The Final RESPA Rule

|

|

|

- Nathan Wiggins

- 10 years ago

- Views:

Transcription

1 The Final RESPA Rule

2 GFE 2

3 GFE Triggers borrower s name Social Security number property address monthly income house value or best estimate amount of loan & any other information 3

4 GFE General provided no later than 3 business days by hand, mail, fax, (but not if application denied or withdrawn by borrower may be provided by mortgage broker, but lender is responsible if lenders prefer to generate the GFE, they must do so within 3 days of the broker receiving the application 4

5 GFE Page 1 5

6 Important Dates 6

7 Important Dates BEFORE LOCK AFTER LOCK AFTER LOCK 7

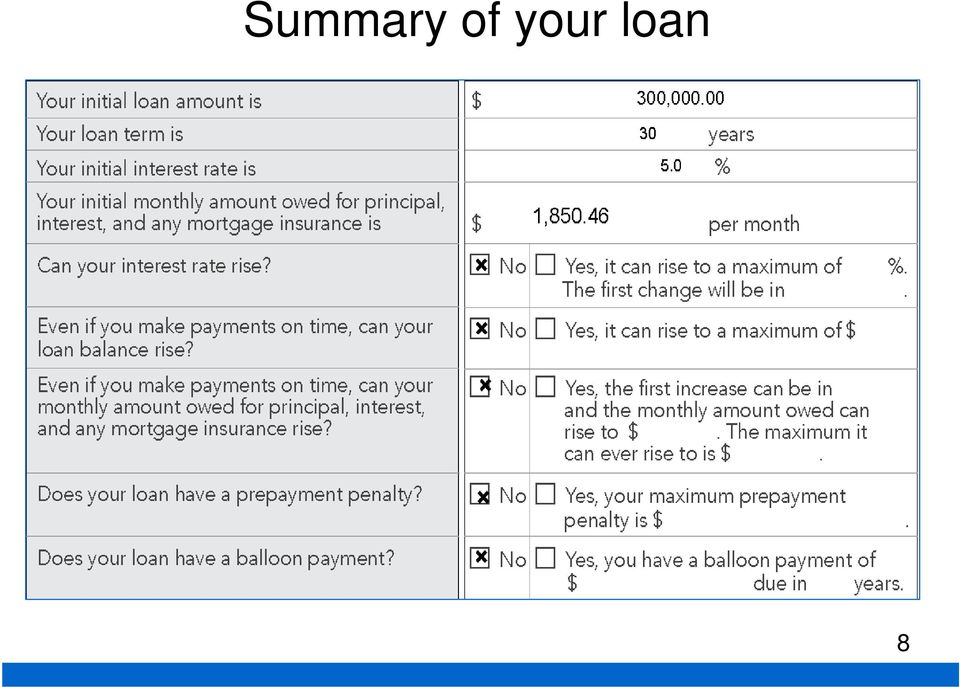

8 Summary of your loan 8

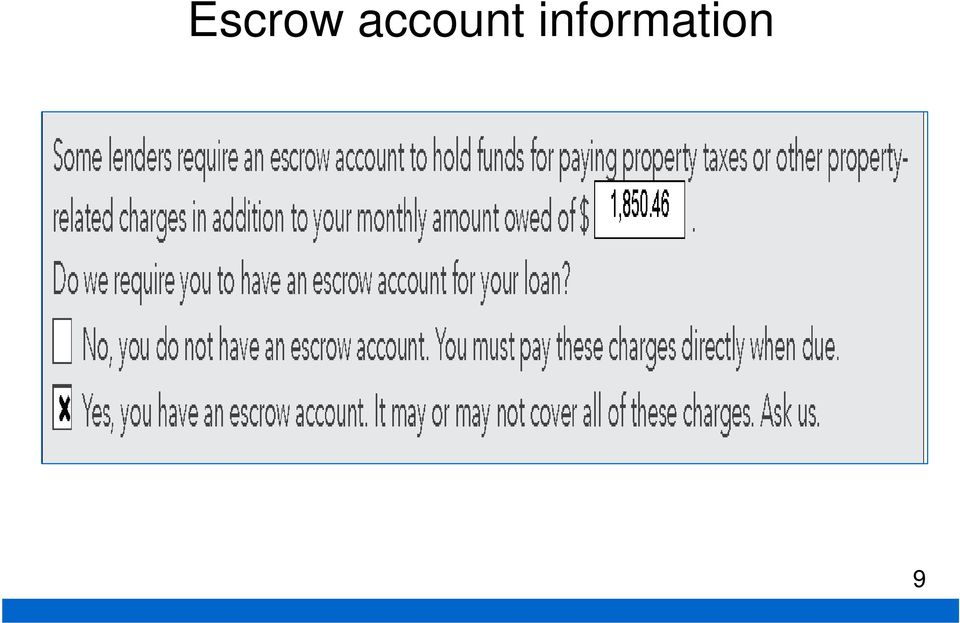

9 Escrow account information 9

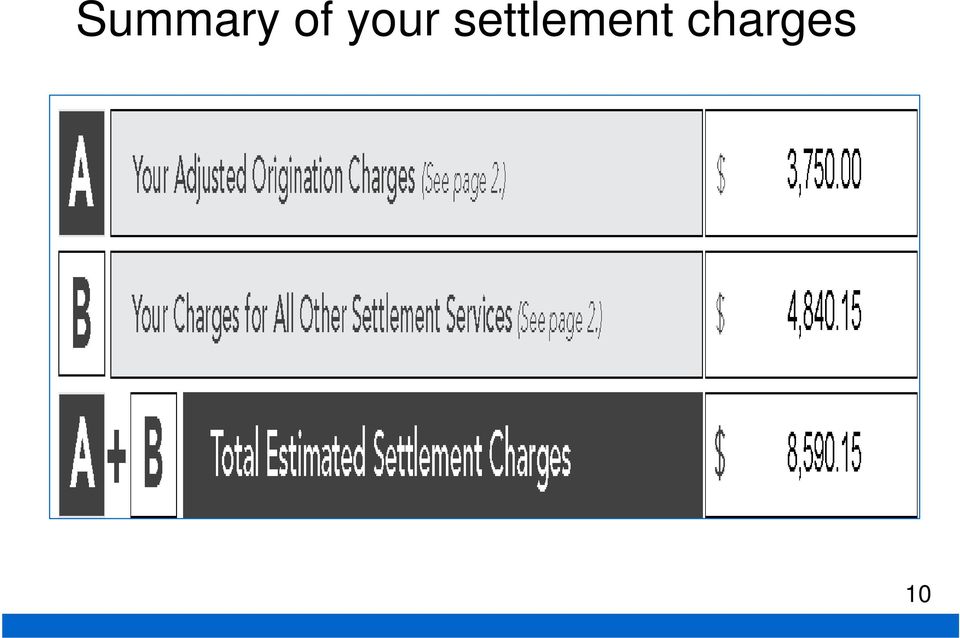

10 Summary of your settlement charges 10

11 GFE Page 2 11

12 Old GFE vs. New GFE for Loan Origination Fees origination fee/point mortgage broker fee processing doc prep commitment application wire MERS registration underwriting delivery/courier admin doc review electronic miscellaneous Our Origination Charge 12

