The Determinants of Complementary Health Insurance (CHI) in France : The predominant role of the level of Income

|

|

|

- Darren Wiggins

- 8 years ago

- Views:

Transcription

1 The Determinants of Complementary Health Insurance (CHI) in France : The predominant role of the level of Income FLORENCE JUSOT, LEDA-LEGOS CLÉMENCE PERRAUDIN, CERMES3 INSERM U988 CNRS U 8211 JÉRÔME WITTWER, LEDA-LEGOS

2 Outline Context Objectives Data Analysis of CHI affordability Analysis of the determinants of CHI demand Conclusion Bibliography

3 Context Important role of CHI alongside the public scheme in France 75% of health expenditures are covered by the French public health insurance and out-of-pocket payments may be insured by CHI Several studies have shown a strong impact of CHI coverage on health expenditures Buchmueller et al. (2004): important effect on dental care and specialist care Raynaud (2005) : CHI induces a 29% increase in ambulatory care Kambia-Chopin et al. (2008): Lack of CHI constitutes financial barriers to access to health care particularly among the poorest : 32% of people without CHI report forgone care

4 Context In order to reduce difficulties to access to care of the poorest, two measures have been implemented «Couverture Maladie Universelle Complémentaire» (CMUC) : 7% of the poorest French population benefit from this free health insurance for most of out-of-pocket payments (Arnould and Vidal, 2008) The CMUC induced an increase in health care use of patients without CHI before the implementation (Grignon et al., 2008) «Aide à l acquisition d une Complémentaire Santé» (ACS) : subsidized health insurance Only 1% of the French population benefit from this voucher (Arnould and Vidal, 2008) However 7% of individuals are not covered by CHI (Arnould and Vidal, 2008)

5 Context Why 7% of the French population remains without CHI? Is CHI non affordable for these individuals? Is non CHI coverage a rational choice explained by lower risks or different preferences? Has income an influence on the choice of CHI quality? Important question for the design of public health policies: universal coverage or subsided health CHI vs private one Need for new researches on the determinants of complementary health insurance demand and particularly on the role of income

6 Aim: Analyzing the demand for CHI 1. Descriptive analysis of CHI status in France Who is covered through his employer? Who is freely covered through the CMUC? Who is covered by an individual contract of CHI? Who is not covered? Individual choice 2. Descriptive analysis of the affordability of non-group CHI 3. Determinants of the Demand for non-group CHI i. To opt for an individual contract of CHI ii. To choose the level of coverage Model with a two-stage decision process

7 Data A French Survey on National Expenditures : «Budget des Familles 2006» Five-year study conducted by INSEE All household resources and expenditures are included households; individuals Strenghts of this survey to studying health insurance demand Precise measure of health insurance expenditures Precise measure of every types of resource which allows a good approximate of CMUC eligibity Another data source than ESPS data (robustness check) Limits : Measurement at the household level and not at the individual level Poor assessment of health status: we know for each household member if the person is disabled or limited in daily activities

8 CHI expenditures and CHI status Respondents are not asked to report their CHI status However CHI status can be derived from household CHI expenditures Two types of CHI expenditures are reported: Deduction at source from the employer (measured at the individual level for every household member in employment) Direct payment of the household to health insurance companies (mutual insurance, private insurance, provident society) CHI status is assessed at the household level: A covered household is defined as an household with non-zero health insurance expenditure (direct or through wage deduction) All household eligible to CMUC are supposed to be covered through the CMUC: residents in France, resources lower than threshold varying according to composition of the household (594 per month for a single) Every member of an covered household are supposed to be covered

9 Potential determinants of CHI Household income: total amount of household resources divided by OCDE equivalent scale (wage and social support less taxes) Household composition: single / single parent family / couple without children / couple with children and other family Household risk: at least one household member disable or limited in daily activities vs none Household head characteristics: Age, sex Educational level: Primary school / Secondary 1/ Secondary 2 / university degree Employment status: employed, unemployed, student, retired, housewife, other inactives Occupation: Farmer / Craftmen / Manager / Associate professional / Office worker/ Elementary jobs / Inactive Location of the residence: rural areas / cities < inhabitants / cities / cities > / Paris

10 Distribution of CHI status 928 eligibles CMUC households 9308 not eligibles CMUC (12.6%) 873 not covered (87.4%) 6043 Individual contract only 8435 covered 2098 Mixed 294 Employer contract only 9.1% of households are eligible to CMUC 8.5% of households are non covered, 9.4% among non eligibles to CMUC, 12.6% among those who are non eligible to CMUC and non covered at least by their employer

11 [0;745] [745;848] [848;1006] [1006;1139] [1139;1267] [1267;1414] [1414;1576] [1576;1778] [1778;2064] [2064;2586] [2586;19396] Distribution of CHI plan according to available income 100% 80% 60% non-group plan 40% 20% 0% employer-sponsored plan uninsured Average disposable income per consumption unit (n=9308 households, CMUC excluded) The proportion of non covered is double in first income quintile than in the highest income quintile.

12 CHI affordability The report of non-group CHI premium allows analyzing CHI affordability Three descriptive analyses: Average non-group CHI expenditures by income decile Effort devoted to non-group CHI expenditure by income decile Affordability of CHI according to Bundorf and Pauly s definition

13 [0;827] [827;979] [979;1106] [1106;1231] [1231;1360] [1360;1526] [1526;1734] [1734;2019] [2019;2544] [2544;19396] Euros Average individual health insurance premium per capita according to available income Available income per CU Among individually insured household: The average health insurance premium per capita is 536 per year. CHI premiums are higher in the highest two deciles

14 [0;827] [827;979] [979;1106] [1106;1231] [1231;1360] [1360;1526] [1526;1734] [1734;2019] [2019;2544] [2544;19396] Average effort rate for individual health insurance plan according to available income 9% 8% 7% 6% 5% 8,5% 6,0% 5,2% Effort rate 4% 4,4% 4,2% 3,9% 3,5% 3,1% 3,0% 3% 2% 2,3% 1% 0% Available income per CU Effort rate is defined for each household as the share of total household income devoted to CHI expenditures Effort rate decreases with disposable income CHI expenditures correspond to 8.5% of total income in the first income

15 Affordability of non-group CHI plan Bundorf and Pauly (2006) define affordability based on socially acceptable levels of consumption of a particular good and the resources left for remaining consumption A particular good x is affordable if: Y p.x* > G* where Y is available income (before x expenditures) x* is the socially defined minimum quantity of the special good (here CHI) p is the unitary price of the good x G* is the socially defined minimum level of spending on all other goods Average non-group CHI premium by type of household is used as a measure of p.x* G* is defined as a poverty line equal to 60% of median disposable income (848 per month per CU) CHI is considered has unaffordable if after deduction of average CHI premium to the total available income, the household is below the poverty line

16 Affordability of non-group CHI plan Percentage of households with and without CHI among households for which CHI is affordable Percentage of households with and without CHI among households for which CHI is not affordable without CHI 8,9% with CHI 91,1% CHI affordable 83,2% CHI not affordable 16,8% without CHI 33.1% with CHI 66,9% % 15.4% of the households are initially bellow the poverty line CHI is not affordable for 16.8% for the sample : CHI expenditures would lead 1.4% of the households below the poverty line

17 Analysis of the determinants of the demand for non-group CHI How to model the probability of take-up and the amount of CHI expenditures? Two stage decision process A lot of zero expenditure (13% of sample) and a not normal distribution Two stages Heckman Sample Selection Model

18 Model (1) The consumer has a sequential behavior: 1. The individual decides to subscribe or not to a CHI contract Y 1i* > 0 : Individual decides to subscribe and y 1i =1 Otherwise y 1i =0 2. If so, he decides the amount devoted to purchase a CHI Log (m i ) = y 2i = y 2i * if y 1i * >0 0, otherwise

