IRA Tax Fundamentals and Strategies

|

|

|

- Pauline Harris

- 10 years ago

- Views:

Transcription

1 IRA Tax Fundamentals and Strategies

2 Today s Objectives Today I ll demonstrate how you can improve your legacy by describing what IRA investors typically do, & comparing it to two simple but powerful ideas so you can maximize your IRA legacy potential 2

3 30 Years Ago Sources of Retirement Cash Flow Pension Social Security Savings Pension Social Security Savings 30 Years Pension Social Security Savings Today 3

4 The dilemma Many people who have been successful in saving for retirement have established a large enough nest-egg to be able to create a legacy for their children, grandchildren and favorite charities, leaving them to wonder how to best leverage their qualified or tax advantaged retirement plans. A common question is whether IRA owners should take larger withdrawals and pay income taxes now, or whether they should take out as little as possible during their lifetime, leaving a likely income tax burden for their heirs and beneficiaries. 4

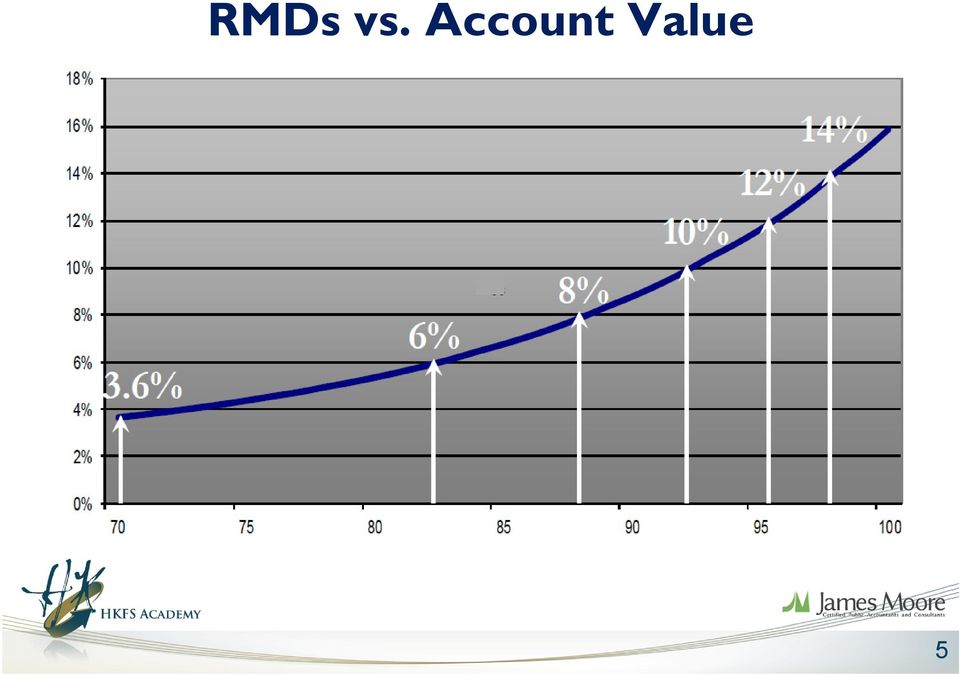

5 RMDs vs. Account Value 5

6 Projected IRA Values $160,000 $140,000 $120,000 $100,000 $80,000 $60,000 $40,000 $20,000 $ $100,000 IRA; 7% hypothetical annual return 6

7 Age Uniform Table Divisor Single-Life Table Divisor RMD Table Age Uniform Table Divisor Single-Life Table Divisor Age Uniform Table Divisor Single-Life Table Divisor

8 I.R.D. Income in Respect of a Decedent

9 IRD: The Bad News Is No step-up in basis at death 2. Beneficiary pays income tax at owner s death Taxes are calculated at Beneficiary s tax rate 3. Deceased IRA owner must include the entire IRA value in his / her estate for estate taxes Even though the $$ pass directly to the designated beneficiary! This is what s known as the Double-Tax 9

10 IRD: The Good News Is... You can overcome these problems, and... The IRS gives you tools to do it! 1. Stretch the inheritance to spread the taxes over many years and continue tax deferral 2. Consider charitable beneficiaries 3. NUA Net Unrealized Appreciation 4. IRD Deduction: Beneficiary receives an income tax deduction for estate taxes paid by owner 10

11 Estate Taxes & IRD IRA values included in decedent s gross estate Decedent s estate pays the estate taxes Beneficiary pays the income taxes Unlimited Marital Deduction (since 1982) Allows first-decedent-spouse to pass IRA to surviving spouse without incurring estate tax IRD income-tax-deduction for beneficiary s For the estate taxes attributable to the IRA The Problem??? Decedent s CPA vs. Beneficiary s CPA 11