13 Block 1, Our Origination Charge Must contain ALL charges by ALL loan originators in the transaction 13

14 Block 2, Your Credit or Charge 14

15 Example 15

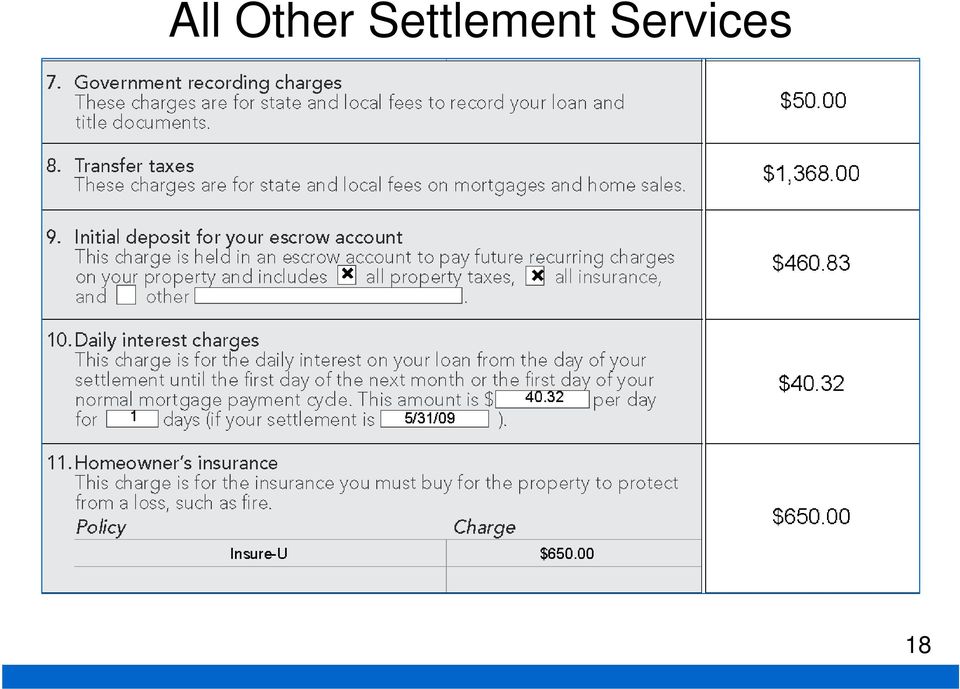

16 All Other Settlement Services 16

17 Old GFE vs. New GFE for Title Services settlement fee abstract/title search title examination doc prep attorney fee commitment/binder notary wire fee lender s title insurance endorsements courier/delivery copying electronic miscellaneous Title services & lender s title insurance 17

18 All Other Settlement Services 18

19 Written List If a loan originator permits a borrower to shop for services (Block 4, 5 & 6), the loan originator must provide a written list of providers that the estimates were based on. 19

20 Written List Must be provided with GFE on a separate piece of paper Must include at least one provider of each shoppable service 20

21 Written List If no service providers are listed, then it is assumed the customer could not shop and fees will be bound by tolerances Lenders are responsible for charges listed by their loan officers and the mortgage broker 21

22 Written List Additional disclosure may be added to the list stating that the originator is not endorsing the service providers Lenders may list their affiliate, but must distribute AfBA disclosure 22

23 Written List May separately identify the service of conducting the closing from title service on the written list. List the separate providers and amount. Combined amount must equal Block 4. 23

24 Example Block 4 = $1,000 Written List Closing Company A $150 Title agency A $850 24

25 Written List May not separate other services contained within title services such as notary, abstract, administrative or processing services. 25

26 GFE Page 3 Instructions 26

27 Which charges can increase 27

28 Tradeoff table 28

29 Shopping Chart 29

30 Changed Circumstances Acts of God, war, disaster or other emergency changed or inaccurate information provided by borrower after issuance of GFE (e.g. credit quality, loan amount, property value, or other information) 30

31 Changed Circumstances If circumstances changed affecting settlement costs or loan: provide revised GFE within 3 days revised GFE may reflect only the increased charges 31

32 Interest Rate: not locked If borrower does not lock interest rate within time period, a new GFE must be issued even if the interest rate does not change 32

33 Expired GFE If borrower does not express intent to proceed with the loan after 10 business days, or longer if specified by originator, the GFE is considered expired. 33

34 New Home Purchases If settlement is anticipated to be more than 60 days after GFE, originator may disclose on separate piece of paper that the GFE may be revised any time up to 60 days before settlement is anticipated. 34

35

36 HUD-1 Settlement Statement 36

37 Seller (or other) Paid Items all GFE charges; put in borrower s column on the HUD-1 credit to borrower from seller in Lines &Lines credit from party other than seller, must identify party giving credit on HUD-1 37

38 Seller credit example 38

39 HUD-1 Page 2 39

40 700s Example 40

41 Line 801 & 802: listed outside column Line 803: listed inside column 41

42 Lines 804 thru 807: charges in borrower s column 42

43 Lines : charges inside column 43

44 Line 1001: charges listed inside column Lines : charges listed outside column 44

45 1100s - Title service: definition Title services Means any service involved in the provision of title insurance 45

46 1100s - Title service Includes, but is not limited to - title examination & evaluation - preparation & issuance of commitment - preparation & issuance of policies - all administrative services & processing services required to perform these functions 46

47 1100s Example 47

48 1200 s: Inside the column charges 48

49 Fee category: 1300s 49

50 HUD-1, page 3 50

51 Comparison Chart 51

52 Charges That Cannot Increase 52

53 10% Tolerance 53

54 Charges That Can Change 54

55 Right-to-cure: tolerance Charges exceeding tolerance not a violation of RESPA Section 5 IF cured within 30 days after settlement 55

56 Loan Terms 56

57 Loan Terms 57

58 Loan Terms 58

59 Right-to-cure: errors Inadvertent or technical errors not a violation of RESPA Section 4 IF revised HUD-1 is provided within 30 days after settlement 59

60 Average Charge 60

61 Average Charge calculations based on specific class of transactions during a specific time period - not less than 30 days - not more than 6 months for a specific geographical area 61

62 Average Charge charge may not exceed average calculation charge may not exceed TOTAL price paid to 3 rd party provider settlement service providers must retain all documentation determining accuracy of pricing method for at least 3 years 62

63 Average Charge may not average on charges based on loan amount or property value (e.g. transfer taxes, interest charges, escrow reserves & all insurances including title insurance) 63

64 Red Flags 64

65 Red Flags Consumers may not be required to show intent to move forward to receive a GFE Consumers may not be required to present purchase contract in order to receive a GFE What if consumer does not receive GFE within 3 days? 65

66 Red Flags Worksheet in lieu of GFE when loan originator has information that constitutes an application Loan originator giving worksheets on refinances Altered GFE Form Inappropriate itemization on GFE (especially Block 1 items these should not be itemized in Blocks 3 or 6) If the LO charges for the credit report prior to issuing GFE, is the charge for the credit report in excess of the cost of credit report 66

67 Red Flags Failure to disclose owner s title on purchase transaction GFE Failure to issue written list (all required services subject to tolerance!) Affiliate in Block 3 (except credit report, appraiser) Failure to issue Affiliated Business Disclosure Form before or with issuance of written list (if affiliate is on written list) 67

68 Red Flags Changed Circumstances review documents to confirm the change and that unrelated costs did not increase New GFE based on Borrower Requested Change check documentation of borrower s request! Increases to Block 1 on a revised GFE (allowed only in very limited circumstances) Increase to Block 1 solely due to the loan going from float to lock 68

