EVERYTHING YOU ALWAYS WANTED TO KNOW ABOUT 1031 EXCHANGE (BUT DIDN T KNOW YOU SHOULD ASK )

|

|

|

- Alisha Wheeler

- 10 years ago

- Views:

Transcription

1 EVERYTHING YOU ALWAYS WANTED TO KNOW ABOUT 1031 EXCHANGE (BUT DIDN T KNOW YOU SHOULD ASK ) Nancy N Grekin McCorriston Miller Mukai MacKinnon 5 Waterfront Plaza, 4 th Floor Honolulu, Hawaii [email protected]

2 DEFINITIONS Taxpayer. The person or entity doing the exchange. Relinquished Property. The property being exchanged. Replacement Property. The property being acquired in the exchange. Buyer. The buyer of the Relinquished Property. Seller. The seller of the Replacement Property. Accommodator. The company which holds Taxpayer s funds between sale of the Relinquished Property and purchase of the Replacement Property. Exchange Value. The gross sales price of the Relinquished Property minus closing costs but including the amount which pays off the mortgage. Realized Proceeds. The sales proceeds received by the Taxpayer including the amount used to pay off the mortgage. Recognized Proceeds. The portion of the realized proceeds which is recognized as gain and taxed. THE STARKER CASE AND EXCHANGE HISTORY Section 1031 provides literally that two Taxpayers exchange properties with each other. Taxpayers wanted to have the flexibility to exchange by selling the Relinquished Property to a buyer, and buying the Replacement Property from a different third-party a deferred exchange. This structure was approved in a case decided by the Federal Courts; the taxpayer was Starker, and now deferred exchanges are often called Starker exchanges. The court made clear in Starker that the seller could not have access to the funds between transactions and this became one of the most important structuring issues in 1031 exchanges. As a result we began to structure exchanges using third parties to hold the funds between transactions and companies like T. G. Exchange were formed to act as accommodators and perform this service. WHY EXCHANGE? A Taxpayer who exchanges can use all of the net funds to buy Replacement Property because tax on the gain is deferred, as explained below. A Taxpayer can continue to exchange through his lifetime and at his death, his heirs will get a stepped up basis in the property: the heirs tax basis in the property will be the fair market value of the property on the date of death of the Taxpayer enabling the heirs to sell the property without recognizing gain or paying taxes.

3 It is not always desirable to exchange, however. If the gain is small it isn t worthwhile to exchange because there are costs to exchange, and the basis of the Relinquished Property which is less than the purchase price is carried over thus reducing depreciable basis in the Replacement Property a gain of less than $25,000 - $50,000 is usually the threshold STRUCTURE OF AN EXCHANGE An exchange is a sale of real property and the usual form of Purchase and Sale Agreement is used. It is not necessary to include special provisions but it is desirable to have a provision requiring that the Buyer cooperate in the exchange since he will have to sign exchange documents. Before closing of the sale, the Taxpayer must enter into an exchange agreement and assign his contract rights to the accommodator so the Taxpayer should choose an accommodator when opening escrow, and inform the escrow officer that the sale is an exchange. A Taxpayer can sell multiple relinquished properties and buy multiple replacement properties. If several Relinquished Properties are sold the time for identification and purchase of Replacement Property will begin at the time of each sale so it might be wise to structure an exchange of multiple Relinquished Properties so that each are exchanged separately and each has its own time deadlines for identification and acquisition of Replacement Property. The Taxpayer will enter into a contract with the accommodator to hold the funds between transactions. When the Relinquished Property is sold, the funds are transferred to the accommodator which holds the funds and transfers to the escrow for purchase of the Replacement Property. The Taxpayer cannot receive, pledge, borrow or otherwise have the benefit of the funds while held by the Accommodator although the Accommodator can allow the Taxpayer to receive interest on the funds which can be paid after receipt of the Replacement Property. The exchange funds can be used only to buy Replacement Property, pay closing costs or pay off a mortgage covering the Relinquished Property. Exchange funds cannot be used to pay off other debts or loans which are not secured by a mortgage of the Relinquished Property without recognizing gain. FIRPTA AND HARPTA Foreign sellers of real estate are required to pay 10% of the gross proceeds of sale as a withholding against Federal income taxes. If the seller is exchanging they are exempt from this deposit although a complex procedure must be following in filing with the Internal Revenue Service if the Replacement Property is not designated at the time of sale of the Relinquished Property. 2

4 Hawaii has a similar statute which requires that an out of state resident who sells real estate pay 5% of the gross proceeds of sale as a withholding against State income taxes. Out of state sellers who exchange are also exempt from the requirement. MORTGAGES A mortgage on the Relinquished Property can be paid off with exchange proceeds. The portion of the proceeds used to pay the mortgage are deemed realized however and are included in the exchange value, so the mortgage must either be replaced with a new mortgage or cash in purchasing of the Replacement Property. If the Taxpayer borrowed funds to purchase the Relinquished Property, the loan cannot be repaid out of exchange funds unless the loan was secured by a mortgage on the Relinquished Property. A Taxpayer cannot take back a note in partial payment of the purchase price of the Relinquished Property without recognizing gain because a note is treated as other property, not Replacement Property. THE QUALIFIED USE TEST AND THE LIKE KIND TEST Qualified Use Both the Relinquished Property and the Replacement Property must be held either for use in a trade or business or for investment. Held for investment means that if the property is improved, it must be rented. That means that a Taxpayer who allows his children to live in property rent-free or a Taxpayer which holds the property but does not rent it is not holding it for investment. Vacant land generally cannot be rented and it will be deemed held for investment if it is held for increase in value. Like Kind Test The Replacement Property and Relinquished Property must be like kind which is very broadly interpreted and means that both must be held either for use in a trade or business or for investment but the properties do not have to be similar in service or related in use. A condominium can be exchanged for a single family dwelling or a shopping center for an office building. Any investment or business property can be exchanged for any other investment property or business property and meet the like kind test. 3