12 IRA Estate Tax Example: Theory vs. Reality Decedent Beneficiary IRA Value: $1,000,000 $1,000,000 Estate Tax (40%): $400,000 $0 Net Value: $600,000 $1,000,000 Income Tax (40%): $0 $400,000 Total Taxes: $800,000 % Lost to Tax: 80% 12

: $0 $400,000 Total")

13 IRA Estate Tax Example: Theory vs. Reality Decedent Beneficiary IRA Value: $1,000,000 $1,000,000 Estate Tax (40%): $400,000 $0 Net Value: $600,000 $1,000,000 Income Tax (40%): $0 $400,000 Total Taxes: $800,000 % Lost to Tax: 80% 13

: $0 $400,000 Total")

14 IRA Estate Tax Example: Theory vs. Reality Estate Tax Income Tax Net Remaining Estate Tax Income Tax Net Remaining 14

15 Estate Tax Exclusion: Then and Now 1997: $600,000 Per Person 2014: $5,340,000 Per Person 15

16 Stretching The IRD Deduction Recall the previous example: IRA Value = $1,000,000 Estate Tax (40%) = $400,000 Creates IRD deduction of 40% of the asset Children inherit $1,000,000 Stretch = $80,000 per year for 30 years (over-simplified) Estate Tax Deduction = 40% So 40% of each stretch payment is excused from income tax until the deduction is used up Each stretch payment is 40% income-tax-free for 12.5 years! Unlimited deduction carry-forward Can amend prior 3-years tax-returns 16

17 2 IRA Wealth Transfer Strategies

18 Typical IRA Transfer IRA Owner(s) Children Grandchildren 18

19 Typical IRA Transfer IRA Owner(s) $500,000 Children $300,000 Grandchildren 19

20 RMD s 1. IRA Income Tax Offset IRA Life Insurance (equal to taxes) Beneficiaries Taxes 20

")

21 1. IRA Income Tax Offset RMD s IRA $500,000 Life Insurance $200,000 Beneficiaries $500,000 Taxes 21

22 2. IRA Income Tax Elimination RMD s IRA Life Insurance (equal to IRA) Charity Beneficiaries 22

23 2. IRA Income Tax Elimination IRA $500,000 RMD s Life Insurance $500,000 Charity $500,000 Beneficiaries Tax-Free Total: $1,000,000 23

24 Comparison of Strategies Total Net After-Tax Legacy 24

25 IRA Beneficiary Income Tax Elimination Comparison 25

26 The Soft Close I know you qualify for this program financially, but... I don t know if you qualify medically. You have time to think about it. 26

27 IRA Tax Fundamentals and Strategies Advisory services offered through Honkamp Krueger Financial Services, Inc., a Registered Investment Advisor.

IRA Maximization. Wealth transfer strategies to enhance your legacy CLC.1124 (05.14)

") Maximization Wealth transfer strategies to enhance your legacy CLC.1124 (05.14) Congratulations! For many years you ve put in the hard work planning, saving and investing for retirement. With all of that

Maximization Wealth transfer strategies to enhance your legacy CLC.1124 (05.14) Congratulations! For many years you ve put in the hard work planning, saving and investing for retirement. With all of that

The Advantages of a Stretch IRA

Lifetime Retirement Planning with Wachovia Securities. The Advantages of a Stretch IRA Much is being heard these days about a concept called the Stretch IRA. This phrase is bandied about as being the answer

Lifetime Retirement Planning with Wachovia Securities. The Advantages of a Stretch IRA Much is being heard these days about a concept called the Stretch IRA. This phrase is bandied about as being the answer

USING IRA ASSETS TO ADDRESS YOUR WEALTH TRANSFER GOALS

U.S. TRUST FIDUCIARY SERVICES FOR MERRILL LYNCH CLIENTS USING IRA ASSETS TO ADDRESS YOUR WEALTH TRANSFER GOALS Trusteed IRAs from U.S. Trust Working together, Merrill Lynch and U.S. Trust bring you the

U.S. TRUST FIDUCIARY SERVICES FOR MERRILL LYNCH CLIENTS USING IRA ASSETS TO ADDRESS YOUR WEALTH TRANSFER GOALS Trusteed IRAs from U.S. Trust Working together, Merrill Lynch and U.S. Trust bring you the

Inheriting retirement assets as a nonspouse beneficiary

Inheriting retirement assets as a nonspouse beneficiary When you inherit IRAs or other retirement plan assets, you will have many planning and distribution considerations. Some of your decisions will be

Inheriting retirement assets as a nonspouse beneficiary When you inherit IRAs or other retirement plan assets, you will have many planning and distribution considerations. Some of your decisions will be

Distributions and Rollovers from

Page 1 of 6 Frequently Asked Questions about Distributions and Rollovers from Retirement Accounts Choosing what to do with your retirement savings is an important decision. Tax implications are just one