69 Red Flags If a service is listed on GFE but was not purchased (usually Owner s title), nothing should be on HUD-1, page 2 or page 3. Loan originators receipt of draft HUD-1 does not, in and of itself, constitute a changed circumstance allowing for the issuance of a revised GFE. 69

70 Red Flags 800 Series itemization (unless required by state law or government loan program) 1100 Series itemization (unless required by state law, government loan program or performed by third party) 70

71 Red Flags Documentation to support average charge Remember to show tolerance cures on amended HUD-1 Tolerance violations without evidence of cure! Is the charge to the consumer for the credit report higher than the amount (or average charge) paid by the loan originator for the credit report? 71

72 Department of Housing and Urban Development Office of RESPA & Interstate Land Sales th Street SW, Room 9154 Washington DC (202) [email protected] 72

73 FDIC KC Regional Banker Conference Call RESPA Violations Forward Looking Supervision With a Glance Back February 8, 2011 Brad Havran, Cedar Rapids Field Office Supervisor Mark Hobert, Cedar Rapids Compliance Examiner

74 RESPA Compliance Management Systems (CMS) Management Oversight Compliance Programs Policies and Procedures Training Monitoring Response to Complaints Audit

75 RESPA Examination results Jan. 1, 2010 to Jan. 12, 2011 Region Number of Examinations Number with violations % of Banks cited with violations Nationwide 1, Kansas City Region

76 RESPA Most Common Violations Cited in Jan. 1, 2010 to Jan. 12, 2011 Nationwide Kansas City Region Bank did not complete HUD-1 or 1A according to Appendix A of RESPA Bank did not complete GFE according to Appendix C of RESPA GFE must be available at least 10 business days after the GFE is provided GFE must be provided within 3 business days of the date of application 53 15

77 RESPA Most Common Reimbursable Violations Cited in Jan. 1, 2010 to Jan. 12, 2011 Charges at settlement exceeded amounts disclosed in GFE for items subject to zero tolerance Nationwide Kansas City Region 6 0 Charges at settlement exceeded amounts disclosed in GFE by more than 10% tolerance allowed for those items. 3 1 Charges at settlement were more than disclosed on GFE without a new GFE issued 2 2 Other reasons; charges not reasonably estimated on GFE 2 0

78 RESPA Questions? at Please start the subject line with the word Question and include your name, bank name, and location (city and state) in the text section. You may also ask a live question at the conclusion of the presentation using instructions provided by the operator. References: 1. HUD RESPA FINAL RULE HUD-1 instructions pages GFE instructions pages FREQUENTLY ASKED QUESTIONS RESPA ROUNDUP 2. FEDERAL RESERVE 3. FDIC

RESPA Training Good Faith Estimate (GFE) & Settlement Statement HUD-1

& Settlement Statement HUD-1") RESPA Training Good Faith Estimate (GFE) & Settlement Statement HUD-1 2013 Rushmore Loan Management Services LLC. All Rights Reserved. 1 REAL ESTATE SETTLEMENT PROCEDURES ACT RESPA NEW RULE TIMELINE NOVEMBER

RESPA Training Good Faith Estimate (GFE) & Settlement Statement HUD-1 2013 Rushmore Loan Management Services LLC. All Rights Reserved. 1 REAL ESTATE SETTLEMENT PROCEDURES ACT RESPA NEW RULE TIMELINE NOVEMBER

New RESPA Rule FAQs. (New items are in bold)

") New RESPA Rule FAQs (New items are in bold) The following FAQs were revised to provide further clarification: GFE General, #33 GFE Important dates, #5 GFE - Block 1, #7 and #8 Sections 4 and 5 Right to

New RESPA Rule FAQs (New items are in bold) The following FAQs were revised to provide further clarification: GFE General, #33 GFE Important dates, #5 GFE - Block 1, #7 and #8 Sections 4 and 5 Right to

Reference for Closing Agents To Provide to Lender Customers. Excerpts from RESPA Rules and FAQ s

Reference for Closing Agents To Provide to Lender Customers Excerpts from RESPA Rules and FAQ s This Reference document may assist closing agents as it includes frequently asked questions related to compliant

Reference for Closing Agents To Provide to Lender Customers Excerpts from RESPA Rules and FAQ s This Reference document may assist closing agents as it includes frequently asked questions related to compliant

New RESPA Rule FAQs. (New items are in bold)

") New RESPA Rule FAQs (New items are in bold) Table of Contents General... 3 GFE... 5 GFE General... 5 GFE Seller paid items... 11 GFE Expiration... 12 GFE Denial... 12 GFE Written list of providers... 12

New RESPA Rule FAQs (New items are in bold) Table of Contents General... 3 GFE... 5 GFE General... 5 GFE Seller paid items... 11 GFE Expiration... 12 GFE Denial... 12 GFE Written list of providers... 12

Completing the New HUD-1 Settlement Statement

Completing the New HUD-1 Settlement Statement The new HUD-1 Settlement Statement ( HUD ) is designed to correlate closely to the new GFE, allowing borrowers to see how the estimate settlement costs disclosed

Completing the New HUD-1 Settlement Statement The new HUD-1 Settlement Statement ( HUD ) is designed to correlate closely to the new GFE, allowing borrowers to see how the estimate settlement costs disclosed

The New RESPA Closing Process

The New RESPA Closing Process Presented by Thomas G. Cullen Managing Attorney Wisconsin Operations Attorneys Title Guaranty Fund, Inc. Roman Reynolds Member Services Representative Member Sales and Support

The New RESPA Closing Process Presented by Thomas G. Cullen Managing Attorney Wisconsin Operations Attorneys Title Guaranty Fund, Inc. Roman Reynolds Member Services Representative Member Sales and Support

Summary of RESPA Rules... 1 Summary of Changes... 2 Required Use... 2 Average Cost Pricing... 3 Calculating the Average Charge...

Summary of RESPA Rules... 1 Summary of Changes... 2 Required Use... 2 Average Cost Pricing... 3 Calculating the Average Charge... 4 Good Faith Estimate... 5 Curing Tolerance Violations... 9 Lenders Disclosure

Summary of RESPA Rules... 1 Summary of Changes... 2 Required Use... 2 Average Cost Pricing... 3 Calculating the Average Charge... 4 Good Faith Estimate... 5 Curing Tolerance Violations... 9 Lenders Disclosure

7 business days after loan estimate delivery is the waiting period for consummation (loan closing) after the Loan Estimate Delivery

after the Loan Estimate Delivery") TRID INFORMATION Delivery of the Loan Estimate The Loan Estimate must be placed in the mail or delivered no later than 3 business days after TRID application is submitted. Helpful Hint: Business days for

TRID INFORMATION Delivery of the Loan Estimate The Loan Estimate must be placed in the mail or delivered no later than 3 business days after TRID application is submitted. Helpful Hint: Business days for

The Good Faith Estimate

Module 3 Module 3 The Good Faith Estimate Explanation: This pdf is only a copy of the module slides. To proceed through the course, you must read and click through each slide. The Good Faith Estimates

Module 3 Module 3 The Good Faith Estimate Explanation: This pdf is only a copy of the module slides. To proceed through the course, you must read and click through each slide. The Good Faith Estimates

Disclosures: Providing the consumer information concerning the condition and other aspects of the property or the loan product.

