ORSA Implementation Challenges

|

|

|

- Phoebe Cross

- 10 years ago

- Views:

Transcription

1 1 ORSA Implementation Challenges Christopher Crombie, FSA, FCIA AVP ERM & Financial Risk Management Standard Life Assurance Company of Canada To CIA Annual Meeting June 21, 2013

2 2 Context Our Own Risk and Solvency Assessment (ORSA) is being introduced in order to: Meet Solvency II requirements for European Business Units; Prepare our Group level ORSA; Adopt best practices being introduced in many jurisdictions including OSFI s required ORSA, expected in 2014.

3 3 Background on Solvency II (S2) S2 proposes: A market consistent balance sheet approach. Regulatory capital requirements closely aligned with the risks firms are running. Risk models genuinely used to help decision making and run the business. Affects all insurers operating within Europe. Other jurisdictions also affected through group solvency assessment. Development ongoing since 2010 in Canada. Involved in all aspects of development.

4 4 Significant Deliveries for S2 Standard Formula Basis under a new Balance Sheet. Ability to calculate regulatory capital requirements using a one size fits all basis. Internal Model Basis. Development of an internal model to calculate regulatory capital requirements. Economic Capital. Internal basis for assessing our capital needs and is based on an adjusted Solvency 2 internal model basis. Internal Model Approval Process (IMAP). A submission to the regulatory body must be made to seek approval to use an Internal Model. Own Risk Self Assessment (ORSA). A draft ORSA report was prepared in In 2012, the ORSA was presented to the Board.

.")

5 5 Significant Deliveries for S2 Other considerations Building up the reporting framework to provide all required information for consolidation at Group level within the needed timeframe. Finalizing the methodology and assumptions for the internal model. Enhance our oversight and governance processes over the internal model. Documentation Significant requirements on the documentation aspects of the methodology and on the data standards.

6 ERM Framework & ORSA Process 6

7 ERM Framework and Own Risk and Solvency Assessment 7 System of Governance ERM Framework ORSA ORSA Internal Model

8 8 ORSA Process IDENTIFY Consider:- current business environment & future strategy. new products/projects. emerging risks. validation activity. List risks and causes on risk registers. ASSESS Assess significance of risk. Assess probability of risk occurring. Determine capital requirement. CONTROL Establish ownership. Identify method of control. Set up risk indicators e.g. Key Risk Metrics Define principles of risk management (via the Group Policy Framework). Determine procedures e.g. Control Self Assessment. MONITOR Collect data. Analyse. Ensure response process followed when controls breached. The ORSA Process comprises all the processes that exist within the ERM Framework for identifying, assessing, controlling and monitoring risks. The key processes are: The Strategy, Capital and Business Planning Process The Emerging Risk Process The Validation Activity and Validation Reporting Process The Risk and Profitability Reporting Process The Risk Appetite Setting and Monitoring Process Stress and Scenario Testing Programme Extreme Scenario Analysis The Liquidity Risk Management Process The Operational Risk Assessment Process The Identification of Risk Modules for the Internal Model Monthly MI Reporting and Monitoring Process Policy Compliance Process Control Self Assessment These processes run concurrently and often operate continuously throughout the year. All of these processes exist within the ERM Framework to identify, assess, monitor, manage and report risks.

9 9 Identify Risks included in the Internal Model The Internal Model must reflect the risk profile of the company and cover all material risks. A risk should be considered material if its exclusion leads to a decision choice that would be considered inappropriate had the risk been included. Available historic data is used to assess materiality. Significant judgement is required for certain risks. For certain risk modules or factors, qualitative techniques and expert judgement will be used.