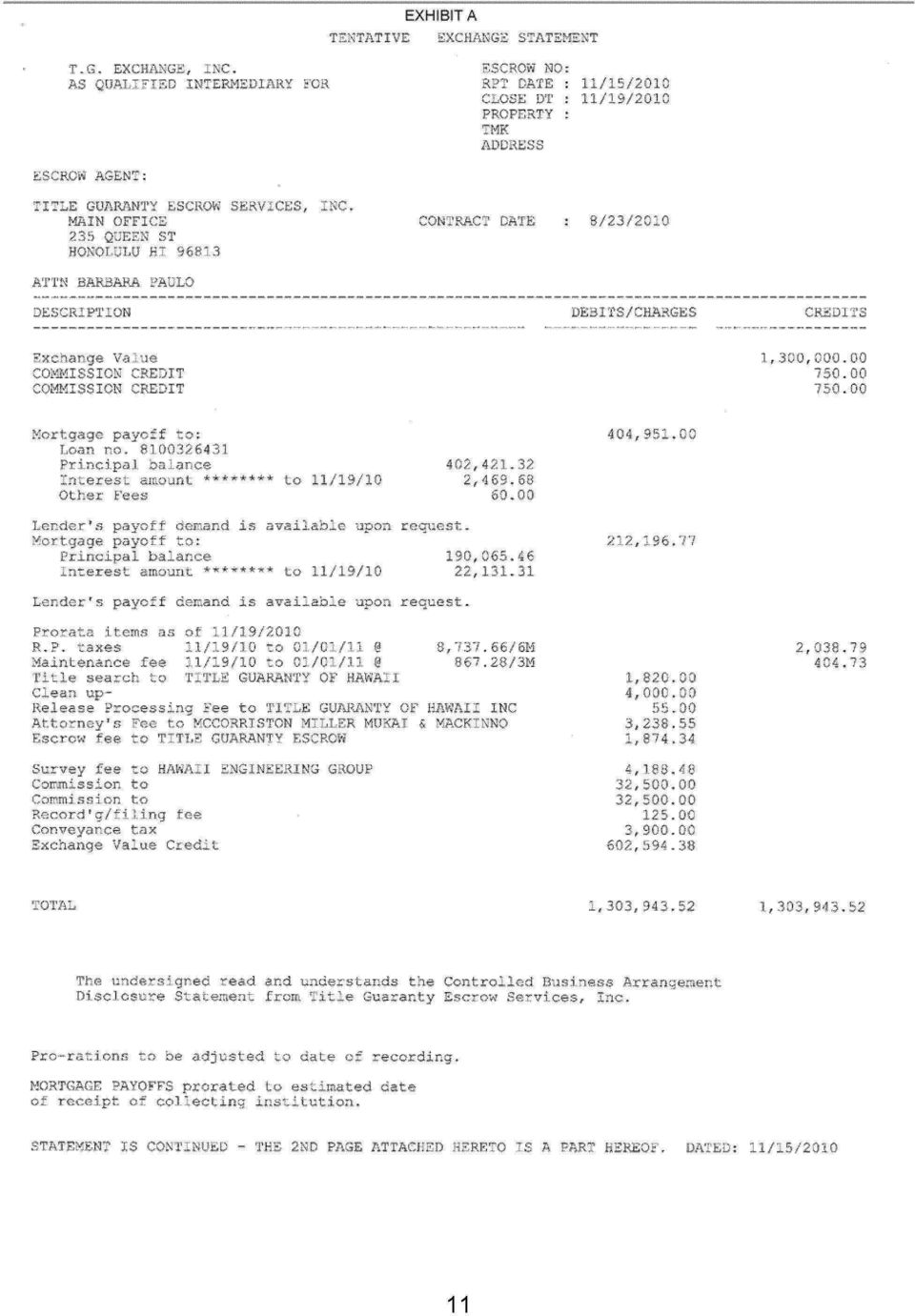

5 Leaseholds and Coops A leasehold is like kind with a fee only if has more than 30 years of term remaining, including options to renew (whether or not renewed). A coop is not real estate in the conventional sense; rather it is stock in a corporation which owns the land upon which the project is located and a space lease of the apartment. A coop is deemed real estate in Hawaii however, so it can be exchanged, but if the apartment lease has less than 30 years of term, it can only be exchanged for a leasehold. TAX CONSEQUENCES OF AN EXCHANGE Basis An exchange is not tax-free as it is often described; rather it is tax-deferred because the Taxpayer carries over its tax basis in the Relinquished Property to the Replacement Property. This means that the gain realized in the exchange transaction but not recognized will be recognized if the Taxpayer does not exchange when he sells the Replacement Property. Basis in the Replacement Property is increased by any gain recognized on the sale of the Relinquished Property or by capital improvements installed after purchase and is also increased by the amount Taxpayer spends in excess of exchange value when acquiring the Replacement Property. It is important to understand the calculation of exchange value is in order to plan purchase of the Replacement Property and to have a fully-deferred exchange. Exchange Value Exchange value is the gross selling of the Relinquished Property minus deductible costs of sale but including the amount used to pay off the mortgage. Deductible costs of sale are items which would be deductible if the transfer were a sale and not an exchange such as Broker s commissions Escrow and title fees Attorneys fees Accommodators fees Fix-up expenses which would be deductible if sold Loan fees and prorations are not deductible and do not reduce exchange value or increase the amount deemed to have spent on the Replacement Property. The Exchange value is not the bottom line on the closing statement and is not an amount some escrow companies call exchange value credit which is usually the amount of 4

6 cash transferred to the accommodator. Exchange value is also not the cash received or the profit or taxable gain. See Exhibit A for a calculation of exchange value. Boot Boot is gain realized in an exchange. Taxpayers can generate boot in five ways: Taking out cash from proceeds of sale Spending less than the exchange value on the Replacement Property Not replacing debt paid off on the Relinquished Property. The Regulations provide that paying off debt is not boot to the Taxpayer. But for the regulations the Taxpayer would be deemed to have used exchange proceeds for something other than acquisition of Replacement Property by paying the debt. Because the portion of proceeds used to pay debt is deemed realized, the Taxpayer must replace it either with new debt or cash in purchase of the Replacement Property in order to avoid recognizing it. Over-mortgaging the Replacement Property. For example: the Taxpayer sells Relinquished Property for $500,000 with a $100,000 mortgage and buys Replacement Property for $500,000 but obtains a $200,000 mortgage The excess mortgage proceeds of $100,000 is recognized as gain. Paying debts not secured by a mortgage on the Relinquished Property If a Taxpayer takes out an equity loan immediately before selling the Relinquished Property or after immediately buying the Replacement Property is it boot? Congress considered a provision a number of years ago which would have made mortgages of Relinquished Property and Replacement Property close to the exchange boot but Congress did not pass it, and has not challenged it. There was a case where the Taxpayer took out a mortgage just before selling the Relinquished Property and the Tax Court held that there were good business reasons for it and allowed it. If a Taxpayer wants to take out cash in an exchange, taking out an equity loan secured by the Replacement Property is the best course since mortgage proceeds are not taxed. IDENTIFICATION OF REPLACEMENT PROPERTY Within 45 days of closing of sale of the Relinquished Property the Taxpayer must identify Replacement Property. This is usually done by letter to the Accommodator. Within 180 days of closing of sale of Relinquished Property, or before the Taxpayer s next tax return is due, the Taxpayer must acquire the Replacement Property. These deadlines are absolute and cannot be changed or extended. 5

7 Replacement property must be unambiguously identified which means it must be identified by address or a tax map key number. A condominium project cannot be identified; the Taxpayer must identify particular unit numbers. It is not necessary for the Taxpayer to enter into a contract for purchase of the Replacement Property in order to identify it but the Taxpayer will be at risk that the properties identified cannot be acquired if he is unable to enter into a contract before expiration of the 45-day identification period. The Regulations allow identifying multiple properties. A Taxpayer may identify as many as 3 alternate properties of any value. If more than 3 properties are identified, the value of the 3 cannot exceed 95% of the value of the Relinquished Property unless 95% of the properties identified are acquired. If any of the rules are not followed, the Taxpayer will be treated as not having identified any Replacement Property. If three properties are identified, the Taxpayer can acquire one or more of the properties, and can acquire multiple replacement properties. Carryover basis is allocated pro rata to the purchase price of all properties acquired REVERSE EXCHANGES A reverse exchange is a transaction in which the Taxpayer has located Replacement Property he wishes to acquire, but has not sold his Relinquished Property. These transactions are popular in cold real estate markets because it is a buyer s market and it is more difficult to sell than it is to buy. In a reverse exchange, the Taxpayer acquires the Replacement Property by parking it with an accommodator until the Relinquished Property can be sold. This is done by forming a single-member LLC of which the accommodator is the member which acquires the Replacement Property. The LLC and the Taxpayer enter into a contract providing for the LLC to hold the property until the Relinquished Property is sold and then to exchange it for the Replacement Property in a structured forward exchange. It is possible to do a partial forward/partial reverse exchange if a Taxpayer wants to sell several relinquished properties. Each time the Taxpayer sells a relinquished Property he purchases a pro rata portion of the Replacement Property from the LLC. While the accommodator holds the Replacement Property, it must pay all expenses and treat the property as if owned by it, not by the Taxpayer and the Accommodator will require that the Taxpayer deposit amounts sufficient to cover insurance premiums, property taxes and any other expenses of ownership, but the Taxpayer is permitted to lease or manage the property. If the Taxpayer leases it, the lease could provide for the Taxpayer to pay taxes or buy insurance so management is simpler and is directly at the expense of the Taxpayer In order for the LLC to acquire the Replacement Property in a reverse exchange, the Taxpayer must loan the funds necessary for purchase to the LLC because the Taxpayer will not have the proceeds of sale of the Relinquished Property. The LLC will give the Taxpayer a note secured by a mortgage of the Replacement Property to 6

