Transparency, Liquidity Uncertainty and Crises. Mark Lang Mark Maffett

|

|

|

- Barry Marsh

- 9 years ago

- Views:

Transcription

1 Transparency, Liquidity Uncertainty and Crises Mark Lang Mark Maffett

2 Why liquidity uncertainty? Current crisis Liquidity dried up Especially for opaque assets Investors worry about liquidity uncertainty the principal challenge is not the average level of financial liquidity, but its variability and uncertainty (Persaud, 2003) As important as the level of liquidity is its uncertainty. Investors may avoid markets altogether where liquidity is uncertain (McCoy, 2003)

As important as the level of liquidity is its")

3 Why might transparency matter to liquidity uncertainty? Grossman and Miller (1988) Investors value immediacy Liquidity providers facilitate immediacy Charge a price for immediacy through discounts Lessons: Illiquidity as price pressure Possibility of illiquidity with volume (e.g., crises) Speculators are our friends

4 Brunnermeier and Pedersen (2009) Liquidity providers rely on borrowed money Subject to margin requirements Liquidity will be affect by: Anything that affects funders willingness to lend or margin requiremens Anything that affects liquidity providers level of capital or risk tolerances

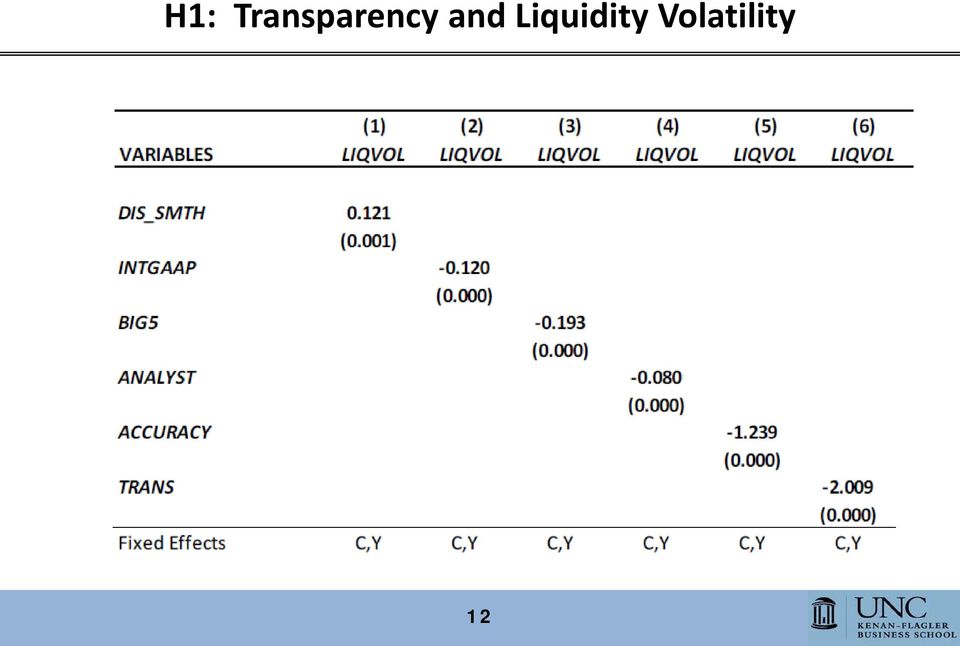

5 Predictions Economic shocks affect availability of liquidity capital Effects will be greater for stocks with greater uncertainty about intrinsic value (opaque stocks) H1: Liquidity variability is greater for opaque stocks Illiquidity effects can spiral into black holes Especially for opaque stocks H2: Extreme illiquidity events are more common for opaque stocks

6 When market-wide liquidity gets tight, opaque stocks suffer more H3: The covariance between firm liquidity and market liquidity is higher for opaque stocks When the market drops, liquidity dries up more for opaque stocks H4: The covariance between firm liquidity and market return is higher for opaque stocks

7 All of the previous effects are more pronounced during crisis periods Market downturns reduce speculator capital and funders willingness to lend, reducing liquidity H5: Crises strengthen the relation between transparency and: liquidity volatility, extreme illiquidity events, covariance of liquidity with market liquidity and covariance of liquidity with market returns. Even more so for greater crises. Transparency mitigates the increase in beta during crises.

8 Investors will prefer stocks with lower liquidity variability H6: Tobin s Q is higher for firms with: lower liquidity variability, fewer extreme illiquidity events, less skewed liquidity, lower correlation with market liquidity, and lower correlation with market returns.

9 Research Design 37 countries in all, including the U.S. Results are robust across countries Liquidity measure: Amihud price impact Price movement for one million dollar trade Unit of observation: firm/month Transparency: Discretionary earnings smoothing Big-5 auditor Non-local accounting standards Analyst following Analyst forecast accuracy 9

10 Control Variables Level of liquidity Firm size Book-to-Market Standard Deviation of Returns Firm Returns Cross-Listing Ownership Structure Profitability Business Risk Country, Year and Firm Fixed Effects 10

11 11

12 H1: Transparency and Liquidity Volatility 12

13 H2: Transparency and Extreme Illiquidity Events 13

14 H3&4: Transparency and Liquidity Covariability 14

15 H5: Transparency, Liquidity Uncertainty and Crises 15

16 H6: Liquidity Uncertainty and Valuation 16

17 Conclusions Liquidity variability, extreme illiquidity events and liquidity covariability with market liquidity and market returns are correlated with transparency Very robust Importance of transparency varies predictably across institutional environments Effects are particularly strongest during crises Each dependent variable is correlated with Tobin s Q 17

