The Greeks Vega. Outline: Explanation of the greeks. Using greeks for short term prediction. How to find vega. Factors influencing vega.

|

|

|

- Delphia Greene

- 8 years ago

- Views:

Transcription

1 The Greeks Vega 1

2 1 The Greeks Vega Outline: Explanation of the greeks. Using greeks for short term prediction. How to find vega. Factors influencing vega.

3 2 Outline continued: Using greeks to shield your portfolio Vega neutral Making both delta and vega neutral Volatility over time.

4 3 What are the Greeks What are the greeks and why be concerned with them? Two reasons: the direction in which an option trade is about to head is predicted by the greeks (given a change in the market); greeks show how to protect your position against adverse movements in critical market variables.

5 4 Black Scholes Price Factors The price C of an option (or combination of options) depends on: BS Factor Corresponding Greek Mathematically share price, S delta C/ S time to expiry, T theta Θ C/ T volatility, σ vega ν C/ σ risk-free rate, r rho ρ C/ r strike price, X no greek, xed This table pairs up each primary greek with the factor it controls. As you can see, delta relates to the price of the

6 5 underlying, vega relates to the volatility of the underlying and so on. But what is the relationship? In fact, delta is a number that tells in what direction and to what extent the option price will move if there is a positive unit change in the stock price, in the stock price only. Similarly, vega is a number that tells in what direction and to what extent the option price will move if there is a positive 1% change in the volatility, and only in the volatility.

7 6 Vega Example For example, consider a 3-month call option with strike price $50 on a stock currently at $50. Assume the current volatility is 40%. The option costs $4.21 and its vega is Since vega is positive, the option price will go up if the volatility goes up; and it will go up by 10 cents for every one percent gain in volatility. (At least for awhile.) Conversely, the option price will retreat by 10 cents for every one percent loss in volatility.

8 7 In fact in this example, with the volatility at 41%, the option price is indeed $4.31. In this same example, if volatility goes up to 50%, the option price goes to $5.19 (not quite $1, vega is now at 0.098).

9 8 Miscellaneous Facts about Vega Vega is always positive, and, moreover, is the same value for puts as for calls; thus option prices always increase as the volatility does. Of course, the vega of a short position is negative. Vega for a portfolio is the sum of the vegas of its constituents. Vega is important to consider for straddles and calendar spreads.

10 9 Black-Scholes Formula for Vega ν = S T 2π e ( log(s/x)+(r+σ 2 /2)T) 2/(2σ 2 T ) or, in the Black-Scholes d 1 notation, ν = S T φ(d 1 ), φ() is the normal density

, φ() is the normal density")

11 10 Factors Influencing Vega As vega becomes smaller, volatility has less effect on the option price. In the example, if vega were 0.05 instead of 0.10, then the option price will increase only half as much. The size of vega itself mainly depends on the relative value between the stock price and the strike price and on the time to expiry of the option. In the following figure we show the dependence of vega on time to expiry.

12 Vega changes with Time to Expiry 11

13 Vega changes with Stock Price 12

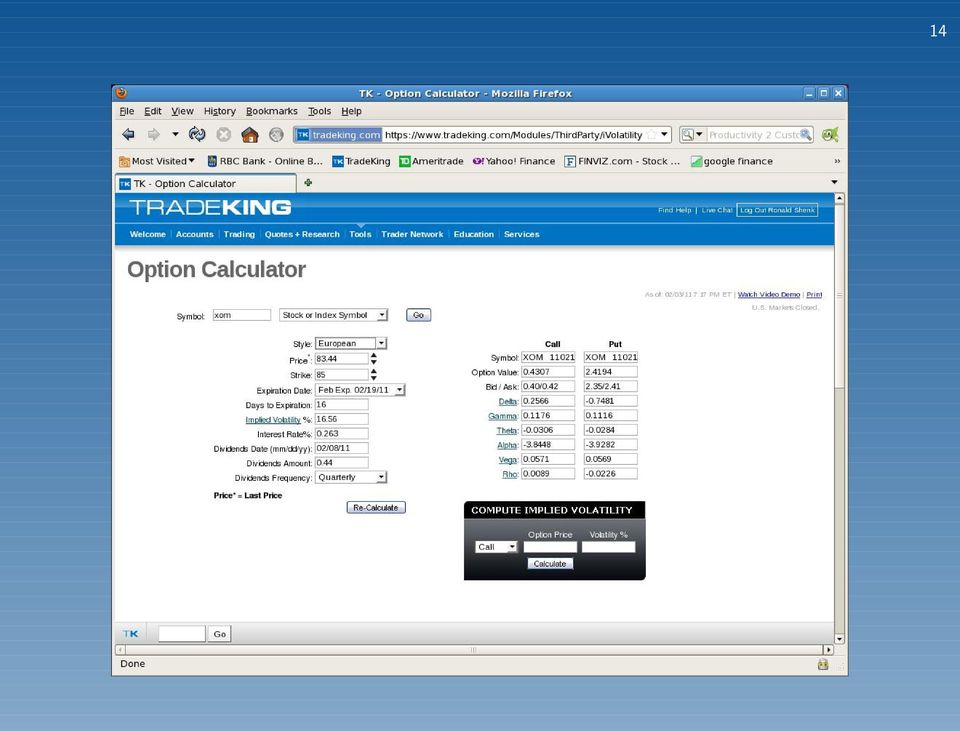

14 13 How to find Vega To figure vega for your portfolio, find vega for all the components and add them up for your long positions and subtract for your short ones, Weight each according to its number of contracts. To find vega for each component, consult your broker s web page. On the next slide I show TradeKing s. I could find no non-login web site calculating vega given an option contract, but there are several that calculate the greeks provided you enter all the relevant information. E.g.

15 14

16 15 The Greeks as a Shield The most famous use of a greek to protect your position from market movements is delta hedging. By making your portfolio delta neutral you are protected to a degree from modest price movements. Similarly if you want to protect yourself from modest volatility movements you make your position vega neutral. But the vega of a stock is 0 so one cannot achieve vega neutrality by shorting stock. It is necessary to short some

17 16 other option to achieve it. Suppose your current portfolio has a vega of ν 0 and you are willing to take a negative position in another derivative whose per unit vega ν A. Shorting w units of the addition makes the combined portfolio vega neutral if w = ν 0 ν A.

18 17 Delta and Vega Neutral Suppose our original portfolio has a delta of 0 and a vega of ν 0 0. We add to the portfolio by shorting w units an option with vega equal to ν A. But now our new portfolio is no longer delta neutral, instead it has a delta of w A where A is the delta of added option (could be negative). We must therefore buy w A shares of A (sell if A is negative) to make the new portfolio both delta and vega neutral.

.")

