TRS PERSONAL FINANCE HOMEWORK: Amounts in Actual column are considered PRE-WORK and must be complete BEFORE the TRS seminar

|

|

|

- Julie Grant

- 8 years ago

- Views:

Transcription

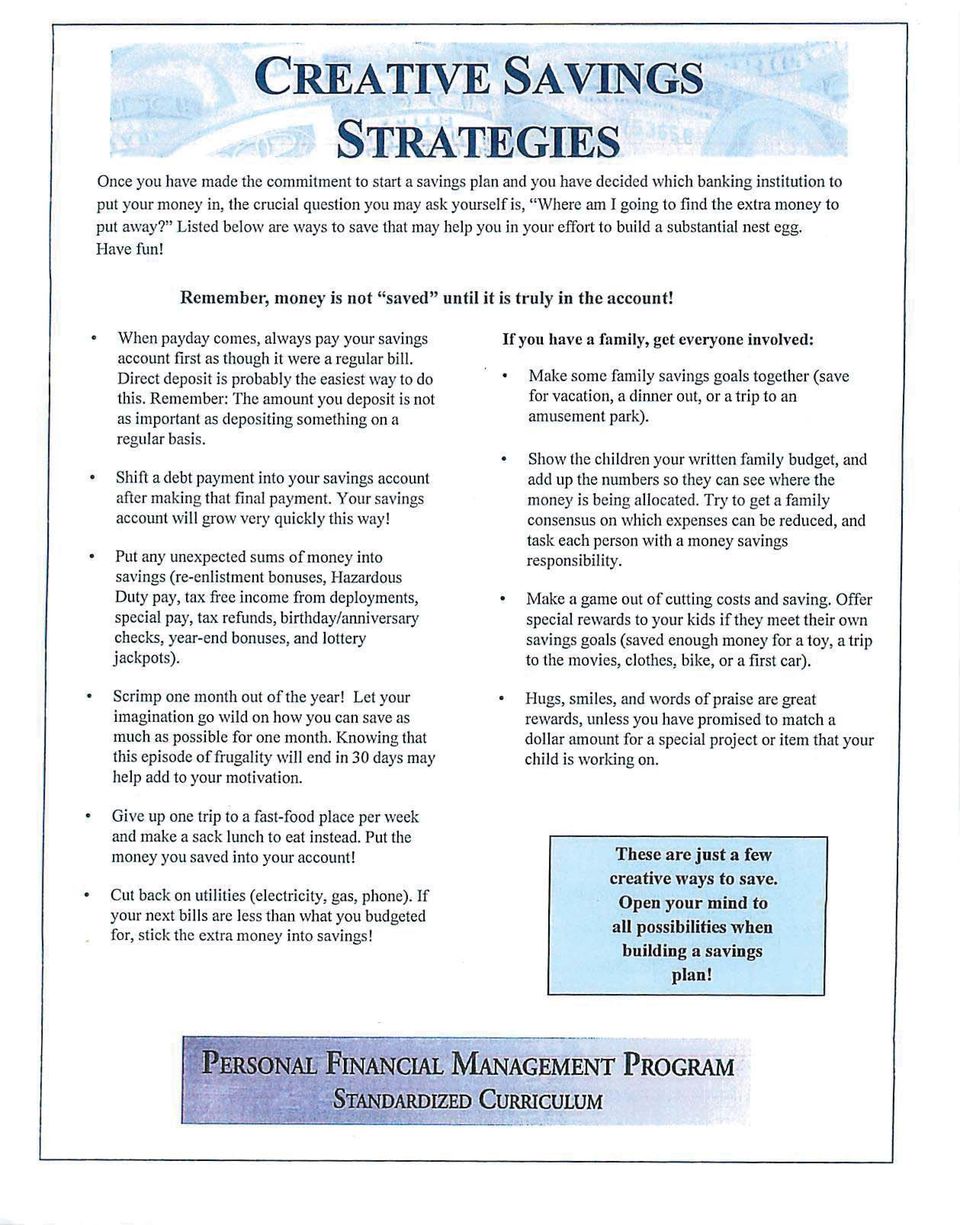

1 PERSONAL IN NATURE F.O.U.O. TRS PERSONAL FINANCE HOMEWORK: Amounts in Actual column are considered PRE-WORK and must be complete BEFORE the TRS seminar DATE: Completed budget- due 0730 TUESDAY (Attach this page as a cover sheet to your budget plan) NAME: Personal Financial Management Program Education Building 220, Room 103 & / Facebook: PFMPHawaii PERSONAL IN NATURE F.O.U.O.