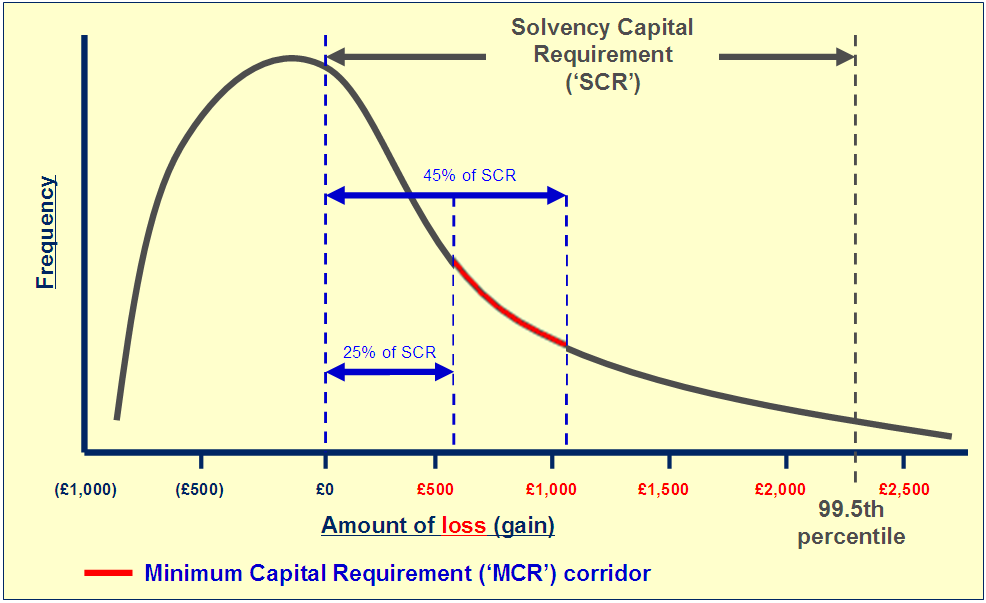

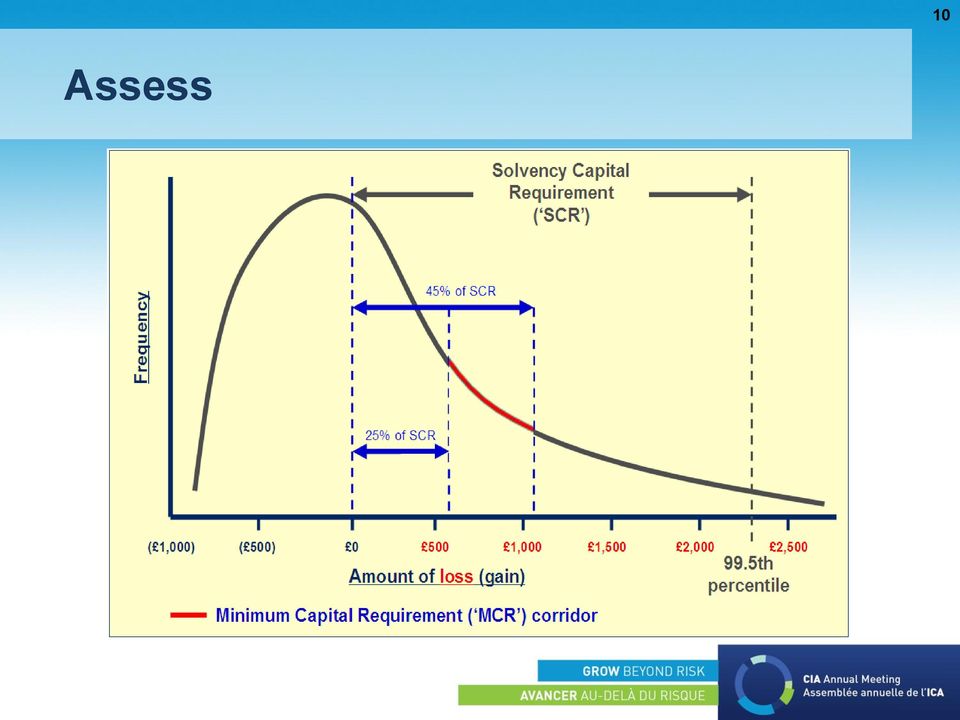

10 Assess 10

11 45.0% Loss 40.0% 35.0% 30.0% 25.0% 20.0% 15.0% 10.0% 5.0% 0.0% 45.0% 40.0% 35.0% 30.0% 25.0% 20.0% 15.0% 10.0% 5.0% 0.0% Key Assumptions Risk distributions Key assumptions Choice of distribution, parameterisation Chosen and calibrated with reference to historical data and expert judgement. Distributions are a simplified model of the real world, and the available data rarely suggests a particular distribution. Expert judgement is used to match the characteristics of a distribution to a risk. Management actions Management actions mitigate the effect of extreme events on the company s capital Modelled management actions: Changes to investment mix Changes to deductions for the cost of guarantees The level of smoothing Functions and Interactions Key assumptions Loss function structure, parameterisation Chosen and calibrated based on the behaviour of assets/liabilities as risk events change. The loss function structure can be a straight line, a curve or even stepped to reflect the impact of hedges. Dependencies Key assumptions Choice of copula, parameterisation The strength of correlation between variables is a key driver of diversification benefit, and is an important area of expert judgement. Modelled using a mathematical function called a copula. Although the strength of relationships can change under stress the choice of copula is less important than the choice of correlation strength, and more complicated copulas would significantly reduce the transparency of the model Risk factor 1 Risk factor 2

12 12 Key benefits of an Internal Model Capital requirements are driven by the real risks Decisions which are beneficial from a risk perspective can reduce regulatory capital requirements (e.g. using reinsurance or hedging) A Standard Formula will not necessarily reflect the risk profile of the company. Risk and capital management is at the heart of decision-making Outputs from the Internal Model play an integral role in operational decision-making. Reputation Seen as an indicator of the strength of a firm s risk management capability under Solvency 2.

13 13 Control: Self assessment tests 1. Use Test Internal model adequately reflects the nature and scale of the business Management can demonstrate understanding of the internal model Outputs from the Internal Model play an integral role in key strategic and operational decision making Internal model integrated with risk management 2. Statistical quality / 3. Calibration standards Model based on appropriate actuarial/statistical techniques Model results are transparent, stable and reflect the company s risk profile Model assumptions are documented, credible and transparent Data complete, accurate and appropriate Cover all material risks and provide ability to judge and prioritise risks Appropriate allowance for diversification/management actions

14 14 Control: Self assessment tests 4. Profit and loss attribution Perform an analysis to allocate actual profit and loss arising to major business units and risk categories Validates that the model covers all material risks observed Supports validation that risk exposures are correctly calibrated Informs on updates to the model 5. Validation standards Validation must be independent from development and operation of model Some validation tools are specified including stress and scenario analysis and reverse stress testing Full validation required at least annually

15 15 Control: Self assessment tests 6. Documentation standards Results in principle reproducible using inputs/documentation Documentation held in an inventory Documentation appropriately structured and detailed Documentation complete and up to date Proper change control Document limitations of the model/risks not included

16 16 Monitor: The ORSA report The ORSA Report is a key requirement of the Solvency 2 Regulations Purpose of the ORSA Report is to document: The current risks to the business; Our assessment of our current solvency and own funds; and, A forward-looking assessment of the risks and solvency needs in light of the business strategy. The report enhances an ERM Framework, bringing information on the framework and risk exposures into a single document. The report is presented to senior management and the Board, allowing a holistic view to be taken and sets out the relationship between risk and capital.

17 17 Monitor: The ORSA report The full ORSA report has been set out in 4 primary sections as follows: Section A sets out the purpose of the report and provides a summary of the Canadian business. Section B provides a comprehensive description of our System of Governance and ERM Framework. Section C provides an overview of the key risk exposures, setting out the nature and sources of these risks in an accessible and understandable manner. Section D provides a detailed capital solvency assessment.

18 18 Conclusion Development of an ORSA is an iterative process Most insurers have an established ERM framework which includes modelling risks and capital. You should build on what you have unless completely inadequate (long process). Complexity of the modelling should not be underestimated. Documentation is one of the biggest elements Need to justify and provide evidence for all assumptions and methodology. Need to document all of the ERM Framework Need to have 2 nd line validation and proper control environment. Not just a calculation or reporting exercise Expected that the results be used to manage the business. Training is a key element. Regulations have still to be finalised Solvency 2 has not yet been adopted. OSFI s guidelines are still in draft form.

19 Questions? 19

This section outlines the Solvency II requirements for a syndicate s own risk and solvency assessment (ORSA).

.") Section 9: ORSA Overview This section outlines the Solvency II requirements for a syndicate s own risk and solvency assessment (ORSA). The ORSA can be defined as the entirety of the processes and procedures

Section 9: ORSA Overview This section outlines the Solvency II requirements for a syndicate s own risk and solvency assessment (ORSA). The ORSA can be defined as the entirety of the processes and procedures

OWN RISK AND SOLVENCY ASSESSMENT AND ENTERPRISE RISK MANAGEMENT

OWN RISK AND SOLVENCY ASSESSMENT AND ENTERPRISE RISK MANAGEMENT ERM as the foundation for regulatory compliance and strategic business decision making CONTENTS Introduction... 3 Steps to developing an

OWN RISK AND SOLVENCY ASSESSMENT AND ENTERPRISE RISK MANAGEMENT ERM as the foundation for regulatory compliance and strategic business decision making CONTENTS Introduction... 3 Steps to developing an

ORSA for Insurers A Global Concept

ORSA for Insurers A Global Concept Stuart Wason, FSA, FCIA, MAAA, CERA Senior Director, Actuarial Division Office of the Superintendent of Financial Institutions Canada (OSFI) Table of Contents Early developments

ORSA for Insurers A Global Concept Stuart Wason, FSA, FCIA, MAAA, CERA Senior Director, Actuarial Division Office of the Superintendent of Financial Institutions Canada (OSFI) Table of Contents Early developments