René Garcia Professor of finance

Liquidity Risk: What is it? How to Measure it? René Garcia Professor of finance EDHEC Business School, CIRANO Cirano, Montreal, January 7, 2009 The financial and economic environment We are living through

Liquidity Risk: What is it? How to Measure it? René Garcia Professor of finance EDHEC Business School, CIRANO Cirano, Montreal, January 7, 2009 The financial and economic environment We are living through

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

ECON 4110: Sample Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Economists define risk as A) the difference between the return on common

ECON 4110: Sample Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Economists define risk as A) the difference between the return on common

Yao Zheng University of New Orleans. Eric Osmer University of New Orleans

ABSTRACT The pricing of China Region ETFs - an empirical analysis Yao Zheng University of New Orleans Eric Osmer University of New Orleans Using a sample of exchange-traded funds (ETFs) that focus on investing

ABSTRACT The pricing of China Region ETFs - an empirical analysis Yao Zheng University of New Orleans Eric Osmer University of New Orleans Using a sample of exchange-traded funds (ETFs) that focus on investing

Global Currency Hedging

Global Currency Hedging John Y. Campbell Harvard University Arrowstreet Capital, L.P. May 16, 2010 Global Currency Hedging Joint work with Karine Serfaty-de Medeiros of OC&C Strategy Consultants and Luis

Global Currency Hedging John Y. Campbell Harvard University Arrowstreet Capital, L.P. May 16, 2010 Global Currency Hedging Joint work with Karine Serfaty-de Medeiros of OC&C Strategy Consultants and Luis

A Primer on Valuing Common Stock per IRS 409A and the Impact of Topic 820 (Formerly FAS 157)

") A Primer on Valuing Common Stock per IRS 409A and the Impact of Topic 820 (Formerly FAS 157) By Stanley Jay Feldman, Ph.D. Chairman and Chief Valuation Officer Axiom Valuation Solutions May 2010 201 Edgewater

A Primer on Valuing Common Stock per IRS 409A and the Impact of Topic 820 (Formerly FAS 157) By Stanley Jay Feldman, Ph.D. Chairman and Chief Valuation Officer Axiom Valuation Solutions May 2010 201 Edgewater

LIQUIDITY AND ASSET PRICING. Evidence for the London Stock Exchange

LIQUIDITY AND ASSET PRICING Evidence for the London Stock Exchange Timo Hubers (358022) Bachelor thesis Bachelor Bedrijfseconomie Tilburg University May 2012 Supervisor: M. Nie MSc Table of Contents Chapter

LIQUIDITY AND ASSET PRICING Evidence for the London Stock Exchange Timo Hubers (358022) Bachelor thesis Bachelor Bedrijfseconomie Tilburg University May 2012 Supervisor: M. Nie MSc Table of Contents Chapter

Draft Prudential Practice Guide

Draft Prudential Practice Guide SPG 532 Investment Risk Management May 2013 www.apra.gov.au Australian Prudential Regulation Authority Disclaimer and copyright This prudential practice guide is not legal

Draft Prudential Practice Guide SPG 532 Investment Risk Management May 2013 www.apra.gov.au Australian Prudential Regulation Authority Disclaimer and copyright This prudential practice guide is not legal

The Foreign Exchange Market Not As Liquid As You May Think

06.09.2012 Seite 1 / 5 The Foreign Exchange Market Not As Liquid As You May Think September 6 2012 1 23 AM GMT By Loriano Mancini Angelo Ranaldo and Jan Wrampelmeyer The foreign exchange market facilitates

06.09.2012 Seite 1 / 5 The Foreign Exchange Market Not As Liquid As You May Think September 6 2012 1 23 AM GMT By Loriano Mancini Angelo Ranaldo and Jan Wrampelmeyer The foreign exchange market facilitates

ANALYSIS AND MANAGEMENT

ANALYSIS AND MANAGEMENT T H 1RD CANADIAN EDITION W. SEAN CLEARY Queen's University CHARLES P. JONES North Carolina State University JOHN WILEY & SONS CANADA, LTD. CONTENTS PART ONE Background CHAPTER 1

ANALYSIS AND MANAGEMENT T H 1RD CANADIAN EDITION W. SEAN CLEARY Queen's University CHARLES P. JONES North Carolina State University JOHN WILEY & SONS CANADA, LTD. CONTENTS PART ONE Background CHAPTER 1

TRANSAMERICA SERIES TRUST Transamerica Vanguard ETF Portfolio Conservative VP. Supplement to the Currently Effective Prospectus and Summary Prospectus

TRANSAMERICA SERIES TRUST Transamerica Vanguard ETF Portfolio Conservative VP Supplement to the Currently Effective Prospectus and Summary Prospectus * * * The following replaces in their entirety the

TRANSAMERICA SERIES TRUST Transamerica Vanguard ETF Portfolio Conservative VP Supplement to the Currently Effective Prospectus and Summary Prospectus * * * The following replaces in their entirety the

Futures Price d,f $ 0.65 = (1.05) (1.04)

(1.04)") 24 e. Currency Futures In a currency futures contract, you enter into a contract to buy a foreign currency at a price fixed today. To see how spot and futures currency prices are related, note that holding

24 e. Currency Futures In a currency futures contract, you enter into a contract to buy a foreign currency at a price fixed today. To see how spot and futures currency prices are related, note that holding

