CHAPTER 12 AUDITING LONG-LIVED ASSETS: ACQUISITION, USE, IMPAIRMENT, AND DISPOSAL

|

|

|

- Edwin Copeland

- 10 years ago

- Views:

Transcription

1 A U D I T I N G A RISK-BASED APPROACH TO CONDUCTING A QUALITY AUDIT 9 th Edition Karla M. Johnstone Audrey A. Gramling Larry E. Rittenberg CHAPTER 12 AUDITING LONG-LIVED ASSETS: ACQUISITION, USE, IMPAIRMENT, AND DISPOSAL

2 LEARNING OBJECTIVES 1. Identify the significant accounts, disclosures, and relevant assertions in auditing long-lived assets 2. Identify and assess inherent risks of material misstatement associated with long-lived assets 3. Identify and assess fraud risks of material misstatement associated with long-lived assets 4. Identify and assess control risks of material misstatement associated with long-lived assets 12-2

3 LEARNING OBJECTIVES 5. Describe how to use preliminary analytical procedures to identify possible material misstatements associated with long-lived assets 6. Determine appropriate responses to identified risks of material misstatement in auditing long-lived assets 7. Determine appropriate tests of controls and consider the results of tests of controls in auditing long-lived assets 12-3

4 LEARNING OBJECTIVES 8. Determine and apply sufficient appropriate substantive audit procedures in auditing long-lived assets 9. Apply the frameworks for professional decision making and ethical decision making to issues involving the audit of long-lived assets 12-4

5 THE AUDIT OPINION FORMULATION PROCESS 12-5

6 PROFESSIONAL JUDGMENT IN CONTEXT - ACCOUNTING PROBLEMS RELATED TO LONG-LIVED ASSETS AT IGNITE RESTAURANT GROUP Ignite Restaurant Group, after going public in 2012, needed to restate its financial statements to correct errors related to treatment of certain leases IRG planned a fixed-asset accounting review assessing historical asset additions, dispositions, useful lives, and depreciation from 2006 through 2012 IRG reviewed the effectiveness of its internal controls over leases and other fixed assets 12-6

7 PROFESSIONAL JUDGMENT IN CONTEXT - ACCOUNTING PROBLEMS RELATED TO LONG-LIVED ASSETS AT IGNITE RESTAURANT GROUP What types of misstatements occur in long-lived asset accounts? (LO 1, 2, 3) What might motivate management to misstate longlived asset accounts? (LO 3) What controls should be in place to mitigate misstatements associated with long-lived assets? (LO 4) What procedures should an auditor perform when auditing long-lived asset accounts? (LO 5, 6, 7, 8) 12-7

What controls should be in place to mitigate misstatements associated with long-lived assets?")

8 LEARNING OBJECTIVE 1 IDENTIFY THE SIGNIFICANT ACCOUNTS, DISCLOSURES, AND RELEVANT ASSERTIONS IN AUDITING LONG-LIVED ASSETS

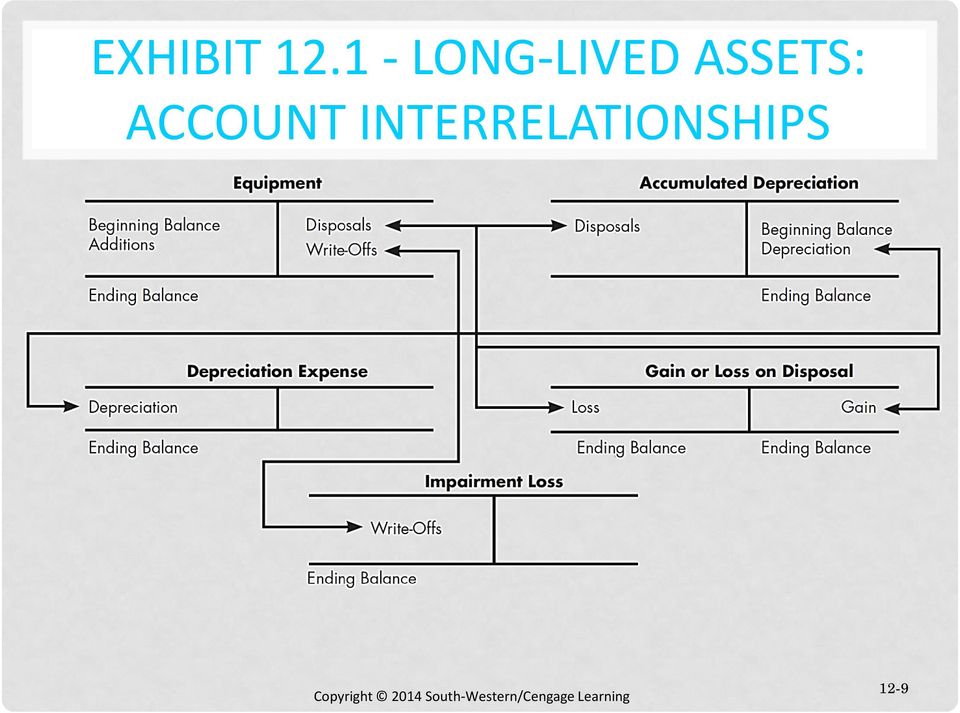

9 EXHIBIT LONG-LIVED ASSETS: ACCOUNT INTERRELATIONSHIPS 12-9

10 SIGNIFICANT ACCOUNTS, DISCLOSURES, AND RELEVANT ASSERTIONS Long-lived assets: Noncurrent assets that are used over multiple operating cycles and include tangible and intangible assets Tangible assets: Have a physical form Machinery, buildings, and land Intangible assets: Have a nonphysical form Patents, trademarks, copyrights, and brand recognition 12-10

11 SIGNIFICANT ACCOUNTS, DISCLOSURES, AND RELEVANT ASSERTIONS Other accounts associated with long-lived assets Related depreciation or impairment expense Related gains caused by disposals Related losses caused by disposals or impairments Accumulated depreciation account Depletion expense: Associated with the extraction of natural resources Amortization expense: Process of expensing acquisition cost minus residual value of intangible assets over their estimated useful economic life 12-11

12 ACTIVITIES IN THE LONG-LIVED ASSET ACQUISITION AND PAYMENT CYCLE Acquisition of long-lived assets is based on organization s planning for long-term productive capacity Such assets are requested and purchased Portion of the asset s cost is then allocated as an expense depending on type of asset Depreciation Amortization Depletion 12-12

13 ACTIVITIES IN THE LONG-LIVED ASSET ACQUISITION AND PAYMENT CYCLE The long-lived tangible and intangible assets are reviewed for possible asset impairment When appropriate, asset is recognized as an impairment loss and written down to its fair value In situations of disposal of assets, companies determine and record the gain or loss on the asset disposal 12-13

14 RELEVANT FINANCIAL STATEMENT Existence or occurrence ASSERTIONS Long-lived assets exist at the balance sheet date The focus is on additions during the year Completeness Long-lived asset account balances include all relevant transactions that have taken place during the period Rights and obligations Organization has ownership rights for the long-lived assets as of balance sheet date Valuation or allocation The recorded balances reflect the balances in accordance with GAAP Presentation and disclosure Long-lived asset balance is reflected on balance sheet in noncurrent section The disclosures for depreciation methods and capital lease terms are adequate 12-14

15 LEARNING OBJECTIVE 2 IDENTIFY AND ASSESS INHERENT RISKS OF MATERIAL MISSTATEMENT ASSOCIATED WITH LONG-LIVED ASSETS

16 IDENTIFYING INHERENT RISKS Asset impairment: Management s recognition that a significant portion of fixed assets is no longer as productive as had originally been expected When assets are so impaired, they should be written down to their expected economic value Factors associated with inherent risk related to asset impairment Management is not interested in identifying and writing down assets Management wants to write down every potentially impaired asset to a minimum realizable value 12-16

17 IDENTIFYING INHERENT RISKS Determining asset impairment requires: Good information system Systematic process and effective controls Professional judgment Incomplete recording of asset disposals Obsolescence of assets Incorrect recording of assets due to complex ownership structures Amortization that does not reflect economic impairment 12-17

18 AUDITOR S AWARENESS OF INHERENT RISKS Knowledge of client s business, industry trends and technological advances Review of various documents, including: Business plan for major acquisitions or changes in the way a company conducts its business Major contracts regarding capital investments or joint ventures with other companies Minutes of board of directors meetings Company filings with the SEC describing company actions, risks, and strategies 12-18

19 AUDITING IN PRACTICE - AUDITING OF LONG-LIVED ASSETS DOES HAVE RISKS Audit of long-lived assets is mechanical in some settings However, the auditor must understand Client s business strategy Current economic conditions Potential changes in the economic value of assets Serious mistakes can be made if auditors always consider long-lived assets a low-risk audit area 12-19

20 INHERENT RISKS ASSOCIATED WITH NATURAL RESOURCES AND INTANGIBLE ASSETS Natural Resources Difficult to identify costs associated with discovery Difficult to estimate commercially available resources to be used in determining a depletion rate Difficult to estimate reclamation cost when the client restores the property Intangible Assets Determination of cost not straightforward Legal costs for obtaining and defending a patent are capital expenditures Cost of patents should be amortized over the lesser of their legal life or their estimated useful life 12-20