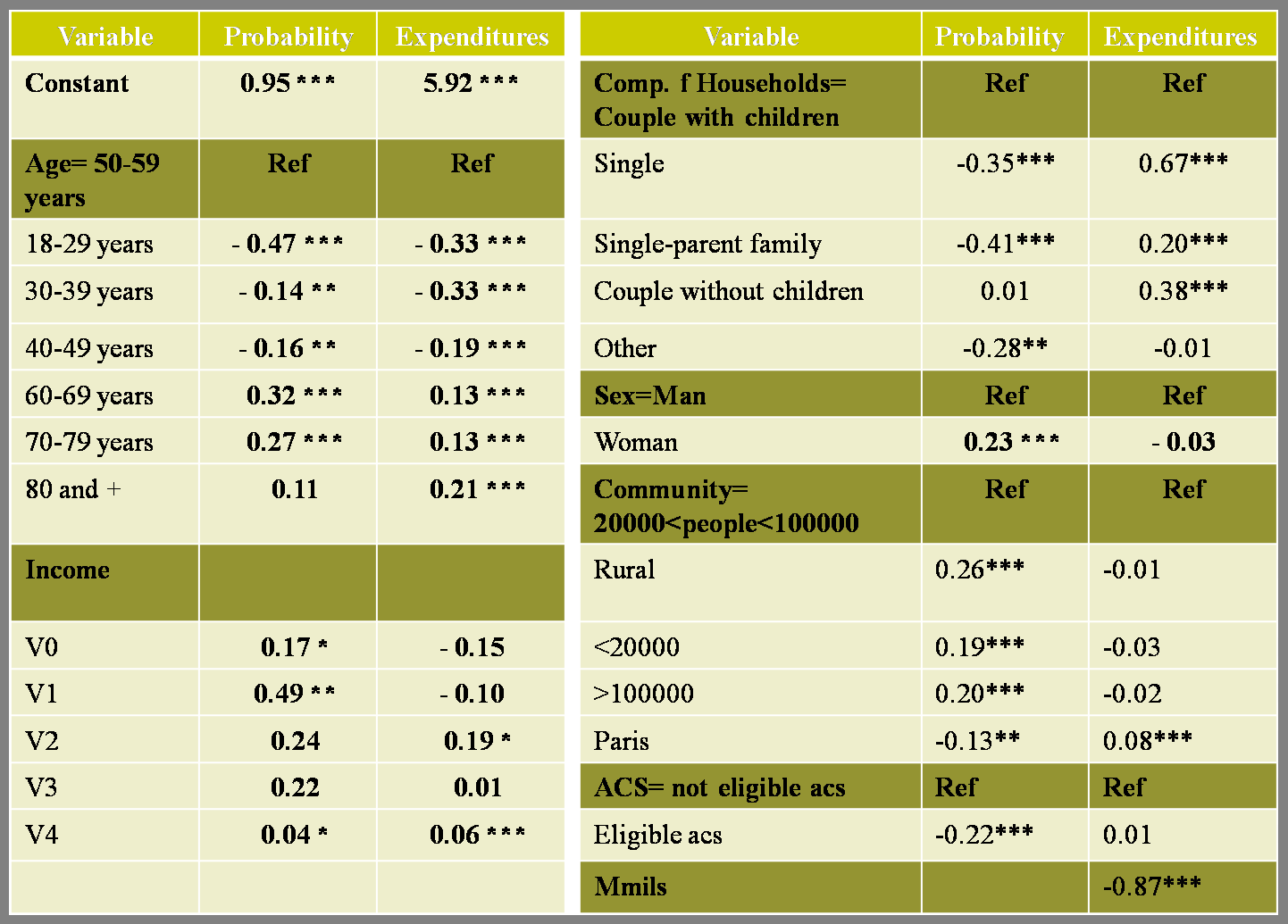

19 Model (2) Definition of the model: E (u 1i, u 2i ) = σ 12 = ρσ 1 σ 2 Y 2i = y 2i * if y 1i *> 0 and Y 1i * = x 1i β 1 + u 1i 0 otherwise Y 2i * = x 2i β 2 + u 2i We take into account the dependence between the two decisions through the fact that the residuals of the two equations are correlated. Independent variables: Age, gender, educational level, employment status, income level*, composition of the household and location of the residence, acs. *specified as a piecwise linear function

20 Results

21 Results Validation of the Model (mmils) Income is the main determinant of the decision to take-up a CHI 2 categories of explicatives variables: 1. Some explain the probability to be covered but not the expenditures involved : gender and acs 2. Some explain the two stages of the decision: Income, composition of the household, location of the residence. We found no effect of health status of the household on health insurance demand but no information on ALD

22 Estimated probability to be covered by CHI according to available income

23 Conclusion This study highlights financial difficulties in access to CHI in France The poorest are more frequently not covered by CHI Non group CHI expenditures correpond to 8.5% of available income in the first quintile CHI is not affordable for 16.8% of French household non eligible to CMUC and not covered by their employer Consistently with previous studies, the analyse of determinant of CHI demand shows predominant role of income in the access to CHI coverage in the quality of CHI Our results raise the issue of equity in the access to CHI and finally, to health care

24 Bibliography (1) ARNOUD M-L, VIDAL G. (2008), "Typologie complémentaires en 2006», Etudes et Résultats, 663. des contrats les plus souscrits auprès des ARROW.K (1974) Essays in the Theory of Risk-Bearing. Amsterdam, North Holland. AUERBACH.D, OHRI.S (2006) «Price and Demand for Non-Group Health Insurance», Inquiry 43: BOCOGNANO.A, COUFFINHAL.A, DUMESNIL.S, and GRIGNON.M (2000) «La complémentaire maladie en France : qui bénéficie de quels remboursements». Résultats de l enquête Santé Protection Sociale 1998». CREDES Rapport n BUCHMUELLER.T, COUFFINHAL.A (2004) «Private Health Insurance in France». OCDE Document de travail n 12. BUCHMUELLER.T, COUFFINHAL.A, GRIGNON M., PERRONNIN M. (2004), «Access to physician services: does supplemental insurance matter? Evidence from France», Health Economics, 13, 7 : BUNDORF.K, PAULY.M (2006) «Is Health Insurance Affordable for the Uninsured?» Journal Of Health Economics, 25(4): COLOMBO.F, TAPAY.N (2004) «Private Health Insurance in OECD Countries : The Benefits and Costs for Individuals and Health Systems» OECD Working Papers. FRANC.C, PERRONNIN.M (2007) «Aide à l acquisition d une assurance maladie complémentaire : une première évaluation de dispositif ACS» Question d économie de la santé. IRDES n 121. FRIEDMAN.M, SAVAGE.L (1948) «The Utility Analysis of Choice Involving Risk», Political Economy, 56: GRIGNON.M, KAMBIA-CHOPIN.B (2009) «Income and the Demand for Complementary health Insurance in France» Document de travail IRDES. GRIGNON.M, PERRONNIN M., LAVIS J.N (2008), Does free complementary health insurance help the poor to access health care? Evidence from France., Health Economics, 17, 2:

25 Bibliography (2) GRUBER.J, POTERBA.J (1994) «Tax Incentives and the Decision to Purchase Health Insurance : Evidence from the Self-Employed», The Quaterly Journal of Economics, 109 (3): KAMBIA-CHOPIN.B, PERRONNIN.M, DOURGNON.P, ROCHEREAU.T (2008) «Les contrats complémentaires individuels : quels poids dans le budget des ménages?», in ALLONIER.C, DOURGNON.P, ROCHEREAU.T, Enquête sur la Santé et la Protection Sociale 2006, Rapport IRDES n KAMBIA-CHOPIN B., PERRONNIN M., PIERRE A., ROCHEREAU T. (2008), "La complémentaire santé en France en 2006 : un accès qui reste inégalitaire Résultats de l Enquête Santé Protection Sociale 2006 (ESPS 2006) ", Questions d économie de la santé, 132. LEVY.H, DELEIRE.T (2003) «What do People Buy When they don t Buy Health Insurance and What does that Say about Why they are Uninsured?», National Bureau of Economic research, Working paper MARICAL.F, SAINT-POL (de).t (2007), «La complémentaire santé : une généralisation qui n efface pas les inégalités», INSEE Première, INSEE n MARQUIS.S, LONG.H (1995) «Worker Demand for Health Insurance in the Non-Group Market», Journal Of Health Economics n 14: MARQUIS.S, BUNTIN.M, ESCARCE.J, KAPUR.K, YEGIAN.J (2004) «Subsidies and the Demand for Individual Health Insurance in California», Health Service Research, 39(5): RAYNAUD.D (2005) «Les déterminants individuels des dépenses de santé : l influence de la catégorie sociale et de l assurance maladie complémentaire», Etudes et résultats n 378. SALIBA.B, VENTELOU.B (2007) «Complementary Health Insurance in France: Who pays? Why? Who will suffer from public disengagement?», Health policy n 81: THOMAS.K (1995) «Are subsidies enough to encourage the uninsured to purchase health insurance?», Inquiry n 31:

Income and the demand for complementary health insurance in France. Bidénam Kambia-Chopin, Michel Grignon (McMaster University, Hamilton, Ontario)

") Income and the demand for complementary health insurance in France Bidénam Kambia-Chopin, Michel Grignon (McMaster University, Hamilton, Ontario) Presentation Workshop IRDES, June 24-25 2010 The 2010 IRDES

Income and the demand for complementary health insurance in France Bidénam Kambia-Chopin, Michel Grignon (McMaster University, Hamilton, Ontario) Presentation Workshop IRDES, June 24-25 2010 The 2010 IRDES

Aprevious study on the mobility of

n 126 - October 2007 Complementary health cover changes at retirement time Analysis of retirees switching behaviour Carine Franc, Marc Perronnin, Aurélie Pierre On retirement, many complementary health

n 126 - October 2007 Complementary health cover changes at retirement time Analysis of retirees switching behaviour Carine Franc, Marc Perronnin, Aurélie Pierre On retirement, many complementary health

q u estions santé d économie de la results Background Issues in health economics

Health economics letter q u estions d économie de la santé results Background At the end of 2003, IRDES carried out a survey of company supplementary social protection (PSCE) in a sample of companies with

Health economics letter q u estions d économie de la santé results Background At the end of 2003, IRDES carried out a survey of company supplementary social protection (PSCE) in a sample of companies with

Private supplemental health insurance: retirees'demand

Document de travail Working paper Private supplemental health insurance: retirees'demand Carine Franc (CERMES, Inserm U750, CNRS UMR 8169, EHESS) Marc Perronnin (IRDES) Aurélie Pierre (IRDES) DT n 9 Avril

Document de travail Working paper Private supplemental health insurance: retirees'demand Carine Franc (CERMES, Inserm U750, CNRS UMR 8169, EHESS) Marc Perronnin (IRDES) Aurélie Pierre (IRDES) DT n 9 Avril

Means-tested complementary health insurance and healthcare utilisation in France: Evidence from a low-income population

Means-tested complementary health insurance and healthcare utilisation in France: Evidence from a low-income population Sophie Guthmullerᵃ1, Jérôme Wittwerᵃ ᵃ Université Paris-Dauphine, Paris, France Very

Means-tested complementary health insurance and healthcare utilisation in France: Evidence from a low-income population Sophie Guthmullerᵃ1, Jérôme Wittwerᵃ ᵃ Université Paris-Dauphine, Paris, France Very

Who Took out Additional Supplementary Health Insurance? A dynamic Analysis of Adverse-Selection

no 150 - January 2010 Who Took out Additional Supplementary Health Insurance? A dynamic Analysis of Adverse-Selection Carine Franc *, Marc Perronnin **, Aurélie Pierre **, in collaboration with Chantal

no 150 - January 2010 Who Took out Additional Supplementary Health Insurance? A dynamic Analysis of Adverse-Selection Carine Franc *, Marc Perronnin **, Aurélie Pierre **, in collaboration with Chantal

Access to Health Services for the Poor and Underserved in France

Access to Health Services for the Poor and Underserved in France Enquête sur l accès aux soins des défavorisés (1996-1997) Thérèse Lecomte, Nathalie Meunier, Andrée Mizrahi, Arié Mizrahi, Valérie Paris,

Access to Health Services for the Poor and Underserved in France Enquête sur l accès aux soins des défavorisés (1996-1997) Thérèse Lecomte, Nathalie Meunier, Andrée Mizrahi, Arié Mizrahi, Valérie Paris,

q u estions Number of insured people + 50 725 + 49 997 * Number of people targeted by the system

H e a l t h é c o n o m i c s l e t t e r q u estions d économie de la santé analysis Background According to article L. 863-5 of the Social Security Code, the Fonds CMU shall provide the Government with

H e a l t h é c o n o m i c s l e t t e r q u estions d économie de la santé analysis Background According to article L. 863-5 of the Social Security Code, the Fonds CMU shall provide the Government with

Alcohol abuse is an important health,

n 129 - January 2008 Alcohol consumption in France: one more glass of French paradox Laure Com-Ruelle, Paul Dourgnon, Florence Jusot, Pascale Lengagne In France, excessive drinking is essentially an issue

n 129 - January 2008 Alcohol consumption in France: one more glass of French paradox Laure Com-Ruelle, Paul Dourgnon, Florence Jusot, Pascale Lengagne In France, excessive drinking is essentially an issue

How Non-Group Health Coverage Varies with Income

How Non-Group Health Coverage Varies with Income February 2008 Policy makers at the state and federal levels are considering proposals to subsidize the direct purchase of health insurance as a way to reduce

How Non-Group Health Coverage Varies with Income February 2008 Policy makers at the state and federal levels are considering proposals to subsidize the direct purchase of health insurance as a way to reduce

How To Understand And Appreciate The French Health Care System

Healthcare Systems: France Based on the 2001 Civitas Report by David Green and Benedict Irvine Updated by Emily Clarke (2012) and Elliot Bidgood (January 2013) Overview Health care in France is characterised

Healthcare Systems: France Based on the 2001 Civitas Report by David Green and Benedict Irvine Updated by Emily Clarke (2012) and Elliot Bidgood (January 2013) Overview Health care in France is characterised

The Role of a Public Health Insurance Plan in a Competitive Market Lessons from International Experience. Timothy Stoltzfus Jost

The Role of a Public Health Insurance Plan in a Competitive Market Lessons from International Experience Timothy Stoltzfus Jost All developed countries have both public and private health insurance plans,

The Role of a Public Health Insurance Plan in a Competitive Market Lessons from International Experience Timothy Stoltzfus Jost All developed countries have both public and private health insurance plans,

Public and private health insurance: where to mark to boundaries? June 16, 2009 Kranjska Gora, Slovenia Valérie Paris - OECD

Public and private health insurance: where to mark to boundaries? June 16, 2009 Kranjska Gora, Slovenia Valérie Paris - OECD 1 Outline of the presentation Respective roles of public and private funding

Public and private health insurance: where to mark to boundaries? June 16, 2009 Kranjska Gora, Slovenia Valérie Paris - OECD 1 Outline of the presentation Respective roles of public and private funding

Lynn A. Blewett, Ph.D. Professor, University of Minnesota

Lynn A. Blewett, Ph.D. Professor, University of Minnesota Westlake Forum III Healthcare Reform in China and the US: Similarities, Differences and Challenges Emory University, Atlanta, GA April 10-12, 2011

Lynn A. Blewett, Ph.D. Professor, University of Minnesota Westlake Forum III Healthcare Reform in China and the US: Similarities, Differences and Challenges Emory University, Atlanta, GA April 10-12, 2011

Documents de Travail du Centre d Economie de la Sorbonne

Documents de Travail du Centre d Economie de la Sorbonne Regulating Private Health Insurance in France : New Challenges for Employer-Based Complementary Health Insurance Monique KERLEAU, Anne FRETEL, Isabelle

Documents de Travail du Centre d Economie de la Sorbonne Regulating Private Health Insurance in France : New Challenges for Employer-Based Complementary Health Insurance Monique KERLEAU, Anne FRETEL, Isabelle

President Bush s Health Care Tax Deduction Proposal: Coverage, Cost and Distributional Impacts. John Sheils and Randy Haught

www.lewin.com President Bush s Health Care Tax Deduction Proposal: Coverage, Cost and Distributional Impacts John Sheils and Randy Haught President Bush proposes to replace the existing tax exemption for

www.lewin.com President Bush s Health Care Tax Deduction Proposal: Coverage, Cost and Distributional Impacts John Sheils and Randy Haught President Bush proposes to replace the existing tax exemption for

Living standards after divorce: does alimony offset gender income inequalities?

