Credit Repair Tool Box

|

|

|

- Aileen Davidson

- 8 years ago

- Views:

Transcription

1 Credit Repair Tool Box There s no such thing as a HOPEless credit situation. We know that bad credit happens to good people all the time. The good news is that we ve been there before and we can help you through it now! By HOPE Credit Experts Ron Lambright and Michelle Black

2 By: Ron Lambright Executive Director HOPE (Home Ownership Program for Everyone) And Michelle Black Junior Executive Director HOPE (Home Ownership Program for Everyone)

3 All Rights Reserved by HOPE USA, Inc. All rights reserved. No part of this publication may be reproduced, distributed, or transmitted in any form or by any means, including photocopying, recording, or other electronic or mechanical methods, without the prior written permission of the publisher, except in the case of brief quotations embodied in critical reviews and certain other noncommercial uses permitted by author. For permission requests, write to the publisher at the address below. HOPE USA, Inc Centre Circle, Suite 101 Fort Mill, SC 29715

4 Important Information About This Book Introduction Credit scores impact every single aspect of your life. If you try to purchase a home, purchase a vehicle, get a new insurance policy, apply for a credit card, activate new utilities, rent an apartment, turn on new mobile phone service, or even apply for a job, someone will look at your credit report in order to decide whether or not you can get the things you need. This book is a great tool to help you take some initial steps toward a healthier credit report. However, please be aware, this book alone is not designed to be a substitute for professional advice and assistance. The HOPE Credit Repair Tool Box will provide you with extremely valuable information from experienced HOPE Credit Experts, Ron Lambright and Michelle Black. You will learn insider secrets that many credit professionals do not even know. This book is your first step towards the healthy credit you deserve! Important Reminder: You may become confused or overwhelmed during the reading of this book. In fact, that is to be expected. It takes many years of study and experience to properly master the intricacies of credit scoring and credit improvement tactics. However, you are not alone! Please reach out to our caring HOPE team if you have any questions. We are happy to share our knowledge and expertise with you! info@hope4usa.com Courtesy of HOPE Page 4

5 What Is a Credit Score? Time for a Quick History Lesson... Years ago, individual banks would make individual decisions regarding whether or not they would loan money to an individual person. A bank loan officer would meet with a potential customer and take an application viewing a credit report and asking questions to help to loan officer determine whether or not the person sitting in front of him was likely to pay back a loan plus interest and make the bank a profit. However, this system was flawed and prone to errors. In 1956, engineer Bill Fair and mathematician Earl Isaac founded a company named FICO. The idea behind FICO was that data could be used to improve business decisions. In 1958, FICO built the first credit scoring system for American Investments. For the next 30 years, FICO slowly began to be used in banks, department stores, credit card companies, and other companies whose business relied upon making decisions regarding whether or not to offer credit to a customer. Equifax was the first credit bureau to begin using the FICO score, and they introduced the BEACON Score (Equifax s version of the FICO score) in Just 2 short years later, FICO credit bureau risk scores were made available at all 3 major credit reporting agencies in the United States Equifax, Trans Union, and Experian. Trans Union debuted the EMPIRICA score and Experian debuted the Experian/FICO score. Now, with FICO scores being used by all 3 credit reporting agencies, a loan officer no longer has to make an individual decision on every loan. In fact, in almost all cases, loan officers are no longer ALLOWED to make individual credit decisions, but they must now base their decisions primarily upon an individual s credit scores. In short, if a consumer applies for a loan and the credit score is lower than the minimum score accepted by the lender, the loan officer has no choice but to turn the consumer down. The individual is reduced to a number. If the number is high enough, the lender will extend credit. If the number is too low, the lender will decline the application. The individual is reduced to a number. If the number is high enough, the lender will extend credit. If the number is too low, the lender will decline the application. Courtesy of HOPE Page 5

6 The Credit Bureaus and the Ugly Truth What do the credit bureaus do? When it comes to credit, the things that you do not know or understand can hurt you tremendously. The credit bureaus are not a government agency and they do not exist to help consumers. The credit bureaus are in business for one purpose and one purpose alone to make money! So, the question becomes, who are the credit bureaus and what exactly do the credit bureaus do? The bureaus (also known as the credit reporting agencies) are mega, billion dollar companies who will control and exert influence over you for your entire adult life. They will compile data and information regarding your spending habits, your ability to make loan payments in a timely fashion, how often you apply for credit, whether or not you borrow money and don t pay it back, etc. Then, with the help of FICO, each bureau will assign you a number. This little 3 digit number, also known as a credit score, will tell future lenders whether or not you are a good credit risk whether or not you should receive a loan. Your credit scores are like a report card for future lenders to read. If you have a history of paying your bills on time (among other things) you get an A. If you have a history of not paying your bills on time (among other things) you get an F. The bureaus hold power over you every single time you try to purchase a home, a car, when you apply for a credit card, when you shop for car insurance, even when you apply for a job. Now comes the scary part. We ve covered who the credit bureaus are and what they do (collect data). The ugly truth is that the credit bureaus do not want you to have a high credit score! Let me repeat THE CREDIT BUREAUS DO NOT WANT YOU TO HAVE A HIGH CREDIT SCORE! You may ask why the credit bureaus want you to have a low to fair credit score. Well, get ready for the answer. It is because the bureaus make MONEY, and a truckload of it, off people with low to fair credit scores. The credit bureaus do not want you to have a high credit score! Courtesy of HOPE Page 6

are mega, billion dollar companies who will control and exert influence over you for your entire adult life.")

7 The Credit Bureaus and the Ugly Truth How the Credit Bureaus Make Money. Check out the following list of some of the ways the bureaus make money off you and your information: Selling your credit report to lenders. Selling your credit report to you (the consumer). Selling credit report monitoring services to you (the consumer). Selling identity theft protection services to you (the consumer). Selling your information to companies for marketing purposes. (Think of all the credit card offers you receive in the mail.) Charging creditors and collection agencies when a consumer disputes inaccurate information on his/her credit report. Charging consumers to place a freeze on their credit file to protect it from fraud. -Etc., etc., etc. As you can plainly see, the bureaus are in the business of selling information. We will show you, on the next page, an example of how the credit bureaus make massive profits off individuals with low to fair credit ratings. The credit bureaus do not want you to have a high credit score! Courtesy of HOPE Page 7

Charging creditors and collection agencies when a consumer disputes inaccurate information on his/her credit report.")

8 The Credit Bureaus and the Ugly Truth How the Credit Bureaus Make Money. Let me show you an example of how the credit bureaus make massive profits off individuals with low to fair credit ratings. Joe Consumer goes to his local bank to apply for a car loan. The loan officer meets with Joe, takes his application, and pulls Joe s credit report. (The bank pays $$$ to access Joe s information.) Joe, who recently faced an illness and was out of work, has some negative items on his credit report. The loan officer turns Joe down but tells Joe if he can boost his credit score just 45 points he can qualify. Joe goes online and pulls a copy of his credit report. (He pays the credit bureaus $$$ to access his own information.) Joe is upset when he discovers inaccurate information on his credit report and even some identity fraud! He joins a monthly monitoring program (for which he pays $$$) and signs up for identity theft protection (for which he pays $$$). Joe then works with a professional credit restoration service to dispute the inaccurate items on his credit report. (Each time an account is disputed the creditor or collection agency has to pay the bureaus $$$ for researching the accuracy of the account.) Once Joe s credit has been restored he goes back to the bank to reapply for his car loan. (The bank pays $$$ again to access Joe s information.) Now, look at what happens when Henry Highscore applies for his loan. Henry goes to his local bank to apply for a car loan. The loan officer meets with Henry, takes his application, and pulls Henry s credit report. (The bank pays $$$ to access Henry s information.) Henry has a great credit score and is approved on the spot. Joe Consumer (Mid Range Credit Scores) Credit Bureaus Made Money 6 Times Estimated Income for Bureaus In Example: $390 Henry Highscore (High Range Credit Scores) Credit Bureaus Made Money 1 Time Estimated Income for Bureaus in Example: $15 Joe Consumer is 26 time more profitable to the credit bureaus than Henry Highscore! Do you see the difference? Consumers with a low to fair credit score are cash cows for the credit bureaus! Why in the world would the bureaus be motivated to help these consumers learn how to achieve and maintain high credit scores? A consumer with a low to mid range credit score can be about 26 times more profitable to the credit bureaus than a consumer with a high credit score! Courtesy of HOPE Page 8

9 Credit Scoring Models Not All Credit Scores Are Equal. There are hundreds of different credit scoring models. Most of the commonly used models come from a company named Fair Isaac. This company does statistical calculations of risk and summarizes it in a numerical value, i.e. credit score. Basically, Fair Isaac creates scoring models which gauge a consumer s risk. To be more specific, their calculations are designed to gauge a consumer s risk of going 90 days late on an account in the next 2 years. Fair Isaac then sells their scoring models to the credit bureaus Equifax, Trans Union, and Experian. Fair Isaac also sells hundreds of other specialized scoring models to other industries. There are Mortgage Industry and Auto Industry Option scoring models, credit card models, banking industry models, global models, and hundreds more. Many industries want their own specific models. So how do these different scores affect you? If on the exact same day you pulled a credit report online yourself, a mortgage company pulled your credit report, and an automobile company pulled your credit report, all 3 reports would have different credit scores. Here is another example, the Auto Industry Option scoring model rates 6 specific auto history accounts types heavier than all other accounts. These variables are known by Fair Isaac as scorecards. Therefore, if you have had repossession or a late payment on a car loan, this will have a much greater effect on the Auto Industry scoring option than it would on a Mortgage Industry score or a score you can pull for yourself. Credit card models will rate credit card late payments heavier than other models will. Each industry specific model will be impacted more if accounts are paid late or defaulted on within that specific industry. To confuse matters even further, there are also different versions of credit scoring models like Classic FICO and FICO 08. (Think of these different versions of credit scoring models like you would think of different versions of your computer software.) The credit bureaus even have their own score named Vantage Score. All together, hundreds of different credit scoring models are used to determine a consumer s credit worthiness in other words, the risk of lending money to that specific consumer. All together, hundreds of different credit scoring models are used to determine a consumer s credit worthiness in other words, the risk of lending money to that specific consumer. Courtesy of HOPE Page 9