GFE INTRODUCTION: Effective January 1, 2010, HUD restructured the Good Faith Estimate ( GFE ) and HUD-1 forms to facilitate comparison shopping and improve their connection. Because of the new links between

GFE INTRODUCTION: Effective January 1, 2010, HUD restructured the Good Faith Estimate ( GFE ) and HUD-1 forms to facilitate comparison shopping and improve their connection. Because of the new links between

Appendix B: Good Faith Estimate

Appendix B: Good Faith Estimate Good Faith Estimate The Real Estate Settlement Procedures Act, commonly referred to as RESPA, requires that within three business days of receipt of the loan application,

Appendix B: Good Faith Estimate Good Faith Estimate The Real Estate Settlement Procedures Act, commonly referred to as RESPA, requires that within three business days of receipt of the loan application,

TRID Frequently Asked Questions

TRID Frequently Asked Questions Q: What is TRID? A: TRID is an acronym for the TILA-RESPA Integrated Disclosure rule. It is a rule mandated by the Consumer Financial Protection Bureau as part of the Dodd-Frank

TRID Frequently Asked Questions Q: What is TRID? A: TRID is an acronym for the TILA-RESPA Integrated Disclosure rule. It is a rule mandated by the Consumer Financial Protection Bureau as part of the Dodd-Frank

FAQs About RESPA for Industry

FAQs About RESPA for Industry 1. What kinds of transactions are covered under RESPA? Transactions involving a federally related mortgage loan, which includes most loans secured by a lien (first or subordinate

FAQs About RESPA for Industry 1. What kinds of transactions are covered under RESPA? Transactions involving a federally related mortgage loan, which includes most loans secured by a lien (first or subordinate

HUD s New RESPA Rules for HUD-1: With Q & A

HUD s New RESPA Rules for HUD-1: With Q & A Presented by: Paul McNutt, Jr. General Counsel Title Resources Guaranty Company The Secretary of HUD announced on Nov. 12, 2008, that effective on January 1,

HUD s New RESPA Rules for HUD-1: With Q & A Presented by: Paul McNutt, Jr. General Counsel Title Resources Guaranty Company The Secretary of HUD announced on Nov. 12, 2008, that effective on January 1,

TRID Settlement Service Provider List (SSP List)

") TRID Settlement Service Provider List (SSP List) Overview The rule permits lenders/mortgage brokers to provide borrowers the ability to select third party service providers. By doing so could favorably

TRID Settlement Service Provider List (SSP List) Overview The rule permits lenders/mortgage brokers to provide borrowers the ability to select third party service providers. By doing so could favorably

The Smart Consumer s Guide to the New Good Faith Estimate

The Smart Consumer s Guide to the New Good Faith Estimate Practical insights on how to use the new GFE and HUD-1 to save money on closing costs for a purchase or refinance. Copyright 2010 ENTITLE DIRECT

The Smart Consumer s Guide to the New Good Faith Estimate Practical insights on how to use the new GFE and HUD-1 to save money on closing costs for a purchase or refinance. Copyright 2010 ENTITLE DIRECT

HUD-1. GFE vs. HUD-1: HUD-1 Introduction:

HUD-1 GFE vs. HUD-1: The new HUD-1 Settlement Statement (the HUD-1 ) is designed to allow the borrower to compare the document with the Good Faith Estimate (the GFE ) received before closing, including

HUD-1 GFE vs. HUD-1: The new HUD-1 Settlement Statement (the HUD-1 ) is designed to allow the borrower to compare the document with the Good Faith Estimate (the GFE ) received before closing, including

CFPB THE NEW DISCLOSURE FORMS AND REQUIREMENTS BE READY!!

CFPB THE NEW DISCLOSURE FORMS AND REQUIREMENTS BE READY!! CELIA C. FLOWERS FLOWERS DAVIS, P.L.L.C. and EAST TEXAS TITLE COMPANY Tyler, Texas 75701 TILA and RESPA History 2012 TEXAS LAND TITLE INSTITUTE

CFPB THE NEW DISCLOSURE FORMS AND REQUIREMENTS BE READY!! CELIA C. FLOWERS FLOWERS DAVIS, P.L.L.C. and EAST TEXAS TITLE COMPANY Tyler, Texas 75701 TILA and RESPA History 2012 TEXAS LAND TITLE INSTITUTE

ADVISORY MEMORANDUM KATHY BURNS, DIRECTOR OF HOMEOWNERSHIP COMPLIANCE DOCUMENTATION REQUIREMENTS

ADVISORY MEMORANDUM TO: FROM: ALL MASSHOUSING LENDERS KATHY BURNS, DIRECTOR OF HOMEOWNERSHIP DATE: NOVEMBER 15, 2010 RE: COMPLIANCE DOCUMENTATION REQUIREMENTS The purpose of this Advisory is to provide

ADVISORY MEMORANDUM TO: FROM: ALL MASSHOUSING LENDERS KATHY BURNS, DIRECTOR OF HOMEOWNERSHIP DATE: NOVEMBER 15, 2010 RE: COMPLIANCE DOCUMENTATION REQUIREMENTS The purpose of this Advisory is to provide

Changes to Mortgage Loan Closing Process

Changes to Mortgage Loan Closing Process 2015 Iowa Title Guaranty Settlement Conference Presented by: Ronette Schlatter, CRCM 1 Background Dodd-Frank Wall Street Reform and Consumer Protection Act (DFA)

Changes to Mortgage Loan Closing Process 2015 Iowa Title Guaranty Settlement Conference Presented by: Ronette Schlatter, CRCM 1 Background Dodd-Frank Wall Street Reform and Consumer Protection Act (DFA)

TILA-RESPA Integrated Disclosure Rule

TILA-RESPA Integrated Disclosure Rule May 13, 2015 Joseph J. Reilly Partner Benjamin K. Olson Partner 1 Key Changes Effective for applications received by the creditor or mortgage broker on or after August

TILA-RESPA Integrated Disclosure Rule May 13, 2015 Joseph J. Reilly Partner Benjamin K. Olson Partner 1 Key Changes Effective for applications received by the creditor or mortgage broker on or after August

New GFE/HUD-1 Mortgage Brokers Really Need to Know This Stuff

United Wholesale Mortgage 2009 RESPA Webinar New GFE/HUD-1 Mortgage Brokers Really Need to Know This Stuff November 18, 2009 Phillip L. Schulman, Esq. [email protected] 202-778-9027 DC-1381985

United Wholesale Mortgage 2009 RESPA Webinar New GFE/HUD-1 Mortgage Brokers Really Need to Know This Stuff November 18, 2009 Phillip L. Schulman, Esq. [email protected] 202-778-9027 DC-1381985

Overview The Regulation The Loan Estimate (LE) The Closing Disclosure (CD) Loan Estimate (LE) Application Date LE Responsibility

The Closing Disclosure (CD) Loan Estimate (LE) Application Date LE Responsibility") To support your preparation efforts when implementing the TILA-RESPA Integrated Disclosure (TRID) rule effective for applications dated on or after October 3, 2015, we have created this Helpful Tips for

To support your preparation efforts when implementing the TILA-RESPA Integrated Disclosure (TRID) rule effective for applications dated on or after October 3, 2015, we have created this Helpful Tips for

