U.S. Tax Benefits for Exporting

|

|

|

- Geoffrey Moore

- 10 years ago

- Views:

Transcription

1 U.S. Tax Benefits for Exporting By Richard S. Lehman, Esq. TAX ATTORNEY

2 Richard S. Lehman Esq. International Tax Attorney LehmanTaxLaw.com 6018 S.W. 18th Street, Suite C-1 Boca Raton, FL Tel: (561) Fax: (561) Masters in Tax Law from New York University Law School Four years of U.S. Tax Court and Internal Revenue Service experience in Washington D.C. The firm regularly works with law firms, accountants, businesses and individuals struggling to find their way through the complexities of the tax law. In short, the firm is a valuable resource to each of these audiences. With over 38 years as a tax lawyer in Florida, Lehman has built a tax law firm with a national reputation for being able to handle the toughest tax cases, structure the most sophisticated income tax and estate tax plans, and defend clients before the IRS.

3 IC-DISC A Major Tax Saving Tool

4 IC-DISC A Major Tax Saving Tool 1)Tax incentive for Americans who export product. 2)Available to manufactures, producers, wholesaler and retailer that sell export property

5 IC-DISC A Major Tax Saving Tool The U.S. Taxpayer pays 15% Tax Rate on export profits. Instead of a 35% Federal Tax Rate.

6 IC-DISC A Major Tax Saving Tool If you live in a State that has City/State Income Tax - You pay 15% tax rate NOT 50% on your export profits. Plus Taxpayer can differ export profits for many years at low interest costs.

7 Major Tax Reductions for Export Profits U.S. taxpayers that sell, lease or license export property which is manufactured, produced or grown in the United States (not more than 50% of which attributable to U.S. imports), can take advantage of strong support for their export profits in the Internal Revenue Code.

8 The United States Tax Benefits of Exporting In 2012 the business world is going to be a tough place for the American Exporter. Take advantage of the Internal Revenue Code and it s strong support for export profits.

9 Major Tax Reductions for Export Profits 1. Establish a new corporation dedicated almost exclusively to export profits; 2. a separate set of export books and records; and 3. abiding by a relatively simple set of rules that govern Domestic International Sales Corporations (now known as IC-DISC).

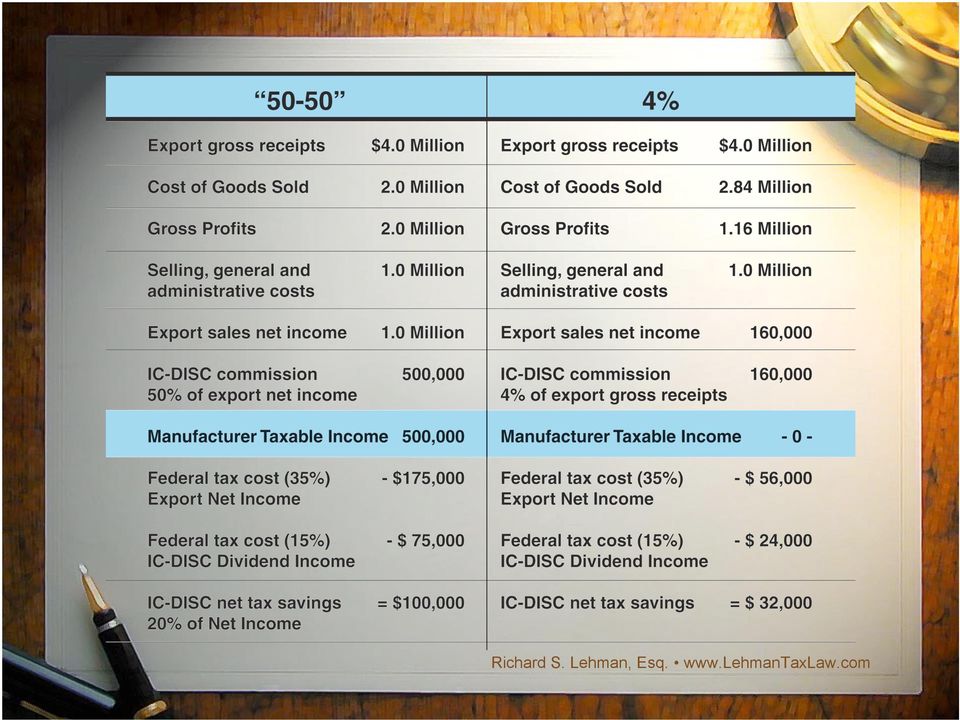

10 How does it work. Typically the U.S. taxpayer that establishes the IC-DISC will be related to the IC-DISC and even own the IC-DISC. The U.S. taxpayer agrees to pay the IC-DISC based on a Commission Agreement. A portion of the U.S. taxpayer s export profits are paid to the IC-DISC and the payment is deducted from the profits of the U.S. manufacturer, seller or licensor. The portion of the U.S. taxpayer s export profits that are paid to the IC DISC are measured under three profit scenarios. The deduction may exceed more than 50% of the U.S. Taxpayers export profits, depending upon gross income, profitability and costs.

11 IC-DISC Rules The IC-DISC must sell, lease, license or service export property Export property means property: Manufactured, produced, grown or extracted in the United States; held for sale, lease or rental, in the ordinary course of business, for use, consumption or disposition outside the United States; and Not more than 50% of the fair market value of which is attributed to articles imported into the United States.

12 IC-DISC Requirements 1. A corporation taxable as a corporation, must be formed under the laws of any State or the District of Columbia to be the IC-DISC 2. The corporation must have only one class of stock and minimum capital of $2,500. The IC-DISC shareholders may be related to the IC-DISC. 3. The IC-DISC must take a tax election to be an IC-DISC that must be filed with the Internal Revenue Service within 90 days after the beginning of the tax year of the IC-DISC. 4. The IC-DISC must maintain separate books and records. 5. The IC-DISC must have at least 95% or more of its gross receipts considered to be Qualified Receipts resulting from the DISC s export activities. 6. The IC-DISC must have at least 95% or more of its assets considered to be Qualified Export Assets.

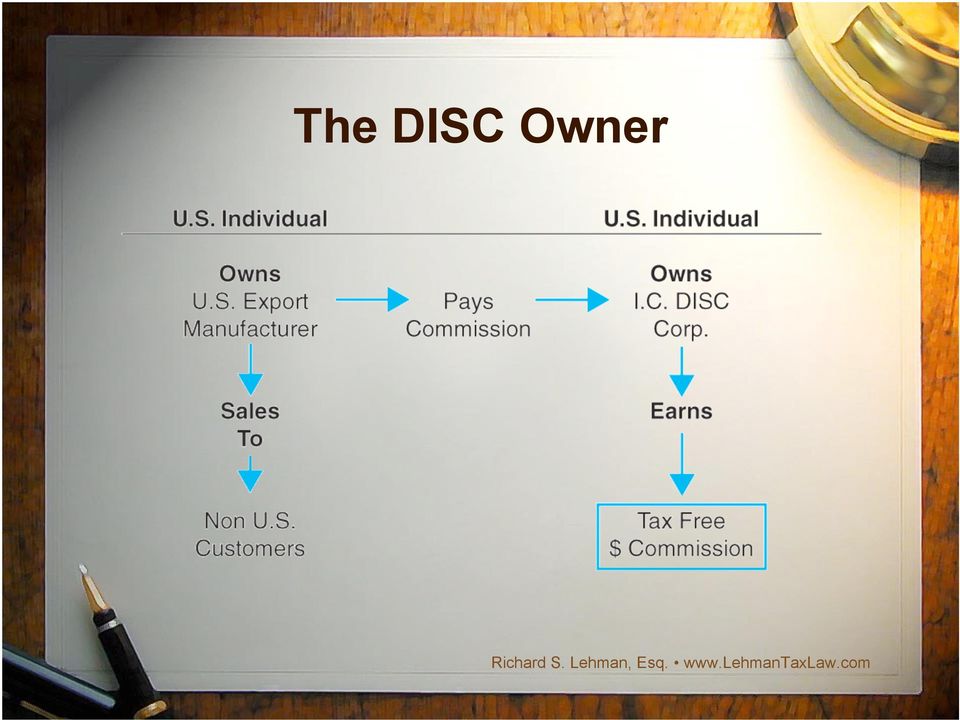

13 The DISC Owner Typically the IC-DISC is established, by a related company that is engaged in a United States business that includes gross revenues from both domestic and international sources. The related company s principals will be the direct or indirect owners of the IC-DISC