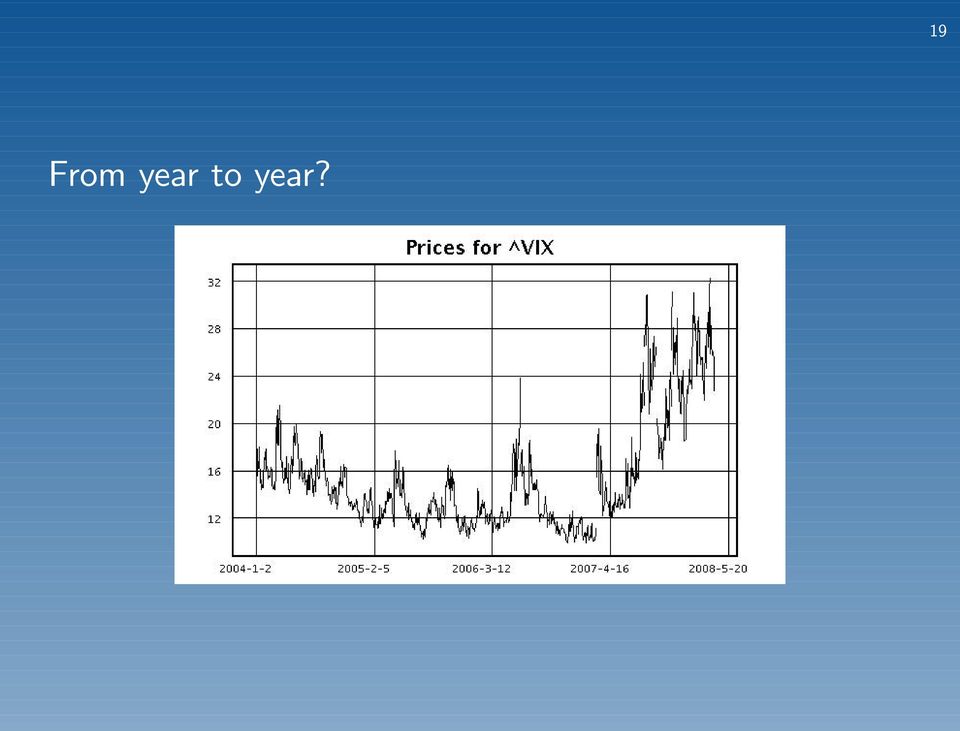

19 18 Volatility Over Time Does volatility really change much from day to day?

20 From year to year? 19

21 Can VIX (volatility trends) foretell of pending trouble? 20

14 Greeks Letters and Hedging

ECG590I Asset Pricing. Lecture 14: Greeks Letters and Hedging 1 14 Greeks Letters and Hedging 14.1 Illustration We consider the following example through out this section. A financial institution sold

ECG590I Asset Pricing. Lecture 14: Greeks Letters and Hedging 1 14 Greeks Letters and Hedging 14.1 Illustration We consider the following example through out this section. A financial institution sold

Hedging. An Undergraduate Introduction to Financial Mathematics. J. Robert Buchanan. J. Robert Buchanan Hedging

Hedging An Undergraduate Introduction to Financial Mathematics J. Robert Buchanan 2010 Introduction Definition Hedging is the practice of making a portfolio of investments less sensitive to changes in

Hedging An Undergraduate Introduction to Financial Mathematics J. Robert Buchanan 2010 Introduction Definition Hedging is the practice of making a portfolio of investments less sensitive to changes in

GAMMA.0279 THETA 8.9173 VEGA 9.9144 RHO 3.5985

14 Option Sensitivities and Option Hedging Answers to Questions and Problems 1. Consider Call A, with: X $70; r 0.06; T t 90 days; 0.4; and S $60. Compute the price, DELTA, GAMMA, THETA, VEGA, and RHO

14 Option Sensitivities and Option Hedging Answers to Questions and Problems 1. Consider Call A, with: X $70; r 0.06; T t 90 days; 0.4; and S $60. Compute the price, DELTA, GAMMA, THETA, VEGA, and RHO

Week 13 Introduction to the Greeks and Portfolio Management:

Week 13 Introduction to the Greeks and Portfolio Management: Hull, Ch. 17; Poitras, Ch.9: I, IIA, IIB, III. 1 Introduction to the Greeks and Portfolio Management Objective: To explain how derivative portfolios

Week 13 Introduction to the Greeks and Portfolio Management: Hull, Ch. 17; Poitras, Ch.9: I, IIA, IIB, III. 1 Introduction to the Greeks and Portfolio Management Objective: To explain how derivative portfolios

Chapters 15. Delta Hedging with Black-Scholes Model. Joel R. Barber. Department of Finance. Florida International University.

Chapters 15 Delta Hedging with Black-Scholes Model Joel R. Barber Department of Finance Florida International University Miami, FL 33199 1 Hedging Example A bank has sold for $300,000 a European call option

Chapters 15 Delta Hedging with Black-Scholes Model Joel R. Barber Department of Finance Florida International University Miami, FL 33199 1 Hedging Example A bank has sold for $300,000 a European call option

Underlier Filters Category Data Field Description

Price//Capitalization Market Capitalization The market price of an entire company, calculated by multiplying the number of shares outstanding by the price per share. Market Capitalization is not applicable

Price//Capitalization Market Capitalization The market price of an entire company, calculated by multiplying the number of shares outstanding by the price per share. Market Capitalization is not applicable

Option pricing in detail

Course #: Title Module 2 Option pricing in detail Topic 1: Influences on option prices - recap... 3 Which stock to buy?... 3 Intrinsic value and time value... 3 Influences on option premiums... 4 Option

Course #: Title Module 2 Option pricing in detail Topic 1: Influences on option prices - recap... 3 Which stock to buy?... 3 Intrinsic value and time value... 3 Influences on option premiums... 4 Option

VALUATION IN DERIVATIVES MARKETS

VALUATION IN DERIVATIVES MARKETS September 2005 Rawle Parris ABN AMRO Property Derivatives What is a Derivative? A contract that specifies the rights and obligations between two parties to receive or deliver

VALUATION IN DERIVATIVES MARKETS September 2005 Rawle Parris ABN AMRO Property Derivatives What is a Derivative? A contract that specifies the rights and obligations between two parties to receive or deliver

Hedging Illiquid FX Options: An Empirical Analysis of Alternative Hedging Strategies

Hedging Illiquid FX Options: An Empirical Analysis of Alternative Hedging Strategies Drazen Pesjak Supervised by A.A. Tsvetkov 1, D. Posthuma 2 and S.A. Borovkova 3 MSc. Thesis Finance HONOURS TRACK Quantitative

Hedging Illiquid FX Options: An Empirical Analysis of Alternative Hedging Strategies Drazen Pesjak Supervised by A.A. Tsvetkov 1, D. Posthuma 2 and S.A. Borovkova 3 MSc. Thesis Finance HONOURS TRACK Quantitative

How To Understand The Greeks

ETF Trend Trading Option Basics Part Two The Greeks Option Basics Separate Sections 1. Option Basics 2. The Greeks 3. Pricing 4. Types of Option Trades The Greeks A simple perspective on the 5 Greeks 1.

ETF Trend Trading Option Basics Part Two The Greeks Option Basics Separate Sections 1. Option Basics 2. The Greeks 3. Pricing 4. Types of Option Trades The Greeks A simple perspective on the 5 Greeks 1.