Living standards after divorce: does alimony offset gender income inequalities? Carole Bonnet (Ined) 1, Bertrand Garbinti (CREST Insee, PSE) 2, Anne Solaz (Ined) 3 Proposal for the XXVII International

Living standards after divorce: does alimony offset gender income inequalities? Carole Bonnet (Ined) 1, Bertrand Garbinti (CREST Insee, PSE) 2, Anne Solaz (Ined) 3 Proposal for the XXVII International

The Detaxation of Overtime Hours: Lessons from the French Experiment

The Detaxation of Overtime Hours: Lessons from the French Experiment Pierre Cahuc (Polytechnique, CREST) Stephane Carcillo (OECD, Université Paris 1) December 2010 1 / 35 Introduction In October 2007:

The Detaxation of Overtime Hours: Lessons from the French Experiment Pierre Cahuc (Polytechnique, CREST) Stephane Carcillo (OECD, Université Paris 1) December 2010 1 / 35 Introduction In October 2007:

ASSESSING THE RESULTS

HEALTH REFORM IN MASSACHUSETTS EXPANDING TO HEALTH INSURANCE ASSESSING THE RESULTS March 2014 Health Reform in Massachusetts, Expanding Access to Health Insurance Coverage: Assessing the Results pulls

HEALTH REFORM IN MASSACHUSETTS EXPANDING TO HEALTH INSURANCE ASSESSING THE RESULTS March 2014 Health Reform in Massachusetts, Expanding Access to Health Insurance Coverage: Assessing the Results pulls

Regulating Private Health Insurance in France : New Challenges for Employer-Based Complementary Health Insurance

Regulating Private Health Insurance in France : New Challenges for Employer-Based Complementary Health Insurance Monique Kerleau, Anne Fretel, Isabelle Hirtzlin To cite this version: Monique Kerleau, Anne

Regulating Private Health Insurance in France : New Challenges for Employer-Based Complementary Health Insurance Monique Kerleau, Anne Fretel, Isabelle Hirtzlin To cite this version: Monique Kerleau, Anne

NBER WORKING PAPER SERIES IS HEALTH INSURANCE AFFORDABLE FOR THE UNINSURED? M. Kate Bundorf Mark V. Pauly

NBER WORKING PAPER SERIES IS HEALTH INSURANCE AFFORDABLE FOR THE UNINSURED? M. Kate Bundorf Mark V. Pauly Working Paper 9281 http://www.nber.org/papers/w9281 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts

NBER WORKING PAPER SERIES IS HEALTH INSURANCE AFFORDABLE FOR THE UNINSURED? M. Kate Bundorf Mark V. Pauly Working Paper 9281 http://www.nber.org/papers/w9281 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts

Tracking Report. Medical Bill Problems Steady for U.S. Families, 2007-2010 MEDICAL BILL PROBLEMS STABILIZE AS CONSUMERS CUT CARE

I N S U R A N C E C O V E R A G E & C O S T S Tracking Report RESULTS FROM THE HEALTH TRACKING HOUSEHOLD SURVEY NO. 28 DECEMBER 2011 Medical Bill Problems Steady for U.S. Families, 2007-2010 By Anna Sommers

I N S U R A N C E C O V E R A G E & C O S T S Tracking Report RESULTS FROM THE HEALTH TRACKING HOUSEHOLD SURVEY NO. 28 DECEMBER 2011 Medical Bill Problems Steady for U.S. Families, 2007-2010 By Anna Sommers

Public / private mix in health care financing

Public / private mix in health care financing Dominique Polton Director of strategy, research and statistics National Health Insurance, France Couverture Public / private mix in health care financing 1.

Public / private mix in health care financing Dominique Polton Director of strategy, research and statistics National Health Insurance, France Couverture Public / private mix in health care financing 1.

Physicians balance billing, supplemental insurance and access to health care

Physicians balance billing, supplemental insurance and access to health care Izabela Jelovac To cite this version: Izabela Jelovac. Physicians balance billing, supplemental insurance and access to health

Physicians balance billing, supplemental insurance and access to health care Izabela Jelovac To cite this version: Izabela Jelovac. Physicians balance billing, supplemental insurance and access to health

Quality, Affordable Health Coverage For Every Missourian. Defining Affordable Health Care for Missouri

Quality, Affordable Health Coverage For Every Missourian Defining Affordable Health Care for Missouri Fall 2008 Table of Contents Introduction... 5 Toward a Definition of Affordability..........................................5

Quality, Affordable Health Coverage For Every Missourian Defining Affordable Health Care for Missouri Fall 2008 Table of Contents Introduction... 5 Toward a Definition of Affordability..........................................5

Health Insurance Coverage for Direct Care Workers: Key Provisions for Reform

Health Insurance Coverage for Direct Care Workers: Key Provisions for Reform Introduction As an organization dedicated to our nation s 3 million direct-care workers and the millions of elders and people

Health Insurance Coverage for Direct Care Workers: Key Provisions for Reform Introduction As an organization dedicated to our nation s 3 million direct-care workers and the millions of elders and people

Non-Group Health Insurance: Many Insured Americans with High Out-of-Pocket Costs Forgo Needed Health Care

Affordable Care Act Non-Group Health Insurance: Many Insured Americans with High Out-of-Pocket Costs Forgo Needed Health Care SPECIAL REPORT / MAY 2015 WWW.FAMILIESUSA.ORG Executive Summary Since its passage

Affordable Care Act Non-Group Health Insurance: Many Insured Americans with High Out-of-Pocket Costs Forgo Needed Health Care SPECIAL REPORT / MAY 2015 WWW.FAMILIESUSA.ORG Executive Summary Since its passage

Health Care in Rural America

Health Care in Rural America Health care in rural communities has many aspects access to physicians, dentists, nurses, and mental health services; the financial circumstances of rural hospitals; federal

Health Care in Rural America Health care in rural communities has many aspects access to physicians, dentists, nurses, and mental health services; the financial circumstances of rural hospitals; federal

FINDINGS FROM THE 2014 MASSACHUSETTS HEALTH INSURANCE SURVEY

CENTER FOR HEALTH INFORMATION AND ANALYSIS FINDINGS FROM THE MASSACHUSETTS HEALTH INSURANCE SURVEY MAY 2015 Prepared by: Laura Skopec and Sharon K. Long, Urban Institute Susan Sherr, David Dutwin, and

CENTER FOR HEALTH INFORMATION AND ANALYSIS FINDINGS FROM THE MASSACHUSETTS HEALTH INSURANCE SURVEY MAY 2015 Prepared by: Laura Skopec and Sharon K. Long, Urban Institute Susan Sherr, David Dutwin, and

Health Economics Program

Health Economics Program Issue Brief 2006-05 August 2006 Medicare Supplemental Coverage and Prescription Drug Use, 2004 Medicare is a federal health insurance program that provides coverage for the elderly

Health Economics Program Issue Brief 2006-05 August 2006 Medicare Supplemental Coverage and Prescription Drug Use, 2004 Medicare is a federal health insurance program that provides coverage for the elderly

medicaid and the uninsured June 2011 Health Coverage for the Unemployed By Karyn Schwartz and Sonya Streeter

I S S U E kaiser commission on medicaid and the uninsured June 2011 P A P E R Health Coverage for the Unemployed By Karyn Schwartz and Sonya Streeter In May 2011, 13.9 million people in the U.S. were unemployed,

I S S U E kaiser commission on medicaid and the uninsured June 2011 P A P E R Health Coverage for the Unemployed By Karyn Schwartz and Sonya Streeter In May 2011, 13.9 million people in the U.S. were unemployed,

May 2012 HEALTH CARE COSTS

HEALTH CARE COSTS A Primer May 2012 KEY INFORMATION ON HEALTH CARE COSTS AND THEIR IMPACT HEALTH CARE COSTS: A Primer KEY INFORMATION ON HEALTH CARE COSTS AND THEIR IMPACT May 2012 TABLE OF CONTENTS

HEALTH CARE COSTS A Primer May 2012 KEY INFORMATION ON HEALTH CARE COSTS AND THEIR IMPACT HEALTH CARE COSTS: A Primer KEY INFORMATION ON HEALTH CARE COSTS AND THEIR IMPACT May 2012 TABLE OF CONTENTS

Health Insurance Buyers Guide. What You Need to Know to Get Started

Health Insurance Buyers Guide What You Need to Know to Get Started Time to Enroll The Affordable Care Act has changed the way that many people get health insurance. You may have more options and more ways

Health Insurance Buyers Guide What You Need to Know to Get Started Time to Enroll The Affordable Care Act has changed the way that many people get health insurance. You may have more options and more ways

Cost-of-Illness Studies: a Five-Country Methodological Comparison

no 143 - June 2009 Cost-of-Illness Studies: a Five-Country Methodological Comparison Australia, Canada, France, Germany and the Netherlands Richard Heijink *, Thomas Renaud ** Produced in different countries

no 143 - June 2009 Cost-of-Illness Studies: a Five-Country Methodological Comparison Australia, Canada, France, Germany and the Netherlands Richard Heijink *, Thomas Renaud ** Produced in different countries

Figure 1. Majority of U.S. Workers Get Health Insurance Through Employers, 2007

Figure 1. Majority of U.S. Workers Get Health Insurance Through Employers, 27 Other coverage* 9% Uninsured 14% Public programs 5% Own employer coverage 56% Other employer coverage 16% 122.2 Million Full-

Figure 1. Majority of U.S. Workers Get Health Insurance Through Employers, 27 Other coverage* 9% Uninsured 14% Public programs 5% Own employer coverage 56% Other employer coverage 16% 122.2 Million Full-

The Affordability of Health Insurance in Colorado

February 2012 CHAS Issue Brief 2011 DATA SERIES NO. 2 The Affordability of Health Insurance in Colorado Prepared for The Colorado Trust by the Colorado Health Institute Abstract The affordability of health

February 2012 CHAS Issue Brief 2011 DATA SERIES NO. 2 The Affordability of Health Insurance in Colorado Prepared for The Colorado Trust by the Colorado Health Institute Abstract The affordability of health

The Healthcare Law April 19, 2010

The Healthcare Law April 19, 2010 This healthcare bill, recently made law, is a comprehensive overhaul that increases coverage to 94% of Americans and makes sweeping changes to our current healthcare system.

