How To Account For A 501(C) Organization

|

|

|

- Emil Lloyd

- 3 years ago

- Views:

Transcription

1 Accounting Accounting Finance and Finance Alliances for Alliances PRESENTED BY: JANET MALASIG IEEE-ISTO CONTROLLER

2 IEEE-ISTO and member Programs Program Financial Statements Membership Dues Accounting

3 IEEE Industry Standards and Technology Organization (IEEE- ISTO) was established in January 1999 as a global, not for profit corporation 501(c)(6)

4 Internal Revenue Service Subsection Codes for Tax-Exempt Organizations Section of Code Description of Categories Annual Return Required to Be Filed 501(c)(1) Corporations Organized under Act of Congress (including Federal Credit Unions) None 501(c)(2) Title Holding Corporation for Exempt Organization Form 9901 or 990-EZ8 501(c)(3) Religious, Educational, Charitable, Scientific, Literary, Testing for Public Safety, to Foster National or International Amateur Sports Competition, or Prevention of Cruelty to Children or Animals Organizations Form 9901, 990-EZ8, or 990-PF 501(c)(4) Civic Leagues, Social Welfare Organizations, and Local Associations of Employees Form 9901 or 990-EZ8 501(c)(5) Labor, Agricultural, and Horticultural Organizations Form 9901 or 990-EZ8 501(c)(6) Business Leagues, Chambers of Commerce, Real Form 990 or 990- Estate Boards, Etc. EZ 501(c)(7) Social and Recreational Clubs Form 9901 or 990-EZ8 501(c)(8) Fraternal Beneficiary Societies and Associations Form 9901 or 990-EZ8 501(c)(9) Voluntary Employees Beneficiary Associations Form 9901 or 990-EZ8 501(c)(10) Domestic Fraternal Societies and Associations Form 9901 or 990-EZ8 501(c)(11) Teacher's Retirement Fund Associations Form 9901 or 990-EZ8 501(c)(12) Benevolent Life Insurance Associations, Mutual Ditch or Irrigation Companies, Mutual or Cooperative Telephone Companies, Etc. Form 9901 or 990-EZ8 501(c)(13) Cemetery Companies Form 9901 or 990-EZ8 501(c)(14) State Chartered Credit Unions, Mutual Reserve Funds Form 9901 or 990-EZ8 501(c)(15) Mutual Insurance Companies or Associations Form 9901 or 990-EZ8 501(c)(16) Cooperative Organizations to Finance Crop Operations Form 9901 or 990-EZ8

(5) Labor, Agricultural, and Horticultural Organizations Form 9901 or 990-EZ8 501(c)(6) Business")

5 501(c)(17) Supplemental Unemployment Benefit Trusts Form 9901 or 990-EZ8 501(c)(18) Employee Funded Pension Trust (created before June 25, 1959) Form 9901 or 990-EZ8 501(c)(19) Post or Organization of Past or Present Members of the Armed Forces Form 9901 or 990-EZ8 501(c)(21) Black Lung Benefit Trusts Form 990-BL 501(c)(22) Withdrawal Liability Payment Fund Form 990 or 990-EZ8 501(c)(23) Veterans Organizations (created before 1880) Form 990 or 990-EZ8 501(c)(25) Title Holding Corporations or Trusts with Multiple Parents Form 990 or 990-EZ 501(c)(26) State-Sponsored Organization Providing Health Coverage for High-Risk Individuals Form 9901 or 990-EZ8 501(c)(27)11 State-Sponsored Workers' Compensation Reinsurance Organization Form 9901 or 990-EZ8 501(c)(28)12 National Railroad Retirement Investment Trust Not yet determined 501(d) Religious and Apostolic Associations Form (e) Cooperative Hospital Service Organizations Form 9901 or 990-EZ8 501(f) Cooperative Service Organizations of Operating Educational Organizations Form 9901 or 990-EZ8 501(k) Child Care Organizations Form 990 or 990-EZ8 501(n) Charitable Risk Pools Form 9901 or 990-EZ8 521(a) Farmers' Cooperative Associations Form 990-C 4947(a)(1) Non-Exempt Charitable Trusts Form 990-PF 4947(a)(2) Split-Interest Trust Form (c)(1) Government Entity None Ref: IRS Publication 557

(27)11 State-Sponsored Workers' Compensation Reinsurance Organization Form 9901 or 990-EZ8 501(c)(28)12 National")

6 Programs (Alliances) Programs (Alliances) IEEE-ISTO Federation of Programs (Business League) Programs (Alliances) Programs (Alliances) IEEE-ISTO collaborates with a wide range of groups to bring Industry standards to fruition and ensure their success in the market

7 Ø Purpose: To communicate relevant informa4on that sa4sfies the interest of members, creditors, and recipients. o o Useful in decision making regarding resource allocation o How much can we spend, can we afford it? Useful in evaluating the effectivity of the Program s Governing bodies (Board of Directors, Officers) in performing their duties and responsibilities

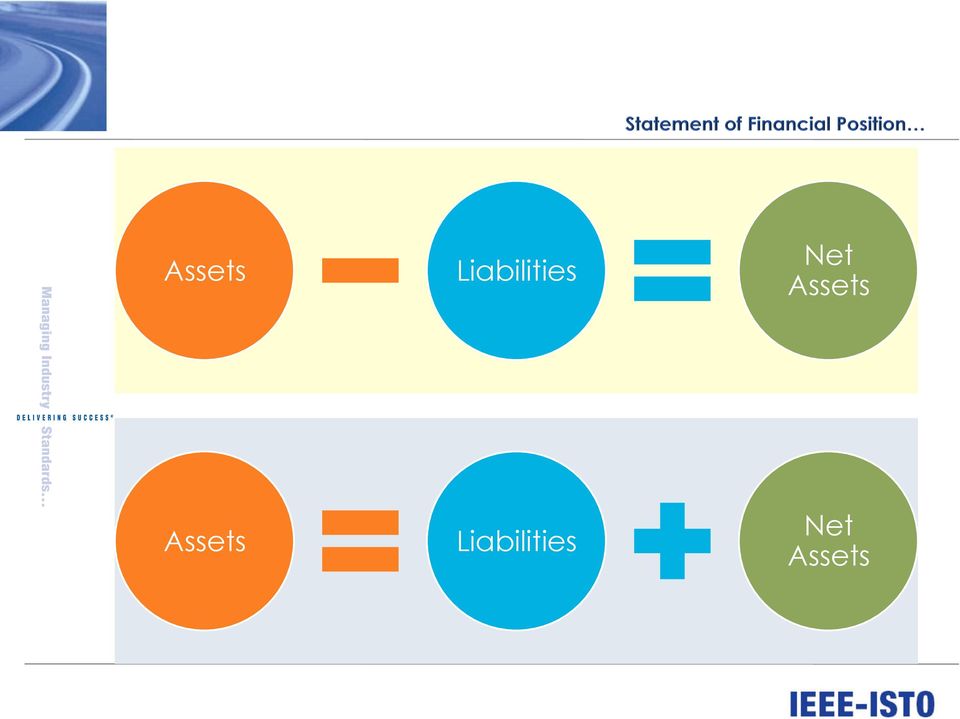

8 Statement of Financial Position = Balance Sheet Statement of Activities = Profit and Loss Program Financial Statements Statement of Cash flows Other schedules: Accounts Receivable Accounts Payable Budget vs. Actual

9 Cash Assets - membership fees collection Prepaid expenses - Insurance - Deposits for events etc. Other assets Liabilities Accounts payable - vendor invoices Deferred membership fees - unamortized portion of annual membership Other liabilities Net Assets (Net worth)

10 Assets Assets are economic resources owned by a business that are expected to benefit future operations. Cash in bank - consist of bank deposits - collections of accounts receivable Accounts Receivable - these are assets that arise from unpaid invoices issued to members. Membership fee(majority of receivable) Sponsorship invoices (for events, member meetings, etc.) Prepaid expenses prepayments for goods and services to be received/used in the near future. Insurance, airfare for future events, booth and hotel deposits. Other Assets

Prepaid expenses prepayments for goods and services to be received/used in the near future.")

