What type of Record Book to use: Animal: student owns or leases animals to market, produce, or compete Business: student owns/operates a business or

|

|

|

- Moris Wiggins

- 8 years ago

- Views:

Transcription

1 What type of Record Book to use: Animal: student owns or leases animals to market, produce, or compete Business: student owns/operates a business or is in a Placement SAE Crop: student is growing a crop to market or consume Science: student plans to conduct a research trial or experiment

2 Yellow Pages Blue Pages Green Pages Salmon Pages Core Pages (white pages)

3 The animal book is designed for students who are operating an animal production enterprise. Only entrepreneurial SAEs should be recorded in this book. It is not designed to record placement data, as they are recorded in a business book. The business agreement should be completed before an SAE begins. It details all the terms of expenses, income, and responsibilities of the SAE. It should be reviewed by the supervising teacher and signed if appropriate. The student and parent should also review and sign the agreement. The other signature is added if equipment, land, or other inputs are rented, borrowed, or traded from a third-party. A new business agreement should be created each record book year and typically operate on a calendar year of January 1 to December 31.

4 The plans and goals/budget is designed for student s to set goals for animal production or profit from their enterprise. By creating this budget expenses can be estimated along with income to determine if the SAE will be a profitable business. It also allows for the proper resources to be identified. This page should be completed prior to the start of the SAE. This will allow for adjustments if needed. It is important to remember this is the expected income and expenses, not actual values.

5 The production records page are used for enterprises that are producing animals. It may not be used for all record books, as some animal enterprises may not be producing offspring. A gestation table should be used to estimate due dates. Death loss is also recorded on this page. Unfortunately death loss occurs in all of animal production and is important to record to track trends or possible disease issues. Note that piglets loss before weaning are not recorded due to large litter size and frequency at birth. A cause of death can be identified by a vet or speculated due to circumstance. Data from this box are transferred to page 4A, line 2.

6 The quantity of animal products is used to record milk, wool, eggs, offspring, and other marketable resources produced by animals. Note this does not include the marketing or sales of product. This page is designed as a checks and balances table. A caption should be placed in the product category above to identify what is being produced. For example if milk was the product the student could record pounds of milk, protein, and fat. The production and returns table is used to calculate totals of animals produced. These totals are used in the final evaluation of the enterprise to determine if growth and profit occurred within a record book year. Note that student s share is calculated. This value is identified in the business agreement.

7 The record of experiences serves as a type of journal of the enterprise. It can be as detailed as daily entries to as vague as monthly entries. The important aspect of this page is to record the number of hours worked on the enterprise. Note that three categories are available for hour entry: unpaid, paid, and other. Unpaid hours work will typically have the most entries as this is the hours worked by the student operating the enterprise. They should not count their hours as paid. Paid hours are recorded in two locations, on this page, and on the expenses page 11A. Paid hours must be recorded as an expense to the enterprise. Examples would including hiring a friend to assist cleaning pens or ear tagging offspring. Other hours worked are recorded but do not transfer to the total hours dedicated to the enterprise. Examples of other hours would include attending a seminar on rotational grazing or a visit by the supervising teacher.

8 A continuation of the data entries as found on the previous page. Note that extra space is supplied so that detailed records can be recorded through out the record book year. Totals transfer for each month should be placed on page 7A.

9 The wage/labor summary is designed to record monthly totals of labor dedicated to the enterprise. In most cases in animal enterprises the employer will be self and unpaid hours worked. Therefore no gross earnings, deductions, or net earnings will be recorded. These monthly totals are important to record as the data is utilized in the State and American Degree application. Income from the enterprise should be entered on the receipt page. Income from non-enterprise sources should be entered on core page 1-2. One common mistake made on this page is students using it in a placement book. While it does allow for the recording of income with deductions, it is not the proper format. A business book is used for ALL placement SAEs.

10 The same data entries as the previous page. Note that extra space is supplied so that detailed records can be recorded through out the record book year. Remember this is not the correct record book for a placement SAE.

11 The receipts page is designed to record income received from the enterprise. This can include the sales of animals and other revenue generating activities such as the sale of embryos or semen. Cash sales should have a detailed description to track which animals are sold and when. Entering an ear tag, name, or tattoo is recommended. The sale of capital items are not recorded on this page. They are entered on page 1-1 of the core pages. Show income includes revenue from premiums received at animal shows, fairs, exhibitions, and in some cases large sums of money from jackpot-type of shows. Totals from this page are transferred to page 14A, line 2.

12 Other receipts from the enterprise are recorded on this page. They are broken down into three categories. Value of labor exchanged for non-cash operating expenses is designed for students working for someone else to pay expenses of their enterprise. This could include working for a family member to pay rent of a pasture or use of equipment. An hourly rate should be determined so that the student has an idea of how many hours are needed to pay expenses. The value of production transferred/bartered is designed to record animals or products from the animals exchanged for an expense. Examples of this may include providing eggs to someone in exchange for the use of the chicken house or giving a rabbit to someone in exchange for the use of their tools. The value of products used at home is designed to record animals or products consumed by the student and/or their family. Values in this box and the previous boxes are important to record for enterprise evaluation. Totals are transferred to page 14A, line 3.

13 The cash operating expenses is designed to record current costs associated with the animal enterprise. This would include the purchase of feed, mineral, and other items that is expected to be utilized in a record book year. Note that items that can be depreciated and used over several record book years should not be entered in this table. For example fencing would not be recorded here, but rather in the core pages. Show expenses are recorded as they are charges associated with the enterprise. This could include entry fees, stall fees, etc. Totals from this page are transferred to page 14A, line 6.

14 Cash operating expenses is designed to record payments to individuals in exchange for labor or service. This would include paying a veterinarian for care or a friend who assisted with pen cleaning or ear tagging. Non-cash operating expenses is designed to record the payment with animals or products in exchange for labor, service, or goods. An example could include paying a family member with a market pig in exchange for doing weekend chores, feed, or use of equipment. Operating inventory purchased is designed to record the purchase of animals for resale. This could include the purchase of feeder animals that will be sold at market weight or young animals developed into breeding animals. Totals from this page are transferred to page 14A, line 7.

15 Non-depreciable inventory in supplies, prepaid expenses, and other current assets are recorded at the beginning and end of the record book year. Items in the table include feed, bedding, and other items purchased to support the enterprise. These items are expected to be used within a record book year. Non-depreciable inventory in merchandise and animals purchased for resale should be recorded at the beginning and end of the record book year. This would include the purchase of feeder animals being grown to market, developing breeding animals, and ear tags or vaccines. Non-depreciable inventory of other items are also recorded at the beginning and end of the record book year. This table is designed to record items that do not fit in other categories. Items listed in this table must be associated with the enterprises recorded in this book.

16 Non-depreciable inventory in draft, pleasure, or breeding animals is recorded to track changes in a record book year. This is recorded to track the growth of current assets associated with the animal enterprise. Animals used for competition, breeding, or work are listed in this table. Non-depreciable inventory of machinery, equipment, and fixtures is designed to track addition of resources added to the enterprise and are of value. Note that these are non-depreciable items. Totals from page 13A-1 and 13A-2 are transferred to page 14A, line 10.

17 The labor and management earnings page of the record book is completed at the conclusion of the record book year. All the data is accumulated into one place to determine how profitable the enterprise was in the operating period. The data on this page transfers automatically in EZ Records but has to be hand transferred in paper books. Also student s share has to be manually calculated in both books, even if the share is 100%. This is a common mistake found in record books.