OPTIONS CALCULATOR QUICK GUIDE. Reshaping Canada s Equities Trading Landscape

OPTIONS CALCULATOR QUICK GUIDE Reshaping Canada s Equities Trading Landscape OCTOBER 2014 Table of Contents Introduction 3 Valuing options 4 Examples 6 Valuing an American style non-dividend paying stock

OPTIONS CALCULATOR QUICK GUIDE Reshaping Canada s Equities Trading Landscape OCTOBER 2014 Table of Contents Introduction 3 Valuing options 4 Examples 6 Valuing an American style non-dividend paying stock

Caput Derivatives: October 30, 2003

Caput Derivatives: October 30, 2003 Exam + Answers Total time: 2 hours and 30 minutes. Note 1: You are allowed to use books, course notes, and a calculator. Question 1. [20 points] Consider an investor

Caput Derivatives: October 30, 2003 Exam + Answers Total time: 2 hours and 30 minutes. Note 1: You are allowed to use books, course notes, and a calculator. Question 1. [20 points] Consider an investor

Steve Meizinger. FX Options Pricing, what does it Mean?

Steve Meizinger FX Options Pricing, what does it Mean? For the sake of simplicity, the examples that follow do not take into consideration commissions and other transaction fees, tax considerations, or

Steve Meizinger FX Options Pricing, what does it Mean? For the sake of simplicity, the examples that follow do not take into consideration commissions and other transaction fees, tax considerations, or

FINANCIAL ENGINEERING CLUB TRADING 201

FINANCIAL ENGINEERING CLUB TRADING 201 STOCK PRICING It s all about volatility Volatility is the measure of how much a stock moves The implied volatility (IV) of a stock represents a 1 standard deviation

FINANCIAL ENGINEERING CLUB TRADING 201 STOCK PRICING It s all about volatility Volatility is the measure of how much a stock moves The implied volatility (IV) of a stock represents a 1 standard deviation

How to use the Options/Warrants Calculator?

How to use the Options/Warrants Calculator? 1. Introduction Options/Warrants Calculator is a tool for users to estimate the theoretical prices of options/warrants in various market conditions by inputting

How to use the Options/Warrants Calculator? 1. Introduction Options/Warrants Calculator is a tool for users to estimate the theoretical prices of options/warrants in various market conditions by inputting

1 The Black-Scholes model: extensions and hedging

1 The Black-Scholes model: extensions and hedging 1.1 Dividends Since we are now in a continuous time framework the dividend paid out at time t (or t ) is given by dd t = D t D t, where as before D denotes

1 The Black-Scholes model: extensions and hedging 1.1 Dividends Since we are now in a continuous time framework the dividend paid out at time t (or t ) is given by dd t = D t D t, where as before D denotes

Options/1. Prof. Ian Giddy

Options/1 New York University Stern School of Business Options Prof. Ian Giddy New York University Options Puts and Calls Put-Call Parity Combinations and Trading Strategies Valuation Hedging Options2

Options/1 New York University Stern School of Business Options Prof. Ian Giddy New York University Options Puts and Calls Put-Call Parity Combinations and Trading Strategies Valuation Hedging Options2

Options: Valuation and (No) Arbitrage

Arbitrage") Prof. Alex Shapiro Lecture Notes 15 Options: Valuation and (No) Arbitrage I. Readings and Suggested Practice Problems II. Introduction: Objectives and Notation III. No Arbitrage Pricing Bound IV. The Binomial

Prof. Alex Shapiro Lecture Notes 15 Options: Valuation and (No) Arbitrage I. Readings and Suggested Practice Problems II. Introduction: Objectives and Notation III. No Arbitrage Pricing Bound IV. The Binomial

http://www.infinity100.com

http://www.infinity100.com THE GREEKS MANAGING AND PROFITING FROM DELTA, VEGA, THETA, GAMMA RISK THE 'GREEKS' RISK MANGEMENT GRID Line Max Profit? * VEGA POSITION 1 Long Vega 2 3, 4 Short Vega Long Vega

http://www.infinity100.com THE GREEKS MANAGING AND PROFITING FROM DELTA, VEGA, THETA, GAMMA RISK THE 'GREEKS' RISK MANGEMENT GRID Line Max Profit? * VEGA POSITION 1 Long Vega 2 3, 4 Short Vega Long Vega

Vanna-Volga Method for Foreign Exchange Implied Volatility Smile. Copyright Changwei Xiong 2011. January 2011. last update: Nov 27, 2013

Vanna-Volga Method for Foreign Exchange Implied Volatility Smile Copyright Changwei Xiong 011 January 011 last update: Nov 7, 01 TABLE OF CONTENTS TABLE OF CONTENTS...1 1. Trading Strategies of Vanilla

Vanna-Volga Method for Foreign Exchange Implied Volatility Smile Copyright Changwei Xiong 011 January 011 last update: Nov 7, 01 TABLE OF CONTENTS TABLE OF CONTENTS...1 1. Trading Strategies of Vanilla

The Binomial Option Pricing Model André Farber

1 Solvay Business School Université Libre de Bruxelles The Binomial Option Pricing Model André Farber January 2002 Consider a non-dividend paying stock whose price is initially S 0. Divide time into small

1 Solvay Business School Université Libre de Bruxelles The Binomial Option Pricing Model André Farber January 2002 Consider a non-dividend paying stock whose price is initially S 0. Divide time into small

Pricing Options: Pricing Options: The Binomial Way FINC 456. The important slide. Pricing options really boils down to three key concepts

Pricing Options: The Binomial Way FINC 456 Pricing Options: The important slide Pricing options really boils down to three key concepts Two portfolios that have the same payoff cost the same. Why? A perfectly

Pricing Options: The Binomial Way FINC 456 Pricing Options: The important slide Pricing options really boils down to three key concepts Two portfolios that have the same payoff cost the same. Why? A perfectly

Lecture 21 Options Pricing

Lecture 21 Options Pricing Readings BM, chapter 20 Reader, Lecture 21 M. Spiegel and R. Stanton, 2000 1 Outline Last lecture: Examples of options Derivatives and risk (mis)management Replication and Put-call

Lecture 21 Options Pricing Readings BM, chapter 20 Reader, Lecture 21 M. Spiegel and R. Stanton, 2000 1 Outline Last lecture: Examples of options Derivatives and risk (mis)management Replication and Put-call

Black-Scholes model: Greeks - sensitivity analysis

VII. Black-Scholes model: Greeks- sensitivity analysis p. 1/15 VII. Black-Scholes model: Greeks - sensitivity analysis Beáta Stehlíková Financial derivatives, winter term 2014/2015 Faculty of Mathematics,

VII. Black-Scholes model: Greeks- sensitivity analysis p. 1/15 VII. Black-Scholes model: Greeks - sensitivity analysis Beáta Stehlíková Financial derivatives, winter term 2014/2015 Faculty of Mathematics,

