GET YOUR FINANCIAL HOUSE IN ORDER FINANCIAL

|

|

|

- Marian Briggs

- 8 years ago

- Views:

Transcription

1 GET YOUR FINANCIAL HOUSE IN ORDER FINANCIAL

2 This publication is designed to provide competent and reliable information regarding the subject matter covered. However, it is provided with the understanding that the author is not engaged in rendering legal, financial, or other professional advice. Laws and practices often vary from state to state and country to country and if legal or other expert assistance is required, the services of a professional should be sought. The author specifically disclaims any liability that is incurred from the use or application of the contents of this book. Copyright 2015 by Robert T. Kiyosaki. All rights reserved. Except as permitted under the U.S. Copyright Act of 1976, no part of this publication may be reproduced, distributed, or transmitted in any form or by any means or stored in a database or retrieval system, without the prior written permission of the publisher. First Download Edition: December 2015

3 Introduction Life is about choice. When I was just nine years old, I made my choice to be rich. I had two fathers, a rich one and a poor one. My real father, my poor dad, was highly educated and intelligent with a PhD. My best friend s father, my rich dad, never finished the eighth grade. Both men were successful in their careers, working hard all their lives. Both earned substantial incomes, yet one always struggled financially. The other would become one of the richest men in Hawaii. One died leaving tens of millions of dollars to his family, charities, and church. The other left bills to be paid. Both men offered me advice, but they did not advise the same things. Both men believed strongly in education but did not recommend the same course of study. If I had had only one dad, I would have had to accept or reject his advice. Having two dads offered me the choice of contrasting points of view: one of a rich man and one of a poor man. Instead of simply accepting or rejecting one or the other, I found myself thinking more, comparing, and then choosing for myself. The problem was that the rich man was not rich yet, and the poor man was not yet poor. Both were just starting out on their careers, and both were struggling with money and families. But they had very different points of view about money. At the age of nine, I chose not to listen to my poor dad, even though he was the one with all the college degrees. I decided to listen to and learn from my rich dad about money. In other words, I chose to be rich. The lessons that I learned from him are the lessons that I share with you now. When we are young, choices are generally made for us. As we grow and mature, we learn to make our own choices, a slow, steady process fraught with both joy and frustration. Now it s time to make one of the most critical decisions of your life whether to take control of your finances. Why critical? Because if you take control of your finances, it will empower you to shape a new life for yourself. This choice is really a series of smaller decisions. The decision to change your financial future is a mere preliminary. The decision to follow up, renewed each day you open your eyes, is the more critical choice. Will you see your choice through to the end? 1

4 What follows is a hands-on, step-by-step program designed to help set you free. You ll begin with a general assessment, filling out your own personal financial statement to determine where you are. After completing this checkup, you ll set new and exciting goals for yourself and tend to your bottom line getting out of debt and cutting costs. Once you take control of your cash flow, you ll be ready to use your mind and your money to invest in the future. Whatever you decide to do become a savvy investor, open your own business, or use the businesses you own as the ultimate investment vehicles by the time you ve completed this book, you will have left the Rat Race behind, or at least be well prepared to take that giant step toward freedom. Go at your own pace. And most important, don t give up. Whenever fear or doubt blocks your path, circle around these obstacles and continue on. You ll find that with every step you take, your confidence grows along with your assets. Remember, the reward is not only the freedom that money buys, but also the confidence you gain in yourself for they are really one and the same. You ve made the choice to seek financial freedom. You ve begun the financial education that will help you on your path. Now we ll create your financial plan. 2

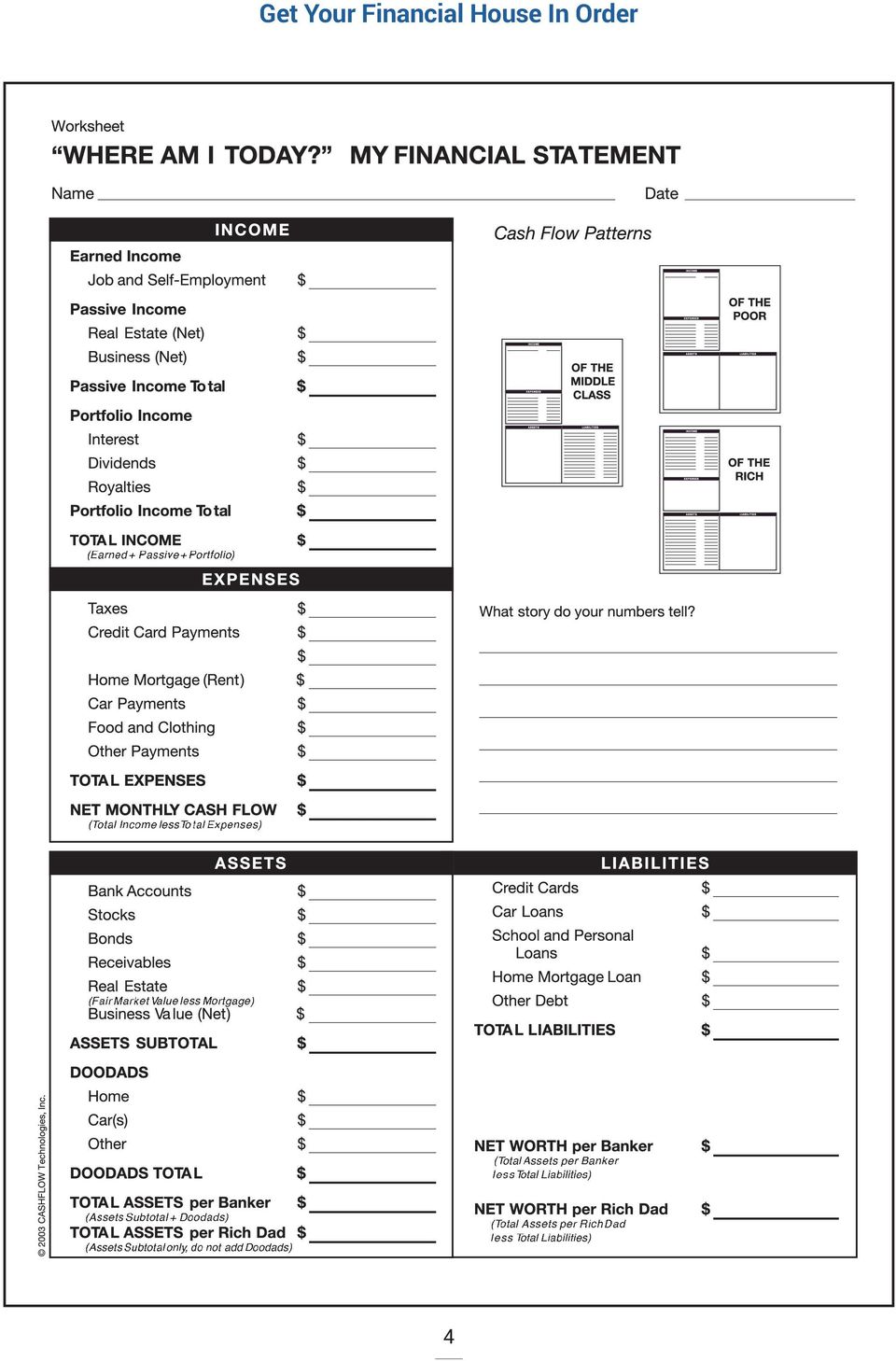

5 1 Where Are You? By now you re probably asking, Where do I begin? You may also be a little intimidated. Know this: You re not alone. Anyone who s ever dared dream of financial freedom and then taken the steps to achieve it has felt the same way at first. Don t lose heart. If the rich can do it, then with determination and a sound plan, you can too. To reach your financial goal, the first thing you must do is figure out where you are. For if you don t know where you are, you can t expect to get where you want to go. Knowing where you are means taking an honest inventory of your financial situation filling out a financial statement and taking a good hard look at the results. This may sound difficult, and maybe even a bit scary, but it s a simple process. And if you make up your mind to do it, you ll be amazed at what you can learn about yourself. Preparing a Financial Statement Numbers are like words. Put them together, and they tell a story. When you fill out your financial statement, the story the numbers tell will be about you about where you ve been, where you are right now, and how to get where you want to go. The exercise that follows is not intended to make you feel guilty for having mishandled your money in the past. It s not about things you can t change. It s about charting a course for your future. To track your flow of cash, you ll need to record all your income and assets and all your expenses and liabilities using the following financial statement worksheet. This is the tool you ll use to record the details of your financial story. You ll be filling out this sheet gradually, as you go through the process of gathering your records. The sections below will walk you through this process. 3

