Insurance Coverage for the Economic Crisis:

|

|

|

- Bernadette Butler

- 8 years ago

- Views:

Transcription

1 Co-Sponsored by: Insurance Coverage for the Economic Crisis: Hedging Your Financial Losses Steve Gilford, Proskauer Rose LLP Marc Rosenthal, Proskauer Rose LLP Jeff Nielsen, Navigant Consulting, Inc. John Failla, Proskauer Rose LLP

2 Topics & Panelists Litigation from Financial Crisis Insurance Coverage for Key Exposures Notice and Renewal Issues Proactive Approach to Policies Steve Gilford Marc Rosenthal Jeff Nielsen John Failla 1

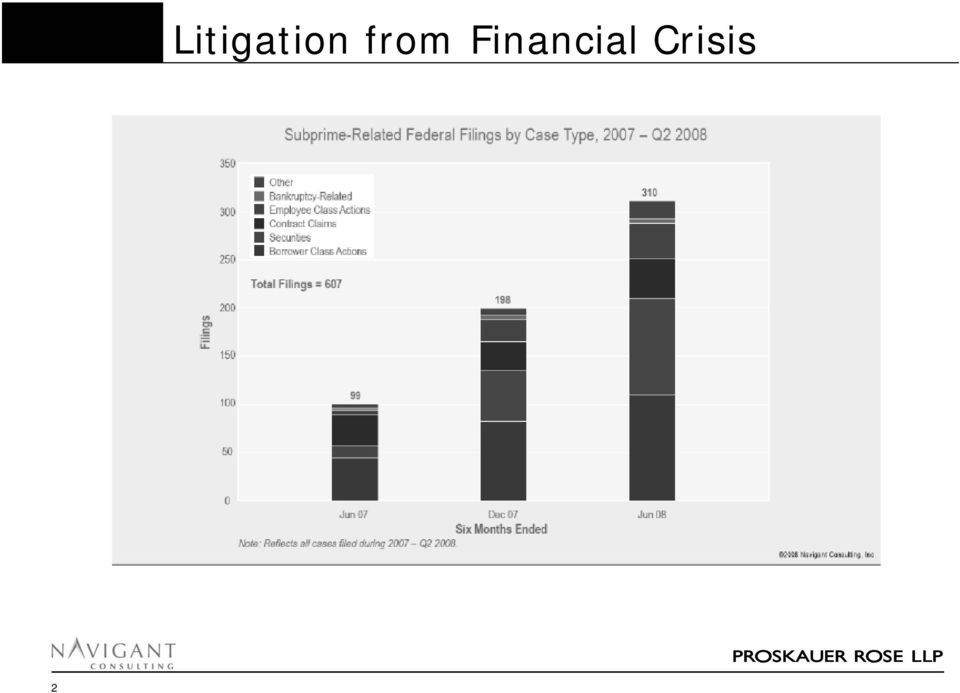

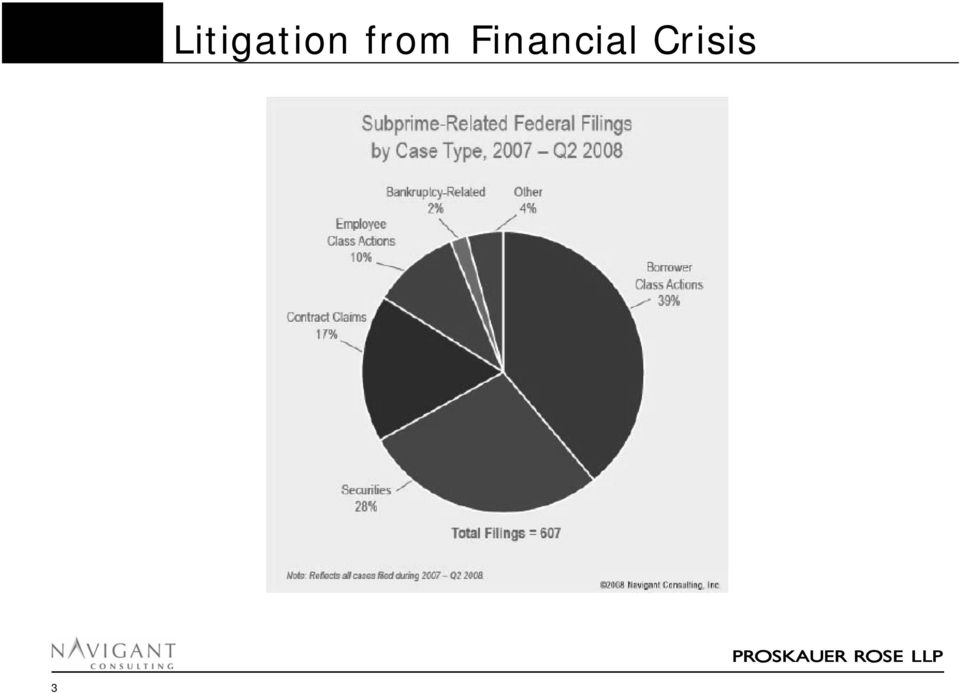

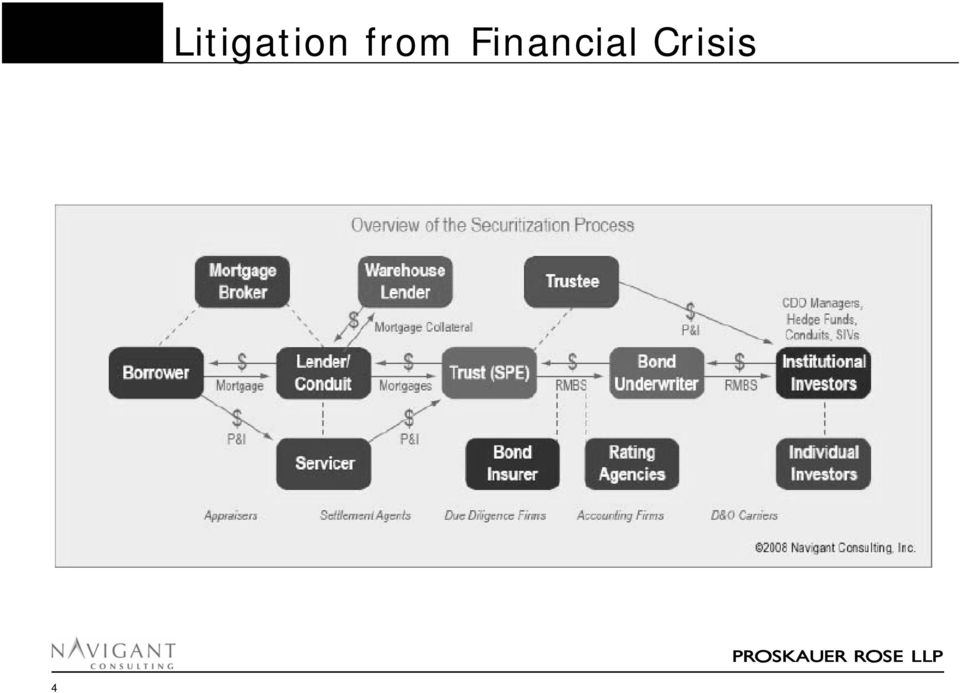

3 2 Litigation from Financial Crisis

4 3 Litigation from Financial Crisis

5 4 Litigation from Financial Crisis

6 Availability of Coverage Many of the exposures inherent in litigation from financial crisis are covered by insurance Historic coverage may be relevant Claims made (D&O/E&O/EPL) vs. occurrence (CGL) vs. discovery (Fidelity/Crime) Need to review carefully and creatively The factual allegations are more important than the captions on the counts or complaints 5

Need to review carefully and creatively The factual")

7 Co-Sponsored by: Category #1: Borrowers Class Actions

8 7 Category #1: Borrowers Class Actions

9 Category #1: Borrowers Class Actions Geneva M. Spicer, et al. v. IndyMac Bank, FSB, et al. U.S. District Court, Central District of California (Case No. CV AHS) Date filed: May 25, 2007 General allegation(s): Alleges IndyMac failed to disclose material information related to option ARMs, concealing that the loan repayment schedule was designed to result in negative amortization Claim(s): TILA, 15 U.S.C.A & 12 C.F.R. 226 California Business & Professions Code California Business & Professions Code Breach of contract Breach of the implied covenant of good faith and fair dealing California Financial Code

10 Category #1: Borrowers Class Actions Time period at issue: June 1, 2003 May 31, 2007 Status: Order granting substitution of FDIC as receiver on August 19, 2008 Stayed until April 13, 2009 Two types of coverage potentially applicable Errors & Omissions ( E&O ) Comprehensive General Liability ( CGL ) 9

Comprehensive General Liability ( CGL")

11 Category #1: Borrowers Class Actions E&O insurance Covers professional negligence of a lender (bankers, mortgage company or broker) Indemnity for claims made during the policy period against the insured for wrongful act in professional capacity Claims made coverage Wrongful acts broadly defined any act, failure to act, error, omission, breach of contract or duty or libel or slander committed or allegedly committed in the insured s professional capacity Generally will not cover ministerial acts Covers intentional acts, but not intentional harm 10

12 Category #1: Borrowers Class Actions Key E&O exclusions Fraud Typically applies only on final adjudication This policy excludes any Claim alleging the fraud or dishonesty of any Insured, if a final judgment or other final adjudication shall establish, or the Insured shall admit in writing, that such fraud or dishonesty was committed Return of fees This Policy excludes claims for return, withdrawal or reduction of fees Difficult issues about what is return of fees and what is damages 11

13 Category #1: Borrowers Class Actions RESPA cases for failure to properly disclose fees Insurer claimed return of fees not covered Court held return of fees was part of compensatory damage arising from insured s breach of fiduciary duty and therefore covered For vs. arising out of Language in exclusion may determine whether negligence or derivative liability claims are excluded 12

14 Category #1: Borrowers Class Actions CGL Occurrence based so may reach back in time Triggered by time of the act Not date of claim or discovery CGL policies are generally limited to coverage for liability due to bodily injury, property damage, personal injury or advertising injury These cases do not involve bodily injury or property damage 13

15 Category #1: Borrowers Class Actions Advertising injury under CGL policy Must be advertising Some cases require injury to a competitor Most modern forms limit coverage to copyright and trademark infringement or misappropriation of advertising idea Some policies are not so limited and may cover liability for falsehoods in advertising Personal injury Some CGL policies, particularly older ones, include coverage for discrimination as part of personal injury 14

