Infrastructure Financing Models A US Perspective

|

|

|

- Briana Barton

- 8 years ago

- Views:

Transcription

1 Infrastructure Financing Models A US Perspective T. Theis, Director IESP UIC M. Krause, Kandiyo Consulting, Minneapolis MN M. Pagano, Dean of Urban Planning/Dean of Business UIC R. Weber, Professor of Urban Planning UIC T. Brecheisen, Ph.D. Student UIC ibuild Assembly November 13-15

2 Outline Background General Observations on Municipal Financing Integration of Design and Financing Value Capture Model Tax Increment Financing Concluding Remarks

3 Background Rapidly changing fiscal and political context in which municipalities operate Steep federal government spending cuts for redevelopment activities Restrictions on tax-exempt bonds Devolution of urban policy to more local levels of government Tax-payer revolts leading to limits on property tax collections Heightened awareness of corporate welfare, leading to increased scrutiny of corporate tax breaks

4

5 Spatialization and Revenue Structures Why promote development or a certain type of development at a particular location? Given a choice, parcels will be identified for development that maximize revenues or minimize costs. The mini-max incentive embedded within the context of a city s revenue structure manifests itself spatially in the design, land-use designations and development patterns of the city, or the spatialization of revenue structure.

6 General Observations on Municipal Financing* STRATEGIC BEHAVIOR OF PROPERTY-TAX CITIES Property-tax cities think strategically about development based on the market value of the development and on the possibility of shifting service-delivery costs to other jurisdictions (fiscal externalities). Characteristics: Concentric urban structure Clear physical and historic identity High-end residences close to center High-end office and retail in center Examples: Most large US cities (e.g. Chicago) *Adapted from Ann O M. Bowman and Michael A. Pagano, Terra Incognita: Vacant Land and Urban Strategies (Washington, DC: Georgetown University Press, 2004).

7

8 STRATEGIC BEHAVIOR OF SALES-TAX CITIES Sales-tax cities think strategically about development based on their mental constructs of shopping sheds and on which market transactions are taxable. Characteristics: Development pressure at urban edge Tax dollars drawn across city borders Development formulaic Urban center languishes Examples: Cities where the cost of municipal services is greater than property tax levies often in southern and southwestern US Many suburban municipalities adjacent to large cities

9 STRATEGIC BEHAVIOR OF INCOME-TAX CITIES Income-tax cities think strategically about development based on their assessment of the income growth potential of the individual or firm. Characteristics: Development less formulaic Development locations idiosyncratic Results depend on from whom the tax is collected Income tax seeks employed, high income residents Commuter tax targets public development projects and pushes private job creation Examples: Income tax--most cities in Ohio Commuter tax Cities in Kentucky, Detroit, Philadelphia

10 Integration of Design with Financing* Multi-functionality and multi-benefit designs allow financing from multiple sources e.g. Complete streets : transportation, walkability, stormwater control Transit-oriented development: public transit, mixed use residential/commercial Sustainable designs: social equity, economic viability, environmental quality Environmental justice: local employment, local expertise and firms, affordable housing, public art, living walls /green roofs Enhance upstream financing Infrastructure trusts, TIFs, Grants Peel off downstream costs Tax advantages Invest in efficiencies and integrate synergies LEED certification Conserve embodied energy Life cycle costing Solar, geothermal, wind credits Accelerated depreciation Innovative design-build contracting/benchmarking Guarantee energy savings Sourcing local/green materials Free up long term capital *From Michael Krause, Kandiyo Consulting, LLC, Minneapolis MN

11 New York Boston San Francisco

12 Life Cycle Energy Expenditures the Value of Transit-Oriented Development Chicago Center for Green Technology (CCGT) Sigma Consulting Milwaukee WI

13 Terajoules (TJ) Lifetime Embodied Energy Comparison Transportation Energy Building Natural Gas Building Electricity Building Assembly Brownfield Remediation CCGT (10 years) SIGMA (9 years)

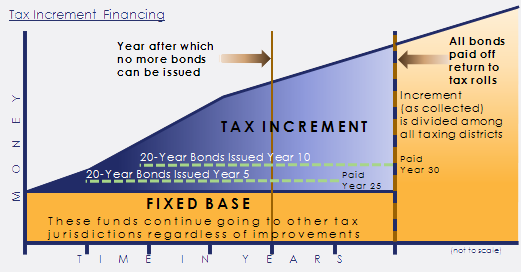

14 Tax Increment Financing (TIF)* TIF districts are designated by local authorities (under Stateenabled legislation and according to local redevelopment plans) as blighted, i.e. normal development and occupancy are undesirable or impossible due to cessation of growth, deterioration of infrastructure, age or obsolescence of the area, character of occupancy, or presence of substandard buildings Reallocation of property tax revenues within a TIF district for approved project or projects Earmark future growth in ad valorem property tax revenues to pay for initial and ongoing development *Adapted from: Weber, R. Tax Incremental Financing in Theory and Practice pp in Financing Economic Development in the 21 st Century, 2 nd edition, S. White, and Z. Kotval editors, ME Sharp (New York, 2013).

15

16 Mechanics of TIF Once designated, the initial assessed property valuation in the district is held constant (or nearly so) for a specific period of time (~20-25 years). This is the base. Municipal authority makes improvements in the area to attract private investors, (who may also receive TIF incentives hence public-private partnerships). With private investment, assessed valuations are expected to rise, creating a tax increment which trickles in over time. This means that TIF increments are committed in advance of being generated, since most development costs accrue up front. Two major ways of financing TIF debt: Revenue bonds issued by the redevelopment corporation, or in some instances general obligation bonds issued by the municipality Developer financing (through lending institutions)

17 Popularity of TIF In response local funding strategies have evolved that rely less on federal funds, circumvent state or locally imposed revenue and spending limits, and at least superficially do not resemble give aways. For property tax-type municipalities, TIF is a major element of these strategies: It is a locally derived, self-financing system Doesn t count against state-imposed debt limits Particularly useful for large redevelopment projects Perceived as less of a drain on public resources Flexible tool (relative ease of initiating, can be used for a variety of development including human resource-focused)

18

19

20 ~ 30% of Chicago is now TIF-designated

21 Former US Steel South Works Phase 1: $97M TIF, $300M private

22 But there are disadvantages and problems Lower tax revenues for ongoing services and non-tif projects (schools, parks, transportation, maintenance, housing, human resource programs) Possibility of lower growth of tax revenues in non-tif regions Gentrification and the subsequent affordability of the area for existing residents Lack of oversight--arguable instances of excessive favorability to developers Other issues Questionable degrees of blightedness Overly rosy projections of tax increments Poaching of retail from adjacent non-tif areas year frozen tax base is excessive

23

Buncombe County Project Development Financing Policy

P and Buncombe County Project Development Financing Policy Overview: Project Development Financing (also known as Tax Increment Financing (TIF)) is a financial tool used by local governments to promote

P and Buncombe County Project Development Financing Policy Overview: Project Development Financing (also known as Tax Increment Financing (TIF)) is a financial tool used by local governments to promote

Tax Increment Financing in Polk County

Tax Increment Financing in Polk County By Peter S. Fisher and Michael Lipsman As Tax Increment Financing (TIF) faces new scrutiny this year by taxpayers, local officials and state legislators, it is important