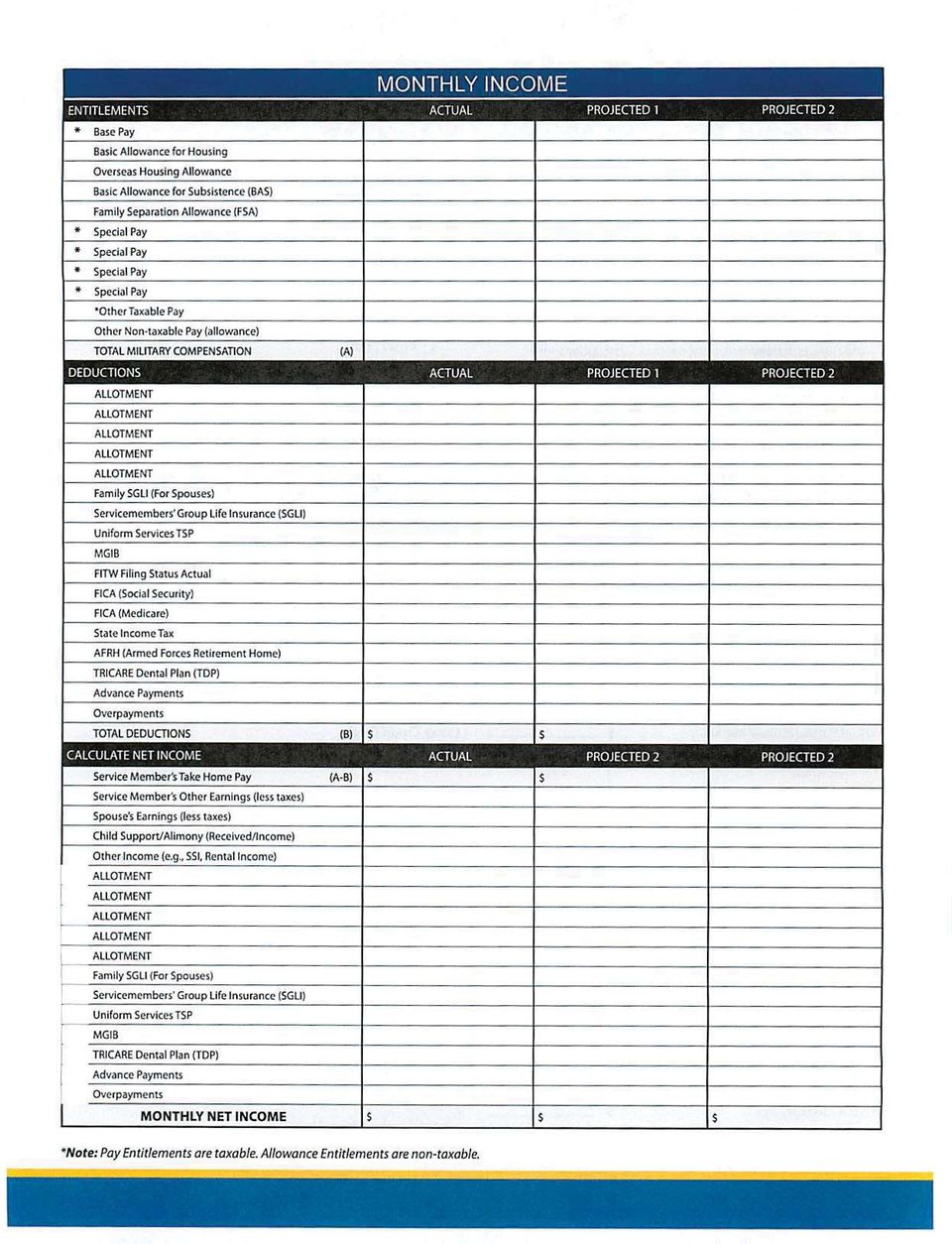

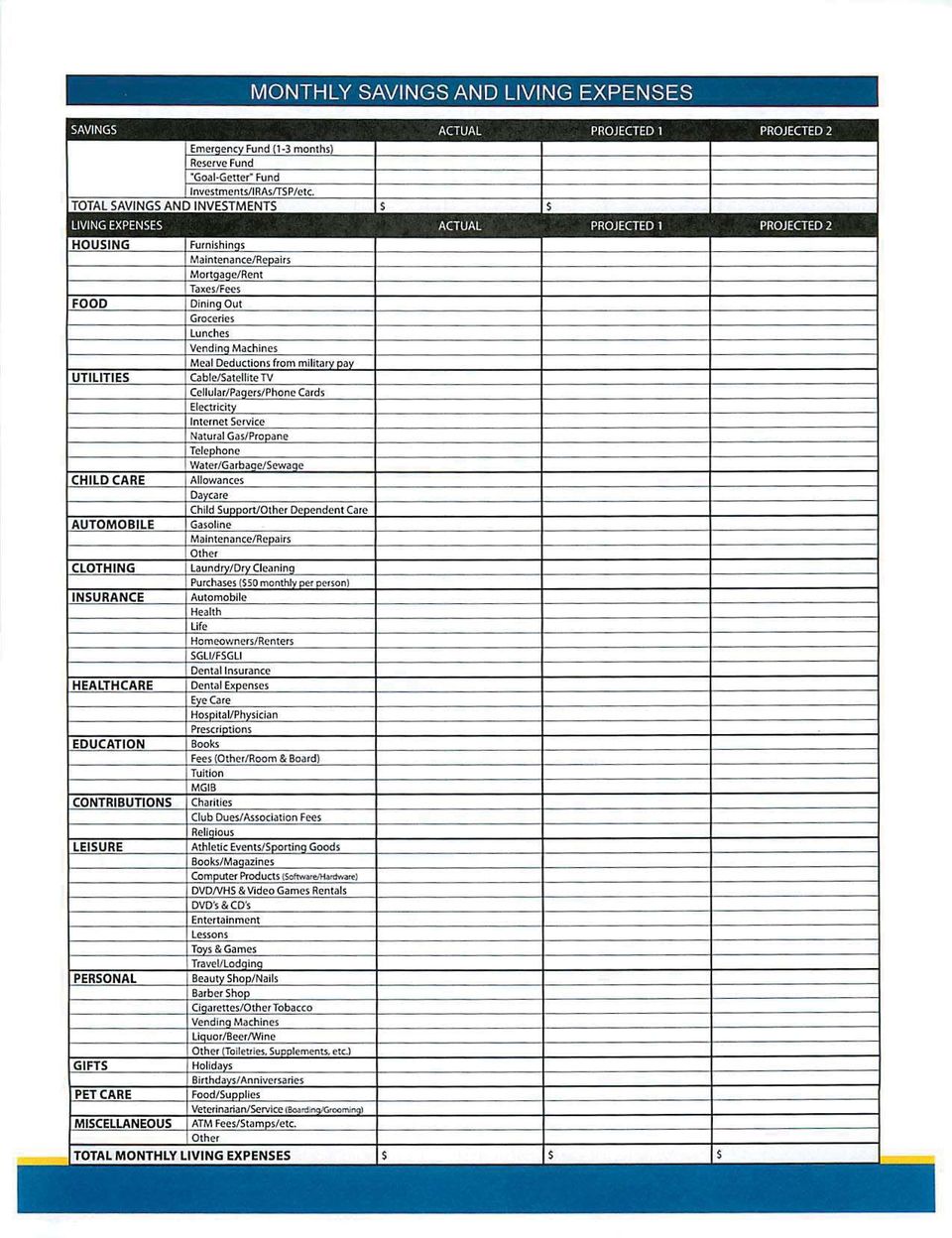

2 Please stop and READ! Tips For Filling Out Your Budget Plan This is a paper budget version, you must do the math calculations yourself. This is a monthly budget, provide monthly numbers when completing your budget, unless otherwise noted. There are 2 columns to your budget: Actual (your current budget for Hawaii) and Projected (for after EAS- either employment, college/vo-tech or as an entrepreneur) Be as complete as possible, as this will provide you a good look at what your future budget will look like compared to your current budget. This will enable you to make timely adjustments, if needed for your future budget. Gather the Items on the checklist you will need to start your Financial Planning Worksheet Explanation of the 8 tabs: 1- Net Worth- (not monthly)- Complete the upper section, starting with Member s Name. Complete the Net Worth section by listing all of your ASSETS at either value (cash, TSP, IRA, primary home, jewelry, etc.), blue book value (vehicles, etc), and yard sale value or what you could reasonable sell items for (furniture, etc.). LIABILITIES- list the current balance of each item. 2- Member s Income- Actual: Use your LES to complete this page for actual, copy it exactly. Note: In the Federal Taxes remarks column, write the tax exemptions you re currently claiming (Single 0, Single 1, Married 0, Married 1, etc.). Current exemptions are found on your LES in the box with your federal and state taxes. In the state income tax remarks column, write the state you claim for tax purposes. Projected: BASE PAY box, is used for your new income. Calculate your monthly earnings. (Ex. $10/hr x 30 hrs a week= $300, then multiple by 4 to get your monthly gross income = $1200. This is not your Net Income/take home. Don t forget taxes to calculate an accurate Net Income!) In the section labeled, Calculate Net Income, determine your net income by subtracting your federal taxes, FICS (Social Security), FICA (Medicare), and state taxes from your new income. To determine your projected taxes use the tax calculator at (This is for all states-find your state). BAH box, if you re attending college, use the BAH calculator at Add other sources of income besides your military income to arrive at your net monthly income or total members monthly income to include spouse. 3- Spouse s Income- If you are or will be married, complete this tab if your spouse has or will have income to support your family. Combined Income- This automatically completes if you re using the electronic form. Other complete the Combined Take Home Pay by adding the take home pay lines from both member and spouse. 4- Savings & Expenses- These are 2 separate categories! Total your monthly SAVINGS contribution separately and then Expenses separately This is how much you SAVE monthly & SPEND monthly NOT the balance of your accounts (Your banking account balances are on the Net Worth/Section 1- not here) To get started, put your Net Income (or Combined- if married) at the top of the page as it will be used to calculate percentages of savings and expenses. Savings and Investments- How much do you contribute monthly to your savings and investments? (If the TSP or savings are taken out via allotments you don t need to calculate them in the actual because it s already deducted from your paycheck BUT you will want to write what is deducted in the remarks section AND be sure to complete the projected amount. Add your total savings/investing in the line Pay Period Savings and Investments (10%).