10 The Anatomy of a Credit Score Payment History 35% Your payment history is the most important factor considered in your credit score, as you might expect. In total, your payment history accounts for 35% of your total score. This aspect of your total score calculation is based on your prior payment history with your creditors. Late payments, defaulted accounts, bankruptcies, and all other NEGATIVE information on your credit report have the greatest effect. Late Payments Late payments damage your credit scores more quickly than any other activity on your credit report. The more recent the late payment, the greater the damage will be to your credit score. If you pay your mortgage late this month, the Mortgage Industry Option scoring model could drop your scores over 120 points. That potential 120 point drop can occur with only a single 30 day late payment! REMEMBER, the scoring model is designed to predict the potential for you to become 90 days late on an account within the next 2 years. ANY recent late payments are a BIG reflection that you will default, and your credit score plummets as a result. Your creditor cannot report you late unless you are 30 days late. HOWEVER, the creditor can claim they need 10 days to process your payment. So, don t think just because you mailed your payment on the 25 th day that you will not be reported to the credit bureaus as late. All together, your entire history of payment counts for 35% of your total scores. The more positive accounts you have and the less negative means a MUCH higher credit score. Late payments damage your credit scores more quickly than any other activity on your credit report. Courtesy of HOPE Page 10

11 The Anatomy of a Credit Score Debt Level 30% The second largest factor considered in calculating your credit scores is the amount you owe in relation to your high credit limits aka your utilization ratio. If you are carrying high credit card balances, you can actually hurt your credit scores almost as much as if you were paying the account late every month. The Debt Level aspect of your credit score is made up of several different factors. The first factor is the relation of balances you owe on all of your accounts combined in relation to the high credit limits on those accounts. Factor number 2 takes into account balances in relation to high credit limits on your individual accounts also. For example, you will be scored higher if you owe 30% or less on your credit card accounts. This means if you have a high credit limit of $1,000 you will have a higher score if you maintain a balance of $300 or less. In fact, it is best to keep your credit cards at a 1% balance (or at a $0 balance if 1% is too difficult to maintain.) High balances on installment loans, car loans, mortgages, and other non revolving accounts can also negatively impact your credit scores. In fact, your credit scores will ALWAYS be immediately lowered if you open new accounts from the aforementioned categories. A new car loan, for example, will lower your scores as soon as it appears on your report. As your loans and mortgages are paid down over time, your scores will steadily increase. This is why one of the BEST things you can do for your credit is open accounts, and pay them as agreed. Your score will be affected by how many open accounts have balances, how much of your total credit lines are being used, and how much of a balance you have on installment loans, like car loans. You can directly improve your credit scores by maintaining lower balances on your accounts and sometimes by spreading balances over several different accounts. If you are carrying high credit card balances, you can actually hurt your credit scores almost as much as if you were paying the account late every month. Courtesy of HOPE Page 11

12 The Anatomy of a Credit Score Length of Credit 15% The age of your credit report accounts for 15% of your credit score. The older you are and the longer the period of time during which you have had credit accounts, the higher your score can become. The Length of Credit component in the calculation of your credit score is why it is near impossible to get to an 800 score at a young age. As you establish more credit accounts throughout your life, and as your credit history grows over time, your scores will naturally increase. Being added as an authorized user to an account with a long pay history is another pay to increase your scores. HOWEVER, exercise this strategy with extreme caution. You should never, ever, ever pay to be added as an authorized user to a stranger s account. Paying to be added to a strangers account is frowned upon and becomes downright illegal if you use a falsely elevated score (as a result of this illegal piggybacking tactic) to receive a loan. As our client we show you a little more about how to obtain legal and legitimate authorized user status with someone you know. The older you are and the longer the period of time during which you have had credit accounts, the higher your credit score can become. Courtesy of HOPE Page 12

13 The Anatomy of a Credit Score Inquiries 10% This Inquiry component of your credit score is comprised of how much new credit for which you apply. This category takes into consideration how many accounts you currently have open, how long it has been since you opened a new account, and how many requests you have for new credit within a 12 month time period. Whenever you apply for credit, the creditor requests information from the credit bureaus. This information request counts as an inquiry on your report. If you have a lot of inquiries in a short period of time, your scores will be impacted negatively. There is no exact number of points deducted from your score when an inquiry occurs. However, here is a hypothetical example: if you apply for a mortgage today, your scores might drop 1 point. Then, if you apply for a car, a mortgage, and a few credit cards this week, your scores could drop significantly. A large number of credit pulls in a short period of time will have a negative impact on your scores. You do not want to apply for too much new credit in a short period of time. Note: A consumer can pull his or her OWN credit report as often as he/she likes. These are considered soft inquiries and do not damage your credit scores in any way, shape, or form. You are entitled to a free credit report every year from (This free report does NOT include your credit scores.) If you would like to see your credit scores you may want to check out or other similar sites. Note: A consumer can pull his or her OWN credit report as often as he/she likes. These are considered soft inquiries and do not damage your credit scores in any way, shape, or form. Courtesy of HOPE Page 13

14 The Anatomy of a Credit Score Mix of Credit 10% Your credit scores also consider the mix of credit items you have on your report. The Mix of Credit component of your credit score is affected by what kinds of accounts you have and how many accounts you have from each of these individual categories. FICO will award you a higher credit score if you have an open mortgage, 3 credit cards, 1 auto loan, and a small amount of other open accounts than if you have little or no diversity on your credit report. If you have a ton of credit cards, your scores may be lowered. If you have several mortgages, your scores may be lowered. Any, unhealthy account mixes lower your scores. The preferred number of credit cards is 3. This means you will actually have a higher credit score if you have 3 open credit cards than if you have more or less than 3 open. HOWEVER, don t run out and cancel your cards just yet. REMEMBER, 30% of your score is comprised of your balances in relation to your high credit limit. So keep your cards open, but focus on having 3 LARGE balance cards for maximum impact. Maintain a healthy mix of accounts and this aspect of your credit score will be golden. Tip: Avoid finance company loans. Finance companies are the lenders of last resort. The terms and rates on these loans are not as favorable as traditional bank loans. Therefore, having finance company accounts on your credit report could likely cost you points in this category. Tip: Avoid finance company loans. Finance companies are the lenders of last resort Therefore, having finance company loans on your credit report could likely cost you points in this category. Courtesy of HOPE Page 14

15 How Can HOPE Help Me? Signs You Could Benefit from a HOPE Membership: *You want to be a homeowner. *You have made mistakes in the past, but want to get your credit back on track. *You are sick of being turned down for loans. *You have faced a hardship or circumstances that were out of your control and you have a damaged credit report as a result. *You desire professional guidance to help you rebuild your credit. *You have tried to fix credit problems on your own in the past, but have failed. *You are tired of getting ripped off by paying high interest rates. *You are tired of fighting the credit bureaus alone. The TRUTH About People with Bad Credit... We know that having bad credit can be embarrassing. It can make you feel like a loser or less than. The truth is that bad credit does NOT have anything to do with your value as a person. When difficult circumstances arise (i.e. job loss, accident, divorce, illness, death of a loved one, etc.), good people are forced to make touch financial decisions. So you decide that it is more important to feed your family than to pay a car payment. Protecting your family is the natural and honorable thing to do! In fact, don t you think that most collection agents would do the very same thing in a similar circumstance?! What you must remember is that bad credit happens to good people all the time! The good news is that you don t have to stand up to the credit bullies in your life alone! Yes, you absolutely have the right to try to correct credit problems all by yourself. You also have the right to represent yourself in a court of law or to pull your own teeth. Fixing credit problems can truly be as difficult as pulling teeth just ask anyone who has ever tried it before! Remember, just because you have the right to do something yourself does not mean that doing so is the right decision. HOPE has the experience, the knowledge, and the program to help you! You don t have to spend another day in credit prison, trying to overcome past credit mistakes and errors on your own. Call today to learn more about how HOPE can help you! Bad credit happens to good people all the time! Courtesy of HOPE Page 15

