Disclaimer: This ACA is not the health reform bill UE would pass. We have been consistent in our support for Single Payer ( Medicare For All ) going

|

|

|

- Asher Pearson

- 8 years ago

- Views:

Transcription

1 Disclaimer: This ACA is not the health reform bill UE would pass. We have been consistent in our support for Single Payer ( Medicare For All ) going back to the 1940s. However, the ACA is the law of the land, so we need to minimize impacts and leverage the law to our own benefit where possible.

2 The excise tax may eliminate health insurance plans that provide good coverage, forcing workers to pay a lot more out of pocket. At the other extreme, workers who can t afford health insurance through their employer now might actually get better and cheaper health coverage through the new state exchanges. For those in between, health insurance premiums will continue to become more and more unaffordable as the price exceeds the wage, high deductible plans will become more common as the industry gets away from HMO s and PPO s, and we will be forced to mount major campaigns to prevent the further discrimination of lower hourly wage earners paying the same percentage of insurance premiums as higher salaried earners.

3

4 Polls of employers have found anywhere from 2%-20% plan to drop insurance, with small employers more likely 45% of employers concerned about excise tax Employer mandate creates the incentives for increased numbers of under 30-hour positions, higher usage of temps

5 The Affordable Care Act frontloaded many good but small changes over the last three years. But much bigger changes, some good and others bad, are now to come. The ACA mandates that for individuals who have a new health insurance plan or insurance policy beginning on or after September 30, 2010, certain preventive services for adults, women, and children must be covered without having to pay a copayment or co-insurance to meet the deductible. This applies only when the services are provided by a network provider. Examples of preventive services that must be covered are immunizations and contraceptives. This is a link to a list of preventive services covered:

6

7 Since the employer mandate kicks in at 30 hours, we want to ensure that no contracts set the threshold for benefits at a higher level. The employer may not care if a few people fall through the cracks (since they have 5% wiggle room), and some of them may be restricted due to income from getting exchange subsidies. New fines provide financial incentives to employers to have probationary periods of 30 days or less regarding health insurance. In contracts with long probationary periods, we may wish to ensure the period is reduced. We should add language regarding the ACA to all contracts just as we have in the past with FMLA.

8

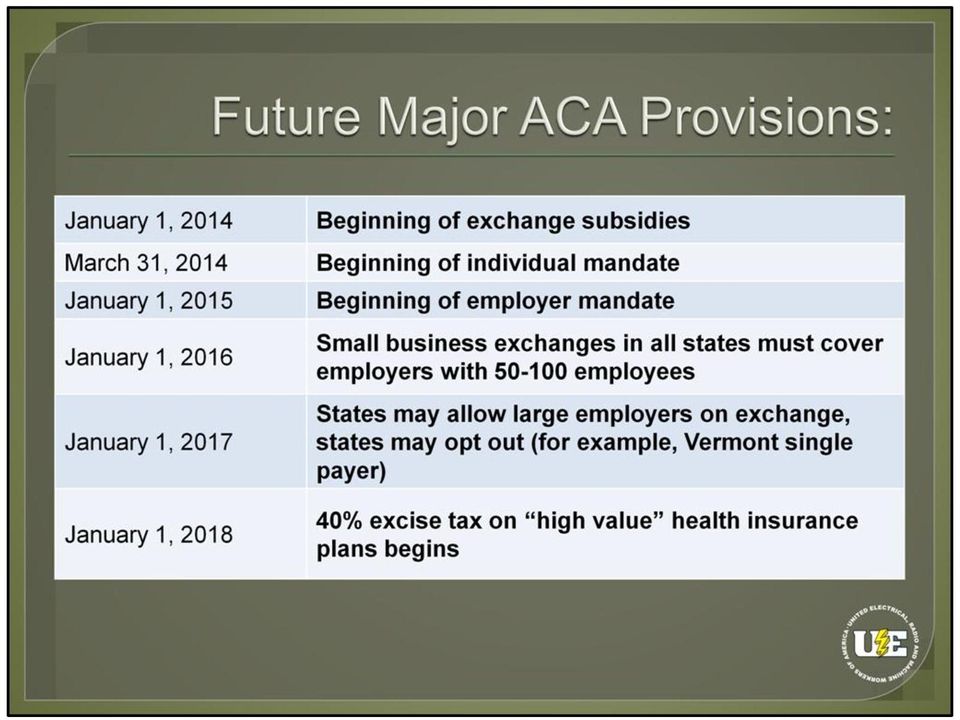

9 There are two major penalties under the Act which apply to employers with more than 50 employees. One is potentially much bigger than the other. Employers are mandated to offer qualified insurance to 95% of their full-time employees in 2014, and dependent children in If they do not, they pay a penalty based on their fulltime workforce. This means there is no financial sense in the employer excluding certain classifications or groups of workers from having insurance. Employers would pay an identical penalty for offering insurance for 90% of the full-time workforce, or 0%, despite having significant costs insuring 90% of the workforce. If an employer offers qualified insurance to 95%+ of the full-time workforce, but some fulltime (30-hour+) workers enroll on the exchange and get subsidies (either because they are excluded from the group plan, or because it would cost more than 9.5% of employee income to purchase single coverage), than the employer is fined $3,000 for each such worker, although the fine can be no greater than the first fine. One note on hours for full-time status: Proposed IRS regulations would treat 130 hours of service (meaning any time an employee is entitled to be paid, not just hours actually worked) in a calendar month as the monthly equivalent of 30 hours of service per week ((52 x 30) 12 = 130). This monthly standard takes into account that the average month consists of more than four weeks. These regulations have not been adopted, but will likely be, as the IRS has maintained a consistent position on this since NOTE: The Employer Mandate has been delayed until January 1, That said, many employers appear to be enacting policies to minimize their own exposure to fines for 2014 regardless of this delay.

10 There are two ways people will go into an exchange, buying a policy individually (either with or without subsidies) or through their employer buying in if they work for a small employer who is qualified. No more differences to pricing based upon preexisting conditions with the exchanges

11 Average private insurance now covers 80% of cost Average HSA-qualified high-deductible plan 67% Within a tier of coverage, all plans should have the same total out-of-pocket costs, but the plan distribution between coinsurance, copays, and deductibles may differ

12 Additional Requirements: Must not qualify for public insurance (Medicare, Medicaid, CHIP, TRICARE, etc) Those with access to employer provided insurance excluded unless plan: 1. Covers less than 60% of medical expenses, or 2. Costs more than 9.5% of household income to pay for the cost of the single premium

13 The special tax benefits to the smallest employers which phased in in 2010 for providing health insurance rise in For-profit businesses see their maximum credit rise from 35% to 50% of the value of insurance, and tax-exempt small-employers see their credit rise from 25% to 35%. They can only get this credit for a maximum of two years, however. The maximum tax credit is earned by employers who have less than 10 workers, or those whose workforce has average taxable wages of $25,000 or less. Employer size is based upon common ownership, meaning separately incorporated branches are not separate small businesses for purposes of the ACA. If there are 40 employees at one location and 70 at another, the count is over 100 and the employer does not qualify as a small business. The only exception is when a larger global company employs less than employees within the U.S. Public employers can enroll in an exchange, if they meet the above requirements, as can nonprofits. Premiums are billed to employers as if they are unsubsidized individual exchange premiums, meaning the oldest workers (64) cost three times what the youngest workers (20) cost, and there is up to a 50% premium surcharge for smoking. Employers do not need to pass on these costs without modification to workers however. Employers don t pay a group rate instead, they get a shopping list totaling the cost for each individual plan a worker chooses. Due to delays, federal-run exchanges (and some state exchanges) won t offer multiple plan choices to small employers until In these cases, if the employer picks a plan in the first year, everyone is enrolled on it. In future years, however, employees will be given a lump of cash which they can use to purchase any small employer plan at any coverage level.

