Research Memo. Comparison of Wyoming and Montana s High-Risk Health Insurance Pools

|

|

|

- Doreen Osborne

- 8 years ago

- Views:

Transcription

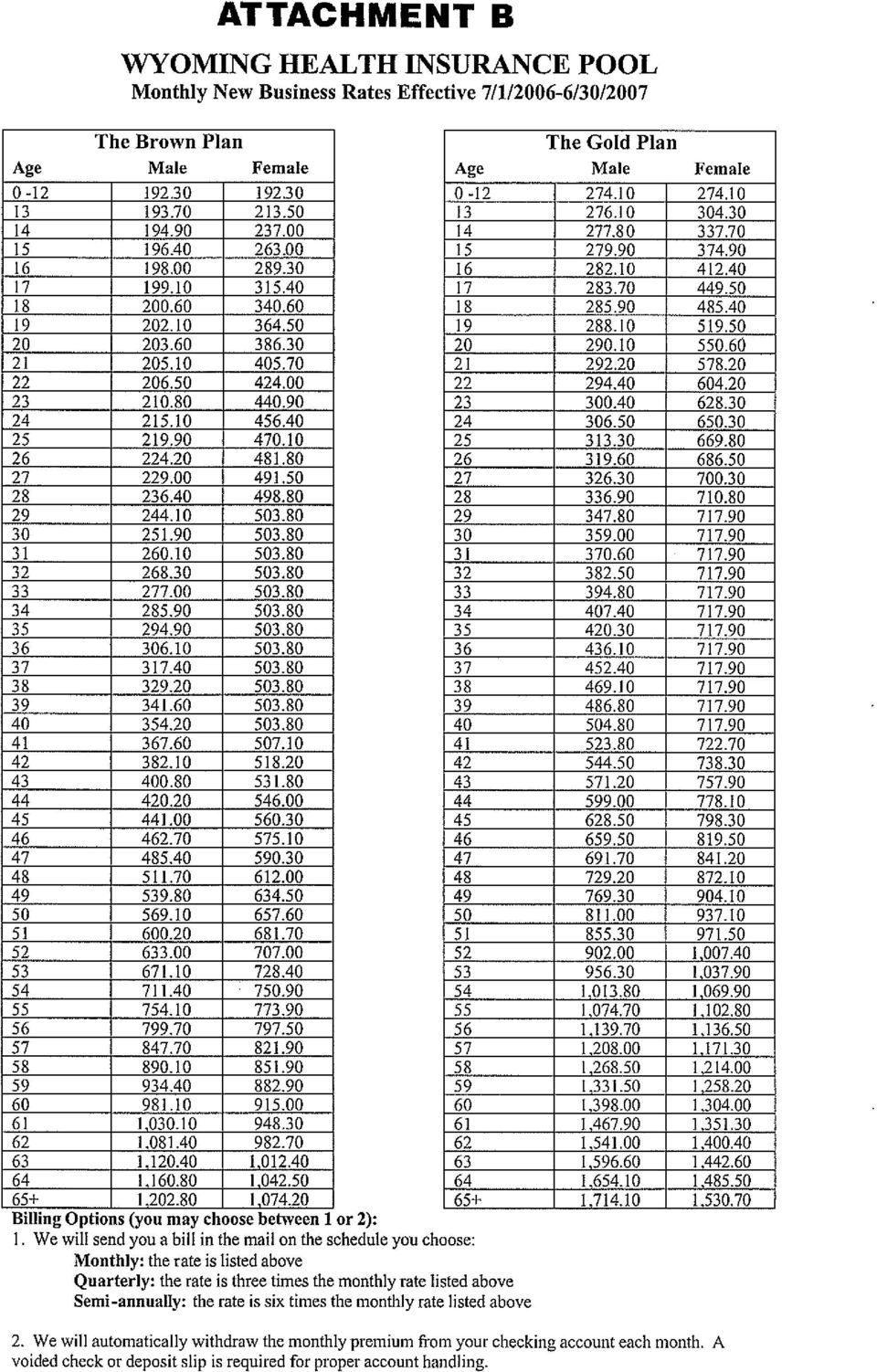

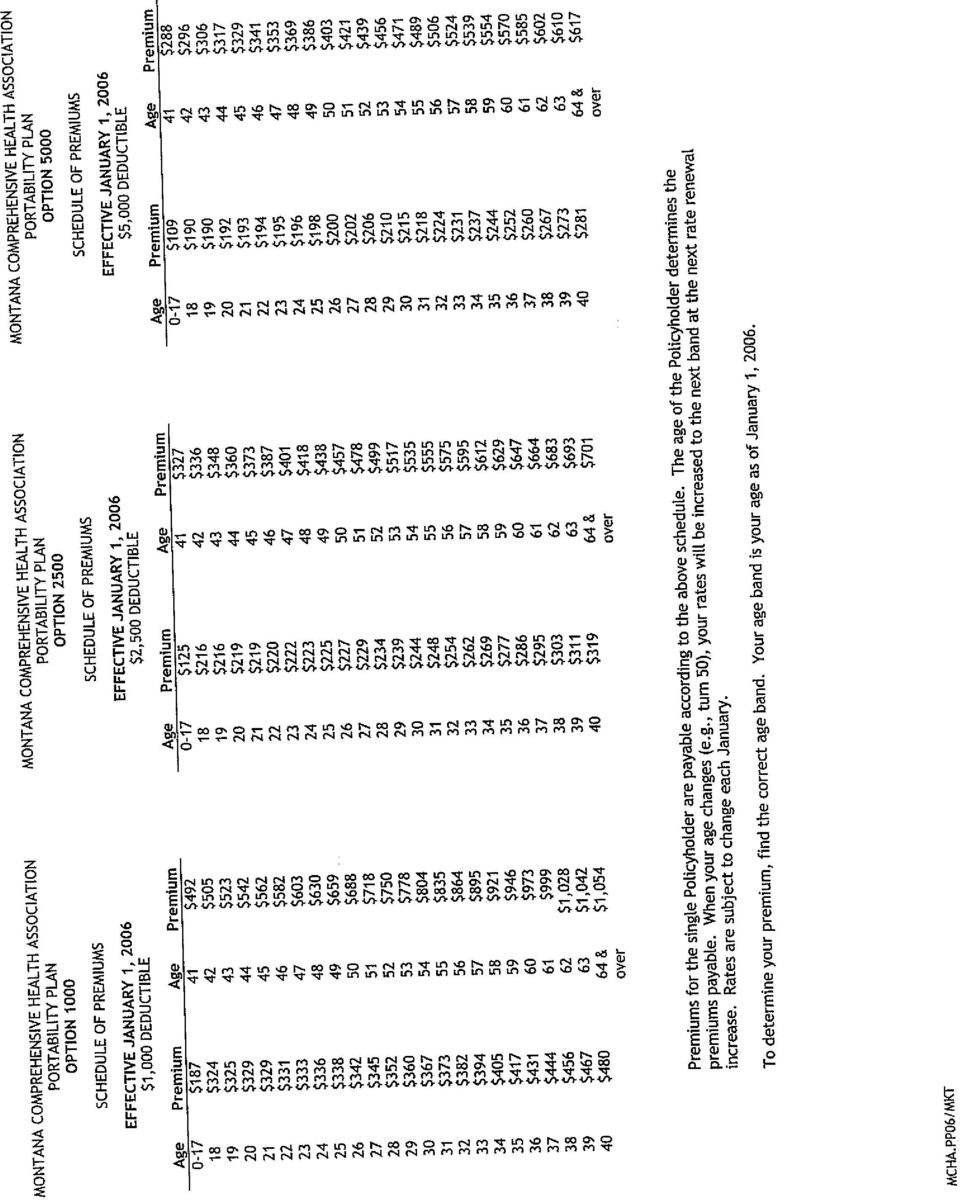

1 8/17/ RM 045 Date: August 17, 2006 Research Memo Author: Don C. Richards, Senior Research Analyst Joy N. Hill, Associate Research Analyst Re: Comparison of Wyoming and Montana s High-Risk Health Insurance Pools QUESTION Compare and contrast the administration, benefits, and participant costs for the Wyoming and Montana high-risk health insurance pools. Consider whether there is evidence that Montana's pool provides better benefits with lower premiums. ANSWER Both the Wyoming and Montana high risk health insurance plans are administered by Blue Cross Blue Shield and appear to offer somewhat similar, or at least somewhat comparable, benefits. In addition, the premiums for participants for comparable plans do appear to be substantially lower in Montana than in Wyoming. However, due to differences in how the plans are structured, and particularly the out-of-pocket maximum expenditures, caution should be exercised when comparing the two states plans. See Table 1, for a comparative assessment of participant premiums and other expenses for comparable plans. Table 1. Wyoming and Montana Health Plan Participant Cost Comparison. WY Brown Plan WY Gold Plan MT Traditional #1 MT Traditional #2 Deductible $5,000 $1,000 $5,000 $1,000 Co-pay 100% (up to 80% / 20% 80% / 20% 80% / 20% deductible) Out-of-pocket maximum $5,000 $2,000 $7,500 $5,000 Maximum Lifetime Benefit $500,000 $750,000 $1,000,000 $1,000,000 Premium Single Female, $ $ $267 $456 age 40 Premium Single Male, age 55 $ $1, $464 $792 Source: LSO Research staff summary based upon published benefit charts and premium rates, WYOMING LEGISLATIVE SERVICE OFFICE 213 State Capitol Cheyenne, Wyoming TELEPHONE (307) FAX (307) lso@state.wy.us WEBSITE