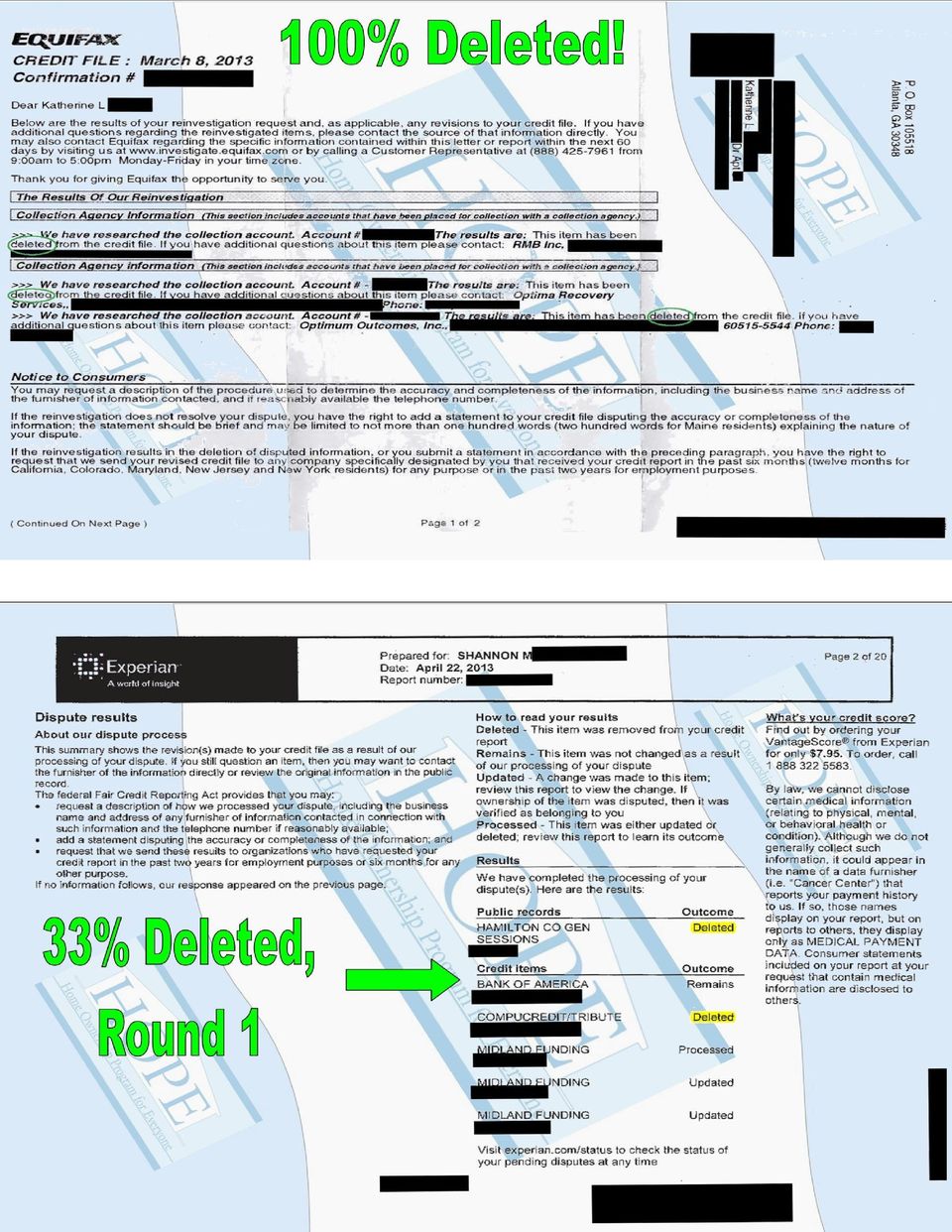

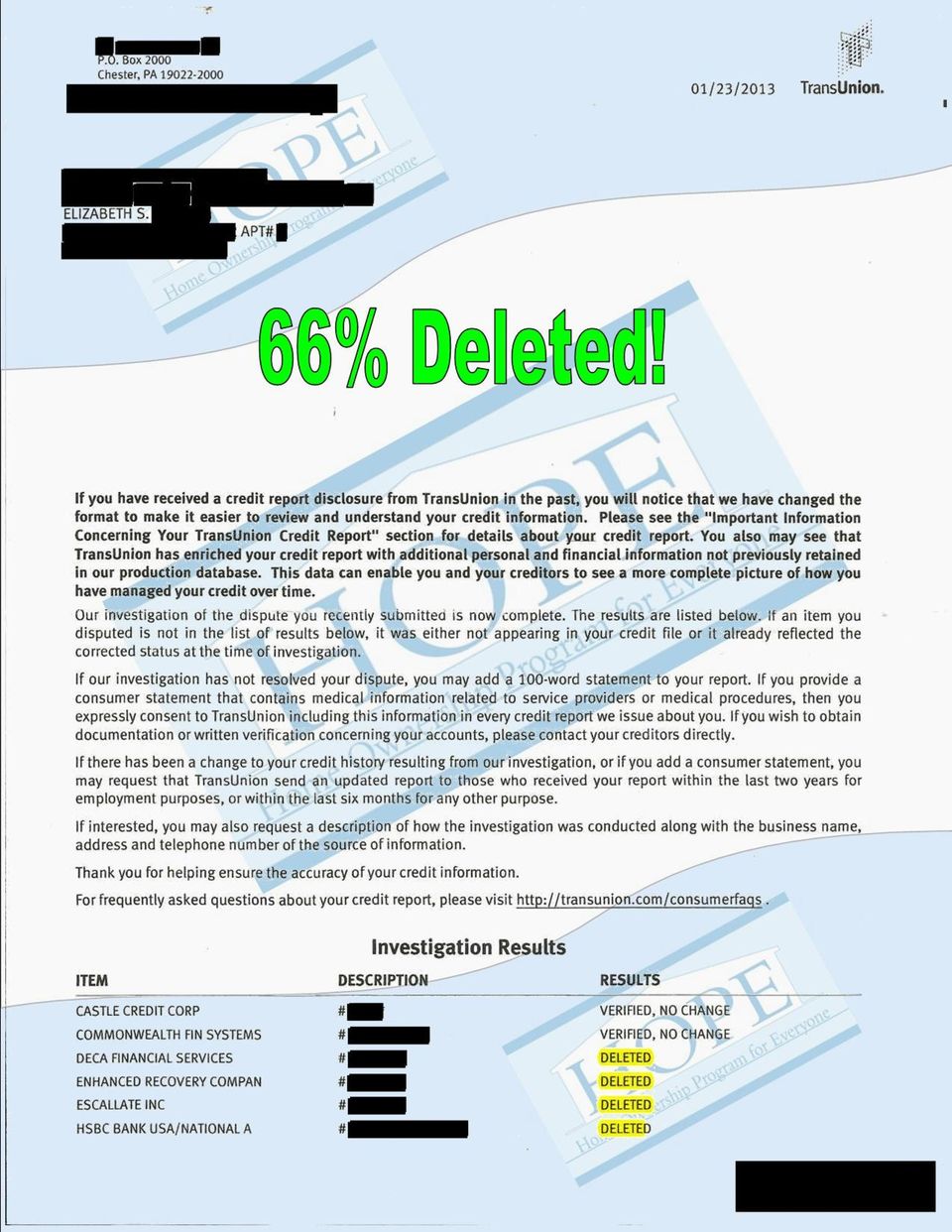

16 Real Examples, Real Results Over a Decade of Proven Success! On this page and the following pages you will see real life examples, just like those our HOPE team receives every single day, from HOPE members working with our credit experts to achieve the healthier credit they deserve! There s no such thing as a HOPEless credit situation! Courtesy of HOPE Page 16

17

18

19

20

21

22

23

24 The HOPE Process A Brief Overview Step One: Schedule a No-Obligation Credit Analysis *Visit or call to reserve your analysis with a HOPE Credit Expert today. A small analysis fee of $30 for an individual or $40 for a couple will be charged on the day of your appointment, at the end of the analysis. Step Two: Professional Credit Analysis *A HOPE Credit Expert will review your full credit report with you, in person or over the phone, and will help you discover everything which is lowering your credit scores. Together, you will uncover mistakes on your reports, and make a plan to move you toward your goals. You DECIDE if HOPE s plan is right for you. We have a strict, nopressure policy. We value the opportunity to earn your business. If HOPE is a good fit for you, your first-work fee of $199 is scheduled (3 days after we begin the initial work on your file). HOPE customizes an online client portal which you can log into 24/7 ensuring complete transparency for you during this process and making sure that you are 100% in the loop regarding the progress on your file. Then, a $99 monthly fee is schedule each month, for work completed the previous month. Fees are never charged in advance. There are no hidden fees. You can cancel any time. Step Three: An Experienced Credit Professional Prepares the Dispute *A legal challenge letter is prepared and mailed to the credit bureaus on your behalf. You can rest assured that a professional team, with years of experience, who has helped thousands of clients to correct credit inaccuracies before, is working their hardest on your behalf. Once you join HOPE, you are a member of the family and we don t let anyone get by with pushing our family around! Step Four: Responses *By law, the credit bureaus have 30 days to respond to your dispute and to send you the results of your investigation. Add on a few days for mailing documents to and from the bureaus and you can expect to receive your replies from the credit bureaus in around 45 days. Forward these replies to your personal HOPE case manager. The letters are reviewed and you are updated with the results which accounts have been deleted and which accounts remain. Your personal case manager will be corresponding with you regularly, via and/or phone, to be sure that everyone is on track with the plan which was developed for you during your initial credit analysis. You plan is customized, and can be adjusted anytime to be sure that you continue to move successfully toward your goals. Once you join HOPE, you are a member of the family and we don t let anyone get by with pushing our family around! Courtesy of HOPE Page 24