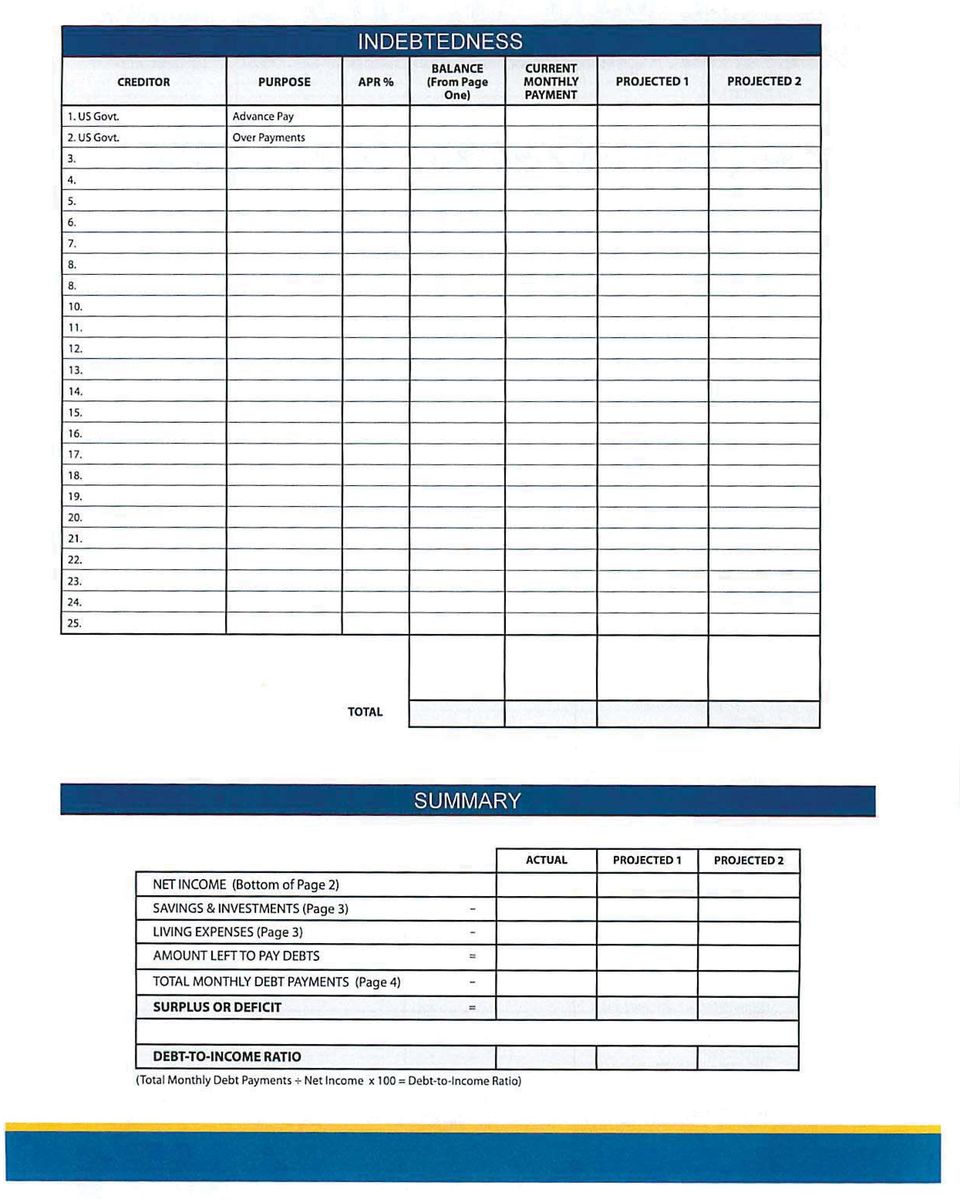

3 Expenses- For your actual expenses, look at your last month s bank statement. A good website to assist in determining the cost of items for your projected expenses is: Honolulu is listed under Urban Honolulu. For occasional or periodic expenses such as vehicle maintenance, clothing, gifts, etc., determine what you plan to spend for a year, and then divide by 12 months. This is the amount you will spend each month (actually putting it away to save for the month you will incur that expense- this is the RESERVE SAVING FUND). For example, if you estimate you will spend $700 for holiday gifts, then you should budget $59 per month to put aside, so that you will have $700 saved come the holiday. Subtotal your expenses pages, and then add them together to arrive at the grand total for your expenses. 5- Indebtedness- List all of your outstanding debts (car loan, credit cards, personal loans, student loans, etc.). Be sure to include the Annual Percentage Rate (APR). Total both the Total Owed and the Total Monthly Payments columns. Summary Section*: This final calculation helps you understand your financial situation. Complete the bottom section by bringing the listed totals from previous sections (Net Income, Savings & Investments, Living Expenses). To determine the Amount left to Pay Debts subtract the Savings & Investments and Living Expenses from Net Income. This is a subtotal of the money you have left for debt. Place the subtotal Amount Left to Pay Debts and then subtract the Total Monthly Debt Payments from indebtedness above. Example: Car payment $200, Credit Card $100, Student Loan $50= $350 is going to be subtracted. *This will tell you how much you have left at the end of the month as a surplus or a deficit. Debt to Income Ratio: Use the worksheet on page 7 to walk you through the calculations. 6- Action Plan & Goals- Action Plan- Use to list action you will take to improve your financial situation. Goals- List your financial goals and what it will take to obtain them. This will help you stay focused on sticking to your budget Terminal Date: EAS Date:

.")

4

5

6

7

8

9

10

11

Unit 4: Taxes. Read this unit including websites. You may want to take your own notes.

Taxes Read Chapter 4 in the text. Read Chapter 7 of The Financial Checkup. Read this unit including websites. You may want to take your own notes. Are taxes your favorite topic? They are not the favorite

Taxes Read Chapter 4 in the text. Read Chapter 7 of The Financial Checkup. Read this unit including websites. You may want to take your own notes. Are taxes your favorite topic? They are not the favorite

A financial statement captures a person s overall wealth at a specific point in time. In this lesson, students will:

PROJECT 3 CASH FLOW AND BALANCE SHEETS INSTRUCTOR OVERVIEW Financial statements are compilations of personal financial data that describe an individual s current financial condition. Financial statements

PROJECT 3 CASH FLOW AND BALANCE SHEETS INSTRUCTOR OVERVIEW Financial statements are compilations of personal financial data that describe an individual s current financial condition. Financial statements

A financial statement captures a person s overall wealth at a specific point in time. In this lesson, students will:

PROJECT 3 CASH FLOW AND BALANC E SHEETS INSTRUCTOR OVERVIEW Financial statements are compilations of personal financial data that describe an individual s current financial condition. Financial statements

PROJECT 3 CASH FLOW AND BALANC E SHEETS INSTRUCTOR OVERVIEW Financial statements are compilations of personal financial data that describe an individual s current financial condition. Financial statements

Personal Financial Planning for Transition Module: Excerpts

Excerpts from the Participant Guide: GPS Core Personal Financial Planning for Transition Instructions Handout, Online Course Lessons: Developing a Spending Plan 1 Completing the Net Income Worksheets ACTIVITY:

Excerpts from the Participant Guide: GPS Core Personal Financial Planning for Transition Instructions Handout, Online Course Lessons: Developing a Spending Plan 1 Completing the Net Income Worksheets ACTIVITY:

INSERT SECTION DAILY EXPENDITURES TRACKING SHEETS EXPENSE WORKSHEET INCOME WORKSHEET

INSERT SECTION DAILY EXPENDITURES TRACKING SHEETS EXPENSE WORKSHEET INCOME WORKSHEET U N D E R S T A N D I N G M O N E Y A N D C R E D I T R E F E R E N C E G U I D E 17 Record Of Daily Expenditures MONTH

INSERT SECTION DAILY EXPENDITURES TRACKING SHEETS EXPENSE WORKSHEET INCOME WORKSHEET U N D E R S T A N D I N G M O N E Y A N D C R E D I T R E F E R E N C E G U I D E 17 Record Of Daily Expenditures MONTH

Personal Finance Unit 1 Chapter 3 2007 Glencoe/McGraw-Hill

0 Chapter 3 Money Management Strategy What You ll Learn Section 3.1 Discuss the relationship between opportunity costs and money management. Explain the benefits of keeping financial records and documents.

0 Chapter 3 Money Management Strategy What You ll Learn Section 3.1 Discuss the relationship between opportunity costs and money management. Explain the benefits of keeping financial records and documents.