THE EFFECTS OF STOCK LENDING ON SECURITY PRICES: AN EXPERIMENT

THE EFFECTS OF STOCK LENDING ON SECURITY PRICES: AN EXPERIMENT Steve Kaplan Toby Moskowitz Berk Sensoy November, 2011 MOTIVATION: WHAT IS THE IMPACT OF SHORT SELLING ON SECURITY PRICES? Does shorting make

THE EFFECTS OF STOCK LENDING ON SECURITY PRICES: AN EXPERIMENT Steve Kaplan Toby Moskowitz Berk Sensoy November, 2011 MOTIVATION: WHAT IS THE IMPACT OF SHORT SELLING ON SECURITY PRICES? Does shorting make

Carry Trades and Currency Crashes

Carry Trades and Currency Crashes Markus K. Brunnermeier, Stefan Nagel, Lasse Pedersen Princeton, Stanford, NYU AEA Meetings, January 2008 BNP (2008) Carry Trades & Currency Crashes AEA, Jan 2008 1 / 23

Carry Trades and Currency Crashes Markus K. Brunnermeier, Stefan Nagel, Lasse Pedersen Princeton, Stanford, NYU AEA Meetings, January 2008 BNP (2008) Carry Trades & Currency Crashes AEA, Jan 2008 1 / 23

The Hendershot-Frederiksen Group

The Hendershot-Frederiksen Group Discussion materials Prepared by: Paul Hendershot, Senior Portfolio Manager, Financial Advisor Carsten Frederiksen, CFP, Financial Advisor 1276790 Contents I. The Hendershot-Frederiksen

The Hendershot-Frederiksen Group Discussion materials Prepared by: Paul Hendershot, Senior Portfolio Manager, Financial Advisor Carsten Frederiksen, CFP, Financial Advisor 1276790 Contents I. The Hendershot-Frederiksen

Long/Short Equity Investing Part I Styles, Strategies, and Implementation Considerations

Long/Short Equity Investing Part I Styles, Strategies, and Implementation Considerations Scott Larson, Associate Portfolio Manager for Directional Strategies This is Part I of a two part series. In Part

Long/Short Equity Investing Part I Styles, Strategies, and Implementation Considerations Scott Larson, Associate Portfolio Manager for Directional Strategies This is Part I of a two part series. In Part

DOUGLAS S. WEISS, CFA! INVESTMENT ADVISOR D E C E M B E R 2 0 1 2

DOUGLAS S. WEISS, CFA! INVESTMENT ADVISOR D E C E M B E R 2 0 1 2 EXPERIENCE / EXPERTISE Registered Investment Advisor ( RIA ) focused on constructing and managing risk optimized portfolios for individual

DOUGLAS S. WEISS, CFA! INVESTMENT ADVISOR D E C E M B E R 2 0 1 2 EXPERIENCE / EXPERTISE Registered Investment Advisor ( RIA ) focused on constructing and managing risk optimized portfolios for individual

CHAPTER 11 INTRODUCTION TO SECURITY VALUATION TRUE/FALSE QUESTIONS

1 CHAPTER 11 INTRODUCTION TO SECURITY VALUATION TRUE/FALSE QUESTIONS (f) 1 The three step valuation process consists of 1) analysis of alternative economies and markets, 2) analysis of alternative industries

1 CHAPTER 11 INTRODUCTION TO SECURITY VALUATION TRUE/FALSE QUESTIONS (f) 1 The three step valuation process consists of 1) analysis of alternative economies and markets, 2) analysis of alternative industries

Effective downside risk management

Effective downside risk management Aymeric Forest, Fund Manager, Multi-Asset Investments November 2012 Since 2008, the desire to avoid significant portfolio losses has, more than ever, been at the front

Effective downside risk management Aymeric Forest, Fund Manager, Multi-Asset Investments November 2012 Since 2008, the desire to avoid significant portfolio losses has, more than ever, been at the front

CHAPTER 17 INTERNATIONAL CAPITAL STRUCTURE AND THE COST OF CAPITAL SUGGESTED ANSWERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLEMS

CHAPTER 17 INTERNATIONAL CAPITAL STRUCTURE AND THE COST OF CAPITAL SUGGESTED ANSERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLES QUESTIONS 1. Suppose that your firm is operating in a segmented

CHAPTER 17 INTERNATIONAL CAPITAL STRUCTURE AND THE COST OF CAPITAL SUGGESTED ANSERS AND SOLUTIONS TO END-OF-CHAPTER QUESTIONS AND PROBLES QUESTIONS 1. Suppose that your firm is operating in a segmented

Pioneer Funds. Supplement to the Summary Prospectuses, as in effect and as may be amended from time to time, for: May 1, 2015

Pioneer Funds May 1, 2015 Supplement to the Summary Prospectuses, as in effect and as may be amended from time to time, for: Fund Pioneer Absolute Return Bond Fund Pioneer AMT-Free Municipal Fund Pioneer

Pioneer Funds May 1, 2015 Supplement to the Summary Prospectuses, as in effect and as may be amended from time to time, for: Fund Pioneer Absolute Return Bond Fund Pioneer AMT-Free Municipal Fund Pioneer

Liquidity in the Foreign Exchange Market: Measurement, Commonality, and Risk Premiums

Liquidity in the Foreign Exchange Market: Measurement, Commonality, and Risk Premiums Loriano Mancini Swiss Finance Institute and EPFL Angelo Ranaldo University of St. Gallen Jan Wrampelmeyer University

Liquidity in the Foreign Exchange Market: Measurement, Commonality, and Risk Premiums Loriano Mancini Swiss Finance Institute and EPFL Angelo Ranaldo University of St. Gallen Jan Wrampelmeyer University

