Central Mortgage Company

|

|

|

- Phillip Mosley

- 8 years ago

- Views:

Transcription

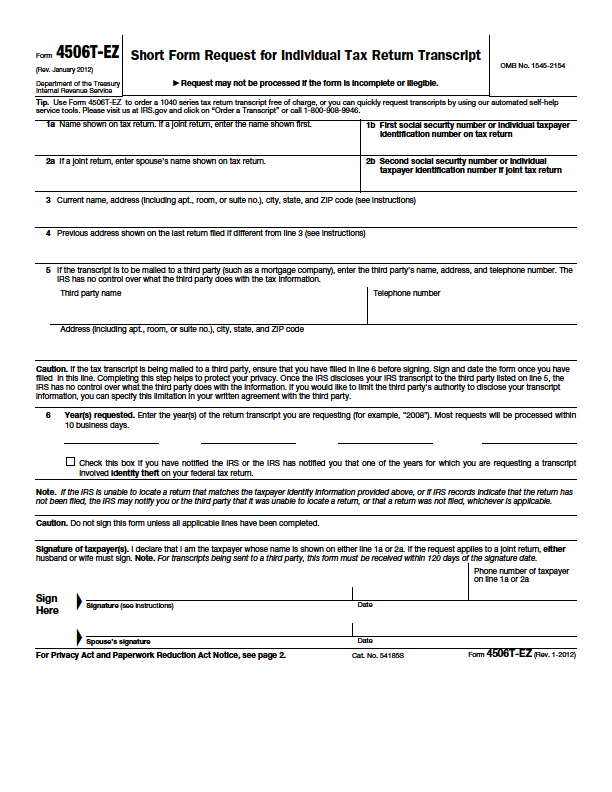

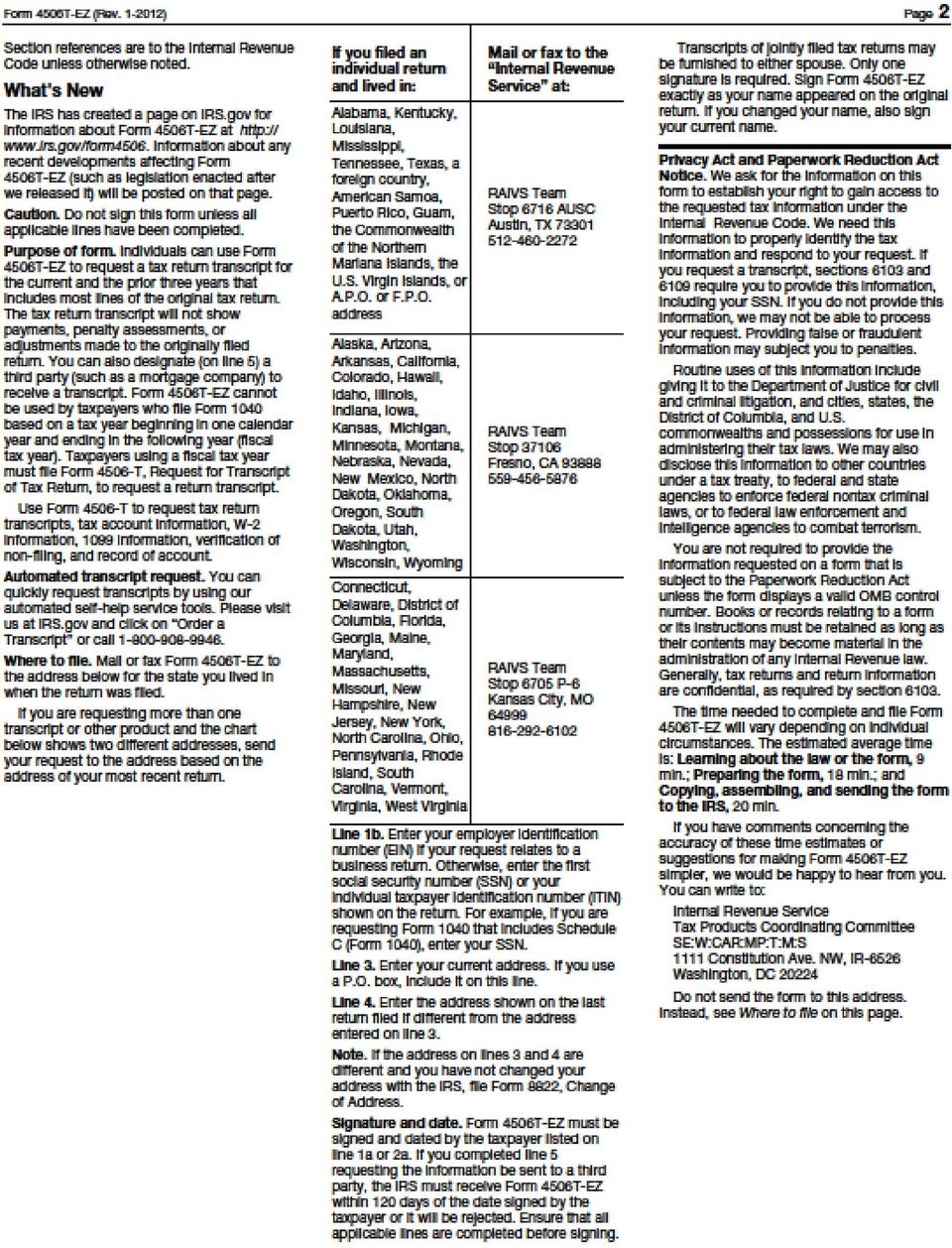

1 Central Mortgage Company Dear Borrower Are you struggling with your mortgage payment? We are concerned about your missed or potentially missed mortgage payment and want you to be aware of assistance available to you. We Are Here to Help You If you are unable to make your payment or bring it current it is critical that you work with us on a resolution for any issues that affect your ability to make timely mortgage payments, whether your challenges are temporary or long term. The sooner you respond, the more quickly we can determine whether you qualify for assistance. Options May Be Available The right option for you depends on your individual circumstances. If you provide all required information and documentation about your situation, we can determine if you qualify for temporary or long-term relief, including solutions that may allow you to stay in your home (refinance, repayment, forbearance, loan modification) or leave your home while avoiding foreclosure (short sale or deed-in-lieu of foreclosure). For more details, please see the attachment on Avoiding Foreclosure. Send Us the Information We Need to Help You Requesting help is the first step. Start by providing information and documentation to help us understand the challenges you are facing. To do this, follow the detailed instructions on the attached Homeowner Checklist to complete and submit your Borrower Response Package to us. Once we have received and evaluated your information, we will contact you regarding your options and next steps. Learn More and Act Now For more information, please see the Frequently Asked Questions and other information provided with this letter. If you need assistance, contact our customer support team at Remember, you need to take action by completing and returning the entire Borrower Response Package as soon as possible Sincerely, Loss Mitigation Department TO RECEIVE HELP WITH YOUR MORTGAGE, YOU NEED TO ACT: 1. See the instructions on the Homeowner Checklist 2. Review: NOW! Avoiding Foreclosure Frequently Asked Questions Beware of Foreclosure Rescue Scams 3. Submit required Borrower Response Package: Uniform Borrower Assistance Form (Borrower Assistance Form) (attached) IRS Form 4506T-EZ (attached) Income Documentation (described on Borrower Assistance Form) Hardship Documentation (described on Borrower Assistance Form) If you need assistance, contact us immediately at: Page 1 of 6