Tax Increment Financing in Polk County By Peter S. Fisher and Michael Lipsman As Tax Increment Financing (TIF) faces new scrutiny this year by taxpayers, local officials and state legislators, it is important

to provide a framework within which the City Council and Mayor can evaluate and compare proposed uses of tax increment financing TIF; and

Note: Minneapolis Tax Increment Financing Policy Proposed Amendment July 8, 2011; Revised October 12, 2011 Additions proposed in the July 8 version are indicated by underlining; deletions are indicated

Note: Minneapolis Tax Increment Financing Policy Proposed Amendment July 8, 2011; Revised October 12, 2011 Additions proposed in the July 8 version are indicated by underlining; deletions are indicated

ARTICLE 345. Tax Incremental Financing Plan

ARTICLE 345 Tax Incremental Financing Plan 345.01 Definitions 345.02 Boundaries of the District 345.03 Creation and Term of District 345.04 Name of District 345.05 Legislative Findings 345.06 Approval

ARTICLE 345 Tax Incremental Financing Plan 345.01 Definitions 345.02 Boundaries of the District 345.03 Creation and Term of District 345.04 Name of District 345.05 Legislative Findings 345.06 Approval

Public Finance. Creative Financings that Build Communities. Attorney Advertising

Public Finance Creative Financings that Build Communities Attorney Advertising After serving as counsel in billions of dollars of financings, we understand how to achieve our clients financial objectives

Public Finance Creative Financings that Build Communities Attorney Advertising After serving as counsel in billions of dollars of financings, we understand how to achieve our clients financial objectives

Tashman Johnson LLC Consultants in Policy, Planning & Project Management

Tashman Johnson LLC Consultants in Policy, Planning & Project Management AN OVERVIEW OF URBAN RENEWAL Tashman Johnson LLC Jeffrey Tashman 503.245.7828 Nina Johnson 503.245.7416 Fax 503.245.3171 6585 S.W.

Tashman Johnson LLC Consultants in Policy, Planning & Project Management AN OVERVIEW OF URBAN RENEWAL Tashman Johnson LLC Jeffrey Tashman 503.245.7828 Nina Johnson 503.245.7416 Fax 503.245.3171 6585 S.W.

FIVE YEAR FINANCIAL PLAN BYLAW, 2015 BYLAW NO. 15-025

FIVE YEAR FINANCIAL PLAN BYLAW, 2015 BYLAW NO. 15-025 This consolidation is a copy of a bylaw consolidated under the authority of section 139 of the Community Charter. (Consolidated on September 1, 2015

FIVE YEAR FINANCIAL PLAN BYLAW, 2015 BYLAW NO. 15-025 This consolidation is a copy of a bylaw consolidated under the authority of section 139 of the Community Charter. (Consolidated on September 1, 2015

CRC Notes. What is tax increment financing? FINANCING COEXIST MILLAGES ICHIGAN?

2013-01 A publication of the Citizens Researc esearch Council of Michig higan January 2013 CAN AN DEDIC EDICATED MILLAGES AND TAX INCREMENT FINANCING COEXIST IN MICHIGAN ICHIGAN? Since 1975, Michigan cities,

2013-01 A publication of the Citizens Researc esearch Council of Michig higan January 2013 CAN AN DEDIC EDICATED MILLAGES AND TAX INCREMENT FINANCING COEXIST IN MICHIGAN ICHIGAN? Since 1975, Michigan cities,

The primary focus of state and local government is to provide basic services,

Tax Relief and Local Government The primary focus of state and local government is to provide basic services, such as public safety, education, a safety net of health care and human services, transportation,

Tax Relief and Local Government The primary focus of state and local government is to provide basic services, such as public safety, education, a safety net of health care and human services, transportation,

Project Financing Tools

OVERVIEW The City of Ramsey has a number of financial tools available for economic development projects. In general, tools include gap financing loans, SBA loans/loan guarantees and project based local

OVERVIEW The City of Ramsey has a number of financial tools available for economic development projects. In general, tools include gap financing loans, SBA loans/loan guarantees and project based local

HB 15-1348 What does it mean to me?

HB 15-1348 What does it mean to me? Presented by Carolynne C. White June 18, 2015 1 June 22, 2015 Does HB 15-1348 apply to my urban renewal plan or authority? If you form a new urban renewal authority

HB 15-1348 What does it mean to me? Presented by Carolynne C. White June 18, 2015 1 June 22, 2015 Does HB 15-1348 apply to my urban renewal plan or authority? If you form a new urban renewal authority

City of Chicago TAX INCREMENT FINANCING POLICY GUIDELINES

TAX INCREMENT FINANCING POLICY GUIDELINES Department of Housing and Economic Development 121 N. LaSalle St. #1000 Chicago, IL 60602 2012 Policy guidelines for the Tax Increment Financing program are subject

TAX INCREMENT FINANCING POLICY GUIDELINES Department of Housing and Economic Development 121 N. LaSalle St. #1000 Chicago, IL 60602 2012 Policy guidelines for the Tax Increment Financing program are subject

Understanding Value Capture as a Transportation Finance Strategy in Massachusetts. March 15, 2013

Understanding Value Capture as a Transportation Finance Strategy in Massachusetts March 15, 2013 Background The Massachusetts Legislature will soon explore options to increase transportation revenue. One

Understanding Value Capture as a Transportation Finance Strategy in Massachusetts March 15, 2013 Background The Massachusetts Legislature will soon explore options to increase transportation revenue. One

Financing Solar Energy for Affordable Housing Projects. May 2009

Financing Solar Energy for Affordable Housing Projects May 2009 Overview Photovoltaic Systems. Installations of photovoltaic systems on the customer side (as opposed to the utility side) of the meter have

Financing Solar Energy for Affordable Housing Projects May 2009 Overview Photovoltaic Systems. Installations of photovoltaic systems on the customer side (as opposed to the utility side) of the meter have

COMMUNITY DEVELOPMENT TOOLS AND TRENDS BRIDGING THE FINANCING GAP APRIL 2, 2015

COMMUNITY DEVELOPMENT TOOLS AND TRENDS BRIDGING THE APRIL 2, 2015 FINANCING GAP Economic Development Finance Leveraging public resources through proactive approaches that solve the needs of industry, business,

COMMUNITY DEVELOPMENT TOOLS AND TRENDS BRIDGING THE APRIL 2, 2015 FINANCING GAP Economic Development Finance Leveraging public resources through proactive approaches that solve the needs of industry, business,

Headwaters Economics Updated January 2014

How New Mexico Returns Unconventional Oil Revenue to Local Governments Headwaters Economics Updated January 2014 Introduction This brief shows how New Mexico s local governments receive production tax

How New Mexico Returns Unconventional Oil Revenue to Local Governments Headwaters Economics Updated January 2014 Introduction This brief shows how New Mexico s local governments receive production tax

TIF For Affordable Housing

TIF For Affordable Housing Presented to Governor s Conference on Affordable Housing Stephen B. Friedman, President How TIF Works 1 Eligibility Basics Blight, Conservation, or Vacant Land Factors 13 Factors