Preparing for ORSA - Some practical issues

2013 Seminar for the Appointed Actuary Colloque pour l actuaire désigné 2013 Session 13 (P&C): Preparing for ORSA - Some practical issues Speaker: Jean-Marc Léveillé Vice-president Corporate Actuarial,

2013 Seminar for the Appointed Actuary Colloque pour l actuaire désigné 2013 Session 13 (P&C): Preparing for ORSA - Some practical issues Speaker: Jean-Marc Léveillé Vice-president Corporate Actuarial,

Solvency II Own Risk and Solvency Assessment (ORSA)

") Solvency II Own Risk and Solvency Assessment (ORSA) Guidance notes September 2011 Contents Introduction Purpose of this Document 3 Lloyd s ORSA framework 3 Guidance for Syndicate ORSAs Overview 7 December

Solvency II Own Risk and Solvency Assessment (ORSA) Guidance notes September 2011 Contents Introduction Purpose of this Document 3 Lloyd s ORSA framework 3 Guidance for Syndicate ORSAs Overview 7 December

Guidance for the Development of a Models-Based Solvency Framework for Canadian Life Insurance Companies

Guidance for the Development of a Models-Based Solvency Framework for Canadian Life Insurance Companies January 2010 Background The MCCSR Advisory Committee was established to develop proposals for a new

Guidance for the Development of a Models-Based Solvency Framework for Canadian Life Insurance Companies January 2010 Background The MCCSR Advisory Committee was established to develop proposals for a new

Deriving Value from ORSA. Board Perspective

Deriving Value from ORSA Board Perspective April 2015 1 This paper has been produced by the Joint Own Risk Solvency Assessment (ORSA) Subcommittee of the Insurance Regulation Committee and the Enterprise

Deriving Value from ORSA Board Perspective April 2015 1 This paper has been produced by the Joint Own Risk Solvency Assessment (ORSA) Subcommittee of the Insurance Regulation Committee and the Enterprise

CRO Forum Paper on the Own Risk and Solvency Assessment (ORSA): Leveraging regulatory requirements to generate value. May 2012.

: Leveraging regulatory requirements to generate value. May 2012.") CRO Forum Paper on the Own Risk and Solvency Assessment (ORSA): Leveraging regulatory requirements to generate value May 2012 May 2012 1 1. Introduction 1.1. Purpose of the paper In this discussion paper

CRO Forum Paper on the Own Risk and Solvency Assessment (ORSA): Leveraging regulatory requirements to generate value May 2012 May 2012 1 1. Introduction 1.1. Purpose of the paper In this discussion paper

Risk Management. Trends for Insurance Companies. Jeffrey Lovern Genworth Financial VP, Enterprise Risk Management Global Mortgage Insurance

Risk Management Trends for Insurance Companies Jeffrey Lovern Genworth Financial VP, Enterprise Risk Management Global Mortgage Insurance Global Association of Risk Professionals March, 2014 Agenda Global

Risk Management Trends for Insurance Companies Jeffrey Lovern Genworth Financial VP, Enterprise Risk Management Global Mortgage Insurance Global Association of Risk Professionals March, 2014 Agenda Global

Solvency II Own risk and solvency assessment (ORSA)

") Solvency II Own risk and solvency assessment (ORSA) Guidance notes MAY 2012 Contents Introduction Page Background 3 Purpose and Scope 3 Structure of guidance document 4 Key Principles and Lloyd s Minimum

Solvency II Own risk and solvency assessment (ORSA) Guidance notes MAY 2012 Contents Introduction Page Background 3 Purpose and Scope 3 Structure of guidance document 4 Key Principles and Lloyd s Minimum

Central Bank of Ireland Guidelines on Preparing for Solvency II Pre-application for Internal Models

2013 Central Bank of Ireland Guidelines on Preparing for Solvency II Pre-application for Internal Models 1 Contents 1 Context... 1 2 General... 2 3 Guidelines on Pre-application for Internal Models...

2013 Central Bank of Ireland Guidelines on Preparing for Solvency II Pre-application for Internal Models 1 Contents 1 Context... 1 2 General... 2 3 Guidelines on Pre-application for Internal Models...

BERMUDA MONETARY AUTHORITY

BERMUDA MONETARY AUTHORITY INSURANCE SUPERVISION DEPARTMENT GUIDANCE NOTES STANDARDS AND APPLICATION FRAMEWORK FOR THE USE OF INTERNAL CAPITAL MODELS FOR REGULATORY CAPITAL PURPOSES - REVISED - September

BERMUDA MONETARY AUTHORITY INSURANCE SUPERVISION DEPARTMENT GUIDANCE NOTES STANDARDS AND APPLICATION FRAMEWORK FOR THE USE OF INTERNAL CAPITAL MODELS FOR REGULATORY CAPITAL PURPOSES - REVISED - September

Solvency II Data audit report guidance. March 2012

Solvency II Data audit report guidance March 2012 Contents Page Introduction Purpose of the Data Audit Report 3 Report Format and Submission 3 Ownership and Independence 4 Scope and Content Scope of the

Solvency II Data audit report guidance March 2012 Contents Page Introduction Purpose of the Data Audit Report 3 Report Format and Submission 3 Ownership and Independence 4 Scope and Content Scope of the

Society of Actuaries in Ireland

Society of Actuaries in Ireland Information and Assistance Note LA-1: Actuaries involved in the Own Risk & Solvency Assessment (ORSA) under Solvency II Life Assurance and Life Reinsurance Business Issued

Society of Actuaries in Ireland Information and Assistance Note LA-1: Actuaries involved in the Own Risk & Solvency Assessment (ORSA) under Solvency II Life Assurance and Life Reinsurance Business Issued

CEIOPS Advice for Level 2 Implementing Measures on Solvency II: Articles 120 to 126. Tests and Standards for Internal Model Approval

CEIOPS-DOC-48/09 CEIOPS Advice for Level 2 Implementing Measures on Solvency II: Articles 120 to 126 Tests and Standards for Internal Model Approval (former Consultation Paper 56) October 2009 CEIOPS e.v.

CEIOPS-DOC-48/09 CEIOPS Advice for Level 2 Implementing Measures on Solvency II: Articles 120 to 126 Tests and Standards for Internal Model Approval (former Consultation Paper 56) October 2009 CEIOPS e.v.