6 4

7 2 Income and Assets Income can be ordinary earned, passive, or portfolio. You work for ordinary earned income. Assets that you own generate passive and portfolio income. In your banker s version of a financial statement, assets also include doodads. In Rich Dad s version, assets don t include doodads. Doodads are things you once probably thought of as assets. According to Rich Dad, because doodads take money out of your pocket, they aren t true assets. Ordinary Earned Income Ordinary earned income is what you earn when you work for your money. It s income you re paid for doing a job as an employee, or income you receive as a self-employed person. Job income, or the salary you earn as an employee, is reported by your employer at the end of each year on a W-2 form. Start with your paycheck. Determine whether you re paid weekly, bi-weekly, twice a month, or monthly. Fill in your monthly gross income. Gross income is the amount received before any deductions are made for taxes or other purposes. Net income is the actual amount of your paycheck after all deductions. For your purposes here, assume a four-week month. Then calculate your monthly income in one of the following ways, and enter the figure on your financial statement next to Job and Self-Employment. (If you re self-employed, continue reading.) Self-employment income is the income you make working for yourself, whether as a sole proprietor or in a partnership, corporation, or limited- liability company. Remember, this is income you receive only when you work. It is not income you receive from your business working for you, which would belong under Business (Net) (see below). To calculate your total earned income, look at the receipts for bills you ve submitted to customers or clients over the past month. Is this a typical month for your business? If not, 5

8 it may be better to add up four months of receipts, then divide by four. (Or better yet, add up a whole year s worth of receipts and divide by 12). An average of your monthly receipts will more accurately reflect the income you record on your financial statement. Log in the monthly average next to Job and Self-Employment on your financial statement. 6

9 3 Passive Income and Assets Passive Income Passive Income is income you ve earned from any asset you own, such as a real estate investment or a business. For your personal financial statement, you need to review each real estate investment property and/or business separately. As laid out below, you ll be calculating all income received from each asset, deducting all expenses related to each, then adding together net income (or net loss) for all real estate assets or all business assets and entering the total in the appropriate section of your financial statement. Real Estate Income is what you earn from a rental property. You ll see this listed on your financial statement in the Income section as Real Estate (Net). Net means the income you have left over once total expenses for the property are deducted. Real estate that is, the property itself can also be an asset. When determining the value of your real estate for the Assets section of your financial statement, you ll need to be honest with yourself and enter the property s fair market value, that is, the amount for which you could sell it today. Fill in the information below for each property you own to ascertain the current value of your asset. Fair market value of property $ Current balance of mortgage Net value of property $ Enter the net value of the property next to Real Estate in the Assets section of your financial statement. If you have more than one property, total the separate values and enter that figure. Business Income is the income you receive from businesses in which you own an interest, whether they are partnerships, limited partnerships, corporations, or LLCs. This is not the self-employment income you listed under Earned Income. This is income you receive from your business working 7

10 for you. You ll see this as Business (Net) in the Income section of your financial statement. Again, net refers to the income you receive once all expenses have been deducted. Enter net business income next to Business (Net) in the Income section of your financial statement. If you have more than one business, add the net income figures and enter the total. A business can also be an asset. When determining the value of your business (or an investment you ve made in a business) for the Assets section of your financial statement, you ll have to ask yourself, in all honesty, how much the business could be sold for today. To determine the value of your business asset, fill out the information below, repeating the exercise for each business you own or are invested in. Current Value of Business How much could you sell it for today? $ Current mortgage balance or business liability Net business value $ It s possible that your net business value is a negative amount. Record the value, whether positive or negative, next to Business Value (Net) in the Assets section of your financial statement. 8

for the Assets section of your financial statement, you ll have to ask yourself, in all honesty, how much the")

11 4 Portfolio Portfolio Income Portfolio income consists of interest and dividends derived from investments such as paper assets and royalties from products or services you create. Interest and Dividends are income you earn on investments as reported at year s end on IRS form To determine your total interest and dividends, look at the statements you ve gathered for all accounts for example, from brokers, mutual funds, companies in which you own stock, and banks. Review your tax returns from the past three years to make sure you ve included all accounts, and make sure you add any statements of receivables, that is, money that people owe you. Then for each account, list the monthly income or average monthly income, whether in the form of interest or dividends. Add together all monthly interest figures and log in that total next to Interest in the Income section of your financial statement. Then total all dividend figures and enter that number right below, next to Dividends. Now move to the Assets section of your financial statement. List the current (month s end) balance for each bank account you have for example, checking, savings, and money-market funds. Add together all the bank account balances. Next to Bank Accounts in the Assets section of your financial statement, record the total. For each stock or mutual fund you own, list the market value at month s end. Add together all the stock and mutual fund values. Then enter the total next to Stocks in the Assets section of your financial statement. For each type of bond you own, record the market value at month s end. Income Add together all bond values. Then enter the total number next to Bonds in the Assets section 9

12 of your financial statement. Now move down to Receivables in the Assets section. A receivable is money owed to you, usually in the form of an IOU or a note receivable. There may be an amortization schedule that identifies the value of the note at any given time. For each receivable, record the most accurate balance of the amount owed to you. Total all your receivable balances. Then enter the total number next to Receivables in the Asset section of your financial statement. Royalties are classified as portfolio income by the IRS. Royalties are any income earned from intellectual property that you own or you ve created. The income is usually generated from the sale or license of patents, copyrights, books, CDs, or oil and gas properties. For each type of royalty-producing property you own, fill out the following: Record the royalty amount, or the total of all royalties, next to Royalties in the Income section of your financial statement. Having filled out your entire Income section, you can enter your Total Income on the appropriate line there. You ve also filled out the first half of your Assets section. Subtotal your assets and enter the number on the appropriate line. 10

13 5 Expenses and Liabilities You ll recall that expenses are not the same as liabilities. The typical monthly amount you pay on a liability is your expense related to that liability. Expenses include monthly payments you make for things such as utilities and food. (Keep in mind that the term expense, for our purposes, includes principal payment along with interest.) Hence you ll be filling out separate Expenses and Liabilities sections. Review several months worth of all your bills, including bills for credit cards and for doodads like your car and home. If you re employed, review the deductions on your paycheck. If you re self-employed, estimate how much you pay for such things as taxes and insurance. Whatever your situation, select the month that represents your typical expenses. Basically, you ll be recording each monthly expense in the Expenses section of your financial sheet, and recording the related balance due in the Liabilities section. Doodads This brings you to Doodads in the Assets section of your financial statement. As you well know by now, doodads are things you once probably thought of as assets. According to Rich Dad, because doodads take money out of your pocket, they aren t true assets. Below, record the current value of each doodad you own that is, the value if you were able to sell it today. Home Personal car(s) Jewelry Furniture Sports equipment Other personal belongings $ $ $ $ $ $ Enter the value of your home and of your car on the appropriate lines in the Assets section. Add together the values of all other doodads (jewelry, furniture, other) and enter the total next to Other in the same section. 11

14 Now that you have your Assets subtotal and your Doodads total, you can figure out your Total Assets. Note that there are separate versions for total assets, a banker version and a Rich Dad version. This is a reflection of the different approach bankers and Rich Dad take toward doodads. To calculate the banker version of total assets, add your assets subtotal and your doodads total and enter the figure on the appropriate line. To calculate Rich Dad s version, enter only your assets subtotal next to Total Assets per Rich Dad. Taxes (and other paycheck deductions) Look at your paycheck. In the following worksheet, enter the amount you re paying monthly for any items that relate to your situation. (Again, if you re self-employed, you ll have to estimate the amount of taxes you pay monthly.) Federal income taxes State income taxes Social Security taxes (FICA) Unemployment taxes (FUTA and state unemployment taxes) Medicare deductions Medical insurance Life insurance Childcare Other deductions (list by type) Now, add all your monthly taxes and enter the total next to Taxes in the Expenses section of your financial statement. Since employees have their taxes withheld before they get paid, there should be no additional balance due, or liability, on their wage income. However, if you are self- employed and make quarterly estimated-income tax payments to the IRS and your state, make sure you include balances due next to Other Debt in the Liabilities section of your statement. Credit Cards For each credit card, fill in the amount you typically pay each month and add them together. Enter the monthly payment, or the total of all monthly payments, next to Credit Card Payments in the Expenses section of your statement. Now fill in the total remaining balance due at month s end for each credit card. Record this balance, or the total of all balances, next to Credit Cards in the Liability section of your financial statement. 12

Look at your paycheck.")

