INTERNAL REVENUE CODE SECTION 280E: CREATING AN IMPOSSIBLE SITUATION FOR LEGITIMATE BUSINESSES

|

|

|

- Oswin Arnold

- 10 years ago

- Views:

Transcription

1 INTERNAL REVENUE CODE SECTION 280E: CREATING AN IMPOSSIBLE SITUATION FOR LEGITIMATE BUSINESSES What is Section 280E? Section 280E of the Internal Revenue Code forbids businesses from deducting otherwise ordinary business expenses from gross income associated with the trafficking of Schedule I or II substances, as defined by the Controlled Substances Act. The IRS has subsequently applied Section 280E to state-legal cannabis businesses, since cannabis is still a Schedule I substance. A throwback from the Reagan Administration, Section 280E originated from a 1981 court case in which a convicted cocaine trafficker asserted his right under federal tax law to deduct ordinary business expenses. In 1982, Congress created 280E to prevent other drug dealers from following suit. It states that no deductions should be allowed on any amount in carrying on any trade or business if such trade or business consists of trafficking in controlled substances. With 23 states and the District of Columbia now allowing some form of legal marijuana, 280E is applied to state-regulated cannabis businesses more often than it is to the types of illegal drug dealers that the provision was intended to penalize. How does Section 280E hurt state-legal cannabis businesses? Federal income taxes are based on a fairly simple formula: start with gross income, subtract business expenses to calculate taxable income, and then pay taxes on this amount. Owners of regular businesses often derive profits from these business deductions. Cannabis businesses, however, pay taxes on gross income. These businesses often pay tax rates that are 70% or higher. As John Davis, owner of the Northwest Patient Resource Center in Seattle, WA states, I m taxed on nearly double the amount that my business actually makes. I m taxed on nearly double the amount that my business actually makes. John Davis, Northwest Patient Resource Center! Below is a simplified model that illustrates the tax structure for cannabis businesses compared to a normal businesses. In this scenario, the normal business s taxable income is $150,000, while the cannabis business is taxed on $350,000, despite having the same costs and expenses. Non-Cannabis Business Cannabis Business Gross Revenue $1,000,000 $1,000,000 Cost of Goods Sold $650,000 $650,000 Gross Income $350,000 $350,000 Deductible Business Expenses $200,000 $0 Taxable Income $150,000 $350,000 Tax (30%) $45,000 $105,000 Effective Tax Rate 30% 70%

2 The taxation problem facing cannabis businesses just got worse. There are a lot of businesses that are going to get absolutely creamed. Jim Marty, Bridge West CPAs In January 2015, the Internal Revenue Service issued an internal memorandum that opined on how state-legal cannabis businesses should compute federal income taxes. Drafted by the IRS Chief Counsel, the memo rejects many of the tax deductions that these businesses have traditionally made. The memo challenges tax strategies that allow these businesses to stay afloat, and imposes a strict interpretation of Section 280E of the Internal Revenue Code. Without even the meager deductions state-legal cannabis businesses were previously allowed to take, these businesses face a bleak financial future. This deeply affects their ability to reinvest profits back into their local communities and fulfill the will of state voters, legislatures, and regulatory bodies that have mandated that cannabis be dispensed through legal storefronts. Jim Marty, a CPA with Colorado s Bridge West CPAs, says that many marijuana businesses are going to struggle under the new rules. There are a lot of businesses that are going to get absolutely creamed, he says. What types of business expenses are scrutinized under 280E? Employee salaries Utility costs such as electricity, internet and telephone service Health insurance premiums Marketing and advertising costs Repairs and maintenance Rental fees for facilities Routine repair and maintenance Payments to contractors State-legal cannabis businesses are allowed to deduct the Cost of Goods Sold (COGS) on their taxes. Also, since 2007, cannabis businesses have made deductions on their non-cannabis business activities. Most importantly, however, cannabis businesses have also followed guidance from section 263A of the IRC, which allows businesses to capitalize on indirect costs such as administrative and inventory costs, as well as the amount paid in state excise taxes and deduct them under COGS. Depending on the business, these indirect costs can be sizable. The strategy of including these costs in COGS is oftentimes what allows cannabis businesses to collect meager profits. What deductions are now likely to be challenged? General and administrative costs (bookkeeping, legal expenses, technology costs) State excise taxes Storage of cannabis Purchasing cannabis Depreciation of cannabis

