Broadband costing and pricing - Approaches and best practices

|

|

|

- Vivien White

- 8 years ago

- Views:

Transcription

1 Broadband costing and pricing - Approaches and best practices AGER, São Tomé 3 February 2015 Pedro Seixas, ITU Expert International Telecommunication Union

2 Agenda Overview situation in Africa Cable landing stations cost modeling Backbone networks The last mile Conclusions 2

3 There have been significant improvements to Africa s Broadband services in recent years Enormous investments have taken place across the value chain, notably in submarine cables and terrestrial backbone These investments have had a dual impact on Internet access services, through lower prices and increased adoption However a number of countries is still underperforming due to policy and regulatory shortfalls This presentation will address the policy issues and regulatory approaches that may enhance improvements in Broadband access services in African countries 3

4 Once a bottleneck, undersea cable contributed to a significant decrease in Internet retail prices Seven major new submarine cable systems have been completed in Sub-Saharan Africa since 2009 Increased availability of bandwidth in coastal regions, and competition between cable operators is leading to a substantial reduction in consumer s internet price: cable connectivity accounts up to 50% of a fixed broadband cost The median monthly charge for an STM-1 circuit (Johannesburg to London) has fallen by more than 40% per year since 2009 Source: accessed in January 2015, Telegeography 4

has fallen by more than 40% per year since 2009 Source: https://manypossibilities.")

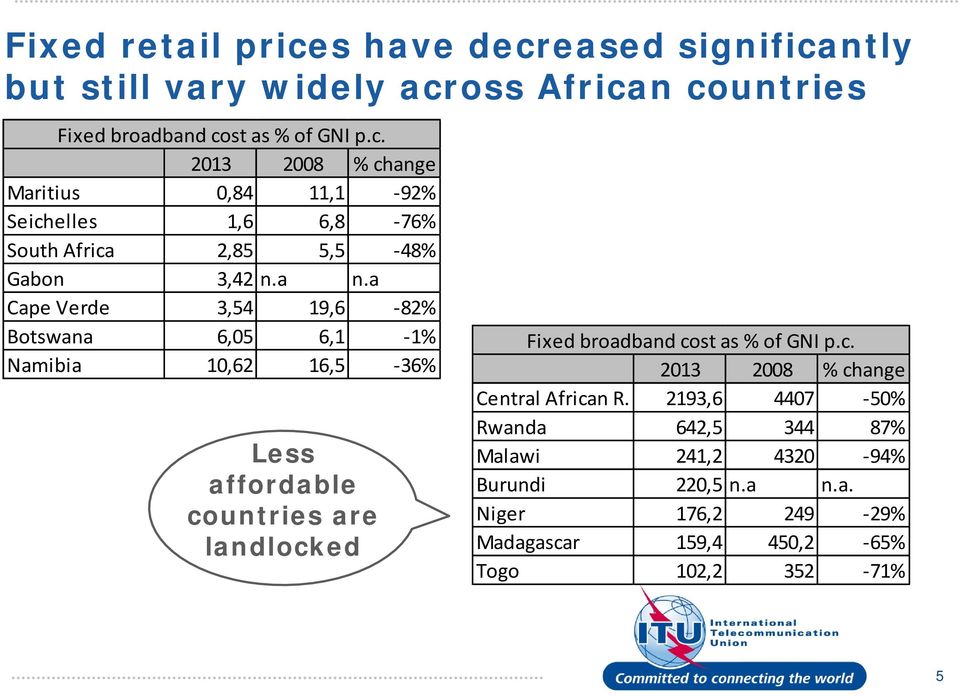

5 Fixed retail prices have decreased significantly but still vary widely across African countries Fixed broadband cost as % of GNI p.c % change Maritius 0,84 11,1-92% Seichelles 1,6 6,8-76% South Africa 2,85 5,5-48% Gabon 3,42 n.a n.a Cape Verde 3,54 19,6-82% Botswana 6,05 6,1-1% Namibia 10,62 16,5-36% Less affordable countries are landlocked Fixed broadband cost as % of GNI p.c % change Central African R. 2193, % Rwanda 642, % Malawi 241, % Burundi 220,5 n.a n.a. Niger 176, % Madagascar 159,4 450,2-65% Togo 102, % 5

6 Investment in capacity has been huge, but a number of obstacles remain in place Submarine Cables USD 3.8 billion invested in recent years Total lit capacity in Sub- Saharan African submarine cable systems increasing by 57% annually between 2007 and 2013 Seven countries have had their first landing station Eleven other countries have an additional landing station Terrestrial Capacity USD 8 billion invested Two coastal countries have no submarine cables, a few others have only one or two 16 landlocked countries in Africa that require crossborder terrestrial capacity to access international connectivity at cable landing stations either than by satellite Evidence that cross-border connections are still limited, resulting in indirect traffic exchange Source: Terabit Consulting submarine-cable-market-industry-report.pdf, accessed January

7 In countries where there will be only one or two cables there may be need for some form of price regulation Forms of price regulation: Price approval the Cable Landing Station (CSL) operator takes the lead Specification of the price the regulator determines Price cap the regulator guides Methods of determining cost-based prices: Cost modelling depends on input data and assumptions Retail minus but in this case what is the retail service? Benchmarking but are the relevant prices published? A price cap based on a cost model is a good solution given the error-margins involved in cost calculation 7

8 What are we pricing? Price of wholesale access to capacity on international submarine cable Expressed as a price per Mbps per month Potentially differentiated by capacity (e.g. E3, STM1) Charge for co-location in the CLS Physical or virtual One-off establishment charges plus recurring rental charges. 8

9 Principles of cost based pricing The CLS operator must recover the costs of: its investment in the international submarine cable the CLS site and building all of the constituent equipment. The costs that are included must be efficientlyincurred (based on best practice techniques and technologies). Prices will recover costs over the lifetime of the assets. 9

10 Simple mechanics of a CLS cost model Take all the relevant costs: Cable costs Site and building costs Equipment costs Indirect operating expenses Cost of capital Estimate annual cost-based wholesale prices for: Capacity services Colocation services Given an assumed level of demand Steps might be simple but are likely to be simply dangerous if the pricing decision is non-strategic that is, left to cost modelling alone 10

11 Undersea cable costs The capital and operating costs relating to the investment in the cable system and the associated CLS Biggest item is the investment in the submarine cable usually $ millions over years in return for IRUs Cost of international cable per 10Gbps (STM64) per annum 10Gbps is the standard capacity unit for international cables typically corresponding to a single wavelength Lower capacities may be derived through demultiplexing 11

12 Site and building costs The capital costs associated with the CLS Costs need to be allocated between the various functions of the CLS, typically on the basis of floor space An annual capital charge (i.e. depreciation expense) Tilted annuity approach 12

13 Equipment costs The capital costs of equipment purchases and associated annual operating costs Some of the capital costs may be included as part of the cable investment cost De-multiplexing equipment costs will depend on the particular capacity services that are to be offered An annual capital charge (i.e. depreciation expense) Tilted annuity approach this allows for the same capital charge each year except tilted to allow for trends in equipment costs. 13

Tilted annuity approach this")

14 Operating expenses Each asset has an annual maintenance cost and some other costs (e.g. power) may be directly attributed. Other operating costs are not directly related to the cable equipment but still form part of the delivery of wholesale capacity services Air-conditioning, security, cleaning. Typical approach is to establish a ratio between capital costs and operational expenditure. 14

15 Illustrative example taken from a ITU CLS training cost model 15

16 Pricing that tries to recover cable and CLS costs as they are incurred is likely to dampen demand below the level assumed Scale ($) Costs Costs are incurred are incurred big chunks in big especially chunks in especially the first year in the first year the first year The main factors that determine the conversion of costs into costbased prices are: The weighted average cost of capital Prices need to The forecasts of market change gradually demand Prices over need the to lifetime change gradually of and smoothly the assets smoothly Time (years) 16