Page 1 of 6 Frequently Asked Questions about Distributions and Rollovers from Retirement Accounts Choosing what to do with your retirement savings is an important decision. Tax implications are just one

Beneficiary Planning Investor Guide. Design a plan for you and your beneficiaries

Beneficiary Planning Investor Guide Design a plan for you and your beneficiaries Today is an important day. It is the day you will develop a comprehensive beneficiary plan that will let you relax, knowing

Beneficiary Planning Investor Guide Design a plan for you and your beneficiaries Today is an important day. It is the day you will develop a comprehensive beneficiary plan that will let you relax, knowing

Frequently asked questions

Page 1 of 6 Frequently asked questions Distributions and rollovers from retirement accounts Choosing what to do with your retirement savings is an important decision. Tax implications are just one of several

Page 1 of 6 Frequently asked questions Distributions and rollovers from retirement accounts Choosing what to do with your retirement savings is an important decision. Tax implications are just one of several

Stretch IRA. What is a stretch IRA? Why stretch?

Stretch IRA Stretch IRA strategies are a popular approach to transferring wealth. Investors are using stretch IRAs to extend their required minimum distributions (RMDs) over an increased period of time,

Stretch IRA Stretch IRA strategies are a popular approach to transferring wealth. Investors are using stretch IRAs to extend their required minimum distributions (RMDs) over an increased period of time,

Estate Planning for Retirement Benefits

Estate Planning for Retirement Benefits April Caudill, J.D., CLU, ChFC, AEP Senior Advanced Planning Attorney Advanced Financial Security Planning Northwestern Mutual The Northwestern Mutual Life Insurance

Estate Planning for Retirement Benefits April Caudill, J.D., CLU, ChFC, AEP Senior Advanced Planning Attorney Advanced Financial Security Planning Northwestern Mutual The Northwestern Mutual Life Insurance

Retirement Plan Distributions Choices & Opportunities

Retirement Plan Distributions Choices & Opportunities Leaving Your Job: Things to Think About» What you want to do next Work full time? Part time? Retire? How much will your lifestyle cost?» Continuing

Retirement Plan Distributions Choices & Opportunities Leaving Your Job: Things to Think About» What you want to do next Work full time? Part time? Retire? How much will your lifestyle cost?» Continuing

To Roth or Not Revised September 2013

Introduction To Roth or Not Revised September 2013 Tax law allows all taxpayers (without income limitation) to convert all or part of their traditional IRAs to Roth IRAs. Even though conversion to Roth

Introduction To Roth or Not Revised September 2013 Tax law allows all taxpayers (without income limitation) to convert all or part of their traditional IRAs to Roth IRAs. Even though conversion to Roth

Understanding. What You Will Learn

Understanding IRA and Retirement Plan Distributions Michael A. Simon, Esq. Law Offices of Michael A. Simon 4425 Jamboree Road, Suite 190 Newport Beach, California 92660 (949) 954-6999 [email protected]

Understanding IRA and Retirement Plan Distributions Michael A. Simon, Esq. Law Offices of Michael A. Simon 4425 Jamboree Road, Suite 190 Newport Beach, California 92660 (949) 954-6999 [email protected]

the t. rowe price Guide for IRA and 403(b) Account Beneficiaries

Account Beneficiaries") the t. rowe price Guide for IRA and 403(b) Account Beneficiaries who should use this guide T. Rowe Price retirement specialists have designed this guide for: 1 : Individuals who are beneficiaries of the

the t. rowe price Guide for IRA and 403(b) Account Beneficiaries who should use this guide T. Rowe Price retirement specialists have designed this guide for: 1 : Individuals who are beneficiaries of the

Taking Your Required Minimum Distributions

RETIREMENT Taking Your Required Minimum Distributions A Guide for Retirement Account Owners and Beneficiaries Taking Distributions During Your Lifetime Most people are required to start withdrawing from

RETIREMENT Taking Your Required Minimum Distributions A Guide for Retirement Account Owners and Beneficiaries Taking Distributions During Your Lifetime Most people are required to start withdrawing from

Leaving your employer? Options for your retirement plan

Leaving your employer? Options for your retirement plan Contents Evaluating your options 1 The benefits of tax-deferred investing 4 Flexibility offered by an IRA rollover 6 How to get started 9 Evaluating

Leaving your employer? Options for your retirement plan Contents Evaluating your options 1 The benefits of tax-deferred investing 4 Flexibility offered by an IRA rollover 6 How to get started 9 Evaluating

Rollover IRAs. Consider the advantages of consolidating your retirement savings

Rollover IRAs Consider the advantages of consolidating your retirement savings Consider the Advantages of Consolidating Your Retirement Savings If you have changed jobs, left the workforce or plan to

Rollover IRAs Consider the advantages of consolidating your retirement savings Consider the Advantages of Consolidating Your Retirement Savings If you have changed jobs, left the workforce or plan to

Required Minimum Distributions: What Every Advisor Needs to Know FOR FINANCIAL PROFESSIONAL USE ONLY / NOT FOR PUBLIC VIEWING OR DISTRIBUTION.