Finance 436 Futures and Options Review Notes for Final Exam. Chapter 9

Finance 436 Futures and Options Review Notes for Final Exam Chapter 9 1. Options: call options vs. put options, American options vs. European options 2. Characteristics: option premium, option type, underlying

Finance 436 Futures and Options Review Notes for Final Exam Chapter 9 1. Options: call options vs. put options, American options vs. European options 2. Characteristics: option premium, option type, underlying

Steve Meizinger. Understanding the FX Option Greeks

Steve Meizinger Understanding the FX Option Greeks For the sake of simplicity, the examples that follow do not take into consideration commissions and other transaction fees, tax considerations, or margin

Steve Meizinger Understanding the FX Option Greeks For the sake of simplicity, the examples that follow do not take into consideration commissions and other transaction fees, tax considerations, or margin

Call Price as a Function of the Stock Price

Call Price as a Function of the Stock Price Intuitively, the call price should be an increasing function of the stock price. This relationship allows one to develop a theory of option pricing, derived

Call Price as a Function of the Stock Price Intuitively, the call price should be an increasing function of the stock price. This relationship allows one to develop a theory of option pricing, derived

Chapter 11 Options. Main Issues. Introduction to Options. Use of Options. Properties of Option Prices. Valuation Models of Options.

Chapter 11 Options Road Map Part A Introduction to finance. Part B Valuation of assets, given discount rates. Part C Determination of risk-adjusted discount rate. Part D Introduction to derivatives. Forwards

Chapter 11 Options Road Map Part A Introduction to finance. Part B Valuation of assets, given discount rates. Part C Determination of risk-adjusted discount rate. Part D Introduction to derivatives. Forwards

Don t be Intimidated by the Greeks, Part 2 August 29, 2013 Joe Burgoyne, OIC

Don t be Intimidated by the Greeks, Part 2 August 29, 2013 Joe Burgoyne, OIC www.optionseducation.org 2 The Options Industry Council Options involve risks and are not suitable for everyone. Prior to buying

Don t be Intimidated by the Greeks, Part 2 August 29, 2013 Joe Burgoyne, OIC www.optionseducation.org 2 The Options Industry Council Options involve risks and are not suitable for everyone. Prior to buying

Lecture 11: The Greeks and Risk Management

Lecture 11: The Greeks and Risk Management This lecture studies market risk management from the perspective of an options trader. First, we show how to describe the risk characteristics of derivatives.

Lecture 11: The Greeks and Risk Management This lecture studies market risk management from the perspective of an options trader. First, we show how to describe the risk characteristics of derivatives.

Does Black-Scholes framework for Option Pricing use Constant Volatilities and Interest Rates? New Solution for a New Problem

Does Black-Scholes framework for Option Pricing use Constant Volatilities and Interest Rates? New Solution for a New Problem Gagan Deep Singh Assistant Vice President Genpact Smart Decision Services Financial

Does Black-Scholes framework for Option Pricing use Constant Volatilities and Interest Rates? New Solution for a New Problem Gagan Deep Singh Assistant Vice President Genpact Smart Decision Services Financial

Two-State Option Pricing

Rendleman and Bartter [1] present a simple two-state model of option pricing. The states of the world evolve like the branches of a tree. Given the current state, there are two possible states next period.

Rendleman and Bartter [1] present a simple two-state model of option pricing. The states of the world evolve like the branches of a tree. Given the current state, there are two possible states next period.

CFD Options Trade and Margin Examples

CFD Options Trade and Margin Examples Example Trades Buying a call Market: UK 100 (current price 6330) View: UK 100 to rise before mid June. Instrument: UK100 Jun Call 6600 (current price 30) Position:

CFD Options Trade and Margin Examples Example Trades Buying a call Market: UK 100 (current price 6330) View: UK 100 to rise before mid June. Instrument: UK100 Jun Call 6600 (current price 30) Position:

An Introduction to Exotic Options

An Introduction to Exotic Options Jeff Casey Jeff Casey is entering his final semester of undergraduate studies at Ball State University. He is majoring in Financial Mathematics and has been a math tutor

An Introduction to Exotic Options Jeff Casey Jeff Casey is entering his final semester of undergraduate studies at Ball State University. He is majoring in Financial Mathematics and has been a math tutor

Swing Trade Warrior Chapter 1. Introduction to swing trading and how to understand and use options How does Swing Trading Work? The idea behind swing trading is to capitalize on short term moves of stocks

Swing Trade Warrior Chapter 1. Introduction to swing trading and how to understand and use options How does Swing Trading Work? The idea behind swing trading is to capitalize on short term moves of stocks

Return to Risk Limited website: www.risklimited.com. Overview of Options An Introduction

Return to Risk Limited website: www.risklimited.com Overview of Options An Introduction Options Definition The right, but not the obligation, to enter into a transaction [buy or sell] at a pre-agreed price,

Return to Risk Limited website: www.risklimited.com Overview of Options An Introduction Options Definition The right, but not the obligation, to enter into a transaction [buy or sell] at a pre-agreed price,

BINOMIAL OPTION PRICING

Darden Graduate School of Business Administration University of Virginia BINOMIAL OPTION PRICING Binomial option pricing is a simple but powerful technique that can be used to solve many complex option-pricing

Darden Graduate School of Business Administration University of Virginia BINOMIAL OPTION PRICING Binomial option pricing is a simple but powerful technique that can be used to solve many complex option-pricing

Trading Strategies Involving Options. Chapter 11

Trading Strategies Involving Options Chapter 11 1 Strategies to be Considered A risk-free bond and an option to create a principal-protected note A stock and an option Two or more options of the same type

Trading Strategies Involving Options Chapter 11 1 Strategies to be Considered A risk-free bond and an option to create a principal-protected note A stock and an option Two or more options of the same type

On Black-Scholes Equation, Black- Scholes Formula and Binary Option Price

On Black-Scholes Equation, Black- Scholes Formula and Binary Option Price Abstract: Chi Gao 12/15/2013 I. Black-Scholes Equation is derived using two methods: (1) risk-neutral measure; (2) - hedge. II.

On Black-Scholes Equation, Black- Scholes Formula and Binary Option Price Abstract: Chi Gao 12/15/2013 I. Black-Scholes Equation is derived using two methods: (1) risk-neutral measure; (2) - hedge. II.

