Deliverability and Regional Pricing

|

|

|

- Veronica Flynn

- 8 years ago

- Views:

Transcription

1 Deliverability and Regional Pricing in U.S. Natural Gas Markets Stephen P. A. Brown and Mine K. Yücel Research Department Working Paper 080 Federal Reserve Bank of Dallas

2 Deliverability and Regional Pricing in U.S. Natural Gas Markets Stephen P. A. Brown and Mine K. Yücel* Federal Reserve Bank of Dallas Abstract: During the 1980s and early 90s, interstate natural gas markets in the United States made a transition away from the regulation that characterized the previous three decades. With abundant supplies and plentiful pipeline capacity, a new order emerged in which freer markets and arbitrage closely linked natural gas price movements throughout the country. After the mid- 1990s, however, U.S. natural gas markets tightened and some pipelines were pushed to capacity. We look for the pricing effects of limited arbitrage through causality testing between prices at nodes on the U.S. natural gas transportation system and interchange prices at regional nodes on North American electricity grids. Our tests do reveal limited arbitrage, which is indicative of bottlenecks in the U.S. natural gas pipeline system. 1. Introduction During the 1980s and early 90s, interstate natural gas markets in the United States made a gradual transition away from the regulation that had characterized the three previous decades. The 1978 Natural Gas Policy Act and subsequent actions by the Federal Energy Regulatory Commission and the U.S. Congress gradually opened up interstate natural gas pricing to market forces. With plentiful pipeline capacity, a surge in natural gas production and growth in consumption, a new order emerged in which freer markets and arbitrage closely linked movements in natural gas prices throughout the United States, as De Vany and Walls (1993, 1995, 1999), Doane and Spulber (1994), and MacAvoy (000) have documented. Production varied to meet seasonal changes in demand, and prices did not show much volatility. U.S. natural gas markets continued to evolve throughout the 1990s. Natural gas consumption grew propelled by the rapid growth of its use in electric power generation, which was driven by regulatory changes and the emergence of new technology. As consumption grew, production and net imports failed to keep pace with the gains in heating season demand (Figure

3 1). Summer production and imports gradually rose to near winter levels, and the market relied 1 more heavily on storage to meet the seasonal variation in demand. At the same time, prices became more volatile. Moreover, once pipeline companies were no longer guaranteed a rate of return (MacAvoy 000), their incentives to build the excess capacity necessary to accommodate rising peak winter usage was reduced. By 000, U.S. natural gas markets looked substantially different than they had in the late 1980s. With the seasonal variation in consumption dependent on inventories rather than changes in production, prices became more volatile, and according to Brown and Yücel (007), inventory swings figured prominently in that volatility. In addition, as some pipelines were pushed to capacity, the physical means for arbitrage was limited, and the links between regional natural gas prices throughout the United States seemingly weakened, as shown by Marmer, et al. (007). These changes in market conditions raise a question about how well the pipeline system supports the arbitrage required to integrate regional natural gas markets in the United States. To examine this issue, we use a series of causality tests to assess whether arbitrage between Henry Hub and two regional nodes on the U.S. natural gas transmission system has become limited. The tests involve daily natural gas prices at Henry Hub and two regional nodes on the U.S. natural gas transmission system, as well as electricity prices at two regional interchange nodes on the North American electricity grids with these electricity prices being indicative of regional demand conditions for natural gas. Our testing reveals limited arbitrage, which suggests that a lack of pipeline capacity contributes to the volatility of regional natural gas prices in the United States.

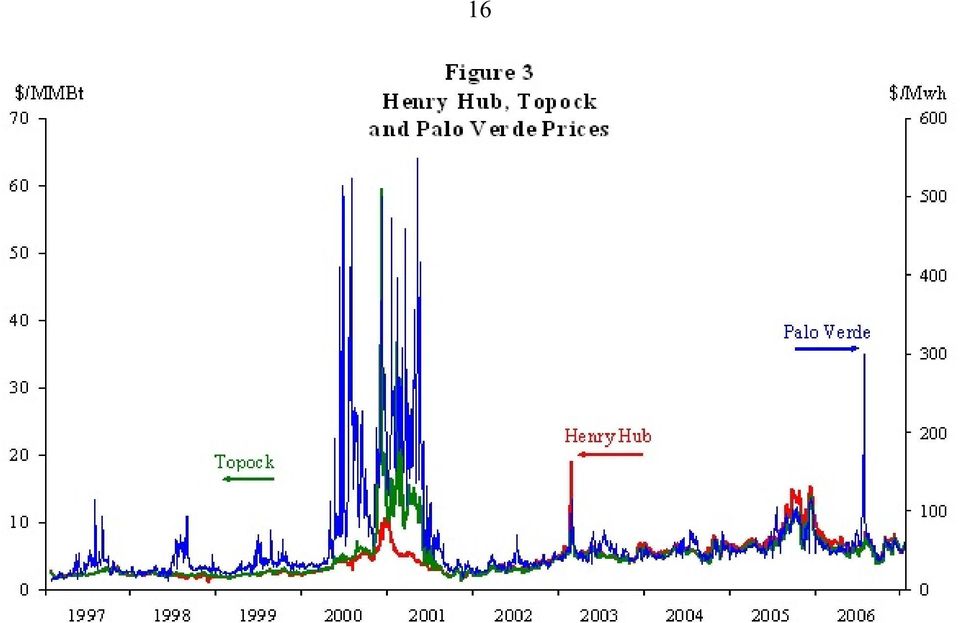

4 3. Price Shocks and Regional Natural Gas Markets To examine how natural gas price shocks are transmitted across the United States and how fluctuations in regional demand might influence natural gas pricing, we undertake a series of causality tests involving daily natural gas and electricity prices at major trading nodes for the period February 3, 1997 through January 17, 007. The natural gas prices include those at Henry Hub, Transco Zone 6 and Topock, and the electricity prices are for PJM and Palo Verde. Although regulation may affect the demand and supply conditions at any of these five trading nodes, the prices at each are set by the interaction of market forces. Henry Hub can thought of as the principal upstream market for natural gas in the United States. Near New Orleans, Henry Hub comprises a series of 16 pipeline interconnects at a single facility that draw their supplies from the largest concentration of natural gas producing regions in the country and nearby terminals for importing Liquefied Natural Gas (LNG). These pipelines directly serve markets throughout the U.S. East Coast, the Gulf Coast, the Midwest, and up to the Canadian border. Interconnections with pipelines across Texas link the Henry Hub market to those in the U.S. West. Serletis and Herbert (1999) find that the Henry Hub spot price is strongly correlated with the NYMEX futures price, which is the most widely traded natural gas contract in the world. As such, the Henry Hub price represents a national market price for natural gas that is determined relatively close to the wellhead. Transco Zone 6 and Topock are two regional trading nodes on the North American natural gas transmission system downstream from Henry Hub, and their prices represent market conditions in the U.S. East and U.S. West, respectively. Transco Zone 6 is a natural gas market center along 300 miles of pipeline, covering a six-state area from Virginia to New York City.

5 Topock is a regional transportation and pricing node for natural gas on the California-Arizona border. 4 In the two regions we examine, considerable natural gas is used to generate electricity. Moreover, natural gas is the marginal fuel for generating electricity in both regions (Hartley et al, 007). Consequently, fluctuations in electricity prices can be used to examine how changing regional demand affects the dynamics of U.S. natural gas markets. Accordingly, we consider the interchange electricity prices at two major nodes on the North American electricity grid PJM in 3 the East and Palo Verde in the West. PJM is a system of interconnected transmission lines that functions as an interchange to supply electric power for Central and Eastern Pennsylvania, nearly all of New Jersey, Delaware, Western Maryland, and Washington D.C. Originally developed as a switch yard for the Palo Verde nuclear power plant in Arizona, Palo Verde is an electricity transmission interchange that offers direct access to power generation and demand centers throughout the U.S. Southwest and southern California. It can also serve markets in the Pacific Northwest and northern Rockies through interconnecting transmission lines..1 Testing for Arbitrage We test for causality in two chains of prices. For the U.S. East, the chain from upstream to downstream is Henry Hub, Transco Zone 6 and PJM. In the U.S. West, the chain from upstream to downstream is Henry Hub, Topock and Palo Verde. As shown in Figures and 3, prices in each of the two groupings are likely to show correlation. The causality tests allow us to trace price shocks that originate close to natural gas supplies, are transmitted downstream to regional natural gas markets, and are pushed onward to regional electricity markets. They also allow us to investigate whether shocks originating in regional electricity markets are transmitted

6 5 backward to regional natural gas markets and then upstream to Henry Hub. Taken together, the causality tests can reveal whether natural gas prices are well arbitraged between Henry Hub and the two regional trading nodes. A lack of such arbitrage would imply delivery constraints in the natural gas pipeline system. In the absence of delivery constraints, we would not expect variations in regional conditions (such as regional demand for natural gas to generate electricity) to exert an influence on regional natural gas prices without also affecting the price at Henry Hub. Any regional fluctuation in natural gas demand would be supplied by the national market, and the regional price fluctuations would be arbitraged back to the Henry Hub price. With pipelines reaching capacity or natural gas flows otherwise restricted, arbitrage could be limited. Regions with constrained delivery could see natural gas price movements that are independent of those at Henry Hub. Such bottlenecks could be the result of physical limitations, regulatory inhibitions, or monopolization. 4 An alternative approach to ours is to test for simple cointegration between upstream and downstream natural gas prices. The lack of simple cointegration between natural gas prices across regions would suggest the possibility of a breakdown in the law of one price brought about by the lack of arbitrage. Cointegration testing does not allow for the potential influence of intervening factors, such as changes in transportation costs, that might affect long-term pricing relationships without being indicative of a breakdown in arbitrage. The causality testing we undertake provides a more comprehensive examination of the transmission of price shocks, and when it reveals a breakdown in arbitrage, there is greater assurance that such a breakdown has occurred. 5

to exert an influence on regional")