25 The HOPE Process A Brief Overview (Continued ) Step Five: Appeals *Once we receive the first round of response letters from the credit bureaus, your HOPE team can elevate the intensity of your next disputes with the credit bureaus. Remember, the credit bureaus and your creditors will likely fight this process just like they would if you were working on your own. The difference is that, as a HOPE member, you have our team s combined experience of over 30 years in the credit industry. We literally have strategy books that are over 1,000 pages thick on ways to help you correct the issues and mistakes on your credit! Step Six: Results *Update letters are received in the mail, just like after your initial disputes. Forward the update letters to your HOPE Case Manager. Results are posted to your client portal and you are able to review the results. Step Seven: Rinse and Repeat *Most HOPE clients repeat the appeals and results processes again at an escalated level. Step Eight: Review a Fresh, New Copy of Your Credit Report *After 3 rounds of disputes, it is time for you to pull and forward a new copy of your credit report, with scores, to your HOPE Case Manager. Don t worry, we ll point you in the right direction and help guide you through this step. Step Nine: Plan and Complete Your Final Steps *You and your HOPE Case Manager will make a new plan to help walk you through the final stages of your HOPE Membership. This plan will vary for each individual, depending upon results from your previous rounds of disputes. Step Ten: Graduation! *Once you have completed the plan designed for you by your HOPE team, it s time to graduate! Nothing makes us happier than to see our members complete the HOPE Program and to see their dreams come true! Remember, the goal of your HOPE team is to teach you how to maintain healthy credit for life. We ll be sure to offer you exit strategies and educational materials to help you maintain your healthier credit in the future. Nothing makes us happier than to see our members complete the HOPE Program and to see their dreams come true! Courtesy of HOPE Page 25

26 Discover the HOPE Difference Experienced. Reliable. Trusted. The credit repair industry has a bad name, for a good reason. There are a lot of scam artists out there taking advantage of people in desperate situations. At HOPE we are never offended when our prospective clients are skeptical about whether or not this process can really work. As a smart consumer, we EXPECT you to have questions and concerns as you decide if the HOPE Program is a good fit for you. We strive to operate with integrity and honesty a company of which our clients can be proud. Whether or not you choose to work with HOPE, you should be aware of few facts in order to protect yourself. 1. Yes, you do have the right to work on your credit yourself. *Again, just because you can do something doesn t mean that you should. However, if you ever come across a credit repair company that doesn t inform you of this right then our advice is to RUN AWAY QUICKLY! 2. There are no guarantees with credit repair work. *It is important to understand that there are no absolute guarantees with any credit repair or restoration work. HOPE cannot offer any guaranteed outcomes and neither can any other company. If a company makes a promise such as 720 Credit Scores in 30 Days, our advice, again, is to RUN AWAY QUICKLY! Why HOPE Is the BEST Choice for Your Credit Needs 1. No Upfront Fees *Work is performed first, fees are charged afterwards. 2. No Promise of a Magic Wand, But the Promise of a Solid Plan. *We don t tell you what we think you want to hear. We tell you the truth. 3. NACSO Certified * 4. Proven Results *Visit 5. Cancel Anytime. Call today or visit to schedule your no-obligation credit analysis with a HOPE Credit Expert. Courtesy of HOPE Page 26

27 HOPE USA 3525 Centre Circle, Suite 101 Fort Mill, SC Phone:

Credit Score Secrets Revealed

Credit Score Secrets Revealed This Complementary Special Report was prepared by: 2 The Secrets Behind Your Credit Scores Your life is your credit. And your Credit Score is the key to everything. As important

Credit Score Secrets Revealed This Complementary Special Report was prepared by: 2 The Secrets Behind Your Credit Scores Your life is your credit. And your Credit Score is the key to everything. As important

The Truth About Credit Repair

The Truth About Credit Repair Discover The Insider Secrets Of How The Credit System Really Works and How To Beat The Credit Bureaus At Their Own Game. David Shapiro Esq. Applied Credit Repair Solutions

The Truth About Credit Repair Discover The Insider Secrets Of How The Credit System Really Works and How To Beat The Credit Bureaus At Their Own Game. David Shapiro Esq. Applied Credit Repair Solutions

Credit History CREDIT REPORTS CREDIT SCORES BUILDING A STRONG CREDIT REPORT

CREDIT What You Should Know About... Credit History CREDIT REPORTS CREDIT SCORES BUILDING A STRONG CREDIT REPORT YourMoneyCounts Understanding what your credit history is what s in it, what s not in it

CREDIT What You Should Know About... Credit History CREDIT REPORTS CREDIT SCORES BUILDING A STRONG CREDIT REPORT YourMoneyCounts Understanding what your credit history is what s in it, what s not in it

How To Get A Credit Report From A Credit Card To A Credit Rating Card

Credit Report Info Packet Information in this Packet What Is a Credit Report?.....................3 What Is a Credit Score?..................... 4 Who Can See Your Credit Report?.............. 5 Ordering

Credit Report Info Packet Information in this Packet What Is a Credit Report?.....................3 What Is a Credit Score?..................... 4 Who Can See Your Credit Report?.............. 5 Ordering

Using Credit to Your Advantage.

Using Credit to Your Advantage. Topic Overview. The Using Credit To Your Advantage topic will provide participants with all the basic information they need to understand credit what it is and how to make

Using Credit to Your Advantage. Topic Overview. The Using Credit To Your Advantage topic will provide participants with all the basic information they need to understand credit what it is and how to make

Why Credit is Important

Page 1 Why Credit is Important Page 6 How to Protect Yourself from Identity Theft Page 7 Cosigning and Money Lending Tips Page 8 How to Avoid Credit Card Interest Why Credit is Important Learning to build

Page 1 Why Credit is Important Page 6 How to Protect Yourself from Identity Theft Page 7 Cosigning and Money Lending Tips Page 8 How to Avoid Credit Card Interest Why Credit is Important Learning to build

Credit Repair 101. Learn how to legally repair your own credit

Credit Repair 101 Learn how to legally repair your own credit The myth is, that you need to spend hundreds or even thousands of dollars with a large company to have your credit repaired. This is just not

Credit Repair 101 Learn how to legally repair your own credit The myth is, that you need to spend hundreds or even thousands of dollars with a large company to have your credit repaired. This is just not

Your Credit Score. 800-491-2328 www.congressionalfcu.org. score of at least 620 for approval and 760 for the best interest rate.

800-491-2328 www.congressionalfcu.org Your Credit Score Your credit score can have a major impact on your life. Not only do creditors typically check your score when deciding whether or not to approve

800-491-2328 www.congressionalfcu.org Your Credit Score Your credit score can have a major impact on your life. Not only do creditors typically check your score when deciding whether or not to approve

How do I get good credit?

Slide 1 Credit The information provided in this e-course is intended for educational purposes only and does not constitute specific advice for you as an individual. When evaluating your particular needs,

Slide 1 Credit The information provided in this e-course is intended for educational purposes only and does not constitute specific advice for you as an individual. When evaluating your particular needs,

Credit Scoring and Wealth

the Problem In most games, it is wise to understand the rules before you begin to play. What if you weren t aware that you were playing a game? What if you had not choice whether to play or not? Everyone

the Problem In most games, it is wise to understand the rules before you begin to play. What if you weren t aware that you were playing a game? What if you had not choice whether to play or not? Everyone

Managing Your Credit Report and Scores. Apprisen. 800.355.2227 www.apprisen.com

Managing Your Credit Report and Scores Apprisen 800.355.2227 www.apprisen.com Managing Your Credit Report and Scores Your credit score is one of the most important aspects of your personal finances. From

Managing Your Credit Report and Scores Apprisen 800.355.2227 www.apprisen.com Managing Your Credit Report and Scores Your credit score is one of the most important aspects of your personal finances. From

Credit Report The single most important document for protection against identity theft.

Understanding your Credit Report The single most important document for protection against identity theft. What to do if you spot errors A recent study shows that 79 percent of credit reports contained

Understanding your Credit Report The single most important document for protection against identity theft. What to do if you spot errors A recent study shows that 79 percent of credit reports contained

MANAGING CREDIT101 TM %*'9 [[[ EPXEREJGY SVK i

MANAGING CREDIT101 TM i This book is intended as a general guide to the topics discussed, and it does not deliver accounting, personal finance, or legal advice. It is not intended, and should not be used,

MANAGING CREDIT101 TM i This book is intended as a general guide to the topics discussed, and it does not deliver accounting, personal finance, or legal advice. It is not intended, and should not be used,

The West Virginia State Treasurer s Office. A free publication provided by

YOUR CREDIT SCORE A free publication provided by The West Virginia State Treasurer s Office Visit www.wvtreasury.com or Call 1.800.422.7498 From the Office of West Virginia State Treasurer, John D. Perdue

YOUR CREDIT SCORE A free publication provided by The West Virginia State Treasurer s Office Visit www.wvtreasury.com or Call 1.800.422.7498 From the Office of West Virginia State Treasurer, John D. Perdue

Understanding your Credit Score

Understanding your Credit Score Understanding Your Credit Score Fair, Isaac and Co. is the San Rafael, California Company founded in 1956 by Bill Fair and Earl Isaac. They pioneered the field of credit

Understanding your Credit Score Understanding Your Credit Score Fair, Isaac and Co. is the San Rafael, California Company founded in 1956 by Bill Fair and Earl Isaac. They pioneered the field of credit

Financial Empowerment Curriculum Moving Ahead Through Financial Management. Workshop Credit Overview

Financial Empowerment Curriculum Moving Ahead Through Financial Management Workshop Credit Overview 1 Workshop Objectives Explain why credit is important. Access and read a copy of your credit report.

Financial Empowerment Curriculum Moving Ahead Through Financial Management Workshop Credit Overview 1 Workshop Objectives Explain why credit is important. Access and read a copy of your credit report.