The Healthcare Law April 19, 2010 This healthcare bill, recently made law, is a comprehensive overhaul that increases coverage to 94% of Americans and makes sweeping changes to our current healthcare system.

American Health Benefit Exchanges Fact Sheet A Provision of the Patient Protection and Affordable Care Act (PPACA)

") American Health Benefit Exchanges Fact Sheet A Provision of the Patient Protection and Affordable Care Act (PPACA) This Fact Sheet reflects the Final Ruling published by the Department of Health and Human

American Health Benefit Exchanges Fact Sheet A Provision of the Patient Protection and Affordable Care Act (PPACA) This Fact Sheet reflects the Final Ruling published by the Department of Health and Human

Tax Subsidies for Health Insurance An Issue Brief

Tax Subsidies for Health Insurance An Issue Brief Prepared by the Kaiser Family Foundation July 2008 Tax Subsidies for Health Insurance Most workers pay both federal and state taxes for wages paid to them

Tax Subsidies for Health Insurance An Issue Brief Prepared by the Kaiser Family Foundation July 2008 Tax Subsidies for Health Insurance Most workers pay both federal and state taxes for wages paid to them

Insuring long-term care needs. Christophe Courbage

Insuring long-term care needs Christophe Courbage Introduction Low public coverage and increasing budgetary constraints prompt a move towards developing insurance solutions to cover LTC. Market evolution

Insuring long-term care needs Christophe Courbage Introduction Low public coverage and increasing budgetary constraints prompt a move towards developing insurance solutions to cover LTC. Market evolution

Swe den Structure, delive ry, administration He althcare Financing Me chanisms and Health Expenditures Quality of Bene fits, C hoice, Access

Sweden Single payer, universal healthcare system, with 21 county councils as the primary payer (reimburser) Administration of healthcare plan is decentralized in the hands of the county councils Central

Sweden Single payer, universal healthcare system, with 21 county councils as the primary payer (reimburser) Administration of healthcare plan is decentralized in the hands of the county councils Central

Affordable Care Act (ACA) Shifts Wealth From Millennials to Baby Boomers

Shifts Wealth From Millennials to Baby Boomers") Affordable Care Act (ACA) Shifts Wealth From Millennials to Baby Boomers April 6, 2015 Brittany Clifton, Gail Werner-Robertson Scholar Creighton Institute for Economic Inquiry Affordable Care Act (ACA)

Affordable Care Act (ACA) Shifts Wealth From Millennials to Baby Boomers April 6, 2015 Brittany Clifton, Gail Werner-Robertson Scholar Creighton Institute for Economic Inquiry Affordable Care Act (ACA)

Moral Hazard in the French Workers Compensation System

The Journal of Risk and Insurance, 1998, Vol. 65, No. 1, 125-133. Moral Hazard in the French Workers Compensation System Thomas Aiuppa James Trieschmann ABSTRACT The study investigates the level of moral

The Journal of Risk and Insurance, 1998, Vol. 65, No. 1, 125-133. Moral Hazard in the French Workers Compensation System Thomas Aiuppa James Trieschmann ABSTRACT The study investigates the level of moral

Second Hour Exam Public Finance - 180.365 Fall, 2007. Answers

Second Hour Exam Public Finance - 180.365 Fall, 2007 Answers HourExam2-Fall07, November 20, 2007 1 Multiple Choice (4 pts each) Correct answer indicated by 1. The portion of income received by the middle

Second Hour Exam Public Finance - 180.365 Fall, 2007 Answers HourExam2-Fall07, November 20, 2007 1 Multiple Choice (4 pts each) Correct answer indicated by 1. The portion of income received by the middle

Voluntary Private Health Care Insurance Among the Over Fifties in Europe: A Comparative Analysis of SHARE Data *

Voluntary Private Health Care Insurance Among the Over Fifties in Europe: A Comparative Analysis of SHARE Data * Omar Paccagnella, Vincenzo Rebba, Guglielmo Weber Department of Economics, University of

Voluntary Private Health Care Insurance Among the Over Fifties in Europe: A Comparative Analysis of SHARE Data * Omar Paccagnella, Vincenzo Rebba, Guglielmo Weber Department of Economics, University of

Irish Findings on Financial Protection

Irish Findings on Financial Protection Bridget Johnston Mapping the Pathways to Universal Healthcare https://medicine.tcd.ie/health-systems-research/ Centre for Health Policy and Management, Trinity College

Irish Findings on Financial Protection Bridget Johnston Mapping the Pathways to Universal Healthcare https://medicine.tcd.ie/health-systems-research/ Centre for Health Policy and Management, Trinity College

Tax subsidies for private health insurance: who currently benefits and what are the implications for new policies?

Also see the report on this topic available at www.taxpolicycenter.org This policy primer is available at www.policysynthesis.org THE SYNTHESIS PROJECT NEW INSIGHTS FROM RESEARCH RESULTS Tax subsidies

Also see the report on this topic available at www.taxpolicycenter.org This policy primer is available at www.policysynthesis.org THE SYNTHESIS PROJECT NEW INSIGHTS FROM RESEARCH RESULTS Tax subsidies

Income Distribution Database (http://oe.cd/idd)

") Income Distribution Database (http://oe.cd/idd) TERMS OF REFERENCE OECD PROJECT ON THE DISTRIBUTION OF HOUSEHOLD INCOMES 2014/15 COLLECTION October 2014 The OECD income distribution questionnaire aims

Income Distribution Database (http://oe.cd/idd) TERMS OF REFERENCE OECD PROJECT ON THE DISTRIBUTION OF HOUSEHOLD INCOMES 2014/15 COLLECTION October 2014 The OECD income distribution questionnaire aims

ICI RESEARCH PERSPECTIVE

ICI RESEARCH PERSPECTIVE 0 H STREET, NW, SUITE 00 WASHINGTON, DC 000 0-6-800 WWW.ICI.ORG OCTOBER 0 VOL. 0, NO. 7 WHAT S INSIDE Introduction Decline in the Share of Workers Covered by Private-Sector DB

ICI RESEARCH PERSPECTIVE 0 H STREET, NW, SUITE 00 WASHINGTON, DC 000 0-6-800 WWW.ICI.ORG OCTOBER 0 VOL. 0, NO. 7 WHAT S INSIDE Introduction Decline in the Share of Workers Covered by Private-Sector DB

Health Care Reform: Major Provisions and Bargaining Strategies for Retirees

Health Care Reform: Major Provisions and Bargaining Strategies for Retirees MEDICARE Summary of Benefit: Medicare is the federal government s healthcare program for the elderly and certain disabled individuals.

Health Care Reform: Major Provisions and Bargaining Strategies for Retirees MEDICARE Summary of Benefit: Medicare is the federal government s healthcare program for the elderly and certain disabled individuals.