7 6. About the Data For purposes of analysis, we use daily data covering the period from February 3, 1997 through January 17, 007. These data cover a nearly ten-year period after the seasonality of production has come to an end and storage is used to meet seasonal swings in demand. The period also contains numerous episodes of volatile natural gas and electricity prices. As the first step in our analysis, we examine the properties of each price series as represented in natural logs. The two regional natural gas prices are somewhat more volatile than the Henry Hub price, although the volatility of the Transco Zone 6 price is lower relative to its mean (Table 1). We see more price volatility in the U.S. West, with the electricity price more volatile than the natural gas price. Augmented Dickey-Fuller tests reveal that natural gas prices at Henry Hub and Topock and the electricity price at Palo Verde are difference stationary (Table ). Similar testing finds that the natural gas price at Transco Zone 6 and the electricity price at PJM are trend stationary..3 Cointegration Tests The finding that the Henry Hub, Topock and Palo Verde prices are difference stationary raises the possibility that these series may be cointegrated. Two integrated series are cointegrated if they move together in the long run. Cointegration implies a stationary, long-run relationship between the two difference-stationary series. As such, the cointegrating term provides information about the long-run relationship. If cointegration is not taken into account, the relationship between the cointegrated variables could be misspecified, and/or parameters could be inefficiently estimated. 6 The Johansen procedure reveals that Henry Hub and Topock prices are trend cointegrated,

8 7 which implies a long-term relationship with a drift (Table 3). The estimated value of is 1.007, which indicates that a one-percent change in the Henry Hub price is met with about a one-percent change in the Topock price and vice-versa. The adjustment coefficients are for Henry Hub and.077 for Topock, indicating that the Topock price adjusts to errors in the long-term relationship between the two prices at about twice the rate that the Henry Hub price adjusts. Similar testing finds the electricity price at Palo Verde price is neither cointegrated nor trend cointegrated with the Henry Hub or Topock natural gas prices at the five-percent level (Table 3)..4 Bivariate Models and Estimation Procedures Causality testing generally requires the use of stationary variables. Accordingly, our causality tests use differences of logged prices at Henry Hub, Topock and Palo Verde, and deviations from trends in the logged prices at Transco Zone 6 and PJM. Errors in the trend cointegrating relationship are also used in causality tests involving Henry Hub and Topock prices together. We use standard causality testing to examine how price changes are transmitted between natural gas and electricity pricing nodes. All tests are conducted with natural logs of the variables in their stationary form. For any pair of upstream and downstream prices that do not have a cointegrating relationship, we use the following generalized specification to test for causality: (1) ()

.")

9 t t 8 where SPD and SPU represent the appropriate stationary form of the downstream and upstream prices, respectively; a 1, a, b 1i, b i, c 1i and c i are parameters to be estimated; and 1t and t are white noise residuals. Because the Henry Hub and Topock price series are cointegrated, we account for cointegration in their relationship by specifying a vector error-correction model in which changes in the dependent variable are expressed as changes in both the independent and the dependent variable, plus an error-correction term, as recommended by Engle and Granger (1987). For cointegrated variables, the error-correction term reflects the deviations from the long-run cointegrating relationship between the variables. The coefficient on the equilibrium error reflects the extent to which the dependent variable adjusts during a given period to deviations from the cointegrating relationship that occurred in the previous period. The resulting model is as follows: (3) (4) where the CI is errors in the estimated trend cointegrating relationship (PD- - PU- t); a 3, a 4, 7 b 3i, b 4i, c 3i, c 4i, 3 and 4 are parameters to be estimated; and 3t and 4t are white noise residuals. The coefficients 3 and 4 represent the adjustment to equilibrium error in the long-term relationship between the upstream and downstream prices. For the models that do not contain a cointegrating relationship, causality runs from the

.")

10 9 upstream to the downstream price if the b 1i are jointly significant. Similarly, causality runs from the downstream price to the upstream price if the b i are jointly significant. For the error- correction models, causality runs from the upstream price to the downstream price if 3 and the b 3i are jointly significant, and causality runs from the downstream price to the upstream price if 4 and the b 4i are jointly significant..5 Natural Gas and Electricity Pricing In examining the transmission of price shocks between Henry Hub and the two regional natural gas nodes, we find bidirectional causality (Table 4). Movements in the Henry Hub price 8 lead movements in Transco Zone 6 and Topock prices. In addition, movements in the two regional natural gas prices lead those at Henry Hub. 9 In both the U.S. East and U.S. West, we find bidirectional causality between regional natural gas and electricity prices. Movements in the Transco Zone 6 and Topock prices lead those of the PJM and Palo Verde prices, respectively. Similarly, movements in the PJM and Palo Verde electricity prices lead the natural gas prices in their respective regions. Such findings are expected because natural gas is the marginal fuel most commonly used for electricity generation in these two regions. When a region s electricity prices are driven up by strong demand, the demand for natural gas is likely to rise in the region, pulling up its price. Similarly, when regional natural gas prices are pushed up by more costly supply, the cost of electricity generation will rise in the region. We also find no causality between the Henry Hub natural gas price and regional electricity prices. Because regional electricity prices influence natural gas price movements in their respective regions, the absence of a relationship with the Henry Hub price of natural gas

.")

11 10 suggests the likelihood that regional electricity prices exert an independent influence on regional natural gas prices that is not arbitraged back to Henry Hub. 3. Assessing the Influence of Regional Electricity Prices Multivariate tests provide a means to more throughly assess the possibility that regional electricity prices exert an independent influence on regional natural gas prices that are are not arbitraged back to Henry Hub. For the U.S. East market, we specify the following multivariate tests: (5) (6) where STZ6 is the stationary form of the natural gas price at Transco Zone 6; SHH is the stationary form of the natural gas price at Henry Hub; SPJM is the stationary form of the electricity price at PJM; a 5, a 6, b 5i, b 6i, c 5i, c 6i, d 5i and d 6i are parameters to be estimated; and 5t and 6t are white noise residuals. Equation 5 can be used determine whether PJM electricity prices exert an independent influence on Transco Zone 6 natural gas prices when the effects of Henry Hub prices are taken into account. Similarly, equation 6 can used to determine whether the regional electricity prices affect natural gas prices at Henry Hub natural when Transco Zone 6 prices are taken into account. For the U.S. West market, where Henry Hub and Topock prices are trend cointegrated,

(6) where STZ6 is the stationary form of the natural gas price at Transco Zone 6; SHH is the stationary form of the natural gas price at")

12 11 we specify the following tests: (7) (8) where PT is the price of natural gas at Topock; PHH is the price of natural gas at Henry Hub; PPV is the price of electricity at Palo Verde; CI is errors in the trend cointegrating relationship between Henry Hub and Topock prices; a 7, a 8, b 7i, b 8i, c 7i, c 8i, d 7i, d 8i, 7 and 8 parameters to be estimated; and and are white noise residuals. Equation 7 can be used to determine whether 7t 8t Palo Verde electricity prices exert an independent influence on Topock natural gas prices when the effects of Henry Hub prices are taken into account. Similarly, equation 8 shows can be used to determine whether regional electricity prices affect natural gas prices at the Henry Hub when Topock prices are taken into account. As shown in Table 5, the two pairs of tests provide similar results. In both regions, the Henry Hub price has a significant effect on regional natural gas prices. In addition, each regional electricity price exerts a significant independent influence on its respective regional natural gas price. Natural gas prices in both regions have a significant effect on Henry Hub prices, but electricity prices in neither region are significant. Movements in regional natural gas prices are shaped by movements in both Henry Hub natural gas prices and regional electricity prices. The influence of regional electricity prices on regional natural gas prices is not arbitraged back to Henry Hub. The lack of arbitrage suggests

13 1 constraints in natural gas delivery from Henry Hub to both the U.S. East and U.S. West markets. 4. Conclusion: Delivery Constraints and U.S. Natural Gas Prices The agents in the newly deregulated U.S. interstate natural gas market inherited a pipeline system with a regulatory-era capacity that facilitated relatively free-flowing natural gas and arbitrage. As consumption grew, however, capacity along existing lines failed to keep pace because the new environment didn t offer the incentives for pipeline companies to build the capacity necessary to handle rising peak loads. The result has been bottlenecks and a breakdown in the pricing conditions once found in the newly freed natural gas market. Electricity prices in both the East and West markets exert an independent influence on natural gas prices in their respective regions, but these effects are not arbitraged back to the natural gas price at Henry Hub. These findings imply that delivery constraints limit the arbitrage between regional natural gas markets with regional prices driven by factors that are independent of those in play at Henry Hub. Our findings suggest that an assessment of the market conditions that follow shortly after a market restructuring should be considered preliminary. In the wake of restructuring, the inherited capital stock will reflect the regulatory environment in which it was created, rather than new market realities. Over time, the new environment will reshape the capital stock whether the changes reflect simple market incentives, new regulatory inhibitions and/or monopolization. For natural gas, the result has been the development of bottlenecks in the regional transmission of natural gas, which seem to have inhibited arbitrage during episodes of peak demand and reduced the integration of prices across the United States.

14 13 5. Post Script: Natural Gas Storage Brown and Yücel (007) find that storage is an important determinant of the U.S. natural gas prices. Natural gas storage might also play role in the relationship between Henry Hub and regional natural gas prices. In particular, regional storage can be a substitute for transmission capacity, and low storage volumes in a given region may be associated with associated with sharp natural gas price movements during episodes of strong regional demand. Because storage data are available only on a weekly basis and for three relatively large geographic regions, we leave such an investigation for further research.