Money Management THEME

THEME 3 Introduction Money Management Do you know people who handle money carelessly? Lots of seemingly smart people are clueless about where they stand financially. There is Beverly, a professional woman,

THEME 3 Introduction Money Management Do you know people who handle money carelessly? Lots of seemingly smart people are clueless about where they stand financially. There is Beverly, a professional woman,

Preparing Family Net Worth and Income Statements

Family and Consumer Sciences FSFCS49 Preparing Family Net Worth and Income Statements Laura Connerly Instructor - Family Resource Management Arkansas Is Our Campus Visit our web site at: http://www.uaex.edu

Family and Consumer Sciences FSFCS49 Preparing Family Net Worth and Income Statements Laura Connerly Instructor - Family Resource Management Arkansas Is Our Campus Visit our web site at: http://www.uaex.edu

Budgeting for Home Ownership

A HOME FOR YOUR FAMILY 7 Budgeting for Home Ownership Perhaps you are just beginning to think about buying a home sometime in the future. Or maybe you have already found a home you would like to buy. Whether

A HOME FOR YOUR FAMILY 7 Budgeting for Home Ownership Perhaps you are just beginning to think about buying a home sometime in the future. Or maybe you have already found a home you would like to buy. Whether

MCRD San Diego Dissolution Worksheet

UNITED STATES MARINE CORPS LEGAL SERVICES SUPPORT TEAM, MIRAMAR MCRD DETACHMENT 3700 CHOSIN AVENUE SAN DIEGO, CA 9210 (619) 524-4110/4111 MCRD San Diego Dissolution Worksheet Uncontested Divorces Only

UNITED STATES MARINE CORPS LEGAL SERVICES SUPPORT TEAM, MIRAMAR MCRD DETACHMENT 3700 CHOSIN AVENUE SAN DIEGO, CA 9210 (619) 524-4110/4111 MCRD San Diego Dissolution Worksheet Uncontested Divorces Only

Financial Planning Worksheet

Financial Planning Worksheet Date SSN Rate Name Age Pay Grade Yrs. in Svc. Date Reported/PRD (Transfer) Marital Status Spouse s Name Age Spouse s Place of Employment Number of Children and Ages Home Address

Financial Planning Worksheet Date SSN Rate Name Age Pay Grade Yrs. in Svc. Date Reported/PRD (Transfer) Marital Status Spouse s Name Age Spouse s Place of Employment Number of Children and Ages Home Address

- all the money you receive in a year - money from wages, tips, interest you earn, dividends, capital gains, etc.

4D Income Taxes there are 5 different categories Single You must be unmarried at the end of the year. Married filing jointly this is how most married people will file. Married filing separately occasionally,

4D Income Taxes there are 5 different categories Single You must be unmarried at the end of the year. Married filing jointly this is how most married people will file. Married filing separately occasionally,

Do you know where your money

Manage Your Money Lesson 2: Where Does Your Money Go?. Do you know where your money goes? You may say, House payments, car loan, utility bills, and food. But after that, things begin to get a bit fuzzy.

Manage Your Money Lesson 2: Where Does Your Money Go?. Do you know where your money goes? You may say, House payments, car loan, utility bills, and food. But after that, things begin to get a bit fuzzy.

Effective Strategies for Personal Money Management

Effective Strategies for Personal Money Management The key to successful money management is developing and following a personal financial plan. Research has shown that people with a financial plan tend

Effective Strategies for Personal Money Management The key to successful money management is developing and following a personal financial plan. Research has shown that people with a financial plan tend

how much would you spend? answer key

scenario 1 Manuel wants to buy a car. But before he goes shopping, he wants to know exactly how much he can afford to spend each month on owning, operating, and maintaining a car. Manuel s net monthly

scenario 1 Manuel wants to buy a car. But before he goes shopping, he wants to know exactly how much he can afford to spend each month on owning, operating, and maintaining a car. Manuel s net monthly

BLR s Human Resources Training Presentations

BLR s Human Resources Training Presentations Basic Tax Guidelines For Employees Background for the Trainer: Obtain recent copies of relevant state and federal tax forms, schedules, and instruction booklets

BLR s Human Resources Training Presentations Basic Tax Guidelines For Employees Background for the Trainer: Obtain recent copies of relevant state and federal tax forms, schedules, and instruction booklets

Debtor s Full Legal Name: Spouse s Full Legal Name: Other Names Ever Used: Email: Tel#: Cell#: Emergency Contact (name & number):

:") Law Office of Jeffrey B. Kelly, P.C. Chapter 7 Chapter 13 Bankruptcy Questionnaire DEBTOR INFO: How did you first hear about my office? Office Location Debtor s Full Legal Name: SS# DOB: Spouse s Full

Law Office of Jeffrey B. Kelly, P.C. Chapter 7 Chapter 13 Bankruptcy Questionnaire DEBTOR INFO: How did you first hear about my office? Office Location Debtor s Full Legal Name: SS# DOB: Spouse s Full

Divorce worksheets. important issues to consider as you start the divorce process. Financial affidavit and property settlement

MFS Heritage Planni Divorce worksheets With so many emotions involved in the dissolution of a marriage, you ll probably want to make the financial aspects of your divorce proceed as smoothly as possible.

MFS Heritage Planni Divorce worksheets With so many emotions involved in the dissolution of a marriage, you ll probably want to make the financial aspects of your divorce proceed as smoothly as possible.

Cash Flow Forecasting & Break-Even Analysis

Cash Flow Forecasting & Break-Even Analysis 1. Cash Flow Cash Flow Projections What is cash flow? Cash flow is an estimate of the timing of when the cash associated with sales will be received and when

Cash Flow Forecasting & Break-Even Analysis 1. Cash Flow Cash Flow Projections What is cash flow? Cash flow is an estimate of the timing of when the cash associated with sales will be received and when

CHAPTER 10 Financial Statements NOTE

NOTE In practice, accruals accounts and prepayments accounts are implied rather than drawn up. It is common for expense accounts to show simply a balance c/d and a balance b/d. The accrual or prepayment

NOTE In practice, accruals accounts and prepayments accounts are implied rather than drawn up. It is common for expense accounts to show simply a balance c/d and a balance b/d. The accrual or prepayment

Official Form 22A 2 Chapter 7 Means Test Calculation 12/13

Fill in this information to identify your case: Check one only as directed in lines 40 or 42: Debtor 1 Debtor 2 (Spouse, if filing) United States Bankruptcy Court for the: District of (State) Case number

Fill in this information to identify your case: Check one only as directed in lines 40 or 42: Debtor 1 Debtor 2 (Spouse, if filing) United States Bankruptcy Court for the: District of (State) Case number

Financial Planning Worksheet

Financial Planning Worksheet Date SSN Rate Name Age Pay Grade Yrs. in Svc. Date Reported/PRD (Transfer) Marital Status Spouse s Name Age Spouse s Place of Employment Number of Children and Ages Home Address

Financial Planning Worksheet Date SSN Rate Name Age Pay Grade Yrs. in Svc. Date Reported/PRD (Transfer) Marital Status Spouse s Name Age Spouse s Place of Employment Number of Children and Ages Home Address

PERSONAL FINANCE. financial planning & goal setting

PERSONAL FINANCE financial planning & goal setting 1 our mission To lead and inspire actions that improve financial readiness for the military and local community. 2 table of contents The Power Of Planning...

PERSONAL FINANCE financial planning & goal setting 1 our mission To lead and inspire actions that improve financial readiness for the military and local community. 2 table of contents The Power Of Planning...

Arizona Form 2013 Individual Amended Income Tax Return 140X

Arizona Form 2013 Individual Amended Income Tax Return 140X Phone Numbers For information or help, call one of the numbers listed: Phoenix (602) 255-3381 From area codes 520 and 928, toll-free (800) 352-4090

Arizona Form 2013 Individual Amended Income Tax Return 140X Phone Numbers For information or help, call one of the numbers listed: Phoenix (602) 255-3381 From area codes 520 and 928, toll-free (800) 352-4090

How to Use the Cash Flow Template

How to Use the Cash Flow Template When you fill in your cash flow you are trying to predict the timing of cash in and out of your bank account to show the affect and timing for each transaction when it

How to Use the Cash Flow Template When you fill in your cash flow you are trying to predict the timing of cash in and out of your bank account to show the affect and timing for each transaction when it

FINANCIAL INTRODUCTION

FINANCIAL INTRODUCTION In earlier sections you calculated your cost of goods sold, overhead expenses and capital cost in order to help you determine the sales price of your product. In your business plan,

FINANCIAL INTRODUCTION In earlier sections you calculated your cost of goods sold, overhead expenses and capital cost in order to help you determine the sales price of your product. In your business plan,

Creating a Successful Financial Plan

Creating a Successful Financial Plan Basic Financial Reports Balance Sheet - Estimates the firm s worth on a given date; built on the accounting equation: Assets = Liabilities + Owner s Equity Income Statement

Creating a Successful Financial Plan Basic Financial Reports Balance Sheet - Estimates the firm s worth on a given date; built on the accounting equation: Assets = Liabilities + Owner s Equity Income Statement

