Documenting, Closing and Servicing SBA 504 and 7(a) Loans

|

|

|

- Todd Terry

- 8 years ago

- Views:

Transcription

1 Documenting, Closing and Servicing SBA 504 and 7(a) Loans William C. Brown Heather E. Ward Engel, Hairston & Johanson, P.C. Engel, Hairston & Johanson, P.C. 109 N. 20 th Street, 4 th Floor 109 N. 20 th Street, 4 th Floor Birmingham, Alabama Birmingham, Alabama (205) (205) cbrown@ehjlaw.com hward@ehjlaw.com 1

")

2 TABLE OF CONTENTS: Page I. SBA Loans...4 A. Lending Programs The 504 Loan The 7(a) Loan...6 II. SBA Loan Approval...7 A. Borrower Eligibility...8 B. Franchise Eligibility...11 C. Credit Analysis...13 D. Use of Proceeds...13 E. Equity Injection...15 F. The Loan Application Contents of the Loan Application Specific Application Forms...19 III. Closing...21 A. Lender s Responsibility (7(a) Loans)...22 B. CDC s Responsibility (504 Loans)...23 C. Borrower s Responsibility...23 D. Issues, Fees and Forms Fees...24 a. The SBA 7(a) Guarantee Fee...24 b. The Ongoing SBA 7(a) Servicing Fee...25 c. Fees Associated with 504 Loans Disbursements Repayment Verification of Use of Proceeds Collateral/Lien Position Guaranties IRS Tax Transcripts Environmental Investigation Insurance Standby Agreements...31

Servicing Fee...25 c. Fees Associated with 504 Loans...25 2. Disbursements...26 3. Repayment...26 4. Verification of Use of Proceeds...27 5. Collateral/Lien Position...28 6.")

3 IV. Servicing...32 A. Necessity of Lender Compliance...33 B. Servicing and Liquidation Action Lender Documentation & Reporting...34 a Reports...34 b. Site Visit Reports...35 c. Transcript of Account Monitoring Creditworthiness Servicing & Liquidation Approval Liquidation & Litigation Plans...38 V. Pitfalls...40 A. Expiration after Maturity Issue...40 B. Lien and Collateral Issues...40 C. Unauthorized Use of Proceeds Issues...41 D. Liquidation Deficiency Issues...41 E. Undocumented Servicing Actions Issues...41 F. Early Default Issues...42 LIST OF EXHIBITS A. SBA Form 1919 (Borrower Information Form 7(a) Loan)...43 B. SBA Form 912 (Statement of Personal History)...50 C. SBA Form 413 (Personal Financial Statement)...53 D. SBA Form 159 (Compensation Agreement 7(a) Loan)...59 E. IRS Form 4506-T (Request for IRS Tax Transcripts)...63 F. SBA Form 147 (Note in 7(a) Loan)...66 G. SBA Form 1505 (Note in 504 Loan)...72 H. SBA Form 148 (Unconditional Guarantee)...78 I. SBA Form 2287 (Third Party Lender Agreement in 504 Loan)...84 J. SBA Form 2288 (Interim Lender Certification in 504 Loan)...82 K. SBA Form 1050 (Settlement Sheet in 7(a) Loan)...96 L. SBA Form 722 (EEO Poster and Notice)...98 M. SBA Form 1502 (Field Descriptions for Lender Reporting in 7(a) Loan) N. SBA Servicing and Liquidation 7(a) Lender Matrix

Loan)...43 B. SBA Form 912 (Statement of Personal History)...50 C. SBA Form 413 (Personal Financial Statement)...53 D.")

4 I. SBA Loans The Small Business Administration (SBA) is a federal agency that was created to assist small businesses and protect the interests of small business concerns in order to preserve free competitive enterprise and strengthen the overall economy. 1 Specifically, SBA strives to help start, build, and grow businesses in order to create jobs and stimulate the economy. SBA is governed by the Small Business Act of 1953, which is codified in 15 U.S.C Under this Act, SBA is empowered to deliver loans, guarantee loans made by lenders, assist with government contracts, counsel small businesses, offer entrepreneur development services, and provide other types of assistance for small businesses. 2 Among these functions, SBA is able to make loans 3 and guarantee private lender loans to qualified small business concerns. Regulations for SBA s loan programs are found in Part 120 of Title 13 in the Code of Federal Regulations (C.F.R.). SBA lending assistance provides benefits to borrowers by making funds available and assisting with long-term financing. These transactions result in, among other things, improved cash flow, fixed maturity, and no balloon payments. Whether under the 7(a) or 504 Loan Programs, borrowers can be eligible for up to $5 million in SBA-backed financing U.S.C Id.; see U.S. Small Business Administration, About SBA: What We Do, 3 Although authorized to make direct non-disaster business loans, SBA has not been funded to do so since the mid 1990s.

5 A. Lending Programs SBA currently has three main lending programs: the 7(a) loan program, the 504 loan program and the disaster loan program. 1. The 504 Loan The 504 loan program is typically used for long-term financing to attain major assets for business development and expansion. 13 C.F.R Instead of guaranteeing the loan of a private lender, the SBA uses a Certified Development Company (CDC) as a lender partner to actually finance the loan secured by a 100 percent SBA-guaranteed debenture. A CDC is nonprofit corporation set up to encourage economic development of its community. Of the projected costs for the venture, a private non-cdc lender provides 50% of the financing with senior lien position; the CDC contributes up to 40% of the financing backed by a 100% SBA-guaranteed debenture with junior lien position; and the borrower is expected to provide at least 10% of the financing. Id.; see also 13 C.F.R The SBA 504 Loan is typically used for acquisition of land, or acquisition of land and existing buildings, construction of improvements, major renovations to existing structures, or purchases of capital equipment or heaving machinery. SBA participates alongside third party lenders in making these loans by funding debentures with terms of either ten (10) or twenty (20) years depending upon the useful life of the assets being financed at fixed interest rates over the life of the SBA loan. These loans benefit borrowers because of the long-term fixed rates and typically lower equity requirements. 5

6 2. The 7(a) Loan These loans are made wholly by the lender who submits application to SBA for approval of the SBA guarantee against lender s deficiency in the event of default. Under the 7(a) Loan Program SBA will guarantee up to 85% for loans up to $150,000 and up to 75% for loans exceeding that amount up to $5,000, SBA will collect a guaranty fee on the guaranteed portion of the loan, which is charged to lenders but can be collected from borrowers. 5 The funds of this fee are designed to reimburse lenders for borrowers who default on repayment. Through SBA s 7(a) eligible use of proceeds requirement, financing can be guaranteed for a variety of business purposes, such as working capital, inventory, machinery and equipment, leasehold improvements, land and building (for purchase, renovation or new construction), and debt refinancing. 6 The loan maturity will depend on the nature of the loan and the borrower s ability to repay. Typically, it is up to 10 years for working capital & equipment and may be up to 25 years for fixed assets, such as real estate. 7 SBA requires the lender to collateralize the loan to the maximum extent possible up to the loan amount, which may include 4 15 U.S.C. 636(a)(2)-(3) 5 15 U.S.C. 636(a)(18) 6 15 U.S.C. 636(a); 13 C.F.R U.S.C. 636(a)(5); 13 C.F.R

7 personal assets if business assets do not fully secure the loan. 8 The lender must verify that the borrower has invested a certain amount of equity into the business to ensure the borrower is committed and indebted to the business. 9 II. SBA Loan Approval To qualify, the borrower must be a for-profit business, meet SBA size requirements, show good character, credit, management, and ability to repay, and must be an eligible type of business. 10 The key factors for eligibility are based on what the business does to receive its income, the character of its ownership and where the business operates. In general, the businesses must meet the following criteria to be eligible for SBA assistance: be a business operating for-profit; be located, engaged, or propose to do business in the United States; qualify as a small business under SBA size requirements; be able to demonstrate the need for the loan proceeds; have reasonable invested equity; attempt to use alternative financial resources before seeking financial assistance from SBA; have a plan to use the funds for a sound business purpose; and not be delinquent on any existing debt obligation to the United States. 11 Additionally, there must be no apparent conflict of interest between the borrower and the lender. 8 U.S. Small Business Administration, 7(a) Loan Program Terms and Conditions, C.F.R C.F.R C.F.R

8 A. Borrower Eligibility As mentioned above, one of the eligibility requirements is that the borrower must be a small business concern. SBA determines a small business concern to be a business that has a net after-tax operating income, averaged over a two-year period, of less than $5 million and a net worth of less than $15 million. Additionally, the lender may use size standard defined under the North American Industry Classification System (NAICS). 12 The Small Business Act defines a small business as a business that is owned and operated and not dominant in its field of operation. 13 The size standards vary from industry to industry and are developed considering the economic characteristics comprising the structure of an average firm size, start-up costs, entry barriers, and distribution of firms by size. 14 Additional considerations include technological changes, competition from other industries, growth trends, historical activity within an industry, unique factors occurring in the industry which may distinguish small firms from other firms, and objectives of the business programs and the impact on those programs of different size standard levels. 15 Certain businesses are automatically ineligible to receive a SBA loan. The following businesses are ineligible: Non-profit businesses (a for-profit subsidiary will be eligible); C.F.R ; The codes can be found at North American Industry Classification System, Introduction to NAICS, U.S.C C.F.R Id.