14 The DISC Owner

15 The Tax Benefits Thus the magic of the IC-DISC is to provide both tax deferral and to apply a 15% maximum dividend tax rate to profits that would otherwise be taxable in the U.S. taxpayer s highest brackets that can range as high as 50%.

16 Tax Deferral There is a cost to take advantage of the tax deferral tax benefit available using an IC-DISC. However, in today s climate and for the foreseeable future, the cost is minimal. The IC-DISC rules provide that an interest charge must be calculated on IC-DISC distributions that are not paid as taxable dividends in the year earned.

17

18 Major Savings IC-DISC shareholders still will receive the 15% tax rate on the DISC dividends in excess of $10 Million.

19 The Commission Payments Gross Receipts Method Taxable Income Method Export promotion expenses means those expenses incurred to advance the distribution or sale of export property for use, consumption, or distributions outside of the United States but does not include income taxes. Arm s Length Method The transfer price for a sale by the related supplier to the DISC is to be determined on the basis of the sale price actually charged but subject to the rules provided by the rules of sales between related parties.

20 IC-DISC The Export Disc Corporation Computer Software, Internet Sales & Licenses

21 IC-DISC A Major Tax Saving Tool The IC-DISC has been approved as an acceptable tax planning entity for the export of American produced computer software and programs as early as 1985.

22 Computer Programs Are Usually Sold Pursuant to License or User Agreements. A computer program transaction is unlike a sale of a physical object since the value of the program copy far exceeds the value of the physical medium on which it is transferred. Often, there is no physical medium at all.

23 For purposes of determining the applicability of the DISC to computer software exports, two key analyses are often required. (1) is the software export property for DISC purposes and (2) is the software product s source of income from without the U.S.? Is the product for use, consumption or sale without the U.S.?

24 I.R.S. Guidance In 1985, the I.R.S. issued guidance that indeed certain computer software programs constituted export property for DISC purposes. In doing so the Technical Advice not only reviewed the legislative history of the DISC rules it also pointed out the distinctively different treatment that patents, inventions, models, decisions, formulas, or processes whether or not patented, copyrights, goodwill, trademarks, trade brands, franchise or other like property receive under the DISC rules, as opposed to the treatment of films, tapes, records or similar reproductions, for commercial or home use.

25 Copyright law is the basis for the Software Regulations The Regulations are based on the concept that it is possible to categorize a computer program transaction by analyzing the copyright rights transferred. The most important distinction created by the Software Regulations is the distinction between copyrighted articles and copyright rights. The Copyright Rights are not export property for DISC purposes while the Copyright Articles are export property.

26 Export Property Analysis Export property is defined to mean, in general, property that is: A. Manufactured, produced, grown or extracted in the United States by a person other than a DISC, B. Held primarily for sale, lease, or rental, in the ordinary course of trade or business, by, or to, a DISC, for direct use, consumption, or disposition outside the United States and C. Not more than 50 percent of the fair market value of which is attributable to articles imported into the United States.

27 Export Property Does Not Include patents, inventions, models, designs, formulas, or processes, whether or not patented, copyrights (other than films, tapes, records, or similar reproductions, for commercial or home use), good will, trademarks, trade brands, franchises, or other like property... Richard S. Lehman, Esq.

28 Computer software can be export property. Computer software tapes are akin to the copyrighted books, which qualify as export property. Computer programs are standardized programs that are manufactured in the United States by a person other than a DISC and then marketed outside the United States. This is not selling the source code or master recording. Those purchasing or leasing programs do not have the right to reproduce the software.

29 Copyright Rights The transfer is classified as a transfer of a copyright if, as a result of a transaction, a person acquires any one or more of the following rights: 1. the right to make copies of the computer program for purposes of distribution to the public by sale or other transfer of ownership, or by rental, lease or lending; 2. the right to prepare derivative computer programs based on the copyrighted computer program; 3. the right to make a public performance of the computer program; or 4. the right to publicly display the computer program.

30 Transfers of Computer Programs A computer program includes any media, user manuals, documentation, database or similar item if the media user manuals, documentation, database or similar item is incidental to the operation of the computer program.

31 Transfers of Computer Programs A copyrighted article is defined as a copy of a computer program from which the work can be perceived, reproduced, or otherwise communicated, either directly or with the aid of a machine or device. If a person acquires a copy of a computer program but does not acquire any of the four copyright rights, the transfer is classified as a transfer of a copyrighted article.

32 A transfer of a computer program is classified in one of the following ways. 1. A sale or exchange of the legal rights constituting a copyright (which generates income sourced according to the rules for sales of personal property); 2. A license of a copyright (which generates royalty income); 3. A sale or exchange of a copyright article produced under a copyright (which generates income sourced according to the rules for sales of personal property); 4. A lease of a copyright article produced under a copyright (which generates rental income) Additional rules allow for the classification of a transfer as partially a transfer of services or of know-how. The provision of know-how, in which the transferor retains continuing use of the know how transferred, is presumably most like a license of a copyright.

33 The Source of Income Analysis Once it is determined that a computer program is a copyright article and thus export property for DISC purposes;...then the issue is to determine whether the Software Program is being sold for use, consumption of disposition outside of the U.S. This analysis depends upon the source of income rules.

34 Income from Sales of Property Generally under the current rules, the source of income from sales of property depends to varying extents upon both the type of property and whether the property sold or leased is inventory property. Income from the lease of a copyright article must also fit this definition of non U.S. source of income. Determination of whether the transaction is a sale of inventory, a rental of property, a license or sale of intellectual property or the provision of services.

35 Income from Sales of Property Generally under the current rules, the source of income from sales of property depends to varying extents upon both the type of property and whether the property sold or leased is inventory property. Income from the lease of a copyright article must also fit this definition of non U.S. source of income. Determination of whether the transaction is a sale of inventory, a rental of property, a license or sale of intellectual property or the provision of services.

36 Income from Sales of Property The regulations focus on (i) acknowledging the special circumstances of computer programs, (ii) distinguishing between transactions in copyright rights and in copyrighted articles, and (iii) focusing on the economic substance of the transaction over the labels applied, the form and the delivery mechanism.

37 Source of Income for Sales of Copyrighted Articles The source of income generated by the sale or exchange of a copyrighted article often depends upon whether the sale took place within or without the United States. The Software Regulations provide that the place of sale is determined under the title passage rule. Richard S. Lehman, Esq.

38 Title Passage Rule There are important categories of copyrighted article transfers for DISC purposes: (i) a transfer of tangible property, such as a tangible medium in which the copyrighted article is embodied, and/or a hard copy of user manuals and documentation; (ii) (e.g., electronically transmitted copyrighted articles without any hard copy of user manuals and documentation). Either one of these can be the subject of a sale.