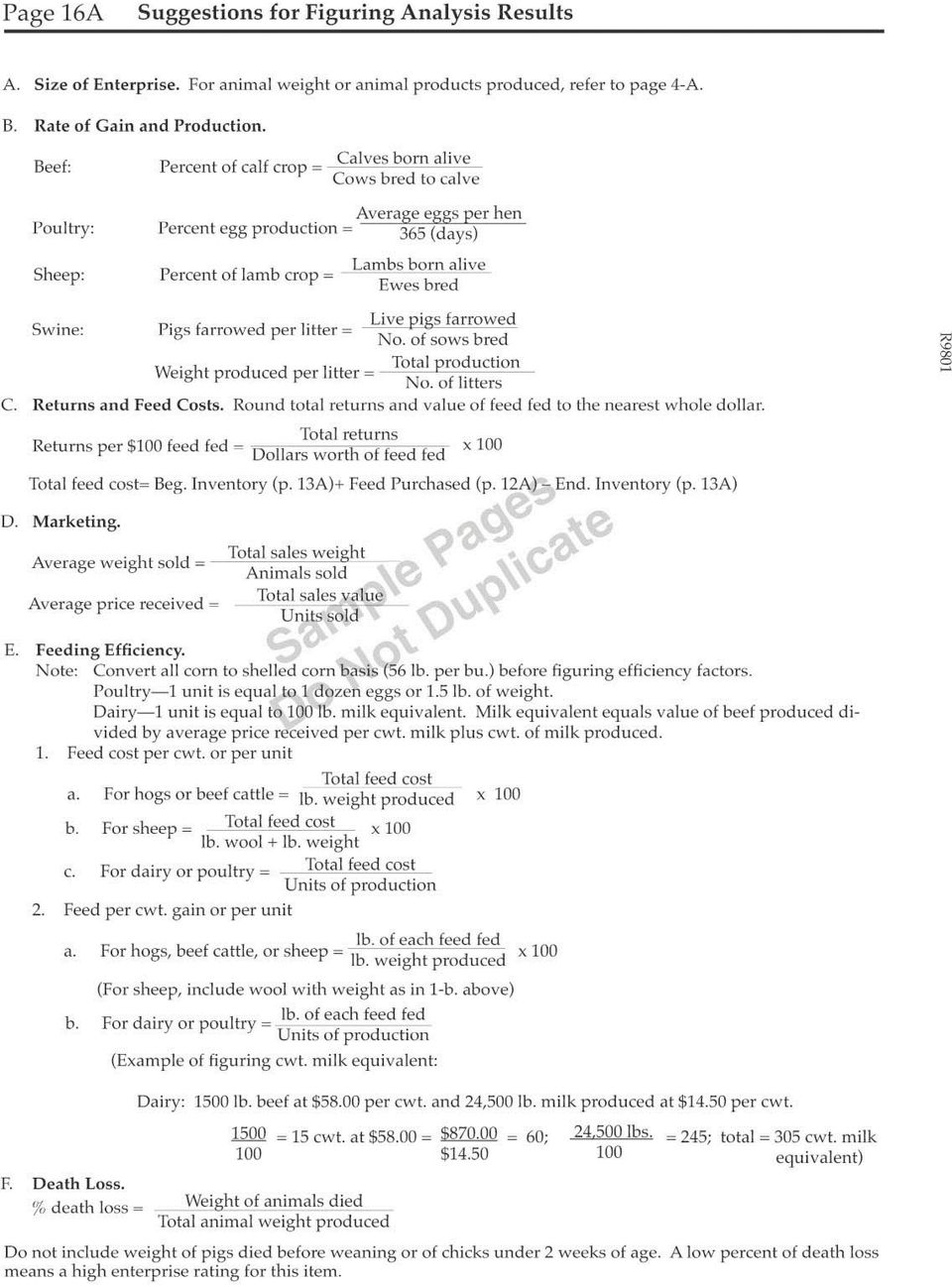

18 Enterprise analysis and comparison is used to determine how the students data compares to state or even national averages. It is also helpful to identify what areas of the enterprise is successful and what areas could use improvement. Note that not all analysis and comparisons need to be completed, as they do not apply to all enterprises. To collect state and national averages it is suggested you refer to the internet for the numbers. In EZ Records clicking the help button will supply the formulas for calculation. They can be found on the following page for paper record books.

19

20 The business book is designed for students who are either operating an entrepreneurial business or in a placement SAE. It is important that this is explained to students and if necessary more than one business book recorded. Data from entrepreneurial SAEs should not be recorded in a placement book and vice versa. A business agreement should only be completed for an entrepreneurial enterprise and should be completed before the SAE begins. It details all the terms of expenses, income, and responsibilities of the SAE. It should be reviewed by the supervising teacher and signed if appropriate. The student and parent should also review and sign the agreement. The other signature is added if equipment, land, or other inputs are rented, borrowed, or traded from a third-party. A new business agreement should be created each record book year and typically operate on a calendar year of January 1 to December 31. Note- this page is left blank in a placement enterprise.

21 The school instruction/planned activities is designed to record classroom instruction and linking it to skills to operate a business or perform a job. This section of the book is utilized in both entrepreneurial and placement SAEs. An example could include 15 hours of school instruction on lawnmower maintenance and the planned activity could be rebuilding a lawnmower. In the case of placement the school instruction could be learning to take soil samples and the planned activity could be to take samples for Farmer Brown. The budget is designed for student s to set goals for income and expenses of the enterprise. By creating this budget expenses can be estimated along with income to determine if the SAE will be a profitable. This page should be completed prior to the start of the SAE. This will allow for adjustments if needed. It is important to remember this is the expected income and expenses, not actual values. This table is expected to be more detailed and complete in an entrepreneurial enterprise in comparison to a placement enterprise.

22 The training agreement is only used in placement enterprises. It does not apply to entrepreneurial enterprises. It replaces the business agreement, which is left blank in placement enterprises. This page is designed to identify the terms of employment, expectations of the employer, and should be reviewed and signed by the student, employer, supervising teacher, and parents. All of this information should be recorded prior to the start of employment. Note- this page is left blank in entrepreneurial enterprises.

23 The training plan is only used in placement enterprises. It does not apply to entrepreneurial enterprises. It is designed to identify the skills and experiences the student can expect to obtain during the employment period. The number of experiences will vary, depending on the length of employment, type of employment, and previous experience of the student. The remarks/responsibilities are provided to supply additional information, such as when it will occur, to what extent of competency, or reason for the experience. Note- this page is left blank in entrepreneurial enterprises.

24 Entrepreneurial: The record of experiences serves as a type of journal of the enterprise. It can be as detailed as daily entries to as vague as monthly entries. The important aspect of this page is to record the number of hours worked on the enterprise. Note that three categories are available for hour entry: unpaid, paid, and other. Unpaid hours work will typically have the most entries as this is the hours worked by the student operating the enterprise. They should not count their hours as paid. Paid hours are recorded in two locations, on this page, and on the expenses page 11B. Paid hours must be recorded as an expense to the enterprise. Examples would including hiring a friend to assist mowing a large lot or prepare metal for painting. Other hours worked are recorded but do not transfer to the total hours dedicated to the enterprise. Examples of other hours would include attending a seminar on animal handling or a visit by the supervising teacher. Placement: The record of experiences serves as a journal of employment. Daily activities should be recorded, new skills obtained, etc. The completion of experiences listed in the training plan should be identified in this table. Several lines can be used to record the work experience and additional pages can be added. Most hours recorded will be paid or unpaid. It is important to keep an accurate record of hours worked.

25 A continuation of the data entries as found on the previous page. Note that extra space is supplied so that detailed records can be recorded through out the record book year. Totals transfer for each month should be placed on page 7B.

26 Entrepreneurial: The wage/labor summary is designed to record monthly totals of labor dedicated to the enterprise. In most cases in business enterprises the employer will be self and unpaid hours worked. Therefore no gross earnings, deductions, or net earnings will be recorded. These monthly totals are important to record as the data is utilized in the State and American Degree application. Income from the enterprise should be entered on the receipt page. Income from non-enterprise sources should be entered on core page 1-2. Placement: The wage/labor summary should have an entry for each time the student is paid for their placement SAE and include all deductions. These deductions should be recorded on core page 1-3 as a personal expense. The hours worked should match the totals on the previous pages. Income from non-enterprise sources should be entered on core page 1-2.

27 The same data entries as the previous page. Note that extra space is supplied so that detailed records can be recorded through out the record book year.

28 Entrepreneurial: The receipts page is designed to record income received from the enterprise. This can include the income from services provided and other revenue generating activities such as the sale of good produced. Cash sales should have a detailed description to track what is being sold and when. Entering a descriptive identification is recommended. The sale of capital items are not recorded on this page. They are entered on page 1-1 of the core pages. Placement: Typically placement enterprises will not have any entries for cash sales. However they may have entries for show income. Show income includes revenue from premiums received at shows, fairs, exhibitions, etc. Totals from this page are transferred to page 14B, line 2.

