Tax-Exempt Rules for Life Insurance And the changes that are coming! Dominik Briault, FSA, FCIA Director, Actuarial Marketing Services

|

|

|

- Emory Bailey

- 8 years ago

- Views:

Transcription

1 Tax-Exempt Rules for Life Insurance And the changes that are coming! Dominik Briault, FSA, FCIA Director, Actuarial Marketing Services

2 This material is for information purposes only and shouldn t be construed as legal or tax advice. Every effort has been made to ensure its accuracy, but errors and omissions are possible. All comments related to taxation are general in nature and are based on current Canadian tax legislation for Canadian residents, which is subject to change. For individual circumstances, consult with legal or tax advisors. 2

3 3 Session Agenda Life Insurance Industry Sales Tax-Exempt Rules: The basics The current rules The new rules Other considerations Participating Insurance Discussion

4 Life Insurance Industry Sales

5 Canadian individual life insurance sales Total premiums 100% 90% 80% 70% 60% 50% 40% 30% 20% 10% 0% Term Life Universal Life Whole Life Source: LIMRA Individual Life Insurance Sales Confidential Participants' Report Note: LIMRA doesn t report participating life insurance separately. It s included in the whole life category. Whole life figures include both participating and non-participating whole life sales.

6 Whole life sales in 2014 Total Canadian industry whole life sales premium: $722 million and 13% growth At the end of 2014, whole life represented 48% of industry life insurance sales Canada Life had the number one market share of whole life sales premium London Life/Great-West Life/Canada Life had a 47% market share of whole life sales at the end of 2014 Canada Life London Life 23% 21% Great-West 3% 53% Other companies Source: LIMRA Individual Life Insurance Sales Confidential Participants' Report. Note: LIMRA doesn t report participating life insurance separately. It s included in the whole life category. Whole life figures include both participating and non-participating whole life sales.

7 Tax-Exempt Rules

8 8 Tax-Exempt Rules Basics Tax-Exempt Rules dictate how much cash value can be held within a life insurance policy given the total death benefit and remain tax-exempt Test is meant to distinguish between policies that are deemed to be protection-oriented versus investment-oriented

9 9 Tax-Exempt Rules Basics Benefits of a tax-exempt life insurance policy: The cash value in the policy grows tax-free; The total death benefit is paid tax-free to the beneficiary(ies) upon the death of the insured There could be exceptions with the new rules When a life insurance policy is non-exempt: The total death benefit is still paid tax-free to the beneficiary(ies) upon the death of the insured; However, the increase in cash value above the ACB since the last policy anniversary becomes taxable on a yearly basis

10 10 Tax-Exempt Rules Basics To be tax-exempt: The Accumulating Fund (AF) of the policy must be lower than the AF of a hypothetical benchmark policy This benchmark mark policy is often called the Exempt-Test Policy (ETP) The legislation will determine the type of life insurance policy to use to determine the ETP Some additional tests, i.e. the 8% Test and the 250% Test will determine the proper ETP to use for the policy

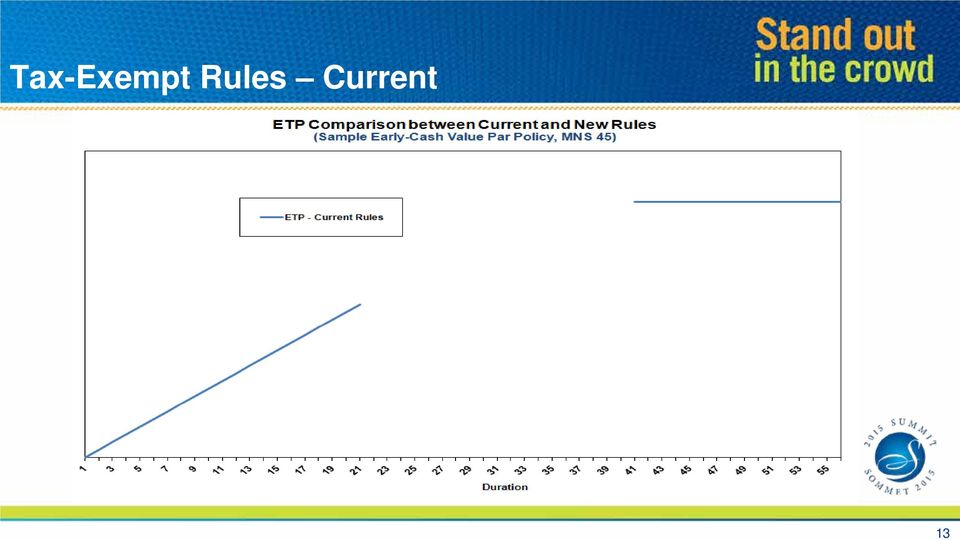

11 11 Tax-Exempt Rules Current Current ETP is based on a 20-Pay Endowment Paid at age 85. The ETP is based on the assumptions used in the pricing of the life insurance product The exempt test must be performed at every policy anniversary The test must ensure that the AF of the policy is less than the ETP of the policy for the current anniversary and all future anniversaries The AF of the policy is the greater of: The cash surrender value of the policy; and The 1.5 Full Preliminary Term (FPT) reserve for the policy

12 Tax-Exempt Rules Current 12

13 Tax-Exempt Rules Current 13

14 Tax-Exempt Rules Current 14

15 Tax-Exempt Rules Current 15

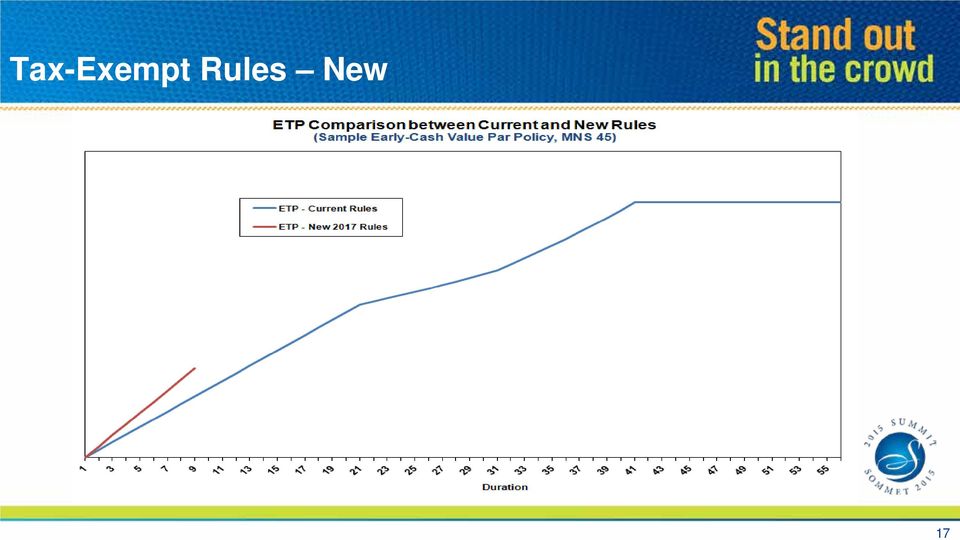

16 16 Tax-Exempt Rules New New ETP is based on an 8-Pay Endowment Paid at age 90 8-pay to reflect the fact that most life insurance policies are paid over a shorter period of time than previously; and At age 90 to reflect mortality improvement since the 1980s The ETP is based on a set of prescribed assumptions in the law The exempt test must be performed at every policy anniversary The test must ensure that the AF of the policy is less than the ETP of the policy for the current anniversary only. and all future anniversary dates The AF of the policy is the greater of: The cash surrender value (ignoring surrender charges and policy loans) of the policy; and The Net Premium Reserve (NPR) for the policy. 1.5FPT reserve for the policy

of the policy; and The Net Premium")

