DISCUSSION PAPER PI-1409

|

|

|

- Domenic Boyd

- 8 years ago

- Views:

Transcription

1 DISCUSSION PAPER PI-1409 The consequences of not having to buy an annuity David Blake June 2014 ISSN X The Pensions Institute Cass Business School City University 106 Bunhill Row London EC1Y 8TZ UNITED KINGDOM

2 The consequences of not having to buy an annuity David Blake Pensions Institute Cass Business School 106 Bunhill Row London EC1Y 8TZ United Kingdom June

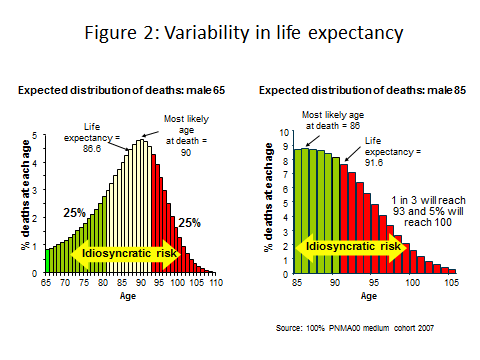

3 Introduction In his Budget speech on 19 March 2014, the Chancellor announced the biggest change in pension policy in 100 years: Pensioners will have complete freedom to draw down as much or as little of their pension pot as they want, any time they want. No caps. No drawdown limit. Let me be clear. No one will have to buy an annuity People who have worked hard and saved hard all their lives, and done the right thing, should be trusted with their own finances. There was widespread approval of this policy change. Typical is the following: For most people the issue isn't about irresponsible spending - they'll want to try to make their pension pot last their remaining lifetime - it's about knowing how much they can safely spend each year without their pot running out. This depends on a number of variables - where they invest, the pattern of investment returns, charges, inflation, how long they live etc. Not only will it encourage people to open their eyes to other retirement income options, which have actually been there for some time, it may also incentivise greater retirement saving overall since people will have a greater feeling of control over their money. This is great for the industry and savers alike. Everybody wins. (Why pensioners won't buy that Lamborghini, by Colin Bell, product director at Aegon Ireland, Professional Adviser, 8 April 2014) The implication of this is that a few variables - where they invest, the pattern of investment returns, charges, inflation, how long they live, etc - can be reliably estimated and so there is no need to buy an annuity in retirement. But how long someone lives cannot be reliably estimated unless they have a terminal condition. Figure 1 shows that in advanced countries, life expectancy has been increasing at the rate of approximately 2 years per decade since But being told their life expectancy, as the Pensions Minister promises to do, is a completely useless piece of information for someone who has just retired, since there is an approximately 50% chance that a 65-year old man will live beyond his life expectancy of 86.7 years as the left chart in Figure 2 shows. It doesn t get easier at higher ages. Telling an 85-year old man that his life expectancy is 91.6 years is also of little use, since one-in-three 85-year old men will reach 93 and 5% will reach 100 as the right chart in Figure 2 shows. Further, individuals are notoriously bad at estimating their own life expectancy. Figure 3 reveals that all age groups and men more than women significantly underestimate their own life expectancy. The extent of the underestimation decreases with age, but men in their 60s underestimate by an average of five years and women by three. So if a retiree plans to draw down their pension fund in line with their own estimate of their life expectancy, a typical male will outlive their pension pot by five years and a typical female by three. 2

4 3

5 One might assume that the government would be better at estimating life expectancy than individuals. Unfortunately this is not the case. The official agency for estimating life expectancy in the UK is the Office for National Statistics. Figure 4 indicates that the ONS has systematically and significantly underestimated the increase in life expectancy since

6 Even if we could improve our forecasts of the trend improvement in life expectancy, there will always be considerable uncertainty around the trend. The longevity fan chart in Figure 5 shows that the best estimate of male life expectancy at age 65 in 2060 is 26 years, but it could be anywhere from 22 years to 28 years, a range of 6 years. There seems to be little point in telling a 20-year old male that his life expectancy could be anywhere between 87 and 93 years. The information contained in Figures 1 to 5 is clearly not well understood at the Treasury. It is also not well understood within much of the pensions industry. Certainly it is not understood by those who agree with the Chancellor that individuals should be trusted with their own finances since they have no intention of engaging in irresponsible spending. This is nothing to do with irresponsibility and everything to do with the flawed proposal that longevity is a risk that individuals can both understand and manage themselves. What the Chancellor proposes, therefore, is to transfer longevity risk (both trend and idiosyncratic) from a collective pooled system (insurance) to individual retail customers (DC scheme members). As members of DC schemes, they already bear all the risks in the accumulation phase: contribution risk, investment risk, and interest rate risk. They now have to face all the risks in the decumulation stage: inflation risk as well as longevity risk. These risks were collectively too big for private sector UK employers to bear which is why they have closed down their defined benefit schemes. It seems that the Chancellor has forgotten the definition of a pension scheme which is to provide retirement income security for however long the scheme member lives. For DC, there is only one financial instrument ever devised that provides this security the lifetime annuity. This is why the use of a lifetime annuity is an essential component of a well-designed DC plan at some point during decumulation. Yet the Chancellor has just decided that annuities are not necessary. 5

7 Lifetime annuities are by far the greatest single financial innovation of all time. The fact that a group of people can pool their pension pots and each one can draw an income for however long they live is truly remarkable. Just as remarkable is the fact that this product can provide good value for money. 1 There is, of course, nothing to stop individual retirees from buying an annuity, but all the evidence indicates that, given the choice, many, if not most, won t: annuity sales have plummeted since the Budget. 2 The problem is that most people do not believe that annuities provide good value for money. Even worse, most people think that they are unnecessary. This is a potentially lethal combination if people have the freedom to choice whether or not to buy an annuity. It s rather like being invited to jump out of an aircraft at 30,000 feet and being told that you now have the freedom to choose whether or not to use a parachute. Choosing not to annuitise is fundamentally no different from choosing not to wear a parachute. But few people see this. We should be under no illusions. The ending of the requirement to annuitise at some stage means the effective end of private sector pensions in the UK. A pension scheme without a lifetime annuity is not a pension scheme. So what originally were pension schemes will now become mere savings schemes. Let us now look more closely at how this monumental change will affect the various participants in the pensions market The individual perspective The decumulation decision the optimal running down of assets in retirement is extremely complex. It involves not only pension assets, but also non-pension assets and decisions have to be made about inheritance, taxation and long term care etc. If mistakes are made and the assets are invested unwisely or spent too quickly, retired people do not generally have the option to re-enter the labour market to earn some more money in the way that younger people do. Further, these decisions might have to be made in presence of reduced mental capacity, as is the case with someone with dementia. I like to use the analogy of an aircraft journey. The ascent stage is equivalent to the accumulation stage of a pension scheme and the descent stage is equivalent to the decumulation stage. Getting a plane to take off is easy. Getting it to land safely in the right place at the right time is an order of 1 Edmund Cannon and Ian Tonks (2009) Money s Worth of Pension Annuities, DWP Research Report No. 563; Edmund Cannon and Ian Tonks (2008) Annuity Markets, Oxford University Press, Oxford. 2 The Pensions Policy Institute identifies a number of countries where the voluntary purchase of annuities is high. In Switzerland, the annuitisation level is around 80% and this is put down to cultural attitudes with financially conservative Swiss workers preferring guaranteed incomes for life. In Chile, 70% of DC assets are annuitised and this is explained by the high charges on drawdown products. Annuitisation levels are also high in Singapore and Denmark and this is put down to the fact the decision about whether to annuitise has to be made at a relatively young age, at 55 in the case of Singapore and even earlier in the accumulation phase in Denmark. Israel s high level of annuitisation is explained by high annuity rates that are subsidised by government bonds. (Pensions Policy Institute (2014) Freedom and Choice in Pensions: Comparing International Retirement Systems and the Role of Annuitisation, PPI Briefing Note No. 66, May 2014). 6