21 LEARNING OBJECTIVE 3 IDENTIFY AND ASSESS FRAUD RISKS OF MATERIAL MISSTATEMENT ASSOCIATED WITH LONG-LIVED ASSETS

22 IDENTIFYING FRAUD RISK FACTORS Overstatement of assets through overvaluing existing assets Sales of assets not recorded, and proceeds misappropriated Assets that have been sold not removed from the books Inappropriate residual values assigned to the assets, resulting in miscalculation of depreciation 12-22

23 IDENTIFYING FRAUD RISK FACTORS Amortization of intangible assets miscalculated Costs that should have been expensed improperly capitalized Impairment losses on long-lived assets not recognized Fair value estimates unreasonable 12-23

24 LEARNING OBJECTIVE 4 IDENTIFY AND ASSESS CONTROL RISKS OF MATERIAL MISSTATEMENT ASSOCIATED WITH LONG-LIVED ASSETS

25 TYPICAL CONTROLS AFFECTING MULTIPLE ASSERTIONS FOR LONG-LIVED ASSETS Formal budgeting process with appropriate follow-up variance analysis Written policies for acquisition and disposals of longlived assets, including required approvals Limited physical access to assets, where appropriate Periodic comparison of physical assets to subsidiary records Periodic reconciliations of subsidiary records with the general ledger 12-25

26 AUDITING IN PRACTICE - WORLDCOM WorldCom s management improperly released $984 million in depreciation reserves to increase pretax earnings by decreasing depreciation expense or increasing miscellaneous income Depreciation reserves were created in a variety of ways Cost of equipment returned to vendors for credit after being placed in service was credited to the reserve Unsupported additions to an asset account were recorded with a corresponding increase in the reserve 12-26

27 AUDITING IN PRACTICE - WASTE MANAGEMENT The company s management increased estimated useful lives of all the depreciable assets to increase reported net income Auditors never questioned the change SEC pointed out these estimated useful lives simply were not realistic Waste Management had misstated earnings of $3.5 billion 12-27

28 CONTROLS RELATED TO EXISTENCE/OCCURRENCE AND VALUATION FOR TANGIBLE ASSETS Identify existing assets, inventory them, and reconcile the physical asset inventory with the property ledger on a periodic basis Provide reasonable assurance that all purchases are authorized and properly valued Appropriately classifying new equipment according to its expected use and valuation Periodically reassess appropriateness of depreciation categories 12-28

29 CONTROLS RELATED TO EXISTENCE/OCCURRENCE AND VALUATION FOR TANGIBLE ASSETS Identify obsolete equipment and write the equipment down to scrap value Review management strategy and systematically assess impairment of assets Use serial numbered asset tags, with bar codes for tracking the location, quantity, condition, maintenance, and deprecation status of assets 12-29

30 MANAGEMENT S CONTROLS RELATED TO ASSET IMPAIRMENT JUDGMENTS Systematically identify assets that are not currently in use Projections of future cash flows, by reporting unit, that are based on management s strategic plans and economic conditions Systematically develop current market values of similar assets prepared by the client 12-30

31 CONTROLS OVER NATURAL RESOURCES Most established natural resource companies: Develop procedures and associated internal controls for identifying costs Use geologists to establish an estimate of reserves contained in a new discovery Reassess the amount of reserves as more information becomes available during the course of mining, harvesting, or extracting resources 12-31

32 CONTROLS RELATED TO VALUATION AND PRESENTATION/DISCLOSURE FOR INTANGIBLE ASSETS Provide reasonable assurance that decisions are appropriately made as to when to capitalize or expense research and development expenditures Develop amortization schedules reflecting the remaining useful life of patents or copyrights associated with the asset Identify and account for intangible-asset impairments 12-32

33 EXHIBIT EXAMPLES OF CONTROLS OVER INTANGIBLE LONG-LIVED ASSETS 12-33

34 DOCUMENTING CONTROLS Auditors need to document their understanding of internal controls for integrated and financial statement only audits Auditors can provide documentation in various formats Control matrix Control risk assessment Questionnaire Memo 12-34

35 LEARNING OBJECTIVE 5 DESCRIBE HOW TO USE PRELIMINARY ANALYTICAL PROCEDURES TO IDENTIFY POSSIBLE MATERIAL MISSTATEMENTS ASSOCIATED WITH LONG-LIVED ASSETS

36 RATIO AND TREND ANALYSES Review and analyze gains/losses on disposals of equipment Perform an overall estimate of depreciation expense Compare capital expenditures with the client s capital budget Compare depreciable lives for various asset categories with those of the industry Compare the asset and related expense account balances in the current period to similar items in the prior audit 12-36

37 RATIOS THAT THE AUDITOR SHOULD PLAN TO REVIEW Ratio of depreciation expense to total depreciable long-lived tangible assets Ratio of repairs and maintenance expense to total depreciable long-lived tangible assets Ratio analysis should involve comparison of the unaudited financial statements with both past results and industry trends 12-37

38 RATIO AND TREND ANALYSES If preliminary analytical procedures do not identify any unexpected relationships If unusual or unexpected relationships exist in preliminary analytical procedures Auditor would conclude that there is not a heightened risk of material misstatements in these accounts Planned audit procedures would be adjusted to address the potential material misstatements 12-38

39 LEARNING OBJECTIVE 6 DETERMINE APPROPRIATE RESPONSES TO IDENTIFIED RISKS OF MATERIAL MISSTATEMENT IN AUDITING LONG-LIVED ASSETS

40 RESPONDING TO IDENTIFIED RISKS OF MATERIAL MISSTATEMENT Developing an audit approach that contains tests of controls (if applicable) and substantive procedures If client s controls related to long-lived assets are effective auditor can rely on substantive analytical procedures Auditors should customize their standardized audit program based on the assessment of risk of material misstatement 12-40

41 EXHIBIT PANEL A: SUFFICIENCY OF EVIDENCE FOR EXISTENCE OF EQUIPMENT 12-41

42 EXHIBIT PANEL B: APPROACHES TO OBTAINING AUDIT EVIDENCE FOR EXISTENCE OF EQUIPMENT 12-42

43 ADDITIONAL CONSIDERATIONS Organizations having only a few assets of relatively high value Use of substantive approach, using tests of details, for obtaining evidence rather than performing tests of controls Organizations having a high volume of long-lived asset transactions Perform tests of controls to support a moderate- or low-assessed level of control risk and then reduce substantive testing 12-43

44 LEARNING OBJECTIVE 7 DETERMINE APPROPRIATE TESTS OF CONTROLS AND CONSIDER THE RESULTS OF TESTS OF CONTROLS IN AUDITING LONG-LIVED ASSETS

45 SELECTING CONTROLS TO TEST AND PERFORMING TESTS OF CONTROLS Auditors select both entity-wide and transaction controls for testing Tests of transaction controls Inquiry of personnel performing the control Observation of the control being performed Inspection of documentation confirming that the control has been performed Reperformance of the control by the auditor testing the control 12-45

46 PERFORMING TESTS OF CONTROLS Inquiry - Inquire about the nature of training to a select sample of personnel Observation - Observe property management actions in process Inspection of documentation - Review documentation showing completion of the training 12-46

47 OUTCOMES OF THE RESULTS OF TESTS OF CONTROLS Assess those deficiencies to determine their severity Auditor analyzes results of tests of controls If control deficiencies are identified Modify the preliminary control risk assessment Document the implications of the control deficiencies Determine whether the preliminary assessment of control risk as low is still appropriate If no control deficiencies are identified Determine the extent that controls can provide evidence on the correctness of account balances Determine planned substantive audit procedures 12-47

48 LEARNING OBJECTIVE 8 DETERMINE AND APPLY SUFFICIENT APPROPRIATE SUBSTANTIVE AUDIT PROCEDURES IN AUDITING LONG-LIVED ASSETS

49 ASSURANCES REQUIRED BY AUDITOR IN PERFORMING SUBSTANTIVE PROCEDURES Long-lived assets reflected in balance sheet physically exist Organization has rights of ownership to recorded long-lived assets Long-lived assets include all relevant items, including those that are purchased, contributed, constructed in-house or by third parties, and leases meeting the criteria for capital leases Long-lived asset additions are recorded correctly 12-49

50 ASSURANCES REQUIRED BY AUDITOR IN PERFORMING SUBSTANTIVE PROCEDURES Items to be capitalized are identified and distinguished from repairs and maintenance expense items Depreciation/amortization/depletion calculations are made and based on appropriate estimated useful lives and methods Retirements, trade-ins, and unused property and equipment are identified and recorded correctly 12-50

51 ASSURANCES REQUIRED BY AUDITOR IN PERFORMING SUBSTANTIVE PROCEDURES Long-lived assets and related expenses are appropriately presented in the financial statements with adequate disclosures Fraudulent transactions are not included in the financial statements 12-51