17 Tax-Exempt Rules New 17

18 Tax-Exempt Rules New 18

19 Tax-Exempt Rules New 19

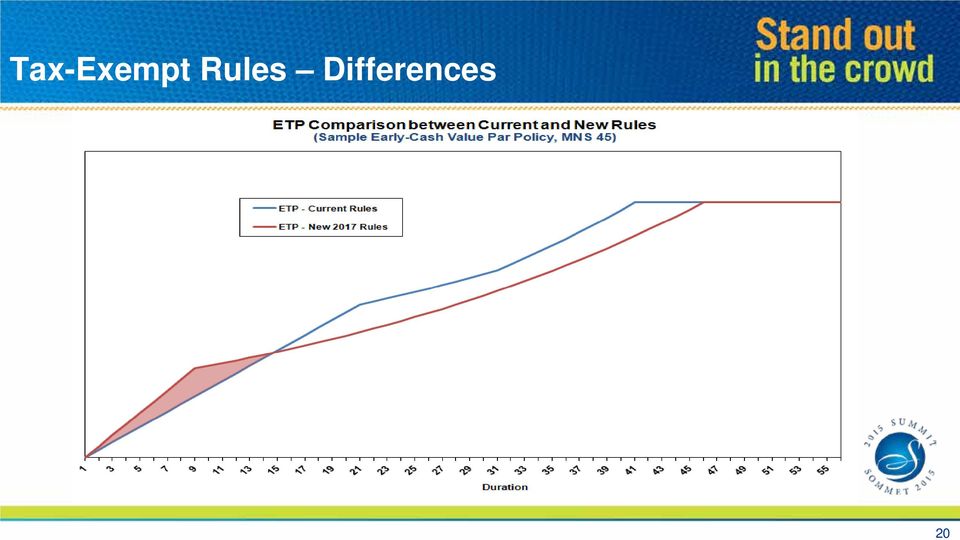

20 Tax-Exempt Rules Differences 20

21 Tax-Exempt Rules Differences 21

22 Tax-Exempt Rules New 22

23 Tax-Exempt Rules New 23

24 24 Tax-Exempt Rules Other Considerations Impact on Universal Life Products: Two major impacts: Reduction in Maximum Premiums; and Potential Cost of Insurance (COI) increase from change in Investment Income Tax (IIT) rules

25 25 Tax-Exempt Rules Other Considerations Impact on Universal Life Products (con t): Reduction in Maximum Premiums: Currently, maximum premiums are calculated using the cash surrender value of the policy Theoretically, you could increase the tax-exempt room within a UL policy by increasing the surrender charges of your product Under the new rules, the maximum premiums will be calculated using the cash surrender value ignoring surrender charges and policy loans As a result, maximum premiums will be decreased under the new rules This change will be bigger for some companies based on their current product design

26 26 Tax-Exempt Rules Other Considerations Impact on Universal Life Products (con t): Potential COI Increase: The current IIT calculation is based on the cash surrender value of the policy Because of the surrender charges and the smaller account values for minimum funded policies, the IIT was smaller as well The new rules will now be using the larger of the Accumulating Fund (AF) and the Net Premium Reserve (NPR), ignoring any policy loan or reinsurance ceded in the IIT calculation This change will increase the amount of IIT that will be paid by each carrier This change will likely lead to an increase in UL COI charges

27 27 Tax-Exempt Rules Other Considerations ACB/NCPI Impact: Adjusted Cost Basis (ACB) is the amount that can be withdrawn from a life insurance policy tax-free upon full surrender Simplistically, the ACB is calculated as follows (the actual formula is more complex): ACB(t) = ACB(t-1) + Premiums(t) NCPI(t) NCPI = Net Cost of Pure Insurance NCPI is currently calculated using the CIA Mortality Table NCPI(t) = [Total Death Benefit(t) Cash Surrender Value(t)] * q(x)

28 28 Tax-Exempt Rules Other Considerations ACB/NCPI Impact (con t): The ACB formula is not changing. Besides a small change in the definition of a premium However, there are two changes in the calculation of the NCPI: A newer mortality table must be used... i.e. CIA Mortality Table NCPI(t) = [Total Death Benefit(t) Net Premium Reserve(t)] * q(x) The overall impact is that the NCPI will be materially reduced versus our current rules

29 29 Tax-Exempt Rules Other Considerations ACB/NCPI Impact (con t): This change in NCPI methodology means: The ACB of the policy will take longer to get to zero, or may never get to zero; More cash value can be withdrawn tax-free for individually-owned policies because of the higher ACB; NCPI deductions will be less for corporately owned policies; The Capital Dividend Account (CDA) credit will likely be less than today for corporately-owned policies because of the higher ACB CDA Credit = Total Death Benefit ACB

30 30 Tax-Exempt Rules Other Considerations Grandfathering of Inforce Policies: The new legislation says that policies issued prior to January 1 st, 2017 will be grandfathered with the old rules The legislation also sets the rules dictating when such a policy will lose its grandfathered status Discussions are ongoing with government to clarify some of the grandfathering rules. What we know for sure: A change resulting in both an increase in coverage and requiring underwriting => loss of grandfathering; A term conversion to another type of coverage => loss of grandfathering Other changes will be communicated as we finalize our discussions with government

31 31 Tax-Exempt Rules Other Considerations Impact on Policy Changes: Still reviewing...

32 Mechanics of participating life insurance

33 Digging deeper into financial facts 33

34 How participating life insurance works 34

35 35 How does participating life insurance work? Participating account operations Policyowner premiums + Investment income - Benefits paid and changes in actuarial liabilities - Expenses and taxes = Participating account earnings Participating surplus account Policyowner Opening balance + Participating account earnings - Distribution Shareholder = Closing balance

36 Summary of participating account Operations and surplus London Life Participating account ($ millions) SUMMARY OF PARTICIPATING ACCOUNT OPERATIONS IN 2014 Participating policyowner premiums $2,033 + Investment income 1,457 - Benefits paid Changes in actuarial liabilities 1,312 - Expenses and taxes Distribution to policyowners & shareholders 823 Policyowner dividends 783 Increase in dividend liability 23 Shareholder portion Cash payment 21 Accrual -4 = Participating account net income $31 PARTICIPATING ACCOUNT BALANCE SHEET Assets $23,844 - Liabilities 22,124 =Closing balance for participating account surplus at Dec. 31, 2014 Participating account surplus $1,720 Opening balance Dec. 31, 2013 $1,661 + Participating account net income 31 + Other comprehensive income 24 + Reallocation of assets 4 = Closing balance for participating account surplus $1,720 Source: December 2014 Financial Facts London Life participating life insurance page 10 36

37 37 Participating Life Insurance Value Client needs Par feature Wants guarantees Guaranteed base premiums Guaranteed base death benefit Guaranteed base cash values Guaranteed level of term enhancement for 10 years or life Vesting Wants professional management of the investment component of their life insurance policy Participating account managed by a team of investment professionals Have a low to moderate investment risk tolerance The par account is managed such that 80% of invested assets are in fixed income with 20% invested in equities Are attracted to historical long-term stability The standard deviation of the par dividend scale interest rate is 1.7% in 2014.

38 Participating account stability

39 Participating account stability Sources: London Life Looking Back at Historical Returns. 39

40 40 10 year Government of Canada bond yields % Source: GLC, Bloomberg, FTSE TMX Global Debt Capital Markets Inc., June 30, 2014 Past performance is no guarantee of future results. There can be no assurance that any trends shown will continue because economic and market conditions change frequently.