14 If we have a small employer plan, bargaining is a much simpler process, coming down to essentially three questions: what tier or tiers the contract provides for the members, whether members can enroll in any plan within a tier, and the structure and level of premium cost sharing. Remember that most insured workforces currently have coverage similar to gold, but silver is the new default, so in most cases, gold or platinum should be our goal. When it comes to cost sharing, keep in mind that small employer plans are unsubsidized by the government, and thus can vary up to 300% between the youngest and oldest workers. Thus if we have contract language specifying employees pay 10% of the premium, workers of different ages could pay anywhere from $50 to $150 per month for identical coverage. This is a very bad idea not just for shop solidarity, but for the employer, as it sets up a payment system which discriminates against older workers.

15 There are three different subsidies you get based upon income on the exchange. The first, for those under 400% of the poverty line, limits the maximum you can pay annually for premiums to a percentage of your income on a sliding scale. Any costs above this are paid for through the government providing a tax credit, which is either given as part of the annual tax refund or, if preferred, in monthly installments. Please note that this is based upon the second cheapest silver plan on the exchange, so if you want better coverage than this, you must pay for the difference yourself. The second subsidy, available to the lowest-income people, reduces the total cost of deductibles, coinsurance, and copays. While for most people a baseline silver plan would result in roughly 30% cost sharing, for some low income people cost sharing could be as low as 6%. These subsidies are only available if you enroll in a silver plan. The federal government directly pays the insurer for the cost of this subsidy, so if your income is below 250% of the FPL, when the plan is offered to you you ll see much higher levels of coverage for baseline plans. The final subsidy is a reduction of the annual out-of-pocket (OOP) maximum. Similar to the second subsidy, this is paid for through direct payments to insurers. As an example, a family at the 250% threshold enrolling in a plan with an out-of-pocket max which would normally be $8000 would see their annual limit reduced to $4,000.

16 Where does it make sense to consider eliminating employer coverage entirely and going over to the individual exchange? First, the workplace must have fairly low wages. With wages over $16 per hour, a substantial number of members will likely be over the 400% FPL threshold, be ineligible for subsidies, and thus really be harmed with any plan to eliminate employer-provided insurance. We should keep in mind that even in lower-paid shops there may be some individuals particularly those who have working spouses and don t have dependent children at home who may fall over the limit if their wages are substantially higher than the workplace average. In addition, we d want to focus on smaller employers for several reasons. First, employers of under 50 don t have an employer mandate, hence pay no fine if they choose not to insure us. Secondly, the deduction of the first 30 workers for all firms means that even those in the small to medium-sized range (50-200) get a substantial fine reduction compared to large employers. Perhaps most important, however, is the mandate that 95%+ of employees must be ensured means it s cost prohibitive for a larger employer to drop coverage for us unless they can drop it for everyone at once. This also goes for employers which are not particularly large, but have several bargaining units. Imagine a school district, for example, which eliminated coverage for support staff. The teacher s contract isn t up for two years, during which time the district would pay a fine on insured teachers as if they were uninsured. Further, many teachers would make too much to qualify for subsidies, and they d thus be very unlikely to wish to follow support staff into the exchange. Generally speaking, the older the workforce of an employer, the better off employees will be with exchange coverage, as the value of subsidies is so much greater than the tax benefits that both the employer and employee gets for having insurance. On the other hand, for small employers with young workforces, the small employer exchange may be a more attractive option, because premiums are so much cheaper. Keep in mind that if the boss is willing to eliminate our coverage, he must be willing to eliminate his as well and he ll have to pay out of pocket.

17 Some groups are offered insurance under a union contract, but not subject to employer mandates. The largest group are spouses employers must provide employee + child coverage, but they don t need to cover spouses at all under the ACA. Certain contracts also allow part-timers or pre-65 retirees into the group plan, often under pretty bad cost-sharing arrangements. We certainly shouldn t eliminate benefits for these people willy-nilly. We need to carefully consider if the cost sharing under contract for these people is worse than what people would pay on the exchange, and if plans with comparable benefit levels exist. For some people, particularly those who are required to pay 50%-100% of the cost to take part, the exchange will be a godsend, but only if we eliminate the contractual obligation to insure these groups.

18 Beginning on January 1, 2014, most people must have health insurance or pay a tax penalty. Exceptions are those with religious exceptions, prisoners, members of Indian tribes, and people uninsured for less than three months. Another exemption is for undocumented workers however their children are covered by the mandate if they are citizens or documented immigrants. Presumably in most cases they will qualify for Medicaid/CHIP. There is also a rule that you cannot be forced to buy insurance if the cheapest regular plan on your exchange costs more than 8% of your income. Due to this rule few people who make too much money to qualify for subsidies (more than 400% of the poverty line) but make less than $150,000 annually will be forced to by health insurance. The tax penalties that individuals pay annually for not having health insurance are based upon one of two measures either a fixed amount for each adult and child in the family, or a percentage of your income, with the HIGHER of the two numbers being your annual fine. In practical terms this means that lower-income households will usually face the annual flat fee, while higher-income households will instead get a percentage of their gross income deducted. The fine phases in in 2014 and By 2016 it reaches its max as a percent of income, but the per-person charges will still increase with inflation. The tax penalty cannot be greater than cost of cheapest bronze coverage on the exchange.

19 Vision & dental plan benefit values NOT INCLUDED! Insurance companies pay tax on premiums over limits for fully-insured plans. Will try to convert tax into increased premiums, or refuse to offer good plans Employer pays tax on HSA, HRA, and FSA contributions, along with self-insured plan. Employers will try to slash benefits or pass costs to employees

20 Certain groups may get higher limits set, if they have unfavorable age/gender spreads. High risk include electrical and telecommunications installation/repair workers, longshoreman, emergency response, firefighting, law enforcement, construction, mining, agriculture, forestry, and fishing. If the costs for benefits to federal employees exceed certain level, limits may be pushed upward. Assuming annual premium increases of 6%, a family plan which costs $1,750 per month today will be above the excise tax threshold in Assuming the same cost escalation, a plan which now has a monthly premium cost for family of $1,500 per month would hit the excise tax threshold by 2023

21 Unions fought tooth and nail against excise tax it ultimately didn t end up as bad as it initially was, and the phase in was delayed by several years as a result of the labor movement. But it will still have a bad impact. If you can t stop reductions in the value of the health plan due to the excise tax, demand pay increases to make up the difference. If we have new out-of-pocket costs, the employer should provide additional wages (even if they aren t pre-tax) to pay for them. It is also possible that members may want to consider other pre-tax benefits, such as increased pension/401(k) contributions, or a child-care Flexible Spending Account. These allow for us to replace pre-tax dollars with other pre-tax dollars. Finally, despite HRAs also coming under the excise tax, we should consider them in the near period as a possible means to lower premium costs while not substantially affecting member s total costs.