Colleen Johnston Group Head Finance & CFO TD Bank Financial Group. Citi Financial Services Conference

Colleen Johnston Group Head Finance & CFO TD Bank Financial Group Citi Financial Services Conference January 28, 2009 Caution regarding forward-looking statements From time to time, the Bank makes written

Colleen Johnston Group Head Finance & CFO TD Bank Financial Group Citi Financial Services Conference January 28, 2009 Caution regarding forward-looking statements From time to time, the Bank makes written

SPDR S&P 400 Mid Cap Value ETF

SPDR S&P 400 Mid Cap Value ETF Summary Prospectus-October 31, 2015 Before you invest in the SPDR S&P 400 Mid Cap Value ETF (the Fund ), you may want to review the Fund's prospectus and statement of additional

SPDR S&P 400 Mid Cap Value ETF Summary Prospectus-October 31, 2015 Before you invest in the SPDR S&P 400 Mid Cap Value ETF (the Fund ), you may want to review the Fund's prospectus and statement of additional

Prof Kevin Davis Melbourne Centre for Financial Studies. Managing Liquidity Risks. Session 5.1. Training Program ~ 8 12 December 2008 SHANGHAI, CHINA

Enhancing Risk Management and Governance in the Region s Banking System to Implement Basel II and to Meet Contemporary Risks and Challenges Arising from the Global Banking System Training Program ~ 8 12

Enhancing Risk Management and Governance in the Region s Banking System to Implement Basel II and to Meet Contemporary Risks and Challenges Arising from the Global Banking System Training Program ~ 8 12

Asset Management Portfolio Solutions Disciplined Process. Customized Approach. Risk-Based Strategies.

INSTITUTIONAL TRUST & CUSTODY Asset Management Portfolio Solutions Disciplined Process. Customized Approach. Risk-Based Strategies. As one of the fastest growing investment managers in the nation, U.S.

INSTITUTIONAL TRUST & CUSTODY Asset Management Portfolio Solutions Disciplined Process. Customized Approach. Risk-Based Strategies. As one of the fastest growing investment managers in the nation, U.S.

SUPPLEMENT TO THE CURRENTLY EFFECTIVE SUMMARY PROSPECTUS

SUPPLEMENT TO THE CURRENTLY EFFECTIVE SUMMARY PROSPECTUS Deutsche Global Real Estate Securities Fund Effective May 1, 2016, the following information replaces the existing disclosure contained under the

SUPPLEMENT TO THE CURRENTLY EFFECTIVE SUMMARY PROSPECTUS Deutsche Global Real Estate Securities Fund Effective May 1, 2016, the following information replaces the existing disclosure contained under the

A guide to investing inexchange-traded products

A guide to investing inexchange-traded products What you should know before you buy Before you make an investment decision, it is important to review your financial situation, investment objectives, risk

A guide to investing inexchange-traded products What you should know before you buy Before you make an investment decision, it is important to review your financial situation, investment objectives, risk

A comparison between different volatility models. Daniel Amsköld

A comparison between different volatility models Daniel Amsköld 211 6 14 I II Abstract The main purpose of this master thesis is to evaluate and compare different volatility models. The evaluation is based

A comparison between different volatility models Daniel Amsköld 211 6 14 I II Abstract The main purpose of this master thesis is to evaluate and compare different volatility models. The evaluation is based

Dataline A look at current financial reporting issues

Dataline A look at current financial reporting issues No.2013-17 July 25, 2013 What s inside: Overview... 1 At a glance... 1 The main details... 1 Contents of the Guide... 3 Overall concepts... 3 Valuation

Dataline A look at current financial reporting issues No.2013-17 July 25, 2013 What s inside: Overview... 1 At a glance... 1 The main details... 1 Contents of the Guide... 3 Overall concepts... 3 Valuation

Accounting for Insurance Contracts

Accounting for Insurance Contracts 2012 ACLI Executive Roundtable Marc Siegel, FASB Board Member This presentation has been prepared by the staff of the FASB to help constituents understand the preliminary

Accounting for Insurance Contracts 2012 ACLI Executive Roundtable Marc Siegel, FASB Board Member This presentation has been prepared by the staff of the FASB to help constituents understand the preliminary

ETF Options. Presented by The Options Industry Council 1-888-OPTIONS

ETF Options Presented by The Options Industry Council 1-888-OPTIONS ETF Options Options involve risks and are not suitable for everyone. Prior to buying or selling options, an investor must receive a copy

ETF Options Presented by The Options Industry Council 1-888-OPTIONS ETF Options Options involve risks and are not suitable for everyone. Prior to buying or selling options, an investor must receive a copy

PROFESSIONAL FIXED-INCOME MANAGEMENT

MARCH 2014 PROFESSIONAL FIXED-INCOME MANAGEMENT A Strategy for Changing Markets EXECUTIVE SUMMARY The bond market has evolved in the past 30 years and become increasingly complex and volatile. Many investors

MARCH 2014 PROFESSIONAL FIXED-INCOME MANAGEMENT A Strategy for Changing Markets EXECUTIVE SUMMARY The bond market has evolved in the past 30 years and become increasingly complex and volatile. Many investors

INVESTMENT POLICY April 2013

Policy approved at 22 April 2013 meeting of the Board of Governors (Minute 133:4:13) INVESTMENT POLICY April 2013 Contents SECTION 1. OVERVIEW SECTION 2. INVESTMENT PHILOSOPHY- MAXIMISING RETURN SECTION