16 Category #1: Borrowers Class Actions For example: Personal Injury means injury covered by an offense of: False arrest, false detention or other false imprisonment Malicious prosecution Wrongful entry, wrongful eviction or other violation of a person s right to private occupancy Electronic, oral or written publication of material that libels or slanders a person or violates a person s right of privacy Discrimination, harassment or segregation based on a person s age, color, national origin, race, religion or sex 15

17 Category #1: Borrowers Class Actions Case law is mixed as to whether such references to discrimination extend beyond discrimination based on race, religion, gender, etc., particularly in employment context Majority of cases are limited Some discriminatory lending practice claims include protective class Some cases find coverage for price discrimination or discrimination in home maintenance under Fair Housing Act Courts find that discrimination merely means differential treatment 16

18 Category #1: Borrowers Class Actions Duty to defend Advantage of CGL policy is that it often includes duty to defend E&O may or may not Duty to defend is normally based on allegations of complaint Claim only needs to be potentially covered If duty to defend, it normally extends to whole case even if some claims are not covered Where there is a duty to defend, issuance of reservation of rights creates conflict between insurer and insured Under the circumstances, in most states, insured can pick counsel and control defense at insurer s expense 17

19 Co-Sponsored by: Category #2: Securities (D&O) Claims

20 19 Category #2: Securities (D&O) Claims

21 Category #2: Securities (D&O) Claims New York State Teachers Retirement System, et al. v. New Century Financial Corporation, et al. U.S. District Court, Central District of California (CV DDP) Date filed: February 8, 2007 General allegation(s): Plaintiffs (purchasers of various New Century securities) allege GAAP violations related to loan loss allowances, repurchase reserves, among others, related to the company s whole loan sales and securitizations. Claim(s): 33 Act 11, Act 10(b) & Rule 10b-5, 20(a) Time period at issue: May 5, 2005 March 13, 2007 Status: Motions to dismiss and strike denied on December 3,

22 Category #2: Securities (D&O) Claims Key sources of insurance coverage: Directors & Officers Liability E&O Investment Advisor Professional Liability Directors & Officers liability insurance Protects directors and officers against claims for loss arising from actual or alleged wrongful acts done in their role as directors or officers Public Company D&O often covers Securities Claims against the Company as well as numerous types of claims against the individuals Private Company D&O often covers a wider variety of claims against both the entity and the individuals Not all policies contain Entity coverage 21

23 Category #2: Securities (D&O) Claims Although most D&O policies contain similar general provisions, their language varies greatly and manuscripting and revisions are both possible and very productive Even what appear to be small and technical language changes often pay enormous dividends in obtaining payment D&O exclusions of concern Fraudulent, dishonest, willfully illegal conduct Often requires final adjudication as discussed above Personal profit to which insured is not entitled Critical language distinction in fact vs. final adjudication Professional services or E&O exclusions For or arising out of predicate is key 22

24 Category #2: Securities (D&O) Claims D&O coverage should address most of the securities lawsuits arising from the financial crisis Stock drop cases Alleged misrepresentations about asset quality, exposure to risk Failed deals, financing issues, alleged broken investment promises or commitments Three important points to consider at the outset Quality and extent of coverage for securities claims Investigation, criminal and regulatory coverage Defense coverage and the duty to defend 23

25 Category #2: Securities (D&O) Claims Quality and extent of coverage for securities claims Two common but alternative formulations in D&O policies Coverage only for claims involving securities issued by the insured company Restrictive coverage fine for stock drop cases or claims involving misrepresentations or omissions involving insured company securities Policies with this formulation will exclude coverage for broader securities claim risks Coverage for claims that involve any violations of securities laws or regulations Broken deal, financing, investment cases covered Example: Apollo Hexion Huntsman Litigation 24

26 Category #2: Securities (D&O) Claims Investigation, criminal and regulatory coverage Common misconception that coverage is limited or unavailable Key is to ensure that coverage applies as early in the investigatory process as possible Significant costs often incurred in early stages Common policy provisions contain important nuances Most restrictive Formal administrative, criminal or regulatory proceeding Formal administrative, regulatory, or criminal investigation Can be triggered by subpoena, formal order of investigation, notice of charges, or Wells notice substantial differences Formal or informal regulatory investigations or inquiries Wells notices 25

27 Category #2: Securities (D&O) Claims Defense coverage and the duty to defend Standard provisions are not optimal for policyholders No duty for insurer to assume defense Sometimes no obligation to advance or reimburse costs as incurred Obligation of D&Os to return advanced defense costs if ultimately determined no coverage exists Unfavorable allocation provisions Positive developments for policyholders Language enhancements provide for contemporaneous advancement or reimbursement Neutral allocation language 26

28 Category #2: Securities (D&O) Claims Advancement or reimbursement decided on same standard as duty to defend Based on allegations of complaint No need to wait until case concluded Claim only needs to be potentially covered If duty to defend, it normally extends to whole case even if some claims are not covered Injunctive relief available to compel insurers to advance 27

29 Category #2: Securities (D&O) Claims New York Insurance Department Office of General Counsel Opinion No (October 16, 2008) Unlawful under New York law for D & O insurers to issue policies that impose the duty to defend on policyholders instead of insurers Unlawful to impose allocation provisions that restrict insurers duty to defend the entire case if an allegation potentially triggers coverage for a portion of the case Applies to sophisticated policyholders Positive implications for policy negotiation and claims handling Caution required to ensure control of the defense 28

30 Category #2: Securities (D&O) Claims Investment management liability coverage Mutual fund complex, private funds, private equity, hedge funds, venture capital Auction rate securities, money funds, investor claims challenging disclosure, risk, investment decisions Broad D&O, E&O coverage Key issues involve program structure (combined or separate funds-only coverage) and limits adequacy 29

31 Co-Sponsored by: Category #3: Contract Claims

32 Category 3: Contract Claims MBIA Insurance Corporation v. Countrywide Home Loans, Inc., et al. Supreme Court of the State of New York (Case No ) Date filed: September 30, 2008 General allegation(s): Countrywide breached certain representations and warranties related to home equity loans sold into securitizations for which MBIA provided credit enhancement. Countrywide subsequently refused to repurchase said loans. 31

33 Category 3: Contract Claims MBIA Insurance Corporation v. Countrywide Home Loans, Inc., et al. Supreme Court of the State of New York (Case No ) (cont d) Claim(s): Fraud Negligent misrepresentation Breach of contract insurance agreement Breach of contract sale and servicing agreement Breach of implied duty of good faith & fair dealing Indemnification Time period at issue: Status: Active 32

34 Category 3: Contract Claims E&O coverage Contractual liability exclusion Exclusion often does not apply if the policyholder would face similar liability in the absence of the contract provision e.g., negligent misrepresentation and contract Duty to defend valuable 33

35 Category 3: Contract Claims Fidelity bond or crime coverage Not limited to embezzlement Often broad coverage extensions in endorsements Endorsements covering losses for mortgage securitization or mortgage pooling and other financial instruments Often covers losses due to forgery or alteration Broader coverage where payor signature obtained through trick, fraud or false pretenses or where mortgage note is for any other reason illegal, invalid, non binding or not enforceable in accordance with its terms. Discovery trigger and strict notice, proof of loss and suit limitation clauses 34

36 Co-Sponsored by: Category #4: Employee Action

37 Category 4: Employee Action Michele Viera, et al. v. Accredited Home Lenders Inc. et al. U.S. District Court, Western District of Texas (Case No. A07CA71988) Date filed: 8/24/2007 General allegation(s): Accredited Home Lenders Inc. failed to give at least 60 days advance notice prior to terminating former employees without cause. Subsequently, said employees failed to receive wages and other employee fringe benefits for a 60-day period following their respective terminations. Claim(s): WARN Act 2101 Time period at issue: August 10-22, 2007 Status: Class certified on April 15,

38 Category 4: Employee Action CGL and D&O policies often exclude employment related claims EPL policies Typically claims made, regardless of when conduct or injury took place Covers discrimination, harassment, wrongful termination, wrongful failure to hire or promote and other wrongs arising from the employment context Generally includes a laundry list of offenses Typically includes duty to defend 37

39 Important EPL exclusions ERISA and benefits claims Claim may include wrongful termination as well as mishandling of ERISA benefits plan ERISA claims would be covered by ERISA fiduciary liability policy Fines, penalties and injunctive relief Intentional acts Category 4: Employee Action Claims of discrimination, sexual harassment and wrongful termination are frequently based on intentional acts General rule is that a liability policy covers unintended results of intentional acts Not really an intentional acts exclusion but, rather, an intentional harm exclusion Intent to harm will not necessarily be inferred in discrimination and harassment type claims 38

40 Co-Sponsored by: Category #5: Bankruptcy Claims

41 Category 5: Bankruptcy Claims Mortgage Lenders Network USA, Inc. v. Merrill Lynch Bank USA et al. U.S. Bankruptcy Court, District of Delaware (Case No PJW) Date filed: March 31, 2007 General allegation(s): Merrill Lynch Bank USA received certain preferential and fraudulent transfers prior to the Chapter 11 bankruptcy of Mortgage Lender Network USA related to mortgage collateral securing certain warehouse lines of credit. 40

42 Category 5: Bankruptcy Claims Mortgage Lenders Network USA, Inc. v. Merrill Lynch Bank USA et al. U.S. Bankruptcy Court, District of Delaware (Case No PJW) Claim(s): Uniform Commercial Code 9-625(b) Uniform Commercial Code 9-608(c) & 11 U.S.C. 542 Avoidance of preferential transfers, 11 U.S.C. 547 & 550 Breach of repurchase agreement Avoidance of fraudulent transfers, 11 U.S.C. 548 & 550 Time period at issue: Chapter 11 filed February 5, 2007 Status: Active 41

43 Category 5: Bankruptcy Claims Claims like preferences and fraudulent conveyances are not usually covered Case law generally holds return of moneys not entitled to are not an insurable loss But misrepresentations may be covered Bankruptcy presents an array of issues, especially for creditors Claim by trustee vs D&Os presents issues of who owns the D&O policy The company or the D&Os If the company owns the policy, it may be property of the estate and the automatic bankruptcy stay may preclude D&O access to policy even though claims against D&O continue Seriously complicates order of payment and ability to obtain advances for defense Absent order of payment provision in the policy, normally has to be resolved by agreement or litigation 42