52 EXHIBIT MANAGEMENT ASSERTIONS AND SUBSTANTIVE PROCEDURES FOR LONG-LIVED ASSETS AND RELATED EXPENSES 12-52

53 EXHIBIT MANAGEMENT ASSERTIONS AND SUBSTANTIVE PROCEDURES FOR LONG-LIVED ASSETS AND RELATED EXPENSES 12-53

54 SUBSTANTIVE TESTS OF DETAILS FOR TANGIBLE ASSETS - TESTING CURRENT PERIOD ADDITIONS Auditor examines supporting documentation of individual long-lived asset transactions by examining a schedule of additions After the schedule is agreed to the general ledger, auditor selects sample items for testing Auditor determines that capitalized additions were appropriate and that none of them should have been expensed as repairs and maintenance or other costs 12-54

55 SUBSTANTIVE TESTS OF DETAILS FOR TANGIBLE ASSETS - TESTING CURRENT PERIOD ADDITIONS If auditor perceives that misstatement risks are applicable to a particular client: Procedure adjusted by requesting the client to prepare a schedule of fixed-asset additions and repair and maintenance expense transactions Selected transactions from both schedules can be vouched to: Vendor invoices Work orders Other supporting evidence 12-55

56 AUDITING IN PRACTICE - IMPROPER CAPITALIZATION OF OPERATING EXPENSES Safety-Kleen Corporation s CFO, controller, and vice president of accounting orchestrated an accounting fraud to overstate SK s revenue and earnings One element of the fraud involved the improper capitalization and deferral of operating expenses Safety-Kleen filed for bankruptcy SEC pursued the company and the individuals involved 12-56

57 EXHIBIT SCHEDULE OF LONG-LIVED ASSET ADDITIONS AND DISPOSALS 12-57

58 SUBSTANTIVE TESTS OF DETAILS FOR TANGIBLE ASSET - TESTING CURRENT PERIOD DELETIONS Auditor should: Trace original cost of item and its accumulated depreciation to supporting documentation Recompute any gain or loss to determine whether it is accounted for in conformity with GAAP Perform procedures to search for any unrecorded disposals 12-58

59 SUBSTANTIVE PROCEDURES RELATED TO DEPRECIATION EXPENSE AND ACCUMULATED DEPRECIATION FOR TANGIBLE ASSETS Objective in testing depreciation is to determine: Whether the client is following a consistent depreciation policy and whether the client s calculations are accurate Whether management s estimates are reasonable 12-59

60 LOW RISK: PERFORM SUBSTANTIVE ANALYTICAL PROCEDURES To determine reasonableness of current charges to the accounts, analytical procedures could incorporate a number of ratios and an overall test of reasonableness Ratios can include: Current depreciation expense as a percentage of the previous-year depreciation expense 12-60

61 LOW RISK: PERFORM SUBSTANTIVE ANALYTICAL PROCEDURES Fixed assets as a percentage of previous-year assets Depreciation expense as a percentage of assets each year Accumulated depreciation as a percentage of gross assets each year Average age of assets 12-61

62 HIGH RISK: PERFORM SUBSTANTIVE TESTS OF DETAILS Perform detailed tests of depreciation by starting with the fixed-asset ledger GAS used to foot the ledger and match it to the general ledger Sample of items contained in detailed property ledger taken to recalculate depreciation for items chosen Samples selected considering materiality and risk and based on recorded depreciation Differences are projected to the population as a whole 12-62

63 HIGH RISK: PERFORM SUBSTANTIVE TESTS OF DETAILS If there are significant differences, the auditor: Determines root cause of problem Request that the client correct the problem GAS is used to identify all entries into the depreciation and accumulated depreciation accounts coming from other than normal depreciation entries and asset disposals 12-63

64 EVALUATING CHANGES IN DEPRECIATION METHODS Auditor makes sure that depreciation methods used are consistent with the prior year Unless client has reasonable justification for changing methods Auditor reads notes of the financial statements to be sure that all relevant information regarding changes has been disclosed 12-64

65 AUDIT PROCEDURES FOR DETERMINING THE COST OF NATURAL RESOURCES Test the capitalization of all new natural resources Verify the costs by examining documents including client s own process of documenting all the costs of exploration and drilling Substantiate the amount of items sold during the year 12-65

66 SUBSTANTIVE TESTS OF DETAILS FOR INTANGIBLE ASSETS Determine that such assets exist by reviewing appropriate documentation Determine that the intangible assets are owned by the organization by inspecting relevant documentation Test management s calculation of any gain or loss on disposal of assets and determine proper reduction of carrying amounts 12-66

67 SUBSTANTIVE TESTS OF DETAILS FOR INTANGIBLE ASSETS Determine whether amortization expense is accurate and whether amortization policy and useful lives are reasonable and consistent with prior years Inquire of management whether circumstances indicate that the carrying amounts of intangibles may not be recoverable 12-67

68 EXHIBIT CIRCUMSTANCES INDICATING POTENTIAL IMPAIRMENT OF INTANGIBLE ASSETS 12-68

69 SUBSTANTIVE PROCEDURES RELATED TO ASSET IMPAIRMENT Auditor needs reasonable assurance that: Long-lived assets are valued at their economic benefit to the organization When value has been impaired, the organization has written down the asset If there is evidence that an asset has been impaired, auditor needs to address the valuation issue Understand the process for assessing impairment Evaluate reasonableness of management s assumptions 12-69

70 AUDITING IN PRACTICE - PCAOB IDENTIFIES AUDIT DEFICIENCIES RELATED TO ASSET IMPAIRMENT ISSUES 2010 PCAOB inspection report of Grant Thornton LLP The firm failed to evaluate the effects on the financial statements of the failure to test the assets for impairment 2010 PCAOB inspection report of PricewaterhouseCoopers LLP There was no evidence in audit documentation that the firm had tested certain assumptions such as all machinery and equipment of more than four years old would have a fair value of zero 12-70

71 AUDITING IN PRACTICE - PCAOB IDENTIFIES AUDIT DEFICIENCIES RELATED TO ASSET IMPAIRMENT ISSUES 2010 PCAOB inspection report of McGladrey & Pullen LLP The firm failed to: Evaluate fair value, useful life, and potential impairment of an indefinite-lived intangible asset related to a marketing agreement Test the fair value that issuer assigned to intangible asset Consider the fact that marketing agreement allowed issuer and counterparty to terminate the agreement Consider potential indicators of impairment 12-71

72 SUBSTANTIVE PROCEDURES RELATED TO LEASES Obtain copies of lease agreements, read the agreements, and develop a schedule of lease expenditures Review lease expense account, select entries to the account, and determine if there are entries that are not covered by leases obtained from client Determine if expenses are properly accounted for Review relevant criteria from the FASB s codified standards (ASC) to determine which leases meet the requirement of capital leases 12-72

73 SUBSTANTIVE PROCEDURES RELATED TO LEASES For all capital leases, determine that assets and lease obligations are recorded at their present value Develop a schedule of all future lease obligations or determine whether client s schedule is correct by referring to underlying lease agreements Review client s disclosure of lease obligations to determine that it is in accordance with GAAP 12-73

74 PERFORMING SUBSTANTIVE FRAUD- RELATED PROCEDURES Physically inspect tangible assets and agree serial numbers with supporting documentation Request client to perform a complete inventory of long-lived assets at year end Scrutinize appraisals and other specialist reports that seem out of line with reasonable expectations, and challenge the underlying assumptions 12-74

75 PERFORMING SUBSTANTIVE FRAUD- RELATED PROCEDURES Use the work of a specialist for asset valuations and impairments When vouching long-lived asset additions, accept only original invoices, purchase orders, receiving reports or similar supporting documentation Confirm terms of significant additions of property or intangibles with other parties involved 12-75

76 DOCUMENTING SUBSTANTIVE For tangible assets PROCEDURES Summary schedule showing: Beginning balances Additions and deletions Ending balances for the asset account and for accumulated depreciation Identification of the specific items tested For intangible assets - Evidence supporting review of the reasonableness of their continuing value 12-76

CHAPTER 13 AUDITING DEBT OBLIGATIONS AND STOCKHOLDERS EQUITY TRANSACTIONS

A U D I T I N G A RISK-BASED APPROACH TO CONDUCTING A QUALITY AUDIT 9 th Edition Karla M. Johnstone Audrey A. Gramling Larry E. Rittenberg CHAPTER 13 AUDITING DEBT OBLIGATIONS AND STOCKHOLDERS EQUITY TRANSACTIONS

A U D I T I N G A RISK-BASED APPROACH TO CONDUCTING A QUALITY AUDIT 9 th Edition Karla M. Johnstone Audrey A. Gramling Larry E. Rittenberg CHAPTER 13 AUDITING DEBT OBLIGATIONS AND STOCKHOLDERS EQUITY TRANSACTIONS

CHAPTER 9 AUDITING THE REVENUE CYCLE

A U D I T I N G A RISK-BASED APPROACH TO CONDUCTING A QUALITY AUDIT 9 th Edition Karla M. Johnstone Audrey A. Gramling Larry E. Rittenberg CHAPTER 9 AUDITING THE REVENUE CYCLE LEARNING OBJECTIVES 1. Identify