15 14 References Brown, Stephen P. A. and Mine K. Yücel (007), What Drives Natural Gas Prices? The Energy Journal (forthcoming). Brown, Stephen P. A. and Mine K. Yücel (1993), The Pricing of Natural Gas in U.S. Markets, Economic Review, Federal Reserve Bank of Dallas (Second Quarter): De Vany, A. and W. David Walls (1993). Pipeline Access and Market Integration in the Natural Gas Industry: Evidence from Cointegration Tests. Energy Journal 14 (4):1-19 De Vany, Arthur S. and W. David Walls (1995), The Emerging New Order in Natural Gas, Quorum Books, Westport, Connecticut. De Vany, A. and W. David Walls (1999), Cointegration Analysis of Spot Electricity Prices: Insights on Transmission Efficiency in the Western U.S. Energy Economics, 1: Doane, Michael J, and Daniel F. Spulber (1994), Open Access and the Revolution of the U.S. Spot Market for Gas. Journal of Law and Economics, 37: Energy Modeling Forum (003), Natural Gas, Fuel Diversity and North American Energy Markets, EMF Report 0, Stanford University (September). Engle, Robert F. and C. W. J. Granger (1987), Co-integration and Error Correction: Representation, Estimation, and Testing, Econometrica (March): Engle, Robert F. and Byung Sam Yoo (1987), Forecasting and Testing in Co-integrated Systems, Journal of Econometrics, Hartley, Peter, Kenneth Medlock and Jennifer Rosthal (007), The Relationship Between Crude Oil and Natural Gas Prices. Rice University, Baker Institute Working Paper. MacAvoy, Paul W. (000), The Natural Gas Market, Yale University Press, New Haven. Marmer, Vadim, Dmitry Shapiro and Paul MacAvoy (007), Bottlenecks in Regional Markets for Natural Gas Transmission Services, Energy Economics 9(1): (January). Natural Gas Regulation Committee (00), Report of the Natural Gas Regulation Committee, Energy Law Journal 3(1). Serletis, Apostolos and John Herbert (1999), The Message in North American Energy Prices. Energy Economics, 1: Villar, Jose and Joutz, Fred (006), The Relationship Between Crude Oil and Natural Gas Prices, EIA manuscript, October.

, The Emerging New Order in Natural Gas, Quorum Books, Westport, Connecticut. De Vany, A. and W.")

16 15

17 16

18 17 Table 1: Descriptive Statistics (Logs of Daily Data, February 3, 1997 through January 17, 007) Henry Hub Transco Zone 6 Topock PJM Palo Verde Mean Median Std. Dev Normalized Std. Dev Table : Unit Root Tests (Logs of Daily Data, February 3, 1997 through January 17, 007) Augmented Dickey-Fuller Tests variables Levels Linear Trend First Differences Henry Hub ** Transco Zone * n/a Topock n/a ** PJM ** ** n/a Palo Verde n/a ** +, * and ** denote significance at better than 0.1, 0.05 and 0.01 percent, respectively. Linear trend is not significant.

19 18 Table 3 A: Bivariate Johansen Cointegration Tests (Henry Hub and Topock) Ho: rank=p Eigenvalue Trace Statistic Max Eigenvalue Statistic p=0 p * * logged Standardized Eigenvalues or s with Standard Errors Henry Hub 1 0 Topock (0.1454) Standardized Coefficients with Standard Errors Henry Hub ( ) Topock ( ) Ho: rank=p Eigenvalue Trace Statistic Max Eigenvalue Statistic p=0 p ** * logged, with trend Standardized Eigenvalues or s with Standard Errors Henry Hub 1 0 Topock ( ) Trend (5.1E-05) Standardized Coefficients with Standard Errors Henry Hub ( ) Topock ( ) +, * and ** denote significance at better than 0.1, 0.05 and 0.01 percent, respectively.

Trend -0.000303 (5.")

20 19 Table 3 B. Bivariate Cointegration Tests (Henry Hub and Palo Verde) Ho: rank=p Eigenvalue Trace Statistic Max Eigenvalue Statistic p=0 p logged Standardized Eigenvalues or s with Standard Errors Henry Hub 1 0 Palo Verde (0.171) Standardized Coefficients with Standard Errors Henry Hub ( ) Palo Verde (0.0104) Ho: rank=p Eigenvalue Trace Statistic Max Eigenvalue Statistic p=0 p logged, with trend Standardized Eigenvalues or s with Standard Errors Henry Hub 1 0 Palo Verde ( ) Trend ( ) Standardized Coefficients with Standard Errors Henry Hub ( ) Palo Verde (0.008) +, * and ** denote significance at better than 0.1, 0.05 and 0.01 percent, respectively.

Trend -0.000366 (0.")

21 0 Table 3 C. Bivariate Cointegration Tests (Topock and Palo Verde) Ho: rank=p Eigenvalue Trace Statistic Max Eigenvalue Statistic p=0 p logged Standardized Eigenvalues or s with Standard Errors Topock 1 0 Palo Verde (0.1131) Standardized Coefficients with Standard Errors Topock ( ) Palo Verde ( ) Ho: rank=p Eigenvalue Trace Statistic Max Eigenvalue Statistic p=0 p logged, with trend Standardized Eigenvalues or s with Standard Errors Henry Hub 1 0 Palo Verde ( ) Trend ( ) Standardized Coefficients with Standard Errors Henry Hub ( ) Palo Verde (0.0167) +, * and ** denote significance at better than 0.1, 0.05 and 0.01 percent, respectively.

22 Table 4. Bivariate Causality Tests for Natural Gas and Electric Prices 1 U.S. East Markets Dependent Variables explanatory variables Transco Zone 6 Henry Hub PJM Transco Zone 6 PJM Henry Hub Henry Hub.0000**.0000** ** Transco Zone **.0001**.0007**.0000** PJM.0000**.0113*.0000**.1346 Optimal Lags R =.94 Adj R =.94 R =.06 Adj R =.05 R =.77 Adj R =.77 R =.94 Adj R =.94 R =.77 Adj R =.77 R =.06 Adj R =.04 U.S. West Markets Dependent Variables explanatory variables Topock Henry Hub Palo Verde Topock Palo Verde Henry Hub Henry Hub.0000**.0000** ** Topock.0000**.0076**.0001**.0000** Palo Verde.0000**.0000**.0000**.165 Optimal Lags R =.5 Adj R =.3 R =.08 Adj R =.05 R =.0 Adj R =.17 R =.7 Adj R =.4 R =.18 Adj R =.15 R =.08 Adj R =.05 Optimal lag length is determined by the Akaike information criterion. Causality test includes term to account for errors in trend cointegration. Reported values are joint significance with, * and ** denoting significance at better + than 0.1, 0.05 and 0.01 percent, respectively.

23 Table 5. Multivariate Tests for Natural Gas Prices U.S. East Markets Dependent Variables U.S. West Markets Dependent Variables explanatory variables Transco Zone 6 Henry Henry Hub Topock Hub explanatory variables Henry Hub.0000**.0000**.0000**.0000** Henry Hub Transco Zone **.0000**.0000**.0033* Topock PJM.0400* **.8639 Palo Verde Optimal Lags Optimal Lags R =.95 Adj R =.95 R =.07 Adj R =.05 R =. Adj R =.1 R =.06 Adj R =.04 Optimal lag length is determined by the Akaike information criterion. Causality test includes term to account for errors in trend cointegration between Topock and Henry Hub. Reported values are joint significance with, * and + ** denoting significance at better than 0.1, 0.05 and 0.01 percent, respectively.

24 3 Notes: *Previous versions of this paper were presented at meetings of Energy Modeling Forum 0 in College Park, Maryland, the International Natural Gas Seminar in Rio de Janeiro and the Western Economic Association Annual Meeting in Seattle. The authors wish to thank two anonymous referees, Mark Rodehohr and participants in the meetings for helpful comments and suggestions; Kevin Forbes, Frank Graves and Olga Zograf for providing data; as well as Raghav Virmani and Priscilla Caputo for capable research assistance. The views expressed are those of the authors and do not necessarily represent those of the Federal Reserve Bank of Dallas or the Federal Reserve System. 1. In the average year, inventories are built during May, June, July, August, September and October, when U.S. natural gas production and imports typically exceed consumption. In the average year, U.S. natural gas consumption exceeds production and imports in November, December, January, February and March. During those months, current production, imports and inventories are used to meet consumption.. Over the period from January 1996 through May 007, the monthly wellhead price of natural gas had a normalized standard deviation nearly three times higher than that for the period from January 1985 through December The North American electricity grid is broken up into a number of nearly autonomous regions, which prevents the direct arbitrage of prices by moving electricity across the continent. 4. See Natural Gas Regulation Committee (00). 5. A more complete model of natural gas pricing could reveal periods of time in which regional and Henry Hub prices of natural gas prices move together and periods in which capacity constraints prevent arbitrage. If the episodes without arbitrage occur with sufficient frequency, causality testing will be sufficient to reveal a breakdown in arbitrage. Such testing will not identify the specific episodes. 6. See Engle and Yoo (1987). 7. If a one-unit change in the upstream price occurs over the long run, it will be met with a change in the downstream price over the long run. 8. The model for Henry Hub and Topock prices yields estimated coefficients on the cointegrating term of and.037 for Henry Hub and Topock equations, respectively with only the latter coefficient significant at better than 5 percent. 9. These findings are similar to those of Brown and Yücel (1993), who found that price shocks transmitted through U.S. natural gas markets could originate either at the wellhead or in those end-use markets in which extensive fuel-switching is possible.