17 Cost of capital Can contribute to a very significant portion of annual expenses Investments in submarine cables are risky, so investors want higher rates of return E.g % Government or donor-funding can result in much lower WACC E.g. 0 5% So the source of funding can substantially affect investment risks, costs and prices. 17

18 Illustrative example taken from a ITU CLS training cost model 18

19 Why might cost model outcomes without more be poor pricing decisions? Specially in the first year of operation of a country s submarine cable demand is very hard to forecast not to say impossible Aiming for full cost recovery during these initial years will keep prices high and suppress demand Low demand will keep unit costs high What actions can the CLS operator or the Government take to break this vicious circle? 19

20 Government as a consumer (without regulating) Government ministries are potentially a very large consumer of broadband internet access Government can therefore help stimulate retail demand for wholesale cable capacity by increasing its demand (and its spending) on broadband connectivity for all Ministry / Department offices Aggregating the demand of multiple ministries might also help Retail, not wholesale This obviously comes at a cost Higher bills for telecoms services and perhaps more IT equipment But all retail consumers potentially benefit from lower prices 20

21 CLS operator ROCE objectives Return on capital employed EBIT / Capital employed Maximum may be set by the regulator in the form of a regulated WACC CLS operator can stimulate demand by accepting a very low or negative ROCE during the early years Reduces value of annual capital charges and thus unit costs Private versus PPP ownership 21

22 Depending on legal provisions, a essential facility status or dominance designation within a CLS market may be necessary In Singapore the regulator added the undersea cable landing station to the Reference Interconnection Offer (RIO) of SingTel. Prices for co-location access and connection to submarine cables are set on a cost-orientated basis using a forward looking economic cost (FLEC) In India the regulatory authority capped the international connectivity prices (cost based) and required dominant players to elaborate a Reference Interconnection Offer (RIA). Mauritius regulator, ICTA, in 2006 set the price of IPLCs on a costoriented basis. Regulation is applied to both the cable landing station and the submarine cable. The charge for IPLCs was determined on the basis of a fully allocated historic costing methodology with an allowance for a reasonable rate of return. Source: Regulator s websites and The regulation of undersea cables and landing stations accessed at undersea-cables.pdf January

23 Effects of undersea cables will be stronger when accompanied by terrestrial networks Weak competition at the national level to link population centres to the international gateways Mobile operators networks in the region have been built for their own use, rather than for resale and aiming at national coverage purposes Only a few countries (Kenya, Nigeria, South Africa, Zambia and Zimbabwe) can be said to have some level of competition due to the presence of multiple players. Cross border networks are rare Regional approaches and solutions based on political cooperation are needed to address the problem of access faced by landlocked countries 23

24 Private sector initiatives such as Liquid Telecom show the relevance of access to other s fiber networks Liquid (founded by former Econet shareholders) has built through acquisition and construction Africa s largest single fibre network (17,000km) including Uganda, Kenya, Rwanda, Zambia, Zimbabwe, Botswana, DRC, Lesotho and South Africa Liquid has so far spent $350m on its internet network Though mainly a wholesale business, Liquid also has 50,000 homes as customers in Zambia and Zimbabwe Source: The Economist, Cabling Africa s interior. Many rivers to cross, July 5 th 2014, printed edition 24

25 Even when the state holds a substantial stake in the incumbent regulatory barriers should be removed Landlocked countries of which there are 16 in the region depend on terrestrial links and access to cables for connectivity The Communications Regulators Association of Southern Africa (CRASA) is spearheading the effort, aimed at giving all countries in the Southern African region equal access to the cables. Crasa s legal and policy committee wants the region s landlocked countries to have access to the region s undersea cables at the same price as countries along the shore. Source: accessed January

26 Broadband services development in Africa will depend a lot more on mobile In Africa copper legacy networks are small compared to developed countries, South Africa maybe the exception Last mile access will probably depend on wireless networks which need more investment to achieve higher levels of service (reliability, higher speeds) so competition among mobile operators can lower prices An open access policy for the backbone and backhaul networks may allow MNO s to increase coverage and the quality of the network by redistribution of the investment The emergence of bundles (data with voice and sms) will increasingly turn more difficult to evaluate and regulate prices at retail level 26

27 Conclusions Liberalization of gateways and national backbones Strategic pricing of connectivity: Pricing based on recovery over the long term to facilitate early take-up Cost and time of rights of way access Sector-specific taxes Regulatory certainty Facilitate infrastructure sharing Public private partnerships Retain ex-ante cost-based regulation for broadband infrastructure access 27

28 Obrigado Thank you Merci Gracias 28

Corporate Overview Creating Business Advantage

Corporate Overview Creating Business Advantage 14 April 2013 Agenda The power of the group Our achievements Quick facts African regulatory environment Portfolio of offerings Creating value in Africa African

Corporate Overview Creating Business Advantage 14 April 2013 Agenda The power of the group Our achievements Quick facts African regulatory environment Portfolio of offerings Creating value in Africa African

Bridging the African Internet

Bridging the African Internet Introduction Mike Silber Head of Legal and Commercial Liquid Telecom Board member ICANN.za Domain Name Authority TENET ISPA (South Africa) Management Committee Bridging the

Bridging the African Internet Introduction Mike Silber Head of Legal and Commercial Liquid Telecom Board member ICANN.za Domain Name Authority TENET ISPA (South Africa) Management Committee Bridging the

Opening up the bandwidth bottleneck in Africa. Martin Mutiiria, Director, Sales, Africa, WIOCC

Opening up the bandwidth bottleneck in Africa Martin Mutiiria, Director, Sales, Africa, WIOCC Martin Mutiiria Director, Sales - Africa Opening up the bandwidth bottleneck in Africa Africa Submarine Cables

Opening up the bandwidth bottleneck in Africa Martin Mutiiria, Director, Sales, Africa, WIOCC Martin Mutiiria Director, Sales - Africa Opening up the bandwidth bottleneck in Africa Africa Submarine Cables

NEPAD ICT BROADBAND INFRASTRUCTURE PROGRAMME Part of the Programme for Infrastructure Development in Africa (PIDA)

") NEPAD ICT BROADBAND INFRASTRUCTURE PROGRAMME Part of the Programme for Infrastructure Development in Africa (PIDA) Presentation to the Open Access Forum Tunis, November 12, 2010 Dr. Edmund Katiti Policy

NEPAD ICT BROADBAND INFRASTRUCTURE PROGRAMME Part of the Programme for Infrastructure Development in Africa (PIDA) Presentation to the Open Access Forum Tunis, November 12, 2010 Dr. Edmund Katiti Policy

International Bandwidth Trends in Africa What Has (and Hasn t) Changed in the Past Five Years

Changed in the Past Five Years") International Bandwidth Trends in Africa What Has (and Hasn t) Changed in the Past Five Years Patrick Christian August 27, 2015 Let s Start with the Global Picture Inter-Regional Internet Bandwidth, 2015

International Bandwidth Trends in Africa What Has (and Hasn t) Changed in the Past Five Years Patrick Christian August 27, 2015 Let s Start with the Global Picture Inter-Regional Internet Bandwidth, 2015

International Bandwidth

AGENDA Definition Implementation Usage of international bandwidth Definition We mean by International Bandwidth the maximum quantity of data transmission (Rate) from a country to the rest of the world.

AGENDA Definition Implementation Usage of international bandwidth Definition We mean by International Bandwidth the maximum quantity of data transmission (Rate) from a country to the rest of the world.

Lifting barriers to Internet development in Africa: suggestions for improving connectivity

. Report for the Internet Society Lifting barriers to Internet development in Africa: suggestions for improving connectivity May 2013 Robert Schumann, Michael Kende Ref: 35729-502d Contents Executive summary

. Report for the Internet Society Lifting barriers to Internet development in Africa: suggestions for improving connectivity May 2013 Robert Schumann, Michael Kende Ref: 35729-502d Contents Executive summary

Regional Interconnection: Presenting the Business Case for African Operators. Densu Richard Ag. Executive, MTN Business rdensu@mtn.com.