9 Financial businesses primarily engaged in the business of lending (such as banks and finance companies); Passive businesses owned by developers and landlords that do not actively use or occupy the assets acquired or improved with loan proceeds (other than eligible passive companies defined in 13 C.F.R ); Life insurance companies; Businesses located in a foreign country (a U.S. business owned by aliens may qualify); Pyramid sale distribution plans; Businesses deriving more than one-third (1/3) of gross annual revenue (not income) from legal gambling activities; Businesses that are involved in any illegal activity; Private businesses that limit the number of memberships for reasons other than capacity; Government-owned entities; Businesses principally engaged in teaching, instructing, counseling or indoctrinating religious beliefs; Consumer and marketing cooperatives (producer cooperatives are eligible); Loan packagers earning more than 1/3 of their gross annual revenue from packaging SBA loans; Businesses with an associate who is in jail, on probation, on parole, or has been indicted for a felony or a crime of moral turpitude. o SBA cannot provide assistance to associates who are presently subject to an 9

10 indictment, criminal information, arraignment, or other means by which formal criminal charges are brought in any jurisdiction (F) Pg o If a subject reveals that he/she is currently on parole or probation under question 9 on a 912, the business is ineligible (F) Pg o Electronic fingerprint submissions are permitted as a substitute for an FD- 258 Fingerprint Card where available (F) Pg o If a small business applicant is owned by a trust, the trustor must be of good character and is required to provide a Form (D) Pg Businesses where the lender, CDC, or any of its associates own an equity interest; Businesses which present live performances of a prurient sexual nature or derive, directly or indirectly, more than de minimis gross revenue through the sale of products, services, or presentation of a prurient sexual nature (revised SOP 50 (10)(F) has eliminated the community standards language); Businesses that have previously defaulted on any federal loan or federally assisted financing (unless waived by SBA for good cause): o The definition of federal debt does not include unpaid/delinquent taxes or loss incurred by the FDIC when it sells a loan at a discount [ (D) Pg. 290] or loans purchased, held or securitized by Fannie Mae or Freddie Mac [ (F) Pg. 264]. o The prior loss/delinquent federal debt rules apply to Associates (as opposed to principals of the small business applicant) and guarantors (D) Pg Associate includes an office, director, owner or more than 20%, key 3

Pg. 284.")

11 employee, business owned or controlled (at least 20%) by any of the foregoing, or individual, or entity that controls or is controlled by the small business. Businesses engaged primarily in political or lobbying activities; and/or Speculative businesses (such as oil wildcatting per SBA s example). 16 B. Franchise Eligibility SBA must review proposed franchise/license/jobber or other similar agreements to determine if the business is eligible on the basis of whether the small business applicant constitutes an affiliate of the franchise. A finding that the agreement is acceptable means that the agreement does not impose unacceptable control provision on the applicant which would result in affiliation. SBA may determine affiliation can exist between the applicant and franchisor through common ownership, common management, excessive restrictions on the sale/transfer of the franchise interest, or excess control of the franchisor over the applicant s business operations. SBA has compiled a list of eligibility issue for franchises, called the Franchise Findings, to determine common requirements found in franchise agreements that would cause the business to be ineligible. 17 The lender is responsible for ensuring the franchise meets the eligibility requirements in accordance with SBA policies in effect at the time the application was filed. To facilitate this review C.F.R SOP (5)(F), Subpart B, Chapter 1.9.a, et seq. 11

12 SBA makes available a list of franchise agreements (the Registry ) that have been approved for size/affiliation/control issues at 18 In General, the CDC and/or SBA Lender must consider: i. When there is a franchise/jobber agreement, the agreement must be executed prior to submission of the closing package to SBA for funding (rather than prior to first disbursement) (D) Pg ii. The fact that a jobber agreement is acceptable does not mean that the small business is eligible. The CDC must still review for other eligibility issues under the SOP (F) Pg iii. Review of a franchise agreement is conducted by SBA for all loans processed through the SLPC (rather than all regular and ALP loans) (F) Pg iv. When the franchise is on the franchise registry, the CDC s file must contain the following: (i) executed franchise agreement and any approved attachments or exhibits, (ii) executed addendum (if required), (iii) executed certification of franchise documents, and (iv) compliance with any required eligibility notes (D) Pg v. When a franchise is not on the registry or when the CDC chooses not to use the registry, CDCs should consult with the Franchise Findings List to determine if there have been any findings that would result in a determination of affiliation and whether there are any fixes 18 Id.

Pg. 243. iii.")

13 available (F) Pg vi. Procedures are set forth for a franchise to appeal the decision not to be placed on the registry (F) Pg C. Credit Analysis In order to qualify for an SBA loan, a borrower must be creditworthy, contribute a small portion of the equity, and provide reasonable assurance of repayment. Lenders are required to assess the applicant s credit factors to determine that the borrower is able to reasonably assure repayment. The most important factor in assuring repayment is the cash flow of the business, not the liquidation of collateral. 19 A lender must review the following to adequately evaluate the borrower s creditworthiness: character, reputation, and credit history; experience and depth of management; strength of business; past earnings, projected cash flow, and future prospects; ability to repay the loan with earnings from the business; sufficient invested equity to operate on a sound financial basis; potential for long-term success; nature and value of collateral; and any affiliates effect on the applicant s repayment ability. 20 D. Use of Proceeds Borrowers may use SBA Loan proceeds for a variety of sound business purposes, including starting a new business or assisting in the operating, acquisition, or expansion 19 SOP (5)(F), Subpart B, Chapter 1.III C.F.R

14 of an existing business. The following are the specific uses that the borrower may use loan proceeds for: Use of Proceeds 7(a) Loans vs. 504 Loans Acquire land and/or Yes Yes purchase, construct or renovate buildings Improve a site (e.g. Yes Yes grading, streets, parking, landscaping), up to 5% for community improvements Acquire and install fixed Yes Yes assets such a capital equipment or heavy machinery Purchase Inventory Yes Cannot be used for inventory financing Supplies Yes No; unless to finance items such as furniture, fixtures and other equipment that are essential to and directly related to the construction project Raw Materials Yes No Working Capital Yes No; except if amount less than 2% of gross debenture as a part of new construction including contingencies (SOP 50 (10) (F) Subpart C. pg. 280) Refinancing Yes; subject to SBA policies regarding debt refinancing (SOP 50 (10)(F) pgs. 114 ff. ) Yes when refinancing in connection with an expansion; or short term bridge financing for Business Acquisition Yes; subject to SBA policies regarding change of ownership and business valuations 13 CFR (SOP 50 (10)(F) pgs. 120 ff.) acquisition of vacant land Only if demonstrates that job would be lost if not for change of ownership and only costs associated with fixed assets. All other costs (i.e. inventory, goodwill, other

, up to 5% for community improvements Acquire and install fixed Yes Yes assets such a capital equipment or heavy machinery Purchase Inventory Yes Cannot")

15 intangibles) must be financed in some other manner, including a 7(a)( Loan (SOP 50 (10)(F) pg. 282) Borrowers are prohibited from using proceeds for certain items. If loan proceeds are used for the following purposes: Effecting a partial change of business ownership or a change that will not benefit the business; Permitting the payments, distributions or loans to be paid to associates of the applicant (except for ordinary compensation for services rendered); Investing in real or personal property acquired and held primarily for sale, lease, or investment; Refinancing existing debt when the lender is in a position to sustain a loss, and SBA would take over the loss by refinancing; Repaying delinquent state or federal withholding taxes or any other funds that should be held in trust or escrow; and/or Paying for a non-sound business purpose. 21 E. Equity Injection Lenders are required to verify the borrower s equity injection before disbursing loan proceeds. The lender should maintain evidence of this verification in their loan files. Lenders must use every reasonable and prudent effort to verify that equity is injected and C.F.R