Terms of Reference - Board Risk Committee

Terms of Reference - Board Risk Committee The Board Risk Committee is authorised by the Board to oversee the Group s risk management arrangements. It ensures that the overarching risk appetite is appropriate

Terms of Reference - Board Risk Committee The Board Risk Committee is authorised by the Board to oversee the Group s risk management arrangements. It ensures that the overarching risk appetite is appropriate

Stress testing in a time of models. Peter Sondhelm, Steve Clark & James Orr

Stress testing in a time of models Peter Sondhelm, Steve Clark & James Orr Agenda Why Stress Test? Users of Stress Tests Imagination vs. Expectation Robust Stress Testing Infrastructure Good / Bad Practice

Stress testing in a time of models Peter Sondhelm, Steve Clark & James Orr Agenda Why Stress Test? Users of Stress Tests Imagination vs. Expectation Robust Stress Testing Infrastructure Good / Bad Practice

University of St. Gallen Law School Law and Economics Research Paper Series. Working Paper No. 2008-19 June 2007

University of St. Gallen Law School Law and Economics Research Paper Series Working Paper No. 2008-19 June 2007 Enterprise Risk Management A View from the Insurance Industry Wolfgang Errath and Andreas

University of St. Gallen Law School Law and Economics Research Paper Series Working Paper No. 2008-19 June 2007 Enterprise Risk Management A View from the Insurance Industry Wolfgang Errath and Andreas

Scenario Analysis Principles and Practices in the Insurance Industry

North American CRO Council Scenario Analysis Principles and Practices in the Insurance Industry 2013 North American CRO Council Incorporated [email protected] December 2013 Acknowledgement The

North American CRO Council Scenario Analysis Principles and Practices in the Insurance Industry 2013 North American CRO Council Incorporated [email protected] December 2013 Acknowledgement The

Solvency II Detailed guidance notes

Solvency II Detailed guidance notes March 2010 Section 1 - System of governance Section 1: System of Governance Overview This section outlines the Solvency II requirements for an effective system of governance,

Solvency II Detailed guidance notes March 2010 Section 1 - System of governance Section 1: System of Governance Overview This section outlines the Solvency II requirements for an effective system of governance,

Stress Testing: Insurance Companies in Canada

Stress Testing: Insurance Companies in Canada August Chow, FSA, FCIA Senior Director OSFI Canada Paper presented at the Expert Forum on Advanced Techniques on Stress Testing: Applications for Supervisors

Stress Testing: Insurance Companies in Canada August Chow, FSA, FCIA Senior Director OSFI Canada Paper presented at the Expert Forum on Advanced Techniques on Stress Testing: Applications for Supervisors

Transforming risk management into a competitive advantage kpmg.com

INSURANCE RISK MANAGEMENT ADVISORY SOLUTIONS Transforming risk management into a competitive advantage kpmg.com 2 Transforming risk management into a competitive advantage Assessing risk. Building value.

INSURANCE RISK MANAGEMENT ADVISORY SOLUTIONS Transforming risk management into a competitive advantage kpmg.com 2 Transforming risk management into a competitive advantage Assessing risk. Building value.

Regulations in General Insurance. Solvency II

Regulations in General Insurance Solvency II Solvency II What is it? Solvency II is a new risk-based regulatory requirement for insurance, reinsurance and bancassurance (insurance) organisations that operate

Regulations in General Insurance Solvency II Solvency II What is it? Solvency II is a new risk-based regulatory requirement for insurance, reinsurance and bancassurance (insurance) organisations that operate

From ICAAP/ORSA to ERM: Board and Senior Management Oversight. Leon Bloom, Partner, Deloitte & Touche LLP [email protected]

From ICAAP/ORSA to ERM: Board and Senior Management Oversight Leon Bloom, Partner, Deloitte & Touche LLP [email protected] Agenda Basel II ICAAP Solvency II ORSA ERM From ICAAP/ORSA to ERM: Governance

From ICAAP/ORSA to ERM: Board and Senior Management Oversight Leon Bloom, Partner, Deloitte & Touche LLP [email protected] Agenda Basel II ICAAP Solvency II ORSA ERM From ICAAP/ORSA to ERM: Governance

Insurance Groups under Solvency II

Insurance Groups under Solvency II November 2013 Table of Contents 1. Introduction... 2 2. Defining an insurance group... 2 3. Cases of application of group supervision... 6 4. The scope of group supervision...

Insurance Groups under Solvency II November 2013 Table of Contents 1. Introduction... 2 2. Defining an insurance group... 2 3. Cases of application of group supervision... 6 4. The scope of group supervision...

Internal Model Approval Process (IMAP) Contents of Application (CoA) Template. August 2011 Version 1.0

Contents of Application (CoA) Template. August 2011 Version 1.0") Internal Model Approval Process (IMAP) Contents of Application (CoA) Template August 2011 Version 1.0 C O N T A C T D E T A I L S Physical Address: Riverwalk Office Park, Block B 41 Matroosberg Road (Corner

Internal Model Approval Process (IMAP) Contents of Application (CoA) Template August 2011 Version 1.0 C O N T A C T D E T A I L S Physical Address: Riverwalk Office Park, Block B 41 Matroosberg Road (Corner

Questions and answers collated at the PRA s Solvency II industry briefings on 12 December 2013

Questions and answers collated at the PRA s Solvency II industry briefings on 12 December 2013 Notes: 1. The responsibility for understanding the requirements of Solvency II and demonstrating that the

Questions and answers collated at the PRA s Solvency II industry briefings on 12 December 2013 Notes: 1. The responsibility for understanding the requirements of Solvency II and demonstrating that the

Preparing for ORSA - Some practical issues Speaker:

2013 Seminar for the Appointed Actuary Colloque pour l actuaire désigné 2013 Session 13: Preparing for ORSA - Some practical issues Speaker: André Racine, Principal Eckler Ltd. Context of ORSA Agenda Place

2013 Seminar for the Appointed Actuary Colloque pour l actuaire désigné 2013 Session 13: Preparing for ORSA - Some practical issues Speaker: André Racine, Principal Eckler Ltd. Context of ORSA Agenda Place

Guideline. Operational Risk Management. Category: Sound Business and Financial Practices. No: E-21 Date: June 2016

Guideline Subject: Category: Sound Business and Financial Practices No: E-21 Date: June 2016 1. Purpose and Scope of the Guideline This Guideline sets out OSFI s expectations for the management of operational

Guideline Subject: Category: Sound Business and Financial Practices No: E-21 Date: June 2016 1. Purpose and Scope of the Guideline This Guideline sets out OSFI s expectations for the management of operational

Principles for An. Effective Risk Appetite Framework

Principles for An Effective Risk Appetite Framework 18 November 2013 Table of Contents Page I. Introduction... 1 II. Key definitions... 2 III. Principles... 3 1. Risk appetite framework... 3 1.1 An effective

Principles for An Effective Risk Appetite Framework 18 November 2013 Table of Contents Page I. Introduction... 1 II. Key definitions... 2 III. Principles... 3 1. Risk appetite framework... 3 1.1 An effective

ERM Exam Core Readings Fall 2015. Table of Contents

i ERM Exam Core Readings Fall 2015 Table of Contents Section A: Risk Categories and Identification The candidate will understand the types of risks faced by an entity and be able to identify and analyze

i ERM Exam Core Readings Fall 2015 Table of Contents Section A: Risk Categories and Identification The candidate will understand the types of risks faced by an entity and be able to identify and analyze

LIFE INSURANCE CAPITAL FRAMEWORK STANDARD APPROACH

LIFE INSURANCE CAPITAL FRAMEWORK STANDARD APPROACH Table of Contents Introduction... 2 Process... 2 and Methodology... 3 Core Concepts... 3 Total Asset Requirement... 3 Solvency Buffer... 4 Framework Details...