Required Minimum Distributions: What Every Advisor Needs to Know 1 Required Minimum Distributions Upon reaching age 70½, clients must begin taking annual distributions from their IRA in accordance with

Required Minimum Distributions: What Every Advisor Needs to Know 1 Required Minimum Distributions Upon reaching age 70½, clients must begin taking annual distributions from their IRA in accordance with

10 common IRA mistakes

10 common mistakes Help protect your valuable retirement assets Not FDIC Insured May Lose Value No Bank Guarantee Not Insured by Any Government Agency You ve worked hard to build your retirement assets......

10 common mistakes Help protect your valuable retirement assets Not FDIC Insured May Lose Value No Bank Guarantee Not Insured by Any Government Agency You ve worked hard to build your retirement assets......

Charitable Gifts of IRA/IRD via a Beneficiary Statement - Good. Charitable Gifts of IRA / IRD Assets The Good, The Bad and The Ugly.

Charitable Gifts of IRA / IRD Assets The Good, The Bad and The Ugly Susan C Dunlop Luther Seminary - Gary G Hargroves Thompson & Associates Minnesota Planned Giving Council Conference 11-5-14 Definitions

Charitable Gifts of IRA / IRD Assets The Good, The Bad and The Ugly Susan C Dunlop Luther Seminary - Gary G Hargroves Thompson & Associates Minnesota Planned Giving Council Conference 11-5-14 Definitions

The owner is usually the purchaser of the policy. However, the owner may also acquire the policy by gift, sale, exchange, or bequest.

Annuity Ownership Considerations What is an annuity owner? What are the owner's rights? Who should be the owner? What if the owner dies? Is the annuity includable in the owner's estate? What risks does

Annuity Ownership Considerations What is an annuity owner? What are the owner's rights? Who should be the owner? What if the owner dies? Is the annuity includable in the owner's estate? What risks does

Facts to Know When You Inherit a Non-Spousal IRA

Facts to Know When You Inherit a Non-Spousal IRA There are many planning and distribution considerations for individuals inheriting a non-spouse s IRA (Traditional, Roth, SEP or SIMPLE). It is imperative

Facts to Know When You Inherit a Non-Spousal IRA There are many planning and distribution considerations for individuals inheriting a non-spouse s IRA (Traditional, Roth, SEP or SIMPLE). It is imperative

Understanding IRA distributions

Understanding IRA distributions A retirement distribution guide Allianz Life Insurance Company of New York Allianz Life Insurance Company of North America AMK-019-N Page 1 of 12 It s important to know

Understanding IRA distributions A retirement distribution guide Allianz Life Insurance Company of New York Allianz Life Insurance Company of North America AMK-019-N Page 1 of 12 It s important to know

Beginning in 2010, the Tax Increase Prevention and ROTH IRA CONVERSION

ROTH IRA CONVERSION Assessing Suitability of the Strategy for Individuals and their Heirs Executive Summary A Roth IRA conversion may benefit individuals during their retirement years by potentially reducing

ROTH IRA CONVERSION Assessing Suitability of the Strategy for Individuals and their Heirs Executive Summary A Roth IRA conversion may benefit individuals during their retirement years by potentially reducing

TEN WAYS TO USE LIFE INSURANCE (AN ESTATE PLANNING PERSPECTIVE)

") TEN WAYS TO USE LIFE INSURANCE (AN ESTATE PLANNING PERSPECTIVE) Oregon State Bar Family Law Section Annual Conference October 2013 Kathy Belcher McGinty & Belcher Attys PC 694 High St NE PO Box 12806 Salem

TEN WAYS TO USE LIFE INSURANCE (AN ESTATE PLANNING PERSPECTIVE) Oregon State Bar Family Law Section Annual Conference October 2013 Kathy Belcher McGinty & Belcher Attys PC 694 High St NE PO Box 12806 Salem

10Common IRA mistakes

10Common IRA mistakes Help protect your valuable retirement assets You ve worked hard to build your retirement assets. And you want them to continue to work hard for you throughout your working career

10Common IRA mistakes Help protect your valuable retirement assets You ve worked hard to build your retirement assets. And you want them to continue to work hard for you throughout your working career

IRAS TAXES AND MOODY STEWARDSHIP. A Ministry of Moody Bible Institute

MOODY STEWARDSHIP A Ministry of Moody Bible Institute IRAS AND TAXES IRAs and Other Qualified Retirement Plans IRAs, pensions, and estate planning are all excellent resources for preparing an enjoyable,