22 In 2017, some states may begin to allow large employers onto their exchanges

23

24

25

THE IMPACT OF THE AFFORDABLE CARE ACT (ACA) ON COLLECTIVE BARGAINING AND UNION BENEFITS June 20, 2014

ON COLLECTIVE BARGAINING AND UNION BENEFITS June 20, 2014") THE IMPACT OF THE AFFORDABLE CARE ACT (ACA) ON COLLECTIVE BARGAINING AND UNION BENEFITS June 20, 2014 Provided lower cost insurance to many lower wage workers and their families. Reduced or slowed the

THE IMPACT OF THE AFFORDABLE CARE ACT (ACA) ON COLLECTIVE BARGAINING AND UNION BENEFITS June 20, 2014 Provided lower cost insurance to many lower wage workers and their families. Reduced or slowed the

The Affordable Care Act: A Guide for Union Negotiators

The Affordable Care Act: A Guide for Union Negotiators AUGUST 2012 The Affordable Care Act (ACA), the health reform law passed in March 2010, includes many provisions that will impact employer-based insurance

The Affordable Care Act: A Guide for Union Negotiators AUGUST 2012 The Affordable Care Act (ACA), the health reform law passed in March 2010, includes many provisions that will impact employer-based insurance

Section 2: INDIVIDUALS WHO CURRENTLY HAVE

Section 2: INDIVIDUALS WHO CURRENTLY HAVE COVERAGE OR AN OFFER OF COVERAGE FROM THEIR EMPLOYER Section 2 covers enrollment issues for individuals who have coverage or an offer of coverage whether through

Section 2: INDIVIDUALS WHO CURRENTLY HAVE COVERAGE OR AN OFFER OF COVERAGE FROM THEIR EMPLOYER Section 2 covers enrollment issues for individuals who have coverage or an offer of coverage whether through

Summary of Provisions Affecting Employer-Sponsored Insurance

JULY 2014 AFFORDABLE CARE ACT Summary of Provisions Affecting Employer-Sponsored Insurance Much of the public discussion about the Affordable Care Act (ACA) has focused on the expansion of coverage to

JULY 2014 AFFORDABLE CARE ACT Summary of Provisions Affecting Employer-Sponsored Insurance Much of the public discussion about the Affordable Care Act (ACA) has focused on the expansion of coverage to

Patient Protection and Affordable Care Act (H.R. 3590)

") on Health Reform Passing comprehensive health care reform has been a priority of the President and Congress. The U.S. House of Representatives passed the Affordable Health Care for America Act on November

on Health Reform Passing comprehensive health care reform has been a priority of the President and Congress. The U.S. House of Representatives passed the Affordable Health Care for America Act on November

Selected Employer Provisions in the Patient Protection and Affordable Care Act and the Health Care and Education Reconciliation Act of 2010

Selected Employer Provisions in the Patient Protection and Affordable Care Act and the Health Care and Education Reconciliation Act of 2010 This chart outlines, in depth, selected provisions in the Patient

Selected Employer Provisions in the Patient Protection and Affordable Care Act and the Health Care and Education Reconciliation Act of 2010 This chart outlines, in depth, selected provisions in the Patient

Health Reform in a Nutshell: What Small Businesses Need to Know Now.

Health Reform in a Nutshell: What Small Businesses Need to Know Now. With the passage of the most significant reform of America s modern-day health care system, many small business owners and human resources

Health Reform in a Nutshell: What Small Businesses Need to Know Now. With the passage of the most significant reform of America s modern-day health care system, many small business owners and human resources

HEALTH CARE REFORM CHECKLIST

HEALTH CARE REFORM CHECKLIST As a small employer, you need to be aware of the new regulations tied to the Affordable Care Act. Refer to this checklist to ensure you understand each one and that you re

HEALTH CARE REFORM CHECKLIST As a small employer, you need to be aware of the new regulations tied to the Affordable Care Act. Refer to this checklist to ensure you understand each one and that you re

Health Care Reform: 2015 Refresher of the Affordable Care Act (ACA)

") Health Care Reform: 2015 Refresher of the Affordable Care Act (ACA) Brought to you by Aon Presented by: Ryan Comstock & Shawna Brown This information is provided for informational purposes only and is

Health Care Reform: 2015 Refresher of the Affordable Care Act (ACA) Brought to you by Aon Presented by: Ryan Comstock & Shawna Brown This information is provided for informational purposes only and is

Federal Health Reform FAQs

Federal Health Reform FAQs Individuals 1. What is an exchange? An exchange, as created under the Affordable Care Act (ACA), is a place where consumers can purchase subsidized health insurance coverage.

Federal Health Reform FAQs Individuals 1. What is an exchange? An exchange, as created under the Affordable Care Act (ACA), is a place where consumers can purchase subsidized health insurance coverage.

EMPLOYEE S GUIDE TO HEALTH CARE REFORM S TAX CREDITS

The EMPLOYEE S GUIDE TO HEALTH CARE REFORM S TAX CREDITS Calculate Your Health Insurance Tax Credit 2 Introduction Beginning in 2014, massive tax credits will become available to help individuals buy health

The EMPLOYEE S GUIDE TO HEALTH CARE REFORM S TAX CREDITS Calculate Your Health Insurance Tax Credit 2 Introduction Beginning in 2014, massive tax credits will become available to help individuals buy health

What an employer should know about Health Care Reform

What an employer should know about Health Presented By David L. Fear, Sr. RHU NAHU Education Foundation Sponsored by PPACA - history Signed into law in March, 2010 2,700 page rough draft became the law

What an employer should know about Health Presented By David L. Fear, Sr. RHU NAHU Education Foundation Sponsored by PPACA - history Signed into law in March, 2010 2,700 page rough draft became the law

Currently, for the very low-income, Medicaid is available for children, parents, and individuals who are disabled, elderly, or pregnant.

0 Currently, for the very low-income, Medicaid is available for children, parents, and individuals who are disabled, elderly, or pregnant. Parents are typically covered at very low income levels, and most

0 Currently, for the very low-income, Medicaid is available for children, parents, and individuals who are disabled, elderly, or pregnant. Parents are typically covered at very low income levels, and most

AFFORDABLE CARE ACT FAQ

AFFORDABLE CARE ACT FAQ What is the Healthcare Insurance Marketplace? The Marketplace is a new way to find quality health coverage. It can help if you don t have coverage now or if you have it but want

AFFORDABLE CARE ACT FAQ What is the Healthcare Insurance Marketplace? The Marketplace is a new way to find quality health coverage. It can help if you don t have coverage now or if you have it but want

Affordable Care Act Employee Education Packet

Affordable Care Act Employee Education Packet Your Health Plan Options under the Affordable Care Act The Affordable Care Act (ACA) requires that most Americans be covered under a health plan by January

Affordable Care Act Employee Education Packet Your Health Plan Options under the Affordable Care Act The Affordable Care Act (ACA) requires that most Americans be covered under a health plan by January

The Insurance Mandates of the Affordable Care Act

1 A. Affordable Care Act Individual Mandate The Insurance Mandates of the Affordable Care Act 1. All citizens of the United States are subject to the individual mandate as are all permanent residents and

1 A. Affordable Care Act Individual Mandate The Insurance Mandates of the Affordable Care Act 1. All citizens of the United States are subject to the individual mandate as are all permanent residents and

4/8/2013. Health Care Reform and the. NYS Exchange. Dr. Arthur Vercillo, MD Regional President April 8, 2013. Health Care Reform and the NYS Exchange

Health Care Reform and the NYS Exchange Presentation to the Health Planning Council Advisory Board April 8, 2013, Ithaca NY By Dr. Arthur Vercillo, MD Additional resources on next to last slide. Health

Health Care Reform and the NYS Exchange Presentation to the Health Planning Council Advisory Board April 8, 2013, Ithaca NY By Dr. Arthur Vercillo, MD Additional resources on next to last slide. Health

Whether to Buy Health Coverage or Pay the Penalty

Whether to Buy Health Coverage or Pay the Penalty By Eddie Adkins and Lynn Ettinger Deciding whether to pay for health insurance or forgo it and pay a penalty is easy for many people. They think, Without

Whether to Buy Health Coverage or Pay the Penalty By Eddie Adkins and Lynn Ettinger Deciding whether to pay for health insurance or forgo it and pay a penalty is easy for many people. They think, Without

