Mortgage Financing and Liability Allocation

|

|

|

- Nicholas Bradley

- 10 years ago

- Views:

Transcription

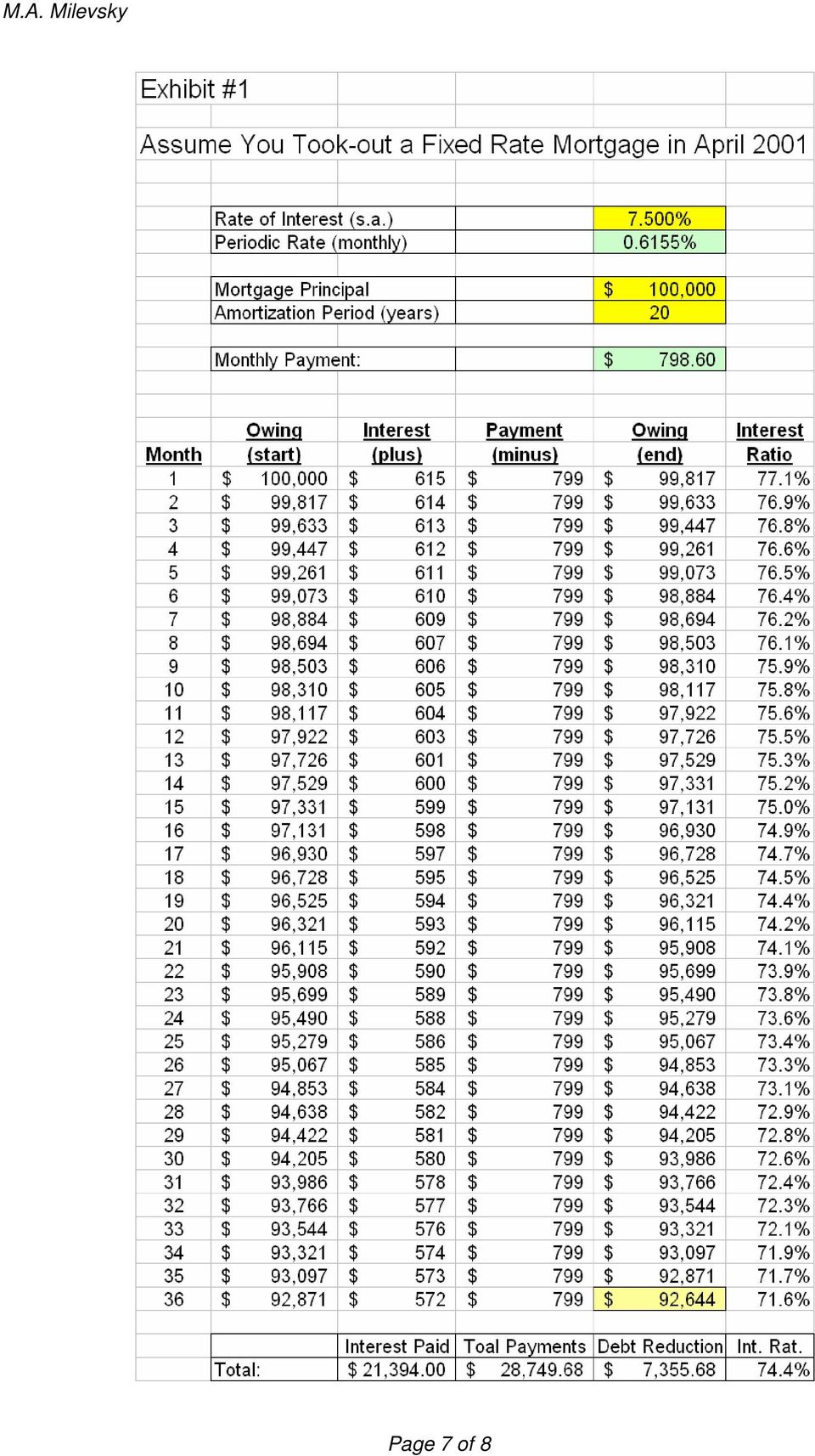

1 Mortgage Financing and Liability Allocation M.A. Milevsky June 2004 In late March 2001 I wrote a widely cited report entitled: Mortgage Financing: Floating Your Way to Prosperity 1 in which I argued that Canadian consumers were better-off financing their mortgage at a floating or variable rate of interest compared to the traditional choice of a 5-year fixed rate. With more than three years since that report, and thousands of Canadians who have since taken variable rate mortgages, it seems this was a good call. But with the Bank of Canada poised to raise rates in the near future it is time to revisit the ideas behind variable rate mortgages and how they can be applied to your client. More importantly, I will take this opportunity to introduce the concept of liability allocation which is the symmetric counter-part to asset allocation on your client s personal financial balance sheet. First, some historical background. In March 2001, the quoted annual percentage rate on a typical variable rate mortgage (VRM) was 6.5% which was also the prime rate of interest at the end of March the average 5-year fixed rate was 7.5% This modest spread of 100 basis points represented an immediate monthly saving of $60 per month on a $100,000 loan that was amortized over 20 years for those who selected the floating route. And, while this number might not have seemed very meaningful at the time, as variable rates dropped from 6.5% to the current neighborhood of 3.5 to 4.0%, the difference compounded to quite a substantial sum. 1 The original report was funded by a research grant from Manulife Financial and is currently available on the website of The IFID Centre at The report was also summarized in a short article entitled Go with the float: Fixed rate mortgages offer piece of mind, but not much else in the April 2001 issue of the National Post Magazine (page 41). Page 1 of 8