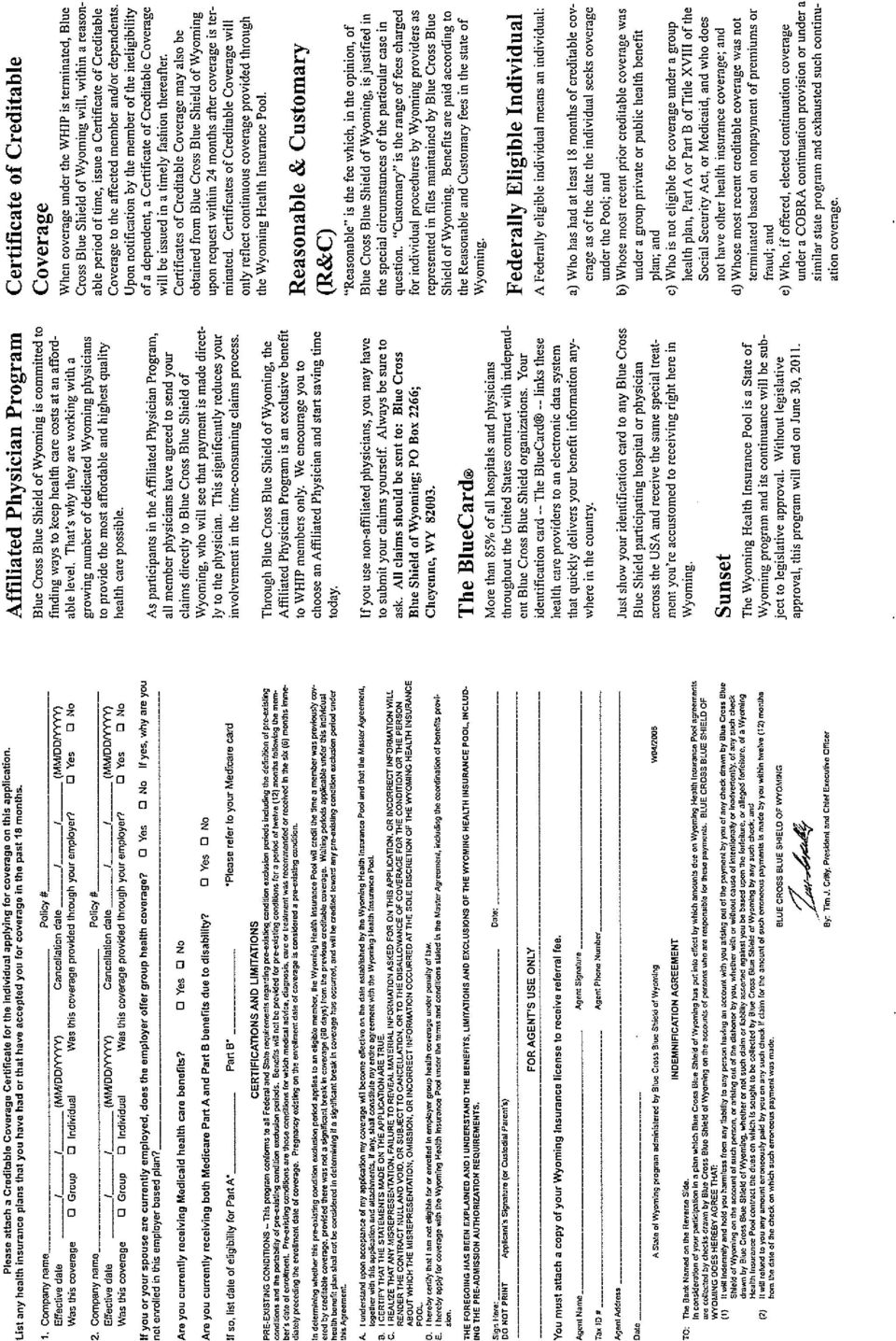

2 PAGE 2 OF 7 WYOMING HEALTH INSURANCE POOL Background and Eligibility. The Wyoming Health Insurance Pool (WHIP) was created in 1990 through W.S et seq. and regulated by Chapter 41 of the Wyoming Insurance Department Regulations. 1 The intent of WHIP is to provide health insurance coverage to Wyoming residents who are denied traditional health insurance coverage due to existing medical conditions. The Wyoming Health Insurance Pool Board, consisting of seven members appointed by the insurance commissioner, operates the pool. Blue Cross Blue Shield, through a contract with the Board, administers the program. Both the Wyoming and the Montana health insurance pools offer options designed to cover cost sharing amounts under Medicare Part A and Part B. Although directly related to the general health insurance pool, comparisons of the Medicare options are not considered in this memo. Revenues for the Wyoming health insurance pool are currently derived from four sources: insurance company assessments, participant health insurance premiums, investment income, and based upon a recent developments this year, a federal grant. The pool does not currently receive support from a state appropriation. Individuals eligible for coverage through WHIP must meet the following criteria: must be a Wyoming resident residing in Wyoming; and must provide proof that they have been refused coverage for health reasons by one insurer; or have health insurance coverage more restrictive than WHIP s coverage; or have health insurance coverage at a rate exceeding WHIP rates; or is a federally eligible individual. 2 Benefits. Currently, two plan options are available from WHIP: The Brown Plan and The Gold Plan. The lifetime maximum benefit amount for the Brown Plan is $500,000; for the Gold Plan the maximum is $750,000, per individual. Coverage under both plan's include maternity care, hospitalization, medical surgery, prescription drugs, adult wellness and well child care, outpatient services, mental and substance abuse, and testing, supplies, ambulance services, etc. More complete information regarding the benefits of these plans, and WHIP generally, is included as Attachment A. 1 All of the benefit and cost information in this memo relates to the Wyoming Health Insurance Pool as of July 1, There are many participants that continue to follow the requirements and receive benefits from priors version of the plan. These "grandfathered" participants are still covered under last year's plans until December 31, Since those benefits and payment requirements are scheduled to expire, this analysis considers only the characteristics of the plans as approved for use as of July 1, All participants will be shifted to these plan requirements on or before January 1, A federally eligible individual, as defined by Health Insurance Portability and Accountability Act (HIPAA) and articulated by the Department of Insurance, is "an individual who has had at least 18 months of creditable coverage as of the date the individual seeks coverage under the Pool; whose most recent prior creditable coverage was under a group private or public health benefit plan; who is not eligible for coverage under a group health plan, Part A or Part B of Title XVIII of the Social Security Act, or Medicaid, and who does not have other health insurance coverage; whose most recent creditable coverage was not terminated based on nonpayment of premiums or fraud; and who, if offered, elected continuation coverage under a COBRA continuation provision or under a similar state program and exhausted such continuation coverage." Insurance Department staff report that there are few federal eligible individuals in the pool as portability is extended to all applicants if they have creditable coverage, or 90 days has not passed since an applicant had creditable coverage. WYOMING LEGISLATIVE SERVICE OFFICE 213 State Capitol Cheyenne, Wyoming TELEPHONE (307) FAX (307) lso@state.wy.us WEBSITE