8 magnitude a more complex problem. The same is true of a pension scheme. Starting a pension scheme is easy compared with task of making the accumulated savings last as long as you do. 3 Yet look at the effort this country put into getting 9 million lower paid workers to start a pension scheme, summarised by the word auto-enrolment. Let us remember how auto-enrolment works. It is wholly dependent on the most powerful behavioural trait - member inertia: inertia over whether to join the pension scheme, inertia over the contribution rate, inertia over the investment strategy. Relying on inertia was universally accepted by all political parties as way to get these 9 million workers to join a pension scheme. The policy change in the Budget completely undermines the inertia principle by turning autoenrolled DC plan members most of whom did not know much about their pension scheme anyway into airline pilots preparing to land an aircraft containing their partner, children and grandchildren. Remember, we are at 30,000 feet with a plane about to begin its descent. A passenger and all auto-enrolees have been passengers up until now is going to be invited into the pilot s seat having never flown a plane before and the plane has limited fuel and no parachutes. Not to worry, help is at hand in the form of advice, or should I say guidance. The pilot is going to get a single piece of advice/guidance at the moment they sit down in the pilot s seat and then they are on their own without any further help. And there are 400,000 newly advised/guided pilots per year in the UK in this position. What could possibly go wrong? The decumulation stage used to be fairly simple. You retired, took a 25% tax-free lump sum and handed the rest of the pension pot to an insurance company in exchange for an annuity. Then it started to get more complicated you could delay the annuity purchase until age 75 and use income drawdown before then. As mentioned, under the Chancellor s proposals, the decumulation landscape will become hugely complicated for individuals in relation to the issues of investment, inflation, longevity, taxation, non-pension assets, inheritance and long-term care. One of the most important things to recognise is that the alternatives to annuitisation principally income drawdown involve more risk. People can only get a higher return than an annuity by taking on more risk and the extra return is not guaranteed. Almost immediately after the Budget, scheme members were being encouraged to take on more risk. 4 Drawdown also has higher charges anyone who believes that annuities are expensive should ask themselves whether the 2-4% annual charge on drawdown represents good value for money. 5,6 3 David Blake, Andrew Cairns, and Kevin Dowd (2009) Designing a Defined-Contribution Plan: What to Learn from Aircraft Designers, Financial Analysts Journal, 65(1), Savers should consider taking more risk with their pensions in light of new government rules, by Chris Torney, express.co.uk, 23 April These are just the visible costs. There are also the hidden costs of investment management which reduce the net returns to savers and these can be larger than the visible costs: see David Blake (2014), On the Disclosure of the Costs of Investment Management, Pensions Institute Discussion Paper PI-1407, May ( 6 Australia is often put forward as an example of a country with a good pension system that does not have mandatory annuitisation. However, the charges in Australian pension schemes are very high: see Jim Minifie 7

9 If people were capable of behaving rationally and were sufficiently well informed, they could calculate the risk-return tradeoff between an annuity and drawdown and choose which was initially better for them and, more important, when it was optimal to switch from drawdown to an annuity. But most people neither behave rationally nor have the technical skills to evaluate the risk-return tradeoff. People have behavioural biases which prevent them behaving rationally. In particular, the emphasis on pot size rather than the income in retirement is very bad from a behavioural perspective. To most people a pot size of 30,000 sounds like a lot of money, but it is not when it has to last possibly for the next 30 years. Surely, it is better to be realistic about what the pension pot buys as an annual income? A particular advantage of an annuity is that it acts as a valuable pre-commitment device (i.e., is a very valuable behavioural tool). An annuity helps control spending in retirement. Many people are unable to control their spending. A survey by Aviva in April 2014 reveals that 61% will find it difficult to resist spending the pension pot. They could spend their money too quickly in retirement and be reduced to living on the single tier pension of 144 per week. This could involve a massive reduction in their standard of living and they will not even have a rainy day fund to fall back on. A more extreme example is people who are desperate for money at any price as Wonga and pension liberation cases show. There will also be people with the opposite set of behavioural traits, those who take excessive precautions and put everything into a rainy day fund and hence spend their money too slowly. Such people could have enjoyed a higher standard of living in their retirement had they had an annuity, taking comfort from the fact that next month another annuity payment will come in should they live that long. The new regime will create other distortions. The virtuous circle of a pension system is that it promotes savings which are transferred to investment which increases the productive capital stock which, in turn, increases productivity and national income. But what happens in the UK? We are not interested in the productive capital stock. We are only interested in houses. That is our capital stock. So (interest only) pension mortgages will come back with the pension lump sum used to pay off the mortgage. In addition, vast amounts of the pension savings of this country will end up in buyto-let property investments. 7 In the light of all this, the idea that a single piece of advice/guidance will be adequate is clearly ludicrous. Nor is it clear the age at which this advice/guidance should take place. The reality is that there would need to be regular annual advice/guidance from age 55 if not earlier. But who is going to pay for this? A survey conducted by Hyman Robertson in May 2014 suggested that only 1.2% would be willing to pay for regular advice, while 50% said they would rely entirely on the free government-backed guidance. (2014), Super Sting: How to Stop Australians Paying Too Much for Superannuation, Grattan Institute Report No , April The value of flats and houses in the buy-to-let market is estimated at 1.25 trillion, not far short of the 1.6 trillion in occupational pension schemes (Richard Dyson, 1,250bn: how buy-to-let is overtaking pensions, Daily Telegraph, Your Money Supplement, 31 May 2014) 8

10 The company perspective If pensions have become more complex for individuals, they have become much easier for companies with one very important exception which will create long-term problems for businesses. Companies with legacy defined benefit (DB) schemes will naturally welcome the new regime. They will welcome and encourage DB scheme members switching via cash equivalent transfer values (CETVs) to the new DC regime, so they can take the cash. This will immediately remove inflation risk and longevity risk from their balance sheets. For older workers with final salary schemes, these pension benefits could be worth hundreds of thousands of pounds if not millions (compared with the current 30,000 average pension pot with a DC scheme). These are huge sums to put at risk in this way and the income drawdown merchants will be contacting everyone in the land. These merchants might actually be encouraged to do this by the DB scheme member s own family, newly aware that grand-dad suddenly has access to a million quid which could provide a very useful deposit for a grand-child s mortgage or be used for more buy-to-let properties. 8 The exception is the reason why companies set up pension schemes in the first place. Pension schemes started to manage the exit of old unproductive workers from the firm initially as a lump sum gratuity and later as a pension annuity. If 55 year olds blow their pension pot, they will not be able to afford to retire, so the new regime takes away the ability of companies to manage the exit of their old workers from the labour force. The relationship between generations There is a potential massive moral hazard if one generation decides to become profligate with its pension wealth and goes on a big spending spree. Once it has run out of money, it will turn to the state and begin demanding means-tested welfare benefits. 9 This is a fine art in Australia a country with no requirement to annuitise where they call this practice double dipping. Since older people tend to vote in larger numbers than younger people, they will be able to put political pressure on politicians to raise these means-tested benefits. This, in turn, will require massive bailouts from the next generation of taxpayers and result in intergenerational inequity. Tax The new regime will bring forward tax revenues the Budget forecasts for tax receipts anticipate this. 8 This has already started. On 21 May 2014, the Financial Conduct Authority (FCA) began warning the public about offers of free pension reviews from companies claiming to act on behalf of the FCA, but in fact are not authorised to conduct such reviews. The FCA said it has evidence of people being contacted out of the blue via phone calls, s, text messages or online adverts. The FCA said the reviews are designed to persuade people to move their pension pot from an existing personal or occupational pension scheme to a self-invested personal pension or small self-administered scheme. The pension pot is then typically invested in unregulated investments like overseas property developments, forestry or storage units known as store pods. 9 Under the Government s proposals, people in receipt of only the full single-tier pension will be able to claim Housing Benefit, Council Tax Reduction and other means-tested benefits. 9