What Drives Natural Gas Prices?

What Drives Natural Gas Prices? Stephen P. A. Brown and Mine K. Yücel* For many years, fuel switching between natural gas and residual fuel oil kept natural gas prices closely aligned with those for crude

What Drives Natural Gas Prices? Stephen P. A. Brown and Mine K. Yücel* For many years, fuel switching between natural gas and residual fuel oil kept natural gas prices closely aligned with those for crude

Recent patterns in natural gas prices have raised

Stephen P. A. Brown Assistant Vice President and Senior Economist Mine K. Yücel Senior Economist and Policy Advisor The Pricing of Natural Gas in U.S. Markets Recent patterns in natural gas prices have

Stephen P. A. Brown Assistant Vice President and Senior Economist Mine K. Yücel Senior Economist and Policy Advisor The Pricing of Natural Gas in U.S. Markets Recent patterns in natural gas prices have

EMPIRICAL INVESTIGATION AND MODELING OF THE RELATIONSHIP BETWEEN GAS PRICE AND CRUDE OIL AND ELECTRICITY PRICES

Page 119 EMPIRICAL INVESTIGATION AND MODELING OF THE RELATIONSHIP BETWEEN GAS PRICE AND CRUDE OIL AND ELECTRICITY PRICES Morsheda Hassan, Wiley College Raja Nassar, Louisiana Tech University ABSTRACT Crude

Page 119 EMPIRICAL INVESTIGATION AND MODELING OF THE RELATIONSHIP BETWEEN GAS PRICE AND CRUDE OIL AND ELECTRICITY PRICES Morsheda Hassan, Wiley College Raja Nassar, Louisiana Tech University ABSTRACT Crude

Business Cycles and Natural Gas Prices

Department of Economics Discussion Paper 2004-19 Business Cycles and Natural Gas Prices Apostolos Serletis Department of Economics University of Calgary Canada and Asghar Shahmoradi Department of Economics

Department of Economics Discussion Paper 2004-19 Business Cycles and Natural Gas Prices Apostolos Serletis Department of Economics University of Calgary Canada and Asghar Shahmoradi Department of Economics

Analysis of Whether the Prices of Renewable Fuel Standard RINs Have Affected Retail Gasoline Prices

Analysis of Whether the Prices of Renewable Fuel Standard RINs Have Affected Retail Gasoline Prices A Whitepaper Prepared for the Renewable Fuels Association Key Findings Changes in prices of renewable

Analysis of Whether the Prices of Renewable Fuel Standard RINs Have Affected Retail Gasoline Prices A Whitepaper Prepared for the Renewable Fuels Association Key Findings Changes in prices of renewable

Business cycles and natural gas prices

Business cycles and natural gas prices Apostolos Serletis and Asghar Shahmoradi Abstract This paper investigates the basic stylised facts of natural gas price movements using data for the period that natural

Business cycles and natural gas prices Apostolos Serletis and Asghar Shahmoradi Abstract This paper investigates the basic stylised facts of natural gas price movements using data for the period that natural

NATURAL GAS PRICES TO REMAIN AT HIGHER LEVELS

I. Summary NATURAL GAS PRICES TO REMAIN AT HIGHER LEVELS This brief white paper on natural gas prices is intended to discuss the continued and sustained level of natural gas prices at overall higher levels.

I. Summary NATURAL GAS PRICES TO REMAIN AT HIGHER LEVELS This brief white paper on natural gas prices is intended to discuss the continued and sustained level of natural gas prices at overall higher levels.

A Regression Model of Natural Gas/Wholesale Electricity Price Relationship and Its Application for Detecting Potentially Anomalous Electricity Prices

A Regression Model of Natural Gas/Wholesale Electricity Price Relationship and Its Application for Detecting Potentially Anomalous Electricity Prices Young Yoo (young.yoo@ferc.gov) Bill Meroney (william.meroney@ferc.gov)

A Regression Model of Natural Gas/Wholesale Electricity Price Relationship and Its Application for Detecting Potentially Anomalous Electricity Prices Young Yoo (young.yoo@ferc.gov) Bill Meroney (william.meroney@ferc.gov)

A Look at Western Natural Gas Infrastructure During the Recent El Paso Pipeline Disruption

A Look at Western Natural Gas Infrastructure During the Recent El Paso Pipeline Disruption This analysis examines the impact of the August 2000 El Paso Natural Gas Pipeline system disruption upon the ability

A Look at Western Natural Gas Infrastructure During the Recent El Paso Pipeline Disruption This analysis examines the impact of the August 2000 El Paso Natural Gas Pipeline system disruption upon the ability

An Analysis of the Increase of Natural Gas Production from 2007-2010: Specific Causes and Implications

An Analysis of the Increase of Natural Gas Production from 2007-2010: Specific Causes and Implications By Sonali Mittal An honors thesis submitted in partial fulfillment of the requirements for the degree

An Analysis of the Increase of Natural Gas Production from 2007-2010: Specific Causes and Implications By Sonali Mittal An honors thesis submitted in partial fulfillment of the requirements for the degree

Falling Oil Prices and US Economic Activity: Implications for the Future

Date Issue Brief # I S S U E B R I E F Falling Oil Prices and US Economic Activity: Implications for the Future Stephen P.A. Brown December 2014 Issue Brief 14-06 Resources for the Future Resources for

Date Issue Brief # I S S U E B R I E F Falling Oil Prices and US Economic Activity: Implications for the Future Stephen P.A. Brown December 2014 Issue Brief 14-06 Resources for the Future Resources for

On the long run relationship between gold and silver prices A note

Global Finance Journal 12 (2001) 299 303 On the long run relationship between gold and silver prices A note C. Ciner* Northeastern University College of Business Administration, Boston, MA 02115-5000,

Global Finance Journal 12 (2001) 299 303 On the long run relationship between gold and silver prices A note C. Ciner* Northeastern University College of Business Administration, Boston, MA 02115-5000,

The Impact of Fuel Costs on Electric Power Prices

The Impact of Fuel Costs on Electric Power Prices by Kenneth Rose 1 June 2007 1 Kenneth Rose is an independent consultant and a Senior Fellow with the Institute of Public Utilities (IPU) at Michigan State

The Impact of Fuel Costs on Electric Power Prices by Kenneth Rose 1 June 2007 1 Kenneth Rose is an independent consultant and a Senior Fellow with the Institute of Public Utilities (IPU) at Michigan State

Working Papers. Cointegration Based Trading Strategy For Soft Commodities Market. Piotr Arendarski Łukasz Postek. No. 2/2012 (68)

") Working Papers No. 2/2012 (68) Piotr Arendarski Łukasz Postek Cointegration Based Trading Strategy For Soft Commodities Market Warsaw 2012 Cointegration Based Trading Strategy For Soft Commodities Market

Working Papers No. 2/2012 (68) Piotr Arendarski Łukasz Postek Cointegration Based Trading Strategy For Soft Commodities Market Warsaw 2012 Cointegration Based Trading Strategy For Soft Commodities Market

Gas storage industry primer

Gas storage industry primer Gas storage industry primer General Underground natural gas storage facilities are a vital and complementary component of the North American natural gas transmission and distribution

Gas storage industry primer Gas storage industry primer General Underground natural gas storage facilities are a vital and complementary component of the North American natural gas transmission and distribution

Energy commodities: Price Relationship in US and Europe

Energy commodities: Price Relationship in US and Europe Rita Laura D Ecclesia "Sapienza" University of Rome January 20th 2012 Rita Laura D Ecclesia "Sapienza" University Energy of Rome commodities: ()

Energy commodities: Price Relationship in US and Europe Rita Laura D Ecclesia "Sapienza" University of Rome January 20th 2012 Rita Laura D Ecclesia "Sapienza" University Energy of Rome commodities: ()

Assessment of the Adequacy of Natural Gas Pipeline Capacity in the Northeast United States

Assessment of the Adequacy of Natural Gas Pipeline in the Northeast United States U.S. Department of Energy Office of Electricity Delivery and Energy Reliability Energy Infrastructure Modeling and Analysis

Assessment of the Adequacy of Natural Gas Pipeline in the Northeast United States U.S. Department of Energy Office of Electricity Delivery and Energy Reliability Energy Infrastructure Modeling and Analysis

Natural Gas: Winter 2012-13 Abundance! and Some Confusion

Natural Gas: Winter 2012-13 Abundance! and Some Confusion NASEO Winter Fuels Outlook Washington, D.C. October 10, 2012 Bruce B. Henning Vice President, Energy Regulatory and Market Analysis BHenning@icfi.com

Natural Gas: Winter 2012-13 Abundance! and Some Confusion NASEO Winter Fuels Outlook Washington, D.C. October 10, 2012 Bruce B. Henning Vice President, Energy Regulatory and Market Analysis BHenning@icfi.com

Natural Gas Markets in 2006

Order Code RL33714 Natural Gas Markets in 2006 Updated December 12, 2006 Robert Pirog Specialist in Energy Economics and Policy Resources, Science, and Industry Division Natural Gas Markets in 2006 Summary

Order Code RL33714 Natural Gas Markets in 2006 Updated December 12, 2006 Robert Pirog Specialist in Energy Economics and Policy Resources, Science, and Industry Division Natural Gas Markets in 2006 Summary

High Prices Show Stresses in New England Natural Gas Delivery System

February 7, 2014 High Prices Show Stresses in New England Natural Gas Delivery System Abstract. Since 2012, limited supply from the Canaport and Everett liquefied natural gas (LNG) terminals coupled with