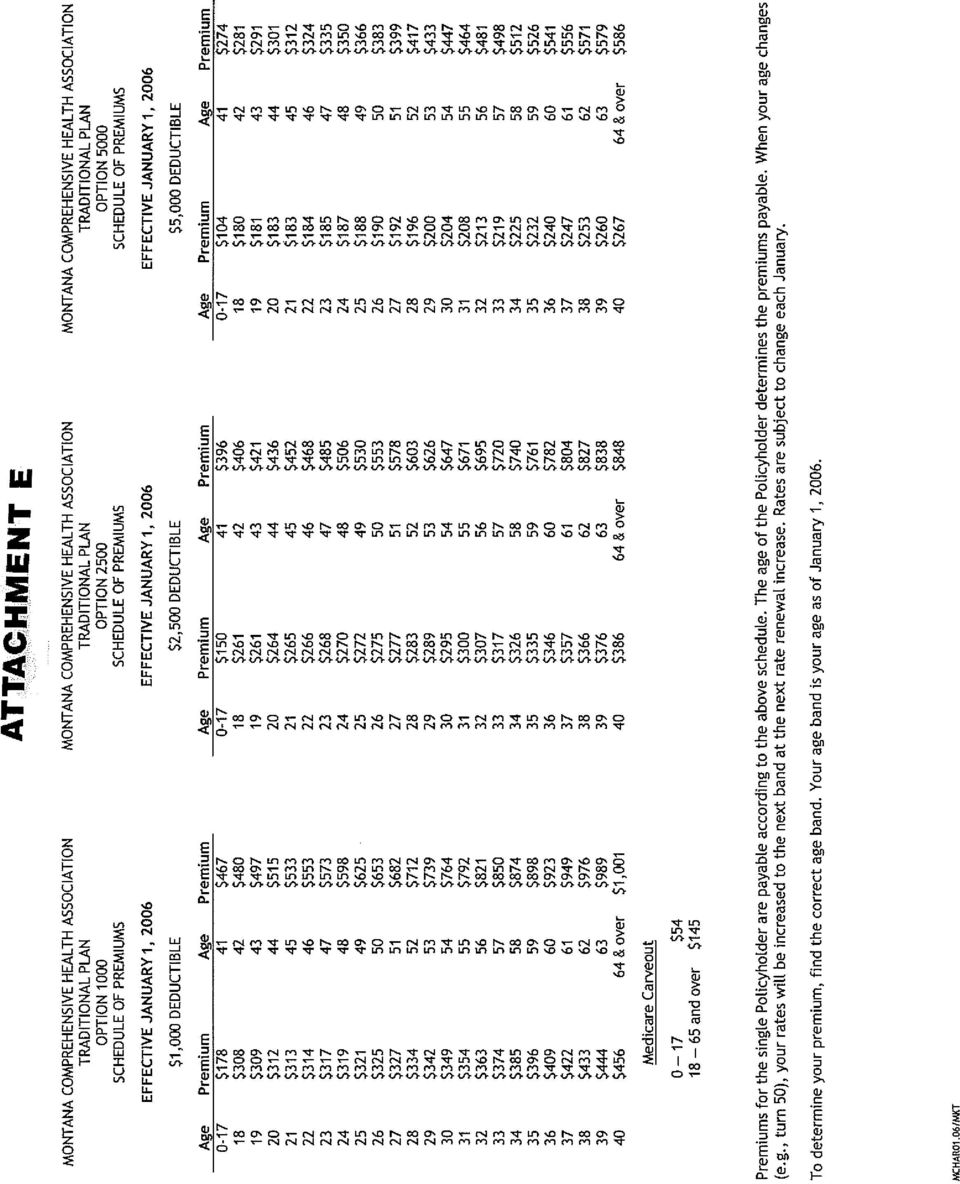

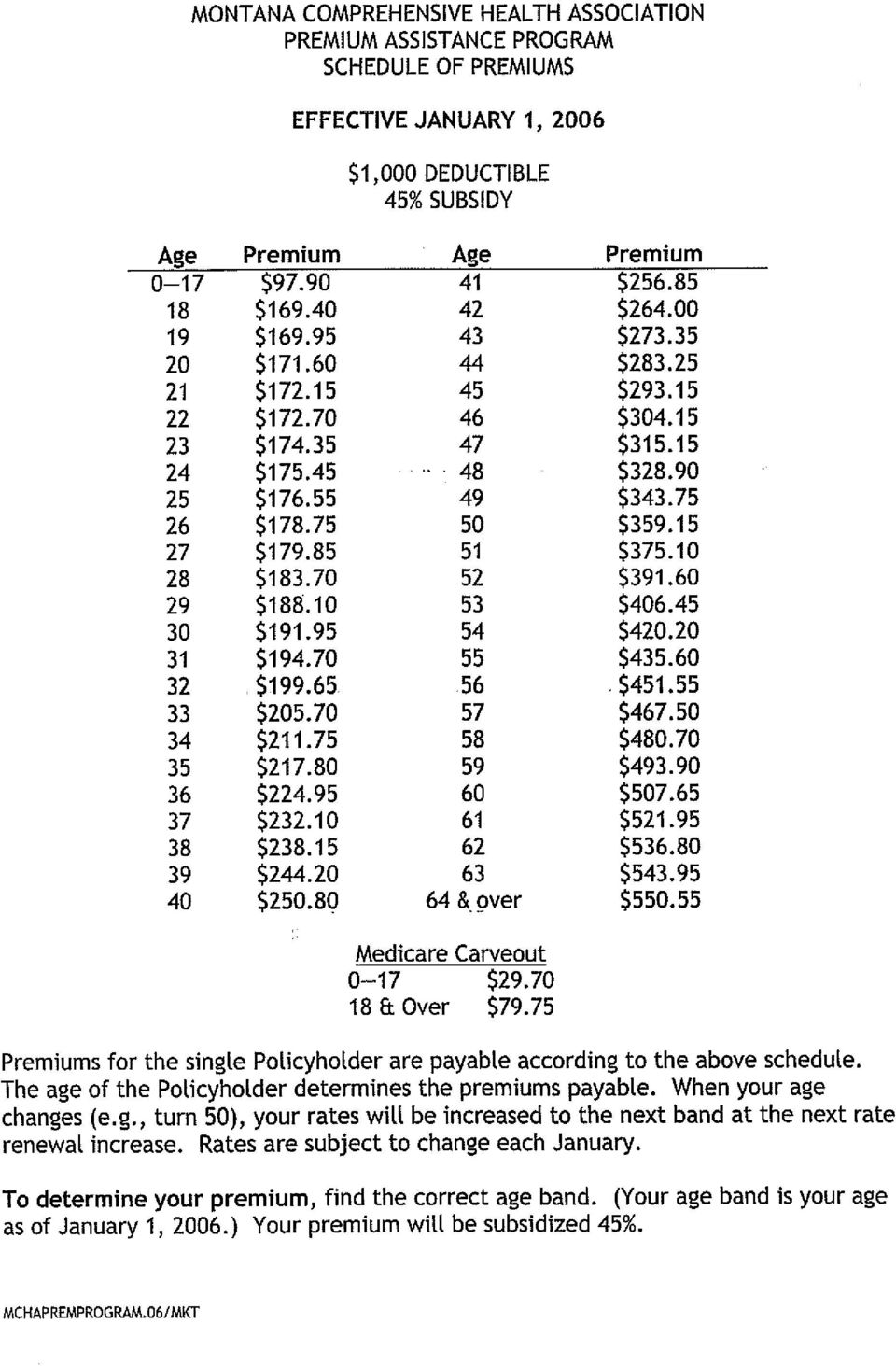

3 PAGE 3 OF 7 Premiums and Deductibles. Every year the Wyoming Health Insurance Pool Board surveys five insurance companies to determine current standard market rates within the state in order to adjust and set rates. W.S (b) requires WHIP rates may not exceed 200 percent of standard market rates. Statute also states, "The rates shall be set as close as practical to the lower end of the range provided by this subsection without undue risk of shifting more than fifty percent (50%) of the burden of assessments to private health insurance." According to Department of Insurance staff, premiums for WHIP currently approach the 200 percent maximum allowed by statute. Further, the assessments on insurance companies likely exceed the fifty percent burden referenced in statute. Monthly premiums, effective as of July 1, 2006, for WHIP plans are included as Attachment B. Below is a general illustration of the premiums, which vary by age of the participant, for the Brown and Gold Plans: The Brown Plan premiums The Gold Plan premiums Single Male: $ $1, Single Male: $ $ Single Female: $ $1, Single Female: $ $1, There are also out-of-pocket costs, including deductibles and co-payments. Once the maximum out-ofpocket amount has been met, the plan will pay 100 percent of reasonable and customary charges for services that are included in the plan's coverage. The rate structures, as described in the informational brochures, are as follows: Brown Plan Gold Plan Deductible $5,000 $1,000 Insurance Provider Payments up to maximum/member 100% / 0% 80% / 20% Out-of-pocket Maximum $5,000 $2,000 MONTANA COMPREHENSIVE HEALTH INSURANCE ASSOCIATION (MCHA) PROGRAM Background and Eligibility. The MCHA program was created by the Montana Legislature in 1985, Mont. Code. Ann. Sec et seq. to provide insurance to individuals considered uninsurable due to medical conditions. The general structure of Montana's health insurance pool is quite similar to Wyoming's pool. For example, it is managed by a board of eight directors. Further, Montana statute states, "the schedule of association plan premiums for eligible persons may not exceed 200% of the average premium rates charged by the five insurers or health service corporations with the largest premium amount of individual plans of major medical insurance in force in this state." 3 (Mont. Code Ann ) Revenues supporting the plan chiefly include both premiums by paid by enrolled persons and assessments on insurance companies, as in Wyoming. However, in contrast, Montana's statute provides, "If the needs of the association plan and the association portability plan exceed the funds generated by the 1% assessment, the association is then authorized to spend any funds appropriated by the legislature for the support of the plans." (Mont. Code Ann (6)(ii)) Furthermore, unlike Wyoming, Montana offers three programs: Traditional Program, the Premium Assistance Program (Pilot Program), and the Portability Plan (federal eligibility). The Traditional Program most closely compares to Wyoming's plans and different deductible options within Montana's program align quite closely with Wyoming's Brown and Gold Plans. Therefore, for purposes of simplicity, the comparative assessment will focus on Montana's Traditional Program, though each is briefly described later in this memo. In general, eligibility for Traditional or Pilot Program coverage requires individuals be: 3 Montana's statute also allows for reduced premiums for persons with income less than 150 percent of the federal poverty rate. WYOMING LEGISLATIVE SERVICE OFFICE 213 State Capitol Cheyenne, Wyoming TELEPHONE (307) FAX (307) lso@state.wy.us WEBSITE

of the burden")

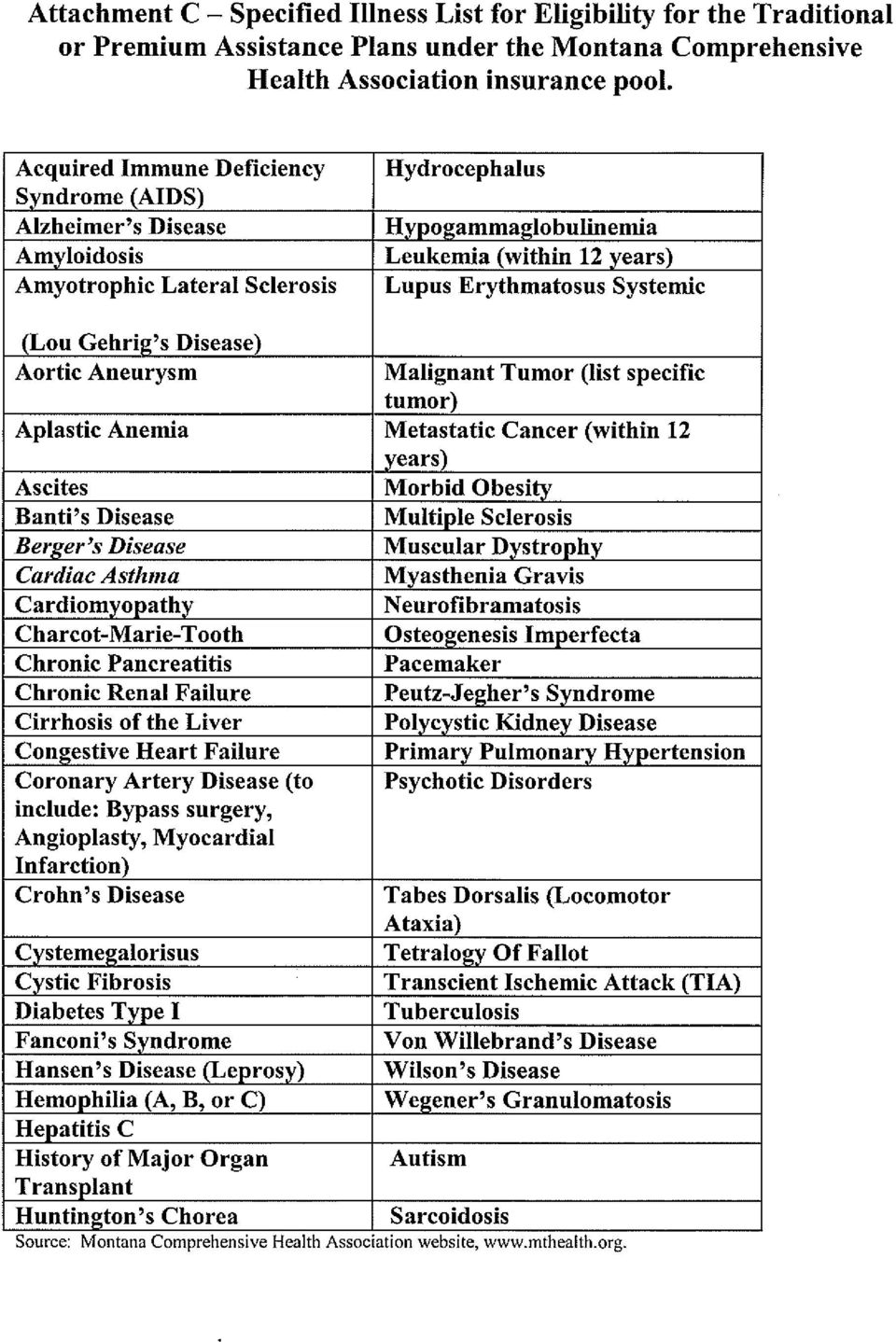

4 PAGE 4 OF 7 residents of Montana for at least 30 days; and rejected or offered a restricted rider by two insurers within the last six months or have a specified illness (Attachment C); and not eligible for any other health insurance coverage 4, or have comparable coverage, but pay more than 150 percent of the average premium rate used to calculate MCHA premiums. Insurance Plans Offered. The three main insurance coverage plans available to those who are eligible include: The Traditional Plan is for individuals with medical conditions who have either been denied coverage or offered a significant rider on a medical condition. There is a 12-month waiting period before pre-existing conditions are covered. This plan is also available to those who are eligible for Medicare coverage, with Medicare as the primary payer and this plan the secondary payer (Medicare Carve-Out Plan). The Traditional Plan offers three levels of deductibles and, for purposes of comparison, is the most directly comparable to Wyoming's Gold and Brown Plans. The brochure for the Traditional Plan contains a list of benefits, as well as services covered, and is provided as Attachment D; The Premium Assistance Program (Pilot Program) is for individuals who have either been denied coverage or offered a significant rider on a medical condition, and meet certain income guidelines. The income guidelines are based on 150 percent of the federal poverty level and vary by family size. This plan offers the same coverage as the Traditional Plan, but, notably, the 12-month waiting period for pre-existing condition coverage is reduced to 4 months (if applicable). In addition, the premiums are subsidized during the pre-existing condition waiting period at a higher rate than after the waiting period has expired. This plan receives federal funds as a subsidy. This plan is also available to those who are eligible for Medicare coverage, with Medicare as the primary payer and this plan the secondary payer (Medicare Carve-Out Plan). The MCHA Portability Plans are for individuals who are federally eligible for coverage under MCHA and are leaving group coverage. Eligibility for this plan is as follows: Montana resident; most recent prior (18 months aggregate) creditable coverage was under a group health plan, governmental plan, or church plan; do not have other health insurance coverage; not eligible for coverage under a group health plan; prior continuing coverage under COBRA or similar state program, which has been exhausted; application for this program is made within 63 days of the last day of previous coverage; individuals certified as eligible for Federal Trade Adjustment Act assistance and a health insurance tax credit or for Pension Benefit Guarantee Corporation assistance may also be eligible under specific circumstances. 4 "Other health insurance coverage" includes any other comprehensive health coverage, such as employer group insurance, individual health coverage, Medicare (except individuals who are eligible to be covered by the Traditional Plan Medicare Carve-out Plan), or Medicaid. WYOMING LEGISLATIVE SERVICE OFFICE 213 State Capitol Cheyenne, Wyoming TELEPHONE (307) FAX (307) lso@state.wy.us WEBSITE