11 But the ending of annuitisation raises fundamental questions over the role of tax relief on contributions and investment returns in pension schemes. The current system of pension tax relief is predicated on the following principle. Individuals are incentivised to save for a pension via tax relief on contributions and investment returns. In exchange for this generosity, pension scheme members were required to annuitise their pension pot in order to control their spending in retirement and not fall back on the state. At the same time, the pension would be taxed and the taxes received would be higher than if the tax relief on contributions and investment returns had not been given, by an amount that makes the system broadly neutral over the life cycle. Now that there is no requirement to annuitise, the justification for providing tax relief has gone. The pension scheme has been turned into a mere wealth accumulation scheme. That raises a big question: why should tax payers pay 54 billion in tax relief on contributions to asset accumulation schemes which could be spent on Lamborghinis even if most people have no plans to buy one. You can still make the regime tax neutral, but why bother in the first place? There will also now be an inconsistency between the system of tax relief on the other big savings scheme in this country, ISAs. With a pension scheme, contributions are tax relieved, investment returns are tax free, and the withdrawals are taxed. With ISAs, contributions are made from post-tax income, investment returns are tax free, and the withdrawals are tax free. There is no logically reason to retain both systems of tax relief, and it seems logical for the government to withdraw the most expensive one. Implications for regulation Regulators now face the same complexity in monitoring the decisions of individuals as those individuals have in making them. It used to be the case that a single decision (buy an annuity) was made on a single day (retirement date). That made life easy for regulators since they could focus on what investment managers were delivering before retirement and what life assurers were delivering after. Then when drawdown was introduced in 1995, two decisions had to be made: annuity or drawdown. This increased the complexity of the regulatory regime, since, for the first time, fund managers were able to encroach on the territory that had previously been exclusively that of insurers. But, there is now the possibility of decisions being made on any day after the age of 55. In addition to all this are the different regimes for contract-based and trust-based schemes. Another important question is who will collect and collate the data on this the Financial Conduct Authority, The Pensions Regulator, or the Treasury? Implications for annuities It is already clear that the Budget changes will devastate the world's biggest annuity market. Prior to the Budget, approximately 400,000 annuities with total premiums of 12 billion were sold annually in the UK. This was more than half of all global sales. The next biggest market is Chile with 22,000 annual sales. At the bottom of the list is Australia with just 30 voluntary annuities sold per year. Within a month of the Budget, sales of annuities have fallen by 40-50%, and could fall by 75% or more, according to predictions made by PwC and Legal & General. At this rate, Chile, where the purchase of annuities at retirement is mandatory, could soon be the world s largest market. While studies have shown that the value for money of annuities sold in the open market is fairly high, it is also true that the internal annuities sold to its existing clients are very poor value in many 10

12 cases 30% poorer than the OMO annuities. So the insurance industry was asking for trouble by failing to rectify this. But the government has not helped either. Quantitative Easing has had a material effect in driving down annuity yields. Further, the government could have helped annuity providers hedge the systematic longevity trend risk they face by issuing longevity bonds, but it has failed to do so. 10 Solvency 2 with its additional capital requirements - will drive down annuity yields even more. The money s worth of annuities reflects the risks insurers take and the regulatory capital they are required to post. These risks have now been passed back to individuals. For those individuals who do buy annuities in the voluntary market the value for money will now be considerably lower due to selection effects and lower overall sales. Further, it is likely that such annuities will be fully underwritten individuals will have to answer a full medical questionnaire. This will further undermine the insurance pool and make the purchase of an annuity unsuitable for a healthy 65-year old. Implications for investment Immediately following the Budget, the shares of annuity providers fell sharply while those of investment managers and brokers rose sharply, reflecting the new opportunities to extract high charges from drawdown products. There is a real danger of another mis-selling scandal, with highrisk high-cost investment strategies being sold to vulnerable old people. The size of the silver vote is so big that they will demand and get compensation for mis-selling. The new regime will also make investing in the accumulation stage considerably more complex. Now that there is no target date for retirement and that it is possible to draw funds from the pension pot from age 55 without being retired, it is no longer clear what de-risking now means and what future investment strategies such as life-style and target date now have. Proponents of target date funds argue that such funds have the flexibility of dealing with changes in the retirement date: members can simply be moved to a later target date fund if they decide to delay retirement. But I am not convinced that it will be that easy. Many people will have had no previous active engagement with their pension scheme and are unlikely to have done much forward thinking about the optimal investment strategy of their pension fund in the lead up to age 55 when suddenly they can access their fund without any restriction. Will 55 become the default target date? Or will it be the scheme s normal retirement date (if that exists any more)? Depending on the answer, there will be big differences in the two target date funds strategic asset allocations and hence risk-return configuration when the member reaches age 55. A great deal of work now needs to be done on the optimal design of the investment strategies in defined contribution pension schemes that fully integrates the accumulation and decumulation phases and efficiently manages all the risks outlined above. A lot of the theoretical work has already been done, 11 but this now needs to be practically implemented David Blake, Tom Boardman, and Andrew Cairns (2014) Sharing Longevity Risk: Why Governments Should Issue Longevity Bonds, North American Actuarial Journal, 18(1), David Blake, Andrew J.G. Cairns, and Kevin Dowd (2001), PensionMetrics: Stochastic Pension Plan Design and Value-At-Risk During the Accumulation Phase, Insurance: Mathematics and Economics, 29, ; 11

13 Implications for long-term care provision The new regime could have a big impact on the financing of long-term care. If people do spend all their money and so would pass the long-term care means test, this will increase the burden on local authorities if they subsequently need care. The government is aware of this possibility and is proposing to classify this behaviour as deliberate deprivation which would allow the local authority to refuse to pay for care. However, this response would appear to create a curious anomaly. You could have two people of the same age with identical salaries throughout their careers. One spent everything and had no savings when they retired, while the other saved for a pension and so had a decent sized pension pot when they retired. Suppose the person with the pension pot drew it all down and spent it. The former would be entitled to care, while the latter would be accused of deliberate deprivation and hence denied care. Yet both people had done exactly the same thing and spent all their income (and a pension is deferred income after all) before needing long-term care. What is the local authority going to do welcome the first person into a care home and allow the second person to sleep in the street outside the care home? Conclusion It took two years of detailed work by the Pensions Commission to create a political consensus for auto-enrolment, and this was followed by seven years of preparation before auto-enrolment was introduced. The ending of private-sector pensions in the UK was introduced overnight without any consultation or any apparent examination of the evidence or the potential consequences. It could turn out to be a completely reckless policy change. How can this be avoided? It is essential that the decumulation stage of a DC scheme is institutionalised in the same way that auto-enrolment has institutionalised the accumulation stage and taken it out of the high-charge world of retail accumulation products, such as personal pensions. In a similar way, economies of scale and more efficient risk sharing need to be exploited in the decumulation phase to enable good value drawdown products to be designed. We urgently need to move away from retail decumulation products like individual drawdown and retail annuities. An appropriate decumulation product that can be integrated into auto-enrolment might be described as one that: Benefits from institutional design, governance, and pricing. David Blake, Andrew J.G. Cairns, and Kevin Dowd (2003), PensionMetrics 2: Stochastic Pension Plan Design During the Distribution Phase, Insurance: Mathematics and Economics, 33, 29 47; David Blake (2003), Take (Smoothed) Risks When You Are Young, Not When You Are Old: How to Get the Best from Your Pension Plan, IMA Journal of Management Mathematics, 14, ; Andrew J.G. Cairns, David Blake, and Kevin Dowd (2006), Stochastic Lifestyling: Optimal Dynamic Asset Allocation for Defined Contribution Pension Plans, Journal of Economic Dynamics & Control, 30, ; David Blake, Douglas Wright, and Yumeng Zhang (2014) Age-Dependent Investing: Optimal Funding and Investment Strategies in Defined Contribution Pension Plans when Members are Rational Life-Cycle Financial Planners, Journal of Economic Dynamics & Control, 38, A survey by Schroders in May 2014 indicated that 82% of pension scheme trustees would be reviewing their default investment strategy. 12

14 Delivers a reasonably reliable income stream (i.e. with minimal fluctuations). Maintains the purchasing power of the fund. Offers the flexibility to purchase a life annuity at any time (or at regular predetermined intervals to hedge interest rate and longevity risk) Is simple to understand, transparent and low-cost Requires minimal consumer engagement Benefits from a low-cost delivery system. 13 But whatever happens, annuities or something very much like them will remain an essential feature of a pension scheme at some stage. As Figure 6 shows, the survival credits built into annuity rates which increase with age means that it is not a question of if but when pensioners should annuitise. It might well be optimal for healthy retirees with sufficient resources to wait until they are in their late 70s or early 80s before annuitising. It will also be necessary to draw on the lessons of behavioural economics to find ways of nudging pension scheme members into buying annuities when the time is right. 14 Certainly, there needs to be innovation in annuity design and behavioural economics suggests that capital protected or cashback annuities might be attractive to scheme members. If individuals do not have access to low-cost institutionalised decumulation products and instead manage their own decumulation following advice/guidance, then I would expect good advice/guidance to strongly indicate that part of the pension pot be ring fenced for later annuitisation (for example, via the purchase of advanced life deferred annuities 15 ) and that single asset investments such as buy-to-let should be avoided as they do not involve good risk diversification. I am all for freedom and choice in pensions and people may well save more as a result of the Budget, 16 but if we are not careful, the new flexibilities introduced by the Budget will lead to a huge pensions mis-selling scandal and we have been there too many times before. 13 These are interim recommendations from a research study being conducted at the Pensions Institute by Debbie Harrison and David Blake. 14 David Blake and Tom Boardman (2013) Spend More Today Safely: Using Behavioral Economics To Improve Retirement Expenditure Decisions With Speedometer Plans, Risk Management and Insurance Review, 17(1), Also known as longevity insurance: see Guan Gong and Anthony Webb (2010) Evaluating the Advanced Life Deferred Annuity: An Annuity People Might Actually Buy, Insurance: Mathematics and Economics 46, A Legal & General MoneyMood survey in May 2014 found that 44% of those aged said they would save more in a pension scheme as a result of the Budget. 13