11 Liabilities Liabilities are legal obligations that result from past transactions (to be paid in the future) or the future performance of services. v v Accounts payable short term obligations to suppliers/ vendors for goods and services received. Deferred Membership fees Deferred revenues are funds that are received for goods and services that have not yet been provided. When revenues are received in advance, the Company has an obligation to deliver goods or perform services. Therefore, deferred membership fees are shown in a liability account. Deferred revenue is not yet revenue. It is an amount that was received by a company in advance of earning it. The amount unearned (and therefore deferred) as of the date of the financial statements should be reported as a liability. When the goods or services are performed or delivered, revenue is recorded and liability is reduced.

12 Assets Liabilities Net Assets Assets Liabilities Net Assets

13 Program revenues Membership Revenues - By membership level Event sponsorship Meeting registration fee Program expenses Trade shows and conferences Legal fees Travel Marketing Etc. Change in Net assets (deficiency)

14 Statement of Cash Flows The purpose of the statement of cash flows is to provide information about a company s cash receipts and cash payments during an accounting period. v This statement adjust the net income(accrual basis) to reflect the actual cash flow that affected cash during the period.

to reflect the")

15 Example: Program name: XYZ Alliance Date of Invoice: November 2014 Member: ABC Tech. Co. Renewal invoice: $12,000 for Annual dues Membership period Jan. Dec November 2014: The full amount will be recorded as a receivable in XYZ Alliance and set up as Deferred membership fees. January 2015: $1k of the $12k membership will be recognized as membership income and deducted from the balance of the Deferred membership fees. February 2015: $1k of the $12k membership will be recognized as membership income and deducted from the balance of the Deferred membership fees. v 1/12 of $12,000 or $1,000 for each subsequent months is recognized as income until December 2015 covering the entire membership year (Jan. Dec.)until the $12k has been fully recognized for the entire membership period. v Collection of the invoice will be recorded as a cash receipt and a reduction in Accounts receivable balance.

16 Annual fees, $12K (for membership period Jan. Dec Dec., $1K Jan, $1K Nov, $1K Feb, $1K Oct., $1K Mar, $1K Sept., $1K April, $1K Aug, $1K May, $1k Jul, $1K June, $1K Revenue recognition: $12K divided by 12 months (no. of membership months)

17 Why Amortize? For proper matching of revenues against expenses Services, membership benefits Revenues

18 Accounting methods

19 IEEE-ISTO Finance team

Introduction to Tax-Exempt Status

State of California Franchise Tax Board Introduction to Tax-Exempt Status Some organizations that may apply for exemption status Business Leagues Cemeteries Chambers of Commerce Charitable Organizations

State of California Franchise Tax Board Introduction to Tax-Exempt Status Some organizations that may apply for exemption status Business Leagues Cemeteries Chambers of Commerce Charitable Organizations

CHAPTER 33 GAMBLING. The outcome is not in the control to any material degree of any person other than the player or players.

CHAPTER 33 GAMBLING 13-3301. Definitions In this chapter, unless the context otherwise requires: 1. "Amusement gambling" means gambling involving a device, game or contest which is played for entertainment

CHAPTER 33 GAMBLING 13-3301. Definitions In this chapter, unless the context otherwise requires: 1. "Amusement gambling" means gambling involving a device, game or contest which is played for entertainment

The credits for the work go to the hard work of the following individuals and their staff:

This downloadable e-book comes straight out of the Small to Mid-sized Workshop participant text books offered at Exempt Organization s workshops for small and midsize section 501(c)(3) exempt organizations.

This downloadable e-book comes straight out of the Small to Mid-sized Workshop participant text books offered at Exempt Organization s workshops for small and midsize section 501(c)(3) exempt organizations.

Economic Benefits of Michigan s Nonprofit Sector May 2014

Economic Benefits of Michigan s Nonprofit Sector May 2014 The following report was prepared for the Michigan Nonprofit Association and the Council of Michigan Foundations by Public Sector Consultants.

Economic Benefits of Michigan s Nonprofit Sector May 2014 The following report was prepared for the Michigan Nonprofit Association and the Council of Michigan Foundations by Public Sector Consultants.

California Franchise Tax Board

Examples of Exempt Organizations Business Leagues Cemeteries Chambers of Commerce Charitable Organizations Churches Civic Leagues Credit Unions Educational Organizations Employee Associations Fraternal

Examples of Exempt Organizations Business Leagues Cemeteries Chambers of Commerce Charitable Organizations Churches Civic Leagues Credit Unions Educational Organizations Employee Associations Fraternal

JAMISON MANAGEMENT AND DEVELOPMENT HC 68, Box 79-S, Gila Hot Springs, Silver City, New Mexico 575-536-9339 sznjmsn@gilanet.com

JAMISON MANAGEMENT AND DEVELOPMENT HC 68, Box 79-S, Gila Hot Springs, Silver City, New Mexico 575-536-9339 sznjmsn@gilanet.com Compiled by Suzanne Jamison for informational purposes only. This does not

JAMISON MANAGEMENT AND DEVELOPMENT HC 68, Box 79-S, Gila Hot Springs, Silver City, New Mexico 575-536-9339 sznjmsn@gilanet.com Compiled by Suzanne Jamison for informational purposes only. This does not

IOWA DEPARTMENT OF INSPECTIONS AND APPEALS SOCIAL AND CHARITABLE GAMBLING LICENSE APPLICATION

IOWA DEPARTMENT OF INSPECTIONS AND APPEALS SOCIAL AND CHARITABLE GAMBLING LICENSE APPLICATION Applicant Information: Please complete the information on behalf of the organization, business, or person for

IOWA DEPARTMENT OF INSPECTIONS AND APPEALS SOCIAL AND CHARITABLE GAMBLING LICENSE APPLICATION Applicant Information: Please complete the information on behalf of the organization, business, or person for

You Want to Form a Nonprofit Corporation in Vermont?

You Want to Form a nprofit Corporation in Vermont? what you should know before you do Dr. Jane A. Van Buren Last updated May 2012 onmark nprofit Services janevb@noonmarkservices.com www.noonmarkservices.com

You Want to Form a nprofit Corporation in Vermont? what you should know before you do Dr. Jane A. Van Buren Last updated May 2012 onmark nprofit Services janevb@noonmarkservices.com www.noonmarkservices.com

2. Corporations Fully Exempt These corporations qualify for the full income tax exemption:

T. Exempt Corporations (G.S. 105-125, G.S. 105-130.11, G.S. 105-130.12) 1. Preliminary Statement Some types of corporations are fully exempt from income and franchise taxes, whereas others are conditionally

T. Exempt Corporations (G.S. 105-125, G.S. 105-130.11, G.S. 105-130.12) 1. Preliminary Statement Some types of corporations are fully exempt from income and franchise taxes, whereas others are conditionally

LOUISIANA SALES TAX & NON-PROFIT ORGANIZATIONS

LOUISIANA SALES TAX & NON-PROFIT ORGANIZATIONS A Brief Overview of the Louisiana Sales Tax Laws and How they Apply to Non-Profit Organizations Presented by Cary B Bryson Bryson Law Firm, L.L.C. Sales Taxes:

LOUISIANA SALES TAX & NON-PROFIT ORGANIZATIONS A Brief Overview of the Louisiana Sales Tax Laws and How they Apply to Non-Profit Organizations Presented by Cary B Bryson Bryson Law Firm, L.L.C. Sales Taxes:

FOREWORD. 2014 by GuideStar USA All rights reserved. No part of this report may be reproduced in any form without written permission of GuideStar USA

SAPLE OREWORD GuideStar s mission is to revolutionize philanthropy and nonprofit practice by providing information that advances transparency, enables users to make better decisions, and encourages charitable

SAPLE OREWORD GuideStar s mission is to revolutionize philanthropy and nonprofit practice by providing information that advances transparency, enables users to make better decisions, and encourages charitable

IRS FORM 990. Removing the Smoke and Mirrors. Demystifying the 990. Kristy L. Spires, CPA, CAE, CGMA, IOM

IRS FORM 990 Removing the Smoke and Mirrors Kristy L. Spires, CPA, CAE, CGMA, IOM Demystifying the 990 COMPETENCY: BUSINESS Competency Level: Level 3: Agenda Driving Themes presentation is designed to

IRS FORM 990 Removing the Smoke and Mirrors Kristy L. Spires, CPA, CAE, CGMA, IOM Demystifying the 990 COMPETENCY: BUSINESS Competency Level: Level 3: Agenda Driving Themes presentation is designed to

Vol. 1, Chapter 3 - Accounting Adjustments

Vol. 1, Chapter 3 - Accounting Adjustments Problem 1 1. ($20,000 2,000) 48 = $375 per month 2. Jan. 31 Depreciation Expense $375 Accumulated Depreciation Van $375 To record depreciation expense for January

Vol. 1, Chapter 3 - Accounting Adjustments Problem 1 1. ($20,000 2,000) 48 = $375 per month 2. Jan. 31 Depreciation Expense $375 Accumulated Depreciation Van $375 To record depreciation expense for January

How To Account For Revenue Under Accrual Accounting

BAT 4M: Chapter 3 ANSWERS TO QUESTIONS 01. (a) Under the time period assumption, an accountant is required to determine the relevance of each business transaction to specific accounting periods, and its

BAT 4M: Chapter 3 ANSWERS TO QUESTIONS 01. (a) Under the time period assumption, an accountant is required to determine the relevance of each business transaction to specific accounting periods, and its

Charitable Registration Tool Tips

Charitable Registration Tool Tips Table of Contents Chapter 1 Online Charitable Registration... 3. Creating an ccount... 3 I. Employer Identification Number (EIN)... 3 II. Parent Organization... 3 III.

Charitable Registration Tool Tips Table of Contents Chapter 1 Online Charitable Registration... 3. Creating an ccount... 3 I. Employer Identification Number (EIN)... 3 II. Parent Organization... 3 III.

Nonprofit Board Excellence:

Nonprofit Board Excellence: Building a More Informed and Accountable Board A training workbook for boards of directors with a focus on nonprofit organizations in Washington State This workbook is the product

Nonprofit Board Excellence: Building a More Informed and Accountable Board A training workbook for boards of directors with a focus on nonprofit organizations in Washington State This workbook is the product

OPERATING FUND. PRELIMINARY & UNAUDITED FINANCIAL HIGHLIGHTS September 30, 2015 RENDELL L. JONES CHIEF FINANCIAL OFFICER

PRELIMINARY & UNAUDITED FINANCIAL HIGHLIGHTS September 30, 2015 RENDELL L. JONES CHIEF FINANCIAL OFFICER MANAGEMENT OVERVIEW September 30, 2015 Balance Sheet Cash and cash equivalents had a month-end balance

PRELIMINARY & UNAUDITED FINANCIAL HIGHLIGHTS September 30, 2015 RENDELL L. JONES CHIEF FINANCIAL OFFICER MANAGEMENT OVERVIEW September 30, 2015 Balance Sheet Cash and cash equivalents had a month-end balance

Income Tax Issues Affecting Small Nonprofit Organizations

Income Tax Issues Affecting Small Nonprofit Organizations A free resource provided by the Virginia Society of Certified Public Accountants 2 Income Tax Issues Affecting Small Nonprofit Organizations A

Income Tax Issues Affecting Small Nonprofit Organizations A free resource provided by the Virginia Society of Certified Public Accountants 2 Income Tax Issues Affecting Small Nonprofit Organizations A

CHAPTER 3. BE3-2 Advertising. Dec. 31 Advertising Supplies Expense 7200 Advertising Supplies 7200 to adjust. BE3-3 Bere Co.

CHAPTER 3 BE3-2 Advertising Advertising Supplies Supplies Expense 8700 7200 7200 1500 7200 Dec. Advertising Supplies Expense 7200 Advertising Supplies 7200 BE3-3 Bere Co. Prepaid Insurance Insurance Expense

CHAPTER 3 BE3-2 Advertising Advertising Supplies Supplies Expense 8700 7200 7200 1500 7200 Dec. Advertising Supplies Expense 7200 Advertising Supplies 7200 BE3-3 Bere Co. Prepaid Insurance Insurance Expense

AT&T Global Network Client for Windows Product Support Matrix January 29, 2015

AT&T Global Network Client for Windows Product Support Matrix January 29, 2015 Product Support Matrix Following is the Product Support Matrix for the AT&T Global Network Client. See the AT&T Global Network

AT&T Global Network Client for Windows Product Support Matrix January 29, 2015 Product Support Matrix Following is the Product Support Matrix for the AT&T Global Network Client. See the AT&T Global Network

Periodicity Assumption... Time Period Assumption... Chapter 4 Accrual Accounting Concepts

Financial Accounting: Tools for Business Decision Making, 4th Ed. CHAPTER 4 Kimmel, Weygandt, Kieso Chapter 4 Accrual Accounting Concepts KEY THINGS WE LL DO: Refresh and expand Ch.3 concepts. Differentiate

Financial Accounting: Tools for Business Decision Making, 4th Ed. CHAPTER 4 Kimmel, Weygandt, Kieso Chapter 4 Accrual Accounting Concepts KEY THINGS WE LL DO: Refresh and expand Ch.3 concepts. Differentiate

INVENTORY AND APPRAISEMENT OF COMMUNITY ESTATE OF THE PARTIES

INVENTORY AND APPRAISEMENT OF COMMUNITY ESTATE OF THE PARTIES 1. Real Property (include any property purchased by contract for deed, such as Texas Veterans Land Board property, property purchased in recreational

INVENTORY AND APPRAISEMENT OF COMMUNITY ESTATE OF THE PARTIES 1. Real Property (include any property purchased by contract for deed, such as Texas Veterans Land Board property, property purchased in recreational

ADVANCED PROSPECTING WITH THE FORM 5500. Brought to you by:

ADVANCED PROSPECTING WITH THE FORM 5500 Brought to you by: What is FreeERISA.com Signing Up The Form 5500 The 5500 is the annual DOL disclosure Form required for all ERISA qualified benefit plans Filed

ADVANCED PROSPECTING WITH THE FORM 5500 Brought to you by: What is FreeERISA.com Signing Up The Form 5500 The 5500 is the annual DOL disclosure Form required for all ERISA qualified benefit plans Filed

Non-Profit Status and Incorporation. LSU Alumni of San Diego, Inc.

Non-Profit Status and Incorporation LSU Alumni of San Diego, Inc. 1 For several years now, auditors and tax advisors have recommended that LSU Alumni Chapters apply for an EIN, attain non-profit status,

Non-Profit Status and Incorporation LSU Alumni of San Diego, Inc. 1 For several years now, auditors and tax advisors have recommended that LSU Alumni Chapters apply for an EIN, attain non-profit status,

The U.S. social welfare structure has been shaped both by long standing traditions and by changing economic and social conditions.