A U D I T I N G A RISK-BASED APPROACH TO CONDUCTING A QUALITY AUDIT 9 th Edition Karla M. Johnstone Audrey A. Gramling Larry E. Rittenberg CHAPTER 9 AUDITING THE REVENUE CYCLE LEARNING OBJECTIVES 1. Identify

Audit Program for Fixed Assets

Form AP 35 Index Audit Program for Fixed Assets Legal Company Name Client: Balance Sheet Date: Instructions: The auditor should refer to the audit planning documentation to gain an understanding of the

Form AP 35 Index Audit Program for Fixed Assets Legal Company Name Client: Balance Sheet Date: Instructions: The auditor should refer to the audit planning documentation to gain an understanding of the

How To Find Out If A Company Misstatement Is True

A U D I T I N G A RISK-BASED APPROACH TO CONDUCTING A QUALITY AUDIT 9 th Edition Karla M. Johnstone Audrey A. Gramling Larry E. Rittenberg CHAPTER 11 AUDITING INVENTORY, GOODS AND SERVICES, AND ACCOUNTS

A U D I T I N G A RISK-BASED APPROACH TO CONDUCTING A QUALITY AUDIT 9 th Edition Karla M. Johnstone Audrey A. Gramling Larry E. Rittenberg CHAPTER 11 AUDITING INVENTORY, GOODS AND SERVICES, AND ACCOUNTS

10-1. Auditing Business Process. Objectives Understand the Auditing of the Enteties Business. Process

10-1 Auditing Business Process Auditing Business Process Objectives Understand the Auditing of the Enteties Business Process Identify the types of transactions in different Business Process Asses Control

10-1 Auditing Business Process Auditing Business Process Objectives Understand the Auditing of the Enteties Business Process Identify the types of transactions in different Business Process Asses Control

Accounting 408 Test 3b Section Row

Accounting 408 Test 3b Name Section Row Multiple Choice. (2 points each) Read the following questions carefully and indicate the one best answer to each question by placing an X (do not circle) over the

Accounting 408 Test 3b Name Section Row Multiple Choice. (2 points each) Read the following questions carefully and indicate the one best answer to each question by placing an X (do not circle) over the

AUDIT PLAN: RECEIVABLES

Audit procedures for receivables AUDIT PLAN: RECEIVABLES Completeness Agree the balance from the individual sales ledger accounts to the aged receivables listing and vice versa. Match the total of the

Audit procedures for receivables AUDIT PLAN: RECEIVABLES Completeness Agree the balance from the individual sales ledger accounts to the aged receivables listing and vice versa. Match the total of the

Audit Program for Prepaid Expenses and Other Assets

Form AP 20 Index Audit Program for Prepaid Expenses and Other Assets Legal Company Name Client: Balance Sheet Date: Instructions: The auditor should refer to the audit planning documentation to gain an

Form AP 20 Index Audit Program for Prepaid Expenses and Other Assets Legal Company Name Client: Balance Sheet Date: Instructions: The auditor should refer to the audit planning documentation to gain an

Inspection Observations Related to PCAOB "Risk Assessment" Auditing Standards (No. 8 through No.15)

") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org Inspection Observations Related to PCAOB "Risk Assessment" Auditing Standards (No. 8 through

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org Inspection Observations Related to PCAOB "Risk Assessment" Auditing Standards (No. 8 through

Understanding the Entity and Its Environment and Assessing the Risks of Material Misstatement

Understanding the Entity and Its Environment 1667 AU Section 314 Understanding the Entity and Its Environment and Assessing the Risks of Material Misstatement (Supersedes SAS No. 55.) Source: SAS No. 109.

Understanding the Entity and Its Environment 1667 AU Section 314 Understanding the Entity and Its Environment and Assessing the Risks of Material Misstatement (Supersedes SAS No. 55.) Source: SAS No. 109.

RELEVANT TO FOUNDATION LEVEL PAPER FAU / ACCA QUALIFICATION PAPER F8

RELEVANT TO FOUNDATION LEVEL PAPER FAU / ACCA QUALIFICATION PAPER F8 Audit procedures Audit procedures are an important area of the syllabus, though candidates often use inappropriate audit procedures

RELEVANT TO FOUNDATION LEVEL PAPER FAU / ACCA QUALIFICATION PAPER F8 Audit procedures Audit procedures are an important area of the syllabus, though candidates often use inappropriate audit procedures

Chapter 15: Accounts Payable and Purchases

Accounting Research Manager - Audit Private Accounting Research Manager Miller Interpretations and Other Resources Knowledge-Based Audit Procedures Chapter 15: Accounts Payable and Purchases Chapter 15:

Accounting Research Manager - Audit Private Accounting Research Manager Miller Interpretations and Other Resources Knowledge-Based Audit Procedures Chapter 15: Accounts Payable and Purchases Chapter 15:

Fixed assets are inherently risky and deserve close attention for a number of reasons:

The balance sheet approach In this approach, substantive procedures are focused on statement of financial position accounts, with only very limited procedures being carried out on income statement/ profit

The balance sheet approach In this approach, substantive procedures are focused on statement of financial position accounts, with only very limited procedures being carried out on income statement/ profit

CHAPTER 8 SPECIALIZED AUDIT TOOLS: SAMPLING AND GENERALIZED AUDIT SOFTWARE

A U D I T I N G A RISK-BASED APPROACH TO CONDUCTING A QUALITY AUDIT 9 th Edition Karla M. Johnstone Audrey A. Gramling Larry E. Rittenberg CHAPTER 8 SPECIALIZED AUDIT TOOLS: SAMPLING AND GENERALIZED AUDIT

A U D I T I N G A RISK-BASED APPROACH TO CONDUCTING A QUALITY AUDIT 9 th Edition Karla M. Johnstone Audrey A. Gramling Larry E. Rittenberg CHAPTER 8 SPECIALIZED AUDIT TOOLS: SAMPLING AND GENERALIZED AUDIT

Long-Lived Assets. 1. How the matching principle underlies the methods used to account for long-lived assets.

CHAPTER 9 Long-Lived Assets SYNOPSIS In this chapter, the author discusses (1) accounting for the acquisition, use, and disposal of long-lived assets, and (2) management's incentives for selecting accounting

CHAPTER 9 Long-Lived Assets SYNOPSIS In this chapter, the author discusses (1) accounting for the acquisition, use, and disposal of long-lived assets, and (2) management's incentives for selecting accounting

Audit Toolbox part 1: Property, Plant and Equipment & Cash

Audit Toolbox part 1: Property, Plant and Equipment & Cash Vienna, February 12, 2014 Atanasko Atanasovski, Consultant, CFRR Substantive testing - Property, plant and equipment Key areas when testing tangible

Audit Toolbox part 1: Property, Plant and Equipment & Cash Vienna, February 12, 2014 Atanasko Atanasovski, Consultant, CFRR Substantive testing - Property, plant and equipment Key areas when testing tangible

Report on. 2010 Inspection of PricewaterhouseCoopers LLP (Headquartered in New York, New York) Public Company Accounting Oversight Board

Public Company Accounting Oversight Board") 1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2010 (Headquartered in New York, New York) Issued by the Public Company Accounting

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8433 www.pcaobus.org Report on 2010 (Headquartered in New York, New York) Issued by the Public Company Accounting

Performing Audit Procedures in Response to Assessed Risks and Evaluating the Audit Evidence Obtained

Performing Audit Procedures in Response to Assessed Risks 1781 AU Section 318 Performing Audit Procedures in Response to Assessed Risks and Evaluating the Audit Evidence Obtained (Supersedes SAS No. 55.)

Performing Audit Procedures in Response to Assessed Risks 1781 AU Section 318 Performing Audit Procedures in Response to Assessed Risks and Evaluating the Audit Evidence Obtained (Supersedes SAS No. 55.)

A&W Food Services of Canada Inc. Consolidated Financial Statements December 30, 2012 and January 1, 2012 (in thousands of dollars)

") A&W Food Services of Canada Inc. Consolidated Financial Statements December 30, and January 1, (in thousands of dollars) February 12, 2013 Independent Auditor s Report To the Shareholders of A&W Food Services

A&W Food Services of Canada Inc. Consolidated Financial Statements December 30, and January 1, (in thousands of dollars) February 12, 2013 Independent Auditor s Report To the Shareholders of A&W Food Services

Part II. Audit process by phase 3. Testing and evidence

Part II. Audit process by phase 3. Testing and evidence Quiz 1: The quality of audit evidence depends on whether it is relevant and reliable in supporting the conclusions of the auditor, and normally the

Part II. Audit process by phase 3. Testing and evidence Quiz 1: The quality of audit evidence depends on whether it is relevant and reliable in supporting the conclusions of the auditor, and normally the

Auditing Module 7 June 2009. Suggested Solutions

Auditing Module 7 June 2009 Suggested Solutions 1 Question 1 1. Tests of control are tests carried out to obtain assurance about the operating and effectiveness of controls. An example of such a test would

Auditing Module 7 June 2009 Suggested Solutions 1 Question 1 1. Tests of control are tests carried out to obtain assurance about the operating and effectiveness of controls. An example of such a test would