2 Homeowner Checklist For Your Information Only - Do Not Return with Your Borrower Response Package GET STARTED use this checklist to ensure you have completed all required forms and have the right information. Step 1 Step 2 Review the information provided to help you understand your options, responsibilities, and next steps: Avoiding Foreclosure Frequently Asked Questions Beware of Foreclosure Rescue Scams Complete and sign the enclosed Borrower Assistance Form. Must be signed by all borrowers on the mortgage (notarization is not required) and must include: All income, expenses, and assets for each borrower An explanation of financial hardship that makes it difficult to pay the mortgage Your acknowledgment and agreement that all information that you provide is true and accurate Step 3 Complete and sign a dated copy of the enclosed IRS Form 4506-T For each borrower, please submit a signed, dated copy of IRS Form 4506T-EZ (Short Form Request for Individual Tax Return Transcript) Borrowers who filed their tax returns jointly may send in one IRS Form 4506T-EZ signed and dated by both joint filers Step 4 Step 5 Step 6 Provide required Hardship Documentation. This documentation will be used to verify your hardship. Follow the instructions set forth on the Borrower Assistance Form (attached) Provide required Income Documentation. This documentation will be used to verify your hardship and all of your income (Notice: Alimony, child support or separate maintenance income need not be revealed if you do not choose to have it considered for repaying this loan). Follow the instructions set forth on the Borrower Assistance Form (attached) You may also disclose any income from a household member who is not on the promissory note (nonborrower), such as a relative, spouse, domestic partner, or fiancé who occupies the property as a primary residence. If you elect to disclose and rely upon this income to qualify, the required income documentation is the same as the income documentation required for a borrower. See Page 2 of the Borrower Assistance Form for specific details on income documentation. Gather and send completed documents your Borrower Response Package You must send in all required documentation listed in steps 2-4 above, and summarized below: Borrower Assistance Form (attached) Form 4506T-EZ (attached) Income Documentation as outlined on Page 2 of the Borrower Assistance Form (attached) Hardship Documentation as outlined on Page 3 of the Borrower Assistance Form (attached) Please mail all documents above to us: Central Mortgage Co., 700 A Southwest Blvd, Jefferson City, MO IMPORTANT REMINDERS: If you cannot provide the documentation within the time frame provided, have other types of income not specified on Page 2 of the Borrower Assistance Form, cannot locate some or all of the required documents, OR have any questions, please contact us at Keep a copy of all documents and proof of mailing/ ing for your records. Don t send original income or hardship documents. Copies are acceptable. Questions? Contact us at Page 2 of 6

3 Information on Avoiding Foreclosure For Your Information Only - Do Not Return with Your Borrower Response Package Mortgage Programs Are Available to Help There are a variety of programs available to help you resolve your delinquency and keep your home. You may be eligible to refinance or modify your mortgage to make your payments and terms more manageable, for instance, lowering your monthly payment to make it more affordable. Or, if you have missed a few payments, you may qualify for a temporary (or permanent) solution to help you get your finances back on track. Depending on your circumstances, staying in your home may not be possible. However, a short sale or deed-in-lieu of foreclosure may be a better choice than foreclosure see the table below for more information: OPTION OVERVIEW BENEFIT Refinance Receive a new loan with lower interest rate or Makes your payment or terms more affordable other favorable terms Reinstatement Pay the total amount you owe, in a lump sum payment and by a specific date. This may follow a forbearance plan as described below Allows you to avoid foreclosure by bringing your mortgage current if you can show you have funds that will become available at a specific date in the future Repayment Plan* Forbearance Plan* Modification Short Sale Deed-in-Lieu of Foreclosure Pay back your past-due payments together with your regular payments over an extended period of time Make reduced mortgage payments or no mortgage payments for a specific period of time Receive modified terms of your mortgage to make it more affordable or manageable after successfully making the reduced payment during a trial period (i.e., completing a three [or four] month trial period plan) Sell your home and pay off a portion of your mortgage balance when you owe more on the home than it is worth Transfer the ownership of your property to us Allows you time to catch up on late payments without having to come up with a lump sum Have time to improve your financial situation and get back on your feet Permanently modifies your mortgage so that your payments or terms are more manageable as a permanent solution to a long-term or permanent hardship Allows you to transition out of your home without going through foreclosure. In some cases relocation assistance may be available Allows you to transition out of your home without going through foreclosure. In some cases relocation assistance may be available. This is useful when there are no other liens on your property We Want to Help Take action and gain peace of mind and control of your situation. Complete and return the Borrower Response Package to start the process of getting the help you need now. Page 3 of 6

solution to help you get your finances back on track.")

4 Frequently Asked Questions For Your Information Only - Do Not Return with Your Borrower Response Package 1. Why Did I Receive This Package? You received this package because we have not received one or more of your monthly mortgage payments and want to help you keep your home if at all possible. We are sending this information to you now so that we can work with you to quickly resolve any temporary or long-term financial challenge you face to making all of your late mortgage payments. 2. Where Can I Find More Information on Foreclosure Prevention? Please see the Avoiding Foreclosure attachment in this package for more information, or you can contact us Central Mortgage Co. at Will I Be Evaluated for the Federal Home Affordable Modification Program (HAMP) When I Submit My Borrower Response Package? If you are not eligible for a refinance, reinstatement, repayment, or forbearance plan based on the information you provide, we will evaluate you for participation in the Home Affordable Modification Program (HAMP). If you are not eligible for HAMP, we will evaluate you for a non-hamp Fannie Mae loan modification. 4. Will It Cost Money to Get Help? There should never be a fee from your servicer or qualified counselor to obtain assistance or information about foreclosure prevention options. However, foreclosure prevention has become a target for scam artists. Be wary of companies or individuals offering to help you for a fee, and never send a mortgage payment to any company other than the one listed on your monthly mortgage statement or one designated to receive your payments under a state assistance program. 5. What Happens Once I Have Sent the Borrower Response Package to You? We will contact you within three business days of our receipt of your Borrower Response Package to confirm that we have received your package and will review it to determine whether it is complete. Within five business days of receipt of your request, we will send you a notice of incompleteness in the event there is any missing information or documentation that you must still submit. We cannot guarantee that you will receive any (or a particular type of) assistance. Within 30 days of receipt of a complete Borrower Response Package, we will let you know which foreclosure alternatives, if any, are available to you and will inform you of your next steps to accept our offer. However, if you submit your complete Borrower Response Package less than 37 days prior to a scheduled foreclosure sale date, we will strive to process your request as quickly as possible, but you may not receive a notice of incompleteness or a decision on your request prior to sale. Please submit your Borrower Response Package as soon as possible. 6. What Happens to My Mortgage While You Are Evaluating My Borrower Response Package? You remain obligated to make all mortgage payments as they come due, even while we are evaluating the types of assistance that may be available. 7. Will the Foreclosure Process Begin If I Do Not Respond to this Letter? If you have missed four monthly payments or there is reason to believe the property is vacant or abandoned, we may refer your mortgage to foreclosure regardless of whether you are being considered for a modification or other types of foreclosure alternatives. Page 4 of 6

5 8. What Happens if I Have Waited Too Long and My Property Has Been Referred to an Attorney for Foreclosure? Should I Still Contact You? Yes, the sooner the better! 9. What if My Property is Scheduled for a Foreclosure Sale in the Future? If you submit a complete Borrower Response Package less than 37 calendar days before a scheduled foreclosure sale, there is no guarantee we can evaluate you for a foreclosure alternative in time to stop the foreclosure sale. Even if we are able to approve you for a foreclosure alternative prior to a sale, a court with jurisdiction over the foreclosure proceeding (if any) or public official charged with carrying out the sale may not halt the scheduled sale. 10. Will My Property be Sold at a Foreclosure Sale If I Accept a Foreclosure Alternative? No. The property will not be sold at a foreclosure sale once you accept a foreclosure alternative, such as a forbearance or repayment plan, and comply with all requirements. 11. Will My Credit Score Be Affected by My Late Payments or Being in Default? The delinquency status of your loan will be reported to credit reporting agencies as well as your entry into a Repayment Plan, Forbearance Plan, or Trial Period Plan in accordance with the requirements of the Fair Credit Reporting Act and the Consumer Data Industry Association requirements. 12. Will My Credit Score Be Affected if I Accept a Foreclosure Prevention Option? While the affect on your credit will depend on your individual credit history, credit scoring companies generally would consider entering into a plan with reduced payments as increasing your credit risk. As a result, entering into a plan with reduced payments may adversely affect your credit score, particularly if you are current on your mortgage or otherwise have a good credit score. 13. Is Foreclosure Prevention Counseling Available? Yes, HUD-approved counselors are available to provide you with the information and assistance you may need to avoid foreclosure. You can use the search tool at to find a counselor near you. 14. I Have Seen Ads and Flyers From Companies Offering to Help Me Avoid Foreclosure for a Fee. Are These Companies on the Level? Foreclosure prevention has become a target for scam artists. We suggest using the HUD Web site referenced in question 13 to locate a counselor near you. Also, please refer to the attached document called Beware of Foreclosure Rescue Scams for more information. Page 5 of 6