BETTER YOUR CREDIT PROFILE

BETTER YOUR CREDIT PROFILE Introduction What there is to your ITC that makes it so important to you and to everyone that needs to give you money. Your credit record shows the way you have been paying your

BETTER YOUR CREDIT PROFILE Introduction What there is to your ITC that makes it so important to you and to everyone that needs to give you money. Your credit record shows the way you have been paying your

GREENPATH FINANCIAL WELLNESS SERIES

GREENPATH FINANCIAL WELLNESS SERIES UNDERSTANDING YOUR CREDIT REPORT & SCORE Through financial knowledge and expertise, we provide high-quality products and services that enable people to enjoy a better

GREENPATH FINANCIAL WELLNESS SERIES UNDERSTANDING YOUR CREDIT REPORT & SCORE Through financial knowledge and expertise, we provide high-quality products and services that enable people to enjoy a better

Credit Scoring. 1-800-444-RATE www.gogsf.com

Credit Scoring 1-800-444-RATE www.gogsf.com Your credit score is a major factor that will be considered by the lender when they review your loan application. They want to know what your credit history

Credit Scoring 1-800-444-RATE www.gogsf.com Your credit score is a major factor that will be considered by the lender when they review your loan application. They want to know what your credit history

Fun, engaging and effective. Aligned with national financial education and core curriculum requirements.

Building Your Financial Foundation Adult Level Curriculum - Instructors Guide Fun, engaging and effective. Aligned with national financial education and core curriculum requirements. Lessons on: Credit

Building Your Financial Foundation Adult Level Curriculum - Instructors Guide Fun, engaging and effective. Aligned with national financial education and core curriculum requirements. Lessons on: Credit

Understanding Credit. Megan Stearns, Credit Counselor

Understanding Credit Megan Stearns, Credit Counselor Obtaining your free credit report will lower your credit score. Closing old accounts can help your credit score. Paying off the balances on your credit

Understanding Credit Megan Stearns, Credit Counselor Obtaining your free credit report will lower your credit score. Closing old accounts can help your credit score. Paying off the balances on your credit

PNC Financial Education FINANCIAL OPS. Banking Solutions for Military Personnel. Credit: Self study Guide

PNC Financial Education FINANCIAL OPS Banking Solutions for Military Personnel Credit: Self study Guide Revision Date: 11/2012 PNC Financial Education:FINANCIAL OPS Understanding Credit We all have financial

PNC Financial Education FINANCIAL OPS Banking Solutions for Military Personnel Credit: Self study Guide Revision Date: 11/2012 PNC Financial Education:FINANCIAL OPS Understanding Credit We all have financial

How to improve your FICO Score in perilous times By Blair Ball. National Distribution of FICO Scores

How to improve your FICO Score in perilous times By Blair Ball When you re applying for credit whether it s a credit card, a car loan, a personal loan or a mortgage lenders want to know your credit risk

How to improve your FICO Score in perilous times By Blair Ball When you re applying for credit whether it s a credit card, a car loan, a personal loan or a mortgage lenders want to know your credit risk

IMPORTANCE OF CREDIT HISTORY AND SUCCESSFUL SAVING

IMPORTANCE OF CREDIT HISTORY AND SUCCESSFUL SAVING From America Saves and Experian WHAT IS A CREDIT REPORT AND SCORE? A credit score is a three digit number that measures how likely you are to repay a

IMPORTANCE OF CREDIT HISTORY AND SUCCESSFUL SAVING From America Saves and Experian WHAT IS A CREDIT REPORT AND SCORE? A credit score is a three digit number that measures how likely you are to repay a

Understanding Credit. The Three C s of Credit. What is a Credit Bureau?

Understanding Credit By definition, the word credit has to do with trust. This is why credit impacts so many financial issues in our lives including the extension of a loan or credit card, how high an

Understanding Credit By definition, the word credit has to do with trust. This is why credit impacts so many financial issues in our lives including the extension of a loan or credit card, how high an

Your Credit Score What It Means to You as a Prospective Home Buyer

Dan L' Altrella Certified Mortgage Planner L'Altrella Lending Group Phone: 203.521.2905 Fax: 203.712.1188 danlaltrella@yahoo.com Your Credit Score What It Means to You as a Prospective Home Buyer Introduction

Dan L' Altrella Certified Mortgage Planner L'Altrella Lending Group Phone: 203.521.2905 Fax: 203.712.1188 danlaltrella@yahoo.com Your Credit Score What It Means to You as a Prospective Home Buyer Introduction

Introduction. The History of Credit Scoring

Your Credit Score 1 CONTENTS: Introduction...2 The History of Credit Scoring...2 Why Your Credit Score is So Important...2 The Five Factors of Credit Scoring...3 How Does a Low Credit Score Affect My Interest

Your Credit Score 1 CONTENTS: Introduction...2 The History of Credit Scoring...2 Why Your Credit Score is So Important...2 The Five Factors of Credit Scoring...3 How Does a Low Credit Score Affect My Interest

12 Your Credit Score Your Credit Score 1

12 Your Credit Score Your Credit Score 1 Notes CONTENTS: Introduction...2 The History of Credit Scoring...2 Why Your Credit Score is So Important...2 The Five Factors of Credit Scoring...3 How Does a Low

12 Your Credit Score Your Credit Score 1 Notes CONTENTS: Introduction...2 The History of Credit Scoring...2 Why Your Credit Score is So Important...2 The Five Factors of Credit Scoring...3 How Does a Low

HOW TO BOOST YOUR CREDIT IN 30 DAYS OR LESS

HOW TO BOOST YOUR CREDIT IN 30 DAYS OR LESS By The Arizona Credit Law Group, PLLC A consumer rights law firm Learn how to improve your credit using 5 simple rules No tricks, no gimmicks, just facts. The

HOW TO BOOST YOUR CREDIT IN 30 DAYS OR LESS By The Arizona Credit Law Group, PLLC A consumer rights law firm Learn how to improve your credit using 5 simple rules No tricks, no gimmicks, just facts. The

Financial payment profile Fair Isaac Corporation (FICO) 300 to 850 the higher, the better

300 to 850 the higher, the better") What is a credit score? Financial payment profile Fair Isaac Corporation (FICO) 300 to 850 the higher, the better National distribution of FICO scores What a low score could cost you? Tens of thousands

What is a credit score? Financial payment profile Fair Isaac Corporation (FICO) 300 to 850 the higher, the better National distribution of FICO scores What a low score could cost you? Tens of thousands

Preparing for Homeownership

Preparing for Homeownership Homeownership Homeownership is a dream for many people. Purchasing a home can be exciting, but it can also be an intimidating process. Educating future homebuyers will help

Preparing for Homeownership Homeownership Homeownership is a dream for many people. Purchasing a home can be exciting, but it can also be an intimidating process. Educating future homebuyers will help

NOTES. 12 Your Credit Score Your Credit Score 1 CONTENTS:

12 Your Credit Score Your Credit Score 1 NOTES CONTENTS: Introduction...2 The History of Credit Scoring...2 Why Your Credit Score is So Important...3 The Five Factors of Credit Scoring...3 How Does a Low

12 Your Credit Score Your Credit Score 1 NOTES CONTENTS: Introduction...2 The History of Credit Scoring...2 Why Your Credit Score is So Important...3 The Five Factors of Credit Scoring...3 How Does a Low

About your credit score. About FICO Score. Other names for FICO Score. http://www.myfico.com/crediteducation/creditscores.aspx

http://www.myfico.com/crediteducation/creditscores.aspx About your credit score Your credit score influences the credit that s available to you and the terms (interest rate, etc.) that lenders offer you.

http://www.myfico.com/crediteducation/creditscores.aspx About your credit score Your credit score influences the credit that s available to you and the terms (interest rate, etc.) that lenders offer you.

redit score 600 APR ebt mortgage rate YOUR CREDIT SCORES payment history Credit scores are vital to your financial health nstallment loan

nstallment loan 20 40 680 ebt 00 redit score 600 665 payment history APR mortgage rate YOUR CREDIT SCORES Credit scores are vital to your financial health A credit score is a number that helps lenders

nstallment loan 20 40 680 ebt 00 redit score 600 665 payment history APR mortgage rate YOUR CREDIT SCORES Credit scores are vital to your financial health A credit score is a number that helps lenders

PRACTICAL MONEY GUIDES CREDIT HISTORY. Your credit history and how it affects your future

PRACTICAL MONEY GUIDES CREDIT HISTORY Your credit history and how it affects your future YOUR CREDIT HISTORY THE RECORD OF HOW WELL YOU HANDLE CREDIT To get a glimpse of your financial future, many businesses

PRACTICAL MONEY GUIDES CREDIT HISTORY Your credit history and how it affects your future YOUR CREDIT HISTORY THE RECORD OF HOW WELL YOU HANDLE CREDIT To get a glimpse of your financial future, many businesses

Understanding Your Credit Score

Understanding Your Credit Score Whether or not you re aware of it, your credit score (or lack thereof) plays a significant role in your financial well being. Build a great score and you ll enjoy the rewards

Understanding Your Credit Score Whether or not you re aware of it, your credit score (or lack thereof) plays a significant role in your financial well being. Build a great score and you ll enjoy the rewards

Your Credit Repair Solution

Your Credit Repair Solution Introduction Your Credit Report Solution will help you understand that there is help available for fixing your credit. Even though you might feel as though you are alone and

Your Credit Repair Solution Introduction Your Credit Report Solution will help you understand that there is help available for fixing your credit. Even though you might feel as though you are alone and