29 Other receipts from the enterprise are recorded on this page. They are broken down into three categories. Value of labor exchanged for non-cash operating expenses is designed for students working for someone else to pay expenses of their enterprise. This could include working for a family member to pay rent of a building or use of equipment. An hourly rate should be determined so that the student has an idea of how many hours are needed to pay expenses. Entries in the box are not common for placement enterprises. The value of production transferred/bartered is designed to record products or service exchanged for an expense. Examples of this may include providing dog care to someone in exchange for the use of dog training tools or mowing someone s yard in exchange for the use of their lawn roller. Entries in the box are not common for placement enterprises. The value of products used at home is designed to record products or service used by the student and/or their family. Entries in the box are not common for placement enterprises. Values in this box and the previous boxes are important to record for enterprise evaluation. Totals are transferred to page 14B, line 3.

30 The cash operating expenses is designed to record current costs associated with the enterprise. Entrepreneurial: This would include the purchase of gas, metal, and other items that is expected to be utilized in a record book year. Note that items that can be depreciated and used over several record book years should not be entered in this table. For example a welder or mower would not be recorded here, but rather in the core pages. Placement: Some cash expenses are expected. They would include transportation expenses such as gas, maintenance, or a bus pass. Special clothing or tools needed for the job. A car or motorcycle would not be listed here, but rather in the core pages. Show expenses are recorded as they are charges associated with the enterprise. This could include entry fees, stall fees, etc. Totals from this page are transferred to page 14B, line 6.

31 Cash operating expenses is designed to record payments to individuals in exchange for labor or service. This would include paying a mechanic to rebuild an engine or repair equipment. Entries in this table are not common for placement enterprises. Non-cash operating expenses is designed to record the payment in goods or service in exchange for labor or service. An example could include paying a friend by walking their dog in exchange for operating one of your mowers. Entries in this table are not common for placement enterprises. Operating inventory purchased is designed to record the purchase of goods or service for resale. This could include the purchase of grass seed or plants that will be sold as part of a landscape design. Totals from this page are transferred to page 14B, line 7.

32 Non-depreciable inventory in supplies, prepaid expenses, and other current assets are recorded at the beginning and end of the record book year. Items in the table include gas, oil, or other inputs used in the enterprise. For a placement enterprise it would include uniforms or tools. Non-depreciable inventory in merchandise and animals purchased for resale should be recorded at the beginning and end of the record book year. This would include the purchase of supplies or goods such as metal for welding or seed for landscaping. Placement entries are not common in this table. Non-depreciable inventory of other items are also recorded at the beginning and end of the record book year. This table is designed to record items that do not fit in other categories. Items listed in this table must be associated with the enterprises recorded in this book. Placement entries are not common in this table.

33 Non-depreciable inventory in supplies, prepaid expenses, and other items is designed to track addition of resources added to the enterprise and are of value. Note that these are non-depreciable items. Non-depreciable inventory of merchandise purchased for resale is recorded to track the movement of items moved in and out of the enterprise. For example grass seed may be purchased in the fall and resold in the spring landscape at a profit. Totals from this page and the previous page are transferred to page 14B, line 10. Placement entries are not common in this table.

34 The labor and management earnings page of the record book is completed at the conclusion of the record book year. All the data is accumulated into one place to determine how profitable the enterprise was in the operating or placement period. The data on this page transfers automatically in EZ Records but has to be hand transferred in paper books. Also student s share has to be manually calculated in both books, even if the share is 100%. This is a common mistake found in record books.

35 Evaluation factors are used to determine how the students data compares to state or even national averages. It is also helpful to identify what areas of the enterprise is successful and what areas could use improvement. Note that not all analysis and comparisons need to be completed, as they do not apply to all enterprises. To collect state and national averages it is suggested you refer to the internet for the numbers. In placement enterprises students can compare their earnings to state and national averages. They can also compare expenses to income to see how profitable it is in their current employment.

36 The crop book is designed for students who are operating a crop production enterprise. Only entrepreneurial SAEs should be recorded in this book. It is not designed to record placement data, as they are recorded in a business book. The business agreement should be completed before an SAE begins. It details all the terms of expenses, income, and responsibilities of the SAE. It should be reviewed by the supervising teacher and signed if appropriate. The student and parent should also review and sign the agreement. The other signature is added if equipment, land, or other inputs are rented, borrowed, or traded from a third-party. A new business agreement should be created each record book year and typically operate on a calendar year of January 1 to December 31.

37 The plans and goals/budget is designed for student s to set goals for their crop production enterprise. By creating this budget expenses can be estimated along with income to determine if the SAE will be a profitable business. It also allows for the proper resources to be identified. A plot plan should be created to determine how the soil will be prepared, what agronomic practices will be used, and how the crop will be marketed. This page should be completed prior to the start of the SAE. This will allow for adjustments if needed. It is important to remember this is the expected income and expenses, not actual values.

38 Soil test results are used to determine the available nutrients and ph of the soil. This data is used to determine how much fertilizer needs to be applied and if the ph needs correction. Production records are recorded in this table to track how well each variety yields and the practices used to plant the crop. Data recorded in this table should be entered at planting and again at harvest. Yield can be measured by whatever means is appropriate for the crop, such as bushels per acre, tons per acre, and other means of measurement. Remarks should be recorded such as extreme or cool temperatures, rainfall, etc. This information can be useful in selecting future varieties for conditions.

39 Crop production should be calculated at the conclusion of the growing season or when all the crop is sold. Note that many factors are taken into consideration when determining exact production. For example seed taken from beginning inventory needs to be deducted as well if the crop is dried, causing the crop to shrink. Remarks such a drought, flood, insect damage, or other factors can be noted to explain poor production. Enterprise analysis and comparison is used to determine how the students data compares to state or even national averages. It is also helpful to identify what areas of the enterprise is successful and what areas could use improvement. Note that not all analysis and comparisons need to be completed, as they do not apply to all enterprises. To collect state and national averages it is suggested you refer to the internet for the numbers. In EZ Records clicking the help button will supply the formulas for calculation. They can be found on the right side of this page for paper record books.

40 The record of experiences serves as a type of journal of the enterprise. It can be as detailed as daily entries to as vague as monthly entries. The important aspect of this page is to record the number of hours worked on the enterprise. Note that three categories are available for hour entry: unpaid, paid, and other. Unpaid hours work will typically have the most entries as this is the hours worked by the student operating the enterprise. They should not count their hours as paid. Paid hours are recorded in two locations, on this page, and on the expenses page 11A. Paid hours must be recorded as an expense to the enterprise. Examples would including hiring a friend to assist pulling weeds or scout for insects. Other hours worked are recorded but do not transfer to the total hours dedicated to the enterprise. Examples of other hours would include attending a seminar on nitrogen rates or a visit by the supervising teacher.

41 A continuation of the data entries as found on the previous page. Note that extra space is supplied so that detailed records can be recorded through out the record book year. Totals transfer for each month should be placed on page 7C.

42 The wage/labor summary is designed to record monthly totals of labor dedicated to the enterprise. In most cases in crop enterprises the employer will be self and unpaid hours worked. Therefore no gross earnings, deductions, or net earnings will be recorded. These monthly totals are important to record as the data is utilized in the State and American Degree application. Income from the enterprise should be entered on the receipt page. Income from non-enterprise sources should be entered on core page 1-2. One common mistake made on this page is students using it in a placement book. While it does allow for the recording of income with deductions, it is not the proper format. A business book is used for ALL placement SAEs.

43 The same data entries as the previous page. Note that extra space is supplied so that detailed records can be recorded through out the record book year. Remember this is not the correct record book for a placement SAE.

44 The receipts page is designed to record income received from the crop enterprise. This can include the sale of the crop and other revenue generating activities such as the sale of straw or roughage from the crop. Cash sales should have a detailed description to track what exactly is being sold and when the sale occurred. The sale of capital items are not recorded on this page. They are entered on page 1-1 of the core pages. Show income includes revenue from premiums received from shows, fairs, or other competitions in which the crop is entered. Totals from this page are transferred to page 14C, line 2.

45 Other receipts from the enterprise are recorded on this page. They are broken down into three categories. Value of labor exchanged for non-cash operating expenses is designed for students working for someone else to pay expenses of their enterprise. This could include working for a family member to pay rent of land or use of equipment. An hourly rate should be determined so that the student has an idea of how many hours are needed to pay expenses. The value of production transferred/bartered is designed to record crops or goods exchanged for an expense. Examples of this may include providing vegetables to someone in exchange for the use of their tractor or giving fruit to someone in exchange for the use of their tools. The value of products used at home is designed to record crops or goods consumed by the student and/or their family. Values in this box and the previous boxes are important to record for enterprise evaluation. Totals are transferred to page 14C, line 3.