Regional Interconnection: Presenting the Business Case for African Operators Densu Richard Ag. Executive, MTN Business rdensu@mtn.com.gh Content About MTN/MTN Business The Benefits of Regional Interconnection

Regional Interconnection: Presenting the Business Case for African Operators Densu Richard Ag. Executive, MTN Business rdensu@mtn.com.gh Content About MTN/MTN Business The Benefits of Regional Interconnection

East African Cable Showcase: The Bandwidth Revolution in Eastern & Southern Africa. Ryan Sher COO, WIOCC

East African Cable Showcase: The Bandwidth Revolution in Eastern & Southern Africa Ryan Sher COO, WIOCC Presenter Profile As COO, Ryan is responsible for developing and managing all WIOCC product offerings,

East African Cable Showcase: The Bandwidth Revolution in Eastern & Southern Africa Ryan Sher COO, WIOCC Presenter Profile As COO, Ryan is responsible for developing and managing all WIOCC product offerings,

Opportunities Availed by Increased Bandwidth Capacity in Africa. James Wekesa Chief Commercial Officer

Opportunities Availed by Increased Bandwidth Capacity in Africa 1 James Wekesa Chief Commercial Officer Presentation Agenda Broadband in Africa.Now Broadband Access Enablers The Power of Broadband, from

Opportunities Availed by Increased Bandwidth Capacity in Africa 1 James Wekesa Chief Commercial Officer Presentation Agenda Broadband in Africa.Now Broadband Access Enablers The Power of Broadband, from

Unlocking Broadband for All:

Unlocking Broadband for All: Infrastructure Sharing for Better Connectivity SADC/CRASA Stakeholder Validation Workshop May 20-21st 2015 Infrastructure Sharing - A Key Strategy for Meeting Universal Access

Unlocking Broadband for All: Infrastructure Sharing for Better Connectivity SADC/CRASA Stakeholder Validation Workshop May 20-21st 2015 Infrastructure Sharing - A Key Strategy for Meeting Universal Access

Michuki Mwangi! Regional Development Manager - Africa! ISOC! European Peering Forum (EPF) 7! Malta! 17 19 Sept 2012!

7! Malta! 17 19 Sept 2012!") Michuki Mwangi! Regional Development Manager - Africa! ISOC! European Peering Forum (EPF) 7! Malta! 17 19 Sept 2012! Agenda! African Fiber Infrastructure! Status of Peering in Africa! The African Peering

Michuki Mwangi! Regional Development Manager - Africa! ISOC! European Peering Forum (EPF) 7! Malta! 17 19 Sept 2012! Agenda! African Fiber Infrastructure! Status of Peering in Africa! The African Peering

List of Figures Analysis Executive Summary 1. International Call Volumes and Growth Rates, 1994-2014 2. Compounded Annual Traffic Growth Rate by

TeleGeography Report Analysis Executive Summary Traffic Analysis Supplementary Figures Traffic by Region Traffic by Country Prices and Revenues Supplementary Figures Retail Rates Wholesale Rates Interconnection

TeleGeography Report Analysis Executive Summary Traffic Analysis Supplementary Figures Traffic by Region Traffic by Country Prices and Revenues Supplementary Figures Retail Rates Wholesale Rates Interconnection

AIO Life Seminar Abidjan - Côte d Ivoire

AIO Life Seminar Abidjan - Côte d Ivoire Life Insurance Market Survey of Selected African Countries Bertus Thomas Africa Committee of the Actuarial Society of South Africa Agenda SECTION 1 SURVEY OBJECTIVE

AIO Life Seminar Abidjan - Côte d Ivoire Life Insurance Market Survey of Selected African Countries Bertus Thomas Africa Committee of the Actuarial Society of South Africa Agenda SECTION 1 SURVEY OBJECTIVE

Financing Education for All in Sub Saharan Africa: Progress and Prospects

Financing Education for All in Sub Saharan Africa: Progress and Prospects Albert Motivans Education for All Working Group Paris, 3 February 211 1 Improving the coverage and quality of education finance

Financing Education for All in Sub Saharan Africa: Progress and Prospects Albert Motivans Education for All Working Group Paris, 3 February 211 1 Improving the coverage and quality of education finance

Distance to frontier

Doing Business 2013 Fact Sheet: Sub-Saharan Africa Of the 50 economies making the most improvement in business regulation for domestic firms since 2005, 17 are in Sub-Saharan Africa. From June 2011 to

Doing Business 2013 Fact Sheet: Sub-Saharan Africa Of the 50 economies making the most improvement in business regulation for domestic firms since 2005, 17 are in Sub-Saharan Africa. From June 2011 to

The Socio-Economic Impact of Broadband in sub-saharan Africa: The Satellite Advantage

The Socio-Economic Impact of Broadband in sub-saharan Africa: The Satellite Advantage The Socio-Economic Impact of Broadband in sub-saharan Africa: The Satellite Advantage By the Commonwealth Telecommunications

The Socio-Economic Impact of Broadband in sub-saharan Africa: The Satellite Advantage The Socio-Economic Impact of Broadband in sub-saharan Africa: The Satellite Advantage By the Commonwealth Telecommunications

THE FUTURE OF BROADBAND & IMPACT ON BUSINESS

THE FUTURE OF BROADBAND & IMPACT ON BUSINESS 1 Broadband Commission Letter to G20 June 2012 Like water, roads, rail and electricity before it, broadband is of fundamental importance to social and economic

THE FUTURE OF BROADBAND & IMPACT ON BUSINESS 1 Broadband Commission Letter to G20 June 2012 Like water, roads, rail and electricity before it, broadband is of fundamental importance to social and economic

Essential facilities and anticompetitive

Essential facilities and anticompetitive practices Rohan Samarajiva 29 September 2013 Taungoo, Myanmar This work was carried out with the aid of a grant from the International Development Research Centre,

Essential facilities and anticompetitive practices Rohan Samarajiva 29 September 2013 Taungoo, Myanmar This work was carried out with the aid of a grant from the International Development Research Centre,

AFFORDABLE INTERNET IN GHANA: THE STATUS QUO AND THE PATH AHEAD

AFFORDABLE INTERNET IN GHANA: THE STATUS QUO AND THE PATH AHEAD Ghana, one of sub-saharan Africa s most influential nations, has prioritized ICT investment in recent years. This case study which is intended

AFFORDABLE INTERNET IN GHANA: THE STATUS QUO AND THE PATH AHEAD Ghana, one of sub-saharan Africa s most influential nations, has prioritized ICT investment in recent years. This case study which is intended

Colocation. Scalable Solutions for a Shared IT Infrastructure. Enterprise. Colocation

Scalable Solutions for a Shared IT Infrastructure Global and domestic competition, rising real estate and power costs, and shrinking IT budgets are causing today s businesses to seek alternatives to building

Scalable Solutions for a Shared IT Infrastructure Global and domestic competition, rising real estate and power costs, and shrinking IT budgets are causing today s businesses to seek alternatives to building

MNS Viewpoint: LTE EVOLUTION IN AFRICA 1. Introduction

MNS Viewpoint: LTE EVOLUTION IN AFRICA 1. Introduction Wireless communications have evolved rapidly since the emergence of 2G networks. 4G technology (also called LTE), enables to answer the new data market

MNS Viewpoint: LTE EVOLUTION IN AFRICA 1. Introduction Wireless communications have evolved rapidly since the emergence of 2G networks. 4G technology (also called LTE), enables to answer the new data market

Company presentation January 2013

Company presentation January 2013 Gilat Satcom HQ in Israel, Main African subsidiary in Nigeria 3 international satellite teleports, 14 Hubs/PoPs in Africa, 2 PoPs in Europe, 2 Fibers Managing over 2.4Gb

Company presentation January 2013 Gilat Satcom HQ in Israel, Main African subsidiary in Nigeria 3 international satellite teleports, 14 Hubs/PoPs in Africa, 2 PoPs in Europe, 2 Fibers Managing over 2.4Gb

Colocation. Scalable Solutions for Shared IT Infrastructure. Enterprise. Colocation

Scalable Solutions for Shared IT Infrastructure Global competition, rising real estate and power costs, and shrinking IT budgets are causing today s businesses to seek alternatives to building their own

Scalable Solutions for Shared IT Infrastructure Global competition, rising real estate and power costs, and shrinking IT budgets are causing today s businesses to seek alternatives to building their own

A Credit Bureau Data Comparison - SA versus Africa The trip through the jungle is easy IF you have the data - question: do we have it?