16 will be used in accordance with its intended purpose. 22 If there is a cash injection, verification should include documentation such as a copy of a check along with evidence that the check was processed. 23 For example, the lender could show one bank account statement dated before the disbursement showing that the funds were available and deposited into the borrower s account. Also, the lender could use a copy of an escrow settlement, as well as a bank statement showing the injection of equity into the business prior to disbursement. Generally, a promissory note or financial statement is not sufficient evidence of cash injection. If the equity injection is funded by assets, the lender has a duty to carefully determine the value of non-cash assets. 24 Additionally, the lender must determine if the equity injection is material to the borrower s operation. For this purpose, material means any equity injection that is greater than 1/3 of the amount of the loan or $200,000. If the cash equity injection is material, the lender must verify the existence of the injection, as described above, in addition to the source of the cash equity injection. The purpose of verifying the source of the injection is to ensure that the funds will be used for the intended business purpose. Specifically, the lender must present evidence demonstrating that the borrower did not use the proceeds of the loan to fund the equity injection C.F.R ; SOP (2)(B), Chapter 13, Paragraph Id. 24 SOP 5010 (5)(F) Chapter 4 (I)(F)(3) 25 SOP (2)(B), Chapter 13, Paragraph 24

17 F. The Loan Application 26 SBA requires an application for a business loan to contain certain forms and documentation for approval of the guaranty application. The information contained within the loan application package should give SBA a clear understanding of the purpose for the financing request, the amount of financing requested, the subject matter to be financed, the business repayment ability, the basis for repayment, and the nature of the business. A primary consideration of the SBA is repayment ability from business cash flow. Other factors to be considered include the ability and experience of the management team, the collateral offered as security, the financial strength of personal guarantees, the ability of the owner to contribute equity, and the strength of historical financial ratios. 1. Contents of the Loan Application Package The loan application package should include any of the following items applicable to the particular facts of the financing request: a. A description of the business, which may include the following: i) Synopsis of company and background; ii) Summary of industry and industry background; iii) Summary of business operational aspects; iv) Detailed description of physical facilities, office and plant locations, size and equipment; v) Product, employee, and marketplace reports; vi) Service information, sales method, and territories; 26 See SOP (5)(F) Subpart B, Chapter 6 17

18 vii) List of major customers; viii) Number of employees; ix) Whether union or non-union; x) Current potential in terms of production, employee numbers and expansion plans; and xi) References from suppliers and trade organization. xii) Industry analysis b. Description of competition. c. Purpose for credit request; d. Amount of credit requested; and e. Proposal for credit repayment. f. Comprehensive and well organized financial records including: i) Current interim financial statements (dated within 120 days); ii) Financial statements for the past 3 fiscal years; iii) Tax returns for the past three fiscal years; iv) Aging of receivables and payables (including supplier and customer terms); and v) Personal financial statement(s) (current within 90 days). g. Cash flow projections for the next 2 years (minimum) with the first year itemized on monthly basis; and h. Summary of assumptions for cash flow projections. i. Appraisal of collateral. j. Type of organization; and k. Date of business inception. l. Breakdown of business ownership (including): i) Listing of officers and percent ownership; ii) Listing of directors and percent ownership; and

19 iii) Listing of members / managers and percent ownership. m. Resumes of management and owners; n. Corporate or organizational documents; o. Organizational chart; and p. Other outstanding financing including leases. 2. Specific Application Forms SBA requires specially designed application forms which are available upon request from any CDC or by contacting the SBA directly. All SBA forms are also available on the web in PDF format at In general, the application must contain the following SBA forms: 7(a) Loans vs. 504 Loans SBA Form , the Borrower Information Form SBA Form 1244 Part A, Checklist of Application Exhibits SBA Form 1920, Lender Application Form SBA Form 1244 Part B, Application for 504 Loan Lender s Credit Memo SBA Form 1244 Part C, Statements Required by Law and Executive Order Documents required Based on Condition of the Loan SBA Form 912, Statement of Personal History (required for all principals, officers, directors and owners of 20% or more of the borrower); SBA Form 1244 Part D, Third Party Lender Certification for Debt Refinancing SBA Form 912, Statement of Personal History (required for all principals, officers, directors and owners of 20% or more of the borrower); 27 SBA Information Notice issued February 7, 2014 announced the release of the updated Forms 1919 and 1920, which consolidated processing methods to one set of forms. Form 1919 replaces the former the former SBA 7(a) Eligibility Questionnaire, while 1920 replaces the former Forms 4 Application for Loan and Form 4-I. 19

Loans vs.")

20 Personal Financial Statement, dated within 90 days of submission to SBA, with all owners of 20% or more and any proposed guarantors (lenders may use their own form or SBA Form 413); SBA Form 159, Fee Disclosure and Compensation Agreement (must be completed for each agent compensated by the borrower or lender); Copy of IRS Form 4506-T, Request for Copy of Tax Return; SBA National 7(a) Authorization Boilerplate language must be complete; and if applicable: Personal Financial Statement, dated within 90 days of submission to SBA, with all owners of 20% or more and any proposed guarantors (lenders may use their own form or SBA Form 413); SBA Form 159, Fee Disclosure and Compensation Agreement (must be completed for each agent compensated by the borrower or lender); Copy of IRS Form 4506-T, Request for Copy of Tax Return; SBA National 504 Authorization Boilerplate, draft complete as applicable for specific transaction The following information may be required in order to complete the SBA forms for loan application listed above: Business Financial Statements dated within 90 days of submission (must consist of year-end balance sheets for the last 3 years, year-end profit and loss statements for the least three years, reconciliation of net worth, interim balance sheet, interim profit and loss statements, affiliate and subsidiary financial statement requirements, and cash flow projection); Description of the business, list of principals, and the copy of the lease if applicable; Detailed list of all machinery and equipment to be purchased with loan proceeds and cost quotes; Equity Injection Form explaining type and source of applicant s equity injection;

21 If real property is to be purchased with loan, need appraisal, lender s environmental questionnaire, cost breakdown, and copy of purchase agreement; If an existing business is being purchased, need a copy of buy-sell agreement, copy of business valuation, pro forma balance sheet for the business being purchased as of the date of the transfer, copy of seller s financial statements for the last three complete fiscal years or for the number of years in business if less than three years, interim statements no older than 90 days, and an alternate source of verifying revenue if seller s financial statements are not available; or If business is a franchise, SBA requires a determination as to whether affiliation exists. In all cases the franchise agreement and any addendums must be executed prior to the first disbursement. To facilitate this review SBA makes a list of franchise agreements available (the Registry at ). In order to rely on the Registry for its determination, the lender s loan file must include the executed franchise agreement (and any addendums), the Executed Certification of Franchise Documents (available on the Registry website) and compliance with any eligibility notes. 28 III. Closing The lender must comply with the Authorization, which lists the required conditions which must be met for closing. A lender is expected to be able to carry out the necessary actions to meet the conditions in the Authorization, including: C.F.R ; see also SOP (5)(F) Subpart B, Chapter 1.III.9.d 21

22 A. Lender s Responsibility (7(a) Loans): 1. Close the Loan in accordance with terms and conditions of the Authorization; 2. Obtain valid and enforceable Loan documents, including obtaining the signatures or written consent of any persons (e.g. spouses of obligors) necessary to bind and create and valid lien on community or marital property; 3. Retain all Loan closing documents, for audit as well as submitted to SBA for request to honor guarantee. B. CDC s Responsibility (504 Loans): 1. Close Loan in accordance with the Authorization 2. Obtain valid and enforceable loan documents and all required lien positions, along with the written consent of any persons (e.g. obligor s spouses) necessary to create a valid lien position on community or marital property; 3. Obtain all necessary certifications; 4. Obtain a legal opinion from CDC counsel or borrower s counsel if there is one; 5. Certify to SBA that there has been no substantial unremedied adverse change in the Borrower s financial condition, organization, operation, or assets (as set forth in CDC Certification, Form 2101);

23 6. Certify that all elements of Project Costs have been paid in full and that the Interim Lender, Third Party Lender, Borrower and CDC have each contributed to the Project in the amount and manner authorized by SBA; 7. Properly complete all closing documents using SBA Required Forms; 8. Submit Form 2286 and the 504 Debenture Closing Checklist and copies of required documents to SBA for review and approval prior to debenture sale deadlines C. Borrower s Responsibility 1. Comply with all conditions reasonably imposed by Lender or CDC, in addition to those of the Authorization; 2. Cooperate with Lender or CDC in closing the Loan and obtaining necessary certifications and documentation; 3. Execute all documents required by SBA; 4. Submit all documents required by CDC or Lender counsel sufficiently in advance of loan closing; 5. Certify that all elements of Project Costs have been paid in full and how they were paid; 6. Certify that any bankruptcy or insolvency proceeding involving, or pending lawsuit against, Borrower, Operating Company or any of their principals as been disclosed in writing to Lender or CDC. 23