Policy approved at 22 April 2013 meeting of the Board of Governors (Minute 133:4:13) INVESTMENT POLICY April 2013 Contents SECTION 1. OVERVIEW SECTION 2. INVESTMENT PHILOSOPHY- MAXIMISING RETURN SECTION

Investment Insight Diversified Factor Premia Edward Qian PhD, CFA, Bryan Belton, CFA, and Kun Yang PhD, CFA PanAgora Asset Management August 2013

Investment Insight Diversified Factor Premia Edward Qian PhD, CFA, Bryan Belton, CFA, and Kun Yang PhD, CFA PanAgora Asset Management August 2013 Modern Portfolio Theory suggests that an investor s return

Investment Insight Diversified Factor Premia Edward Qian PhD, CFA, Bryan Belton, CFA, and Kun Yang PhD, CFA PanAgora Asset Management August 2013 Modern Portfolio Theory suggests that an investor s return

Chapter Two FINANCIAL AND ECONOMIC INDICATORS

Chapter Two FINANCIAL AND ECONOMIC INDICATORS 1. Introduction In Chapter One we discussed the concept of risk and the importance of protecting a portfolio from losses. Managing your investment risk should

Chapter Two FINANCIAL AND ECONOMIC INDICATORS 1. Introduction In Chapter One we discussed the concept of risk and the importance of protecting a portfolio from losses. Managing your investment risk should

Bullion and Mining Stocks Two Different Investments

BMG ARTICLES Bullion and Mining Stock Two Different Investments 1 Bullion and Mining Stocks Two Different Investments March 2009 M By Nick Barisheff any investors believe their portfolios have exposure

BMG ARTICLES Bullion and Mining Stock Two Different Investments 1 Bullion and Mining Stocks Two Different Investments March 2009 M By Nick Barisheff any investors believe their portfolios have exposure

FUNDAMENTALS. an introduction to ALTERNATIVES [1]

![FUNDAMENTALS. an introduction to ALTERNATIVES [1]](/thumbs/27/10598275.jpg "FUNDAMENTALS. an introduction to ALTERNATIVES [1]") ALTEGRIS ACADEMY FUNDAMENTALS an introduction to ALTERNATIVES [1] Important Risk Disclosure Alternative investments involve a high degree of risk and can be illiquid due to restrictions on transfer and

ALTEGRIS ACADEMY FUNDAMENTALS an introduction to ALTERNATIVES [1] Important Risk Disclosure Alternative investments involve a high degree of risk and can be illiquid due to restrictions on transfer and

How To Invest In American Funds Insurance Series Portfolio Series

American Funds Insurance Series Portfolio Series Prospectus May 1, 2015 Class 4 shares American Funds Global Growth Portfolio American Funds Growth and Income Portfolio Class P2 shares American Funds Managed

American Funds Insurance Series Portfolio Series Prospectus May 1, 2015 Class 4 shares American Funds Global Growth Portfolio American Funds Growth and Income Portfolio Class P2 shares American Funds Managed

FAIR VALUE ACCOUNTING: VISIONARY THINKING OR OXYMORON? Aswath Damodaran

FAIR VALUE ACCOUNTING: VISIONARY THINKING OR OXYMORON? Aswath Damodaran Three big questions about fair value accounting Why fair value accounting? What is fair value? What are the first principles that

FAIR VALUE ACCOUNTING: VISIONARY THINKING OR OXYMORON? Aswath Damodaran Three big questions about fair value accounting Why fair value accounting? What is fair value? What are the first principles that

Index Options Beginners Tutorial

Index Options Beginners Tutorial 1 BUY A PUT TO TAKE ADVANTAGE OF A RISE A diversified portfolio of EUR 100,000 can be hedged by buying put options on the Eurostoxx50 Index. To avoid paying too high a

Index Options Beginners Tutorial 1 BUY A PUT TO TAKE ADVANTAGE OF A RISE A diversified portfolio of EUR 100,000 can be hedged by buying put options on the Eurostoxx50 Index. To avoid paying too high a

Moody s Analytics Solutions for the Asset Manager

ASSET MANAGER Moody s Analytics Solutions for the Asset Manager Moody s Analytics Solutions for the Asset Manager COVERING YOUR ENTIRE WORKFLOW Moody s is the leader in analyzing and monitoring credit

ASSET MANAGER Moody s Analytics Solutions for the Asset Manager Moody s Analytics Solutions for the Asset Manager COVERING YOUR ENTIRE WORKFLOW Moody s is the leader in analyzing and monitoring credit

Valuations of Large Publicly Traded Real Estate Companies and their Asset Portfolios.

Dept of Real Estate and Construction Management Master of Science Thesis no. 478 Div of Building and Real Estate Economics Valuations of Large Publicly Traded Real Estate Companies and their Asset Portfolios.

Dept of Real Estate and Construction Management Master of Science Thesis no. 478 Div of Building and Real Estate Economics Valuations of Large Publicly Traded Real Estate Companies and their Asset Portfolios.