41 41 Long-Term Bond Yields since US Source:

42 42 London Life participating account performance Asset class Return on total participating account assets Jan 1, 2013 to Dec 31, 2013 Jul 1, 2013 to Jun 30, 2014 Jan 1, 2014 to Dec 31, 2014 Public bonds and private 4.6% 4.2% 4.1% placements Mortgages 4.8% 4.6% 4.5% Stock 19.9% 30.9% 10.8% Real Estate 4.4% 7.7% 8.2% Total Portfolio Yield* 7.0% 7.8% 5.5% * Net of investment expenses Asset returns available in January and February 2015 for new par account investments in bonds and mortgages during this period were about 3.3% Approximately 110 bps below the average return for similar par account assets maturing throughout 2015

43 Participating insurance competition

44 London Life vs. Great-West Life / Canada Life Information as of December 31 st, 2014 Product options London Life Great-West Life Canada Life 20 Pay Life, JWL, LP 65 Early CV and Delayed CV products, both with 20-pay and life-pay options, ADO available on all products. Total assets $23.8 billion $4.3 billion $979 million (open block only) Surplus position $1.7 billion $579 million $163 million (open block only) Target investment mix 2015 dividend scale interest rate (DSIR) 80% fixed income 5.90% 6.15% 6.50% Rating reduction program No Yes lower premiums for rated cases Policyowner portion of distributed surplus 97.5% 97.5% 97.0% Sources: 2014 London Life Financial Facts; 2014 Great-West Life Financial Facts, 2014 Canada Life Financial Facts 44

45 London Life vs. Sun Life Participating Accounts Information as of December 31 st, 2014 London Life Sun Life Product options 20 Pay Life, JWL, LP 65 Early CV and Delayed CV products, both with 20-pay and life-pay options, ADO available on all products Total assets $23.8 billion $426.0 million (open block only) Surplus position $1.7 billion $35 million (open block only) Investment mix 19% equities 34% equities 2015 dividend scale interest rate (DSIR) 5.90% 6.75% Policy loan rate 6.5% 4.5% Policyowner dividends paid $783 million $38 million (open block only) Sources: 2014 London Life Financial Facts; 2014 Sun Life Financial Participating Whole Life Insurance Facts and figures 45

46 46 Differences in Asset Mix London Life participating account invested assets As at December 31, 2014 Sun Life participating account invested assets As at December 31, % 0.1% 4.9% London Life participating account invested assets At June 30, % Cash & Equivalents Public Bonds Private Placements 1.2% Cash & Equivalents 17.4% Public Bonds Private Placements Residential Mortgages 36.8% Residential Mortgages 23.5% 46.1% Commercial Mortgages Common Stock Real Estate 16.4% Commercial Mortgages Common Stock Real Estate 2.5% 3.9% Preferred Stock 11.6% 16.6% Preferred Stock Sun Life: Sun Life 2014 participating whole life facts LondonLife: 2014 London Life participating life insurance financial facts

47 47 Agency Ratings Ratings* Rating agency London Life Sun Life Assurance Company of Canada Manulife Financial A.M. Best Company A+ A+ A+ Fitch Ratings AA AA-** AA- Moody s Investors Service Aa3 Aa3 A1 Standard & Poor s Ratings Services AA AA- AA- * As of July 29, 2014 ** Source: fitchratings.com

48 Participating Account Asset Quality (December 31 st, 2014) Public Bonds Asset Quality Sun Life Par account London Life Par account AAA 14.0% 49.8% AA 34.3% 13.0% A 39.9% 22.4% BBB 11.8% 14.3% BB or less 0.0% 0.5% Total 100% 100% Sources: 2014 London Life Financial Facts; 2014 Sun Life Financial Participating Whole Life Insurance Facts and figures 48

49 Change in Participating Account Surplus Participating Account Surplus End of Year London Life Par account Sun Life Par account 2011 $1,598 million $49 million 2012 $1,811 million $49 million 2013 $1,661 million* $38 million 2014 $1,720 million $35 million Change since % -28.6% * 2013 London Life participating account surplus was reduced by $196 million due to a litigation provision release. Sources: 2014, 2013 & 2012 Par Financial facts London Life; Sun Life Participating Whole Life insurance Facts and figures 49

50 Thank you!

Life insurance provides

ADVISOR USE ONLY 1 Impact of 217 tax changes on life insurance THE DETAILS Life insurance provides protection, but some policies also allow clients to accumulate savings on a tax-preferred basis. The Income

ADVISOR USE ONLY 1 Impact of 217 tax changes on life insurance THE DETAILS Life insurance provides protection, but some policies also allow clients to accumulate savings on a tax-preferred basis. The Income

Financialfacts. Great-West Life participating life insurance. Accountability Strength Performance

2014 Financialfacts Great-West Life participating life insurance Accountability Strength Performance This guide provides key financial facts about the management, strength and performance of the Great-West

2014 Financialfacts Great-West Life participating life insurance Accountability Strength Performance This guide provides key financial facts about the management, strength and performance of the Great-West

Financialfacts. Participating life insurance. Accountability Strength Performance

2014 Financialfacts Participating life insurance Accountability Strength Performance This guide provides key financial facts about the management, performance and strength of the Canada Life participating

2014 Financialfacts Participating life insurance Accountability Strength Performance This guide provides key financial facts about the management, performance and strength of the Canada Life participating

Financialfacts. London Life participating life insurance. Accountability Strength Performance

2014 Financialfacts London Life participating life insurance Accountability Strength Performance This guide provides key financial facts about the management, strength and performance of the London Life

2014 Financialfacts London Life participating life insurance Accountability Strength Performance This guide provides key financial facts about the management, strength and performance of the London Life

Overview of Canadian taxation of life insurance policies. New tax legislation for life insurance policies. January 2015

January 2015 Overview of Canadian taxation of life insurance policies Life insurance plays an increasingly important role in financial planning due to the growing wealth of Canadians. Besides the traditional

January 2015 Overview of Canadian taxation of life insurance policies Life insurance plays an increasingly important role in financial planning due to the growing wealth of Canadians. Besides the traditional

Universal Life Insurance An Introduction for Professional Advisors

Page 1 of 17 Universal Life Insurance An Introduction for Professional Advisors Introduction... 2 Life Insurance uses... 2 Taxation of Life Insurance... 3 Accumulating Cash/Fund Values... 4 Maximizing

Page 1 of 17 Universal Life Insurance An Introduction for Professional Advisors Introduction... 2 Life Insurance uses... 2 Taxation of Life Insurance... 3 Accumulating Cash/Fund Values... 4 Maximizing

CORPORATE RETIREMENT STRATEGY ADVISOR GUIDE. *Advisor USE ONLY

CORPORATE RETIREMENT STRATEGY ADVISOR GUIDE *Advisor USE ONLY TABLE OF CONTENTS Introduction to the corporate retirement strategy...2 Identify the opportunity - target markets... 3 Policy ownership: corporate

CORPORATE RETIREMENT STRATEGY ADVISOR GUIDE *Advisor USE ONLY TABLE OF CONTENTS Introduction to the corporate retirement strategy...2 Identify the opportunity - target markets... 3 Policy ownership: corporate

Your guide to Canada Life s participating life insurance. Estate Achiever Wealth Achiever

Your guide to Canada Life s participating life insurance Estate Achiever Wealth Achiever This guide provides an overview of key features of participating life insurance products offered by Canada Life.

Your guide to Canada Life s participating life insurance Estate Achiever Wealth Achiever This guide provides an overview of key features of participating life insurance products offered by Canada Life.

insurance solutions isn t static, neither is your business Protect life Corporate collateral loan strategy

Life insurance solutions isn t static, neither is your business Protect life Corporate collateral loan strategy Increase your business cash flow with corporately owned life insurance from Canada Life Business

Life insurance solutions isn t static, neither is your business Protect life Corporate collateral loan strategy Increase your business cash flow with corporately owned life insurance from Canada Life Business

EXPLANATORY NOTES LIFE INSURANCE POLICY EXEMPTION TEST INCOME TAX ACT

Page 1 EXPLANATORY NOTES LIFE INSURANCE POLICY EXEMPTION TEST INCOME TAX ACT The Income Tax Act (the Act ) contains rules regarding the taxation of the income earned on the savings in a life insurance

Page 1 EXPLANATORY NOTES LIFE INSURANCE POLICY EXEMPTION TEST INCOME TAX ACT The Income Tax Act (the Act ) contains rules regarding the taxation of the income earned on the savings in a life insurance

How To Tax A Life Insurance Policy On A Policy In The United States

Taxation of Life Insurance Policy Loans and Dividends Introduction Policyholders are required to include in income any gains realized upon the disposition of all or a portion of their interest in a life