TIF For Affordable Housing Presented to Governor s Conference on Affordable Housing Stephen B. Friedman, President How TIF Works 1 Eligibility Basics Blight, Conservation, or Vacant Land Factors 13 Factors

City of Orlando Economic Development Tools for Job Growth and Economic Prosperity

City of Orlando Economic Development Tools for Job Growth and Economic Prosperity Orlando s Current Economic Climate Well positioned to recover from the recession. The fastest-growing metro area in Florida

City of Orlando Economic Development Tools for Job Growth and Economic Prosperity Orlando s Current Economic Climate Well positioned to recover from the recession. The fastest-growing metro area in Florida

How Texas Returns Unconventional Oil Revenue to Local Governments

How Texas Returns Unconventional Oil Revenue to Local Governments Headwaters Economics Updated January 2014 Introduction This brief shows how Texas s local governments receive production tax revenue from

How Texas Returns Unconventional Oil Revenue to Local Governments Headwaters Economics Updated January 2014 Introduction This brief shows how Texas s local governments receive production tax revenue from

Tax Increment Financing and Affordable Housing in Minnesota: The very BASICS. Bill Reinke Central Minnesota Housing Partnership (CMHP)

") Tax Increment Financing and Affordable Housing in Minnesota: The very BASICS Bill Reinke Central Minnesota Housing Partnership (CMHP) What is TIF? Tax increment financing (TIF) is a public financing method

Tax Increment Financing and Affordable Housing in Minnesota: The very BASICS Bill Reinke Central Minnesota Housing Partnership (CMHP) What is TIF? Tax increment financing (TIF) is a public financing method

COMPREHENSIVE PLAN HOUSING ELEMENT

COMPREHENSIVE PLAN HOUSING ELEMENT Policy Document CHAPTER 3: HOUSING ELEMENT TABLE OF CONTENTS Chapter 3: HOUSING ELEMENT... 1 INTRODUCTION... 2 GOALS, OBJECTIVES AND POLICIES... 3 Goal: Housing... 3

COMPREHENSIVE PLAN HOUSING ELEMENT Policy Document CHAPTER 3: HOUSING ELEMENT TABLE OF CONTENTS Chapter 3: HOUSING ELEMENT... 1 INTRODUCTION... 2 GOALS, OBJECTIVES AND POLICIES... 3 Goal: Housing... 3

MEGA applications are awarded at the discretion of the CEO of the Michigan Economic Development Corporation (MEDC) and the MEGA board.

and the MEGA board.") Tax Incentives Lakeshore Economic Development Tools: The following is a list of tools that our staff has extensive knowldege in working with. Not all programs are appropriate for all situations. Our Staff

Tax Incentives Lakeshore Economic Development Tools: The following is a list of tools that our staff has extensive knowldege in working with. Not all programs are appropriate for all situations. Our Staff

MICHIGAN ASSOCIATION of COUNTY TREASURERS. Tax Increment Financing Programs: An Interactive Overview

MICHIGAN ASSOCIATION of COUNTY TREASURERS Tax Increment Financing Programs: An Interactive Overview August 12, 2013 Thompsonville, MI Authorities using Tax Increment Financing 1. DDAs 2. TIFAs 3. LDFAs

MICHIGAN ASSOCIATION of COUNTY TREASURERS Tax Increment Financing Programs: An Interactive Overview August 12, 2013 Thompsonville, MI Authorities using Tax Increment Financing 1. DDAs 2. TIFAs 3. LDFAs

Welcome. From the President. To the Residents of Cook County,

Welcome From the President To the Residents of Cook County, Cook County is the economic engine that drives our region. It holds the majority of the region's jobs, population and businesses. Economic development

Welcome From the President To the Residents of Cook County, Cook County is the economic engine that drives our region. It holds the majority of the region's jobs, population and businesses. Economic development

Dr. Dave. Do state and local economic development tax incentives help state and local economies?

Dr. Dave. Do state and local economic development tax incentives help state and local economies? A. In the vast majority of cases, the answer is no. Robert G. Lynch, Chairman of the Department of Economics

Dr. Dave. Do state and local economic development tax incentives help state and local economies? A. In the vast majority of cases, the answer is no. Robert G. Lynch, Chairman of the Department of Economics

GREEN BUILDING INCENTIVES GUIDE

GREEN BUILDING INCENTIVES GUIDE AUGUST 2013 A Comprehensive Collection of the Latest Green Financial Incentives in Western Pennsylvania and Beyond. Do you want to build or retrofit a space to be healthy

GREEN BUILDING INCENTIVES GUIDE AUGUST 2013 A Comprehensive Collection of the Latest Green Financial Incentives in Western Pennsylvania and Beyond. Do you want to build or retrofit a space to be healthy

Southwest Center Mall: Moving Forward. Economic Development Committee August 17, 2009

Southwest Center Mall: Moving Forward Economic Development Committee August 17, 2009 1 Background Southern Dallas Task Force Southwest Oak Cliff Work Team identified redevelopment of Southwest Center Mall

Southwest Center Mall: Moving Forward Economic Development Committee August 17, 2009 1 Background Southern Dallas Task Force Southwest Oak Cliff Work Team identified redevelopment of Southwest Center Mall

EXPERIENCE INVESTMENT MANAGEMENT & REAL ESTATE SERVICES

INVESTMENT & REAL ESTATE SERVICES Who We Are A trusted advisor. A consistent presence. A valued resource. Forest City Investment Management & Real Estate Services is the investment management and third-party

INVESTMENT & REAL ESTATE SERVICES Who We Are A trusted advisor. A consistent presence. A valued resource. Forest City Investment Management & Real Estate Services is the investment management and third-party

Olmsted County Regional Housing Needs Forum. Stacie Kvilvang Ehlers

Olmsted County Regional Housing Needs Forum Stacie Kvilvang Ehlers July 23, 2014 1 Housing Finance Tools and Strategies Tax Increment Financing Tax Abatement HRA Levy Creative uses of local funds Public

Olmsted County Regional Housing Needs Forum Stacie Kvilvang Ehlers July 23, 2014 1 Housing Finance Tools and Strategies Tax Increment Financing Tax Abatement HRA Levy Creative uses of local funds Public

TABLE OF CONTENTS INTRODUCTION...1 SECTION I TIF GENERAL POLICIES AND GUIDELINES...2 A. TIF POLICIES AND GUIDELINES...2 B. TIF REVIEW COMMITTEE...

!" TABLE OF CONTENTS INTRODUCTION...1 SECTION I TIF GENERAL POLICIES AND GUIDELINES...2 A. TIF POLICIES AND GUIDELINES...2 B. TIF REVIEW COMMITTEE...3 C. REDEVELOPMENT PLAN AND PROJECT CRITERIA...3 D.

!" TABLE OF CONTENTS INTRODUCTION...1 SECTION I TIF GENERAL POLICIES AND GUIDELINES...2 A. TIF POLICIES AND GUIDELINES...2 B. TIF REVIEW COMMITTEE...3 C. REDEVELOPMENT PLAN AND PROJECT CRITERIA...3 D.