MOODY STEWARDSHIP A Ministry of Moody Bible Institute IRAS AND TAXES IRAs and Other Qualified Retirement Plans IRAs, pensions, and estate planning are all excellent resources for preparing an enjoyable,

IRA. Mistakes and Opportunities. Dru Donatelli, JD-MBA, ChFC, CLU. AVP, Field Director, and Advanced Planning Attorney Special Markets

IRA Mistakes and Opportunities Dru Donatelli, JD-MBA, ChFC, CLU AVP, Field Director, and Advanced Planning Attorney Special Markets Wood Logan Academy We give financial professionals a lot of credit Not

IRA Mistakes and Opportunities Dru Donatelli, JD-MBA, ChFC, CLU AVP, Field Director, and Advanced Planning Attorney Special Markets Wood Logan Academy We give financial professionals a lot of credit Not

LIQUIDATING RETIREMENT ASSETS

LIQUIDATING RETIREMENT ASSETS IN A TAX-EFFICIENT MANNER By William A. Raabe and Richard B. Toolson When you enter retirement, you retire from work, not from decision-making. Among the more important decisions

LIQUIDATING RETIREMENT ASSETS IN A TAX-EFFICIENT MANNER By William A. Raabe and Richard B. Toolson When you enter retirement, you retire from work, not from decision-making. Among the more important decisions

A New Use for Your. a donor s guide. The Stelter Company

A New Use for Your R E T I R E M E N T P L A N A S S E T S a donor s guide The Stelter Company APPRECIATED PROPERTY Learn how to uncover the value of your appreciated assets. Like many Americans, you are

A New Use for Your R E T I R E M E N T P L A N A S S E T S a donor s guide The Stelter Company APPRECIATED PROPERTY Learn how to uncover the value of your appreciated assets. Like many Americans, you are

Inherited Annuity/IRA Analysis

Phase 1 Income to match your lifestyle and preserve your wealth Phase 2 Continuing income for spousal security and independence Phase 3 A legacy that passes to the next generation Prepared For : Thomas

Phase 1 Income to match your lifestyle and preserve your wealth Phase 2 Continuing income for spousal security and independence Phase 3 A legacy that passes to the next generation Prepared For : Thomas

Wealth Structuring and Estate Planning. Your vision and your legacy. Life s better when we re connected

Wealth Structuring and Estate Planning Your vision and your legacy Life s better when we re connected Inside 1 Helping you shape the future 2 The elements of wealth structuring 4 The power and flexibility

Wealth Structuring and Estate Planning Your vision and your legacy Life s better when we re connected Inside 1 Helping you shape the future 2 The elements of wealth structuring 4 The power and flexibility

Converting to a Roth IRA Eliminating the Pain by using Life Insurance. Lanny D. Levin, CLU, ChFC, President LANNY D. LEVIN AGENCY, INC.

Converting to a Roth IRA Eliminating the Pain by using Life Insurance Lanny D. Levin, CLU, ChFC, President LANNY D. LEVIN AGENCY, INC. The Roth Advantage as an estate tool Traditional IRAs are great for

Converting to a Roth IRA Eliminating the Pain by using Life Insurance Lanny D. Levin, CLU, ChFC, President LANNY D. LEVIN AGENCY, INC. The Roth Advantage as an estate tool Traditional IRAs are great for

10 Rules of Thumb for Trust Income Taxation Presented by Adam Scott

10 Rules of Thumb for Trust Income Taxation Presented by Adam Scott Rule #1: When in doubt, refer to the trust document; an investment policy for a trust cannot be created without it. One advantage of

10 Rules of Thumb for Trust Income Taxation Presented by Adam Scott Rule #1: When in doubt, refer to the trust document; an investment policy for a trust cannot be created without it. One advantage of

EVERYTHING YOU OWN & EVERYONE YOU CARE ABOUT. An Estate Planning Primer

EVERYTHING YOU OWN & EVERYONE YOU CARE ABOUT An Estate Planning Primer For The Clients Of 7350 Cirque Drive W, Suite 201 University Place, WA 98467 (253) 759 8354 www.ppatpa.com Presented By T. Gary Connett

EVERYTHING YOU OWN & EVERYONE YOU CARE ABOUT An Estate Planning Primer For The Clients Of 7350 Cirque Drive W, Suite 201 University Place, WA 98467 (253) 759 8354 www.ppatpa.com Presented By T. Gary Connett

Charitable Giving and Retirement Assets

Charitable Giving and Retirement Assets In this issue: Basics of IRAs Retirement Plan Basics Lifetime Taxation of Distributions from Retirement Accounts Estate Taxation of IRAs and Tax-Deferred Retirement