Taxation of Life Insurance Policy Loans and Dividends Introduction Policyholders are required to include in income any gains realized upon the disposition of all or a portion of their interest in a life

Wealth Achiever participating life insurance illustration Max 20

Wealth Achiever participating life insurance illustration Max 20 Canada Life's permanent participating life insurance gives you a foundation of basic cash value that is guaranteed, tax-advantaged growth,

Wealth Achiever participating life insurance illustration Max 20 Canada Life's permanent participating life insurance gives you a foundation of basic cash value that is guaranteed, tax-advantaged growth,

UNIVERSAL LIFE INSURANCE. Flexible permanent protection

UNIVERSAL LIFE INSURANCE Flexible permanent protection A solution to your financial security needs and goals Universal life insurance from London Life At London Life, we create products to help you meet

UNIVERSAL LIFE INSURANCE Flexible permanent protection A solution to your financial security needs and goals Universal life insurance from London Life At London Life, we create products to help you meet

A Technical Guide for Individuals. The Whole Story. Understanding the features and benefits of whole life insurance. Insurance Strategies

A Technical Guide for Individuals The Whole Story Understanding the features and benefits of whole life insurance Insurance Strategies Contents 1 Insurance for Your Lifetime 3 How Does Whole Life Insurance

A Technical Guide for Individuals The Whole Story Understanding the features and benefits of whole life insurance Insurance Strategies Contents 1 Insurance for Your Lifetime 3 How Does Whole Life Insurance

Financial Information Package for the Fourth Quarter 2004. As at December 31, 2004

Financial Information Package for the Fourth Quarter 2004 As at December 31, 2004 TABLE OF CONTENTS PAGE HIGHLIGHTS 1 PROFITABILITY 3 Profit (2003 restated) Return on common shareholders' equity (2003

Financial Information Package for the Fourth Quarter 2004 As at December 31, 2004 TABLE OF CONTENTS PAGE HIGHLIGHTS 1 PROFITABILITY 3 Profit (2003 restated) Return on common shareholders' equity (2003

Your guide to Great-West Life Participating life insurance

Your guide to Great-West Life Participating life insurance This guide provides a high-level overview of key features of Great-West Life participating life insurance. After you review this guide, talk with

Your guide to Great-West Life Participating life insurance This guide provides a high-level overview of key features of Great-West Life participating life insurance. After you review this guide, talk with

Business Insurance Part 1

Business Insurance Part 1 Working with Business Owners A PARTNER YOU CAN TRUST. Jorge Ramos, CFP,CLU Director of Advanced Marketing 1 Business Structures and Taxation A PARTNER YOU CAN TRUST. 1 Business

Business Insurance Part 1 Working with Business Owners A PARTNER YOU CAN TRUST. Jorge Ramos, CFP,CLU Director of Advanced Marketing 1 Business Structures and Taxation A PARTNER YOU CAN TRUST. 1 Business

Accessing the Cash Values in Your RBC Insurance Universal Life Plan

Accessing the Cash Values in Your RBC Insurance Universal Life Plan Learn the advantages and disadvantages of the three ways you can access your money Contents: Three ways to access your Cash Values...............................

Accessing the Cash Values in Your RBC Insurance Universal Life Plan Learn the advantages and disadvantages of the three ways you can access your money Contents: Three ways to access your Cash Values...............................

A strategy to maximize your support of your favourite charity

A strategy to maximize your support of your favourite charity Planned giving Planned giving using life insurance is for individuals who Feel compassion and want to give to a cause in which they personally

A strategy to maximize your support of your favourite charity Planned giving Planned giving using life insurance is for individuals who Feel compassion and want to give to a cause in which they personally

TAX, RETIREMENT & ESTATE PLANNING SERVICES. A Guide to Leveraged Life Insurance WHAT YOU NEED TO KNOW BEFORE YOU LEVERAGE YOUR LIFE INSURANCE POLICY

TAX, RETIREMENT & ESTATE PLANNING SERVICES A Guide to Leveraged Life Insurance WHAT YOU NEED TO KNOW BEFORE YOU LEVERAGE YOUR LIFE INSURANCE POLICY This guide provides information on leveraged life insurance.

TAX, RETIREMENT & ESTATE PLANNING SERVICES A Guide to Leveraged Life Insurance WHAT YOU NEED TO KNOW BEFORE YOU LEVERAGE YOUR LIFE INSURANCE POLICY This guide provides information on leveraged life insurance.

Canada Life 2013 participating policyowner dividend scale announcement

Nov. 8, 2012 Canada Life 2013 participating policyowner dividend scale announcement New dividend scale effective Jan. 1, 2013 Why the decrease for 2013 Detailed information important for advisors Updated

Nov. 8, 2012 Canada Life 2013 participating policyowner dividend scale announcement New dividend scale effective Jan. 1, 2013 Why the decrease for 2013 Detailed information important for advisors Updated

Financial security protection tailored for your lifestyle

G R E A T - W E S T L I F E U n i v e r s a l l i f e i n s u r a n c e Financial security protection tailored for your lifestyle F A L L 2 0 0 6 G r e a t - W e s t u n i v e r s a l l i f e i n s u

G R E A T - W E S T L I F E U n i v e r s a l l i f e i n s u r a n c e Financial security protection tailored for your lifestyle F A L L 2 0 0 6 G r e a t - W e s t u n i v e r s a l l i f e i n s u

Sharing interests in a life insurance policy

Sharing interests in a life insurance policy Important considerations All comments related to taxation are general in nature and are based on current Canadian tax legislation for Canadian residents, which

Sharing interests in a life insurance policy Important considerations All comments related to taxation are general in nature and are based on current Canadian tax legislation for Canadian residents, which

Continuing Education for Advisors

Continuing Education for Advisors knowledge continuing training educate online awareness participate Participating life insurance Learning objectives By the end of this course you will be able to: Explain

Continuing Education for Advisors knowledge continuing training educate online awareness participate Participating life insurance Learning objectives By the end of this course you will be able to: Explain

Corporate asset efficiency

Life insurance solutions Corporate asset efficiency Manage. Access. Preserve. A smart solution for professionals permanent life insurance, a unique asset that can offer tax-advantaged growth. Consider

Life insurance solutions Corporate asset efficiency Manage. Access. Preserve. A smart solution for professionals permanent life insurance, a unique asset that can offer tax-advantaged growth. Consider

APPENDIX 4 - LIFE INSURANCE POLICIES PREMIUMS, RESERVES AND TAX TREATMENT

APPENDIX 4 - LIFE INSURANCE POLICIES PREMIUMS, RESERVES AND TAX TREATMENT Topics in this section include: 1.0 Types of Life Insurance 1.1 Term insurance 1.2 Type of protection 1.3 Premium calculation for

APPENDIX 4 - LIFE INSURANCE POLICIES PREMIUMS, RESERVES AND TAX TREATMENT Topics in this section include: 1.0 Types of Life Insurance 1.1 Term insurance 1.2 Type of protection 1.3 Premium calculation for

Millennium universal life insurance

Millennium universal life insurance Permanent protection that can change with you Millennium universal life insurance Over the years, you ve worked hard to build the lifestyle you enjoy today. You ve made

Millennium universal life insurance Permanent protection that can change with you Millennium universal life insurance Over the years, you ve worked hard to build the lifestyle you enjoy today. You ve made

Do creditor protection concerns exist within the company? Ultimately, who will receive the proceeds of your insurance?