5 PAGE 5 OF 7 Benefits. Each plan program has similar benefit packages, but there are some important differences that deserve mentioning. All three plans cover, overall, the same services, with some difference in the pre-existing condition wait period. The Traditional Plan, Premium Assistance Plan, and Medicare Carve-Out Plan cover the same services, but the Traditional plan requires a twelve (12) month pre-existing wait period, while the Premium Assistance Plan reduces the wait period to four (4) months. However, the pre-existing condition wait period does not apply to newborn children or children placed for adoption or if previous creditable coverage was not voluntarily canceled by the applicant, application was made within thirty days of the last day of previous coverage, or if all other options for health insurance, including COBRA or state continuation, have been exhausted. The Portability Plan covers the same services as the Traditional and Premium Assistance Plans, but with a 12 month pre-existing condition wait period that may apply, depending upon circumstances. However, the requirement for 18 months of previous creditable coverage is waived for children under 18 months of age. In addition, children born to individuals covered under the Portability Plan can be placed on their own Portability Plan after 31 days of coverage on their parent s plan. LSO Research staff are not able to conduct an actuarial assessment of the value of the benefits for both the Wyoming and Montana plans. However, consumers are likely unable to conduct that assessment either. Therefore, based upon the summary of benefits available and their structure, many of the same services appear to be covered. However, the structure of the prescription drug benefits, for example, are quite different among comparable plans between the two states and even among the Gold Plan and Brown Plan within Wyoming. A comparison would also depend upon whether the consumer required several less expensive prescriptions or a few expensive prescriptions. The Wyoming Plan advertises an adult wellness plan, not advertised by the Montana plan. These are just a few examples of the differences. It is likely there are other differences that have not been identified in this memorandum, but even those that have been identified serve as a hindrance to direct comparison. In summary, the benefits of the two state plans are not identical. The quality of the benefits would likely depend upon the specific health characteristics of the consumer. Each reader may chose to compare the advertised covered benefits (which are likely not exhaustive) by considering page 2 of Attachment A, for Wyoming's plans and page 2 of Attachment D, for Montana's Traditional Plan. After such an assessment, it may be prudent to ask whether the difference in benefits, which may be subjective, justifies the demonstrated difference in monthly premiums. It would be difficult for this researcher to conclude that the difference in benefits for Montana's Traditional Plan justifies the difference in the premium levels. In fact, in some areas, Montana's benefits may be greater than Wyoming's, e.g., the maximum lifetime benefit. However, this determination has been made without the benefit of a full actuarial analysis and may differ depending upon the health of each consumer. Premiums and Deductibles. The premiums for Montana's plans are provided as Attachment E. Like Wyoming's plans, no family premiums and deductibles are offered. Individuals are required to apply to the program and pay separate premiums. The annual deductibles for the three plans are as follows: WYOMING LEGISLATIVE SERVICE OFFICE 213 State Capitol Cheyenne, Wyoming TELEPHONE (307) FAX (307) lso@state.wy.us WEBSITE

months.")

6 PAGE 6 OF 7 Maximum Annual Deductible Plan Deductible Co-pay & Co-pay limit (out-of-pocket expenses) Traditional $1,000 80/20 $5,000 $2,500 80/20 $6,000 $5,000 80/20 $7,500 Premium Assistance $1,000 80/20 $5,000 Portability Plan $1,000 70/30 $3,000 $2,500 70/30 $5,000 $5,000 70/30 $8,000 COMPARATIVE DISCUSSION REVENUES AND OTHER FACTORS Some state plans reportedly have the benefit of other sources of revenues which, in effect, serve to subsidize either the assessments on insurance companies or the premiums paid by participants. Historically, that does not appear to be the case for Wyoming and Montana, based upon discussions with each state's staff. No state funds are currently used in either plan, although both use a credit on the premium tax for insurance companies, which could serve as an indirect subsidy for the companies, but not for the plans. Also, in the recent past, neither the Wyoming plans or the Montana Traditional Plan benefited from outside revenue such as federal funds. 5 Table 2 illustrates a snapshot summary of the funding of the two state health insurance pools. The interest income has been removed from the revenue of both plans in order to provide a more comparable illustration. As you can see, the premiums paid by participants in Montana, even though they are lower, make up a similar, or even larger share of the core revenues of the two pools. This suggests that the revenue structure of the two pools is not substantially favorable for Montana. In addition, Wyoming's plan has historically reduced their net asset balance, suggesting reserves collected in a prior time period were, in effect, subsidizing the expenses to some degree during FY04 and FY05. Table 2. FY04 and FY05 Key Revenue Statistics. Montana Traditional Plan Wyoming FY04 FY05 FY04 FY05 Premiums Earned $5,417,151 $6,839,638 $3,473,192 $3,850,905 Membership Assessment $2,111,271 $1,535,508 $1,249,488 $1,599,614 % Assessments 28% 18% 26% 29% Change in (Net) Asset Balance $437,300 ($677,019) ($756,877) ($1,214,720) Source: LSO Research staff summary of Montana and Wyoming's Health Insurance Pool Statements of Operations. Without a full comparative actuarial assessment of the two plans, it is not possible for LSO Research staff to definitively explain the reasons for premium disparities between the two pools. However, after removing the potential for a substantial revenue subsidy in some form, it appears that at least three potential causes still remain. 1) While the monthly premiums in Montana currently do appear to be comparatively lower than for Wyoming's pool, the potential total annual out-of-pocket expenses appear to be much more comparable. That is, although Montana's premiums are lower, the Traditional Plan in Montana has higher out-of-pocket 5 Wyoming's plan will receive approximately $370,000 in federal funds for this year, according to Department of Insurance staff, and Montana's Premium Assistance Plan is federally subsidized, according to Montana plan documents. WYOMING LEGISLATIVE SERVICE OFFICE 213 State Capitol Cheyenne, Wyoming TELEPHONE (307) FAX (307) lso@state.wy.us WEBSITE

7 PAGE 7 OF 7 maximum expenditures. In particular, for populations that include high users of medical services, the total, annual personal expenses may offer a better, or at least an additional, comparison of the true participant costs. Table 3 summarizes this comparison and directly relates to the same hypothetical populations illustrated earlier in Table 1. Table 3. Annual, Potential Out-of-Pocket Expenses: Montana and Wyoming. 1. Monthly Premium Single Female age Premium & Out-of- Pocket Potential Single Female age Monthly Premium Single Male age Premium & Out-of- Pocket Potential Single Male age 55 Wyoming Brown Plan Source: LSO Research staff computations. Montana Traditional #1 WY Cost as a Percentage of MT's Plan Wyoming Gold Plan Montana Traditional #2 WY Cost as a Percentage of MT's Plan $504 $ % $718 $ % $11,048 $10, % $10,616 $10, % $754 $ % $1,075 $ % $14,048 $13, % $14,900 $14, % As shown in Table 3, the total, annual out-of-pocket potential expenditures for pool participants in the two pools are quite close (rows 2 and 4), even though the monthly premiums in Montana's plan are currently substantially lower (rows 1 and 3). 2) Wyoming's pool had a negative equity balance at the close of FY05 of $290,197. Furthermore, the equity balance had been declining for at least two years. Therefore, it seems possible that the pool premiums and assessments were designed to insure that an appropriate equity balance is maintained. Put differently, the assessments and premiums in FY06 and FY07 may include this "build-up" effort. 3) Finally, the claims' history of the two pools could provide yet another explanation for the difference in premiums. In short, even if the eligibility criteria is similar, perhaps the claims experience is different between the two state pool populations. This difference in claims history is evident even between two plans in Montana for FY04 and FY05 for the Traditional Plan and the Portability Plan. If you need anything further, please contact LSO Research at WYOMING LEGISLATIVE SERVICE OFFICE 213 State Capitol Cheyenne, Wyoming TELEPHONE (307) FAX (307) lso@state.wy.us WEBSITE

8

9

10

11

12

13

14

15

16

17

18

SOMETHING OLD, SOMETHING NEW: TEXAS TWO HIGH-RISK POOLS

July 19, 2010 Contact: Stacey Pogue, pogue@cppp.org SOMETHING OLD, SOMETHING NEW: TEXAS TWO HIGH-RISK POOLS Thanks to national health reform, Texas now has two separate high-risk pools that offer health

July 19, 2010 Contact: Stacey Pogue, pogue@cppp.org SOMETHING OLD, SOMETHING NEW: TEXAS TWO HIGH-RISK POOLS Thanks to national health reform, Texas now has two separate high-risk pools that offer health

HEALTH CARE REFORM DOCUMENT FROM THE WEBSITE OF BLUE CROSS BLUE SHIELD OF NORTH DAKOTA

HEALTH CARE REFORM DOCUMENT FROM THE WEBSITE OF BLUE CROSS BLUE SHIELD OF NORTH DAKOTA Frequently Asked Questions I ve heard the federal government launched a new website called Healthcare.gov. How can

HEALTH CARE REFORM DOCUMENT FROM THE WEBSITE OF BLUE CROSS BLUE SHIELD OF NORTH DAKOTA Frequently Asked Questions I ve heard the federal government launched a new website called Healthcare.gov. How can

Minnesota Comprehensive Health Association (MCHA) - Frequently Asked Questions & Answers about Eligibility/Application

- Frequently Asked Questions & Answers about Eligibility/Application") Minnesota Comprehensive Health Association (MCHA) - Frequently Asked Questions & Answers about Eligibility/Application I. Medicare Supplement Plans Application Materials and Processing 1. Why does the

Minnesota Comprehensive Health Association (MCHA) - Frequently Asked Questions & Answers about Eligibility/Application I. Medicare Supplement Plans Application Materials and Processing 1. Why does the

Arizona Health Care Cost Containment System Issue Paper on High-Risk Pools

Arizona Health Care Cost Containment System Issue Paper on High-Risk Pools Prepared by: T. Scott Bentley, A.S.A. Associate Actuary David F. Ogden, F.S.A. Consulting Actuary August 27, 2001 Arizona Health

Arizona Health Care Cost Containment System Issue Paper on High-Risk Pools Prepared by: T. Scott Bentley, A.S.A. Associate Actuary David F. Ogden, F.S.A. Consulting Actuary August 27, 2001 Arizona Health

AN ACT RELATING TO THE COMPREHENSIVE HEALTH INSURANCE POOL ACT; AUTHORIZING THE BOARD OF DIRECTORS TO IDENTIFY ADDITIONAL UNINSURED POPULATIONS FOR COVERAGE PURSUANT TO THAT ACT; AUTHORIZING THE BOARD

AN ACT RELATING TO THE COMPREHENSIVE HEALTH INSURANCE POOL ACT; AUTHORIZING THE BOARD OF DIRECTORS TO IDENTIFY ADDITIONAL UNINSURED POPULATIONS FOR COVERAGE PURSUANT TO THAT ACT; AUTHORIZING THE BOARD

INDIVIDUAL (NON-GROUP) POLICIES

POLICIES") CHAPTER 3 INDIVIDUAL (NON-GROUP) POLICIES What are they? Who are they for? How to obtain coverage INTRODUCTION An individual health insurance policy is one that is purchased outside a group setting. (Most

CHAPTER 3 INDIVIDUAL (NON-GROUP) POLICIES What are they? Who are they for? How to obtain coverage INTRODUCTION An individual health insurance policy is one that is purchased outside a group setting. (Most

Minnesota Comprehensive Health Association. Summary of Benefits and Plan Options

Minnesota Comprehensive Health Association Summary of Benefits and Options www.mchamn.com MCHA Customer Service 1-866-894-8053 TTY: 952-992-3190 or toll-free at 1-800-841-6753 Monday Friday: 7 a.m. 6 p.m.

Minnesota Comprehensive Health Association Summary of Benefits and Options www.mchamn.com MCHA Customer Service 1-866-894-8053 TTY: 952-992-3190 or toll-free at 1-800-841-6753 Monday Friday: 7 a.m. 6 p.m.