The U.S. social welfare structure has been shaped both by long standing traditions and by changing economic and social conditions. In its early history, the United States was an expanding country with

The U.S. social welfare structure has been shaped both by long standing traditions and by changing economic and social conditions. In its early history, the United States was an expanding country with

Instructions for Schedule L (Form 990 or 990-EZ)

") 2011 Instructions for Schedule L (Form 990 or 990-EZ) Transactions With Interested Persons Department of the Treasury Internal Revenue Service Section references are to the Internal do so, it must file

2011 Instructions for Schedule L (Form 990 or 990-EZ) Transactions With Interested Persons Department of the Treasury Internal Revenue Service Section references are to the Internal do so, it must file

Nonprofit Organization

Starting a Nonprofit Organization in New Jersey Questions and Answers New Jersey Division of of Taxation Technical Regulatory Services Activity Branch January August 2006 2002 Table of Contents Getting

Starting a Nonprofit Organization in New Jersey Questions and Answers New Jersey Division of of Taxation Technical Regulatory Services Activity Branch January August 2006 2002 Table of Contents Getting

Step 1 - Determine Eligibility

Step 1 - Determine Eligibility For a car donation to be eligible for a tax deduction, it must be made solely for charitable or public purposes by an individual who will itemize deduction on Schedule A

Step 1 - Determine Eligibility For a car donation to be eligible for a tax deduction, it must be made solely for charitable or public purposes by an individual who will itemize deduction on Schedule A

COMPARISON OF FIXED & VARIABLE RATES (25 YEARS) CHARTERED BANK ADMINISTERED INTEREST RATES - PRIME BUSINESS*

CHARTERED BANK ADMINISTERED INTEREST RATES - PRIME BUSINESS*") COMPARISON OF FIXED & VARIABLE RATES (25 YEARS) 2 Fixed Rates Variable Rates FIXED RATES OF THE PAST 25 YEARS AVERAGE RESIDENTIAL MORTGAGE LENDING RATE - 5 YEAR* (Per cent) Year Jan Feb Mar Apr May Jun

COMPARISON OF FIXED & VARIABLE RATES (25 YEARS) 2 Fixed Rates Variable Rates FIXED RATES OF THE PAST 25 YEARS AVERAGE RESIDENTIAL MORTGAGE LENDING RATE - 5 YEAR* (Per cent) Year Jan Feb Mar Apr May Jun

COMPARISON OF FIXED & VARIABLE RATES (25 YEARS) CHARTERED BANK ADMINISTERED INTEREST RATES - PRIME BUSINESS*

CHARTERED BANK ADMINISTERED INTEREST RATES - PRIME BUSINESS*") COMPARISON OF FIXED & VARIABLE RATES (25 YEARS) 2 Fixed Rates Variable Rates FIXED RATES OF THE PAST 25 YEARS AVERAGE RESIDENTIAL MORTGAGE LENDING RATE - 5 YEAR* (Per cent) Year Jan Feb Mar Apr May Jun

COMPARISON OF FIXED & VARIABLE RATES (25 YEARS) 2 Fixed Rates Variable Rates FIXED RATES OF THE PAST 25 YEARS AVERAGE RESIDENTIAL MORTGAGE LENDING RATE - 5 YEAR* (Per cent) Year Jan Feb Mar Apr May Jun

105-228.4: Recodified as 58-6-7 by Session Laws 1995, c. 360, s. 1(c).

.") Article 8B. Taxes Upon Insurance Companies. 105-228.3. Definitions. The following definitions apply in this Article: (1) Article 65 corporation. - A corporation subject to Article 65 of Chapter 58 of the

Article 8B. Taxes Upon Insurance Companies. 105-228.3. Definitions. The following definitions apply in this Article: (1) Article 65 corporation. - A corporation subject to Article 65 of Chapter 58 of the

INFORMATION BULLETIN #10 SALES TAX APRIL 2012. (Replaces Bulletin #10 dated June 2008)

") INFORMATION BULLETIN #10 SALES TAX APRIL 2012 (Replaces Bulletin #10 dated June 2008) DISCLAIMER: SUBJECT: Informational bulletins are intended to provide nontechnical assistance to the general public.

INFORMATION BULLETIN #10 SALES TAX APRIL 2012 (Replaces Bulletin #10 dated June 2008) DISCLAIMER: SUBJECT: Informational bulletins are intended to provide nontechnical assistance to the general public.

CHAPTER 9 Charitable Giving

CHAPTER 9 Charitable Giving DISCUSSION QUESTIONS 1. What factors must an individual consider before making a charitable gift? A donor needs to consider his charitable objectives and the desired timing

CHAPTER 9 Charitable Giving DISCUSSION QUESTIONS 1. What factors must an individual consider before making a charitable gift? A donor needs to consider his charitable objectives and the desired timing

FORM NP OCCUPATIONAL LICENSE TAX NET PROFIT RETURN

City of Henderson PO Box 671 Henderson, KY 42419-0671 OCCUPATIONAL LICENSE TAX NET PROFIT RETURN DUE APRIL 15TH OR THE 15TH DAY OF THE 4TH MONTH FOLLOWING THE CLOSE OF THE FEDERAL TAX YEAR FORM NP Name

City of Henderson PO Box 671 Henderson, KY 42419-0671 OCCUPATIONAL LICENSE TAX NET PROFIT RETURN DUE APRIL 15TH OR THE 15TH DAY OF THE 4TH MONTH FOLLOWING THE CLOSE OF THE FEDERAL TAX YEAR FORM NP Name

CONSUMER. Protecting Social Security and other Federal Benefits in Bank Accounts from Garnishment by Debt Collectors

CONSUMER Information for Advocates Representing Older Adults N a t i o n a l C o n s u m e r L a w C e n t e r CONCERNS Protecting Social Security and other Federal Benefits in Bank Accounts from Garnishment

CONSUMER Information for Advocates Representing Older Adults N a t i o n a l C o n s u m e r L a w C e n t e r CONCERNS Protecting Social Security and other Federal Benefits in Bank Accounts from Garnishment

Taxable profits from unrelated business

Unrelated Business Income of Nonprofit Organizations, 1997 by Margaret Riley 102 102 Taxable profits from unrelated business income reported by 39,302 nonprofit organizations on Forms 990-T, Exempt Organization

Unrelated Business Income of Nonprofit Organizations, 1997 by Margaret Riley 102 102 Taxable profits from unrelated business income reported by 39,302 nonprofit organizations on Forms 990-T, Exempt Organization

Working Capital and the Financing Decision C H A P T E R S I X

Working Capital and the Financing Decision C H A P T E R S I X Limited 2000 Figure 6-1a The nature of asset growth A. Stage I: Limited or no Growth PPT 6-1 Dollars Temporary current assets Capital assets

Working Capital and the Financing Decision C H A P T E R S I X Limited 2000 Figure 6-1a The nature of asset growth A. Stage I: Limited or no Growth PPT 6-1 Dollars Temporary current assets Capital assets

Business Organization\Tax Structure

Business Organization\Tax Structure One of the first decisions a new business owner faces is choosing a structure for the business. Businesses range in size and complexity, from someone who is self-employed

Business Organization\Tax Structure One of the first decisions a new business owner faces is choosing a structure for the business. Businesses range in size and complexity, from someone who is self-employed

CLIENT QUESTIONNAIRE - Inventory and Appraisement. Community Estate of the Parties

CLIENT NAME: [name] CLIENT QUESTIONNAIRE - Inventory and Appraisement. Community Estate of the Parties 1. Real Property (include any property purchased by contract for deed, such as Texas Veterans Land

CLIENT NAME: [name] CLIENT QUESTIONNAIRE - Inventory and Appraisement. Community Estate of the Parties 1. Real Property (include any property purchased by contract for deed, such as Texas Veterans Land

Short Form Return of Organization Exempt From Income Tax

Form 990-EZ PUBLIC DISCLOSURE COPY ** PUBLIC DISCLOSURE COPY ** Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(1) of the Internal Revenue Code (except private