Financial Affidavit of Information - Short Form

Connecticut Judicial Branch Self-Represented Parties Information Series Filling Out and Filing a Financial Affidavit Short Form Slide 1 Welcome to the Connecticut Judicial Branch Law Libraries Self-Represented

Connecticut Judicial Branch Self-Represented Parties Information Series Filling Out and Filing a Financial Affidavit Short Form Slide 1 Welcome to the Connecticut Judicial Branch Law Libraries Self-Represented

Designing Your Budget

2 Designing Your Budget Budgeting is needed to get the most mileage out of your income. It is your road map for managing your money. Planning your spending is called Budgeting. Smart investing@your library

2 Designing Your Budget Budgeting is needed to get the most mileage out of your income. It is your road map for managing your money. Planning your spending is called Budgeting. Smart investing@your library

Questions and Answers about Medicaid for Those Receiving Long-Term Care in Idaho

Questions and Answers about Medicaid for Those Receiving Long-Term Care in Idaho Question 1: What is Medicaid? Answer: Medicaid is a government program that pays for medical services, including long-term

Questions and Answers about Medicaid for Those Receiving Long-Term Care in Idaho Question 1: What is Medicaid? Answer: Medicaid is a government program that pays for medical services, including long-term

Official Form B 22A2 Chapter 7 Means Test Calculation 12/14

Fill in this information to identify your case: Debtor 1 Debtor 2 (Spouse, if filing) United States Bankruptcy Court for the: District District of of (State) Case number (If known) Check the appropriate

Fill in this information to identify your case: Debtor 1 Debtor 2 (Spouse, if filing) United States Bankruptcy Court for the: District District of of (State) Case number (If known) Check the appropriate

INSTRUCTIONS TO ASSIST IN COMPLETING ATTACHMENT B: PERSONAL FINANCIAL STATEMENT WORKSHEET

INSTRUCTIONS TO ASSIST IN COMPLETING ATTACHMENT B: PERSONAL FINANCIAL STATEMENT WORKSHEET This instruction sheet is intended to provide guidance on how to complete the Attachment B: Personal Financial

INSTRUCTIONS TO ASSIST IN COMPLETING ATTACHMENT B: PERSONAL FINANCIAL STATEMENT WORKSHEET This instruction sheet is intended to provide guidance on how to complete the Attachment B: Personal Financial

Credit 100 understanding credit

Credit 100 understanding credit An investment in knowledge always pays the best interest. Franklin D. Roosevelt Credit 100 1 Credit can open doors to buying a home or a car. But it can also lead to significant

Credit 100 understanding credit An investment in knowledge always pays the best interest. Franklin D. Roosevelt Credit 100 1 Credit can open doors to buying a home or a car. But it can also lead to significant

Taking Control of Your Finances A Plan to Reduce Debt and Build Savings

Taking Control of Your Finances A Plan to Reduce Debt and Build Savings From Credit to Debt A Slippery Slope Purchasing on credit reflects confidence in our ability to pay We often use credit to buy what

Taking Control of Your Finances A Plan to Reduce Debt and Build Savings From Credit to Debt A Slippery Slope Purchasing on credit reflects confidence in our ability to pay We often use credit to buy what

Familiarize yourself with laws that authorize and regulate vehicle dealership financing and leasing.

W ith prices averaging more than $28,000 for a new vehicle and $15,000 for a used vehicle, most consumers need financing or leasing to acquire a vehicle. In some cases, buyers use direct lending: they

W ith prices averaging more than $28,000 for a new vehicle and $15,000 for a used vehicle, most consumers need financing or leasing to acquire a vehicle. In some cases, buyers use direct lending: they

It s Your Paycheck! Glossary of Terms

Annual percentage rate The percentage cost of credit on an annual basis and the total cost of credit to the consumer. APR combines the interest paid over the life of the loan and all fees that are paid

Annual percentage rate The percentage cost of credit on an annual basis and the total cost of credit to the consumer. APR combines the interest paid over the life of the loan and all fees that are paid

Accounting Self Study Guide for Staff of Micro Finance Institutions

Accounting Self Study Guide for Staff of Micro Finance Institutions LESSON 2 The Balance Sheet OBJECTIVES The purpose of this lesson is to introduce the Balance Sheet and explain its components: Assets,

Accounting Self Study Guide for Staff of Micro Finance Institutions LESSON 2 The Balance Sheet OBJECTIVES The purpose of this lesson is to introduce the Balance Sheet and explain its components: Assets,

WEALTH CARE KIT SM. A consumer s guide to establishing and maintaining a financial wellness plan.

WEALTH CARE KIT SM A consumer s guide to establishing and maintaining a financial wellness plan. A website built by the dedicated to your financial well-being. THE WEALTH CARE KIT an INTRODUCTION You plan

WEALTH CARE KIT SM A consumer s guide to establishing and maintaining a financial wellness plan. A website built by the dedicated to your financial well-being. THE WEALTH CARE KIT an INTRODUCTION You plan

Slide 2. Income Taxes

Slide 1 Taxes Income taxes have been a part of American life since 1909 when the 16 th Amendment to the Constitution was ratified. You can t avoid taxes, so you might as well understand how taxes are structured

Slide 1 Taxes Income taxes have been a part of American life since 1909 when the 16 th Amendment to the Constitution was ratified. You can t avoid taxes, so you might as well understand how taxes are structured

Associated Files: Ratios worksheet

Unit 4 Business accounting Ratios Instructions and answers for Teachers These instructions should accompany the OCR resource Ratios which supports the OCR Level 3 Cambridge Technicals in Business Unit

Unit 4 Business accounting Ratios Instructions and answers for Teachers These instructions should accompany the OCR resource Ratios which supports the OCR Level 3 Cambridge Technicals in Business Unit

Lesson Description. Texas Essential Knowledge and Skills (Target standards) Skills (Prerequisite standards) National Standards (Supporting standards)

Skills (Prerequisite standards) National Standards (Supporting standards)") Lesson Description Students will analyze families finances to identify assets and liabilities. They will use this information to calculate the families net worth and learn the benefits of having a positive

Lesson Description Students will analyze families finances to identify assets and liabilities. They will use this information to calculate the families net worth and learn the benefits of having a positive

KENT FAMILY FINANCES

FACTS KENT FAMILY FINANCES Ken and Kendra Kent have been married twelve years and have twin 4-year-old sons. Kendra earns $78,000 as a Walmart assistant manager and Ken is a stay-at-home dad. They give

FACTS KENT FAMILY FINANCES Ken and Kendra Kent have been married twelve years and have twin 4-year-old sons. Kendra earns $78,000 as a Walmart assistant manager and Ken is a stay-at-home dad. They give

Plan and Track Your Finances

Plan and Track Your Finances 9.1 Financing Your Business 9.2 Pro Forma Financial Statements 9.3 Recordkeeping for Businesses Lesson 9.1 Financing Your Business Goals Estimate your startup costs and personal

Plan and Track Your Finances 9.1 Financing Your Business 9.2 Pro Forma Financial Statements 9.3 Recordkeeping for Businesses Lesson 9.1 Financing Your Business Goals Estimate your startup costs and personal

Check if this is an amended filing

Fill in this information to identify your case: Debtor 1 Debtor 2 (Spouse, if filing) United States Bankruptcy Court for the: District of of Case number (If known) Check if this is an amended filing Official

Fill in this information to identify your case: Debtor 1 Debtor 2 (Spouse, if filing) United States Bankruptcy Court for the: District of of Case number (If known) Check if this is an amended filing Official

Keys for Planning a. Happy Retirement. www.theaiatrust.com. - Larry Gaffey, CPA

Keys for Planning a Happy Retirement - Larry Gaffey, CPA www.theaiatrust.com RETIREMENT GOAL Worksheet Handout 2 DESCRIPTION HOW IMPORTANT IS THIS TO ME (Scale of 1-10) Family/Relationships Visit children/grandchildren

Keys for Planning a Happy Retirement - Larry Gaffey, CPA www.theaiatrust.com RETIREMENT GOAL Worksheet Handout 2 DESCRIPTION HOW IMPORTANT IS THIS TO ME (Scale of 1-10) Family/Relationships Visit children/grandchildren

students can throw the bills away or make a pile of the discarded bills.)