Corporate Owned or Personal Owned Life Insurance When considering life insurance as a shareholder of an incorporated business, you may have wondered if your life insurance policy should be personally owned,

Corporate Owned or Personal Owned Life Insurance When considering life insurance as a shareholder of an incorporated business, you may have wondered if your life insurance policy should be personally owned,

Understanding Participating Whole. equimax

Understanding Participating Whole Life Insurance equimax CLIENT GUIDE ABOUT EQUITABLE LIFE OF CANADA Equitable Life is one of Canada s largest mutual life insurance companies in Canada. For generations

Understanding Participating Whole Life Insurance equimax CLIENT GUIDE ABOUT EQUITABLE LIFE OF CANADA Equitable Life is one of Canada s largest mutual life insurance companies in Canada. For generations

The Empire Life Insurance Company

The Empire Life Insurance Company Condensed Interim Consolidated Financial Statements For the six months ended June 30, 2015 Unaudited Issue Date: August 7, 2015 DRAFT NOTICE OF NO AUDITOR REVIEW OF CONDENSED

The Empire Life Insurance Company Condensed Interim Consolidated Financial Statements For the six months ended June 30, 2015 Unaudited Issue Date: August 7, 2015 DRAFT NOTICE OF NO AUDITOR REVIEW OF CONDENSED

Update on Mutual Company Dividend Interest Rates for 2013

Update on Mutual Company Dividend Interest Rates for 2013 1100 Kenilworth Ave., Suite 110 Charlotte, NC 28204 704.333.0508 704.333.0510 Fax www.bejs.com Prepared and Researched by June 2013 Near the end

Update on Mutual Company Dividend Interest Rates for 2013 1100 Kenilworth Ave., Suite 110 Charlotte, NC 28204 704.333.0508 704.333.0510 Fax www.bejs.com Prepared and Researched by June 2013 Near the end

MassMutual Whole Life Insurance

A Technical Overview for Clients and their Advisors MassMutual Whole Life Insurance The product design and pricing process Contents 1 Foreword 2 A Brief History of Whole Life Insurance 3 Whole Life Basics

A Technical Overview for Clients and their Advisors MassMutual Whole Life Insurance The product design and pricing process Contents 1 Foreword 2 A Brief History of Whole Life Insurance 3 Whole Life Basics

PARTICIPATING WHOLE LIFE INSURANCE. Facts and figures. As of December 31, 2013. Life s brighter under the sun

WHOLE LIFE INSURANCE PARTICIPATING Facts and figures As of December 31, 2013 Life s brighter under the sun FINANCIAL HIGHLIGHTS Sun Life Financial YOUR CHOICE for participating whole life insurance Our

WHOLE LIFE INSURANCE PARTICIPATING Facts and figures As of December 31, 2013 Life s brighter under the sun FINANCIAL HIGHLIGHTS Sun Life Financial YOUR CHOICE for participating whole life insurance Our

Insurance Corporate Insured Retirement Plan

Advisor Guide The BMO Insurance Corporate Insured Retirement Plan Because successful businesses need security and income Table of Contents Introduction to The BMO Insurance Corporate Insured Retirement

Advisor Guide The BMO Insurance Corporate Insured Retirement Plan Because successful businesses need security and income Table of Contents Introduction to The BMO Insurance Corporate Insured Retirement

Corporate Estate Transfer Strategy

Transamerica s Monarch Series Client Guide Corporate Estate Transfer Strategy Monarch Series The logic behind the solution Monarch Series The logic behind the solution The logic behind the solution Transamerica

Transamerica s Monarch Series Client Guide Corporate Estate Transfer Strategy Monarch Series The logic behind the solution Monarch Series The logic behind the solution The logic behind the solution Transamerica

TAX-EXEMPT LIFE INSURANCE

TAX-EXEMPT LIFE INSURANCE For wealth creation and estate maximization The strategies, advice and technical content in this publication are provided for the general guidance and benefit of our clients,

TAX-EXEMPT LIFE INSURANCE For wealth creation and estate maximization The strategies, advice and technical content in this publication are provided for the general guidance and benefit of our clients,

Life Insurance Review Using Legacy Advantage SUL Insurance Policy

Using Legacy Advantage SUL Insurance Policy Supplemental Illustration Prepared by: MetLife Agent 200 Park Ave. New York, NY 10166 Insurance Products: Not A Deposit Not FDIC-Insured Not Insured By Any Federal

Using Legacy Advantage SUL Insurance Policy Supplemental Illustration Prepared by: MetLife Agent 200 Park Ave. New York, NY 10166 Insurance Products: Not A Deposit Not FDIC-Insured Not Insured By Any Federal

LEVERAGING A LIFE INSURANCE POLICY

ADVISOR USE ONLY LEVERAGING A LIFE INSURANCE POLICY A GUIDE FOR LAWYERS, ACCOUNTANTS AND INSURANCE ADVISORS Using life insurance as collateral for personal and business planning Life s brighter under the

ADVISOR USE ONLY LEVERAGING A LIFE INSURANCE POLICY A GUIDE FOR LAWYERS, ACCOUNTANTS AND INSURANCE ADVISORS Using life insurance as collateral for personal and business planning Life s brighter under the

Asset/liability Management for Universal Life. Grant Paulsen Rimcon Inc. November 15, 2001

Asset/liability Management for Universal Life Grant Paulsen Rimcon Inc. November 15, 2001 Step 1: Split the product in two Premiums Reinsurance Premiums Benefits Policyholder fund Risk charges Expense

Asset/liability Management for Universal Life Grant Paulsen Rimcon Inc. November 15, 2001 Step 1: Split the product in two Premiums Reinsurance Premiums Benefits Policyholder fund Risk charges Expense

London Life participating life insurance

Your guide to London Life participating life insurance Value, strength and choice What you ll learn from this guide This guide, combined with professional advice from your financial security advisor, helps

Your guide to London Life participating life insurance Value, strength and choice What you ll learn from this guide This guide, combined with professional advice from your financial security advisor, helps

A Primer on Corporate-Owned Insurance What You Need to Know Now to Protect Your Family s Future. by Shafik Hirani

What You Need to Know Now to Protect Your Family s Future by Shafik Hirani Business Owners need life insurance like anyone else, but many don t understand how to properly structure their Policies to take

What You Need to Know Now to Protect Your Family s Future by Shafik Hirani Business Owners need life insurance like anyone else, but many don t understand how to properly structure their Policies to take

SAVINGS PRODUCTS AND THE LIFE INSURANCE INDUSTRY IN CANADA

SAVINGS PRODUCTS AND THE LIFE INSURANCE INDUSTRY IN CANADA Carl Hiralal 25 November 2004 1 Topics OSFI s Role Canadian Industry Insurance Products in Canada Insurance versus Savings Segregated Funds Universal

SAVINGS PRODUCTS AND THE LIFE INSURANCE INDUSTRY IN CANADA Carl Hiralal 25 November 2004 1 Topics OSFI s Role Canadian Industry Insurance Products in Canada Insurance versus Savings Segregated Funds Universal

Designing The Ideal Investment Policy Presented To The Actuaries Club of the Southwest & the Southeastern Actuarial Conference

Designing The Ideal Investment Policy Presented To The Actuaries Club of the Southwest & the Southeastern Actuarial Conference Presented by: Greg Curran, CFA & Michael Kelch, CFA AAM - Insurance Investment

Designing The Ideal Investment Policy Presented To The Actuaries Club of the Southwest & the Southeastern Actuarial Conference Presented by: Greg Curran, CFA & Michael Kelch, CFA AAM - Insurance Investment

OPTIMAX. PRODUCT GUIDE Permanent Participating Life Insurance The future begins today FOR ADVISOR USE ONLY

OPTIMAX PRODUCT GUIDE Permanent Participating Life Insurance The future begins today FOR ADVISOR USE ONLY HIGHLIGHTS Premium Options Optimax 100 Optimax 20 Pay Coverage Options Single Joint First or Second

OPTIMAX PRODUCT GUIDE Permanent Participating Life Insurance The future begins today FOR ADVISOR USE ONLY HIGHLIGHTS Premium Options Optimax 100 Optimax 20 Pay Coverage Options Single Joint First or Second

Your guide to participating life insurance SUN PAR PROTECTOR SUN PAR ACCUMULATOR

Your guide to participating life insurance SUN PAR PROTECTOR SUN PAR ACCUMULATOR Participate in your brighter future with Sun Life Financial. Participating life insurance is a powerful tool that protects

Your guide to participating life insurance SUN PAR PROTECTOR SUN PAR ACCUMULATOR Participate in your brighter future with Sun Life Financial. Participating life insurance is a powerful tool that protects