February 7, 2014 High Prices Show Stresses in New England Natural Gas Delivery System Abstract. Since 2012, limited supply from the Canaport and Everett liquefied natural gas (LNG) terminals coupled with

FSC S LAW & ECONOMICS INSIGHTS

FSC S LAW & ECONOMICS INSIGHTS Issue 04-4 Fisher, Sheehan & Colton, Public Finance and General Economics July/August 2004 IN THIS ISSUE High Winter Natural Gas Heating Costs for Poor NOTE TO READERS ON-LINE

FSC S LAW & ECONOMICS INSIGHTS Issue 04-4 Fisher, Sheehan & Colton, Public Finance and General Economics July/August 2004 IN THIS ISSUE High Winter Natural Gas Heating Costs for Poor NOTE TO READERS ON-LINE

Do Heating Oil Prices Adjust Asymmetrically To Changes In Crude Oil Prices Paul Berhanu Girma, State University of New York at New Paltz, USA

Do Heating Oil Prices Adjust Asymmetrically To Changes In Crude Oil Prices Paul Berhanu Girma, State University of New York at New Paltz, USA ABSTRACT This study investigated if there is an asymmetric

Do Heating Oil Prices Adjust Asymmetrically To Changes In Crude Oil Prices Paul Berhanu Girma, State University of New York at New Paltz, USA ABSTRACT This study investigated if there is an asymmetric

IS THERE ANY CRUCIAL RELATIONSHIP AMONGST ENERGY COMMODITY PRICES AND PRICE VOLATILITIES IN THE U.S.?

IS THERE ANY CRUCIAL RELATIONSHIP AMONGST ENERGY COMMODITY PRICES AND PRICE VOLATILITIES IN THE U.S.? Dr. Alok Kumar Mishra Assistant Professor School of Economics, University of Hyderabad ABSTRACT: The

IS THERE ANY CRUCIAL RELATIONSHIP AMONGST ENERGY COMMODITY PRICES AND PRICE VOLATILITIES IN THE U.S.? Dr. Alok Kumar Mishra Assistant Professor School of Economics, University of Hyderabad ABSTRACT: The

Led by growth in Texas, the Southeast, and Northeast, power burn is headed for a January record

EIA - Natural Gas Weekly Update for week ending January 28, 2015 Release Date: January 29, 2015 Next Release: February 5, 2015 In the News: Led by growth in Texas, the Southeast, and Northeast, power burn

EIA - Natural Gas Weekly Update for week ending January 28, 2015 Release Date: January 29, 2015 Next Release: February 5, 2015 In the News: Led by growth in Texas, the Southeast, and Northeast, power burn

OUR CONVERSATION TODAY

OUR CONVERSATION TODAY Our goal is to raise the level of awareness around the natural gas supply chain among key stakeholders in order to facilitate positive working relationships and more informed decision

OUR CONVERSATION TODAY Our goal is to raise the level of awareness around the natural gas supply chain among key stakeholders in order to facilitate positive working relationships and more informed decision

The VAR models discussed so fare are appropriate for modeling I(0) data, like asset returns or growth rates of macroeconomic time series.

data, like asset returns or growth rates of macroeconomic time series.") Cointegration The VAR models discussed so fare are appropriate for modeling I(0) data, like asset returns or growth rates of macroeconomic time series. Economic theory, however, often implies equilibrium

Cointegration The VAR models discussed so fare are appropriate for modeling I(0) data, like asset returns or growth rates of macroeconomic time series. Economic theory, however, often implies equilibrium

Winter 2013-14 Energy Market Assessment Report to the Commission

Winter 2013-14 Energy Market Assessment Report to the Commission Docket No. AD06-3-000 October 2013 Disclaimer: The matters presented in this staff report do not necessarily represent the views of the

Winter 2013-14 Energy Market Assessment Report to the Commission Docket No. AD06-3-000 October 2013 Disclaimer: The matters presented in this staff report do not necessarily represent the views of the

Macroeconomics, monetary theory, financial economics, cost-of capital and public utility regulation

Curriculum Vitae John Anthony Neri Work Contact: Benjamin Schlesinger & Associates Department of Economics 7201 Wisconsin Avenue, Suite 740 University of Maryland Bethesda, MD 20814 College Park, MD 20742

Curriculum Vitae John Anthony Neri Work Contact: Benjamin Schlesinger & Associates Department of Economics 7201 Wisconsin Avenue, Suite 740 University of Maryland Bethesda, MD 20814 College Park, MD 20742

LNG Poised to Significantly Increase its Share of Global Gas Market David Wood February 2004 Petroleum Review p.38-39

LNG Poised to Significantly Increase its Share of Global Gas Market David Wood February 2004 Petroleum Review p.38-39 For the past few years LNG has experienced high levels of activity and investment in

LNG Poised to Significantly Increase its Share of Global Gas Market David Wood February 2004 Petroleum Review p.38-39 For the past few years LNG has experienced high levels of activity and investment in

LONG-TERM ASSESSMENT OF NATURAL GAS INFRASTRUCTURE TO SERVE ELECTRIC GENERATION NEEDS WITHIN ERCOT

LONG-TERM ASSESSMENT OF NATURAL GAS INFRASTRUCTURE TO SERVE ELECTRIC GENERATION NEEDS WITHIN ERCOT Prepared for The Electric Reliability Council of Texas JUNE 2013 Black & Veatch Holding Company 2011.

LONG-TERM ASSESSMENT OF NATURAL GAS INFRASTRUCTURE TO SERVE ELECTRIC GENERATION NEEDS WITHIN ERCOT Prepared for The Electric Reliability Council of Texas JUNE 2013 Black & Veatch Holding Company 2011.

What Drives Natural Gas Prices?

-A Structural VAR Approach - Changing World of Natural Gas I Moscow I 27th September I Sebastian Nick I Stefan Thoenes Institute of Energy Economics at the University of Cologne Agenda 1.Research Questions

-A Structural VAR Approach - Changing World of Natural Gas I Moscow I 27th September I Sebastian Nick I Stefan Thoenes Institute of Energy Economics at the University of Cologne Agenda 1.Research Questions

Market fundamentals, competition and natural gas prices

03-02-2015 1 Market fundamentals, competition and natural gas prices MACHIEL MULDER University of Groningen, Department of Economics, Econometrics and Finance Authority for Consumers & Markets International

03-02-2015 1 Market fundamentals, competition and natural gas prices MACHIEL MULDER University of Groningen, Department of Economics, Econometrics and Finance Authority for Consumers & Markets International

Do Electricity Prices Reflect Economic Fundamentals?: Evidence from the California ISO

Do Electricity Prices Reflect Economic Fundamentals?: Evidence from the California ISO Kevin F. Forbes and Ernest M. Zampelli Department of Business and Economics The Center for the Study of Energy and

Do Electricity Prices Reflect Economic Fundamentals?: Evidence from the California ISO Kevin F. Forbes and Ernest M. Zampelli Department of Business and Economics The Center for the Study of Energy and

Displacement of Coal with Natural Gas to Generate Electricity

Displacement of Coal with Natural Gas to Generate Electricity The American Coalition for Clean Coal Electricity (ACCCE) supports a balanced energy strategy that will ensure affordable and reliable energy,

Displacement of Coal with Natural Gas to Generate Electricity The American Coalition for Clean Coal Electricity (ACCCE) supports a balanced energy strategy that will ensure affordable and reliable energy,

Title: Comparing Price Forecast Accuracy of Natural Gas Models and Futures Markets

Title: Comparing Price Forecast Accuracy of Natural Gas Models and Futures Markets Gabrielle Wong-Parodi (Corresponding Author) Lawrence Berkeley National Laboratory One Cyclotron Road, MS 90-4000 Berkeley,

Title: Comparing Price Forecast Accuracy of Natural Gas Models and Futures Markets Gabrielle Wong-Parodi (Corresponding Author) Lawrence Berkeley National Laboratory One Cyclotron Road, MS 90-4000 Berkeley,

Relationship among crude oil prices, share prices and exchange rates

Relationship among crude oil prices, share prices and exchange rates Do higher share prices and weaker dollar lead to higher crude oil prices? Akira YANAGISAWA Leader Energy Demand, Supply and Forecast

Relationship among crude oil prices, share prices and exchange rates Do higher share prices and weaker dollar lead to higher crude oil prices? Akira YANAGISAWA Leader Energy Demand, Supply and Forecast

Main Street. Economic information. By Jason P. Brown, Economist, and Andres Kodaka, Research Associate

THE Main Street ECONOMIST: ECONOMIST Economic information Agricultural for the and Cornhusker Rural Analysis State S e Issue p t e m b2, e r 214 2 1 Feed de er ra al l RR e es se er rv ve e BBa an nk k

THE Main Street ECONOMIST: ECONOMIST Economic information Agricultural for the and Cornhusker Rural Analysis State S e Issue p t e m b2, e r 214 2 1 Feed de er ra al l RR e es se er rv ve e BBa an nk k

Slides prepared by the Northeast Gas Association

Natural gas represents 27% of total energy consumption in the U.S. There are 70 million natural gas customers in the country. Gas is the leading home fuel in the country, and also is a leading fuel of

Natural gas represents 27% of total energy consumption in the U.S. There are 70 million natural gas customers in the country. Gas is the leading home fuel in the country, and also is a leading fuel of

JAMES A. BAKER III INSTITUTE FOR PUBLIC POLICY RICE UNIVERSITY

JAMES A. BAKER III INSTITUTE FOR PUBLIC POLICY RICE UNIVERSITY Testimony of Kenneth B. Medlock III, PhD James A. Baker, III, and Susan G. Baker Fellow in Energy and Resource Economics, and Senior Director,