46 The cash operating expenses is designed to record current costs associated with the crop enterprise. This would include the purchase of seed, fertilizer, and other items that is expected to be utilized in a record book year. Note that items that can be depreciated and used over several record book years should not be entered in this table. For example a tractor would not be listed here, but rather in the core pages. Show expenses are recorded as they are charges associated with the enterprise. This could include entry fees, participation fees, etc. Totals from this page are transferred to page 14C, line 6.

47 Cash operating expenses is designed to record payments to individuals in exchange for labor or service. This would include paying an applicator to spray a crop or insect scouting service. Non-cash operating expenses is designed to record the payment with crops or goods in exchange for labor or service. An example could include paying a friend with vegetables for watering and weeding while the student was on vacation. Operating inventory purchased is designed to record the purchase of crops or goods for resale. This could include the purchase of seedling plugs that will be sold as garden ready plants or cuttings that will be grown and sold as mature plants. Totals from this page are transferred to page 14C, line 7.

48 Non-depreciable inventory in harvested and growing crops are recorded at the beginning and end of the record book year. Items in the table include crops not-sold in storage, winter wheat, or other crops planted and not harvested until the next record book year. Non-depreciable inventory in seed, fertilizer, chemicals, prepaid expense, and other current items paid in one record book year but may be used in the next record book year. This would include fall applied fertilizer to be utilized in the spring growing season. Or purchasing seed in the previous record book year. Non-depreciable inventory of crops and items purchased for resale are also recorded at the beginning and end of the record book year. This table is designed to record items that do not fit in other categories. Items listed in this table must be associated with the enterprises recorded in this book.

49 Non-depreciable inventory of machinery, equipment, and fixtures is designed to track addition of resources added to the enterprise and are of value. Note that these are non-depreciable items. Non-depreciable inventory of merchandise purchased for resale is recorded to track the movement of items moved in and out of the enterprise. For example corn may be purchased in the fall and resold in the winter or spring at a profit. Totals from this page and the previous page are transferred to page 14C, line 10.

50 The labor and management earnings page of the record book is completed at the conclusion of the record book year. All the data is accumulated into one place to determine how profitable the enterprise was in the operating period. The data on this page transfers automatically in EZ Records but has to be hand transferred in paper books. Also student s share has to be manually calculated in both books, even if the share is 100%. This is a common mistake found in record books.

51 The agriscience book is designed for students who are conducting a research project or doing a science exploratory enterprise. It is not designed to record placement data for a student working in the science industry, as they are recorded in a business book. The research agreement should be completed before an SAE begins. It details all the terms of expenses, income, and responsibilities of the SAE. It should be reviewed by the supervising teacher and signed if appropriate. The student and parent should also review and sign the agreement. The other signature is added if equipment or other inputs are rented, borrowed, or traded from a third-party. A new research agreement should be created each record book year or if multiple, unrelated SAEs are conducted.

52 The purpose of this section is to identify the problem or reason for the research, identify the hypothesis or expected outcome, and an explanation of the research and why it is being conductive. These explanations should be fairly descriptive so that when evaluating the book, one can understand its purpose. It is appropriate to reference previous studies and outcomes, as a lot of research is always on going. The budget is designed for student s to determine how much the research will cost and if income will be received. By creating this budget expenses can be estimated along with income to determine if the SAE will be possible. It also allows for the proper resources to be identified. This page should be completed prior to the start of the SAE. This will allow for adjustments if needed. It is important to remember this is the expected income and expenses, not actual values.

53 The research plan is similar to the business agreement in other books. It should be completed before an SAE begins. It details all the terms of the SAE and should be reviewed by the supervising teacher and signed if appropriate. The student and parent should also review and sign the agreement. The adult sponsor signature is added if equipment, land, or other inputs are rented, borrowed, or traded from a third-party or they are overseeing the research. A new business agreement should be created each record book year. Note that several endorsements are identified and the parents and/or teacher are responsible for the student following applicable laws, rules, and regulations.

54 This section is designed to identify materials needed to conduct the research. Also step by step procedures should be listed in chronological order. The table is designed so that someone could use this page as a lab sheet and recreate the research. Be sure that students identify quantity of materials used, temperatures, treatment periods, etc.

55 The record of experiences serves as a type of journal of the enterprise. In the agriscience book this section should be much more detailed. Observations should be recorded, even if done every few minutes, hours, etc. Another important aspect of this page is to record the number of hours worked on the enterprise. Note that three categories are available for hour entry: unpaid, paid, and other. Unpaid hours work will typically have the most entries as this is the hours worked by the student operating the enterprise. They should not count their hours as paid. Paid hours are recorded in two locations, on this page, and on the expenses page 7S. Paid hours must be recorded as an expense to the enterprise. Examples would including hiring a friend to assist with the research. Other hours worked are recorded but do not transfer to the total hours dedicated to the enterprise. Examples of other hours would include attending a seminar or a visit by the supervising teacher. Multiple pages may be needed if recorded on paper.

56 The research skills, competencies, and knowledge is similar to the previous page, except it is to record accomplishments of the student as they advance in their research skills and become more proficient in different tasks. Note that unpaid, paid, and other hours are recorded. The same rules apply as the previous page.

57 The wage/labor summary is designed to record monthly totals of labor dedicated to the enterprise. In most cases in agriscience enterprises the employer will be self and unpaid hours worked. Therefore no gross earnings, deductions, or net earnings will be recorded. These monthly totals are important to record as the data is utilized in the State and American Degree application. Income from the enterprise should be entered on the receipt page. Income from non-enterprise sources should be entered on core page 1-2. One common mistake made on this page is students using it in a placement book. While it does allow for the recording of income with deductions, it is not the proper format. A business book is used for ALL placement SAEs.

58 The same data entries as the previous page. Note that extra space is supplied so that detailed records can be recorded through out the record book year. Remember this is not the correct record book for a placement SAE.

59 The receipts page is designed to record income received from the enterprise. This can include the sales of products and other revenue generating activities. Cash sales should have a detailed description to track what is sold and when. The sale of capital items are not recorded on this page. They are entered on page 1-1 of the core pages. Show income includes revenue from premiums received at shows, fairs, exhibitions and in some cases large sums of money from science competitions. Totals from this page and the next page are transferred to page 14S, line 2.

60 A continuation of the previous page. Totals from this page are transferred to page 14S, line 2.

61 The cash operating expenses is designed to record current costs associated with the enterprise. This would include the purchase of materials, research items, and other items that is expected to be utilized in a record book year. Note that items that can be depreciated and used over several record book years should not be entered in this table. For example a microscope would not be recorded here, but rather in the core pages. Show expenses are recorded as they are charges associated with the enterprise. This could include entry fees, stall fees, etc. Totals from this page are transferred to page 14S, line 6.

62 The school instruction and planned activities are recorded in these boxes. The school instruction would be course work done in your agriculture or other classes related to your research. This could include ag science, biology, chemistry, or math. Planned activities are designed to identify topics or skills the student plans to learn. This could include learning to prepare a microscope slide or preserve a specimen. Completion of these activates should also be recorded in the record of experiences. Review of literature is important to any research and many times are the source for developing a new research project. This can include documented studies on the internet or accredited journals. It is suggested that a literature is done before and after the research to develop the hypothesis and compare results.

63 Non-depreciable inventory in supplies, prepaid expenses, and other current assets are recorded at the beginning and end of the record book year. Items in the table include consumables and other items purchased to support the enterprise. These items are expected to be used within a record book year. Non-depreciable inventory of merchandise purchased for resale should be recorded at the beginning and end of the record book year. Non-depreciable inventory of other items are also recorded at the beginning and end of the record book year. This table is designed to record items that do not fit in other categories. Items listed in this table must be associated with the enterprises recorded in this book.

64 Non-depreciable inventory of supplies, prepaid expenses, and other items is recorded to track changes in a record book year. This is recorded to track the growth of current assets associated with the enterprise. Non-depreciable inventory of merchandise purchased for resale is designed to track addition of resources added to the enterprise and are of value. Note that these are non-depreciable items. Totals from page 13S-1 and 13S-2 are transferred to page 14S, line 10.

65 The labor and management earnings page of the record book is completed at the conclusion of the record book year. All the data is accumulated into one place to determine how profitable the enterprise was in the operating period. The data on this page transfers automatically in EZ Records but has to be hand transferred in paper books. Also student s share has to be manually calculated in both books, even if the share is 100%. This is a common mistake found in record books.