2 Exhibit #1 and #2 display the savings from having followed this advice during the last three years. It assumes two hypothetical clients, Linda Long and Shelly Short who each borrowed $100,000 in early April 2001 to finance the purchase of house. Linda fixed her mortgage at the 5-year 7.5% rate, which led to monthly payments of $799. Shelly borrowed at the floating rate which was 6.5% at the time, but decided to make monthly payments of $799, identical to Linda s. Note that Shelly s interest clock was ticking at the variable (prime rate), so as rates fell from 6.5% to the current 4.0% her debt was declining and being paid back at a faster rate compared to Linda s. In fact, at the end of 3 years i.e. in early April 2004 the principal outstanding on Linda s mortgage was $92,644 compared to Shelly s $84,424, even though they both made the exact same monthly mortgage payments! Note that Shelly paid a total $13,173 in interest payments during the last three years, which is $8,221 or 40% less than Linda s $21,394 in interest payments. They both paid a total of $28,749 but the split between interest and principal was different. And, if they borrowed $200,000 or $400,000 at a variable rate in April 2001, they saved 2 to 4 times $8,221 between then and the early summer of Furthermore, if Shelly selected the VRM and left this mortgage open, she gained the additional benefit of being able to pay down her mortgage with extra cash at anytime, without penalty. This particular feature is hard to quantify, but extremely valuable over the long-run. Even if your client did not follow Shelly s precise strategy of making artificially higher mortgage payments, and instead made payments based on the fluctuating variable rate applicable for that month, the effective present value of her savings was $8,221 per $100,000 of mortgage principal. In addition, if she were able to negotiate a loan at prime minus 75 basis points which was not uncommon for those who closed their floating mortgage over the term I estimate the current outstanding balance is approximately $82,000 and the savings from floating was closer to $10,000. Without a doubt, anyone who took Shelly s lead during the last three years gained handsomely. Page 2 of 8

, so as rates fell from 6.5% to the current 4.")

3 Against this backdrop, most financial commentators have interpreted recent remarks by the Bank of Canada to imply that we have reached the bottom of the interest rate cycle and the next inevitable move will be up. Quite likely a number of your clients have asked YOU whether it is now time to lock in a mortgage, since it is estimated that over 30% of Canadian have VRMs. And while you might feel that your mandate lies on the asset and not liability side of their balance sheet, I believe this is a great opportunity to implement total asset allocation with your client and provide some guidance and valuable education on prudent debt management. First, a common mistake made by many mortgage borrowers although not necessarily the avid readers of the financial press is that there is only one interest rate to be considered, one which goes either up or down based on the Bank of Canada s actions. This is not true. In fact, quite distinct from the price of gold or the USD exchange rate, there is an entire collection of different interest rates (called a yield curve) which can move in very different directions on any given day. For example, on Monday short-term (money market, T.Bill) rates can decline while long-term bond yields can increase and vice versa on Tuesday. These rates correspond to different terms on a loan. If they borrow money for one year they might pay 3% per year, but if they borrow for 10 years it will be 6%. Lenders prefer to issue loans that are re-negotiated over shorter periods of time, while borrowers favor extended commitments. Thus, in order to induce these reluctant lenders to give-up their precious funds for longer, the interest rates (or rent) on longerterm loans is usually higher, to compensate for the longer lock-up. Ergo, borrowers who are willing to accommodate the lender s natural desire to keep the money on a short leash, and who agree to shorter term loans, will gain a financial edge in the long-run. I believe this to be true, even in today s low interest rate and low inflation rate environment, since I would expect lenders are even more reluctant to make longer term (nominal, i.e. non-inflation adjusted) commitments. But like all things financial, risk and return are inseparable partners. Page 3 of 8

4 Therefore, advocating a variable rate mortgage is not predicated by, or based on, a speculative (bearish) bet on interest rates. Indeed, going forward, I don t know whether the prime rate of interest will stay at it s current levels for the next 3 6 months, in which case you certainly don t lose from floating your mortgage, or if it will decline further (unlikely, but even better) or if it will only start to increase in 6 to 12 months. Rather, the point is as that when contemplating a mortgage strategy, your client should examine the range of possible payments likely computed and displayed by you, their financial advisor -- and they should decide whether they can live with the risk. Questions you should be asking them are. Can they afford to pay $200 to $300 more per month in a worse case scenario? Is there enough slack in their monthly budget to cut-out discretionary expenses and make up the shortfall? Do they perhaps have other investments that might increase in value if interest rate increase? The decision of whether to long (fixed) or short (floating) should depend on their tolerance for risk the same concept used in traditional asset allocation -- and their ability to withstand increases in mortgage payments. I believe that they can still expect a financial reward for going with the float, although the precise magnitude will ebb and flow depending on the economic environment. Remember, you and they are not smarter than the billion dollar bond market. Ok. So, where does this leave your client who seeks practical advice and is asking you what to do? Well, this depends on the type of homeowner they are. I see four distinct financial personalities, each of which should being doing something slightly different. 1. The first-time homebuyer and especially those who placed minimal initial down payments with high leverage ratios, are the ideal candidates for long-term fixed rate mortgages. People in this category should not be taking any chances with a fluctuating interest rate. In fact, they might be hit with a double whammy if the value of their (overpriced) house declines leaving them with negative equity. To them you should say, count your blessing, don t be greedy and lock-in a fixed rate. Page 4 of 8

5 2. The risk-averse worrywart who is constantly looking at interest rates and wondering if now is the time, should do what all risk-averse investors do: diversify. Indeed, there is a strong argument to be made for diversifying your mortgage debt, similar to the prudent strategy with your investment portfolio. Now, in general diversifying your debts is a silly idea since you should put all your eggs in the one basket with the lowest interest rate. I am willing to concede that split rate mortgages have some merit in today s ultra-low environment. This is true debt allocation and the ideal strategy is to partition the mortgage in two parts, one linked to a variable rate and the other closed for a longer period of time. The exact ratio should depend on cash-flow assessment and the odds on whether your client will have any cash sitting in your bank account that can be used to pay down your mortgage. 3. The seasoned veteran, possibly with two stable breadwinners in the family and with a substantial amount of built-up equity in the house should still follow Shelly Short s strategy. They can afford the risk and continue with a variable rate mortgage, making payments based on a high fixed rate schedule. This is an easy way to (think you) have your cake and eat it too. From a purely psychological point of view -- as long as they pick the payment rate to be 2% to 3% above the initial floating rate -- if and when interest rates do (finally) start to increase, it should have no noticeable impact on the monthly budget. 4. The financially savvy arbitrageur can do even better. Most banks allow you to pre-approve a fixed rate mortgage for between 90 and 120 days. They are guaranteed the pre-approved rate regardless of what happens to mortgage rates over the next 3-4 months. This is the closest thing to a free lunch (actually, call option on interest rates) you will ever get from a Canadian bank. If they have a floating (open) rate mortgage that allows them to pre-pay any amount anytime without penalty, then encourage them to walk across the street to their bank s competitor and ask for a pre-approval on a 5-year fixed rate mortgage. Then, keep a close eye on the Bank of Canada and the bond market. If rates increase tomorrow, they should exercise their free option and move your mortgage across the street, at yesterday s rate. Otherwise, they should do nothing and start the Page 5 of 8