39 Lease and Rental Source of Income If less than all of the benefits and burdens associated with a copyrighted article have passed to the transferee, the Software Regulations treat the transaction as a lease. As a general rule, rents and royalties are sourced to the place where the leased or licensed property is located, or where the lessee or licensee uses, or is entitled to use the property.

40 Sale of Copyright Article Example 1 A U.S. corporation, (the U.S. corporation ) owns the copyright in a computer program, (the Program ). The U.S. corporation, (the U.S. Corporation ), makes the Program available, for a fee, on a World Wide Web home page on the Internet. Mr. P, a resident of Country Z, in return for payment to the U.S. Corporation, downloads the Program X (via modem) onto the hard drive of his computer. As part of the electronic communications, P signifies his assent to a license agreement. Mr. P receives the right to use the program on his own computers (for example, a laptop and a desktop). None of the copyright rights have been transferred in this transaction. P has received a copy of the Program. P has acquired solely a copyrighted article. P is properly treated as the owner of a copyrighted article. There has been a sale of a copyrighted article rather than the grant of a lease.

41 Lease of Copyright Article Example 2 The facts are the same as those in Example 1, except that the U.S. Corporation only allows Mr. P, the right to use the Program for one week. If P wishes to use the Program for a further period he must enter into a new agreement to use the program for an additional charge. P is not properly treated as the owner of a copyrighted article. There has been a lease of a copyrighted article rather than a sale.

42 Sale of Copyright Example 3 A U.S. Corporation, transfers a disk containing the Program to a Foreign Corporation (the Foreign Corporation ) and grants the Foreign Corporation an exclusive license for the remaining term of the copyright to copy and distribute an unlimited number of copies of the Program in the geographic area of the Country in which the Foreign Corporation makes public performances of the Program and publicly displays the Program. Applying the all substantial rights test, the U.S. Corporation will be treated as having sold copyright rights to the Foreign Corporation. The Foreign Corporation has acquired all of the copyright rights in the Program and has received the right to use them exclusively within the Foreign Country.

43 Lease of Copyright Rights Example 4 A U.S. corporation, transfers a disk containing the Program to a Foreign Corporation in Country X and grants the Foreign Corporation the non exclusive right to reproduce (either directly or by contracting with another person to do so) and distribute for sale to the public an unlimited number of disks at its factory in return for a payment related to the number of disks copied and sold. The term of the agreement is two years, which is less than the remaining life of the copyright. There is a lease of copyright rights since copyright right have been assigned but for a limited time period only.

44 Richard S. Lehman, Esq. TAX ATTORNEY 6018 S.W. 18th Street, Suite C-1, Boca Raton, FL Tel: Value can be lost without good professional advice.

How To Determine If A Computer Program Is A Copyright Right Or A Copyright Article

IRS Software Regulations for Purchasing Software from Foreign Vendors Reg 251520-96 - Sec. 1.861-18 Classification of transactions involving computer programs. (a) General -- (1) Scope. This section provides

IRS Software Regulations for Purchasing Software from Foreign Vendors Reg 251520-96 - Sec. 1.861-18 Classification of transactions involving computer programs. (a) General -- (1) Scope. This section provides

U.S. Taxation of Foreign Investors

PART OF THE LEHMAN TAX LAW KNOWLEDGE BASE SERIES United States Taxation Of Investors U.S. Taxation of Foreign Investors Non Resident Alien Individuals & Foreign Corporations By Richard S. Lehman Esq. TAX

PART OF THE LEHMAN TAX LAW KNOWLEDGE BASE SERIES United States Taxation Of Investors U.S. Taxation of Foreign Investors Non Resident Alien Individuals & Foreign Corporations By Richard S. Lehman Esq. TAX

U.S. Taxation of Foreign Investors

U.S. Taxation of Foreign Investors By Richard S. Lehman & Associates Attorneys at Law Copyright 2004 Copyright by Richard S. Lehman Page 1 U.S. Taxation of Foreign Corporations And Nonresident Aliens General

U.S. Taxation of Foreign Investors By Richard S. Lehman & Associates Attorneys at Law Copyright 2004 Copyright by Richard S. Lehman Page 1 U.S. Taxation of Foreign Corporations And Nonresident Aliens General

Tax Advantages of IC-DISCS. 2013 National Pecan Shellers Association / Annual Meeting

Tax Advantages of IC-DISCS 2013 National Pecan Shellers Association / Annual Meeting WHAT IS A DISC???? Statutory Requirements - Formation The IC-DISC must be a U.S. Corporation Typically incorporated

Tax Advantages of IC-DISCS 2013 National Pecan Shellers Association / Annual Meeting WHAT IS A DISC???? Statutory Requirements - Formation The IC-DISC must be a U.S. Corporation Typically incorporated

How To Tax An Indian Company In The United States

Introduction Taxation of software supplied by foreign companies -Raj Shroff & Daksha Baxi Nishith Desai Associates With the growth of information technology, business process outsourcing and bio-informatics

Introduction Taxation of software supplied by foreign companies -Raj Shroff & Daksha Baxi Nishith Desai Associates With the growth of information technology, business process outsourcing and bio-informatics

Department of Taxation

Department of Taxation Commerce Tax Presentation Deonne E. Contine, Executive Director Sumiko Maser, Chief Deputy Executive Director Paulina Oliver, Deputy Executive Director What do I need to do to determine

Department of Taxation Commerce Tax Presentation Deonne E. Contine, Executive Director Sumiko Maser, Chief Deputy Executive Director Paulina Oliver, Deputy Executive Director What do I need to do to determine

TAX PLANNING FOR THE FOREIGN REAL ESTATE INVESTOR

TAX PLANNING FOR THE FOREIGN REAL ESTATE INVESTOR Tax Benefits and Tax Traps By Richard S. Lehman & Associates Attorneys at Law TAX PLANNING FOR THE FOREIGN REAL ESTATE INVESTOR Tax Benefits and Tax Traps

TAX PLANNING FOR THE FOREIGN REAL ESTATE INVESTOR Tax Benefits and Tax Traps By Richard S. Lehman & Associates Attorneys at Law TAX PLANNING FOR THE FOREIGN REAL ESTATE INVESTOR Tax Benefits and Tax Traps

TAX ISSUES RAISED BY LNG PROJECTS

TAX ISSUES RAISED BY LNG PROJECTS Jon Lobb Baker Botts L.L.P. ABSTRACT This paper discusses tax issues that may be encountered by a company investing in an LNG project. 1. Income Taxes A seller's income

TAX ISSUES RAISED BY LNG PROJECTS Jon Lobb Baker Botts L.L.P. ABSTRACT This paper discusses tax issues that may be encountered by a company investing in an LNG project. 1. Income Taxes A seller's income

Instructions for 2013 Form 4A-1: Wisconsin Apportionment Data for Single Factor Formulas

Instructions for 2013 Form 4A-1: Wisconsin Apportionment Data for Single Factor Formulas Purpose of Form 4A-1 Corporations, partnerships, tax-option (S) corporations and nonresident estates, trusts, and

Instructions for 2013 Form 4A-1: Wisconsin Apportionment Data for Single Factor Formulas Purpose of Form 4A-1 Corporations, partnerships, tax-option (S) corporations and nonresident estates, trusts, and

Willamette Management Associates

Valuation Analyst Considerations in the C Corporation Conversion to Pass-Through Entity Tax Status Robert F. Reilly, CPA For a variety of economic and taxation reasons, this year may be a particularly

Valuation Analyst Considerations in the C Corporation Conversion to Pass-Through Entity Tax Status Robert F. Reilly, CPA For a variety of economic and taxation reasons, this year may be a particularly

SALE BY TRUSTEE IN BANKRUPTCY 1003.10

SALE BY TRUSTEE IN BANKRUPTCY 1003.10 Sales by a trustee in bankruptcy are subject to the tax if made during the operation of the business of the debtor to the same extent as sales by other retailers.