66 Evaluation factors are calculated on this page to determine how many hours are worked within the enterprise, skills learned, etc. Note that this box may be limited as research is hard to compare across other experiments. The conclusion should be completed at the end of the record book year or when the project is complete. It is expected that this should complete and identify the findings of the project. Attached materials are acceptable, such as tables, charts, or other supporting materials.

67 The abstract is a compressed version of the hypothesis, methods, and conclusions. It should be concluded at the end of the year or when the research is complete. An abstract should be limited to this page and only include the key elements. Note that step by step procedures are note expected, but the findings are expected to be descriptive. An abstract should be written even if the project was not successful as lessons can be learned for future projects. Many times an abstract are the only part of research that is reviewed.

68 Human vertebrate endorsement is required for all research and projects conducted at this level. The above regulations must be observed and borderline projects should be avoided. It is important is reviewed. This form should be completed prior to the beginning of the project.

69 Non-human vertebrate endorsement is required for all research and projects conducted at this level. The above regulations must be observed and borderline projects should be avoided. It is important is reviewed. This form should be completed prior to the beginning of the project.

70 The hazardous materials wavier form is designed to be sure safe and proper procedures are used when utilized. This serves as an accountability for those who oversee research and hazardous material use should be limited if possible. Safety is key to safe research for all involved. This form should be completed prior to the beginning of the project.

71 Capital inventory is tangible items purchased or sold, are considered investments in the enterprise, and are not completely consumed or used in one production cycle. Examples include investments in facilities, equipment, some breeding stock, loans, and capital sales. (breeding stock included are expected to breed and produce multiple times) Capital transactions are recorded in this box. That includes the purchase and sale of capital items as well as money borrowed and principal repayments. Note a date, good description, and enterprise must be provided. Miscellaneous income is money earned outside of the SAEs recorded in the record book. This type of income is broken down into three categories; ag. not related to SAE, gifts and unearned income, and non-ag. Examples of ag not related to SAE include baling hay for the neighbor, cleaning a barn, fixing fences, etc. Examples of gifts and unearned income include birthday money, inheritance, grants, and scholarships. Non-ag. income includes working at the paint store, helping the neighbor roof their house, babysitting, etc.

72 Personal expenses are recorded for use in the State or American Degree application. It also serves as a way for students to learn budgeting and track spending. Educational expenses should be recorded on this page. This would include lab fees, tuition, books, supplies, etc. Personal expenses would include gas, state and federal taxes and withholdings, recreational funds, etc. Note that these are expenses the student is actually paying themselves. Record personal expenses that are paid from funds earned from SAE and non-sae activities. (gifts, ag., non-ag. income) The date, whom the expense was paid, description, and total are to be recorded. For monthly recreational, gas, and spending money expenses it is appropriate to identify the whom as various.

73

74 The depreciation schedule is one of the hardest concepts in the record book to understand. Typically student-share s of non-current capital inventory is recorded into a depreciation schedule. Non-current capital inventory items are used for more than one production cycle. Because they are used for more than one production cycle the cost of the item should be spread over the life of the item and not charged to a single production cycle. This is done to account for accurate production costs and to take into consideration wear and tear. Depreciation is calculated each month the item is owned, regardless if purchased new or used. Note when depreciating breeding stock it only applies to purchased animals and are not classified new or used. If an item is traded in to purchase a different item the actual value is the cash difference of what is owed, not the original purchase price. Salvage value is determined by the value of an item at the conclusion of its productive life. Once deducted from the cash difference at purchase you have identified the Balance for Regular Depreciation. Life of an item varies by what it is; a building may be depreciated over 20 years whereas breeding sows may be depreciated over 3 years. The method of depreciation recommended for record books is Straight Line (Regular Depreciation Value/# years of life). It is the easiest to understand, provides tax value, and typically applies to SAEs. EZ Records is programed with this type of depreciation. Remaining book value is determined from the previous year s depreciation schedule. New items would have a balance of zero. See the example below of a John Deere 3010 is traded for a John Deere / JD 4020 used $3500 $6500 $6500 $1500 $ yr. SL 0 $5000 $1000 $4000

75 Examples: Corn Swine Lawn Care Summary of entrepreneurial income and expenses data must be hand transferred on paper, but is done automatically in EZ Records. Only student share values should be transferred to this page and should match the value within the enterprise pages. Note no data is entered on this page for Placement SAEs.

76 This page is an end of year summary for wage earning enterprises, such as Placement SAEs. When an enterprise is of the exploratory type only hours are recorded. In Placement SAEs both hours and wages are recorded, less expenses to determine net earnings. These values are used in the State and American Degree application. EZ Records users do not enter any data into this table, all data is auto transferred from the record book.

77 The summary of assets is a listing of personal and business property that has value. Business assets are items used within the business to produce goods or services. This would include a lawnmower, farm equipment, livestock, etc. Personal assets are items such as a car, ATV, gaming system, cash, savings, etc. Current assets are items that will be used in a production cycle or within a year. This would include feed, fertilizer, fuel, market animals, etc. Non-current capital assets are items used over several production cycles or years. These are items typically found in the depreciation schedule. This would include breeding stock, buildings, equipment, land, etc.

78 Liabilities Liabilities are defined as money owed; debts or financial obligations. They are divided into current and non-current liabilities. Current liabilities are loans, debts, or financial obligations that will be paid off in one record book year. This would include operating loans, fertilizer or feed bills, etc. Non-current liabilities are loans, debts, or financial obligations that will be paid over a period of years. This would include items that may be found on the depreciation schedule. That would include equipment, buildings, mortgages on land or property, etc. Many values can be determined by calculating assets and liabilities. Net worth is determined by subtracting liabilities from assets. A change in net worth can be expected during a calendar year as items are added or sold from a business. Current ratio or liquidity determines the business s ability to pay current liabilities. Working capital is the difference between current assets and current liabilities. This is money that could be used to grow a business or apply towards non-current liabilities. Debt worth ratio or leverage is calculated by dividing all liabilities by all assets. A number less than 1 equals good financial standing. Liability ratio is determined by dividing post tax profits + depreciation divided by all liabilities. All of these calculations are used by financial institutions to determine if a business is eligible for credit, loans, etc.

79 The narrative of experience is part of the record book that should be completed at the end of the year. It is a place for students to discuss activities or event not covered in the enterprise pages. This would include identifying knowledge gained to be applied to a career or future direction of the SAEs. Major achievements such as business expansion, significant increase in yields, and other accomplishments are appropriate for the narrative. It is important that each enterprise is identified by title and written in first person.

Agriculture & Business Management Notes...

Agriculture & Business Management Notes... SPA Standardized Performance Analysis For Sheep Producers -- A Worksheet Approach -- Sheep producers have been challenged to be lower cost producers, to become

Agriculture & Business Management Notes... SPA Standardized Performance Analysis For Sheep Producers -- A Worksheet Approach -- Sheep producers have been challenged to be lower cost producers, to become

Farm Financial Management

Farm Financial Management Your Farm Income Statement How much did your farm business earn last year? There are many ways to answer this question. A farm income statement (sometimes called a profit and

Farm Financial Management Your Farm Income Statement How much did your farm business earn last year? There are many ways to answer this question. A farm income statement (sometimes called a profit and

Farm Tax Record Book SAMPLE

Farm Tax Record Book TABLE OF CONTENTS Farm Receipts... Milk Sales and Deductions Worksheet... Government Payments Worksheet... Commodity Certificates... Sale of Livestock Worksheet... Farm Expenses...0

Farm Tax Record Book TABLE OF CONTENTS Farm Receipts... Milk Sales and Deductions Worksheet... Government Payments Worksheet... Commodity Certificates... Sale of Livestock Worksheet... Farm Expenses...0

How much did your farm business earn last year?