The Affordable Care Act: What Public Employers Need to be Doing Now

The Affordable Care Act: What Public Employers Need to be Doing Now April 30, 2014 J. Richard Johnson IPMA-HR Webinar Copyright 2014 by The Segal Group, Inc. All rights reserved. 1 ACA Update Discussion

The Affordable Care Act: What Public Employers Need to be Doing Now April 30, 2014 J. Richard Johnson IPMA-HR Webinar Copyright 2014 by The Segal Group, Inc. All rights reserved. 1 ACA Update Discussion

INDIVIDUAL RESPONSIBILITY

Health Care Reform (HCR), Affordable Care Act (ACA), Mandates, Regulations, Health Insurance Marketplace, Health Insurance Exchanges, Penalties What does all this mean to you in 2014? There are many health

Health Care Reform (HCR), Affordable Care Act (ACA), Mandates, Regulations, Health Insurance Marketplace, Health Insurance Exchanges, Penalties What does all this mean to you in 2014? There are many health

What the Health Care Reform Bill Means to Employers

What the Health Care Reform Bill Means to Employers No doubt you have heard the news that on Tuesday, March 23, 2010, President Obama signed into law sweeping health care overhaul legislation. This followed

What the Health Care Reform Bill Means to Employers No doubt you have heard the news that on Tuesday, March 23, 2010, President Obama signed into law sweeping health care overhaul legislation. This followed

Q. My company already offers employee health coverage, how does the law impact me?

Frequently Asked Questions Q. Will my business be required to provide employee health insurance under the health care law? A. The law does not mandate employers provide employees health care coverage.

Frequently Asked Questions Q. Will my business be required to provide employee health insurance under the health care law? A. The law does not mandate employers provide employees health care coverage.

Introduction. Affordable Care Act Overview of Changes

Introduction Affordable Care Act Overview of Changes Presented by: Tim Dillingham, CLU Benefit Resource Group, Inc. 201 E Broad Street, Suite 1 Linden, MI 48451 810-735-6500 810-735-6610 (fax) tim@benefitresourcegroup.net

Introduction Affordable Care Act Overview of Changes Presented by: Tim Dillingham, CLU Benefit Resource Group, Inc. 201 E Broad Street, Suite 1 Linden, MI 48451 810-735-6500 810-735-6610 (fax) tim@benefitresourcegroup.net

Exchanges and the ACA What You Need to Know for 2014

Exchanges and the ACA What You Need to Know for 2014 How the Affordable Care Act affects the Individual Health Insurance Market This presentation is for informational purposes only and does not constitute

Exchanges and the ACA What You Need to Know for 2014 How the Affordable Care Act affects the Individual Health Insurance Market This presentation is for informational purposes only and does not constitute

How ACA is Changing Employer Health Benefits and the Marketplace Presented by:

North Carolina State Health Plan How ACA is Changing Employer Health Benefits and the Marketplace Presented by: J. Richard Johnson Senior Vice President, Public Sector Health Practice Leader rjohnson@segalco.com

North Carolina State Health Plan How ACA is Changing Employer Health Benefits and the Marketplace Presented by: J. Richard Johnson Senior Vice President, Public Sector Health Practice Leader rjohnson@segalco.com

Health Insurance Marketplace Frequently Asked Questions

Health Insurance Marketplace Frequently Asked Questions Q & A SPECIFIC TO THE HEALTH INSURANCE MARKETPLACE & ASSISTANCE Q1: Why is health insurance important? A: No one plans to get sick or hurt, but at

Health Insurance Marketplace Frequently Asked Questions Q & A SPECIFIC TO THE HEALTH INSURANCE MARKETPLACE & ASSISTANCE Q1: Why is health insurance important? A: No one plans to get sick or hurt, but at

Presented by South Dakota Community Action Partnership

Presented by South Dakota Community Action Partnership The project described was supported by Funding Opportunity Number CA-NAV-13-001 from the U.S Department of Health and Human Services, Centers for

Presented by South Dakota Community Action Partnership The project described was supported by Funding Opportunity Number CA-NAV-13-001 from the U.S Department of Health and Human Services, Centers for

Health Care Reform: General Q&A for Employees

From Baugher Financial & Associates, Inc. Health Care Reform: General Q&A for Employees Common questions answered I ve heard a lot about the health care reform law. When do the reforms become effective?

From Baugher Financial & Associates, Inc. Health Care Reform: General Q&A for Employees Common questions answered I ve heard a lot about the health care reform law. When do the reforms become effective?

Premium Tax Credits: Answers to Frequently Asked Questions

Updated July 2013 Premium Tax Credits: Answers to Frequently Asked Questions Beginning in 2014, millions of Americans will become eligible for a new premium tax credit that will help them pay for health

Updated July 2013 Premium Tax Credits: Answers to Frequently Asked Questions Beginning in 2014, millions of Americans will become eligible for a new premium tax credit that will help them pay for health

Prescribed Side Effects of the Patient Protection and Affordable Care Act (PPACA): Healthcare Reform Update

: Healthcare Reform Update") August 14, 2013 Presented by: Jay Hutto, CPA Prescribed Side Effects of the Patient Protection and Affordable Care Act (PPACA): Healthcare Reform Update Click HERE to listen to webinar. August 14, 2013

August 14, 2013 Presented by: Jay Hutto, CPA Prescribed Side Effects of the Patient Protection and Affordable Care Act (PPACA): Healthcare Reform Update Click HERE to listen to webinar. August 14, 2013

Scott Lyon, Senior Vice President Small Business Association of Michigan

Scott Lyon, Senior Vice President Small Business Association of Michigan Patient Protection and Affordable Care Act H.R. 3590 Health Care & Education Affordability Reconciliation Act H.R. 4872 20,000 30,000

Scott Lyon, Senior Vice President Small Business Association of Michigan Patient Protection and Affordable Care Act H.R. 3590 Health Care & Education Affordability Reconciliation Act H.R. 4872 20,000 30,000

Health Insurance Marketplace 101. Find health care options that meet your needs and fit your budget.

Health Insurance Marketplace 101 Find health care options that meet your needs and fit your budget. March 2014 The Health Care Law In March 2010, President Obama signed the Affordable Care Act into law

Health Insurance Marketplace 101 Find health care options that meet your needs and fit your budget. March 2014 The Health Care Law In March 2010, President Obama signed the Affordable Care Act into law

Why the Affordable Care Act Matters for Women: Health Insurance Coverage for Lower- and Moderate- Income Pregnant Women

Why the Affordable Care Act Matters for Women: ISSUE BRIEF Health Insurance Coverage for Lower- and Moderate- Income Pregnant Women Many women of childbearing age will gain access to affordable health

Why the Affordable Care Act Matters for Women: ISSUE BRIEF Health Insurance Coverage for Lower- and Moderate- Income Pregnant Women Many women of childbearing age will gain access to affordable health

FAQ New Health Insurance Law

FAQ New Health Insurance Law (Enacted on March 21, signed into law on March 23, and amended on March 25) On March 23, 2010 President Barack Obama signed the Patient Protection & Affordable Care Act (H.R.

FAQ New Health Insurance Law (Enacted on March 21, signed into law on March 23, and amended on March 25) On March 23, 2010 President Barack Obama signed the Patient Protection & Affordable Care Act (H.R.