A Credit Bureau Data Comparison - SA versus Africa The trip through the jungle is easy IF you have the data - question: do we have it? presented by Frank Lenisa Director, Compuscan Agenda Regula+on 144

A Credit Bureau Data Comparison - SA versus Africa The trip through the jungle is easy IF you have the data - question: do we have it? presented by Frank Lenisa Director, Compuscan Agenda Regula+on 144

Building regional connectivity: Insights from research for policy

Building regional connectivity: Insights from research for policy Rohan Samarajiva United Nations ESCAP Committee on ICT 3 rd Session 20 22 November 2012 This work was carried out with the aid of a grant

Building regional connectivity: Insights from research for policy Rohan Samarajiva United Nations ESCAP Committee on ICT 3 rd Session 20 22 November 2012 This work was carried out with the aid of a grant

Regional Internet Carrier Policy and Regulation Best Practice. Cross Border and Interconnection Policies

Regional Internet Carrier Policy and Regulation Best Practice Cross Border and Interconnection Policies The Vision/Goal Outline the key national and regional policy changes needed to address the current

Regional Internet Carrier Policy and Regulation Best Practice Cross Border and Interconnection Policies The Vision/Goal Outline the key national and regional policy changes needed to address the current

Ministry of Technology, Communication and Innovation

Ministry of Technology, Communication and Innovation Expression of Interest for a Market Sounding Exercise For the implementation of a Third International gateway through the installation of a new submarine

Ministry of Technology, Communication and Innovation Expression of Interest for a Market Sounding Exercise For the implementation of a Third International gateway through the installation of a new submarine

International Market Trends. Presentation by TeleGeography. January 15, 2012

International Market Trends Presentation by TeleGeography January 15, 2012 TeleGeography Research Areas International voice traffic Internet backbone capacity, traffic, and IP transit pricing Long-haul

International Market Trends Presentation by TeleGeography January 15, 2012 TeleGeography Research Areas International voice traffic Internet backbone capacity, traffic, and IP transit pricing Long-haul

Enabling e-commerce: recent trends in broadband deployment and uptake

WTO Workshop on E-Commerce, Development and Small and Medium-sized Enterprises (SMEs) Geneva, 8-9 April 2013 Enabling e-commerce: recent trends in broadband deployment and uptake Susan Teltscher Head,

WTO Workshop on E-Commerce, Development and Small and Medium-sized Enterprises (SMEs) Geneva, 8-9 April 2013 Enabling e-commerce: recent trends in broadband deployment and uptake Susan Teltscher Head,

International Carriers

International Carriers Mauritel: ACE and IP services developments December 2013 Agenda 1 2 ACE background ACE for Mauritel ACE 17 000 km long 1 express landing in France, Senegal, Ivory Coast and Sao Tome

International Carriers Mauritel: ACE and IP services developments December 2013 Agenda 1 2 ACE background ACE for Mauritel ACE 17 000 km long 1 express landing in France, Senegal, Ivory Coast and Sao Tome

IMPLICATIONS OF OVERLAPPING MEMBERSHIP ON THE EXPECTED GAINS FROM ACCELERATED PROGRAM FOR ECONOMIC INTEGRATION (APEI)

") IMPLICATIONS OF OVERLAPPING MEMBERSHIP ON THE EXPECTED GAINS FROM ACCELERATED PROGRAM FOR ECONOMIC INTEGRATION (APEI) ABSTRACT In September 2012, five like-minded and reform oriented countries namely Malawi,

IMPLICATIONS OF OVERLAPPING MEMBERSHIP ON THE EXPECTED GAINS FROM ACCELERATED PROGRAM FOR ECONOMIC INTEGRATION (APEI) ABSTRACT In September 2012, five like-minded and reform oriented countries namely Malawi,

Appendix A: Country Case Study: Cambodia

Antelope Consulting FINAL, JULY 2001 DFID Internet Costs Study Appendix A: Country Case Study: Cambodia Executive Summary Cambodia is a very poor country, emerging from a civil war. The lack of fixed

Antelope Consulting FINAL, JULY 2001 DFID Internet Costs Study Appendix A: Country Case Study: Cambodia Executive Summary Cambodia is a very poor country, emerging from a civil war. The lack of fixed

Pensions Core Course Mark Dorfman The World Bank. March 7, 2014

PENSION PATTERNS & REFORM CHALLENGES IN SUB-SAHARAN AFRICA Pensions Core Course Mark Dorfman The World Bank Slide 1 Organization 1. Design summary 2. Challenges 3. Design reform principles 4. A process

PENSION PATTERNS & REFORM CHALLENGES IN SUB-SAHARAN AFRICA Pensions Core Course Mark Dorfman The World Bank Slide 1 Organization 1. Design summary 2. Challenges 3. Design reform principles 4. A process

International Submarine Cables and Hi-Speed Broadband in Australia and New Zealand

International Submarine Cables and Hi-Speed Broadband in Australia and New Zealand Ross Pfeffer Since the birth of the internet, Australasian users Whitepaper First published: April 2010 have depended

International Submarine Cables and Hi-Speed Broadband in Australia and New Zealand Ross Pfeffer Since the birth of the internet, Australasian users Whitepaper First published: April 2010 have depended

JAMII TELECOMMUNICATIONS LTD COMPANYPROFILE

YOUR TRUSTED BUSINESS PARTN E R JAMII TELECOMMUNICATIONS LTD COMPANYPROFILE Table of Contents 1. Introduction 2. Our Vision 3. Our Mission 4. Our Core Values 5. Our Customer Service Vision 6. The Company

YOUR TRUSTED BUSINESS PARTN E R JAMII TELECOMMUNICATIONS LTD COMPANYPROFILE Table of Contents 1. Introduction 2. Our Vision 3. Our Mission 4. Our Core Values 5. Our Customer Service Vision 6. The Company

Consumers benefit from lower mobile

Consumers benefit from lower mobile termination rates Mobile termination rates no longer pose an obstacle to competition. Cell C and Telkom Mobile have continued to place pressure on MTN and Vodacom to

Consumers benefit from lower mobile termination rates Mobile termination rates no longer pose an obstacle to competition. Cell C and Telkom Mobile have continued to place pressure on MTN and Vodacom to

country profiles WHO regions

country profiles WHO regions AFR AMR EMR EUR SEAR WPR Algeria Total population: 37 63 aged years and older (+): 73% in urban areas: 66% Income group (World Bank): Upper middle income 196 196 197 197 198

country profiles WHO regions AFR AMR EMR EUR SEAR WPR Algeria Total population: 37 63 aged years and older (+): 73% in urban areas: 66% Income group (World Bank): Upper middle income 196 196 197 197 198

T-Systems Singapore. IIC Singapore TRPC Forum. International and Domestic Broadband Connectivity in Singapore -Connectivity Cost and Competition-

T-Systems Singapore IIC Singapore TRPC Forum -Connectivity Cost and Competition- Singapore, 01. April 2014 Contents 1. Deutsche Telekom/T-Systems 2. Disclaimer 3. Demand 4. International Connectivity 5.

T-Systems Singapore IIC Singapore TRPC Forum -Connectivity Cost and Competition- Singapore, 01. April 2014 Contents 1. Deutsche Telekom/T-Systems 2. Disclaimer 3. Demand 4. International Connectivity 5.