Figure S9.1 Profit from long position in Problem 9.9

Problem 9.9 Suppose that a European call option to buy a share for $100.00 costs $5.00 and is held until maturity. Under what circumstances will the holder of the option make a profit? Under what circumstances

Problem 9.9 Suppose that a European call option to buy a share for $100.00 costs $5.00 and is held until maturity. Under what circumstances will the holder of the option make a profit? Under what circumstances

CHAPTER 21: OPTION VALUATION

CHAPTER 21: OPTION VALUATION 1. Put values also must increase as the volatility of the underlying stock increases. We see this from the parity relation as follows: P = C + PV(X) S 0 + PV(Dividends). Given

CHAPTER 21: OPTION VALUATION 1. Put values also must increase as the volatility of the underlying stock increases. We see this from the parity relation as follows: P = C + PV(X) S 0 + PV(Dividends). Given

Research on Option Trading Strategies

Research on Option Trading Strategies An Interactive Qualifying Project Report: Submitted to the Faculty of the WORCESTER POLYTECHNIC INSTITUTE In partial fulfillment of the requirements for the Degree

Research on Option Trading Strategies An Interactive Qualifying Project Report: Submitted to the Faculty of the WORCESTER POLYTECHNIC INSTITUTE In partial fulfillment of the requirements for the Degree

TABLE OF CONTENTS. Introduction Delta Delta as Hedge Ratio Gamma Other Letters Appendix

GLOBAL TABLE OF CONTENTS Introduction Delta Delta as Hedge Ratio Gamma Other Letters Appendix 3 4 5 7 9 10 HIGH RISK WARNING: Before you decide to trade either foreign currency ( Forex ) or options, carefully

GLOBAL TABLE OF CONTENTS Introduction Delta Delta as Hedge Ratio Gamma Other Letters Appendix 3 4 5 7 9 10 HIGH RISK WARNING: Before you decide to trade either foreign currency ( Forex ) or options, carefully

Option pricing. Vinod Kothari

Option pricing Vinod Kothari Notation we use this Chapter will be as follows: S o : Price of the share at time 0 S T : Price of the share at time T T : time to maturity of the option r : risk free rate

Option pricing Vinod Kothari Notation we use this Chapter will be as follows: S o : Price of the share at time 0 S T : Price of the share at time T T : time to maturity of the option r : risk free rate

CHAPTER 15. Option Valuation

CHAPTER 15 Option Valuation Just what is an option worth? Actually, this is one of the more difficult questions in finance. Option valuation is an esoteric area of finance since it often involves complex

CHAPTER 15 Option Valuation Just what is an option worth? Actually, this is one of the more difficult questions in finance. Option valuation is an esoteric area of finance since it often involves complex

CURRENCY OPTION PRICING II

Jones Grauate School Rice University Masa Watanabe INTERNATIONAL FINANCE MGMT 657 Calibrating the Binomial Tree to Volatility Black-Scholes Moel for Currency Options Properties of the BS Moel Option Sensitivity

Jones Grauate School Rice University Masa Watanabe INTERNATIONAL FINANCE MGMT 657 Calibrating the Binomial Tree to Volatility Black-Scholes Moel for Currency Options Properties of the BS Moel Option Sensitivity

Derivatives: Options

Derivatives: Options Call Option: The right, but not the obligation, to buy an asset at a specified exercise (or, strike) price on or before a specified date. Put Option: The right, but not the obligation,

Derivatives: Options Call Option: The right, but not the obligation, to buy an asset at a specified exercise (or, strike) price on or before a specified date. Put Option: The right, but not the obligation,

Pair Trading with Options

Pair Trading with Options Jeff Donaldson, Ph.D., CFA University of Tampa Donald Flagg, Ph.D. University of Tampa Ashley Northrup University of Tampa Student Type of Research: Pedagogy Disciplines of Interest:

Pair Trading with Options Jeff Donaldson, Ph.D., CFA University of Tampa Donald Flagg, Ph.D. University of Tampa Ashley Northrup University of Tampa Student Type of Research: Pedagogy Disciplines of Interest:

UCLA Anderson School of Management Daniel Andrei, Derivative Markets 237D, Winter 2014. MFE Midterm. February 2014. Date:

UCLA Anderson School of Management Daniel Andrei, Derivative Markets 237D, Winter 2014 MFE Midterm February 2014 Date: Your Name: Your Equiz.me email address: Your Signature: 1 This exam is open book,

UCLA Anderson School of Management Daniel Andrei, Derivative Markets 237D, Winter 2014 MFE Midterm February 2014 Date: Your Name: Your Equiz.me email address: Your Signature: 1 This exam is open book,

Valuing Stock Options: The Black-Scholes-Merton Model. Chapter 13

Valuing Stock Options: The Black-Scholes-Merton Model Chapter 13 Fundamentals of Futures and Options Markets, 8th Ed, Ch 13, Copyright John C. Hull 2013 1 The Black-Scholes-Merton Random Walk Assumption

Valuing Stock Options: The Black-Scholes-Merton Model Chapter 13 Fundamentals of Futures and Options Markets, 8th Ed, Ch 13, Copyright John C. Hull 2013 1 The Black-Scholes-Merton Random Walk Assumption

Chapter 3.4. Forex Options

Chapter 3.4 Forex Options 0 Contents FOREX OPTIONS Forex options are the next frontier in forex trading. Forex options give you just what their name suggests: options in your forex trading. If you have

Chapter 3.4 Forex Options 0 Contents FOREX OPTIONS Forex options are the next frontier in forex trading. Forex options give you just what their name suggests: options in your forex trading. If you have

Fundamentals of Futures and Options (a summary)

") Fundamentals of Futures and Options (a summary) Roger G. Clarke, Harindra de Silva, CFA, and Steven Thorley, CFA Published 2013 by the Research Foundation of CFA Institute Summary prepared by Roger G.

Fundamentals of Futures and Options (a summary) Roger G. Clarke, Harindra de Silva, CFA, and Steven Thorley, CFA Published 2013 by the Research Foundation of CFA Institute Summary prepared by Roger G.

Financial Options: Pricing and Hedging

Financial Options: Pricing and Hedging Diagrams Debt Equity Value of Firm s Assets T Value of Firm s Assets T Valuation of distressed debt and equity-linked securities requires an understanding of financial

Financial Options: Pricing and Hedging Diagrams Debt Equity Value of Firm s Assets T Value of Firm s Assets T Valuation of distressed debt and equity-linked securities requires an understanding of financial

Goals. Options. Derivatives: Definition. Goals. Definitions Options. Spring 2007 Lecture Notes 4.6.1 Readings:Mayo 28.

Goals Options Spring 27 Lecture Notes 4.6.1 Readings:Mayo 28 Definitions Options Call option Put option Option strategies Derivatives: Definition Derivative: Any security whose payoff depends on any other

Goals Options Spring 27 Lecture Notes 4.6.1 Readings:Mayo 28 Definitions Options Call option Put option Option strategies Derivatives: Definition Derivative: Any security whose payoff depends on any other

More on Market-Making and Delta-Hedging

More on Market-Making and Delta-Hedging What do market makers do to delta-hedge? Recall that the delta-hedging strategy consists of selling one option, and buying a certain number shares An example of

More on Market-Making and Delta-Hedging What do market makers do to delta-hedge? Recall that the delta-hedging strategy consists of selling one option, and buying a certain number shares An example of

Options, Derivatives, Risk Management

1/1 Options, Derivatives, Risk Management (Welch, Chapter 27) Ivo Welch UCLA Anderson School, Corporate Finance, Winter 2014 January 13, 2015 Did you bring your calculator? Did you read these notes and

1/1 Options, Derivatives, Risk Management (Welch, Chapter 27) Ivo Welch UCLA Anderson School, Corporate Finance, Winter 2014 January 13, 2015 Did you bring your calculator? Did you read these notes and

Overview. Option Basics. Options and Derivatives. Professor Lasse H. Pedersen. Option basics and option strategies

Options and Derivatives Professor Lasse H. Pedersen Prof. Lasse H. Pedersen 1 Overview Option basics and option strategies No-arbitrage bounds on option prices Binomial option pricing Black-Scholes-Merton

Options and Derivatives Professor Lasse H. Pedersen Prof. Lasse H. Pedersen 1 Overview Option basics and option strategies No-arbitrage bounds on option prices Binomial option pricing Black-Scholes-Merton

Summary of Interview Questions. 1. Does it matter if a company uses forwards, futures or other derivatives when hedging FX risk?