6 BEWARE OF FORECLOSURE RESCUE SCAMS TIPS & WARNING SIGNS For Your Information Only - Do Not Return with Your Borrower Response Package Scam artists are stealing millions of dollars from distressed homeowners by promising immediate relief from foreclosure, or demanding cash for counseling services when HUD approved counseling agencies provide the same services for FREE. If you receive an offer, information or advice that sounds too good to be true, it probably is. Don't let them take advantage of you, your situation, your house or your money. Remember, help is FREE. How to Spot a Scam beware of a company or person who: Asks for a fee in advance to work with your lender to modify, refinance or reinstate your mortgage. Guarantees they can stop a foreclosure or get your loan modified. Advises you to stop paying your mortgage company and pay them instead. Pressures you to sign over the deed to your home or sign any paperwork that you haven't had a chance to read, and you don't fully understand. Claims to offer "government approved" or "official government" loan modifications. Asks you to release personal financial information online or over the phone and you have not been working with this person and/or do not know them. How to Report a Scam do one of the following: Go to and fill out the Loan Modification Scam Prevention Network s (LMSPN) complaint form online and get more information on how to fight back. Note: you can also fill out this form and send to the fax number/ /address (your choice!) on the back of the form. Call 1(888)995 HOPE (4673) and tell the counselor about your situation and that you believe you got scammed or know of a scam. Appendix A Beware of Scams Provides tips for The avoiding Loan Modification scams and Scam instructions Prevention Network is a national coalition of governmental how to report a and potentim. private organizations led by Fannie Mae, Freddie Mac, NeighborWorks America and the Lawyers Committee for Civil Rights Under Law. Page 6 of 6

7

8

9

10

11

12 Supplemental Information for Modification Consideration Please provide the monthly household expenses for any additional items that apply. Sign and return with all other required documents. Child Care $ Water/Sewer/Utilities $ Telephone Cell Phone $ $ Health Insc. Premiums $ (include only if not withheld from pay) Medical $ (including co-pays and monthly prescriptions----include only if not withheld from pay) Auto Expense/Insc. $ Life Insc. Premiums (include only if not withheld from pay) $ Food Other/Misc. $ $ Page 1 of 1

Auto Expense/Insc. $ Life Insc. Premiums (include only if not withheld from pay) $ Food Other/Misc.")

13

14

Homeowner Request for Assistance

Homeowner Request for Assistance In this packet. Thank you in advance for allowing your Credit Union to review your account for mortgage assistance. Homeowner Checklist Details the documents and forms

Homeowner Request for Assistance In this packet. Thank you in advance for allowing your Credit Union to review your account for mortgage assistance. Homeowner Checklist Details the documents and forms

Information on Avoiding Foreclosure

Whitney Bank offers and provides financial products and services through its locations in Louisiana and Texas as "Whitney Bank" and as "Hancock Bank" in Mississippi, Alabama and Florida. Information on

Whitney Bank offers and provides financial products and services through its locations in Louisiana and Texas as "Whitney Bank" and as "Hancock Bank" in Mississippi, Alabama and Florida. Information on

Call us today to learn more about your options. 866-743-4931

Hello from Umpqua, Thank you for requesting information about assistance with your mortgage loan. We Are Here to Help You It is critical that you work with us on a resolution for any issues that affect

Hello from Umpqua, Thank you for requesting information about assistance with your mortgage loan. We Are Here to Help You It is critical that you work with us on a resolution for any issues that affect

Guide. Completing the Mortgage Assistance Application

Guide Completing the Mortgage Assistance Application Getting Started PNC Mortgage Assistance Application Early communication with PNC is very important to ensure your assistance options are not limited.

Guide Completing the Mortgage Assistance Application Getting Started PNC Mortgage Assistance Application Early communication with PNC is very important to ensure your assistance options are not limited.

Borrower Response Package Directions Mortgage Assistance Request Form Follows

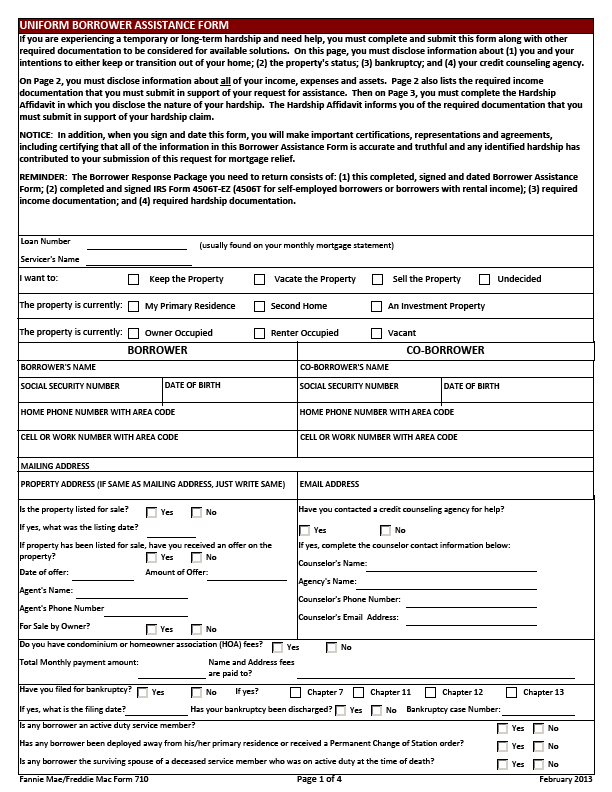

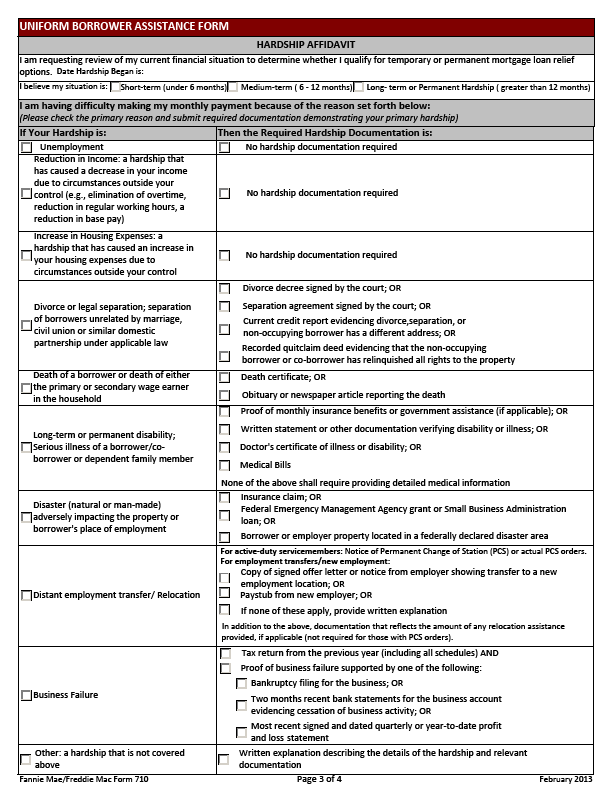

Borrower Response Package Directions Mortgage Assistance Request Form Follows If you are experiencing a temporary or long-term hardship and need help, you must complete and submit this form along with

Borrower Response Package Directions Mortgage Assistance Request Form Follows If you are experiencing a temporary or long-term hardship and need help, you must complete and submit this form along with

AVOID FORECLOSURE HOW TO A CONSUMER GUIDE. Open mail from your mortgage company. Can you afford your home? Contact your mortgage company

HOW TO AVOID FORECLOSURE A CONSUMER GUIDE Open mail from your mortgage company Can you afford your home? Contact your mortgage company Keeping or not keeping your home What happens if you do not contact

HOW TO AVOID FORECLOSURE A CONSUMER GUIDE Open mail from your mortgage company Can you afford your home? Contact your mortgage company Keeping or not keeping your home What happens if you do not contact

Avoid Foreclosure. How to Help Yourself (or someone you know) A Step-By-Step Consumer Self-Help Kit. Plus: How to Spot & Report Loan Scams!

A Step-By-Step Consumer Self-Help Kit. Plus: How to Spot & Report Loan Scams!") How to Help Yourself (or someone you know) Plus: How to Spot & Report Loan Scams! Avoid Foreclosure A Step-By-Step Consumer Self-Help Kit Open mail from your mortgage company Can you afford your home?

How to Help Yourself (or someone you know) Plus: How to Spot & Report Loan Scams! Avoid Foreclosure A Step-By-Step Consumer Self-Help Kit Open mail from your mortgage company Can you afford your home?