40 Technology Parkway South, Suite 202 Norcross, Georgia 30092-2906 www.franzen-salzano.com. November 12, 2008

Jennifer L. Dozier Telephone: 770-248-2885, ext. 241 Facsimile: 770-248-2883 e-mail: [email protected] 40 Technology Parkway South, Suite 202 Norcross, Georgia 30092-2906 www.franzen-salzano.com

Jennifer L. Dozier Telephone: 770-248-2885, ext. 241 Facsimile: 770-248-2883 e-mail: [email protected] 40 Technology Parkway South, Suite 202 Norcross, Georgia 30092-2906 www.franzen-salzano.com

TILA-RESPA Integrated Disclosure (TRID) Correspondent Division. Overview. Loan Estimate (LE) Key points. Topic The Regulation

Correspondent Division. Overview. Loan Estimate (LE) Key points. Topic The Regulation") Overview The Regulation The Consumer Financial Protection Bureau (CFPB) issued a final rule amending Regulation Z (Truth in Lending Act) and Regulation X (Real Estate Settlement Procedures Act) to integrate

Overview The Regulation The Consumer Financial Protection Bureau (CFPB) issued a final rule amending Regulation Z (Truth in Lending Act) and Regulation X (Real Estate Settlement Procedures Act) to integrate

MORTGAGE BANKERS ASSOCIATION OF THE GENESEE REGION MAY 21, 2015. Presenter: Bonnie S. Nachamie

MORTGAGE BANKERS ASSOCIATION OF THE GENESEE REGION MAY 21, 2015 Presenter: Bonnie S. Nachamie The Closing Disclosure ( CD ) is the new form that amends, enhances and replaces the Final TIL and HUD-1 The

MORTGAGE BANKERS ASSOCIATION OF THE GENESEE REGION MAY 21, 2015 Presenter: Bonnie S. Nachamie The Closing Disclosure ( CD ) is the new form that amends, enhances and replaces the Final TIL and HUD-1 The

CFPB Consumer Laws and Regulations

Real Estate Settlement Procedures Act 1 The Real Estate Settlement Procedures Act of 1974 () (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders, mortgage brokers,

Real Estate Settlement Procedures Act 1 The Real Estate Settlement Procedures Act of 1974 () (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders, mortgage brokers,

Regulation X Real Estate Settlement Procedures Act

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 (RESPA) (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders,

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 (RESPA) (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders,

First Mortgage Documents User Guide 139

HUD 1 Settlement Statement Line instructions General Instructions Information and amounts may be filled in by typewriter, hand printing, computer printing, or any other method producing clear and legible

HUD 1 Settlement Statement Line instructions General Instructions Information and amounts may be filled in by typewriter, hand printing, computer printing, or any other method producing clear and legible

Understanding the Good Faith Estimate.

Understanding the Good Faith Estimate. OLYMPI TITLE & ESCROW 401 EST LS OLS BLVD, STE 1400 FORT LUDERDLE, FL 33301 PHONE: (954) 695-7598 The Good Faith Estimate (GFE) is a required disclosure that provides

Understanding the Good Faith Estimate. OLYMPI TITLE & ESCROW 401 EST LS OLS BLVD, STE 1400 FORT LUDERDLE, FL 33301 PHONE: (954) 695-7598 The Good Faith Estimate (GFE) is a required disclosure that provides

Know Before You Owe. TILA-RESPA Integrated Disclosure (TRID) Rule

Rule") Know Before You Owe TILA-RESPA Integrated Disclosure (TRID) Rule Background of CFPB The Consumer Financial Protection Bureau (CFPB) was established in 2010 under the Dodd-Frank Act Directed to publish

Know Before You Owe TILA-RESPA Integrated Disclosure (TRID) Rule Background of CFPB The Consumer Financial Protection Bureau (CFPB) was established in 2010 under the Dodd-Frank Act Directed to publish

Regulation X Real Estate Settlement Procedures Act

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 (RESPA) (12 U.S.C. 2601 et seq.) (the act) became effective on June 20, 1975. The act requires lenders,

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 (RESPA) (12 U.S.C. 2601 et seq.) (the act) became effective on June 20, 1975. The act requires lenders,

APPENDIX A TO PART 3500 INSTRUCTIONS FOR COMPLETING HUD-1 AND HUD-1A SETTLEMENT STATEMENTS; SAMPLE HUD-1 AND HUD-1A STATEMENTS

APPENDIX A TO PART 3500 INSTRUCTIONS FOR COMPLETING HUD-1 AND HUD-1A SETTLEMENT STATEMENTS; SAMPLE HUD-1 AND HUD-1A STATEMENTS The following are instructions for completing the HUD-1 settlement statement,

APPENDIX A TO PART 3500 INSTRUCTIONS FOR COMPLETING HUD-1 AND HUD-1A SETTLEMENT STATEMENTS; SAMPLE HUD-1 AND HUD-1A STATEMENTS The following are instructions for completing the HUD-1 settlement statement,

TRID Overview. Provided by Primary Capital Mortgage. Presented by Stacie Weider, Training Manager

Provided by Primary Capital Mortgage Presented by Stacie Weider, Training Manager What is TRID? TILA RESPA Integrated Disclosure Rule, which is effective October, 3, 2015. History Notes The Goal To provide

Provided by Primary Capital Mortgage Presented by Stacie Weider, Training Manager What is TRID? TILA RESPA Integrated Disclosure Rule, which is effective October, 3, 2015. History Notes The Goal To provide

FAQs About RESPA for Industry

FAQs About RESPA for Industry Scope of RESPA 1. What kinds of transactions are covered under RESPA? Transactions involving a federally related mortgage loan, which includes most loans secured by a lien

FAQs About RESPA for Industry Scope of RESPA 1. What kinds of transactions are covered under RESPA? Transactions involving a federally related mortgage loan, which includes most loans secured by a lien

10 LOAN CLOSING. [email protected]

10 LOAN CLOSING COMPLIANCE APPROVAL Once the Commission approves the Mortgage Loan for compliance, the Mortgage Lender may close the loan. CLOSING DOCUMENTS [email protected] In general, the Mortgage

10 LOAN CLOSING COMPLIANCE APPROVAL Once the Commission approves the Mortgage Loan for compliance, the Mortgage Lender may close the loan. CLOSING DOCUMENTS [email protected] In general, the Mortgage

Good Faith Estimate (GFE)

") OMB Approval No. 2502-0265 Good Faith Estimate (GFE) Name of Originator Originator Address Borrower Property Address Originator Phone Number Originator Email Date of GFE Purpose Shopping for your loan

OMB Approval No. 2502-0265 Good Faith Estimate (GFE) Name of Originator Originator Address Borrower Property Address Originator Phone Number Originator Email Date of GFE Purpose Shopping for your loan

2015 Fidelity National Title Group

Five Things You Need to Know Before August 2015 WHAT IS THE CFPB? THE NEW LINGO Dodd-Frank Act --Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 CFPB Consumer Financial Protection Bureau

Five Things You Need to Know Before August 2015 WHAT IS THE CFPB? THE NEW LINGO Dodd-Frank Act --Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 CFPB Consumer Financial Protection Bureau

A New Era in Closings CFPB s Final Rule for Integrated Mortgage Disclosures. Michelle L. Korsmo Chief Executive Officer Steven Gottheim Counsel