Quote Reference. Underwriting Terms. Premium Currency USD. Payment Frequency. Quotation Validity BUPA AFRICA PROPOSAL.

Quote Reference Family Quote 2013 Underwriting Terms BUPA AFRICA PROPOSAL Full Medical Underwriting and/or Continuous PreviousMedical Exclusions Premium Currency USD Payment Frequency One annual payment

Quote Reference Family Quote 2013 Underwriting Terms BUPA AFRICA PROPOSAL Full Medical Underwriting and/or Continuous PreviousMedical Exclusions Premium Currency USD Payment Frequency One annual payment

Frost & Sullivan African Operations

Frost & Sullivan African Operations Research Service Schedules Current, historical and planning 2010 Information & Technology We Accelerate Growth 1 Information & Technology 2010 Planned Research Titles

Frost & Sullivan African Operations Research Service Schedules Current, historical and planning 2010 Information & Technology We Accelerate Growth 1 Information & Technology 2010 Planned Research Titles

DEFINITION OF THE CHILD: THE INTERNATIONAL/REGIONAL LEGAL FRAMEWORK. The African Charter on the Rights and Welfare of the Child, 1990

DEFINITION OF THE CHILD: THE INTERNATIONAL/REGIONAL LEGAL FRAMEWORK Article 2: Definition of a Child The African Charter on the Rights and Welfare of the Child, 1990 For tile purposes of this Charter.

DEFINITION OF THE CHILD: THE INTERNATIONAL/REGIONAL LEGAL FRAMEWORK Article 2: Definition of a Child The African Charter on the Rights and Welfare of the Child, 1990 For tile purposes of this Charter.

Feasibility Study for Alternative Yukon Fibre Optic Link. Summary Report

Feasibility Study for Alternative Yukon Fibre Optic Link Summary Report February, 2014 Contents 1 Executive Summary...3 2 Project Background...3 3 Situation...4 3.1 Telecommunications Market... 4 3.1 Service

Feasibility Study for Alternative Yukon Fibre Optic Link Summary Report February, 2014 Contents 1 Executive Summary...3 2 Project Background...3 3 Situation...4 3.1 Telecommunications Market... 4 3.1 Service

Higher Education Financing

Higher Education Financing Trends and Possibilities in SADC Outline The HE Financing Context Note on HE and Development HE Funding Key Questions Common Funding Themes Good Practices Possible Lessons Way

Higher Education Financing Trends and Possibilities in SADC Outline The HE Financing Context Note on HE and Development HE Funding Key Questions Common Funding Themes Good Practices Possible Lessons Way

Botswana - Telecoms, Mobile and Broadband - Statistics and Analyses

Brochure More information from http://www.researchandmarkets.com/reports/1205940/ Botswana - Telecoms, Mobile and Broadband - Statistics and Analyses Description: Regulator issues consultation on migration

Brochure More information from http://www.researchandmarkets.com/reports/1205940/ Botswana - Telecoms, Mobile and Broadband - Statistics and Analyses Description: Regulator issues consultation on migration

TRANSITIONING PCCW David Prince, Group CFO. CLSA Investors Forum Hong Kong - 15 May, 2001

TRANSITIONING PCCW David Prince, Group CFO CLSA Investors Forum Hong Kong - 15 May, 2001 FORWARD LOOKING STATEMENTS This presentation contains forward-looking statements that involve risks and uncertainties.

TRANSITIONING PCCW David Prince, Group CFO CLSA Investors Forum Hong Kong - 15 May, 2001 FORWARD LOOKING STATEMENTS This presentation contains forward-looking statements that involve risks and uncertainties.

SEACOM Infrastructure, Private Line & Colocation November 2013

SEACOM Infrastructure, Private Line & Colocation November 2013 The Agenda is... SEACOM Overview Network Infrastructure Private Line Services Colocation Services Company Overview Launched 23 July 2009 privately

SEACOM Infrastructure, Private Line & Colocation November 2013 The Agenda is... SEACOM Overview Network Infrastructure Private Line Services Colocation Services Company Overview Launched 23 July 2009 privately

TELECOM REGULATORY AUTHORITY OF INDIA

TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART III, SECTION 4 TELECOM REGULATORY AUTHORITY OF INDIA NOTIFICATION New Delhi, the 21 st December, 2012 THE INTERNATIONAL TELECOMMUNICATION CABLE

TO BE PUBLISHED IN THE GAZETTE OF INDIA, EXTRAORDINARY, PART III, SECTION 4 TELECOM REGULATORY AUTHORITY OF INDIA NOTIFICATION New Delhi, the 21 st December, 2012 THE INTERNATIONAL TELECOMMUNICATION CABLE

Sub-Saharan Africa Mobile Observatory 2012

Sub-Saharan Africa Mobile Observatory 2012 13 November 2012 Prepared by: and Sub-Saharan Africa Mobile Observatory 2012 2 Contents Executive Summary... 3 1 Introduction... 8 1.1 SSA comprises a set of

Sub-Saharan Africa Mobile Observatory 2012 13 November 2012 Prepared by: and Sub-Saharan Africa Mobile Observatory 2012 2 Contents Executive Summary... 3 1 Introduction... 8 1.1 SSA comprises a set of

SEACOM IP & MPLS Services. November 2013

SEACOM IP & MPLS Services November 2013 The Agenda is... SEACOM Overview IP Transit Services Ethernet Service Remote Peering Service Company Overview Launched 23 July 2009 privately funded and over three

SEACOM IP & MPLS Services November 2013 The Agenda is... SEACOM Overview IP Transit Services Ethernet Service Remote Peering Service Company Overview Launched 23 July 2009 privately funded and over three

Data Services Portfolio

Data Services Portfolio Carrier Relations & Wholesale Department Local Services enet ewan Microwave National MPLS Local Leased Circuits Extended Services IP Transit International MPLS International Private

Data Services Portfolio Carrier Relations & Wholesale Department Local Services enet ewan Microwave National MPLS Local Leased Circuits Extended Services IP Transit International MPLS International Private

Interconnec(on, Bandwidth, Complexity and Costs. Gaurab Raj Upadhaya gaurab@llnw.com

Interconnec(on, Bandwidth, Complexity and Costs Gaurab Raj Upadhaya gaurab@llnw.com About Myself Director, Interna(onal Networking at Limelight Networks Execu(ve Council Member APNIC Previously (2002-2010),

Interconnec(on, Bandwidth, Complexity and Costs Gaurab Raj Upadhaya gaurab@llnw.com About Myself Director, Interna(onal Networking at Limelight Networks Execu(ve Council Member APNIC Previously (2002-2010),

ACTO Response to TRAI Consultation paper No 09/2010, 10th June, 2010 on National Broadband Plan (NBP) SUMMARY

SUMMARY") ACTO Response to TRAI Consultation paper No 09/2010, 10th June, 2010 on National Broadband Plan (NBP) SUMMARY The Association of Competitive Telecommunications Operators (ACTO) is thankful to TRAI for

ACTO Response to TRAI Consultation paper No 09/2010, 10th June, 2010 on National Broadband Plan (NBP) SUMMARY The Association of Competitive Telecommunications Operators (ACTO) is thankful to TRAI for

Post, Broadcasting & Telecommunications Annual Market Review 2012/2013

Post, Broadcasting & Telecommunications Annual Market Review 2012/2013 Legal Disclaimer 2 Contents 5 10 14 18 24 28 32 35 36 3 Overview Godfrey Mutabazi Executive Director This review presents the performance

Post, Broadcasting & Telecommunications Annual Market Review 2012/2013 Legal Disclaimer 2 Contents 5 10 14 18 24 28 32 35 36 3 Overview Godfrey Mutabazi Executive Director This review presents the performance

THE ELEMENTS OF COST FOR LEASED LINES

THE ELEMENTS OF COST FOR LEASED LINES Talk to EC Sector Inquiry on the Competitive Provision of Leased Lines in EU Telecoms Market, Brussels 22 September, 2000 1. Definitions Leased lines services can