SALE BY TRUSTEE IN BANKRUPTCY 1003.10 Sales by a trustee in bankruptcy are subject to the tax if made during the operation of the business of the debtor to the same extent as sales by other retailers.

FYI For Your Information

TAXPAYER SERVICE DIVISION FYI For Your Information Apportionment of Income C CORPORATIONS A C Corporation doing business only in Colorado will compute its tax on 100% of the Colorado taxable income. However,

TAXPAYER SERVICE DIVISION FYI For Your Information Apportionment of Income C CORPORATIONS A C Corporation doing business only in Colorado will compute its tax on 100% of the Colorado taxable income. However,

SHOULD MY BUSINESS BE AN S CORPORATION OR A LIMITED LIABILITY COMPANY?

SHOULD MY BUSINESS BE AN S CORPORATION OR A LIMITED LIABILITY COMPANY? 2015 Keith J. Kanouse One Boca Place, Suite 324 Atrium 2255 Glades Road Boca Raton, Florida 33431 Telephone: (561) 451-8090 Fax: (561)

SHOULD MY BUSINESS BE AN S CORPORATION OR A LIMITED LIABILITY COMPANY? 2015 Keith J. Kanouse One Boca Place, Suite 324 Atrium 2255 Glades Road Boca Raton, Florida 33431 Telephone: (561) 451-8090 Fax: (561)

FEDERAL TAXATION OF INTERNATIONAL TRANSACTIONS

Chapter 10 FEDERAL TAXATION OF INTERNATIONAL TRANSACTIONS Daniel Cassidy 1 10.1 INTRODUCTION Foreign companies with U.S. business transactions face various layers of taxation. These include income, sales,

Chapter 10 FEDERAL TAXATION OF INTERNATIONAL TRANSACTIONS Daniel Cassidy 1 10.1 INTRODUCTION Foreign companies with U.S. business transactions face various layers of taxation. These include income, sales,

Instructions for Form 1120-IC-DISC (Rev. December 2012)

") Instructions for Form 1120-IC-DISC (Rev. December 2012) Interest Charge Domestic International Sales Corporation Return Department of the Treasury Internal Revenue Service Section references are to the

Instructions for Form 1120-IC-DISC (Rev. December 2012) Interest Charge Domestic International Sales Corporation Return Department of the Treasury Internal Revenue Service Section references are to the

The I.R.S. Amnesty Program & The New Streamlined Filing Compliance Procedures

TOPICS IN THE SEMINAR INCLUDE: The I.R.S. Amnesty Program & The New Streamlined Filing Compliance Procedures By Richard S. Lehman, Esq. TAX ATTORNEY www.lehmantaxlaw.com SEMINAR INTRODUCTION by Richard

TOPICS IN THE SEMINAR INCLUDE: The I.R.S. Amnesty Program & The New Streamlined Filing Compliance Procedures By Richard S. Lehman, Esq. TAX ATTORNEY www.lehmantaxlaw.com SEMINAR INTRODUCTION by Richard

2013 Ohio Small Business Investor Income Deduction

2013 Ohio Small Business Investor Income Deduction Instructions for Apportioning Business Income Solely for Purposes of Computing the Small Business Investor Income Deduction hio Department of Taxation

2013 Ohio Small Business Investor Income Deduction Instructions for Apportioning Business Income Solely for Purposes of Computing the Small Business Investor Income Deduction hio Department of Taxation

Limited Liability Companies (LLCs) Benefits and advantages associated with an LLC

Benefits and advantages associated with an LLC") Limited Liability Companies (LLCs) In the early 1980s Florida became the second state to authorize the formation of limited liability companies ("LLCs"). Now more than 100,000 LLCs are formed in Florida

Limited Liability Companies (LLCs) In the early 1980s Florida became the second state to authorize the formation of limited liability companies ("LLCs"). Now more than 100,000 LLCs are formed in Florida

SC REVENUE RULING #06-12. All previous advisory opinions and any oral directives in conflict herewith.

State of South Carolina Department of Revenue 301 Gervais Street, P. O. Box 125, Columbia, South Carolina 29214 Website Address: http://www.sctax.org SC REVENUE RULING #06-12 SUBJECT: Tax Rate Reduction

State of South Carolina Department of Revenue 301 Gervais Street, P. O. Box 125, Columbia, South Carolina 29214 Website Address: http://www.sctax.org SC REVENUE RULING #06-12 SUBJECT: Tax Rate Reduction

Florida Partnership Information Return

Florida Partnership Information Return For the taxable year beginning, and ending,. F-1065 Rule 12C-1.051 Florida Administrative Code Effective 01/16 Name of Partnership Street Address City State ZIP -

Florida Partnership Information Return For the taxable year beginning, and ending,. F-1065 Rule 12C-1.051 Florida Administrative Code Effective 01/16 Name of Partnership Street Address City State ZIP -

1. Nonresident Alien or Resident Alien?

U..S.. Tax Guiide for Non-Resiidents Table of Contents A. U.S. INCOME TAXES ON NON-RESIDENTS 1. Nonresident Alien or Resident Alien? o Nonresident Aliens o Resident Aliens Green Card Test Substantial Presence

U..S.. Tax Guiide for Non-Resiidents Table of Contents A. U.S. INCOME TAXES ON NON-RESIDENTS 1. Nonresident Alien or Resident Alien? o Nonresident Aliens o Resident Aliens Green Card Test Substantial Presence

Cross Border Tax Issues

Cross Border Tax Issues By Reinhold G. Krahn December 2000 This is a general overview of the subject matter and should not be relied upon as legal advice or opinion. For specific legal advice on the information

Cross Border Tax Issues By Reinhold G. Krahn December 2000 This is a general overview of the subject matter and should not be relied upon as legal advice or opinion. For specific legal advice on the information

Non-Financial Assets Tax and Other Special Rules

Wealth Strategy Report Non-Financial Assets Tax and Other Special Rules OVERVIEW Because unique attributes distinguish them from other asset classes, nonfinancial assets may offer you valuable financial

Wealth Strategy Report Non-Financial Assets Tax and Other Special Rules OVERVIEW Because unique attributes distinguish them from other asset classes, nonfinancial assets may offer you valuable financial

BRIEF OVERVIEW OF PENNSYLVANIA PERSONAL INCOME TAX

CHAPTER 6: BRIEF OVERVIEW OF PENNSYLVANIA PERSONAL INCOME TAX TABLE OF CONTENTS I. OVERVIEW 2 II. TAX RATE...3 III. EIGHT CLASSES OF INCOME 3 A. Gross Compensation... 3 B. Interest... 4 C. Dividends...

CHAPTER 6: BRIEF OVERVIEW OF PENNSYLVANIA PERSONAL INCOME TAX TABLE OF CONTENTS I. OVERVIEW 2 II. TAX RATE...3 III. EIGHT CLASSES OF INCOME 3 A. Gross Compensation... 3 B. Interest... 4 C. Dividends...