Finding the Right Fit with Commercial Mortgages

Finding the Right Fit with Commercial Mortgages Key Takeaways Mortgages provide strong risk-adjusted return potential Investors can implement mortgages as a stand-alone alternative or integrated bond exposure

Finding the Right Fit with Commercial Mortgages Key Takeaways Mortgages provide strong risk-adjusted return potential Investors can implement mortgages as a stand-alone alternative or integrated bond exposure

Private Placement Insurance Products AN EXCLUSIVE AND FLEXIBLE OPPORTUNITY FOR THE AFFLUENT

Executive Summary Private placement insurance products occupy a unique place in the spectrum of financial products. While having the same tax benefits, private placement insurance products offer policy

Executive Summary Private placement insurance products occupy a unique place in the spectrum of financial products. While having the same tax benefits, private placement insurance products offer policy

Canadian Life Insurance Company Asset/Liability Management Summary Report as at: 31-Jan-08 interest rates as of: 29-Feb-08 Run: 2-Apr-08 20:07 Book

Canadian Life Insurance Company Asset/Liability Management Summary Report as at: 31Jan08 interest rates as of: 29Feb08 Run: 2Apr08 20:07 Book Book Present Modified Effective Projected change in net present

Canadian Life Insurance Company Asset/Liability Management Summary Report as at: 31Jan08 interest rates as of: 29Feb08 Run: 2Apr08 20:07 Book Book Present Modified Effective Projected change in net present

CURRICULUM LLQP MODULE: Life insurance DURATION OF THE EXAM: 75 minutes - NUMBER OF QUESTIONS: 30 questions

CURRICULUM LLQP MODULE: DURATION OF THE EXAM: 75 minutes - NUMBER OF QUESTIONS: 30 questions Competency: Recommend individual and group life insurance products adapted to the client s needs and situation

CURRICULUM LLQP MODULE: DURATION OF THE EXAM: 75 minutes - NUMBER OF QUESTIONS: 30 questions Competency: Recommend individual and group life insurance products adapted to the client s needs and situation

SOA 2012 Life & Annuity Symposium May 21-22, 2012. Session 31 PD, Life Insurance Illustration Regulation: 15 Years Later

SOA 2012 Life & Annuity Symposium May 21-22, 2012 Session 31 PD, Life Insurance Illustration Regulation: 15 Years Later Moderator: Kurt A. Guske, FSA, MAAA Presenters: Gayle L. Donato, FSA, MAAA Donna

SOA 2012 Life & Annuity Symposium May 21-22, 2012 Session 31 PD, Life Insurance Illustration Regulation: 15 Years Later Moderator: Kurt A. Guske, FSA, MAAA Presenters: Gayle L. Donato, FSA, MAAA Donna

Life 2008 Spring Meeting June 16-18, 2008. Session 93, Insurance Taxation in the United States and Canada Similarities and Differences

Life 2008 Spring Meeting June 16-18, 2008 Session 93, Insurance Taxation in the United States and Canada Similarities and Differences Moderator Christian J. DesRochers, FSA, MAAA Authors John T. Adney,

Life 2008 Spring Meeting June 16-18, 2008 Session 93, Insurance Taxation in the United States and Canada Similarities and Differences Moderator Christian J. DesRochers, FSA, MAAA Authors John T. Adney,

Participating life insurance

Participating life insurance Wealth Achiever Estate Achiever advisor guide Stability, accountability & strength What s new May 2011 New riders for Wealth Achiever and Estate Achiever max 20 Simply Preferred

Participating life insurance Wealth Achiever Estate Achiever advisor guide Stability, accountability & strength What s new May 2011 New riders for Wealth Achiever and Estate Achiever max 20 Simply Preferred

Practice Education Course Individual Life and Annuities Exam June 2011 TABLE OF CONTENTS

Practice Education Course Individual Life and Annuities Exam June 2011 TABLE OF CONTENTS THIS EXAM CONSISTS OF SEVEN (7) WRITTEN ANSWER QUESTIONS WORTH 51 POINTS AND EIGHT (8) MULTIPLE CHOICE QUESTIONS

Practice Education Course Individual Life and Annuities Exam June 2011 TABLE OF CONTENTS THIS EXAM CONSISTS OF SEVEN (7) WRITTEN ANSWER QUESTIONS WORTH 51 POINTS AND EIGHT (8) MULTIPLE CHOICE QUESTIONS

Nationwide YourLife Indexed UL. Give clients a balanced life FOR INSURANCE PROFESSIONAL USE ONLY NOT FOR DISTRIBUTION WITH THE PUBLIC

advisor GUIDE Nationwide YourLife Indexed UL Give clients a balanced life FOR INSURANCE PROFESSIONAL USE ONLY NOT FOR DISTRIBUTION WITH THE PUBLIC Preparing for the future can be stressful for your clients.

advisor GUIDE Nationwide YourLife Indexed UL Give clients a balanced life FOR INSURANCE PROFESSIONAL USE ONLY NOT FOR DISTRIBUTION WITH THE PUBLIC Preparing for the future can be stressful for your clients.

Understanding the Income Taxation of Life Insurance

A Reference Guide for Individuals and Businesses Understanding the Income Taxation of Life Insurance Answers to Frequently Asked Questions Tax Insights Contents 1 General Questions 4 Non-MEC Policy Questions

A Reference Guide for Individuals and Businesses Understanding the Income Taxation of Life Insurance Answers to Frequently Asked Questions Tax Insights Contents 1 General Questions 4 Non-MEC Policy Questions

Participating life insurance

Participating life insurance Wealth Achiever Estate Achiever Canada Life offers two participating life insurance products from which to choose: Wealth Achiever and Estate Achiever. Both combine the strength

Participating life insurance Wealth Achiever Estate Achiever Canada Life offers two participating life insurance products from which to choose: Wealth Achiever and Estate Achiever. Both combine the strength

Canada Life participating life insurance Historical performance

Canada Life participating life insurance Historical performance Even during times of economic uncertainty Canada Life s participating account dividend scale interest rate has been relatively stable, compared

Canada Life participating life insurance Historical performance Even during times of economic uncertainty Canada Life s participating account dividend scale interest rate has been relatively stable, compared

UNDERSTANDING PARTICIPATING WHOLE LIFE INSURANCE

UNDERSTANDING PARTICIPATING WHOLE LIFE INSURANCE equimax CLIENT GUIDE ABOUT EQUITABLE LIFE OF CANADA Equitable Life is one of Canada s largest mutual life insurance companies. For generations we ve provided

UNDERSTANDING PARTICIPATING WHOLE LIFE INSURANCE equimax CLIENT GUIDE ABOUT EQUITABLE LIFE OF CANADA Equitable Life is one of Canada s largest mutual life insurance companies. For generations we ve provided

Are Insurance Premiums Deductible?

Are Insurance Premiums Deductible? August 2014 Can I deduct the premiums? That s a question you probably hear when you re presenting an insurance concept. Unfortunately, the answer is generally no insurance

Are Insurance Premiums Deductible? August 2014 Can I deduct the premiums? That s a question you probably hear when you re presenting an insurance concept. Unfortunately, the answer is generally no insurance

Whole Life Insurance. John Perre Regional Life Sales Manager

Introduction to Whole Life Insurance John Perre Regional Life Sales Manager Agenda Introduction to Equitable Life Stock company VS a mutual company Benefits of dealing with a Mutual Company Introduction

Introduction to Whole Life Insurance John Perre Regional Life Sales Manager Agenda Introduction to Equitable Life Stock company VS a mutual company Benefits of dealing with a Mutual Company Introduction

Life Insurance Review

Supplemental Illustration Prepared by: MetLife Agent Financial Services Representative 200 Park Ave. New York, NY 10166 Insurance Products: Not A Deposit Not FDIC-Insured Not Insured By Any Federal Government

Supplemental Illustration Prepared by: MetLife Agent Financial Services Representative 200 Park Ave. New York, NY 10166 Insurance Products: Not A Deposit Not FDIC-Insured Not Insured By Any Federal Government

holistic retirement advice

Protecting your v business with holistic retirement advice a Let s talk about the Corporate Investment Shelter strategy a Life insurance is wealth protection Total wealth = human capital + financial capital

Protecting your v business with holistic retirement advice a Let s talk about the Corporate Investment Shelter strategy a Life insurance is wealth protection Total wealth = human capital + financial capital

Corporate Insured Retirement Plan. Because successful businesses need security and income

Corporate Insured Retirement Plan Because successful businesses need security and income The Opportunity Business owners who need insurance to Fund a buy-sell agreement between partners of the company

Corporate Insured Retirement Plan Because successful businesses need security and income The Opportunity Business owners who need insurance to Fund a buy-sell agreement between partners of the company

SunUniversalLife. Advisor guide. What s inside. Life s brighter under the sun ADVISOR USE ONLY. investment accounts. product overview.