8 document the loan. The Taxpayer can mortgage either the Relinquished Property or the Replacement Property or use a home equity line of credit to generate the funds. If the Taxpayer mortgages the Replacement Property the mortgage will be given by the LLC although the note can be signed by the Taxpayer. When the Relinquished Property is sold, the Taxpayer and Accommodator enter into an exchange agreement, and the proceeds are used to pay off the note so the Taxpayer gets back the cash loaned for the purchase. The LLC membership interest can be conveyed to the Taxpayer rather than the property thus avoiding a second conveyance tax RELATED PARTY EXCHANGES Section 1031(f) provides that if a Taxpayer exchanges with a related party then the party who got the property in the exchange must hold it for 2 years or the exchange will be disallowed. Related parties are linear blood relatives and entities in which the Taxpayer owns an interest, but also include some complex relationships with trusts and entities. The related party rules are complicated by Section 1031(f)(4) which provides that if a Taxpayer attempts to avoid the 2-year rule by structuring an exchange to avoid it, then the exchange is disallowed. The example of such a structure in the legislative history is if the seller sells the Replacement Property to the buyer of the Relinquished Property, and the buyer exchanges the Replacement Property for the Relinquished Property with the Taxpayer, then the Taxpayer will not be subject to the 2-year rule because she would not have exchanged with a related party. This is the only structure which could have this result yet the Tax Court ruled in a case which arose in Honolulu (and there have been several since as well as some IRS rulings) that a Taxpayer which used an accommodator to hold funds in an exchange was essentially trying to avoid the 2-year rule by exchanging with a third party which was not a related party. The effect of this case is to eliminate the possibility of a Taxpayer acquiring Replacement Property from a related party even if the Taxpayer holds the Replacement Property for 2 years. PARTNERSHIP EXCHANGES Taxpayers cannot exchange partnership interests or acquire a partnership interest in a partnership which owns real estate except an interest in a single-member LLC. Single member LLCs are disregarded for tax purposes and treated as if the sole member owns the real estate. Multi-member LLCs and partnerships are not disregarded for purposes of an exchange. Thus if a partnership owns real estate and wants to exchange it is the partnership which must exchange not the partners. The Partnership must acquire the Replacement Property. In one ruling the partnership distributed the proceeds of sale of 7

9 the Relinquished Properties to the partners, and each acquired their own Replacement Property. The exchange was disallowed. What if some partners want to exchange and some do not? This can be done I three ways: (1) the partnership can dissolve before selling the Relinquished Property, distribute pro rata shares to the partners, and each can sell or exchange, (2) the partnership can acquire multiple Replacement Properties and then dissolve distributing the properties to the partners, or (3) the partnership can exchange, spend less than the exchange value, recognize the gain and specially allocate it to the partner who doesn t want to exchange, and distribute the cash to that partner in liquidation of his partnership interest. CONCLUSION An exchange is a very useful planning tool which allows maximizing returns on investment by allowing a Taxpayer to invest all proceeds of sale and defer capital gains taxes. If continued through a Taxpayer s lifetime it is a great estate planning tool because the Taxpayer s heirs will get the property with a basis stepped up to fair market value at the Taxpayer s death and then can sell without recognizing any gain. 8

10 9

11 EXCHANGE VALUE Gross Sales Price $1,300, Title Search -$1, Clean up -$4, Release Processing Fee -$55.00 Attorney's fee -$3, Escrow fee -$1, Survey -$4, Commission -$32, Commission -$232, Recording fee -$ Conveyance tax -$3, Exchange Value $1,015,

PRESENTED BY: BOB BOWER SENIOR VICE PRESIDENT CBRE

PRESENTED BY: BOB BOWER SENIOR VICE PRESIDENT CBRE TABLE OF CONTENTS SECTION I 1031 EXCHANGE SECTION III SECTION IV SECTION V SECTION VI SECTION VII SECTION VIII SECTION IX SECTION X SECTION XI LEASEHOLD

PRESENTED BY: BOB BOWER SENIOR VICE PRESIDENT CBRE TABLE OF CONTENTS SECTION I 1031 EXCHANGE SECTION III SECTION IV SECTION V SECTION VI SECTION VII SECTION VIII SECTION IX SECTION X SECTION XI LEASEHOLD

Home Mortgage Interest Deduction

Department of the Treasury Internal Revenue Service Publication 936 Cat.. 10426G Home Mortgage Interest Deduction For use in preparing 1998 Returns Contents Introduction... 1 Part I: Home Mortgage Interest...

Department of the Treasury Internal Revenue Service Publication 936 Cat.. 10426G Home Mortgage Interest Deduction For use in preparing 1998 Returns Contents Introduction... 1 Part I: Home Mortgage Interest...

Lesson 15: Closing Real Estate Transactions

1 Real Estate Principles of Georgia Lesson 15: Closing Real Estate Transactions 2 Closing Closing: Final stage in real estate transaction. Also called settlement. Buyer pays seller; seller transfers title

1 Real Estate Principles of Georgia Lesson 15: Closing Real Estate Transactions 2 Closing Closing: Final stage in real estate transaction. Also called settlement. Buyer pays seller; seller transfers title

Tax Considerations Of Foreign

FIRPTA requires that a buyer withhold 10% of the gross sales price, subject to certain exceptions, and send it to the Internal Revenue Service if the seller is a foreign person. U.S. Taxes Foreign investors

FIRPTA requires that a buyer withhold 10% of the gross sales price, subject to certain exceptions, and send it to the Internal Revenue Service if the seller is a foreign person. U.S. Taxes Foreign investors

Choice of Entity: Corporation or Limited Liability Company?

September 2012 Choice of Entity: Corporation or Limited Liability Company? By Gianfranco A. Pietrafesa* Attorney at Law There are many different types of business entities, including corporations, general

September 2012 Choice of Entity: Corporation or Limited Liability Company? By Gianfranco A. Pietrafesa* Attorney at Law There are many different types of business entities, including corporations, general

TAX ISSUES IN SALES. The nature of the sale should govern the deal, not the tax consequences.

TAX ISSUES IN SALES The nature of the sale should govern the deal, not the tax consequences. If the sale is due to belief that the real estate market & the stock market are at or near the top, then it

TAX ISSUES IN SALES The nature of the sale should govern the deal, not the tax consequences. If the sale is due to belief that the real estate market & the stock market are at or near the top, then it

Choice of Entity: Corporation or Limited Liability Company?