44 Category 5: Bankruptcy Claims Some of these issues may be avoided by purchase of commercially available clauses Side A only coverage 100% allocation to D&Os where company is co-defendant usually for securities claims Order of payments clause Pay D&Os first Next pay company for indemnity paid to D&Os Last pay claims against company 43

45 Co-Sponsored by: Notice and Renewal Issues

46 Notice and Renewal Issues Prompt notice is key Claims made and occurrence policies require prompt notice of a claim May hinge on knowledge of risk manager or general counsel Failure to give notice may preclude coverage even without prejudice to insurers Whether prejudice required varies by state New York s recently enacted Chapter 388 repeals state s no prejudice rule for personal injury or property damage claims under occurrence-based policies, but generally does not impact on coverages discussed today (possible exception of CGL discrimination claims) Notice of circumstances Most claims made policies permit notice of circumstances to tie circumstances which have not yet resulted in a claim to an expiring policy Some claims made policies require such notice 45

47 Notice and Renewal Issues Exclusions typically preclude coverage for claims or circumstances likely to give rise to a claim known before inception of policy Application typically requires disclosure of claims or circumstances likely to give rise to a claim Many applications require warranties of no such claims or circumstances Unless existing claims are likely to exhaust coverage, important to shake the trees to identify and notice all existing claims and circumstances under an expiring policy by appropriate deadline Establishment of paper trail and procedures helps to defend insurer claims of inadequate disclosure and rescission 46

48 Notice and Renewal Issues Interplay of notice of circumstance and renewal application requirements can raise significant issues Notice of circumstances typically requires full particulars Insurers want particulars so can identify what is noticed Insurers may contend notice of circumstance is insufficient without them Renewal application and required warranty may seek broader disclosure of any event which may lead to a claim 47

49 Notice and Renewal Issues Example Bank issued mortgage backed securities, but not sued or threatened with suit Other banks issuing similar instruments were sued Shareholders and employee benefit plans claiming negligence or failure to disclose Do you disclose? As circumstance? At renewal? Insurers will argue insufficient particulars for notice of circumstance on expiring policy If not disclosed, insurers will argue for rescission based on material omission in application leading to rescission May rescind as to all claims Particularly problematic under UK law where arguably required to disclose all material information to underwriters even if not requested 48

50 Notice and Renewal Issues Important to make notice decision early enough to permit insurer response and renewal If give notice of circumstances, easy to give notice on renewal If notice of circumstances is not required, more pressure on renewal disclosure Case-by-case analysis Standard not same (probable/possible/likely) but need to coordinate with those responsible for securities and Sarbanes Oxley compliance 49

51 Co-Sponsored by: Provisions to Seek on Renewal

52 Provisions to Seek on Renewal Important Provisions to Review and Revise Loss definition Contains buried exclusions Must ensure explicit coverage for Section 11 and 12 claims under 1933 Act to avoid disgorgement, ill-gotten gains, uninsurable as a matter of law restrictions Critical importance because many of latest filings in financial crisis cases are state court Section 11 and 12 cases Conduct exclusions Final adjudication Severability Defense provisions 51

53 Provisions to Seek on Renewal Allocation Application and rescission protection Materiality threshold Severability Limits on application materials Claim cooperation, settlement approval, and hammer provisions Exclusions of significance to particular businesses Professional services Libel and defamation Environmental 52

54 Provisions to Seek on Renewal Excess layer issues Follow form Beware of inconsistent provisions and additional exclusions Representation and warranty letters and application severability REFCO example Exhaustion and attachment traps Avoid excess policies that will not pay unless the underlying insurers actually pay their full policy limits Insolvency of underlying insurer or settlement with primary or lower level excess insurer for less than full limits could cause massive program failure Avoid sharing of limits clauses Insist on language that requires excess policy to attach if underlying insurer OR policyholder pays the underlying limits and which has insolvency protection 53

55 Provisions to Seek on Renewal Protecting against insurer insolvency Often unpredictable and rapid Can use ratings downgrade clauses with pro-rata premium return Better to address through program structure Excess program with more layers and diversity of insurers Language, cost and capacity issues Quota share programs Reinsurance cut-through (captive and industry insurer groups) Flex excess policies upper layer resembles umbrella policy and drops down to cover lower insolvent layer DIC coverage to protect individuals against rescission, insolvency, coverage denial, exclusions 54

56 Co-Sponsored by: Questions & Answers Steve Gilford, Proskauer Rose (312) Marc Rosenthal, Proskauer Rose (312) Jeff Nielsen, Navigant Consulting (202) John Failla, Proskauer Rose (212)

Insurance Coverage During the Economic Crisis. by Bianca R. Chapman and Marc Rosenthal

Insurance Coverage During the Economic Crisis by Bianca R. Chapman and Marc Rosenthal The current financial crisis has resulted in unprecedented market volatility, credit concerns, market losses and bankruptcies

Insurance Coverage During the Economic Crisis by Bianca R. Chapman and Marc Rosenthal The current financial crisis has resulted in unprecedented market volatility, credit concerns, market losses and bankruptcies

Covenants to Insure in Commercial Agreements. In House Training Seminar Presented by Satinder K. Sidhu March 8, 2013

Covenants to Insure in Commercial Agreements A Review of the CGL Policy In House Training Seminar Presented by Satinder K. Sidhu March 8, 2013 Introduction & Overview Examples of Covenants to Insure in

Covenants to Insure in Commercial Agreements A Review of the CGL Policy In House Training Seminar Presented by Satinder K. Sidhu March 8, 2013 Introduction & Overview Examples of Covenants to Insure in

Introduction to Directors and Offi cers Liability Insurance

CHAPTER 1 Martin J. O Leary Introduction to Directors and Offi cers Liability Insurance The following is a brief, general overview of coverage afforded under the Directors and Officers Liability Insurance

CHAPTER 1 Martin J. O Leary Introduction to Directors and Offi cers Liability Insurance The following is a brief, general overview of coverage afforded under the Directors and Officers Liability Insurance

THE COMMERCIAL GENERAL LIABILITY POLICY: A Brief Introduction for Clark Wilson LLP Clients

THE COMMERCIAL GENERAL LIABILITY POLICY: A Brief Introduction for Clark Wilson LLP Clients by Nigel Kent Clark Wilson LLP tel. 604.643.3135 npk@cwilson.com www.cwilson.com TABLE OF CONTENTS APPLICABLE

THE COMMERCIAL GENERAL LIABILITY POLICY: A Brief Introduction for Clark Wilson LLP Clients by Nigel Kent Clark Wilson LLP tel. 604.643.3135 npk@cwilson.com www.cwilson.com TABLE OF CONTENTS APPLICABLE

Employment Practices Liability Insurance and Insurance Coverage for Employee Dishonesty

Employment Practices Liability Insurance and Insurance Coverage for Employee Dishonesty Michael Conley, Esq. (267) 216-2707 mconley@andersonkill.com AAPA Port Administration and Legal Issues Seminar Baltimore,

Employment Practices Liability Insurance and Insurance Coverage for Employee Dishonesty Michael Conley, Esq. (267) 216-2707 mconley@andersonkill.com AAPA Port Administration and Legal Issues Seminar Baltimore,

US Youth Soccer Workshop St. Louis, MO March 3, 2007

Directors & Officers Liability Insurance Q&A Session: Enhancements to make this coverage work for you US Youth Soccer Workshop St. Louis, MO March 3, 2007 Presented by: John Spiotta Bollinger, Inc. Tony

Directors & Officers Liability Insurance Q&A Session: Enhancements to make this coverage work for you US Youth Soccer Workshop St. Louis, MO March 3, 2007 Presented by: John Spiotta Bollinger, Inc. Tony

How To Insure An Investment Advisor

SPOTLIGHT ON Insurance and Bonding Considerations for Registered Investment Advisors The contents of this Spotlight have been prepared for informational purposes only, and should not be construed as legal

SPOTLIGHT ON Insurance and Bonding Considerations for Registered Investment Advisors The contents of this Spotlight have been prepared for informational purposes only, and should not be construed as legal

The Solution for General Partnership Liability Coverage Part

The Solution for General Partnership Liability Coverage Part In consideration of the payment of the premium and subject to the General Terms and Conditions, the Insurer and the Insureds agree as follows:

The Solution for General Partnership Liability Coverage Part In consideration of the payment of the premium and subject to the General Terms and Conditions, the Insurer and the Insureds agree as follows:

Management liability - Employment practices liability Policy wording

Special definitions for this section Benefits Claim Defence costs The General terms and conditions and the following terms and conditions all apply to this section. Any compensation awarded to an employee

Special definitions for this section Benefits Claim Defence costs The General terms and conditions and the following terms and conditions all apply to this section. Any compensation awarded to an employee

PUBLIC ENTITY POLICY PUBLIC OFFICIALS LIABILITY COVERAGE FORM CLAIMS MADE COVERAGE

A Stock Insurance Company, herein called the Company PUBLIC ENTITY POLICY PUBLIC OFFICIALS LIABILITY COVERAGE FORM CLAIMS MADE COVERAGE Various provisions in this policy restrict coverage. Please read

A Stock Insurance Company, herein called the Company PUBLIC ENTITY POLICY PUBLIC OFFICIALS LIABILITY COVERAGE FORM CLAIMS MADE COVERAGE Various provisions in this policy restrict coverage. Please read

Insurance to Protect ESOP Trustees

Insurance to Protect ESOP Trustees OEOC 20 th Annual Conference Friday, April 21, 2006 Jeffrey S. Gelburd, CPCU, ARM Two North Second Street, 10th Floor Penn National Plaza Harrisburg, PA 17101 \\USHSBFP01\Groups\dep\Custom

Insurance to Protect ESOP Trustees OEOC 20 th Annual Conference Friday, April 21, 2006 Jeffrey S. Gelburd, CPCU, ARM Two North Second Street, 10th Floor Penn National Plaza Harrisburg, PA 17101 \\USHSBFP01\Groups\dep\Custom

INSTRUCTIONS FOR COMPLETING THIS APPLICATION

MAIN FORM APPLICATION FOR PRIVATE COMPANY DIRECTORS AND OFFICERS AND CORPORATE LIABILITY INCLUDING EMPLOYMENT PRACTICES LIABILITY INSURANCE ( PRIVATE PLUS ) Name of Insurance Company to which this Application