Your Farm Ag Decision Maker Income Statement File C3-25 How much did your farm business earn last year? Was it profitabile? There are many ways to answer these questions. A farm income statement (sometimes

Your Farm Ag Decision Maker Income Statement File C3-25 How much did your farm business earn last year? Was it profitabile? There are many ways to answer these questions. A farm income statement (sometimes

Science of Life Explorations

Science of Life Explorations Celebrate the Growing Year: The Farmer s Year A Farmer s Year While you are in school or on a vacation, farmers are working hard to provide us with the foods we eat and the

Science of Life Explorations Celebrate the Growing Year: The Farmer s Year A Farmer s Year While you are in school or on a vacation, farmers are working hard to provide us with the foods we eat and the

How much financing will your farm business

Twelve Steps to Ag Decision Maker Cash Flow Budgeting File C3-15 How much financing will your farm business require this year? When will money be needed and from where will it come? A little advance planning

Twelve Steps to Ag Decision Maker Cash Flow Budgeting File C3-15 How much financing will your farm business require this year? When will money be needed and from where will it come? A little advance planning

Setting up your Chart of Accounts

FARM FUNDS WORKSHEETS Setting up your Chart of Accounts Supplies Supplies are any inputs that will be used on a field, group of livestock, or equipment. Setting up a supply will set up the related expense

FARM FUNDS WORKSHEETS Setting up your Chart of Accounts Supplies Supplies are any inputs that will be used on a field, group of livestock, or equipment. Setting up a supply will set up the related expense

How To Write A Business Plan

Business Planning for Livestock Producers James McWhorter UF/IFAS Highlands County Livestock Agent Introduction Why create a business plan Components of a business plan Financial statements Five C s of

Business Planning for Livestock Producers James McWhorter UF/IFAS Highlands County Livestock Agent Introduction Why create a business plan Components of a business plan Financial statements Five C s of

Agriculture & Business Management Notes...

Agriculture & Business Management Notes... Preparing an Income Statement Quick Notes... The income statement measures the profitability of a business over a specific period of time. Cash reporting of income

Agriculture & Business Management Notes... Preparing an Income Statement Quick Notes... The income statement measures the profitability of a business over a specific period of time. Cash reporting of income

Cash to Accrual Income Approximation

Cash to Accrual Income Approximation With this program, the user can estimate accrual income using the Schedule F from his/her federal income tax return. Fast Tools & Resources Farmers typically report

Cash to Accrual Income Approximation With this program, the user can estimate accrual income using the Schedule F from his/her federal income tax return. Fast Tools & Resources Farmers typically report

Calculating Your Milk Production Costs and Using the Results to Manage Your Expenses

Calculating Your Milk Production Costs and Using the Results to Manage Your Expenses by Gary G. Frank 1 Introduction Dairy farms producing milk have numerous sources of income: milk, cull cows, calves,

Calculating Your Milk Production Costs and Using the Results to Manage Your Expenses by Gary G. Frank 1 Introduction Dairy farms producing milk have numerous sources of income: milk, cull cows, calves,

Contents. Acknowledgements... iv. Source of Data...v

Kentucky Farm Business Management Program Annual Summary Data: Kentucky Grain Farms - 2011 Agricultural Economics Extension No. 2012-17 June 2012 By: Amanda R. Jenkins Michael C. Forsythe University of

Kentucky Farm Business Management Program Annual Summary Data: Kentucky Grain Farms - 2011 Agricultural Economics Extension No. 2012-17 June 2012 By: Amanda R. Jenkins Michael C. Forsythe University of

AGRICULTURE FINANCIAL STATEMENT Borrower # AND LOAN APPLICATION Telephone #

AGRICULTURE FINANCIAL STATEMENT Borrower # AND LOAN APPLICATION Telephone # For the purpose of obtaining credit from Ramsey National Bank (RNB) and any future credit granted by the RNB, or to support an

AGRICULTURE FINANCIAL STATEMENT Borrower # AND LOAN APPLICATION Telephone # For the purpose of obtaining credit from Ramsey National Bank (RNB) and any future credit granted by the RNB, or to support an

Livestock Budget Estimates for Kentucky - 2000

Livestock Budget Estimates for Kentucky - 2000 Agricultural Economics Extension No. 2000-17 October 2000 By: RICHARD L. TRIMBLE, STEVE ISAACS, LAURA POWERS, AND A. LEE MEYER University of Kentucky Department

Livestock Budget Estimates for Kentucky - 2000 Agricultural Economics Extension No. 2000-17 October 2000 By: RICHARD L. TRIMBLE, STEVE ISAACS, LAURA POWERS, AND A. LEE MEYER University of Kentucky Department

Enterprise Budgeting. By: Rod Sharp and Dennis Kaan Colorado State University

Enterprise Budgeting By: Rod Sharp and Dennis Kaan Colorado State University One of the most basic and important production decisions is choosing the combination of products or enterprises to produce.

Enterprise Budgeting By: Rod Sharp and Dennis Kaan Colorado State University One of the most basic and important production decisions is choosing the combination of products or enterprises to produce.

Would you like to know more about the

Your Net Worth Ag Decision Maker Statement File C3-20 Would you like to know more about the current financial situation of your farming operation? A simple listing of the property you own and the debts

Your Net Worth Ag Decision Maker Statement File C3-20 Would you like to know more about the current financial situation of your farming operation? A simple listing of the property you own and the debts

Course: AG 460-Agribusiness Management and Marketing

Course: AG 460-Agribusiness Management and Marketing Unit Objective CAERT Lesson Plan Library Unit Problem Area Lesson Agricultural Careers 1. Identify and describe careers in agriculture Agribusiness

Course: AG 460-Agribusiness Management and Marketing Unit Objective CAERT Lesson Plan Library Unit Problem Area Lesson Agricultural Careers 1. Identify and describe careers in agriculture Agribusiness

Farm Financial Statements Net Worth Statement Statement of Cash Flows Net Income Statement Statement of Owner Equity

Farm Financial Statements Net Worth Statement Statement of Cash Flows Net Income Statement Statement of Owner Equity Recording Transactions in the Date Cash Journal Description Value Amount (bu., lb.,

Farm Financial Statements Net Worth Statement Statement of Cash Flows Net Income Statement Statement of Owner Equity Recording Transactions in the Date Cash Journal Description Value Amount (bu., lb.,

Instruction Sheet for Recordkeeping Template: Monthly Operational Expenses for Farm

Instruction Sheet for Recordkeeping Template: The intent of this table is to provide a place for recording farm expenses that you incurred and paid in the tax year. Generally, farmers can deduct the current

Instruction Sheet for Recordkeeping Template: The intent of this table is to provide a place for recording farm expenses that you incurred and paid in the tax year. Generally, farmers can deduct the current

AGRICULTURAL LOAN APPLICATION

AGRICULTURAL LOAN APPLICATION REQUESTED LOAN AMOUNT PURPOSE APPLICANT TYPE INDIVIDUAL JOINT CORPORATION PARTNERSHIP OTHER REQUESTED LOAN TYPE OPERATING LINE OF CREDIT TERM EQUIPMENT REAL ESTATE INDIVIDUAL

AGRICULTURAL LOAN APPLICATION REQUESTED LOAN AMOUNT PURPOSE APPLICANT TYPE INDIVIDUAL JOINT CORPORATION PARTNERSHIP OTHER REQUESTED LOAN TYPE OPERATING LINE OF CREDIT TERM EQUIPMENT REAL ESTATE INDIVIDUAL

Preparing Agricultural Financial Statements

Preparing Agricultural Financial Statements Thoroughly understanding your business financial performance is critical for success in today s increasingly competitive agricultural environment. Accurate records

Preparing Agricultural Financial Statements Thoroughly understanding your business financial performance is critical for success in today s increasingly competitive agricultural environment. Accurate records

Developing a Chart of Accounts for the Farm or Ranch

Developing a Chart of Accounts for the Farm or Ranch EB 132 April 1995 Developing a Chart of Accounts for the Farm or Ranch by Genice Garner and Duane Griffith* Keep receipts Memo on checks Track only

Developing a Chart of Accounts for the Farm or Ranch EB 132 April 1995 Developing a Chart of Accounts for the Farm or Ranch by Genice Garner and Duane Griffith* Keep receipts Memo on checks Track only

Farm Business Analysis Report BEEF SUMMARY

Extension No. M M-356 ESQ No. 490 1977 Farm Business Analysis Report BEEF SUMMARY Department of Agricultural Economics and Rural Sociology Cooperative Extension Service The Ohio State University Columbus,

Extension No. M M-356 ESQ No. 490 1977 Farm Business Analysis Report BEEF SUMMARY Department of Agricultural Economics and Rural Sociology Cooperative Extension Service The Ohio State University Columbus,

The BASICS of FINANCIAL STATEMENTS For Agricultural Producers

The BASICS of FINANCIAL STATEMENTS For Agricultural Producers Authors: James McGrann Francisco Abelló Doug Richardson Christy Waggoner Department of Agricultural Economics Texas Cooperative Extension Texas

The BASICS of FINANCIAL STATEMENTS For Agricultural Producers Authors: James McGrann Francisco Abelló Doug Richardson Christy Waggoner Department of Agricultural Economics Texas Cooperative Extension Texas

Basics of accounting Documentation basics Choosing an accounting system Common tax issues Get an advisor!!!