JAMES A. BAKER III INSTITUTE FOR PUBLIC POLICY RICE UNIVERSITY Testimony of Kenneth B. Medlock III, PhD James A. Baker, III, and Susan G. Baker Fellow in Energy and Resource Economics, and Senior Director,

Regional Short-term Electricity Consumption Models

Regional Short-term Electricity Consumption Models Prepared for Brown Bag Seminar on Forecasting of the Federal Forecasters Consortium (FFC), in alliance with Research Program on Forecasting at The George

Regional Short-term Electricity Consumption Models Prepared for Brown Bag Seminar on Forecasting of the Federal Forecasters Consortium (FFC), in alliance with Research Program on Forecasting at The George

An Analysis of Siting Opportunities for Concentrating Solar Power Plants in the Southwestern United States

An of Siting Opportunities for Concentrating Solar Power Plants in the Southwestern United States Mark S. Mehos National Renewable Energy Laboratory Golden, Colorado Phone: 303-384-7458 Email: mark_mehos@nrel.gov

An of Siting Opportunities for Concentrating Solar Power Plants in the Southwestern United States Mark S. Mehos National Renewable Energy Laboratory Golden, Colorado Phone: 303-384-7458 Email: mark_mehos@nrel.gov

The Weak Tie Between Natural Gas and Oil Prices

The Weak Tie Between Natural Gas and Oil Prices David J. Ramberg* and John E. Parsons** Several recent studies establish that crude oil and natural gas prices are cointegrated. Yet at times in the past,

The Weak Tie Between Natural Gas and Oil Prices David J. Ramberg* and John E. Parsons** Several recent studies establish that crude oil and natural gas prices are cointegrated. Yet at times in the past,

NBER WORKING PAPER SERIES THE PREDICTIVE CONTENT OF ENERGY FUTURES: AN UPDATE ON PETROLEUM, NATURAL GAS, HEATING OIL AND GASOLINE

NBER WORKING PAPER SERIES THE PREDICTIVE CONTENT OF ENERGY FUTURES: AN UPDATE ON PETROLEUM, NATURAL GAS, HEATING OIL AND GASOLINE Menzie D. Chinn Michael LeBlanc Olivier Coibion Working Paper 11033 http://www.nber.org/papers/w11033

NBER WORKING PAPER SERIES THE PREDICTIVE CONTENT OF ENERGY FUTURES: AN UPDATE ON PETROLEUM, NATURAL GAS, HEATING OIL AND GASOLINE Menzie D. Chinn Michael LeBlanc Olivier Coibion Working Paper 11033 http://www.nber.org/papers/w11033

Short-Term Energy Outlook Market Prices and Uncertainty Report

February 2016 Short-Term Energy Outlook Market Prices and Uncertainty Report Crude Oil Prices: The North Sea Brent front month futures price settled at $34.46/b on February 4 $2.76 per barrel (b) below

February 2016 Short-Term Energy Outlook Market Prices and Uncertainty Report Crude Oil Prices: The North Sea Brent front month futures price settled at $34.46/b on February 4 $2.76 per barrel (b) below

Delaware. 2 All data are expressed in terms of 2010 U.S. dollars. These calculations were performed using implicit price deflators

Venture Capital in the Philadelphia Metro Area* Jennifer Knudson October 2011 Many consider venture capital to be a barometer of innovation and economic growth. It is an important source of capital for

Venture Capital in the Philadelphia Metro Area* Jennifer Knudson October 2011 Many consider venture capital to be a barometer of innovation and economic growth. It is an important source of capital for

Energy Efficiency s Role in Getting America Out of Its Energy Straightjacket

Energy Efficiency s Role in Getting America Out of Its Energy Straightjacket R. Neal Elliott, Ph.D., P.E. Industrial Program Director ACEEE Jan-06 Industrial Energy Prices 17.00 15.00 13.00 11.00 9.00

Energy Efficiency s Role in Getting America Out of Its Energy Straightjacket R. Neal Elliott, Ph.D., P.E. Industrial Program Director ACEEE Jan-06 Industrial Energy Prices 17.00 15.00 13.00 11.00 9.00

ANALYSIS OF EUROPEAN, AMERICAN AND JAPANESE GOVERNMENT BOND YIELDS

Applied Time Series Analysis ANALYSIS OF EUROPEAN, AMERICAN AND JAPANESE GOVERNMENT BOND YIELDS Stationarity, cointegration, Granger causality Aleksandra Falkowska and Piotr Lewicki TABLE OF CONTENTS 1.

Applied Time Series Analysis ANALYSIS OF EUROPEAN, AMERICAN AND JAPANESE GOVERNMENT BOND YIELDS Stationarity, cointegration, Granger causality Aleksandra Falkowska and Piotr Lewicki TABLE OF CONTENTS 1.

The price-volume relationship of the Malaysian Stock Index futures market

The price-volume relationship of the Malaysian Stock Index futures market ABSTRACT Carl B. McGowan, Jr. Norfolk State University Junaina Muhammad University Putra Malaysia The objective of this study is

The price-volume relationship of the Malaysian Stock Index futures market ABSTRACT Carl B. McGowan, Jr. Norfolk State University Junaina Muhammad University Putra Malaysia The objective of this study is

PJM Electric Market. PJM Electric Market: Overview and Focal Points. Federal Energy Regulatory Commission Market Oversight www.ferc.

PJM Electric Market: Overview and Focal Points Page 1 of 14 PJM Electric Market Source: Velocity Suite Intelligent Map Updated August 23, 21 145 PJM Electric Market: Overview and Focal Points Page 2 of

PJM Electric Market: Overview and Focal Points Page 1 of 14 PJM Electric Market Source: Velocity Suite Intelligent Map Updated August 23, 21 145 PJM Electric Market: Overview and Focal Points Page 2 of

Statement for the Record

Statement for the Record Kevin R. Hennessy Director Federal, State and Local Affairs New England Dominion Resources, Inc. Infrastructure Needs for Heat and Power Quadrennial Energy Review Task Force April

Statement for the Record Kevin R. Hennessy Director Federal, State and Local Affairs New England Dominion Resources, Inc. Infrastructure Needs for Heat and Power Quadrennial Energy Review Task Force April

Regional Short-term Electricity Consumption Models

Regional Short-term Electricity Consumption Models Prepared for 25 th Annual North American Conference of the USAEE/IAEE, Denver September 18-21, 25 Frederick L. Joutz, Department of Economics The George

Regional Short-term Electricity Consumption Models Prepared for 25 th Annual North American Conference of the USAEE/IAEE, Denver September 18-21, 25 Frederick L. Joutz, Department of Economics The George

Creating more Value out of Storage

Creating more Value out of Storage By Gary Howorth, Founder Energy-Redefined Introduction Gas Storage is a complicated business which carries with it large risks and potentially low rewards. Assets can

Creating more Value out of Storage By Gary Howorth, Founder Energy-Redefined Introduction Gas Storage is a complicated business which carries with it large risks and potentially low rewards. Assets can

Northeastern Winter Gas Outlook New York City remains constrained, but increased Marcellus production is bearish for non-ny deliveries.

? Northeastern Winter Gas Outlook New York City remains constrained, but increased Marcellus production is bearish for non-ny deliveries. Morningstar Commodities Research 2 December Jordan Grimes Sr. Commodities

? Northeastern Winter Gas Outlook New York City remains constrained, but increased Marcellus production is bearish for non-ny deliveries. Morningstar Commodities Research 2 December Jordan Grimes Sr. Commodities

PROJECT EXPERIENCE Development/Transaction Support United States MANAGING DIRECTOR

Peter Abt Mr. Abt is a Managing Director in Black & Veatch s Management Consulting Division. He leads the division s Oil & Gas Strategy practice and holds primary responsibility for client management and

Peter Abt Mr. Abt is a Managing Director in Black & Veatch s Management Consulting Division. He leads the division s Oil & Gas Strategy practice and holds primary responsibility for client management and

Spectra Energy Builds a Business

» Introducing Spectra Energy Builds a Business CEO Fowler on Challenges Ahead By Martin Rosenberg Natural gas once again looms as an important fuel for electricity generation, given a spate of cancellations

» Introducing Spectra Energy Builds a Business CEO Fowler on Challenges Ahead By Martin Rosenberg Natural gas once again looms as an important fuel for electricity generation, given a spate of cancellations

Note No. 141 April 1998. The United States enjoys a highly competitive natural gas market and an increasingly efficient

Privatesector P U B L I C P O L I C Y F O R T H E Note No. 141 April 1998 Development of Competitive Natural Gas Markets in the United States Andrej Juris The United States enjoys a highly competitive

Privatesector P U B L I C P O L I C Y F O R T H E Note No. 141 April 1998 Development of Competitive Natural Gas Markets in the United States Andrej Juris The United States enjoys a highly competitive

North American Natural Gas Midstream Infrastructure Through 2035: A Secure Energy Future

North American Natural Gas Midstream Infrastructure Through 2035: A Secure Energy Future Updated Supply Demand Outlook Background Executive Summary June 28, 2011 Sufficient midstream natural gas infrastructure,

North American Natural Gas Midstream Infrastructure Through 2035: A Secure Energy Future Updated Supply Demand Outlook Background Executive Summary June 28, 2011 Sufficient midstream natural gas infrastructure,

Indiana Utility Regulatory Commission. Natural Gas Forum October 16, 2007

Indiana Utility Regulatory Commission Natural Gas Forum October 16, 2007 1 Today s Objectives Gas Supply Natural Gas Issues Energy efficiency Usage reduction continues Emerging Issues Forecast for Winter