Health Reform. Presented by USI Affinity

Health Reform Presented by USI Affinity USI Affinity Introduction USI Affinity has been working with Associations and their members for over 50 years. USI Affinity has offices in Philadelphia, Harrisburg,

Health Reform Presented by USI Affinity USI Affinity Introduction USI Affinity has been working with Associations and their members for over 50 years. USI Affinity has offices in Philadelphia, Harrisburg,

Health Care Reform: Ready or Not, Here it Comes! Presented by:

Broader Perspective. Business Solutions. Health Care Reform: Ready or Not, Here it Comes! Presented by: Ryan Fridborg, MAOD, SPHR Executive Vice President, Employee Benefits rfridborg@boltonco.com Marilyn

Broader Perspective. Business Solutions. Health Care Reform: Ready or Not, Here it Comes! Presented by: Ryan Fridborg, MAOD, SPHR Executive Vice President, Employee Benefits rfridborg@boltonco.com Marilyn

Health care reform at-a-glance. August 2014

Health care reform at-a-glance August 2014 Employer mandate Shared responsibility payment for failing to offer coverage to at least 95%* of all fulltime employees (FTE) and children if any FTE gets subsidy

Health care reform at-a-glance August 2014 Employer mandate Shared responsibility payment for failing to offer coverage to at least 95%* of all fulltime employees (FTE) and children if any FTE gets subsidy

INDIVIDUAL HEALTH INSURANCE GUIDE. Introduction. What is the Health Insurance Marketplace?

INDIVIDUAL HEALTH INSURANCE GUIDE Introduction On November 15th, 2014, the second annual Open Enrollment Period for Individual Health Insurance begins. The Affordable Care Act (ACA) requires all US citizens

INDIVIDUAL HEALTH INSURANCE GUIDE Introduction On November 15th, 2014, the second annual Open Enrollment Period for Individual Health Insurance begins. The Affordable Care Act (ACA) requires all US citizens

Health care reform at-a-glance. December 2013

December 2013 Employer mandate Play or pay penalty for failing to offer coverage to at least 95% of all full-time employees (FTE) and children if any FTE gets subsidy in exchange $2,000 (indexed) times

December 2013 Employer mandate Play or pay penalty for failing to offer coverage to at least 95% of all full-time employees (FTE) and children if any FTE gets subsidy in exchange $2,000 (indexed) times

Healthcare Provisions 2013/2014. What Small Businesses Need to Know

Healthcare Provisions 2013/2014 What Small Businesses Need to Know Healthcare Provisions 2013/2014 PPACA The healthcare reforms in the Patient Protection and Affordable Care Act (PPACA), commonly referred

Healthcare Provisions 2013/2014 What Small Businesses Need to Know Healthcare Provisions 2013/2014 PPACA The healthcare reforms in the Patient Protection and Affordable Care Act (PPACA), commonly referred

The Affordable Care Act: Health Coverage Options & Considerations in 2014

The Affordable Care Act: Health Coverage Options & Considerations in 2014 J A C K S O N V I L L E A R E A C H A M B E R O F C O M M E R C E A U G U S T 2 7, 2 0 1 3 L A U R A M I N Z E R E X E C U T I

The Affordable Care Act: Health Coverage Options & Considerations in 2014 J A C K S O N V I L L E A R E A C H A M B E R O F C O M M E R C E A U G U S T 2 7, 2 0 1 3 L A U R A M I N Z E R E X E C U T I

Things Small Businesses Need To Know About Health Care Reform

7 Things Small Businesses Need To Know About Health Care Reform Make sure your business meets the requirements of the Affordable Care Act on schedule 7 Things Small Businesses Need To Know About Health

7 Things Small Businesses Need To Know About Health Care Reform Make sure your business meets the requirements of the Affordable Care Act on schedule 7 Things Small Businesses Need To Know About Health

Health Care Reform Update

Small Businesses No Financial Requirements for Small Businesses: The ACA imposes no financial requirements for small businesses to contribute to their employees health insurance. However, beginning in

Small Businesses No Financial Requirements for Small Businesses: The ACA imposes no financial requirements for small businesses to contribute to their employees health insurance. However, beginning in

THE AFFORDABLE CARE ACT ( ACT ), NEW EMPLOYER MANDATES, AND IMPACTS ON EMPLOYER- SPONSORED HEALTH INSURANCE PLANS

, NEW EMPLOYER MANDATES, AND IMPACTS ON EMPLOYER- SPONSORED HEALTH INSURANCE PLANS") Community THE AFFORDABLE CARE ACT ( ACT ), NEW EMPLOYER MANDATES, AND IMPACTS ON EMPLOYER- SPONSORED HEALTH INSURANCE PLANS Prepared for the 2014 Massachusetts Municipal Association Annual Meeting On March

Community THE AFFORDABLE CARE ACT ( ACT ), NEW EMPLOYER MANDATES, AND IMPACTS ON EMPLOYER- SPONSORED HEALTH INSURANCE PLANS Prepared for the 2014 Massachusetts Municipal Association Annual Meeting On March

HEALTH INSURANCE MARKETPLACE SURVIVAL GUIDE FOR SMALL BUSINESS. Vermont Edition

HEALTH INSURANCE MARKETPLACE SURVIVAL GUIDE FOR SMALL BUSINESS Vermont Edition NAVIGATING NEXT STEPS IN HEALTH CARE REFORM There s a constant stream of changes and updates related to health care reform,

HEALTH INSURANCE MARKETPLACE SURVIVAL GUIDE FOR SMALL BUSINESS Vermont Edition NAVIGATING NEXT STEPS IN HEALTH CARE REFORM There s a constant stream of changes and updates related to health care reform,

SURVIVAL GUIDE FOR SMALL BUSINESS

HEALTH INSURANCE MARKETPLACE SURVIVAL GUIDE FOR SMALL BUSINESS Vermont edition NAVIGATING NEXT STEPS IN HEALTH CARE REFORM There s a constant stream of changes and updates related to health care reform,

HEALTH INSURANCE MARKETPLACE SURVIVAL GUIDE FOR SMALL BUSINESS Vermont edition NAVIGATING NEXT STEPS IN HEALTH CARE REFORM There s a constant stream of changes and updates related to health care reform,

What Healthcare Providers Need to Know about the Affordable Care Act (ACA)

") What Healthcare Providers Need to Know about the Affordable Care Act (ACA) General Housekeeping If you experience any technical difficulties during the webinar, please contact GoToMeeting.com Corporate

What Healthcare Providers Need to Know about the Affordable Care Act (ACA) General Housekeeping If you experience any technical difficulties during the webinar, please contact GoToMeeting.com Corporate

How the Affordable Care Act Affects Medical Support Orders in Oklahoma Frequently Asked Questions Spring, 2014 1

How the Affordable Care Act Affects Medical Support Orders in Oklahoma Frequently Asked Questions Spring, 2014 1 General 1. Did Oklahoma expand Medicaid? No, Oklahoma did not expand Medicaid. 2. Who is

How the Affordable Care Act Affects Medical Support Orders in Oklahoma Frequently Asked Questions Spring, 2014 1 General 1. Did Oklahoma expand Medicaid? No, Oklahoma did not expand Medicaid. 2. Who is

Sandy Wood, CEBS (Certified Employee Benefit Specialist) Healthcare Consultant sandy@thebenefitsacademy.com 206-669-3345

Healthcare Consultant sandy@thebenefitsacademy.com 206-669-3345") 1 Sandy Wood, CEBS (Certified Employee Benefit Specialist) Healthcare Consultant sandy@thebenefitsacademy.com 206-669-3345 2 Terms you need to know Required Notices 2014 Plan Requirements The Grandfathered

1 Sandy Wood, CEBS (Certified Employee Benefit Specialist) Healthcare Consultant sandy@thebenefitsacademy.com 206-669-3345 2 Terms you need to know Required Notices 2014 Plan Requirements The Grandfathered

Health-Care Reform. Begley Insurance Group, Inc. Mary Angelo 5225 Old Orchard Rd. Skokie, IL 60077 800-867-7074

