Succession Planning... 4 Pre-Test... 5 Determining If a Business Should Be Sold... 6 Discussion Point #1 Reason for Selling

Table of Contents Welcome... 3 What Do You Know? Selling a Small Business and Succession Planning... 4 Pre-Test... 5 Determining If a Business Should Be Sold... 6 Discussion Point #1 Reason for Selling

BOOKKEEPING FUNDAMENTALS TRAINING

Phone:1300 121 400 Email: enquiries@pdtraining.com.au BOOKKEEPING FUNDAMENTALS TRAINING Generate a group quote today or register now for the next public course date COURSE LENGTH: 1.0 DAYS Developing essential

Phone:1300 121 400 Email: enquiries@pdtraining.com.au BOOKKEEPING FUNDAMENTALS TRAINING Generate a group quote today or register now for the next public course date COURSE LENGTH: 1.0 DAYS Developing essential

Accounting and Administrative Manual Section 100: Accounting and Finance

No.: G-03 Page: 1 of 6 General: The application of good financial management requires the prompt reconciliation of accounts. Since departmental revenue and expenditure accounts are scrutinized monthly

No.: G-03 Page: 1 of 6 General: The application of good financial management requires the prompt reconciliation of accounts. Since departmental revenue and expenditure accounts are scrutinized monthly

for Sage 100 ERP Bank Reconciliation Overview Document

for Sage 100 ERP Bank Reconciliation Document 2012 Sage Software, Inc. All rights reserved. Sage Software, Sage Software logos, and the Sage Software product and service names mentioned herein are registered

for Sage 100 ERP Bank Reconciliation Document 2012 Sage Software, Inc. All rights reserved. Sage Software, Sage Software logos, and the Sage Software product and service names mentioned herein are registered

Credit Card Processing 101

Credit Card Processing 101 Customers have come to expect credit cards as a payment option. With ATM fees continuing to rise, some consumers may even exclusively choose to take their purchasing power to

Credit Card Processing 101 Customers have come to expect credit cards as a payment option. With ATM fees continuing to rise, some consumers may even exclusively choose to take their purchasing power to

Plan and Track Your Finances

Plan and Track Your Finances 9.1 Financing Your Business 9.2 Pro Forma Financial Statements 9.3 Recordkeeping for Businesses Lesson 9.1 Financing Your Business Goals Estimate your startup costs and personal

Plan and Track Your Finances 9.1 Financing Your Business 9.2 Pro Forma Financial Statements 9.3 Recordkeeping for Businesses Lesson 9.1 Financing Your Business Goals Estimate your startup costs and personal

Financial Statements LESSON 15. What are Financial Statements?

Financial Statements LESSON 15 Main Idea Business owners must have accurate and timely information about the fi nancial status of their business to make the best decisions. Most of this fi nancial information

Financial Statements LESSON 15 Main Idea Business owners must have accurate and timely information about the fi nancial status of their business to make the best decisions. Most of this fi nancial information

RAPID REVIEW Chapter Content

RAPID REVIEW BASIC ACCOUNTING EQUATION (Chapter 2) INVENTORY (Chapters 5 and 6) Basic Equation Assets Owner s Equity Expanded Owner s Owner s Assets Equation = Liabilities Capital Drawing Revenues Debit

RAPID REVIEW BASIC ACCOUNTING EQUATION (Chapter 2) INVENTORY (Chapters 5 and 6) Basic Equation Assets Owner s Equity Expanded Owner s Owner s Assets Equation = Liabilities Capital Drawing Revenues Debit

RECORD RETENTION. .. Architectural Plans and Surveys.. Equipment Maintenance and Repair Records.. Maintenance Contracts..

RECORD RETENTION. The holding period begins on the due date of the timely filed tax return, including extensions... The holding period begins on the date of disposal or termination. In some cases, the

RECORD RETENTION. The holding period begins on the due date of the timely filed tax return, including extensions... The holding period begins on the date of disposal or termination. In some cases, the

Accounting Visa & HR Support B2B Events Marketing. Visa (Corporate, Business, & Visit) Administration & Liaising with local Authorities ( PRO )

Administration & Liaising with local Authorities ( PRO )") Sesam Services Accounting Accounting Visa & HR Support B2B Events Marketing Bookkeeping Payroll & WPS Preparing Financial Statements Audit Preparation Visa (Corporate, Business, & Visit) Administration

Sesam Services Accounting Accounting Visa & HR Support B2B Events Marketing Bookkeeping Payroll & WPS Preparing Financial Statements Audit Preparation Visa (Corporate, Business, & Visit) Administration

Plan and Track Your Finances

Chapter 9 Plan and Track Your Finances 9.1 Finance Your Business 9.2 Pro Forma Financial Statements 9.3 Record Keeping for Businesses Ideas in Action Electronic Safekeeping Katelin Shea addressed the unmet

Chapter 9 Plan and Track Your Finances 9.1 Finance Your Business 9.2 Pro Forma Financial Statements 9.3 Record Keeping for Businesses Ideas in Action Electronic Safekeeping Katelin Shea addressed the unmet

The Statement of Cash Flows Direct Method

23 The Statement of Cash Flows Direct Method DEMONSTRATION PROBLEM The financial statements of Bolero Corporation follow. Copyright Houghton Mifflin Company. All rights reserved. 1 Bolero Corporation Income

23 The Statement of Cash Flows Direct Method DEMONSTRATION PROBLEM The financial statements of Bolero Corporation follow. Copyright Houghton Mifflin Company. All rights reserved. 1 Bolero Corporation Income

Account Numbering. By separating each account by several numbers, many new accounts can be added between any two while maintaining the logical order.