Indiana Utility Regulatory Commission Natural Gas Forum October 16, 2007 1 Today s Objectives Gas Supply Natural Gas Issues Energy efficiency Usage reduction continues Emerging Issues Forecast for Winter

Hedging Natural Gas Prices

Hedging Natural Gas Prices Luke Miller Assistant Professor of Finance Office of Economic Analysis & Business Research School of Business Administration Fort Lewis College Natural Gas Industry U.S. natural

Hedging Natural Gas Prices Luke Miller Assistant Professor of Finance Office of Economic Analysis & Business Research School of Business Administration Fort Lewis College Natural Gas Industry U.S. natural

PREPARED FOR THE OAK RIDGE NATIONAL LABORATORY

NATURAL GAS AND ENERGY PRICE VOLATILITY PREPARED FOR THE OAK RIDGE NATIONAL LABORATORY BY THE 400 NORTH CAPITOL STREET, NW WASHINGTON, DC 20001 PRINCIPAL AUTHORS: BRUCE HENNING, MICHAEL SLOAN, MARIA DE

NATURAL GAS AND ENERGY PRICE VOLATILITY PREPARED FOR THE OAK RIDGE NATIONAL LABORATORY BY THE 400 NORTH CAPITOL STREET, NW WASHINGTON, DC 20001 PRINCIPAL AUTHORS: BRUCE HENNING, MICHAEL SLOAN, MARIA DE

Natural Gas Prices Forecast Comparison - AEO vs. Natural Gas Markets

LBNL-55701 Natural Gas Prices Forecast Comparison - AEO vs. Natural Gas Markets Gabrielle Wong-Parodi, Alex Lekov, and Larry Dale Energy Analysis Department Environmental Energy Technologies Division Ernest

LBNL-55701 Natural Gas Prices Forecast Comparison - AEO vs. Natural Gas Markets Gabrielle Wong-Parodi, Alex Lekov, and Larry Dale Energy Analysis Department Environmental Energy Technologies Division Ernest

Comments and Responses of North Baja Pipeline

Comments and Responses of North Baja Pipeline North Baja Pipeline, LP (North Baja) respectfully submits these comments and responses to the Arizona Corporation Commission (Commission), Utilities Division

Comments and Responses of North Baja Pipeline North Baja Pipeline, LP (North Baja) respectfully submits these comments and responses to the Arizona Corporation Commission (Commission), Utilities Division

seasonal causality in the energy commodities

PROFESSIONAL BRIEFING aestimatio, the ieb international journal of finance, 2011. 3: 02-9 2011 aestimatio, the ieb international journal of finance seasonal causality in the energy commodities Díaz Rodríguez,

PROFESSIONAL BRIEFING aestimatio, the ieb international journal of finance, 2011. 3: 02-9 2011 aestimatio, the ieb international journal of finance seasonal causality in the energy commodities Díaz Rodríguez,

Dynamics of Real Investment and Stock Prices in Listed Companies of Tehran Stock Exchange

Dynamics of Real Investment and Stock Prices in Listed Companies of Tehran Stock Exchange Farzad Karimi Assistant Professor Department of Management Mobarakeh Branch, Islamic Azad University, Mobarakeh,

Dynamics of Real Investment and Stock Prices in Listed Companies of Tehran Stock Exchange Farzad Karimi Assistant Professor Department of Management Mobarakeh Branch, Islamic Azad University, Mobarakeh,

Modeling the US Natural Gas Network

Modeling the US Natural Gas Network James Ellison Sandia National Laboratories, Critical Infrastructure Modeling and Simulation Group Abstract In order to better understand how the US natural gas network

Modeling the US Natural Gas Network James Ellison Sandia National Laboratories, Critical Infrastructure Modeling and Simulation Group Abstract In order to better understand how the US natural gas network

Electricity Costs White Paper

Electricity Costs White Paper ISO New England Inc. June 1, 2006 Table of Contents Executive Summary...1 Highlights of the Analysis...1 Components of Electricity Rates...2 Action Plan for Managing Electricity

Electricity Costs White Paper ISO New England Inc. June 1, 2006 Table of Contents Executive Summary...1 Highlights of the Analysis...1 Components of Electricity Rates...2 Action Plan for Managing Electricity

The Long-Run Relation Between The Personal Savings Rate And Consumer Sentiment

The Long-Run Relation Between The Personal Savings Rate And Consumer Sentiment Bradley T. Ewing 1 and James E. Payne 2 This study examined the long run relationship between the personal savings rate and

The Long-Run Relation Between The Personal Savings Rate And Consumer Sentiment Bradley T. Ewing 1 and James E. Payne 2 This study examined the long run relationship between the personal savings rate and

Stock market booms and real economic activity: Is this time different?

International Review of Economics and Finance 9 (2000) 387 415 Stock market booms and real economic activity: Is this time different? Mathias Binswanger* Institute for Economics and the Environment, University

International Review of Economics and Finance 9 (2000) 387 415 Stock market booms and real economic activity: Is this time different? Mathias Binswanger* Institute for Economics and the Environment, University

UNITED STATES OF AMERICA BEFORE THE FEDERAL ENERGY REGULATORY COMMISSION

UNITED STATES OF AMERICA BEFORE THE FEDERAL ENERGY REGULATORY COMMISSION Coordination between Natural Gas and Electricity Markets Docket No. AD12-12-000 Prepared Statement of Brad Bouillon on behalf of

UNITED STATES OF AMERICA BEFORE THE FEDERAL ENERGY REGULATORY COMMISSION Coordination between Natural Gas and Electricity Markets Docket No. AD12-12-000 Prepared Statement of Brad Bouillon on behalf of

Co-movements of NAFTA trade, FDI and stock markets

Co-movements of NAFTA trade, FDI and stock markets Paweł Folfas, Ph. D. Warsaw School of Economics Abstract The paper scrutinizes the causal relationship between performance of American, Canadian and Mexican

Co-movements of NAFTA trade, FDI and stock markets Paweł Folfas, Ph. D. Warsaw School of Economics Abstract The paper scrutinizes the causal relationship between performance of American, Canadian and Mexican

How Do Energy Suppliers Make Money? Copyright 2015. Solomon Energy. All Rights Reserved.

Bills for electricity and natural gas can be a very high proportion of a company and household budget. Accordingly, the way in which commodity prices are set is of material importance to most consumers.

Bills for electricity and natural gas can be a very high proportion of a company and household budget. Accordingly, the way in which commodity prices are set is of material importance to most consumers.

Changes in the Relationship between Currencies and Commodities

Bank of Japan Review 2012-E-2 Changes in the Relationship between Currencies and Commodities Financial Markets Department Haruko Kato March 2012 This paper examines the relationship between so-called commodity

Bank of Japan Review 2012-E-2 Changes in the Relationship between Currencies and Commodities Financial Markets Department Haruko Kato March 2012 This paper examines the relationship between so-called commodity

The Natural Gas-Electric Interface: Summary of Four Natural Gas-Electric Interdependency Assessments WIEB Staff November 30, 2012

Introduction. The Natural Gas-Electric Interface: Summary of Four Natural Gas-Electric Interdependency Assessments WIEB Staff November 30, 2012 The increased reliance on natural gas as the primary fuel

Introduction. The Natural Gas-Electric Interface: Summary of Four Natural Gas-Electric Interdependency Assessments WIEB Staff November 30, 2012 The increased reliance on natural gas as the primary fuel

An Econometric Assessment of Electricity Demand in the United States Using Panel Data and the Impact of Retail Competition on Prices

9 June 2015 An Econometric Assessment of Electricity Demand in the United States Using Panel Data and the Impact of Retail Competition on Prices By Dr. Agustin J. Ros This paper was originally presented

9 June 2015 An Econometric Assessment of Electricity Demand in the United States Using Panel Data and the Impact of Retail Competition on Prices By Dr. Agustin J. Ros This paper was originally presented

How To Know If Natural Gas Is Cheap Or Expensive

Price Volatility in Today's Energy Markets NATURAL GAS AND ENERGY PRICE VOLATILITY PREPARED FOR THE OAK RIDGE NATIONAL LABORATORY BY THE 400 NORTH CAPITOL STREET, NW WASHINGTON, DC 20001 PRINCIPAL AUTHORS:

Price Volatility in Today's Energy Markets NATURAL GAS AND ENERGY PRICE VOLATILITY PREPARED FOR THE OAK RIDGE NATIONAL LABORATORY BY THE 400 NORTH CAPITOL STREET, NW WASHINGTON, DC 20001 PRINCIPAL AUTHORS:

Revisiting Share Market Efficiency: Evidence from the New Zealand Australia, US and Japan Stock Indices

American Journal of Applied Sciences 2 (5): 996-1002, 2005 ISSN 1546-9239 Science Publications, 2005 Revisiting Share Market Efficiency: Evidence from the New Zealand Australia, US and Japan Stock Indices

American Journal of Applied Sciences 2 (5): 996-1002, 2005 ISSN 1546-9239 Science Publications, 2005 Revisiting Share Market Efficiency: Evidence from the New Zealand Australia, US and Japan Stock Indices

Outlook for the North American and Ontario Gas Markets

Outlook for the North American and Ontario Gas Markets Union Gas Customer Meeting London, Ontario June 5, 2014 Presented by: Frank Brock Senior Energy Market Specialist ICF International Frank.Brock@ICFI.COM

Outlook for the North American and Ontario Gas Markets Union Gas Customer Meeting London, Ontario June 5, 2014 Presented by: Frank Brock Senior Energy Market Specialist ICF International Frank.Brock@ICFI.COM

Chapter 3: Commodity Forwards and Futures

Chapter 3: Commodity Forwards and Futures In the previous chapter we study financial forward and futures contracts and we concluded that are all alike. Each commodity forward, however, has some unique