Agenda. Saving and Investment in the Open Economy, Part 2. Globalization and the U.S. economy. Globalization and the U.S. economy

Agenda Globalization and the U.S. Economy Saving and Investment in the Open Economy, Part 2 Saving and Investment in Large Open Economies (LOE) The U.S. Current Account Deficit Fiscal Policy and the Current

Agenda Globalization and the U.S. Economy Saving and Investment in the Open Economy, Part 2 Saving and Investment in Large Open Economies (LOE) The U.S. Current Account Deficit Fiscal Policy and the Current

Investing in International Financial Markets

APPENDIX 3 Investing in International Financial Markets http:// Visit http://money.cnn.com for current national and international market data and analyses. The trading of financial assets (such as stocks

APPENDIX 3 Investing in International Financial Markets http:// Visit http://money.cnn.com for current national and international market data and analyses. The trading of financial assets (such as stocks

Understanding investment concepts Version 5.0

Understanding investment concepts Version 5.0 This document provides some additional information about the investment concepts discussed in the SOA so that you can understand the benefits of the strategies

Understanding investment concepts Version 5.0 This document provides some additional information about the investment concepts discussed in the SOA so that you can understand the benefits of the strategies

Are you protected against market risk?

Are you protected against market risk? The Aston Hill Capital Growth Fund provides low volatility access to U.S. equities with a strong focus on downside protection. Since taking over management of the

Are you protected against market risk? The Aston Hill Capital Growth Fund provides low volatility access to U.S. equities with a strong focus on downside protection. Since taking over management of the

Alternative Investing

Alternative Investing An important piece of the puzzle Improve diversification Manage portfolio risk Target absolute returns Innovation is our capital. Make it yours. Manage Risk and Enhance Performance

Alternative Investing An important piece of the puzzle Improve diversification Manage portfolio risk Target absolute returns Innovation is our capital. Make it yours. Manage Risk and Enhance Performance

The case for high yield

The case for high yield Jennifer Ponce de Leon, Vice President, Senior Sector Leader Wendy Price, Director, Institutional Product Management We believe high yield is a compelling relative investment opportunity

The case for high yield Jennifer Ponce de Leon, Vice President, Senior Sector Leader Wendy Price, Director, Institutional Product Management We believe high yield is a compelling relative investment opportunity

Inflation Target Of The Lunda Krona

Inflation Targeting The Swedish Experience Lars Heikensten We in Sweden owe a great debt of thanks to the Bank of Canada for all the help we have received in recent years. We have greatly benefited from

Inflation Targeting The Swedish Experience Lars Heikensten We in Sweden owe a great debt of thanks to the Bank of Canada for all the help we have received in recent years. We have greatly benefited from

Investing in Stocks 14-1. Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

Investing in Stocks McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. 14-1 Invest in stocks Learning Objectives Identify the most important features of common and

Investing in Stocks McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. 14-1 Invest in stocks Learning Objectives Identify the most important features of common and

CORPORATE STRATEGY AND MARKET COMPETITION

CORPORATE STRATEGY AND MARKET COMPETITION MFE PROGRAM OXFORD UNIVERSITY TRINITY TERM PROFESSORS: MARZENA J. ROSTEK AND GUESTS TH 8:45AM 12:15PM, SAID BUSINESS SCHOOL, LECTURE THEATRE 4 COURSE DESCRIPTION:

CORPORATE STRATEGY AND MARKET COMPETITION MFE PROGRAM OXFORD UNIVERSITY TRINITY TERM PROFESSORS: MARZENA J. ROSTEK AND GUESTS TH 8:45AM 12:15PM, SAID BUSINESS SCHOOL, LECTURE THEATRE 4 COURSE DESCRIPTION:

Important Information about Initial Public Offerings

Robert W. Baird & Co. Incorporated Important Information about Initial Public Offerings Baird has prepared this document to help you understand the characteristics and risks associated with investing in

Robert W. Baird & Co. Incorporated Important Information about Initial Public Offerings Baird has prepared this document to help you understand the characteristics and risks associated with investing in

Why Invest in a Non-Traded Business Development Company?

Why Invest in a Non-Traded Business Development Company? This literature must be read in conjunction with the prospectus in order to fully understand all of the implications and risks of the offering of

Why Invest in a Non-Traded Business Development Company? This literature must be read in conjunction with the prospectus in order to fully understand all of the implications and risks of the offering of

Stock Market Liquidity and the Business Cycle

Stock Market Liquidity and the Business Cycle Forthcoming, Journal of Finance Randi Næs a Johannes Skjeltorp b Bernt Arne Ødegaard b,c Jun 2010 a: Ministry of Trade and Industry b: Norges Bank c: University

Stock Market Liquidity and the Business Cycle Forthcoming, Journal of Finance Randi Næs a Johannes Skjeltorp b Bernt Arne Ødegaard b,c Jun 2010 a: Ministry of Trade and Industry b: Norges Bank c: University

Economic Value Added in the Hong Kong Listed Companies: A Preliminary Evidence

Economic Value Added in the Hong Kong Listed Companies: A Preliminary Evidence V.I. Tian a, E.Y.L. Keung a and Y.F. Chow a a Department of Finance, The Chinese University of Hong Kong, Hong Kong. Abstract:

Economic Value Added in the Hong Kong Listed Companies: A Preliminary Evidence V.I. Tian a, E.Y.L. Keung a and Y.F. Chow a a Department of Finance, The Chinese University of Hong Kong, Hong Kong. Abstract:

Mortgage Lending Analytics

Mortgage Lending Analytics Operational Practices December 2, 2014 Leslie Deich Today s Agenda The basics of mortgage lending from both the borrower and lender s perspective Overview of the operational

Mortgage Lending Analytics Operational Practices December 2, 2014 Leslie Deich Today s Agenda The basics of mortgage lending from both the borrower and lender s perspective Overview of the operational

Black Scholes Merton Approach To Modelling Financial Derivatives Prices Tomas Sinkariovas 0802869. Words: 3441