SUMMARY OF THE MISSOURI REAL PROPERTY TAX INCREMENT ALLOCATION REDEVELOPMENT ACT

SUMMARY OF THE MISSOURI REAL PROPERTY TAX INCREMENT ALLOCATION REDEVELOPMENT ACT PREPARED BY: JAMES E. MELLO ROBERT D. KLAHR LAUREN ASHLEY SMITH ARMSTRONG TEASDALE LLP 7700 FORSYTH BOULEVARD, SUITE 1800

SUMMARY OF THE MISSOURI REAL PROPERTY TAX INCREMENT ALLOCATION REDEVELOPMENT ACT PREPARED BY: JAMES E. MELLO ROBERT D. KLAHR LAUREN ASHLEY SMITH ARMSTRONG TEASDALE LLP 7700 FORSYTH BOULEVARD, SUITE 1800

Infrastructure Financing Programs

Infrastructure Financing Programs March 16, 2013 Massachusetts Development Finance Agency Self-supported quasi-public finance and development agency. Promotes capital investment and economic development

Infrastructure Financing Programs March 16, 2013 Massachusetts Development Finance Agency Self-supported quasi-public finance and development agency. Promotes capital investment and economic development

AN INTRODUCTION TO MUNICIPAL LEASE FINANCING: ANSWERS TO FREQUENTLY ASKED QUESTIONS

AN INTRODUCTION TO MUNICIPAL LEASE FINANCING: ANSWERS TO FREQUENTLY ASKED QUESTIONS Dated July 1, 2000 Copyright 2000. Association for Governmental Leasing & Finance, Washington, DC. All rights reserved.

AN INTRODUCTION TO MUNICIPAL LEASE FINANCING: ANSWERS TO FREQUENTLY ASKED QUESTIONS Dated July 1, 2000 Copyright 2000. Association for Governmental Leasing & Finance, Washington, DC. All rights reserved.

DELAWARE, MARYLAND, AND NEW YORK BUSINESS DEVELOPMENT TAX INCENTIVES

February 17, 2015 Office of Legislative Research Research Report 2015-R-0018 DELAWARE, MARYLAND, AND NEW YORK BUSINESS DEVELOPMENT TAX INCENTIVES By: Rute Pinho, Principal Analyst Heather Poole, Legislative

February 17, 2015 Office of Legislative Research Research Report 2015-R-0018 DELAWARE, MARYLAND, AND NEW YORK BUSINESS DEVELOPMENT TAX INCENTIVES By: Rute Pinho, Principal Analyst Heather Poole, Legislative

Question: What revenue options are being considered? Answer: A public service tax, a fire services assessment and property taxes.

REVENUE OPTIONS FOR ECONOMIC SUSTAINABILITY Updated 4-25-13 (New Information in Green) Question: Why is the City going to be out of money? Answer: The City needs more revenue to maintain services and begin

REVENUE OPTIONS FOR ECONOMIC SUSTAINABILITY Updated 4-25-13 (New Information in Green) Question: Why is the City going to be out of money? Answer: The City needs more revenue to maintain services and begin

Tax Increment Financing

Tax Increment Financing Set aside new "incremental" tax revenues to raise financing for a project or public improvements. Financing can be on pay as you go basis, debt, or developer financing Base year

Tax Increment Financing Set aside new "incremental" tax revenues to raise financing for a project or public improvements. Financing can be on pay as you go basis, debt, or developer financing Base year

SBA 504 Loan Program. Presented by Linda Reilly Acting Director Office of Financial Assistance/ 504 Program Chief U.S. Small Business Administration

SBA 504 Loan Program Presented by Linda Reilly Acting Director Office of Financial Assistance/ 504 Program Chief U.S. Small Business Administration SBA 504 Loan Program It s an Economic Development Financing

SBA 504 Loan Program Presented by Linda Reilly Acting Director Office of Financial Assistance/ 504 Program Chief U.S. Small Business Administration SBA 504 Loan Program It s an Economic Development Financing

City of Missoula Debt Management. Major Bond Issues. Outstanding Debt DEBT MANAGEMENT. City of Missoula FY 2015 Annual Budget Page I - 1

City of Missoula Debt Management Debt in a governmental entity is an effective financial management tool. Active debt management provides fiscal advantages to the City of Missoula and its citizens. Debt

City of Missoula Debt Management Debt in a governmental entity is an effective financial management tool. Active debt management provides fiscal advantages to the City of Missoula and its citizens. Debt

Innovative Financing Options for State of Good Repair Investments

Innovative Financing Options for State of Good Repair Investments Tools and Case Studies Presented by: Jeffrey D. Ensor Parsons Brinckerhoff PB Strategic Consulting Washington, DC ensor@pbworld.com 1.202.661.5317

Innovative Financing Options for State of Good Repair Investments Tools and Case Studies Presented by: Jeffrey D. Ensor Parsons Brinckerhoff PB Strategic Consulting Washington, DC ensor@pbworld.com 1.202.661.5317

ENERGY EFFICIENCY AND RENEWABLE ENERGY TAX INCENTIVES FEDERAL AND STATE ENERGY TAX PROGRAMS JEROME L. GARCIANO

ENERGY EFFICIENCY AND RENEWABLE ENERGY TAX INCENTIVES FEDERAL AND STATE ENERGY TAX PROGRAMS JEROME L. GARCIANO JULY 2013 Renewable Energy and Green Building Tax Incentives Federal and State Energy Tax

ENERGY EFFICIENCY AND RENEWABLE ENERGY TAX INCENTIVES FEDERAL AND STATE ENERGY TAX PROGRAMS JEROME L. GARCIANO JULY 2013 Renewable Energy and Green Building Tax Incentives Federal and State Energy Tax

ECONOMIC DEVELOPMENT INVESTMENT POLICY May 2008

ECONOMIC DEVELOPMENT INVESTMENT POLICY May 2008 Cedar Rapids, a vibrant urban hometown a beacon for people and businesses invested in building a greater community for the next generation. 1.0 Background

ECONOMIC DEVELOPMENT INVESTMENT POLICY May 2008 Cedar Rapids, a vibrant urban hometown a beacon for people and businesses invested in building a greater community for the next generation. 1.0 Background

SCHOOL LOCAL PROPERTY TAX OPTION 1999 Legislation

STATE OF OREGON LEGISLATIVE REVENUE OFFICE H-197 State Capitol Building Salem, Oregon 97310-1347 Research Report (503) 986-1266 Research Report # 5-99 SCHOOL LOCAL PROPERTY TAX OPTION 1999 Legislation

STATE OF OREGON LEGISLATIVE REVENUE OFFICE H-197 State Capitol Building Salem, Oregon 97310-1347 Research Report (503) 986-1266 Research Report # 5-99 SCHOOL LOCAL PROPERTY TAX OPTION 1999 Legislation

county Tax Planning - The White Flint Sector Plan Area of Montgomery, Maryland

Resolution No.: Introduced: Adopted: 16-1570 October 5,2010 November 30, 2010 COUNTY COUNCIL FOR MONTGOlVIERY COUNTY, MARYLAND By: Council President at the Request of the County Executive SUBJECT: White

Resolution No.: Introduced: Adopted: 16-1570 October 5,2010 November 30, 2010 COUNTY COUNCIL FOR MONTGOlVIERY COUNTY, MARYLAND By: Council President at the Request of the County Executive SUBJECT: White

New York City Independent Budget Office Fiscal Brief

IBO New York City Independent Budget Office Fiscal Brief September 2002 Learning from Experience: A Primer on Tax Increment Financing SUMMARY To fund the estimated $1.5 billion extension of the No. 7 subway

IBO New York City Independent Budget Office Fiscal Brief September 2002 Learning from Experience: A Primer on Tax Increment Financing SUMMARY To fund the estimated $1.5 billion extension of the No. 7 subway

Economic Development Strategy.