Summary of Interview Questions 1. Does it matter if a company uses forwards, futures or other derivatives when hedging FX risk? 2. Give me an example of how a company can use derivative instruments to

Summary of Interview Questions 1. Does it matter if a company uses forwards, futures or other derivatives when hedging FX risk? 2. Give me an example of how a company can use derivative instruments to

Understanding Options and Their Role in Hedging via the Greeks

Understanding Options and Their Role in Hedging via the Greeks Bradley J. Wogsland Department of Physics and Astronomy, University of Tennessee, Knoxville, TN 37996-1200 Options are priced assuming that

Understanding Options and Their Role in Hedging via the Greeks Bradley J. Wogsland Department of Physics and Astronomy, University of Tennessee, Knoxville, TN 37996-1200 Options are priced assuming that

CHAPTER 21: OPTION VALUATION

CHAPTER 21: OPTION VALUATION PROBLEM SETS 1. The value of a put option also increases with the volatility of the stock. We see this from the put-call parity theorem as follows: P = C S + PV(X) + PV(Dividends)

CHAPTER 21: OPTION VALUATION PROBLEM SETS 1. The value of a put option also increases with the volatility of the stock. We see this from the put-call parity theorem as follows: P = C S + PV(X) + PV(Dividends)

Trading Options MICHAEL BURKE

Trading Options MICHAEL BURKE Table of Contents Important Information and Disclosures... 3 Options Risk Disclosure... 4 Prologue... 5 The Benefits of Trading Options... 6 Options Trading Primer... 8 Options

Trading Options MICHAEL BURKE Table of Contents Important Information and Disclosures... 3 Options Risk Disclosure... 4 Prologue... 5 The Benefits of Trading Options... 6 Options Trading Primer... 8 Options

The Call Option. Options Boot Camp Part 2

Options Boot Camp Part 2 About Sunset Partners Our Presenters Today Robert Hamer, Principal Chief Investment Strategist & Portfolio Manager Experience Trader Chicago Board Options Exchange: 1983-1998 Senior

Options Boot Camp Part 2 About Sunset Partners Our Presenters Today Robert Hamer, Principal Chief Investment Strategist & Portfolio Manager Experience Trader Chicago Board Options Exchange: 1983-1998 Senior

Option Spread and Combination Trading

Option Spread and Combination Trading J. Scott Chaput* Louis H. Ederington** January 2002 Initial Draft: January 2000 * University of Otago ** Until 31 January, 2002: Department of Finance Visiting Professor,

Option Spread and Combination Trading J. Scott Chaput* Louis H. Ederington** January 2002 Initial Draft: January 2000 * University of Otago ** Until 31 January, 2002: Department of Finance Visiting Professor,

A Day in the Life of a Trader

Siena, April 2014 Introduction 1 Examples of Market Payoffs 2 3 4 Sticky Smile e Floating Smile 5 Examples of Market Payoffs Understanding risk profiles of a payoff is conditio sine qua non for a mathematical

Siena, April 2014 Introduction 1 Examples of Market Payoffs 2 3 4 Sticky Smile e Floating Smile 5 Examples of Market Payoffs Understanding risk profiles of a payoff is conditio sine qua non for a mathematical

Handbook FXFlat FX Options

Handbook FXFlat FX Options FXFlat Trading FX Options When you open an FX options account at FXFlat, you can trade options on currency pairs 24- hours a day, 5.5 days per week. The FX options features in

Handbook FXFlat FX Options FXFlat Trading FX Options When you open an FX options account at FXFlat, you can trade options on currency pairs 24- hours a day, 5.5 days per week. The FX options features in

Institutional Finance 08: Dynamic Arbitrage to Replicate Non-linear Payoffs. Binomial Option Pricing: Basics (Chapter 10 of McDonald)

") Copyright 2003 Pearson Education, Inc. Slide 08-1 Institutional Finance 08: Dynamic Arbitrage to Replicate Non-linear Payoffs Binomial Option Pricing: Basics (Chapter 10 of McDonald) Originally prepared

Copyright 2003 Pearson Education, Inc. Slide 08-1 Institutional Finance 08: Dynamic Arbitrage to Replicate Non-linear Payoffs Binomial Option Pricing: Basics (Chapter 10 of McDonald) Originally prepared

Dimensions Trading Lab. 2004. Sean Tseng. Trading Greeks. Greeks based trading strategies. Sean Tseng s presentation

Trading Greeks Greeks based trading strategies Position and Greeks position Delta Gamma Theta Vega Long + 0 0 0 Short - 0 0 0 Long call + (0 to 1) + - + Long put Short call - (-1 to 0) + - + - (0 to 1)

Trading Greeks Greeks based trading strategies Position and Greeks position Delta Gamma Theta Vega Long + 0 0 0 Short - 0 0 0 Long call + (0 to 1) + - + Long put Short call - (-1 to 0) + - + - (0 to 1)

Trading Options with TradeStation OptionStation

Trading Options with TradeStation OptionStation michael burke Trading Options with TradeStation OptionStation contents Prologue...1 The Benefits of Trading Options...3 Flexibility...3 Options Trading

Trading Options with TradeStation OptionStation michael burke Trading Options with TradeStation OptionStation contents Prologue...1 The Benefits of Trading Options...3 Flexibility...3 Options Trading

Risk Management and Governance Hedging with Derivatives. Prof. Hugues Pirotte

Risk Management and Governance Hedging with Derivatives Prof. Hugues Pirotte Several slides based on Risk Management and Financial Institutions, e, Chapter 6, Copyright John C. Hull 009 Why Manage Risks?

Risk Management and Governance Hedging with Derivatives Prof. Hugues Pirotte Several slides based on Risk Management and Financial Institutions, e, Chapter 6, Copyright John C. Hull 009 Why Manage Risks?