Health Insurance Risk-Sharing Plan (HIRSP)

") Health Insurance Risk-Sharing Plan (HIRSP) Informational Paper 53 Wisconsin Legislative Fiscal Bureau January, 2013 Wisconsin Legislative Fiscal Bureau January, 2013 Health Insurance Risk-Sharing Plan

Health Insurance Risk-Sharing Plan (HIRSP) Informational Paper 53 Wisconsin Legislative Fiscal Bureau January, 2013 Wisconsin Legislative Fiscal Bureau January, 2013 Health Insurance Risk-Sharing Plan

As of January 1, 2014, most individuals must have some form of health coverage, or pay a penalty to the federal government.

Consumer Alert Health Insurance for 2014: What You Need to Know Before You Enroll (Individuals) As of January 1, 2014, most individuals must have some form of health coverage, or pay a penalty to the federal

Consumer Alert Health Insurance for 2014: What You Need to Know Before You Enroll (Individuals) As of January 1, 2014, most individuals must have some form of health coverage, or pay a penalty to the federal

Simply BLUE MEDICARE SUPPLEMENT PLANS SR BRO 2013.1.A

Simply BLUE MEDICARE SUPPLEMENT PLANS 2013 SR BRO 2013.1.A Simply BLUE Table of Contents Standard Benefit Offerings... 2 Disclosures... 3 Important Facts to Consider... 4 Supplement Plan Premiums... 5

Simply BLUE MEDICARE SUPPLEMENT PLANS 2013 SR BRO 2013.1.A Simply BLUE Table of Contents Standard Benefit Offerings... 2 Disclosures... 3 Important Facts to Consider... 4 Supplement Plan Premiums... 5

Health Insurance Coverage

Protecting Your Health Insurance Coverage This booklet explains... Your rights and protections under recent Federal law How to help maintain existing coverage Where you can get more help For additional

Protecting Your Health Insurance Coverage This booklet explains... Your rights and protections under recent Federal law How to help maintain existing coverage Where you can get more help For additional

Wisconsin typically ranks among the states with the highest level of health

Health Insurance Marketplace in Wisconsin by Wisconsin Office of the Commissioner of Insurance Staff Wisconsin typically ranks among the states with the highest level of health care coverage for its citizens.

Health Insurance Marketplace in Wisconsin by Wisconsin Office of the Commissioner of Insurance Staff Wisconsin typically ranks among the states with the highest level of health care coverage for its citizens.

Simply BLUE MEDICARE SUPPLEMENT PLANS SR BRO 2015

Simply BLUE MEDICARE SUPPLEMENT PLANS 2015 SR BRO 2015 Simply BLUE Table of Contents Standard Benefit Offerings...2 Disclosures...3 Important Facts to Consider...4 Supplement Plan Premiums...5 Benefit

Simply BLUE MEDICARE SUPPLEMENT PLANS 2015 SR BRO 2015 Simply BLUE Table of Contents Standard Benefit Offerings...2 Disclosures...3 Important Facts to Consider...4 Supplement Plan Premiums...5 Benefit

BlueCross65. Medicare Supplement Plans

BlueCross65 Medicare Supplement Plans Medicare Supplement Coverage Filling the Gaps of Your Medicare Coverage With Medicare Part A and Part B alone, you are required to pay deductibles and coinsurance

BlueCross65 Medicare Supplement Plans Medicare Supplement Coverage Filling the Gaps of Your Medicare Coverage With Medicare Part A and Part B alone, you are required to pay deductibles and coinsurance

NEW JERSEY INDIVIDUAL HEALTH COVERAGE PROGRAM and SMALL EMPLOYER HEALTH BENEFITS PROGRAM 20 West State Street, 10th Floor PO Box 325 Trenton, NJ 08625

Date: November 3, 1997 NEW JERSEY INDIVIDUAL HEALTH COVERAGE PROGRAM and SMALL EMPLOYER HEALTH BENEFITS PROGRAM 20 West State Street, 10th Floor PO Box 325 Trenton, NJ 08625 ADVISORY BULLETIN 97-JOINT-02

Date: November 3, 1997 NEW JERSEY INDIVIDUAL HEALTH COVERAGE PROGRAM and SMALL EMPLOYER HEALTH BENEFITS PROGRAM 20 West State Street, 10th Floor PO Box 325 Trenton, NJ 08625 ADVISORY BULLETIN 97-JOINT-02

NEW HEALTH MARKETPLACE

NEW HEALTH INSURANCE MARKETPLACE DISCLAIMER The information in this presentation is based on information provided www.healthcare.gov. It is not provided as advice for your personal situation. Georgia Perimeter

NEW HEALTH INSURANCE MARKETPLACE DISCLAIMER The information in this presentation is based on information provided www.healthcare.gov. It is not provided as advice for your personal situation. Georgia Perimeter

Skilled Nursing Facility Coinsurance Part A Deductible Part B. Part B Excess (100%) Foreign Travel Emergency. Foreign Travel Emergency

Foreign Travel Emergency. Foreign Travel Emergency") Montana OLD SURETY LIFE INSURANCE COMPANY 2014 ( effective 01/01/2014 ) Outline of Medicare Supplement Coverage Benefit Plans A and F Only are being offered by the company at this time. These charts show

Montana OLD SURETY LIFE INSURANCE COMPANY 2014 ( effective 01/01/2014 ) Outline of Medicare Supplement Coverage Benefit Plans A and F Only are being offered by the company at this time. These charts show

Oklahoma Temporary High Risk Pool 2012 All Rights Reserved

1 What is it? A temporary insurance plan created and funded by Section 1101 of The Patient Protection & Affordable Care Act (ACA) A bridge until January 2014 when new laws are expected to take effect Also

1 What is it? A temporary insurance plan created and funded by Section 1101 of The Patient Protection & Affordable Care Act (ACA) A bridge until January 2014 when new laws are expected to take effect Also

Benefit Chart of Medicare Supplement Plans Sold on or After January 1, 2014

Benefit Chart of Medicare Supplement Plans Sold on or After January 1, 2014 This chart shows the benefits included in each of the standard Medicare Supplement plans. Every company must make available Plans

Benefit Chart of Medicare Supplement Plans Sold on or After January 1, 2014 This chart shows the benefits included in each of the standard Medicare Supplement plans. Every company must make available Plans

Health plans for every body

Health plans for every body Supplemental coverage for Medicare members Medicare modahealth.com/medicare Available April 1 through Dec. 31, 2015 Hello. Welcome to Moda Health, the place you go when you

Health plans for every body Supplemental coverage for Medicare members Medicare modahealth.com/medicare Available April 1 through Dec. 31, 2015 Hello. Welcome to Moda Health, the place you go when you

This booklet constitutes a small entity compliance guide for purposes of the Small Business Regulatory Enforcement Fairness Act of 1996.

This publication has been developed by the U.S. Department of Labor, Employee Benefits Security Administration (EBSA). To view this and other EBSA publications, visit the agency s Website at dol.gov/ebsa.

This publication has been developed by the U.S. Department of Labor, Employee Benefits Security Administration (EBSA). To view this and other EBSA publications, visit the agency s Website at dol.gov/ebsa.

HIPAA Portability & Accountability: How HIPAA Affects Individual Coverage

HIPAA Portability & Accountability: How HIPAA Affects Individual Coverage The Health Insurance Portability and Accountability Act of 1996, known as HIPAA, affects the way state and federal governments

HIPAA Portability & Accountability: How HIPAA Affects Individual Coverage The Health Insurance Portability and Accountability Act of 1996, known as HIPAA, affects the way state and federal governments

Health Care Reform Frequently Asked Questions (FAQ) Consumers Employers

Consumers Employers") This page provides answers to frequently asked questions (FAQ) regarding The Patient Protection and Affordable Care Act (PPACA; P.L. 111-148) and the Health Care and Education Reconciliation Act of 2010

This page provides answers to frequently asked questions (FAQ) regarding The Patient Protection and Affordable Care Act (PPACA; P.L. 111-148) and the Health Care and Education Reconciliation Act of 2010

Section 2: INDIVIDUALS WHO CURRENTLY HAVE

Section 2: INDIVIDUALS WHO CURRENTLY HAVE COVERAGE OR AN OFFER OF COVERAGE FROM THEIR EMPLOYER Section 2 covers enrollment issues for individuals who have coverage or an offer of coverage whether through

Section 2: INDIVIDUALS WHO CURRENTLY HAVE COVERAGE OR AN OFFER OF COVERAGE FROM THEIR EMPLOYER Section 2 covers enrollment issues for individuals who have coverage or an offer of coverage whether through

Understanding the ObamaCare Health Insurance Plans in North Carolina Understanding Insurance and Affordable Care Act Terminology: ACA- Marketplace

Understanding the ObamaCare Health Insurance Plans in North Carolina As a result of the Affordable Care Act (a.k.a. ObamaCare) the following provisions are now in place for health insurance policies with

Understanding the ObamaCare Health Insurance Plans in North Carolina As a result of the Affordable Care Act (a.k.a. ObamaCare) the following provisions are now in place for health insurance policies with

Deciding Whether to Elect COBRA Health Care Continuation Coverage After Enactment of HIPAA INTRODUCTION

Deciding Whether to Elect COBRA Health Care Continuation Coverage After Enactment of HIPAA Notice 98-12 INTRODUCTION A key decision that millions of Americans face each year is whether to elect COBRA 1

Deciding Whether to Elect COBRA Health Care Continuation Coverage After Enactment of HIPAA Notice 98-12 INTRODUCTION A key decision that millions of Americans face each year is whether to elect COBRA 1

MedicareBlue Supplement

SM MedicareBlue Supplement Plans A, D, F, High Deductible F, and N 2015 Outlines of Coverage Benefit Chart of Medicare Supplement Plans Sold for Effective Dates on or after January 1, 2015 This chart shows

SM MedicareBlue Supplement Plans A, D, F, High Deductible F, and N 2015 Outlines of Coverage Benefit Chart of Medicare Supplement Plans Sold for Effective Dates on or after January 1, 2015 This chart shows

Horizon Blue Cross Blue Shield of New Jersey

Horizon Blue Cross Blue Shield of New Jersey Pre Existing Condition and Certificate of Creditable Coverage For Individual Insurance, Excluding Medigap An independent licensee of the Blue Cross and Blue

Horizon Blue Cross Blue Shield of New Jersey Pre Existing Condition and Certificate of Creditable Coverage For Individual Insurance, Excluding Medigap An independent licensee of the Blue Cross and Blue

Your Health Care Benefit Program

Your Health Care Benefit Program HMO ILLINOIS A Blue Cross HMO a product of Blue Cross and Blue Shield of Illinois HMO GROUP CERTIFICATE RIDER This Certificate, to which this Rider is attached to and becomes

Your Health Care Benefit Program HMO ILLINOIS A Blue Cross HMO a product of Blue Cross and Blue Shield of Illinois HMO GROUP CERTIFICATE RIDER This Certificate, to which this Rider is attached to and becomes

Health Care Reform Checklist: Provisions, Obstacles and Solutions

Health Care Reform Checklist: Provisions, Obstacles and Solutions HEALTH CARE REFORM PROVISION: COVERAGE FOR CHILDREN UNTIL AGE 26 Summary of Benefit: Benefits are the same as those for other dependent