Making Home Affordable Act Now to Get the Help You Need

Making Home Affordable Act Now to Get the Help You Need Help for America s Homeowners SM MAKING HOME AFFORDABLE The Obama Administration s Making Home Affordable Program is a critical part of the effort

Making Home Affordable Act Now to Get the Help You Need Help for America s Homeowners SM MAKING HOME AFFORDABLE The Obama Administration s Making Home Affordable Program is a critical part of the effort

H O W T O A V O I D F O R E C L O S U R E F O R E C L O S U R E

U.S. Department of Housing and Urban Development H O W T O A V O I D F O R E C L O S U R E F O R E C L O S U R E This booklet explains how property owners can avoid losing their homes because of delinquent

U.S. Department of Housing and Urban Development H O W T O A V O I D F O R E C L O S U R E F O R E C L O S U R E This booklet explains how property owners can avoid losing their homes because of delinquent

AVOID FORECLOSURE HOW TO A CONSUMER GUIDE. Open mail from your mortgage company. Can you afford your home? Contact your mortgage company

HOW TO AVOID FORECLOSURE A CONSUMER GUIDE Open mail from your mortgage company Can you afford your home? Contact your mortgage company Keeping or not keeping your home What happens if you do not contact

HOW TO AVOID FORECLOSURE A CONSUMER GUIDE Open mail from your mortgage company Can you afford your home? Contact your mortgage company Keeping or not keeping your home What happens if you do not contact

How To Avoid Foreclosure

For most families, a home is a place to live and raise children; it s a plan for the future, and also a source of pride. The Town of Davie promotes home preservation. Your home is not only a significant

For most families, a home is a place to live and raise children; it s a plan for the future, and also a source of pride. The Town of Davie promotes home preservation. Your home is not only a significant

Fannie Mae Mortgage Help Center Tampa Homeowner Packet

1300 N Westshore Blvd., Suite 220 Tampa, FL 33607 (866) 442-8554 phone (866) 442-6250 fax Fannie Mae Mortgage Help Center Tampa Homeowner Packet 1300 N. Westshore Blvd., Suite 220 Tampa, FL 33607 (866)

1300 N Westshore Blvd., Suite 220 Tampa, FL 33607 (866) 442-8554 phone (866) 442-6250 fax Fannie Mae Mortgage Help Center Tampa Homeowner Packet 1300 N. Westshore Blvd., Suite 220 Tampa, FL 33607 (866)

Step-by-step process to apply for a loan modification with your lender/servicer

Step-by-step process to apply for a loan modification with your lender/servicer Step 1: Determine your eligibility status before contacting your lender You must have a steady income and a positive budget

Step-by-step process to apply for a loan modification with your lender/servicer Step 1: Determine your eligibility status before contacting your lender You must have a steady income and a positive budget

BORROWER Q&AS. 2. I'm current on my mortgage. Will the Home Affordable Refinance help me?

MAKING HOME AFFORDABLE BORROWER Q&AS 1. What is Making Home Affordable" all about? Making Home Affordable is part of President Obama's comprehensive strategy to get the housing market back on track. Through

MAKING HOME AFFORDABLE BORROWER Q&AS 1. What is Making Home Affordable" all about? Making Home Affordable is part of President Obama's comprehensive strategy to get the housing market back on track. Through

Need Help With Your Mortgage?

ACT NOW TO GET THE HELP YOU NEED! Need Help With Your Mortgage? Learn how you may be able to make your mortgage payment more affordable. Beware of Foreclosure Rescue Scams Assistance from a HUD-approved

ACT NOW TO GET THE HELP YOU NEED! Need Help With Your Mortgage? Learn how you may be able to make your mortgage payment more affordable. Beware of Foreclosure Rescue Scams Assistance from a HUD-approved

FOR SALE. Sheeley Moving Co. AVOIDING FORECLOSURE & FORECLOSURE SCAMS

FAIR HOUSING UNIVERSITY FOR SALE Sheeley Moving Co. AVOIDING FORECLOSURE & FORECLOSURE SCAMS WHAT IS FORECLOSURE When a lender takes possession of a house from a homeowner who has not met the mortgage

FAIR HOUSING UNIVERSITY FOR SALE Sheeley Moving Co. AVOIDING FORECLOSURE & FORECLOSURE SCAMS WHAT IS FORECLOSURE When a lender takes possession of a house from a homeowner who has not met the mortgage

Handling Default and Foreclosure

Handling Default and Foreclosure Delinquency Vs. Default Delinquency = less than 3 payments behind. A collections account. Only late fees accrue Default= more than 3 payments behind. Mortgage automatically

Handling Default and Foreclosure Delinquency Vs. Default Delinquency = less than 3 payments behind. A collections account. Only late fees accrue Default= more than 3 payments behind. Mortgage automatically

HOME PRESERVATION BASICS

HOME PRESERVATION BASICS - Know what to do and when to do it The current economic crisis has greatly affected the housing industry, and our local community is no exception. This has forced different households

HOME PRESERVATION BASICS - Know what to do and when to do it The current economic crisis has greatly affected the housing industry, and our local community is no exception. This has forced different households

Submission Avenues. Fax: You may fax all documents to 877-589-0758. A fax cover sheet with directions has been included for your use.

SunTrust Mortgage 1001 Semmes Avenue Richmond, Virginia 23224 Tel 800.443.1032 Submission Avenues Fax: You may fax all documents to 877-589-0758. A fax cover sheet with directions has been included for

SunTrust Mortgage 1001 Semmes Avenue Richmond, Virginia 23224 Tel 800.443.1032 Submission Avenues Fax: You may fax all documents to 877-589-0758. A fax cover sheet with directions has been included for

Bank of America Home Affordable Foreclosure Alternative (HAFA) Matrix

Matrix") Bank of America Home Affordable Foreclosure Alternative (HAFA) Matrix If you do not qualify for the Home Affordable Modification Program (HAMP) or other modification programs that we offer, you will be

Bank of America Home Affordable Foreclosure Alternative (HAFA) Matrix If you do not qualify for the Home Affordable Modification Program (HAMP) or other modification programs that we offer, you will be

Questions and Answers for Borrowers about the. Homeowner Affordability and Stability Plan

Questions and Answers for Borrowers about the Homeowner Affordability and Stability Plan Borrowers Who Are Current on Their Mortgage Are Asking: 1. What help is available for borrowers who stay current

Questions and Answers for Borrowers about the Homeowner Affordability and Stability Plan Borrowers Who Are Current on Their Mortgage Are Asking: 1. What help is available for borrowers who stay current

OPTIONS IN FORECLOSURE

Section II: KEEPING YOUR HOME OPTIONS IN FORECLOSURE Deciding whether or not to keep your home is something that only you, the homeowner, can determine. The best housing counselors will ask what you d

Section II: KEEPING YOUR HOME OPTIONS IN FORECLOSURE Deciding whether or not to keep your home is something that only you, the homeowner, can determine. The best housing counselors will ask what you d

Borrower FAQ. 1 of 12 8/6/2010 9:11 AM. In this section BORROWER FREQUENTLY ASKED QUESTIONS. Revised June 8, 2010

Text A+ A- A Need urgent help? Contact the Homeowner s HOPE Hotline: (888) 995-HOPE ABOUT ELIGIBILITY LOAN LOOK UP FIND A COUNSELOR REQUEST A MODIFICATION RESOURCES AUDIO AND VIDEO EN ESPAÑOL Borrower

Text A+ A- A Need urgent help? Contact the Homeowner s HOPE Hotline: (888) 995-HOPE ABOUT ELIGIBILITY LOAN LOOK UP FIND A COUNSELOR REQUEST A MODIFICATION RESOURCES AUDIO AND VIDEO EN ESPAÑOL Borrower

GLOSSARY COMMONLY USED REAL ESTATE TERMS

GLOSSARY COMMONLY USED REAL ESTATE TERMS Adjustable-Rate Mortgage (ARM): a mortgage loan with an interest rate that is subject to change and is not fixed at the same level for the life of the loan. These

GLOSSARY COMMONLY USED REAL ESTATE TERMS Adjustable-Rate Mortgage (ARM): a mortgage loan with an interest rate that is subject to change and is not fixed at the same level for the life of the loan. These

6 Steps to Completing Your Loan Modification Yourself

6 Steps to Completing Your Loan Modification Yourself Page 1 of 12 You hear it in the news almost every day, more and more hard working Americans are falling behind on their mortgage payments. Many real

6 Steps to Completing Your Loan Modification Yourself Page 1 of 12 You hear it in the news almost every day, more and more hard working Americans are falling behind on their mortgage payments. Many real

FORECLOSURE. I don t think I can make my mortgage payments but I don t want to go through a foreclosure. What are some of my options?

FORECLOSURE When you borrow money to buy a house or land, the creditor usually takes a security interest in the property you buy. This means that if you don t pay, the creditor can foreclose upon (or take

FORECLOSURE When you borrow money to buy a house or land, the creditor usually takes a security interest in the property you buy. This means that if you don t pay, the creditor can foreclose upon (or take

<Servicer Logo> Questions and Answers About Reverse Mortgages. If you have questions or need our help, call <8XX-XXX-XXXX>.