Economic Development Strategy. j Prepared by: Wendy Ford, Economic Development Coordinator, 410 E. Washington St., Iowa City, IA 52240 319) 356-5248 RESOLUTION NO. 11-180 RESOLUTION ADOPTING CITY OF IOWA

Economic Development Strategy. j Prepared by: Wendy Ford, Economic Development Coordinator, 410 E. Washington St., Iowa City, IA 52240 319) 356-5248 RESOLUTION NO. 11-180 RESOLUTION ADOPTING CITY OF IOWA

Revitalization Tax Exemptions. A Primer on the Provisions in the Community Charter

Revitalization Tax Exemptions A Primer on the Provisions in the Community Charter January 2008 REVITALIZATION TAX EXEMPTIONS Legislation Section 226 of the Community Charter provides authority to exempt

Revitalization Tax Exemptions A Primer on the Provisions in the Community Charter January 2008 REVITALIZATION TAX EXEMPTIONS Legislation Section 226 of the Community Charter provides authority to exempt

MULTI-FAMILY DEVELOPMENT AND INVESTMENT

MULTI-FAMILY DEVELOPMENT AND INVESTMENT IT S ALL ABOUT LIVING HIGH STREET RESIDENTIAL, a wholly-owned operating subsidiary of Trammell Crow Company, specializes in the development of multifamily housing.

MULTI-FAMILY DEVELOPMENT AND INVESTMENT IT S ALL ABOUT LIVING HIGH STREET RESIDENTIAL, a wholly-owned operating subsidiary of Trammell Crow Company, specializes in the development of multifamily housing.

Policy No.: F-7 CITY OF OLATHE COUNCIL POLICY STATEMENT. Date Issued: 12-15-15. Effective Date: 1-1-16. Cancellation Date: 12-31-17

CITY OF OLATHE COUNCIL POLICY STATEMENT Policy No.: F-7 Date Issued: 12-15-15 General Scope: Specific Subject: Finance Tax Increment Financing Policy Effective Date: 1-1-16 Cancellation Date: 12-31-17

CITY OF OLATHE COUNCIL POLICY STATEMENT Policy No.: F-7 Date Issued: 12-15-15 General Scope: Specific Subject: Finance Tax Increment Financing Policy Effective Date: 1-1-16 Cancellation Date: 12-31-17

How To Get Rid Of Property Tax In Pennsylvania

Personal Property Tax Reform Legislation By David Zin, Chief Economist On December 27, 2012, the Governor signed Public Acts (PAs) 397 through 404 of 2012, as well as PAs 406, 407, and 408. Public Acts

Personal Property Tax Reform Legislation By David Zin, Chief Economist On December 27, 2012, the Governor signed Public Acts (PAs) 397 through 404 of 2012, as well as PAs 406, 407, and 408. Public Acts

MEMORANDUM. Corinne Verdery, NBC Universal. Paul J. Silvern and David Berneman. Date: November 4, 2012

MEMORANDUM To: From: Corinne Verdery, NBC Universal Paul J. Silvern and David Berneman Date: November 4, 2012 Re: Supplemental Analysis of Tax Revenue Impacts in the City of Los Angeles from the Proposed

MEMORANDUM To: From: Corinne Verdery, NBC Universal Paul J. Silvern and David Berneman Date: November 4, 2012 Re: Supplemental Analysis of Tax Revenue Impacts in the City of Los Angeles from the Proposed

PROPERTY TAX RELIEF VIA INCENTIVES AND ABATEMENT PROGRAMS. COST Property Tax Workshop. Dallas January 2015

PROPERTY TAX RELIEF VIA INCENTIVES AND ABATEMENT PROGRAMS COST Property Tax Workshop Dallas January 2015 Thomas T. Dubel, Jr., CPA Director, State & Local Tax and Advisory Altus Group US Inc. 910 Ridgebrook

PROPERTY TAX RELIEF VIA INCENTIVES AND ABATEMENT PROGRAMS COST Property Tax Workshop Dallas January 2015 Thomas T. Dubel, Jr., CPA Director, State & Local Tax and Advisory Altus Group US Inc. 910 Ridgebrook

The "Total (Memorandum Only)" column is the aggregate of the columns being presented and does not represent consolidated financial information.

column is the aggregate of the columns being presented and does not represent consolidated financial information.") City of Madison NOTES TO COMBINED FINANCIAL STATEMENTS December 31, 1999 NOTE A - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES The following is a summary of the City's significant accounting policies consistently

City of Madison NOTES TO COMBINED FINANCIAL STATEMENTS December 31, 1999 NOTE A - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES The following is a summary of the City's significant accounting policies consistently

No. 1040 A publication of the Citizens Research Council of Michigan February 1996

Government Research Since 1916 CRC Memorandum No. 1040 A publication of the Citizens Research Council of Michigan February 1996 PUBLIC FUNDING FOR STADIUM CONSTRUCTION IN DETROIT On March 19, 1996, two

Government Research Since 1916 CRC Memorandum No. 1040 A publication of the Citizens Research Council of Michigan February 1996 PUBLIC FUNDING FOR STADIUM CONSTRUCTION IN DETROIT On March 19, 1996, two

ABOUT TECTA Best Integrated National Roofing Company 45 Locations which are wholly owned subsidiaries; More than 2800 Employees Local operating units average 60+ years in business Best safety rating in

ABOUT TECTA Best Integrated National Roofing Company 45 Locations which are wholly owned subsidiaries; More than 2800 Employees Local operating units average 60+ years in business Best safety rating in

Global Growth Strategy

Global Growth Strategy Jones Lang LaSalle Global strategy for renewed growth G1 Build our leading local and regional market positions G2 G3 G4 Grow our leading positions in Corporate Solutions Capture

Global Growth Strategy Jones Lang LaSalle Global strategy for renewed growth G1 Build our leading local and regional market positions G2 G3 G4 Grow our leading positions in Corporate Solutions Capture

CBOs and Affordable Housing

CBOs and Affordable Housing BY ROBERT MARK SILVERMAN Since the late 1960s, community-based organizations (CBOs) have become increasingly responsible for implementing affordable housing policy. Scholars

CBOs and Affordable Housing BY ROBERT MARK SILVERMAN Since the late 1960s, community-based organizations (CBOs) have become increasingly responsible for implementing affordable housing policy. Scholars

Near West Side Comprehensive Plan Executive Summary (Revised) April 2004 City of Milwaukee DCD

April 2004 City of Milwaukee DCD") Near West Side Comprehensive Plan Executive Summary (Revised) April 2004 City of Milwaukee DCD Boundaries The Near West Side Comprehensive Plan covers a broad area immediately west of Milwaukee s downtown.

Near West Side Comprehensive Plan Executive Summary (Revised) April 2004 City of Milwaukee DCD Boundaries The Near West Side Comprehensive Plan covers a broad area immediately west of Milwaukee s downtown.