Chart of Accounts The chart of accounts is a listing of all the accounts in the general ledger, each account accompanied by a reference number. To set up a chart of accounts, one first needs to define

Chart of Accounts The chart of accounts is a listing of all the accounts in the general ledger, each account accompanied by a reference number. To set up a chart of accounts, one first needs to define

Best Online Business Sites - Part 1

PO BOX 20092 New York, NY 10017 APPLICATION TO ENTER INTO A FACTORING AGREEMENT Incorporation Certificate $1000.00 Check (One time Setup Fee for due diligence/search) Please make check payable to Geneva

PO BOX 20092 New York, NY 10017 APPLICATION TO ENTER INTO A FACTORING AGREEMENT Incorporation Certificate $1000.00 Check (One time Setup Fee for due diligence/search) Please make check payable to Geneva

For more course tutorials visit www.uoptutorial.com

ACC 290 Final Exam Guide (New) Click Here to Buy the Tutorial http://www.uoptutorial.com/index.php?route=product/ product&path=737&product_id=11101 For more course tutorials visit www.uoptutorial.com ACC

ACC 290 Final Exam Guide (New) Click Here to Buy the Tutorial http://www.uoptutorial.com/index.php?route=product/ product&path=737&product_id=11101 For more course tutorials visit www.uoptutorial.com ACC

Jackson Company recorded the following cash transactions for the year:

ACC 290 Final Exam Guide (New) Click Here to Buy the Tutorial http://www.uoptutorial.com/index.php?route=product/product&path=7 37&product_id=11101 For more course tutorials visit www.uoptutorial.com ACC

ACC 290 Final Exam Guide (New) Click Here to Buy the Tutorial http://www.uoptutorial.com/index.php?route=product/product&path=7 37&product_id=11101 For more course tutorials visit www.uoptutorial.com ACC

Thomas A. Bessant, Jr. (817) 335-1100

335-1100") Additional Information: Thomas A. Bessant, Jr. (817) 335-1100 For Immediate Release ********************************************************************************** CASH AMERICA FIRST QUARTER NET INCOME

Additional Information: Thomas A. Bessant, Jr. (817) 335-1100 For Immediate Release ********************************************************************************** CASH AMERICA FIRST QUARTER NET INCOME

(Rates and funding amounts are generally a point of negotiation)

") INVESTORS MUTUAL OF NUECES, INC.DBA ACCOUNTS RECEIVABLE FUNDING CORPORATION 6802 Mapleridge, Suite 206 Bellaire, TX 77401 Phone: 713-661-3100 or 888-713-6099 Fax: 713-661-3289 Web Site: http://www.arfc.com

INVESTORS MUTUAL OF NUECES, INC.DBA ACCOUNTS RECEIVABLE FUNDING CORPORATION 6802 Mapleridge, Suite 206 Bellaire, TX 77401 Phone: 713-661-3100 or 888-713-6099 Fax: 713-661-3289 Web Site: http://www.arfc.com

SEAGATE TECHNOLOGY PLC CONDENSED CONSOLIDATED BALANCE SHEETS

CONDENSED CONSOLIDATED BALANCE SHEETS (In millions) June 28, ASSETS Current assets: Cash and cash equivalents $ 2,259 $ 1,708 Short-term investments 47 480 Restricted cash and investments 4 101 Accounts

CONDENSED CONSOLIDATED BALANCE SHEETS (In millions) June 28, ASSETS Current assets: Cash and cash equivalents $ 2,259 $ 1,708 Short-term investments 47 480 Restricted cash and investments 4 101 Accounts

Managing Research Subject Payments Draft

UNIVERSITY OF OREGON Managing Research Subject Payments Draft Rob Freytag, Brett Giles, Dan Patten, Martha Schumacher, Teri Rowe, Lynette Schenkel, Beverly Morehouse, Olivia Pierce, Marisa Zuskar THIS

UNIVERSITY OF OREGON Managing Research Subject Payments Draft Rob Freytag, Brett Giles, Dan Patten, Martha Schumacher, Teri Rowe, Lynette Schenkel, Beverly Morehouse, Olivia Pierce, Marisa Zuskar THIS

COMPUTER ACCOUNTING WITH QUICKBOOKS 2013 CHAPTER 10

COMPUTER ACCOUNTING WITH QUICKBOOKS 2013 CHAPTER 10 Donna Kay Copyright 2014 by The McGraw-Hill Companies, Inc. All rights reserved 10-2 CHAPTER 10 OVERVIEW Setup a New Company Customize Chart of Accounts

COMPUTER ACCOUNTING WITH QUICKBOOKS 2013 CHAPTER 10 Donna Kay Copyright 2014 by The McGraw-Hill Companies, Inc. All rights reserved 10-2 CHAPTER 10 OVERVIEW Setup a New Company Customize Chart of Accounts

If you are currently using a factoring company, we will need a release letter from your factoring company.