Begley Insurance Group, Inc. Mary Angelo 5225 Old Orchard Rd. Skokie, IL 60077 800-867-7074 Health-Care Reform August 14, 2012 Page 1 of 8, see disclaimer on final page One primary goal of the Patient

Begley Insurance Group, Inc. Mary Angelo 5225 Old Orchard Rd. Skokie, IL 60077 800-867-7074 Health-Care Reform August 14, 2012 Page 1 of 8, see disclaimer on final page One primary goal of the Patient

Health Care Reform Update. Spring 2014

Health Care Reform Update Spring 2014 Quincy Quinlan Texas Association of Counties 512 478 8753 quincyq@county.org http://www.county.org Today s Agenda Timeline Fees/Taxes Individual Mandate Marketplace

Health Care Reform Update Spring 2014 Quincy Quinlan Texas Association of Counties 512 478 8753 quincyq@county.org http://www.county.org Today s Agenda Timeline Fees/Taxes Individual Mandate Marketplace

Health Care Reform: Major Provisions and Bargaining Strategies for Retirees

Health Care Reform: Major Provisions and Bargaining Strategies for Retirees MEDICARE Summary of Benefit: Medicare is the federal government s healthcare program for the elderly and certain disabled individuals.

Health Care Reform: Major Provisions and Bargaining Strategies for Retirees MEDICARE Summary of Benefit: Medicare is the federal government s healthcare program for the elderly and certain disabled individuals.

Health Policy Essentials: Private Health Insurance. Bernadette Fernandez, Annie Mach, & Namrata Uberoi February 13, 2015

Health Policy Essentials: Private Health Insurance Bernadette Fernandez, Annie Mach, & Namrata Uberoi February 13, 2015 Briefing Agenda What is the purpose of private health insurance (PHI)? How is PHI

Health Policy Essentials: Private Health Insurance Bernadette Fernandez, Annie Mach, & Namrata Uberoi February 13, 2015 Briefing Agenda What is the purpose of private health insurance (PHI)? How is PHI

A Digital Insurance Health Care Reform Handbook for Employers

A Digital Insurance Health Care Reform Handbook for Employers Health care reform is complicated. Sifting through all the regulations and provisions can be time-consuming and confusing. That s why Digital

A Digital Insurance Health Care Reform Handbook for Employers Health care reform is complicated. Sifting through all the regulations and provisions can be time-consuming and confusing. That s why Digital

Affordable Care Act and Employers

Affordable Care Act and Employers Important Details about Health Care Reform The Affordable Care Act (ACA, i.e., federal health care reform) makes significant changes to health insurance practices nationwide.

Affordable Care Act and Employers Important Details about Health Care Reform The Affordable Care Act (ACA, i.e., federal health care reform) makes significant changes to health insurance practices nationwide.

HEALTH CARE REFORM: FREQUENTLY ASKED QUESTIONS (Group, Individual, Seasonal)

") Group Health Insurance Q & A HEALTH CARE REFORM: FREQUENTLY ASKED QUESTIONS (Group, Individual, Seasonal) 1. Will small employers continue to have 12 month rates as they exist today? a. Yes. Employer groups

Group Health Insurance Q & A HEALTH CARE REFORM: FREQUENTLY ASKED QUESTIONS (Group, Individual, Seasonal) 1. Will small employers continue to have 12 month rates as they exist today? a. Yes. Employer groups

A simple guide to. health care reform. for small business. From a company that believes in making things simple

A simple guide to health care reform for small business From a company that believes in making things simple Document prepared July, 2013 Be prepared. Motto of the Boy Scouts of America After much discussion

A simple guide to health care reform for small business From a company that believes in making things simple Document prepared July, 2013 Be prepared. Motto of the Boy Scouts of America After much discussion

Corporate Health Exchange Frequently Asked Questions

Corporate Health Exchange Frequently Asked Questions FAQs Quick Start Menu If you have a specific question, see if it s here in the list below and click on the link to be taken directly to the answer you

Corporate Health Exchange Frequently Asked Questions FAQs Quick Start Menu If you have a specific question, see if it s here in the list below and click on the link to be taken directly to the answer you

NEW YORK STATE HEALTH INSURANCE EXCHANGE

NEW YORK STATE HEALTH INSURANCE EXCHANGE INFORMATIONAL GUIDE Vista Health Solutions www.nyhealthinsurer.com 1 Table of Contents What is the New York State Health Insurance Exchange?...3 Essential Benefits...3

NEW YORK STATE HEALTH INSURANCE EXCHANGE INFORMATIONAL GUIDE Vista Health Solutions www.nyhealthinsurer.com 1 Table of Contents What is the New York State Health Insurance Exchange?...3 Essential Benefits...3

An Employer s Guide to Health Care Reform

An Employer s Guide to Health Care Reform Important details to navigate employer-provided benefits amidst a changing health care landscape. PAGE 1 Navigating a new health care landscape Health care reform,

An Employer s Guide to Health Care Reform Important details to navigate employer-provided benefits amidst a changing health care landscape. PAGE 1 Navigating a new health care landscape Health care reform,

Health Reform. Senate Leadership Bill Patient Protection and Affordable Care Act (H.R. 3590)

") on Health Reform Comprehensive health reform legislation is currently being debated in Congress. On November 7, 2009, the U.S. House of Representatives passed the Affordable Health Care for America Act

on Health Reform Comprehensive health reform legislation is currently being debated in Congress. On November 7, 2009, the U.S. House of Representatives passed the Affordable Health Care for America Act

The Affordable Care Act: What it Means for Seniors

December 12, 2013 The Affordable Care Act: What it Means for Seniors Amber Cutler, Staff Attorney National Senior Citizens Law Center www.nsclc.org 1 The National Senior Citizens Law Center is a non-profit

December 12, 2013 The Affordable Care Act: What it Means for Seniors Amber Cutler, Staff Attorney National Senior Citizens Law Center www.nsclc.org 1 The National Senior Citizens Law Center is a non-profit

Tax Implications of the Affordable Care Act

Year-by-Year Guide Tax Implications of the Affordable Care Act 1 Year-by-Year Guide: Tax Implications of the Affordable Care Act Introduction The Patient Protection and Affordable Care Act, commonly referred

Year-by-Year Guide Tax Implications of the Affordable Care Act 1 Year-by-Year Guide: Tax Implications of the Affordable Care Act Introduction The Patient Protection and Affordable Care Act, commonly referred

Understanding The Goals Of The Affordable Care Act

Understanding The New World Of Health Insurance Webinar Kitces.com Michael E. Kitces MSFS, MTAX, CFP, CLU, ChFC, RHU, REBC, CASL Partner. Director of Research, Pinnacle Advisory Group Publisher. The Kitces

Understanding The New World Of Health Insurance Webinar Kitces.com Michael E. Kitces MSFS, MTAX, CFP, CLU, ChFC, RHU, REBC, CASL Partner. Director of Research, Pinnacle Advisory Group Publisher. The Kitces

Healthcare Reform Preparedness for Small Businesses

Healthcare Reform Preparedness for Small Businesses Blue KC on Wheels Community awareness initiative Health screenings Wellness information Seminars on healthcare reform, health insurance and wellness

Healthcare Reform Preparedness for Small Businesses Blue KC on Wheels Community awareness initiative Health screenings Wellness information Seminars on healthcare reform, health insurance and wellness

Find health care options that meet your needs and fit your budget.