Taxable Bonds = -------------------------------------------------------------------------------- ------------------------------

Number: 200641002 Release Date: 10/13/2006 Internal Revenue Service Index Number: 141.00-00, 141.01-02, 141.02-00 ----------------------------- ------------------------------- ------------------------------------------------------------

Number: 200641002 Release Date: 10/13/2006 Internal Revenue Service Index Number: 141.00-00, 141.01-02, 141.02-00 ----------------------------- ------------------------------- ------------------------------------------------------------

Business Owners Guide to Illinois Tax Benefits

DEVELOPMENT INCENTIVES For New and Existing Businesses Leon Rockingham, Jr. Mayor Figure 1. Waukegan-North Chicago Enterprise Zone Page 3 Incentives Sales Tax Exemption. A 6.25 percent sales tax exemption

DEVELOPMENT INCENTIVES For New and Existing Businesses Leon Rockingham, Jr. Mayor Figure 1. Waukegan-North Chicago Enterprise Zone Page 3 Incentives Sales Tax Exemption. A 6.25 percent sales tax exemption

CITY OF MORENO VALLEY, CALIFORNIA COMMUNITY FACILITIES DISTRICT NO. 3

CITY OF MORENO VALLEY, CALIFORNIA COMMUNITY FACILITIES DISTRICT NO. 3 CONTINUING DISCLOSURE REPORT FOR FISCAL YEAR 2012/13 THESE BONDS HAVE BEEN FULLY REDEMED Report Date: March 2014 Prepared by: FINANCIAL

CITY OF MORENO VALLEY, CALIFORNIA COMMUNITY FACILITIES DISTRICT NO. 3 CONTINUING DISCLOSURE REPORT FOR FISCAL YEAR 2012/13 THESE BONDS HAVE BEEN FULLY REDEMED Report Date: March 2014 Prepared by: FINANCIAL

Financing Renewable Energy in New Jersey

Financing Renewable Energy in New Jersey Renewable Energy Procurement Workshop Sustainable Jersey and the Atlantic County Utilities Authority Presenters Douglas J. Bacher, Managing Director Dianna C. Geist,

Financing Renewable Energy in New Jersey Renewable Energy Procurement Workshop Sustainable Jersey and the Atlantic County Utilities Authority Presenters Douglas J. Bacher, Managing Director Dianna C. Geist,

Village of Cambridge. Tax Incremental Financing Policy & Application

Village of Cambridge Tax Incremental Financing Policy & Application Village of Cambridge, Wisconsin 200 Spring Street Cambridge, WI 53563 www.cambridge.wi.us (608) 423-3712 Table of Contents Table of Contents...1

Village of Cambridge Tax Incremental Financing Policy & Application Village of Cambridge, Wisconsin 200 Spring Street Cambridge, WI 53563 www.cambridge.wi.us (608) 423-3712 Table of Contents Table of Contents...1

Economic Incentives. Local Incentives

Economic Incentives There are a range of economic incentives available to qualifying new, relocating or expanding companies in the Conroe area. GCEDC Staff will work with you to develop an incentive proposal

Economic Incentives There are a range of economic incentives available to qualifying new, relocating or expanding companies in the Conroe area. GCEDC Staff will work with you to develop an incentive proposal

BUSINESS. BY THE BAY!

City of La Porte BUSINESS. BY THE BAY! ECONOMIC DEVELOPMENT INCENTIVES La Porte, Texas 604 W. Fairmont Parkway La Porte, Texas 77571 (281) 470-5016 Local Incentives Tax Abatements The City of La Porte

City of La Porte BUSINESS. BY THE BAY! ECONOMIC DEVELOPMENT INCENTIVES La Porte, Texas 604 W. Fairmont Parkway La Porte, Texas 77571 (281) 470-5016 Local Incentives Tax Abatements The City of La Porte

METROPOLITAN GOVERNANCE AND STRATEGIC PLANNING ALLIANCES AND AGREEMENTS

8 METROPOLITAN GOVERNANCE AND STRATEGIC PLANNING ALLIANCES AND AGREEMENTS An important task of the continuation work of the Greater Helsinki Vision 2050 ideas competition is to envision processes and institutional

8 METROPOLITAN GOVERNANCE AND STRATEGIC PLANNING ALLIANCES AND AGREEMENTS An important task of the continuation work of the Greater Helsinki Vision 2050 ideas competition is to envision processes and institutional

Elliot Perry West Virginia Development Office (304) 558-2234 eperry@wvdo.org

558-2234 eperry@wvdo.org") The West Virginia Development Office is currently revising Property Tax Increment Financing in West Virginia: A Guide for Counties and Class I and II Municipalities. The revisions will reflect all amendments

The West Virginia Development Office is currently revising Property Tax Increment Financing in West Virginia: A Guide for Counties and Class I and II Municipalities. The revisions will reflect all amendments

A Note on Business Tax Competitiveness in British Columbia

A Note on Business Tax Competitiveness in British Columbia Volume 21, Issue 2, May 2014 It s slightly more than one year since BC scrapped the Harmonized Sales Tax (HST) and returned to the former Provincial

A Note on Business Tax Competitiveness in British Columbia Volume 21, Issue 2, May 2014 It s slightly more than one year since BC scrapped the Harmonized Sales Tax (HST) and returned to the former Provincial

KALAMAZOO DOWNTOWN DEVELOPMENT AUTHORITY BUILDING REHABILITATION PROGRAM

KALAMAZOO DOWNTOWN DEVELOPMENT AUTHORITY BUILDING REHABILITATION PROGRAM PURPOSE As a fundamental goal of the Downtown Development Plan and Tax Increment Financing Plan (Plan), the Kalamazoo Downtown Development

KALAMAZOO DOWNTOWN DEVELOPMENT AUTHORITY BUILDING REHABILITATION PROGRAM PURPOSE As a fundamental goal of the Downtown Development Plan and Tax Increment Financing Plan (Plan), the Kalamazoo Downtown Development

taxation Exempt Financing For Development District Projects

Economic Development Commission Development Financing Policy and Procedures Purpose The objective of this policy is to establish procedures for Washington County in considering applications for development

Economic Development Commission Development Financing Policy and Procedures Purpose The objective of this policy is to establish procedures for Washington County in considering applications for development

J. OF PUBLIC BUDGETING, ACCOUNTING & FINANCIAL MANAGEMENT, 11(3), 417-430 FALL 1999

, 417-430 FALL 1999") J. OF PUBLIC BUDGETING, ACCOUNTING & FINANCIAL MANAGEMENT, 11(3), 417-430 FALL 1999 THE IMPACT OF TAX INCREMENT FINANCING PROGRAMS ON LOCAL ECONOMIC DEVELOPMENT Joyce Y. Man* ABSTRACT: The Tax Increment

J. OF PUBLIC BUDGETING, ACCOUNTING & FINANCIAL MANAGEMENT, 11(3), 417-430 FALL 1999 THE IMPACT OF TAX INCREMENT FINANCING PROGRAMS ON LOCAL ECONOMIC DEVELOPMENT Joyce Y. Man* ABSTRACT: The Tax Increment

B U S I N E S S C O S T S

Introduction A company s success in today s highly competitive global economy is determined by its ability to produce the highest quality products and services at the lowest costs. This competitive imperative

Introduction A company s success in today s highly competitive global economy is determined by its ability to produce the highest quality products and services at the lowest costs. This competitive imperative

Property Tax Real. hio. Taxpayer The tax is paid by all real property owners unless specifically exempt.