Life insurance Permanent ADVISOR USE ONLY SunUniversalLife Advisor guide What s inside product overview cost of insurance death benefit options joint and multiple life coverages investment accounts taxation

Life insurance Permanent ADVISOR USE ONLY SunUniversalLife Advisor guide What s inside product overview cost of insurance death benefit options joint and multiple life coverages investment accounts taxation

George F. Lengvari, Sr., Ph.D., LL.B., C.L.U.

George F. Lengvari, Sr., Ph.D., LL.B., C.L.U. George Lengvari is Chairman, Lengvari & Associates Inc., Vancouver, B.C., President & CEO, John Wordsworth, CLU. Past President of the Chartered Life Underwriters

George F. Lengvari, Sr., Ph.D., LL.B., C.L.U. George Lengvari is Chairman, Lengvari & Associates Inc., Vancouver, B.C., President & CEO, John Wordsworth, CLU. Past President of the Chartered Life Underwriters

INSURANCE 10 FORUM APRIL 2013

INSURANCE 10 FORUM APRIL 2013 Change PHOTO: ERIC PEARLE / GETTY The winds of change are blowing through Canada s insurance industry in the form of a shrinking product lineup on the shelves of many insurance

INSURANCE 10 FORUM APRIL 2013 Change PHOTO: ERIC PEARLE / GETTY The winds of change are blowing through Canada s insurance industry in the form of a shrinking product lineup on the shelves of many insurance

Policyholder Protection In Mutual Life Insurance Company Reorganizations

Policyholder Protection In Mutual Life Insurance Company Reorganizations Introduction This practice note was prepared by a work group organized by the Committee on Life Insurance Financial Reporting of

Policyholder Protection In Mutual Life Insurance Company Reorganizations Introduction This practice note was prepared by a work group organized by the Committee on Life Insurance Financial Reporting of

Lifetime income benefit

London Life segregated policies Lifetime income benefit Guarantee your income for life GUARANTEES PROTECTION STRENGTH Financial strength and stability London Life, together with Great-West Life and Canada

London Life segregated policies Lifetime income benefit Guarantee your income for life GUARANTEES PROTECTION STRENGTH Financial strength and stability London Life, together with Great-West Life and Canada

Lifetime income benefit

Canada life segregated Funds Lifetime income benefit Guarantee your income for life Grow income don t allow it to decrease Financial strength and stability Founded in 1847, Canada Life TM was Canada s

Canada life segregated Funds Lifetime income benefit Guarantee your income for life Grow income don t allow it to decrease Financial strength and stability Founded in 1847, Canada Life TM was Canada s

Are you satisfied with the progress you ve made toward your retirement?

Are you satisfied with the progress you ve made toward your retirement? Neither New York Life Insurance Company nor its agents provides tax, legal, or accounting advice. Please consult your own tax, legal,

Are you satisfied with the progress you ve made toward your retirement? Neither New York Life Insurance Company nor its agents provides tax, legal, or accounting advice. Please consult your own tax, legal,

Pricing exercise based on a collection of actuarial assumptions Assumptions generally divided into two sets

Whole Life Pricing Pricing exercise based on a collection of actuarial assumptions Assumptions generally divided into two sets Company specific: Mortality, Lapsation, Expenses, Dividends, etc. Prescription

Whole Life Pricing Pricing exercise based on a collection of actuarial assumptions Assumptions generally divided into two sets Company specific: Mortality, Lapsation, Expenses, Dividends, etc. Prescription

Insured Annuities Introduction How Does it Work? Annuity Characteristics Life Insurance Characteristics

Insured Annuities Introduction An insured annuity is an arrangement that involves the purchase of two contracts: a life annuity and an insurance policy. When viewed together, the combination of these contracts

Insured Annuities Introduction An insured annuity is an arrangement that involves the purchase of two contracts: a life annuity and an insurance policy. When viewed together, the combination of these contracts

Leveraged Life Insurance Personal Ownership

Leveraged Life Insurance Personal Ownership Introduction Leveraged life insurance is a financial planning strategy that uses the cash value of an exempt life insurance policy as collateral security for

Leveraged Life Insurance Personal Ownership Introduction Leveraged life insurance is a financial planning strategy that uses the cash value of an exempt life insurance policy as collateral security for

SAMPLE. is equal to the Death Benefit less the Account Value of your policy.

DEFINITIONS EquiLife Limited Pay UL (Joint first-to-die) The following are definitions of some of the terms used in your EquiLife Joint First-to-Die policy. If you need additional information or clarification

DEFINITIONS EquiLife Limited Pay UL (Joint first-to-die) The following are definitions of some of the terms used in your EquiLife Joint First-to-Die policy. If you need additional information or clarification

MML Bay State Life Insurance Company Management s Discussion and Analysis Of the 2005 Financial Condition and Results of Operations

MML Bay State Life Insurance Company Management s Discussion and Analysis Of the 2005 Financial Condition and Results of Operations General Management s Discussion and Analysis of Financial Condition and

MML Bay State Life Insurance Company Management s Discussion and Analysis Of the 2005 Financial Condition and Results of Operations General Management s Discussion and Analysis of Financial Condition and

Insured Annuity Strategy General Issues

February 7, 2005 Insured Annuity Strategy General Issues Additional considerations that apply to corporations, individuals or trusts Tax Hélène Marquis, LL.L., D. Fis., Pl. Fin, TEP Senior Planning Consultant

February 7, 2005 Insured Annuity Strategy General Issues Additional considerations that apply to corporations, individuals or trusts Tax Hélène Marquis, LL.L., D. Fis., Pl. Fin, TEP Senior Planning Consultant

THE EMPIRE LIFE INSURANCE COMPANY TRILOGY. Policy Summary

Policy Summary This Policy Summary is dated June 1, 2012. When you make a change to your Contract, we will issue a new version of these pages. The Policy Summary with the most recent date replaces any

Policy Summary This Policy Summary is dated June 1, 2012. When you make a change to your Contract, we will issue a new version of these pages. The Policy Summary with the most recent date replaces any

Estate Planning. Insured Inheritance. Income Shelter. Insured Annuity. Capital Gains Protector

Estate Planning Insured Inheritance The Insured Inheritance concept demonstrates an opportunity to shelter a lump sum investment from income tax and to ensure that the maximum tax-free dollars become available

Estate Planning Insured Inheritance The Insured Inheritance concept demonstrates an opportunity to shelter a lump sum investment from income tax and to ensure that the maximum tax-free dollars become available

M INTELLIGENCE. Dividend Interest Rates for 2015. Dividend Interest Rate. July 2015. Life insurance due. care requires an

M INTELLIGENCE July 2015 Life insurance due care requires an understanding of the factors that impact policy performance and drive product selection. M Financial Group continues to lead the industry in

M INTELLIGENCE July 2015 Life insurance due care requires an understanding of the factors that impact policy performance and drive product selection. M Financial Group continues to lead the industry in

InsuranceIQ Bank & Trust. Prepared for: Gregory & Patricia Toppins Insurance Trust Dated 3/15/2007. Policy Owner: InsuranceIQ#: 0001-00010-01