March 2014 Choice of Entity: Corporation or Limited Liability Company? By Gianfranco A. Pietrafesa* Attorney at Law There are many different types of business entities, including corporations, general

March 2014 Choice of Entity: Corporation or Limited Liability Company? By Gianfranco A. Pietrafesa* Attorney at Law There are many different types of business entities, including corporations, general

1031EXCHANGE HANDBOOK

SECTION 1031EXCHANGE HANDBOOK YOUR QUESTIONS ANSWERED Investment Exchange Group Toll free 800.908.1031 www.ixg1031.com Investment Exchange Group This 1031 Exchange Handbook will simplify and clarify terminology

SECTION 1031EXCHANGE HANDBOOK YOUR QUESTIONS ANSWERED Investment Exchange Group Toll free 800.908.1031 www.ixg1031.com Investment Exchange Group This 1031 Exchange Handbook will simplify and clarify terminology

NATIONAL INTERACTIVE STUDY GROUP UNIT 8 QUESTIONS

NATIONAL INTERACTIVE STUDY GROUP UNIT 8 QUESTIONS National Interactive Study Group 2 SESSION 8 JOHN MATHIS Notes for Tonight 1. To MUTE your phone line use *6 2. To UNMUTE your phone line use #6 3. Chat

NATIONAL INTERACTIVE STUDY GROUP UNIT 8 QUESTIONS National Interactive Study Group 2 SESSION 8 JOHN MATHIS Notes for Tonight 1. To MUTE your phone line use *6 2. To UNMUTE your phone line use #6 3. Chat

A Like Kind 1031 Exchange Go to Guide for Attorneys

A Like Kind 1031 Exchange Go to Guide for Attorneys Lawyers often advise their clients on whether they would benefit from tax deferral strategies such as Internal Revenue Code (IRC) Section 1031 like kind

A Like Kind 1031 Exchange Go to Guide for Attorneys Lawyers often advise their clients on whether they would benefit from tax deferral strategies such as Internal Revenue Code (IRC) Section 1031 like kind

1031 Tax Deferred Exchanges. A More Detailed Look

1031 Tax Deferred Exchanges A More Detailed Look A reference guide encompassing all aspects of the 1031 Tax Deferred Exchange. The information contained inside is compliments of: James T. Saint, CCIM,

1031 Tax Deferred Exchanges A More Detailed Look A reference guide encompassing all aspects of the 1031 Tax Deferred Exchange. The information contained inside is compliments of: James T. Saint, CCIM,

Inland Private Capital Corporation. 1031 Exchange Solutions & Investing in Private Placements A Presentation for Certified Public Accountants

Inland Private Capital Corporation 1031 Exchange Solutions & Investing in Private Placements A Presentation for Certified Public Accountants Disclaimers Investments are suitable for accredited investors

Inland Private Capital Corporation 1031 Exchange Solutions & Investing in Private Placements A Presentation for Certified Public Accountants Disclaimers Investments are suitable for accredited investors

FAQ s (FOREIGN INVESTORS)

") FAQ s (FOREIGN INVESTORS) WHAT IS FIRPTA? Foreign Investment in Real Property Tax Act, a statute that requires that a seller who is a foreign person permit a withholding of a part of the selling price

FAQ s (FOREIGN INVESTORS) WHAT IS FIRPTA? Foreign Investment in Real Property Tax Act, a statute that requires that a seller who is a foreign person permit a withholding of a part of the selling price

Technology Companies Practice Tax Practice Goodwin Procter LLP. 2010. Goodwin Procter LLP

Technology Companies Practice Tax Practice 2010. Entity Type Number of People Separate Entity? Limited Liability Formation/ Existence Formalities C-Corporation 1+ Yes Yes Filings/Fees On-going S-Corporation

Technology Companies Practice Tax Practice 2010. Entity Type Number of People Separate Entity? Limited Liability Formation/ Existence Formalities C-Corporation 1+ Yes Yes Filings/Fees On-going S-Corporation

Foreign Person Investing in U.S. Real Estate

Foreign Person Investing in U.S. Real Estate Ian Shane Golenbock Eiseman Assor Bell & Peskoe LLP TTN New York Conference 2013 Foreign Purchases of U.S. Homes Foreign Home Buyers want to: Minimize tax on

Foreign Person Investing in U.S. Real Estate Ian Shane Golenbock Eiseman Assor Bell & Peskoe LLP TTN New York Conference 2013 Foreign Purchases of U.S. Homes Foreign Home Buyers want to: Minimize tax on

The mechanics of foreclosure are specific to the laws of the State in

Unraveling the Mystery of Cancellation of Indebtedness Income What Borrowers Need to Know of the Potential Tax Costs of Loan Workouts and Foreclosures by Edward J. Hannon, Partner, Corporate and Real Estate

Unraveling the Mystery of Cancellation of Indebtedness Income What Borrowers Need to Know of the Potential Tax Costs of Loan Workouts and Foreclosures by Edward J. Hannon, Partner, Corporate and Real Estate

Estate Planning. Insight on. The basics of basis. Does a private annuity have a place in your estate plan? Estate tax relief for family businesses

Insight on Estate Planning June/July 2015 The basics of basis Basis planning can result in significant tax savings Does a private annuity have a place in your estate plan? Estate tax relief for family

Insight on Estate Planning June/July 2015 The basics of basis Basis planning can result in significant tax savings Does a private annuity have a place in your estate plan? Estate tax relief for family

Exclusion of Gain on the Sale of a Principal Residence, Interest Deductions, Home Office Rules

Exclusion of Gain on the Sale of a Principal Residence, Interest Deductions, Home Office Rules 'Walter D. Schwidetzky Professor of Law University of Baltimore School of Law 1420 N. Charles St. Baltimore,

Exclusion of Gain on the Sale of a Principal Residence, Interest Deductions, Home Office Rules 'Walter D. Schwidetzky Professor of Law University of Baltimore School of Law 1420 N. Charles St. Baltimore,

PURCHASING REAL ESTATE IN A SELF DIRECTED IRA OR QUALIFIED PENSION PLAN. By Maurice M. Glazer, CEO GLAZER FINANCIAL NETWORK

PURCHASING REAL ESTATE IN A SELF DIRECTED IRA OR QUALIFIED PENSION PLAN By Maurice M. Glazer, CEO GLAZER FINANCIAL NETWORK In today s market or lack of market, most baby boomers have most of their retirement

PURCHASING REAL ESTATE IN A SELF DIRECTED IRA OR QUALIFIED PENSION PLAN By Maurice M. Glazer, CEO GLAZER FINANCIAL NETWORK In today s market or lack of market, most baby boomers have most of their retirement

LLC Operating Agreement. Table Of Contents

LLC Operating Agreement Table Of Contents ARTICLE I. Formation and Name: Office; Purpose; Term... 113 Section 1.1. Name of the Company...113 Section 1.2. Purpose...113 Section 1.3. Term...115 Section 1.4.

LLC Operating Agreement Table Of Contents ARTICLE I. Formation and Name: Office; Purpose; Term... 113 Section 1.1. Name of the Company...113 Section 1.2. Purpose...113 Section 1.3. Term...115 Section 1.4.

NON-RESIDENTS PURCHASING REAL PROPERTY IN THE U.S.

NON-RESIDENTS PURCHASING REAL PROPERTY IN THE U.S. A. The Attorneys Role in the Purchase of Real Estate The purchase of real estate in the U.S. without the proper assistance can become a complex transaction.

NON-RESIDENTS PURCHASING REAL PROPERTY IN THE U.S. A. The Attorneys Role in the Purchase of Real Estate The purchase of real estate in the U.S. without the proper assistance can become a complex transaction.

FAMILY PARTNERSHIP OR LIMITED LIABILITY COMPANY CHECKLIST

CHERRY CREEK CORPORATE CENTER 4500 CHERRY CREEK DRIVE SOUTH #600 DENVER, CO 80246-1500 303.322.8943 WWW.WADEASH.COM DISCLAIMER Material presented on the Wade Ash Woods Hill & Farley, P.C., website is intended

CHERRY CREEK CORPORATE CENTER 4500 CHERRY CREEK DRIVE SOUTH #600 DENVER, CO 80246-1500 303.322.8943 WWW.WADEASH.COM DISCLAIMER Material presented on the Wade Ash Woods Hill & Farley, P.C., website is intended

The prospect of investing in U.S. real estate can be attractive for citizens of

in United States Real Estate It is critical that you educate yourself and consult with an experienced tax professional that specializes in international taxation such as the Esquire Group. The prospect

in United States Real Estate It is critical that you educate yourself and consult with an experienced tax professional that specializes in international taxation such as the Esquire Group. The prospect

Chapter 18. Corporations: Distributions Not in Complete Liquidation. Eugene Willis, William H. Hoffman, Jr., David M. Maloney and William A.