Charitable Giving and Retirement Assets In this issue: Basics of IRAs Retirement Plan Basics Lifetime Taxation of Distributions from Retirement Accounts Estate Taxation of IRAs and Tax-Deferred Retirement

The IRA Rollover. Making Sense Out of Your Retirement Plan Distribution

The IRA Rollover Making Sense Out of Your Retirement Plan Distribution Expecting a Distribution? You have been a participant in your employer s retirement plan for a number of years, and you have earned

The IRA Rollover Making Sense Out of Your Retirement Plan Distribution Expecting a Distribution? You have been a participant in your employer s retirement plan for a number of years, and you have earned

MFS Retirement Strategies Stretch IRA and distribution options READY, SET, RETIRE. Taking income distributions during retirement

MFS Retirement Strategies Stretch IRA and distribution options READY, SET, RETIRE Taking income distributions during retirement ASSESS YOUR NEEDS INCOME WHEN YOU NEED IT Choosing the right income distribution

MFS Retirement Strategies Stretch IRA and distribution options READY, SET, RETIRE Taking income distributions during retirement ASSESS YOUR NEEDS INCOME WHEN YOU NEED IT Choosing the right income distribution

Traditional IRAs. Understanding Required Distributions at 70 1 / 2. Questions & Answers

Traditional IRAs Understanding Required Distributions at 70 1 / 2 Questions & Answers Why are there federal tax rules mandating required minimum distributions from a traditional IRA? The primary purpose

Traditional IRAs Understanding Required Distributions at 70 1 / 2 Questions & Answers Why are there federal tax rules mandating required minimum distributions from a traditional IRA? The primary purpose

This article focuses on rollovers by a

Rollovers From Retirement Plans and IRAs By Marcia Chadwick Holt This article focuses on rollovers by a surviving spouse and by a nonspouse to retirement plans and individual retirement accounts (IRAs).

Rollovers From Retirement Plans and IRAs By Marcia Chadwick Holt This article focuses on rollovers by a surviving spouse and by a nonspouse to retirement plans and individual retirement accounts (IRAs).

Wealth Strategies. www.rfawealth.com. Saving For Retirement: Tax Deductible vs Roth Contributions. www.rfawealth.com

www.rfawealth.com Wealth Strategies Saving For Retirement: Tax Deductible vs Roth Contributions Part 2 of 12 Your Guide to Saving for Retirement WEALTH STRATEGIES Page 1 Saving For Retirement: Tax Deductible

www.rfawealth.com Wealth Strategies Saving For Retirement: Tax Deductible vs Roth Contributions Part 2 of 12 Your Guide to Saving for Retirement WEALTH STRATEGIES Page 1 Saving For Retirement: Tax Deductible

1099R BOX DESCRIPTIONS

For additional details and instructions refer to IRS 1099R Instructions 1 Gross Distribution Enter the total amount of the distribution before income tax or other deductions were withheld. This can include:

For additional details and instructions refer to IRS 1099R Instructions 1 Gross Distribution Enter the total amount of the distribution before income tax or other deductions were withheld. This can include:

IRAs & Roth IRAs. Beneficiary or Inherited IRAs. Questions & Answers

IRAs & Roth IRAs Beneficiary or Inherited IRAs Questions & Answers Purpose The purpose of this brochure is to provide a person who is a beneficiary of a traditional IRA (including SEPs and SIMPLEs) or

IRAs & Roth IRAs Beneficiary or Inherited IRAs Questions & Answers Purpose The purpose of this brochure is to provide a person who is a beneficiary of a traditional IRA (including SEPs and SIMPLEs) or

chart retirement plans 8 Retirement plans available to self-employed individuals include:

retirement plans Contributing to retirement plans can provide you with financial security as well as reducing and/or deferring your taxes. However, there are complex rules that govern the type of plans

retirement plans Contributing to retirement plans can provide you with financial security as well as reducing and/or deferring your taxes. However, there are complex rules that govern the type of plans

AN ANALYSIS OF ROTH CONVERSIONS 1

AN ANALYSIS OF ROTH CONVERSIONS In 1997, Congress introduced the Roth IRA, giving investors a new product for retirement savings. The Roth IRA is essentially a mirror image of the Traditional IRA, but

AN ANALYSIS OF ROTH CONVERSIONS In 1997, Congress introduced the Roth IRA, giving investors a new product for retirement savings. The Roth IRA is essentially a mirror image of the Traditional IRA, but

The IRA opportunity: To Roth or not to Roth?

The IRA opportunity: To Roth or not to Roth? Vanguard research July 2011 Executive summary. The year 2010, which may well go down in IRA history as the year of the Roth, saw three notable legislative changes

The IRA opportunity: To Roth or not to Roth? Vanguard research July 2011 Executive summary. The year 2010, which may well go down in IRA history as the year of the Roth, saw three notable legislative changes

MAXIMIZATION ANNUITY STRATEGY. An estate planning technique for individuals who own deferred annuities with sizable growth.