15 Home Mortgage List the monthly payment for each mortgage you hold, and for each equity line of credit or other home loan. List your monthly rent or other fees if you don t own your dwelling. For each mortgage, include the total amount of payment, including amounts for insurance, real estate taxes, and other fees, even if these are paid separately. Home mortgage monthly payment Equity line of credit monthly payment Other home loan monthly payment Add these numbers together and enter the total next to Home Mortgage in the Expenses section of your financial statement. Then list the balance you owe on each. Home mortgage balance Equity line of credit balance Other home loan balance $ $ $ Total the balances and enter the figure next to Home Mortgage Loan in the Liabilities section of your financial statement. Cars For each car you own, fill in your monthly payment next to Car Payments in the Expenses section of your financial statement. Now record the balance remaining for each car you own next to Car Loans in the Liabilities section. Other Payments, School and Personal Loans Calculate the amount you spend on a monthly basis for food and clothing, and enter the total on your financial statement. Fill in the monthly payment for each school or personal loan you re paying off. Take this figure, or the total of all school and personal loan payment figures, and add it to any other average monthly expenses you have remaining (that is, anything other than taxes, credit cards, home loans, and car payments, which you ve already noted). Remaining monthly expenses might include, for example, utility payments or travel and entertainment. Review your checkbook carefully for any regular payments you may have missed. Include any other deductions from your paycheck that would be considered expenses, such as insurance or childcare. Review your tax returns to make sure you ve included expenses for items you may have deducted in earlier years but overlooked now. 13

16 Enter the new total next to Other Payments in the Expenses section of your financial statement. Now you can add up all your expenses in the Expenses section and enter the total figure next to Total Expenses. Next list the balance remaining for each school or personal loan for which you ve included a monthly payment. Enter this figure, or the total of all such loan balances, next to School and Personal Loans in the Liabilities section of your financial statement. Other Debt Now that you ve completed your Expenses section, turn your attention to the remainder of the Liabilities section. For any additional debt you have, over and above what you ve already included, record the total balance due as a liability. For instance, perhaps you owe money to your parents but aren t currently making payments. The total balance you owe them should be listed as a liability, even though you aren t making payments and therefore have no related expense for that liability. Below, fill in the balance due on each of your additional debts. Additional debt balance $ Enter the balance due on each of your additional debts next to Other Debt in the Liabilities section of your financial statement. Now add up all the liabilities listed in this section and enter the figure next to Total Liabilities. 14

17 6 Net Remember, Rich Dad wouldn t consider your home, car, furniture, clothes, collectibles, or other personal property to be financial assets unless they put money in your pocket. If they take money out, they re doodads. That s why you ll see two versions of net worth in the Liabilities section of your financial statement: the banker version, which includes doodads, and the Rich Dad version, which excludes doodads. Follow either one of the two equations below, depending on which version you want. Remember, the Rich Dad total is the more truthful reflection of where you are financially. It is how a sophisticated investor would view your financial statement. Total assets (per banker, with doodads) Total liabilities = Net worth (per banker) Total assets (per Rich Dad, no doodads) Total liabilities = Net worth (per Rich Dad) Worth Where Are You? Whew! You ve come a long way. How many people can say they ve created an honest, thorough financial portrait of themselves? You deserve a round of applause. A quick glance at the totals in each section of your financial statement total income, total expenses, total assets, and total liabilities will give you a general idea of where you are financially. As you look at these totals, make sure you also review the cash flow patterns in the upper- righthand side of the statement. Generally speaking, if the money you have coming in as income goes right out as expenses, you ve got the cash flow pattern of the poor. If your income is used to pay expenses and liabilities, then the cash flow pattern of the middle class best describes you. You re bringing in money through ordinary earned income, which pays expenses and buys more liabilities, which you mistake for assets. In either case, poor or middle class, you need to read on and get your financial house in order. 15

18 What if you have more income and assets than expenses and liabilities? Then your Rich Dad net worth is impressive. You re building assets that create passive income, which in turn pays expenses. You re enjoying the cash flow pattern of the rich. Don t let that stop you from reading on. There is probably even more you can do to make your assets grow. Unless you re an ultimate investor, the Rich Dad program can still be of benefit to you. Where to now? In the next section you re going to analyze your financial statement and set new long-term financial goals for yourself. In this step you ll be analyzing the results of your financial statement. This will give you a clearer idea of exactly where you stand in the cash flow patterns of the poor, middle class, or rich and provide a starting point for setting your new goals. But before you do that, you ll meet certain fictional people and find out all about their financial situations. You ll see how people in different quadrants set different goals and use different strategies to reach those goals with varying degrees of success. Once you finish reading, you ll have a better idea how to get yourself from the life you re in now to the life you want to be in. Please note that wealth is measured in time, not money. You should have your money working for you so you don t have to spend all your time working for money. Analysis of Your Financial Statement Now that you ve prepared your financial statement it s time to do an analysis of your own statement. This will indicate where you are and suggest ways you can set new goals. In this section, you ll see some standard ratios used to analyze financial statements. Not everything will be applicable to your scenario, but some will prove useful in moving you down the path to financial freedom. How Much Do You Keep? Your total monthly income A = Less your total monthly expenses B = Difference is how much you keep C = Percentage of income you are keeping C/A = % Goal: Increase the percentage of income you keep. Start with 1% and increase it from there if you have to. 16

19 Does Your Money Work For You? Your total monthly income A = Your total ordinary earned income B = Your total passive and portfolio income C = What percentage of your income is passive or portfolio, that is, your money working for you? C/A = % Goal: Increase the percentage of income you keep. Start with 1% and increase it from there if you have to. What Is Your Income After Tax? Your total income per month A = Taxes you pay per month B = Your net income per month C = What percentage of your gross income is paid in taxes? B/A = % Goal: Decrease the amount of tax you pay. Consult your tax advisor to see if you are taking full advantage of the tax deductions allowed to you. If you have started a business, make sure you are deducting all legitimate business deductions. How Much of Your Net Income Goes To Housing Each Month? Mortgage payment $ Rent payment $ Insurance (home) $ Real estate taxes $ Utilities $ Maintenance $ Total $ How much do you spend as a percentage of net income? Total / C (net income) = % Goal: Keep housing costs under 33 percent of net income. 17

20 How Much Do You Spend On Doodads? Doodads aren t necessarily bad things. They re the reward for a job well done. Unfortunately, many people reward themselves first and never get around to building assets. The following figures will help identify your doodad habits. Note that Total assets carries the tag banker version. You ll recall that there is a fundamental difference between how Rich Dad calculates assets and thus net worth and how a banker does. Rich Dad defines an asset as something that puts money in your pocket. Thus, for example, your personal residence is not an asset. But when it comes time to do your personal financial statement for your banker, he or she will count your personal residence, if you have one, as an asset. Total doodad amount Total assets (banker version) Doodad percentage of total assets % (doodad total / total assets) Goal: Keep your doodads under 33 percent of total assets. The lower the percentage, the faster your assets will grow. What Is Your Return On Assets? One way to increase your passive income is to reallocate your invested assets. This ratio will tell you overall how you are doing. If the return is low, you can look at where the assets are and decide whether you want to reinvest them. You may want to liquidate some of your doodads and invest that amount in assets to help you get started. Total assets (Rich Dad version) A = $ Total passive and portfolio income B = $ x12 = $ Cash-on-asset return (Annualized income B / Total assets A) % Goal: Increase your Cash-on-asset return. 18

21 How Wealthy Are You? Total assets (Rich Dad version) Total expenses Your wealth (assets / expenses) Total passive income $ $ months $ Goal: To purchase assets that generate passive and/or portfolio income in excess of your monthly expenses. Note: Once your monthly passive income exceeds your monthly expenses, you re infinitely wealthy because your assets are working for you. 19

22 utro What Is Your Cash Flow Pattern? The numbers you ve come up with tell a story about your cash flow pattern. Which of the stories below best describes you? Poor If you have the cash flow pattern of the poor, you re using ordinary earned income to pay expenses. There are no assets, no passive income, and no liabilities. You could own lots of things and owe nothing on them. But if, in addition to having no debt, you have no passive income or assets, your cash flow pattern is that of the poor. Middle class If you have the cash flow pattern of the middle class, you re bringing in money primarily through ordinary earned income, which goes to paying expenses and building more liabilities, creating more expenses. If this is your pattern, you re rewarding yourself with doodads and building liabilities. This is the toughest pattern to change. Your cash flow is building more and more debt. Rich The cash flow pattern of the rich is to build assets that create passive income, which in turn pays expenses. The term rich here refers to the cash flow pattern only. What counts isn t whether someone makes $5,000 per month or $500,000 per month. What counts is whether that person s assets pay his or her expenses, with additional cash going each month to build assets. That is the cash flow pattern of the rich. (Someone who makes $50,000 per month might still have the cash flow pattern of the middle class.) It is not the amount you have, but what you do with it that counts.

23 Having studied this program, you ve received a financial education that can help you change your approach to money as well as to life. This is my way of giving back, of teaching those who don t have a rich dad how the world of money works. Day in and day out, you can choose to be rich. You now know how to draft a financial plan to be secure, to be comfortable, and to be rich. And you also now know that financial literacy and self-confidence will help you achieve your long-range goals. I hope that you ve also learned more about yourself about your attitude towards money, your avoidance of change, and your tolerance of risk. For when you get right down to it, Rich Dad s program is less about changing the mix of assets in your portfolio than changing the mixed-up ideas about security that keep you living from paycheck to paycheck. I ve said it before, and I ll say it again: The old advice, Get a good education so you can get a good job and be secure for life, is obsolete in the Information Age. Whether you like it or not, the clock can t be turned back to the old Industrial Age. The sooner you learn financial skills for the new age, the sooner you ll take control of your life. I ve spent a lifetime learning these lessons. But while it s important to proceed at your own pace, don t use learning as an excuse to procrastinate. The best teacher of all is experience. Don t be afraid to make mistakes. Make a mistake, learn from it, and go out and try again. You ll never master a financial skill or strategy until you ve actually put it to use. If the only change you make is to think twice about buying assets instead of doodads, you ll gain more control of your cash flow and thereby increase your financial options. If you can do that much, you know you can do much more. Go ahead, seize the opportunities out there! Robert Kiyosaki 21

24 It s Time to Get Out of the Rat Race! N. Civic Center Plaza Suite 100 Scottsdale, AZ USA tel fax info@richdad.com CASHFLOW Technologies, Inc. All rights reserved. CASHFLOW may not be used for commercial purposes without prior written approval from CASHFLOW Technologies, Inc.