NINTH EDITION A RISK-BASED APPROACH TO CONDUCTING A QUALITY AUDIT

NINTH EDITION AUDITING A RISK-BASED APPROACH TO CONDUCTING A QUALITY AUDIT Kar la M. Johnstone University of Wisconsin Madison Audrey A. Gramling Bellarmine University Larry E. Rittenberg University of

NINTH EDITION AUDITING A RISK-BASED APPROACH TO CONDUCTING A QUALITY AUDIT Kar la M. Johnstone University of Wisconsin Madison Audrey A. Gramling Bellarmine University Larry E. Rittenberg University of

Chapter 15 Auditing the Expenditure Cycle

Chapter 15 Auditing the Expenditure Cycle Expenditure cycle consists of activities related to the acquisition of and payment for plant assets and goods and services. Two major transaction classes: 1 purchases

Chapter 15 Auditing the Expenditure Cycle Expenditure cycle consists of activities related to the acquisition of and payment for plant assets and goods and services. Two major transaction classes: 1 purchases

Audit Risk and Materiality in Conducting an Audit

Audit Risk and Materiality in Conducting an Audit 1647 AU Section 312 Audit Risk and Materiality in Conducting an Audit (Supersedes SAS No. 47.) Source: SAS No. 107. See section 9312 for interpretations

Audit Risk and Materiality in Conducting an Audit 1647 AU Section 312 Audit Risk and Materiality in Conducting an Audit (Supersedes SAS No. 47.) Source: SAS No. 107. See section 9312 for interpretations

ACCOUNTING FOR AND AUDIT OF PROPERTY, PLANT AND EQUIPMENT

ACCOUNTING FOR AND AUDIT OF PROPERTY, PLANT AND EQUIPMENT PRESENTED BY SOLOMON SIMEON MANAGER: PEAK PROFESSIONAL SERVICES IN HOUSE SEMINAR SERIES NO 2 PEAK PROFESSIONAL SERVICES (CHARTERED ACCOUNTANTS)

ACCOUNTING FOR AND AUDIT OF PROPERTY, PLANT AND EQUIPMENT PRESENTED BY SOLOMON SIMEON MANAGER: PEAK PROFESSIONAL SERVICES IN HOUSE SEMINAR SERIES NO 2 PEAK PROFESSIONAL SERVICES (CHARTERED ACCOUNTANTS)

Information about 2015 Inspections

Vol. 2015/2 October 2015 Staff Inspection Brief The staff of the Public Company Accounting Oversight Board ( PCAOB or Board ) prepares Inspection Briefs to assist auditors, audit committees, investors,

Vol. 2015/2 October 2015 Staff Inspection Brief The staff of the Public Company Accounting Oversight Board ( PCAOB or Board ) prepares Inspection Briefs to assist auditors, audit committees, investors,

Manual of Accounting and Financial Reporting for Pennsylvania Public Schools CHAPTER 11 TABLE OF CONTENTS 11.A. Chapter 11 11.1

Manual of Accounting and Financial Reporting for Pennsylvania Public Schools CHAPTER 11 TABLE OF CONTENTS 11.1 Capital Assets And Infrastructure 11.1 What Are Capital Assets? 11.1 Valuation Of Capital

Manual of Accounting and Financial Reporting for Pennsylvania Public Schools CHAPTER 11 TABLE OF CONTENTS 11.1 Capital Assets And Infrastructure 11.1 What Are Capital Assets? 11.1 Valuation Of Capital

Substantive Tests of Transactions and Balances

10 CHAPTER Substantive Tests of Transactions and Balances LEARNING OBJECTIVES After studying this chapter you should be able to: 1 2 identify and distinguish between tests of controls and substantive tests

10 CHAPTER Substantive Tests of Transactions and Balances LEARNING OBJECTIVES After studying this chapter you should be able to: 1 2 identify and distinguish between tests of controls and substantive tests

Illustrative Financial Statements Prepared Using the Financial Reporting Framework for Small- and Medium-Entities

Illustrative Financial Statements Prepared Using the Financial Reporting Framework for Small- and Medium-Entities Illustrative Financial Statements This component of the toolkit contains sample financial

Illustrative Financial Statements Prepared Using the Financial Reporting Framework for Small- and Medium-Entities Illustrative Financial Statements This component of the toolkit contains sample financial

SCHEDULES OF CHAPTER 40B MAXIMUM ALLOWABLE PROFIT FROM SALES AND TOTAL CHAPTER 40B COSTS EXAMINATION PROGRAM

7/30/07 SCHEDULES OF CHAPTER 40B MAXIMUM ALLOWABLE PROFIT FROM SALES AND TOTAL CHAPTER 40B COSTS Instructions: EXAMINATION PROGRAM This Model Program lists the major procedures and steps that should be

7/30/07 SCHEDULES OF CHAPTER 40B MAXIMUM ALLOWABLE PROFIT FROM SALES AND TOTAL CHAPTER 40B COSTS Instructions: EXAMINATION PROGRAM This Model Program lists the major procedures and steps that should be

Auditing Derivative Instruments, Hedging Activities, and Investments in Securities 1

Auditing Derivative Instruments 1915 AU Section 332 Auditing Derivative Instruments, Hedging Activities, and Investments in Securities 1 (Supersedes SAS No. 81.) Source: SAS No. 92. See section 9332 for

Auditing Derivative Instruments 1915 AU Section 332 Auditing Derivative Instruments, Hedging Activities, and Investments in Securities 1 (Supersedes SAS No. 81.) Source: SAS No. 92. See section 9332 for

Communicating Internal Control Related Matters Identified in an Audit

Communicating Internal Control 1843 AU Section 325 Communicating Internal Control Related Matters Identified in an Audit (Supersedes SAS No. 112.) Source: SAS No. 115. Effective for audits of financial

Communicating Internal Control 1843 AU Section 325 Communicating Internal Control Related Matters Identified in an Audit (Supersedes SAS No. 112.) Source: SAS No. 115. Effective for audits of financial

AUDIT PROCEDURES RECEIVABLE AND SALES

184 AUDIT PROCEDURES RECEIVABLE AND SALES Ștefan Zuca Abstract The overall objective of the audit of accounts receivable and sales is to determine if they are fairly presented in the context of the financial

184 AUDIT PROCEDURES RECEIVABLE AND SALES Ștefan Zuca Abstract The overall objective of the audit of accounts receivable and sales is to determine if they are fairly presented in the context of the financial

Audit Program for Accounts Payable and Purchases

Form AP 50 Index Audit Program for Accounts Payable and Purchases Legal Company Name Client: Balance Sheet Date: Instructions: The auditor should refer to the audit planning documentation to gain an understanding

Form AP 50 Index Audit Program for Accounts Payable and Purchases Legal Company Name Client: Balance Sheet Date: Instructions: The auditor should refer to the audit planning documentation to gain an understanding

INTERNATIONAL STANDARD ON AUDITING (UK AND IRELAND) 315

315") INTERNATIONAL STANDARD ON AUDITING (UK AND IRELAND) 315 IDENTIFYING AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT THROUGH UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT (Effective for audits of financial

INTERNATIONAL STANDARD ON AUDITING (UK AND IRELAND) 315 IDENTIFYING AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT THROUGH UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT (Effective for audits of financial

Accounting Norms and Principles January 7, 2003

1 Accounting Norms and Principles January 7, 2003 The purpose of an accounting system is to provide credit union management with complete and accurate financial information that can be used to operate

1 Accounting Norms and Principles January 7, 2003 The purpose of an accounting system is to provide credit union management with complete and accurate financial information that can be used to operate

Dear Members, The Directors have pleasure in presenting their Annual Report and Audited Accounts for the year ended March 31, 2015.

DIRECTORS REPORT Dear Members, The Directors have pleasure in presenting their Annual Report and Audited Accounts for the year ended March 31, 2015. 1. FINANCIAL HIGHLIGHTS: Particulars 2014-2015 2013-2014

DIRECTORS REPORT Dear Members, The Directors have pleasure in presenting their Annual Report and Audited Accounts for the year ended March 31, 2015. 1. FINANCIAL HIGHLIGHTS: Particulars 2014-2015 2013-2014

CITY OF PORT ST LUCIE FINANCIAL POLICY CAPITAL ASSETS

CITY OF PORT ST LUCIE FINANCIAL POLICY CAPITAL ASSETS I. PURPOSE To provide effective guidelines for the recording, tracking, capitalizing, and safeguarding of the City's Capital assets. II. POLICY In

CITY OF PORT ST LUCIE FINANCIAL POLICY CAPITAL ASSETS I. PURPOSE To provide effective guidelines for the recording, tracking, capitalizing, and safeguarding of the City's Capital assets. II. POLICY In

FASB Issues PCC Alternative for Identifiable Intangible Assets in a Business Combination

FASB Issues PCC Alternative for Identifiable Intangible Assets in a Business Combination February 25, 2015 Highlights of the Update In This Update Highlights of the Update... 1 Appendix A Frequently Asked

FASB Issues PCC Alternative for Identifiable Intangible Assets in a Business Combination February 25, 2015 Highlights of the Update In This Update Highlights of the Update... 1 Appendix A Frequently Asked