THE ELEMENTS OF COST FOR LEASED LINES Talk to EC Sector Inquiry on the Competitive Provision of Leased Lines in EU Telecoms Market, Brussels 22 September, 2000 1. Definitions Leased lines services can

A review of wholesale leased line pricing in the Bailiwick of Guernsey

A review of wholesale leased line pricing in the Bailiwick of Guernsey A REPORT PREPARED FOR THE OFFICE OF UTILITY REGULATION January 2007 Frontier Economics Ltd, London. i Frontier Economics January 2007

A review of wholesale leased line pricing in the Bailiwick of Guernsey A REPORT PREPARED FOR THE OFFICE OF UTILITY REGULATION January 2007 Frontier Economics Ltd, London. i Frontier Economics January 2007

How the Internet Works

How the Internet Works Kyle Spencer, June 2014 Director, Uganda Internet exchange Point Technology for Development Specialist, UNICEF E-mail: kyle@stormzero.com Agenda This talk will take approximately

How the Internet Works Kyle Spencer, June 2014 Director, Uganda Internet exchange Point Technology for Development Specialist, UNICEF E-mail: kyle@stormzero.com Agenda This talk will take approximately

Gender and ICT issues in Africa

+ Gender and ICT issues in Africa + Trends in ICTs in Africa 2010 Big growth in Internet, HUGE growth in mobile (cellular subscribers) ICT use 2000 2008 increase Internet users 3 M. 32M 10 times Cellular

+ Gender and ICT issues in Africa + Trends in ICTs in Africa 2010 Big growth in Internet, HUGE growth in mobile (cellular subscribers) ICT use 2000 2008 increase Internet users 3 M. 32M 10 times Cellular

i) Minimum technology limit bandwidth to be offered in the following areas will be: Pricing will be benchmarked against metro prices in New Zealand

Minimum technology limit bandwidth to be offered in the following areas will be: Pricing will be benchmarked against metro prices in New Zealand") Bay of Plenty Broadband Business Case Study Summary of Conclusions from the Deliverables We propose to take you through the following conclusions from each of the deliverables. This will enable us to identify

Bay of Plenty Broadband Business Case Study Summary of Conclusions from the Deliverables We propose to take you through the following conclusions from each of the deliverables. This will enable us to identify

Global Fuel Economy Initiative Africa Auto Club Event Discussion and Background Paper Venue TBA. Draft not for circulation

Global Fuel Economy Initiative Africa Auto Club Event Discussion and Background Paper Venue TBA Draft not for circulation Launched on March 4, 2009 by the United Nations Environment Programme (UNEP), the

Global Fuel Economy Initiative Africa Auto Club Event Discussion and Background Paper Venue TBA Draft not for circulation Launched on March 4, 2009 by the United Nations Environment Programme (UNEP), the

Internet Services- How to make the Affordable. John Walubengo Ag. Director, ICT Services Multimedia University College.

Internet Services- How to make the Affordable John Walubengo Ag. Director, ICT Services Multimedia University College. 1 Summary Introduction. Affordability. Methodology. Stakeholder Analysis. Possible

Internet Services- How to make the Affordable John Walubengo Ag. Director, ICT Services Multimedia University College. 1 Summary Introduction. Affordability. Methodology. Stakeholder Analysis. Possible

The Africa Infrastructure

AIDI May 2016 www.afdb.org Chief Economist Complex Table of Contents 1. Introduction and Background 1. Introduction and Background 2. The AIDI 2016 Highlights 3. Main Results 4. Conclusions References

AIDI May 2016 www.afdb.org Chief Economist Complex Table of Contents 1. Introduction and Background 1. Introduction and Background 2. The AIDI 2016 Highlights 3. Main Results 4. Conclusions References

Access network costing A REPORT PREPARED FOR VODAFONE GROUP. June 2011. Frontier Economics Ltd, London.

Access network costing A REPORT PREPARED FOR VODAFONE GROUP June 2011 Frontier Economics Ltd, London. Confidential June 2011 Frontier Economics i Access network costing 1 Introduction and summary 4 2

Access network costing A REPORT PREPARED FOR VODAFONE GROUP June 2011 Frontier Economics Ltd, London. Confidential June 2011 Frontier Economics i Access network costing 1 Introduction and summary 4 2

Convergence: challenges from the perspective of regulation

Convergence: challenges from the perspective of regulation Remko Bos Director department of Markets Independent Post and Telecommunications Authority (OPTA), The Netherlands EETT s 4th International Conference:

Convergence: challenges from the perspective of regulation Remko Bos Director department of Markets Independent Post and Telecommunications Authority (OPTA), The Netherlands EETT s 4th International Conference:

INTERNET CONNECTIVITY

Regulatory and market environment STUDY ON INTERNATIONAL INTERNET CONNECTIVITY IN SUB-SAHARAN AFRICA m a r c h 2 0 1 3 Telecommunication Development Sector Study on international Internet connectivity

Regulatory and market environment STUDY ON INTERNATIONAL INTERNET CONNECTIVITY IN SUB-SAHARAN AFRICA m a r c h 2 0 1 3 Telecommunication Development Sector Study on international Internet connectivity

UNFCCC initiatives: CDM and DNA Help Desks, the CDM Loan Scheme, Regional Collaboration Centres

UNFCCC initiatives: CDM and DNA Help Desks, the CDM Loan Scheme, Regional Collaboration Centres Africa Carbon Forum 03 July 2013 - Abidjan, Côte d Ivoire Ms. Flordeliza Andres Programme Officer, UNFCCC

UNFCCC initiatives: CDM and DNA Help Desks, the CDM Loan Scheme, Regional Collaboration Centres Africa Carbon Forum 03 July 2013 - Abidjan, Côte d Ivoire Ms. Flordeliza Andres Programme Officer, UNFCCC

International Wholesale: Increasingly regional, on the brink of change

International Wholesale: Increasingly regional, on the brink of change The wholesale connectivity business, once dominated by giants such as voice carriers like Verizon, Tata or Deutsche Telekom and global

International Wholesale: Increasingly regional, on the brink of change The wholesale connectivity business, once dominated by giants such as voice carriers like Verizon, Tata or Deutsche Telekom and global

Information and Communications Technology

Information and Communications Technology 8 Policy Recommendations For the advancement of Knowledge Societies across Africa A Product of the African Leadership in ICT Course www.gesci.org Senthil Kumar,

Information and Communications Technology 8 Policy Recommendations For the advancement of Knowledge Societies across Africa A Product of the African Leadership in ICT Course www.gesci.org Senthil Kumar,

GLOBAL BANDWIDTH RESEARCH SERVICE EXECUTIVE SUMMARY. Executive Summary

Executive Summary The international bandwidth market is undergoing a transformation. The traditional dynamic by which carriers link broadband users to global networks is still a core part of the market,

Executive Summary The international bandwidth market is undergoing a transformation. The traditional dynamic by which carriers link broadband users to global networks is still a core part of the market,

Broadband Infrastructure in the ASEAN 9 9 Region

Broadband Infrastructure in the ASEAN 9 9 Region Markets, Infrastructure, Missing Links, and Policy Options for Enhancing Cross Border Connectivity Michael Ruddy Director of International Research Terabit

Broadband Infrastructure in the ASEAN 9 9 Region Markets, Infrastructure, Missing Links, and Policy Options for Enhancing Cross Border Connectivity Michael Ruddy Director of International Research Terabit

International Conference on the Great Lakes Region

i International Conference on the Great Lakes Region Regional Programme of Action for Economic Development and Regional Integration Project No. 3.3.10 East African Submarine Cable System Project (EASSy)

i International Conference on the Great Lakes Region Regional Programme of Action for Economic Development and Regional Integration Project No. 3.3.10 East African Submarine Cable System Project (EASSy)

Identifying key regulatory and policy issues to ensure open access to regional backbone infrastructure initiatives in Africa