Whole Life Insurance is not A Retirement Plan

Whole Life Insurance is not A Retirement Plan By Kyle J Christensen, CFP I decided to write this article because over the years I have had several clients forget how their whole life insurance fits in

Whole Life Insurance is not A Retirement Plan By Kyle J Christensen, CFP I decided to write this article because over the years I have had several clients forget how their whole life insurance fits in

Effective Strategies for Personal Money Management

Effective Strategies for Personal Money Management The key to successful money management is developing and following a personal financial plan. Research has shown that people with a financial plan tend

Effective Strategies for Personal Money Management The key to successful money management is developing and following a personal financial plan. Research has shown that people with a financial plan tend

1Planning Your Financial Future: It Begins Here

This sample chapter is for review purposes only. Copyright The Goodheart-Willcox Co., Inc. All rights reserved. 1Planning Your Financial Future: It Begins Here Terms Financial plan Financial goals Needs

This sample chapter is for review purposes only. Copyright The Goodheart-Willcox Co., Inc. All rights reserved. 1Planning Your Financial Future: It Begins Here Terms Financial plan Financial goals Needs

THEME: UNDERSTANDING EQUITY ACCOUNTS

THEME: UNDERSTANDING EQUITY ACCOUNTS By John W. Day, MBA ACCOUNTING TERM: Equity Equity is the difference between assets and liabilities as shown on a balance sheet. In other words, equity represents the

THEME: UNDERSTANDING EQUITY ACCOUNTS By John W. Day, MBA ACCOUNTING TERM: Equity Equity is the difference between assets and liabilities as shown on a balance sheet. In other words, equity represents the

Financial Freedom: Three Steps to Creating and Enjoying the Wealth You Deserve

Financial Freedom: Three Steps to Creating and Enjoying the Wealth You Deserve What does financial freedom mean to you? Does it mean freedom from having to work, yet still being able to enjoy life without

Financial Freedom: Three Steps to Creating and Enjoying the Wealth You Deserve What does financial freedom mean to you? Does it mean freedom from having to work, yet still being able to enjoy life without

1. Overconfidence {health care discussion at JD s} 2. Biased Judgments. 3. Herding. 4. Loss Aversion

In conditions of laissez-faire the avoidance of wide fluctuations in employment may, therefore, prove impossible without a far-reaching change in the psychology of investment markets such as there is no

In conditions of laissez-faire the avoidance of wide fluctuations in employment may, therefore, prove impossible without a far-reaching change in the psychology of investment markets such as there is no

What do other high school students know about investing?

Investment Options What do other high school students know about investing? We asked high school students to describe the weirdest get rich quick scheme they ve ever heard of. Someone told me that I could

Investment Options What do other high school students know about investing? We asked high school students to describe the weirdest get rich quick scheme they ve ever heard of. Someone told me that I could

Double-Entry Bookkeeping: Assets and Liabilities

Double-Entry Bookkeeping: Assets and Liabilities The purpose of this chapter is to introduce the fundamentals of double-entry bookkeeping and its role in accounting for business. The objectives of accounting

Double-Entry Bookkeeping: Assets and Liabilities The purpose of this chapter is to introduce the fundamentals of double-entry bookkeeping and its role in accounting for business. The objectives of accounting

Understanding Financial Statements. For Your Business

Understanding Financial Statements For Your Business Disclaimer The information provided is for informational purposes only, does not constitute legal advice or create an attorney-client relationship,

Understanding Financial Statements For Your Business Disclaimer The information provided is for informational purposes only, does not constitute legal advice or create an attorney-client relationship,

Unit 4: Taxes. Read this unit including websites. You may want to take your own notes.

Taxes Read Chapter 4 in the text. Read Chapter 7 of The Financial Checkup. Read this unit including websites. You may want to take your own notes. Are taxes your favorite topic? They are not the favorite

Taxes Read Chapter 4 in the text. Read Chapter 7 of The Financial Checkup. Read this unit including websites. You may want to take your own notes. Are taxes your favorite topic? They are not the favorite

Awaken Your Financial Genius

Awaken Your Financial Genius Rules of the Game The More You Play this Game the Richer You Become MONEY IS NOT THE MOST IMPORTANT THING IN LIFE but it does seem to affect everything that is important. THE

Awaken Your Financial Genius Rules of the Game The More You Play this Game the Richer You Become MONEY IS NOT THE MOST IMPORTANT THING IN LIFE but it does seem to affect everything that is important. THE

Chapter 1 The Financial Assessment

Chapter 1 The Financial Assessment 64 P leasant S treet P hon e: ( 415) 830-52 44 Copyright 2007-2009 Harrison Lazarus Advisors, Inc. All Rights Reserved Page 1 of 15 It doesn t matter where you are in

Chapter 1 The Financial Assessment 64 P leasant S treet P hon e: ( 415) 830-52 44 Copyright 2007-2009 Harrison Lazarus Advisors, Inc. All Rights Reserved Page 1 of 15 It doesn t matter where you are in

What is a business plan?

What is a business plan? A business plan is the presentation of an idea for a new business. When a person (or group) is planning to open a business, there is a great deal of research that must be done

What is a business plan? A business plan is the presentation of an idea for a new business. When a person (or group) is planning to open a business, there is a great deal of research that must be done

the Personal Finance Kit

the Personal Finance Kit The Practical Financial Management Resource Guide toussaint gaskins This publication is designed to provide accurate and authoritative information in regard to the subject matter

the Personal Finance Kit The Practical Financial Management Resource Guide toussaint gaskins This publication is designed to provide accurate and authoritative information in regard to the subject matter

Accounts Payable are the total amounts your business owes its suppliers for goods and services purchased.

Accounts Payable are the total amounts your business owes its suppliers for goods and services purchased. Accounts Receivable are the total amounts customers owe your business for goods or services sold

Accounts Payable are the total amounts your business owes its suppliers for goods and services purchased. Accounts Receivable are the total amounts customers owe your business for goods or services sold

7 Things You MUST DO To Create Financial Certainty. AllianceGroupFinancial.com 801-545-9494

7 Things You MUST DO To Create Financial Certainty AllianceGroupFinancial.com 801-545-9494 1 In This Report Are you rolling the dice with your retirement? Page 3 What is financial certainty? Page 4 Reaching

7 Things You MUST DO To Create Financial Certainty AllianceGroupFinancial.com 801-545-9494 1 In This Report Are you rolling the dice with your retirement? Page 3 What is financial certainty? Page 4 Reaching

RETIREMENT ACCOUNTS (c) Gary R. Evans, 2006-2011, September 24, 2011. Alternative Retirement Financial Plans and Their Features

Gary R. Evans, 2006-2011, September 24, 2011. Alternative Retirement Financial Plans and Their Features") RETIREMENT ACCOUNTS (c) Gary R. Evans, 2006-2011, September 24, 2011. The various retirement investment accounts discussed in this document all offer the potential for healthy longterm returns with substantial

RETIREMENT ACCOUNTS (c) Gary R. Evans, 2006-2011, September 24, 2011. The various retirement investment accounts discussed in this document all offer the potential for healthy longterm returns with substantial

We respect your privacy and will not disclose this information to any outside parties without your expressed written consent.

CLIENT INTAKE FORM Date: Complete this form prior to your appointment. Please print clearly. If you are unsure of any information, leave it blank. It is okay to approximate amounts and include attachments

CLIENT INTAKE FORM Date: Complete this form prior to your appointment. Please print clearly. If you are unsure of any information, leave it blank. It is okay to approximate amounts and include attachments

Tax Planning and Reporting for a Small Business

Table of Contents Welcome... 3 What Do You Know? Tax Planning and Reporting for a Small Business... 4 Pre-Test... 5 Tax Obligation Management... 6 Business Taxes... 6 Federal Income Tax Forms... 7 Discussion

Table of Contents Welcome... 3 What Do You Know? Tax Planning and Reporting for a Small Business... 4 Pre-Test... 5 Tax Obligation Management... 6 Business Taxes... 6 Federal Income Tax Forms... 7 Discussion

Accounting Basics. (Explanation)

") Accounting Basics (Explanation) Your AccountingCoach PRO membership includes lifetime access to all of our materials. Take a quick tour by visiting www.accountingcoach.com/quicktour. Introduction to Accounting

Accounting Basics (Explanation) Your AccountingCoach PRO membership includes lifetime access to all of our materials. Take a quick tour by visiting www.accountingcoach.com/quicktour. Introduction to Accounting

What does student success mean to you?