Form 990-EZ PUBLIC DISCLOSURE COPY ** PUBLIC DISCLOSURE COPY ** Short Form Return of Organization Exempt From Income Tax Under section 501, 527, or 4947(1) of the Internal Revenue Code (except private

CHAPTER 7 GROUP LIFE INSURANCE

CHAPTER 7 GROUP LIFE INSURANCE Group insurance is one of the general categories of life insurance as noted in Chapter 3. Any life insurer may issue life, disability, term, and endowment insurance on a

CHAPTER 7 GROUP LIFE INSURANCE Group insurance is one of the general categories of life insurance as noted in Chapter 3. Any life insurer may issue life, disability, term, and endowment insurance on a

The General Journal and the General Ledger

4-1 McGraw-Hill 2009 The McGraw-Hill Companies, Inc. All rights reserved. Chapter 4 The General Journal and the General Ledger Section 1: The General Journal Section Objectives 1. Record transactions in

4-1 McGraw-Hill 2009 The McGraw-Hill Companies, Inc. All rights reserved. Chapter 4 The General Journal and the General Ledger Section 1: The General Journal Section Objectives 1. Record transactions in

A GUIDE TO MINNESOTA S CHARITIES LAWS

A GUIDE TO MINNESOTA S CHARITIES LAWS This Guide summarizes certain Minnesota laws that govern charitable organizations, professional fund-raisers and charitable trusts, including laws that require registration

A GUIDE TO MINNESOTA S CHARITIES LAWS This Guide summarizes certain Minnesota laws that govern charitable organizations, professional fund-raisers and charitable trusts, including laws that require registration

SOLUTIONS. Learning Goal 5

Learning Goal 5: Prepare Adjusting Entries for s S1 Learning Goal 5 Multiple Choice 1. b To record the supplies used up. 2. d To record the amount of revenue earned as time passes. 3. d 4. d Debit an expense,

Learning Goal 5: Prepare Adjusting Entries for s S1 Learning Goal 5 Multiple Choice 1. b To record the supplies used up. 2. d To record the amount of revenue earned as time passes. 3. d 4. d Debit an expense,

Chapter 9 - Current Liabilities. Accounting For Current Liabilities

Chapter 9 - Current Liabilities Accounting For Current Liabilities C 1 Defining Liabilities Because of a past event... The company has a present obligation... For future sacrifices Past Present Future

Chapter 9 - Current Liabilities Accounting For Current Liabilities C 1 Defining Liabilities Because of a past event... The company has a present obligation... For future sacrifices Past Present Future

MONTHLY REMINDERS FOR 2013

MONTHLY REMINDERS FOR 2013 Legend: Red IRS Due Dates Green Department of Revenue Due Dates Blue Parish Finance Due Dates Black Second Collections JANUARY 4 Deposit payroll tax for payments on Jan 1 if

MONTHLY REMINDERS FOR 2013 Legend: Red IRS Due Dates Green Department of Revenue Due Dates Blue Parish Finance Due Dates Black Second Collections JANUARY 4 Deposit payroll tax for payments on Jan 1 if

CLIENT NAME: CLIENT QUESTIONNAIRE - Inventory and Appraisement. Community Estate of the Parties. Current fair market value (as of ): $

: $") CLIENT NAME: CLIENT QUESTIONNAIRE - Inventory and Appraisement. Community Estate of the Parties 1. Real Property (include any property purchased by contract for deed, such as Texas Veterans Land Board

CLIENT NAME: CLIENT QUESTIONNAIRE - Inventory and Appraisement. Community Estate of the Parties 1. Real Property (include any property purchased by contract for deed, such as Texas Veterans Land Board

Income Tax Issues Affecting Small Nonprofit Organizations

Income Tax Issues Affecting Small Nonprofit Organizations A free resource provided by the Virginia Society of Certified Public Accountants 2 Income Tax Issues Affecting Small Nonprofit Organizations A

Income Tax Issues Affecting Small Nonprofit Organizations A free resource provided by the Virginia Society of Certified Public Accountants 2 Income Tax Issues Affecting Small Nonprofit Organizations A

Club Administration 101. The Basics of Club Operations and Management

Club Administration 101 The Basics of Club Operations and Management What Is A Soccer Club? A soccer club does many things: Service to the community Provides a place for kids to play Develops skills Teaches

Club Administration 101 The Basics of Club Operations and Management What Is A Soccer Club? A soccer club does many things: Service to the community Provides a place for kids to play Develops skills Teaches

SIPP Core and Topical Modules Organization and Issues

SIPP Core and Topical Modules Organization and Issues Jason Fields US Census Bureau Session 4: Designs that effectively mix global and detail information to reduce burden and measurement error. June 1-2,

SIPP Core and Topical Modules Organization and Issues Jason Fields US Census Bureau Session 4: Designs that effectively mix global and detail information to reduce burden and measurement error. June 1-2,

The Accounting Process

GAAP LITERATURE The Accounting Process Chapter 3 TRADITIONAL: Original pronouncements, issued by the FASB. SEPT. 2009 CHANGE: Codification issued by the FASB. DIFFERENCE: Codification is listed by topic

GAAP LITERATURE The Accounting Process Chapter 3 TRADITIONAL: Original pronouncements, issued by the FASB. SEPT. 2009 CHANGE: Codification issued by the FASB. DIFFERENCE: Codification is listed by topic

CLIENT QUESTIONNAIRE - Inventory and Appraisement. Community Estate of the Parties

CLIENT NAME: CLIENT QUESTIONNAIRE - Inventory and Appraisement. Community Estate of the Parties 1. Real Property (include any property purchased by contract for deed, such as Texas Veterans Land Board

CLIENT NAME: CLIENT QUESTIONNAIRE - Inventory and Appraisement. Community Estate of the Parties 1. Real Property (include any property purchased by contract for deed, such as Texas Veterans Land Board

COMPONENTS OF THE STATEMENT OF CASH FLOWS

ILLUSTRATION 24-1 OPERATING, INVESTING, AND FINANCING ACTIVITIES COMPONENTS OF THE STATEMENT OF CASH FLOWS CASH FLOWS FROM OPERATING ACTIVITIES + Sales and Service Revenue Received Cost of Sales Paid Selling

ILLUSTRATION 24-1 OPERATING, INVESTING, AND FINANCING ACTIVITIES COMPONENTS OF THE STATEMENT OF CASH FLOWS CASH FLOWS FROM OPERATING ACTIVITIES + Sales and Service Revenue Received Cost of Sales Paid Selling

A basic paycheque will show gross pay, deductions and net pay:

Accounting (HOSP 1860) Learning Centre Payroll Accounting Understanding payroll will help you as an or an. It explains all the deductions that are removed from your paycheque, where the numbers on your

Accounting (HOSP 1860) Learning Centre Payroll Accounting Understanding payroll will help you as an or an. It explains all the deductions that are removed from your paycheque, where the numbers on your

Guide to Starting Self Employment or Business. Guide No.6 in the Tax Guide Series

Guide to Starting Self Employment or Business Guide No.6 in the Tax Guide Series About This Guide This Guide has been prepared to help someone starting out in a new business or self employment venture

Guide to Starting Self Employment or Business Guide No.6 in the Tax Guide Series About This Guide This Guide has been prepared to help someone starting out in a new business or self employment venture

PRIVATE FOUNDATION CAUTION: The purposes of this memorandum are to assist you, the directors of your private foundation, and your accountant in:

CHERRY CREEK CORPORATE CENTER 4500 CHERRY CREEK DRIVE SOUTH #600 DENVER, CO 80246-1500 303.322.8943 WWW.WADEASH.COM DISCLAIMER Material presented on the Wade Ash Woods Hill & Farley, P.C., website is intended

CHERRY CREEK CORPORATE CENTER 4500 CHERRY CREEK DRIVE SOUTH #600 DENVER, CO 80246-1500 303.322.8943 WWW.WADEASH.COM DISCLAIMER Material presented on the Wade Ash Woods Hill & Farley, P.C., website is intended

Page 1287 TITLE 26 INTERNAL REVENUE CODE 419

Page 1287 TITLE 26 INTERNAL REVENUE CODE 419 into account the plan s recent and anticipated financial experience, that the plan s available resources are not sufficient to pay benefits under the plan when

Page 1287 TITLE 26 INTERNAL REVENUE CODE 419 into account the plan s recent and anticipated financial experience, that the plan s available resources are not sufficient to pay benefits under the plan when

Key Person Insurance. Protect your business from the loss of a key person with life insurance payable to the business.