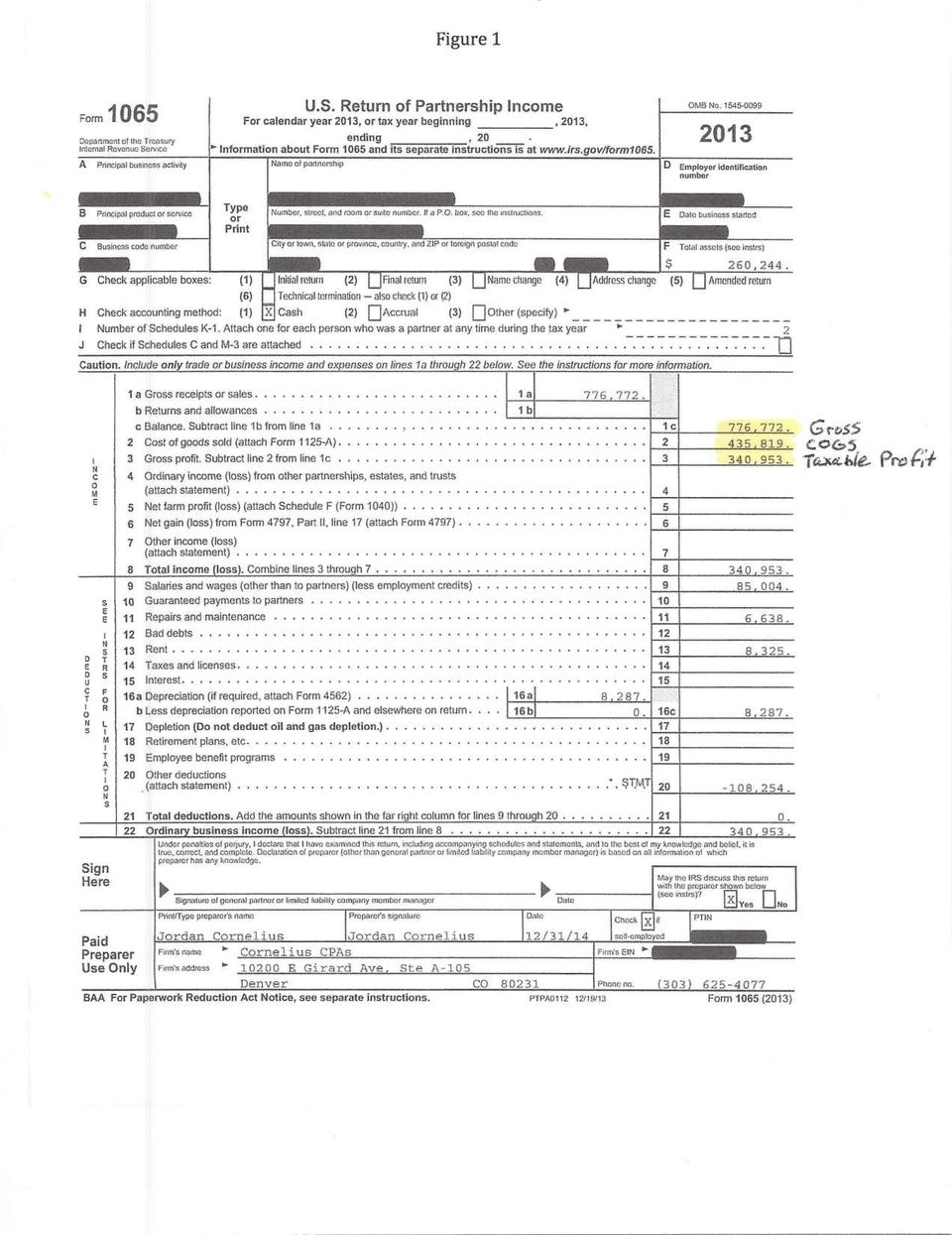

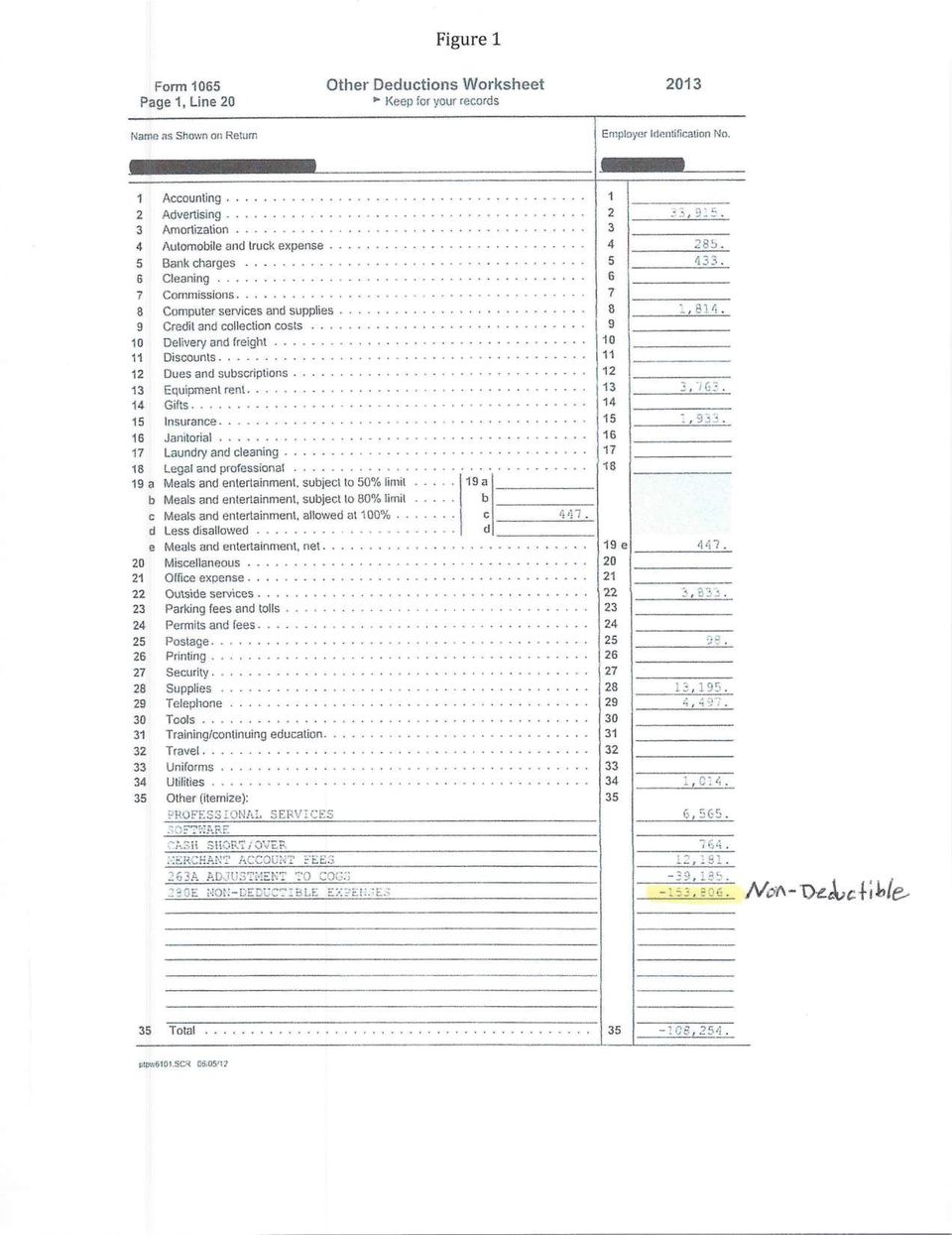

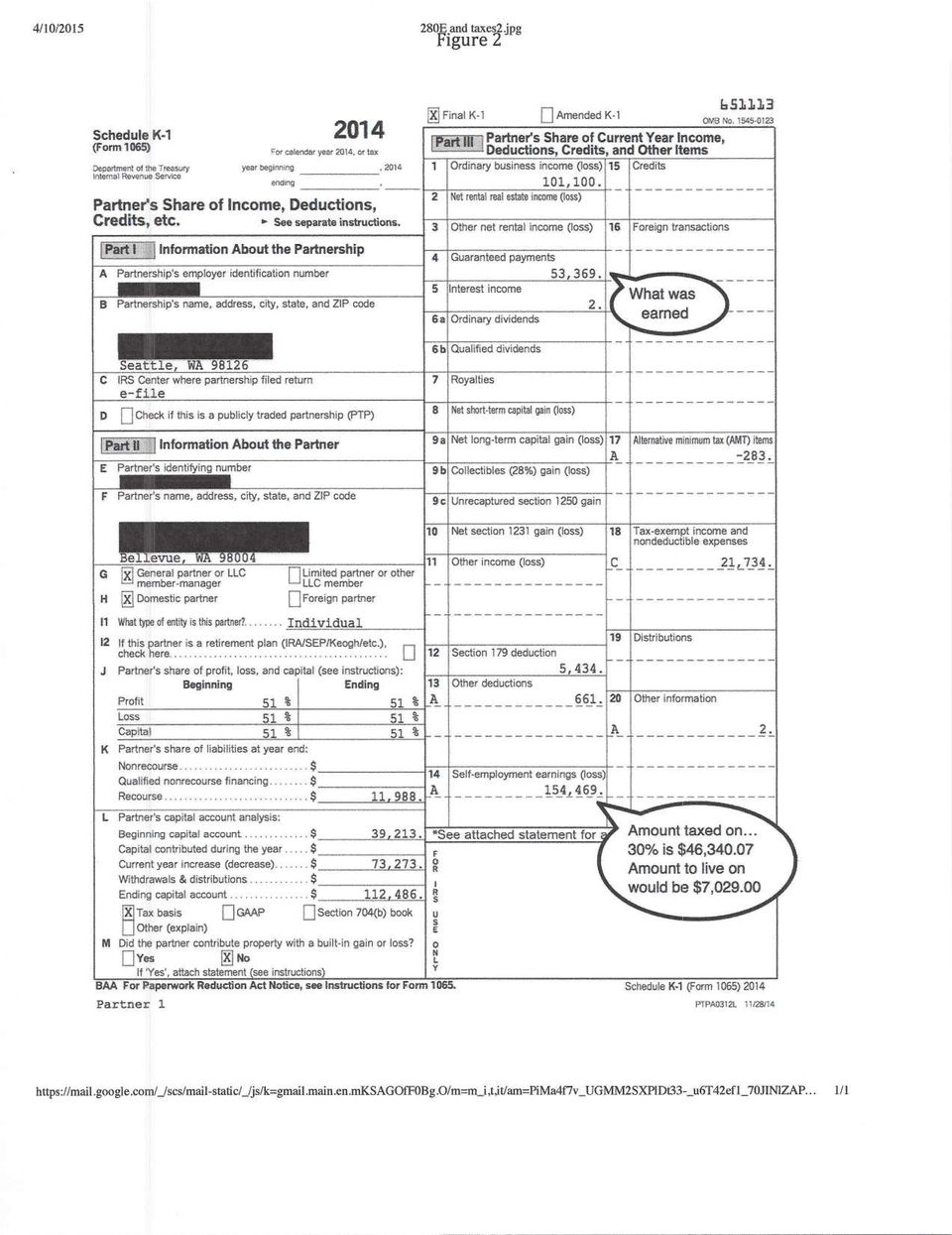

3 How did these deductions benefit cannabis businesses? Attached below are three documents that illustrate how 280E has applied to typical cannabis businesses both before and after the tightening of IRS rules. Figure 1 is a 1065 tax filing from 2013 from a medical cannabis business in Denver, Colorado. Gross receipts totaled $776,772, and thanks to some strong work by a CPA, the business was able to deduct $435,819 in Cost of Goods Sold, leaving a gross income of $340,953. The business had an additional $153,806 in deductions that any other business would be able to take, but were disallowed under 280E. Since the business was allowed deductions on Cost of Goods Sold, it paid taxes on $340,953 instead of on $776,772. Its effective tax rate was still 55% of its final earnings, but the business owner was able to invest the remaining cash back into the business. Without these deductions, what does a final tax bill look like for a state-authorized cannabis business? Figure 2 is a 1065 tax filing from 2014 from a medical cannabis dispensary in Seattle, Washington. The business followed the new, even stricter 280E rules in its filing. As the documents show, gross income from this business totaled $154,469 for 2014, and the business had $101,100 in expenses. If this business were a regular business, it would be taxed on its earnings, which were $53,369. In order to comply with 280E, however, the business was unable to take these deductions, and instead it paid taxes on $154,469. The business tax payment totaled $46,340, which equates to 87% of its true earnings. The business owner had only $7,029 to either invest back into his business or keep as profit. What s the worst-case scenario for a business under 280E? Figure 3 is a 1065 and Statement of Activities and Changes In Net Assets from a medical marijuana dispensary in Arizona. The business produced $876,420 in gross receipts and was permitted to deduct $319,386 in Cost of Goods Sold, but could take no deductions for its other expenses. The business, thus, was taxed on its gross income, which was $557,034. Like many startup businesses, however, the dispensary had significant first-year expenses, which totaled $867,863. These operating expenses were nondeductible under 280E. So while the business actually lost a total $310,829 for the year, its tax bill was still $189,781. Despite bringing in $876,420, the business ended up more than half a million dollars in the red. Mitch Woolheiser, owner of Northern Lights Cannabis in Edgewater, Colorado, said he s hoarding cash in preparation for his tax payment. I can t give my employees raises. I can t put money back into my business. Instead I ve been hoarding cash in anticipation of what the IRS is going to take, Woolheiser says. I can t give my employees raises. I can t put money back into my business. Instead I ve been hoarding cash in anticipation of what the IRS is going to take. Mitch Woolheiser, Northern Lights Cannabis! How many state economies are affected by 280E? Section 280E affects all businesses that engage in the cultivation, sale, or processing of the cannabis plant. This includes cultivators, medical dispensaries, marijuana retail stores, and infused product manufacturers, as well as concentrates and cannabis oil manufacturers. Cannabis is now legal in some form in 23 U.S. states as well as the District of Columbia, with Oregon and Alaska joining Colorado and Washington as states with laws regulating marijuana sales to adults over 21. Several other states are expected to enact similar laws regulating marijuana in 2016.