ANNUITY MAXIMIZATION STRATEGY An estate planning technique for individuals who own deferred annuities with sizable growth. Transamerica Occidental Life Insurance Company Preserving Hard-Earned Assets As

ANNUITY MAXIMIZATION STRATEGY An estate planning technique for individuals who own deferred annuities with sizable growth. Transamerica Occidental Life Insurance Company Preserving Hard-Earned Assets As

THE IRA CHARITABLE ROLLOVER

THE IRA CHARITABLE ROLLOVER The IRA Charitable Rollover was first added to the Internal Revenue Code of 1986, as amended, under legislation enacted in 2006. It permitted individuals to roll over up to

THE IRA CHARITABLE ROLLOVER The IRA Charitable Rollover was first added to the Internal Revenue Code of 1986, as amended, under legislation enacted in 2006. It permitted individuals to roll over up to

Minimum Distributions & Beneficiary Designations: Planning Opportunities

28 $ $ $ RETIREMENT PLANS The rules regarding distributions and designated beneficiaries are complex, but there are strategies that will help minimize income and estate taxes. Minimum Distributions & Beneficiary

28 $ $ $ RETIREMENT PLANS The rules regarding distributions and designated beneficiaries are complex, but there are strategies that will help minimize income and estate taxes. Minimum Distributions & Beneficiary

ESTATE PLANNING WITH RETIREMENT ACCOUNTS. $5 million Gift Tax * * $5 million GST * * 35% tax rate * * Portability for married couples * *

ESTATE PLANNING FOR RETIREMENT ACCOUNTS The Collision of Income Tax, ERISA, and Estate Tax Laws CHRISTOPHER R. HOYT Professor of Law University of Missouri - Kansas City School of Law ESTATE PLANNING WITH

ESTATE PLANNING FOR RETIREMENT ACCOUNTS The Collision of Income Tax, ERISA, and Estate Tax Laws CHRISTOPHER R. HOYT Professor of Law University of Missouri - Kansas City School of Law ESTATE PLANNING WITH

KEY FACTORS WHEN CONSIDERING A ROTH IRA CONVERSION

KEY FACTORS WHEN CONSIDERING A ROTH IRA CONVERSION PERTINENT INFORMATION Mr. Kugler has accumulated $1,000,000 in a traditional IRA. Mrs. Kugler is the designated beneficiary (DB) and their daughter is

KEY FACTORS WHEN CONSIDERING A ROTH IRA CONVERSION PERTINENT INFORMATION Mr. Kugler has accumulated $1,000,000 in a traditional IRA. Mrs. Kugler is the designated beneficiary (DB) and their daughter is

HERMENZE & MARCANTONIO LLC ADVANCED ESTATE PLANNING TECHNIQUES - 2015

HERMENZE & MARCANTONIO LLC ADVANCED ESTATE PLANNING TECHNIQUES - 2015 I. Overview of federal, Connecticut, and New York estate and gift taxes. A. Federal 1. 40% tax rate. 2. Unlimited estate and gift tax

HERMENZE & MARCANTONIO LLC ADVANCED ESTATE PLANNING TECHNIQUES - 2015 I. Overview of federal, Connecticut, and New York estate and gift taxes. A. Federal 1. 40% tax rate. 2. Unlimited estate and gift tax

The joy of charitable giving: Strategies and opportunities

The joy of charitable giving: Strategies and opportunities Vanguard research September 2013 Executive summary. The tax benefits available through various charitable giving strategies can play a critical

The joy of charitable giving: Strategies and opportunities Vanguard research September 2013 Executive summary. The tax benefits available through various charitable giving strategies can play a critical

Beneficiary Payment Options for Traditional IRAs (Death Before Required Beginning Date)

") Beneficiary Payment Options Beneficiary Payment Options for Traditional IRAs (Death Before Required Beginning Date) Frequently Asked Questions Payment Options Payment Flexibility Withholding Elections

Beneficiary Payment Options Beneficiary Payment Options for Traditional IRAs (Death Before Required Beginning Date) Frequently Asked Questions Payment Options Payment Flexibility Withholding Elections

Passing on the Good Stuff! Implementing a Roth IRA Conversion Using Life Insurance

Passing on the Good Stuff! Implementing a Roth IRA Conversion Using Life Insurance Passing On The Good Stuff! All inheritances aren t equal. Even two different assets that are worth similar amounts may

Passing on the Good Stuff! Implementing a Roth IRA Conversion Using Life Insurance Passing On The Good Stuff! All inheritances aren t equal. Even two different assets that are worth similar amounts may