Chapter 18 Corporations: Distributions Not in Complete Liquidation Eugene Willis, William H. Hoffman, Jr., David M. Maloney and William A. Raabe Copyright 2004 South-Western/Thomson Learning Taxable Dividends

Chapter 18 Corporations: Distributions Not in Complete Liquidation Eugene Willis, William H. Hoffman, Jr., David M. Maloney and William A. Raabe Copyright 2004 South-Western/Thomson Learning Taxable Dividends

Advanced Markets Combining Estate Planning Techniques A Powerful Strategy

Life insurance can help meet many wealth transfer goals. The death benefit could cover estate taxes, for instance, avoiding liquidation of much of the estate to meet the estate tax bill. Even though a

Life insurance can help meet many wealth transfer goals. The death benefit could cover estate taxes, for instance, avoiding liquidation of much of the estate to meet the estate tax bill. Even though a

First Time Home Buyer Glossary

First Time Home Buyer Glossary For first time home buyers, knowing and understanding the following terms are very important when purchasing your first home. By understanding these terms, you will make

First Time Home Buyer Glossary For first time home buyers, knowing and understanding the following terms are very important when purchasing your first home. By understanding these terms, you will make

TAX FACTS. From the State of Hawaii, Department of Taxation

TAX FACTS From the State of Hawaii, Department of Taxation October, 2010 UNDERSTANDING HARPTA 2010-1 Note: All references to the IRC are to the Internal Revenue Code of 1986, as amended. All quoted IRC

TAX FACTS From the State of Hawaii, Department of Taxation October, 2010 UNDERSTANDING HARPTA 2010-1 Note: All references to the IRC are to the Internal Revenue Code of 1986, as amended. All quoted IRC

Corpus Christi Excel Properties, Inc. Tim A. Voorkamp, Certified Exchange Specialist

THE TAX DEFERRED EXCHANGE The tax deferred exchange, as defined in Section 1031 of the Internal Revenue Code of 1986, as amended, offers investors one of the last great opportunities to build wealth and

THE TAX DEFERRED EXCHANGE The tax deferred exchange, as defined in Section 1031 of the Internal Revenue Code of 1986, as amended, offers investors one of the last great opportunities to build wealth and

Buy-to-let guide about tax

Perrys Chartered Accountants Buy-to-let guide about tax Introduction As a buy-to-let landlord it is important you know about tax and how it affects you and your investment. This is why Perrys Chartered

Perrys Chartered Accountants Buy-to-let guide about tax Introduction As a buy-to-let landlord it is important you know about tax and how it affects you and your investment. This is why Perrys Chartered

News Flash. September, 2015. Tax guide for property investment in Hungary

News Flash September, 2015 Tax guide for property investment in Hungary Tax guide for property investment in Hungary In our current newsletter we would like to inform you about the most important taxation

News Flash September, 2015 Tax guide for property investment in Hungary Tax guide for property investment in Hungary In our current newsletter we would like to inform you about the most important taxation

SELLING THE BUSINESS: PRACTICAL, TAX AND LEGAL ISSUES. William C. Staley. Attorney www.staleylaw.com 818 936-3490

SELLING THE BUSINESS: PRACTICAL, TAX AND LEGAL ISSUES William C. Staley, Attorney www.staleylaw.com 818 936-3490 WEST SAN GABRIEL VALLEY DISCUSSION GROUP LOS ANGELES CHAPTER CALIFORNIA SOCIETY OF CPAS

SELLING THE BUSINESS: PRACTICAL, TAX AND LEGAL ISSUES William C. Staley, Attorney www.staleylaw.com 818 936-3490 WEST SAN GABRIEL VALLEY DISCUSSION GROUP LOS ANGELES CHAPTER CALIFORNIA SOCIETY OF CPAS

What is a 1035 Exchange?

What is a 1035 Exchange? Why would a client want to exchange an insurance policy? There are a number of reasons why a client might want to exchange an existing policy for a new policy. Today there are

What is a 1035 Exchange? Why would a client want to exchange an insurance policy? There are a number of reasons why a client might want to exchange an existing policy for a new policy. Today there are

A Sole Proprietor Insured Buy-Sell Plan

A Sole Proprietor Insured Buy-Sell Plan At a sole proprietor s death, the business is dissolved and all business assets and liabilities become part of the sole proprietor's personal estate. Have you evaluated

A Sole Proprietor Insured Buy-Sell Plan At a sole proprietor s death, the business is dissolved and all business assets and liabilities become part of the sole proprietor's personal estate. Have you evaluated

Transferring Business Assets

Transferring Business Assets In the future, you may either want to transfer your business to heirs or sell your business to employees, competitors, or others. Planning for transfer of a family business

Transferring Business Assets In the future, you may either want to transfer your business to heirs or sell your business to employees, competitors, or others. Planning for transfer of a family business

Housing Cooperatives. An Accessible and Lasting Tool for Home Ownership. Northcountry Cooperative Development Fund

Housing Cooperatives An Accessible and Lasting Tool for Home Ownership Northcountry Cooperative Development Fund Did you know. that in the United States, more than 1.5 million families of all income levels

Housing Cooperatives An Accessible and Lasting Tool for Home Ownership Northcountry Cooperative Development Fund Did you know. that in the United States, more than 1.5 million families of all income levels

GETTING THE MOST OUT OF YOUR ESOP

GETTING THE MOST OUT OF YOUR ESOP Michael G. Keeley Hunton & Williams LLP 1445 Ross Avenue Suite 3700 Dallas, Texas 75202 (214) 468-3345 [email protected] Traditional Sources of Capital for Community

GETTING THE MOST OUT OF YOUR ESOP Michael G. Keeley Hunton & Williams LLP 1445 Ross Avenue Suite 3700 Dallas, Texas 75202 (214) 468-3345 [email protected] Traditional Sources of Capital for Community

Buyers and Sellers of an S Corporation Should Consider the Section 338 Election

Income Tax Valuation Insights Buyers and Sellers of an S Corporation Should Consider the Section 338 Election Robert P. Schweihs There are a variety of factors that buyers and sellers consider when deciding

Income Tax Valuation Insights Buyers and Sellers of an S Corporation Should Consider the Section 338 Election Robert P. Schweihs There are a variety of factors that buyers and sellers consider when deciding

SHOPPING FOR A MORTGAGE

SHOPPING FOR A MORTGAGE The Traditional Fixed-Rate Mortgage Key characteristics: Level payments, fixed interest rate, fixed term. This mortgage is the one which most of us know, and it is still the loan

SHOPPING FOR A MORTGAGE The Traditional Fixed-Rate Mortgage Key characteristics: Level payments, fixed interest rate, fixed term. This mortgage is the one which most of us know, and it is still the loan

U.S. Taxation of Foreign Investors

PART OF THE LEHMAN TAX LAW KNOWLEDGE BASE SERIES United States Taxation Of Investors U.S. Taxation of Foreign Investors Non Resident Alien Individuals & Foreign Corporations By Richard S. Lehman Esq. TAX

PART OF THE LEHMAN TAX LAW KNOWLEDGE BASE SERIES United States Taxation Of Investors U.S. Taxation of Foreign Investors Non Resident Alien Individuals & Foreign Corporations By Richard S. Lehman Esq. TAX

S Corporation vs. LLC in California Here is an overview of the differences between doing business as an S corporation or as an LLC.