Marketing Ingenuity and Invention an Innovation Guidebook

The following is an extraction from Marketing Ingenuity and Invention: an Innovation Guidebook, a publication from the Wisconsin Innovation Service Center. Marketing Ingenuity and Invention an Innovation

The following is an extraction from Marketing Ingenuity and Invention: an Innovation Guidebook, a publication from the Wisconsin Innovation Service Center. Marketing Ingenuity and Invention an Innovation

TO: OUR FRIENDS AND PROSPECTIVE CLIENTS FROM: THOMAS WILLIAMS, CPA RE: U.S. INCOME TAX ISSUES OF FOREIGN NATIONALS DATE: AS OF JANUARY 1, 2010

THOMAS WILLIAMS CPA, PLLC TO: OUR FRIENDS AND PROSPECTIVE CLIENTS FROM: THOMAS WILLIAMS, CPA RE: U.S. INCOME TAX ISSUES OF FOREIGN NATIONALS DATE: AS OF JANUARY 1, 2010 Dear Friends: The following is an

THOMAS WILLIAMS CPA, PLLC TO: OUR FRIENDS AND PROSPECTIVE CLIENTS FROM: THOMAS WILLIAMS, CPA RE: U.S. INCOME TAX ISSUES OF FOREIGN NATIONALS DATE: AS OF JANUARY 1, 2010 Dear Friends: The following is an

INTERNATIONAL TAX COMPLIANCE FOR GOVERNMENT CONTRACTORS

INTERNATIONAL TAX COMPLIANCE FOR GOVERNMENT CONTRACTORS Mark T. Gossart Alison N. Dougherty September 26, 2012 2012 All Rights Reserved 805 King Farm Boulevard Suite 300 Rockville, Maryland 20850 301.231.6200

INTERNATIONAL TAX COMPLIANCE FOR GOVERNMENT CONTRACTORS Mark T. Gossart Alison N. Dougherty September 26, 2012 2012 All Rights Reserved 805 King Farm Boulevard Suite 300 Rockville, Maryland 20850 301.231.6200

Financial Statements Tutorial

Financial Statement Review: Financial Statements Tutorial There are four major financial statements used to communicate information to external users (creditors, investors, suppliers, etc.) - 1. Balance

Financial Statement Review: Financial Statements Tutorial There are four major financial statements used to communicate information to external users (creditors, investors, suppliers, etc.) - 1. Balance

Intangible Assets. HKAS 38 Revised March 2010June 2014. Effective for annual periods beginning on or after 1 January 2005

HKAS 38 Revised March 2010June 2014 Effective for annual periods beginning on or after 1 January 2005 Hong Kong Accounting Standard 38 Intangible Assets HKAS 38 COPYRIGHT Copyright 2014 Hong Kong Institute

HKAS 38 Revised March 2010June 2014 Effective for annual periods beginning on or after 1 January 2005 Hong Kong Accounting Standard 38 Intangible Assets HKAS 38 COPYRIGHT Copyright 2014 Hong Kong Institute

Chapter 9. Plant Assets. Determining the Cost of Plant Assets

Chapter 9 Plant Assets Plant Assets are also called fixed assets; property, plant and equipment; plant and equipment; long-term assets; operational assets; and long-lived assets. They are characterized

Chapter 9 Plant Assets Plant Assets are also called fixed assets; property, plant and equipment; plant and equipment; long-term assets; operational assets; and long-lived assets. They are characterized

SAN FRANCISCO S NEW GROSS RECEIPTS TAX AND BUSINESS REGISTRATION FEES

SAN FRANCISCO S NEW GROSS RECEIPTS TAX AND BUSINESS REGISTRATION FEES This summary provides basic information regarding San Francisco Business and Tax Regulations Code ( Code ), Article 12-A-1, Gross Receipts

SAN FRANCISCO S NEW GROSS RECEIPTS TAX AND BUSINESS REGISTRATION FEES This summary provides basic information regarding San Francisco Business and Tax Regulations Code ( Code ), Article 12-A-1, Gross Receipts

Sales and Use Taxes: Texas

Jay M. Chadha, Fulbright & Jaworski LLP A Q&A guide to sales and use tax law in Texas. This Q&A addresses key areas of sales and use tax law such as tax scope, multi-state transactions and collecting taxes

Jay M. Chadha, Fulbright & Jaworski LLP A Q&A guide to sales and use tax law in Texas. This Q&A addresses key areas of sales and use tax law such as tax scope, multi-state transactions and collecting taxes

INVESTING IRA AND QUALIFIED RETIREMENT PLAN ASSETS IN REAL ESTATE

INVESTING IRA AND QUALIFIED RETIREMENT PLAN ASSETS IN REAL ESTATE By: Charles M. Lax, Esq. I. DEFINITIONS A. What is a prohibited transaction? 1. A prohibited transaction is defined in IRC 4975(c)(1) as

INVESTING IRA AND QUALIFIED RETIREMENT PLAN ASSETS IN REAL ESTATE By: Charles M. Lax, Esq. I. DEFINITIONS A. What is a prohibited transaction? 1. A prohibited transaction is defined in IRC 4975(c)(1) as

Tax Rates. For personal income tax purposes, for tax years beginning after 2014, the tax rates are as follows:

October 2014 District of Columbia Reduced Tax Rates, Single Sales Factor, Other Changes Adopted Permanent District of Columbia budget legislation makes numerous significant changes to the corporation franchise

October 2014 District of Columbia Reduced Tax Rates, Single Sales Factor, Other Changes Adopted Permanent District of Columbia budget legislation makes numerous significant changes to the corporation franchise

Business Organization\Tax Structure

Business Organization\Tax Structure Kansas Secretary of State s Office Business Services Division First Floor, Memorial Hall 120 S.W. 10th Avenue Topeka, KS 66612-1594 Phone: (785) 296-4564 Fax: (785)

Business Organization\Tax Structure Kansas Secretary of State s Office Business Services Division First Floor, Memorial Hall 120 S.W. 10th Avenue Topeka, KS 66612-1594 Phone: (785) 296-4564 Fax: (785)

Reg. 1.5833-1 (Effective for tax years beginning on and after January 1, 1998) Allocation and apportionment of Vermont net income by corporations

Allocation and apportionment of Vermont net income by corporations") Reg. 1.5833 ALLOCATION AND APPORTIONMENT OF INCOME Reg. 1.5833-1 (Effective for tax years beginning on and after January 1, 1998) Allocation and apportionment of Vermont net income by corporations (a)

Reg. 1.5833 ALLOCATION AND APPORTIONMENT OF INCOME Reg. 1.5833-1 (Effective for tax years beginning on and after January 1, 1998) Allocation and apportionment of Vermont net income by corporations (a)

Exclusion of Gain on the Sale of a Principal Residence, Interest Deductions, Home Office Rules

Exclusion of Gain on the Sale of a Principal Residence, Interest Deductions, Home Office Rules 'Walter D. Schwidetzky Professor of Law University of Baltimore School of Law 1420 N. Charles St. Baltimore,

Exclusion of Gain on the Sale of a Principal Residence, Interest Deductions, Home Office Rules 'Walter D. Schwidetzky Professor of Law University of Baltimore School of Law 1420 N. Charles St. Baltimore,

Tax Reform in Texas: Was it the Perfect Storm? Karey Barton Principal

Tax Reform in Texas: Was it the Perfect Storm? Karey Barton Principal December 15, 2008 Agenda The background: What was the emphasis driving tax reform? How did the process work? The basics: Who is subject

Tax Reform in Texas: Was it the Perfect Storm? Karey Barton Principal December 15, 2008 Agenda The background: What was the emphasis driving tax reform? How did the process work? The basics: Who is subject

NAR Frequently Asked Questions Health Insurance Reform

NEW MEDICARE TAX ON UNEARNED NET INVESTMENT INCOME Q-1: Who will be subject to the new taxes imposed in the health legislation? A: A new 3.8% tax will apply to the unearned income of High Income taxpayers.