LIFE INSURANCE CAPITAL FRAMEWORK STANDARD APPROACH Table of Contents Introduction... 2 Process... 2 and Methodology... 3 Core Concepts... 3 Total Asset Requirement... 3 Solvency Buffer... 4 Framework Details...

Table of contents 2015 ORSA OUTLOOK

2015 ORSA OUTLOOK Table of contents Introduction... 1 ORSA within the business... 2 Industry s view of its ORSA preparedness... 4 Maturity state of ORSA... 6 Internal models and risk assessment... 8 Cost

2015 ORSA OUTLOOK Table of contents Introduction... 1 ORSA within the business... 2 Industry s view of its ORSA preparedness... 4 Maturity state of ORSA... 6 Internal models and risk assessment... 8 Cost

Own Risk and Solvency Assessment

A closer look at Solvency II: The Actuary s role in the ORSA Visesh Gosrani, Barbara Illingworth Own Risk and Solvency Assessment 2010 The Actuarial Profession www.actuaries.org.uk Agenda Introduction

A closer look at Solvency II: The Actuary s role in the ORSA Visesh Gosrani, Barbara Illingworth Own Risk and Solvency Assessment 2010 The Actuarial Profession www.actuaries.org.uk Agenda Introduction

Subject ST9 Enterprise Risk Management Syllabus

Subject ST9 Enterprise Risk Management Syllabus for the 2015 exams 1 June 2014 Aim The aim of the Enterprise Risk Management (ERM) Specialist Technical subject is to instil in successful candidates the

Subject ST9 Enterprise Risk Management Syllabus for the 2015 exams 1 June 2014 Aim The aim of the Enterprise Risk Management (ERM) Specialist Technical subject is to instil in successful candidates the

DATA AUDIT: Scope and Content

DATA AUDIT: Scope and Content The schedule below defines the scope of a review that will assist the FSA in its assessment of whether a firm s data management complies with the standards set out in the

DATA AUDIT: Scope and Content The schedule below defines the scope of a review that will assist the FSA in its assessment of whether a firm s data management complies with the standards set out in the

ERM from a Small Insurance Company Perspective

ERM from a Small Insurance Company Perspective NABRICO Sept 30, 2011 Agenda Section 1 Section 2 Section 3 Section 4 ERM Introduction Key Risks Streamlined Quantitative Process Other Influences 1 1 Section

ERM from a Small Insurance Company Perspective NABRICO Sept 30, 2011 Agenda Section 1 Section 2 Section 3 Section 4 ERM Introduction Key Risks Streamlined Quantitative Process Other Influences 1 1 Section

EIOPACP 13/011. Guidelines on PreApplication of Internal Models

EIOPACP 13/011 Guidelines on PreApplication of Internal Models EIOPA Westhafen Tower, Westhafenplatz 1 60327 Frankfurt Germany Tel. + 49 6995111920; Fax. + 49 6995111919; site: www.eiopa.europa.eu Guidelines

EIOPACP 13/011 Guidelines on PreApplication of Internal Models EIOPA Westhafen Tower, Westhafenplatz 1 60327 Frankfurt Germany Tel. + 49 6995111920; Fax. + 49 6995111919; site: www.eiopa.europa.eu Guidelines

Actuarial Risk Management

ARA syllabus Actuarial Risk Management Aim: To provide the technical skills to apply the principles and methodologies studied under actuarial technical subjects for the identification, quantification and

ARA syllabus Actuarial Risk Management Aim: To provide the technical skills to apply the principles and methodologies studied under actuarial technical subjects for the identification, quantification and

Enterprise Risk Management A View. Clive Kelly CRO Zurich Insurance plc/zfs Europe (GI)

") Enterprise Risk Management A View Clive Kelly CRO Zurich Insurance plc/zfs Europe (GI) Topics ERM some basics Responsibilities CRO evolution Challenges and priorities Conclusion Introduction 3 Zurich s

Enterprise Risk Management A View Clive Kelly CRO Zurich Insurance plc/zfs Europe (GI) Topics ERM some basics Responsibilities CRO evolution Challenges and priorities Conclusion Introduction 3 Zurich s

Capital Adequacy: Advanced Measurement Approaches to Operational Risk

Prudential Standard APS 115 Capital Adequacy: Advanced Measurement Approaches to Operational Risk Objective and key requirements of this Prudential Standard This Prudential Standard sets out the requirements

Prudential Standard APS 115 Capital Adequacy: Advanced Measurement Approaches to Operational Risk Objective and key requirements of this Prudential Standard This Prudential Standard sets out the requirements

Model Risk, A company perspective Peter K. Reilly, FSA Valuation Actuary & Head of Actuarial Strategic Initiatives Aetna, Inc

Model Risk, A company perspective Peter K. Reilly, FSA Valuation Actuary & Head of Actuarial Strategic Initiatives Aetna, Inc 1 Agenda Thoughts/Observations on Model Risk Practical Considerations Aetna

Model Risk, A company perspective Peter K. Reilly, FSA Valuation Actuary & Head of Actuarial Strategic Initiatives Aetna, Inc 1 Agenda Thoughts/Observations on Model Risk Practical Considerations Aetna

An update on QIS5. Agenda 4/27/2010. Context, scope and timelines The draft Technical Specification Getting into gear Questions

A Closer Look at Solvency II Eleanor Beamond-Pepler, FSA An update on QIS5 2010 The Actuarial Profession www.actuaries.org.uk Agenda Context, scope and timelines The draft Technical Specification Getting

A Closer Look at Solvency II Eleanor Beamond-Pepler, FSA An update on QIS5 2010 The Actuarial Profession www.actuaries.org.uk Agenda Context, scope and timelines The draft Technical Specification Getting

IRSG Response to IAIS Consultation Paper on Basic Capital Requirements (BCR) for Global Systemically Important Insurers (G-SIIS)

for Global Systemically Important Insurers (G-SIIS)") EIOPA-IRSG-14-10 IRSG Response to IAIS Consultation Paper on Basic Capital Requirements (BCR) for Global Systemically Important Insurers (G-SIIS) 1/10 Executive Summary The IRSG supports the development

EIOPA-IRSG-14-10 IRSG Response to IAIS Consultation Paper on Basic Capital Requirements (BCR) for Global Systemically Important Insurers (G-SIIS) 1/10 Executive Summary The IRSG supports the development

Guideline. Category: Sound Business and Financial Practices. No: E-18 Date: December 2009

Guideline Subject: Category: Sound Business and Financial Practices No: E-18 Date: December 2009 Stress testing is an important tool for senior management to use in making business strategy, risk management