Voluntary Private Health Care Insurance Among the Over Fifties: A Comparative Analysis of SHARE Data

1 st SHARE ELSA HRS User Conference 26 28 September 2005, Lund, Sweden Voluntary Private Health Care Insurance Among the Over Fifties: A Comparative Analysis of SHARE Data Omar Paccagnella, Vincenzo Rebba,

1 st SHARE ELSA HRS User Conference 26 28 September 2005, Lund, Sweden Voluntary Private Health Care Insurance Among the Over Fifties: A Comparative Analysis of SHARE Data Omar Paccagnella, Vincenzo Rebba,

Coverage Effects of Limiting the Tax Exclusion for Employment-Based Health Insurance

Congressional Budget Office June 23, 2014 Coverage Effects of Limiting the Tax Exclusion for Employment-Based Health Insurance Presentation at the Fifth Biennial Conference of the American Society of Health

Congressional Budget Office June 23, 2014 Coverage Effects of Limiting the Tax Exclusion for Employment-Based Health Insurance Presentation at the Fifth Biennial Conference of the American Society of Health

The Effect of the Affordable Care Act on the Labor Supply, Savings, and Social Security of Older Americans

The Effect of the Affordable Care Act on the Labor Supply, Savings, and Social Security of Older Americans Eric French University College London Hans-Martin von Gaudecker University of Bonn John Bailey

The Effect of the Affordable Care Act on the Labor Supply, Savings, and Social Security of Older Americans Eric French University College London Hans-Martin von Gaudecker University of Bonn John Bailey

Analysis of the effects of family benefits and financing of early childhood education and care on poverty and work incentives

Analysis of the effects of family benefits and financing of early childhood education and care on poverty and work incentives A summary of the study s results Full version (in Estonian) accessible at:

Analysis of the effects of family benefits and financing of early childhood education and care on poverty and work incentives A summary of the study s results Full version (in Estonian) accessible at:

Eligibility for Medi-Cal and the Health Insurance Exchange in California under the Affordable Care Act

UNIVERSITY OF CALIFORNIA, BERKELEY CENTER FOR LABOR RESEARCH AND EDUCATION ISSUE BRIEF Eligibility for Medi-Cal and the Health Insurance Exchange in California under the Affordable Care Act by Ken Jacobs,

UNIVERSITY OF CALIFORNIA, BERKELEY CENTER FOR LABOR RESEARCH AND EDUCATION ISSUE BRIEF Eligibility for Medi-Cal and the Health Insurance Exchange in California under the Affordable Care Act by Ken Jacobs,

PENSIONS AT A GLANCE 2009: RETIREMENT INCOME SYSTEMS IN OECD COUNTRIES UNITED STATES

PENSIONS AT A GLANCE 29: RETIREMENT INCOME SYSTEMS IN OECD COUNTRIES Online Country Profiles, including personal income tax and social security contributions UNITED STATES United States: pension system

PENSIONS AT A GLANCE 29: RETIREMENT INCOME SYSTEMS IN OECD COUNTRIES Online Country Profiles, including personal income tax and social security contributions UNITED STATES United States: pension system

NBER WORKING PAPER SERIES ACCESS TO PHYSICIAN SERVICES: DOES SUPPLEMENTAL INSURANCE MATTER? EVIDENCE FROM FRANCE

NBER WORKING PAPER SERIES ACCESS TO PHYSICIAN SERVICES: DOES SUPPLEMENTAL INSURANCE MATTER? EVIDENCE FROM FRANCE Thomas C. Buchmueller Agnès Couffinhal Michel Grignon Marc Perronnin Working Paper 9238

NBER WORKING PAPER SERIES ACCESS TO PHYSICIAN SERVICES: DOES SUPPLEMENTAL INSURANCE MATTER? EVIDENCE FROM FRANCE Thomas C. Buchmueller Agnès Couffinhal Michel Grignon Marc Perronnin Working Paper 9238

Development of Health Insurance Scheme for the Rural Population in China

Development of Health Insurance Scheme for the Rural Population in China Meng Qingyue China Center for Health Development Studies Peking University DPO Conference, NayPyiTaw, Feb 15, 2012 China has experienced

Development of Health Insurance Scheme for the Rural Population in China Meng Qingyue China Center for Health Development Studies Peking University DPO Conference, NayPyiTaw, Feb 15, 2012 China has experienced

COST IMPACT ANALYSIS FOR THE HEALTH CARE FOR AMERICA PROPOSAL

COST IMPACT ANALYSIS FOR THE HEALTH CARE FOR AMERICA PROPOSAL Final Report Prepared for: The Economic Policy Institute Submitted by: The Lewin Group, Inc. Embargoed Until Midnight February 15, 2008 Table

COST IMPACT ANALYSIS FOR THE HEALTH CARE FOR AMERICA PROPOSAL Final Report Prepared for: The Economic Policy Institute Submitted by: The Lewin Group, Inc. Embargoed Until Midnight February 15, 2008 Table

2015 OEP: Insight into consumer behavior

2015 OEP: Insight into consumer behavior Center for U.S. Health System Reform March 11, 2015 OVERVIEW As the Affordable Care Act s (ACA s) second individual market open enrollment period (OEP) came to

2015 OEP: Insight into consumer behavior Center for U.S. Health System Reform March 11, 2015 OVERVIEW As the Affordable Care Act s (ACA s) second individual market open enrollment period (OEP) came to

Medicare Buy-In Options for Uninsured Adults

MEDICARE BUY-IN OPTIONS: ESTIMATING COVERAGE AND COSTS John Sheils and Ying-Jun Chen The Lewin Group, Inc. February 2001 Support for this research was provided by The Commonwealth Fund. The views presented

MEDICARE BUY-IN OPTIONS: ESTIMATING COVERAGE AND COSTS John Sheils and Ying-Jun Chen The Lewin Group, Inc. February 2001 Support for this research was provided by The Commonwealth Fund. The views presented

Prescribed Side Effects of the Patient Protection and Affordable Care Act (PPACA): Healthcare Reform Update

: Healthcare Reform Update") August 14, 2013 Presented by: Jay Hutto, CPA Prescribed Side Effects of the Patient Protection and Affordable Care Act (PPACA): Healthcare Reform Update Click HERE to listen to webinar. August 14, 2013

August 14, 2013 Presented by: Jay Hutto, CPA Prescribed Side Effects of the Patient Protection and Affordable Care Act (PPACA): Healthcare Reform Update Click HERE to listen to webinar. August 14, 2013

WE RE HERE TO HELP YOU TRANSITION TO THE NEW HEALTH BENEFIT EXCHANGE

HEALTH CARE REFORM: INFORMATION VERMONTERS NEED TO KNOW The Federal Affordable Care Act means new health insurance products, new rules and new systems for purchasing plans beginning in 2013. Blue Cross

HEALTH CARE REFORM: INFORMATION VERMONTERS NEED TO KNOW The Federal Affordable Care Act means new health insurance products, new rules and new systems for purchasing plans beginning in 2013. Blue Cross

THE FUTURE OF EMPLOYER BASED HEALTH INSURANCE FOLLOWING HEALTH REFORM

THE FUTURE OF EMPLOYER BASED HEALTH INSURANCE FOLLOWING HEALTH REFORM National Congress on Health Insurance Reform Washington, D.C., January 20, 2011 Elise Gould, PhD Health Policy Research Director Economic

THE FUTURE OF EMPLOYER BASED HEALTH INSURANCE FOLLOWING HEALTH REFORM National Congress on Health Insurance Reform Washington, D.C., January 20, 2011 Elise Gould, PhD Health Policy Research Director Economic

The President s Health Savings Account Proposals

The President s Health Savings Account Proposals Roy Ramthun, National Economic Council Kate Baicker, Council of Economic Advisers March 10, 2006 Broader Policy Goals Create a system where spending decisions

The President s Health Savings Account Proposals Roy Ramthun, National Economic Council Kate Baicker, Council of Economic Advisers March 10, 2006 Broader Policy Goals Create a system where spending decisions

U.S. TREASURY DEPARTMENT OFFICE OF ECONOMIC POLICY COBRA INSURANCE COVERAGE SINCE THE RECOVERY ACT: RESULTS FROM NEW SURVEY DATA

U.S. TREASURY DEPARTMENT OFFICE OF ECONOMIC POLICY COBRA INSURANCE COVERAGE SINCE THE RECOVERY ACT: RESULTS FROM NEW SURVEY DATA COBRA INSURANCE COVERAGE SINCE THE RECOVERY ACT: RESULTS FROM NEW SURVEY

U.S. TREASURY DEPARTMENT OFFICE OF ECONOMIC POLICY COBRA INSURANCE COVERAGE SINCE THE RECOVERY ACT: RESULTS FROM NEW SURVEY DATA COBRA INSURANCE COVERAGE SINCE THE RECOVERY ACT: RESULTS FROM NEW SURVEY