What does student success mean to you? Student success to me means to graduate with a B average with no failing grades. Ferris is ridicules tuition rates don t affect me since I was fortunate enough to

What does student success mean to you? Student success to me means to graduate with a B average with no failing grades. Ferris is ridicules tuition rates don t affect me since I was fortunate enough to

Creating a Personal Financial Plan

Creating a Personal Financial Plan Overview Setting goals are important and often used to measure success. However, simply setting goals does not ensure you will someday accomplish them. Achieving goals

Creating a Personal Financial Plan Overview Setting goals are important and often used to measure success. However, simply setting goals does not ensure you will someday accomplish them. Achieving goals

How to Use Your Retirement Funds to Finance Your Small Business with No Taxes or Penalties. How To Use Your Retirement Funds to Finance Your Business

How To Use Your Retirement Funds to Finance Your Business By Bill Seagraves, President January 25, 2009 TABLE OF CONTENTS Overview Succeed in Business and Retire Wealthy: It s All About Cash Flow The Rich

How To Use Your Retirement Funds to Finance Your Business By Bill Seagraves, President January 25, 2009 TABLE OF CONTENTS Overview Succeed in Business and Retire Wealthy: It s All About Cash Flow The Rich

THE ABC S OF VEHICLE FINANCING CURRICULUM. Counting Your Money

Counting Your Money Section Objectives Counting your money and managing your money wisely is the most important part of your trip on the road to personal financial success. It is a critical step in achieving

Counting Your Money Section Objectives Counting your money and managing your money wisely is the most important part of your trip on the road to personal financial success. It is a critical step in achieving

A financial statement captures a person s overall wealth at a specific point in time. In this lesson, students will:

PROJECT 3 CASH FLOW AND BALANCE SHEETS INSTRUCTOR OVERVIEW Financial statements are compilations of personal financial data that describe an individual s current financial condition. Financial statements

PROJECT 3 CASH FLOW AND BALANCE SHEETS INSTRUCTOR OVERVIEW Financial statements are compilations of personal financial data that describe an individual s current financial condition. Financial statements

A financial statement captures a person s overall wealth at a specific point in time. In this lesson, students will:

PROJECT 3 CASH FLOW AND BALANC E SHEETS INSTRUCTOR OVERVIEW Financial statements are compilations of personal financial data that describe an individual s current financial condition. Financial statements

PROJECT 3 CASH FLOW AND BALANC E SHEETS INSTRUCTOR OVERVIEW Financial statements are compilations of personal financial data that describe an individual s current financial condition. Financial statements

1 Tools for Financial Planning

PART 1 Tools for Financial Planning Chapter 2 Planning with Personal Financial Statements How to increase net cash flows in the near future How to increase net cash flows in the distant future Chapter

PART 1 Tools for Financial Planning Chapter 2 Planning with Personal Financial Statements How to increase net cash flows in the near future How to increase net cash flows in the distant future Chapter

UNDERSTANDING WHERE YOU STAND. A Simple Guide to Your Company s Financial Statements

UNDERSTANDING WHERE YOU STAND A Simple Guide to Your Company s Financial Statements Contents INTRODUCTION One statement cannot diagnose your company s financial health. Put several statements together

UNDERSTANDING WHERE YOU STAND A Simple Guide to Your Company s Financial Statements Contents INTRODUCTION One statement cannot diagnose your company s financial health. Put several statements together

How to Avoid The Five Biggest First-time Homebuyer Mistakes. Mistake #1

How to Avoid The Five Biggest First-time Homebuyer Mistakes Mistake #1 Failure To Examine And Repair Any Credit Problems Prior To Applying For Your Loan Many potential new home buyers have no idea what

How to Avoid The Five Biggest First-time Homebuyer Mistakes Mistake #1 Failure To Examine And Repair Any Credit Problems Prior To Applying For Your Loan Many potential new home buyers have no idea what

Gr. 6-12 English Language arts Standards, Literacy in History/Social Studies and Technical Studies

Credit Lesson Description Concepts In this lesson, students, through a series of interactive and group activities, will explore the concept of credit and the impact of liabilities on an individual s net

Credit Lesson Description Concepts In this lesson, students, through a series of interactive and group activities, will explore the concept of credit and the impact of liabilities on an individual s net

OBJECTIVES. The BIG Idea MONEY MATTERS. How much will it cost to buy, operate, and insure a car? Paying for a Car

Paying for a Car 4 MONEY MATTERS The BIG Idea How much will it cost to buy, operate, and insure a car? AGENDA Approx. 45 minutes I. Warm Up (5 minutes) II. What Can You Spend? (15 minutes) III. Getting

Paying for a Car 4 MONEY MATTERS The BIG Idea How much will it cost to buy, operate, and insure a car? AGENDA Approx. 45 minutes I. Warm Up (5 minutes) II. What Can You Spend? (15 minutes) III. Getting

Using Credit to Your Advantage.

Using Credit to Your Advantage. Topic Overview. The Using Credit To Your Advantage topic will provide participants with all the basic information they need to understand credit what it is and how to make

Using Credit to Your Advantage. Topic Overview. The Using Credit To Your Advantage topic will provide participants with all the basic information they need to understand credit what it is and how to make

NOLO. Nolo s Guide to Limited Liability Companies: Forming an LLC

NOLO Nolo s Guide to Limited Liability Companies: Forming an LLC Table of Contents LLC Basics...3 Limited Personal Liability for LLC Owners...3 Exceptions to LLC Owners Limited Liability...4 LLC Management...4

NOLO Nolo s Guide to Limited Liability Companies: Forming an LLC Table of Contents LLC Basics...3 Limited Personal Liability for LLC Owners...3 Exceptions to LLC Owners Limited Liability...4 LLC Management...4

Retirement: Get Ready...1 Why planning makes sense...1 Where are you?...2 Getting Started: 20 s and early 30 s...3

Retirement: Get Ready...1 Why planning makes sense...1 Where are you?...2 Getting Started: 20 s and early 30 s...3 On Your Way: Mid-30 s to early 40 s...4 Crunch Time: Mid-40 s to early 50 s...5 Just Around

Retirement: Get Ready...1 Why planning makes sense...1 Where are you?...2 Getting Started: 20 s and early 30 s...3 On Your Way: Mid-30 s to early 40 s...4 Crunch Time: Mid-40 s to early 50 s...5 Just Around

A Beginner s Guide to Financial Freedom through the Stock-market. Includes The 6 Steps to Successful Investing

A Beginner s Guide to Financial Freedom through the Stock-market Includes The 6 Steps to Successful Investing By Marcus de Maria The experts at teaching beginners how to make money in stocks Web-site:

A Beginner s Guide to Financial Freedom through the Stock-market Includes The 6 Steps to Successful Investing By Marcus de Maria The experts at teaching beginners how to make money in stocks Web-site:

Money Math for Teens. Dividend-Paying Stocks

Money Math for Teens Dividend-Paying Stocks This Money Math for Teens lesson is part of a series created by Generation Money, a multimedia financial literacy initiative of the FINRA Investor Education

Money Math for Teens Dividend-Paying Stocks This Money Math for Teens lesson is part of a series created by Generation Money, a multimedia financial literacy initiative of the FINRA Investor Education

Chapter Review Problems

Chapter Review Problems Unit 17.1 Income statements 1. When revenues exceed expenses, is the result (a) net income or (b) net loss? (a) net income 2. Do income statements reflect profits of a business

Chapter Review Problems Unit 17.1 Income statements 1. When revenues exceed expenses, is the result (a) net income or (b) net loss? (a) net income 2. Do income statements reflect profits of a business

Alternative Retirement Financial Plans and Their Features

RETIREMENT ACCOUNTS Gary R. Evans, 2006-2013, November 20, 2013. The various retirement investment accounts discussed in this document all offer the potential for healthy longterm returns with substantial

RETIREMENT ACCOUNTS Gary R. Evans, 2006-2013, November 20, 2013. The various retirement investment accounts discussed in this document all offer the potential for healthy longterm returns with substantial

JPMorgan INVEST. You work hard for your money. Now keep it working for you with a JPMorgan Invest IRA. IRA Decision Guide

IRA Decision Guide JPMorgan INVEST You work hard for your money. Now keep it working for you with a JPMorgan Invest IRA. JPMorgan Invest One Beacon Street, Boston, MA 0208 (800) 776-606 jpmorganinvest.com

IRA Decision Guide JPMorgan INVEST You work hard for your money. Now keep it working for you with a JPMorgan Invest IRA. JPMorgan Invest One Beacon Street, Boston, MA 0208 (800) 776-606 jpmorganinvest.com

MODULE 6 Financial Statements

Introduction. 102 Projected Outcomes 103 Facilitators Notes. 104 What is Accounting. 104 The Accounting Equation.. 105 Accounting Terminology 106 Assets 106 Liabilities. 106 Owner s Equity, Partner s Equity,

Introduction. 102 Projected Outcomes 103 Facilitators Notes. 104 What is Accounting. 104 The Accounting Equation.. 105 Accounting Terminology 106 Assets 106 Liabilities. 106 Owner s Equity, Partner s Equity,

Registered Investment Advisor Firm

Registered Investment Advisor Firm Issue VI, Vol. III Bud Heng Registered Adviser (925) 360-6819 June 2014 Congratulation Graduates! For the graduating class of 2014, let me be among the first to say congratulations!