15 14

GUIDE TO RETIREMENT PLANNING FINANCIAL GUIDE. Making the most of the new pension rules to enjoy freedom and choice in your retirement

GUIDE TO RETIREMENT PLANNING Making the most of the new pension rules to enjoy freedom and choice in your retirement FINANCIAL GUIDE WELCOME Making the most of the new pension rules to enjoy freedom and

GUIDE TO RETIREMENT PLANNING Making the most of the new pension rules to enjoy freedom and choice in your retirement FINANCIAL GUIDE WELCOME Making the most of the new pension rules to enjoy freedom and

Annuities Market Briefing

Annuities Market Briefing Written by Pensions specialist Dr. Ros Altmann You can read Ros' blog here: http://pensionsandsavings.com/ Annuities are a unique financial product. There is no other investment

Annuities Market Briefing Written by Pensions specialist Dr. Ros Altmann You can read Ros' blog here: http://pensionsandsavings.com/ Annuities are a unique financial product. There is no other investment

Age 75 Annuities Consultation. Response from Dr. Ros Altmann 9 th September 2010

Age 75 Annuities Consultation Response from Dr. Ros Altmann 9 th September 2010 The Government has issued a consultation on its proposals to reform the Age 75 rules for mandatory annuity purchase from

Age 75 Annuities Consultation Response from Dr. Ros Altmann 9 th September 2010 The Government has issued a consultation on its proposals to reform the Age 75 rules for mandatory annuity purchase from

KEY GUIDE. Pensions freedom drawing from your pension

KEY GUIDE Pensions freedom drawing from your pension Radical reform The changes revealed in the 2014 Budget were described by some retirement planning experts as a pensions revolution. The radical proposals

KEY GUIDE Pensions freedom drawing from your pension Radical reform The changes revealed in the 2014 Budget were described by some retirement planning experts as a pensions revolution. The radical proposals

KEY GUIDE. Investing for income when you retire

KEY GUIDE Investing for income when you retire Planning the longest holiday of your life There comes a time when you stop working for your money and put your money to work for you. For most people, that

KEY GUIDE Investing for income when you retire Planning the longest holiday of your life There comes a time when you stop working for your money and put your money to work for you. For most people, that

How To Calculate A Life Insurance Premium

IMF Seminar on Ageing, Financial Risk Management and Financial Stability The views expressed in this paper are those of the author(s) only, and the presence of them, or of links to them, on the IMF website

IMF Seminar on Ageing, Financial Risk Management and Financial Stability The views expressed in this paper are those of the author(s) only, and the presence of them, or of links to them, on the IMF website

Planning a prosperous retirement

Planning a prosperous retirement Towry s Guide to Retirement Planning About Towry We are one of the UK s leading Wealth Advisers and specialise in providing high quality, expert financial advice to private

Planning a prosperous retirement Towry s Guide to Retirement Planning About Towry We are one of the UK s leading Wealth Advisers and specialise in providing high quality, expert financial advice to private

Investment Association response to the FCA s Retirement income market study: Interim Report

Investment Association response to the FCA s Retirement income market study: Interim Report 30 th January 2015 General comments 1. The Investment Association 1 is a long-standing supporter of greater flexibility

Investment Association response to the FCA s Retirement income market study: Interim Report 30 th January 2015 General comments 1. The Investment Association 1 is a long-standing supporter of greater flexibility

A Guide to RETIREMENT PLANNING

A Guide to RETIREMENT PLANNING PARTNERS IN MANAGING YOUR WEALTH Contents 3 Retirement planning guide 4 Retirement - the facts 5 How much will you need in retirement? 7 Investing for your retirement 8 What

A Guide to RETIREMENT PLANNING PARTNERS IN MANAGING YOUR WEALTH Contents 3 Retirement planning guide 4 Retirement - the facts 5 How much will you need in retirement? 7 Investing for your retirement 8 What

PENSIONS POLICY INSTITUTE. Tax relief for pension saving in the UK

Tax relief for pension saving in the UK This report is sponsored by Age UK, the Institute and Faculty of Actuaries, Partnership and the TUC. The PPI is grateful for the support of the following sponsors

Tax relief for pension saving in the UK This report is sponsored by Age UK, the Institute and Faculty of Actuaries, Partnership and the TUC. The PPI is grateful for the support of the following sponsors

How to achieve quality retirement outcomes for your members

How to achieve quality retirement outcomes for your members Speakers Andrew Pennie, Marketing Director, Intelligent Pensions Steve Patterson, Managing Director, Intelligent Pensions Chair John Moret, Chairman,

How to achieve quality retirement outcomes for your members Speakers Andrew Pennie, Marketing Director, Intelligent Pensions Steve Patterson, Managing Director, Intelligent Pensions Chair John Moret, Chairman,

NEST consultation response from Dr. Ros Altmann. Independent Pensions Policy Expert

6 January 2015 NEST consultation response from Dr. Ros Altmann. Independent Pensions Policy Expert 1. How will the trend for changing retirement patterns and provision affect a. What members need b. What

6 January 2015 NEST consultation response from Dr. Ros Altmann. Independent Pensions Policy Expert 1. How will the trend for changing retirement patterns and provision affect a. What members need b. What

Creating a Secondary Annuity Market: a response by the National Association of Pension Funds

Creating a Secondary Annuity Market: a response by the National Association of Pension Funds June 2015 www.napf.co.uk Creating a secondary annuity market: a response by the NAPF Contents Executive Summary

Creating a Secondary Annuity Market: a response by the National Association of Pension Funds June 2015 www.napf.co.uk Creating a secondary annuity market: a response by the NAPF Contents Executive Summary

Freedom and choice in pensions

Freedom and choice in pensions Response from NEST Overview The recent liberalisation of the rules on decumulation present us with a welcome opportunity to think about what our members need from their pension

Freedom and choice in pensions Response from NEST Overview The recent liberalisation of the rules on decumulation present us with a welcome opportunity to think about what our members need from their pension

The Money Charity is the UK s leading financial capability charity.

The Money Charity is the UK s leading financial capability charity. We believe that being on top of your money means you are more in control of your life, your finances and your debts, reducing stress

The Money Charity is the UK s leading financial capability charity. We believe that being on top of your money means you are more in control of your life, your finances and your debts, reducing stress

The Difference Between Providing A Pension And Retirement

Pensions made simple Take control of your future MIND THE GAP PENSIONS MADE SIMPLE FROM AVIVA Contents Page 1 First things first 2 2 Why pensions are so important 4 3 How a pension plan works 8 4 The tax

Pensions made simple Take control of your future MIND THE GAP PENSIONS MADE SIMPLE FROM AVIVA Contents Page 1 First things first 2 2 Why pensions are so important 4 3 How a pension plan works 8 4 The tax

PENSIONS POLICY INSTITUTE. Retirement income and assets: outlook for the future

Retirement income and assets: outlook for the future The PPI is grateful for the support of the following sponsors of this project: Sponsorship has been given to help fund the research, and does not necessarily

Retirement income and assets: outlook for the future The PPI is grateful for the support of the following sponsors of this project: Sponsorship has been given to help fund the research, and does not necessarily

How to... Help your clients use their pensions freedom wisely

How to... Help your clients use their pensions freedom wisely How To Guide Introduction The new pension freedoms that came into effect in April 2015, may, at first, seem like a very attractive prospect.

How to... Help your clients use their pensions freedom wisely How To Guide Introduction The new pension freedoms that came into effect in April 2015, may, at first, seem like a very attractive prospect.