Key Person Insurance Protect your business from the loss of a key person with life insurance payable to the business. We offer you this concept piece to help you understand how life insurance can be used

Key Person Insurance Protect your business from the loss of a key person with life insurance payable to the business. We offer you this concept piece to help you understand how life insurance can be used

CLIENT QUESTIONNAIRE - Inventory and Appraisement. INSTRUCTIONS: We prefer that you type up your answers separately, and just refer to the

CLIENT NAME: CLIENT QUESTIONNAIRE - Inventory and Appraisement. INSTRUCTIONS: We prefer that you type up your answers separately, and just refer to the Question #. You do not have to re-type the question.

CLIENT NAME: CLIENT QUESTIONNAIRE - Inventory and Appraisement. INSTRUCTIONS: We prefer that you type up your answers separately, and just refer to the Question #. You do not have to re-type the question.

Inventory and Appraisement of [Name of Party] Community Estate of the Parties

![Inventory and Appraisement of [Name of Party] Community Estate of the Parties](/thumbs/27/12153358.jpg "Inventory and Appraisement of [Name of Party] Community Estate of the Parties") Inventory and Appraisement of [Name of Party] [Name], [Petitioner/Respondent], submits this inventory and appraisement of all assets and liabilities, community and separate estates, as follows: Community

Inventory and Appraisement of [Name of Party] [Name], [Petitioner/Respondent], submits this inventory and appraisement of all assets and liabilities, community and separate estates, as follows: Community

FULLER LANDAU LLP. Tax Return Questionnaire - 2014 Tax Year. Name and Address: Social Security Occupation Number:

FULLER LANDAU LLP Print this form out, take some time to fill it out, and bring it with you when you come to the office. This will save you time and money, and help us help you more effectively. Tax Return

FULLER LANDAU LLP Print this form out, take some time to fill it out, and bring it with you when you come to the office. This will save you time and money, and help us help you more effectively. Tax Return

Impacts of Government Jobs in Lake County Oregon

Impacts of Government Jobs in Lake County Oregon April 2011 Prepared by Betty Riley, Executive Director South Central Oregon Economic Development District Annual Average Pay Based on Oregon Labor Market

Impacts of Government Jobs in Lake County Oregon April 2011 Prepared by Betty Riley, Executive Director South Central Oregon Economic Development District Annual Average Pay Based on Oregon Labor Market

1040 U.S. Individual Income Tax Return 2015

Form - (99) 1040 U.S. Individual Tax Return For the year Jan. 1-Dec. 31,, or other tax year beginning,, ending, 20 Your first name and initial Last name If a joint return, spouse's first name and initial

Form - (99) 1040 U.S. Individual Tax Return For the year Jan. 1-Dec. 31,, or other tax year beginning,, ending, 20 Your first name and initial Last name If a joint return, spouse's first name and initial

THE INSURANCE CODE OF 1956 (EXCERPT)

") THE INSURANCE CODE OF 1956 (EXCERPT) Act 218 of 1956 CHAPTER 44 GROUP LIFE INSURANCE 500.4400 Scope of chapter; compliance required. Sec. 4400. (1) This chapter applies only with respect to group life

THE INSURANCE CODE OF 1956 (EXCERPT) Act 218 of 1956 CHAPTER 44 GROUP LIFE INSURANCE 500.4400 Scope of chapter; compliance required. Sec. 4400. (1) This chapter applies only with respect to group life

MITSUI SUMITOMO INSURANCE COMPANY, LIMITED AND SUBSIDIARIES. CONSOLIDATED BALANCE SHEETS March 31, 2005 and 2006

CONSOLIDATED BALANCE SHEETS March 31, 2005 and 2006 2005 2006 ASSETS Investments - other than investments in affiliates: Securities available for sale: Fixed maturities, at fair value 3,043,851 3,193,503

CONSOLIDATED BALANCE SHEETS March 31, 2005 and 2006 2005 2006 ASSETS Investments - other than investments in affiliates: Securities available for sale: Fixed maturities, at fair value 3,043,851 3,193,503

Internal Revenue Service Tax Exempt and Government Entities Exempt Organizations. Applying for 501(c)(3) Tax-Exempt Status

(3) Tax-Exempt Status") Internal Revenue Service Tax Exempt and Government Entities Exempt Organizations Applying for 501(c)(3) Tax-Exempt Status 01 Why apply for 501(c)(3) status?... 2 Who is eligible for 501(c)(3) status?....

Internal Revenue Service Tax Exempt and Government Entities Exempt Organizations Applying for 501(c)(3) Tax-Exempt Status 01 Why apply for 501(c)(3) status?... 2 Who is eligible for 501(c)(3) status?....

Analysis One Code Desc. Transaction Amount. Fiscal Period

Analysis One Code Desc Transaction Amount Fiscal Period 57.63 Oct-12 12.13 Oct-12-38.90 Oct-12-773.00 Oct-12-800.00 Oct-12-187.00 Oct-12-82.00 Oct-12-82.00 Oct-12-110.00 Oct-12-1115.25 Oct-12-71.00 Oct-12-41.00

Analysis One Code Desc Transaction Amount Fiscal Period 57.63 Oct-12 12.13 Oct-12-38.90 Oct-12-773.00 Oct-12-800.00 Oct-12-187.00 Oct-12-82.00 Oct-12-82.00 Oct-12-110.00 Oct-12-1115.25 Oct-12-71.00 Oct-12-41.00

Cash and Accrual Basis Accounting

Earn 2 CE credits This course was written for dentists, dental hygienists, and assistants. Cash and Accrual Basis Accounting (Keeping Two Sets of Books Could be a Good Thing) A Peer-Reviewed Publication

Earn 2 CE credits This course was written for dentists, dental hygienists, and assistants. Cash and Accrual Basis Accounting (Keeping Two Sets of Books Could be a Good Thing) A Peer-Reviewed Publication

What s News in Tax Analysis That Matters from Washington National Tax

What s News in Tax Analysis That Matters from Washington National Tax Health Insurance Companies and Employers: There s a New Fee to Consider A new fee may apply to issuers of health insurance policies

What s News in Tax Analysis That Matters from Washington National Tax Health Insurance Companies and Employers: There s a New Fee to Consider A new fee may apply to issuers of health insurance policies

The Pension Benefits Regulations, 1993

1 The Pension Benefits Regulations, 1993 being Chapter P-6.001 Reg 1 (effective January 1, 1993) as amended by an Errata Notice (published in The Saskatchewan Gazette August 27, 1993) and by Saskatchewan

1 The Pension Benefits Regulations, 1993 being Chapter P-6.001 Reg 1 (effective January 1, 1993) as amended by an Errata Notice (published in The Saskatchewan Gazette August 27, 1993) and by Saskatchewan

Instructions for Schedule L (Form 990 or 990-EZ)

") 2010 Instructions for Schedule L (Form 990 or 990-EZ) Transactions With Interested Persons Department of the Treasury Internal Revenue Service State whether the transaction has been Section references