How To Audit A Company

1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202)862-8430 www.pcaobus.org STAFF AUDIT PRACTICE ALERT NO. 11 CONSIDERATIONS FOR AUDITS OF INTERNAL CONTROL OVER FINANCIAL

1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202)862-8430 www.pcaobus.org STAFF AUDIT PRACTICE ALERT NO. 11 CONSIDERATIONS FOR AUDITS OF INTERNAL CONTROL OVER FINANCIAL

The Use of Assertions by Auditor

E. AUDIT EVIDENCE 1. The Use of Assertions by Auditor 2. Audit Procedures 3. The Audit of Specific Items 4. Audit Sampling and Other means of Testing 5. Computer-Assisted Audit Techniques 6. Not-for-Profit

E. AUDIT EVIDENCE 1. The Use of Assertions by Auditor 2. Audit Procedures 3. The Audit of Specific Items 4. Audit Sampling and Other means of Testing 5. Computer-Assisted Audit Techniques 6. Not-for-Profit

Chapter 9. Plant Assets. Determining the Cost of Plant Assets

Chapter 9 Plant Assets Plant Assets are also called fixed assets; property, plant and equipment; plant and equipment; long-term assets; operational assets; and long-lived assets. They are characterized

Chapter 9 Plant Assets Plant Assets are also called fixed assets; property, plant and equipment; plant and equipment; long-term assets; operational assets; and long-lived assets. They are characterized

Audit Evidence. AU Section 326. Introduction. Concept of Audit Evidence AU 326.03

Audit Evidence 1859 AU Section 326 Audit Evidence (Supersedes SAS No. 31.) Source: SAS No. 106. See section 9326 for interpretations of this section. Effective for audits of financial statements for periods

Audit Evidence 1859 AU Section 326 Audit Evidence (Supersedes SAS No. 31.) Source: SAS No. 106. See section 9326 for interpretations of this section. Effective for audits of financial statements for periods

CHAPTER 12. Intangible Assets 1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12, 13, 14 9, 10, 13, 14, 25. 3. Goodwill. 12, 13, 14, 18 6, 8 6, 12, 13, 15

CHAPTER 12 Intangible Assets ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Intangible assets; concepts, definitions; items comprising

CHAPTER 12 Intangible Assets ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Intangible assets; concepts, definitions; items comprising

Management Representations

Management Representations 1941 AU Section 333 Management Representations (Supersedes SAS No. 19.) Source: SAS No. 85; SAS No. 89; SAS No. 99; SAS No. 113. See section 9333 for interpretations of this

Management Representations 1941 AU Section 333 Management Representations (Supersedes SAS No. 19.) Source: SAS No. 85; SAS No. 89; SAS No. 99; SAS No. 113. See section 9333 for interpretations of this

PBL: Accounting for Professionals. Competency: Accounts Concepts, Principles, Terminology

Competency: Accounts Concepts, Principles, Terminology 1. Identify and apply Generally Accepted Accounting Principles (GAAP). 2. Apply the steps in the Accounting cycle. 3. Post and analyze transactions

Competency: Accounts Concepts, Principles, Terminology 1. Identify and apply Generally Accepted Accounting Principles (GAAP). 2. Apply the steps in the Accounting cycle. 3. Post and analyze transactions

PROPERTY AND EQUIPMENT

PROPERTY AND EQUIPMENT Policy: Purchases or acquisitions of property, plant, and equipment shall be properly authorized and accurate records shall be maintained for cost/ acquisition value and accumulated

PROPERTY AND EQUIPMENT Policy: Purchases or acquisitions of property, plant, and equipment shall be properly authorized and accurate records shall be maintained for cost/ acquisition value and accumulated

Appendix A. Specific Learning Objectives by Course

Appendix A by Course MGMT 0630: Foundations in Ethics: Applications to Business and the CPA Profession Identify the regulatory bodies that regulate the CPA profession. Discuss the Code of Professional

Appendix A by Course MGMT 0630: Foundations in Ethics: Applications to Business and the CPA Profession Identify the regulatory bodies that regulate the CPA profession. Discuss the Code of Professional

Dumfries Mutual Insurance Company Financial Statements For the year ended December 31, 2010

Dumfries Mutual Insurance Company Financial Statements For the year ended December 31, 2010 Contents Independent Auditors' Report 2 Financial Statements Balance Sheet 3 Statement of Operations and Unappropriated

Dumfries Mutual Insurance Company Financial Statements For the year ended December 31, 2010 Contents Independent Auditors' Report 2 Financial Statements Balance Sheet 3 Statement of Operations and Unappropriated

ONLINE VACATION CENTER HOLDINGS CORP. CONSOLIDATED FINANCIAL STATEMENTS December 31, 2013

ONLINE VACATION CENTER HOLDINGS CORP. CONSOLIDATED FINANCIAL STATEMENTS Fort Lauderdale, Florida CONSOLIDATED FINANCIAL STATEMENTS CONTENTS INDEPENDENT AUDITORS REPORT... 1 FINANCIAL STATEMENTS CONSOLIDATED

ONLINE VACATION CENTER HOLDINGS CORP. CONSOLIDATED FINANCIAL STATEMENTS Fort Lauderdale, Florida CONSOLIDATED FINANCIAL STATEMENTS CONTENTS INDEPENDENT AUDITORS REPORT... 1 FINANCIAL STATEMENTS CONSOLIDATED

Investments and advances... 313,669

Consolidated Financial Statements of the Company The consolidated balance sheet, statement of income, and statement of equity of the Company are as follows. Please note the Company s consolidated financial

Consolidated Financial Statements of the Company The consolidated balance sheet, statement of income, and statement of equity of the Company are as follows. Please note the Company s consolidated financial

Auditing Accounting Estimates

Auditing Accounting Estimates 2057 AU Section 342 Auditing Accounting Estimates Source: SAS No. 57; SAS No. 113. See section 9342 for interpretations of this section. Effective for audits of financial

Auditing Accounting Estimates 2057 AU Section 342 Auditing Accounting Estimates Source: SAS No. 57; SAS No. 113. See section 9342 for interpretations of this section. Effective for audits of financial

2012 AICPA Newly Released Questions Auditing

Following are multiple choice questions recently released by the AICPA. These questions were released by the AICPA with letter answers only. Our editorial board has provided the accompanying explanation.

Following are multiple choice questions recently released by the AICPA. These questions were released by the AICPA with letter answers only. Our editorial board has provided the accompanying explanation.

Article: Control Systems and Controls Testing: General Review

Article: Control Systems and Controls Testing: General Review By: Paul Lydon, BA, CPA, MBS (Hons), PGCLTHE, FHEA Current Examiner in P1 Auditing The main duty of auditors is to report to the members on

Article: Control Systems and Controls Testing: General Review By: Paul Lydon, BA, CPA, MBS (Hons), PGCLTHE, FHEA Current Examiner in P1 Auditing The main duty of auditors is to report to the members on

CHAPTER 12. Intangible Assets 1, 2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12, 13, 14, 25. 3. Goodwill. 12, 13, 14, 18 5, 8, 9 12, 13, 15 5, 6

CHAPTER 12 Intangible Assets ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Intangible assets; concepts, definitions; items comprising

CHAPTER 12 Intangible Assets ASSIGNMENT CLASSIFICATION TABLE (BY TOPIC) Topics Questions Brief Exercises Exercises Problems Concepts for Analysis 1. Intangible assets; concepts, definitions; items comprising

Fixed Asset Inventory

Fixed Asset Inventory The purpose of the district-wide fixed asset inventory system is to gather information for the preparation of financial statements, including estimated annual depreciation costs of

Fixed Asset Inventory The purpose of the district-wide fixed asset inventory system is to gather information for the preparation of financial statements, including estimated annual depreciation costs of

Chapter 18 Auditing Investments and Cash Balances

Chapter 18 Auditing Investments and Cash Balances General Considerations Cash balances include undeposited receipts on hand, cash in bank in unrestricted accounts, and imprest accounts such as petty cash

Chapter 18 Auditing Investments and Cash Balances General Considerations Cash balances include undeposited receipts on hand, cash in bank in unrestricted accounts, and imprest accounts such as petty cash

Consideration of Fraud in a Financial Statement Audit

Consideration of Fraud in a Financial Statement Audit 1719 AU Section 316 Consideration of Fraud in a Financial Statement Audit (Supersedes SAS No. 82.) Source: SAS No. 99; SAS No. 113. Effective for audits

Consideration of Fraud in a Financial Statement Audit 1719 AU Section 316 Consideration of Fraud in a Financial Statement Audit (Supersedes SAS No. 82.) Source: SAS No. 99; SAS No. 113. Effective for audits

In-Depth Guide to Public Company Auditing: The Financial Statement Audit

In-Depth Guide to Public Company Auditing: The Financial Statement Audit Why an In-Depth Guide to Public Company Auditing? The foundation for confidence in U.S. capital markets is strengthened through

In-Depth Guide to Public Company Auditing: The Financial Statement Audit Why an In-Depth Guide to Public Company Auditing? The foundation for confidence in U.S. capital markets is strengthened through