NEW MEDICARE TAX ON UNEARNED NET INVESTMENT INCOME Q-1: Who will be subject to the new taxes imposed in the health legislation? A: A new 3.8% tax will apply to the unearned income of High Income taxpayers.

Buy-Sell Agreements Funded With Life Insurance in brief

Buy-Sell Agreements Funded With Life Insurance in brief Buy-Sell Agreements Funded With Life Insurance Why enter into a Buy-Sell Agreement? Create a market for the owner s interest. Provide for mutually

Buy-Sell Agreements Funded With Life Insurance in brief Buy-Sell Agreements Funded With Life Insurance Why enter into a Buy-Sell Agreement? Create a market for the owner s interest. Provide for mutually

Texas - Franchise tax relief, R&D incentives, sales and use tax exemptions for telecommunication, internet providers

No. 2013-301 June 17, 2013 Texas - Franchise tax relief, R&D incentives, sales and use tax exemptions for telecommunication, internet providers June 17: Texas Governor Rick Perry on June 14 signed three

No. 2013-301 June 17, 2013 Texas - Franchise tax relief, R&D incentives, sales and use tax exemptions for telecommunication, internet providers June 17: Texas Governor Rick Perry on June 14 signed three

Proposed Washington Capital Gains Tax HB 1484/SB 5699. Frequently Asked Questions

Proposed Washington Capital Gains Tax HB 1484/SB 5699 Governor Inslee is proposing a capital gains tax on the sale of stocks, bonds and other assets to increase the share of state taxes paid by Washington

Proposed Washington Capital Gains Tax HB 1484/SB 5699 Governor Inslee is proposing a capital gains tax on the sale of stocks, bonds and other assets to increase the share of state taxes paid by Washington

TAX TREATY CHARACTERISATION ISSUES ARISING FROM E-COMMERCE

TAX AND COMMERCE @ OECD TAX TREATY CHARACTERISATION ISSUES ARISING FROM E-COMMERCE REPORT TO WORKING PARTY NO. 1 OF THE OECD COMMITTEE ON FISCAL AFFAIRS 1 February 2001 By the Technical Advisory Group

TAX AND COMMERCE @ OECD TAX TREATY CHARACTERISATION ISSUES ARISING FROM E-COMMERCE REPORT TO WORKING PARTY NO. 1 OF THE OECD COMMITTEE ON FISCAL AFFAIRS 1 February 2001 By the Technical Advisory Group

CASH FLOW STATEMENT & BALANCE SHEET GUIDE

CASH FLOW STATEMENT & BALANCE SHEET GUIDE The Agriculture Development Council requires the submission of a cash flow statement and balance sheet that provide annual financial projections for the business

CASH FLOW STATEMENT & BALANCE SHEET GUIDE The Agriculture Development Council requires the submission of a cash flow statement and balance sheet that provide annual financial projections for the business

Considerations in the Health Care Company Tax Status Conversion from C Corporation to Pass-Through Entity

Health Care Forensic Analysis Insights Considerations in the Health Care Company Tax Status Conversion from C Corporation to Pass-Through Entity Robert F. Reilly, CPA For a variety of economic and taxation

Health Care Forensic Analysis Insights Considerations in the Health Care Company Tax Status Conversion from C Corporation to Pass-Through Entity Robert F. Reilly, CPA For a variety of economic and taxation

FME SOFTWARE LICENSE AGREEMENT

FME SOFTWARE LICENSE AGREEMENT IMPORTANT READ CAREFULLY: This FME Software License Agreement ("Agreement") is a legal agreement between You (either an individual or a single legal entity) and Safe Software

FME SOFTWARE LICENSE AGREEMENT IMPORTANT READ CAREFULLY: This FME Software License Agreement ("Agreement") is a legal agreement between You (either an individual or a single legal entity) and Safe Software

Overview. Texas Tax Code Chapter 171. Teresa Bostick, Claire Jamal, Jerry Oxford, Martha Preston, Nat Robberson & Jennifer Specchio

Overview Texas Tax Code Chapter 171 Presented by: Organizer: Panelists: Franchise Tax Policy Staff Janet Spies Teresa Bostick, Claire Jamal, Jerry Oxford, Martha Preston, Nat Robberson & Jennifer Specchio

Overview Texas Tax Code Chapter 171 Presented by: Organizer: Panelists: Franchise Tax Policy Staff Janet Spies Teresa Bostick, Claire Jamal, Jerry Oxford, Martha Preston, Nat Robberson & Jennifer Specchio

Business Organization\Tax Structure

Business Organization\Tax Structure One of the first decisions a new business owner faces is choosing a structure for the business. Businesses range in size and complexity, from someone who is self-employed

Business Organization\Tax Structure One of the first decisions a new business owner faces is choosing a structure for the business. Businesses range in size and complexity, from someone who is self-employed

Internal Revenue Service

Internal Revenue Service Department of the Treasury Number: 200327029 Release Date: 7/3/2003 Index Number: 1362.02-03 Washington, DC 20224 Person to Contact: Telephone Number: Refer Reply To: CC:PSI:2

Internal Revenue Service Department of the Treasury Number: 200327029 Release Date: 7/3/2003 Index Number: 1362.02-03 Washington, DC 20224 Person to Contact: Telephone Number: Refer Reply To: CC:PSI:2

Choice of Entity: Corporation or Limited Liability Company?

March 2014 Choice of Entity: Corporation or Limited Liability Company? By Gianfranco A. Pietrafesa* Attorney at Law There are many different types of business entities, including corporations, general

March 2014 Choice of Entity: Corporation or Limited Liability Company? By Gianfranco A. Pietrafesa* Attorney at Law There are many different types of business entities, including corporations, general

STATE OF NEW YORK COMMISSIONER OF TAXATION AND FINANCE. Petitioner submitted the following facts as the basis for this Advisory Opinion.

New York State Department of Taxation and Finance Taxpayer Services Division Technical Services Bureau STATE OF NEW YORK COMMISSIONER OF TAXATION AND FINANCE ADVISORY OPINION PETITION NO. S990316A On March

New York State Department of Taxation and Finance Taxpayer Services Division Technical Services Bureau STATE OF NEW YORK COMMISSIONER OF TAXATION AND FINANCE ADVISORY OPINION PETITION NO. S990316A On March

Presents: The Solo 401(k) Plan The Ultimate Retirement Solution for the Self Employed January 2012

Plan The Ultimate Retirement Solution for the Self Employed January 2012") Presents: The Solo 401(k) Plan The Ultimate Retirement Solution for the Self Employed January 2012 Disclaimer: The information provided in this presentation/document is not legal advice, but general information

Presents: The Solo 401(k) Plan The Ultimate Retirement Solution for the Self Employed January 2012 Disclaimer: The information provided in this presentation/document is not legal advice, but general information

PENNSYLVANIA PERSONAL INCOME TAX GUIDE TABLE OF CONTENTS

CHAPTER 23: NATURAL RESOURCES TABLE OF CONTENTS I. FEDERAL INCOME TAX TREATMENT OF DEPLETION... 3 A. Depletion Overview... 3 B. Federal Statute... 3 C. Economic Interest... 4 D. Cost Depletion... 4 E.

CHAPTER 23: NATURAL RESOURCES TABLE OF CONTENTS I. FEDERAL INCOME TAX TREATMENT OF DEPLETION... 3 A. Depletion Overview... 3 B. Federal Statute... 3 C. Economic Interest... 4 D. Cost Depletion... 4 E.