Credit Repair Made Easy

Credit Repair Made Easy A simple self help guide to credit repair By Don Troiano Introduction My name is Don Troiano and I spent over 15 years in the mortgage industry. Knowing how to guide customers in

Credit Repair Made Easy A simple self help guide to credit repair By Don Troiano Introduction My name is Don Troiano and I spent over 15 years in the mortgage industry. Knowing how to guide customers in

Credit Reports. published by AAA Fair Credit Foundation

Credit Reports published by AAA Fair Credit Foundation Credit Reports 1. What is a Credit Report?..........................................................2 2. What Your Credit Report Reveals About You...................................4

Credit Reports published by AAA Fair Credit Foundation Credit Reports 1. What is a Credit Report?..........................................................2 2. What Your Credit Report Reveals About You...................................4

SOME IDEAS THAT MAY HELP WITH. Credit Problems and How to Get Help

66308 1083 9/9/04 3:03 PM Page Cov1 SOME IDEAS THAT MAY HELP WITH Credit Problems and How to Get Help 66308 1083 9/9/04 3:03 PM Page Cov2 Table of Contents Do you have a credit problem? 1 Minor credit

66308 1083 9/9/04 3:03 PM Page Cov1 SOME IDEAS THAT MAY HELP WITH Credit Problems and How to Get Help 66308 1083 9/9/04 3:03 PM Page Cov2 Table of Contents Do you have a credit problem? 1 Minor credit

Credit Reports Credit Scores. Understanding reports and scores Correcting errors Obtaining a free report

Credit Reports Credit Scores Understanding reports and scores Correcting errors Obtaining a free report What goes into your credit report...and who uses it? A A credit report is a summary of your financial

Credit Reports Credit Scores Understanding reports and scores Correcting errors Obtaining a free report What goes into your credit report...and who uses it? A A credit report is a summary of your financial

Understanding Your Credit Report

Understanding Your Credit Report What is credit? Credit is the use of someone else s money in exchange for a promise to pay it back on a given date. There are two major types of credit: Revolving and Installment.

Understanding Your Credit Report What is credit? Credit is the use of someone else s money in exchange for a promise to pay it back on a given date. There are two major types of credit: Revolving and Installment.

Your Credit Score What It Means to You as a Prospective Home Buyer

Ken Buckery Mortgage Lender Alpha Mortgage Phone: (910) 256-8999 Fax: (910) 795-4922 ken.buckery@alphamortgage.com www.kenbuckery.com Your Credit Score What It Means to You as a Prospective Home Buyer

Ken Buckery Mortgage Lender Alpha Mortgage Phone: (910) 256-8999 Fax: (910) 795-4922 ken.buckery@alphamortgage.com www.kenbuckery.com Your Credit Score What It Means to You as a Prospective Home Buyer

The USA Mortgage Smart-Loan Guide

The USA Mortgage Smart-Loan Guide Page 1 of 8 The USA Mortgage Smart-Loan Guide Hello! Welcome to the USA Mortgage Smart-Loan Guide. Please keep in mind that this simple guide is not intended to be an

The USA Mortgage Smart-Loan Guide Page 1 of 8 The USA Mortgage Smart-Loan Guide Hello! Welcome to the USA Mortgage Smart-Loan Guide. Please keep in mind that this simple guide is not intended to be an

Financial Empowerment Curriculum. Moving Ahead Through Financial Management. Module Three: Mastering Credit Basics

Financial Empowerment Curriculum Moving Ahead Through Financial Management Mastering Credit Basics Reviewing, Understanding and Improving Your Credit Module 3: Mastering Credit Basics Time Clock: 11:00-12:00

Financial Empowerment Curriculum Moving Ahead Through Financial Management Mastering Credit Basics Reviewing, Understanding and Improving Your Credit Module 3: Mastering Credit Basics Time Clock: 11:00-12:00

Your Credit Report. 595 Market Street, 16th Floor San Francisco, CA 94105 888.456.2227 www.balancepro.net

Your Credit Report 750. 670. 620. 575. You may not think about them every day, but your credit report and the three little digits that make up your credit score probably influence your life in many ways.

Your Credit Report 750. 670. 620. 575. You may not think about them every day, but your credit report and the three little digits that make up your credit score probably influence your life in many ways.

Understanding Your Credit Score and Credit Report. George Williams, CPA, JD, LLM Ross, Rosenthal & Company, LLP June 21, 2012

Understanding Your Credit Score and Credit Report George Williams, CPA, JD, LLM Ross, Rosenthal & Company, LLP June 21, 2012 What is a Credit Score? What is a Credit Report? A credit score is a number

Understanding Your Credit Score and Credit Report George Williams, CPA, JD, LLM Ross, Rosenthal & Company, LLP June 21, 2012 What is a Credit Score? What is a Credit Report? A credit score is a number

CREDIT REPORT: Adapted from the National Consumer Law Center Inc s. brochure entitled, The Truth About Credit Reports and Credit Repair Companies.

CREDIT REPORT: HOW TO CHECK YOUR CREDIT Getting a copy of your credit report is important because: it gives you an idea of what your credit history looks like, you can make sure that the information on

CREDIT REPORT: HOW TO CHECK YOUR CREDIT Getting a copy of your credit report is important because: it gives you an idea of what your credit history looks like, you can make sure that the information on

All About Credit Reports from A to Z

All About Credit Reports from A to Z Adverse Action Notice A notice that you have been denied credit, employment, insurance, or other benefits based on information in a credit report. The notice should

All About Credit Reports from A to Z Adverse Action Notice A notice that you have been denied credit, employment, insurance, or other benefits based on information in a credit report. The notice should

Credit Repair For Court Reporters. When Bad Dings Happen To Good People. By Julie Samford Realtime Ready. Julie Samford julie@realtimeready.

Credit Repair For Court Reporters When Bad Dings Happen To Good People By Realtime Ready 1 $96,634.00 difference! That s $5,496.00 straight out of your pocket when you could have had 0% interest! (Info

Credit Repair For Court Reporters When Bad Dings Happen To Good People By Realtime Ready 1 $96,634.00 difference! That s $5,496.00 straight out of your pocket when you could have had 0% interest! (Info

Building a CREDIT REPORT. Federal Trade Commission consumer.ftc.gov

Building a CREDIT REPORT Federal Trade Commission consumer.ftc.gov Shopping for a car? Applying for a job? Looking for a home? Getting your financial house in order? It s time to check your credit report.

Building a CREDIT REPORT Federal Trade Commission consumer.ftc.gov Shopping for a car? Applying for a job? Looking for a home? Getting your financial house in order? It s time to check your credit report.

Introduction The History of Credit Scoring Why Your Credit Score is So Important

Introduction The subject of credit scoring has become an increasingly hot topic, and for good reason. For many years, the general public only associated the concept of credit scoring with the need to purchase

Introduction The subject of credit scoring has become an increasingly hot topic, and for good reason. For many years, the general public only associated the concept of credit scoring with the need to purchase

Make the most of your credit score

Make the most of your credit score Consolidated Credit 5701 West Sunrise Boulevard Fort Lauderdale, FL 33313 1-800-210-3481 www.consolidatedcredit.org Congratulations on taking this important step to learn

Make the most of your credit score Consolidated Credit 5701 West Sunrise Boulevard Fort Lauderdale, FL 33313 1-800-210-3481 www.consolidatedcredit.org Congratulations on taking this important step to learn

Contents 1 WHAT'S ON YOUR CREDIT REPORT?... 3 WHAT IS IT?... 3 HOW TO GET YOUR CREDIT REPORT... 5 WHAT'S ON YOUR REPORT?... 7

DIY Credit Repair Contents 1 WHAT'S ON YOUR CREDIT REPORT?... 3 WHAT IS IT?... 3 HOW TO GET YOUR CREDIT REPORT... 5 WHAT'S ON YOUR REPORT?... 7 2 LOCATE THE CREDIT REPORT MISTAKES... 10 WHY ARE THERE MISTAKES?...

DIY Credit Repair Contents 1 WHAT'S ON YOUR CREDIT REPORT?... 3 WHAT IS IT?... 3 HOW TO GET YOUR CREDIT REPORT... 5 WHAT'S ON YOUR REPORT?... 7 2 LOCATE THE CREDIT REPORT MISTAKES... 10 WHY ARE THERE MISTAKES?...

Solving the Credit Puzzle. L G & W Federal Credit Union

Solving the Credit Puzzle L G & W Federal Credit Union Knowledge Check How much do you already know about credit scoring? Sample Credit Report Credit Bureaus Equifax TransUnion Experian Who Can Pull Your

Solving the Credit Puzzle L G & W Federal Credit Union Knowledge Check How much do you already know about credit scoring? Sample Credit Report Credit Bureaus Equifax TransUnion Experian Who Can Pull Your

Your Credit Report. 595 Market Street, 16th Floor San Francisco, CA 94105 888.456.2227 www.balancepro.net

Your Credit Report 750. 670. 620. 575. You may not think about them every day, but your credit reports and the three little digits that make up your credit score probably influence your life in many ways.

Your Credit Report 750. 670. 620. 575. You may not think about them every day, but your credit reports and the three little digits that make up your credit score probably influence your life in many ways.