Guideline Subject: Category: Sound Business and Financial Practices No: E-18 Date: December 2009 Stress testing is an important tool for senior management to use in making business strategy, risk management

Dealing with Predictable Irrationality. Actuarial Ideas to Strengthen Global Financial Risk Management. At a macro or systemic level:

Actuarial Ideas to Strengthen Global Financial Risk Management The recent developments in global financial markets have raised serious questions about the management and oversight of the financial services

Actuarial Ideas to Strengthen Global Financial Risk Management The recent developments in global financial markets have raised serious questions about the management and oversight of the financial services

INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS

Standard No. 13 INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS STANDARD ON ASSET-LIABILITY MANAGEMENT OCTOBER 2006 This document was prepared by the Solvency and Actuarial Issues Subcommittee in consultation

Standard No. 13 INTERNATIONAL ASSOCIATION OF INSURANCE SUPERVISORS STANDARD ON ASSET-LIABILITY MANAGEMENT OCTOBER 2006 This document was prepared by the Solvency and Actuarial Issues Subcommittee in consultation

EIOPA-CP-11/008 7 November 2011. Consultation Paper On the Proposal for Guidelines on Own Risk and Solvency Assessment

EIOPA-CP-11/008 7 November 2011 Consultation Paper On the Proposal for Guidelines on Own Risk and Solvency Assessment EIOPA Westhafen Tower, Westhafenplatz 1-60327 Frankfurt Germany - Tel. + 49 69-951119-20;

EIOPA-CP-11/008 7 November 2011 Consultation Paper On the Proposal for Guidelines on Own Risk and Solvency Assessment EIOPA Westhafen Tower, Westhafenplatz 1-60327 Frankfurt Germany - Tel. + 49 69-951119-20;

Solvency II. PwC. *connected thinking. Internal models requirements and an example

Solvency II Internal models requirements and an example *connected thinking PwC Solvency II introduced the possibility to use an internal model to estimate solvency capital requirements (SCR) No cherry-picking

Solvency II Internal models requirements and an example *connected thinking PwC Solvency II introduced the possibility to use an internal model to estimate solvency capital requirements (SCR) No cherry-picking

Own Risk and Solvency Assessment

Own Risk and Solvency Assessment Presented by Padraic O Malley 1 December 2011 Own Risk and Solvency Assessment Top down process owned by the Board Board needs to know what risks the Company is running

Own Risk and Solvency Assessment Presented by Padraic O Malley 1 December 2011 Own Risk and Solvency Assessment Top down process owned by the Board Board needs to know what risks the Company is running

1. INTRODUCTION AND PURPOSE

Solvency Assessment and Management: Pillar 1 - Sub Committee Capital Requirements Task Group Discussion Document 73 (v 2) Treatment of new business in SCR EXECUTIVE SUMMARY As for the Solvency II Framework

Solvency Assessment and Management: Pillar 1 - Sub Committee Capital Requirements Task Group Discussion Document 73 (v 2) Treatment of new business in SCR EXECUTIVE SUMMARY As for the Solvency II Framework

SOLVENCY II HEALTH INSURANCE

2014 Solvency II Health SOLVENCY II HEALTH INSURANCE 1 Overview 1.1 Background and scope The current UK regulatory reporting regime is based on the EU Solvency I Directives. Although the latest of those

2014 Solvency II Health SOLVENCY II HEALTH INSURANCE 1 Overview 1.1 Background and scope The current UK regulatory reporting regime is based on the EU Solvency I Directives. Although the latest of those

Solvency II Preparation and IMAP James Latto

and James Latto Contents 2 1 Balancing priorities Insurers need to balance priorities over the next year: Main focus is often on Pillar 3 and external reporting needs sufficient focus Ensure smooth transition

and James Latto Contents 2 1 Balancing priorities Insurers need to balance priorities over the next year: Main focus is often on Pillar 3 and external reporting needs sufficient focus Ensure smooth transition

ACCELUS RISK MANAGEMENT SOLUTIONS THOMSON REUTERS ACCELUS ACCELUS RISK MANAGEMENT SOLUTIONS

ACCELUS RISK MANAGEMENT SOLUTIONS THOMSON REUTERS ACCELUS ACCELUS RISK MANAGEMENT SOLUTIONS THOMSON REUTERS ACCELUS Our solutions dynamically connect business transactions, strategy, and operations to

ACCELUS RISK MANAGEMENT SOLUTIONS THOMSON REUTERS ACCELUS ACCELUS RISK MANAGEMENT SOLUTIONS THOMSON REUTERS ACCELUS Our solutions dynamically connect business transactions, strategy, and operations to

ENTERPRISE RISK MANAGEMENT BENCHMARK REVIEW: 2013 UPDATE

March 2014 ENTERPRISE RISK MANAGEMENT BENCHMARK REVIEW: 2013 UPDATE In April and October 2009, Guy Carpenter published two briefings titled Risk Profile, Appetite and Tolerance: Fundamental Concepts in

March 2014 ENTERPRISE RISK MANAGEMENT BENCHMARK REVIEW: 2013 UPDATE In April and October 2009, Guy Carpenter published two briefings titled Risk Profile, Appetite and Tolerance: Fundamental Concepts in

ORSA for Dummies. Institute of Risk Management Solvency II Group April 17th 2012. Peter Taylor

ORSA for Dummies Institute of Risk Management Solvency II Group April 17th 2012 Peter Taylor ORSA for - the Dummies heart of Solvency II Institute of Risk Management Solvency II Group April 17th 2012 Peter

ORSA for Dummies Institute of Risk Management Solvency II Group April 17th 2012 Peter Taylor ORSA for - the Dummies heart of Solvency II Institute of Risk Management Solvency II Group April 17th 2012 Peter

Enterprise Risk Management in a Highly Uncertain World. A Presentation to the Government-University- Industry Research Roundtable June 20, 2012

Enterprise Risk Management in a Highly Uncertain World A Presentation to the Government-University- Industry Research Roundtable June 20, 2012 CRO Council Introduction Mission The North American CRO Council

Enterprise Risk Management in a Highly Uncertain World A Presentation to the Government-University- Industry Research Roundtable June 20, 2012 CRO Council Introduction Mission The North American CRO Council

Stress testing and capital planning - the key to making the ICAAP forward looking PRMIA Greece Chapter Meeting Athens, 25 October 2007

Stress testing and capital planning - the key to making the ICAAP forward looking Athens, *connectedthinking Agenda Introduction on ICAAP requirements What is stress testing? Regulatory guidance on stress

Stress testing and capital planning - the key to making the ICAAP forward looking Athens, *connectedthinking Agenda Introduction on ICAAP requirements What is stress testing? Regulatory guidance on stress

IRM CERTIFICATE AND DIPLOMA OUTLINE SYLLABUS

IRM CERTIFICATE AND DIPLOMA OUTLINE SYLLABUS 1 Module 1: Principles of Risk and Risk Management Module aims The aim of this module is to provide an introduction to the principles and concepts of risk and