6 process over in a few months. Understandably, the branch manager might get a bit weary Ah yes, one last thing for the record. I currently have an (open) variable rate mortgage, and I have absolutely no intention of locking-in, at least for now.but, I ll keep you updated Page 6 of 8

variable rate mortgage, and I have")

7 Page 7 of 8

8 Page 8 of 8

First Timer s Guide PREParing First Time Homebuyers

First Timer s Guide PREParing First Time Homebuyers SO MANY QUESTIONS Maybe you live in the best apartment with a great landlord and don t want to change a thing. Or maybe you ve looked at the rent going

First Timer s Guide PREParing First Time Homebuyers SO MANY QUESTIONS Maybe you live in the best apartment with a great landlord and don t want to change a thing. Or maybe you ve looked at the rent going

The Ultimate Mortgage Checklist

The Ultimate Mortgage Checklist The Rate 1. Is the rate you re quoting me the lowest I can possibly get, given my qualifications and mortgage preferences? 2. If I find a lower rate for a similar product

The Ultimate Mortgage Checklist The Rate 1. Is the rate you re quoting me the lowest I can possibly get, given my qualifications and mortgage preferences? 2. If I find a lower rate for a similar product

Accounting for securitizations treated as a financing (on-balance sheet) verses securitizations treated as a sale (off-balance sheet)

verses securitizations treated as a sale (off-balance sheet)") Accounting for securitizations treated as a financing (on-balance sheet) verses securitizations treated as a sale (off-balance sheet) The hypothetical example below is provided for informational purposes

Accounting for securitizations treated as a financing (on-balance sheet) verses securitizations treated as a sale (off-balance sheet) The hypothetical example below is provided for informational purposes

Managing your surplus cash

Managing your surplus cash Savings and investments BusinESS Coach series Establishing a plan Putting your plan to work Thinking long term Business Coach series Your money should work as hard as you do

Managing your surplus cash Savings and investments BusinESS Coach series Establishing a plan Putting your plan to work Thinking long term Business Coach series Your money should work as hard as you do

Your Assets: Financing and Refinancing Properties

The Business Library Resource Report #35 Your Assets: Financing and Refinancing Properties Personal, Investment, and Business Properties! Basic Analysis of How and When! Fixed vs. Variable Interest Rate!

The Business Library Resource Report #35 Your Assets: Financing and Refinancing Properties Personal, Investment, and Business Properties! Basic Analysis of How and When! Fixed vs. Variable Interest Rate!

Homeownership. Your First Steps toward. Getting Started. Know Your Finances. Which Mortgage Is Right for You?

Your First Steps toward Homeownership Identify the type of mortgage that meets your specific financial needs Getting Started Many people don t consider buying a home because they re afraid they can t afford

Your First Steps toward Homeownership Identify the type of mortgage that meets your specific financial needs Getting Started Many people don t consider buying a home because they re afraid they can t afford

Determining your investment mix.

Determining your investment mix. Ten minutes from now, you could know your investment mix: And if your goal is to choose investment options that you can be comfortable with, this is an important step.

Determining your investment mix. Ten minutes from now, you could know your investment mix: And if your goal is to choose investment options that you can be comfortable with, this is an important step.

A Case for Variable Rate Mortgages ( P. d. Last Fall's Policy Changes: A Sound Program for Reducing Inflation < P. 5) Winter 1979

Winter 1979") Federal Reserve Bank of Minneapolis Q u a r t e r l y R e v i e w Winter 1979 A Case for Variable Rate Mortgages ( P. d Last Fall's Policy Changes: A Sound Program for Reducing Inflation < P. 5) District

Federal Reserve Bank of Minneapolis Q u a r t e r l y R e v i e w Winter 1979 A Case for Variable Rate Mortgages ( P. d Last Fall's Policy Changes: A Sound Program for Reducing Inflation < P. 5) District

Part 10. Small Business Finance and IPOs

Part 10. Small Business Finance and IPOs In the last section, we looked at how large corporations raised money. In this section, we will examine some of the financing issues facing small and start-up businesses.

Part 10. Small Business Finance and IPOs In the last section, we looked at how large corporations raised money. In this section, we will examine some of the financing issues facing small and start-up businesses.

22Most Common. Mistakes You Must Avoid When Investing in Stocks! FREE e-book

22Most Common Mistakes You Must Avoid When Investing in s Keep the cost of your learning curve down Respect fundamental principles of successful investors. You Must Avoid When Investing in s Mistake No.

22Most Common Mistakes You Must Avoid When Investing in s Keep the cost of your learning curve down Respect fundamental principles of successful investors. You Must Avoid When Investing in s Mistake No.