4 What impact does this have on the cannabis industry and states attempting to regulate marijuana? Section 280E de-incentivizes people from filing tax returns. It penalizes people who are trying to be transparent and operate within the law. Henry Wykowski, Henry G. Wykowski & Associates Cannabis entrepreneurs want to pay federal and state taxes. Maintaining a strong working relationship with the IRS legitimizes these businesses and, in turn, the entire cannabis industry. But the current taxation climate has convinced some cannabis entrepreneurs to either ignore 280E on their tax filings, or forego paying taxes altogether. These businesses would rather gamble on the IRS overlooking their filing than see their revenues evaporate due to 280E. As Henry Wykowski, a California attorney who works with marijuana clients on tax issues, states, Section 280E de-incentivizes people from filing tax returns. It penalizes people who are trying to be transparent and operate within the law. We believe the most recent IRS memo will force even more cannabis businesses to sidestep the IRS. This will undoubtedly lead to long and expensive audits, as well as lawsuits that will challenge the IRS memo and 280E as a whole. How can this problem be resolved? The National Cannabis Industry Association believes that the best fix to the situation is to remove marijuana from the Controlled Substances Act. However, The Small Business Tax Equity Act companion Senate and House legislation introduced in the 114 th Congress by Sen. Ron Wyden (D-OR) and Rep. Earl Blumenauer (D-OR) would more narrowly address the unfair impact 280E has on states with regulated cannabis markets without necessitating a sweeping shift in U.S. marijuana policy. The intent of the law was to go after criminals, not law-abiding job creators. Congress needs to step up and clarify that this provision has become a case study in unintended consequences. Grover Norquist, Americans for Tax Reform! The legislation S. 987 and H.R would exempt cannabis businesses acting in compliance with state law from the 280E provision, thereby allowing them to take the ordinary business deductions afforded to all other legal businesses. In his endorsement of The Small Business Tax Equity Act, Americans for Tax Reform President Grover Norquist said, The intent of the law was to go after criminals, not law abiding job creators. Congress needs to step up and clarify that this provision has become a case study in unintended consequences.! This sensible solution would bring this outdated provision of the tax code into the modern era and allow cannabis businesses to operate in accordance with the will of state voters and legislative bodies who have mandated that these businesses work within a legitimate, above-ground environment. Amending 280E will also allow businesses in the emerging cannabis industry to better invest in their local communities by hiring additional employees and offering more competitive salaries rather than sending inordinate amounts of revenue into the federal tax coffers. This document does not constitute legal or tax advice. National Cannabis Industry Association, April 2015