Questions and Answers , If you have questions or need our help, call . What is a reverse mortgage? A reverse mortgage is a loan

Questions and Answers , If you have questions or need our help, call . What is a reverse mortgage? A reverse mortgage is a loan

Ocwen Loan Servicing, LLC HELPING HOMEOWNERS IS WHAT WE DO! WWW.OCWEN.COM

12/20/11 Paula Bachaman (203) 548-9046 paula@propertychoicesllc.com Property Address: 1024 Lindley Street, Bridgeport, CT 06606 Borrower Name: Jacqueline Muniz Antonio Muniz RE: Short Sale Request Package

12/20/11 Paula Bachaman (203) 548-9046 paula@propertychoicesllc.com Property Address: 1024 Lindley Street, Bridgeport, CT 06606 Borrower Name: Jacqueline Muniz Antonio Muniz RE: Short Sale Request Package

How To Modify A First Lien Mortgage

Making Home Affordable Program and Home Affordable Modification Program Frequently Asked Questions for Bankruptcy Filers Q1. What do these FAQs cover? These FAQs provide information on the Home Affordable

Making Home Affordable Program and Home Affordable Modification Program Frequently Asked Questions for Bankruptcy Filers Q1. What do these FAQs cover? These FAQs provide information on the Home Affordable

Step 1. Step 2. Step 4

Doc Rev 10/23/14 Homeowner Checklist For Your Information Only Do Not Return with the Borrower Request for Assistance Form GET STARTED use this checklist to ensure you have completed all required forms

Doc Rev 10/23/14 Homeowner Checklist For Your Information Only Do Not Return with the Borrower Request for Assistance Form GET STARTED use this checklist to ensure you have completed all required forms

Glossary of Foreclosure Fairness Mediation Terminology

Glossary of Foreclosure Fairness Mediation Terminology Adjustable-Rate Mortgage (ARM) Mortgage repaid at the rate of interest that increases or decreases over the life of the loan based on market conditions.

Glossary of Foreclosure Fairness Mediation Terminology Adjustable-Rate Mortgage (ARM) Mortgage repaid at the rate of interest that increases or decreases over the life of the loan based on market conditions.

As soon as you know you can t make your payment, take the following steps:

As soon as you know you can t make your payment, take the following steps: Call your lender. Ask for the loss mitigation department. Be honest about your situation so you can get the best, most realistic

As soon as you know you can t make your payment, take the following steps: Call your lender. Ask for the loss mitigation department. Be honest about your situation so you can get the best, most realistic

HOW TO AVOID FORECLOSURE

U.S. Department of Housing and Urban Development HOW TO AVOID FORECLOSURE This booklet explains how property owners can avoid losing their homes because of delinquent payments. Este folleto explica a los

U.S. Department of Housing and Urban Development HOW TO AVOID FORECLOSURE This booklet explains how property owners can avoid losing their homes because of delinquent payments. Este folleto explica a los

Short Sale Seller Advisory

Short Sale Seller Advisory Short Sale Seller Advisory Recent economic challenges have resulted in many homeowners needing to sell their home but owing more on their home than the home is worth. This advisory

Short Sale Seller Advisory Short Sale Seller Advisory Recent economic challenges have resulted in many homeowners needing to sell their home but owing more on their home than the home is worth. This advisory

To see if you qualify for this program, send the items listed below to Northwest Savings Bank.

COMPLETE YOUR CHECKLIST We need this information to help you modify your mortgage payment. To see if you qualify for this program, send the items listed below to Northwest Savings Bank. 1. The enclosed

COMPLETE YOUR CHECKLIST We need this information to help you modify your mortgage payment. To see if you qualify for this program, send the items listed below to Northwest Savings Bank. 1. The enclosed

Homeowners are NOT eligible if: The loan is a land contract transaction or privately held mortgage A Foreclosure Sale has already been completed

Frequently Asked Questions 1. What is the Michigan s Hardest Hit Funds program? It is a federally funded loan program designed to help eligible homeowners who are struggling to make their mortgage payments.

Frequently Asked Questions 1. What is the Michigan s Hardest Hit Funds program? It is a federally funded loan program designed to help eligible homeowners who are struggling to make their mortgage payments.

Do You HAFA? The HAFA Short Sale Program under Making Home Affordable 2

Table of Contents Do You HAFA? The HAFA Short Sale Program under Making Home Affordable 2 INTRODUCTION 2 Overview: Making Home Affordable ( MHA ) 2 HOME AFFORDABLE FORECLOSURE ALTERNATIVES PROGRAM ( HAFA

Table of Contents Do You HAFA? The HAFA Short Sale Program under Making Home Affordable 2 INTRODUCTION 2 Overview: Making Home Affordable ( MHA ) 2 HOME AFFORDABLE FORECLOSURE ALTERNATIVES PROGRAM ( HAFA

About Northwest Counseling Service

About Northwest Counseling Service Non Profit Agency No Cost Housing Counseling Services Any Service Related To A Home Specialize In Mortgage Delinquency 96% Rate In Keeping Residents In Homes HUD Certified/OHCD

About Northwest Counseling Service Non Profit Agency No Cost Housing Counseling Services Any Service Related To A Home Specialize In Mortgage Delinquency 96% Rate In Keeping Residents In Homes HUD Certified/OHCD

To help you better understand the foreclosure process, these definitions are presented in a logical order, rather than alphabetical order.

FORECLOSURE GLOSSARY NOTICE: This glossary of legal words and phrases related to foreclosure is provided to you by the Clermont County Common Pleas Court to help you better understand your legal problem

FORECLOSURE GLOSSARY NOTICE: This glossary of legal words and phrases related to foreclosure is provided to you by the Clermont County Common Pleas Court to help you better understand your legal problem

General Program Questions

General Program Questions What is Save the Dream Ohio (Ohio s Hardest-Hit Fund)? The Housing Finance Agency Innovation Fund for the Hardest-Hit Housing Markets gave 18 states including Ohio, via Save the

General Program Questions What is Save the Dream Ohio (Ohio s Hardest-Hit Fund)? The Housing Finance Agency Innovation Fund for the Hardest-Hit Housing Markets gave 18 states including Ohio, via Save the

Frequently Asked Questions

Frequently Asked Questions On March 26, 2010, the Administration announced several enhancements to the existing Making Home Affordable Program (MHA) and the Federal Housing Administration (FHA) refinance

Frequently Asked Questions On March 26, 2010, the Administration announced several enhancements to the existing Making Home Affordable Program (MHA) and the Federal Housing Administration (FHA) refinance

TEN LOOPHOLES THAT CAN STOP FORCLOSURE FAST

TEN LOOPHOLES THAT CAN STOP FORCLOSURE FAST Copyright Notice All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means electronic or mechanical. Any

TEN LOOPHOLES THAT CAN STOP FORCLOSURE FAST Copyright Notice All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means electronic or mechanical. Any

Foreclosure Rescue. You Have Options! Inside: Powerful Strategies to Avoid Foreclosure. Are You at Risk of Losing Your Home in Foreclosure?

inside >>> The Foreclosure Process Your Options: - Negotiate a Loan Modification - Work out a Forbearance Plan - Obtain A Deed in Lieu of Foreclosure - Refinance Your House - File for Bankruptcy - Sell

inside >>> The Foreclosure Process Your Options: - Negotiate a Loan Modification - Work out a Forbearance Plan - Obtain A Deed in Lieu of Foreclosure - Refinance Your House - File for Bankruptcy - Sell

CALL TODAY: 480.948.6260. Options for Avoiding Foreclosure in Arizona ArizonaForeclosureRelief.com

Options for Avoiding Foreclosure in Arizona ArizonaForeclosureRelief.com Thank you for taking the time to request our free report on how to avoid foreclosure in Arizona. We greatly empathize with anyone

Options for Avoiding Foreclosure in Arizona ArizonaForeclosureRelief.com Thank you for taking the time to request our free report on how to avoid foreclosure in Arizona. We greatly empathize with anyone

Countrywide Settlement FAQ s

Countrywide Settlement FAQ s 1. Does the settlement impact my Countrywide loan? The Attorney General s settlement with Countrywide provides for loan modifications for eligible borrowers who are 60 days

Countrywide Settlement FAQ s 1. Does the settlement impact my Countrywide loan? The Attorney General s settlement with Countrywide provides for loan modifications for eligible borrowers who are 60 days

EHLP Homeowner Post Closing Counseling Summary and Confirmation

EHLP Homeowner Post Closing Counseling Summary and Confirmation NOTE: This form was updated and redesigned to be used for either 5b Post-Approval Counseling or for 5d Transition Counseling as applicable.

EHLP Homeowner Post Closing Counseling Summary and Confirmation NOTE: This form was updated and redesigned to be used for either 5b Post-Approval Counseling or for 5d Transition Counseling as applicable.