MAIN FORM APPLICATION FOR PRIVATE COMPANY DIRECTORS AND OFFICERS AND CORPORATE LIABILITY INCLUDING EMPLOYMENT PRACTICES LIABILITY INSURANCE ( PRIVATE PLUS ) Name of Insurance Company to which this Application

April 10, 2015 FLANNER HOUSE OF INDIANAPOLIS INC FLANNER HOUSE ELEMENTARY 2424 DR MARTIN LUTHER KING ST INDIANAPOLIS IN 46208

Liberty Mutual Insurance Processing Center PO Box 515097 Los Angeles, CA 90051-5097 April 10, 2015 FLANNER HOUSE OF INDIANAPOLIS INC FLANNER HOUSE ELEMENTARY 2424 DR MARTIN LUTHER KING ST INDIANAPOLIS

Liberty Mutual Insurance Processing Center PO Box 515097 Los Angeles, CA 90051-5097 April 10, 2015 FLANNER HOUSE OF INDIANAPOLIS INC FLANNER HOUSE ELEMENTARY 2424 DR MARTIN LUTHER KING ST INDIANAPOLIS

PUBLIC ENTITY POLICY LAW ENFORCEMENT LIABILITY COVERAGE FORM OCCURRENCE COVERAGE

A Stock Insurance Company, herein called the Company PUBLIC ENTITY POLICY LAW ENFORCEMENT LIABILITY COVERAGE FORM OCCURRENCE COVERAGE Various provisions in this policy restrict coverage. Please read the

A Stock Insurance Company, herein called the Company PUBLIC ENTITY POLICY LAW ENFORCEMENT LIABILITY COVERAGE FORM OCCURRENCE COVERAGE Various provisions in this policy restrict coverage. Please read the

EMPLOYMENT-RELATED PRACTICES LIABILITY ENDORSEMENT

POLICY NUMBER: CL CG 04 57 07 09 THIS ENDORSEMENT CHANGES THE POLICY. PLEASE READ IT CAREFULLY. EMPLOYMENT-RELATED PRACTICES LIABILITY ENDORSEMENT This endorsement modifies insurance provided under the

POLICY NUMBER: CL CG 04 57 07 09 THIS ENDORSEMENT CHANGES THE POLICY. PLEASE READ IT CAREFULLY. EMPLOYMENT-RELATED PRACTICES LIABILITY ENDORSEMENT This endorsement modifies insurance provided under the

EMPLOYEE BENEFITS LIABILITY COVERAGE FORM

EMPLOYEE BENEFITS LIABILITY COVERAGE FORM THIS FORM PROVIDES CLAIMS MADE COVERAGE. PLEASE READ THE ENTIRE FORM CAREFULLY. Various provisions in this policy restrict coverage. Read the entire policy carefully

EMPLOYEE BENEFITS LIABILITY COVERAGE FORM THIS FORM PROVIDES CLAIMS MADE COVERAGE. PLEASE READ THE ENTIRE FORM CAREFULLY. Various provisions in this policy restrict coverage. Read the entire policy carefully

(1) Commercial Crime Insurance or Employee Fidelity Bond

Commercial Crime Insurance or Employee Fidelity Bond") INSURANCE (A) GENERAL CONSIDERATIONS This document presents the minimum insurance requirements as set forth by the United States Trustee Program (USTP). A standing trustee must purchase property insurance

INSURANCE (A) GENERAL CONSIDERATIONS This document presents the minimum insurance requirements as set forth by the United States Trustee Program (USTP). A standing trustee must purchase property insurance

How To Get Out Of A Liability Claim For A Wrongful Act By An Insurance Company

Three Courts Look At Interrelated Wrongful Acts By: Robert S. Fraser and Gavin J. Curley Three cases decided this year in three different jurisdictions focus on the critical coverage determination of whether

Three Courts Look At Interrelated Wrongful Acts By: Robert S. Fraser and Gavin J. Curley Three cases decided this year in three different jurisdictions focus on the critical coverage determination of whether

Directors, Officers and Corporate Liability Insurance Coverage Section. This is a Claims Made Policy. Please read it carefully.

Directors, Officers and Corporate Liability Insurance Coverage Section This is a Claims Made Policy. Please read it carefully. CLAIMS MADE WARNING FOR POLICY NOTICE: THIS POLICY PROVIDES COVERAGE ON A

Directors, Officers and Corporate Liability Insurance Coverage Section This is a Claims Made Policy. Please read it carefully. CLAIMS MADE WARNING FOR POLICY NOTICE: THIS POLICY PROVIDES COVERAGE ON A

2 Summary of California Law (10th), Insurance

, Insurance") 2 Summary of California Law (10th), Insurance I. INTRODUCTION A. Generally. 1. [ 1] In General. 2. [ 2] Commentary and Practice Works. 3. [ 3] Classes of Insurance. 4. [ 4] Insurer's Rights of Subrogation,

2 Summary of California Law (10th), Insurance I. INTRODUCTION A. Generally. 1. [ 1] In General. 2. [ 2] Commentary and Practice Works. 3. [ 3] Classes of Insurance. 4. [ 4] Insurer's Rights of Subrogation,

Sport & Social Clubs and Not For Profit Organisations Directors & Officers Liability Select

Allianz Insurance plc Sport & Social Clubs and Not For Profit Organisations Directors & Officers Liability Select Policy Overview Product Name/Subject Line Professional Indemnity Policy Overview Contents

Allianz Insurance plc Sport & Social Clubs and Not For Profit Organisations Directors & Officers Liability Select Policy Overview Product Name/Subject Line Professional Indemnity Policy Overview Contents

EMPLOYMENT PRACTICES LIABILITY ENDORSEMENT

ENDORSEMENT NO: This endorsement, effective 12:01 am, policy number forms part of issued to: by: THIS ENDORSEMENT CHANGES THE POLICY. PLEASE READ IT CAREFULLY. EMPLOYMENT PRACTICES LIABILITY ENDORSEMENT

ENDORSEMENT NO: This endorsement, effective 12:01 am, policy number forms part of issued to: by: THIS ENDORSEMENT CHANGES THE POLICY. PLEASE READ IT CAREFULLY. EMPLOYMENT PRACTICES LIABILITY ENDORSEMENT

INDIAN HARBOR INSURANCE COMPANY (herein called the Company)

") INDIAN HARBOR INSURANCE COMPANY (herein called the Company) This is a claims made Policy with defense expenses included. Please read and review the Policy carefully. INSURANCE AGENTS AND BROKERS ERRORS

INDIAN HARBOR INSURANCE COMPANY (herein called the Company) This is a claims made Policy with defense expenses included. Please read and review the Policy carefully. INSURANCE AGENTS AND BROKERS ERRORS

Individual Pharmacist Professional Liability Insurance Policy

THIS IS A LEGAL CONTRACT -- PLEASE READ THIS CAREFULLY -- Individual Pharmacist Professional Liability Insurance Policy Table of Contents Page DEFINITIONS... 1 PROFESSIONAL LIABILITY COVERAGE... 3 SUPPLEMENTAL

THIS IS A LEGAL CONTRACT -- PLEASE READ THIS CAREFULLY -- Individual Pharmacist Professional Liability Insurance Policy Table of Contents Page DEFINITIONS... 1 PROFESSIONAL LIABILITY COVERAGE... 3 SUPPLEMENTAL

EMPLOYMENT PRACTICES LIABILITY INSURANCE STANDARD COVERAGE PART CLAIMS FIRST MADE AND REPORTED

COVERAGE PART NUMBER: EMPLOYMENT PRACTICES LIABILITY INSURANCE STANDARD COVERAGE PART CLAIMS FIRST MADE AND REPORTED NOTICE: This Coverage is Provided on a Claims Made and Reported Basis. Except to such

COVERAGE PART NUMBER: EMPLOYMENT PRACTICES LIABILITY INSURANCE STANDARD COVERAGE PART CLAIMS FIRST MADE AND REPORTED NOTICE: This Coverage is Provided on a Claims Made and Reported Basis. Except to such

THIS ENDORSEMENT CHANGES THE POLICY. PLEASE READ IT CAREFULLY PRINTERS ERRORS AND OMISSIONS LIABILITY COVERAGE

THIS ENDORSEMENT CHANGES THE POLICY. PLEASE READ IT CAREFULLY PRINTERS ERRORS AND OMISSIONS LIABILITY COVERAGE This endorsement modifies insurance provided under the following: BUSINESSOWNERS LIABILITY

THIS ENDORSEMENT CHANGES THE POLICY. PLEASE READ IT CAREFULLY PRINTERS ERRORS AND OMISSIONS LIABILITY COVERAGE This endorsement modifies insurance provided under the following: BUSINESSOWNERS LIABILITY

From GCL to E&O, With a Bit of D&O:

From GCL to E&O, With a Bit of D&O: Getting the Most Out of Your Insurance Coverage David R. McDonald, Partner Nossaman Guthner Knox & Elliott LLP 50 California Street, 34 th Floor San Francisco, CA 94111

From GCL to E&O, With a Bit of D&O: Getting the Most Out of Your Insurance Coverage David R. McDonald, Partner Nossaman Guthner Knox & Elliott LLP 50 California Street, 34 th Floor San Francisco, CA 94111

THE MORTGAGE LENDING MELTDOWN: PENDING LITIGATION AND INSURANCE ISSUES

Subprime White Paper For Immediate Release November 26, 2007 CONTACT: Daniel J. Callahan Edward Susolik Callahan & Blaine California s Premier Litigation Firm Tel: (714) 241-4444 E-mail: daniel@callahan-law.com

Subprime White Paper For Immediate Release November 26, 2007 CONTACT: Daniel J. Callahan Edward Susolik Callahan & Blaine California s Premier Litigation Firm Tel: (714) 241-4444 E-mail: daniel@callahan-law.com

NonProfit 101. Notes: Session 1B: Insurance, What you do not know can hurt you! From Survivability to Sustainability. June 10, 2015 Session 1B page 1

Session 1B: Insurance, What you do not know can hurt you! Notes: June 10, 2015 Session 1B page 1 Session 1B: Insurance, What you do not know can hurt you! Notes: June 10, 2015 Session 1B page 2 June 10,