108 Property Tax Real Taxpayer The tax is paid by all real property owners unless specifically exempt. Tax Base The tax is based on the assessed value of land and buildings. Assessed value is 35 percent

108 Property Tax Real Taxpayer The tax is paid by all real property owners unless specifically exempt. Tax Base The tax is based on the assessed value of land and buildings. Assessed value is 35 percent

LEX HELIUS: THE LAW OF SOLAR ENERGY Tax Issues

LEX HELIUS: THE LAW OF SOLAR ENERGY Tax Issues Charles S. Lewis, III 600 University Street, Suite 3600 Seattle, WA 98101-4109 206-386-7688 cslewis@stoel.com Kevin T. Pearson 900 SW Fifth Avenue, Suite

LEX HELIUS: THE LAW OF SOLAR ENERGY Tax Issues Charles S. Lewis, III 600 University Street, Suite 3600 Seattle, WA 98101-4109 206-386-7688 cslewis@stoel.com Kevin T. Pearson 900 SW Fifth Avenue, Suite

Percent of. Amount 797,840 Market Value

Three Rivers Park District, MN 1 Three Rivers Park District, Minnesota General Obligation Bonds, Series 2015B $7,965,000, and General Obligation Capital Equipment Notes, Series 2015C, $710,000, Dated:

Three Rivers Park District, MN 1 Three Rivers Park District, Minnesota General Obligation Bonds, Series 2015B $7,965,000, and General Obligation Capital Equipment Notes, Series 2015C, $710,000, Dated:

October 18, 2005 Smart Metropolitan Neighborhoods Series: Land Bank Authorities Tools for Vacant Property Reclamation

Experts Online October 18, 2005 Smart Metropolitan Neighborhoods Series: Land Bank Authorities Tools for Vacant Property Reclamation Land Bank Authorities A Guide for the Creation and Operation of Local

Experts Online October 18, 2005 Smart Metropolitan Neighborhoods Series: Land Bank Authorities Tools for Vacant Property Reclamation Land Bank Authorities A Guide for the Creation and Operation of Local

SOLAR BEST PRACTICES FOR CITIES IN THE SOUTH

SOLAR INITIATIVE POLICY BRIEF SOLAR BEST PRACTICES FOR CITIES IN THE SOUTH Solar energy is an increasingly affordable way for cities to increase their use of clean energy, bringing a wealth of benefits

SOLAR INITIATIVE POLICY BRIEF SOLAR BEST PRACTICES FOR CITIES IN THE SOUTH Solar energy is an increasingly affordable way for cities to increase their use of clean energy, bringing a wealth of benefits

Deep Ellum Crossroads Redevelopment Project

Deep Ellum Crossroads Redevelopment Project Deep Ellum TIF District Economic Development Committee September 15, 2014 Office of Economic Development Overview Discuss the redevelopment and site improvements

Deep Ellum Crossroads Redevelopment Project Deep Ellum TIF District Economic Development Committee September 15, 2014 Office of Economic Development Overview Discuss the redevelopment and site improvements

USER GUIDE FOR MARYLAND SUSTAINABLE COMMUNITY REVITALIZATION

m&g USER GUIDE FOR MARYLAND SUSTAINABLE COMMUNITY REVITALIZATION m&g USER GUIDE FOR MARYLAND SUSTAINABLE COMMUNITY REVITALIZATION State of Maryland Martin O Malley Governor Anthony G. Brown Lt. Governor

m&g USER GUIDE FOR MARYLAND SUSTAINABLE COMMUNITY REVITALIZATION m&g USER GUIDE FOR MARYLAND SUSTAINABLE COMMUNITY REVITALIZATION State of Maryland Martin O Malley Governor Anthony G. Brown Lt. Governor

Financing Options for Commercial Solar Projects

2010 Financing Options for Commercial Solar Projects EXECUTIVE SUMMARY Thanks to a range of innovative financing options, transitioning to solar energy has never been more affordable for businesses and

2010 Financing Options for Commercial Solar Projects EXECUTIVE SUMMARY Thanks to a range of innovative financing options, transitioning to solar energy has never been more affordable for businesses and

NEIGHBORHOOD LAND BANK

NEIGHBORHOOD LAND BANK Purpose: Contribute to the community stabilization, revitalization and preservation of San Diego County s communities, particularly San Diego s low and moderate income communities,

NEIGHBORHOOD LAND BANK Purpose: Contribute to the community stabilization, revitalization and preservation of San Diego County s communities, particularly San Diego s low and moderate income communities,

Financial Analysis and Funding

California High- Speed Rail Authority Revised 2012 Business Plan Chapter 7 Financial Analysis and Funding Introduction This chapter presents the financial analysis and funding strategy for the California

California High- Speed Rail Authority Revised 2012 Business Plan Chapter 7 Financial Analysis and Funding Introduction This chapter presents the financial analysis and funding strategy for the California

Financing Business Expansion through Tax-Exempt Private Activity Bonds

January 2011 Practice Group(s): Public Finance Seattle Scott A. McJannet Robert D. Starin David O. Thompson Cynthia M. Weed Spokane /Coeur d Alene Kevin R. Connelly Laura D. McAloon Brian M. Werst Financing

January 2011 Practice Group(s): Public Finance Seattle Scott A. McJannet Robert D. Starin David O. Thompson Cynthia M. Weed Spokane /Coeur d Alene Kevin R. Connelly Laura D. McAloon Brian M. Werst Financing

WHAT IS A REAL (504) LOAN?

LOAN?") WHAT IS A REAL (504) LOAN? The Real Estate Advantage Loan (also known as a REAL or 504 Loan) is a 10% down, fixed-rate, long-term loan designed to expand capital access, filling a market gap in long-term

WHAT IS A REAL (504) LOAN? The Real Estate Advantage Loan (also known as a REAL or 504 Loan) is a 10% down, fixed-rate, long-term loan designed to expand capital access, filling a market gap in long-term

LEGISLATIVE GUIDE TO URBAN RENEWAL AND TAX INCREMENT FINANCING

LEGISLATIVE GUIDE TO URBAN RENEWAL AND TAX INCREMENT FINANCING Legislative Services Agency Note to Reader: Research is conducted by the Legal Services Division of the Iowa Legislative Services Agency in

LEGISLATIVE GUIDE TO URBAN RENEWAL AND TAX INCREMENT FINANCING Legislative Services Agency Note to Reader: Research is conducted by the Legal Services Division of the Iowa Legislative Services Agency in

13.01 TAX INCREMENT FINANCING

13.01 TAX INCREMENT FINANCING The Primary Purpose of TIF Tax increment financing (TIF) is a method of financing real estate development costs to promote development, redevelopment and housing in areas

13.01 TAX INCREMENT FINANCING The Primary Purpose of TIF Tax increment financing (TIF) is a method of financing real estate development costs to promote development, redevelopment and housing in areas

REITs and infrastructure projects The next investment frontier?