Countrywide Settlement FAQs

The Tennessee Attorney General s settlement with Countrywide offers several options for borrowers. If you do not see the answer to your question here, please contact Countrywide toll free at (800) 669

The Tennessee Attorney General s settlement with Countrywide offers several options for borrowers. If you do not see the answer to your question here, please contact Countrywide toll free at (800) 669

FORECLOSURE INTERVENTION PRESENTED BY BRIGHTON CENTER FINANCIAL SERVICES

FORECLOSURE INTERVENTION PRESENTED BY BRIGHTON CENTER FINANCIAL SERVICES WHAT IS FORECLOSURE Foreclosure is a legal remedy used by a mortgage company to assume ownership of a property when the required

FORECLOSURE INTERVENTION PRESENTED BY BRIGHTON CENTER FINANCIAL SERVICES WHAT IS FORECLOSURE Foreclosure is a legal remedy used by a mortgage company to assume ownership of a property when the required

The key components of the Making Home Affordable Program are:

REVISED AS OF JULY 13, 2009 HOUSING COUNSELOR FREQUENTLY ASKED QUESTIONS 1. What is the Making Home Affordable (MHA) Program? The Making Home Affordable Program is part of the Obama Administration s broad,

REVISED AS OF JULY 13, 2009 HOUSING COUNSELOR FREQUENTLY ASKED QUESTIONS 1. What is the Making Home Affordable (MHA) Program? The Making Home Affordable Program is part of the Obama Administration s broad,

FTC FACTS for Consumers

ftc.gov FEDERAL TRADE COMMISSION FOR THE CONSUMER 1-877-FTC-HELP FTC FACTS for Consumers Mortgage Payments Sending You Reeling? Here s What to Do T he possibility of losing your home because you can t

ftc.gov FEDERAL TRADE COMMISSION FOR THE CONSUMER 1-877-FTC-HELP FTC FACTS for Consumers Mortgage Payments Sending You Reeling? Here s What to Do T he possibility of losing your home because you can t

HAFA Short Sales, US Treasury, Fannie Mae & Freddie Mac Programs. Learning Objectives

HAFA Short Sales, US Treasury, Fannie Mae & Freddie Mac Programs Learning Objectives Module 1: HARP, HAMP & HAFA Overview Upon completion of Module 1 the student will be able to: Explain the advantages

HAFA Short Sales, US Treasury, Fannie Mae & Freddie Mac Programs Learning Objectives Module 1: HARP, HAMP & HAFA Overview Upon completion of Module 1 the student will be able to: Explain the advantages

HAMP vs. HARP vs. HAFA

HAMP vs. HARP vs. HAFA Over the last four years, the government has made a few sizable efforts to reduce the rising tide of foreclosures and help a significant number of homeowners stay in their homes.

HAMP vs. HARP vs. HAFA Over the last four years, the government has made a few sizable efforts to reduce the rising tide of foreclosures and help a significant number of homeowners stay in their homes.

What to Do When You Can t Pay Your Mortgage

What to Do When You Can t Pay Your Mortgage Marti Kilby, REALTOR Broker/Owner Steele Group Realty Distressed Property Consultant CA DRE License #01474222 Copyright 2013 Steele Group, Inc. Introduction

What to Do When You Can t Pay Your Mortgage Marti Kilby, REALTOR Broker/Owner Steele Group Realty Distressed Property Consultant CA DRE License #01474222 Copyright 2013 Steele Group, Inc. Introduction

Homeownership Preservation Toolkit

Homeownership Preservation Toolkit A guide to understanding and avoiding foreclosure Sponsored and Endorsed by Loveland Berthoud Association of REALTORS CONSUMER CREDIT COUNSELING SERVICE OF NORTHERN COLORADO

Homeownership Preservation Toolkit A guide to understanding and avoiding foreclosure Sponsored and Endorsed by Loveland Berthoud Association of REALTORS CONSUMER CREDIT COUNSELING SERVICE OF NORTHERN COLORADO

Home Affordable Modification Program (HAMP )

") Home Affordable Modification Program (HAMP ) Training for Trusted Advisors April 2015 Making Home Affordable Objectives 1 2 3 4 5 6 Step 1 Step 2 Step 3 Step 4 Step 5 7 8 MHA Program Highlights HAMP Overview

Home Affordable Modification Program (HAMP ) Training for Trusted Advisors April 2015 Making Home Affordable Objectives 1 2 3 4 5 6 Step 1 Step 2 Step 3 Step 4 Step 5 7 8 MHA Program Highlights HAMP Overview

REALTORS Guide to FORECLOSURE RESOURCES

REALTORS Guide to FORECLOSURE RESOURCES Federal & State Programs That May Help Those Facing Foreclosure Making Home Affordable Program Designed to assist families who may face foreclosure, the federal

REALTORS Guide to FORECLOSURE RESOURCES Federal & State Programs That May Help Those Facing Foreclosure Making Home Affordable Program Designed to assist families who may face foreclosure, the federal

Instructions for Mortgage Payment Assistance

Instructions for Mortgage Payment Assistance Below is a list of items needed for the Mortgage Servicing Loss Mitigation team to review your request for mortgage payment assistance. Please return all items

Instructions for Mortgage Payment Assistance Below is a list of items needed for the Mortgage Servicing Loss Mitigation team to review your request for mortgage payment assistance. Please return all items

Making Home Affordable

Making Home Affordable Overview of Programs What to Expect Overview of MHA Programs This presentation will: Provide an overview of Making Home Affordable (MHA) and its various components. Show you how

Making Home Affordable Overview of Programs What to Expect Overview of MHA Programs This presentation will: Provide an overview of Making Home Affordable (MHA) and its various components. Show you how

I m behind in my mortgage payments, what should I do?

FORECLOSURES This handout was prepared by Legal Services of Greater Miami, Inc.(LSGMI) with support from the Institute for Foreclosure Legal Assistance. LSGMI represents homeowners in foreclosure and homeowners

FORECLOSURES This handout was prepared by Legal Services of Greater Miami, Inc.(LSGMI) with support from the Institute for Foreclosure Legal Assistance. LSGMI represents homeowners in foreclosure and homeowners

Ocwen Loan Servicing, LLC HELPING HOMEOWNERS IS WHAT WE DO! WWW.OCWEN.COM

Ocwen Loan Servicing, LLC HELPING HOMEOWNERS IS WHAT WE DO! WWW.OCWEN.COM Loan Number: Dear Customer, Ocwen is committed to helping our customers facing financial difficulties. Since 2010, we have successfully

Ocwen Loan Servicing, LLC HELPING HOMEOWNERS IS WHAT WE DO! WWW.OCWEN.COM Loan Number: Dear Customer, Ocwen is committed to helping our customers facing financial difficulties. Since 2010, we have successfully

When life happens... Avoiding Foreclosure: How to Save Your Home. Finding the Right Help for Your Needs to Save Your Home & Salvage Your Credit

When life happens... Avoiding Foreclosure: How to Save Your Home Finding the Right Help for Your Needs to Save Your Home & Salvage Your Credit Taking Steps to Save Your Home Not only is your home where

When life happens... Avoiding Foreclosure: How to Save Your Home Finding the Right Help for Your Needs to Save Your Home & Salvage Your Credit Taking Steps to Save Your Home Not only is your home where

unemployed? Get Mortgage Relief and Get Back on Your Feet R E A L H E L P. R E A L A N S W E R S. R I G H T N O W.

unemployed? earning less than before? Get Mortgage Relief and Get Back on Your Feet R E A L H E L P. R E A L A N S W E R S. R I G H T N O W. IS THIS YOU? Are you having a tough time making your mortgage

unemployed? earning less than before? Get Mortgage Relief and Get Back on Your Feet R E A L H E L P. R E A L A N S W E R S. R I G H T N O W. IS THIS YOU? Are you having a tough time making your mortgage

Foreclosure Options. Know Your Rights! Your Trusted Real Estate Resource

Foreclosure Options Know Your Rights! Kirk Russell Managing Broker John L. Scott Firm Kirkrussell@johnlscott.com 206.390.5640 Your Trusted Real Estate Resource If you re listed with a license Realtor,

Foreclosure Options Know Your Rights! Kirk Russell Managing Broker John L. Scott Firm Kirkrussell@johnlscott.com 206.390.5640 Your Trusted Real Estate Resource If you re listed with a license Realtor,

Effective Foreclosure Time Line Management Reference Guide

Effective Foreclosure Time Line Management Reference Guide A foreclosure time line is the number of days it takes to process a foreclosure, from the due date of the last paid installment (DDLPI) to the

Effective Foreclosure Time Line Management Reference Guide A foreclosure time line is the number of days it takes to process a foreclosure, from the due date of the last paid installment (DDLPI) to the

T E X A S Y O U N G L A W Y E R S A S S O C I A T I O N A N D T H E S T A T E B A R O F T E X A S FA CING

T E X A S Y O U N G L A W Y E R S A S S O C I A T I O N A N D T H E S T A T E B A R O F T E X A S FA CING F ORECLOSURE FACING F O RECLOSURE "Facing Foreclosure" has been prepared as a public service by

T E X A S Y O U N G L A W Y E R S A S S O C I A T I O N A N D T H E S T A T E B A R O F T E X A S FA CING F ORECLOSURE FACING F O RECLOSURE "Facing Foreclosure" has been prepared as a public service by

These sample documents are for your reference only and are not to be filled out or submitted as originals.