24 D. Issues, Fees and Forms A part of the responsibility of the parties to the transaction, as outlined above, is to obtain and use SBA required forms in closing the transaction. In addition to outlining terms and conditions for the SBA loan, the Authorization lists which SBA forms should be used. Specific forms typically listed in the SBA Authorization are as follows: 7(a) Loans SBA Form 147 Note SBA Form 1050 Settlement Sheet SBA Form 159 7(a) Compensation Agreement SBA Form 148, Guarantee SBA Form 148L, Limited Guarantee, when required SBA Form 601, Agreement of Compliance, when required SBA Form 722, Equal Opportunity Poster SBA Form 1624, Certificate of Debarment SBA Loan Agreement Borrower and Operating Company Certifications IRS Form W Loans SBA Form 1505 Note SBA Form 1504 Debenture SBA Form 159 (504) Compensation Agreement SBA Form 148, Guarantee SBA Form 148L, Limited Guarantee, when required SBA Form 2101, CDC Certification SBA Form 722, Equal Opportunity Poster SBA Form 1506, Servicing Agent Agreement SBA Form 1528, CDC Board Resolution SBA Form 2286, 504 Debenture Closing Checklist SBA Form 2287, Third Party Lender Agreement SBA Form 2288, Interim Lender Certification SBA Form 2289, Borrower and Operating Company Certification Opinion of CDC Counsel IRS Form W-9 1. Fees. a. The SBA 7(a) Guarantee Fee. To counteract the costs of the 7(a) loan program, SBA charges the lender a guaranty fee and a servicing fee for each 7(a) loan. The guarantee fee is a one-time charge that the lender is obligated to pay SBA. If the loan has a maturity of less than twelve months, the guaranty fee must be submitted with the application, and the fee will

25 be 0.25 percent of the guaranteed portion of the loan. For loans with a maturity greater than one year, the guaranty fee can be anywhere between 2 percent to 3.75 percent depending on the amount of the guaranteed portion of the loan, and the fee must be paid within 90 days of the loan s approval. 29 The lender can charge this fee to the borrower once SBA gives a loan approval. If the lender does not pay the guaranty fee in a timely manner, SBA can terminate the guaranty. 30 b. The SBA 7(a) Ongoing Servicing Fee. Unlike the one-time charge for the guaranty fee, the servicing fee is an ongoing charge paid annually. This fee will be a percent of the outstanding balance of the guaranteed portion of the loan. The servicing fee will remain in effect for the life of the loan. Contrary to the guaranty fee, the lender may not charge the borrower for this fee. 31 c. Fees Associated with SBA 504 Loans. Some of the fees that a Borrower may be charged at the time of closing and are specifically associated with a 504 Loan are outlined below (13 CFR ; 13 CFR ; SOP 50 10(5)(F), Subpart C, Chapter 8, I.). Processing Fee (13 CFR (a)) Closing Fee (13 CFR (a)) Up to 1.5% of Net Debenture Up to $2,500 Paid by Borrower to CDC, financed as part of Gross Debenture Fee that CDC may charge for its expenses associated with closing and costs of counsel; limited to a maximum of $2,500 that may be U.S.C. 636(a)(18); 13 C.F.R (a)-(b) C.F.R (e) C.F.R (f) 25

26 Underwriter s Fee (13 CFR (c)) Underwriter s Fee (13 CFR (c)) SBA Guaranty Fee (13 CFR (d)) Funding Fee (13 CFR (d)) Participation Fee (Third Party Lender Fee) (13 CFR ) 0.4% at closing for 20-year Debentures 0.375% at closing for 10-year Debentures 0.5% of Net Debenture collected at closing 0.25% of Net Debenture collected at closing 0.50% of the amount of the mortgage held in senior lien position One-time fee financed into the Debenture proceeds Paid by Borrower to CDC, financed as part of Gross Debenture Paid by Borrower to CDC, financed as part of Gross Debenture Paid by Borrower to CDC, financed as part of Gross Debenture Paid by Borrower to CDC, financed as part of Gross Debenture Fee from Third Party Lender to CDC; fee may be paid by Borrower, CDC or Third Party Lender 2. Disbursements. As far as disbursing the loan, the lender can establish its own disbursement schedule, but all proceeds must be disbursed within 48 months after the date of the approval. 32 Also, the lender has the option of calculating the loan maturity date from either the date of the note or the date of the initial disbursement. However, a lender must abide by the maximum maturity dates, which are 25 years for real estate and up to 10 years for equipment, machinery, and inventory loans Repayment. When using the SBA Note (Form 147) to document for documenting a SBA 7(a) Loan, the repayment terms must contain the exact boilerplate language for the 32 SOP (5)(F), Subpart B, Chapter 7.IV.A U.S.C. 636(a)(5); 13 C.F.R

27 conditions in the Authorization. 34 The lender has no option to enter its own specific language for the repayment terms, without approval from SBA. Generally, 7(a) term loans are repaid on a monthly basis with principal and interest from the loan. For any variations that occur between agreed upon repayment terms and the language of the Authorization, lender must request SBA modify the SBA Authorization to conform. For variable rate loans, the lender can require different payment amounts as the interest increases; whereas, a fixed-rate loan will require the same payment throughout the life of the loan because the interest rate is constant. If the maturity is less than 15 years, the lender may not charge the borrower if the loan is paid off before maturity. The lender must be sure that it abides by these conditions when structuring the terms of the loan. 4. Verification of Use of Proceeds Lenders are responsible for verifying that loan proceeds are being used in accordance with its authorized purpose. SBA Form 1050 Settlement Sheet requires lenders to document disbursement of loan proceeds through the issuance of joint payee checks. If the lender does not use joint payee checks to evidence use of loan proceeds, the lender should provide copies of paid receipts, paid invoices or other supporting documentation clearly showing that the proceeds were used in accordance with the loan 34 U.S. Small Business Administration, 7(a) Loan Repayment Terms, 27

28 authorization. Prudent lending standards mandate that the lender take reasonable measures to verify the use of loan proceeds Collateral/Lien Position The lender must obtain proper lien position on collateral. The lender should collateralize the loan to the maximum extent possible. If business assets do not fully secure the loan, the lender should take/require available personal assets to be used as collateral. Typically, the lender should create a list of significant collateral securing the loan. The list of collateral should be kept with a UCC financing statement to ensure that the lender will be able to establish priority of its secured position on the specified collateral. 36 Additionally, the collateral list with the UCC financing statement will greatly assist the process in the event of default and consequent liquidation of the collateral. 6. Guaranties The lender must obtain at least one individual or corporate guaranty for each loan. If there is any entity that owns at least 20% of the borrower entity, this entity must provide an unlimited full guaranty. If an individual owns 20% or more of the borrower entity, the lender must obtain an unlimited full personal guaranty from this individual. Additionally, the spouse of the personal guarantor must sign a guaranty on any interest that he or she has in the collateral. In order to determine the assets available to support 35 SOP B, Chapter 13, Paragraph SOP B, Chapter 13, Paragraph 27

29 the guaranty, the lender must obtain financial statements from all necessary individuals and entities IRS Tax Transcripts Lenders must verify the financial information submitted with a loan application using IRS Form IRS Form 4506 can be downloaded from IRS website at IRS.gov. The IRS requires a fee for processing IRS Form However IRS Form 4506-T can be downloaded from the SBA website at SBA.gov and the processing fee will be waived. Even if this requirement is not specified in the Authorization, the lender must verify the financial information to be sent to SBA against the information sent to the IRS to ensure there are no discrepancies. Also, it is important to ensure the borrower is up to date on taxes because the borrower is prohibited from using any of the loan proceeds to pay past-due taxes Environmental Investigation The lender is required to get an environmental investigation on all commercial property offered as security for the loan. The lender must check the NAICS to ensure that the property is not in an environmentally sensitive area. Once the lender determines that it is not likely that the property has environmental contamination, the lender must submit an environmental questionnaire to SBA with recommendations and request SBA send an 37 SOP (5)(F), Subpart B, Chapter 4.II.B 38 SOP (5)(F), Subpart B, Chapter 5.III C.F.R

30 environmental approval. 40 If there is evidence of contamination, the lender must get a Phase I and/or Phase II Environmental Site Assessment (ESA) and take necessary actions depending on the assessment results Insurance The Loan Authorization will contain the insurance requirements from origination of the loan. The Authorization will always require hazard insurance to insure the collateral. 42 Also, the lender should always get a title commitment (and associated policy of title insurance) on the property to insure the required lien position on the property. 43 Additionally, the lender must get a Standard Flood Hazard Determination (FEMA Form 81-93) done on the property. 44 If the property is in a special flood hazard area, the lender should require the borrower to get flood insurance through the National Flood Insurance Program (NFIP). As opposed to insuring the collateral with hazard and flood insurance, life insurance is actually considered collateral. When the viability of the business and repayment ability is directly attached to one individual, the lender should require an assignment of life insurance. If the loan is fully collateralized otherwise, life insurance may not be necessary, but it should be obtained if possible to protect the lender s interest in a key individual of the entity. In addition to the common insurance requirements 40 SOP (5)(F), Subpart B, Chapter 4.III 41 SOP (5)(F), Subpart B, Chapter 4.III C.F.R (C) 43 SOP 50 57, Chapter 9, Paragraph B C.F.R