Stages of the Audit Process

Chapter 5 Stages of the Audit Process Learning Objectives Upon completion of this chapter you should be able to explain: LO 1 Explain the audit process. LO 2 Accept a new client or confirming the continuance

Chapter 5 Stages of the Audit Process Learning Objectives Upon completion of this chapter you should be able to explain: LO 1 Explain the audit process. LO 2 Accept a new client or confirming the continuance

Consolidated Financial Statements of THE CANADIAN RED CROSS SOCIETY

Consolidated Financial Statements of THE CANADIAN RED CROSS SOCIETY March 31, 2013 and 2012 Deloitte LLP 800-100 Queen Street Ottawa, ON K1P 5T8 Canada Tel: (613) 236 2442 Fax: (613) 236 2195 www.deloitte.ca

Consolidated Financial Statements of THE CANADIAN RED CROSS SOCIETY March 31, 2013 and 2012 Deloitte LLP 800-100 Queen Street Ottawa, ON K1P 5T8 Canada Tel: (613) 236 2442 Fax: (613) 236 2195 www.deloitte.ca

CONSOLIDATED FINANCIAL STATEMENTS

CONSOLIDATED FINANCIAL STATEMENTS TABLE OF CONTENTS MANAGEMENT S STATEMENT OF RESPONSIBILITY FOR FINANCIAL REPORTING 65 INDEPENDENT AUDITOR S REPORT 66 CONSOLIDATED FINANCIAL STATEMENTS 67 Consolidated

CONSOLIDATED FINANCIAL STATEMENTS TABLE OF CONTENTS MANAGEMENT S STATEMENT OF RESPONSIBILITY FOR FINANCIAL REPORTING 65 INDEPENDENT AUDITOR S REPORT 66 CONSOLIDATED FINANCIAL STATEMENTS 67 Consolidated

U S I N G D A T A A N A L Y S I S T O M E E T T H E R E Q U I R E M E N T S O F R I S K B A S E D A U D I T I N G S T A N D A R D S

U S I N G D A T A A N A L Y S I S T O M E E T T H E R E Q U I R E M E N T S O F R I S K B A S E D A U D I T I N G S T A N D A R D S A C a s e W a r e I D E A R e s e a r c h R e p o r t CaseWare IDEA Inc.

U S I N G D A T A A N A L Y S I S T O M E E T T H E R E Q U I R E M E N T S O F R I S K B A S E D A U D I T I N G S T A N D A R D S A C a s e W a r e I D E A R e s e a r c h R e p o r t CaseWare IDEA Inc.

How To Audit A Company

INTERNATIONAL STANDARD ON AUDITING 315 IDENTIFYING AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT THROUGH UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT (Effective for audits of financial statements for

INTERNATIONAL STANDARD ON AUDITING 315 IDENTIFYING AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT THROUGH UNDERSTANDING THE ENTITY AND ITS ENVIRONMENT (Effective for audits of financial statements for

WEEK 6. Objective 1: Sales Transaction Cycle Risks

WEEK 6 CSA ch4 & GS ch10: pp457-488 Objective 1: Sales Transaction Cycle Risks The major assertions of interest to the auditor in ST of balances for account receivable are existence and valuation and allocation.

WEEK 6 CSA ch4 & GS ch10: pp457-488 Objective 1: Sales Transaction Cycle Risks The major assertions of interest to the auditor in ST of balances for account receivable are existence and valuation and allocation.

INDONESIAN INSTITUTE OF ACCOUNTANTS FIXED ASSETS AND OTHER ASSETS

STATEMENT OF SFAS No. FINANCIAL ACCOUNTING STANDARD 16 INDONESIAN INSTITUTE OF ACCOUNTANTS FIXED ASSETS AND OTHER ASSETS Statement of Financial Accounting Standard (SFAS) No.16, Fixed Assets and Other

STATEMENT OF SFAS No. FINANCIAL ACCOUNTING STANDARD 16 INDONESIAN INSTITUTE OF ACCOUNTANTS FIXED ASSETS AND OTHER ASSETS Statement of Financial Accounting Standard (SFAS) No.16, Fixed Assets and Other

Fundamentals Level Skills Module, Paper F8. Section A

Answers Fundamentals Level Skills Module, Paper F8 Audit and Assurance June 2015 Answers Section A Question Answer See Note 1 D 1 2 C 2 3 A 3 4 D 4 5 C 5 6 B 6 7 C 7 8 B 8 9 A 9 10 A 10 11 B 11 12 D 12

Answers Fundamentals Level Skills Module, Paper F8 Audit and Assurance June 2015 Answers Section A Question Answer See Note 1 D 1 2 C 2 3 A 3 4 D 4 5 C 5 6 B 6 7 C 7 8 B 8 9 A 9 10 A 10 11 B 11 12 D 12

Lebanese Association of Certified Public Accountants - AUDIT December Exam 2014

MULTIPLE CHOICE QUESTIONS (40%) 1) When qualifying an opinion because of an insufficiency of audit evidence, an auditor should refer to the situation in the Opinion (introductory) Scope paragraph paragraph

MULTIPLE CHOICE QUESTIONS (40%) 1) When qualifying an opinion because of an insufficiency of audit evidence, an auditor should refer to the situation in the Opinion (introductory) Scope paragraph paragraph

OBSERVATIONS FROM 2010 INSPECTIONS OF DOMESTIC ANNUALLY INSPECTED FIRMS REGARDING DEFICIENCIES IN AUDITS OF INTERNAL CONTROL OVER FINANCIAL REPORTING

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org OBSERVATIONS FROM 2010 INSPECTIONS OF DOMESTIC ANNUALLY INSPECTED FIRMS REGARDING DEFICIENCIES

1666 K Street, N.W. Washington, DC 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org OBSERVATIONS FROM 2010 INSPECTIONS OF DOMESTIC ANNUALLY INSPECTED FIRMS REGARDING DEFICIENCIES

Accounting Core Course Learning Outcomes ACCT-3111 Cost Accounting Course Learning Outcomes

Accounting Core Course Learning Outcomes Updated 9/26/15 ACCT-3111 Cost Accounting ACCT-3151 Intermediate Accounting I ACCT-3152 Intermediate Accounting II ACCT-3252 Accounting Information Systems ACCT-4251

Accounting Core Course Learning Outcomes Updated 9/26/15 ACCT-3111 Cost Accounting ACCT-3151 Intermediate Accounting I ACCT-3152 Intermediate Accounting II ACCT-3252 Accounting Information Systems ACCT-4251

FEDERATED CO-OPERATIVES LIMITED CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME year ended October 31, 2012

CONSOLIDATED Financial Statements Federated Co-operatives Limited / OCTOBER 31, 2012 In Millions of CAD $ FEDERATED CO-OPERATIVES LIMITED CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME year ended October

CONSOLIDATED Financial Statements Federated Co-operatives Limited / OCTOBER 31, 2012 In Millions of CAD $ FEDERATED CO-OPERATIVES LIMITED CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME year ended October

CHAPTER 7 PLANNING THE AUDIT: IDENTIFYING AND RESPONDING TO THE RISKS OF MATERIAL MISSTATEMENT

A U D I T I N G A RISK-BASED APPROACH TO CONDUCTING A QUALITY AUDIT 9 th Edition Karla M. Johnstone Audrey A. Gramling Larry E. Rittenberg CHAPTER 7 PLANNING THE AUDIT: IDENTIFYING AND RESPONDING TO THE

A U D I T I N G A RISK-BASED APPROACH TO CONDUCTING A QUALITY AUDIT 9 th Edition Karla M. Johnstone Audrey A. Gramling Larry E. Rittenberg CHAPTER 7 PLANNING THE AUDIT: IDENTIFYING AND RESPONDING TO THE

Internal Control Systems

D. INTERNAL CONTROL 1. Internal Control Systems 2. The Use of Internal Control Systems by Auditors 3. Transaction Cycles 4. Tests of Control 5. The Evaluation of Internal Control Component 6. Communication

D. INTERNAL CONTROL 1. Internal Control Systems 2. The Use of Internal Control Systems by Auditors 3. Transaction Cycles 4. Tests of Control 5. The Evaluation of Internal Control Component 6. Communication

BRITISH COLUMBIA TRANSIT

Audited Financial Statements of BRITISH COLUMBIA TRANSIT Years ended March 31, 2005 and 2004 AUDITOR S REPORT BC TRANSIT 41 REPORT OF MANAGEMENT Years ended March 31, 2005 and 2004 The financial statements

Audited Financial Statements of BRITISH COLUMBIA TRANSIT Years ended March 31, 2005 and 2004 AUDITOR S REPORT BC TRANSIT 41 REPORT OF MANAGEMENT Years ended March 31, 2005 and 2004 The financial statements

SUGGESTED CONTROLS TO MITIGATE THE POTENTIAL RISK (Internal Audit)

") Unit: Subject: Sarbanes-Oxley Act Review - Fixed Assets Cycle Title: Risk and Control Identification Year end: Acquisition of Fixed Assets Recorded fixed asset acquisitions represent fixed assets acquired

Unit: Subject: Sarbanes-Oxley Act Review - Fixed Assets Cycle Title: Risk and Control Identification Year end: Acquisition of Fixed Assets Recorded fixed asset acquisitions represent fixed assets acquired

This Executive Summary is part of McGladrey s A Guide to Accounting for Business Combinations and should be read in conjunction with that guide.