Chapter 3: Commodity Forwards and Futures In the previous chapter we study financial forward and futures contracts and we concluded that are all alike. Each commodity forward, however, has some unique

The Engle-Granger representation theorem

The Engle-Granger representation theorem Reference note to lecture 10 in ECON 5101/9101, Time Series Econometrics Ragnar Nymoen March 29 2011 1 Introduction The Granger-Engle representation theorem is

The Engle-Granger representation theorem Reference note to lecture 10 in ECON 5101/9101, Time Series Econometrics Ragnar Nymoen March 29 2011 1 Introduction The Granger-Engle representation theorem is

Texas: An Energy and Economic Analysis

Texas: An Energy and Economic Analysis Posted on 9/30/2013 Texas leads the nation in oil and natural gas reserves and production. In just over 2 years, Texas has doubled its oil production with large quantities

Texas: An Energy and Economic Analysis Posted on 9/30/2013 Texas leads the nation in oil and natural gas reserves and production. In just over 2 years, Texas has doubled its oil production with large quantities

WP-07 Power Rate Case Workshop

WP-07 Power Rate Case Workshop Date of Workshop: Topic(s): , Overview Results BPA price forecast and comparison with other forecasts Assumptions Supply and demand fundamentals for the short / medium /

WP-07 Power Rate Case Workshop Date of Workshop: Topic(s): , Overview Results BPA price forecast and comparison with other forecasts Assumptions Supply and demand fundamentals for the short / medium /

A Trading Strategy Based on the Lead-Lag Relationship of Spot and Futures Prices of the S&P 500

A Trading Strategy Based on the Lead-Lag Relationship of Spot and Futures Prices of the S&P 500 FE8827 Quantitative Trading Strategies 2010/11 Mini-Term 5 Nanyang Technological University Submitted By:

A Trading Strategy Based on the Lead-Lag Relationship of Spot and Futures Prices of the S&P 500 FE8827 Quantitative Trading Strategies 2010/11 Mini-Term 5 Nanyang Technological University Submitted By:

The Political Economy of Electricity Markets A Brief History January 10, 2008. Peter Van Doren Senior Fellow Editor, Regulation Cato Institute

The Political Economy of Electricity Markets A Brief History January 10, 2008 Peter Van Doren Senior Fellow Editor, Regulation Cato Institute I. Economists critique of regulated vertically integrated electricity

The Political Economy of Electricity Markets A Brief History January 10, 2008 Peter Van Doren Senior Fellow Editor, Regulation Cato Institute I. Economists critique of regulated vertically integrated electricity

Relationship between Stock Futures Index and Cash Prices Index: Empirical Evidence Based on Malaysia Data

2012, Vol. 4, No. 2, pp. 103-112 ISSN 2152-1034 Relationship between Stock Futures Index and Cash Prices Index: Empirical Evidence Based on Malaysia Data Abstract Zukarnain Zakaria Universiti Teknologi

2012, Vol. 4, No. 2, pp. 103-112 ISSN 2152-1034 Relationship between Stock Futures Index and Cash Prices Index: Empirical Evidence Based on Malaysia Data Abstract Zukarnain Zakaria Universiti Teknologi

THE U.S. CURRENT ACCOUNT: THE IMPACT OF HOUSEHOLD WEALTH

THE U.S. CURRENT ACCOUNT: THE IMPACT OF HOUSEHOLD WEALTH Grant Keener, Sam Houston State University M.H. Tuttle, Sam Houston State University 21 ABSTRACT Household wealth is shown to have a substantial

THE U.S. CURRENT ACCOUNT: THE IMPACT OF HOUSEHOLD WEALTH Grant Keener, Sam Houston State University M.H. Tuttle, Sam Houston State University 21 ABSTRACT Household wealth is shown to have a substantial

The Orthogonal Response of Stock Returns to Dividend Yield and Price-to-Earnings Innovations

The Orthogonal Response of Stock Returns to Dividend Yield and Price-to-Earnings Innovations Vichet Sum School of Business and Technology, University of Maryland, Eastern Shore Kiah Hall, Suite 2117-A

The Orthogonal Response of Stock Returns to Dividend Yield and Price-to-Earnings Innovations Vichet Sum School of Business and Technology, University of Maryland, Eastern Shore Kiah Hall, Suite 2117-A

Expanding Natural Gas Service: Opportunities for American Homes and Business

Expanding Natural Gas Service: Opportunities for American Homes and Business NARUC Staff Subcommittee on Gas Washington, D.C. February 3, 2013 Bruce B. Henning Vice President, Energy Regulatory and Market

Expanding Natural Gas Service: Opportunities for American Homes and Business NARUC Staff Subcommittee on Gas Washington, D.C. February 3, 2013 Bruce B. Henning Vice President, Energy Regulatory and Market

An Analysis of Spot and Futures Prices for Natural Gas: The Roles of Economic Fundamentals, Market Structure, Speculation, and Manipulation

An Analysis of Spot and Futures Prices for Natural Gas: The Roles of Economic Fundamentals, Market Structure, Speculation, and Manipulation Robert J. Shapiro and Nam D. Pham August 2006 S O N E C O N An

An Analysis of Spot and Futures Prices for Natural Gas: The Roles of Economic Fundamentals, Market Structure, Speculation, and Manipulation Robert J. Shapiro and Nam D. Pham August 2006 S O N E C O N An

PETROLEUM WATCH September 16, 2011 Fossil Fuels Office Fuels and Transportation Division California Energy Commission

PETROLEUM WATCH September 16, 2011 Fossil Fuels Office Fuels and Transportation Division California Energy Commission Summary As of September 14, retail regular-grade gasoline prices in California increased

PETROLEUM WATCH September 16, 2011 Fossil Fuels Office Fuels and Transportation Division California Energy Commission Summary As of September 14, retail regular-grade gasoline prices in California increased

CHAO WEI. February 2010. Assistant Professor of Economics at the George Washington University, 2003 - present

CHAO WEI Department of Economics George Washington University Washington, DC 20052 Phone: (202) 994-2374 Fax: (202) 994-6147 E-mail: cdwei@gwu.edu http://home.gwu.edu/~cdwei February 2010 EDUCATION Ph.D.,

CHAO WEI Department of Economics George Washington University Washington, DC 20052 Phone: (202) 994-2374 Fax: (202) 994-6147 E-mail: cdwei@gwu.edu http://home.gwu.edu/~cdwei February 2010 EDUCATION Ph.D.,

Short-Term Energy Outlook Supplement: Summer 2013 Outlook for Residential Electric Bills

Short-Term Energy Outlook Supplement: Summer 2013 Outlook for Residential Electric Bills June 2013 Independent Statistics & Analysis www.eia.gov U.S. Department of Energy Washington, DC 20585 This report

Short-Term Energy Outlook Supplement: Summer 2013 Outlook for Residential Electric Bills June 2013 Independent Statistics & Analysis www.eia.gov U.S. Department of Energy Washington, DC 20585 This report

Luke Saban, Peregrine Midstream Partners. Gas Storage Strategies Financing new asset development and expansion

Luke Saban, Peregrine Midstream Partners Gas Storage Strategies Financing new asset development and expansion How are developers raising capital for new asset construction: Good projects with contracted

Luke Saban, Peregrine Midstream Partners Gas Storage Strategies Financing new asset development and expansion How are developers raising capital for new asset construction: Good projects with contracted

ENERGY ADVISORY COMMITTEE. Electricity Market Review : Electricity Tariff

ENERGY ADVISORY COMMITTEE Electricity Market Review : Electricity Tariff The Issue To review the different tariff structures and tariff setting processes being adopted in the electricity supply industry,

ENERGY ADVISORY COMMITTEE Electricity Market Review : Electricity Tariff The Issue To review the different tariff structures and tariff setting processes being adopted in the electricity supply industry,

Efficient Retail Pricing in Electricity and Natural Gas Markets

Efficient Retail Pricing in Electricity and Natural Gas Markets Steven L. Puller Department of Economics Texas A&M University and NBER Jeremy West Department of Economics Texas A&M University January 2013

Efficient Retail Pricing in Electricity and Natural Gas Markets Steven L. Puller Department of Economics Texas A&M University and NBER Jeremy West Department of Economics Texas A&M University January 2013

Natural Gas Monthly. May 2016. Office of Oil, Gas, and Coal Supply Statistics www.eia.gov. U.S. Department of Energy Washington, DC 20585

Natural Gas Monthly May 2016 Office of Oil, Gas, and Coal Supply Statistics www.eia.gov U.S. Department of Energy Washington, DC 20585 This report was prepared by the U.S. Energy Information Administration

Natural Gas Monthly May 2016 Office of Oil, Gas, and Coal Supply Statistics www.eia.gov U.S. Department of Energy Washington, DC 20585 This report was prepared by the U.S. Energy Information Administration

Understanding. Natural Gas Markets

Understanding Natural Gas Markets Table of Contents Overview 1 The North American Natural Gas Marketplace 3 Understanding Natural Gas Markets Natural Gas Demand 9 Natural Gas Supply 12 Summary 25 Glossary

Understanding Natural Gas Markets Table of Contents Overview 1 The North American Natural Gas Marketplace 3 Understanding Natural Gas Markets Natural Gas Demand 9 Natural Gas Supply 12 Summary 25 Glossary

IS THERE A LONG-RUN RELATIONSHIP

7. IS THERE A LONG-RUN RELATIONSHIP BETWEEN TAXATION AND GROWTH: THE CASE OF TURKEY Salih Turan KATIRCIOGLU Abstract This paper empirically investigates long-run equilibrium relationship between economic