9000 Southside Blvd Jacksonville, FL 32256 FL9-400-01-21 Phone: 1 (866) 413-3757 Email: jaxhelocshortsales@bankofamerica.com The following is a sample of the Home Equity Line of Credit (HELOC) Welcome

9000 Southside Blvd Jacksonville, FL 32256 FL9-400-01-21 Phone: 1 (866) 413-3757 Email: jaxhelocshortsales@bankofamerica.com The following is a sample of the Home Equity Line of Credit (HELOC) Welcome

HUD Housing Counselors Training

Module 5.2 Study Guide HUD Housing Counselors Training U.S. Department of Housing and Urban Development Table of Contents Module Introduction 3 Module Introduction 3 Lesson Objectives 3 Modifying or Refinancing

Module 5.2 Study Guide HUD Housing Counselors Training U.S. Department of Housing and Urban Development Table of Contents Module Introduction 3 Module Introduction 3 Lesson Objectives 3 Modifying or Refinancing

WAYNE COUNTY MORTGAGE FORECLOSURE PREVENTION PROGRAM

WAYNE COUNTY MORTGAGE FORECLOSURE PREVENTION PROGRAM Fight Mortgage Foreclosure SURVING FORECLOSURE Some Definitions Delinquency: When you are 15 days or more late Foreclosure: when the lender has filed

WAYNE COUNTY MORTGAGE FORECLOSURE PREVENTION PROGRAM Fight Mortgage Foreclosure SURVING FORECLOSURE Some Definitions Delinquency: When you are 15 days or more late Foreclosure: when the lender has filed

USDA Rural Development/Special Loan Servicing

Guidance Lender (Loan Holder/Loan Servicer) Borrowers USDA Rural Development/Special Loan Servicing The Lender must be a Section 502 Single Family Housing Guaranteed Loan Program approved Lender. The current

Guidance Lender (Loan Holder/Loan Servicer) Borrowers USDA Rural Development/Special Loan Servicing The Lender must be a Section 502 Single Family Housing Guaranteed Loan Program approved Lender. The current

Find the Solutions to Make Your Home More Affordable

Struggling To Make Your Mortgage Payments? Find the Solutions to Make Your Home More Affordable R E A L H E L P. R E A L A N S W E R S. R I G H T N O W. Having trouble making your mortgage payments? DO

Struggling To Make Your Mortgage Payments? Find the Solutions to Make Your Home More Affordable R E A L H E L P. R E A L A N S W E R S. R I G H T N O W. Having trouble making your mortgage payments? DO

FTC FACTS for Consumers

ftc.gov FEDERAL TRADE COMMISSION FOR THE CONSUMER 1-877-FTC-HELP FTC FACTS for Consumers Mortgage Payments Sending You Reeling? Here s What to Do T he possibility of losing your home because you can t

ftc.gov FEDERAL TRADE COMMISSION FOR THE CONSUMER 1-877-FTC-HELP FTC FACTS for Consumers Mortgage Payments Sending You Reeling? Here s What to Do T he possibility of losing your home because you can t

Guide to Fair Mortgage Lending and Home Preservation

Guide to Fair Mortgage Lending and Home Preservation Fair Housing Legal Support Center & Clinic Guide to Fair Mortgage Lending and Home Preservation What does this guide cover? What is Fair Lending? What

Guide to Fair Mortgage Lending and Home Preservation Fair Housing Legal Support Center & Clinic Guide to Fair Mortgage Lending and Home Preservation What does this guide cover? What is Fair Lending? What

Steps to a Home Retention Solution. Required Document Checklist Please verify that you have submitted the following items by checking the box:

Steps to a Home Retention Solution Follow these easy steps! 1. Call BCL of Texas and discuss your homeownership situation 2. Have Counselor explain the guidelines, check list, eligibility, and requirements

Steps to a Home Retention Solution Follow these easy steps! 1. Call BCL of Texas and discuss your homeownership situation 2. Have Counselor explain the guidelines, check list, eligibility, and requirements

Common Mortgage and Foreclosure Terms

H ELP FOR N EW Y ORK S TATE H OMEOWNERS C ONCERNED A BOUT F ORECLOSURE Common Mortgage and Foreclosure Terms Talking about mortgages can feel like speaking a foreign language and is even more confusing

H ELP FOR N EW Y ORK S TATE H OMEOWNERS C ONCERNED A BOUT F ORECLOSURE Common Mortgage and Foreclosure Terms Talking about mortgages can feel like speaking a foreign language and is even more confusing

Northern Arizona Council of Governments

Northern Arizona Council of Governments 119 EAST ASPEN AVENUE FLAGSTAFF, ARIZONA 86001-5222 (928) 774-1895 FAX (928) 773-1135 E-MAIL: khaislet@nacog.org KENNETH J. SWEET EXECUTIVE DIRECTOR Dear Homeowner,

Northern Arizona Council of Governments 119 EAST ASPEN AVENUE FLAGSTAFF, ARIZONA 86001-5222 (928) 774-1895 FAX (928) 773-1135 E-MAIL: khaislet@nacog.org KENNETH J. SWEET EXECUTIVE DIRECTOR Dear Homeowner,

AVOIDING FORECLOSURE

AVOIDING FORECLOSURE Consolidated Credit 5701 West Sunrise Boulevard Fort Lauderdale, FL 33313 1-800-210-3481 www.consolidatedcredit.org Congratulations on taking this important step to a brighter financial

AVOIDING FORECLOSURE Consolidated Credit 5701 West Sunrise Boulevard Fort Lauderdale, FL 33313 1-800-210-3481 www.consolidatedcredit.org Congratulations on taking this important step to a brighter financial

Arizona Agency Foreclosure Training January 28, 2007

Arizona Agency Foreclosure Training January 28, 2007 Presented by: Andrew J. Loubert Community Reinvestment Solutions, Inc. Arizona Foreclosure Process: Notice of Default Notice must specify: 1. The default

Arizona Agency Foreclosure Training January 28, 2007 Presented by: Andrew J. Loubert Community Reinvestment Solutions, Inc. Arizona Foreclosure Process: Notice of Default Notice must specify: 1. The default

LEARN ABOUT YOUR RIGHTS AND OPTIONS IN A FORECLOSURE

Helpful Agencies Here are some agencies which may lead you to lawyers who can help you: Lake County Bar Association 7 North County Street Waukegan, IL 60085 847-244-3140 www.lakebar.org Prairie State Legal

Helpful Agencies Here are some agencies which may lead you to lawyers who can help you: Lake County Bar Association 7 North County Street Waukegan, IL 60085 847-244-3140 www.lakebar.org Prairie State Legal

F.A.C.T. Starter Kit. Foreclosure Avoidance Comprehensive Training. COPYRIGHT 2009 Will Weaver

F.A.C.T. Foreclosure Avoidance Comprehensive Training Starter Kit COPYRIGHT 2009 Will Weaver Foreclosure Prevention Law Public Acts 29 31 of 2009 Requires lenders to send a default notice to borrowers;

F.A.C.T. Foreclosure Avoidance Comprehensive Training Starter Kit COPYRIGHT 2009 Will Weaver Foreclosure Prevention Law Public Acts 29 31 of 2009 Requires lenders to send a default notice to borrowers;

Fax completed package to: 703-580-8842

Fax Cover Sheet/Check List Borrower Name: Please Print Co-Borrowers Name: Please Print Loan Number(s): Owner Occupied n-owner Occupied Required Documentation for Borrower and Co-Borrower If you are a Wage

Fax Cover Sheet/Check List Borrower Name: Please Print Co-Borrowers Name: Please Print Loan Number(s): Owner Occupied n-owner Occupied Required Documentation for Borrower and Co-Borrower If you are a Wage

MPF Xtra PFI Advisory

MPF Xtra PFI Advisory March 14, 2014 Special Attention: PFI MPF Program Management and Servicing Management Subject: Transfer of Servicing, Lender-Placed Insurance, Bankruptcy and Foreclosure Attorney

MPF Xtra PFI Advisory March 14, 2014 Special Attention: PFI MPF Program Management and Servicing Management Subject: Transfer of Servicing, Lender-Placed Insurance, Bankruptcy and Foreclosure Attorney

NON BORROWING SPOUSES AND REVERSE MORTGAGES OVERVIEW

WHAT IS A REVERSE MORTGAGE NON BORROWING SPOUSES AND REVERSE MORTGAGES OVERVIEW The Home Equity Conversion Mortgage Program, i.e. the reverse mortgage, was enacted by Congress in 1987 to meet the special

WHAT IS A REVERSE MORTGAGE NON BORROWING SPOUSES AND REVERSE MORTGAGES OVERVIEW The Home Equity Conversion Mortgage Program, i.e. the reverse mortgage, was enacted by Congress in 1987 to meet the special

What is a Short Sale?