Date Completed: 3/22/2013 Prepared for: InsuranceIQ Bank & Trust Policy Owner: InsuranceIQ#: 0001-00010-01 Prepared for: InsuranceIQ Bank & Trust Branch Code: West 1st Street External Trustee(s): Trustee:

Date Completed: 3/22/2013 Prepared for: InsuranceIQ Bank & Trust Policy Owner: InsuranceIQ#: 0001-00010-01 Prepared for: InsuranceIQ Bank & Trust Branch Code: West 1st Street External Trustee(s): Trustee:

Corporate estate transfer with cash withdrawal

Life Insurance Solutions guarantees products assets opportunities growth capital protection income benefit solutions options stability Plan today. Provide tomorrow. Corporate estate transfer with cash

Life Insurance Solutions guarantees products assets opportunities growth capital protection income benefit solutions options stability Plan today. Provide tomorrow. Corporate estate transfer with cash

THE CHALLENGE OF LOWER

Recent interest rates have declined to levels not seen in many years. Although the downward trend has reversed, low interest rates have already had a major impact on the life insurance industry. INTEREST

Recent interest rates have declined to levels not seen in many years. Although the downward trend has reversed, low interest rates have already had a major impact on the life insurance industry. INTEREST

DUE CARE BULLETIN. Assessing the Impact of Low Interest Rates on Life Insurance Products. February 2012. Life insurance due

DUE CARE BULLETIN February 2012 Life insurance due care requires an understanding of the factors that impact policy performance and drive product selection. M Financial Group continues to lead the industry

DUE CARE BULLETIN February 2012 Life insurance due care requires an understanding of the factors that impact policy performance and drive product selection. M Financial Group continues to lead the industry

INDUSTRIAL-ALLIANCE LIFE INSURANCE COMPANY. FIRST QUARTER 2000 Consolidated Financial Statements (Non audited)

") INDUSTRIAL-ALLIANCE LIFE INSURANCE COMPANY FIRST QUARTER 2000 Consolidated Financial Statements (Non audited) March 31,2000 TABLE OF CONTENTS CONSOLIDATED INCOME 2 CONSOLIDATED CONTINUITY OF EQUITY 3 CONSOLIDATED

INDUSTRIAL-ALLIANCE LIFE INSURANCE COMPANY FIRST QUARTER 2000 Consolidated Financial Statements (Non audited) March 31,2000 TABLE OF CONTENTS CONSOLIDATED INCOME 2 CONSOLIDATED CONTINUITY OF EQUITY 3 CONSOLIDATED

your guide to equation gen IV

your guide to EQUATION GENERATION IV equation gen IV CLIENT GUIDE ABOUT EQUITABLE LIFE OF CANADA Equitable Life is the largest federally regulated mutual life insurance company in Canada. For generations

your guide to EQUATION GENERATION IV equation gen IV CLIENT GUIDE ABOUT EQUITABLE LIFE OF CANADA Equitable Life is the largest federally regulated mutual life insurance company in Canada. For generations

Understanding Sun Par Protector and Sun Par Accumulator

LIFE INSURANCE Participating whole life Understanding Sun Par Protector and Sun Par Accumulator POLICYHOLDER DIVIDENDS Sun Par Protector and Sun Par Accumulator are participating life insurance products.

LIFE INSURANCE Participating whole life Understanding Sun Par Protector and Sun Par Accumulator POLICYHOLDER DIVIDENDS Sun Par Protector and Sun Par Accumulator are participating life insurance products.

Kansas City 2Life Insurance Company

Kansas City 2Life Insurance Company 2011 Second Quarter Report Includes our subsidiaries: Sunset Life Insurance Company of America Old American Insurance Company Sunset Financial Services, Inc. Post Office

Kansas City 2Life Insurance Company 2011 Second Quarter Report Includes our subsidiaries: Sunset Life Insurance Company of America Old American Insurance Company Sunset Financial Services, Inc. Post Office

An Assessment of No Lapse Guarantee Products and Alternatives. Prepared and Researched by

An Assessment of No Lapse Guarantee Products and Alternatives Prepared and Researched by No Lapse Guarantee (NLG) products continue to be very popular with clients, primarily for their low cost and guaranteed

An Assessment of No Lapse Guarantee Products and Alternatives Prepared and Researched by No Lapse Guarantee (NLG) products continue to be very popular with clients, primarily for their low cost and guaranteed

UNDERSTANDING PARTICIPATING WHOLE LIFE INSURANCE

UNDERSTANDING PARTICIPATING WHOLE LIFE INSURANCE equimax CLIENT GUIDE ABOUT EQUITABLE LIFE OF CANADA Equitable Life is one of Canada s largest mutual life insurance companies. For generations we ve provided

UNDERSTANDING PARTICIPATING WHOLE LIFE INSURANCE equimax CLIENT GUIDE ABOUT EQUITABLE LIFE OF CANADA Equitable Life is one of Canada s largest mutual life insurance companies. For generations we ve provided

YOUR GUIDE TO EQUILIFE LIMITED PAY UNIVERSAL LIFE

YOUR GUIDE TO EQUILIFE LIMITED PAY UNIVERSAL LIFE equilife CLIENT GUIDE ABOUT EQUITABLE LIFE OF CANADA Equitable Life is one of Canada s largest mutual life insurance companies. For generations we ve provided

YOUR GUIDE TO EQUILIFE LIMITED PAY UNIVERSAL LIFE equilife CLIENT GUIDE ABOUT EQUITABLE LIFE OF CANADA Equitable Life is one of Canada s largest mutual life insurance companies. For generations we ve provided

Lifetime income benefit

Canada life segregated Funds Lifetime income benefit Guarantee your income for life Grow income don t allow it to decrease Financial strength and stability Canada Life, founded in 1847, was Canada s first

Canada life segregated Funds Lifetime income benefit Guarantee your income for life Grow income don t allow it to decrease Financial strength and stability Canada Life, founded in 1847, was Canada s first

Arshil Jamal President and Chief Operating Officer Canada Life Capital Corporation

Scotia Capital Financials Summit September 8, 2011 Arshil Jamal President and Chief Operating Officer Canada Life Capital Corporation Cautionary Note regarding Forward-looking Information This report contains

Scotia Capital Financials Summit September 8, 2011 Arshil Jamal President and Chief Operating Officer Canada Life Capital Corporation Cautionary Note regarding Forward-looking Information This report contains

Key Person Insurance. Protecting Your Business From The Loss Of Key Employees. Place Image Here. Prepared For: Valued Company. Presented By:... Tel.:.

Key Person Insurance Protecting Your Business From The Loss Of Key Employees Place Image Here Prepared For: d Company Presented By:.... Tel.:. Insurance products are issued by: Insurance John Hancock products

Key Person Insurance Protecting Your Business From The Loss Of Key Employees Place Image Here Prepared For: d Company Presented By:.... Tel.:. Insurance products are issued by: Insurance John Hancock products

The Corporate Investment Shelter. Corporate investments

September 2012 The Corporate Investment Shelter Many successful business owners retire with more assets than they need to live well. With that realization, their focus can shift from providing retirement

September 2012 The Corporate Investment Shelter Many successful business owners retire with more assets than they need to live well. With that realization, their focus can shift from providing retirement

PRIVATE FIXED INCOME ASSETS: CAPTURING THE LIQUIDITY PREMIUM

PRIVATE FIXED INCOME ASSETS: CAPTURING THE LIQUIDITY PREMIUM EUGENE LUNDRIGAN CHIEF OPERATING OFFICER SUN LIFE INVESTMENT MANAGEMENT INC. AGENDA 1 2 3 4 5 Challenging times for pension funds Search for

PRIVATE FIXED INCOME ASSETS: CAPTURING THE LIQUIDITY PREMIUM EUGENE LUNDRIGAN CHIEF OPERATING OFFICER SUN LIFE INVESTMENT MANAGEMENT INC. AGENDA 1 2 3 4 5 Challenging times for pension funds Search for