Hedging Barriers. Liuren Wu. Zicklin School of Business, Baruch College (http://faculty.baruch.cuny.edu/lwu/)

") Hedging Barriers Liuren Wu Zicklin School of Business, Baruch College (http://faculty.baruch.cuny.edu/lwu/) Based on joint work with Peter Carr (Bloomberg) Modeling and Hedging Using FX Options, March

Hedging Barriers Liuren Wu Zicklin School of Business, Baruch College (http://faculty.baruch.cuny.edu/lwu/) Based on joint work with Peter Carr (Bloomberg) Modeling and Hedging Using FX Options, March

Sensex Realized Volatility Index

Sensex Realized Volatility Index Introduction: Volatility modelling has traditionally relied on complex econometric procedures in order to accommodate the inherent latent character of volatility. Realized

Sensex Realized Volatility Index Introduction: Volatility modelling has traditionally relied on complex econometric procedures in order to accommodate the inherent latent character of volatility. Realized

WHS FX options guide. Getting started with FX options. Predict the trend in currency markets or hedge your positions with FX options.

Getting started with FX options WHS FX options guide Predict the trend in currency markets or hedge your positions with FX options. Refine your trading style and your market outlook. Learn how FX options

Getting started with FX options WHS FX options guide Predict the trend in currency markets or hedge your positions with FX options. Refine your trading style and your market outlook. Learn how FX options

Volatility as an indicator of Supply and Demand for the Option. the price of a stock expressed as a decimal or percentage.

Option Greeks - Evaluating Option Price Sensitivity to: Price Changes to the Stock Time to Expiration Alterations in Interest Rates Volatility as an indicator of Supply and Demand for the Option Different

Option Greeks - Evaluating Option Price Sensitivity to: Price Changes to the Stock Time to Expiration Alterations in Interest Rates Volatility as an indicator of Supply and Demand for the Option Different

Simplified Option Selection Method

Simplified Option Selection Method Geoffrey VanderPal Webster University Thailand Options traders and investors utilize methods to price and select call and put options. The models and tools range from

Simplified Option Selection Method Geoffrey VanderPal Webster University Thailand Options traders and investors utilize methods to price and select call and put options. The models and tools range from

Call and Put. Options. American and European Options. Option Terminology. Payoffs of European Options. Different Types of Options

Call and Put Options A call option gives its holder the right to purchase an asset for a specified price, called the strike price, on or before some specified expiration date. A put option gives its holder

Call and Put Options A call option gives its holder the right to purchase an asset for a specified price, called the strike price, on or before some specified expiration date. A put option gives its holder

Chapter 7 - Find trades I

Chapter 7 - Find trades I Find Trades I Help Help Guide Click PDF to get a PDF printable version of this help file. Find Trades I is a simple way to find option trades for a single stock. Enter the stock

Chapter 7 - Find trades I Find Trades I Help Help Guide Click PDF to get a PDF printable version of this help file. Find Trades I is a simple way to find option trades for a single stock. Enter the stock

a. What is the portfolio of the stock and the bond that replicates the option?

Practice problems for Lecture 2. Answers. 1. A Simple Option Pricing Problem in One Period Riskless bond (interest rate is 5%): 1 15 Stock: 5 125 5 Derivative security (call option with a strike of 8):?

Practice problems for Lecture 2. Answers. 1. A Simple Option Pricing Problem in One Period Riskless bond (interest rate is 5%): 1 15 Stock: 5 125 5 Derivative security (call option with a strike of 8):?

Exam MFE Spring 2007 FINAL ANSWER KEY 1 B 2 A 3 C 4 E 5 D 6 C 7 E 8 C 9 A 10 B 11 D 12 A 13 E 14 E 15 C 16 D 17 B 18 A 19 D

Exam MFE Spring 2007 FINAL ANSWER KEY Question # Answer 1 B 2 A 3 C 4 E 5 D 6 C 7 E 8 C 9 A 10 B 11 D 12 A 13 E 14 E 15 C 16 D 17 B 18 A 19 D **BEGINNING OF EXAMINATION** ACTUARIAL MODELS FINANCIAL ECONOMICS

Exam MFE Spring 2007 FINAL ANSWER KEY Question # Answer 1 B 2 A 3 C 4 E 5 D 6 C 7 E 8 C 9 A 10 B 11 D 12 A 13 E 14 E 15 C 16 D 17 B 18 A 19 D **BEGINNING OF EXAMINATION** ACTUARIAL MODELS FINANCIAL ECONOMICS

Session X: Lecturer: Dr. Jose Olmo. Module: Economics of Financial Markets. MSc. Financial Economics. Department of Economics, City University, London

Session X: Options: Hedging, Insurance and Trading Strategies Lecturer: Dr. Jose Olmo Module: Economics of Financial Markets MSc. Financial Economics Department of Economics, City University, London Option

Session X: Options: Hedging, Insurance and Trading Strategies Lecturer: Dr. Jose Olmo Module: Economics of Financial Markets MSc. Financial Economics Department of Economics, City University, London Option

2. How is a fund manager motivated to behave with this type of renumeration package?

MØA 155 PROBLEM SET: Options Exercise 1. Arbitrage [2] In the discussions of some of the models in this course, we relied on the following type of argument: If two investment strategies have the same payoff

MØA 155 PROBLEM SET: Options Exercise 1. Arbitrage [2] In the discussions of some of the models in this course, we relied on the following type of argument: If two investment strategies have the same payoff

FINANCIAL ECONOMICS OPTION PRICING

OPTION PRICING Options are contingency contracts that specify payoffs if stock prices reach specified levels. A call option is the right to buy a stock at a specified price, X, called the strike price.

OPTION PRICING Options are contingency contracts that specify payoffs if stock prices reach specified levels. A call option is the right to buy a stock at a specified price, X, called the strike price.

w w w.c a t l e y l a k e m a n.c o m 0 2 0 7 0 4 3 0 1 0 0

A ADR-Style: for a derivative on an underlying denominated in one currency, where the derivative is denominated in a different currency, payments are exchanged using a floating foreign-exchange rate. The

A ADR-Style: for a derivative on an underlying denominated in one currency, where the derivative is denominated in a different currency, payments are exchanged using a floating foreign-exchange rate. The

Lecture 4: The Black-Scholes model

OPTIONS and FUTURES Lecture 4: The Black-Scholes model Philip H. Dybvig Washington University in Saint Louis Black-Scholes option pricing model Lognormal price process Call price Put price Using Black-Scholes

OPTIONS and FUTURES Lecture 4: The Black-Scholes model Philip H. Dybvig Washington University in Saint Louis Black-Scholes option pricing model Lognormal price process Call price Put price Using Black-Scholes

DISTRIBUTION-BASED PRICING FORMULAS ARE NOT ARBITRAGE-FREE DAVID RUHM DISCUSSION BY MICHAEL G. WACEK. Abstract

DISTRIBUTION-BASED PRICING FORMULAS ARE NOT ARBITRAGE-FREE DAVID RUHM DISCUSSION BY MICHAEL G. WACEK Abstract David Ruhm s paper is a welcome addition to the actuarial literature. It illustrates some difficult

DISTRIBUTION-BASED PRICING FORMULAS ARE NOT ARBITRAGE-FREE DAVID RUHM DISCUSSION BY MICHAEL G. WACEK Abstract David Ruhm s paper is a welcome addition to the actuarial literature. It illustrates some difficult