Health Care Reform Checklist: Provisions, Obstacles and Solutions HEALTH CARE REFORM PROVISION: COVERAGE FOR CHILDREN UNTIL AGE 26 Summary of Benefit: Benefits are the same as those for other dependent

AN EMPLOYEE S GUIDE TO HEALTH BENEFITS UNDER COBRA EMPLOYEE BENEFITS SECURITY ADMINISTRATION UNITED STATES DEPARTMENT OF LABOR

AN EMPLOYEE S GUIDE TO HEALTH BENEFITS UNDER COBRA EMPLOYEE BENEFITS SECURITY ADMINISTRATION UNITED STATES DEPARTMENT OF LABOR This publication has been developed by the U.S. Department of Labor, Employee

AN EMPLOYEE S GUIDE TO HEALTH BENEFITS UNDER COBRA EMPLOYEE BENEFITS SECURITY ADMINISTRATION UNITED STATES DEPARTMENT OF LABOR This publication has been developed by the U.S. Department of Labor, Employee

Indiana Comprehensive Health Insurance Association. Program Overview

Indiana Comprehensive Health Insurance Association Program Overview Eligibility ICHIA was designed to cover eligible citizens with pre-existing medical conditions and the chronically ill obtain comprehensive

Indiana Comprehensive Health Insurance Association Program Overview Eligibility ICHIA was designed to cover eligible citizens with pre-existing medical conditions and the chronically ill obtain comprehensive

The Health Benefit Exchange and the Commercial Insurance Market

The Health Benefit Exchange and the Commercial Insurance Market Overview The federal health care reform law directs states to set up health insurance marketplaces, called Health Benefit Exchanges, that

The Health Benefit Exchange and the Commercial Insurance Market Overview The federal health care reform law directs states to set up health insurance marketplaces, called Health Benefit Exchanges, that

The Large Business Guide to Health Care Law

The Large Business Guide to Health Care Law How the new changes in health care law will affect you and your employees Table of contents Introduction 3 Part I: A general overview of the health care law

The Large Business Guide to Health Care Law How the new changes in health care law will affect you and your employees Table of contents Introduction 3 Part I: A general overview of the health care law

THE KANSAS AFFORDABLE CARE ACT IMPLEMENTATION. Linda J. Sheppard November 6, 2014

THE KANSAS AFFORDABLE CARE ACT IMPLEMENTATION Linda J. Sheppard November 6, 2014 The Kansas Market Approximately 348,000 Kansans are uninsured - 12.3% of the state s population 44,130 are children, but

THE KANSAS AFFORDABLE CARE ACT IMPLEMENTATION Linda J. Sheppard November 6, 2014 The Kansas Market Approximately 348,000 Kansans are uninsured - 12.3% of the state s population 44,130 are children, but

Coinsurance A percentage of a health care provider's charge for which the patient is financially responsible under the terms of the policy.

Glossary of Health Insurance Terms On March 23, 2010, President Obama signed the Patient Protection and Affordable Care Act (PPACA) into law. When making decisions about health coverage, consumers should

Glossary of Health Insurance Terms On March 23, 2010, President Obama signed the Patient Protection and Affordable Care Act (PPACA) into law. When making decisions about health coverage, consumers should

HEALTH INSURANCE FOR SMALL BUSINESSES

HEALTH INSURANCE FOR SMALL BUSINESSES CHAPTER 8 What is it? The North Carolina General Assembly enacted special laws that make it easier for small employers to purchase health insurance for their employees.

HEALTH INSURANCE FOR SMALL BUSINESSES CHAPTER 8 What is it? The North Carolina General Assembly enacted special laws that make it easier for small employers to purchase health insurance for their employees.

Effective Date: The date on which coverage under an insurance policy begins.

Key Healthcare Insurance Terms Agent: A person who represents an insurance company and solicits or sells the company s insurance products. An agent may represent a single company or multiple companies.

Key Healthcare Insurance Terms Agent: A person who represents an insurance company and solicits or sells the company s insurance products. An agent may represent a single company or multiple companies.

NC General Statutes - Chapter 58 Article 68 1

Article 68. Health Insurance Portability and Accountability. 58-68-1 through 58-68-20: Repealed by Session Laws 1997-259, s. 1(a). Part A. Group Market Reforms. Subpart 1. Portability, Access, and Renewability

Article 68. Health Insurance Portability and Accountability. 58-68-1 through 58-68-20: Repealed by Session Laws 1997-259, s. 1(a). Part A. Group Market Reforms. Subpart 1. Portability, Access, and Renewability

Insurance Discrimination

Insurance Discrimination Michael Bachhuber, Attorney Wisconsin Coalition for Advocacy Fair or unfair discrimination Introduction Insurance discrimination is a bit different conceptually from other forms

Insurance Discrimination Michael Bachhuber, Attorney Wisconsin Coalition for Advocacy Fair or unfair discrimination Introduction Insurance discrimination is a bit different conceptually from other forms

The Affordable Care Act in New Hampshire

The State of New Hampshire Insurance Department 21 South Fruit Street, Suite 14 Concord, NH 03301 (603) 271-2261 Fax (603) 271-1406 TDD Access: Relay NH 1-800-735-2964 The Affordable Care Act in New Hampshire

The State of New Hampshire Insurance Department 21 South Fruit Street, Suite 14 Concord, NH 03301 (603) 271-2261 Fax (603) 271-1406 TDD Access: Relay NH 1-800-735-2964 The Affordable Care Act in New Hampshire

Health Care Reform Update

Small Businesses No Financial Requirements for Small Businesses: The ACA imposes no financial requirements for small businesses to contribute to their employees health insurance. However, beginning in

Small Businesses No Financial Requirements for Small Businesses: The ACA imposes no financial requirements for small businesses to contribute to their employees health insurance. However, beginning in

STATE OF IOWA HEALTH INSURANCE PLAN COMPARISON EFFECTIVE JANUARY 1, 2016

This comparison is only a summary of benefits. Benefits will be administered as described in each plan s Summary of Benefits & Coverage. For further details, refer to those documents or call Wellmark Blue

This comparison is only a summary of benefits. Benefits will be administered as described in each plan s Summary of Benefits & Coverage. For further details, refer to those documents or call Wellmark Blue

An Employer s Guide to Group Health Continuation Coverage Under COBRA

An Employer s Guide to Group Health Continuation Coverage Under COBRA The Consolidated Omnibus Budget Reconciliation Act EMPLOYEE BENEFITS SECURITY ADMINISTRATION UNITED STATES DEPARTMENT OF LABOR This

An Employer s Guide to Group Health Continuation Coverage Under COBRA The Consolidated Omnibus Budget Reconciliation Act EMPLOYEE BENEFITS SECURITY ADMINISTRATION UNITED STATES DEPARTMENT OF LABOR This

Basic, including 100% Part B coinsurance Skilled Nursing Facility Coinsurance

Group Health Options, Inc. Outline of Medicare Supplement Coverage - Cover Page Benefit Plans A, F, K and N See Outlines of Coverage sections for details about ALL plans These charts show the benefits

Group Health Options, Inc. Outline of Medicare Supplement Coverage - Cover Page Benefit Plans A, F, K and N See Outlines of Coverage sections for details about ALL plans These charts show the benefits

MedicareBlue Supplement SM

MedicareBlue Supplement SM Important Information about the enclosed premiums and Medicare deductibles and cost-sharing amounts The MedicareBlue Supplement information enclosed in this Outline of Coverage

MedicareBlue Supplement SM Important Information about the enclosed premiums and Medicare deductibles and cost-sharing amounts The MedicareBlue Supplement information enclosed in this Outline of Coverage

Guide to Purchasing Health Insurance

Guide to Purchasing Health Insurance What are your health insurance choices? Which type is right for you? Sample questions Looking for insurance in specific situations Tips for shopping for health coverage

Guide to Purchasing Health Insurance What are your health insurance choices? Which type is right for you? Sample questions Looking for insurance in specific situations Tips for shopping for health coverage

How To Comply With The Health Care Act

AFFORDABLE CARE ACT Employers that provide health coverage to employees are responsible for complying with many of the provisions of the Affordable Care Act (ACA). Provisions take effect on staggered dates

AFFORDABLE CARE ACT Employers that provide health coverage to employees are responsible for complying with many of the provisions of the Affordable Care Act (ACA). Provisions take effect on staggered dates

IC 27-8-15 Chapter 15. Small Employer Group Health Insurance

IC 27-8-15 Chapter 15. Small Employer Group Health Insurance IC 27-8-15-0.1 Application of certain amendments to chapter Sec. 0.1. The following amendments to this chapter apply as follows: (1) The addition

IC 27-8-15 Chapter 15. Small Employer Group Health Insurance IC 27-8-15-0.1 Application of certain amendments to chapter Sec. 0.1. The following amendments to this chapter apply as follows: (1) The addition

FAQ: PARTICIPANTS ON EARNED COVERAGE

FAQ: PARTICIPANTS ON EARNED COVERAGE What should I do when the Health Insurance Marketplace goes into effect on January 1? You don t need to do anything if you have earned coverage through the DGA Producer

FAQ: PARTICIPANTS ON EARNED COVERAGE What should I do when the Health Insurance Marketplace goes into effect on January 1? You don t need to do anything if you have earned coverage through the DGA Producer

OVERVIEW OF PRIVATE INSURANCE MARKET REFORMS IN THE PATIENT PROTECTION AND AFFORDABLE CARE ACT AND RESOURCES FOR FREQUENTLY ASKED QUESTIONS

OVERVIEW OF PRIVATE INSURANCE MARKET REFORMS IN THE PATIENT PROTECTION AND AFFORDABLE CARE ACT AND RESOURCES FOR FREQUENTLY ASKED QUESTIONS Brief Prepared by MATTHEW COKE Senior Research Attorney LEGISLATIVE

OVERVIEW OF PRIVATE INSURANCE MARKET REFORMS IN THE PATIENT PROTECTION AND AFFORDABLE CARE ACT AND RESOURCES FOR FREQUENTLY ASKED QUESTIONS Brief Prepared by MATTHEW COKE Senior Research Attorney LEGISLATIVE

CHAPTER 2016-194. Committee Substitute for Committee Substitute for Senate Bill No. 1170

CHAPTER 2016-194 Committee Substitute for Committee Substitute for Senate Bill No. 1170 An act relating to health plan regulatory administration; amending s. 112.08, F.S.; authorizing local governmental

CHAPTER 2016-194 Committee Substitute for Committee Substitute for Senate Bill No. 1170 An act relating to health plan regulatory administration; amending s. 112.08, F.S.; authorizing local governmental

Hospitalization and preventive care paid at 100%; other basic benefits paid at 50% Basic, including 100% Part B coinsurance. 100% Part B coinsurance

Health First Insurance, Inc. OUTLINE OF COVERAGE 2014 Benefit Plans A, F, N Benefit Chart of Medicare Supplement Plans Sold on or After June 1, 2010 This chart shows the benefits included in each of the

Health First Insurance, Inc. OUTLINE OF COVERAGE 2014 Benefit Plans A, F, N Benefit Chart of Medicare Supplement Plans Sold on or After June 1, 2010 This chart shows the benefits included in each of the

Research Memo. 04 RM 027 Date: August 17, 2004 Author: Don Richards, Senior Research Analyst

Research Memo 04 RM 027 Date: August 17, 2004 Author: Don Richards, Senior Research Analyst Re: Descriptive s on K-12 School District Health Insurance Plans PURPOSE Summarize the range of health insurance

Research Memo 04 RM 027 Date: August 17, 2004 Author: Don Richards, Senior Research Analyst Re: Descriptive s on K-12 School District Health Insurance Plans PURPOSE Summarize the range of health insurance

Affordable Care Act (ACA) Frequently Asked Questions

Frequently Asked Questions") Grandfathered policies Q1: What is grandfathered health plan coverage? A: The interim final rule on grandfathering under ACA generally defines grandfathered health plan coverage as coverage provided by

Grandfathered policies Q1: What is grandfathered health plan coverage? A: The interim final rule on grandfathering under ACA generally defines grandfathered health plan coverage as coverage provided by

An Employer s Guide to Group Health Continuation Coverage Under COBRA

An Employer s Guide to Group Health Continuation Coverage Under COBRA The Consolidated Omnibus Budget Reconciliation Act U.S. Department of Labor Employee Benefits Security Administration This publication

An Employer s Guide to Group Health Continuation Coverage Under COBRA The Consolidated Omnibus Budget Reconciliation Act U.S. Department of Labor Employee Benefits Security Administration This publication

A B C D F l F* G K L M N Basic including

Aetna Life Insurance Company Outline of Medicare Supplement Coverage Benefit Plans A, B, C, F, G and N are Offered This chart shows the benefits included in each of the standard Medicare supplement plans.