KEY GUIDE. Investing for income at retirement

KEY GUIDE Investing for income at retirement Introduction The decisions you make at retirement could have repercussions for the rest of your life. That might be considerably longer than you think, as the

KEY GUIDE Investing for income at retirement Introduction The decisions you make at retirement could have repercussions for the rest of your life. That might be considerably longer than you think, as the

Guide to Annuity Purchase

Fiducia Wealth Management Limited Guide to Annuity Purchase September 2012 For Professional Advisers Only Fiducia Wealth Management Ltd. Dedham Hall Business Centre, Brook Street, Colchester, Essex, CO7

Fiducia Wealth Management Limited Guide to Annuity Purchase September 2012 For Professional Advisers Only Fiducia Wealth Management Ltd. Dedham Hall Business Centre, Brook Street, Colchester, Essex, CO7

Pension reforms in the UK: what can be learned from other countries?

Agenda Advancing economics in business Pension reforms in the UK: what can be learned from other countries? Reforms in the UK pensions market announced by the Chancellor of the Exchequer, George Osborne,

Agenda Advancing economics in business Pension reforms in the UK: what can be learned from other countries? Reforms in the UK pensions market announced by the Chancellor of the Exchequer, George Osborne,

PENSIONS POLICY INSTITUTE. Comparison of pension outcomes under EET and TEE tax treatment

Comparison of pension outcomes under EET and TEE tax treatment Comparison of pension outcomes under EET and TEE tax treatment Executive Summary 1 Introduction 4 1. Impact of tax treatment on a single

Comparison of pension outcomes under EET and TEE tax treatment Comparison of pension outcomes under EET and TEE tax treatment Executive Summary 1 Introduction 4 1. Impact of tax treatment on a single

A guide to the pension changes in April 2015

A guide to the pension changes in April 2015 106027837.indd 1 05/01/2015 10:00 Contents What do the changes mean for you? 3 Summary of the changes from 6 April 2015 5 What s changed in practice? 6 How

A guide to the pension changes in April 2015 106027837.indd 1 05/01/2015 10:00 Contents What do the changes mean for you? 3 Summary of the changes from 6 April 2015 5 What s changed in practice? 6 How

FCA Retirement income market study: Interim Report. A response by the National Association of Pension Funds. January 2015 www.napf.co.

FCA Retirement income market study: Interim Report A response by the National Association of Pension Funds January 2015 www.napf.co.uk NAPF response to FCA retirement income market study Contents Overview...

FCA Retirement income market study: Interim Report A response by the National Association of Pension Funds January 2015 www.napf.co.uk NAPF response to FCA retirement income market study Contents Overview...

KEY GUIDE. Investing for income when you retire

KEY GUIDE Investing for income when you retire Planning the longest holiday of your life There comes a time when you stop working for your money and put your money to work for you. For most people, that

KEY GUIDE Investing for income when you retire Planning the longest holiday of your life There comes a time when you stop working for your money and put your money to work for you. For most people, that

A BETTER RETIREMENT PORTFOLIO FOR MEMBERS IN DC INVESTMENT DEFAULTS

A BETTER RETIREMENT PORTFOLIO FOR MEMBERS IN DC INVESTMENT DEFAULTS JUNE 2014 TALENT HEALTH RETIREMENT INVESTMENTS EXECUTIVE SUMMARY The majority of defined contribution (DC) plan members typically end

A BETTER RETIREMENT PORTFOLIO FOR MEMBERS IN DC INVESTMENT DEFAULTS JUNE 2014 TALENT HEALTH RETIREMENT INVESTMENTS EXECUTIVE SUMMARY The majority of defined contribution (DC) plan members typically end

DISCUSSION PAPER PI-1302

DISCUSSION PAPER PI-1302 Good Practice Principles in Modelling Defined Contribution Pension Plans Kevin Dowd and David Blake September 2013 ISSN 1367-580X The Pensions Institute Cass Business School City

DISCUSSION PAPER PI-1302 Good Practice Principles in Modelling Defined Contribution Pension Plans Kevin Dowd and David Blake September 2013 ISSN 1367-580X The Pensions Institute Cass Business School City

Contents: What is an Annuity?

Contents: What is an Annuity? When might I need an annuity policy? Types of annuities Pension annuities Annuity income options Enhanced and Lifestyle annuities Impaired Life annuities Annuity rates FAQs

Contents: What is an Annuity? When might I need an annuity policy? Types of annuities Pension annuities Annuity income options Enhanced and Lifestyle annuities Impaired Life annuities Annuity rates FAQs

Post Budget At Retirement Market - A Report

Post Budget At Retirement Market - Qualitative Consumer Research Commissioned by syndicate members: This report is for media use only and may not be reproduced or circulated in its entirety. Any quotes

Post Budget At Retirement Market - Qualitative Consumer Research Commissioned by syndicate members: This report is for media use only and may not be reproduced or circulated in its entirety. Any quotes

The path to retirement success

The path to retirement success How important are your investment and spending strategies? In this VIEW, Towers Watson Australia managing director ANDREW BOAL reports on investing for retirement success

The path to retirement success How important are your investment and spending strategies? In this VIEW, Towers Watson Australia managing director ANDREW BOAL reports on investing for retirement success

How To Encourage People To Save

Beyond Tax Relief - a new savings incentive framework Dr. Ros Altmann Currently the UK has relatively high per capita retirement savings - higher than most of Europe. The development of a *strong pension

Beyond Tax Relief - a new savings incentive framework Dr. Ros Altmann Currently the UK has relatively high per capita retirement savings - higher than most of Europe. The development of a *strong pension

IMPLEMENTING THE RESTRICTION OF PENSIONS TAX RELIEF: NAPF SUBMISSION TO THE HMT/HMRC CONSULTATION

IMPLEMENTING THE RESTRICTION OF PENSIONS TAX RELIEF: NAPF SUBMISSION TO THE HMT/HMRC CONSULTATION Executive Summary The NAPF welcomes the Coalition Government s decision to adopt a tax regime based principally

IMPLEMENTING THE RESTRICTION OF PENSIONS TAX RELIEF: NAPF SUBMISSION TO THE HMT/HMRC CONSULTATION Executive Summary The NAPF welcomes the Coalition Government s decision to adopt a tax regime based principally

Financial Conduct Authority Retirement Income Market Data

Financial Conduct Authority Retirement Income Market Data July September 2015 Contents Introduction 1 1 Executive summary 2 2 Our sample 5 3 Consumer choices 6 4 Withdrawals 12 5 Use of regulated advisers

Financial Conduct Authority Retirement Income Market Data July September 2015 Contents Introduction 1 1 Executive summary 2 2 Our sample 5 3 Consumer choices 6 4 Withdrawals 12 5 Use of regulated advisers

Accessing your Additional Voluntary Contribution (AVC)

") Accessing your Additional Voluntary Contribution (AVC) Accessing your AVC savings Now is the time to start making decisions about your retirement and your future. One of the most important things to think

Accessing your Additional Voluntary Contribution (AVC) Accessing your AVC savings Now is the time to start making decisions about your retirement and your future. One of the most important things to think

Your retirement income. Exploring your options

Your retirement income Exploring your options Contents 02 What do you want to do with your pension fund? 07 A regular retirement income for the rest of your life 10 A flexible income from a Self Invested

Your retirement income Exploring your options Contents 02 What do you want to do with your pension fund? 07 A regular retirement income for the rest of your life 10 A flexible income from a Self Invested

A Guide to RETIREMENT PLANNING PARTNERS IN MANAGING YOUR WEALTH PARTNERS IN MANAGING 1 YOUR WEALTH

A Guide to RETIREMENT PLANNING PARTNERS IN MANAGING 1 YOUR WEALTH Contents Retirement planning guide 3 Retirement the facts 4 How much will you need in retirement? 5 Investing for your retirement 7 What

A Guide to RETIREMENT PLANNING PARTNERS IN MANAGING 1 YOUR WEALTH Contents Retirement planning guide 3 Retirement the facts 4 How much will you need in retirement? 5 Investing for your retirement 7 What

Changes announced in last year s Budget have removed some of the

The Australian Journal of Financial Planning 71 Reverse mortgages and pension planning By Benedict Davies Technical Services Manager, Over Fifty Group Changes announced in last year s Budget have removed