How To Value Options In Black-Scholes Model

Option Pricing Basics Aswath Damodaran Aswath Damodaran 1 What is an option? An option provides the holder with the right to buy or sell a specified quantity of an underlying asset at a fixed price (called

Option Pricing Basics Aswath Damodaran Aswath Damodaran 1 What is an option? An option provides the holder with the right to buy or sell a specified quantity of an underlying asset at a fixed price (called

Options 1 OPTIONS. Introduction

Options 1 OPTIONS Introduction A derivative is a financial instrument whose value is derived from the value of some underlying asset. A call option gives one the right to buy an asset at the exercise or

Options 1 OPTIONS Introduction A derivative is a financial instrument whose value is derived from the value of some underlying asset. A call option gives one the right to buy an asset at the exercise or

About Volatility Index. About India VIX

About Volatility Index Volatility Index is a measure of market s expectation of volatility over the near term. Volatility is often described as the rate and magnitude of changes in prices and in finance

About Volatility Index Volatility Index is a measure of market s expectation of volatility over the near term. Volatility is often described as the rate and magnitude of changes in prices and in finance

FTS Real Time System Project: Using Options to Manage Price Risk

FTS Real Time System Project: Using Options to Manage Price Risk Question: How can you manage price risk using options? Introduction The option Greeks provide measures of sensitivity to price and volatility

FTS Real Time System Project: Using Options to Manage Price Risk Question: How can you manage price risk using options? Introduction The option Greeks provide measures of sensitivity to price and volatility

Volatility Dispersion Presentation for the CBOE Risk Management Conference

Volatility Dispersion Presentation for the CBOE Risk Management Conference Izzy Nelken 3943 Bordeaux Drive Northbrook, IL 60062 (847) 562-0600 www.supercc.com www.optionsprofessor.com Izzy@supercc.com

Volatility Dispersion Presentation for the CBOE Risk Management Conference Izzy Nelken 3943 Bordeaux Drive Northbrook, IL 60062 (847) 562-0600 www.supercc.com www.optionsprofessor.com Izzy@supercc.com

Factors Affecting Option Prices

Factors Affecting Option Prices 1. The current stock price S 0. 2. The option strike price K. 3. The time to expiration T. 4. The volatility of the stock price σ. 5. The risk-free interest rate r. 6. The

Factors Affecting Option Prices 1. The current stock price S 0. 2. The option strike price K. 3. The time to expiration T. 4. The volatility of the stock price σ. 5. The risk-free interest rate r. 6. The

American and European. Put Option

American and European Put Option Analytical Finance I Kinda Sumlaji 1 Table of Contents: 1. Introduction... 3 2. Option Style... 4 3. Put Option 4 3.1 Definition 4 3.2 Payoff at Maturity... 4 3.3 Example

American and European Put Option Analytical Finance I Kinda Sumlaji 1 Table of Contents: 1. Introduction... 3 2. Option Style... 4 3. Put Option 4 3.1 Definition 4 3.2 Payoff at Maturity... 4 3.3 Example

Derivative Users Traders of derivatives can be categorized as hedgers, speculators, or arbitrageurs.

OPTIONS THEORY Introduction The Financial Manager must be knowledgeable about derivatives in order to manage the price risk inherent in financial transactions. Price risk refers to the possibility of loss

OPTIONS THEORY Introduction The Financial Manager must be knowledgeable about derivatives in order to manage the price risk inherent in financial transactions. Price risk refers to the possibility of loss

BINOMIAL OPTIONS PRICING MODEL. Mark Ioffe. Abstract

BINOMIAL OPTIONS PRICING MODEL Mark Ioffe Abstract Binomial option pricing model is a widespread numerical method of calculating price of American options. In terms of applied mathematics this is simple

BINOMIAL OPTIONS PRICING MODEL Mark Ioffe Abstract Binomial option pricing model is a widespread numerical method of calculating price of American options. In terms of applied mathematics this is simple

Introduction to Options. Derivatives

Introduction to Options Econ 422: Investment, Capital & Finance University of Washington Summer 2010 August 18, 2010 Derivatives A derivative is a security whose payoff or value depends on (is derived

Introduction to Options Econ 422: Investment, Capital & Finance University of Washington Summer 2010 August 18, 2010 Derivatives A derivative is a security whose payoff or value depends on (is derived

FX Options and Smile Risk_. Antonio Castagna. )WILEY A John Wiley and Sons, Ltd., Publication

WILEY A John Wiley and Sons, Ltd., Publication") FX Options and Smile Risk_ Antonio Castagna )WILEY A John Wiley and Sons, Ltd., Publication Preface Notation and Acronyms IX xiii 1 The FX Market 1.1 FX rates and spot contracts 1.2 Outright and FX swap

FX Options and Smile Risk_ Antonio Castagna )WILEY A John Wiley and Sons, Ltd., Publication Preface Notation and Acronyms IX xiii 1 The FX Market 1.1 FX rates and spot contracts 1.2 Outright and FX swap

Consider a European call option maturing at time T

Lecture 10: Multi-period Model Options Black-Scholes-Merton model Prof. Markus K. Brunnermeier 1 Binomial Option Pricing Consider a European call option maturing at time T with ihstrike K: C T =max(s T

Lecture 10: Multi-period Model Options Black-Scholes-Merton model Prof. Markus K. Brunnermeier 1 Binomial Option Pricing Consider a European call option maturing at time T with ihstrike K: C T =max(s T

Lecture Notes: Basic Concepts in Option Pricing - The Black and Scholes Model

Brunel University Msc., EC5504, Financial Engineering Prof Menelaos Karanasos Lecture Notes: Basic Concepts in Option Pricing - The Black and Scholes Model Recall that the price of an option is equal to

Brunel University Msc., EC5504, Financial Engineering Prof Menelaos Karanasos Lecture Notes: Basic Concepts in Option Pricing - The Black and Scholes Model Recall that the price of an option is equal to

Lecture 17/18/19 Options II

1 Lecture 17/18/19 Options II Alexander K. Koch Department of Economics, Royal Holloway, University of London February 25, February 29, and March 10 2008 In addition to learning the material covered in

1 Lecture 17/18/19 Options II Alexander K. Koch Department of Economics, Royal Holloway, University of London February 25, February 29, and March 10 2008 In addition to learning the material covered in

Introduction to Options

Introduction to Options By: Peter Findley and Sreesha Vaman Investment Analysis Group What Is An Option? One contract is the right to buy or sell 100 shares The price of the option depends on the price

Introduction to Options By: Peter Findley and Sreesha Vaman Investment Analysis Group What Is An Option? One contract is the right to buy or sell 100 shares The price of the option depends on the price

You can find the Report on the SaxoTrader under the Account tab. On the SaxoWebTrader, it is located under the Account tab, on the Reports menu.

The FX Options Report What is the FX Options Report? The FX Options Report gives you a detailed analysis of your FX and FX Options positions across multiple currency pairs, enabling you to manage your

The FX Options Report What is the FX Options Report? The FX Options Report gives you a detailed analysis of your FX and FX Options positions across multiple currency pairs, enabling you to manage your