REITs and infrastructure projects The next investment frontier? 2 Coming out of the economic downturn, private investors are seeking new avenues to generate tax-efficient returns on their invested funds.

REITs and infrastructure projects The next investment frontier? 2 Coming out of the economic downturn, private investors are seeking new avenues to generate tax-efficient returns on their invested funds.

The Impact Of Retail Wheeling On Municipal Electric Utilities In Kansas

The Impact Of Retail Wheeling On Municipal Electric Utilities In Kansas - EXECUTIVE SUMMARY - Copyright 1997 All Rights Reserved Several developments create a movement for deregulation of the electric

The Impact Of Retail Wheeling On Municipal Electric Utilities In Kansas - EXECUTIVE SUMMARY - Copyright 1997 All Rights Reserved Several developments create a movement for deregulation of the electric

OBSOLETE PROPERTY REHABILITATION ACT Act 146 of 2000. The People of the State of Michigan enact:

OBSOLETE PROPERTY REHABILITATION ACT Act 146 of 2000 AN ACT to provide for the establishment of obsolete property rehabilitation districts in certain local governmental units; to provide for the exemption

OBSOLETE PROPERTY REHABILITATION ACT Act 146 of 2000 AN ACT to provide for the establishment of obsolete property rehabilitation districts in certain local governmental units; to provide for the exemption

All About Qualified Energy Conservation Bonds

All About Qualified Energy Conservation Bonds Thursday, April 30, 2015 www.southeastfinancenetwork.com 1 About the Finance Network The goal is to facilitate the expansion of energy efficiency investments

All About Qualified Energy Conservation Bonds Thursday, April 30, 2015 www.southeastfinancenetwork.com 1 About the Finance Network The goal is to facilitate the expansion of energy efficiency investments

DOWNTOWN HOUSTON DEVELOPMENT ASSISTANCE

DOWNTOWN HOUSTON DEVELOPMENT ASSISTANCE The following programs have been utilized in the past for downtown Houston developments. This list is meant to provide information that might potentially be applicable

DOWNTOWN HOUSTON DEVELOPMENT ASSISTANCE The following programs have been utilized in the past for downtown Houston developments. This list is meant to provide information that might potentially be applicable

PA WORKS. Job Creation and Investment to Move Pennsylvania Forward

PA WORKS Job Creation and Investment to Move Pennsylvania Forward Job creation is the number one issue for Senate Democrats. We must adopt policies and programs at every level of government to grow Pennsylvania

PA WORKS Job Creation and Investment to Move Pennsylvania Forward Job creation is the number one issue for Senate Democrats. We must adopt policies and programs at every level of government to grow Pennsylvania

A Guidebook of Massachusetts Public Financing Programs for Infrastructure Investment

A Guidebook of Massachusetts Public Financing Programs for Infrastructure Investment Page 1 TABLE OF CONTENTS CHAPTER 1 INTRODUCTION 6 PLANNING AHEAD FOR GROWTH EMPOWERING MUNICIPALITIES TAX REVENUE FINANCING

A Guidebook of Massachusetts Public Financing Programs for Infrastructure Investment Page 1 TABLE OF CONTENTS CHAPTER 1 INTRODUCTION 6 PLANNING AHEAD FOR GROWTH EMPOWERING MUNICIPALITIES TAX REVENUE FINANCING

May 23, 1996 AGO 96-039. Mr. James D. Palermo Tampa City Attorney 315 East Kennedy Boulevard Fifth Floor Tampa, Florida 33602. Dear Mr.

May 23, 1996 AGO 96-039 Mr. James D. Palermo Tampa City Attorney 315 East Kennedy Boulevard Fifth Floor Tampa, Florida 33602 Dear Mr. Palermo: You ask substantially the following question: Which value

May 23, 1996 AGO 96-039 Mr. James D. Palermo Tampa City Attorney 315 East Kennedy Boulevard Fifth Floor Tampa, Florida 33602 Dear Mr. Palermo: You ask substantially the following question: Which value

Fiscal Note. Fiscal Services Division

Fiscal Note Fiscal Services Division SF 295 Property Tax Changes (LSB 1464SV.2) Analyst: Jeff Robinson (Phone: (515) 281-4614) (jeff.robinson@legis.iowa.gov) Fiscal Note Version Conference Committee Report

Fiscal Note Fiscal Services Division SF 295 Property Tax Changes (LSB 1464SV.2) Analyst: Jeff Robinson (Phone: (515) 281-4614) (jeff.robinson@legis.iowa.gov) Fiscal Note Version Conference Committee Report

STRAYING FROM GOOD INTENTIONS: How States are Weakening Enterprise Zone and Tax Increment Financing Programs

STRAYING FROM GOOD INTENTIONS: How States are Weakening Enterprise Zone and Tax Increment Financing Programs by Good Jobs First Alyssa Talanker and Kate Davis with Greg LeRoy August 2003 Copyright 2003

STRAYING FROM GOOD INTENTIONS: How States are Weakening Enterprise Zone and Tax Increment Financing Programs by Good Jobs First Alyssa Talanker and Kate Davis with Greg LeRoy August 2003 Copyright 2003

Convention Center Expansion & Headquarters Hotel Feasibility Study for the Washington Convention Center. Summary of Study Findings

Convention Center Expansion & Headquarters Hotel Feasibility Study for the Washington Convention Center In March 2003, the new $850 million Washington Convention Center (WCC) opened to the public. The

Convention Center Expansion & Headquarters Hotel Feasibility Study for the Washington Convention Center In March 2003, the new $850 million Washington Convention Center (WCC) opened to the public. The

Creative Financing for Brownfields-Grayfields Redevelopment

Creative Financing for Brownfields-Grayfields Redevelopment New Partners for Smart Growth Evans Paull Redevelopment Economics ev@redevelopmenteconomics.com www.redevelopmenteconomics.com Redevelopment

Creative Financing for Brownfields-Grayfields Redevelopment New Partners for Smart Growth Evans Paull Redevelopment Economics ev@redevelopmenteconomics.com www.redevelopmenteconomics.com Redevelopment

Tax Increment Financing: Process and Planning Issues. Rachel Weber and Laura Goddeeris. 2007 Lincoln Institute of Land Policy

Tax Increment Financing: Process and Planning Issues Rachel Weber and Laura Goddeeris 2007 Lincoln Institute of Land Policy Lincoln Institute of Land Policy Working Paper The findings and conclusions of

Tax Increment Financing: Process and Planning Issues Rachel Weber and Laura Goddeeris 2007 Lincoln Institute of Land Policy Lincoln Institute of Land Policy Working Paper The findings and conclusions of

COUNTY OF RIVERSIDE, CALIFORNIA BOARD OF SUPERVISORS POLICY. Policy Subject: Number Page LAND SECURED FINANCING DISTRICTS B-12 1 of 22

LAND SECURED FINANCING DISTRICTS B-12 1 of 22 : Set forth herein are the goals and policies of the County of Riverside (the County ) concerning the County s use of community facilities districts ( Community

LAND SECURED FINANCING DISTRICTS B-12 1 of 22 : Set forth herein are the goals and policies of the County of Riverside (the County ) concerning the County s use of community facilities districts ( Community