S Corporation vs. LLC in California Here is an overview of the differences between doing business as an S corporation or as an LLC. After you have read this article, we can discuss in detail what would

S Corporation vs. LLC in California Here is an overview of the differences between doing business as an S corporation or as an LLC. After you have read this article, we can discuss in detail what would

Avoiding U.S. Investment Tax Traps

Avoiding U.S. Investment Tax Traps Structuring Real Estate and Other Fund Investments Presented by: Joseph Gulant and Daniel Blickman Major Categories of Tax to Consider in Planning International Transactions

Avoiding U.S. Investment Tax Traps Structuring Real Estate and Other Fund Investments Presented by: Joseph Gulant and Daniel Blickman Major Categories of Tax to Consider in Planning International Transactions

ACCOUNTANT'S CHECKLIST FOR DOING A 1031 EXCHANGE OF REAL ESTATE

Law Offices of Robert A. Briskin, a Professional Corporation 1901 Avenue of the Stars, Suite 1700, Los Angeles, California 90067 Certified Specialist - Taxation Law Telephone (310) 201-0507 The State Bar

Law Offices of Robert A. Briskin, a Professional Corporation 1901 Avenue of the Stars, Suite 1700, Los Angeles, California 90067 Certified Specialist - Taxation Law Telephone (310) 201-0507 The State Bar

Broker. Federal Income Tax Laws Affecting Real Estate. Chapter 14. Copyright Gold Coast Schools 1

Broker Chapter 14 Federal Income Tax Laws Affecting Real Estate Copyright Gold Coast Schools 1 Learning Objectives List the 2 principal tax deductions available to homeowners List the 2 types of home loans

Broker Chapter 14 Federal Income Tax Laws Affecting Real Estate Copyright Gold Coast Schools 1 Learning Objectives List the 2 principal tax deductions available to homeowners List the 2 types of home loans

Business Activities Definitions

Business Activities s Mortgage First mortgage brokering Second mortgage brokering First mortgage lending Second mortgage lending First mortgage servicing Third party first mortgage servicing Subordinate

Business Activities s Mortgage First mortgage brokering Second mortgage brokering First mortgage lending Second mortgage lending First mortgage servicing Third party first mortgage servicing Subordinate

LIFE INSURANCE OVERVIEW

LIFE INSURANCE OVERVIEW Most people think of life insurance in terms of death benefit protection. However, today s policies also provide the vehicles for meeting other goals, such as saving for retirement

LIFE INSURANCE OVERVIEW Most people think of life insurance in terms of death benefit protection. However, today s policies also provide the vehicles for meeting other goals, such as saving for retirement

Self-Directed Retirement Accounts. 1031 Exchange Investments

Self-Directed Retirement Accounts & 1031 Exchange Investments Security Trust Company & James Brennan Esq., LL.M. Exchange Solutions Group Security Trust Company Security Trust Company is a retirement plan

Self-Directed Retirement Accounts & 1031 Exchange Investments Security Trust Company & James Brennan Esq., LL.M. Exchange Solutions Group Security Trust Company Security Trust Company is a retirement plan

More than just housing... CO-OP HOUSING

More than just housing... CO-OP HOUSING How you can profit by living in a housing cooperative. Introduction A combination of factors including the rising cost of housing in recent years, have forced many

More than just housing... CO-OP HOUSING How you can profit by living in a housing cooperative. Introduction A combination of factors including the rising cost of housing in recent years, have forced many

GIVE AND YOU SHALL RECEIVE CHARITABLE GIVING, CREATING A PLAN THAT S RIGHT FOR YOU

GIVE AND YOU SHALL RECEIVE CHARITABLE GIVING, CREATING A PLAN THAT S RIGHT FOR YOU Contents 1 Give and you shall receive 3 Techniques summary 5 Planning for charitable giving NOT FDIC OR NCUA INSURED NOT

GIVE AND YOU SHALL RECEIVE CHARITABLE GIVING, CREATING A PLAN THAT S RIGHT FOR YOU Contents 1 Give and you shall receive 3 Techniques summary 5 Planning for charitable giving NOT FDIC OR NCUA INSURED NOT

timing is everything One issue in an array of decisions involving capital Taxes TAX PLANNING FOR CAPITAL ASSET DISPOSAL IS COMPLEX YET NECESSARY.

timing is everything Taxes TAX PLANNING FOR CAPITAL ASSET DISPOSAL IS COMPLEX YET NECESSARY. B Y D A VID J OY, C PA ; S TEPHEN C. DEL V ECCHIO, C PA ; B. DOUGLAS C LINTON, C PA ; AND J AMES C. YOUNG, C

timing is everything Taxes TAX PLANNING FOR CAPITAL ASSET DISPOSAL IS COMPLEX YET NECESSARY. B Y D A VID J OY, C PA ; S TEPHEN C. DEL V ECCHIO, C PA ; B. DOUGLAS C LINTON, C PA ; AND J AMES C. YOUNG, C

Equity Compensation in Limited Liability Companies

Equity Compensation in Limited Liability Companies October 6, 2010 Presented by: Pamela A. Grinter Frank C. Woodruff Introduction to Limited Liability Companies Limited liability companies were created

Equity Compensation in Limited Liability Companies October 6, 2010 Presented by: Pamela A. Grinter Frank C. Woodruff Introduction to Limited Liability Companies Limited liability companies were created

Partner's Instructions for Schedule K-1 (Form 1065)

") 2014 Partner's Instructions for Schedule K-1 (Form 1065) Partner's Share of Income, Deductions, Credits, etc. (For Partner's Use Only) Department of the Treasury Internal Revenue Service Section references

2014 Partner's Instructions for Schedule K-1 (Form 1065) Partner's Share of Income, Deductions, Credits, etc. (For Partner's Use Only) Department of the Treasury Internal Revenue Service Section references

CHOICE OF ENTITY CONSIDERATIONS. A Basic Guide to Entrepreneurs. October 9, 2012

CHOICE OF ENTITY CONSIDERATIONS A Basic Guide to Entrepreneurs October 9, 2012 Bill Osterbrock, Of Counsel Baker Donelson [email protected] 404-589-3418 Iliana Malinov, Tax Manager HLB Gross

CHOICE OF ENTITY CONSIDERATIONS A Basic Guide to Entrepreneurs October 9, 2012 Bill Osterbrock, Of Counsel Baker Donelson [email protected] 404-589-3418 Iliana Malinov, Tax Manager HLB Gross

INTRODUCTION TO REVERSE EXCHANGES

INTRODUCTION TO REVERSE EXCHANGES By Lee David Medinets, Esq. Certified Exchange Specialist Senior Counsel, Madison Exchange, LLC The purpose of this memo is to give introductory, generic information on

INTRODUCTION TO REVERSE EXCHANGES By Lee David Medinets, Esq. Certified Exchange Specialist Senior Counsel, Madison Exchange, LLC The purpose of this memo is to give introductory, generic information on

Incorporating Your Business

A Guide To Incorporating Your Business How to Form a Corporation or LLC Reduce Your Taxes Protect Your Assets Minimize Your Liability Improve Financial Flexibility By Attorney Brian P.Y. Liu Founder of

A Guide To Incorporating Your Business How to Form a Corporation or LLC Reduce Your Taxes Protect Your Assets Minimize Your Liability Improve Financial Flexibility By Attorney Brian P.Y. Liu Founder of

Owning a Co-op 10 questions to ask before you buy

Owning a Co-op 10 questions to ask before you buy So you want to own a Co-Op! If you re a first-time homebuyer, this is probably one of the biggest financial decisions you have ever made. As rents escalate

Owning a Co-op 10 questions to ask before you buy So you want to own a Co-Op! If you re a first-time homebuyer, this is probably one of the biggest financial decisions you have ever made. As rents escalate

Choosing the Right Entity for Maximum Tax Benefits for Your Construction Company

Choosing the Right Entity for Maximum Tax Benefits for Your Construction Company Timely re-evaluation of choice of entity will enhance the shareholder value of your contractor client By Theran J. Welsh