Free Ride: The Senate Health Bill s Approach to Employer Responsibility Means Some Large Employers Get to Take It Easy

Issue Brief December 2009 Center for Economic and Policy Research 1611 Connecticut Ave, NW Suite 400 Washington, DC 20009 tel: 202-293-5380 fax: 202-588-1356 www.cepr.net Free Ride: The Senate Health Bill

Issue Brief December 2009 Center for Economic and Policy Research 1611 Connecticut Ave, NW Suite 400 Washington, DC 20009 tel: 202-293-5380 fax: 202-588-1356 www.cepr.net Free Ride: The Senate Health Bill

Courrier des statistiques, English series no.4, 1998 7

H e a l t h c a r e As in other countries, the healthcare sector in France is undergoing profound change. The pressure to rationalize the system is coming from financial constraints and the steady growth

H e a l t h c a r e As in other countries, the healthcare sector in France is undergoing profound change. The pressure to rationalize the system is coming from financial constraints and the steady growth

Health insurance, efficiency and equity: French debates

Health insurance, efficiency and equity: French debates Brigitte Dormont (University of Paris Dauphine and Cepremap) The French health care system is based on social insurance. It shares many features

Health insurance, efficiency and equity: French debates Brigitte Dormont (University of Paris Dauphine and Cepremap) The French health care system is based on social insurance. It shares many features

Swami, B.N., Okurut, F.N., Yinusa, D.O., Bonu, V., Pelaelo, P.S. and Sethibe, A.

Swami, B.N., Okurut, F.N., Yinusa, D.O., Bonu, V., Pelaelo, P.S. and Sethibe, A. Motivation of the Study Health is an important resource for a nation to pursue national development goals Health raises

Swami, B.N., Okurut, F.N., Yinusa, D.O., Bonu, V., Pelaelo, P.S. and Sethibe, A. Motivation of the Study Health is an important resource for a nation to pursue national development goals Health raises

CHAPTER 04 maintaining income adequacy in retirement

CHAPTER 04 Maintaining Income Adequacy in Retirement 36 Introduction 4.1 Pensioners living standards are supported by the pensions system, through Social Welfare pensions and tax-supported supplementary

CHAPTER 04 Maintaining Income Adequacy in Retirement 36 Introduction 4.1 Pensioners living standards are supported by the pensions system, through Social Welfare pensions and tax-supported supplementary

OECD PROJECT ON FINANCIAL INCENTIVES AND RETIREMENT SAVINGS Project Outline 2014-2016

OECD PROJECT ON FINANCIAL INCENTIVES AND RETIREMENT SAVINGS Project Outline 2014-2016 The OECD argues in favour of complementary private pension savings to boost overall saving for retirement. Financial

OECD PROJECT ON FINANCIAL INCENTIVES AND RETIREMENT SAVINGS Project Outline 2014-2016 The OECD argues in favour of complementary private pension savings to boost overall saving for retirement. Financial

FISCAL INCENTIVES AND RETIREMENT SAVINGS Project Outline 2014-2015

FISCAL INCENTIVES AND RETIREMENT SAVINGS Project Outline 2014-2015 The OECD argues in favour of complementary private pension savings to boost overall saving for retirement. Financial incentives may be

FISCAL INCENTIVES AND RETIREMENT SAVINGS Project Outline 2014-2015 The OECD argues in favour of complementary private pension savings to boost overall saving for retirement. Financial incentives may be

HEALTH INSURANCE COVERAGE AND ADVERSE SELECTION

HEALTH INSURANCE COVERAGE AND ADVERSE SELECTION Philippe Lambert, Sergio Perelman, Pierre Pestieau, Jérôme Schoenmaeckers 229-2010 20 Health Insurance Coverage and Adverse Selection Philippe Lambert, Sergio

HEALTH INSURANCE COVERAGE AND ADVERSE SELECTION Philippe Lambert, Sergio Perelman, Pierre Pestieau, Jérôme Schoenmaeckers 229-2010 20 Health Insurance Coverage and Adverse Selection Philippe Lambert, Sergio

Complex Case Scenarios Preventing Gaps in Health Care Coverage Mini-Series: Transitioning from Employer-Sponsored Coverage to Other Health Coverage

Complex Case Scenarios Preventing Gaps in Health Care Coverage Mini-Series: Transitioning from Employer-Sponsored Coverage to Other Health Coverage Center for Consumer Information and Insurance Oversight

Complex Case Scenarios Preventing Gaps in Health Care Coverage Mini-Series: Transitioning from Employer-Sponsored Coverage to Other Health Coverage Center for Consumer Information and Insurance Oversight

Office of the Actuary

DEPARTMENT OF HEALTH & HUMAN SERVICES Centers for Medicare & Medicaid Services 7500 Security Boulevard, Mail Stop N3-01-21 Baltimore, Maryland 21244-1850 Office of the Actuary DATE: March 25, 2008 FROM:

DEPARTMENT OF HEALTH & HUMAN SERVICES Centers for Medicare & Medicaid Services 7500 Security Boulevard, Mail Stop N3-01-21 Baltimore, Maryland 21244-1850 Office of the Actuary DATE: March 25, 2008 FROM:

The Impact of the Medicare Drug Benefit on Health Care Spending by Older Households

The Impact of the Medicare Drug Benefit on Health Care Spending by Older Households Dean Baker and Ben Zipperer December 2008 Center for Economic and Policy Research 1611 Connecticut Avenue, NW, Suite

The Impact of the Medicare Drug Benefit on Health Care Spending by Older Households Dean Baker and Ben Zipperer December 2008 Center for Economic and Policy Research 1611 Connecticut Avenue, NW, Suite

How To Get A Small Business Health Insurance Plan For Free

Statement of Linda J. Blumberg, Ph.D. Senior Fellow The Urban Institute Committee on Energy and Commerce Subcommittee on Oversight and Investigations United States House of Representatives Hearing: The

Statement of Linda J. Blumberg, Ph.D. Senior Fellow The Urban Institute Committee on Energy and Commerce Subcommittee on Oversight and Investigations United States House of Representatives Hearing: The

HEALTH CARE REFORM DOCUMENT FROM THE WEBSITE OF BLUE CROSS BLUE SHIELD OF NORTH DAKOTA

HEALTH CARE REFORM DOCUMENT FROM THE WEBSITE OF BLUE CROSS BLUE SHIELD OF NORTH DAKOTA Frequently Asked Questions I ve heard the federal government launched a new website called Healthcare.gov. How can

HEALTH CARE REFORM DOCUMENT FROM THE WEBSITE OF BLUE CROSS BLUE SHIELD OF NORTH DAKOTA Frequently Asked Questions I ve heard the federal government launched a new website called Healthcare.gov. How can

Section 2: INDIVIDUALS WHO CURRENTLY HAVE

Section 2: INDIVIDUALS WHO CURRENTLY HAVE COVERAGE OR AN OFFER OF COVERAGE FROM THEIR EMPLOYER Section 2 covers enrollment issues for individuals who have coverage or an offer of coverage whether through

Section 2: INDIVIDUALS WHO CURRENTLY HAVE COVERAGE OR AN OFFER OF COVERAGE FROM THEIR EMPLOYER Section 2 covers enrollment issues for individuals who have coverage or an offer of coverage whether through

PPACA Subsidy Model Description

PPACA Subsidy Model Description John A. Graves Vanderbilt University November 2011 This draft paper is intended for review and comments only. It is not intended for citation, quotation, or other use in

PPACA Subsidy Model Description John A. Graves Vanderbilt University November 2011 This draft paper is intended for review and comments only. It is not intended for citation, quotation, or other use in

Health, Private and Public Insurance, G 15, 16. U.S. Health care > 16% of GDP (7% in 1970), 8% in U.K. and Sweden, 11% in Switzerland.

, 8% in U.K. and Sweden, 11% in Switzerland.") Health, Private and Public Insurance, G 15, 16 U.S. Health care > 16% of GDP (7% in 1970), 8% in U.K. and Sweden, 11% in Switzerland. 60% have private ins. as primary ins. Insured pay about 20% out of

Health, Private and Public Insurance, G 15, 16 U.S. Health care > 16% of GDP (7% in 1970), 8% in U.K. and Sweden, 11% in Switzerland. 60% have private ins. as primary ins. Insured pay about 20% out of

What Do People Buy When They Don t Buy Health Insurance? Harris Graduate School of Public Policy Studies University of Chicago.