IRM CERTIFICATE AND DIPLOMA OUTLINE SYLLABUS 1 Module 1: Principles of Risk and Risk Management Module aims The aim of this module is to provide an introduction to the principles and concepts of risk and

ALM Stress Testing: Gaining Insight on Modeled Outcomes

ALM Stress Testing: Gaining Insight on Modeled Outcomes 2013 Financial Conference Ballantyne Resort Charlotte, NC September 18, 2013 Thomas E. Bowers, CFA Vice President Client Services ZM Financial Systems

ALM Stress Testing: Gaining Insight on Modeled Outcomes 2013 Financial Conference Ballantyne Resort Charlotte, NC September 18, 2013 Thomas E. Bowers, CFA Vice President Client Services ZM Financial Systems

Solvency II in practice. Speaker: Tim O Hanrahan Deputy Head, Insurance, Central Bank of Ireland 16 March 2016

1 Solvency II in practice Speaker: Tim O Hanrahan Deputy Head, Insurance, Central Bank of Ireland 16 March 2016 1 Recap on Solvency II Regulatory Framework under Solvency II Pillar I - Capital Pillar II

1 Solvency II in practice Speaker: Tim O Hanrahan Deputy Head, Insurance, Central Bank of Ireland 16 March 2016 1 Recap on Solvency II Regulatory Framework under Solvency II Pillar I - Capital Pillar II

SOLVENCY II LIFE INSURANCE

SOLVENCY II LIFE INSURANCE 1 Overview 1.1 Background and scope The current UK regulatory reporting regime is based on the EU Solvency I Directives. Although the latest of those Directives was implemented

SOLVENCY II LIFE INSURANCE 1 Overview 1.1 Background and scope The current UK regulatory reporting regime is based on the EU Solvency I Directives. Although the latest of those Directives was implemented

Solvency II Revealed. October 2011

Solvency II Revealed October 2011 Contents 4 An Optimal Insurer in a Post-Solvency II World 10 Changing the Landscape of Insurance Asset Strategy 16 Capital Relief Through Reinsurance 21 Natural Catastrophe

Solvency II Revealed October 2011 Contents 4 An Optimal Insurer in a Post-Solvency II World 10 Changing the Landscape of Insurance Asset Strategy 16 Capital Relief Through Reinsurance 21 Natural Catastrophe

Direct Line Insurance Group plc (the Company ) Board Risk Committee (the Committee ) Terms of Reference

Board Risk Committee (the Committee ) Terms of Reference") Direct Line Insurance Group plc (the Company ) Board Risk Committee (the Committee ) Terms of Reference Chair An Independent Non-Executive Director In the absence of the Committee Chairman and an appointed

Direct Line Insurance Group plc (the Company ) Board Risk Committee (the Committee ) Terms of Reference Chair An Independent Non-Executive Director In the absence of the Committee Chairman and an appointed

NEW YORK STATE DEPARTMENT OF FINANCIAL SERVICES 11 NYCRR 82 (INSURANCE REGULATION 203) ENTERPRISE RISK MANAGEMENT AND OWN RISK AND SOLVENCY ASSESSMENT

ENTERPRISE RISK MANAGEMENT AND OWN RISK AND SOLVENCY ASSESSMENT") NEW YORK STATE DEPARTMENT OF FINANCIAL SERVICES 11 NYCRR 82 (INSURANCE REGULATION 203) ENTERPRISE RISK MANAGEMENT AND OWN RISK AND SOLVENCY ASSESSMENT I, Benjamin M. Lawsky, Superintendent of Financial

NEW YORK STATE DEPARTMENT OF FINANCIAL SERVICES 11 NYCRR 82 (INSURANCE REGULATION 203) ENTERPRISE RISK MANAGEMENT AND OWN RISK AND SOLVENCY ASSESSMENT I, Benjamin M. Lawsky, Superintendent of Financial

International Diploma in Risk Management Syllabus

International Diploma in Risk Management Syllabus Module 1: Principles of Risk and Risk Management The aim of this module is to provide an introduction to the principles and concepts of risk and risk management.

International Diploma in Risk Management Syllabus Module 1: Principles of Risk and Risk Management The aim of this module is to provide an introduction to the principles and concepts of risk and risk management.

Placing a Value on Enterprise Risk Management ADVISORY

Placing a Value on Enterprise Risk Management ADVISORY Placing a Value on Enterprise Risk Management 1 In turbulent economic times, the case for investing in an enterprise risk management (ERM) program

Placing a Value on Enterprise Risk Management ADVISORY Placing a Value on Enterprise Risk Management 1 In turbulent economic times, the case for investing in an enterprise risk management (ERM) program

GUIDELINES ON CORPORATE GOVERNANCE FOR LABUAN BANKS

GUIDELINES ON CORPORATE GOVERNANCE FOR LABUAN BANKS 1.0 Introduction 1.1 Good corporate governance practice improves safety and soundness through effective risk management and creates the ability to execute

GUIDELINES ON CORPORATE GOVERNANCE FOR LABUAN BANKS 1.0 Introduction 1.1 Good corporate governance practice improves safety and soundness through effective risk management and creates the ability to execute

Solvency II benchmarking survey

INSURaNce Solvency II benchmarking survey Life Insurers November 2011 kpmg.co.uk/solvencyii 2 SoLveNcy II benchmarking SURvey - LIfe INSUReRS SoLveNcy II benchmarking SURvey - LIfe INSUReRS 3 Contents

INSURaNce Solvency II benchmarking survey Life Insurers November 2011 kpmg.co.uk/solvencyii 2 SoLveNcy II benchmarking SURvey - LIfe INSUReRS SoLveNcy II benchmarking SURvey - LIfe INSUReRS 3 Contents

Solvency II for Beginners 16.05.2013

Solvency II for Beginners 16.05.2013 Agenda Why has Solvency II been created? Structure of Solvency II The Solvency II Balance Sheet Pillar II & III Aspects Where are we now? Solvency II & Actuaries Why

Solvency II for Beginners 16.05.2013 Agenda Why has Solvency II been created? Structure of Solvency II The Solvency II Balance Sheet Pillar II & III Aspects Where are we now? Solvency II & Actuaries Why

Final Report on Public Consultation No. 14/017 on Guidelines on own risk and solvency assessment

EIOPA-BoS-14/259 28 January 2015 Final Report on Public Consultation No. 14/017 on Guidelines on own risk and solvency assessment EIOPA Westhafen Tower, Westhafenplatz 1-60327 Frankfurt Germany - Tel.

EIOPA-BoS-14/259 28 January 2015 Final Report on Public Consultation No. 14/017 on Guidelines on own risk and solvency assessment EIOPA Westhafen Tower, Westhafenplatz 1-60327 Frankfurt Germany - Tel.