Choosing the Right Entity for Maximum Tax Benefits for Your Construction Company Timely re-evaluation of choice of entity will enhance the shareholder value of your contractor client By Theran J. Welsh

Overview of 1031 Like-Kind Exchanges for Farmers

Overview of 1031 Like-Kind Exchanges for Farmers By Jessica A. Shoemaker 2006 Farmers Legal Action Group, Inc. (FLAG) www.flaginc.org This document provides a general overview of tax-deferred property

Overview of 1031 Like-Kind Exchanges for Farmers By Jessica A. Shoemaker 2006 Farmers Legal Action Group, Inc. (FLAG) www.flaginc.org This document provides a general overview of tax-deferred property

RETIREMENT ACCOUNTS (c) Gary R. Evans, 2006-2011, September 24, 2011. Alternative Retirement Financial Plans and Their Features

Gary R. Evans, 2006-2011, September 24, 2011. Alternative Retirement Financial Plans and Their Features") RETIREMENT ACCOUNTS (c) Gary R. Evans, 2006-2011, September 24, 2011. The various retirement investment accounts discussed in this document all offer the potential for healthy longterm returns with substantial

RETIREMENT ACCOUNTS (c) Gary R. Evans, 2006-2011, September 24, 2011. The various retirement investment accounts discussed in this document all offer the potential for healthy longterm returns with substantial

Real Estate Exchange Under Section 1031

Real Estate Exchange Under Section 1031 Jack C. Harris Research Economist Texas A&M University Revised July 2000 2000, Real Estate Center. All rights reserved. Real Estate Exchange Under Section 1031 Contents

Real Estate Exchange Under Section 1031 Jack C. Harris Research Economist Texas A&M University Revised July 2000 2000, Real Estate Center. All rights reserved. Real Estate Exchange Under Section 1031 Contents

Buyer s Guide BASIC INFORMATION:

Buyer s Guide Buying an apartment in NYC can be overwhelming. Our Buyer s Guide provides useful information that can help you familiarize yourself with the process. BASIC INFORMATION: Financing: Find out

Buyer s Guide Buying an apartment in NYC can be overwhelming. Our Buyer s Guide provides useful information that can help you familiarize yourself with the process. BASIC INFORMATION: Financing: Find out

SHOULD MY BUSINESS BE AN S CORPORATION OR A LIMITED LIABILITY COMPANY?

SHOULD MY BUSINESS BE AN S CORPORATION OR A LIMITED LIABILITY COMPANY? 2015 Keith J. Kanouse One Boca Place, Suite 324 Atrium 2255 Glades Road Boca Raton, Florida 33431 Telephone: (561) 451-8090 Fax: (561)

SHOULD MY BUSINESS BE AN S CORPORATION OR A LIMITED LIABILITY COMPANY? 2015 Keith J. Kanouse One Boca Place, Suite 324 Atrium 2255 Glades Road Boca Raton, Florida 33431 Telephone: (561) 451-8090 Fax: (561)

OFFSHORE INVESTMENT U.S. INTERNATIONAL TAX PLANNING AN ASIAN PERSPECTIVE. June 9th and 10th, 2010 SHANGHAI

OFFSHORE INVESTMENT U.S. INTERNATIONAL TAX PLANNING AN ASIAN PERSPECTIVE June 9th and 10th, 2010 SHANGHAI Harriet Leung [email protected] Brian [email protected] & Company LLP 101 Second Street, Suite

OFFSHORE INVESTMENT U.S. INTERNATIONAL TAX PLANNING AN ASIAN PERSPECTIVE June 9th and 10th, 2010 SHANGHAI Harriet Leung [email protected] Brian [email protected] & Company LLP 101 Second Street, Suite

Alternative Retirement Financial Plans and Their Features

RETIREMENT ACCOUNTS Gary R. Evans, 2006-2013, November 20, 2013. The various retirement investment accounts discussed in this document all offer the potential for healthy longterm returns with substantial

RETIREMENT ACCOUNTS Gary R. Evans, 2006-2013, November 20, 2013. The various retirement investment accounts discussed in this document all offer the potential for healthy longterm returns with substantial

A Quick Guide to Real Estate IRAs. American IRA, LLC

A Quick Guide to Real Estate IRAs American IRA, LLC Declare independence from Wall Street! Self-directed IRAs and other retirement accounts let you take personal control of your assets. YES! You CAN Own

A Quick Guide to Real Estate IRAs American IRA, LLC Declare independence from Wall Street! Self-directed IRAs and other retirement accounts let you take personal control of your assets. YES! You CAN Own

Succession Planning Case Studies

Succession Planning Case Studies Prepared by NCFC Business Consulting INTRODUCTION The following are brief descriptions of how some intergenerational business succession plans have been implemented. These

Succession Planning Case Studies Prepared by NCFC Business Consulting INTRODUCTION The following are brief descriptions of how some intergenerational business succession plans have been implemented. These

PARTNERSHIP/LLC TAX ORGANIZER FORM 1065 (LONG VERSION)

") PARTNERSHIP/LLC TAX ORGANIZER FORM 1065 (LONG VERSION) Enclosed is an organizer that I (we) provide to our tax clients to assist in gathering the information necessary to prepare the current year tax returns.

PARTNERSHIP/LLC TAX ORGANIZER FORM 1065 (LONG VERSION) Enclosed is an organizer that I (we) provide to our tax clients to assist in gathering the information necessary to prepare the current year tax returns.

Ipx!up!hfu!uif Dsfeju!zpv!Eftfswf

Ipx!up!hfu!uif Dsfeju!zpv!Eftfswf Credit is the lifeblood of South Louisiana business, especially for the smaller firm. It helps the small business owner get started, obtain equipment, build inventory,

Ipx!up!hfu!uif Dsfeju!zpv!Eftfswf Credit is the lifeblood of South Louisiana business, especially for the smaller firm. It helps the small business owner get started, obtain equipment, build inventory,

Appraisal A written analysis prepared by a qualified appraiser and estimating the value of a property

REAL ESTATE BASICS Affordability Analysis An analysis of a buyer s ability to afford the purchase of a home, reviews income, liabilities, and available funds, and considers the type of mortgage a buyer

REAL ESTATE BASICS Affordability Analysis An analysis of a buyer s ability to afford the purchase of a home, reviews income, liabilities, and available funds, and considers the type of mortgage a buyer

PARTNERSHIP/LLC TAX ORGANIZER (FORM 1065)

") Enclosed is an organizer that provide to our tax clients to assist in gathering the information necessary to prepare the current year tax returns. The Internal Revenue Service matches information returns

Enclosed is an organizer that provide to our tax clients to assist in gathering the information necessary to prepare the current year tax returns. The Internal Revenue Service matches information returns

A Consumer s Guide to. Buying a Co-op

A Consumer s Guide to Buying a Co-op A Consumer s Guide to Buying a Co-op In the United States, more than 1.2 million families of all income levels live in homes owned and operated through cooperative

A Consumer s Guide to Buying a Co-op A Consumer s Guide to Buying a Co-op In the United States, more than 1.2 million families of all income levels live in homes owned and operated through cooperative

Mortgage Interest & Tracing Rules

Mortgage Interest & Tracing Rules By Phil Shaffer, EA, CFP Acquisition Debt Main or second home Acquire Construct Substantially Improve» Can be additional amounts Must be secured by the home Debt is limited

Mortgage Interest & Tracing Rules By Phil Shaffer, EA, CFP Acquisition Debt Main or second home Acquire Construct Substantially Improve» Can be additional amounts Must be secured by the home Debt is limited