The Australian Journal of Financial Planning 71 Reverse mortgages and pension planning By Benedict Davies Technical Services Manager, Over Fifty Group Changes announced in last year s Budget have removed

With new options available from April 2015, we can help you plan your finances for a worry-free retirement

Your retirement With new options available from April 2015, we can help you plan your finances for a worry-free retirement Life is full of financial decisions and planning your retirement is one of the

Your retirement With new options available from April 2015, we can help you plan your finances for a worry-free retirement Life is full of financial decisions and planning your retirement is one of the

Key Features of investing in an Old Mutual Wealth Collective. via an Old Mutual International - International Portfolio Bond

Key Features of investing in an Old Mutual Wealth Collective Investment Account* via an Old Mutual International - International Portfolio Bond For UK Customers *Provided by Old Mutual Wealth Limited The

Key Features of investing in an Old Mutual Wealth Collective Investment Account* via an Old Mutual International - International Portfolio Bond For UK Customers *Provided by Old Mutual Wealth Limited The

Your Guide to Pension Freedom

Your Guide to Pension Freedom 3 From April 2015, individuals will have more freedom to access their pensions. These changes mark a radical departure from the existing system, by giving you greater choice

Your Guide to Pension Freedom 3 From April 2015, individuals will have more freedom to access their pensions. These changes mark a radical departure from the existing system, by giving you greater choice

Group Additional Voluntary Contributions Plan Key features

Group Additional Voluntary Contributions Plan Key features This is an important document. Please read it and keep for future reference. The Financial Conduct Authority is a financial services regulator.

Group Additional Voluntary Contributions Plan Key features This is an important document. Please read it and keep for future reference. The Financial Conduct Authority is a financial services regulator.

Pension Liability Risks: Manage or Sell?

Pension Liability Risks: Manage or Sell? David Blake Pensions Institute Cass Business School The views expressed in this paper are those of the author(s) only, and the presence of them, or of links to

Pension Liability Risks: Manage or Sell? David Blake Pensions Institute Cass Business School The views expressed in this paper are those of the author(s) only, and the presence of them, or of links to

The five-step plan to a better retirement. A step by step guide to organising your finances

The five-step plan to a better retirement A step by step guide to organising your finances This is one of the biggest financial decisions you ll make so it s important to get it right. At Fidelity we strongly

The five-step plan to a better retirement A step by step guide to organising your finances This is one of the biggest financial decisions you ll make so it s important to get it right. At Fidelity we strongly

8th Bowles Symposium and 2nd International Longevity Risk and Capital Market Solutions Symposium

8th Bowles Symposium and 2nd International Longevity Risk and Capital Market Solutions Symposium Annuitization lessons from the UK Money-Back annuities and other developments Tom Boardman UK Policy Development

8th Bowles Symposium and 2nd International Longevity Risk and Capital Market Solutions Symposium Annuitization lessons from the UK Money-Back annuities and other developments Tom Boardman UK Policy Development

Our guide to. buying an annuity

Our guide to buying an annuity 2 Our guide to buying an annuity Contents Introduction 3 Pension reforms Thinking about retirement 3 Money and budgeting How can we help? Your retirement timeline Key questions

Our guide to buying an annuity 2 Our guide to buying an annuity Contents Introduction 3 Pension reforms Thinking about retirement 3 Money and budgeting How can we help? Your retirement timeline Key questions

Freedom and choice in pensions: government response to the consultation

Freedom and choice in pensions: government response to the consultation Cm 8901 July 2014 Freedom and choice in pensions: government response to the consultation Presented to Parliament by the Chancellor

Freedom and choice in pensions: government response to the consultation Cm 8901 July 2014 Freedom and choice in pensions: government response to the consultation Presented to Parliament by the Chancellor

Annuities and decumulation phase of retirement. Chris Daykin UK Government Actuary Chairman, PBSS Section of IAA

Annuities and decumulation phase of retirement Chris Daykin UK Government Actuary Chairman, PBSS Section of IAA CASH LUMP SUM AT RETIREMENT CASH INSTEAD OF PENSION > popular with pension scheme members

Annuities and decumulation phase of retirement Chris Daykin UK Government Actuary Chairman, PBSS Section of IAA CASH LUMP SUM AT RETIREMENT CASH INSTEAD OF PENSION > popular with pension scheme members

Annuities - A Brief Guide

Verschoyle House 28/30 Lower Mount Street Dublin 2 Tel 01 613 1900 Fax 01 631 8602 Email info@pensionsboard.ie www.pensionsboard.ie The Pensions Board has prepared this booklet to help people understand

Verschoyle House 28/30 Lower Mount Street Dublin 2 Tel 01 613 1900 Fax 01 631 8602 Email info@pensionsboard.ie www.pensionsboard.ie The Pensions Board has prepared this booklet to help people understand

Current Issues April 2015

In this issue: Pension tax: a post-election change - whoever wins Further help to buy from the government A savings tax cut Selling your pension annuity Income tax changes Pension tax: a post-election

In this issue: Pension tax: a post-election change - whoever wins Further help to buy from the government A savings tax cut Selling your pension annuity Income tax changes Pension tax: a post-election

How To Understand The Economic And Social Costs Of Living In Australia

Australia s retirement provision: the decumulation challenge John Piggott Director CEPAR Outline of talk Introduction to Australian retirement policy Issues in Longevity Current retirement products in

Australia s retirement provision: the decumulation challenge John Piggott Director CEPAR Outline of talk Introduction to Australian retirement policy Issues in Longevity Current retirement products in

Retirement Account Plan Key features

Retirement Account Plan Key features This is an important document. Please read it and keep for future reference. The Financial Conduct Authority is a financial services regulator. It requires us, Standard

Retirement Account Plan Key features This is an important document. Please read it and keep for future reference. The Financial Conduct Authority is a financial services regulator. It requires us, Standard

ISAs GUIDE. An introduction to Individual Savings Accounts

ISAs GUIDE 2015 An introduction to Individual Savings Accounts ISAs GUIDE 2015 Introduction Most people s experience of saving starts in childhood. Your parents encourage you to save up a few pennies,

ISAs GUIDE 2015 An introduction to Individual Savings Accounts ISAs GUIDE 2015 Introduction Most people s experience of saving starts in childhood. Your parents encourage you to save up a few pennies,

M&G Guide to Retirement Income

M&G Guide to Retirement Income 2 Working out how to make adequate financial provision for retirement is one of the most important financial decisions most of us will ever face. However, it can be a daunting

M&G Guide to Retirement Income 2 Working out how to make adequate financial provision for retirement is one of the most important financial decisions most of us will ever face. However, it can be a daunting

Collective Retirement Account

Key features of the Collective Retirement Account The Financial Conduct Authority is a financial services regulator. It requires us, Old Mutual Wealth, to give you this important information to help you

Key features of the Collective Retirement Account The Financial Conduct Authority is a financial services regulator. It requires us, Old Mutual Wealth, to give you this important information to help you

Retirement Advantage response to HM Treasury - Strengthening the incentive to save: a consultation on pension tax relief

Retirement Advantage response to HM Treasury - Strengthening the incentive to save: a consultation on pension tax relief Overview and Executive Summary It is clear later life in the UK has changed dramatically

Retirement Advantage response to HM Treasury - Strengthening the incentive to save: a consultation on pension tax relief Overview and Executive Summary It is clear later life in the UK has changed dramatically

CREATE TAX ADVANTAGED RETIREMENT INCOME YOU CAN T OUTLIVE. create tax advantaged retirement income you can t outlive

create tax advantaged retirement income you can t outlive 1 Table Of Contents Insurance Companies Don t Just Sell Insurance... 4 Life Insurance Investing... 5 Guarantees... 7 Tax Strategy How to Get Tax-Free

create tax advantaged retirement income you can t outlive 1 Table Of Contents Insurance Companies Don t Just Sell Insurance... 4 Life Insurance Investing... 5 Guarantees... 7 Tax Strategy How to Get Tax-Free

Helping your loved ones. Simple steps to providing for your family and friends

Helping your loved ones Simple steps to providing for your family and friends Contents 01 How can I take control of who gets what? 02 Inheritance Tax 04 Do you know how much you re worth? 06 Making lifetime

Helping your loved ones Simple steps to providing for your family and friends Contents 01 How can I take control of who gets what? 02 Inheritance Tax 04 Do you know how much you re worth? 06 Making lifetime