Health Insurance Marketplace 101 Find health care options that meet your needs and fit your budget. October 2015 Objectives This session will help you Explain the Health Insurance Marketplace Define who

Health Insurance Marketplace 101 Find health care options that meet your needs and fit your budget. October 2015 Objectives This session will help you Explain the Health Insurance Marketplace Define who

to Health Care Reform

The Employer s Guide to Health Care Reform What you need to know now to: Consider your choices Decide what s best for you Follow the rules 2013-2014 Health care reform is the law of the land. Some don

The Employer s Guide to Health Care Reform What you need to know now to: Consider your choices Decide what s best for you Follow the rules 2013-2014 Health care reform is the law of the land. Some don

Healthy Business Chat 07/10/2014

Healthy Business Chat 07/10/2014 1 What Is An Insurance Exchange? An Insurance Exchange is an organized marketplace for insurance plans to compete and offer services efficiently in the small group and

Healthy Business Chat 07/10/2014 1 What Is An Insurance Exchange? An Insurance Exchange is an organized marketplace for insurance plans to compete and offer services efficiently in the small group and

As of January 1, 2014, most individuals must have some form of health coverage, or pay a penalty to the federal government.

Consumer Alert Health Insurance for 2014: What You Need to Know Before You Enroll (Individuals) As of January 1, 2014, most individuals must have some form of health coverage, or pay a penalty to the federal

Consumer Alert Health Insurance for 2014: What You Need to Know Before You Enroll (Individuals) As of January 1, 2014, most individuals must have some form of health coverage, or pay a penalty to the federal

Health Insurance Marketplace 101

Health Insurance Marketplace 101 The Marketplace is open! Find health care options that meet your needs and fit your budget. The Health Care Law In March 2010, President Obama signed the Affordable Care

Health Insurance Marketplace 101 The Marketplace is open! Find health care options that meet your needs and fit your budget. The Health Care Law In March 2010, President Obama signed the Affordable Care

A Digital Benefit Advisors Health Care Reform Handbook for Employers

A Digital Benefit Advisors Health Care Reform Handbook for Employers Health care reform is complicated. Sifting through all the regulations and provisions can be time-consuming and confusing. That s why

A Digital Benefit Advisors Health Care Reform Handbook for Employers Health care reform is complicated. Sifting through all the regulations and provisions can be time-consuming and confusing. That s why

HEALTH INSURANCE MARKETPLACE SURVIVAL GUIDE FOR SMALL BUSINESS. New York Edition

HEALTH INSURANCE MARKETPLACE SURVIVAL GUIDE FOR SMALL BUSINESS New York Edition NAVIGATING NEXT STEPS IN HEALTH CARE REFORM PAGE 2 www.discovermvp.com There s a constant stream of changes and updates related

HEALTH INSURANCE MARKETPLACE SURVIVAL GUIDE FOR SMALL BUSINESS New York Edition NAVIGATING NEXT STEPS IN HEALTH CARE REFORM PAGE 2 www.discovermvp.com There s a constant stream of changes and updates related

Find health care options that meet your needs and fit your budget. ctober 2014

O Health Insurance Find health care options that meet your needs and fit your budget. ctober 2014 The Health Care Law In March 2010, President Obama signed the Affordable Care Act into law generally requiring

O Health Insurance Find health care options that meet your needs and fit your budget. ctober 2014 The Health Care Law In March 2010, President Obama signed the Affordable Care Act into law generally requiring

HEALTH BENEFIT EXCHANGE SURVIVAL GUIDE FOR SMALL BUSINESS. New York Edition

HEALTH BENEFIT EXCHANGE SURVIVAL GUIDE FOR SMALL BUSINESS New York Edition NAVIGATING NEXT STEPS IN HEALTH CARE REFORM PAGE 2 www.discovermvp.com There s a constant stream of changes and updates related

HEALTH BENEFIT EXCHANGE SURVIVAL GUIDE FOR SMALL BUSINESS New York Edition NAVIGATING NEXT STEPS IN HEALTH CARE REFORM PAGE 2 www.discovermvp.com There s a constant stream of changes and updates related

FAQ: Health Care Reform and Minnesota s Nonprofit Employers

FAQ: Health Care Reform and Minnesota s Nonprofit Employers Minnesota s health insurance landscape has been undergoing some significant improvements, leading to better and more affordable coverage for

FAQ: Health Care Reform and Minnesota s Nonprofit Employers Minnesota s health insurance landscape has been undergoing some significant improvements, leading to better and more affordable coverage for

SURVIVAL GUIDE FOR SMALL BUSINESS

HEALTH INSURANCE MARKETPLACE SURVIVAL GUIDE FOR SMALL BUSINESS New York edition NAVIGATING NEXT STEPS IN HEALTH CARE REFORM PAGE 2 www.discovermvp.com There s a constant stream of changes and updates related

HEALTH INSURANCE MARKETPLACE SURVIVAL GUIDE FOR SMALL BUSINESS New York edition NAVIGATING NEXT STEPS IN HEALTH CARE REFORM PAGE 2 www.discovermvp.com There s a constant stream of changes and updates related

ABC Company 123 Main Street Anywhere, USA 12345 www.sampleabccompany.com 800.123.4567

WHAT HEALTH CARE REFORM MEANS FOR YOUR BUSINESS Your promotional imprint here and/or back cover. ABC Company 123 Main Street Anywhere, USA 12345 www.sampleabccompany.com 800.123.4567 The Patient Protection

WHAT HEALTH CARE REFORM MEANS FOR YOUR BUSINESS Your promotional imprint here and/or back cover. ABC Company 123 Main Street Anywhere, USA 12345 www.sampleabccompany.com 800.123.4567 The Patient Protection

Preparing for 2015. A compliance and decision guide for large (more than 50 employees) private, government, and not-for-profit employers

private, government, and not-for-profit employers") Preparing for 2015 A compliance and decision guide for large (more than 50 employees) private, government, and not-for-profit employers 1 This guide is intended to provide information to help employers

Preparing for 2015 A compliance and decision guide for large (more than 50 employees) private, government, and not-for-profit employers 1 This guide is intended to provide information to help employers

Senate HELP Committee Affordable Health Choices Act (S. 1679) June 9, 2009 (passed by Committee July 15, 2009)

June 9, 2009 (passed by Committee July 15, 2009)") on Health Reform This side-by-side compares the leading comprehensive reform proposals across a number of key characteristics and plan components. Included in this side-byside are proposals for moving

on Health Reform This side-by-side compares the leading comprehensive reform proposals across a number of key characteristics and plan components. Included in this side-byside are proposals for moving

Frequently Asked Questions

Frequently Asked Questions What is Covered California? What is Obamacare? Are they the same? What is the Medi-Cal program? Who can buy health insurance through Covered California? When will I be able to

Frequently Asked Questions What is Covered California? What is Obamacare? Are they the same? What is the Medi-Cal program? Who can buy health insurance through Covered California? When will I be able to

Answers about. Health Care REFORM. for your business

Answers about Health Care REFORM for your business Since the time of its enactment in 2010, the health care reform law has remained controversial at least in part due to a constitutional challenge to the

Answers about Health Care REFORM for your business Since the time of its enactment in 2010, the health care reform law has remained controversial at least in part due to a constitutional challenge to the

Health insurance Marketplace. What to expect in 2014

Health insurance Marketplace What to expect in 2014 Overview The Affordable Care Act (ACA) includes several provisions geared to extend greater access to health insurance benefits to more people. Beginning

Health insurance Marketplace What to expect in 2014 Overview The Affordable Care Act (ACA) includes several provisions geared to extend greater access to health insurance benefits to more people. Beginning

THE AFFORDABLE CARE ACT: THE AFFORDABLE COVERAGE OPTIONS AND CONSIDERATIONS IN 2014 THE NEW HEALTH INSURANCE: MARKETPLACE AND MEDICAID

THE AFFORDABLE CARE ACT: THE AFFORDABLE COVERAGE OPTIONS AND CONSIDERATIONS IN 2014 THE NEW HEALTH INSURANCE: MARKETPLACE AND MEDICAID Deloris Summers Deaf In-Person Counselor Navigator Jacksonville Area