Basics of accounting Documentation basics Choosing an accounting system Common tax issues Get an advisor!!! Money TRANSACTIONS CHART OF ACCTS GENERAL LEDGER BALANCE SHEET INCOME STATEMENT FINANCIAL STATEMENTS

Basics of accounting Documentation basics Choosing an accounting system Common tax issues Get an advisor!!! Money TRANSACTIONS CHART OF ACCTS GENERAL LEDGER BALANCE SHEET INCOME STATEMENT FINANCIAL STATEMENTS

Section II: Problem Solving (200 points) KEY

KEY") ARE 495U Assignment 2-10 points Create 5 or more marketing plan questions that need to be answered related to FF. 2013 North Carolina FFA Farm Business Management Career Development Event Section II: Problem

ARE 495U Assignment 2-10 points Create 5 or more marketing plan questions that need to be answered related to FF. 2013 North Carolina FFA Farm Business Management Career Development Event Section II: Problem

Assessing and Improving Farm Profitability

1 Fact Sheet 539 Assessing and Improving Farm Profitability Is my farm making money? This is a question farm managers think about often. To stay in business, the farm must generate a profit, at least in

1 Fact Sheet 539 Assessing and Improving Farm Profitability Is my farm making money? This is a question farm managers think about often. To stay in business, the farm must generate a profit, at least in

Can You Make Money With Sheep? David L. Thomas Department of Animal Sciences University of Wisconsin-Madison dlthomas@wisc.edu

Can You Make Money With Sheep? David L. Thomas Department of Animal Sciences University of Wisconsin-Madison dlthomas@wisc.edu Before entering into sheep production, you should be aware of the capital

Can You Make Money With Sheep? David L. Thomas Department of Animal Sciences University of Wisconsin-Madison dlthomas@wisc.edu Before entering into sheep production, you should be aware of the capital

Forage Economics, page2. Production Costs

Forage Economics Geoffrey A. Benson, Professor Emeritus, Department of Agricultural and Resource Economics, and James T. Green, Jr., Professor Emeritus, Department of Crop Science, NC State University

Forage Economics Geoffrey A. Benson, Professor Emeritus, Department of Agricultural and Resource Economics, and James T. Green, Jr., Professor Emeritus, Department of Crop Science, NC State University

BUSINESS TOOLS. Preparing Agricultural Financial Statements. How do financial statements prove useful?

Preparing Agricultural Financial Statements Thoroughly understanding your business financial performance is critical for success in today s increasingly competitive agricultural, forestry and fisheries

Preparing Agricultural Financial Statements Thoroughly understanding your business financial performance is critical for success in today s increasingly competitive agricultural, forestry and fisheries

Using Enterprise Budgets in Farm Financial Planning

Oklahoma Cooperative Extension Service AGEC-243 Using Enterprise Budgets in Farm Financial Planning Damona Doye Regents Professor and Extension Economist Roger Sahs Extension Assistant Oklahoma Cooperative

Oklahoma Cooperative Extension Service AGEC-243 Using Enterprise Budgets in Farm Financial Planning Damona Doye Regents Professor and Extension Economist Roger Sahs Extension Assistant Oklahoma Cooperative

SELF-EMPLOYED HOUSEHOLDS Section 104 Page 1

SELF-EMPLOYED HOUSEHOLDS Section 104 Page 1 104.1 Purpose This section describes the special policies that apply to households that have self-employment income. 104.2 General Information All the policies

SELF-EMPLOYED HOUSEHOLDS Section 104 Page 1 104.1 Purpose This section describes the special policies that apply to households that have self-employment income. 104.2 General Information All the policies

Swine Farm Business Analysis Workbook

Swine Farm Business Analysis Workbook Swine AoE Team Michigan State University Lead author and editor: Roger Betz Section contributing authors: Sherrill Nott Gerry Schwab Janice Knuth Mike Staton Aug.

Swine Farm Business Analysis Workbook Swine AoE Team Michigan State University Lead author and editor: Roger Betz Section contributing authors: Sherrill Nott Gerry Schwab Janice Knuth Mike Staton Aug.

Agriculture & Business Management Notes...

Agriculture & Business Management Notes... Preparing and Analyzing a Cash Flow Statement Quick Notes... Cash Flow Statements summarize cash inflows and cash outflows over a period of time. Uses of a Cash

Agriculture & Business Management Notes... Preparing and Analyzing a Cash Flow Statement Quick Notes... Cash Flow Statements summarize cash inflows and cash outflows over a period of time. Uses of a Cash

Agricultural Balance Sheet (Financial Statement)

") Agricultural Balance Sheet (Financial Statement) This form can be used as a guide to collect information for an annual financial statement or for an application for credit. If you are using the Adobe PDF

Agricultural Balance Sheet (Financial Statement) This form can be used as a guide to collect information for an annual financial statement or for an application for credit. If you are using the Adobe PDF

Virginia SAE Record Book

Virginia SAE Record Book STUDENT EDITION Name: School: Dates Covered: From through Copyright 2009 by the Virginia Department of Education P.O. Box 2120 Richmond, Virginia 23218-2120 www.doe.virginia.gov

Virginia SAE Record Book STUDENT EDITION Name: School: Dates Covered: From through Copyright 2009 by the Virginia Department of Education P.O. Box 2120 Richmond, Virginia 23218-2120 www.doe.virginia.gov

Lesson 2. Cash Flow Budgets

A Project Funded by USDA BFRDP Grant #10506276 Development Partners Include: Lesson 2. Cash Flow Budgets Introduction Cash flow budgets provide detail about periods when cash outflows exceed cash inflows.

A Project Funded by USDA BFRDP Grant #10506276 Development Partners Include: Lesson 2. Cash Flow Budgets Introduction Cash flow budgets provide detail about periods when cash outflows exceed cash inflows.

Guidelines for Estimating. Beef Cow-Calf Production Costs 2015. in Manitoba

Guidelines for Estimating Beef Cow-Calf Production Costs 2015 in Manitoba ................................................. Guidelines For Estimating Beef Cow-Calf Production Costs Based on a 150 Head

Guidelines for Estimating Beef Cow-Calf Production Costs 2015 in Manitoba ................................................. Guidelines For Estimating Beef Cow-Calf Production Costs Based on a 150 Head

Farm Accounting Using QuickBooks

Farm Accounting Using QuickBooks Users Manual Stanley Schraufnagel Jenny Vanderlin TABLE OF CONTENTS Page Introduction and Acknowledgements. i Chapter 1: Accounting Basics 1 Chapter 2: Getting Started.

Farm Accounting Using QuickBooks Users Manual Stanley Schraufnagel Jenny Vanderlin TABLE OF CONTENTS Page Introduction and Acknowledgements. i Chapter 1: Accounting Basics 1 Chapter 2: Getting Started.