5 ACKNOWLEDGMENTS Special thanks to the industry experts whose contributions of time, insight, and materials made this report possible: Hilary Bricken, Harris Moure Erik Briones, Minerva Canna Group Jordan Cornelius, Cornelius CPAs John B. Davis, Northwest Patient Resource Center Darin Guthrie, Darin Guthrie CPA James Hunt, James G. Hunt PLLC Jim Marty, Bridge West CPAs James Thorburn and Rich Walker, Thorburn-Walker Matthew Walstatter, Pure Green Cannabis Mitch and Eva Woolheiser, Northern Lights Henry Wykowski, Henry G. Wykowski and Associates Luigi Zamarra, Luigi CPA

6

7

8

9

10

11

This advice responds to your request for assistance. This advice may not be used or cited as precedent.

Office of Chief Counsel Internal Revenue Service Memorandum Number: 201504011 Release Date: 1/23/2015 CC:ITA:6 LFNolanII POSTS-125750-13 UILC: 280E.00-00, 61.00-00, 263A.00-00, 446.00-00, 446.01-00, 471.00-00

Office of Chief Counsel Internal Revenue Service Memorandum Number: 201504011 Release Date: 1/23/2015 CC:ITA:6 LFNolanII POSTS-125750-13 UILC: 280E.00-00, 61.00-00, 263A.00-00, 446.00-00, 446.01-00, 471.00-00

Federal Income Taxation of Medical Marijuana Businesses

Federal Income Taxation of Medical Marijuana Businesses Professor Edward J. Roche, Jr. University of Denver Sturm College of Law and Graduate Tax Program Federal Income Taxation of Medical and Recreational

Federal Income Taxation of Medical Marijuana Businesses Professor Edward J. Roche, Jr. University of Denver Sturm College of Law and Graduate Tax Program Federal Income Taxation of Medical and Recreational

PENNSYLVANIA BAR ASSOCIATION LEGAL ETHICS AND PROFESSIONAL RESPONSIBILITY COMMITTEE PHILADELPHIA BAR ASSOCIATION PROFESSIONAL GUIDANCE COMMITTEE

PENNSYLVANIA BAR ASSOCIATION LEGAL ETHICS AND PROFESSIONAL RESPONSIBILITY COMMITTEE Summary PHILADELPHIA BAR ASSOCIATION PROFESSIONAL GUIDANCE COMMITTEE JOINT FORMAL OPINION 2015-100 PROVIDING ADVICE TO

PENNSYLVANIA BAR ASSOCIATION LEGAL ETHICS AND PROFESSIONAL RESPONSIBILITY COMMITTEE Summary PHILADELPHIA BAR ASSOCIATION PROFESSIONAL GUIDANCE COMMITTEE JOINT FORMAL OPINION 2015-100 PROVIDING ADVICE TO

Seattle City Attorney Peter S. Holmes

Seattle City Attorney Peter S. Holmes January 20, 2011 Members of the Health & Long-Term Care Committee Washington State Senate 466 J.A. Cherberg Building P.O. Box 40466 Olympia, WA 98504-0466 Re: SB 5073

Seattle City Attorney Peter S. Holmes January 20, 2011 Members of the Health & Long-Term Care Committee Washington State Senate 466 J.A. Cherberg Building P.O. Box 40466 Olympia, WA 98504-0466 Re: SB 5073

What s News in Tax Analysis That Matters from Washington National Tax

What s News in Tax Analysis That Matters from Washington National Tax IRS Issues Proposed Regulations on Disguised Payments for Services Proposed regulations relating to disguised payments for services

What s News in Tax Analysis That Matters from Washington National Tax IRS Issues Proposed Regulations on Disguised Payments for Services Proposed regulations relating to disguised payments for services

Preprinted Logo will go here

June 15, 2015 Hon. Kamala D. Harris Attorney General 1300 I Street, 17 th Floor Sacramento, California 95814 Attention: Ms. Ashley Johansson Initiative Coordinator Dear Attorney General Harris: Pursuant

June 15, 2015 Hon. Kamala D. Harris Attorney General 1300 I Street, 17 th Floor Sacramento, California 95814 Attention: Ms. Ashley Johansson Initiative Coordinator Dear Attorney General Harris: Pursuant

T.C. Memo. 2015-149 UNITED STATES TAX COURT. JASON R. BECK, Petitioner v. COMMISSIONER OF INTERNAL REVENUE, Respondent

T.C. Memo. 2015-149 UNITED STATES TAX COURT JASON R. BECK, Petitioner v. COMMISSIONER OF INTERNAL REVENUE, Respondent Docket No. 25842-10. Filed August 10, 2015. Jason R. Beck, pro se. Carolyn A. Schenck

T.C. Memo. 2015-149 UNITED STATES TAX COURT JASON R. BECK, Petitioner v. COMMISSIONER OF INTERNAL REVENUE, Respondent Docket No. 25842-10. Filed August 10, 2015. Jason R. Beck, pro se. Carolyn A. Schenck

Gordon Warren Epperly c/o P.O. Box 34358 Juneau, Alaska 99803. Tel: (907) 789-5659

789-5659") Gordon Warren Epperly c/o P.O. Box 34358 Juneau, Alaska 99803 Tel: (907) 789-5659 December 15, 2014 Sally Amanda Marshall United States Attorney 1000 SW Third Ave, Suite 600 Portland, Oregon 97204 Dear

Gordon Warren Epperly c/o P.O. Box 34358 Juneau, Alaska 99803 Tel: (907) 789-5659 December 15, 2014 Sally Amanda Marshall United States Attorney 1000 SW Third Ave, Suite 600 Portland, Oregon 97204 Dear