2010 Instructions for Schedule L (Form 990 or 990-EZ) Transactions With Interested Persons Department of the Treasury Internal Revenue Service State whether the transaction has been Section references

Texas Nonprofit Sector: Describing the Size & Scope

Texas Nonprofit Sector: Describing the Size & Scope AUTHORS William Brown Suyeon Jo Fredrik O. Andersson September 2013 4220 TAMU College Station, TX 77843-4220 Acknowledgements This report is part of

Texas Nonprofit Sector: Describing the Size & Scope AUTHORS William Brown Suyeon Jo Fredrik O. Andersson September 2013 4220 TAMU College Station, TX 77843-4220 Acknowledgements This report is part of

501 (c)(3) TAX EXEMPTION

(3) TAX EXEMPTION") 501 (c)(3) TAX EXEMPTION 501(c) Tax Exemption What is 501 (c)(3)? Should we be a 501 (c)(3)? How do we get 501 (c)(3) status? Who is eligible under 501(c)(3)? By-Laws Requirements How to Apply Responding

501 (c)(3) TAX EXEMPTION 501(c) Tax Exemption What is 501 (c)(3)? Should we be a 501 (c)(3)? How do we get 501 (c)(3) status? Who is eligible under 501(c)(3)? By-Laws Requirements How to Apply Responding

Income Tax Guide to the Non-Profit Organization (NPO) Information Return

Information Return") Income Tax Guide to the Non-Profit Organization (NPO) Information Return Includes Form T1044 T4117 (E) Rev. 10 Is this guide for you? This guide is for you if you represent an organization that is: a non-profit

Income Tax Guide to the Non-Profit Organization (NPO) Information Return Includes Form T1044 T4117 (E) Rev. 10 Is this guide for you? This guide is for you if you represent an organization that is: a non-profit

Sample Only. Grant & Aid Application For the School Year Beginning Fall 2012. Save Time Apply Online. Information needed to complete your application:

10000028406 Save Time Apply Online. Apply online at www.factstuitionaid.com - Applying online is the fastest and most direct method of submitting your application. It allows your institution to view your

10000028406 Save Time Apply Online. Apply online at www.factstuitionaid.com - Applying online is the fastest and most direct method of submitting your application. It allows your institution to view your

FINANCIAL & ESTATE PLANNING ORGANIZER. R.W. Rogé & Company, Inc.

FINANCIAL & ESTATE PLANNING ORGANIZER Blank FINANCIAL & ESTATE PLANNING ORGANIZER In order to simplify matters, the following pages of financial and estate planning information serve to aid my family in

FINANCIAL & ESTATE PLANNING ORGANIZER Blank FINANCIAL & ESTATE PLANNING ORGANIZER In order to simplify matters, the following pages of financial and estate planning information serve to aid my family in

GAMING PUBLICATION TAX-EXEMPT ORGANIZATIONS FOR. Pub. 3079 (4-98) Cat. No. 25706L

Cat. No. 25706L") Pub. 3079 (4-98) Cat. No. 25706L GAMING PUBLICATION FOR TAX-EXEMPT ORGANIZATIONS This page was left blank intentionally. Please go to next page. GAMING PUBLICATION FOR TAX-EXEMPT ORGANIZATIONS TaBLE OF

Pub. 3079 (4-98) Cat. No. 25706L GAMING PUBLICATION FOR TAX-EXEMPT ORGANIZATIONS This page was left blank intentionally. Please go to next page. GAMING PUBLICATION FOR TAX-EXEMPT ORGANIZATIONS TaBLE OF

Legislative Brief: PAY OR PLAY PENALTIES LOOK BACK MEASUREMENT METHOD EXAMPLES. EmPowerHR

EmPowerHR Legislative Brief: PAY OR PLAY PENALTIES LOOK BACK MEASUREMENT METHOD EXAMPLES The Affordable Care Act (ACA) imposes a penalty on applicable large employers (ALEs) that do not offer health insurance

EmPowerHR Legislative Brief: PAY OR PLAY PENALTIES LOOK BACK MEASUREMENT METHOD EXAMPLES The Affordable Care Act (ACA) imposes a penalty on applicable large employers (ALEs) that do not offer health insurance

SAMPLE ONLY. FACTS Grant & Aid Application For the School Year Beginning Fall 2015. Save Time Apply Online.

10000028406 Save Time Apply Online. Apply online at online.factsmgt.com/aid w available in Spanish. Applying online allows your institution to view your application electronically within minutes of submission.

10000028406 Save Time Apply Online. Apply online at online.factsmgt.com/aid w available in Spanish. Applying online allows your institution to view your application electronically within minutes of submission.

PUBLIC. Am ''Ie A. sion 3Cc)l\ Ü. AUG i 0 1998. Facts RESPONSE OF THE OFFICE OF INSURANCE PRODUCTS DIVISION OF INVESTMENT MANAGEMENT

l\ Ü. AUG i 0 1998. Facts RESPONSE OF THE OFFICE OF INSURANCE PRODUCTS DIVISION OF INVESTMENT MANAGEMENT") PUBLIC Am ''Ie A sion 3Cc)l\ Ü BU ~ J) JJ~ ~ iò 9'3". ~ AUG i 0 1998 RESPONSE OF THE OFFICE OF INSURANCE PRODUCTS DIVISION OF INVESTMENT MANAGEMENT OUf-Reference No. IP-1-98 Massachusetts Mutual Life Insurance

PUBLIC Am ''Ie A sion 3Cc)l\ Ü BU ~ J) JJ~ ~ iò 9'3". ~ AUG i 0 1998 RESPONSE OF THE OFFICE OF INSURANCE PRODUCTS DIVISION OF INVESTMENT MANAGEMENT OUf-Reference No. IP-1-98 Massachusetts Mutual Life Insurance

- - If this claim is awarded, do you want a password to use SSA's Internet/phone service? Yes

SOCIAL SECURITY ADMINISTRATION APPLICATION FOR RETIREMENT INSURANCE BENEFITS TEL TOE 120/145/155 Form Approved OMB. 0960-0618 (Do not write in this space) I apply for all insurance benefits for which I

SOCIAL SECURITY ADMINISTRATION APPLICATION FOR RETIREMENT INSURANCE BENEFITS TEL TOE 120/145/155 Form Approved OMB. 0960-0618 (Do not write in this space) I apply for all insurance benefits for which I

Accounting Cycle. Matching Principle

CHAPTER 3 Accounting Cycle Analyze and record the transactions Post the transactions and prepare trial balance Adjust the accounts and prepare trial balance Prepare the financial statements Close the accounts

CHAPTER 3 Accounting Cycle Analyze and record the transactions Post the transactions and prepare trial balance Adjust the accounts and prepare trial balance Prepare the financial statements Close the accounts

BUSINESS PLAN GUIDE. Send completed business plans to:

BUSINESS PLAN GUIDE Send completed business plans to: Waubetek Business Development Corporation 6 Rainbow Ridge Road P.O. Box 209 Birch Island, ON P0P 1A0 1-800-665-2248 toll-free (705) 285-4275 phone

BUSINESS PLAN GUIDE Send completed business plans to: Waubetek Business Development Corporation 6 Rainbow Ridge Road P.O. Box 209 Birch Island, ON P0P 1A0 1-800-665-2248 toll-free (705) 285-4275 phone

Expense Section No. 700

Expense Section No. 700 Page No. GENERAL RULES FOR RECORDING EXPENSES 1 OPERATING EXPENSES (GL Control Account) 1 Approval Of 1 Entries in the Journal and Cash Record 2 Postings in the General Ledger 2

Expense Section No. 700 Page No. GENERAL RULES FOR RECORDING EXPENSES 1 OPERATING EXPENSES (GL Control Account) 1 Approval Of 1 Entries in the Journal and Cash Record 2 Postings in the General Ledger 2

INVENTORY AND APPRAISEMENT., files this inventory and appraisement of all assets and COMMUNITY PROPERTY

INVENTORY AND APPRAISEMENT OF, files this inventory and appraisement of all assets and liabilities, community and separate estates, as follows: COMMUNITY PROPERTY 1. REAL PROPERTY (including any property

INVENTORY AND APPRAISEMENT OF, files this inventory and appraisement of all assets and liabilities, community and separate estates, as follows: COMMUNITY PROPERTY 1. REAL PROPERTY (including any property

Guidance for companies, trusts and partnerships on completing a self-certification form

Guidance for companies, trusts and partnerships on completing a self-certification form In order to combat tax evasion by both individuals and businesses, the UK and many other countries have entered into

Guidance for companies, trusts and partnerships on completing a self-certification form In order to combat tax evasion by both individuals and businesses, the UK and many other countries have entered into

ONLY. FACTS Grant & Aid Application For the School Year Beginning Fall 2014. Save Time Apply Online.