Registered Investment Advisor Firm Issue VI, Vol. III Bud Heng Registered Adviser (925) 360-6819 June 2014 Congratulation Graduates! For the graduating class of 2014, let me be among the first to say congratulations!

Ipx!up!hfu!uif Dsfeju!zpv!Eftfswf

Ipx!up!hfu!uif Dsfeju!zpv!Eftfswf Credit is the lifeblood of South Louisiana business, especially for the smaller firm. It helps the small business owner get started, obtain equipment, build inventory,

Ipx!up!hfu!uif Dsfeju!zpv!Eftfswf Credit is the lifeblood of South Louisiana business, especially for the smaller firm. It helps the small business owner get started, obtain equipment, build inventory,

Introduction to Accounting

Introduction to Accounting Text File Slide 1 Introduction to Accounting Welcome to SBA s online training course, Introduction to Accounting. This program is a product of the agency s Small Business Training

Introduction to Accounting Text File Slide 1 Introduction to Accounting Welcome to SBA s online training course, Introduction to Accounting. This program is a product of the agency s Small Business Training

Income Sources Recap Jot down your streams of income, even if it s just a trickle right now.

Income Sources Recap Jot down your streams of income, even if it s just a trickle right now. Money s fun. If you ve got some. You ve got money coming in from somewhere, right? Then write it down. This

Income Sources Recap Jot down your streams of income, even if it s just a trickle right now. Money s fun. If you ve got some. You ve got money coming in from somewhere, right? Then write it down. This

The Basics of Building Credit

The Basics of Building Credit This program was developed to help middle school students learn the basics of building credit. At the end of this lesson, you should know about all of the Key Topics below:»

The Basics of Building Credit This program was developed to help middle school students learn the basics of building credit. At the end of this lesson, you should know about all of the Key Topics below:»

BUILDING YOUR MONEY PYRAMID: FINANCIAL PLANNING CFE 3218V

BUILDING YOUR MONEY PYRAMID: FINANCIAL PLANNING CFE 3218V OPEN CAPTIONED MERIDIAN EDUCATION CORP. 1994 Grade Levels: 10-13+ 14 minutes 1 Instructional Graphic Enclosed DESCRIPTION Most people will earn

BUILDING YOUR MONEY PYRAMID: FINANCIAL PLANNING CFE 3218V OPEN CAPTIONED MERIDIAN EDUCATION CORP. 1994 Grade Levels: 10-13+ 14 minutes 1 Instructional Graphic Enclosed DESCRIPTION Most people will earn

Slide 2. What is Investing?

Slide 1 Investments Investment choices can be overwhelming if you don t do your homework. There s the potential for significant gain, but also the potential for significant loss. In this module, you ll

Slide 1 Investments Investment choices can be overwhelming if you don t do your homework. There s the potential for significant gain, but also the potential for significant loss. In this module, you ll

Retiring from the Family Business Last update: October 27, 2011

Summary Retiring from the Family Business Last update: October 27, 2011 If you are the owner or a major partner in a small business, your retirement concerns are more complex than most people s. It is

Summary Retiring from the Family Business Last update: October 27, 2011 If you are the owner or a major partner in a small business, your retirement concerns are more complex than most people s. It is

Key points to remember when using this template:

Writing a business plan is hard work. One professional estimates it s as hard as writing a novel. To assist you in preparing your plan, we ve prepared the following Business Plan Questionnaire. Please

Writing a business plan is hard work. One professional estimates it s as hard as writing a novel. To assist you in preparing your plan, we ve prepared the following Business Plan Questionnaire. Please

GOT TAX PROBLEMS? THINGS THE IRS DOESN T WANT YOU TO KNOW (BUT YOU WILL LEARN BY READING THIS!)

") GOT TAX PROBLEMS? THINGS THE IRS DOESN T WANT YOU TO KNOW (BUT YOU WILL LEARN BY READING THIS!) When I was a young lawyer, I assumed the Internal Revenue Service was like my father strict and stern, but

GOT TAX PROBLEMS? THINGS THE IRS DOESN T WANT YOU TO KNOW (BUT YOU WILL LEARN BY READING THIS!) When I was a young lawyer, I assumed the Internal Revenue Service was like my father strict and stern, but

Loan Lessons. The Low-Down on Loans, Interest and Keeping Your Head Above Water. Course Objectives Learn About:

usbank.com/student financialgenius.usbank.com Course Objectives Learn About: Different Types of Loans How to Qualify for a Loan Different Types of Interest Loan Lessons The Low-Down on Loans, Interest

usbank.com/student financialgenius.usbank.com Course Objectives Learn About: Different Types of Loans How to Qualify for a Loan Different Types of Interest Loan Lessons The Low-Down on Loans, Interest

What to Do With a Windfall Episode # 511

What to Do With a Windfall Episode # 511 LESSON LEVEL Grades 6-8 Key topics Decision Making Investing Personal Financial Plan Entrepreneurs & Stories LA Sparks WNBA Basketball Candace Layla West Dance

What to Do With a Windfall Episode # 511 LESSON LEVEL Grades 6-8 Key topics Decision Making Investing Personal Financial Plan Entrepreneurs & Stories LA Sparks WNBA Basketball Candace Layla West Dance

EDUCATIONAL BENEFITS GROUP Providing solutions to make college an affordable reality. Cash Flow Planning for College & Retirement

EDUCATIONAL BENEFITS GROUP Providing solutions to make college an affordable reality Cash Flow Planning for College & Retirement Table of Contents Cash Flow Planning for College & Retirement Introduction

EDUCATIONAL BENEFITS GROUP Providing solutions to make college an affordable reality Cash Flow Planning for College & Retirement Table of Contents Cash Flow Planning for College & Retirement Introduction

FINANCIAL STRATEGIES By Charles R. Liberty, CPA

FINANCIAL STRATEGIES By Charles R. Liberty, CPA DON T BE AFRAID TO PAY SOME TAX Tax rates are as low as they have ever been, and possibly as low as they will ever be again. Take advantage of the 15% bracket.

FINANCIAL STRATEGIES By Charles R. Liberty, CPA DON T BE AFRAID TO PAY SOME TAX Tax rates are as low as they have ever been, and possibly as low as they will ever be again. Take advantage of the 15% bracket.

Club Accounts. 2011 Question 6.

Club Accounts. 2011 Question 6. Anyone familiar with Farm Accounts or Service Firms (notes for both topics are back on the webpage you found this on), will have no trouble with Club Accounts. Essentially

Club Accounts. 2011 Question 6. Anyone familiar with Farm Accounts or Service Firms (notes for both topics are back on the webpage you found this on), will have no trouble with Club Accounts. Essentially

Assist. Financial Calculators. Technology Solutions. About Our Financial Calculators. Benefits of Financial Calculators. Getting Answers.

Assist. Financial s Technology Solutions. About Our Financial s. Helping members with their financial planning should be a key function of every credit union s website. At Technology Solutions, we provide

Assist. Financial s Technology Solutions. About Our Financial s. Helping members with their financial planning should be a key function of every credit union s website. At Technology Solutions, we provide

financial One Two Punch Activity...51 You ve Got the Power of Compounding Activity...51 One Two Punch Answer Sheet...53

financial Financial Planning Financial Planning Pre-/Post-Quiz...49 Lesson 1: Building the Future Introduction to Financial Planning...50 One Two Punch Activity...51 You ve Got the Power of Compounding

financial Financial Planning Financial Planning Pre-/Post-Quiz...49 Lesson 1: Building the Future Introduction to Financial Planning...50 One Two Punch Activity...51 You ve Got the Power of Compounding

Synthesis of Financial Planning

P 7A R T Synthesis of Financial Planning 1. Tools for Financial Planning Budgeting (Chapter 2) Planned Savings (Chapter 3) Tax Planning (Chapter 4) 2. Managing Your Liquidity Bank Services (Chapter 5)

P 7A R T Synthesis of Financial Planning 1. Tools for Financial Planning Budgeting (Chapter 2) Planned Savings (Chapter 3) Tax Planning (Chapter 4) 2. Managing Your Liquidity Bank Services (Chapter 5)

Susan & David Example

Personal Financial Analysis for Susan & David Example Asset Advisors Example, LLC A Registered Investment Advisor 2430 NW Professional Drive Corvallis, OR 97330 877-421-9815 www.moneytree.com IMPORTANT:

Personal Financial Analysis for Susan & David Example Asset Advisors Example, LLC A Registered Investment Advisor 2430 NW Professional Drive Corvallis, OR 97330 877-421-9815 www.moneytree.com IMPORTANT:

NAR Frequently Asked Questions Health Insurance Reform

NEW MEDICARE TAX ON UNEARNED NET INVESTMENT INCOME Q-1: Who will be subject to the new taxes imposed in the health legislation? A: A new 3.8% tax will apply to the unearned income of High Income taxpayers.