Letter of Findings: 06-0349 Individual Income Tax For the Year 2004

DEPARTMENT OF STATE REVENUE Letter of Findings: 06-0349 Individual Income Tax For the Year 2004 01-20060349.LOF NOTICE: Under IC 4-22-7-7, this document is required to be published in the Indiana Register

DEPARTMENT OF STATE REVENUE Letter of Findings: 06-0349 Individual Income Tax For the Year 2004 01-20060349.LOF NOTICE: Under IC 4-22-7-7, this document is required to be published in the Indiana Register

------------------------, --------, Branch 5, Office of the Associate Chief Counsel (Passthroughs and Special Industries) CC:PSI:B5

CC:PSI:B5") Office of Chief Counsel Internal Revenue Service memorandum Number: 201313020 Release Date: 3/29/2013 CC:PSI:B5: POSTN-136312-11 Third Party Communication: None Date of Communication: Not Applicable UILC:

Office of Chief Counsel Internal Revenue Service memorandum Number: 201313020 Release Date: 3/29/2013 CC:PSI:B5: POSTN-136312-11 Third Party Communication: None Date of Communication: Not Applicable UILC:

Michigan Business Tax Frequently Asked Questions

NOTICE: The MBT was amended by 145 PA 2007 on December 1, 2007. Act 145 imposes an annual surcharge to taxpayers' MBT liability, as well as makes other changes. Some of the FAQs below have revised answers

NOTICE: The MBT was amended by 145 PA 2007 on December 1, 2007. Act 145 imposes an annual surcharge to taxpayers' MBT liability, as well as makes other changes. Some of the FAQs below have revised answers

IPSAS 2 CASH FLOW STATEMENTS

IPSAS 2 CASH FLOW STATEMENTS Acknowledgment This International Public Sector Accounting Standard (IPSAS) is drawn primarily from International Accounting Standard (IAS) 7, Cash Flow Statements published

IPSAS 2 CASH FLOW STATEMENTS Acknowledgment This International Public Sector Accounting Standard (IPSAS) is drawn primarily from International Accounting Standard (IAS) 7, Cash Flow Statements published

International Accounting Standard 38 Intangible Assets

EC staff consolidated version as of 24 March 2010 FOR INFORMATION PURPOSES ONLY International Accounting Standard 38 Intangible Assets Objective 1 The objective of this Standard is to prescribe the accounting

EC staff consolidated version as of 24 March 2010 FOR INFORMATION PURPOSES ONLY International Accounting Standard 38 Intangible Assets Objective 1 The objective of this Standard is to prescribe the accounting

Coming to America. U.S. Tax Planning for Foreign-Owned U.S. Operations

Coming to America U.S. Tax Planning for Foreign-Owned U.S. Operations September 2015 Table of Contents Introduction... 2 Tax Checklist for Foreign-Owned U.S. Operations... 2 Typical Life Cycle of Foreign-Owned

Coming to America U.S. Tax Planning for Foreign-Owned U.S. Operations September 2015 Table of Contents Introduction... 2 Tax Checklist for Foreign-Owned U.S. Operations... 2 Typical Life Cycle of Foreign-Owned

MTC APPORTIONMENT AND ALLOCATION RULES FOR FINANCIAL INSTITUTIONS

MTC APPORTIONMENT AND ALLOCATION RULES FOR FINANCIAL INSTITUTIONS On the July 8, 2008 definitions working group conference call, states were asked to submit written comments outlining the issues that each

MTC APPORTIONMENT AND ALLOCATION RULES FOR FINANCIAL INSTITUTIONS On the July 8, 2008 definitions working group conference call, states were asked to submit written comments outlining the issues that each

DETERMINING THE BUSINESS ENTITY BEST FOR YOUR BUSINESS

DETERMINING THE BUSINESS ENTITY BEST FOR YOUR BUSINESS 2015 Keith J. Kanouse One Boca Place, Suite 324 Atrium 2255 Glades Road Boca Raton, Florida 33431 Telephone: (561) 451-8090 Fax: (561) 451-8089 E-mail:

DETERMINING THE BUSINESS ENTITY BEST FOR YOUR BUSINESS 2015 Keith J. Kanouse One Boca Place, Suite 324 Atrium 2255 Glades Road Boca Raton, Florida 33431 Telephone: (561) 451-8090 Fax: (561) 451-8089 E-mail:

Nevada enacts Commerce Tax effective July 1, 2015

from State and Local Tax Services Nevada enacts Commerce Tax effective July 1, 2015 June 10, 2015 In brief Signed on June 10, 2015, and effective July 1, 2015, S.B. 483 imposes an annual commerce tax on

from State and Local Tax Services Nevada enacts Commerce Tax effective July 1, 2015 June 10, 2015 In brief Signed on June 10, 2015, and effective July 1, 2015, S.B. 483 imposes an annual commerce tax on

Financial Statements

Financial Statements The financial information forms the basis of financial planning, analysis & decision making for an organization or an individual. Financial information is needed to predict, compare

Financial Statements The financial information forms the basis of financial planning, analysis & decision making for an organization or an individual. Financial information is needed to predict, compare

IRS Issues Reliance Proposed Regulations On Some Net Investment Income Tax Issues. Background

/////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////// Special Report Series on Section 1411

/////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////////// Special Report Series on Section 1411

At your request, we have examined three alternative plans for restructuring Gapple s

MEMORANDUM TO: Senior Partner FROM: LL.M. Team Number DATE: November 18, 2011 SUBJECT: 2011 Law Student Tax Challenge Problem At your request, we have examined three alternative plans for restructuring

MEMORANDUM TO: Senior Partner FROM: LL.M. Team Number DATE: November 18, 2011 SUBJECT: 2011 Law Student Tax Challenge Problem At your request, we have examined three alternative plans for restructuring

2015 NEVADA TAX REFORMS. Commerce Tax, Modified Business Tax, Business License Fee

Joshua J. Hicks Attorney at Law 775.622.9450 tel 775.622.9554 fax [email protected] 2015 NEVADA TAX REFORMS Commerce Tax, Modified Business Tax, Business License Fee Current as of June 10, 2015 A. Commerce

Joshua J. Hicks Attorney at Law 775.622.9450 tel 775.622.9554 fax [email protected] 2015 NEVADA TAX REFORMS Commerce Tax, Modified Business Tax, Business License Fee Current as of June 10, 2015 A. Commerce

International Accounting Standard 38 Intangible Assets. Objective. Scope IAS 38

International Accounting Standard 38 Intangible Assets Objective 1 The objective of this Standard is to prescribe the accounting treatment for intangible assets that are not dealt with specifically in

International Accounting Standard 38 Intangible Assets Objective 1 The objective of this Standard is to prescribe the accounting treatment for intangible assets that are not dealt with specifically in

Revenue. Compiled AASB Standard AASB 118

Compiled AASB Standard AASB 118 Revenue This compiled Standard applies to annual reporting periods beginning on or after 1 January 2011 but before 1 January 2013. Early application is permitted. It incorporates

Compiled AASB Standard AASB 118 Revenue This compiled Standard applies to annual reporting periods beginning on or after 1 January 2011 but before 1 January 2013. Early application is permitted. It incorporates

Tax Considerations Of Foreign

FIRPTA requires that a buyer withhold 10% of the gross sales price, subject to certain exceptions, and send it to the Internal Revenue Service if the seller is a foreign person. U.S. Taxes Foreign investors

FIRPTA requires that a buyer withhold 10% of the gross sales price, subject to certain exceptions, and send it to the Internal Revenue Service if the seller is a foreign person. U.S. Taxes Foreign investors

Instructions for Schedule D (Form 1065)

") 2014 Instructions for Schedule D (Form 1065) Capital Gains and Losses Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise noted. Future

2014 Instructions for Schedule D (Form 1065) Capital Gains and Losses Department of the Treasury Internal Revenue Service Section references are to the Internal Revenue Code unless otherwise noted. Future

SC REVENUE RULING #97-15. Public Law 86-272 and South Carolina Income Tax. EFFECTIVE DATE: Applies to all periods open under the statute.