Guidance. FIN-2014-G001 Issued: February 14, 2014 Subject: BSA Expectations Regarding Marijuana-Related Businesses

Guidance FIN-2014-G001 Issued: February 14, 2014 Subject: BSA Expectations Regarding Marijuana-Related Businesses The Financial Crimes Enforcement Network ( FinCEN ) is issuing guidance to clarify Bank

Guidance FIN-2014-G001 Issued: February 14, 2014 Subject: BSA Expectations Regarding Marijuana-Related Businesses The Financial Crimes Enforcement Network ( FinCEN ) is issuing guidance to clarify Bank

Take Action and Support Net Operating Loss for Companies of All Sizes

Take Action and Support Net Operating Loss for Companies of All Sizes Tax relief for companies of all sizes is critically needed for many businesses to survive the economic downturn. Net Operating Loss

Take Action and Support Net Operating Loss for Companies of All Sizes Tax relief for companies of all sizes is critically needed for many businesses to survive the economic downturn. Net Operating Loss

History of Federal Criminalization

Legal Implications of Recommending Medical Marijuana April 19, 2015 Kevin C. Riach, Esq. [email protected] (612) 492-7435 History of Federal Criminalization In 1800 s, states regulated cannabis under

Legal Implications of Recommending Medical Marijuana April 19, 2015 Kevin C. Riach, Esq. [email protected] (612) 492-7435 History of Federal Criminalization In 1800 s, states regulated cannabis under

PENNSYLVANIA BAR ASSOCIATION LEGAL ETHICS AND PROFESSIONAL RESPONSIBILITY COMMITTEE RECOMMENDATION AND REPORT RECOMMENDATION

PENNSYLVANIA BAR ASSOCIATION LEGAL ETHICS AND PROFESSIONAL RESPONSIBILITY COMMITTEE RECOMMENDATION AND REPORT RECOMMENDATION The PBA Legal Ethics and Professional Responsibility Committee recommends that

PENNSYLVANIA BAR ASSOCIATION LEGAL ETHICS AND PROFESSIONAL RESPONSIBILITY COMMITTEE RECOMMENDATION AND REPORT RECOMMENDATION The PBA Legal Ethics and Professional Responsibility Committee recommends that

Medical Marijuana: The Legal Landscape. Rachelle Yeung, J.D. Legislative Analyst, Marijuana Policy Project

Medical Marijuana: The Legal Landscape Rachelle Yeung, J.D. Legislative Analyst, Marijuana Policy Project Virginia s Medical Marijuana Law Currently, possession of even a single joint is punishable by:

Medical Marijuana: The Legal Landscape Rachelle Yeung, J.D. Legislative Analyst, Marijuana Policy Project Virginia s Medical Marijuana Law Currently, possession of even a single joint is punishable by:

Module 10 S Corporation/Corporation Workbook Introduction

Module 10 Workbook Introduction Running your own business presents many challenges. One of the most difficult is complying with complex and ever-changing tax laws. This small-business tax education program

Module 10 Workbook Introduction Running your own business presents many challenges. One of the most difficult is complying with complex and ever-changing tax laws. This small-business tax education program

ISBA Professional Conduct Advisory Opinion

ISBA Professional Conduct Advisory Opinion **** This Advisory Opinion expresses an interpretation of Illinois Rule of Professional Conduct 1.2(d) for the situation in which a lawyer provides services to

ISBA Professional Conduct Advisory Opinion **** This Advisory Opinion expresses an interpretation of Illinois Rule of Professional Conduct 1.2(d) for the situation in which a lawyer provides services to

Memorandum. Office of Chief Counsel Internal Revenue Service. Number: AM 2007-008 Release Date: 4/20/07 CC:FIP:1:LJMedovoy POSTS-156981-06

Office of Chief Counsel Internal Revenue Service Memorandum Number: AM 2007-008 Release Date: 4/20/07 CC:FIP:1:LJMedovoy POSTS-156981-06 UILC: 1234.00-00 date: April 06, 2007 to: Director, Financial Services

Office of Chief Counsel Internal Revenue Service Memorandum Number: AM 2007-008 Release Date: 4/20/07 CC:FIP:1:LJMedovoy POSTS-156981-06 UILC: 1234.00-00 date: April 06, 2007 to: Director, Financial Services

Medical Marijuana Update: Accounting, Ethics & Tax Issues

Medical Marijuana Update: Accounting, Ethics & Tax Issues Continuing Professional Education Business Valuation Resources October 24, 2012 Jim Marty CPA,ABV, MS Ron Seigneur MBA, ASA, CPA/ABV/CFF, CVA Overview

Medical Marijuana Update: Accounting, Ethics & Tax Issues Continuing Professional Education Business Valuation Resources October 24, 2012 Jim Marty CPA,ABV, MS Ron Seigneur MBA, ASA, CPA/ABV/CFF, CVA Overview

Medical Marijuana Ordinances: Problems Local Governments Are Facing

Medical Marijuana Ordinances: Problems Local Governments Are Facing Matthew R. Silver, Esq. Best Best & Krieger LLP 1 CONTACT INFORMATION Matthew R. Silver, Esq. (949) 263-6588 [email protected]

Medical Marijuana Ordinances: Problems Local Governments Are Facing Matthew R. Silver, Esq. Best Best & Krieger LLP 1 CONTACT INFORMATION Matthew R. Silver, Esq. (949) 263-6588 [email protected]

CITY COUNCIL AGENDA REPORT. DEPARTMENT: City Attorney MEETING DATE: December 15, 2015

CITY COUNCIL AGENDA REPORT DEPARTMENT: City Attorney MEETING DATE: December 15, 2015 PREPARED BY: Craig Steele, City Attorney AGENDA LOCATION: AR-2 TITLE: Amendment to Chapters 5.04 and 5.96 of Title 5

CITY COUNCIL AGENDA REPORT DEPARTMENT: City Attorney MEETING DATE: December 15, 2015 PREPARED BY: Craig Steele, City Attorney AGENDA LOCATION: AR-2 TITLE: Amendment to Chapters 5.04 and 5.96 of Title 5

The Regulate, Control and Tax Cannabis Act of 2010

The Regulate, Control and Tax Cannabis Act of 2010 Title and Summary: Changes California Law to Legalize Marijuana and Allow It to Be Regulated and Taxed. Initiative Statute. Allows people 21 years old

The Regulate, Control and Tax Cannabis Act of 2010 Title and Summary: Changes California Law to Legalize Marijuana and Allow It to Be Regulated and Taxed. Initiative Statute. Allows people 21 years old