Session 1B: Insurance, What you do not know can hurt you! Notes: June 10, 2015 Session 1B page 1 Session 1B: Insurance, What you do not know can hurt you! Notes: June 10, 2015 Session 1B page 2 June 10,

IN THE COURT OF COMMON PLEAS OF PHILADELPHIA COUNTY FIRST JUDICIAL DISTRICT OF PENNSYLVANIA CIVIL TRIAL DIVISION

IN THE COURT OF COMMON PLEAS OF PHILADELPHIA COUNTY FIRST JUDICIAL DISTRICT OF PENNSYLVANIA CIVIL TRIAL DIVISION COPLEY ASSOCIATES, LTD., DECEMBER TERM, 2005 Plaintiff, NO. 01332 v. COMMERCE PROGRAM ERIE

IN THE COURT OF COMMON PLEAS OF PHILADELPHIA COUNTY FIRST JUDICIAL DISTRICT OF PENNSYLVANIA CIVIL TRIAL DIVISION COPLEY ASSOCIATES, LTD., DECEMBER TERM, 2005 Plaintiff, NO. 01332 v. COMMERCE PROGRAM ERIE

Directors and Officers Liability Insurance in Bankruptcy Settings What Directors and Officers Really Need to Know

Directors and Officers Liability Insurance in Bankruptcy Settings What Directors and Officers Really Need to Know April 30, 2010 By Paul A. Ferrillo While director and officer ( D&O ) liability insurance

Directors and Officers Liability Insurance in Bankruptcy Settings What Directors and Officers Really Need to Know April 30, 2010 By Paul A. Ferrillo While director and officer ( D&O ) liability insurance

THE INVESTMENT INDUSTRY S GUIDE TO INSURANCE COVERAGE AND TERMS

4th Edition THE INVESTMENT INDUSTRY S GUIDE TO INSURANCE COVERAGE AND TERMS A handy, quick-reference source for directors, officers, investment advisors, hedge funds, securities broker/dealers, mutual

4th Edition THE INVESTMENT INDUSTRY S GUIDE TO INSURANCE COVERAGE AND TERMS A handy, quick-reference source for directors, officers, investment advisors, hedge funds, securities broker/dealers, mutual

Are You Covered? Understanding Vendor Endorsements and Harmonizing Risk Transfer Arrangements. Kevin B. Dreher & Jennifer D. Katz Reed Smith LLP

Are You Covered? Understanding Vendor Endorsements and Harmonizing Risk Transfer Arrangements July 14, 2015 Kevin B. Dreher & Jennifer D. Katz Reed Smith LLP Program Overview 1. How to Transfer Risk and

Are You Covered? Understanding Vendor Endorsements and Harmonizing Risk Transfer Arrangements July 14, 2015 Kevin B. Dreher & Jennifer D. Katz Reed Smith LLP Program Overview 1. How to Transfer Risk and

MISCELLANEOUS PROFESSIONAL LIABILITY COVERAGE FORM CLAIMS MADE BASIS

This Form Provides Claims-Made Coverage. Please Read The Entire Form Completely. MISCELLANEOUS PROFESSIONAL LIABILITY COVERAGE FORM CLAIMS MADE BASIS Throughout this document, the word Insured means any

This Form Provides Claims-Made Coverage. Please Read The Entire Form Completely. MISCELLANEOUS PROFESSIONAL LIABILITY COVERAGE FORM CLAIMS MADE BASIS Throughout this document, the word Insured means any

CORNERSTONE A-SIDE MANAGEMENT LIABILITY INSURANCE COVERAGE FORM

CORNERSTONE A-SIDE MANAGEMENT LIABILITY INSURANCE COVERAGE FORM THIS IS A CLAIMS MADE POLICY WITH DEFENSE EXPENSES INCLUDED IN THE LIMIT OF LIABILITY. PLEASE READ AND REVIEW THE POLICY CAREFULLY. In consideration

CORNERSTONE A-SIDE MANAGEMENT LIABILITY INSURANCE COVERAGE FORM THIS IS A CLAIMS MADE POLICY WITH DEFENSE EXPENSES INCLUDED IN THE LIMIT OF LIABILITY. PLEASE READ AND REVIEW THE POLICY CAREFULLY. In consideration

General Liability Insurance

General Liability Insurance Insurance Company: Alberta School Boards Insurance Exchange (ASBIE) Insuring Agreement ASBIE agrees to pay on behalf of the Subscriber all sums that they are legally obligated

General Liability Insurance Insurance Company: Alberta School Boards Insurance Exchange (ASBIE) Insuring Agreement ASBIE agrees to pay on behalf of the Subscriber all sums that they are legally obligated

* Each Will Comply With LR IA 10 2 Within 45 days Attorneys for Plaintiff, Goldman, Sachs & Co.

Case :-cv-00-lrh -WGC Document Filed 0// Page of 0 Stanley W. Parry Esq. Nevada Bar No. Jon T. Pearson, Esq. Nevada Bar No. 0 BALLARD SPAHR LLP 00 North City Parkway, Suite 0 Las Vegas, NV 0 Telephone:

Case :-cv-00-lrh -WGC Document Filed 0// Page of 0 Stanley W. Parry Esq. Nevada Bar No. Jon T. Pearson, Esq. Nevada Bar No. 0 BALLARD SPAHR LLP 00 North City Parkway, Suite 0 Las Vegas, NV 0 Telephone:

INSURANCE OVERVIEW. Presented by The McLaughlin Company

INSURANCE OVERVIEW Presented by The McLaughlin Company Is the Liability Loss Covered? Was policy in effect for responsible party? Does the allegation trigger coverage? Is the entity that is being asked

INSURANCE OVERVIEW Presented by The McLaughlin Company Is the Liability Loss Covered? Was policy in effect for responsible party? Does the allegation trigger coverage? Is the entity that is being asked

D&O and E&O Insurance Claims in the Economic Downturn

presents D&O and E&O Insurance Claims in the Economic Downturn Litigating Claims, Assessing and Renegotiating Current Policies, and Optimizing Future Coverage A Live 90-Minute Audio Conference with Interactive

presents D&O and E&O Insurance Claims in the Economic Downturn Litigating Claims, Assessing and Renegotiating Current Policies, and Optimizing Future Coverage A Live 90-Minute Audio Conference with Interactive

TORUS NATIONAL INSURANCE COMPANY MANAGEMENT LIABILITY APPLICATION FOR PRIVATE COMPANIES (NON-FINANCIAL INSTITUTIONS)

") TORUS NATIONAL INSURANCE COMPANY MANAGEMENT LIABILITY APPLICATION FOR PRIVATE COMPANIES (NON-FINANCIAL INSTITUTIONS) THIS APPLICATION APPLIES TO MANY COVERAGE PARTS. ACCORDINGLY, IT IS ONLY NECESSARY TO

TORUS NATIONAL INSURANCE COMPANY MANAGEMENT LIABILITY APPLICATION FOR PRIVATE COMPANIES (NON-FINANCIAL INSTITUTIONS) THIS APPLICATION APPLIES TO MANY COVERAGE PARTS. ACCORDINGLY, IT IS ONLY NECESSARY TO

CHAPTER 2 APPOINTMENT AND QUALIFICATIONS OF THE STANDING TRUSTEE AND GENERAL REQUIREMENTS

CHAPTER 2 APPOINTMENT AND QUALIFICATIONS OF THE STANDING TRUSTEE AND GENERAL REQUIREMENTS The United States Trustee is authorized by law to appoint one or more individuals to serve as standing trustee

CHAPTER 2 APPOINTMENT AND QUALIFICATIONS OF THE STANDING TRUSTEE AND GENERAL REQUIREMENTS The United States Trustee is authorized by law to appoint one or more individuals to serve as standing trustee

Breakout Session III The Insurance Breakdown: D&O and E&O Delineated Studio E 10:45 am 11:45 am

Breakout Session III The Insurance Breakdown: D&O and E&O Delineated Studio E 10:45 am 11:45 am Thank you to our Alliance Partners Speakers Barry Peters, President Hays Insurance Henry Cifuentes, Vice

Breakout Session III The Insurance Breakdown: D&O and E&O Delineated Studio E 10:45 am 11:45 am Thank you to our Alliance Partners Speakers Barry Peters, President Hays Insurance Henry Cifuentes, Vice

A GUIDE TO PURCHASING LAWYER S PROFESSIONAL LIABILITY INSURANCE IN VIRGINIA

A GUIDE TO PURCHASING LAWYER S PROFESSIONAL LIABILITY INSURANCE IN VIRGINIA Presented By The Virginia State Bar's Special Committee on Lawyer Malpractice Insurance May 2008 The Need For Professional Liability

A GUIDE TO PURCHASING LAWYER S PROFESSIONAL LIABILITY INSURANCE IN VIRGINIA Presented By The Virginia State Bar's Special Committee on Lawyer Malpractice Insurance May 2008 The Need For Professional Liability

How To Protect A Company From Liability

DIRECTORS & OFFICERS ESSENTIAL BUSINESS INSURANCE COVER POLICY RISK FACT introducing FirstUnited FirstUnited is a leading insurance intermediary group operating in Malta and under Freedom of Services throughout

DIRECTORS & OFFICERS ESSENTIAL BUSINESS INSURANCE COVER POLICY RISK FACT introducing FirstUnited FirstUnited is a leading insurance intermediary group operating in Malta and under Freedom of Services throughout

Hudson Insurance Company 100 William Street, New York, NY 10038

Hudson Insurance Company 100 William Street, New York, NY 10038 APPLICATION FOR DIRECTORS & OFFICERS INSURANCE POLICY COMPLETION OF THIS APPLICATION DOES NOT COMMIT OR BIND THE UNDERSIGNED TO PURCHASE

Hudson Insurance Company 100 William Street, New York, NY 10038 APPLICATION FOR DIRECTORS & OFFICERS INSURANCE POLICY COMPLETION OF THIS APPLICATION DOES NOT COMMIT OR BIND THE UNDERSIGNED TO PURCHASE

Our specialist insurance services for Professionals risks

Our specialist insurance services for Professionals risks Price Forbes & Partners is an independent Lloyd s broker based in the heart of London s insurance sector. We trade with all of the major international

Our specialist insurance services for Professionals risks Price Forbes & Partners is an independent Lloyd s broker based in the heart of London s insurance sector. We trade with all of the major international

Specimen THIS IS A CLAIMS-MADE COVERAGE WITH DEFENSE EXPENSES INCLUDED IN THE LIMIT OF LIABILITY. PLEASE READ ALL TERMS CAREFULLY.