Identifying key regulatory and policy issues to ensure open access to regional backbone infrastructure initiatives in Africa Submitted to: The Global ICT Policy Division (CITPO), World Bank Prepared for:

Identifying key regulatory and policy issues to ensure open access to regional backbone infrastructure initiatives in Africa Submitted to: The Global ICT Policy Division (CITPO), World Bank Prepared for:

Point Topic s Broadband Operators and Tariffs

1 Point Topic s Broadband Operators and Tariffs Broadband tariff benchmarks: Q2 2013 July 2013 Point Topic Ltd 73 Farringdon Road London EC1M 3JQ, UK Tel. +44 (0) 20 3301 3303 Email tariffs@point-topic.com

1 Point Topic s Broadband Operators and Tariffs Broadband tariff benchmarks: Q2 2013 July 2013 Point Topic Ltd 73 Farringdon Road London EC1M 3JQ, UK Tel. +44 (0) 20 3301 3303 Email tariffs@point-topic.com

Presentation to 38th General Assembly of FANAF Ouagadougou, 17-21 February 2014. Thierry Tanoh- Group CEO

Presentation to 38th General Assembly of FANAF Ouagadougou, 17-21 February 2014 Thierry Tanoh- Group CEO Contents Global Demographics Africa Market Size & Growth Drivers Key players & Competitive Landscape

Presentation to 38th General Assembly of FANAF Ouagadougou, 17-21 February 2014 Thierry Tanoh- Group CEO Contents Global Demographics Africa Market Size & Growth Drivers Key players & Competitive Landscape

Comments of MCI. Regarding the. 30 June 2003

Comments of MCI Regarding the Designation of Singapore Telecommunications Limited s Local Leased Circuits as Mandatory Wholesale Service 30 June 2003 For additional information, please contact: Joseph

Comments of MCI Regarding the Designation of Singapore Telecommunications Limited s Local Leased Circuits as Mandatory Wholesale Service 30 June 2003 For additional information, please contact: Joseph

ITU ADVANCED LEVEL TRAINING Strategic Costing and Business Planning for Quadplay

ITU ADVANCED LEVEL TRAINING Strategic Costing and Business Planning for Quadplay WINDHOEK, NAMIBIA 6-10 October, 2014 David Rogerson and Harm Aben ITU Experts 1 Session 9: Practical exercise 4: using a

ITU ADVANCED LEVEL TRAINING Strategic Costing and Business Planning for Quadplay WINDHOEK, NAMIBIA 6-10 October, 2014 David Rogerson and Harm Aben ITU Experts 1 Session 9: Practical exercise 4: using a

Doing Business 2015 Fact Sheet: Sub-Saharan Africa

Doing Business 2015 Fact Sheet: Sub-Saharan Africa Thirty-five of 47 economies in Sub-Saharan Africa implemented at least one regulatory reform making it easier to do business in the year from June 1,

Doing Business 2015 Fact Sheet: Sub-Saharan Africa Thirty-five of 47 economies in Sub-Saharan Africa implemented at least one regulatory reform making it easier to do business in the year from June 1,

Ministry of Information and Communication Technology EXPRESSION OF INTEREST

EXPRESSION OF INTEREST Consultancy Services for SubmarineFibre Optic Connectivity in Rodrigues (Authorised under Section 24(2) of the Public Procurement Act 2006) Reference No. : MICT/Q3/2012/EOI 1.0 Introduction

EXPRESSION OF INTEREST Consultancy Services for SubmarineFibre Optic Connectivity in Rodrigues (Authorised under Section 24(2) of the Public Procurement Act 2006) Reference No. : MICT/Q3/2012/EOI 1.0 Introduction

WHO Global Health Expenditure Atlas

WHO Global Health Expenditure Atlas September 214 WHO Library Cataloguing-in-Publication Data WHO global health expenditure atlas. 1.Health expenditures statistics and numerical data. 2.Health systems

WHO Global Health Expenditure Atlas September 214 WHO Library Cataloguing-in-Publication Data WHO global health expenditure atlas. 1.Health expenditures statistics and numerical data. 2.Health systems

Manufacturing & Reproducing Magnetic & Optical Media Africa Report

Brochure More information from http://www.researchandmarkets.com/reports/3520587/ Manufacturing & Reproducing Magnetic & Optical Media Africa Report Description: MANUFACTURING & REPRODUCING MAGNETIC &

Brochure More information from http://www.researchandmarkets.com/reports/3520587/ Manufacturing & Reproducing Magnetic & Optical Media Africa Report Description: MANUFACTURING & REPRODUCING MAGNETIC &

FINANCIAL AND ECONOMIC ANALYSES

Tonga-Fiji Submarine Cable Project (RRP TON 44172) FINANCIAL AND ECONOMIC ANALYSES A. Introduction 1. The Tonga Fiji Submarine Cable Project will support the Government of Tonga to establish an 827 kilometer

Tonga-Fiji Submarine Cable Project (RRP TON 44172) FINANCIAL AND ECONOMIC ANALYSES A. Introduction 1. The Tonga Fiji Submarine Cable Project will support the Government of Tonga to establish an 827 kilometer

FRANCE TELECOM GROUP ORANGE

FRANCE TELECOM GROUP ORANGE Response to an IDA Public Consultation on Request by Singapore Telecommunications Limited for exemption from Dominant Licensee obligations with respect to the Business and Government

FRANCE TELECOM GROUP ORANGE Response to an IDA Public Consultation on Request by Singapore Telecommunications Limited for exemption from Dominant Licensee obligations with respect to the Business and Government

Regulatory models for broadband in emerging markets

THINKING TELECOMS SERIES Sydney Auckland Singapore London May 2014 Regulatory models for broadband in emerging markets All governments want to promote broadband access. The key point here is that governments

THINKING TELECOMS SERIES Sydney Auckland Singapore London May 2014 Regulatory models for broadband in emerging markets All governments want to promote broadband access. The key point here is that governments

EXPLORER HEALTH PLAN. Product Summary From 1 September 2013. bupa-intl.com. Insured by Working with Brokered by

EXPLORER HEALTH PLAN Product Summary From 1 September 2013 bupa-intl.com Insured by Working with Brokered by ABOUT BUPA AND JUBILEE ABOUT ABOUT BUPA BUPA, AND JUBILEE AND JUBILEE JUBILEE AND JWS GLOBAL

EXPLORER HEALTH PLAN Product Summary From 1 September 2013 bupa-intl.com Insured by Working with Brokered by ABOUT BUPA AND JUBILEE ABOUT ABOUT BUPA BUPA, AND JUBILEE AND JUBILEE JUBILEE AND JWS GLOBAL

Analysis of. The Measuring the Information Society Report 2013

Analysis of The Measuring the Information Society Report 2013 December 2013 Table of Contents 1. Introduction... 2 2. Key Highlights... 2 2.1 ICT Development Index (IDI)... 2 2.2 ICT Prices... 3 2.2.1

Analysis of The Measuring the Information Society Report 2013 December 2013 Table of Contents 1. Introduction... 2 2. Key Highlights... 2 2.1 ICT Development Index (IDI)... 2 2.2 ICT Prices... 3 2.2.1

Etisalat Group. Q4 2014 Results Presentation

Etisalat Group Q4 2014 Results Presentation 26 th February 2015 Disclaimer Emirates Telecommunications Corporation and its subsidiaries ( Etisalat or the Company ) have prepared this presentation ( Presentation

Etisalat Group Q4 2014 Results Presentation 26 th February 2015 Disclaimer Emirates Telecommunications Corporation and its subsidiaries ( Etisalat or the Company ) have prepared this presentation ( Presentation

The Profitability of BT s Regulated Services

The Profitability of BT s Regulated Services A REPORT PREPARED FOR VODAFONE November 2013 Frontier Economics Ltd, London. November 2013 Frontier Economics 1 Summary The analysis described below shows that

The Profitability of BT s Regulated Services A REPORT PREPARED FOR VODAFONE November 2013 Frontier Economics Ltd, London. November 2013 Frontier Economics 1 Summary The analysis described below shows that