It s flexible. Key features of the Flexible Income Annuity. Flexible Income Annuity

It s flexible Key features of the Flexible Income Annuity Flexible Income Annuity This is an important document and you should read it before deciding whether to buy your pension annuity from us Purpose

It s flexible Key features of the Flexible Income Annuity Flexible Income Annuity This is an important document and you should read it before deciding whether to buy your pension annuity from us Purpose

BAE SYSTEMS PENSIONS BECAUSE PLANNING IS PART OF THE JOURNEY RETIREMENT ACCOUNT GUIDE LEVEL 100+ MARCH 2015

BAE SYSTEMS PENSIONS BECAUSE PLANNING IS PART OF THE JOURNEY RETIREMENT ACCOUNT GUIDE LEVEL 100+ MARCH 2015 CONTENTS Where your Scheme benefits come from 4 Your choices affect your retirement account 5

BAE SYSTEMS PENSIONS BECAUSE PLANNING IS PART OF THE JOURNEY RETIREMENT ACCOUNT GUIDE LEVEL 100+ MARCH 2015 CONTENTS Where your Scheme benefits come from 4 Your choices affect your retirement account 5

How To Take A Pension From A Pension Fund

UPDATED: 6 April 2015 NEW pension freedoms Your options at retirement How to take tax-free lump sums and income, under new pension freedoms One College Square South, Anchor Road, Bristol, BS1 5HL www.hl.co.uk

UPDATED: 6 April 2015 NEW pension freedoms Your options at retirement How to take tax-free lump sums and income, under new pension freedoms One College Square South, Anchor Road, Bristol, BS1 5HL www.hl.co.uk

Pension Annuities: A review of consumer behaviour. Report prepared for the Financial Conduct Authority

Pension Annuities: A review of consumer behaviour Report prepared for the Financial Conduct Authority Jackie Wells January 2014 Pension Annuities: A review of consumer behaviour Report prepared for the

Pension Annuities: A review of consumer behaviour Report prepared for the Financial Conduct Authority Jackie Wells January 2014 Pension Annuities: A review of consumer behaviour Report prepared for the

DISCUSSION PAPER PI-1305

DISCUSSION PAPER PI-1305 Longevity Insurance Annuities: Lessons from the United Kingdom David Blake and John A. Turner July 2013 ISSN 1367-580X The Pensions Institute Cass Business School City University

DISCUSSION PAPER PI-1305 Longevity Insurance Annuities: Lessons from the United Kingdom David Blake and John A. Turner July 2013 ISSN 1367-580X The Pensions Institute Cass Business School City University

Nurturing your investment

helping life flow smoothly UNITED UTILITIES PENSION SCHEME Investment choices Nurturing your investment Contents Investment choices 1. A BRIEF GUIDE TO INVESTMENTS A reminder of the main different types

helping life flow smoothly UNITED UTILITIES PENSION SCHEME Investment choices Nurturing your investment Contents Investment choices 1. A BRIEF GUIDE TO INVESTMENTS A reminder of the main different types

Annuities Guide. Simply Retirement make it easy for you to find the best deal in retirement. Simply Retirement Ltd who are we? Who is this guide for?

Simply Retirement make it easy for you to find the best deal in retirement Jan Leeming Annuities Guide Simply Retirement Ltd who are we? Thank you for requesting this annuity guide. I would just like to

Simply Retirement make it easy for you to find the best deal in retirement Jan Leeming Annuities Guide Simply Retirement Ltd who are we? Thank you for requesting this annuity guide. I would just like to

KEY GUIDE. Pensions and tax planning for high earners

KEY GUIDE Pensions and tax planning for high earners The rising tax burden on income If you find more and more of your income is taxed at over the basic rate, you are not alone. The point at which you

KEY GUIDE Pensions and tax planning for high earners The rising tax burden on income If you find more and more of your income is taxed at over the basic rate, you are not alone. The point at which you

Key Features of the Local Government Additional Voluntary Contributions (AVC) Scheme for England & Wales

Scheme for England & Wales") Key Features of the Local Government Additional Voluntary Contributions (AVC) Scheme for England & Wales Important information you need to read The Financial Conduct Authority is an independent financial

Key Features of the Local Government Additional Voluntary Contributions (AVC) Scheme for England & Wales Important information you need to read The Financial Conduct Authority is an independent financial

Important information. Key Features of the Teachers Additional Voluntary Contributions (AVC) Scheme

Scheme") Important information Key Features of the Teachers Additional Voluntary Contributions (AVC) Scheme > Contents About this booklet 4 About the Teachers AVC Scheme 5 Its aim 5 Your commitment 5 Risks 6 Questions

Important information Key Features of the Teachers Additional Voluntary Contributions (AVC) Scheme > Contents About this booklet 4 About the Teachers AVC Scheme 5 Its aim 5 Your commitment 5 Risks 6 Questions

Your pension: it s time to choose

Your pension: it s time to choose Thinking about retiring Deciding how to take your retirement income Shopping around for the best income The Money Advice Service is independent and set up by government

Your pension: it s time to choose Thinking about retiring Deciding how to take your retirement income Shopping around for the best income The Money Advice Service is independent and set up by government

Freedom and Choice in Pensions. Your guide to the changes

Freedom and Choice in Pensions Your guide to the changes Contents Freedom and Choice 3-5 in Pensions Buy an annuity 6-7 Remain invested - 8-9 entering drawdown Take a cash lump sum 10 Will providers offer

Freedom and Choice in Pensions Your guide to the changes Contents Freedom and Choice 3-5 in Pensions Buy an annuity 6-7 Remain invested - 8-9 entering drawdown Take a cash lump sum 10 Will providers offer

Basic Guide to Retirement Income Options

Basic Guide to Retirement Income Options Can I afford to retire? Which retirement income solution is best for me? Should I take all my tax-free cash entitlement? Will my family benefit from my pension

Basic Guide to Retirement Income Options Can I afford to retire? Which retirement income solution is best for me? Should I take all my tax-free cash entitlement? Will my family benefit from my pension

The Partnership Enhanced Retirement Account

For financial advisers only not for retail clients The Partnership Enhanced Retirement Account ADVISER GUIDE 2 ENHANCED RETIREMENT ACCOUNT Contents Introduction 3 The ERA an all-in-one solution 4 Benefits

For financial advisers only not for retail clients The Partnership Enhanced Retirement Account ADVISER GUIDE 2 ENHANCED RETIREMENT ACCOUNT Contents Introduction 3 The ERA an all-in-one solution 4 Benefits

Older savers report: the impact on older people of savings accounts where interest rates have dropped from their initial rate to negligible amounts

All Party Parliamentary Group for Ageing and Older People Older savers report: the impact on older people of savings accounts where interest rates have dropped from their initial rate to negligible amounts

All Party Parliamentary Group for Ageing and Older People Older savers report: the impact on older people of savings accounts where interest rates have dropped from their initial rate to negligible amounts

Key Features of the Prudential Personal Pension Scheme

Key Features of the Prudential Personal Pension Scheme Important information you need to read The Financial Conduct Authority is the independent financial services regulator. It requires us, Prudential,

Key Features of the Prudential Personal Pension Scheme Important information you need to read The Financial Conduct Authority is the independent financial services regulator. It requires us, Prudential,

TAKING CONTROL OF YOUR PENSION PLAN. The value of pension contributions

TAKING CONTROL OF YOUR PENSION PLAN If you add together all the money you have in pension arrangements, the total may well dwarf every other investment you ever make. Despite this, many people are happy

TAKING CONTROL OF YOUR PENSION PLAN If you add together all the money you have in pension arrangements, the total may well dwarf every other investment you ever make. Despite this, many people are happy

FSA Retail Conduct Risk Outlook 2012

March 2012 FSA Retail Conduct Risk Outlook 2012 Summary The FSA has published its Retail Conduct Risk Outlook (RCRO) for 2012. The RCRO sets out the FSA s assessment of the 15 most significant retail conduct

March 2012 FSA Retail Conduct Risk Outlook 2012 Summary The FSA has published its Retail Conduct Risk Outlook (RCRO) for 2012. The RCRO sets out the FSA s assessment of the 15 most significant retail conduct

Making the right pension transfer decision

Making the right pension transfer decision Clearing away confusion between QROPS, SIPPs, and QNUPS Over 30 years experience providing independent pension advice to expatriates and people working abroad