MISCELLANEOUS PROFESSIONAL LIABILITY THIS IS A CLAIMS-MADE COVERAGE WITH DEFENSE EXPENSES INCLUDED IN THE LIMIT OF LIABILITY. PLEASE READ ALL TERMS CAREFULLY. I. INSURING AGREEMENTS

MISCELLANEOUS PROFESSIONAL LIABILITY THIS IS A CLAIMS-MADE COVERAGE WITH DEFENSE EXPENSES INCLUDED IN THE LIMIT OF LIABILITY. PLEASE READ ALL TERMS CAREFULLY. I. INSURING AGREEMENTS

Fiduciary Insurance and the Board of Retirement in New York State

ORANGE COUNTY EMPLOYEES RETIREMENT SYSTEM MEMORANDUM DATE: October 7, 2015 TO: FROM: SUBJECT: Members of the Board of Retirement Robert Valer, Chief Legal Officer Fiduciary Insurance Recommendation: Receive

ORANGE COUNTY EMPLOYEES RETIREMENT SYSTEM MEMORANDUM DATE: October 7, 2015 TO: FROM: SUBJECT: Members of the Board of Retirement Robert Valer, Chief Legal Officer Fiduciary Insurance Recommendation: Receive

DIRECTORS & OFFICERS LIABILITY INSURANCE

DIRECTORS & OFFICERS LIABILITY INSURANCE WHAT D&O INSURANCE DOES: Protects the personal assets of a company s directors and officers from potential unlimited liability; Protects the company s assets; Provides

DIRECTORS & OFFICERS LIABILITY INSURANCE WHAT D&O INSURANCE DOES: Protects the personal assets of a company s directors and officers from potential unlimited liability; Protects the company s assets; Provides

MPL SECURE: MISCELLANEOUS PROFESSIONAL AND NETWORK SECURITY LIABILITY INSURANCE POLICY APPLICATION

MPL SECURE: MISCELLANEOUS PROFESSIONAL AND NETWORK SECURITY LIABILITY INSURANCE POLICY APPLICATION NOTICE: THE POLICY FOR WHICH THIS APPLICATION IS MADE IS A CLAIMS MADE AND REPORTED POLICY SUBJECT TO

MPL SECURE: MISCELLANEOUS PROFESSIONAL AND NETWORK SECURITY LIABILITY INSURANCE POLICY APPLICATION NOTICE: THE POLICY FOR WHICH THIS APPLICATION IS MADE IS A CLAIMS MADE AND REPORTED POLICY SUBJECT TO

THIS IS A CLAIMS MADE COVERAGE WITH DEFENSE EXPENSES INCLUDED IN THE LIMIT OF LIABILITY. PLEASE READ ALL TERMS CAREFULLY.

Wrap Miscellaneous Professional Liability SM THIS IS A CLAIMS MADE COVERAGE WITH DEFENSE EXPENSES INCLUDED IN THE LIMIT OF LIABILITY. PLEASE READ ALL TERMS CAREFULLY. I. INSURING AGREEMENTS A. The Company

Wrap Miscellaneous Professional Liability SM THIS IS A CLAIMS MADE COVERAGE WITH DEFENSE EXPENSES INCLUDED IN THE LIMIT OF LIABILITY. PLEASE READ ALL TERMS CAREFULLY. I. INSURING AGREEMENTS A. The Company

Indemnity and Insurance Provisions in Commercial Contracts

Survey Says: The Feud Over Insurance and Indemnity Provisions in Business Contracts Indemnity and Insurance Provisions in Commercial Contracts Kenneth M. Gorenberg Stefan R. Dandelles Indemnity and insurance

Survey Says: The Feud Over Insurance and Indemnity Provisions in Business Contracts Indemnity and Insurance Provisions in Commercial Contracts Kenneth M. Gorenberg Stefan R. Dandelles Indemnity and insurance

Case 3:06-cv-00701-MJR-DGW Document 526 Filed 07/20/15 Page 1 of 8 Page ID #13631 IN THE UNITED STATES DISTRICT COURT SOUTHERN DISTRICT OF ILLINOIS

Case 3:06-cv-00701-MJR-DGW Document 526 Filed 07/20/15 Page 1 of 8 Page ID #13631 IN THE UNITED STATES DISTRICT COURT SOUTHERN DISTRICT OF ILLINOIS ANTHONY ABBOTT, et al., ) ) No: 06-701-MJR-DGW Plaintiffs,

Case 3:06-cv-00701-MJR-DGW Document 526 Filed 07/20/15 Page 1 of 8 Page ID #13631 IN THE UNITED STATES DISTRICT COURT SOUTHERN DISTRICT OF ILLINOIS ANTHONY ABBOTT, et al., ) ) No: 06-701-MJR-DGW Plaintiffs,

CLASSIC A-SIDE MANAGEMENT LIABILITY INSURANCE COVERAGE FORM

CLASSIC A-SIDE MANAGEMENT LIABILITY INSURANCE COVERAGE FORM THIS IS A CLAIMS MADE POLICY WITH DEFENSE EXPENSES INCLUDED IN THE LIMIT OF LIABILITY. PLEASE READ AND REVIEW THE POLICY CAREFULLY. In consideration

CLASSIC A-SIDE MANAGEMENT LIABILITY INSURANCE COVERAGE FORM THIS IS A CLAIMS MADE POLICY WITH DEFENSE EXPENSES INCLUDED IN THE LIMIT OF LIABILITY. PLEASE READ AND REVIEW THE POLICY CAREFULLY. In consideration

"Insurance Services Office, Inc. Copyright"

POLICY NUMBER: COMMERCIAL AUTO CA 25 34 12 05 THIS ENDORSEMENT CHANGES THE POLICY. PLEASE READ IT CAREFULLY. "Insurance Services Office, Inc. Copyright" This form has been promulgated by the Virginia State

POLICY NUMBER: COMMERCIAL AUTO CA 25 34 12 05 THIS ENDORSEMENT CHANGES THE POLICY. PLEASE READ IT CAREFULLY. "Insurance Services Office, Inc. Copyright" This form has been promulgated by the Virginia State

DIRECTORS & OFFICERS LIABILITY INSURANCE

DIRECTORS & OFFICERS LIABILITY INSURANCE INTRODUCTION C or p or ate indemni cation and insurance policies designed to protect D i r e c t o r s a n d c e r s ( D & O s ) a r e complex technical documents.

DIRECTORS & OFFICERS LIABILITY INSURANCE INTRODUCTION C or p or ate indemni cation and insurance policies designed to protect D i r e c t o r s a n d c e r s ( D & O s ) a r e complex technical documents.

Joe A. Ramirez Catherine Crane

RIMS/RMAFP PRESENTATION Joe A. Ramirez Catherine Crane RISK TRANSFER VIA INSURANCE Most Common Method Involves Assessment of Risk and Loss Potential Risk of Loss Transferred For a Premium Insurance Contract

RIMS/RMAFP PRESENTATION Joe A. Ramirez Catherine Crane RISK TRANSFER VIA INSURANCE Most Common Method Involves Assessment of Risk and Loss Potential Risk of Loss Transferred For a Premium Insurance Contract

MISCELLANEOUS PROFESSIONAL LIABILITY INSURANCE COVERAGE FORM

MISCELLANEOUS PROFESSIONAL LIABILITY INSURANCE COVERAGE FORM THIS IS A CLAIMS MADE POLICY WITH DEFENSE EXPENSES INCLUDED IN THE LIMIT OF LIABILITY. PLEASE READ AND REVIEW THE POLICY CAREFULLY. In consideration

MISCELLANEOUS PROFESSIONAL LIABILITY INSURANCE COVERAGE FORM THIS IS A CLAIMS MADE POLICY WITH DEFENSE EXPENSES INCLUDED IN THE LIMIT OF LIABILITY. PLEASE READ AND REVIEW THE POLICY CAREFULLY. In consideration

APPLICATION FOR EMPLOYEE BENEFIT PLAN FIDUCIARY INSURANCE

APPLICATION FOR EMPLOYEE BENEFIT PLAN FIDUCIARY INSURANCE NOTICE: THIS IS AN APPLICATION FOR A CLAIMS MADE AND REPORTED POLICY. THE POLICY FOR WHICH THIS APPLICATION IS MADE IS LIMITED TO LIABILITY FOR

APPLICATION FOR EMPLOYEE BENEFIT PLAN FIDUCIARY INSURANCE NOTICE: THIS IS AN APPLICATION FOR A CLAIMS MADE AND REPORTED POLICY. THE POLICY FOR WHICH THIS APPLICATION IS MADE IS LIMITED TO LIABILITY FOR

Tools Conference Toronto November 26, 2014 Insurance for NFP s. Presented by Paul Spark HUB International HKMB Limited

Tools Conference Toronto November 26, 2014 Insurance for NFP s Presented by Paul Spark HUB International HKMB Limited Topics Insurance Policies Basics Directors and Officers Liability Insurance Commercial

Tools Conference Toronto November 26, 2014 Insurance for NFP s Presented by Paul Spark HUB International HKMB Limited Topics Insurance Policies Basics Directors and Officers Liability Insurance Commercial

D&O FAQ. Report Title. Directors & Officers (D&O) Liability and Insurance Frequently Asked Questions

Liability and Insurance Frequently Asked Questions") D&O FAQ Report Title Directors & Officers (D&O) Liability and Insurance Frequently Asked Questions Contents 1. What is a D&O policy intended to do?...3 2. When does wrongful conduct have to occur to be

D&O FAQ Report Title Directors & Officers (D&O) Liability and Insurance Frequently Asked Questions Contents 1. What is a D&O policy intended to do?...3 2. When does wrongful conduct have to occur to be

Questions Every Outside Director Should Ask About Their Portfolio Company s D&O Insurance

By Pamela W. Mason, AAI Questions Every Outside Director Should Ask About Their Portfolio Company s D&O Insurance Venture capital and private equity partners are being sued in their capacity as directors

By Pamela W. Mason, AAI Questions Every Outside Director Should Ask About Their Portfolio Company s D&O Insurance Venture capital and private equity partners are being sued in their capacity as directors