State of South Carolina Department of Revenue 301 Gervais Street, P. O. Box 125, Columbia, South Carolina 29214 SC REVENUE RULING #97-15 SUBJECT: Public Law 86-272 and South Carolina Income Tax EFFECTIVE

State of South Carolina Department of Revenue 301 Gervais Street, P. O. Box 125, Columbia, South Carolina 29214 SC REVENUE RULING #97-15 SUBJECT: Public Law 86-272 and South Carolina Income Tax EFFECTIVE

Different Types of Corporations: Advantages/ Disadvantages of Corporations

Different Types of Corporations: Advantages/ Disadvantages of Corporations Article published at: http://www.morebusiness.com/getting_started/incorporating/d934832501.brc Anyone who operates a business,

Different Types of Corporations: Advantages/ Disadvantages of Corporations Article published at: http://www.morebusiness.com/getting_started/incorporating/d934832501.brc Anyone who operates a business,

The Lifetime Capital Gains Exemption

The Lifetime Capital Gains Exemption Introduction This Tax Topic briefly reviews the rules contained in section 110.6 of the Income Tax Act (the "Act") concerning the lifetime capital gains exemption and

The Lifetime Capital Gains Exemption Introduction This Tax Topic briefly reviews the rules contained in section 110.6 of the Income Tax Act (the "Act") concerning the lifetime capital gains exemption and

Module 10 S Corporation/Corporation Workbook Introduction

Module 10 Workbook Introduction Running your own business presents many challenges. One of the most difficult is complying with complex and ever-changing tax laws. This small-business tax education program

Module 10 Workbook Introduction Running your own business presents many challenges. One of the most difficult is complying with complex and ever-changing tax laws. This small-business tax education program

(1) Purpose; General Rule; Relationship to Other Rules; Outline.

Purpose; General Rule; Relationship to Other Rules; Outline.") 830 CMR: DEPARTMENT OF REVENUE 830 CMR 63.00: TAXATION OF CORPORATIONS 830 CMR 63.32B.2: Combined Reporting (1) Purpose; General Rule; Relationship to Other Rules; Outline. (a) Purpose. The purpose of

830 CMR: DEPARTMENT OF REVENUE 830 CMR 63.00: TAXATION OF CORPORATIONS 830 CMR 63.32B.2: Combined Reporting (1) Purpose; General Rule; Relationship to Other Rules; Outline. (a) Purpose. The purpose of

Instructions for Form 1116

2014 Instructions for Form 1116 Foreign Tax Credit (Individual, Estate, or Trust) Section references are to the Internal Revenue Code unless otherwise noted. Future Developments For the latest information

2014 Instructions for Form 1116 Foreign Tax Credit (Individual, Estate, or Trust) Section references are to the Internal Revenue Code unless otherwise noted. Future Developments For the latest information

U.S. Corporation Income Tax Return For calendar year 2015 or tax year beginning, 2015, ending, 20

Form 1120 Department of the Treasury Internal Revenue Service A Check if: 1a Consolidated return (attach Form 851). b Life/nonlife consolidated return... 2 Personal holding co. (attach Sch. PH).. 3 Personal

Form 1120 Department of the Treasury Internal Revenue Service A Check if: 1a Consolidated return (attach Form 851). b Life/nonlife consolidated return... 2 Personal holding co. (attach Sch. PH).. 3 Personal

STATE OF ARIZONA Department of Revenue

STATE OF ARIZONA Department of Revenue Janice K. Brewer Governor PRIVATE TAXPAYER RULING LR13-002 John A. Greene Director The Department issues this private taxpayer ruling in response to your letters

STATE OF ARIZONA Department of Revenue Janice K. Brewer Governor PRIVATE TAXPAYER RULING LR13-002 John A. Greene Director The Department issues this private taxpayer ruling in response to your letters

Appendix to the Questionnaire on Initial accounting for intangible assets acquired in Business Combinations

Appendix to the Questionnaire on Initial accounting for intangible assets acquired in Business Combinations In January 2008, the IASB completed the second phase of its Business Combinations project. As

Appendix to the Questionnaire on Initial accounting for intangible assets acquired in Business Combinations In January 2008, the IASB completed the second phase of its Business Combinations project. As

ENGROSSED HOUSE By: Deutschendorf of the House. ( revenue and taxation amending 68 O.S., Section. 1352 definitions - Sales Tax Code effective

ENGROSSED HOUSE BILL NO. 2736 By: Deutschendorf of the House and Robinson of the Senate ( revenue and taxation amending 68 O.S., Section 1352 definitions - Sales Tax Code effective date emergency ) BE

ENGROSSED HOUSE BILL NO. 2736 By: Deutschendorf of the House and Robinson of the Senate ( revenue and taxation amending 68 O.S., Section 1352 definitions - Sales Tax Code effective date emergency ) BE

INCORPORATING YOUR BUSINESS IS POTENTIALLY THE SINGLE MOST IMPORTANT THING A BUSINESS OWNER CAN DO

INCORPORATING YOUR BUSINESS IS POTENTIALLY THE SINGLE MOST IMPORTANT THING A BUSINESS OWNER CAN DO Mark D. Klein, Esq. KLEIN LAW CORPORATION 15615 Alton Parkway, Suite 175 Irvine, CA 92618 (949) 453-7979

INCORPORATING YOUR BUSINESS IS POTENTIALLY THE SINGLE MOST IMPORTANT THING A BUSINESS OWNER CAN DO Mark D. Klein, Esq. KLEIN LAW CORPORATION 15615 Alton Parkway, Suite 175 Irvine, CA 92618 (949) 453-7979

U.S.A. Chapter I. Scope of the Convention

U.S.A. Convention between the Kingdom of the Netherlands and the United States of America for the avoidance of double taxation and the prevention of fiscal evasion with respect to taxes on income Done

U.S.A. Convention between the Kingdom of the Netherlands and the United States of America for the avoidance of double taxation and the prevention of fiscal evasion with respect to taxes on income Done

TENNESSEE DEPARTMENT OF REVENUE REVENUE RULING #98-47

TENNESSEE DEPARTMENT OF REVENUE REVENUE RULING #98-47 WARNING Revenue rulings are not binding on the Department. This presentation of the ruling in a redacted form is information only. Rulings are made

TENNESSEE DEPARTMENT OF REVENUE REVENUE RULING #98-47 WARNING Revenue rulings are not binding on the Department. This presentation of the ruling in a redacted form is information only. Rulings are made

United States Corporate Income Tax Summary

United States Corporate Income Tax Summary SECTION 1: AT A GLANCE CliftonLarsonAllen LLP 222 Main Street, PO Box 1347 Racine, WI 53401 262-637-9351 fax 262-637-0734 www.cliftonlarsonallen.com Corporate

United States Corporate Income Tax Summary SECTION 1: AT A GLANCE CliftonLarsonAllen LLP 222 Main Street, PO Box 1347 Racine, WI 53401 262-637-9351 fax 262-637-0734 www.cliftonlarsonallen.com Corporate

Guide to Japanese Taxes

Guide to Japanese Taxes CONTENTS 1. Introduction --------------------------------------------------------------------------------------------- 1 (1) Principle of Taxation under the Law (2) Self-Assessment

Guide to Japanese Taxes CONTENTS 1. Introduction --------------------------------------------------------------------------------------------- 1 (1) Principle of Taxation under the Law (2) Self-Assessment