Determining your investment mix

Determining your investment mix Ten minutes from now, you could know your investment mix. And if your goal is to choose investment options that you can be comfortable with, this is an important step. The

Determining your investment mix Ten minutes from now, you could know your investment mix. And if your goal is to choose investment options that you can be comfortable with, this is an important step. The

Understanding Investment Leverage

Understanding Investment Leverage Understanding Investment Leverage What is investment leverage? Each year, more and more Canadians are taking advantage of a simple yet powerful wealthcreation strategy

Understanding Investment Leverage Understanding Investment Leverage What is investment leverage? Each year, more and more Canadians are taking advantage of a simple yet powerful wealthcreation strategy

How To Calculate Financial Leverage Ratio

What Do Short-Term Liquidity Ratios Measure? What Is Working Capital? HOCK international - 2004 1 HOCK international - 2004 2 How Is the Current Ratio Calculated? How Is the Quick Ratio Calculated? HOCK

What Do Short-Term Liquidity Ratios Measure? What Is Working Capital? HOCK international - 2004 1 HOCK international - 2004 2 How Is the Current Ratio Calculated? How Is the Quick Ratio Calculated? HOCK

INSURANCE. Life Insurance. as an. Asset Class

INSURANCE Life Insurance as an Asset Class 16 FORUM JUNE / JULY 2013 Permanent life insurance has always been an exceptional estate planning tool, but as Wayne Miller and Sally Murdock report, it has additional

INSURANCE Life Insurance as an Asset Class 16 FORUM JUNE / JULY 2013 Permanent life insurance has always been an exceptional estate planning tool, but as Wayne Miller and Sally Murdock report, it has additional

There are two types of returns that an investor can expect to earn from an investment.

Benefits of investing in the Stock Market There are many benefits to investing in shares and we will explore how this common form of investment can be an effective way to make money. We will discuss some

Benefits of investing in the Stock Market There are many benefits to investing in shares and we will explore how this common form of investment can be an effective way to make money. We will discuss some

Mezzanine Finance. by Corry Silbernagel Davis Vaitkunas Bond Capital. With a supplement by Ian Giddy

Mezzanine Finance by Corry Silbernagel Davis Vaitkunas Bond Capital With a supplement by Ian Giddy Mezzanine Debt--Another Level To Consider Mezzanine debt is used by companies that are cash flow positive

Mezzanine Finance by Corry Silbernagel Davis Vaitkunas Bond Capital With a supplement by Ian Giddy Mezzanine Debt--Another Level To Consider Mezzanine debt is used by companies that are cash flow positive

ISAs GUIDE. An introduction to Individual Savings Accounts

ISAs GUIDE 2015 An introduction to Individual Savings Accounts ISAs GUIDE 2015 Introduction Most people s experience of saving starts in childhood. Your parents encourage you to save up a few pennies,

ISAs GUIDE 2015 An introduction to Individual Savings Accounts ISAs GUIDE 2015 Introduction Most people s experience of saving starts in childhood. Your parents encourage you to save up a few pennies,

Standard Life Active Retirement For accessing your pension money

Standard Life Active Retirement For accessing your pension money Standard Life Active Retirement our ready-made investment solution that allows you to access your pension savings while still giving your

Standard Life Active Retirement For accessing your pension money Standard Life Active Retirement our ready-made investment solution that allows you to access your pension savings while still giving your

Understanding Fixed Income

Understanding Fixed Income 2014 AMP Capital Investors Limited ABN 59 001 777 591 AFSL 232497 Understanding Fixed Income About fixed income at AMP Capital Our global presence helps us deliver outstanding

Understanding Fixed Income 2014 AMP Capital Investors Limited ABN 59 001 777 591 AFSL 232497 Understanding Fixed Income About fixed income at AMP Capital Our global presence helps us deliver outstanding

Guide for Homebuyers

Guide for Homebuyers Tips for Getting a Safe Mortgage You Can Afford Q u i c k S u m m a ry Figure out what you can afford. Contact at least 3 different lenders or brokers. When you call, say: I m buying

Guide for Homebuyers Tips for Getting a Safe Mortgage You Can Afford Q u i c k S u m m a ry Figure out what you can afford. Contact at least 3 different lenders or brokers. When you call, say: I m buying

CHG Companies, Inc. Employee 401(k) Plan

Plan") CHG Companies, Inc. Employee 401(k) Plan There are many great benefits to being part of the CHG Companies, Inc. Employee 401(k) Plan. Among those benefits is exceptional customer service online, by phone,

CHG Companies, Inc. Employee 401(k) Plan There are many great benefits to being part of the CHG Companies, Inc. Employee 401(k) Plan. Among those benefits is exceptional customer service online, by phone,

How should I invest my Pension/Investment money? Thank you to AXA Wealth for their contribution to this guide.

How should I invest my Pension/Investment money? Thank you to AXA Wealth for their contribution to this guide. www.increaseyourpension.co.uk Welcome to making investing simple Investing doesn t have to

How should I invest my Pension/Investment money? Thank you to AXA Wealth for their contribution to this guide. www.increaseyourpension.co.uk Welcome to making investing simple Investing doesn t have to

Managing Home Equity to Build Wealth By Ray Meadows CPA, CFA, MBA

Managing Home Equity to Build Wealth By Ray Meadows CPA, CFA, MBA About the Author Ray Meadows is the president of Berkeley Investment Advisors, a real estate brokerage and investment advisory firm. He

Managing Home Equity to Build Wealth By Ray Meadows CPA, CFA, MBA About the Author Ray Meadows is the president of Berkeley Investment Advisors, a real estate brokerage and investment advisory firm. He

A GUIDE TO MUTUAL FUND INVESTING

Many investors turn to mutual funds to meet their long-term financial goals. They offer the benefits of diversification and professional management and are seen as an easy and efficient way to invest.

Many investors turn to mutual funds to meet their long-term financial goals. They offer the benefits of diversification and professional management and are seen as an easy and efficient way to invest.

Is now a good time to refinance?

Is now a good time to refinance? Our Business Is The American Dream At Fannie Mae, we are in the American Dream business. Our Mission is to tear down barriers, lower costs, and increase the opportunities

Is now a good time to refinance? Our Business Is The American Dream At Fannie Mae, we are in the American Dream business. Our Mission is to tear down barriers, lower costs, and increase the opportunities

Asset allocation A key component of a successful investment strategy

Asset allocation A key component of a successful investment strategy This guide has been produced for educational purposes only and should not be regarded as a substitute for investment advice. Vanguard

Asset allocation A key component of a successful investment strategy This guide has been produced for educational purposes only and should not be regarded as a substitute for investment advice. Vanguard

Westpac. Home Loans. Enjoy a place of your own with your. Westpac. Home Loan

Westpac Home Loans Enjoy a place of your own with your Westpac Home Loan We know you d rather talk about your new home than a new home loan. After all, buying a home is an exciting journey. But we d like

Westpac Home Loans Enjoy a place of your own with your Westpac Home Loan We know you d rather talk about your new home than a new home loan. After all, buying a home is an exciting journey. But we d like

Advantages and disadvantages of investing in the Stock Market

Advantages and disadvantages of investing in the Stock Market There are many benefits to investing in shares and we will explore how this common form of investment can be an effective way to make money.