Understanding How Insurers Use Credit Information

Understanding How Insurers Use Credit Information UNDERSTANDING HOW INSURERS USE CREDIT INFORMATION Many personal auto and homeowners insurance companies look at several factors, including consumer credit

Understanding How Insurers Use Credit Information UNDERSTANDING HOW INSURERS USE CREDIT INFORMATION Many personal auto and homeowners insurance companies look at several factors, including consumer credit

Overcoming Credit Obstacles

Overcoming Credit Obstacles Ever wondered how your credit impacts your overall financial wellness? Let us tell you: It plays a starring role in many of your life s important financial endeavors! Whether

Overcoming Credit Obstacles Ever wondered how your credit impacts your overall financial wellness? Let us tell you: It plays a starring role in many of your life s important financial endeavors! Whether

How to Use Credit. Latino Community Credit Union & Latino Community Development Center

How to Use Credit Latino Community Credit Union & Latino Community Development Center How to Use Credit Latino Community Credit Union & the Latino Community Development Center www.latinoccu.org Copyright

How to Use Credit Latino Community Credit Union & Latino Community Development Center How to Use Credit Latino Community Credit Union & the Latino Community Development Center www.latinoccu.org Copyright

Consumer Guides to Credit Reporting and Credit Scores (Appropriate for General Distribution)

") Appendix L Consumer Guides to Credit Reporting and Credit Scores (Appropriate for General Distribution) This appendix contains two consumer guides on credit reports and credit scores. The first guide summarizes

Appendix L Consumer Guides to Credit Reporting and Credit Scores (Appropriate for General Distribution) This appendix contains two consumer guides on credit reports and credit scores. The first guide summarizes

BalanceTrack. The World of Credit Reports

BalanceTrack The World of Credit Reports Credit reports and credit scores influence our lives in many ways. Your history of credit management can affect the cost of the credit you receive, your ability

BalanceTrack The World of Credit Reports Credit reports and credit scores influence our lives in many ways. Your history of credit management can affect the cost of the credit you receive, your ability

2/7/2015 Credit Scoring Handbook. https://vip.vantageproduction.com/htmltemplate/44909/37d8475b-cf7b-46fa-8091-5d80543e1511/render?

We r eher et ohel p. Cal l T oday! 4808324343 https://vip.vantageproduction.com/htmltemplate/44909/37d8475b-cf7b-46fa-8091-5d80543e1511/render?preview 2/10 2/7/2015 Credit Scoring Handbook Notes YourCreditScore

We r eher et ohel p. Cal l T oday! 4808324343 https://vip.vantageproduction.com/htmltemplate/44909/37d8475b-cf7b-46fa-8091-5d80543e1511/render?preview 2/10 2/7/2015 Credit Scoring Handbook Notes YourCreditScore

UNDERSTANDING HOW INSURERS USE CREDIT INFORMATION

The State of New Hampshire Insurance Department 21 South Fruit Street, Suite 14 Concord, NH 03301 (603) 271-2261 Fax (603) 271-1406 TDD Access: Relay NH 1-800-735-2964 Roger A. Sevigny Commissioner Alexander

The State of New Hampshire Insurance Department 21 South Fruit Street, Suite 14 Concord, NH 03301 (603) 271-2261 Fax (603) 271-1406 TDD Access: Relay NH 1-800-735-2964 Roger A. Sevigny Commissioner Alexander

Unlimited Business Financing Without A Personal Guarantee!

Unlimited Business Financing Without A Personal Guarantee! Now YOU Can Have ALL The Business Credit You Need Faster Than You Thought Possible! Finally a Business Credit Asset that will Rid You of Business

Unlimited Business Financing Without A Personal Guarantee! Now YOU Can Have ALL The Business Credit You Need Faster Than You Thought Possible! Finally a Business Credit Asset that will Rid You of Business

Take control of your credit score

Take control of your credit score A guide to understanding and improving your credit. What is a credit score? Your credit score is a number between 300 and 850, assigned to you by a credit bureau, that

Take control of your credit score A guide to understanding and improving your credit. What is a credit score? Your credit score is a number between 300 and 850, assigned to you by a credit bureau, that

Overcoming the Credit Barrier. Poor Credit Affects Your Ability to Plan

Overcoming the Credit Barrier: Clearing the Way to Your Financial Goals was written and designed for The National Foundation for Credit Counseling (NFCC ) and the Financial Planning Association (FPA )

Overcoming the Credit Barrier: Clearing the Way to Your Financial Goals was written and designed for The National Foundation for Credit Counseling (NFCC ) and the Financial Planning Association (FPA )

Mortgage Secrets. What the banks don t want you to know.

Mortgage Secrets What the banks don t want you to know. Copyright Notice: Copyright 2006 - All Rights Reserved Contents may not be shared or transmitted in any form, so don t even think about it. Trust

Mortgage Secrets What the banks don t want you to know. Copyright Notice: Copyright 2006 - All Rights Reserved Contents may not be shared or transmitted in any form, so don t even think about it. Trust

How To Know Your Credit Risk

Understanding Your FICO Score Understanding FICO Scores 2013 Fair Isaac Corporation. All rights reserved. 1 August 2013 Table of Contents Introduction to Credit Scoring 1 What s in Your Credit Reports

Understanding Your FICO Score Understanding FICO Scores 2013 Fair Isaac Corporation. All rights reserved. 1 August 2013 Table of Contents Introduction to Credit Scoring 1 What s in Your Credit Reports

IMPROVE YOUR CREDIT SCORE. Effective Credit Management At Your Fingertips

IMPROVE YOUR CREDIT SCORE Effective Credit Management At Your Fingertips Introduction In this ebook, you will get valuable information including: What is a credit score The score breakdown Managing your

IMPROVE YOUR CREDIT SCORE Effective Credit Management At Your Fingertips Introduction In this ebook, you will get valuable information including: What is a credit score The score breakdown Managing your

Your Credit Score What It Means to You as a Prospective Home Buyer

James Lindquist Mortgage Planner / Broker Cendera Funding Phone: (214)616-9067 Fax: (214)547-8225 jlindquist@cenderafunding.com Your Credit Score What It Means to You as a Prospective Home Buyer Introduction

James Lindquist Mortgage Planner / Broker Cendera Funding Phone: (214)616-9067 Fax: (214)547-8225 jlindquist@cenderafunding.com Your Credit Score What It Means to You as a Prospective Home Buyer Introduction

Your Credit Score What It Means to You as a Prospective Home Buyer

Dan Keller Mortgage Advisor Pacific Trust Mortgage Phone: (425) 350-7136 Fax: (206) 339-6343 dan.mortgageadvisor@gmail.com www.mylenderdankeller.com Your Credit Score What It Means to You as a Prospective

Dan Keller Mortgage Advisor Pacific Trust Mortgage Phone: (425) 350-7136 Fax: (206) 339-6343 dan.mortgageadvisor@gmail.com www.mylenderdankeller.com Your Credit Score What It Means to You as a Prospective

The AFI Resource Center is pleased to provide this presentation about credit reports.

The AFI Resource Center is pleased to provide this presentation about credit reports. This is one of several presentations developed for AFI grantees on a variety of financial education topics, including

The AFI Resource Center is pleased to provide this presentation about credit reports. This is one of several presentations developed for AFI grantees on a variety of financial education topics, including

Understanding Your FICO Score

Understanding Your FICO Score 2013 Fair Isaac Corporation. All rights reserved. 1 August 2013 Table of Contents Introduction to Credit Scoring 1 What s in Your Credit Report 1 Checking Your Credit Report

Understanding Your FICO Score 2013 Fair Isaac Corporation. All rights reserved. 1 August 2013 Table of Contents Introduction to Credit Scoring 1 What s in Your Credit Report 1 Checking Your Credit Report

Understanding Your Credit Score

Understanding Your Credit Score Contents Your Credit Score A Vital Part of Your Credit Health...... 1 How Credit Scoring Helps You........ 2 Your Credit Report The Basis of Your Score............. 4 How

Understanding Your Credit Score Contents Your Credit Score A Vital Part of Your Credit Health...... 1 How Credit Scoring Helps You........ 2 Your Credit Report The Basis of Your Score............. 4 How

Credit Scores. www.howtogainwealth.com. Copyright 2009 How to Gain Wealth. All rights reserved.

Credit Scores Why is my Credit Score important? Lenders, such as banks and credit card companies, use credit scores to evaluate the potential risk posed by lending money to consumers and to mitigate losses

Credit Scores Why is my Credit Score important? Lenders, such as banks and credit card companies, use credit scores to evaluate the potential risk posed by lending money to consumers and to mitigate losses

CREDIT BASICS About your credit score

CREDIT BASICS About your credit score Your credit score influences the credit that s available to you and the terms (interest rate, etc.) that lenders offer you. It s a vital part of your credit health.

CREDIT BASICS About your credit score Your credit score influences the credit that s available to you and the terms (interest rate, etc.) that lenders offer you. It s a vital part of your credit health.

Improving Your Credit

Teacher Homebuyer Guide to: Improving Your Credit By John Godbey, Founder and Broker of Teacher Homebuyer Real Estate Introduction Thank you for signing up for our Ebook "Improving Your Credit." We find

Teacher Homebuyer Guide to: Improving Your Credit By John Godbey, Founder and Broker of Teacher Homebuyer Real Estate Introduction Thank you for signing up for our Ebook "Improving Your Credit." We find

JUST BEGINNING. Your financial life is. I m Buying a Car!