Black Scholes Merton Approach To Modelling Financial Derivatives Prices Tomas Sinkariovas 0802869 Words: 3441 1 1. Introduction In this paper I present Black, Scholes (1973) and Merton (1973) (BSM) general

Black Scholes Merton Approach To Modelling Financial Derivatives Prices Tomas Sinkariovas 0802869 Words: 3441 1 1. Introduction In this paper I present Black, Scholes (1973) and Merton (1973) (BSM) general

LIQUIDITY RISK MANAGEMENT GUIDELINE

LIQUIDITY RISK MANAGEMENT GUIDELINE April 2009 Table of Contents Preamble... 3 Introduction... 4 Scope... 5 Coming into effect and updating... 6 1. Liquidity risk... 7 2. Sound and prudent liquidity risk

LIQUIDITY RISK MANAGEMENT GUIDELINE April 2009 Table of Contents Preamble... 3 Introduction... 4 Scope... 5 Coming into effect and updating... 6 1. Liquidity risk... 7 2. Sound and prudent liquidity risk

Alternatives 101. Tools for Enhancing Asset Allocation ALTERNATIVES 101: TOOLS FOR ENHANCING ASSET ALLOCATION 1

Alternatives 101 Tools for Enhancing Asset Allocation ALTERNATIVES 101: TOOLS FOR ENHANCING ASSET ALLOCATION 1 Your financial advisor may recommend an alternative investment to enhance your portfolio s

Alternatives 101 Tools for Enhancing Asset Allocation ALTERNATIVES 101: TOOLS FOR ENHANCING ASSET ALLOCATION 1 Your financial advisor may recommend an alternative investment to enhance your portfolio s

IASB/FASB Meeting Week beginning 11 April 2011. Top down approaches to discount rates

IASB/FASB Meeting Week beginning 11 April 2011 IASB Agenda reference 5A FASB Agenda Staff Paper reference 63A Contacts Matthias Zeitler [email protected] +44 (0)20 7246 6453 Shayne Kuhaneck [email protected]

IASB/FASB Meeting Week beginning 11 April 2011 IASB Agenda reference 5A FASB Agenda Staff Paper reference 63A Contacts Matthias Zeitler [email protected] +44 (0)20 7246 6453 Shayne Kuhaneck [email protected]

I.e., the return per dollar from investing in the shares from time 0 to time 1,

XVII. SECURITY PRICING AND SECURITY ANALYSIS IN AN EFFICIENT MARKET Consider the following somewhat simplified description of a typical analyst-investor's actions in making an investment decision. First,

XVII. SECURITY PRICING AND SECURITY ANALYSIS IN AN EFFICIENT MARKET Consider the following somewhat simplified description of a typical analyst-investor's actions in making an investment decision. First,

C Evolution General Brochure 1114:C Gen Evolution Broch 0314 24/11/2014 12:22 Page 1 Evolution Strategy

Evolution Strategy Introduction to Chryson Chryson is a boutique stockbroking firm, operating from Glasgow. We are regulated by the Financial Conduct Authority, reference 491208, and have been trading

Evolution Strategy Introduction to Chryson Chryson is a boutique stockbroking firm, operating from Glasgow. We are regulated by the Financial Conduct Authority, reference 491208, and have been trading

Central Bank of Ireland Macro-prudential policy for residential mortgage lending Consultation Paper CP87

Central Bank of Ireland Macro-prudential policy for residential mortgage lending Consultation Paper CP87 An initial assessment from Genworth Financial The Central Bank ( CB ) published a consultation paper

Central Bank of Ireland Macro-prudential policy for residential mortgage lending Consultation Paper CP87 An initial assessment from Genworth Financial The Central Bank ( CB ) published a consultation paper

Good [morning, afternoon, evening]. I m [name] with [firm]. Today, we will talk about alternative investments.

![Good [morning, afternoon, evening]. I m [name] with [firm]. Today, we will talk about alternative investments.](/thumbs/40/20590846.jpg "Good [morning, afternoon, evening]. I m [name] with [firm]. Today, we will talk about alternative investments.") Good [morning, afternoon, evening]. I m [name] with [firm]. Today, we will talk about alternative investments. Historic economist Benjamin Graham famously said, The essence of investment management is

Good [morning, afternoon, evening]. I m [name] with [firm]. Today, we will talk about alternative investments. Historic economist Benjamin Graham famously said, The essence of investment management is

MACROECONOMIC AND INDUSTRY ANALYSIS VALUATION PROCESS

MACROECONOMIC AND INDUSTRY ANALYSIS VALUATION PROCESS BUSINESS ANALYSIS INTRODUCTION To determine a proper price for a firm s stock, security analyst must forecast the dividend & earnings that can be expected

MACROECONOMIC AND INDUSTRY ANALYSIS VALUATION PROCESS BUSINESS ANALYSIS INTRODUCTION To determine a proper price for a firm s stock, security analyst must forecast the dividend & earnings that can be expected

for Analysing Listed Private Equity Companies

8 Steps for Analysing Listed Private Equity Companies Important Notice This document is for information only and does not constitute a recommendation or solicitation to subscribe or purchase any products.

8 Steps for Analysing Listed Private Equity Companies Important Notice This document is for information only and does not constitute a recommendation or solicitation to subscribe or purchase any products.