A New Era in Closings CFPB s Final Rule for Integrated Mortgage Disclosures Michelle L. Korsmo Chief Executive Officer Steven Gottheim Counsel Agenda Basics: Why We re Here Final Rule The New Forms Evaluating

A New Era in Closings CFPB s Final Rule for Integrated Mortgage Disclosures Michelle L. Korsmo Chief Executive Officer Steven Gottheim Counsel Agenda Basics: Why We re Here Final Rule The New Forms Evaluating

CFPB Consumer Laws and Regulations

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 () (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders, mortgage

Regulation X Real Estate Settlement Procedures Act The Real Estate Settlement Procedures Act of 1974 () (12 U.S.C. 2601 et seq.) (the Act) became effective on June 20, 1975. The Act requires lenders, mortgage

CFPB Integrated Mortgage Disclosures

CFPB Integrated Mortgage Disclosures Today s Goal To help you not only understand the rule changes, but make sure you have the tools, resources and support to take action to implement in your credit union

CFPB Integrated Mortgage Disclosures Today s Goal To help you not only understand the rule changes, but make sure you have the tools, resources and support to take action to implement in your credit union

Broker Compensation Overview

Broker Compensation Overview Paid Pid by either the Borrower or the Lender, but not both. Lender paid compensation is: Calculated as a percentage of the loan amount according to the Compensation Agreement

Broker Compensation Overview Paid Pid by either the Borrower or the Lender, but not both. Lender paid compensation is: Calculated as a percentage of the loan amount according to the Compensation Agreement

FRESH. Agenda. Credit Union Integrated Mortgage Disclosures Are you Prepared?

MCUL & Affiliates 2015 Annual Convention and Exposition Credit Union Integrated Mortgage Disclosures Are you Prepared? Glory LeDu Thursday, June 4, 2015 2:00 p.m. Sponsored by: FRESH Ideas to Reinvent

MCUL & Affiliates 2015 Annual Convention and Exposition Credit Union Integrated Mortgage Disclosures Are you Prepared? Glory LeDu Thursday, June 4, 2015 2:00 p.m. Sponsored by: FRESH Ideas to Reinvent

How To Write A Disclosure Form

Office of Consumer Protection Truth-In-Lending Real Estate Settlement Procedures Act Integrated Disclosures Webinar February 11, 2015 The information contained in this presentation is for informational

Office of Consumer Protection Truth-In-Lending Real Estate Settlement Procedures Act Integrated Disclosures Webinar February 11, 2015 The information contained in this presentation is for informational

TILA-RESPA Integrated Disclosure Rule * January 21, 2015

TILA-RESPA Integrated Disclosure Rule * January 21, 2015 Presented by David Kantor Stinson Leonard Street LLP [email protected] 612-335-1620 1. Effective Date. The new Integrated Disclosures

TILA-RESPA Integrated Disclosure Rule * January 21, 2015 Presented by David Kantor Stinson Leonard Street LLP [email protected] 612-335-1620 1. Effective Date. The new Integrated Disclosures

RESPA REFORM 2010 THE NEW GOOD FAITH ESTIMATE

2010-2011 UPDATE COURSE SECTION THREE RESPA REFORM 2010 THE NEW GOOD FAITH ESTIMATE AND HUD-1 FORMS Outline: Real Estate Settlement Procedures Act RESPA s Purpose Applicability of Law Reforms Implemented

2010-2011 UPDATE COURSE SECTION THREE RESPA REFORM 2010 THE NEW GOOD FAITH ESTIMATE AND HUD-1 FORMS Outline: Real Estate Settlement Procedures Act RESPA s Purpose Applicability of Law Reforms Implemented

HUD-1 CHANGES. HUD-1 form. www.rgtc.com

2010 HUD-1 form Highlights New HUD-1 (HUD-1 ver. 2010) is required on all RESPA regulated transactions (residential refinances, residential purchases) beginning 1/1/2010. New HUD-1 adds a new page (page

2010 HUD-1 form Highlights New HUD-1 (HUD-1 ver. 2010) is required on all RESPA regulated transactions (residential refinances, residential purchases) beginning 1/1/2010. New HUD-1 adds a new page (page

General Resources CFPB Resources ALTA Best Practices Closing Insight Notaries Business & Commercial Loans Foreign Consumers

Remember, a knowing or reckless violation of TRID, even if done under instructions from the lender, may result in penalties of up to $1 million a day per violation against the individual settlement agent.

Remember, a knowing or reckless violation of TRID, even if done under instructions from the lender, may result in penalties of up to $1 million a day per violation against the individual settlement agent.

Answer: ppddocs.com we don t endorse this site or this product, it is just a site we used to input examples for the webinar

BAI Learning & Development Webinar Q&A TILA-RESPA Integration Part 1 A New Way to Disclose 1. How should we handle Lender Paid Fees? Since we have to send the Loan Estimate 3 days after application, we

BAI Learning & Development Webinar Q&A TILA-RESPA Integration Part 1 A New Way to Disclose 1. How should we handle Lender Paid Fees? Since we have to send the Loan Estimate 3 days after application, we

CLARIFICATION OF MAJOR CHANGES. Integrated Mortgage Disclosures

CLARIFICATION OF MAJOR CHANGES Integrated Mortgage Disclosures One of the mortgage industry s most anticipated provisions of the Dodd-Frank Act has been the integration of the Truth-in-Lending Act (TILA)

CLARIFICATION OF MAJOR CHANGES Integrated Mortgage Disclosures One of the mortgage industry s most anticipated provisions of the Dodd-Frank Act has been the integration of the Truth-in-Lending Act (TILA)

TRID CHECKLIST. RETAIL and WHOLESALE: STAFF and SALES FORCE TECHNICAL TRAINING

TRAINING STAFF and SALES FORCE TECHNICAL TRAINING Prepare training materials to define TRID Business day Total interest percentage 6 items of an Application (removal of 7th catch all item) Loan Estimate

TRAINING STAFF and SALES FORCE TECHNICAL TRAINING Prepare training materials to define TRID Business day Total interest percentage 6 items of an Application (removal of 7th catch all item) Loan Estimate

January 20, 2015 Updated Changes:

Get Ready! Get Set! August 1, 2015 is Around the Corner THE COMBINED TILA AND RESPA MORTGAGE DISCLOSURES (Memo Updated on 1/27/15 to include the changes below) As most of you are probably aware, a major

Get Ready! Get Set! August 1, 2015 is Around the Corner THE COMBINED TILA AND RESPA MORTGAGE DISCLOSURES (Memo Updated on 1/27/15 to include the changes below) As most of you are probably aware, a major

TILA RESPA Procedural Impacts Are You Ready? Presenters. CUNA Mutual Group 2015 All rights reserved. 1. July 7, 2015

Presented by: TILA RESPA Procedural Impacts Presenters Jon Bundy Regulatory Compliance Manager CUNA Mutual Group 608-665-7101 [email protected] Theresa Reinke LOANLINER Compliance Consultant

Presented by: TILA RESPA Procedural Impacts Presenters Jon Bundy Regulatory Compliance Manager CUNA Mutual Group 608-665-7101 [email protected] Theresa Reinke LOANLINER Compliance Consultant

TRID Quick Reference Guide

TRID General Rules and Definitions New Required Disclosures Loan Estimate (LE) replaces the GFE and Initial TIL Closing Disclosure (CD) replaces the Final TIL and HUD-1 Home Loan Toolkit replaces the HUD

TRID General Rules and Definitions New Required Disclosures Loan Estimate (LE) replaces the GFE and Initial TIL Closing Disclosure (CD) replaces the Final TIL and HUD-1 Home Loan Toolkit replaces the HUD

TILA RESPA Integrated Disclosures. On October 3 rd, life as we know it will change forever. One of the new forms is.