Tax Return Questionnaire - 2013 Tax Year

Print this form out, take some time to fill it out, and bring it with you when you come to the office. This will save you time and money, and help us help you more effectively. Tax Return Questionnaire

Print this form out, take some time to fill it out, and bring it with you when you come to the office. This will save you time and money, and help us help you more effectively. Tax Return Questionnaire

3. If you received any interest from a "Seller Financed" mortgage, provide: Name and Address of Payer Social Security Number Amount

Print this form out, take some time to fill it out, and bring it with you when you come to the office. This will save you time and money, and help us help you more effectively. Tax Return Questionnaire

Print this form out, take some time to fill it out, and bring it with you when you come to the office. This will save you time and money, and help us help you more effectively. Tax Return Questionnaire

Business Planning and Economics of Sheep Farm Establishment and Cost of Production in Nova Scotia

Business Planning and Economics of Sheep Farm Establishment and Cost of Production in Nova Scotia Prepared by: Christina Jones, Economist, Nova Scotia Department of Agriculture Although care has been taken

Business Planning and Economics of Sheep Farm Establishment and Cost of Production in Nova Scotia Prepared by: Christina Jones, Economist, Nova Scotia Department of Agriculture Although care has been taken

Computerized Farm Records

Computerized Farm Records Peg Brune ~ Dodge, NE 402-693-2801 Email: brune@skyww.net Agricultural Bookkeeping: Quickbooks or Quicken???? Accounting: Accountants prefer Quickbooks, mostly because a lot of

Computerized Farm Records Peg Brune ~ Dodge, NE 402-693-2801 Email: brune@skyww.net Agricultural Bookkeeping: Quickbooks or Quicken???? Accounting: Accountants prefer Quickbooks, mostly because a lot of

Income Taxes. Description. Main Federal Tax Forms

Income Taxes Description Income in the U.S. is taxed by the Federal government to provide revenue to run the government and provide services to the citizens. Each year businesses and individuals must file

Income Taxes Description Income in the U.S. is taxed by the Federal government to provide revenue to run the government and provide services to the citizens. Each year businesses and individuals must file

STANDARDIZED PERFORMANCE ANALYSIS

STANDARDIZED PERFORMANCE ANALYSIS SPA-6 COW-CALF ENTERPRISE FINANCIAL PERFORMANCE MEASURES WORKSHEET (SPA-FCC) * 6-16-06 SPA is a standardized cow-calf enterprise production and financial performance analysis

STANDARDIZED PERFORMANCE ANALYSIS SPA-6 COW-CALF ENTERPRISE FINANCIAL PERFORMANCE MEASURES WORKSHEET (SPA-FCC) * 6-16-06 SPA is a standardized cow-calf enterprise production and financial performance analysis

FARM LEGAL SERIES June 2015 Security Interests in Personal Property

Agricultural Business Management FARM LEGAL SERIES June 2015 Security Interests in Personal Property Phillip L. Kunkel, Jeffrey A. Peterson, Jason Thibodeaux Attorneys, Gray Plant Mooty INTRODUCTION The

Agricultural Business Management FARM LEGAL SERIES June 2015 Security Interests in Personal Property Phillip L. Kunkel, Jeffrey A. Peterson, Jason Thibodeaux Attorneys, Gray Plant Mooty INTRODUCTION The

The financial position and performance of a farm

Farm Financial Ag Decision Maker Statements File C3-56 The financial position and performance of a farm business can be summarized by four important financial statements. The relationship of these statements

Farm Financial Ag Decision Maker Statements File C3-56 The financial position and performance of a farm business can be summarized by four important financial statements. The relationship of these statements

1420 n. CLAREMONT BLVD., SUITE 101-B TEL (909) 398-4737 CLAREMONT, CALIFORNIA 91711 FAX (909) 398-4733

398-4737 CLAREMONT, CALIFORNIA 91711 FAX (909) 398-4733") 1420 n. CLAREMONT BLVD., SUITE 101-B TEL (909) 398-4737 CLAREMONT, CALIFORNIA 91711 FAX (909) 398-4733 www.nicholscpas.com Email: info@nicholscpas.com January 12, 2015 RE: 2014 Tax Returns It is hard to

1420 n. CLAREMONT BLVD., SUITE 101-B TEL (909) 398-4737 CLAREMONT, CALIFORNIA 91711 FAX (909) 398-4733 www.nicholscpas.com Email: info@nicholscpas.com January 12, 2015 RE: 2014 Tax Returns It is hard to

Assessing and Improving Your Farm Cash Flow

Fact Sheet 541 Assessing and Improving Your Farm Cash Flow What Is Liquidity? Liquidity refers to the ability of your farm to generate enough cash to meet financial obligations as they come due without

Fact Sheet 541 Assessing and Improving Your Farm Cash Flow What Is Liquidity? Liquidity refers to the ability of your farm to generate enough cash to meet financial obligations as they come due without

Account Numbering. By separating each account by several numbers, many new accounts can be added between any two while maintaining the logical order.

Chart of Accounts The chart of accounts is a listing of all the accounts in the general ledger, each account accompanied by a reference number. To set up a chart of accounts, one first needs to define

Chart of Accounts The chart of accounts is a listing of all the accounts in the general ledger, each account accompanied by a reference number. To set up a chart of accounts, one first needs to define

Check One: Single Married Filing Joint Surviving Widow/Widower Married Filing Separately (enter spouse s name/ss No. Above) Dependents Name

Dependents Name") Felix Guillot, EA, ABA, ATA Kendyl Guillot, ABA E-Tax, LLC 318-445-5564 etaxla.com tax@etaxla.com Tax Organizer Tax Year 2014 Name: Taxpayer SS No. Birthdate/ Spouse SS No. Birthdate/ Address: Telephone

Felix Guillot, EA, ABA, ATA Kendyl Guillot, ABA E-Tax, LLC 318-445-5564 etaxla.com tax@etaxla.com Tax Organizer Tax Year 2014 Name: Taxpayer SS No. Birthdate/ Spouse SS No. Birthdate/ Address: Telephone

The estimated costs of corn, corn silage,

Estimated Costs of Crop Ag Decision Maker Production in Iowa - 2015 File A1-20 The estimated costs of corn, corn silage, soybeans, alfalfa, and pasture maintenance in this report are based on data from

Estimated Costs of Crop Ag Decision Maker Production in Iowa - 2015 File A1-20 The estimated costs of corn, corn silage, soybeans, alfalfa, and pasture maintenance in this report are based on data from

Commercial Fruit Production. Essential Commercial Fruit Production Decisions

2014 Farming For Profit Workshop Series Commercial Fruit Production Essential Commercial Fruit Production Decisions The questions in this document are intended to help you make the key decisions necessary

2014 Farming For Profit Workshop Series Commercial Fruit Production Essential Commercial Fruit Production Decisions The questions in this document are intended to help you make the key decisions necessary

PERSONAL FINANCIAL STATEMENT

PERSONAL FINANCIAL STATEMENT As of, 20 BUSINESS PLAN GUIDELINES Name: Residence Phone: Residence Address: City, State, Zip Code: Social Security Number: PERSONAL ASSETS PERSONAL LIABILITIES Cash in Bank

PERSONAL FINANCIAL STATEMENT As of, 20 BUSINESS PLAN GUIDELINES Name: Residence Phone: Residence Address: City, State, Zip Code: Social Security Number: PERSONAL ASSETS PERSONAL LIABILITIES Cash in Bank

Stocker Grazing or Grow Yard Feeder Cattle Profit Projection Calculator Users Manual and Definitions

Stocker Grazing or Grow Yard Feeder Cattle Profit Projection Calculator Users Manual and Definitions The purpose of this decision aid is to help facilitate the organization of stocker or feeder cattle

Stocker Grazing or Grow Yard Feeder Cattle Profit Projection Calculator Users Manual and Definitions The purpose of this decision aid is to help facilitate the organization of stocker or feeder cattle

Personal Study Assignment #1: Inventory Assessment

The purpose of this activity is for you to conduct an inventory of your farm business assets. Think about your farm business and list all of the assets you own and/or control that make up the farm business.

The purpose of this activity is for you to conduct an inventory of your farm business assets. Think about your farm business and list all of the assets you own and/or control that make up the farm business.

Estimation of Deferred Taxes

Estimation of Deferred Taxes With this program, the user can estimate current and noncurrent deferred taxes. Deferred Taxes Deferred taxes represent the federal income, state income, and Social Security

Estimation of Deferred Taxes With this program, the user can estimate current and noncurrent deferred taxes. Deferred Taxes Deferred taxes represent the federal income, state income, and Social Security

COOPERATIVE EXTENSION Bringing the University to You

COOPERATIVE EXTENSION Bringing the University to You Special Publication 05-12 Importance & Use of Enterprise Budgets in Agricultural Operations William W. Riggs, Eureka County Extension Educator, University

COOPERATIVE EXTENSION Bringing the University to You Special Publication 05-12 Importance & Use of Enterprise Budgets in Agricultural Operations William W. Riggs, Eureka County Extension Educator, University

JOB ANNOUNCEMENT. Nursery Manager DEGREE AND CURRICULUM:

Horticulture Nursery Manager Associate degree in Horticulture or related degree. Will consider all qualified agriculture degrees. Manages nursery to grow horticultural plants, such as trees, shrubs, flowers,

Horticulture Nursery Manager Associate degree in Horticulture or related degree. Will consider all qualified agriculture degrees. Manages nursery to grow horticultural plants, such as trees, shrubs, flowers,

Cash Flow Analysis Worksheets