Conceptual Framework: What Does the Financial System Do? 1. Financial contracting: Get funds from savers to investors

Conceptual Framework: What Does the Financial System Do? 1. Financial contracting: Get funds from savers to investors Transactions costs Contracting costs (from asymmetric information) Adverse Selection

Conceptual Framework: What Does the Financial System Do? 1. Financial contracting: Get funds from savers to investors Transactions costs Contracting costs (from asymmetric information) Adverse Selection

Catalyst Macro Strategy Fund

Catalyst Macro Strategy Fund MCXAX, MCXCX & MCXIX 2015 Q2 About Catalyst Funds Intelligent Alternatives We strive to provide innovative strategies to support financial advisors and their clients in meeting

Catalyst Macro Strategy Fund MCXAX, MCXCX & MCXIX 2015 Q2 About Catalyst Funds Intelligent Alternatives We strive to provide innovative strategies to support financial advisors and their clients in meeting

Monetary policy assessment of 13 September 2007 SNB aiming to calm the money market

Communications P.O. Box, CH-8022 Zurich Telephone +41 44 631 31 11 Fax +41 44 631 39 10 Zurich, 13 September 2007 Monetary policy assessment of 13 September 2007 SNB aiming to calm the money market The

Communications P.O. Box, CH-8022 Zurich Telephone +41 44 631 31 11 Fax +41 44 631 39 10 Zurich, 13 September 2007 Monetary policy assessment of 13 September 2007 SNB aiming to calm the money market The

Senior Floating Rate Loans

Senior floating rate loans have become a staple of the U.S. debt market and have grown from a market value of $126 billion in 2001 to $607 billion as of year-end 2011. 1 For over 20 years, managed senior

Senior floating rate loans have become a staple of the U.S. debt market and have grown from a market value of $126 billion in 2001 to $607 billion as of year-end 2011. 1 For over 20 years, managed senior

Solutions Platform & Due Diligence Executing from the foundation of strategic asset allocation

Solutions Platform & Due Diligence Executing from the foundation of strategic asset allocation We emphasize a thorough, disciplined process designed to identify and monitor what we believe to be the best

Solutions Platform & Due Diligence Executing from the foundation of strategic asset allocation We emphasize a thorough, disciplined process designed to identify and monitor what we believe to be the best

The package of measures to avoid artificial volatility and pro-cyclicality

The package of measures to avoid artificial volatility and pro-cyclicality Explanation of the measures and the need to include them in the Solvency II framework Contents 1. Key messages 2. Why the package

The package of measures to avoid artificial volatility and pro-cyclicality Explanation of the measures and the need to include them in the Solvency II framework Contents 1. Key messages 2. Why the package

Financial stability, systemic risk & macroprudential supervision: an actuarial perspective

Financial stability, systemic risk & macroprudential supervision: an actuarial perspective Paul Thornton International Actuarial Association Presentation to OECD Insurance and Pensions Committee June 2010

Financial stability, systemic risk & macroprudential supervision: an actuarial perspective Paul Thornton International Actuarial Association Presentation to OECD Insurance and Pensions Committee June 2010

INTRODUCTION TO OPTIONS MARKETS QUESTIONS

INTRODUCTION TO OPTIONS MARKETS QUESTIONS 1. What is the difference between a put option and a call option? 2. What is the difference between an American option and a European option? 3. Why does an option

INTRODUCTION TO OPTIONS MARKETS QUESTIONS 1. What is the difference between a put option and a call option? 2. What is the difference between an American option and a European option? 3. Why does an option

Finanzdienstleistungen (Praxis) Algorithmic Trading

Algorithmic Trading") Finanzdienstleistungen (Praxis) Algorithmic Trading Definition A computer program (Software) A process for placing trade orders like Buy, Sell It follows a defined sequence of instructions At a speed and

Finanzdienstleistungen (Praxis) Algorithmic Trading Definition A computer program (Software) A process for placing trade orders like Buy, Sell It follows a defined sequence of instructions At a speed and

Reducing Opaqueness in Over-the-Counter Markets

Reducing Opaqueness in Over-the-Counter Markets Zhuo Zhong Discussion by Joshua Slive Recent Innovations in Financial Market Structure Bank of Canada Reform of OTC Derivatives Markets Instability in OTC

Reducing Opaqueness in Over-the-Counter Markets Zhuo Zhong Discussion by Joshua Slive Recent Innovations in Financial Market Structure Bank of Canada Reform of OTC Derivatives Markets Instability in OTC

FRBSF ECONOMIC LETTER

FRBSF ECONOMIC LETTER 01-1 April, 01 Commercial Real Estate and Low Interest Rates BY JOHN KRAINER Commercial real estate construction faltered during the 00 recession and has improved only slowly during

FRBSF ECONOMIC LETTER 01-1 April, 01 Commercial Real Estate and Low Interest Rates BY JOHN KRAINER Commercial real estate construction faltered during the 00 recession and has improved only slowly during

A: SGEAX C: SGECX I: SGEIX

A: SGEAX C: SGECX I: SGEIX NOT FDIC INSURED MAY LOSE VALUE NO BANK GUARANTEE Salient Global Equity Fund The investment objective of the Salient Global Equity Fund (the Fund ) is to seek long term capital

A: SGEAX C: SGECX I: SGEIX NOT FDIC INSURED MAY LOSE VALUE NO BANK GUARANTEE Salient Global Equity Fund The investment objective of the Salient Global Equity Fund (the Fund ) is to seek long term capital

Purer return and reduced volatility: Hedging currency risk in international-equity portfolios

Purer return and reduced volatility: Hedging currency risk in international-equity portfolios Currency-hedged exchange-traded funds (ETFs) offer investors a compelling way to access international-equity

Purer return and reduced volatility: Hedging currency risk in international-equity portfolios Currency-hedged exchange-traded funds (ETFs) offer investors a compelling way to access international-equity