Advantages and disadvantages of investing in the Stock Market There are many benefits to investing in shares and we will explore how this common form of investment can be an effective way to make money.

January 2008. Bonds. An introduction to bond basics

January 2008 Bonds An introduction to bond basics The information contained in this publication is for general information purposes only and is not intended by the Investment Industry Association of Canada

January 2008 Bonds An introduction to bond basics The information contained in this publication is for general information purposes only and is not intended by the Investment Industry Association of Canada

Renewing and Renegotiating Your Mortgage

ABCs of Mortgages Series Renewing and Renegotiating Your Mortgage Smart mortgage decisions start here Table of Contents Overview 1 The renewal process 2 Renegotiating your mortgage agreement: breaking

ABCs of Mortgages Series Renewing and Renegotiating Your Mortgage Smart mortgage decisions start here Table of Contents Overview 1 The renewal process 2 Renegotiating your mortgage agreement: breaking

Renewing and Renegotiating Your Mortgage

ABCs of Mortgages Series Renewing and Renegotiating Your Mortgage Smart mortgage decisions start here table of contents overview 1 the renewal process 2 renegotiating your mortgage agreement: breaking

ABCs of Mortgages Series Renewing and Renegotiating Your Mortgage Smart mortgage decisions start here table of contents overview 1 the renewal process 2 renegotiating your mortgage agreement: breaking

A mortgage is a loan that is used to finance the purchase of your home. It consists of 5 parts: collateral, principal, interest, taxes, and insurance.

A mortgage is a loan that is used to finance the purchase of your home. It consists of 5 parts: collateral, principal, interest, taxes, and insurance. When you agree to a mortgage, you enter into a legal

A mortgage is a loan that is used to finance the purchase of your home. It consists of 5 parts: collateral, principal, interest, taxes, and insurance. When you agree to a mortgage, you enter into a legal

PNC is a registered mark of The PNC Financial Services Group, Inc.( PNC ) 2013 The PNC Financial Services Group, Inc. All rights reserved.

2013 The PNC Financial Services Group, Inc. All rights reserved.") The seminar and/or webinar and materials that you will view were prepared for general information purposes only by Baker Tilly and are not intended as legal, tax or accounting advice or as recommendations

The seminar and/or webinar and materials that you will view were prepared for general information purposes only by Baker Tilly and are not intended as legal, tax or accounting advice or as recommendations

Answers to Review Questions

Answers to Review Questions 1. The real rate of interest is the rate that creates an equilibrium between the supply of savings and demand for investment funds. The nominal rate of interest is the actual

Answers to Review Questions 1. The real rate of interest is the rate that creates an equilibrium between the supply of savings and demand for investment funds. The nominal rate of interest is the actual

Buying Your First Home in Canada. What Newcomers Need to Know

Buying Your First Home in Canada What Newcomers Need to Know A PLACE TO CALL HOME. A PLACE OF YOUR OWN. You ve made Canada your new home and now you re looking for a place of your own. Buying a house is

Buying Your First Home in Canada What Newcomers Need to Know A PLACE TO CALL HOME. A PLACE OF YOUR OWN. You ve made Canada your new home and now you re looking for a place of your own. Buying a house is

The essentials of investing for retirement.

The essentials of investing for retirement. Fidelity has been helping people invest for retirement for more than 65 years. Some investors use our actively managed and index mutual funds. Some use our powerful

The essentials of investing for retirement. Fidelity has been helping people invest for retirement for more than 65 years. Some investors use our actively managed and index mutual funds. Some use our powerful

Investment Guide Funds offered through the Washington State Investment Board

Investment Guide Funds offered through the Washington State Investment Board Investing Overview Asset allocation 2 Two investment approaches 2 Build and Monitor 3 One-Step 3 Diversification 4 Trading restrictions

Investment Guide Funds offered through the Washington State Investment Board Investing Overview Asset allocation 2 Two investment approaches 2 Build and Monitor 3 One-Step 3 Diversification 4 Trading restrictions

It is more important than ever for

Multicurrency attribution: not as easy as it looks! With super choice looming Australian investors (including superannuation funds) are becoming increasingly aware of the potential benefits of international

Multicurrency attribution: not as easy as it looks! With super choice looming Australian investors (including superannuation funds) are becoming increasingly aware of the potential benefits of international

Slide 2. What is Investing?

Slide 1 Investments Investment choices can be overwhelming if you don t do your homework. There s the potential for significant gain, but also the potential for significant loss. In this module, you ll

Slide 1 Investments Investment choices can be overwhelming if you don t do your homework. There s the potential for significant gain, but also the potential for significant loss. In this module, you ll

The Search for Yield Continues: A Re-introduction to Bank Loans

INSIGHTS The Search for Yield Continues: A Re-introduction to Bank Loans 203.621.1700 2013, Rocaton Investment Advisors, LLC Executive Summary With the Federal Reserve pledging to stick to its zero interest-rate

INSIGHTS The Search for Yield Continues: A Re-introduction to Bank Loans 203.621.1700 2013, Rocaton Investment Advisors, LLC Executive Summary With the Federal Reserve pledging to stick to its zero interest-rate

What You Should Know About Home Equity Lines of Credit and Important Terms of FlexEquity SM

What You Should Know About Home Equity Lines of Credit and Important Terms of FlexEquity SM Effective March 1, 2008 The Housing Financial Discrimination Act of 1977 Fair Lending Notice It is illegal to

What You Should Know About Home Equity Lines of Credit and Important Terms of FlexEquity SM Effective March 1, 2008 The Housing Financial Discrimination Act of 1977 Fair Lending Notice It is illegal to