APPLICATION FOR ACCOUNTANTS PROFESSIONAL LIABILITY INSURANCE

Executive Risk Indemnity Inc. Home Office Wilmington, Delaware 19805-1297 Administrative Offices/Mailing Address: 82 Hopmeadow Street Simsbury, Connecticut 06070-7683 APPLICATION FOR ACCOUNTANTS PROFESSIONAL

Executive Risk Indemnity Inc. Home Office Wilmington, Delaware 19805-1297 Administrative Offices/Mailing Address: 82 Hopmeadow Street Simsbury, Connecticut 06070-7683 APPLICATION FOR ACCOUNTANTS PROFESSIONAL

THIRD PARTY ADMINISTRATOR AGREEMENT. (Hereinafter, Agreement ) Between

Between") THIRD PARTY ADMINISTRATOR AGREEMENT (Hereinafter, Agreement ) Between Those underwriting members of Lloyd s, and those other insurers (if any), individually and severally subscribing to the Contract(s)

THIRD PARTY ADMINISTRATOR AGREEMENT (Hereinafter, Agreement ) Between Those underwriting members of Lloyd s, and those other insurers (if any), individually and severally subscribing to the Contract(s)

LAWYERS PROFESSIONAL LIABILITY INSURANCE APPLICATION

LAWYERS PROFESSIONAL LIABILITY INSURANCE APPLICATION ProAssurance Casualty Company PO Box 150 Okemos, MI 48805-0150 800.292.1036 517.349.6500 Fax 517.347.6321 NOTICE: This professional liability coverage

LAWYERS PROFESSIONAL LIABILITY INSURANCE APPLICATION ProAssurance Casualty Company PO Box 150 Okemos, MI 48805-0150 800.292.1036 517.349.6500 Fax 517.347.6321 NOTICE: This professional liability coverage

Chapter 13: Repayment of All or Part of the Debts of an Individual with Regular Income ($235 filing fee, $39 administrative fee: Total fee $274)

") B 201A (Form 201A) (12/09) WARNING: Effective December 1, 2009, the 15-day deadline to file schedules and certain other documents under Bankruptcy Rule 1007(c) is shortened to 14 days. For further information,

B 201A (Form 201A) (12/09) WARNING: Effective December 1, 2009, the 15-day deadline to file schedules and certain other documents under Bankruptcy Rule 1007(c) is shortened to 14 days. For further information,

MINIMIZING EXPOSURE: CORPORATE FORMALITIES AND INSURANCE COVERAGE by Sheldon Mak Rose & Anderson

MINIMIZING EXPOSURE: CORPORATE FORMALITIES AND INSURANCE COVERAGE by Sheldon Mak Rose & Anderson INTRODUCTIONa, Americans like to sue. Businesses get tangled in costly litigation, often not by choice.

MINIMIZING EXPOSURE: CORPORATE FORMALITIES AND INSURANCE COVERAGE by Sheldon Mak Rose & Anderson INTRODUCTIONa, Americans like to sue. Businesses get tangled in costly litigation, often not by choice.

In an ever changing business and social environment it has become increasingly

DIRECTORS AND OFFICERS INSURANCE ISSUES By: National Business Institute June 20, 2008 Howard L. Lieber FISHER KANARIS, P.C. 200 South Wacker Drive 22nd Floor Chicago, Illinois 60606 312/474-1400 In an

DIRECTORS AND OFFICERS INSURANCE ISSUES By: National Business Institute June 20, 2008 Howard L. Lieber FISHER KANARIS, P.C. 200 South Wacker Drive 22nd Floor Chicago, Illinois 60606 312/474-1400 In an

Be In The Know About D&O and E&O

Be In The Know About D&O and E&O February 3, 2009 2:00 pm 3:30 pm (Eastern) Sponsored by ASAE Services, Inc. and ASAE-endorsed partners Aon Association Services and Media/Professional Presenters: Eric

Be In The Know About D&O and E&O February 3, 2009 2:00 pm 3:30 pm (Eastern) Sponsored by ASAE Services, Inc. and ASAE-endorsed partners Aon Association Services and Media/Professional Presenters: Eric

Insurance basics for nonprofit organizations

Insurance basics for nonprofit organizations Updated: July 2012 This document is intended as general and abbreviated guidance for nonprofit organizations. Because every organization s insurance needs are

Insurance basics for nonprofit organizations Updated: July 2012 This document is intended as general and abbreviated guidance for nonprofit organizations. Because every organization s insurance needs are

Residents Associations Directors & Officers Liability Select. Policy Overview

Allianz Insurance plc Residents Associations Directors & Officers Liability Select Policy Overview Product Name/Subject Line Professional Indemnity Policy Overview Contents Introduction 1 Significant Features

Allianz Insurance plc Residents Associations Directors & Officers Liability Select Policy Overview Product Name/Subject Line Professional Indemnity Policy Overview Contents Introduction 1 Significant Features

BANKRUPTCY INFORMATION SHEET

BANKRUPTCY INFORMATION SHEET BANKRUPTCY LAW IS A FEDERAL LAW. THIS SHEET GIVES YOU SOME GENERAL INFORMATION ABOUT WHAT HAPPENS IN A BANKRUPTCY CASE. THE INFORMATIONHERE IS NOT COMPLETE. YOU MAY NEED LEGAL

BANKRUPTCY INFORMATION SHEET BANKRUPTCY LAW IS A FEDERAL LAW. THIS SHEET GIVES YOU SOME GENERAL INFORMATION ABOUT WHAT HAPPENS IN A BANKRUPTCY CASE. THE INFORMATIONHERE IS NOT COMPLETE. YOU MAY NEED LEGAL

DIRECTORS & OFFICERS LIABILITY INSURANCE

DIRECTORS & OFFICERS LIABILITY INSURANCE Top 10 Negotiating Strategies December 9, 2008 Beverly B. Godbey Gardere Wynne Sewell LLP 1601 Elm Street, Ste. 3000 Dallas, TX 75201 214-999-4855 Phone 214-999-3855

DIRECTORS & OFFICERS LIABILITY INSURANCE Top 10 Negotiating Strategies December 9, 2008 Beverly B. Godbey Gardere Wynne Sewell LLP 1601 Elm Street, Ste. 3000 Dallas, TX 75201 214-999-4855 Phone 214-999-3855

BEAZLEY ARMOUR SIDE A DIRECTORS AND OFFICERS LIABILITY INSURANCE POLICY

BEAZLEY ARMOUR SIDE A DIRECTORS AND OFFICERS LIABILITY INSURANCE POLICY In consideration of the payment of the premium, in reliance on all statements made in the application and subject to all of the provisions

BEAZLEY ARMOUR SIDE A DIRECTORS AND OFFICERS LIABILITY INSURANCE POLICY In consideration of the payment of the premium, in reliance on all statements made in the application and subject to all of the provisions

Insurance Coverage In Consumer Class Actions

This article first appeared in the October 2010 issue of The Corporate Counselor. Insurance Coverage In Consumer Class Actions John W. McGuinness and Justin F. Lavella The business world is an increasingly

This article first appeared in the October 2010 issue of The Corporate Counselor. Insurance Coverage In Consumer Class Actions John W. McGuinness and Justin F. Lavella The business world is an increasingly

INTERNATIONAL INSURANCE SERVICES AND RISK MANAGEMENT

INTERNATIONAL INSURANCE SERVICES AND RISK MANAGEMENT Directors & Officers Liability D&O Insurance Service is our passion CONTENTS Legal framework of statutory and supervisory board members liability in

INTERNATIONAL INSURANCE SERVICES AND RISK MANAGEMENT Directors & Officers Liability D&O Insurance Service is our passion CONTENTS Legal framework of statutory and supervisory board members liability in

Management liability - Directors and officers liability Policy wording

Special definitions for this section Bail costs Claim Defence costs The General terms and conditions and the following terms and conditions all apply to this section. Costs incurred with our prior written

Special definitions for this section Bail costs Claim Defence costs The General terms and conditions and the following terms and conditions all apply to this section. Costs incurred with our prior written

LAWYERS PROFESSIONAL LIABILITY NEW BUSINESS APPLICATION

ASPEN AMERICAN INSURANCE COMPANY LAWYERS PROFESSIONAL LIABILITY NEW BUSINESS APPLICATION NOTICE: This is an application for a claims-made and reported policy. Coverage for prior acts and claims made after

ASPEN AMERICAN INSURANCE COMPANY LAWYERS PROFESSIONAL LIABILITY NEW BUSINESS APPLICATION NOTICE: This is an application for a claims-made and reported policy. Coverage for prior acts and claims made after

SPECIMEN. (1) a written demand for monetary damages or non-monetary relief;

a written demand for monetary damages or non-monetary relief;") In consideration of payment of the premium and subject to the Declarations, General Terms and Conditions, limitations, conditions, provisions and other terms of this Policy, the Company and the Insureds

In consideration of payment of the premium and subject to the Declarations, General Terms and Conditions, limitations, conditions, provisions and other terms of this Policy, the Company and the Insureds

B.C. LAWYERS COMPULSORY PROFESSIONAL LIABILITY INSURANCE POLICY NUMBER: LPL 00-01-01

B.C. LAWYERS COMPULSORY PROFESSIONAL LIABILITY INSURANCE POLICY NUMBER: LPL 00-01-01 INSURER: THE LSBC CAPTIVE INSURANCE COMPANY LTD. (the Company ) Administrative Offices, 6th Floor, 845 Cambie Street

B.C. LAWYERS COMPULSORY PROFESSIONAL LIABILITY INSURANCE POLICY NUMBER: LPL 00-01-01 INSURER: THE LSBC CAPTIVE INSURANCE COMPANY LTD. (the Company ) Administrative Offices, 6th Floor, 845 Cambie Street

Fiduciary Liability Insurance for the Credit Crisis

Looking for Coverage By John W. Egan and Michael C. Cannata Fiduciary Liability Insurance for the Credit Crisis Insurance implications for the financial services industry of recent ERISA class actions

Looking for Coverage By John W. Egan and Michael C. Cannata Fiduciary Liability Insurance for the Credit Crisis Insurance implications for the financial services industry of recent ERISA class actions

Access to Information X X X X X. Acquisition X X X X X X X X. Acquisition or sale of business X X X X X X X. Adjudication of Grievances X X X

Access to Information Acquisition Acquisition or sale of business Adjudication of Grievances Administration of Collective Agreements Administrative Law Advertising Liability Agent/Broker Liability Agreements