31 mentioned above, the lender may also need to require other insurance suitable to the loan, such as liability insurance, disability insurance, and worker s compensation insurance. 45 It is crucial that the lender monitor the status of the insurance. If the insurance lapses and the property is destroyed or the insured dies, the lender will be accountable for the loss. As soon as the lender becomes aware of a lapse in the insurance, the lender must determine what action is considered prudent and reasonable. In some instances, the prudent and reasonable action may be to force the insured to guarantee that the lender and SBA are protected under the insurance policy, either by reinstating the insurance or signing a new policy Standby Agreements A lender must obtain a Standby Agreement (SBA Form 155) if there are other creditors involved in the secured property. The standby creditor must agree to subordinate any lien rights in collateral securing the loan to the lender s rights in the collateral, or if applicable subordinate, in full or in part, any payment rights due standby creditor to lender s rights to payment. The standby creditor must also agree not to take any action against the borrower or any collateral without lender s consent. 47 This agreement is essential to ensure that the lender obtains the necessary lien and debt position. 45 SOP (5)(F), Subpart B, Chapter 5.II 46 U.S. Small Business Administration, Helpful Hints for Navigating the National Guaranty Purchase Center, 47 SOP (5)(F), Subpart B, Chapter 5.IV 31

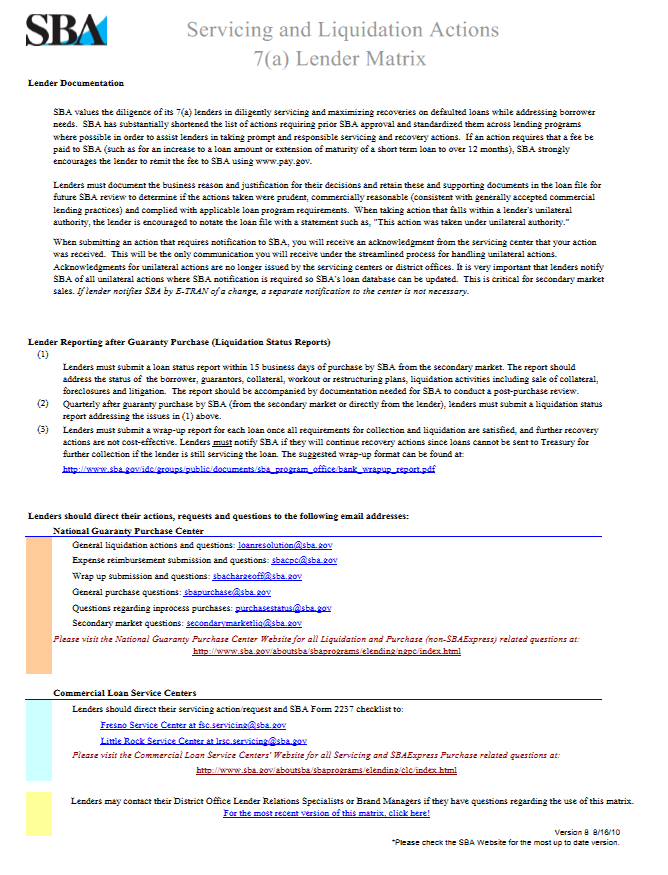

32 IV. Servicing All lender actions must comply with SBA loan program requirements. 48 While the lender is servicing or liquidating a loan, there are many actions which require prior SBA approval or notification. 49 The Office of Financial Program Operations (OFPO) has developed a Servicing and Liquidation Actions 7(a) Lender Matrix to ensure SBA lenders are able to find and comply with Agency Loan Program Requirements. 50 While servicing a loan, the lender is responsible for actions necessary to support the growth of the business, as well as evaluating and responding to problems which may arise. 51 There are red flags indicating potential problems that must be addressed when servicing loans, including: payment default notices; requests for relief in loan terms or conditions; cash flow problems; adverse changes; cancellation of life or hazard insurance policies; death or illness of a principal; tax problems; substantive changes in management or control of the business; fire or loss of collateral due to natural disasters; legal actions; loss of contracts; borrower s failure to submit financial statements timely; and/or loan delinquencies in excess of 60 days. 52 The lender s handling of the abovementioned situations in the servicing process is crucial to the final review of the guaranty purchase. 48 See SOP , Subpart B and SOP 50 57; 13 C.F.R ; 13 C.F.R C.F.R U.S. Small Business Administration, 7(a) Servicing and Liquidation Actions Matrix, 51 SOP A 52 Id.

33 A. Necessity of Lender Compliance In order to safeguard the SBA guaranty and interest, loans must be structured in accordance with SBA loan requirements, comply with the SBA loan authorization, and certify that all matters were performed with due diligence. 53 It is imperative for lenders to understand that the SBA authorization is not a contract to make a loan, so there is not an actual guaranty 54 against loss or commitment to fund at the time the Authorization is issued. Nor can a potential borrower force a lender to make a loan to a borrower merely because SBA has issued a loan authorization. The making of the loan remains a credit decision of the lender. If a loan is made by a lender under the SBA loan authorization, it is an agreement between SBA, as an agency of the United States Government, and the lender. The borrower is not a party or a third party beneficiary to any loan authorization. SBA has established Standard Operating Procedures (SOPs) as practical requirements for lenders based on sound lending practices for all steps of the loan process. In addition to complying with statutory and regulatory law, lenders must abide by the SOPs to ensure that the borrower is creditworthy and the loan proceeds will be disbursed according to the authorization, so that the guaranty will be realized. 55 In the event of any conflict between a loan Authorization and the guidelines established by the SOP, the SOP controls (SOP 50 10(5)(F), page 298, super priority of SOP versus loan authorization boilerplate) C.F.R Id. 55 U.S. Small Business Administration, Standard Operating Procedures, 33

34 B. Servicing and Liquidation Actions 1. Lender Documentation & Reporting SBA is concerned with materiality and harm. 56 The lender should proactively approach any issues because early identification could lead to possible solutions to ensure the guaranty. Therefore, the lender should ensure all actions are properly documented and prudent to minimize the effect of an adverse action on SBA s decision to purchase. 57 The lender s actions will be reviewed to determine if they were prudent, lawful and commercially reasonable, and consistent with the lender s practice on its non-sba loans. 58 Therefore, documentation is crucial to evidence justifications for decisions. a Reports In addition to documenting all actions, all SBA loans must be reported on the SBA 1502 report to the Fiscal Transfer Agent (FTA) once a month. 59 When the loan is transferred into liquidation status, the lender must change the status code on the monthly 1502 report to 5 for liquidation status. After purchase of the guaranty, quarterly liquidation reports must be submitted to SBA at sbachargeoff@sba.gov. 60 Once the lender becomes reasonably aware that the loan is ready for charge off, the Wrap-Up report should be sent, but 56 SOP 50 57, Chapter 24, Subpart B 57 U.S. Small Business Administration, Sale-Release of Collateral, C.F.R SOP 50 57, Chapter 3, Subpart F; U.S. Small Business Administration, Lender Reporting, 60 Id.

35 only after the lender has made a final determination that the loan will not be fully repaid after all worthwhile collateral has been liquidated and no further recoveries are anticipated within a reasonable time. 61 This report should address the status of the borrower, guarantors, collateral, workout or restructuring plans, and liquidation activities, including sale of collateral, foreclosures and litigation. 62 b. Site Visit Reports Additionally, the lender must submit a Site Visit Report after every visit to the borrower s business premise. 63 All lenders are required to make timely site visits to assess the value of the property. Additionally, lenders must take inventory of loan collateral to assess workout possibilities and develop a significant liquidation plan. A site visit is generally considered timely within 15 calendar days of the occurrence of an event that would cause the loan to be placed in liquidation, such as abandonment of the business, bankruptcy of the borrower when loan is in default and substantial collateral exists, litigation against the borrower that may have a substantial adverse effect on the lender s interest, or foreclosure by a prior lien holder on substantial collateral. If there is significant collateral that could be removed or the value could be depleted, 61 SOP 50 57, Chapter SOP 50 57, Chapter 3, Subpart F 63 Id. 35

36 the site visit should be made as soon as possible. A current appraisal or third party inspection is acceptable to assess the current collateral value. 64 Once all the requirements for collection and liquidation are satisfied, the lender must submit a Wrap-Up Report for each loan. 65 Before sending a Wrap-Up Report, the lender must be reasonably aware that the loan is ready for charge off because loans cannot be sent to Treasury for further collection if the lender is still servicing the loan. 66 A lender must comply with all reporting requirements to realize the guaranty. c. Transcript of Account A lender should document all transactions to the borrower s account. If the loan is in default, the lender must submit a certified transcript of account to SBA when the lender requests guaranty purchase. 67 The transcript must adequately reflect all transactions on the borrower s account. Specifically, the lender must include the payment receipt dates, next due date, interest rates in effect throughout loan s term, application of payments and sale of collateral proceeds, and the interest paid to date. 68 The lender must carefully document all information because the lender has to certify that it is a true and accurate reflection of the account. 64 SOP (2)(B), Chapter 13, Paragraph SOP 50 57, Chapter Id. 67 SOP (4)(D) 68 Id.