With Scholar s Edge, New Mexico s 529 College Savings Plan,

With Scholar s Edge, New Mexico s 529 College Savings Plan, You Can Get an Edge When You Save for College Table of Contents 1 3 EDGE 1 A 529 Plan that s almost as smart as your child EDGE 2 Potentially

With Scholar s Edge, New Mexico s 529 College Savings Plan, You Can Get an Edge When You Save for College Table of Contents 1 3 EDGE 1 A 529 Plan that s almost as smart as your child EDGE 2 Potentially

HOME EQUITY LOANS. How to put your home s equity to work for you Save money and negotiate better terms

guideto: How to put your home s equity to work for you Save money and negotiate better terms HOME EQUITY LOANS Copyright 2007 LendingTree All Rights Reserved The LendingTree Smart Borrower Center offers

guideto: How to put your home s equity to work for you Save money and negotiate better terms HOME EQUITY LOANS Copyright 2007 LendingTree All Rights Reserved The LendingTree Smart Borrower Center offers

CORPORATE RETIREMENT STRATEGY ADVISOR GUIDE. *Advisor USE ONLY

CORPORATE RETIREMENT STRATEGY ADVISOR GUIDE *Advisor USE ONLY TABLE OF CONTENTS Introduction to the corporate retirement strategy...2 Identify the opportunity - target markets... 3 Policy ownership: corporate

CORPORATE RETIREMENT STRATEGY ADVISOR GUIDE *Advisor USE ONLY TABLE OF CONTENTS Introduction to the corporate retirement strategy...2 Identify the opportunity - target markets... 3 Policy ownership: corporate

Chapter Seven STOCK SELECTION

Chapter Seven STOCK SELECTION 1. Introduction The purpose of Part Two is to examine the patterns of each of the main Dow Jones sectors and establish relationships between the relative strength line of

Chapter Seven STOCK SELECTION 1. Introduction The purpose of Part Two is to examine the patterns of each of the main Dow Jones sectors and establish relationships between the relative strength line of

1. Overconfidence {health care discussion at JD s} 2. Biased Judgments. 3. Herding. 4. Loss Aversion

In conditions of laissez-faire the avoidance of wide fluctuations in employment may, therefore, prove impossible without a far-reaching change in the psychology of investment markets such as there is no

In conditions of laissez-faire the avoidance of wide fluctuations in employment may, therefore, prove impossible without a far-reaching change in the psychology of investment markets such as there is no

Chapter 1 The Financial Assessment

Chapter 1 The Financial Assessment 64 P leasant S treet P hon e: ( 415) 830-52 44 Copyright 2007-2009 Harrison Lazarus Advisors, Inc. All Rights Reserved Page 1 of 15 It doesn t matter where you are in

Chapter 1 The Financial Assessment 64 P leasant S treet P hon e: ( 415) 830-52 44 Copyright 2007-2009 Harrison Lazarus Advisors, Inc. All Rights Reserved Page 1 of 15 It doesn t matter where you are in

Measuring Lending Profitability at the Loan Level: An Introduction

FINANCIAL P E RF O R MA N C E Measuring Lending Profitability at the Loan Level: An Introduction [email protected] 877.827.7101 How much am I making on this deal? has been a fundamental question posed

FINANCIAL P E RF O R MA N C E Measuring Lending Profitability at the Loan Level: An Introduction [email protected] 877.827.7101 How much am I making on this deal? has been a fundamental question posed

Conservative Investment Strategies and Financial Instruments Last update: May 14, 2014

Summary Conservative Investment Strategies and Financial Instruments Last update: May 14, 2014 Most retirees should hold a significant portion in many cases, 100% of their savings in conservative financial

Summary Conservative Investment Strategies and Financial Instruments Last update: May 14, 2014 Most retirees should hold a significant portion in many cases, 100% of their savings in conservative financial

UNIT 6 2 The Mortgage Amortization Schedule

UNIT 6 2 The Mortgage Amortization Schedule A home mortgage is a contract that requires the homeowner to make a fixed number of monthly payments over the life of the mortgage. The duration, or length of

UNIT 6 2 The Mortgage Amortization Schedule A home mortgage is a contract that requires the homeowner to make a fixed number of monthly payments over the life of the mortgage. The duration, or length of

Home Financing Guide

Home Financing Guide Table of Contents Is Home Ownership Right for You? 1 Basics about Your Mortgage Options 2 Conventional or High Ratio Mortgage 3 Options for a Down Payment 3 Understanding Amortization

Home Financing Guide Table of Contents Is Home Ownership Right for You? 1 Basics about Your Mortgage Options 2 Conventional or High Ratio Mortgage 3 Options for a Down Payment 3 Understanding Amortization

PURCHASE MORTGAGE. Mortgage loan types

PURCHASE MORTGAGE Mortgage loan types There are many types of mortgages used worldwide, but several factors broadly define the characteristics of the mortgage. All of these may be subject to local regulation

PURCHASE MORTGAGE Mortgage loan types There are many types of mortgages used worldwide, but several factors broadly define the characteristics of the mortgage. All of these may be subject to local regulation

Research. What Impact Will Ballooning Government Debt Levels Have on Government Bond Yields?

Research What Impact Will Ballooning Government Debt Levels Have on Government Bond Yields? The global economy appears to be on the road to recovery and the risk of a double dip recession is receding.

Research What Impact Will Ballooning Government Debt Levels Have on Government Bond Yields? The global economy appears to be on the road to recovery and the risk of a double dip recession is receding.

Peter Elston: Investment Letter

Issue 3: July 2015 Peter Elston: Investment Letter For the love of charts... This document is intended for professional investors only I like charts. This month I take a look at MSCI s major global sectors

Issue 3: July 2015 Peter Elston: Investment Letter For the love of charts... This document is intended for professional investors only I like charts. This month I take a look at MSCI s major global sectors

A guide to the world of investing

A guide to the world of investing Investments Introduction If you are thinking about investing, then this booklet is designed to help lead you through the investment landscape. It s a quick,simple guide

A guide to the world of investing Investments Introduction If you are thinking about investing, then this booklet is designed to help lead you through the investment landscape. It s a quick,simple guide

Debt Service Analysis: Can I Repay?