") SM2-1: Budget Busters Purpose: Examine current personal money management habits by participating in this activity. Materials: Play money: enough so that each class member can have 10 bills. All bills can

SM2-1: Budget Busters Purpose: Examine current personal money management habits by participating in this activity. Materials: Play money: enough so that each class member can have 10 bills. All bills can

Self-Service Center CONSERVATORSHIP. INSTRUCTIONS for the AMENDED BUDGET

Self-Service Center CONSERVATORSHIP INSTRUCTIONS for the AMENDED BUDGET I. GENERAL INFORMATION A. WHO should file the AMENDED BUDGET? The Conservator or Guardian/Conservator responsible for the protected

Self-Service Center CONSERVATORSHIP INSTRUCTIONS for the AMENDED BUDGET I. GENERAL INFORMATION A. WHO should file the AMENDED BUDGET? The Conservator or Guardian/Conservator responsible for the protected

Chapter 13 Financial Statements and Closing Procedures

Chapter 13 - Financial Statements and Closing Procedures Chapter 13 Financial Statements and Closing Procedures TEACHING OBJECTIVES 13-1) Prepare a classified income statement from the worksheet. 13-2)

Chapter 13 - Financial Statements and Closing Procedures Chapter 13 Financial Statements and Closing Procedures TEACHING OBJECTIVES 13-1) Prepare a classified income statement from the worksheet. 13-2)

List any past due bills provide account balance and status, i.e., in collections, charged off, etc.

Dear Workshop Participant (s): Welcome to the Increasing Your Cash Flow workshop! I am looking forward to working with you as we explore ways to improve your current financial situation and secure your

Dear Workshop Participant (s): Welcome to the Increasing Your Cash Flow workshop! I am looking forward to working with you as we explore ways to improve your current financial situation and secure your

how much would you spend?

name: date: how much would you spend? scenario 1 Manuel wants to buy a car. But before he goes shopping, he wants to know exactly how much he can afford to spend each month on owning, operating, and maintaining

name: date: how much would you spend? scenario 1 Manuel wants to buy a car. But before he goes shopping, he wants to know exactly how much he can afford to spend each month on owning, operating, and maintaining

Wisdom and Wealth: There are specific financial planning. A Workbook for Wealth Creation

Wisdom and Wealth: A Workbook for Wealth Creation There are specific financial planning goals that should be considered during each decade of life. This workbook presents a series of questions meant to

Wisdom and Wealth: A Workbook for Wealth Creation There are specific financial planning goals that should be considered during each decade of life. This workbook presents a series of questions meant to

budgeting Budgeting Money planning to meet your financial goals Inside... What is a budget? Making a budget Getting help

budgeting Budgeting Money planning to meet your financial goals Inside... What is a budget? Making a budget Getting help What is a budget? A budget is a plan for the money you expect to receive and how

budgeting Budgeting Money planning to meet your financial goals Inside... What is a budget? Making a budget Getting help What is a budget? A budget is a plan for the money you expect to receive and how

3Budgeting: Keeping Track of Your Money

This sample chapter is for review purposes only. Copyright The Goodheart-Willcox Co., Inc. All rights reserved. 3Budgeting: Keeping Track of Your Money Chapter 3 Budgeting: Keeping Track of Your Money

This sample chapter is for review purposes only. Copyright The Goodheart-Willcox Co., Inc. All rights reserved. 3Budgeting: Keeping Track of Your Money Chapter 3 Budgeting: Keeping Track of Your Money

Account a service provided by a bank allowing a customer s money to be handled and tracks money coming in and going out of the account.

Account a service provided by a bank allowing a customer s money to be handled and tracks money coming in and going out of the account. Account fee the amount charged by a financial institution for the

Account a service provided by a bank allowing a customer s money to be handled and tracks money coming in and going out of the account. Account fee the amount charged by a financial institution for the

Managing Your Finances - A Lesson for Teens

CHAPTER 6: Managing Income, Expenses, Savings and Credit INTRODUCTION Managing Income, Expenses, Savings and Credit is a 90-minute program designed to provide Marines and their families with an understanding

CHAPTER 6: Managing Income, Expenses, Savings and Credit INTRODUCTION Managing Income, Expenses, Savings and Credit is a 90-minute program designed to provide Marines and their families with an understanding

Lesson Description. Concepts. Objectives. Content Standards. Time Required. KaChing! Lesson 4: Your Budget Plan

Lesson Description Students work in pairs to participate in a Track Star game that illustrates positive and negative spending behaviors. Each pair of students analyzes the Track Star results, identifies

Lesson Description Students work in pairs to participate in a Track Star game that illustrates positive and negative spending behaviors. Each pair of students analyzes the Track Star results, identifies

Section 12.1 Financial Ratios Section 12.2 Break-Even Analysis

Section 12.1 Financial Ratios Section 12.2 Break-Even Analysis OBJECTIVES Explain what a financial ratio is Describe how income statements are used for financial analysis Compare operating ratios and return-on-sales

Section 12.1 Financial Ratios Section 12.2 Break-Even Analysis OBJECTIVES Explain what a financial ratio is Describe how income statements are used for financial analysis Compare operating ratios and return-on-sales

Instructions for INCOME AND EXPENSE DECLARATION

Instructions for INCOME AND EXPENSE DECLARATION This packet is designed to help you complete an Income and Expense Declaration [FL-150] and it includes a blank Income and Expense Declaration. An Income

Instructions for INCOME AND EXPENSE DECLARATION This packet is designed to help you complete an Income and Expense Declaration [FL-150] and it includes a blank Income and Expense Declaration. An Income

Income Sources: Income 1 Living Expenses Budget Actual Variance Food. Personal. Income ❶ License* minus % Parking

My Monthly Budget Month: Income Sources: Income 1 Living Expenses Budget Actual Variance Income 2 Food Income 3 Toiletries/supplies Total Income ❶ Support Expenses: Entertainment Savings Budget Actual

My Monthly Budget Month: Income Sources: Income 1 Living Expenses Budget Actual Variance Income 2 Food Income 3 Toiletries/supplies Total Income ❶ Support Expenses: Entertainment Savings Budget Actual

You ve worked hard for your savings. Now keep your savings working hard for you.

You ve worked hard for your savings. Now keep your savings working hard for you. Retire with confidence A guide to your distribution options. You are now faced with an important financial decision When

You ve worked hard for your savings. Now keep your savings working hard for you. Retire with confidence A guide to your distribution options. You are now faced with an important financial decision When

Income Sources Recap Jot down your streams of income, even if it s just a trickle right now.

Income Sources Recap Jot down your streams of income, even if it s just a trickle right now. Money s fun. If you ve got some. You ve got money coming in from somewhere, right? Then write it down. This

Income Sources Recap Jot down your streams of income, even if it s just a trickle right now. Money s fun. If you ve got some. You ve got money coming in from somewhere, right? Then write it down. This

Financial Statements LESSON 15. What are Financial Statements?