Aetna Life Insurance Company Outline of Medicare Supplement Coverage Benefit Plans A, B, C, F, G and N are Offered This chart shows the benefits included in each of the standard Medicare supplement plans.

Vermont Blue 65. Coverage for Vermonters with Medicare. 2016 Medicare Supplemental Products. Group Brochure. An independent, local Vermont company

Vermont Blue 65 SM Coverage for Vermonters with Medicare 2016 Medicare Supplemental Products Group Brochure An independent, local Vermont company Three smart steps to quality health care after retirement:

Vermont Blue 65 SM Coverage for Vermonters with Medicare 2016 Medicare Supplemental Products Group Brochure An independent, local Vermont company Three smart steps to quality health care after retirement:

Senate-Passed Bill (Patient Protection and Affordable Care Act H.R. 3590)**

**") Prevention and Screening Services Cost-sharing Eliminates cost sharing requirements for requirements for all preventive services (including prevention and colorectal cancer screening) that have a screening

Prevention and Screening Services Cost-sharing Eliminates cost sharing requirements for requirements for all preventive services (including prevention and colorectal cancer screening) that have a screening

MHA Comparison of Michigan Legislative Health Insurance Reform Proposals

Overall approach to expanding health care coverage Amends the Insurance Code to create Health Care Affordability Fund within Treasury. These funds are used to: expand MIChild to 300% of poverty level Subsidize

Overall approach to expanding health care coverage Amends the Insurance Code to create Health Care Affordability Fund within Treasury. These funds are used to: expand MIChild to 300% of poverty level Subsidize

Issue Brief: The Health Benefit Exchange and the Small Employer Market

Issue Brief: The Health Benefit Exchange and the Small Employer Market Overview The federal health care reform law directs states to set up health insurance marketplaces, called Health Benefit Exchanges,

Issue Brief: The Health Benefit Exchange and the Small Employer Market Overview The federal health care reform law directs states to set up health insurance marketplaces, called Health Benefit Exchanges,

Your Health Care Benefit Program

Your Health Care Benefit Program HMO ILLINOIS A Blue Cross HMO a product of Blue Cross and Blue Shield of Illinois A message from BLUE CROSS AND BLUE SHIELD Your Group has entered into an agreement with

Your Health Care Benefit Program HMO ILLINOIS A Blue Cross HMO a product of Blue Cross and Blue Shield of Illinois A message from BLUE CROSS AND BLUE SHIELD Your Group has entered into an agreement with

MAYFLOWER MUNICIPAL HEALTH GROUP ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~ PPO REVIEW OF BENEFITS

Fiscal Year 2015 2016 MAYFLOWER MUNICIPAL HEALTH GROUP ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~ PPO REVIEW OF S ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Fiscal Year 2015 2016 MAYFLOWER MUNICIPAL HEALTH GROUP ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~ PPO REVIEW OF S ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

How To Get A New Bronwell Drug Plan

Questions and Answers New Brunswick Drug Plan December 10, 2013 1) What is the New Brunswick Drug Plan? The New Brunswick Drug Plan is a prescription drug insurance plan that provides drug coverage for

Questions and Answers New Brunswick Drug Plan December 10, 2013 1) What is the New Brunswick Drug Plan? The New Brunswick Drug Plan is a prescription drug insurance plan that provides drug coverage for

Outline of coverage. January 2015 May 2015

January 2015 May 2015 Outline of coverage The federal government has asked us to provide this outline of coverage to help you decide which plan best fits your needs and meets your budget. D98, 10/14, SM

January 2015 May 2015 Outline of coverage The federal government has asked us to provide this outline of coverage to help you decide which plan best fits your needs and meets your budget. D98, 10/14, SM

Outline of coverage. June 2014 May 2015

June 2014 May 2015 Outline of coverage The federal government has asked us to provide this outline of coverage to help you decide which plan best fits your needs and meets your budget. D98, 3/14, SM Marks

June 2014 May 2015 Outline of coverage The federal government has asked us to provide this outline of coverage to help you decide which plan best fits your needs and meets your budget. D98, 3/14, SM Marks

Outline of coverage. June 2015 - May 2016

June 2015 - May 2016 Outline of coverage The federal government has asked us to provide this outline of coverage to help you decide which plan best fits your needs and meets your budget. D98, 2/15, SM

June 2015 - May 2016 Outline of coverage The federal government has asked us to provide this outline of coverage to help you decide which plan best fits your needs and meets your budget. D98, 2/15, SM

Health Insurance Overview

Spotsylvania County Open Enrollment August 10 to 28, 2015 Plan Year: October 1, 2015 to September 30, 2016 Health Insurance Overview All Full Time employees are eligible to participate in the County Health

Spotsylvania County Open Enrollment August 10 to 28, 2015 Plan Year: October 1, 2015 to September 30, 2016 Health Insurance Overview All Full Time employees are eligible to participate in the County Health

Health Care Reform Basics

Health Care Reform Basics You may be asking yourself what health care reform is all about. Don t worry, you re not alone many people are asking the same question! This booklet will give you the basics

Health Care Reform Basics You may be asking yourself what health care reform is all about. Don t worry, you re not alone many people are asking the same question! This booklet will give you the basics

Washington State. Preston W. Cody Assistant Administrator, Basic Health Washington State Health Care Authority

Washington State Basic Health Plan Council of State Governments Preston W. Cody Assistant Administrator, Basic Health Washington State Health Care Authority Health Care Authority Cabinet-level agency with

Washington State Basic Health Plan Council of State Governments Preston W. Cody Assistant Administrator, Basic Health Washington State Health Care Authority Health Care Authority Cabinet-level agency with

Fact Sheet. AARP Public Policy Institute. Health Reform Changes Insurance Rules

Fact Sheet Health Reform Changes Insurance Rules The Affordable Care Act (ACA) will greatly increase the availability of health insurance and broadly impact the delivery of health care in America. This

Fact Sheet Health Reform Changes Insurance Rules The Affordable Care Act (ACA) will greatly increase the availability of health insurance and broadly impact the delivery of health care in America. This

[COMPANY NAME] Outline of Medicare Supplement Coverage-Cover Page: 1 of 2 Benefit Plans [insert letters of plans being offered

![[COMPANY NAME] Outline of Medicare Supplement Coverage-Cover Page: 1 of 2 Benefit Plans [insert letters of plans being offered](/thumbs/39/20138780.jpg "[COMPANY NAME] Outline of Medicare Supplement Coverage-Cover Page: 1 of 2 Benefit Plans [insert letters of plans being offered") Incorporated Document (6) [COMPANY NAME] Outline of Medicare Supplement Coverage-Cover Page: 1 of 2 Benefit Plans [insert letters of plans being offered These charts show the benefits included in each

Incorporated Document (6) [COMPANY NAME] Outline of Medicare Supplement Coverage-Cover Page: 1 of 2 Benefit Plans [insert letters of plans being offered These charts show the benefits included in each

Your Right to HealthCare Coverage When Leaving or Switching Jobs

Your Right to HealthCare Coverage When Leaving or Switching Jobs Part of PHLP s Healthcare For Workers Publication Series A Consumer s Guide to Accessing Health Care Through Employment Copyright 2007 The

Your Right to HealthCare Coverage When Leaving or Switching Jobs Part of PHLP s Healthcare For Workers Publication Series A Consumer s Guide to Accessing Health Care Through Employment Copyright 2007 The

www.thinkhr.com AFFORDABLE CARE ACT SMALL EMPLOYER HEALTH REFORM CHECKLIST

www.thinkhr.com AFFORDABLE CARE ACT SMALL EMPLOYER HEALTH REFORM CHECKLIST Employers that provide health coverage to employees are responsible for complying with many of the provisions of the Affordable

www.thinkhr.com AFFORDABLE CARE ACT SMALL EMPLOYER HEALTH REFORM CHECKLIST Employers that provide health coverage to employees are responsible for complying with many of the provisions of the Affordable

This booklet constitutes a small entity compliance guide for purposes of the Small Business Regulatory Enforcement Act of 1996.

This publication has been developed by the U.S. Department of Labor, Employee Benefits Security Administration (EBSA), and is available on the Web at www.dol.gov/ebsa. For a complete list of EBSA publications,

This publication has been developed by the U.S. Department of Labor, Employee Benefits Security Administration (EBSA), and is available on the Web at www.dol.gov/ebsa. For a complete list of EBSA publications,

A Consumer Guide to Continuation of Group Health Insurance Coverage

A Consumer Guide to Continuation of Group Health Insurance Coverage Prepared by the Iowa Insurance Division Consumer Advocate 330 Maple Street Des Moines, IA 50319 877-955-1212 http://www.insuranceca.iowa.gov

A Consumer Guide to Continuation of Group Health Insurance Coverage Prepared by the Iowa Insurance Division Consumer Advocate 330 Maple Street Des Moines, IA 50319 877-955-1212 http://www.insuranceca.iowa.gov

Outline of Coverage. Medicare Supplement

Outline of Coverage Medicare Supplement 2015 Security Health Plan of Wisconsin, Inc. Medicare Supplement Outline of Coverage Medicare Supplement policy The Wisconsin Insurance Commissioner has set standards

Outline of Coverage Medicare Supplement 2015 Security Health Plan of Wisconsin, Inc. Medicare Supplement Outline of Coverage Medicare Supplement policy The Wisconsin Insurance Commissioner has set standards

Outline of Medicare Supplement Coverage Cover Page: 1 of 2 Benefit Plan A, Plan D, Plan F, Plan K and Plan L

Outline of Medicare Supplement Coverage Cover Page: 1 of 2 Benefit Plan A, Plan D, Plan F, Plan K and Plan L Medicare Supplement insurance can be sold in only 12 standard plans plus two high-deductible