Executive Summary This Executive Summary is part of McGladrey s A Guide to Accounting for Business Combinations and should be read in conjunction with that guide. Introduction The current guidance on accounting

Executive Summary This Executive Summary is part of McGladrey s A Guide to Accounting for Business Combinations and should be read in conjunction with that guide. Introduction The current guidance on accounting

Property, Plant and Equipment

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 16 Property, Plant and Equipment SB-FRS 16 Property, Plant and Equipment applies to Statutory Boards for annual periods beginning on or after 1 January

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 16 Property, Plant and Equipment SB-FRS 16 Property, Plant and Equipment applies to Statutory Boards for annual periods beginning on or after 1 January

Investments and advances... 344,499

Consolidated Financial Statements of the Company The consolidated balance sheet, statement of income, and statement of equity of the Company are as follows. Please note the Company s consolidated financial

Consolidated Financial Statements of the Company The consolidated balance sheet, statement of income, and statement of equity of the Company are as follows. Please note the Company s consolidated financial

Accounting for Changes and Errors

CHAPTER Accounting for Changes and Errors OBJECTIVES After careful study of this chapter, you will be able to: 1. Identify the types of accounting changes. 2. Explain the methods of disclosing an accounting

CHAPTER Accounting for Changes and Errors OBJECTIVES After careful study of this chapter, you will be able to: 1. Identify the types of accounting changes. 2. Explain the methods of disclosing an accounting

Uniform Accounting Network Inventory Manual. Table of Contents. Warranty Maintenance Debt Management Depreciation Disposal

Inventory Manual Uniform Accounting Network Inventory Manual Table of Contents Introduction Parts of the Manual Part 1 Assets Chapter 1 Acquisition Warranty Maintenance Debt Management Depreciation Disposal

Inventory Manual Uniform Accounting Network Inventory Manual Table of Contents Introduction Parts of the Manual Part 1 Assets Chapter 1 Acquisition Warranty Maintenance Debt Management Depreciation Disposal

ACCOUNTING FOR AND AUDIT OF INVENTORIES

ACCOUNTING FOR AND AUDIT OF INVENTORIES PRESENTED BY MICHEAL AGHWANA MANAGER: PEAK PROFESSIONAL SERVICES IN HOUSE SEMINAR SERIES NO 3 PEAK PROFESSIONAL SERVICES (CHARTERED ACCOUNTANTS) NIGERIA A member

ACCOUNTING FOR AND AUDIT OF INVENTORIES PRESENTED BY MICHEAL AGHWANA MANAGER: PEAK PROFESSIONAL SERVICES IN HOUSE SEMINAR SERIES NO 3 PEAK PROFESSIONAL SERVICES (CHARTERED ACCOUNTANTS) NIGERIA A member

PART III. Consolidated Financial Statements of Hitachi, Ltd. and Subsidiaries: Independent Auditors Report 47

PART III Item 17. Financial Statements Consolidated Financial Statements of Hitachi, Ltd. and Subsidiaries: Schedule: Page Number Independent Auditors Report 47 Consolidated Balance Sheets as of March

PART III Item 17. Financial Statements Consolidated Financial Statements of Hitachi, Ltd. and Subsidiaries: Schedule: Page Number Independent Auditors Report 47 Consolidated Balance Sheets as of March

The auditors responsibility to consider fraud in an audit of financial statements

The auditors responsibility to consider fraud in an audit of financial statements Audit in a nutshell Reality Picture (= financial statements) Balance sheet Assets Liabilities Equity Process Detection

The auditors responsibility to consider fraud in an audit of financial statements Audit in a nutshell Reality Picture (= financial statements) Balance sheet Assets Liabilities Equity Process Detection

Accounting for Costs of Computer Software for Internal Use 20,411 NOTE

Accounting for Costs of Computer Software for Internal Use 20,411 Section 10,720 Statement of Position 98-1 Accounting for the Costs of Computer Software Developed or Obtained for Internal Use March 4,

Accounting for Costs of Computer Software for Internal Use 20,411 Section 10,720 Statement of Position 98-1 Accounting for the Costs of Computer Software Developed or Obtained for Internal Use March 4,

Executive Summary... 2. Background... 3-5. Objectives and Approach... 6-7. Issues Matrix... 8-9. Observations and Considerations...

Internal Audit Committee of Brevard County, Florida Internal Audit of Asset Management Prepared By: Internal Auditors of Brevard County June 5, 2009 Table of Contents Transmittal Letter... 1 Executive

Internal Audit Committee of Brevard County, Florida Internal Audit of Asset Management Prepared By: Internal Auditors of Brevard County June 5, 2009 Table of Contents Transmittal Letter... 1 Executive

Consolidated Financial Statements. FUJIFILM Holdings Corporation and Subsidiaries. March 31, 2015 with Report of Independent Auditors

Consolidated Financial Statements FUJIFILM Holdings Corporation and Subsidiaries March 31, 2015 with Report of Independent Auditors Consolidated Financial Statements March 31, 2015 Contents Report of Independent

Consolidated Financial Statements FUJIFILM Holdings Corporation and Subsidiaries March 31, 2015 with Report of Independent Auditors Consolidated Financial Statements March 31, 2015 Contents Report of Independent

Asset management policy

Asset management policy POL-C-002 Version 3.1 26 February 2007 Contents 1. Title... 3 2. Introduction... 3 3. Scope... 3 4. Principles and guidelines... 3 5. Definition of responsibilities... 10 6. References...

Asset management policy POL-C-002 Version 3.1 26 February 2007 Contents 1. Title... 3 2. Introduction... 3 3. Scope... 3 4. Principles and guidelines... 3 5. Definition of responsibilities... 10 6. References...

Accounting for the Costs of Computer Software Developed or Obtained for Internal Use

Exhibit No.: A- 1_ (AJB-1) Page No.: 1 of 27 Statement of Position 98-1 Accounting for the Costs of Computer Software Developed or Obtained for Internal Use March 4, 1998 NOTE Statements of Position on

Exhibit No.: A- 1_ (AJB-1) Page No.: 1 of 27 Statement of Position 98-1 Accounting for the Costs of Computer Software Developed or Obtained for Internal Use March 4, 1998 NOTE Statements of Position on

Guide to Internal Control Over Financial Reporting

Guide to Internal Control Over Financial Reporting The Center for Audit Quality prepared this Guide to provide an overview for the general public of internal control over financial reporting ( ICFR ).

Guide to Internal Control Over Financial Reporting The Center for Audit Quality prepared this Guide to provide an overview for the general public of internal control over financial reporting ( ICFR ).

Chapter 14 Completing the Tests in the Sales and Collection Cycle: Accounts Receivable

Chapter 14 Completing the Tests in the Sales and Collection Cycle: Accounts Receivable Review Questions 14-1 Tests of details of financial balances are designed to determine the reasonableness of the balances

Chapter 14 Completing the Tests in the Sales and Collection Cycle: Accounts Receivable Review Questions 14-1 Tests of details of financial balances are designed to determine the reasonableness of the balances

Financial Statements. August 31, 2013 and 2012. (With Independent Auditors Report Thereon)

") Financial Statements (With Independent Auditors Report Thereon) Table of Contents Page Independent Auditors Report 1 Statements of Financial Position 2 Statement of Activities Year ended August 31, 2013

Financial Statements (With Independent Auditors Report Thereon) Table of Contents Page Independent Auditors Report 1 Statements of Financial Position 2 Statement of Activities Year ended August 31, 2013

Ian Shuman, CPA Trevor Williams, CPA. Center for Nonprofit Advancement

Preparing for Your Audit Ian Shuman, CPA Trevor Williams, CPA Center for Nonprofit Advancement Final Products & Reports Audit Report The end product of the audit is the expression of an opinion as to the

Preparing for Your Audit Ian Shuman, CPA Trevor Williams, CPA Center for Nonprofit Advancement Final Products & Reports Audit Report The end product of the audit is the expression of an opinion as to the

Audit Planning, Types of Audit Tests and Materiality

Chapter 3 Audit Planning, Types of Audit Tests and Materiality Learning Objectives Upon completion of this chapter you will LO1 Understand the auditor s requirements for client acceptance and continuance.

Chapter 3 Audit Planning, Types of Audit Tests and Materiality Learning Objectives Upon completion of this chapter you will LO1 Understand the auditor s requirements for client acceptance and continuance.

i) Question Type The following are guidelines on the type of questions and their approximate weightings:

Question Type The following are guidelines on the type of questions and their approximate weightings:") Purpose Financial Accounting: Assets [FA2] Examination Blueprint 2014/2015 The Financial Accounting: Assets [FA2] examination has been constructed using an examination blueprint. The blueprint, also referred

Purpose Financial Accounting: Assets [FA2] Examination Blueprint 2014/2015 The Financial Accounting: Assets [FA2] examination has been constructed using an examination blueprint. The blueprint, also referred