Access to Information Acquisition Acquisition or sale of business Adjudication of Grievances Administration of Collective Agreements Administrative Law Advertising Liability Agent/Broker Liability Agreements

How To Recover From A Financial Loss

Portfolio Media, Inc. 648 Broadway, Suite 200 New York, NY 10012 www.law360.com Phone: +1 212 537 6331 Fax: +1 212 537 6371 customerservice@portfoliomedia.com Insurance Companies On Offense Law360, New

Portfolio Media, Inc. 648 Broadway, Suite 200 New York, NY 10012 www.law360.com Phone: +1 212 537 6331 Fax: +1 212 537 6371 customerservice@portfoliomedia.com Insurance Companies On Offense Law360, New

INSURANCE AGENTS AND BROKERS PROFESSIONAL LIABILITY POLICY

A Stock Insurance Company, herein called the Company INSURANCE AGENTS AND BROKERS PROFESSIONAL LIABILITY POLICY THIS POLICY APPLIES ONLY TO CLAIMS FIRST MADE AGAINST THE INSURED DURING THE POLICY PERIOD

A Stock Insurance Company, herein called the Company INSURANCE AGENTS AND BROKERS PROFESSIONAL LIABILITY POLICY THIS POLICY APPLIES ONLY TO CLAIMS FIRST MADE AGAINST THE INSURED DURING THE POLICY PERIOD

How To Cover A Claim For A Claim On A Life Insurance Policy

Directors and Officers Liability Insurance Quick reference guide The Quick Reference Guide provides a snapshot of the changes that have been made in comparison to the previous Directors and Officers Liability

Directors and Officers Liability Insurance Quick reference guide The Quick Reference Guide provides a snapshot of the changes that have been made in comparison to the previous Directors and Officers Liability

INITIAL REQUIRED NOTICES FOR BANKRUPTCY CLIENTS

INITIAL REQUIRED NOTICES FOR BANKRUPTCY CLIENTS You are hereby requesting the opportunity to consult with and obtain information and advice from Michael Jones and the Law Office of James P. Cronn ( Law

INITIAL REQUIRED NOTICES FOR BANKRUPTCY CLIENTS You are hereby requesting the opportunity to consult with and obtain information and advice from Michael Jones and the Law Office of James P. Cronn ( Law

What are the main liability policies you should consider for your commercial business?

A PUBLICATION BY: GODFREY MORROW GODFREY INSURANCE MORROW AND INSURANCE FINANCIAL AND SERVICES FINANCIAL LTD. SERVICES LTD. 2012 What are the main liability policies you should consider for your commercial

A PUBLICATION BY: GODFREY MORROW GODFREY INSURANCE MORROW AND INSURANCE FINANCIAL AND SERVICES FINANCIAL LTD. SERVICES LTD. 2012 What are the main liability policies you should consider for your commercial

Directors & Officers Liability Select

Allianz Insurance plc Directors & Officers Liability Select Policy Overview Product Name/Subject Line Professional Indemnity Policy Overview Contents Introduction 1 Significant Features and Benefits 2

Allianz Insurance plc Directors & Officers Liability Select Policy Overview Product Name/Subject Line Professional Indemnity Policy Overview Contents Introduction 1 Significant Features and Benefits 2

Understanding Your DesignOne Coverage:

Understanding Your DesignOne Coverage: Commercial General Liability Insurance An educational resource from CNA and Schinnerer CGL insurance is an important coverage for any business. Understanding this

Understanding Your DesignOne Coverage: Commercial General Liability Insurance An educational resource from CNA and Schinnerer CGL insurance is an important coverage for any business. Understanding this

AFB TECHNOLOGY SERVICES, TECHNOLOGY PRODUCTS AND PROFESSIONAL LIABILITY INSURANCE POLICY

Multimedia and Broadcaster s Professional Liability Insurance Application AFB TECHNOLOGY SERVICES, TECHNOLOGY PRODUCTS AND PROFESSIONAL LIABILITY INSURANCE POLICY NOTICE: COVERAGE IS PROVIDED ON AN OCCURRENCE

Multimedia and Broadcaster s Professional Liability Insurance Application AFB TECHNOLOGY SERVICES, TECHNOLOGY PRODUCTS AND PROFESSIONAL LIABILITY INSURANCE POLICY NOTICE: COVERAGE IS PROVIDED ON AN OCCURRENCE

Insurance 101. Presented by. The McLaughlin Company

Insurance 101 He that scatters thorns, let him not go barefoot -Benjamin Franklin Presented by The McLaughlin Company 1725 DeSales Street, N. W. Suite 900 Washington, D. C. 20036 (202) 293-5566 (800) 233-2258

Insurance 101 He that scatters thorns, let him not go barefoot -Benjamin Franklin Presented by The McLaughlin Company 1725 DeSales Street, N. W. Suite 900 Washington, D. C. 20036 (202) 293-5566 (800) 233-2258

EDUCATORS LEGAL LIABILITY COVERAGE PART DECLARATIONS (Claims Made Form)

") EDUCATORS LEGAL LIABILITY COVERAGE PART DECLARATIONS (Claims Made Form) Policy No. NAMED INSURED: ITEM 1: POLICY PERIOD: POLICY COVERS FROM: TO: 12:01 A.M. standard time at your mailing address shown above.

EDUCATORS LEGAL LIABILITY COVERAGE PART DECLARATIONS (Claims Made Form) Policy No. NAMED INSURED: ITEM 1: POLICY PERIOD: POLICY COVERS FROM: TO: 12:01 A.M. standard time at your mailing address shown above.

PERSONAL AND ADVERTISING INJURY COVERAGE FOR PROFESSIONAL ATHLETES, SPORTS LEAGUES AND ASSOCIATIONS

PERSONAL AND ADVERTISING INJURY COVERAGE FOR PROFESSIONAL ATHLETES, SPORTS LEAGUES AND ASSOCIATIONS By Michelle Worrall Tilton UIA - 55 th Congress, Miami, FL November 2, 2011 Liability Insurance Terms

PERSONAL AND ADVERTISING INJURY COVERAGE FOR PROFESSIONAL ATHLETES, SPORTS LEAGUES AND ASSOCIATIONS By Michelle Worrall Tilton UIA - 55 th Congress, Miami, FL November 2, 2011 Liability Insurance Terms

NAVIGATORS INSURANCE COMPANY

NAVIGATORS INSURANCE COMPANY APPLICATION FOR LAWYERS' PROFESSIONAL LIABILITY INSURANCE THIS APPLICATION IS FOR A CLAIMS MADE AND REPORTED POLICY (must complete in ink) 1. Name of Applicant (type or print)

NAVIGATORS INSURANCE COMPANY APPLICATION FOR LAWYERS' PROFESSIONAL LIABILITY INSURANCE THIS APPLICATION IS FOR A CLAIMS MADE AND REPORTED POLICY (must complete in ink) 1. Name of Applicant (type or print)

UNITED STATES BANKRUPTCY COURT WESTERN DISTRICT OF MICHIGAN. NOTICE TO CONSUMER DEBTOR(S) UNDER 342(b) OF THE BANKRUPTCY CODE

UNDER 342(b) OF THE BANKRUPTCY CODE") B 201A (Form 201A) (11/11) UNITED STATES BANKRUPTCY COURT WESTERN DISTRICT OF MICHIGAN NOTICE TO CONSUMER DEBTOR(S) UNDER 342(b) OF THE BANKRUPTCY CODE In accordance with 342(b) of the Bankruptcy Code,

B 201A (Form 201A) (11/11) UNITED STATES BANKRUPTCY COURT WESTERN DISTRICT OF MICHIGAN NOTICE TO CONSUMER DEBTOR(S) UNDER 342(b) OF THE BANKRUPTCY CODE In accordance with 342(b) of the Bankruptcy Code,

DISCHARGE. The Discharge in Bankruptcy. From an individual. debtor s standpoint, one. of the primary goals of. filing a bankruptcy case

The Discharge in Bankruptcy DISCHARGE The bankruptcy discharge varies depending on the type of case a debtor files: chapter 7, 11, 12, or 13. This Public Information Series pamphlet attempts to answer

The Discharge in Bankruptcy DISCHARGE The bankruptcy discharge varies depending on the type of case a debtor files: chapter 7, 11, 12, or 13. This Public Information Series pamphlet attempts to answer

How To Pay A Policy On Insurance For A Car Accident

Law Firm Employment Practices Insurance Claims First Made and Reported NOTICE: This Coverage is Provided on a Claims Made and Reported Basis. Except to such extent as may otherwise be provided herein,

Law Firm Employment Practices Insurance Claims First Made and Reported NOTICE: This Coverage is Provided on a Claims Made and Reported Basis. Except to such extent as may otherwise be provided herein,

D&O Liability Insurance: Persistent Problems & Simple Solutions

D&O Liability Insurance: Persistent Problems & Simple Solutions Scott C. Hecht Stinson Morrison Hecker LLP presented to Association of Corporate Counsel Mid-America Chapter Thursday, January 13, 2011 D&O

D&O Liability Insurance: Persistent Problems & Simple Solutions Scott C. Hecht Stinson Morrison Hecker LLP presented to Association of Corporate Counsel Mid-America Chapter Thursday, January 13, 2011 D&O

Notice Required by 11 U.S.C. 342(b) and 527(a)

and 527(a)") 1 P a g e Notice Required by 11 U.S.C. 342(b) and 527(a) In accordance with section 342(b) of the Bankruptcy Code, this notice: (1) Describes briefly the services available from credit counseling services;

1 P a g e Notice Required by 11 U.S.C. 342(b) and 527(a) In accordance with section 342(b) of the Bankruptcy Code, this notice: (1) Describes briefly the services available from credit counseling services;

LAWYERS PROFESSIONAL LIABILITY INSURANCE APPLICATION

DARWIN NATIONAL ASSURANCE COMPANY 1690 New Britain Avenue, Suite 101, Farmington, CT 06032 Tel. (860) 284-1300 Fax (860) 284-1301 LAWYERS PROFESSIONAL LIABILITY INSURANCE APPLICATION NOTICE: THE POLICY

DARWIN NATIONAL ASSURANCE COMPANY 1690 New Britain Avenue, Suite 101, Farmington, CT 06032 Tel. (860) 284-1300 Fax (860) 284-1301 LAWYERS PROFESSIONAL LIABILITY INSURANCE APPLICATION NOTICE: THE POLICY