Financial Statements LESSON 15 Main Idea Business owners must have accurate and timely information about the fi nancial status of their business to make the best decisions. Most of this fi nancial information

Financial Statements LESSON 15 Main Idea Business owners must have accurate and timely information about the fi nancial status of their business to make the best decisions. Most of this fi nancial information

YOUR PERSONAL FINANCIAL PLAN AND FACT FIND

Document name: YOUR PERSONAL FINANCIAL PLAN AND FACT FIND Document date: 2014 Copyright information: Content is made available under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 Licence

Document name: YOUR PERSONAL FINANCIAL PLAN AND FACT FIND Document date: 2014 Copyright information: Content is made available under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 Licence

Date of Interview: NAME DURATION REASON FOR LEAVING. Marital status: Single Married Separated Divorced Widowed Common Law

Date of Interview: CRAWFORD SMITH & SWALLOW INC. Page 1 531 LAKE STREET, ST. CATHARINES, ONTARIO L2N 4H6 Tel: (905) 937-2100 Fax: (905) 937-7363 Website: www.crawfordss.com Email: css@crawfordss.com APPLICATION

Date of Interview: CRAWFORD SMITH & SWALLOW INC. Page 1 531 LAKE STREET, ST. CATHARINES, ONTARIO L2N 4H6 Tel: (905) 937-2100 Fax: (905) 937-7363 Website: www.crawfordss.com Email: css@crawfordss.com APPLICATION

Financial planning. Financial planning. Financial goals

Financial planning Where are you now? How d you get there? Where do you want to be? How re you going to get there? Financial planning Process of developing and implementing a coordinated series of strategies

Financial planning Where are you now? How d you get there? Where do you want to be? How re you going to get there? Financial planning Process of developing and implementing a coordinated series of strategies

Developing Financial Statements

New York StartUP! Business Plan Competition Developing Financial Statements Presented by Paisley Demby, CEO PBN Consulting, LLC www.pbnconsulting.com 1 Invitation to Tweet #2015NYStartUp PaisleyDemby Contents

New York StartUP! Business Plan Competition Developing Financial Statements Presented by Paisley Demby, CEO PBN Consulting, LLC www.pbnconsulting.com 1 Invitation to Tweet #2015NYStartUp PaisleyDemby Contents

PERSONAL FINANCIAL STATEMENT

PERSONAL FINANCIAL STATEMENT As of, 20 BUSINESS PLAN GUIDELINES Name: Residence Phone: Residence Address: City, State, Zip Code: Social Security Number: PERSONAL ASSETS PERSONAL LIABILITIES Cash in Bank

PERSONAL FINANCIAL STATEMENT As of, 20 BUSINESS PLAN GUIDELINES Name: Residence Phone: Residence Address: City, State, Zip Code: Social Security Number: PERSONAL ASSETS PERSONAL LIABILITIES Cash in Bank

Lifetime Income Financial Evaluation

Lifetime Income Financial Evaluation Client Name We will hold in the strictest confidence the information collected and entered in this document, other documents, and computerized software programs. We

Lifetime Income Financial Evaluation Client Name We will hold in the strictest confidence the information collected and entered in this document, other documents, and computerized software programs. We

Financial Planning Worksheet

Financial Planning Worksheet PAGE 1 Date Name Pay Grade Marital Status Spouse s Place of Employment Yrs. in Svc. Spouse s Name Rank Age Date Reported/PRD (Transfer) Age Number of Chil dren and Ages Home

Financial Planning Worksheet PAGE 1 Date Name Pay Grade Marital Status Spouse s Place of Employment Yrs. in Svc. Spouse s Name Rank Age Date Reported/PRD (Transfer) Age Number of Chil dren and Ages Home

Budgeting: Making the Most of Your Money

? Did You Know? Almost 60% of millionaires use a budget to manage their money. The Millionaire Next Door: The Surprising Secrets of America s Wealthy. In this unit, you will: Examine your spending habits

? Did You Know? Almost 60% of millionaires use a budget to manage their money. The Millionaire Next Door: The Surprising Secrets of America s Wealthy. In this unit, you will: Examine your spending habits

Complimentary Financial Planner

Complimentary Financial Planner Creating Wealth Since 1922 PERSONAL INFORMATION Name Social Security Number Date of Birth Home Street Address You Your Spouse City, State, Zip Home Telephone Marital Status

Complimentary Financial Planner Creating Wealth Since 1922 PERSONAL INFORMATION Name Social Security Number Date of Birth Home Street Address You Your Spouse City, State, Zip Home Telephone Marital Status

FINANCIAL ASSESSMENT FOR

FINANCIAL ASSESSMENT FOR Joe Sample Introduction BENEFIT OF FINANCIAL ASSESSMENTS The benefit of the financial assessment is to help you gather the facts so you can take an honest look at your finances.

FINANCIAL ASSESSMENT FOR Joe Sample Introduction BENEFIT OF FINANCIAL ASSESSMENTS The benefit of the financial assessment is to help you gather the facts so you can take an honest look at your finances.

GET CREDITWISE SM SM

GET CREDITWISE SM SM Table Of Contents October, 2006 Credit Matters 1 An introduction Establishing Credit 3 Begin building a solid financial base Using Credit Wisely 5 Narrowing your options Monitoring

GET CREDITWISE SM SM Table Of Contents October, 2006 Credit Matters 1 An introduction Establishing Credit 3 Begin building a solid financial base Using Credit Wisely 5 Narrowing your options Monitoring

Banning Law Firm. 10801 Lomas NE Ste. 104 Albuquerque, NM 87112 Office 883-9577 Fax 866-677-0508

Banning Law Firm 10801 Lomas NE Ste. 104 Albuquerque, NM 87112 Office 883-9577 Fax 866-677-0508 Questionnaire Taxes Credit Report Paper Work Needed To File Counseling Certificate Pay Check Stubs Payment

Banning Law Firm 10801 Lomas NE Ste. 104 Albuquerque, NM 87112 Office 883-9577 Fax 866-677-0508 Questionnaire Taxes Credit Report Paper Work Needed To File Counseling Certificate Pay Check Stubs Payment

Understanding Vehicle Financing

Understanding Vehicle Financing Understanding Vehicle Financing With prices averaging more than $31,000 for a new vehicle and $17,000 for a used model from a dealership, you might consider financing or

Understanding Vehicle Financing Understanding Vehicle Financing With prices averaging more than $31,000 for a new vehicle and $17,000 for a used model from a dealership, you might consider financing or

Online Application Steps and Helpful Hints. Under Borrower: If you select a Marital Status of Married, you will need to mark Yes for Joint Credit.

Get Started: Select a type of loan The property you are looking to purchase must be located in Florida in order to utilize GTE Financial financing. Purchase This a typical mortgage, whereby the borrower

Get Started: Select a type of loan The property you are looking to purchase must be located in Florida in order to utilize GTE Financial financing. Purchase This a typical mortgage, whereby the borrower

Medicaid Nursing Home Information

Medicaid Nursing Home Information January 2015 This pamphlet tells you about Medicaid rules for: Utah Nursing Homes. Intermediate Care Facilities for people with Intellectual Disabilities (ICF/ID) This

Medicaid Nursing Home Information January 2015 This pamphlet tells you about Medicaid rules for: Utah Nursing Homes. Intermediate Care Facilities for people with Intellectual Disabilities (ICF/ID) This

baj01275_app_433-454 02/09/2007 17:10PM Page 433 EPG_Team-C 105:JWQD032:bajapp: APPENDIX PERSONAL FINANCE WORKSHEETS

baj01275_app_433-454 02/09/2007 17:10PM Page 433 EPG_Team-C 105:JWQD032:bajapp: APPENDIX PERSONAL FINANCE WORKSHEETS baj01275_app_433-454 02/09/2007 17:10PM Page 434 EPG_Team-C 105:JWQD032:bajapp: 434

baj01275_app_433-454 02/09/2007 17:10PM Page 433 EPG_Team-C 105:JWQD032:bajapp: APPENDIX PERSONAL FINANCE WORKSHEETS baj01275_app_433-454 02/09/2007 17:10PM Page 434 EPG_Team-C 105:JWQD032:bajapp: 434

EDUCATIONAL BENEFITS GROUP Providing solutions to make college an affordable reality. Cash Flow Planning for College & Retirement

EDUCATIONAL BENEFITS GROUP Providing solutions to make college an affordable reality Cash Flow Planning for College & Retirement Table of Contents Cash Flow Planning for College & Retirement Introduction

EDUCATIONAL BENEFITS GROUP Providing solutions to make college an affordable reality Cash Flow Planning for College & Retirement Table of Contents Cash Flow Planning for College & Retirement Introduction

Lesson Description. Texas Essential Knowledge and Skills (Target standards) Skills (Prerequisite standards) National Standards (Supporting standards)

Skills (Prerequisite standards) National Standards (Supporting standards)") Lesson Description This lesson builds on Grade 7, Lesson 1. Students will calculate net income and categorize expenses to create a budget. Percentages for each category will be calculated and analyzed.

Lesson Description This lesson builds on Grade 7, Lesson 1. Students will calculate net income and categorize expenses to create a budget. Percentages for each category will be calculated and analyzed.