NEW MEDICARE TAX ON UNEARNED NET INVESTMENT INCOME Q-1: Who will be subject to the new taxes imposed in the health legislation? A: A new 3.8% tax will apply to the unearned income of High Income taxpayers.

Roll over an inherited 401(k), help your children earn a credit for retirement savings and rack up tax savings in the process.

, help your children earn a credit for retirement savings and rack up tax savings in the process.") P a g e 1 Article: Tax Savings for Empty-Nesters Author: Editor Date: April 2013 Source: Kiplinger Roll over an inherited 401(k), help your children earn a credit for retirement savings and rack up tax

P a g e 1 Article: Tax Savings for Empty-Nesters Author: Editor Date: April 2013 Source: Kiplinger Roll over an inherited 401(k), help your children earn a credit for retirement savings and rack up tax

GETTING A BUSINESS LOAN

GETTING A BUSINESS LOAN With few exceptions, most businesses require an influx of cash now and then. Sometimes it is for maintaining growth; sometimes it is for maintaining the status quo. From where does

GETTING A BUSINESS LOAN With few exceptions, most businesses require an influx of cash now and then. Sometimes it is for maintaining growth; sometimes it is for maintaining the status quo. From where does

RETIREMENT PLANNING GUIDE. Getting you on the right track

RETIREMENT PLANNING GUIDE Getting you on the right track Table of Contents Why is a retirement plan important? 2 How much will you need? 4 How can your retirement plan help? 6 Where should you invest?

RETIREMENT PLANNING GUIDE Getting you on the right track Table of Contents Why is a retirement plan important? 2 How much will you need? 4 How can your retirement plan help? 6 Where should you invest?

Loan Lessons. The Low-Down on Loans, Interest and Keeping Your Head Above Water. Course Objectives Learn About:

Loan Lessons Course Objectives Learn About: Different Types of Loans How to Qualify for a Loan Different Types of Interest The Low-Down on Loans, Interest and Keeping Your Head Above Water usbank.com/financialeducation

Loan Lessons Course Objectives Learn About: Different Types of Loans How to Qualify for a Loan Different Types of Interest The Low-Down on Loans, Interest and Keeping Your Head Above Water usbank.com/financialeducation

MANAGING YOUR BUSINESS S CASH FLOW. Managing Your Business s Cash Flow. David Oetken, MBA CPM

MANAGING YOUR BUSINESS S CASH FLOW Managing Your Business s Cash Flow David Oetken, MBA CPM 1 2 Being a successful entrepreneur takes a unique mix of skills and practices. You need to generate exciting

MANAGING YOUR BUSINESS S CASH FLOW Managing Your Business s Cash Flow David Oetken, MBA CPM 1 2 Being a successful entrepreneur takes a unique mix of skills and practices. You need to generate exciting

Unit One: The Basics of Investing

Unit One: The Basics of Investing DISCLAIMER: The information contained in this document is solely for educational purposes. CompareCards.com, owned by Iron Horse Holdings LLC is not a registered investment

Unit One: The Basics of Investing DISCLAIMER: The information contained in this document is solely for educational purposes. CompareCards.com, owned by Iron Horse Holdings LLC is not a registered investment

Materials Lesson Objectives

165 Materials 1. Play money ($2,000 per student) 2. Candy (Different types, 10 per student) 3. Savvy student reward, which is an item perceived by the students to be of greater value than all the candy

165 Materials 1. Play money ($2,000 per student) 2. Candy (Different types, 10 per student) 3. Savvy student reward, which is an item perceived by the students to be of greater value than all the candy

BankFirst Mortgage Services

BankFirst Mortgage Services Thank you for taking the time to educate yourself on your new mortgage loan. We understand that it is a difficult process for new home buyers. We ll be happy to answer any question

BankFirst Mortgage Services Thank you for taking the time to educate yourself on your new mortgage loan. We understand that it is a difficult process for new home buyers. We ll be happy to answer any question

S Corporation vs. LLC in California Here is an overview of the differences between doing business as an S corporation or as an LLC.

S Corporation vs. LLC in California Here is an overview of the differences between doing business as an S corporation or as an LLC. After you have read this article, we can discuss in detail what would

S Corporation vs. LLC in California Here is an overview of the differences between doing business as an S corporation or as an LLC. After you have read this article, we can discuss in detail what would

Financial Statements

Financial Statements The financial information forms the basis of financial planning, analysis & decision making for an organization or an individual. Financial information is needed to predict, compare

Financial Statements The financial information forms the basis of financial planning, analysis & decision making for an organization or an individual. Financial information is needed to predict, compare

TRS PERSONAL FINANCE HOMEWORK: Amounts in Actual column are considered PRE-WORK and must be complete BEFORE the TRS seminar

PERSONAL IN NATURE F.O.U.O. TRS PERSONAL FINANCE HOMEWORK: Amounts in Actual column are considered PRE-WORK and must be complete BEFORE the TRS seminar DATE: Completed budget- due 0730 TUESDAY (Attach

PERSONAL IN NATURE F.O.U.O. TRS PERSONAL FINANCE HOMEWORK: Amounts in Actual column are considered PRE-WORK and must be complete BEFORE the TRS seminar DATE: Completed budget- due 0730 TUESDAY (Attach

account statement a record of transactions in an account at a financial institution, usually provided each month

GLOSSARY GLOSSARY Following are definitions for key words as they are used in the financial life skills resource. They may have different or additional meanings in other contexts. A account an arrangement

GLOSSARY GLOSSARY Following are definitions for key words as they are used in the financial life skills resource. They may have different or additional meanings in other contexts. A account an arrangement

The Nature of Financial Risk and How to Manage It

Offering Complete Wealth Management Services Steve H. Hornstein, Esq., CPA, LL.M., CFP, LPL Financial Advisor Evan Press, LPL Financial Advisor 20335 Ventura Blvd., Suite 203 Woodland Hills, CA 91364 Office:

Offering Complete Wealth Management Services Steve H. Hornstein, Esq., CPA, LL.M., CFP, LPL Financial Advisor Evan Press, LPL Financial Advisor 20335 Ventura Blvd., Suite 203 Woodland Hills, CA 91364 Office:

What Lawyers Don t Tell You The Realities of Record Keeping

What Lawyers Don t Tell You The Realities of Record Keeping Welcome to the Power of Attorney Podcast which is part of our Conversations that Matter Podcasts. My name is Mary Bart, Chair of Caregiving Matters.

What Lawyers Don t Tell You The Realities of Record Keeping Welcome to the Power of Attorney Podcast which is part of our Conversations that Matter Podcasts. My name is Mary Bart, Chair of Caregiving Matters.

Business Planner. Your small business planning guide

Business Planner Your small business planning guide What s Inside the TD Canada Trust Business Planner Glossary...4 Your Business Profile What your business does or intends to do and your competitive advantage

Business Planner Your small business planning guide What s Inside the TD Canada Trust Business Planner Glossary...4 Your Business Profile What your business does or intends to do and your competitive advantage

ABOUT FINANCIAL RATIO ANALYSIS

ABOUT FINANCIAL RATIO ANALYSIS Over the years, a great many financial analysis techniques have developed. They illustrate the relationship between values drawn from the balance sheet and income statement

ABOUT FINANCIAL RATIO ANALYSIS Over the years, a great many financial analysis techniques have developed. They illustrate the relationship between values drawn from the balance sheet and income statement

Guide to Financial Statements Study Guide

Guide to Financial Statements Study Guide Overview (Topic 1) Three major financial statements: The Income Statement The Balance Sheet The Cash Flow Statement Objectives: Explain the underlying equation

Guide to Financial Statements Study Guide Overview (Topic 1) Three major financial statements: The Income Statement The Balance Sheet The Cash Flow Statement Objectives: Explain the underlying equation

IGCSE Business Studies revision notes Finance Neil.elrick@tes.tp.edu.tw

IGCSE FINANCE REVISION NOTES Table of contents Table of contents... 2 SOURCES OF FINANCE... 3 CASH FLOW... 5 HOW TO CALCULATE THE CASH BALANCE... 5 HOW TO WORK OUT THE CASH AVAILABLE TO THE BUSINESS...

IGCSE FINANCE REVISION NOTES Table of contents Table of contents... 2 SOURCES OF FINANCE... 3 CASH FLOW... 5 HOW TO CALCULATE THE CASH BALANCE... 5 HOW TO WORK OUT THE CASH AVAILABLE TO THE BUSINESS...