Understanding the APOD How to Crunch the Numbers on Your Investment Transaction

Understanding the APOD How to Crunch the Numbers on Your Investment Transaction Commercial Investment Education Alliance Commercial Success Series 105 1 Commercial Investment Education Alliance Please

Understanding the APOD How to Crunch the Numbers on Your Investment Transaction Commercial Investment Education Alliance Commercial Success Series 105 1 Commercial Investment Education Alliance Please

The IRA Rollover. Making Sense Out of Your Retirement Plan Distribution

The IRA Rollover Making Sense Out of Your Retirement Plan Distribution Expecting a Distribution? You have been a participant in your employer s retirement plan for a number of years, and you have earned

The IRA Rollover Making Sense Out of Your Retirement Plan Distribution Expecting a Distribution? You have been a participant in your employer s retirement plan for a number of years, and you have earned

How should banks account for their investment in other real estate owned (OREO) property?

property?") TOPIC 5: OTHER ASSETS 5A. REAL ESTATE Question 1: (December 2008) How should banks account for their investment in other real estate owned (OREO) property? Detailed accounting guidance for OREO is provided

TOPIC 5: OTHER ASSETS 5A. REAL ESTATE Question 1: (December 2008) How should banks account for their investment in other real estate owned (OREO) property? Detailed accounting guidance for OREO is provided

GENERAL MATH PROBLEM CATEGORIES AND ILLUSTRATED SOLUTIONS MEASUREMENT STANDARDS WHICH MUST BE MEMORIZED FOR THE BROKER TEST

Chapter 17 Math Problem Solutions CHAPTER 17 GENERAL MATH PROBLEM CATEGORIES AND ILLUSTRATED SOLUTIONS MEASUREMENT STANDARDS WHICH MUST BE MEMORIZED FOR THE BROKER TEST Linear Measure 12 inches = 1 ft

Chapter 17 Math Problem Solutions CHAPTER 17 GENERAL MATH PROBLEM CATEGORIES AND ILLUSTRATED SOLUTIONS MEASUREMENT STANDARDS WHICH MUST BE MEMORIZED FOR THE BROKER TEST Linear Measure 12 inches = 1 ft

Module 10 S Corporation/Corporation Workbook Introduction

Module 10 Workbook Introduction Running your own business presents many challenges. One of the most difficult is complying with complex and ever-changing tax laws. This small-business tax education program

Module 10 Workbook Introduction Running your own business presents many challenges. One of the most difficult is complying with complex and ever-changing tax laws. This small-business tax education program

NORTH AMERICAN TITLE COMPANY Like Clockwork. www.nat.com/cfpb

NORTH AMERICAN TITLE COMPANY Like Clockwork www.nat.com/cfpb UNDERSTANDING THE NEW LOAN ESTIMATE AND CLOSING DISCLOSURE FORMS American Title, we want to make sure all of our customers have the information

NORTH AMERICAN TITLE COMPANY Like Clockwork www.nat.com/cfpb UNDERSTANDING THE NEW LOAN ESTIMATE AND CLOSING DISCLOSURE FORMS American Title, we want to make sure all of our customers have the information

Valuation of S-Corporations

Valuation of S-Corporations Prepared by: Presented by: Hugh H. Woodside, ASA, CFA Empire Valuation Consultants, LLC 777 Canal View Blvd., Suite 200 Rochester, NY 14623 Phone: (585) 475-9260 Fax: (585)

Valuation of S-Corporations Prepared by: Presented by: Hugh H. Woodside, ASA, CFA Empire Valuation Consultants, LLC 777 Canal View Blvd., Suite 200 Rochester, NY 14623 Phone: (585) 475-9260 Fax: (585)

THE FOREIGN INVESTMENT IN REAL PROPERTY TAX ACT (FIRPTA)

") THE FOREIGN INVESTMENT IN REAL PROPERTY TAX ACT (FIRPTA) FIRPTA s is to ensure non-resident aliens file U.S. income tax returns and pay taxes on profits generated in the U.S. FIRPTA requires 10% of the

THE FOREIGN INVESTMENT IN REAL PROPERTY TAX ACT (FIRPTA) FIRPTA s is to ensure non-resident aliens file U.S. income tax returns and pay taxes on profits generated in the U.S. FIRPTA requires 10% of the

PLANNING FOR FOREIGN INVESTMENT IN U.S. REAL ESTATE

PLANNING FOR FOREIGN INVESTMENT IN U.S. REAL ESTATE R I C H A R D L. H E R R M A N N GRANT, HERRMANN, SCHWARTZ & KLINGER LLP 675 THIRD AVENUE NEW YORK, NY 10017 Tel: 212-682-1800 Fax: 212-682-1850 www.ghsklaw.com

PLANNING FOR FOREIGN INVESTMENT IN U.S. REAL ESTATE R I C H A R D L. H E R R M A N N GRANT, HERRMANN, SCHWARTZ & KLINGER LLP 675 THIRD AVENUE NEW YORK, NY 10017 Tel: 212-682-1800 Fax: 212-682-1850 www.ghsklaw.com

Appendix C: HUD-1 Settlement Statement

Appendix C: HUD-1 Settlement Statement HUD-1 Settlement Statement The Settlement Statement, or HUD-1 Form, details the exact breakdown of all the money paid or received by both the buyer and the seller.

Appendix C: HUD-1 Settlement Statement HUD-1 Settlement Statement The Settlement Statement, or HUD-1 Form, details the exact breakdown of all the money paid or received by both the buyer and the seller.

Money Management Test - MoneyPower

Money Management Test - MoneyPower Multiple Choice Identify the choice that best completes the statement or answers the question. 1. A person s debt ratio shows the relationship between debt and net worth.

Money Management Test - MoneyPower Multiple Choice Identify the choice that best completes the statement or answers the question. 1. A person s debt ratio shows the relationship between debt and net worth.

Accounts payable Money which you owe to an individual or business for goods or services that have been received but not yet paid for.

A Account A record of a business transaction. A contract arrangement, written or unwritten, to purchase and take delivery with payment to be made later as arranged. Accounts payable Money which you owe

A Account A record of a business transaction. A contract arrangement, written or unwritten, to purchase and take delivery with payment to be made later as arranged. Accounts payable Money which you owe

Spin-Off of Time Warner Cable Inc. Tax Information Statement As of March 19, 2009

Spin-Off of Time Warner Cable Inc. Tax Information Statement As of March 19, 2009 On March 12, 2009, Time Warner Inc. ( Time Warner ) completed the spin-off (the Spin-Off ) of Time Warner s ownership interest

Spin-Off of Time Warner Cable Inc. Tax Information Statement As of March 19, 2009 On March 12, 2009, Time Warner Inc. ( Time Warner ) completed the spin-off (the Spin-Off ) of Time Warner s ownership interest

2010 Partner s Instructions for Schedule K-1 (Form 1065) Partner s Share of Income, Deductions, Credits, etc. (For Partner s Use Only)

Partner s Share of Income, Deductions, Credits, etc. (For Partner s Use Only)") 2010 Partner s Instructions for Schedule K-1 (Form 1065) Partner s Share of Income, Deductions, Credits, etc. (For Partner s Use Only) Section references are to the Internal Revenue Code unless otherwise

2010 Partner s Instructions for Schedule K-1 (Form 1065) Partner s Share of Income, Deductions, Credits, etc. (For Partner s Use Only) Section references are to the Internal Revenue Code unless otherwise

Your U.S. vacation property could be quite taxing by Jamie Golombek

June 2015 Your U.S. vacation property could be quite taxing by Jamie Golombek It seems everywhere we look, Canadians are snapping up U.S. vacation properties. Though your vacation property may be located

June 2015 Your U.S. vacation property could be quite taxing by Jamie Golombek It seems everywhere we look, Canadians are snapping up U.S. vacation properties. Though your vacation property may be located