Purdue Extension Knowledge to Go Debt Service Analysis: Can I Repay? Low prices and incomes have made many farmers and their lenders concerned about the farmers ability to fulfill debt obligations. Lenders

Purdue Extension Knowledge to Go Debt Service Analysis: Can I Repay? Low prices and incomes have made many farmers and their lenders concerned about the farmers ability to fulfill debt obligations. Lenders

INVESTMENT. Understanding your investment in super doesn t have to be hard. You don t need to be a financial whiz to make it work for you!

1 Understanding your investment in super doesn t have to be hard. You don t need to be a financial whiz to make it work for you! You just need to understand your options and how you can make the most of

1 Understanding your investment in super doesn t have to be hard. You don t need to be a financial whiz to make it work for you! You just need to understand your options and how you can make the most of

smart Two Paths to Investing for Retirement Which one is right for you? Massachusetts Deferred Compensation SMART Plan INVEST

smart S A V E M O N E Y A N D R E T I R E T O M O R R O W INVEST Two Paths to Investing for Retirement Which one is right for you? Massachusetts Deferred Compensation SMART Plan Office of the State Treasurer

smart S A V E M O N E Y A N D R E T I R E T O M O R R O W INVEST Two Paths to Investing for Retirement Which one is right for you? Massachusetts Deferred Compensation SMART Plan Office of the State Treasurer

Small Business Finance Thinking Strategically

Small Business Finance Thinking Strategically Copyright 2007 by AbdulJaami, PLLC. All Rights Reserved. This publication is intended as a general guide only. It does not contain a general legal analysis

Small Business Finance Thinking Strategically Copyright 2007 by AbdulJaami, PLLC. All Rights Reserved. This publication is intended as a general guide only. It does not contain a general legal analysis

Types of Debt & Debt Lingo Quick Reference. http://breakingintowallstreet.com. Here s the 10-second version of everything you need to know about debt:

Here s the 10-second version of everything you need to know about debt: Debt Type Revolver Term Loan A Term Loan B Senior Notes Subordinated Notes Mezzanine Interest Rate: Lowest Low Higher Higher Higher

Here s the 10-second version of everything you need to know about debt: Debt Type Revolver Term Loan A Term Loan B Senior Notes Subordinated Notes Mezzanine Interest Rate: Lowest Low Higher Higher Higher

Today s bond market is riskier and more volatile than in several generations. As

Fixed Income Approach 2014 Volume 1 Executive Summary Today s bond market is riskier and more volatile than in several generations. As interest rates rise so does the anxiety of fixed income investors

Fixed Income Approach 2014 Volume 1 Executive Summary Today s bond market is riskier and more volatile than in several generations. As interest rates rise so does the anxiety of fixed income investors

Overview. Growing a Real Estate Portfolio. Risks of Real Estate Investing

Overview Over the past decade, Strongbrook has established a reputation as an industry leader in assisting clients with placing and managing real estate within their investment and retirement portfolios.

Overview Over the past decade, Strongbrook has established a reputation as an industry leader in assisting clients with placing and managing real estate within their investment and retirement portfolios.

Understanding RSPs. Your Guide to Retirement Savings Plans

Understanding RSPs Your Guide to Retirement Savings Plans Getting Started Some retirement basics Getting Ahead Setting your retirement savings goals Getting the Most Maximizing your RSP growth Getting

Understanding RSPs Your Guide to Retirement Savings Plans Getting Started Some retirement basics Getting Ahead Setting your retirement savings goals Getting the Most Maximizing your RSP growth Getting

800.550.9435 www.pwsb.com

800.550.9435 www.pwsb.com Thinking of buying your first home? Bet you re pretty nervous, huh? Maybe even cold sweats nervous. How in the world are you going to afford it? Where do you start? All these

800.550.9435 www.pwsb.com Thinking of buying your first home? Bet you re pretty nervous, huh? Maybe even cold sweats nervous. How in the world are you going to afford it? Where do you start? All these

Exit Strategies for Fixed Rate Financing. Comparing Yield Maintenance and Defeasance Alternatives. by Regan Campbell and Jehane Walsh

Defeasance Vs. Yield Maintenance Exit Strategies for Fixed Rate Financing Comparing Yield Maintenance and Defeasance Alternatives by Regan Campbell and Jehane Walsh When looking to refinance or sell a

Defeasance Vs. Yield Maintenance Exit Strategies for Fixed Rate Financing Comparing Yield Maintenance and Defeasance Alternatives by Regan Campbell and Jehane Walsh When looking to refinance or sell a

Introduction 4. What is Refinancing? 5. Changing Home Loans 5 Changing Needs 6 Identifying Better Opportunities 6 Additional Home Loan Features 6

Contents Introduction 4 What is Refinancing? 5 Changing Home Loans 5 Changing Needs 6 Identifying Better Opportunities 6 Additional Home Loan Features 6 What are the Advantages of Refinancing? 7 1. Consolidating

Contents Introduction 4 What is Refinancing? 5 Changing Home Loans 5 Changing Needs 6 Identifying Better Opportunities 6 Additional Home Loan Features 6 What are the Advantages of Refinancing? 7 1. Consolidating

Financial Ratio Cheatsheet MyAccountingCourse.com PDF

Financial Ratio Cheatsheet MyAccountingCourse.com PDF Table of contents Liquidity Ratios Solvency Ratios Efficiency Ratios Profitability Ratios Market Prospect Ratios Coverage Ratios CPA Exam Ratios to

Financial Ratio Cheatsheet MyAccountingCourse.com PDF Table of contents Liquidity Ratios Solvency Ratios Efficiency Ratios Profitability Ratios Market Prospect Ratios Coverage Ratios CPA Exam Ratios to

Why Cash-Flow Positive Property Is Essential To Building Your Property Portfolio

Why Cash-Flow Positive Property Is Essential To Building Your Property Portfolio Contents 1. Letter from the CEO: 3 2. Introduction 4 3. What are cash flow positive properties? 5 4. Why it s important

Why Cash-Flow Positive Property Is Essential To Building Your Property Portfolio Contents 1. Letter from the CEO: 3 2. Introduction 4 3. What are cash flow positive properties? 5 4. Why it s important

Our managed funds products are issued by

Our managed funds products are issued by 1 According to the Investment and Financial Services Association 1, Australia s first managed funds were introduced in 1954. Since then the industry has grown substantially

Our managed funds products are issued by 1 According to the Investment and Financial Services Association 1, Australia s first managed funds were introduced in 1954. Since then the industry has grown substantially

Mutual Funds 101. What is a Mutual Fund?