Tax Rates. For personal income tax purposes, for tax years beginning after 2014, the tax rates are as follows:

October 2014 District of Columbia Reduced Tax Rates, Single Sales Factor, Other Changes Adopted Permanent District of Columbia budget legislation makes numerous significant changes to the corporation franchise

October 2014 District of Columbia Reduced Tax Rates, Single Sales Factor, Other Changes Adopted Permanent District of Columbia budget legislation makes numerous significant changes to the corporation franchise

The State Board of Equalization Welcomes You to the Basic Sales and Use Tax Seminar

The State Board of Equalization Welcomes You to the Basic Sales and Use Tax Seminar Welcome to the California State Board of Equalization s presentation on Basic Sales and Use Tax. 1 About This Presentation

The State Board of Equalization Welcomes You to the Basic Sales and Use Tax Seminar Welcome to the California State Board of Equalization s presentation on Basic Sales and Use Tax. 1 About This Presentation

Transmitted via Electronic Mail ([email protected]) and ([email protected] )

and (individual@finance.senate.gov )") April 15, 2015 The Honorable Orrin G. Hatch Chairman Committee on Finance United States Senate 219 Dirksen Senate Office Building Washington, D.C. 20510 The Honorable Ron Wyden Ranking Member Committee

April 15, 2015 The Honorable Orrin G. Hatch Chairman Committee on Finance United States Senate 219 Dirksen Senate Office Building Washington, D.C. 20510 The Honorable Ron Wyden Ranking Member Committee

What brings you to the work of the Blue Ribbon Commission, and marijuana?

Policy Perspective: An Interview with Paul Gallegos Paul Gallegos is a private attorney practicing state and federal civil litigation and criminal defense. He served as District Attorney of Humboldt County

Policy Perspective: An Interview with Paul Gallegos Paul Gallegos is a private attorney practicing state and federal civil litigation and criminal defense. He served as District Attorney of Humboldt County

The Changing Environment of R&R (REITs and Renewables)

") The Changing Environment of R&R (REITs and Renewables) A discussion of selected tax developments and considerations Jessica Duran is a senior manager in the San Francisco office of Deloitte Tax, LLP. Charles

The Changing Environment of R&R (REITs and Renewables) A discussion of selected tax developments and considerations Jessica Duran is a senior manager in the San Francisco office of Deloitte Tax, LLP. Charles

Private Health Insurance: Changes Made by the Reconciliation Act of 2010 to Senate-Passed H.R. 3590

Private Health Insurance: Changes Made by the Reconciliation Act of 2010 to Senate-Passed H.R. 3590 Hinda Chaikind Specialist in Health Care Financing Bernadette Fernandez Analyst in Health Care Financing

Private Health Insurance: Changes Made by the Reconciliation Act of 2010 to Senate-Passed H.R. 3590 Hinda Chaikind Specialist in Health Care Financing Bernadette Fernandez Analyst in Health Care Financing

9 Tips to Save Time, Lower Taxes, & Improve Profits

9 Tips to Save Time, Lower Taxes, & Improve Profits By Evie Alvarez & Ivan Alvarez, CPA Ivan Alvarez, CPA PLLC Audit, Tax, Bookkeeping, & Advisory Disclaimer This notice is required by IRS Circular 230,

9 Tips to Save Time, Lower Taxes, & Improve Profits By Evie Alvarez & Ivan Alvarez, CPA Ivan Alvarez, CPA PLLC Audit, Tax, Bookkeeping, & Advisory Disclaimer This notice is required by IRS Circular 230,

2014-2015 Tax Update: Another Year For Tax Breaks By Kurt J. Kilwein, CPA, CFP, Partner and Olga Zarney, CPA, MBT, Manager

WINTER 2014-2015 2014-2015 Tax Update: Another Year For Tax Breaks By Kurt J. Kilwein, CPA, CFP, Partner and Olga Zarney, CPA, MBT, Manager Individual Taxation Many of the tax breaks which expired at the

WINTER 2014-2015 2014-2015 Tax Update: Another Year For Tax Breaks By Kurt J. Kilwein, CPA, CFP, Partner and Olga Zarney, CPA, MBT, Manager Individual Taxation Many of the tax breaks which expired at the

Tax Night: Planning for Higher Income, Estate, and Medicare Taxes

Tax Night: Planning for Higher Income, Estate, and Medicare Taxes after the 2012 Elections, Attorney Tax Section of the Los Angeles County Bar Association 1, Business and Tax Attorney Law Office of 818-936-3490

Tax Night: Planning for Higher Income, Estate, and Medicare Taxes after the 2012 Elections, Attorney Tax Section of the Los Angeles County Bar Association 1, Business and Tax Attorney Law Office of 818-936-3490

Small Businesses and Tax Reform

Small Businesses and Tax Reform Professor Annette Nellen San José State University http://www.21stcenturytaxation.com/ 1 [email protected] Testimony Submitted for the Written Record of a Hearing

Small Businesses and Tax Reform Professor Annette Nellen San José State University http://www.21stcenturytaxation.com/ 1 [email protected] Testimony Submitted for the Written Record of a Hearing

Tax Implications of Health Care Reform

Tax Implications of Health Care Reform Presented by: Art Sparks, CPA Partner Certified Public Accountants Summary Summary The Patient Protection and Affordable Care Act (PPACA) and the companion Health

Tax Implications of Health Care Reform Presented by: Art Sparks, CPA Partner Certified Public Accountants Summary Summary The Patient Protection and Affordable Care Act (PPACA) and the companion Health

ILLINOIS REGISTER DEPARTMENT OF REVENUE JANUARY 2016 REGULATORY AGENDA

a) Part (Heading and Code Citations): Income Tax, 86 Ill. Adm. Code 100 A) Description: New rules will be added to Part 100 concerning the tax credit for Tech Prep Youth Vocational Programs (IITA Section

a) Part (Heading and Code Citations): Income Tax, 86 Ill. Adm. Code 100 A) Description: New rules will be added to Part 100 concerning the tax credit for Tech Prep Youth Vocational Programs (IITA Section

The Patient Protection and Affordable Care Act ( ACA ) and Your Facility

and Your Facility") The Patient Protection and Affordable Care Act ( ACA ) and Your Facility By Christine Garrity: Chief Administrative Officer & General Counsel for The Professional Golfers' Association of America President

The Patient Protection and Affordable Care Act ( ACA ) and Your Facility By Christine Garrity: Chief Administrative Officer & General Counsel for The Professional Golfers' Association of America President

Key Provisions of 2010 Healthcare Reform Legislation for Small (under 50) Employers. By Alice Eastman Helle. October 2013 Update