WiMAX technology. An opportunity that can lead African Countries to the NET Economy. Annamaria Raviola SVP - Marketing and Business Development

WiMAX technology An opportunity that can lead African Countries to the NET Economy Annamaria Raviola SVP - Marketing and Business Development Agenda Telecommunications in Africa: the present picture Wi-MAX:

WiMAX technology An opportunity that can lead African Countries to the NET Economy Annamaria Raviola SVP - Marketing and Business Development Agenda Telecommunications in Africa: the present picture Wi-MAX:

DETERMINATION OF DOMINANCE IN SELECTED COMMUNICATIONS MARKETS IN NIGERIA ISSUED BY

DETERMINATION OF DOMINANCE IN SELECTED COMMUNICATIONS MARKETS IN NIGERIA ISSUED BY NIGERIAN COMMUNICATIONS COMMISSION 1 BACKGROUND AND INTRODUCTION Consistent with the liberalization of the Nigerian telecommunications

DETERMINATION OF DOMINANCE IN SELECTED COMMUNICATIONS MARKETS IN NIGERIA ISSUED BY NIGERIAN COMMUNICATIONS COMMISSION 1 BACKGROUND AND INTRODUCTION Consistent with the liberalization of the Nigerian telecommunications

Point Topic s Broadband Operators and Tariffs

1 Point Topic s Broadband Operators and Tariffs Broadband tariff benchmarks: Q1 2013 May 2013 Point Topic Ltd 73 Farringdon Road London EC1M 3JQ, UK Tel. +44 (0) 20 3301 3305 Email tariffs@point-topic.com

1 Point Topic s Broadband Operators and Tariffs Broadband tariff benchmarks: Q1 2013 May 2013 Point Topic Ltd 73 Farringdon Road London EC1M 3JQ, UK Tel. +44 (0) 20 3301 3305 Email tariffs@point-topic.com

&RPSHWLWLRQDQGGHUHJXODWLRQLQ )LQODQGDQGLQ(8

LQODQGDQGLQ(8") &RPSHWLWLRQDQGGHUHJXODWLRQLQ )LQODQGDQGLQ(8 The liberalization of European telecom markets The Finnish market situation New regulatory demands in promoting competition 7KH(87HOHFRPPXQLFDWLRQV PDUNHW 150

&RPSHWLWLRQDQGGHUHJXODWLRQLQ )LQODQGDQGLQ(8 The liberalization of European telecom markets The Finnish market situation New regulatory demands in promoting competition 7KH(87HOHFRPPXQLFDWLRQV PDUNHW 150

Mobile Broadband, DSL, & International Bandwidth Prices

Mobile Broadband, DSL, & International Bandwidth Prices Market and Competition Unit TELECOMMUNICATIONS REGULATORY AUTHORITY (TRA), LEBANON November 2011 Table of Contents I. Mobile Broadband Pricing in

Mobile Broadband, DSL, & International Bandwidth Prices Market and Competition Unit TELECOMMUNICATIONS REGULATORY AUTHORITY (TRA), LEBANON November 2011 Table of Contents I. Mobile Broadband Pricing in

Wholesale carrier value Cost vs quality

Wholesale carrier value Cost vs quality Craig Skinner, Senior Consultant, Telecoms February 2013 1 Global communications trends Global economy increasingly dependent on communications Focus of growth has

Wholesale carrier value Cost vs quality Craig Skinner, Senior Consultant, Telecoms February 2013 1 Global communications trends Global economy increasingly dependent on communications Focus of growth has

The Partnership between Dolphin & Telecom Italia Sparkle

The Partnership between Dolphin & Telecom Italia Sparkle Rome, 31 October 2014 0 Dolphin and TI Sparkle Partnership in Ghana: the two partners Dolphin group, part of Expresso Telecom group, is a 2nd largest

The Partnership between Dolphin & Telecom Italia Sparkle Rome, 31 October 2014 0 Dolphin and TI Sparkle Partnership in Ghana: the two partners Dolphin group, part of Expresso Telecom group, is a 2nd largest

Telecommunications Regulation. SOUTH AFRICA Bowman Gilfillan

Telecommunications Regulation SOUTH AFRICA Bowman Gilfillan CONTACT INFORMATION Daniel Pretorius Bowman Gilfillan 165 West Street, Sandton P.O. Box 785812 Johannesburg, 2146 +27116699381 d.pretorius@bowman.co.za

Telecommunications Regulation SOUTH AFRICA Bowman Gilfillan CONTACT INFORMATION Daniel Pretorius Bowman Gilfillan 165 West Street, Sandton P.O. Box 785812 Johannesburg, 2146 +27116699381 d.pretorius@bowman.co.za

Market size and market opportunity for agricultural value-added-services (Agri VAS)

") ANALYSIS Market size and market opportunity for agricultural value-added-services (Agri VAS) February 2015 GSMA Intelligence gsmaintelligence.com info@gsmaintelligence.com @GSMAi Agenda Context Growth

ANALYSIS Market size and market opportunity for agricultural value-added-services (Agri VAS) February 2015 GSMA Intelligence gsmaintelligence.com info@gsmaintelligence.com @GSMAi Agenda Context Growth

Review of recent CCSA experiences in the Telecommunications Sector Kazan, Russia. Selelo Ramohlola & Tapera Muzata 31 March 3 April 2015

Review of recent CCSA experiences in the Telecommunications Sector Kazan, Russia Selelo Ramohlola & Tapera Muzata 31 March 3 April 2015 Outline of Presentation Opening remarks Introduction & background

Review of recent CCSA experiences in the Telecommunications Sector Kazan, Russia Selelo Ramohlola & Tapera Muzata 31 March 3 April 2015 Outline of Presentation Opening remarks Introduction & background

LRIC Model Guidelines for the Kingdom of Saudi Arabia. Final Guidelines- Main Document

LRIC Model Guidelines for the Kingdom of Saudi Arabia Final Guidelines- Main Document March 1, 2008 1 Table of Contents 1 Introduction 4 11 Background 4 12 Purpose of this document 6 13 Objectives and

LRIC Model Guidelines for the Kingdom of Saudi Arabia Final Guidelines- Main Document March 1, 2008 1 Table of Contents 1 Introduction 4 11 Background 4 12 Purpose of this document 6 13 Objectives and

BENCHMARKING CONNECTIVITY IN AFRICA: TOWARDS EFFECTIVE INDICATORS FOR MEASURING PROGRESS IN THE USE OF ICTS IN DEVELOPING COUNTRIES.

Distr. GENERAL CES/SEM.52/10 17 November 2003 ENGLISH ONLY STATISTICAL COMMISSION and UNITED NATIONS ECONOMIC COMMISSION FOR EUROPE (UNECE) CONFERENCE OF EUROPEAN STATISTICIANS INTERNATIONAL TELECOMMUNICATION

Distr. GENERAL CES/SEM.52/10 17 November 2003 ENGLISH ONLY STATISTICAL COMMISSION and UNITED NATIONS ECONOMIC COMMISSION FOR EUROPE (UNECE) CONFERENCE OF EUROPEAN STATISTICIANS INTERNATIONAL TELECOMMUNICATION

Chart 1: Zambia's Major Trading Partners (Exports + Imports) Q4 2008 - Q4 2009. Switzernd RSA Congo DR China UAE Kuwait UK Zimbabwe India Egypt Other

Q4 2008 - Q4 2009. Switzernd RSA Congo DR China UAE Kuwait UK Zimbabwe India Egypt Other") Bank of Zambia us $ Million 1. INTRODUCTION This report shows Zambia s direction of merchandise trade for the fourth quarter of 2009 compared with the corresponding quarter in 2008. Revised 1 statistics,

Bank of Zambia us $ Million 1. INTRODUCTION This report shows Zambia s direction of merchandise trade for the fourth quarter of 2009 compared with the corresponding quarter in 2008. Revised 1 statistics,