THE AFFORDABLE CARE ACT: THE AFFORDABLE COVERAGE OPTIONS AND CONSIDERATIONS IN 2014 THE NEW HEALTH INSURANCE: MARKETPLACE AND MEDICAID Deloris Summers Deaf In-Person Counselor Navigator Jacksonville Area

Health Reform: A Guide for Employers

Updated with information on the Supreme Court health reform decision July 2012 Health Reform: A Guide for Employers Simple answers to health reform s complex issues facing every employer and what you can

Updated with information on the Supreme Court health reform decision July 2012 Health Reform: A Guide for Employers Simple answers to health reform s complex issues facing every employer and what you can

Health Care Reform PPACA. General Assembly Greensboro, NC 2013

Health Care Reform PPACA General Assembly Greensboro, NC 2013 Near-term Provisions 1 These fees apply to both insured and self-insured plans. Additional Coming Changes PPACA Patient Protection and Affordable

Health Care Reform PPACA General Assembly Greensboro, NC 2013 Near-term Provisions 1 These fees apply to both insured and self-insured plans. Additional Coming Changes PPACA Patient Protection and Affordable

Nebraska Health Insurance Exchange Update

Nebraska Health Insurance Exchange Update Overview of the Affordable Care Act and the Federally Facilitated marketplace. September 2014 AFFORDABLE CARE ACT» The Affordable Care Act: Establishes a Health

Nebraska Health Insurance Exchange Update Overview of the Affordable Care Act and the Federally Facilitated marketplace. September 2014 AFFORDABLE CARE ACT» The Affordable Care Act: Establishes a Health

Important Effective Dates for Employers and Health Plans

Brought to you by Sullivan Benefits Important Effective Dates for Employers and Health Plans On March 23, 2010, President Obama signed the health care reform bill, or Affordable Care Act (ACA), into law.

Brought to you by Sullivan Benefits Important Effective Dates for Employers and Health Plans On March 23, 2010, President Obama signed the health care reform bill, or Affordable Care Act (ACA), into law.

Important Effective Dates for Employers and Health Plans

Brought to you by Hipskind Seyfarth Risk Solutions Important Effective Dates for Employers and Health Plans On March 23, 2010, President Obama signed the health care reform bill, or Affordable Care Act

Brought to you by Hipskind Seyfarth Risk Solutions Important Effective Dates for Employers and Health Plans On March 23, 2010, President Obama signed the health care reform bill, or Affordable Care Act

A Consumer s Guide to the Affordable Care Act

A Consumer s Guide to the Affordable Care Act The Affordable Care Act was designed to help make health care affordable for everyone. This guide will help you understand how the ACA affects individuals

A Consumer s Guide to the Affordable Care Act The Affordable Care Act was designed to help make health care affordable for everyone. This guide will help you understand how the ACA affects individuals

Employee Benefits Compliance

Employee Benefits Compliance Pay or Play Delay, Does it Apply and Strategies to Comply Wells Fargo Insurance 2014 Issues and beyond. U.S. citizens and legal residents are required to have "minimum essential

Employee Benefits Compliance Pay or Play Delay, Does it Apply and Strategies to Comply Wells Fargo Insurance 2014 Issues and beyond. U.S. citizens and legal residents are required to have "minimum essential

How To Get A Health Insurance Plan In Texas

Anticipating the Health Insurance Marketplace in Texas HFMA Lone Star Chapter Fall Institute September 16, 2013 1 About Community Health Choice Non-profit Health Maintenance Organization licensed by the

Anticipating the Health Insurance Marketplace in Texas HFMA Lone Star Chapter Fall Institute September 16, 2013 1 About Community Health Choice Non-profit Health Maintenance Organization licensed by the

Health care reform for large businesses

FOR PRODUCERS AND EMPLOYERS Health care reform for large businesses A guide to what you need to know now DECEMBER 2013 CONTENTS 2 Introduction Since 2010 when the Affordable Care Act (ACA) was signed into

FOR PRODUCERS AND EMPLOYERS Health care reform for large businesses A guide to what you need to know now DECEMBER 2013 CONTENTS 2 Introduction Since 2010 when the Affordable Care Act (ACA) was signed into

Connecticut Health Insurance Exchange. June 2012 [SHOP BRIEFING] An overview of the Small Business Health Options Program (SHOP) Exchange

![Connecticut Health Insurance Exchange. June 2012 [SHOP BRIEFING] An overview of the Small Business Health Options Program (SHOP) Exchange](/thumbs/32/15645614.jpg "Connecticut Health Insurance Exchange. June 2012 [SHOP BRIEFING] An overview of the Small Business Health Options Program (SHOP) Exchange") Connecticut Health Insurance Exchange June 2012 [SHOP BRIEFING] An overview of the Small Business Health Options Program (SHOP) Exchange Overview The federal health care reform law directs states to set

Connecticut Health Insurance Exchange June 2012 [SHOP BRIEFING] An overview of the Small Business Health Options Program (SHOP) Exchange Overview The federal health care reform law directs states to set

The Impact on Business

The Impact on Business Affordable Care Act Reform addresses access to coverage not healthcare cost or population health ACA passed in 2010. The Supreme Court upheld ACA in 2012 and President Obama was

The Impact on Business Affordable Care Act Reform addresses access to coverage not healthcare cost or population health ACA passed in 2010. The Supreme Court upheld ACA in 2012 and President Obama was

Exchange 101. August 2013

Exchange 101 August 2013 455430 27517 Penalties for individuals 2017 and beyond: Annual adjustments 2016: Greater of $695 or 2.5% of taxable income 2015: Greater of $325 or 2% of taxable income 2014: Greater

Exchange 101 August 2013 455430 27517 Penalties for individuals 2017 and beyond: Annual adjustments 2016: Greater of $695 or 2.5% of taxable income 2015: Greater of $325 or 2% of taxable income 2014: Greater

Introduction to the New Health Care Laws Michelle Walker, Rocky Mountain Health Plans January 14, 2015

Introduction to the New Health Care Laws Michelle Walker, Rocky Mountain Health Plans January 14, 2015 Agenda Basics of Health Care Reform Changes in Individual Healthcare Coverage Mandates Affordability

Introduction to the New Health Care Laws Michelle Walker, Rocky Mountain Health Plans January 14, 2015 Agenda Basics of Health Care Reform Changes in Individual Healthcare Coverage Mandates Affordability

Parker, Smith & Feek - ACA Update: 2014 November 2013

Affordable Care Act (ACA) Background Core of law is an attempt to reduce # of uninsured Multiple approaches to expanding insurance coverage Requires most in US to have health insurance Creates state-based

Affordable Care Act (ACA) Background Core of law is an attempt to reduce # of uninsured Multiple approaches to expanding insurance coverage Requires most in US to have health insurance Creates state-based

The Large Business Guide to Health Care Law

The Large Business Guide to Health Care Law How the new changes in health care law will affect you and your employees Table of contents Introduction 3 Part I: A general overview of the health care law

The Large Business Guide to Health Care Law How the new changes in health care law will affect you and your employees Table of contents Introduction 3 Part I: A general overview of the health care law

Health Reform Changes: What s New for 2014? New Hampshire Insurance Department September 11, 2013

Health Reform Changes: What s New for 2014? New Hampshire Insurance Department September 11, 2013 1 New Hampshire Insurance Department Presentation Overview What s New in 2014 Key Questions for Individuals

Health Reform Changes: What s New for 2014? New Hampshire Insurance Department September 11, 2013 1 New Hampshire Insurance Department Presentation Overview What s New in 2014 Key Questions for Individuals