10000028406 Save Time Apply Online. Apply online at online.factsmgt.com/aid w available in Spanish. Applying online allows your institution to view your application electronically within minutes of submission.

10000028406 Save Time Apply Online. Apply online at online.factsmgt.com/aid w available in Spanish. Applying online allows your institution to view your application electronically within minutes of submission.

YEARLY ANALYSIS SHEET - CASH RECEIPTS 20

YEARLY ANALYSIS SHEET - CASH RECEIPTS 20 Name: (Unit/District/Division/Region/Support Group/District Management Team) Month 5 6 7 8 9 10 11 12 13 14 15 JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC TOTAL

YEARLY ANALYSIS SHEET - CASH RECEIPTS 20 Name: (Unit/District/Division/Region/Support Group/District Management Team) Month 5 6 7 8 9 10 11 12 13 14 15 JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC TOTAL

SUBCHAPTER XI. GENERAL POLICE REGULATIONS.

SUBCHAPTER XI. GENERAL POLICE REGULATIONS. Article 37. Lotteries, Gaming, Bingo and Raffles. Part 2. Bingo and Raffles. 14-309.5. Bingo. (a) The purpose of the conduct of bingo is to insure a maximum availability

SUBCHAPTER XI. GENERAL POLICE REGULATIONS. Article 37. Lotteries, Gaming, Bingo and Raffles. Part 2. Bingo and Raffles. 14-309.5. Bingo. (a) The purpose of the conduct of bingo is to insure a maximum availability

Employee Relations L A W J O U R N A L

Employee Relations L A W J O U R N A L Reprinted from Employee Relations Law Journal, Volume 29, No. 1 Summer 2003, pages 83-95, with permission from Aspen Publishers Inc., a Wolters Kluwer business, New

Employee Relations L A W J O U R N A L Reprinted from Employee Relations Law Journal, Volume 29, No. 1 Summer 2003, pages 83-95, with permission from Aspen Publishers Inc., a Wolters Kluwer business, New

Financial Ratio Operating Statistics SURVEY

2013 Financial Ratio Operating Statistics SURVEY Compare your own numbers to the national norms, and find out where you need to focus to increase your profits. Balance Sheet Prior Year Assets Current Assets

2013 Financial Ratio Operating Statistics SURVEY Compare your own numbers to the national norms, and find out where you need to focus to increase your profits. Balance Sheet Prior Year Assets Current Assets

Financial Statement Consolidation

Financial Statement Consolidation We will consolidate the previously completed worksheets in this financial plan. In order to complete this section of the plan, you must have already completed all of the

Financial Statement Consolidation We will consolidate the previously completed worksheets in this financial plan. In order to complete this section of the plan, you must have already completed all of the

Christian Brothers Academy

Christian Brothers Academy Syracuse, NY 2016-2017 STUDENT FINANCIAL AID APPLICATION This form must be postmarked on or before 1/31/16 Information needed to complete your application: * Copies of your complete

Christian Brothers Academy Syracuse, NY 2016-2017 STUDENT FINANCIAL AID APPLICATION This form must be postmarked on or before 1/31/16 Information needed to complete your application: * Copies of your complete

Case 2:08-cv-02463-ABC-E Document 1-4 Filed 04/15/2008 Page 1 of 138. Exhibit 8

Case 2:08-cv-02463-ABC-E Document 1-4 Filed 04/15/2008 Page 1 of 138 Exhibit 8 Case 2:08-cv-02463-ABC-E Document 1-4 Filed 04/15/2008 Page 2 of 138 Domain Name: CELLULARVERISON.COM Updated Date: 12-dec-2007

Case 2:08-cv-02463-ABC-E Document 1-4 Filed 04/15/2008 Page 1 of 138 Exhibit 8 Case 2:08-cv-02463-ABC-E Document 1-4 Filed 04/15/2008 Page 2 of 138 Domain Name: CELLULARVERISON.COM Updated Date: 12-dec-2007

Financial Statements. Canadian Baptist Ministries December 31, 2014

Financial Statements Canadian Baptist Ministries INDEPENDENT AUDITORS' REPORT To the Members of Canadian Baptist Ministries We have audited the accompanying financial statements of Canadian Baptist Ministries,

Financial Statements Canadian Baptist Ministries INDEPENDENT AUDITORS' REPORT To the Members of Canadian Baptist Ministries We have audited the accompanying financial statements of Canadian Baptist Ministries,

Managing Your Money: A Family Plan

Managing Your Money: A Family Plan Managing Your Money: A Family Plan Everyone wants enough money to live on. Many people feel they need more. Use money to help get what you want by the following: making

Managing Your Money: A Family Plan Managing Your Money: A Family Plan Everyone wants enough money to live on. Many people feel they need more. Use money to help get what you want by the following: making

Business Organization\Tax Structure

Business Organization\Tax Structure Kansas Secretary of State s Office Business Services Division First Floor, Memorial Hall 120 S.W. 10th Avenue Topeka, KS 66612-1594 Phone: (785) 296-4564 Fax: (785)

Business Organization\Tax Structure Kansas Secretary of State s Office Business Services Division First Floor, Memorial Hall 120 S.W. 10th Avenue Topeka, KS 66612-1594 Phone: (785) 296-4564 Fax: (785)

Lane County, Oregon Statement of Net Assets June 30, 2010. Governmental Activities. Business-type

Statement of Net Assets June 30, 2010 Governmental Activities Business-type Activities Assets Current assets Cash and cash equivalents $ 152,238,503 $ 32,077,526 $ 184,316,029 Investments - 3,748,272 3,748,272

Statement of Net Assets June 30, 2010 Governmental Activities Business-type Activities Assets Current assets Cash and cash equivalents $ 152,238,503 $ 32,077,526 $ 184,316,029 Investments - 3,748,272 3,748,272

Midterm Fall 2012 Solution

Midterm Fall 2012 Solution Instructions: 1) Answers for the multiple-choice questions must be recorded on the UW answer card. All other questions must be answered in the space provided on the examination

Midterm Fall 2012 Solution Instructions: 1) Answers for the multiple-choice questions must be recorded on the UW answer card. All other questions must be answered in the space provided on the examination

Major and Planned Gifts Fact Sheets

Comparison of Life Income Gifts Charitable Gift Annuity vs. Charitable Remainder Trust Rescue Rehab Rehome Major and Planned Gifts Fact Sheets Major and Planned Gifts Overview Beneficiary Designations

Comparison of Life Income Gifts Charitable Gift Annuity vs. Charitable Remainder Trust Rescue Rehab Rehome Major and Planned Gifts Fact Sheets Major and Planned Gifts Overview Beneficiary Designations