Dear TranSource Carrier Network Member, As a transportation leader, TranSource LLC understands the pressures today s carriers face from rising fuel and insurance to a cash flow squeeze when shippers take

Dear TranSource Carrier Network Member, As a transportation leader, TranSource LLC understands the pressures today s carriers face from rising fuel and insurance to a cash flow squeeze when shippers take

How To Read The Financial Results Of 20Xx And 200X

Name SAMPLE Financial Statements December 31, 20XX CPA Accounting Firm Name Table of Contents Page Accountant s Review Report 1 Financial Statements Balance Sheet 2 Income Statement 3 Schedule of General

Name SAMPLE Financial Statements December 31, 20XX CPA Accounting Firm Name Table of Contents Page Accountant s Review Report 1 Financial Statements Balance Sheet 2 Income Statement 3 Schedule of General

In the event of a tie, the score on the last ten questions will be used as a tie-breaker.

NEW YORK STATE ASSOCIATION FUTURE BUSINESS LEADERS OF AMERICA SPRING DISTRICT MEETING ACCOUNTING II 2010 TEST DIRECTIONS 1. Complete the information requested on the answer sheet. PRINT your name on the

NEW YORK STATE ASSOCIATION FUTURE BUSINESS LEADERS OF AMERICA SPRING DISTRICT MEETING ACCOUNTING II 2010 TEST DIRECTIONS 1. Complete the information requested on the answer sheet. PRINT your name on the

Record Retention Guidelines

Record Retention Guidelines for businesses and not-for-profit organizations Bader Martin, P.S. Certified Public Accountants + Business Advisors 1000 Second Avenue, 34 th Floor, Seattle, Washington 98104-1022

Record Retention Guidelines for businesses and not-for-profit organizations Bader Martin, P.S. Certified Public Accountants + Business Advisors 1000 Second Avenue, 34 th Floor, Seattle, Washington 98104-1022

7 Accounting for Sales and Accounts Receivable

7-1 McGraw-Hill 2009 The McGraw-Hill Companies, Inc. All rights reserved. Chapter 7 Accounting for Sales and Accounts Receivable Section 1: Merchandise Sales Section Objectives 1. Record credit sales in

7-1 McGraw-Hill 2009 The McGraw-Hill Companies, Inc. All rights reserved. Chapter 7 Accounting for Sales and Accounts Receivable Section 1: Merchandise Sales Section Objectives 1. Record credit sales in

Advanced QuickBooks Troubleshooting Techniques For Accounting Professionals Webinar Workshop

Advanced QuickBooks Troubleshooting Techniques For Accounting Professionals Webinar Workshop Course Fee: $125.00 5 hour hands-on, webinar instruction. Class size limited to 20 participants. Course Description:

Advanced QuickBooks Troubleshooting Techniques For Accounting Professionals Webinar Workshop Course Fee: $125.00 5 hour hands-on, webinar instruction. Class size limited to 20 participants. Course Description:

Chapter Review Problems

Chapter Review Problems Unit 17.1 Income statements 1. When revenues exceed expenses, is the result (a) net income or (b) net loss? (a) net income 2. Do income statements reflect profits of a business

Chapter Review Problems Unit 17.1 Income statements 1. When revenues exceed expenses, is the result (a) net income or (b) net loss? (a) net income 2. Do income statements reflect profits of a business

INDICE Preface Part 1 the accounting cycle 1 Accounting, the language of business What is accounting?

INDICE Preface XV Part 1 the accounting cycle 1 Accounting, the language of business 2 What is accounting? The purpose and nature and accounting information, creating accounting information. Communicating

INDICE Preface XV Part 1 the accounting cycle 1 Accounting, the language of business 2 What is accounting? The purpose and nature and accounting information, creating accounting information. Communicating

HIGHLIGHTS FIRST QUARTER 2016

Q1-16 EUROPRIS ASA 2 CONTENTS / HIGHLIGHTS FIRST QUARTER 2016 HIGHLIGHTS FIRST QUARTER 2016 (Figures for the corresponding period of last year in brackets. The figures are unaudited.) Group revenues increased

Q1-16 EUROPRIS ASA 2 CONTENTS / HIGHLIGHTS FIRST QUARTER 2016 HIGHLIGHTS FIRST QUARTER 2016 (Figures for the corresponding period of last year in brackets. The figures are unaudited.) Group revenues increased