TILA RESPA Integrated Disclosures The Loan Estimate and Miscellaneous Requirements Lynne Murphy Breen, Esquire Sue Ellen Rogal, Esquire September 16, 2015 On October 3 rd, life as we know it will change

TILA RESPA Integrated Disclosures The Loan Estimate and Miscellaneous Requirements Lynne Murphy Breen, Esquire Sue Ellen Rogal, Esquire September 16, 2015 On October 3 rd, life as we know it will change

HUD-1 Page 1. All of these fields should be complete.

Final HUD 1 The requirements for accurately completing the HUD-1 Settlement Statement are published based on the rules set forth by HUD, RESPA and Regulation X. The information must be both accurate and

Final HUD 1 The requirements for accurately completing the HUD-1 Settlement Statement are published based on the rules set forth by HUD, RESPA and Regulation X. The information must be both accurate and

Please stand by, the presentation will begin shortly. Your phones have been muted. If you re using the speakers on your PC you don t need to call in.

Please stand by, the presentation will begin shortly. Your phones have been muted. If you re using the speakers on your PC you don t need to call in. While you are waiting, you may download the presentation

Please stand by, the presentation will begin shortly. Your phones have been muted. If you re using the speakers on your PC you don t need to call in. While you are waiting, you may download the presentation

TILA-RESPA Integrated Disclosure Rule FAQs for Wholesale Brokers

TILA-RESPA Integrated Disclosure Rule FAQs for Wholesale Brokers DEFINITIONS AND ACRONYMS TRID: TILA-RESPA Integrated Disclosure Know Before You Owe Rule, text of the rule and more information available

TILA-RESPA Integrated Disclosure Rule FAQs for Wholesale Brokers DEFINITIONS AND ACRONYMS TRID: TILA-RESPA Integrated Disclosure Know Before You Owe Rule, text of the rule and more information available

How To Understand The Veteran Loan Policy

Chapter 8. Borrower Fees and Charges and the VA Funding Fee Overview In this Chapter This chapter contains the following topics. Topic Topic Name See Page 1 VA Policy on Fees and Charges Paid by the Veteran-Borrower

Chapter 8. Borrower Fees and Charges and the VA Funding Fee Overview In this Chapter This chapter contains the following topics. Topic Topic Name See Page 1 VA Policy on Fees and Charges Paid by the Veteran-Borrower

CFPB and Lenders. A presentation on the Consumer Financial Protection Bureau and its impact on the lending industry

CFPB and Lenders A presentation on the Consumer Financial Protection Bureau and its impact on the lending industry What is the Consumer Financial Protection Bureau (CFPB)? Independent agency of the United

CFPB and Lenders A presentation on the Consumer Financial Protection Bureau and its impact on the lending industry What is the Consumer Financial Protection Bureau (CFPB)? Independent agency of the United

Updated January 2014. X = Required to Provide = Provide if applicable = Optional. At Loan Application (or within 3 business days)

") Sample List of Closed-End Residential Mortgage Disclosures Required to be Given to Consumers at Loan Application by Maryland Mortgage and Brokers Updated January 2014 Prepared by Marjorie A. Corwin, Esquire

Sample List of Closed-End Residential Mortgage Disclosures Required to be Given to Consumers at Loan Application by Maryland Mortgage and Brokers Updated January 2014 Prepared by Marjorie A. Corwin, Esquire

PART 2: THE LOAN ESTIMATE. Integrated Disclosures Rule Effective August 1, 2015

PART 2: THE LOAN ESTIMATE Integrated Disclosures Rule Effective August 1, 2015 1 Thank you for your time today! Integrated Disclosures Webinar Series brought to you by HomeBridge Wholesale Visit: www.homebridgewholesale.com

PART 2: THE LOAN ESTIMATE Integrated Disclosures Rule Effective August 1, 2015 1 Thank you for your time today! Integrated Disclosures Webinar Series brought to you by HomeBridge Wholesale Visit: www.homebridgewholesale.com

EXPLANATION OF THE HUD-1 Settlement Statement

EXPLANATION OF THE HUD-1 Settlement Statement The Settlement Statement is the financial picture of the closing. All money deposited into the escrow account and the disbursals out of the escrow account

EXPLANATION OF THE HUD-1 Settlement Statement The Settlement Statement is the financial picture of the closing. All money deposited into the escrow account and the disbursals out of the escrow account

TRID In the Weeds. Article by Alice Alvey January 2015

TRID In the Weeds Article by Alice Alvey January 2015 TRID BY ALICE ALVEY Alice Alvey It s not easy to see into the weeds of this regulation by attending a few webinars. It takes hundreds of man-hours

TRID In the Weeds Article by Alice Alvey January 2015 TRID BY ALICE ALVEY Alice Alvey It s not easy to see into the weeds of this regulation by attending a few webinars. It takes hundreds of man-hours

When do I have to start following the TILA-RESPA rule and using the new Integrated Disclosures?

............................................................................................. Overview of the TILA-RESPA Rule.............................................................................................

............................................................................................. Overview of the TILA-RESPA Rule.............................................................................................

Guide to Completing the Loan Estimate The following list highlights requirements needed to complete each section of the Loan Estimate.

Guide to Completing the Loan Estimate The following list highlights requirements needed to complete each section of the Loan Estimate. General Information Page 1 Date Issued Date the LE is mailed or delivered

Guide to Completing the Loan Estimate The following list highlights requirements needed to complete each section of the Loan Estimate. General Information Page 1 Date Issued Date the LE is mailed or delivered

Update on CFPB s TILA- RESPA Integrated Disclosure Rule

Update on CFPB s TILA- RESPA Integrated Disclosure Rule Mortgage Bankers Ruth A. Dillingham, Special Counsel First American Title Insurance Company This presentation is for informational purposes only

Update on CFPB s TILA- RESPA Integrated Disclosure Rule Mortgage Bankers Ruth A. Dillingham, Special Counsel First American Title Insurance Company This presentation is for informational purposes only

Shopping for your home loan. Settlement cost booklet

Shopping for your home loan Settlement cost booklet January 2014 This booklet was initially prepared by the U.S. Department of Housing and Urban Development. The Consumer Financial Protection Bureau (CFPB)

Shopping for your home loan Settlement cost booklet January 2014 This booklet was initially prepared by the U.S. Department of Housing and Urban Development. The Consumer Financial Protection Bureau (CFPB)

Changed Circumstance TRID Loan Estimate

1. What Are Changed Circumstances A changed circumstance is defined under RESPA as: An Act of God, war, disaster or other emergency New information regarding the consumer, the loan or the property Information

1. What Are Changed Circumstances A changed circumstance is defined under RESPA as: An Act of God, war, disaster or other emergency New information regarding the consumer, the loan or the property Information

TRID FAQs: You Asked. We Answered!