Employers. By Alice Eastman Helle. October 2013 Update") Key Provisions of 2010 Healthcare Reform Legislation for Small (under 50) Employers By Alice Eastman Helle October 2013 Update The sweeping healthcare reform legislation enacted in 2010 is exceedingly

Key Provisions of 2010 Healthcare Reform Legislation for Small (under 50) Employers By Alice Eastman Helle October 2013 Update The sweeping healthcare reform legislation enacted in 2010 is exceedingly

PRIVATE FOUNDATION CAUTION: The purposes of this memorandum are to assist you, the directors of your private foundation, and your accountant in:

CHERRY CREEK CORPORATE CENTER 4500 CHERRY CREEK DRIVE SOUTH #600 DENVER, CO 80246-1500 303.322.8943 WWW.WADEASH.COM DISCLAIMER Material presented on the Wade Ash Woods Hill & Farley, P.C., website is intended

CHERRY CREEK CORPORATE CENTER 4500 CHERRY CREEK DRIVE SOUTH #600 DENVER, CO 80246-1500 303.322.8943 WWW.WADEASH.COM DISCLAIMER Material presented on the Wade Ash Woods Hill & Farley, P.C., website is intended

Understanding Financial Statements. For Your Business

Understanding Financial Statements For Your Business Disclaimer The information provided is for informational purposes only, does not constitute legal advice or create an attorney-client relationship,

Understanding Financial Statements For Your Business Disclaimer The information provided is for informational purposes only, does not constitute legal advice or create an attorney-client relationship,

Passive Activities Estate and Trust Considerations. By: Robert Barnett CPA, JD, MS (TAXATION)

") Passive Activities Estate and Trust Considerations By: Robert Barnett CPA, JD, MS (TAXATION) 1. Why are passive activities important for Trust and Estate? Passive activities play an important role in many

Passive Activities Estate and Trust Considerations By: Robert Barnett CPA, JD, MS (TAXATION) 1. Why are passive activities important for Trust and Estate? Passive activities play an important role in many

business owner issues and depreciation deductions

business owner issues and depreciation deductions Individuals who are owners of a business, whether as sole proprietors or through a partnership, limited liability company or S corporation, have specific

business owner issues and depreciation deductions Individuals who are owners of a business, whether as sole proprietors or through a partnership, limited liability company or S corporation, have specific

U.S. Tax Benefits for Exporting

U.S. Tax Benefits for Exporting By Richard S. Lehman, Esq. TAX ATTORNEY www.lehmantaxlaw.com Richard S. Lehman Esq. International Tax Attorney LehmanTaxLaw.com 6018 S.W. 18th Street, Suite C-1 Boca Raton,

U.S. Tax Benefits for Exporting By Richard S. Lehman, Esq. TAX ATTORNEY www.lehmantaxlaw.com Richard S. Lehman Esq. International Tax Attorney LehmanTaxLaw.com 6018 S.W. 18th Street, Suite C-1 Boca Raton,

STATEMENT OF DAVID A. O NEIL ACTING ASSISTANT ATTORNEY GENERAL CRIMINAL DIVISION UNITED STATES DEPARTMENT OF JUSTICE BEFORE THE

STATEMENT OF DAVID A. O NEIL ACTING ASSISTANT ATTORNEY GENERAL CRIMINAL DIVISION UNITED STATES DEPARTMENT OF JUSTICE BEFORE THE COMMITTEE ON OVERSIGHT & GOVERNMENT REFORM SUBCOMMITTEE ON GOVERNMENT OPERATIONS

STATEMENT OF DAVID A. O NEIL ACTING ASSISTANT ATTORNEY GENERAL CRIMINAL DIVISION UNITED STATES DEPARTMENT OF JUSTICE BEFORE THE COMMITTEE ON OVERSIGHT & GOVERNMENT REFORM SUBCOMMITTEE ON GOVERNMENT OPERATIONS

Legal Considerations when Advising Marijuana / Cannabusiness Clients FEATURED FACULTY:

Legal Considerations when Advising Marijuana / Cannabusiness Clients FEATURED FACULTY: Matthew R. Abel, Attorney at Law, Cannabis Counsel, P.L.C [email protected] Matthew R. Abel, Attorney at Law, Cannabis

Legal Considerations when Advising Marijuana / Cannabusiness Clients FEATURED FACULTY: Matthew R. Abel, Attorney at Law, Cannabis Counsel, P.L.C [email protected] Matthew R. Abel, Attorney at Law, Cannabis

IN THE COURT OF APPEALS STATE OF ARIZONA DIVISION II ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) )

) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) ) )") JASON OSIFIE, v. Petitioner-Appellant, THE SUPERIOR COURT OF THE STATE OF ARIZONA, In and For the County of Pinal, and the Honorable Gilberto V. Figueroa, a judge thereof, and, Respondent, THE STATE OF

JASON OSIFIE, v. Petitioner-Appellant, THE SUPERIOR COURT OF THE STATE OF ARIZONA, In and For the County of Pinal, and the Honorable Gilberto V. Figueroa, a judge thereof, and, Respondent, THE STATE OF

FINAL BILL REPORT ESHB 1947

FINAL BILL REPORT C 6 L 13 E2 Synopsis as Enacted Brief Description: Concerning the operating expenses of the Washington health benefit exchange. Sponsors: House Committee on Appropriations (originally

FINAL BILL REPORT C 6 L 13 E2 Synopsis as Enacted Brief Description: Concerning the operating expenses of the Washington health benefit exchange. Sponsors: House Committee on Appropriations (originally

LLC ENTITY FORMATION. This is a Questionnaire. The purpose of this Limited Liability Company questionnaire is

LLC ENTITY FORMATION This is a Questionnaire. The purpose of this Limited Liability Company questionnaire is for us to determine what must be done to form a proper LLC for you. Its purpose is to fully

LLC ENTITY FORMATION This is a Questionnaire. The purpose of this Limited Liability Company questionnaire is for us to determine what must be done to form a proper LLC for you. Its purpose is to fully

Using ERISA Accounts to Help Manage Fee-Related Fiduciary Responsibilities

Defined Contribution Plans Fiduciary Focus Series Using ERISA Accounts to Help Manage Fee-Related Fiduciary Responsibilities Contents 1 Employer Fee Responsibilities 2 Revenue Sharing 3 DOL s View of ERISA

Defined Contribution Plans Fiduciary Focus Series Using ERISA Accounts to Help Manage Fee-Related Fiduciary Responsibilities Contents 1 Employer Fee Responsibilities 2 Revenue Sharing 3 DOL s View of ERISA

Health Care Law Implementation: What Nonprofits Need to Know WELCOME!