Making the right pension transfer decision Clearing away confusion between QROPS, SIPPs, and QNUPS Over 30 years experience providing independent pension advice to expatriates and people working abroad

Certificate for Introduction to Securities & Investment (Cert.ISI) Unit 1

Unit 1") 14cis Certificate for Introduction to Securities & Investment (Cert.ISI) Unit 1 Lesson 14: Pension funds Insurance companies Who buys government bonds? Government bonds are bought in large quantities by

14cis Certificate for Introduction to Securities & Investment (Cert.ISI) Unit 1 Lesson 14: Pension funds Insurance companies Who buys government bonds? Government bonds are bought in large quantities by

secure your future the lump sum scheme Everything you need to know about your super DIVISION 2 - MEMBERS BOOKLET DIVISION 2 - MEMBERS BOOKLET

the lump sum scheme secure your future Everything you need to know about your super DIVISION 2 - MEMBERS BOOKLET 1 Adding power to your financial future 3 THE LUMP sum scheme MADE EASY 4 CONTRIBUTIONS

the lump sum scheme secure your future Everything you need to know about your super DIVISION 2 - MEMBERS BOOKLET 1 Adding power to your financial future 3 THE LUMP sum scheme MADE EASY 4 CONTRIBUTIONS

Population Ageing and the Role of the State. Affording Our Future Conference 10-11 December, 2012

Population Ageing and the Role of the State Affording Our Future Conference 10-11 December, 2012 Entitlement Reform Old and Broke: 1 Old International comparisons of demographic changes present challenges.

Population Ageing and the Role of the State Affording Our Future Conference 10-11 December, 2012 Entitlement Reform Old and Broke: 1 Old International comparisons of demographic changes present challenges.

Is equity release the right choice for you? Protecting yourself If it isn t right for you, what are the alternatives?

Buyer s Guide : Content Page 1: What is equity release? Page 2: Is equity release the right choice for you? Page 3: Protecting yourself If it isn t right for you, what are the alternatives? Page 4: Lifetime

Buyer s Guide : Content Page 1: What is equity release? Page 2: Is equity release the right choice for you? Page 3: Protecting yourself If it isn t right for you, what are the alternatives? Page 4: Lifetime

PLANNING THE RETIREMENT YOU WANT

PLANNING THE RETIREMENT YOU WANT Charlotte Supply Chain Graduate HEINEKEN UK Flexible Retirement Plan Contents A reminder of... How the Flexible Retirement Plan works 4 The benefits 6 Consider what you

PLANNING THE RETIREMENT YOU WANT Charlotte Supply Chain Graduate HEINEKEN UK Flexible Retirement Plan Contents A reminder of... How the Flexible Retirement Plan works 4 The benefits 6 Consider what you

How To Pay Out Of Pocket

Longevity risk and life annuity challenges around the world Professor David Blake d.blake@city.ac.uk www.pensions-institute.org Santiago, Chile March 2013 1 Agenda Longevity and other retirement risks

Longevity risk and life annuity challenges around the world Professor David Blake d.blake@city.ac.uk www.pensions-institute.org Santiago, Chile March 2013 1 Agenda Longevity and other retirement risks

DECEMBER 2014 AUTUMN STATEMENT

DECEMBER 2014 AUTUMN STATEMENT SUMMARY The key announcements by The Chancellor providing opportunities for financial planning advice are outlined below. PENSIONS Summary of all the pension changes to apply

DECEMBER 2014 AUTUMN STATEMENT SUMMARY The key announcements by The Chancellor providing opportunities for financial planning advice are outlined below. PENSIONS Summary of all the pension changes to apply

The Oracle My Pension Plan. Giving you the power to choose

The Oracle My Pension Plan A Flexible Retirement Plan from Standard Life Giving you the power to choose Contents 03 Welcome 04 Benefits to you 06 Why should you join? 08 The state won t keep you warm 10

The Oracle My Pension Plan A Flexible Retirement Plan from Standard Life Giving you the power to choose Contents 03 Welcome 04 Benefits to you 06 Why should you join? 08 The state won t keep you warm 10

Your essential guide to equity release. from the UK s No. 1 specialist

Your essential guide to equity release from the UK s No. 1 specialist What is equity release? 03 03 04 05 06 07 08 09 10 15 Contents What is equity release? How could equity release help you? Why choose

Your essential guide to equity release from the UK s No. 1 specialist What is equity release? 03 03 04 05 06 07 08 09 10 15 Contents What is equity release? How could equity release help you? Why choose

Make the most of your retirement. Retire with Friends. It s good to talk to Friends

Make the most of your retirement Retire with Friends It s good to talk to Friends You can count on Friends Retirement today looks a lot different than it did for previous generations. It s good news. There

Make the most of your retirement Retire with Friends It s good to talk to Friends You can count on Friends Retirement today looks a lot different than it did for previous generations. It s good news. There

Can DC members afford to ignore inflation?

May 2013 Can DC members afford to ignore inflation? Mark Humphreys, Head of UK Strategic Solutions, Schroders Introduction Around 95% of individuals are forgoing inflation protection for their retirement

May 2013 Can DC members afford to ignore inflation? Mark Humphreys, Head of UK Strategic Solutions, Schroders Introduction Around 95% of individuals are forgoing inflation protection for their retirement

Pension Reforms. Key points: By Nigel Aston UK Head of Defined Contribution

Pension Reforms Herald New Era By Nigel Aston UK Head of Defined Contribution Key points: Rather than most people having to secure a pension income by purchasing an annuity, people retiring from April

Pension Reforms Herald New Era By Nigel Aston UK Head of Defined Contribution Key points: Rather than most people having to secure a pension income by purchasing an annuity, people retiring from April

PPI PRESS RELEASE FOR IMMEDIATE RELEASE

Tax relief offers important advantages to pension savers, but does little to encourage pension saving, particularly among low and medium earners says Pensions Policy Institute The Pensions Policy Institute

Tax relief offers important advantages to pension savers, but does little to encourage pension saving, particularly among low and medium earners says Pensions Policy Institute The Pensions Policy Institute

Strengthening the incentive to save: a consultation on pensions tax relief. Response to the consultation document published on 8 July 2015

Strengthening the incentive to save: a consultation on pensions tax relief Response to the consultation document published on 8 July 2015 Grant Thornton UK LLP (Grant Thornton) has considered the proposals

Strengthening the incentive to save: a consultation on pensions tax relief Response to the consultation document published on 8 July 2015 Grant Thornton UK LLP (Grant Thornton) has considered the proposals

Your essential guide to equity release. from the UK s No. 1 specialist

Your essential guide to equity release from the UK s No. 1 specialist 03 03 04 05 06 07 08 09 10 15 Contents What is equity release? How could equity release help you? Why choose Key Retirement? Mr & Mrs

Your essential guide to equity release from the UK s No. 1 specialist 03 03 04 05 06 07 08 09 10 15 Contents What is equity release? How could equity release help you? Why choose Key Retirement? Mr & Mrs

Standard Life Active Retirement For accessing your pension money

Standard Life Active Retirement For accessing your pension money Standard Life Active Retirement our ready-made investment solution that allows you to access your pension savings while still giving your

Standard Life Active Retirement For accessing your pension money Standard Life Active Retirement our ready-made investment solution that allows you to access your pension savings while still giving your

Spotlight. Defined benefit (DB) pensions and the new pension flexibilities. Have I got a defined benefit pension?

pensions and the new pension flexibilities. Have I got a defined benefit pension?") This factsheet outlines how defined benefit (DB) pensions are affected by the new pension flexibilities. The Pensions Advisory Service is unable to give individual specific advice and you should seek alternative

This factsheet outlines how defined benefit (DB) pensions are affected by the new pension flexibilities. The Pensions Advisory Service is unable to give individual specific advice and you should seek alternative

Let s talk pension flexibility The current position

Let s talk pension flexibility The current position 1 Let s talk pension flexibility the current position Change is coming. Budget 2014 heralded a shake-up of the pension system that will change how we

Let s talk pension flexibility The current position 1 Let s talk pension flexibility the current position Change is coming. Budget 2014 heralded a shake-up of the pension system that will change how we

In this issue: employee benefits wealth management pensions life assurance mortgages healthcare. Summer 2015

independent financial advice everyone can follow... Summer 2015 employee benefits wealth management pensions life assurance mortgages healthcare In this issue: Pensions freedom: what s in store? The investment