GUIDANCE NOTE FOR DEPOSIT-TAKERS. Operational Risk Management. March 2012

GUIDANCE NOTE FOR DEPOSIT-TAKERS Operational Risk Management March 2012 Version 1.0 Contents Page No 1 Introduction 2 2 Overview 3 Operational risk - fundamental principles and governance 3 Fundamental

GUIDANCE NOTE FOR DEPOSIT-TAKERS Operational Risk Management March 2012 Version 1.0 Contents Page No 1 Introduction 2 2 Overview 3 Operational risk - fundamental principles and governance 3 Fundamental

STANDARD & POOR S ECONOMIC CAPITAL MODEL REVIEW PROMISES CAPITAL REWARDS

STANDARD & POOR S ECONOMIC CAPITAL MODEL REVIEW PROMISES CAPITAL REWARDS Willis Re Standard & Poor s Economic Capital Model Review Promises Capital Rewards 2 Standard & Poor s Economic Capital Model Review

STANDARD & POOR S ECONOMIC CAPITAL MODEL REVIEW PROMISES CAPITAL REWARDS Willis Re Standard & Poor s Economic Capital Model Review Promises Capital Rewards 2 Standard & Poor s Economic Capital Model Review

Operational Risk Management Table of Contents

Operational Management Table of Contents SECTION 1 Operational The Definition of Operational Drivers of Operational Management Governance Culture and Awareness Policies and Procedures SECTION 2 Operational

Operational Management Table of Contents SECTION 1 Operational The Definition of Operational Drivers of Operational Management Governance Culture and Awareness Policies and Procedures SECTION 2 Operational

Guidance Note: Stress Testing Class 2 Credit Unions. November, 2013. Ce document est également disponible en français

Guidance Note: Stress Testing Class 2 Credit Unions November, 2013 Ce document est également disponible en français This Guidance Note is for use by all Class 2 credit unions with assets in excess of $1

Guidance Note: Stress Testing Class 2 Credit Unions November, 2013 Ce document est également disponible en français This Guidance Note is for use by all Class 2 credit unions with assets in excess of $1

Insurance Core Principles

ICP 16 Enterprise Risk Management for Solvency Purposes The supervisor establishes enterprise risk management requirements for solvency purposes that require insurers to address all relevant and material

ICP 16 Enterprise Risk Management for Solvency Purposes The supervisor establishes enterprise risk management requirements for solvency purposes that require insurers to address all relevant and material

LIQUIDITY RISK MANAGEMENT GUIDELINE

LIQUIDITY RISK MANAGEMENT GUIDELINE April 2009 Table of Contents Preamble... 3 Introduction... 4 Scope... 5 Coming into effect and updating... 6 1. Liquidity risk... 7 2. Sound and prudent liquidity risk

LIQUIDITY RISK MANAGEMENT GUIDELINE April 2009 Table of Contents Preamble... 3 Introduction... 4 Scope... 5 Coming into effect and updating... 6 1. Liquidity risk... 7 2. Sound and prudent liquidity risk

Managing Risk at Bank of America Corporation. Overview

Managing Risk at Bank of America Corporation Overview Risk is inherent in every material business activity that we undertake. Our business exposes us to strategic, credit, market, liquidity, compliance,

Managing Risk at Bank of America Corporation Overview Risk is inherent in every material business activity that we undertake. Our business exposes us to strategic, credit, market, liquidity, compliance,

Bermuda s Insurance Solvency Framework. The Roadmap to Regulatory Equivalence

Bermuda s Insurance Solvency Framework The Roadmap to Regulatory Equivalence May 2012 Contents This publication provides details of the Authority s progress to date and planned initiatives in the regulatory

Bermuda s Insurance Solvency Framework The Roadmap to Regulatory Equivalence May 2012 Contents This publication provides details of the Authority s progress to date and planned initiatives in the regulatory

Regulatory Solvency Assessment of Property/Casualty Insurance Companies in the United States

Regulatory Solvency Assessment of Property/Casualty Insurance Companies in the United States A presentation by Robert F. Conger Past-President, Casualty Actuarial Society September 2013 Regulatory Solvency

Regulatory Solvency Assessment of Property/Casualty Insurance Companies in the United States A presentation by Robert F. Conger Past-President, Casualty Actuarial Society September 2013 Regulatory Solvency

Insurance Guidance Note No. 14 System of Governance - Insurance Transition to Governance Requirements established under the Solvency II Directive

Insurance Guidance Note No. 14 Transition to Governance Requirements established under the Solvency II Directive Date of Paper : 31 December 2013 Version Number : V1.00 Table of Contents General governance

Insurance Guidance Note No. 14 Transition to Governance Requirements established under the Solvency II Directive Date of Paper : 31 December 2013 Version Number : V1.00 Table of Contents General governance

Risk Management & ORSA. kpmg.ca/insuranceconference2014

Risk Management & ORSA kpmg.ca/insuranceconference2014 Agenda What s happening globally Benchmarking Results U.K., Canada Maturity observations by area Challenges in completing and developing the ORSA

Risk Management & ORSA kpmg.ca/insuranceconference2014 Agenda What s happening globally Benchmarking Results U.K., Canada Maturity observations by area Challenges in completing and developing the ORSA

RISK MANAGEMENT OVERVIEW 2011 RISK CONFERENCE SPONSORED BY THE FEDERAL RESERVE BANK OF CHICAGO AND DEPAUL UNIVERSITY

RISK MANAGEMENT OVERVIEW 2011 RISK CONFERENCE SPONSORED BY THE FEDERAL RESERVE BANK OF CHICAGO AND DEPAUL UNIVERSITY PRESENTED BY: LEN WIATR, CHIEF RISK OFFICER Len s Risk Management Philosophy Build a

RISK MANAGEMENT OVERVIEW 2011 RISK CONFERENCE SPONSORED BY THE FEDERAL RESERVE BANK OF CHICAGO AND DEPAUL UNIVERSITY PRESENTED BY: LEN WIATR, CHIEF RISK OFFICER Len s Risk Management Philosophy Build a

SOLVENCY II LIFE INSURANCE

2016 Solvency II Life SOLVENCY II LIFE INSURANCE 1 Overview 1.1 Background and scope The key objectives of Solvency II were to increase the level of harmonisation of solvency regulation across Europe,

2016 Solvency II Life SOLVENCY II LIFE INSURANCE 1 Overview 1.1 Background and scope The key objectives of Solvency II were to increase the level of harmonisation of solvency regulation across Europe,

CRO Guide to Solvency II

CRO Guide to Solvency II The journey from complexity to best practice October 2012 Empower Results Contents Introduction 1 Pillar 1 Solvency II Ratio Capital Planning: Best Practice Under Solvency II 2

CRO Guide to Solvency II The journey from complexity to best practice October 2012 Empower Results Contents Introduction 1 Pillar 1 Solvency II Ratio Capital Planning: Best Practice Under Solvency II 2