37 2. Monitoring Creditworthiness The lender is required to continually monitor the borrower s creditworthiness. The lender is responsible for ensuring the borrower maintain a steady financial and operational condition. The lender can monitor credit by requiring the borrower to submit financial statements, maintaining constant contact with the borrower on the status of the business, and reviewing credit reports, credit scores, or tax information when needed to verify the borrower is still creditworthy Servicing & Liquidation Approval As mentioned earlier, the lender should refer to the Servicing and Liquidation Action 7(a) Lender Matrix before any action to determine whether it requires prior SBA approval or notification. 70 Generally, the lender will need written approval from SBA for the following types of servicing activities: Altering substantially the terms or conditions of any loan (including an increase in principal amount or change in interest rate); Releasing collateral having a cumulative value in excess of 20 percent of the original loan amount; Accelerating the maturity of the note; 69 SOP 50 57, Chapter 3, Paragraph E 70 U.S. Small Business Administration, 7(a) Servicing and Liquidation Actions Matrix, 37

38 Bringing a suit upon any loan; Compromising or waiving a claim against any borrower, guarantor, obligor, or creditor arising out of the loan; and/or Increasing the amount of any prior lien by the lender on collateral securing the loan. 71 If any servicing or liquidation action does not require prior approval, lenders should document all justifications for their decisions with supporting documentation in their file. 4. Liquidation & Litigation Plans All Lenders are expected to liquidate and conduct debt collection litigation for 7(a) loans in their portfolio no less diligently than for their non-sba portfolio. This includes liquidating in a prompt, cost-effective, and commercially reasonable manner, consistent with prudent lending standards, and in accordance with Loan Program Requirements. All collateral should be liquidated and all worthwhile avenues of collection should be pursued until loans can be charged off. Lenders must take precaution in liquidation actions to ensure that no actual or apparent conflict of interest will result from the lender s actions. For instance, if the lender has any loans that are not guaranteed by SBA, the lender may not take any action which confers a preference to the lender over recovery on the SBA loan C.F.R U.S. Small Business Administration, Helpful Hints for Navigating the National Guaranty Purchase Center,

39 Lenders should prepare a liquidation plan based on the facts known and reasonable assumptions. This practice is considered prudent and commercially reasonable to maximize recovery. SBA Form 1979 can be used to properly prepare your liquidation plan. 73 Further, lenders must liquidate all business personal property that secures the loan before the lender submits a purchase package to SBA, unless the borrower has filed for bankruptcy. 74 In addition to a liquidation plan, lenders should prepare a litigation plan to include any work to be performed and fees to be charged. Depending on the anticipated cost and the nature of the work, lenders must obtain SBA s prior approval of a litigation plan before entering into any non-routine litigation. Nonroutine litigation includes factual or legal issues in dispute that require resolution through adjudication; legal fees that are estimated to exceed $10,000; lender has a potential or actual conflict of interest with SBA; or lender has made a separate loan to the borrower, which was not a loan by SBA. 75 Practice Tip: If a lender engages in non-routine litigation, incurs legal expenses, and then submits its litigation plan and invoices for legal work already performed, these legal expenses could be challenged and might be disallowed. 73 U.S. Small Business Administration, SBA Form 1979, Liquidation Plan Format, C.F.R (a) 75 U.S. Small Business Administration, Litigation Plans, 39

40 V. Pitfalls SBA does not have to honor a guaranty purchase request in full or in part on a 7(a) loan if the lender failed to comply materially with a loan program requirement; failed to make, close, service, liquidate or litigate the loan in a prudent manner; placed SBA at risk through improper action or inaction; failed to disclose a material fact to SBA in a timely manner; or misrepresented a material fact to SBA regarding the loan. 76 The following are the common reasons cited by SBA for which a guaranty is repaired or denied: A. Expiration after Maturity Issue If the lender does not request purchase within 180 days after loan maturity, SBA is not obligated to purchase the guaranty. B. Lien and Collateral Issues Lien and collateral issues may result in a missed recovery. Examples of lien and collateral issues that may arise are as follows: Failure to obtain required lien position; Failure to properly perfect security interest; and/or Failure to fully collateralize loan at origination when additional collateral was unavailable C.F.R (a)

41 C. Unauthorized Use of Proceeds Issues Recovery can be repaired or denied when proceeds are disbursed for purposes inconsistent with the loan authorization or subsequent modifications without a business justification. Typically, if proceeds are distributed in a manner not consistent with authorization, the guaranteed amount may be repaired. However, a complete denial will result when early default and improper use of the proceeds cause the failure of the business. D. Liquidation Deficiency Issues Liquidation deficiency will generally result in a repair. However, a denial may occur when harm is the full value of the outstanding balance. The following situations are examples of liquidation deficiencies: Failure to conduct a Site Visit which resulted in a missed recovery; Improper safeguarding or disposition of collateral which resulted in missed recoveries; and/or Misapplication of recoveries to lender s loan when SBA-guaranteed loan has lien priority. E. Undocumented Servicing Actions Issues An undocumented servicing action will generally result in a repair of recovery under the following situations: Liens not properly renewed during servicing on worthwhile collateral; Release or subordination of collateral without documented business justification; 41

42 Allowing hazard insurance to lapse on major collateral when collateral is subsequently destroyed; and/or Failure to maintain life insurance on principal when principal subsequently dies. F. Early Default Issues Early default can result in a denial if it is determined to be the reason for business failure under the following circumstances: Missing or unsupported verification of required equity injection, which will include verification of source in certain cases; and/or Missing or unsupported documentation of verification of borrower financial information with IRS when financial information was relied on in lender s credit analysis.

43 EXHIBIT A SBA Form 1919 (Borrower Application for 7(a) Loan) 43

44

45 45

46

47 47

48

49 49

50 EXHIBIT B SBA Form 912 (Statement of Personal History)

51 51

52

53 EXHIBIT C SBA Form 413 (Personal Financial Statement) 53

54

55 55

56

57 57

58

59 EXHIBIT D SBA Form 159 (Compensation Agreement for 7(a) Loan) 59

60

61 61

62

63 EXHIBIT E IRS Form 4506T (Request for Tax Transcript) 63

64

65 65

66 EXHIBIT F SBA Form 147 (Note for 7(a) Loan)

67 U.S. Small Business Administration NOTE SBA Loan # SBA Date 2014 Loan Amount Interest Rate Borrower Operating Company Lender Adjusting years from the date of @@ 1. PROMISE TO PAY: In return for the Loan, Borrower promises to pay to the order of Lender the amount -($@@) Dollars, interest on the unpaid principal balance, and all other amounts required by this Note. 2. DEFINITIONS: Collateral means any property taken as security for payment of this Note or any guarantee of this Note. Guarantor means each person or entity that signs a guarantee of payment of this Note. Loan means the loan evidenced by this Note. Loan Documents means the documents related to this loan signed by Borrower, any Guarantor, or anyone who pledges collateral. SBA means the Small Business Administration, an Agency of the United States of America. 67

68 3. PAYMENT TERMS: Borrower must make all payments at the place Lender designates. The payment terms for this Note are: Note will mature in 10 years from date of Note. initial interest rate is 6.00% per year for 3 years. This initial rate is the prime rate in effect on the first business day of the month in which SBA received the loan application, plus 2.75%. The interest rate on this Note will then begin to fluctuate as described below. The initial interest rate must remain in effect until the first change period must pay principal and interest payments of $4, every month, beginning one month from the month this Note is dated; payments must be made on the first calendar day in the months they are will apply each installment payment first to pay interest accrued to the day Lender receives the payment, then to bring principal current, then to pay any late fees, and will apply any remaining balance to reduce interest rate will be adjusted every 3 years from the date of the Note (the "change "Prime Rate" is the prime rate in effect on the first business day of the month (as published in the Wall Street Journal) in which SBA received the application, or any interest rate change occurs. Base Rates will be rounded to two decimal places with.004 being rounded down and.005 being rounded adjusted interest rate will be 2.75% above the Prime Rate. Lender will adjust the interest rate on the first calendar day of each change period. The change in interest rate is effective on that day whether or not Lender gives Borrower notice of the must adjust the payment amount at least annually as needed to amortize principal over the remaining term of the SBA purchases the guaranteed portion of the unpaid principal balance, the interest rate becomes fixed at the rate in effect at the time of the earliest uncured payment default. If there is no uncured payment default, the rate becomes fixed at the rate in effect at the time of purchase. Loan any provision in this Note to the may prepay this Note. Borrower may prepay 20% or less of the unpaid principal balance at any time without notice. If Borrower prepays more than 20% and the Loan has been sold on the secondary market, Borrower must: a. Give Lender written notice; b. Pay all accrued interest; and c. If the prepayment is received less than 21 days from the date Lender receives the notice, pay an amount equal to 21 days' interest from the date lender receives the notice, less any interest accrued during the 21 days and paid under subparagraph b., Borrower does not prepay within 30 days from the date Lender receives the notice, Borrower must give Lender a new remaining principal and accrued interest is due and payable 10 years from date of Charge: If a payment on this Note is more than 10 days late, Lender may charge Borrower a late fee of up to 5.00% of the unpaid portion of the regularly scheduled payment.