Mutual Funds 101 So you re looking to get into the investment game? Great! Mutual funds are a good investment option. But before you invest, make sure to do your research! You would never go to a car dealership,

Mutual Funds 101 So you re looking to get into the investment game? Great! Mutual funds are a good investment option. But before you invest, make sure to do your research! You would never go to a car dealership,

PLAN A SOUND FINANCIAL. A Note from Gary:

A SOUND FINANCIAL PLAN DECEMBER 2014 + A Note from Gary PG1 + A Note from Scott PG2 + Manulife One PG3 + Critical Illness Insurance PG4 + Term Insurance vs. Mortgage Insurance PG5 + Year End Checklist

A SOUND FINANCIAL PLAN DECEMBER 2014 + A Note from Gary PG1 + A Note from Scott PG2 + Manulife One PG3 + Critical Illness Insurance PG4 + Term Insurance vs. Mortgage Insurance PG5 + Year End Checklist

Contribution 787 1,368 1,813 983. Taxable cash flow 682 1,253 1,688 858 Tax liabilities (205) (376) (506) (257)

(376) (506) (257)") Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2012 Answers 1 (a) Calculation of net present value (NPV) As nominal after-tax cash flows are to be discounted, the nominal

Answers Fundamentals Level Skills Module, Paper F9 Financial Management June 2012 Answers 1 (a) Calculation of net present value (NPV) As nominal after-tax cash flows are to be discounted, the nominal

ATTITUDE TO RISK. In this module we take a look at risk management and its importance. MODULE 5 INTRODUCTION PROGRAMME NOVEMBER 2012, EDITION 18

INTRODUCTION PROGRAMME MODULE 5 ATTITUDE TO RISK In this module we take a look at risk management and its importance. NOVEMBER 2012, EDITION 18 CONTENTS 3 6 RISK MANAGEMENT 2 In the previous module we

INTRODUCTION PROGRAMME MODULE 5 ATTITUDE TO RISK In this module we take a look at risk management and its importance. NOVEMBER 2012, EDITION 18 CONTENTS 3 6 RISK MANAGEMENT 2 In the previous module we

INVESTMENT DICTIONARY

INVESTMENT DICTIONARY Annual Report An annual report is a document that offers information about the company s activities and operations and contains financial details, cash flow statement, profit and

INVESTMENT DICTIONARY Annual Report An annual report is a document that offers information about the company s activities and operations and contains financial details, cash flow statement, profit and

HOMEOWNERSHIP: Understanding What You Can Afford, Mortgages, and Closing Costs. Illinois Association of REALTORS. Springfield, IL 62701

Illinois Association of REALTORS 522 S. Fifth Street Springfield, IL 62701 www.illinoisrealtor.org www.yourillinoishome.com HOMEOWNERSHIP: Understanding What You Can Afford, Mortgages, and Closing Costs

Illinois Association of REALTORS 522 S. Fifth Street Springfield, IL 62701 www.illinoisrealtor.org www.yourillinoishome.com HOMEOWNERSHIP: Understanding What You Can Afford, Mortgages, and Closing Costs

Financial Planning in a Low Interest Rate Environment: The Good, the Bad and the Potentially Ugly

Financial Planning in a Low Interest Rate Environment: The Good, the Bad and the Potentially Ugly In June of 2012, the 10 year Treasury note hit its lowest rate level in history when it fell to 1.62%.

Financial Planning in a Low Interest Rate Environment: The Good, the Bad and the Potentially Ugly In June of 2012, the 10 year Treasury note hit its lowest rate level in history when it fell to 1.62%.

Paying Off your Mortgage

ABCs of Mortgages Series Paying Off your Mortgage Faster Smart mortgage decisions start here Table of Contents Overview 1 Understanding principal versus interest 1 Ways to pay off your mortgage faster

ABCs of Mortgages Series Paying Off your Mortgage Faster Smart mortgage decisions start here Table of Contents Overview 1 Understanding principal versus interest 1 Ways to pay off your mortgage faster

CREATE TAX ADVANTAGED RETIREMENT INCOME YOU CAN T OUTLIVE. create tax advantaged retirement income you can t outlive

create tax advantaged retirement income you can t outlive 1 Table Of Contents Insurance Companies Don t Just Sell Insurance... 4 Life Insurance Investing... 5 Guarantees... 7 Tax Strategy How to Get Tax-Free

create tax advantaged retirement income you can t outlive 1 Table Of Contents Insurance Companies Don t Just Sell Insurance... 4 Life Insurance Investing... 5 Guarantees... 7 Tax Strategy How to Get Tax-Free

Using derivatives to hedge interest rate risk: A student exercise

ABSTRACT Using derivatives to hedge interest rate risk: A student exercise Jeff Donaldson University of Tampa Donald Flagg University of Tampa In a world of fluctuating asset prices, many firms find the

ABSTRACT Using derivatives to hedge interest rate risk: A student exercise Jeff Donaldson University of Tampa Donald Flagg University of Tampa In a world of fluctuating asset prices, many firms find the

MANAGING YOUR BUSINESS S CASH FLOW. Managing Your Business s Cash Flow. David Oetken, MBA CPM

MANAGING YOUR BUSINESS S CASH FLOW Managing Your Business s Cash Flow David Oetken, MBA CPM 1 2 Being a successful entrepreneur takes a unique mix of skills and practices. You need to generate exciting

MANAGING YOUR BUSINESS S CASH FLOW Managing Your Business s Cash Flow David Oetken, MBA CPM 1 2 Being a successful entrepreneur takes a unique mix of skills and practices. You need to generate exciting