The Basics of Building Credit

The Basics of Building Credit This program was developed to help middle school students learn the basics of building credit. At the end of this lesson, you should know about all of the Key Topics below:»

The Basics of Building Credit This program was developed to help middle school students learn the basics of building credit. At the end of this lesson, you should know about all of the Key Topics below:»

How to Prepare a Cash Flow Forecast

The Orangeville & Area Small Business Enterprise Centre (SBEC) 87 Broadway, Orangeville ON L9W 1K1 519-941-0440 Ext. 2286 or 2291 sbec@orangeville.ca www.orangevillebusiness.ca Supported by its Partners:

The Orangeville & Area Small Business Enterprise Centre (SBEC) 87 Broadway, Orangeville ON L9W 1K1 519-941-0440 Ext. 2286 or 2291 sbec@orangeville.ca www.orangevillebusiness.ca Supported by its Partners:

BUDGETING FOR COLLEGE

LESSON THREE BUDGETING FOR COLLEGE INTRODUCTION & LEARNING GOALS It is important for students to consider the kinds of expenses they may need to be prepared to cover during college. This lesson will help

LESSON THREE BUDGETING FOR COLLEGE INTRODUCTION & LEARNING GOALS It is important for students to consider the kinds of expenses they may need to be prepared to cover during college. This lesson will help

THE NEF APPLICATION FORM R250 000 - R75 million

THE NEF APPLICATION FORM R250 000 - R75 million Name */ Male/Female Contribution Shareholding % (Pre-NEF funding) Shareholding % (Post-NEF funding) TOTAL D D M M Y Y Y Y PARTICIPATION IN: Current Future

THE NEF APPLICATION FORM R250 000 - R75 million Name */ Male/Female Contribution Shareholding % (Pre-NEF funding) Shareholding % (Post-NEF funding) TOTAL D D M M Y Y Y Y PARTICIPATION IN: Current Future

Financial Planning. Introduction. Learning Objectives

Financial Planning Introduction Financial Planning Learning Objectives Lesson 1 Budgeting: How to Live on Your Own and Not Move Home in a Week Prepare a budget and determine disposable income. Identify

Financial Planning Introduction Financial Planning Learning Objectives Lesson 1 Budgeting: How to Live on Your Own and Not Move Home in a Week Prepare a budget and determine disposable income. Identify

1. I have something called a Chapter 13 plan. What is that exactly?

1. I have something called a Chapter 13 plan. What is that exactly? The Bankruptcy Code requires that every Chapter 13 bankruptcy have a plan. It is a summary sent to your creditors that, in effect, tells

1. I have something called a Chapter 13 plan. What is that exactly? The Bankruptcy Code requires that every Chapter 13 bankruptcy have a plan. It is a summary sent to your creditors that, in effect, tells

2014 Client Organizer Questionnaire

2014 Client Organizer Questionnaire NOTE: We cannot complete your 2014 personal income tax returns without these questions being answered and the last page being signed. Please check the appropriate box

2014 Client Organizer Questionnaire NOTE: We cannot complete your 2014 personal income tax returns without these questions being answered and the last page being signed. Please check the appropriate box

Corporation, a copy of the file stamped Articles or Certificate of Incorporation

Thank you for choosing Frost for your business credit needs. We are committed to helping you determine the best financing option for your business. To assist us, we ask that you complete and submit the

Thank you for choosing Frost for your business credit needs. We are committed to helping you determine the best financing option for your business. To assist us, we ask that you complete and submit the

Instructions for E-PLAN Financial Planning Template

Instructions for E-PLAN Financial Planning Template The EPLAN template will assist you in preparing financial projections for your existing business. The template uses Microsoft Excel to prepare your projected

Instructions for E-PLAN Financial Planning Template The EPLAN template will assist you in preparing financial projections for your existing business. The template uses Microsoft Excel to prepare your projected

After Bankruptcy: What You Need to Know

After Bankruptcy: What You Need to Know The Path to Creditworthiness Bankruptcy offers some resolution to your financial worries. However, it also carries negative consequences and major responsibilities

After Bankruptcy: What You Need to Know The Path to Creditworthiness Bankruptcy offers some resolution to your financial worries. However, it also carries negative consequences and major responsibilities

Personal. Shaping Up Your Finances

Personal Shaping Up Your Finances 210.229.1128 MyGenFCU.org 1 Repaying Loans If you are having trouble making a payment on pre-existing loans, consider taking the following steps: Talk to your creditor.

Personal Shaping Up Your Finances 210.229.1128 MyGenFCU.org 1 Repaying Loans If you are having trouble making a payment on pre-existing loans, consider taking the following steps: Talk to your creditor.

The Newlywed s Guide. To Budgeting

The Newlywed s Guide To Budgeting How to create and manage a budget for your new life together. Congratulations! Whether you re about to be married or have been married for a few years now, I m glad that

The Newlywed s Guide To Budgeting How to create and manage a budget for your new life together. Congratulations! Whether you re about to be married or have been married for a few years now, I m glad that

Income, Expenses and Budget module

Income, Expenses and Budget module Trainer s introduction The skills to control your personal income, expenses and budget are the most basic tools that people need in their financial toolkit. But many

Income, Expenses and Budget module Trainer s introduction The skills to control your personal income, expenses and budget are the most basic tools that people need in their financial toolkit. But many

Financial Statements

Financial Statements The financial information forms the basis of financial planning, analysis & decision making for an organization or an individual. Financial information is needed to predict, compare

Financial Statements The financial information forms the basis of financial planning, analysis & decision making for an organization or an individual. Financial information is needed to predict, compare

Susan & David Example

Personal Financial Analysis for Susan & David Example Asset Advisors Example, LLC A Registered Investment Advisor 2430 NW Professional Drive Corvallis, OR 97330 877-421-9815 www.moneytree.com IMPORTANT:

Personal Financial Analysis for Susan & David Example Asset Advisors Example, LLC A Registered Investment Advisor 2430 NW Professional Drive Corvallis, OR 97330 877-421-9815 www.moneytree.com IMPORTANT:

Current liabilities - Obligations that are due within one year. Obligations due beyond that period of time are classified as long-term liabilities.

Accounting Fundamentals Lesson 8 8.0 Liabilities Current liabilities - Obligations that are due within one year. Obligations due beyond that period of time are classified as long-term liabilities. Current

Accounting Fundamentals Lesson 8 8.0 Liabilities Current liabilities - Obligations that are due within one year. Obligations due beyond that period of time are classified as long-term liabilities. Current

FCHD 3350: Family Finance Summer 2005 Syllabus

FCHD 3350: Family Finance Summer 2005 Syllabus Instructor: Alena Johnson 3 credit hours TEXTS: Garman, E. T. & Forgue, R. E. (2006) Personal Finance Chilton, D. (1998) The Wealthy Barber (3rd edition)

FCHD 3350: Family Finance Summer 2005 Syllabus Instructor: Alena Johnson 3 credit hours TEXTS: Garman, E. T. & Forgue, R. E. (2006) Personal Finance Chilton, D. (1998) The Wealthy Barber (3rd edition)

Tax Payments Checklist (Year to Date Payroll)

") Tax Payments Checklist (Year to Date Payroll) Important: Before you enter tax payments in the Enter Payroll Tax Payments window: Enter all your year to date paychecks in the Enter Paychecks window. Print

Tax Payments Checklist (Year to Date Payroll) Important: Before you enter tax payments in the Enter Payroll Tax Payments window: Enter all your year to date paychecks in the Enter Paychecks window. Print

How To Setup & Use Insight Salon & Spa Software Payroll - Australia

How To Setup & Use Insight Salon & Spa Software Payroll - Australia Introduction The Insight Salon & Spa Software Payroll system is one of the most powerful sections of Insight. It can save you a lot of

How To Setup & Use Insight Salon & Spa Software Payroll - Australia Introduction The Insight Salon & Spa Software Payroll system is one of the most powerful sections of Insight. It can save you a lot of

Understanding Financial Statements. For Your Business

Understanding Financial Statements For Your Business Disclaimer The information provided is for informational purposes only, does not constitute legal advice or create an attorney-client relationship,

Understanding Financial Statements For Your Business Disclaimer The information provided is for informational purposes only, does not constitute legal advice or create an attorney-client relationship,