What is a Short Sale? A Short Sale is used to describe the sale of a home in which the homeowner owes the bank more than the home is worth. The bank agrees to allow the home to be sold for less than what

What is a Short Sale? A Short Sale is used to describe the sale of a home in which the homeowner owes the bank more than the home is worth. The bank agrees to allow the home to be sold for less than what

PATHS OF A FORECLOSURE IN NEW YORK STATE

PATHS OF A FORECLOSURE IN NEW YORK STATE BORROWER DELINQUENT 2-3 months late with mortgage payments Lender sends notices, bills, letters to borrower stating that he/she is delinquent Borrower has multiple

PATHS OF A FORECLOSURE IN NEW YORK STATE BORROWER DELINQUENT 2-3 months late with mortgage payments Lender sends notices, bills, letters to borrower stating that he/she is delinquent Borrower has multiple

Supplemental Directive 11-12 December 27, 2011. Making Home Affordable Program Servicing Transfers

Supplemental Directive 11-12 December 27, 2011 Making Home Affordable Program Servicing Transfers In February 2009, the Obama Administration introduced the Making Home Affordable (MHA) Program to stabilize

Supplemental Directive 11-12 December 27, 2011 Making Home Affordable Program Servicing Transfers In February 2009, the Obama Administration introduced the Making Home Affordable (MHA) Program to stabilize

Q. Under what circumstances wil my loan be cal ed due and payable? Q. What happens if one of the above occurs and my loan is cal ed due and payable?

Financial Freedom, as servicer for your Home Equity Conversion Mortgage ( HECM or loan ), is required by the U.S. Department of Housing and Urban Development ( HUD ) to perform certain actions depending

Financial Freedom, as servicer for your Home Equity Conversion Mortgage ( HECM or loan ), is required by the U.S. Department of Housing and Urban Development ( HUD ) to perform certain actions depending

Early Delinquency Intervention: Saving Your Home From Foreclosure

Early Delinquency Intervention: Saving Your Home From Foreclosure There are many circumstances in a homeowner s life that could result in missed mortgage payments: unexpected expenses, loss of overtime,

Early Delinquency Intervention: Saving Your Home From Foreclosure There are many circumstances in a homeowner s life that could result in missed mortgage payments: unexpected expenses, loss of overtime,

LOSS MITIGATION APPLICATION

Loan Number: {1} LOSS MITIGATION APPLICATION COMPLETE ALL PAGES OF THIS FORM See Instructions corresponding with numbers in brackets {} on form BORROWER {3} CO BORROWER {4} Borrower s Name Co Borrower

Loan Number: {1} LOSS MITIGATION APPLICATION COMPLETE ALL PAGES OF THIS FORM See Instructions corresponding with numbers in brackets {} on form BORROWER {3} CO BORROWER {4} Borrower s Name Co Borrower

Reverse Mortgage Is it right for you?

Reverse Mortgage Is it right for you? Reverse Mortgages are being hyped as a tremendous tool for retirement income. This type of mortgage uses part of the equity in a home as collateral. A Reverse Mortgage,

Reverse Mortgage Is it right for you? Reverse Mortgages are being hyped as a tremendous tool for retirement income. This type of mortgage uses part of the equity in a home as collateral. A Reverse Mortgage,

The Cumberland County Residential Mortgage Foreclosure Diversion Program

The Cumberland County Residential Mortgage Foreclosure Diversion Program March 9, 2012 Training Materials THE CUMBERLAND COUNTY RESIDENTIAL MORTGAGE FORECLOSURE DIVERSION PROGRAM 8:30 a.m. Welcome: President

The Cumberland County Residential Mortgage Foreclosure Diversion Program March 9, 2012 Training Materials THE CUMBERLAND COUNTY RESIDENTIAL MORTGAGE FORECLOSURE DIVERSION PROGRAM 8:30 a.m. Welcome: President

STRUGGLING TO MAKE YOUR MORTGAGE PAYMENT PAGE 4

Michigan Lending & Foreclosure Guide Attorney General Bill Schuette TABLE OF CONTENTS PREDATORY MORTGAGE LENDING PAGE 1 PREDATORY LENDING RED FLAGS PAGE 3 STRUGGLING TO MAKE YOUR MORTGAGE PAYMENT PAGE

Michigan Lending & Foreclosure Guide Attorney General Bill Schuette TABLE OF CONTENTS PREDATORY MORTGAGE LENDING PAGE 1 PREDATORY LENDING RED FLAGS PAGE 3 STRUGGLING TO MAKE YOUR MORTGAGE PAYMENT PAGE

The 8 Fastest Ways to STOP FORECLOSURE in 48 Hours or Less

The 8 Fastest Ways to STOP FORECLOSURE in 48 Hours or Less Copyright Notice All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means electronic or mechanical.

The 8 Fastest Ways to STOP FORECLOSURE in 48 Hours or Less Copyright Notice All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means electronic or mechanical.

What to Expect at Foreclosure Prevention Counseling

What to Expect at Foreclosure Prevention Counseling Who should go to foreclosure prevention counseling? Homeowners who are having, or soon may have, problems with their home ownership costs should seek

What to Expect at Foreclosure Prevention Counseling Who should go to foreclosure prevention counseling? Homeowners who are having, or soon may have, problems with their home ownership costs should seek

Home Mortgage Foreclosures in Maine

Home Mortgage Foreclosures in Maine Find more easy-to-read legal information at www.ptla.org Important Note: This is very general information about home mortgage and foreclosure rules in Maine. It is not

Home Mortgage Foreclosures in Maine Find more easy-to-read legal information at www.ptla.org Important Note: This is very general information about home mortgage and foreclosure rules in Maine. It is not

Poll: Domestic Violence in Foreclosure: The Foreclosure Process, Defenses and Alternatives for Survivors. Do you consider yourself: advocate; or

Domestic Violence in Foreclosure: The Foreclosure Process, Defenses and Alternatives for Survivors Karen Merrill Tjapkes Legal Aid of Western Michigan (616) 774-0672 ext. 120 ktjapkes@legalaidwestmich.net

Domestic Violence in Foreclosure: The Foreclosure Process, Defenses and Alternatives for Survivors Karen Merrill Tjapkes Legal Aid of Western Michigan (616) 774-0672 ext. 120 ktjapkes@legalaidwestmich.net

Single Family Claim Status

Single Family Claim Status The Single Family Claim Status function provides information on cases for which a claim for FHA single family mortgage insurance benefits were paid or suspended (i.e., not paid

Single Family Claim Status The Single Family Claim Status function provides information on cases for which a claim for FHA single family mortgage insurance benefits were paid or suspended (i.e., not paid

Mortgage & Home Equity Reporting Guidelines In Response to Current Financial Conditions

Mortgage & Home Equity Reporting Guidelines In Response to Current Financial Conditions General Reporting Guidelines Report accounts in the standard Metro 2 Format. Refer to the Credit Reporting Resource

Mortgage & Home Equity Reporting Guidelines In Response to Current Financial Conditions General Reporting Guidelines Report accounts in the standard Metro 2 Format. Refer to the Credit Reporting Resource

Your Reverse Mortgage Guide. Reaping The Rewards Of A Lifetime Investment In Homeownership

Your Reverse Mortgage Guide Reaping The Rewards Of A Lifetime Investment In Homeownership Contents Make The Most Of Retirement!...3 Program Overview...3 4 What Is A Reverse Mortgage? Why Get A Reverse

Your Reverse Mortgage Guide Reaping The Rewards Of A Lifetime Investment In Homeownership Contents Make The Most Of Retirement!...3 Program Overview...3 4 What Is A Reverse Mortgage? Why Get A Reverse

Keys to Preserving Homeownership through Housing Counseling

Keys to Preserving Homeownership through Housing Counseling NeighborWorks Week 2015: Empowering Neighborhood Leaders! June 6, 2015 St. Luke's Episcopal Church Overview According to a Minneapolis Study

Keys to Preserving Homeownership through Housing Counseling NeighborWorks Week 2015: Empowering Neighborhood Leaders! June 6, 2015 St. Luke's Episcopal Church Overview According to a Minneapolis Study