69 4. Borrower is in default under this Note if Borrower does not make a payment when due under this Note, or if Borrower or Operating Company: A. Fails to do anything required by this Note and other Loan Documents; B. Defaults on any other loan with Lender; C. Does not preserve, or account to Lender s satisfaction for, any of the Collateral or its proceeds; D. Does not disclose, or anyone acting on their behalf does not disclose, any material fact to Lender or SBA; E. Makes, or anyone acting on their behalf makes, a materially false or misleading representation to Lender or SBA; F. Defaults on any loan or agreement with another creditor, if Lender believes the default may materially affect Borrower s ability to pay this Note; G. Fails to pay any taxes when due; H. Becomes the subject of a proceeding under any bankruptcy or insolvency law; I. Has a receiver or liquidator appointed for any part of their business or property; J. Makes an assignment for the benefit of creditors; K. Has any adverse change in financial condition or business operation that Lender believes may materially affect Borrower s ability to pay this Note; L. Reorganizes, merges, consolidates, or otherwise changes ownership or business structure without Lender s prior written consent; or M. Becomes the subject of a civil or criminal action that Lender believes may materially affect Borrower s ability to pay this Note. S RIGHTS IF THERE IS A DEFAULT: Without notice or demand and without giving up any of its rights, Lender may: A. Require immediate payment of all amounts owing under this Note; B. Collect all amounts owing from any Borrower or Guarantor; C. File suit and obtain judgment; D. Take possession of any Collateral; or E. Sell, lease, or otherwise dispose of, any Collateral at public or private sale, with or without advertisement. S GENERAL POWERS: Without notice and without Borrower s consent, Lender may: A. Bid on or buy the Collateral at its sale or the sale of another lienholder, at any price it chooses; B. Incur expenses to collect amounts due under this Note, enforce the terms of this Note or any other Loan Document, and preserve or dispose of the Collateral. Among other things, the expenses may include payments for property taxes, prior liens, insurance, appraisals, environmental remediation costs, and reasonable attorney s fees and costs. If Lender incurs such expenses, it may demand immediate repayment from Borrower or add the expenses to the principal balance; 69

70 C. Release anyone obligated to pay this Note; D. Compromise, release, renew, extend or substitute any of the Collateral; and E. Take any action necessary to protect the Collateral or collect amounts owing on this Note. 7. FEDERAL LAW APPLIES: When SBA is the holder, this Note will be interpreted and enforced under federal law, including SBA regulations. Lender or SBA may use state or local procedures for filing papers, recording documents, giving notice, foreclosing liens, and other purposes. By using such procedures, SBA does not waive any federal immunity from state or local control, penalty, tax, or liability. As to this Note, Borrower may not claim or assert against SBA any local or state law to deny any obligation, defeat any claim of SBA, or preempt federal law. 8. AND ASSIGNS: Under this Note, Borrower and Operating Company include the successors of each, and Lender includes its successors and assigns. 9. PROVISIONS: A. All individuals and entities signing this Note are jointly and severally liable. B. Borrower waives all suretyship defenses. C. Borrower must sign all documents necessary at any time to comply with the Loan Documents and to enable Lender to acquire, perfect, or maintain Lender s liens on Collateral. D. Lender may exercise any of its rights separately or together, as many times and in any order it chooses. Lender may delay or forgo enforcing any of its rights without giving up any of them. E. Borrower may not use an oral statement of Lender or SBA to contradict or alter the written terms of this Note. F. If any part of this Note is unenforceable, all other parts remain in effect. G. To the extent allowed by law, Borrower waives all demands and notices in connection with this Note, including presentment, demand, protest, and notice of dishonor. Borrower also waives any defenses based upon any claim that Lender did not obtain any guarantee; did not obtain, perfect, or maintain a lien upon Collateral; impaired Collateral; or did not obtain the fair market value of Collateral at a sale.

71 10. PROVISIONS: [Initialed ] [Initialed ] 11. BORROWER S NAME(S) AND SIGNATURE(S): By signing below, each individual or entity becomes obligated under this Note as @@ 71

72 EXHIBIT G SBA Form 1505 (Note for 504 Loan)

73 SBA Loan # SBA Date 2014 Loan Amount Borrower Operating Company @@ Funding * Interest Rate: % First Payment Note Maturity * P&I Amount: $ * Monthly Payment: $ (* blank at signing) 1. PROMISE TO PAY: In return for the Loan, Borrower promises to pay to the order of CDC the amount --- ($@@) --- Dollars, interest on the unpaid principal balance, the fees specified in the Servicing Agent Agreement, and all other amounts required by this Note. 2. DEFINITIONS: "Collateral" means any property taken as security for payment of this Note or any guarantee of this Note. "Debenture" means the debenture issued by CDC to fund the Loan "Guarantor" means each person or entity that signs a guarantee of payment of this Note. 73

74 "Loan" means the loan evidenced by this Note. "Loan Documents" means the documents related to this loan signed by Borrower, Guarantor, or anyone who pledges collateral. "SBA" means the Small Business Administration, an Agency of the United States of America. "Servicing Agent Agreement" means the agreement between the Borrower and the CDC that, among other things, appoints a servicing agent ("Servicing Agent") for this Note. 3. INTEREST RATE AND PAYMENTS: The terms of the Debenture sale will establish the interest rate, P & I amount, and Monthly Payment for this Note. Borrower acknowledges that these terms are unknown when Borrower signs this Note. A. Once established, the interest rate is fixed. Interest begins to accrue on the Funding Date. B. Monthly Payments are due on the first business day of each month, beginning on the First Payment Date and continuing until the Note Maturity Date, when all unpaid amounts will be due. Borrower must pay at the place and by the method the Servicing Agent or CDC designates. The Monthly Payment includes the monthly principal and interest installment (P & I Amount), and the monthly fees in the Servicing Agent Agreement. The Servicing Agent will apply regular Monthly Payments in the following order: 1) monthly fees, 2) accrued interest, and 3) principal. 4. LATE-PAYMENT FEE: CDC charges a late fee if the Servicing Agent receives a Monthly Payment after the fifteenth day of the month when it is due. The late fee is five percent of the payment amount, or $100.00, whichever is greater. The late fee is in addition to the regular Monthly Payment. 5. RIGHT TO PREPAY: Borrower may prepay this Note in full on a specific date each month set by the Servicing Agent. Borrower may not make partial prepayments. Borrower must give CDC at least 45 days' prior written notice. When it receives the notice, CDC will give Borrower prepayment instructions. At least 10 days before the payment date, Borrower must wire a non-refundable deposit of $1,000 to the Servicing Agent. The Servicing Agent will apply the deposit to the prepayment if Borrower prepays. In any prepayment, Borrower must pay the sum of all of the following amounts due and owing through the date of the next semi-annual Debenture payment: A. Principal balance; B. Interest; C. SBA guarantee fees; D. Servicing agent fees; E. CDC servicing fees; F. Late fees;