Outline of Medicare Supplement Coverage Cover Page: 1 of 2 Benefit Plan A, Plan D, Plan F, Plan K and Plan L Medicare Supplement insurance can be sold in only 12 standard plans plus two high-deductible

www.thinkhr.com 877-225-1101 Employer Health Reform Checklist

www.thinkhr.com 877-225-1101 Employer Health ThinkHR grants the reader non-exclusive, non-transferable, and limited permission to use this document. The reader may not sell or otherwise use this document

www.thinkhr.com 877-225-1101 Employer Health ThinkHR grants the reader non-exclusive, non-transferable, and limited permission to use this document. The reader may not sell or otherwise use this document

Every New Hampshire Resident Qualifies For Health Insurance. About NHHP. Eligibility

About NHHP New Hampshire Health Plan (NHHP) is a non-profit organization formed by the New Hampshire legislature. NHHP provides health coverage to New Hampshire residents who otherwise may have trouble

About NHHP New Hampshire Health Plan (NHHP) is a non-profit organization formed by the New Hampshire legislature. NHHP provides health coverage to New Hampshire residents who otherwise may have trouble

An Employer s Guide to Group Health Continuation Coverage Under COBRA

An Employer s Guide to Group Health Continuation Coverage Under COBRA The Consolidated Omnibus Reconciliation Act of 1986 U.S. Department of Labor Employee Benefits Security Administration This publication

An Employer s Guide to Group Health Continuation Coverage Under COBRA The Consolidated Omnibus Reconciliation Act of 1986 U.S. Department of Labor Employee Benefits Security Administration This publication

Presented to: 2007 Kansas Legislature. February 1, 2007

MARCIA J. NIELSEN, PhD, MPH Executive Director ANDREW ALLISON, PhD Deputy Director SCOTT BRUNNER Chief Financial Officer Report on: Massachusetts Commonwealth Health Insurance Connector Program Presented

MARCIA J. NIELSEN, PhD, MPH Executive Director ANDREW ALLISON, PhD Deputy Director SCOTT BRUNNER Chief Financial Officer Report on: Massachusetts Commonwealth Health Insurance Connector Program Presented

OUTLINE OF MEDICARE SUPPLEMENT COVERAGE COVER PAGE BENEFIT STANDARD PLANS A, B, C, D, F, J AND HIGH DEDUCTIBLE PLAN F

Anthem Blue Cross Blue Shield Connecticut Administrative Office: PO Box 1014 North Haven, CT 06473 Toll Free Telephone Number: 1-800-238-1143 OUTLINE OF MEDICARE SUPPLEMENT COVERAGE COVER PAGE BENEFIT

Anthem Blue Cross Blue Shield Connecticut Administrative Office: PO Box 1014 North Haven, CT 06473 Toll Free Telephone Number: 1-800-238-1143 OUTLINE OF MEDICARE SUPPLEMENT COVERAGE COVER PAGE BENEFIT

CONSTRUCTION INDUSTRY LABORERS HEALTH & WELFARE FUND FREQUENTLY ASKED QUESTIONS & ANSWERS Q. HOW DO I BECOME ELIGIBLE FOR HEALTH & WELFARE BENEFITS?

Q. HOW DO I BECOME ELIGIBLE FOR HEALTH & WELFARE BENEFITS? A. You can become eligible and receive benefits by working a sufficient number of hours for a Contributing Employer who makes contributions to

Q. HOW DO I BECOME ELIGIBLE FOR HEALTH & WELFARE BENEFITS? A. You can become eligible and receive benefits by working a sufficient number of hours for a Contributing Employer who makes contributions to

Health Insurance in West Virginia

Cancer Legal Resource Center 919 Albany Street Los Angeles, CA 90015 Toll Free: 866.THE.CLRC (866.843.2572) Phone: 213.736.1455 TDD: 213.736.8310 Fax: 213.736.1428 Email: CLRC@LLS.edu Web: www.disabilityrightslegalcenter.org

Cancer Legal Resource Center 919 Albany Street Los Angeles, CA 90015 Toll Free: 866.THE.CLRC (866.843.2572) Phone: 213.736.1455 TDD: 213.736.8310 Fax: 213.736.1428 Email: CLRC@LLS.edu Web: www.disabilityrightslegalcenter.org

The Instant Insurance Guide: Federal Health Care Reform

The Instant Insurance Guide: Federal Health Care Reform From Karen Weldin Stewart, CIR-ML Delaware Insurance Commissioner 1-800-282-8611 www.delawareinsurance.gov A Message From The Delaware Department

The Instant Insurance Guide: Federal Health Care Reform From Karen Weldin Stewart, CIR-ML Delaware Insurance Commissioner 1-800-282-8611 www.delawareinsurance.gov A Message From The Delaware Department

Federal Health Reform FAQs

Federal Health Reform FAQs Individuals 1. What is an exchange? An exchange, as created under the Affordable Care Act (ACA), is a place where consumers can purchase subsidized health insurance coverage.

Federal Health Reform FAQs Individuals 1. What is an exchange? An exchange, as created under the Affordable Care Act (ACA), is a place where consumers can purchase subsidized health insurance coverage.

Medicare Supplement Solutions

Medicare Supplement Solutions Medicare Supplement Solutions 1 Cameron Hill Circle Chattanooga, TN 37402 bcbst-medicare.com Thank you for your interest in BlueElite SM Medicare Supplement Solutions Dear

Medicare Supplement Solutions Medicare Supplement Solutions 1 Cameron Hill Circle Chattanooga, TN 37402 bcbst-medicare.com Thank you for your interest in BlueElite SM Medicare Supplement Solutions Dear

Outline of Medicare Supplement Coverage

Outline of Medicare Supplement Coverage Benefit Plans A, C, F, L, N for 2016 Outline of Medicare Supplement Coverage Benefit Plans A, C, F, L, N for 2016 These charts show the benefits included in each

Outline of Medicare Supplement Coverage Benefit Plans A, C, F, L, N for 2016 Outline of Medicare Supplement Coverage Benefit Plans A, C, F, L, N for 2016 These charts show the benefits included in each

1 AN ACT to amend the Comprehensive Health Insurance Plan. 3 Be it enacted by the People of the State of Illinois,

HB3004 Enrolled LRB9200745JSpc 1 AN ACT to amend the Comprehensive Health Insurance Plan 2 Act by changing Sections 2 and 15. 3 Be it enacted by the People of the State of Illinois, 4 represented in the

HB3004 Enrolled LRB9200745JSpc 1 AN ACT to amend the Comprehensive Health Insurance Plan 2 Act by changing Sections 2 and 15. 3 Be it enacted by the People of the State of Illinois, 4 represented in the

HEALTHY INDIANA PLAN FREQUENTLY ASKED QUESTIONS (FAQs)

") HEALTHY INDIANA PLAN FREQUENTLY ASKED QUESTIONS (FAQs) Eligibility Plan Benefits The Healthy Indiana Plan Requirements POWER Accounts Administration Employers Enrollment Additional Information Eligibility

HEALTHY INDIANA PLAN FREQUENTLY ASKED QUESTIONS (FAQs) Eligibility Plan Benefits The Healthy Indiana Plan Requirements POWER Accounts Administration Employers Enrollment Additional Information Eligibility

Skilled Nursing Facility Coinsurance. Skilled Nursing Facility Coinsurance Part A Deductible Part B. Part A Deductible Part B.

Aetna Life Insurance Company Outline of Medicare Supplement Coverage Benefit Plans A, B, F, G and N are Offered Benefit Chart of Medicare Supplement Plans Sold for Effective Dates on or After June 1, 2010

Aetna Life Insurance Company Outline of Medicare Supplement Coverage Benefit Plans A, B, F, G and N are Offered Benefit Chart of Medicare Supplement Plans Sold for Effective Dates on or After June 1, 2010

The Small Business Guide to Health Care Law

The Small Business Guide to Health Care Law How new changes in health care law will affect you and your employees Table of Contents Introduction 3 Part I: A General Overview of Health Care Law 4 The Affects

The Small Business Guide to Health Care Law How new changes in health care law will affect you and your employees Table of Contents Introduction 3 Part I: A General Overview of Health Care Law 4 The Affects

HEALTH INSURANCE. Types of Health Plans and How They Operate. Reimbursement and Fixed Allowance Insurance Plans (Department of Insurance Jurisdiction)

") HEALTH INSURANCE Illness for non-work related injuries can be financial devastating. Insurance can help protect against disastrous health care expenses and lost wages. If you have a job, your employer

HEALTH INSURANCE Illness for non-work related injuries can be financial devastating. Insurance can help protect against disastrous health care expenses and lost wages. If you have a job, your employer

to Health Care Reform

The Employer s Guide to Health Care Reform What you need to know now to: Consider your choices Decide what s best for you Follow the rules 2013-2014 Health care reform is the law of the land. Some don

The Employer s Guide to Health Care Reform What you need to know now to: Consider your choices Decide what s best for you Follow the rules 2013-2014 Health care reform is the law of the land. Some don

HEALTHY INDIANA PLAN FREQUENTLY ASKED QUESTIONS (FAQs)

") HEALTHY INDIANA PLAN FREQUENTLY ASKED QUESTIONS (FAQs) Eligibility Who is eligible for The Healthy Indiana Plan? The Healthy Indiana Plan (HIP) will provide health insurance for uninsured adult Hoosiers

HEALTHY INDIANA PLAN FREQUENTLY ASKED QUESTIONS (FAQs) Eligibility Who is eligible for The Healthy Indiana Plan? The Healthy Indiana Plan (HIP) will provide health insurance for uninsured adult Hoosiers

Part B. Coinsurance. Skilled Nursing Facility. 50% Skilled Nursing Facility. Coinsurance. Coinsurance 75% Part A Deductible.

AMERICAN RETIREMENT LIFE INSURANCE COMPANY P. O. BOX 26580 AUSTIN, TX 78755-0580 866-459-4272 Outline of Medicare Supplement Coverage - Benefit Plans A, F, G and N This chart shows the benefits included

AMERICAN RETIREMENT LIFE INSURANCE COMPANY P. O. BOX 26580 AUSTIN, TX 78755-0580 866-459-4272 Outline of Medicare Supplement Coverage - Benefit Plans A, F, G and N This chart shows the benefits included

Health insurance Marketplace. What to expect in 2014

Health insurance Marketplace What to expect in 2014 Overview The Affordable Care Act (ACA) includes several provisions geared to extend greater access to health insurance benefits to more people. Beginning

Health insurance Marketplace What to expect in 2014 Overview The Affordable Care Act (ACA) includes several provisions geared to extend greater access to health insurance benefits to more people. Beginning

304.17A-220 Pre-existing condition exclusion in group coverage -- Definitions for section. (1) All group health plans and insurers offering group

All group health plans and insurers offering group") 304.17A-220 Pre-existing condition exclusion in group coverage -- Definitions for section. (1) All group health plans and insurers offering group health insurance coverage in the Commonwealth shall comply

304.17A-220 Pre-existing condition exclusion in group coverage -- Definitions for section. (1) All group health plans and insurers offering group health insurance coverage in the Commonwealth shall comply

FUNDAMENTALS OF HEALTH INSURANCE: What Health Insurance Products Are Available?

http://www.naic.org/ FUNDAMENTALS OF HEALTH INSURANCE: PURPOSE The purpose of this session is to acquaint the participants with the basic principles of health insurance, areas of health insurance regulation

http://www.naic.org/ FUNDAMENTALS OF HEALTH INSURANCE: PURPOSE The purpose of this session is to acquaint the participants with the basic principles of health insurance, areas of health insurance regulation