Key Concepts for Required Minimum Distributions from IRAs and Qualified Retirement Plans

Key Concepts for Required Minimum Distributions from IRAs and Qualified Retirement Plans WSU Accounting & Auditing Conference Tuesday, May 20, 2014 Presented By: Steven P. Smith Hinkle Law Firm LLC 301

Key Concepts for Required Minimum Distributions from IRAs and Qualified Retirement Plans WSU Accounting & Auditing Conference Tuesday, May 20, 2014 Presented By: Steven P. Smith Hinkle Law Firm LLC 301

Distribution Options for IRA Beneficiaries. Choose the option that s best for you

Distribution Options for IRA Beneficiaries Choose the option that s best for you Let Us Help You Make An Informed Decision Before you begin It s important to understand your choices and the best options

Distribution Options for IRA Beneficiaries Choose the option that s best for you Let Us Help You Make An Informed Decision Before you begin It s important to understand your choices and the best options

Roth IRA Conversions: A Powerful Wealth-Transfer Tool

July 2014 Private Wealth Advisory Roth IRA Conversions: A Powerful Wealth-Transfer Tool Converting a traditional IRA or another qualified retirement plan to a Roth IRA can be a powerful wealth-transfer

July 2014 Private Wealth Advisory Roth IRA Conversions: A Powerful Wealth-Transfer Tool Converting a traditional IRA or another qualified retirement plan to a Roth IRA can be a powerful wealth-transfer

The IRA Protection and Maximization Trust Maximizing Tax Deferred Growth and Asset Protection For Inherited IRAs and 401K Plans

888 Worcester Street Wellesley, Massachusetts (781) 237-2815 phone (781) 237-3141 fax The IRA Protection and Maximization Trust Maximizing Tax Deferred Growth and Asset Protection For Inherited IRAs and

888 Worcester Street Wellesley, Massachusetts (781) 237-2815 phone (781) 237-3141 fax The IRA Protection and Maximization Trust Maximizing Tax Deferred Growth and Asset Protection For Inherited IRAs and

t. rowe price Required Minimum Distribution (RMD) Guide

Guide") t. rowe price Required Minimum Distribution (RMD) Guide contents at a glance RMD Basics 2 RMD Calculation Instructions 7 IRS Uniform Lifetime Table 8 RMD Investment Options 10 Selecting and Educating Your

t. rowe price Required Minimum Distribution (RMD) Guide contents at a glance RMD Basics 2 RMD Calculation Instructions 7 IRS Uniform Lifetime Table 8 RMD Investment Options 10 Selecting and Educating Your

Tax Alpha. Robert S. Keebler, CPA, M.S.T., AEP. Keebler & Associates, LLP 420 South Washington Street Green Bay, WI 54301.

Tax Alpha Presented by Robert S. Keebler, CPA, M.S.T., AEP Keebler & Associates, LLP 420 South Washington Street Green Bay, WI 54301 Agenda 1. Five Dimensional Tax System Ordinary Income Rates Capital

Tax Alpha Presented by Robert S. Keebler, CPA, M.S.T., AEP Keebler & Associates, LLP 420 South Washington Street Green Bay, WI 54301 Agenda 1. Five Dimensional Tax System Ordinary Income Rates Capital

An n u i t y. Preserving Hard-Earned Annuity Assets. t r a n s a m e r i c a 1

An n u i t y Maximization Strategy Preserving Hard-Earned Annuity Assets t r a n s a m e r i c a 1 Alternatives to help protect financial assets, increase current income stream, or decrease income tax

An n u i t y Maximization Strategy Preserving Hard-Earned Annuity Assets t r a n s a m e r i c a 1 Alternatives to help protect financial assets, increase current income stream, or decrease income tax

Rollovers from Employer-Sponsored Retirement Plans

Nolan Wealth Management, LLC Brian A. Nolan, CLTC President 4454 Main Street PO Box 505 Kingston, NJ 08528-0505 Direct: 609.436.4448 Toll Free877.NOLANWM [email protected] www.nolanwealth.com Rollovers

Nolan Wealth Management, LLC Brian A. Nolan, CLTC President 4454 Main Street PO Box 505 Kingston, NJ 08528-0505 Direct: 609.436.4448 Toll Free877.NOLANWM [email protected] www.nolanwealth.com Rollovers

Wealthiest Families Know: 2013 & Beyond

What the Wealthiest Families Know: 2013 & Beyond Determine How Estate Planning Strategies and Life Insurance May Help You Turn Your Goals into a Wealth Legacy Whether you acquired it or inherited it, wealth

What the Wealthiest Families Know: 2013 & Beyond Determine How Estate Planning Strategies and Life Insurance May Help You Turn Your Goals into a Wealth Legacy Whether you acquired it or inherited it, wealth