What Do People Buy When They Don t Buy Health Insurance? Helen Levy hlevy@uchicago.edu Thomas DeLeire t-deleire@uchicago.edu Harris Graduate School of Public Policy Studies University of Chicago June 26,

What Do People Buy When They Don t Buy Health Insurance? Helen Levy hlevy@uchicago.edu Thomas DeLeire t-deleire@uchicago.edu Harris Graduate School of Public Policy Studies University of Chicago June 26,

Redistributional impact of the National Health Insurance System

Redistributional impact of the National Health Insurance System in France: A microsimulation approach Valrie Albouy (INSEE) Laurent Davezies (INSEE-CREST-IRDES) Thierry Debrand (IRDES) Brussels, 4-5 March

Redistributional impact of the National Health Insurance System in France: A microsimulation approach Valrie Albouy (INSEE) Laurent Davezies (INSEE-CREST-IRDES) Thierry Debrand (IRDES) Brussels, 4-5 March

Timeline of New Health Care Law and Its Impact on American Businesses

Timeline of New Health Care Law and Its Impact on American Businesses Summaries of the Patient Protection and Affordable Health Care Act (Public Law 111-148) Health Care and Education Reconciliation Act

Timeline of New Health Care Law and Its Impact on American Businesses Summaries of the Patient Protection and Affordable Health Care Act (Public Law 111-148) Health Care and Education Reconciliation Act

FACULTY RETIREMENT PLANS: THE ROLE OF RETIREE HEALTH INSURANCE

TRENDS AND ISSUES SEPTEMBER 2015 FACULTY RETIREMENT PLANS: THE ROLE OF RETIREE HEALTH INSURANCE Robert L. Clark Zelnak Professor Poole College of Management North Carolina State University Retiree health

TRENDS AND ISSUES SEPTEMBER 2015 FACULTY RETIREMENT PLANS: THE ROLE OF RETIREE HEALTH INSURANCE Robert L. Clark Zelnak Professor Poole College of Management North Carolina State University Retiree health

Can the President s Health Care Tax Proposal Serve as an Effective Substitute for SCHIP Expansion?

Can the President s Health Care Tax Proposal Serve as an Effective Substitute for SCHIP Expansion? Timely Analysis of Immediate Health Policy Issues October 2007 By: Linda J. Blumberg Summary The Bush

Can the President s Health Care Tax Proposal Serve as an Effective Substitute for SCHIP Expansion? Timely Analysis of Immediate Health Policy Issues October 2007 By: Linda J. Blumberg Summary The Bush

kaiser medicaid uninsured commission on Health Insurance Coverage of the Near Elderly Prepared by John Holahan, Ph.D. The Urban Institute and the

kaiser commission on medicaid and the uninsured Health Insurance Coverage of the ear Elderly Prepared by John Holahan, Ph.D. The Urban Institute July 2004 kaiser commission medicaid uninsured and the The

kaiser commission on medicaid and the uninsured Health Insurance Coverage of the ear Elderly Prepared by John Holahan, Ph.D. The Urban Institute July 2004 kaiser commission medicaid uninsured and the The

Insurance Markets Ready or Not: Consumers Face New Health Insurance Choices. Employer-based. Insurance Premium. Contribution.

Insurance Markets Ready or Not: Consumers Face New Health Insurance Choices Introduction Not long ago, most working Californians, at least those working for large or midsize companies, could expect a standard

Insurance Markets Ready or Not: Consumers Face New Health Insurance Choices Introduction Not long ago, most working Californians, at least those working for large or midsize companies, could expect a standard

Small Employers and Health Insurance. Results of a survey of small employers in six rural California counties

Small Employers and Health Insurance Results of a survey of small employers in six rural California counties The Small Business Health Insurance Survey Project Why study small employers? Small businesses

Small Employers and Health Insurance Results of a survey of small employers in six rural California counties The Small Business Health Insurance Survey Project Why study small employers? Small businesses

Turning Logic and Evidence on it Head: Australia's Subsidy to Private Insurance

Turning Logic and Evidence on it Head: Australia's Subsidy to Private Insurance Jeremiah Hurley Centre for Health Economics and Policy Analysis Department of Economics McMaster University Thank Jamie Daw

Turning Logic and Evidence on it Head: Australia's Subsidy to Private Insurance Jeremiah Hurley Centre for Health Economics and Policy Analysis Department of Economics McMaster University Thank Jamie Daw

UHI Explained. Frequently asked questions on the proposed new model of Universal Health Insurance

UHI Explained Frequently asked questions on the proposed new model of Universal Health Insurance Overview of Universal Health Insurance What kind of health system does Ireland currently have? At the moment

UHI Explained Frequently asked questions on the proposed new model of Universal Health Insurance Overview of Universal Health Insurance What kind of health system does Ireland currently have? At the moment

Asymmetric Information in the Portuguese Health Insurance Market

Asymmetric Information in the Portuguese Health Insurance Market Teresa Bago d Uva Instituto Nacional de Estatística J.M.C. Santos Silva ISEG/Universidade Técnica de Lisboa 1 1 Introduction ² The negative

Asymmetric Information in the Portuguese Health Insurance Market Teresa Bago d Uva Instituto Nacional de Estatística J.M.C. Santos Silva ISEG/Universidade Técnica de Lisboa 1 1 Introduction ² The negative

the Affordable Care Act: What Colorado Businesses Need to Know

22 About questions the Affordable Care Act: What Colorado Businesses Need to Know 1 What is the Affordable Care Act? Who is impacted (small, large businesses and self-insured)? The Patient Protection and

22 About questions the Affordable Care Act: What Colorado Businesses Need to Know 1 What is the Affordable Care Act? Who is impacted (small, large businesses and self-insured)? The Patient Protection and

Congressional Budget Office

Congressional Budget Office June 9, 2014 Microsimulation of Demand for Health Insurance: A Method Based on Elasticities Methods Workshop Presentation AcademyHealth Annual Research Meetings San Diego, California

Congressional Budget Office June 9, 2014 Microsimulation of Demand for Health Insurance: A Method Based on Elasticities Methods Workshop Presentation AcademyHealth Annual Research Meetings San Diego, California

Parker, Smith & Feek - ACA Update: 2014 November 2013

Affordable Care Act (ACA) Background Core of law is an attempt to reduce # of uninsured Multiple approaches to expanding insurance coverage Requires most in US to have health insurance Creates state-based

Affordable Care Act (ACA) Background Core of law is an attempt to reduce # of uninsured Multiple approaches to expanding insurance coverage Requires most in US to have health insurance Creates state-based

Household level access. Extra household access. Sustainability of services. Current global goals end in 2015

Current global goals end in 2015 Accès à l Eau potable et à l Assainissement - Vers un objectif mondial post-2015 MDGs Post-MDGs??? Water Target: Halving the proportion of population without safe drinking

Current global goals end in 2015 Accès à l Eau potable et à l Assainissement - Vers un objectif mondial post-2015 MDGs Post-MDGs??? Water Target: Halving the proportion of population without safe drinking

Health Insurance Coverage, Poverty, and Income of Veterans: 2000 to 2009

Health Insurance Coverage, Poverty, and Income of Veterans: 2 to 29 February 211 NCVAS National Center for Veterans Analysis and Statistics Data Source and Methods Data for this analysis come from years

Health Insurance Coverage, Poverty, and Income of Veterans: 2 to 29 February 211 NCVAS National Center for Veterans Analysis and Statistics Data Source and Methods Data for this analysis come from years

Health Insurance as Social Protection in Latin America

Health Insurance as Social Protection in Latin America Marcos Vera-Hernandez (m.vera@ucl.ac.uk) University College London & Institute for Fiscal Studies 1 st Kenya Social Protection Conference Week Enhancing

Health Insurance as Social Protection in Latin America Marcos Vera-Hernandez (m.vera@ucl.ac.uk) University College London & Institute for Fiscal Studies 1 st Kenya Social Protection Conference Week Enhancing

Health. for Life. Nearly one in five people under age. Health Coverage for All Paid for by All. Better Health Care

Health for Life Better Health Better Health Care National Framework for Change Health Coverage for All Paid for by All Focus on We llness Health Coverage for All Paid for by All Nearly one in five people

Health for Life Better Health Better Health Care National Framework for Change Health Coverage for All Paid for by All Focus on We llness Health Coverage for All Paid for by All Nearly one in five people