Health Care Law Implementation: What Nonprofits Need to Know WELCOME! Health Care Law Implementation: What Nonprofits Need to Know (PPACA) Health Care Law Implementation: What Nonprofits Need to Know Heather

Health Care Law Implementation: What Nonprofits Need to Know WELCOME! Health Care Law Implementation: What Nonprofits Need to Know (PPACA) Health Care Law Implementation: What Nonprofits Need to Know Heather

Questions & Answers Concerning the Agricultural Act of 2014 Sections4005, 4007, 4008, 4009, 4015, 4022, 4025, 4031

- USDA United States Department of Agriculture Food and Nutrition Service JUN'I 0 2014 Park Office Center 3101 Park Center Drive Alexandria VA 22302 SUBJECT: TO: Questions & Answers Concerning the Agricultural

- USDA United States Department of Agriculture Food and Nutrition Service JUN'I 0 2014 Park Office Center 3101 Park Center Drive Alexandria VA 22302 SUBJECT: TO: Questions & Answers Concerning the Agricultural

UNITED STATES COURT OF APPEALS FOR THE NINTH CIRCUIT

FOR PUBLICATION UNITED STATES COURT OF APPEALS FOR THE NINTH CIRCUIT MARTIN OLIVE, Petitioner-Appellant, v. COMMISSIONER OF INTERNAL REVENUE, Respondent-Appellee. No. 13-70510 Tax Ct. No. 14406-08 OPINION

FOR PUBLICATION UNITED STATES COURT OF APPEALS FOR THE NINTH CIRCUIT MARTIN OLIVE, Petitioner-Appellant, v. COMMISSIONER OF INTERNAL REVENUE, Respondent-Appellee. No. 13-70510 Tax Ct. No. 14406-08 OPINION

The Three Basic Types of Charitable Foundations

FAMILY CHARITABLE ENTITIES Dorothy K. Foster, Esq. FOSTER LAW GROUP, PLLC 800 Fifth Avenue, Suite 4100 Seattle, Washington 98104 355 Erickson Avenue, Suite 410 Bainbridge Island, Washington 98110 Ph: (206)

FAMILY CHARITABLE ENTITIES Dorothy K. Foster, Esq. FOSTER LAW GROUP, PLLC 800 Fifth Avenue, Suite 4100 Seattle, Washington 98104 355 Erickson Avenue, Suite 410 Bainbridge Island, Washington 98110 Ph: (206)

FATCA FAQs: Frequently asked questions on the Foreign Account Tax Compliance

www.pwc.com/us/fatca July 2011 FATCA FAQs: Frequently asked questions on the Foreign Account Tax Compliance Act 1. What is FATCA? FATCA is an acronym for The Foreign Account Tax Compliance Act (FATCA)

www.pwc.com/us/fatca July 2011 FATCA FAQs: Frequently asked questions on the Foreign Account Tax Compliance Act 1. What is FATCA? FATCA is an acronym for The Foreign Account Tax Compliance Act (FATCA)

Tax Planning and Reporting for a Small Business

Table of Contents Welcome... 3 What Do You Know? Tax Planning and Reporting for a Small Business... 4 Pre-Test... 5 Tax Obligation Management... 6 Business Taxes... 6 Federal Income Tax Forms... 7 Discussion

Table of Contents Welcome... 3 What Do You Know? Tax Planning and Reporting for a Small Business... 4 Pre-Test... 5 Tax Obligation Management... 6 Business Taxes... 6 Federal Income Tax Forms... 7 Discussion

LEX HELIUS: THE LAW OF SOLAR ENERGY Tax Issues

LEX HELIUS: THE LAW OF SOLAR ENERGY Tax Issues Charles S. Lewis, III 600 University Street, Suite 3600 Seattle, WA 98101-4109 206-386-7688 [email protected] Kevin T. Pearson 900 SW Fifth Avenue, Suite

LEX HELIUS: THE LAW OF SOLAR ENERGY Tax Issues Charles S. Lewis, III 600 University Street, Suite 3600 Seattle, WA 98101-4109 206-386-7688 [email protected] Kevin T. Pearson 900 SW Fifth Avenue, Suite

---------------------------------: Graduate Level Tuition Waivers as Taxable Fringe Benefits

Office of Chief Counsel Internal Revenue Service Memorandum Release Number: 20103901F Release Date: 10/1/10 CC:TEGE:FS:MABAL:MLenius POSTF-122161-10 UIL: 117.00-00; 127.00-00; 132.03-00 date: July 27,

Office of Chief Counsel Internal Revenue Service Memorandum Release Number: 20103901F Release Date: 10/1/10 CC:TEGE:FS:MABAL:MLenius POSTF-122161-10 UIL: 117.00-00; 127.00-00; 132.03-00 date: July 27,

Case 1:13-cv-21304-XXXX Document 1 Entered on FLSD Docket 04/15/2013 Page 1 of 15

Case 1:13-cv-21304-XXXX Document 1 Entered on FLSD Docket 04/15/2013 Page 1 of 15 IN THE UNITED STATES DISTRICT COURT FOR THE SOUTHERN DISTRICT OF FLORIDA MIAMI DIVISION UNITED STATES OF AMERICA, ) ) Plaintiff,

Case 1:13-cv-21304-XXXX Document 1 Entered on FLSD Docket 04/15/2013 Page 1 of 15 IN THE UNITED STATES DISTRICT COURT FOR THE SOUTHERN DISTRICT OF FLORIDA MIAMI DIVISION UNITED STATES OF AMERICA, ) ) Plaintiff,

GAO LIFE INSURANCE SETTLEMENTS. Regulatory Inconsistencies May Pose a Number of Challenges. Report to the Special Committee on Aging, U.S.

GAO United States Government Accountability Office Report to the Special Committee on Aging, U.S. Senate July 2010 LIFE INSURANCE SETTLEMENTS Regulatory Inconsistencies May Pose a Number of Challenges

GAO United States Government Accountability Office Report to the Special Committee on Aging, U.S. Senate July 2010 LIFE INSURANCE SETTLEMENTS Regulatory Inconsistencies May Pose a Number of Challenges

American employers need prompt action on these six significant challenges. We urge Congress and the administration to address them now.

In June 2014, the Board of Directors of the American Benefits Council (the Council) approved a long-term public policy strategic plan, A 2020 Vision: Flexibility and the Future of Employee Benefits. It

In June 2014, the Board of Directors of the American Benefits Council (the Council) approved a long-term public policy strategic plan, A 2020 Vision: Flexibility and the Future of Employee Benefits. It

Breakeven Analysis. Breakeven for Services.

Dollars and Sense Introduction Your dream is to operate a profitable business and make a good living. Before you open, however, you want some indication that your business will be profitable, if not immediately

Dollars and Sense Introduction Your dream is to operate a profitable business and make a good living. Before you open, however, you want some indication that your business will be profitable, if not immediately