Planning for the Stages of Retirement

Planning for the Stages of Retirement The Financial Planning Association (FPA ) connects those who need, support and deliver financial planning. We believe that everyone is entitled to objective advice

Planning for the Stages of Retirement The Financial Planning Association (FPA ) connects those who need, support and deliver financial planning. We believe that everyone is entitled to objective advice

5 Secrets to Wealth. Every Woman Needs To Know To Be Financially Free. By Nancy L. Gaines, Founder Women Gaining Wealth, LLC

5 Secrets to Wealth Every Woman Needs To Know To Be Financially Free By Nancy L. Gaines, Founder Women Gaining Wealth, LLC Thank you for requesting this free report and taking steps toward your own financial

5 Secrets to Wealth Every Woman Needs To Know To Be Financially Free By Nancy L. Gaines, Founder Women Gaining Wealth, LLC Thank you for requesting this free report and taking steps toward your own financial

Chapter 3 How to analyse a balance sheet

Chapter 3 How to analyse a balance sheet In the previous chapter we looked at how a balance sheet was put together and the numbers that go into it. In this chapter, we are going to take all those numbers

Chapter 3 How to analyse a balance sheet In the previous chapter we looked at how a balance sheet was put together and the numbers that go into it. In this chapter, we are going to take all those numbers

Financial Planning. Introduction. Learning Objectives

Financial Planning Introduction Financial Planning Learning Objectives Lesson 1 Budgeting: How to Live on Your Own and Not Move Home in a Week Prepare a budget and determine disposable income. Identify

Financial Planning Introduction Financial Planning Learning Objectives Lesson 1 Budgeting: How to Live on Your Own and Not Move Home in a Week Prepare a budget and determine disposable income. Identify

SPECIAL REPORT: 4 BIG REASONS YOU CAN T AFFORD TO IGNORE BUSINESS CREDIT!

SPECIAL REPORT: 4 BIG REASONS YOU CAN T AFFORD TO IGNORE BUSINESS CREDIT! 4 BIG REASONS YOU CAN T AFFORD TO IGNORE BUSINESS CREDIT! Provided compliments of: FIRSTUSA DATA SERVICES, LLC 877-857-5045 SUPPORT@FIRSTUSADATA.COM

SPECIAL REPORT: 4 BIG REASONS YOU CAN T AFFORD TO IGNORE BUSINESS CREDIT! 4 BIG REASONS YOU CAN T AFFORD TO IGNORE BUSINESS CREDIT! Provided compliments of: FIRSTUSA DATA SERVICES, LLC 877-857-5045 SUPPORT@FIRSTUSADATA.COM

Saving and Investing: Getting Started

STUDENT MODULE 5.1 SAVING AND INVESTING PAGE 1 Standard 5: The student will analyze the costs and benefits of saving and investing. Saving and Investing: Getting Started But Mom, why can I not have it

STUDENT MODULE 5.1 SAVING AND INVESTING PAGE 1 Standard 5: The student will analyze the costs and benefits of saving and investing. Saving and Investing: Getting Started But Mom, why can I not have it

By John W. Day, MBA. FEATURE ARTICLE: The Structure And Purpose Of Liabilities

THEME: LIABILITIES By John W. Day, MBA ACCOUNTING TERM: Liability Generally, a liability can be defined as an obligation, based on a past transaction, to convey assets or perform services in the future.

THEME: LIABILITIES By John W. Day, MBA ACCOUNTING TERM: Liability Generally, a liability can be defined as an obligation, based on a past transaction, to convey assets or perform services in the future.

Online Advisor October 2015. Major Tax Deadlines For October 2015

Online Advisor October 2015 Major Tax Deadlines For October 2015 * October 1 - Generally the deadline for self-employeds and small businesses to establish a SIMPLE retirement plan for 2015. * October 15

Online Advisor October 2015 Major Tax Deadlines For October 2015 * October 1 - Generally the deadline for self-employeds and small businesses to establish a SIMPLE retirement plan for 2015. * October 15

Slide 2. Income Taxes

Slide 1 Taxes Income taxes have been a part of American life since 1909 when the 16 th Amendment to the Constitution was ratified. You can t avoid taxes, so you might as well understand how taxes are structured

Slide 1 Taxes Income taxes have been a part of American life since 1909 when the 16 th Amendment to the Constitution was ratified. You can t avoid taxes, so you might as well understand how taxes are structured

Vanguard Financial Education Series investing. How to invest your retirement savings

Vanguard Financial Education Series investing How to invest your retirement savings During your working life, you ve saved and invested for retirement. Now that you re finally reaching retirement, consider

Vanguard Financial Education Series investing How to invest your retirement savings During your working life, you ve saved and invested for retirement. Now that you re finally reaching retirement, consider

Developing Financial Statements

New York StartUP! Business Plan Competition Developing Financial Statements Presented by Paisley Demby, CEO PBN Consulting, LLC www.pbnconsulting.com 1 Invitation to Tweet #2015NYStartUp PaisleyDemby Contents

New York StartUP! Business Plan Competition Developing Financial Statements Presented by Paisley Demby, CEO PBN Consulting, LLC www.pbnconsulting.com 1 Invitation to Tweet #2015NYStartUp PaisleyDemby Contents

Basic Business Plan Outline

Basic Business Plan Outline A business plan needs to be a well thought out, honest, appraisal of the business and opportunity. This outline is meant to be used for your road map. It should be a living

Basic Business Plan Outline A business plan needs to be a well thought out, honest, appraisal of the business and opportunity. This outline is meant to be used for your road map. It should be a living

Plan and Track Your Finances

Plan and Track Your Finances 9.1 Financing Your Business 9.2 Pro Forma Financial Statements 9.3 Recordkeeping for Businesses Lesson 9.1 Financing Your Business Goals Estimate your startup costs and personal

Plan and Track Your Finances 9.1 Financing Your Business 9.2 Pro Forma Financial Statements 9.3 Recordkeeping for Businesses Lesson 9.1 Financing Your Business Goals Estimate your startup costs and personal

Wealth Strategies. The Building Blocks to Creating Your Financial Road Map Part 3 of 12. w w w.rfawea lth.com

w w w.rfawea lth.com w w w.rfawea lth.com Wealth Strategies The Building Blocks to Creating Your Financial Road Map Part 3 of 12 Financial Roadmap Building Blocks WEALTH STRATEGIES Page 1 So you re planning

w w w.rfawea lth.com w w w.rfawea lth.com Wealth Strategies The Building Blocks to Creating Your Financial Road Map Part 3 of 12 Financial Roadmap Building Blocks WEALTH STRATEGIES Page 1 So you re planning

Choosing the Right Entity for Maximum Tax Benefits for Your Construction Company

Choosing the Right Entity for Maximum Tax Benefits for Your Construction Company Timely re-evaluation of choice of entity will enhance the shareholder value of your contractor client By Theran J. Welsh

Choosing the Right Entity for Maximum Tax Benefits for Your Construction Company Timely re-evaluation of choice of entity will enhance the shareholder value of your contractor client By Theran J. Welsh

Financial Planning. Presented by Emma's Garden

+ Financial Planning Presented by Emma's Garden Financial Planning A comprehensive financial plan helps you to forecast and set your financial goals and milestones. Your financial forecasts are an essential

+ Financial Planning Presented by Emma's Garden Financial Planning A comprehensive financial plan helps you to forecast and set your financial goals and milestones. Your financial forecasts are an essential

Jim Olsen CPA Phone: 772-545-7922 8875 Robwyn Street Fax: 772-545-7923. The Minister and His Taxes

Jim Olsen CPA Phone: 772-545-7922 8875 Robwyn Street Fax: 772-545-7923 Hobe Sound, FL 33455 Jolsencpa@aol.com www.jimolsencpa.com The Minister and His Taxes One of the reasons for the confusion surrounding

Jim Olsen CPA Phone: 772-545-7922 8875 Robwyn Street Fax: 772-545-7923 Hobe Sound, FL 33455 Jolsencpa@aol.com www.jimolsencpa.com The Minister and His Taxes One of the reasons for the confusion surrounding

- all the money you receive in a year - money from wages, tips, interest you earn, dividends, capital gains, etc.

4D Income Taxes there are 5 different categories Single You must be unmarried at the end of the year. Married filing jointly this is how most married people will file. Married filing separately occasionally,

4D Income Taxes there are 5 different categories Single You must be unmarried at the end of the year. Married filing jointly this is how most married people will file. Married filing separately occasionally,

YOUR PERSONAL FINANCIAL ORGANIZER

YOUR PERSONAL FINANCIAL ORGANIZER WHAT'S INSIDE INTRODUCTION: UNDERSTANDING YOUR FINANCIAL ORGANIZER...1 I. FIGURING YOUR FINANCES...2 Net Worth Analysis...2 Cash Flow Analysis...4 II. GOALS, PRODUCTS