Your financial life is JUST BEGINNING. The decisions you make now will put a steering wheel and a credit card in your hands. But they will also affect your financial future. Your choices may even prevent

Your financial life is JUST BEGINNING. The decisions you make now will put a steering wheel and a credit card in your hands. But they will also affect your financial future. Your choices may even prevent

Self Help Credit Repair Guide

Self Help Credit Repair Guide This report will inform you of your rights under the Fair Credit Reporting Act (FCRA) and what you can do about it! In 1971 Congress passed legislation to protect consumer

Self Help Credit Repair Guide This report will inform you of your rights under the Fair Credit Reporting Act (FCRA) and what you can do about it! In 1971 Congress passed legislation to protect consumer

How To Check Your Credit Report For Not Credit History

Your Credit Report P.O. Box 15128 Spokane Valley, WA 99215 800.852.5316 www.hzcu.org You may not think about them every day, but your credit report and the three little digits that make up your credit

Your Credit Report P.O. Box 15128 Spokane Valley, WA 99215 800.852.5316 www.hzcu.org You may not think about them every day, but your credit report and the three little digits that make up your credit

YOUR CREDIT SCORE. Payment History - 35%

YOUR REDIT SORE Many of our clients are concerned about their ability to obtain credit in the future. There are several issues related to those concerns. redit reporting agencies (Experian, Equifax, and

YOUR REDIT SORE Many of our clients are concerned about their ability to obtain credit in the future. There are several issues related to those concerns. redit reporting agencies (Experian, Equifax, and

Introduction. Purpose. Student Introductions. Agenda and Ground Rules. Objectives

Introduction Instructor and student introductions. Module overview. 1 2 Your name. Student Introductions Your expectations, questions, and concerns about credit. Purpose will: Show you how to read a credit

Introduction Instructor and student introductions. Module overview. 1 2 Your name. Student Introductions Your expectations, questions, and concerns about credit. Purpose will: Show you how to read a credit

Chapter 06. What is Consumer Credit? Chapter 6 Learning Objectives. Introduction to Consumer Credit

Chapter 06 Introduction to Consumer Credit McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. 6-1 Chapter 6 Learning Objectives 1. Define consumer credit and analyze

Chapter 06 Introduction to Consumer Credit McGraw-Hill/Irwin Copyright 2012 by The McGraw-Hill Companies, Inc. All rights reserved. 6-1 Chapter 6 Learning Objectives 1. Define consumer credit and analyze

GL 04/09. How To Improve Your Credit Score

GL 04/09 How To Improve Your Credit Score Table of Contents 1. What is Credit and What is Debt? 2. The 4 C S of Credit 3. Keeping Score With Your Credit 4. The FICO Score Breakdown 5. How to Rebuild Your

GL 04/09 How To Improve Your Credit Score Table of Contents 1. What is Credit and What is Debt? 2. The 4 C S of Credit 3. Keeping Score With Your Credit 4. The FICO Score Breakdown 5. How to Rebuild Your

Reviewing C Your Credit Report

chapter 2 Reviewing C Your Credit Report What do your creditors have to say about the way you handle money? Having a good credit score can help you turn your home-buying dream into a reality. There s much

chapter 2 Reviewing C Your Credit Report What do your creditors have to say about the way you handle money? Having a good credit score can help you turn your home-buying dream into a reality. There s much

Over the last decade, Americans have been able to access credit too easily.

Over the last decade, Americans have been able to access credit too easily. Being able to borrow too much allowed many of us to make bad decisions decisions that led to painful consequences. Now, the business

Over the last decade, Americans have been able to access credit too easily. Being able to borrow too much allowed many of us to make bad decisions decisions that led to painful consequences. Now, the business

When & Where CREDIT. to Apply for. How to Know. Discover when your credit is good enough to get approved FIX YOUR CREDIT YOURSELF HOW TO

HOW TO FIX YOUR CREDIT YOURSELF (without an attorney) How to Know When & Where to Apply for CREDIT Discover when your credit is good enough to get approved Introduction Now that you ve been through the

HOW TO FIX YOUR CREDIT YOURSELF (without an attorney) How to Know When & Where to Apply for CREDIT Discover when your credit is good enough to get approved Introduction Now that you ve been through the

3/13/2013. US Consumer Credit Restoration Association 2013 All Rights Reserved

1 FREE REPORT How to Settle Collections and Request That They Be Deleted! Jim Hogle Your Credit Expert Resource Internationally known public speaker Author of numerous publications, articles and training

1 FREE REPORT How to Settle Collections and Request That They Be Deleted! Jim Hogle Your Credit Expert Resource Internationally known public speaker Author of numerous publications, articles and training

TABLE OF CONTENTS. CHAPTER 1: Credit Report.. Page 1. CHAPTER 2: Credit Score...Page 3. CHAPTER 3: Credit Reporting Agencies.

TABLE OF CONTENTS CHAPTER 1: Credit Report.. Page 1 CHAPTER 2: Credit Score.....Page 3 CHAPTER 3: Credit Reporting Agencies.Page 6 CHAPTER 4: How to get a FREE Credit Report Page 8 CHAPTER 5: The 4 th

TABLE OF CONTENTS CHAPTER 1: Credit Report.. Page 1 CHAPTER 2: Credit Score.....Page 3 CHAPTER 3: Credit Reporting Agencies.Page 6 CHAPTER 4: How to get a FREE Credit Report Page 8 CHAPTER 5: The 4 th

FICO Vantage Will Include Rent # of People in this category

What You Must Know About Your Credit Report and Score Must Know: There is more than one company reporting on your credit; you need to know most websites and rental companies use vantage scores and most

What You Must Know About Your Credit Report and Score Must Know: There is more than one company reporting on your credit; you need to know most websites and rental companies use vantage scores and most

Navigating the Credit Bureau

by Nancy Jakubic Navigating the Credit Bureau beyond the Credit Score A HIGH CREDIT SCORE IS OFTEN seen as the magic number to close a deal. Sometimes it is. Sometimes it s not. While many lenders use

by Nancy Jakubic Navigating the Credit Bureau beyond the Credit Score A HIGH CREDIT SCORE IS OFTEN seen as the magic number to close a deal. Sometimes it is. Sometimes it s not. While many lenders use

Improve Your Credit Put Bad Credit Behind You

Improve Your Credit Put Bad Credit Behind You Improve your credit While it s possible to get by without credit, access to credit is essential for buying a home, financing a car or getting a credit card.

Improve Your Credit Put Bad Credit Behind You Improve your credit While it s possible to get by without credit, access to credit is essential for buying a home, financing a car or getting a credit card.

The materials presented during the webinar are for informational purposes only. They are not offered as and do not constitute an offer for a loan,

The materials presented during the webinar are for informational purposes only. They are not offered as and do not constitute an offer for a loan, professional or legal advice or legal opinion and should

The materials presented during the webinar are for informational purposes only. They are not offered as and do not constitute an offer for a loan, professional or legal advice or legal opinion and should

Your Credit Score What It Means to You as a Prospective Home Buyer

Brian Berman President / Sr. Loan Specialist Mortgage Atlanta, LLC Phone: 678.564.1522 Fax: 888.727.0145 bberman@mortgage-atlanta.com Your Credit Score What It Means to You as a Prospective Home Buyer

Brian Berman President / Sr. Loan Specialist Mortgage Atlanta, LLC Phone: 678.564.1522 Fax: 888.727.0145 bberman@mortgage-atlanta.com Your Credit Score What It Means to You as a Prospective Home Buyer

Understanding Credit Reports and Scores and How to Improve It!

Understanding Credit Reports and Scores and How to Improve It! Robin Minor, CCCC What Will We Cover? When we are finished, you will understand: Credit Reports and Credit Scores - What they are and how

Understanding Credit Reports and Scores and How to Improve It! Robin Minor, CCCC What Will We Cover? When we are finished, you will understand: Credit Reports and Credit Scores - What they are and how

Using Credit to Your Advantage

Hands on Banking Using Credit to Your Advantage Credit Reports, Credit Scores and Dealing with Debt The Hands on Banking program is a free public service provided by Wells Fargo. You may also access the

Hands on Banking Using Credit to Your Advantage Credit Reports, Credit Scores and Dealing with Debt The Hands on Banking program is a free public service provided by Wells Fargo. You may also access the

UNDERSTANDING YOUR CREDIT REPORT (Part 1) By Bill Taylor

By Bill Taylor") UNDERSTANDING YOUR CREDIT REPORT (Part 1) By Bill Taylor Most studies about consumer debt have only focused on credit cards and mortgages. However, personal debt also may include medical expenses, school

UNDERSTANDING YOUR CREDIT REPORT (Part 1) By Bill Taylor Most studies about consumer debt have only focused on credit cards and mortgages. However, personal debt also may include medical expenses, school

Tracking Your Credit History By Mark Schug

By Mark Schug Financial institutions (banks, savings and loan associations, credit unions, and consumer finance companies) are private, profit seeking businesses. They expect to be paid back most of the

By Mark Schug Financial institutions (banks, savings and loan associations, credit unions, and consumer finance companies) are private, profit seeking businesses. They expect to be paid back most of the

About credit reports. Credit Reporting Agencies. Creating Your Credit Report

About credit reports Credit Reporting Agencies Credit reporting agencies maintain files on millions of borrowers. Lenders making credit decisions buy credit reports on their prospects, applicants and customers

About credit reports Credit Reporting Agencies Credit reporting agencies maintain files on millions of borrowers. Lenders making credit decisions buy credit reports on their prospects, applicants and customers

The ABCs of Credit Credit Scores Establishing Credit Maintaining Good Credit Credit Cards Managing Credit Challenges

The ABCs of Credit Credit Scores Establishing Credit Maintaining Good Credit Credit Cards Managing Credit Challenges CREDIT DEFINITIONS Credit Trust given to another person for future payment of a loan,