75 G. Expenses incurred by CDC for which Borrower is responsible; and H. Any prepayment premium. 6. PREPAYMENT PREMIUM; If Borrower prepays during the first half of the Note term, Borrower must pay a prepayment premium. The formula for the prepayment premium is specified in the Debenture and may be obtained from CDC. 7. DEFAULT: Borrower is in default under this Note if Borrower does not make a payment when due under this Note, or if Borrower or Operating Company: A. Fails to do anything required by this Note and other Loan Documents; B. Defaults on any other loan made or guaranteed by SBA; C. Does not preserve or account to CDC's satisfaction for any of the Collateral or its proceeds; D. Does not disclose, or anyone acting on their behalf does not disclose, any material fact to CDC or SBA; E. Makes, or anyone acting on their behalf makes, a materially false or misleading representation to CDC or SBA; F. Defaults on any loan or agreement with another creditor, if CDC believes the default may materially affect Borrower's ability to pay this Note; G. Fails to pay any taxes when due; H. Becomes the subject of a proceeding under any bankruptcy or insolvency law; I. Has a receiver or liquidator appointed for any part of their business or property; J. Makes an assignment for the benefit of creditors; K. Has any adverse change in financial condition or business operation that CDC believes may materially affect Borrower's ability to pay this Note; L. Reorganizes, merges, consolidates, or otherwise changes ownership or business structure without CDC's prior written consent, except for ownership changes of up to 5 percent beginning six months after the Loan closes; or M. Becomes the subject of a civil or criminal action that CDC believes may materially affect Borrower's ability to pay this Note. 8. CDC'S RIGHTS IF THERE IS A DEFAULT: Without notice or demand and without giving up any of its rights, CDC may: A. Require immediate payment of all amounts owing under this Note; B. Collect all amounts owing from any Borrower or Guarantor; C. File suit and obtain judgment; D. Take possession of any Collateral; and, E. Sell, lease, or otherwise dispose of, any Collateral at public or private sale, with or without advertisement. 75

76 9. CDC'S GENERAL POWERS: Without notice and without Borrower's consent, CDC may: A. Bid or buy at any sale of Collateral by Lender or another lienholder, at any price it chooses; B. Incur expenses to collect amounts due under this Note, enforce the terms of this Note or any other Loan Document, and preserve or dispose of the Collateral. Among other things, the expenses may include payments for property taxes, prior liens, insurance, appraisals, environmental remediation costs, and reasonable attorney's fees and costs. If CDC incurs such expenses, it may demand immediate repayment from Borrower or add the expenses to the principal balance; C. Release anyone obligated to pay this Note; D. Compromise, release, renew, extend or substitute any of the Collateral; and E. Take any action necessary to protect the Collateral or collect amounts owing on this Note. 10. FEDERAL LAW: When SBA is the holder, this Note will be interpreted and enforced under federal law, including SBA regulations. CDC or SBA may use state or local procedures for filing papers, recording documents, giving notice, foreclosing liens, and other purposes. By using such procedures, SBA does not waive any federal immunity from state or local control, penalty, tax, or liability. As to this Note, Borrower may not claim or assert against SBA any local or state law to deny any obligation, defeat any claim of SBA, or preempt federal law. 11. SUCCESSORS AND ASSIGNS: Under this Note, Borrower and Operating Company include the successors of each, and CDC includes its successors and assigns. 12. GENERAL PROVISIONS: A. All individuals and entities signing this Note are jointly and severally liable. B. Borrower authorizes CDC, the Servicing Agent, or SBA to complete any blank terms in this Note and any other Loan Documents. The completed terms will bind Borrower as if they were completed prior to this Note being signed. C. Borrower waives all suretyship defenses. D. Borrower must sign all documents necessary at any time to comply with the Loan Documents and to enable CDC to acquire, perfect, or maintain CDC's liens on Collateral. E. CDC may exercise any of its rights separately or together, as many times and in any order it chooses. CDC may delay or forgo enforcing any of its rights without giving any up. F. Borrower may not use any oral statement to contradict or alter the written terms of, or raise a defense to, this Note. G. If any part of this Note is unenforceable, all other parts remain in effect. H. To the extent allowed by law, Borrower waives all demands and notices in connection with this Note, including presentment, demand, protest, and notice of dishonor. Borrower also waives any defenses based upon any claim that CDC did not obtain any guarantee; did not obtain, perfect, or maintain a lien upon Collateral; impaired Collateral; or did not obtain the fair market value of Collateral at a sale.

77 13. STATE-SPECIFIC PROVISIONS: NONE BORROWER'S NAME(S) AND SIGNATURE(S): By signing below, each individual or entity becomes obligated under this Note as Borrower. IN WITNESS WHEREOF, we have hereunto set our hands and seals on the date first above written. By: 77

78 EXHIBIT H SBA Form 148 (SBA Unconditional Guarantee)

79 SBA Loan # SBA Loan Name Guarantor @@ Date 2014 Note Amount $@@ 1. GUARANTEE: Guarantor unconditionally guarantees payment to Lender of all amounts owing under the Note. This Guarantee remains in effect until the Note is paid in full. Guarantor must pay all amounts due under the Note when Lender makes written demand upon Guarantor. Lender is not required to seek payment from any other source before demanding payment from Guarantor. 2. NOTE: The "Note" is the promissory note dated this date, in the principal amount --- ($@@) --- Dollars, from Borrower to Lender. It includes any assumption, renewal, substitution, or replacement of the Note, and multiple notes under a line of credit. 3. DEFINITIONS: "Collateral" means any property taken as security for payment of the Note or any guarantee of the Note. "Loan" means the loan evidenced by the Note. "Loan Documents" means the documents related to the Loan signed by Borrower, Guarantor or any other guarantor, or anyone who pledges Collateral. "SBA" means the Small Business Administration, an Agency of the United States of America. 79

80 4. LENDER'S GENERAL POWERS: Lender may take any of the following actions at any time, without notice, without Guarantor's consent, and without making demand upon Guarantor: A. Modify the terms of the Note or any other Loan Document except to increase the amounts due under the Note; B. Refrain from taking any action on the Note, the Collateral, or any guarantee; C. Release any Borrower or any guarantor of the Note; D. Compromise or settle with the Borrower or any guarantor of the Note; E. Substitute or release any of the Collateral, whether or not Lender receives anything in return; F. Foreclose upon or otherwise obtain, and dispose of, any Collateral at public or private sale, with or without advertisement; G. Bid or buy at any sale of Collateral by Lender or any other lienholder, at any price Lender chooses; and H. Exercise any right it has, including those in the Note and other Loan Documents. These actions will not release or reduce the obligations of Guarantor or create any rights or claims against Lender. 5. FEDERAL LAW: When SBA is the holder, the Note and this Guarantee will be construed and enforced under federal law, including SBA regulations. Lender or SBA may use state or local procedures for filing papers, recording documents, giving notice, foreclosing liens, and other purposes. By using such procedures, SBA does not waive any federal immunity from state or local control, penalty, tax, or liability. As to this Guarantee, Guarantor may not claim or assert any local or state law against SBA to deny any obligation, defeat any claim of SBA, or preempt federal law. 6. RIGHTS, NOTICES, AND DEFENSES THAT GUARANTOR WAIVES: To the extent permitted by law, A. Guarantor waives all rights to: 1) Require presentment, protest, or demand upon Borrower; 2) Redeem any Collateral before or after Lender disposes of it; 3) Have any disposition of Collateral advertised; and 4) Require a valuation of Collateral before or after Lender disposes of it.

81 B. Guarantor waives any notice of: 1) Any default under the Note; 2) Presentment, dishonor, protest, or demand; 3) Execution of the Note; 4) Any action or inaction on the Note or Collateral, such as disbursements, payment, nonpayment, acceleration, intent to accelerate, assignment, collection activity, and incurring enforcement expenses; 5) Any change in the financial condition or business operations of Borrower or any guarantor; 6) Any changes in the terms of the Note or other Loan Documents, except increases in the amounts due under the Note; and 7) The time or place of any sale or other disposition of Collateral. C. Guarantor waives defenses based upon any claim that: 1) Lender failed to obtain any guarantee; 2) Lender failed to obtain, perfect, or maintain a security interest in any property offered or taken as Collateral; 3) Lender or others improperly valued or inspected the Collateral; 4) The Collateral changed in value, or was neglected, lost, destroyed, or underinsured; 5) Lender impaired the Collateral; 6) Lender did not dispose of any of the Collateral; 7) Lender did not conduct a commercially reasonable sale; 8) Lender did not obtain the fair market value of the Collateral; 9) Lender did not make or perfect a claim upon the death or disability of Borrower or any guarantor of the Note; 10) The financial condition of Borrower or any guarantor was overstated or has adversely changed; 11) Lender make errors or omissions in Loan Documents or administration of the Loan; 12) Lender did not seek payment from the Borrower, any other guarantors, or any Collateral before demanding payment from Guarantor; 13) Lender impaired Guarantor's suretyship rights; 14) Lender modified the Note terms, other than to increase amounts due under the Note. If Lender modifies the Note to increase the amounts due under the Note without Guarantor's consent, Guarantor will not be liable for the increased amounts and related interest and expenses, but remains liable for all other amounts; 15) Borrower has avoided liability on the Note; or 16) Lender has taken an action allowed under the Note, this Guarantee, or other Loan Documents. 81