TRID FAQs: You Asked. We Answered! 1. Category Question Answer 2. Common Terms and LDW LDWholesale Definitions 3. Common Terms and Loan Estimate (LE) Replaces the GFE and TIL Definitions 4. Common Terms

TRID FAQs: You Asked. We Answered! 1. Category Question Answer 2. Common Terms and LDW LDWholesale Definitions 3. Common Terms and Loan Estimate (LE) Replaces the GFE and TIL Definitions 4. Common Terms

8 Hour MA SAFE Comprehensive: Key Topics for MLO s. Syllabus. Course Provider

8 Hour MA SAFE Comprehensive: Key for MLO s Course Provider Host Group Real Estate Academy 236 Huntington Avenue Suite #312 Boston, MA 02115 800-918-5240 www.hostgroup.us / www.hostgroupboston.com [email protected]

8 Hour MA SAFE Comprehensive: Key for MLO s Course Provider Host Group Real Estate Academy 236 Huntington Avenue Suite #312 Boston, MA 02115 800-918-5240 www.hostgroup.us / www.hostgroupboston.com [email protected]

1100 Section Title Services and Title Insurance The Comparison page (HUD Page 3) Item #4 / HUD page 2, line 1103

Item #4 / HUD page 2, line 1103") 1100 Section Title Services and Title Insurance The Comparison page (HUD Page 3) Item #4 / HUD page 2, line 1103 In general, the borrower pays for the loan policy. The sales contract or agreement determines

1100 Section Title Services and Title Insurance The Comparison page (HUD Page 3) Item #4 / HUD page 2, line 1103 In general, the borrower pays for the loan policy. The sales contract or agreement determines

Appendix C: HUD-1 Settlement Statement

Appendix C: HUD-1 Settlement Statement HUD-1 Settlement Statement The Settlement Statement, or HUD-1 Form, details the exact breakdown of all the money paid or received by both the buyer and the seller.

Appendix C: HUD-1 Settlement Statement HUD-1 Settlement Statement The Settlement Statement, or HUD-1 Form, details the exact breakdown of all the money paid or received by both the buyer and the seller.

VA Borrower Fees and Charges

VA Borrower Fees and OVERVIEW Purpose The VA home loan program involves a veteran s benefit. VA policy has evolved around the objective of helping the veteran to use his/her home loan benefit. Therefore,

VA Borrower Fees and OVERVIEW Purpose The VA home loan program involves a veteran s benefit. VA policy has evolved around the objective of helping the veteran to use his/her home loan benefit. Therefore,

CFPB Proposes New Mortgage Disclosure Rules

A DV I S O RY July 2012 On July 9, 2012, the Bureau of Consumer Financial Protection (CFPB) issued a proposed rule on mortgage disclosures (Proposed Rule) implementing requirements of the Dodd-Frank Wall

A DV I S O RY July 2012 On July 9, 2012, the Bureau of Consumer Financial Protection (CFPB) issued a proposed rule on mortgage disclosures (Proposed Rule) implementing requirements of the Dodd-Frank Wall

RESPA QUESTIONS and ANSWERS

What follows are unofficial answers to the questions received by the TLTA-IBAT Panel in connection with the two February Line by Line webinars. Thanks to everyone for sending in such great questions. Hopefully

What follows are unofficial answers to the questions received by the TLTA-IBAT Panel in connection with the two February Line by Line webinars. Thanks to everyone for sending in such great questions. Hopefully

Disclosure Process. 1 WSL:1241 Issued: 09/04/15

NYCB Gemstone Closing Disclosure Process 1 WSL:1241 Issued: 09/04/15 Items being covered today: Closing Disclosure Overview Gemstone Process Flow Overview Walkthroughs of the new modules in Gemstone The

NYCB Gemstone Closing Disclosure Process 1 WSL:1241 Issued: 09/04/15 Items being covered today: Closing Disclosure Overview Gemstone Process Flow Overview Walkthroughs of the new modules in Gemstone The

Colorado Housing and Finance Authority (CHFA) CHFA HomeAccess sm Second Mortgage Loan Instructions for Completion of Documents

CHFA HomeAccess sm Second Mortgage Loan Instructions for Completion of Documents") page 1 of 6 Colorado Housing and Finance Authority (CHFA) CHFA HomeAccess sm Second Mortgage Loan Instructions for Completion of Documents The Instructions below are provided to assist CHFA s Participating

page 1 of 6 Colorado Housing and Finance Authority (CHFA) CHFA HomeAccess sm Second Mortgage Loan Instructions for Completion of Documents The Instructions below are provided to assist CHFA s Participating

Understanding the CFPB s TILA-RESPA Integrated Disclosures. Marvin Stone SVP, Business Integration CFPB Program Manager Stewart Title Guaranty Corp.

Understanding the CFPB s TILA-RESPA Integrated Disclosures Marvin Stone SVP, Business Integration CFPB Program Manager Stewart Title Guaranty Corp. A Brief History. Truth-in-Lending Act (TILA) of 1968

Understanding the CFPB s TILA-RESPA Integrated Disclosures Marvin Stone SVP, Business Integration CFPB Program Manager Stewart Title Guaranty Corp. A Brief History. Truth-in-Lending Act (TILA) of 1968

RESPA Reform FAQs. Good Faith Estimate

RESPA Reform FAQs Good Faith Estimate Q. If a loan originator expects to receive compensation from the lender in the form of Yield Spread how is that disclosed on the new GFE? A. All broker fees and compensation

RESPA Reform FAQs Good Faith Estimate Q. If a loan originator expects to receive compensation from the lender in the form of Yield Spread how is that disclosed on the new GFE? A. All broker fees and compensation

VA Allowable Closing Costs

VA Allowable Closing Costs VA limits the closing costs that the veteran can pay to obtain a home loan. Strict adherence to the limitations on borrower paid fees and charges is required on all VA loans.

VA Allowable Closing Costs VA limits the closing costs that the veteran can pay to obtain a home loan. Strict adherence to the limitations on borrower paid fees and charges is required on all VA loans.

TILA-RESPA INTEGRATED DISCLOSURE RULE

TILA-RESPA INTEGRATED DISCLOSURE RULE Speakers: David Baghdady, Assoc. State Counsel/AVP, First American Title Ins. Co. Richard Hogan, Vice President and Associate General Counsel, CATIC Jeremy Potter,

TILA-RESPA INTEGRATED DISCLOSURE RULE Speakers: David Baghdady, Assoc. State Counsel/AVP, First American Title Ins. Co. Richard Hogan, Vice President and Associate General Counsel, CATIC Jeremy Potter,

Disclosure Specialist Responsibilities. Lock Procedures. Processor Responsibilities. Appraisal Ordering

FHA 203K Streamline - Policies & Procedures FHA 203K Streamline will now be underwritten and funded in house. These applications should be originated in Mortgage Builder under the FHA203K-SR program code.

FHA 203K Streamline - Policies & Procedures FHA 203K Streamline will now be underwritten and funded in house. These applications should be originated in Mortgage Builder under the FHA203K-SR program code.

PRMG is Ramping Up for the TILA RESPA Rule

PRMG is Ramping Up for the TILA RESPA Rule Paramount Residential Mortgage Group, Inc. (PRMG) is ramping up for the new TILA RESPA rule. Effective with applications taken on or after August 1, 2015, lenders

PRMG is Ramping Up for the TILA RESPA Rule Paramount Residential Mortgage Group, Inc. (PRMG) is ramping up for the new TILA RESPA rule. Effective with applications taken on or after August 1, 2015, lenders