Business Cycles, Theory and Empirical Applications

|

|

|

- Gwendolyn Jenkins

- 8 years ago

- Views:

Transcription

1 Business Cycles, Theory and Empirical Applications Seminar Presentation Country of interest France Jan Krzyzanowski June 9, 2012

2 Table of Contents Business Cycle Analysis Data Quantitative Analysis Stochastic RBC Model TFP Calibration and Simulation Local RBC Model

3 Business Cycle Analysis Data Quantitative Analysis

4 Data Capital Data (1) Problem: no data from national sources on quarterly basis Own estimates on Capital Stock based on methods of the Kiel Institute for World Economy

5 Data Capital Data (2) Initial capital stock add Capital Formations on existing capital stock take into account of depretiation rates take into account dierences in sectors Private Sector Govermental Sector

6 Data Capital Data (3) Procedure: Annual depretiation: δ j t = δ j min [( δ j max δ j min ) 1 50 ] t Quarterly depretiation: (1 δ j t quarterly )4 = 1 δ j t annual Capital Stock in t+1: K j t+1 = ( 1 δ quartely ) Kt + I j t Total Capital Stock: K total t+1 priv res priv nonres = Kt+1 + Kt+1 + K gov t+1

7 Data Employment Data Quarterly Data taken from OECD database - no problems Output Data Quarterly Data taken from OECD database - no problems Private Consumption Data Quarterly Data taken from OECD database - no problems Private Investment Data Quarterly Data taken from OECD database - no problems

8 Quantitative Analysis Extraction of Cyclical Fluctuations: take logs of data, i.e. y t HP-lter the data: min (τt) T t=1 T t=1 (y t τ t ) 2 + λ T 1 [ t=2 (τt+1 τ t ) (τ t τ t 1 ) ]2 = min (τt) T t=1 T t=1 (y t τ t ) 2 + λ T 1 t=2 ( τ,t+1 τ,t ) 2 c t = y t τ t

(τ t τ t 1 ) ]2 = min (τt) T t=1 T t=1 (y t τ")

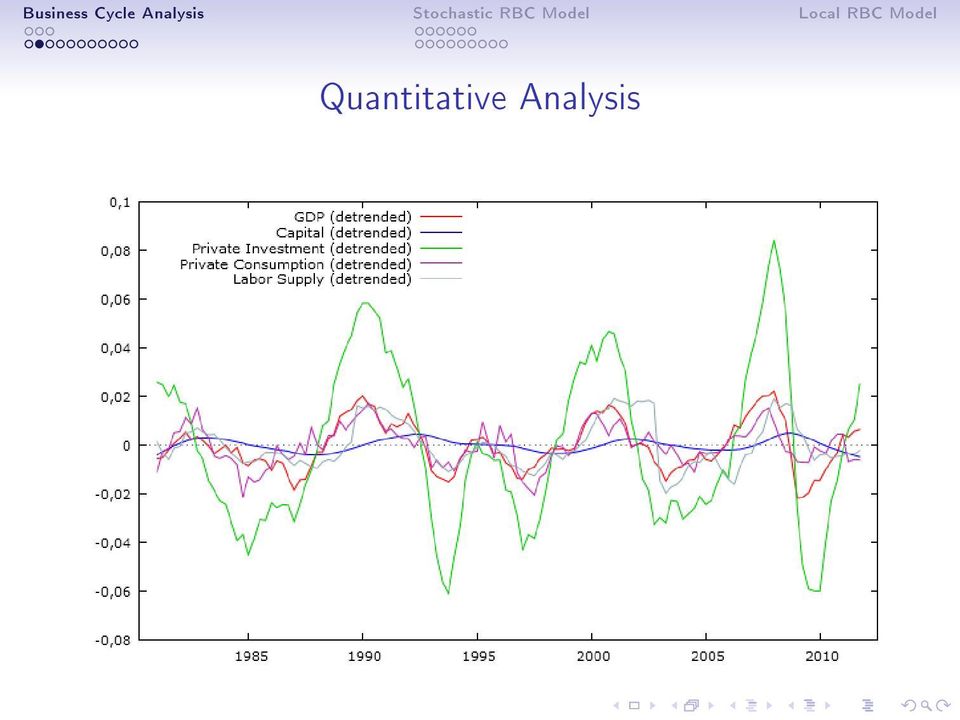

9 Quantitative Analysis

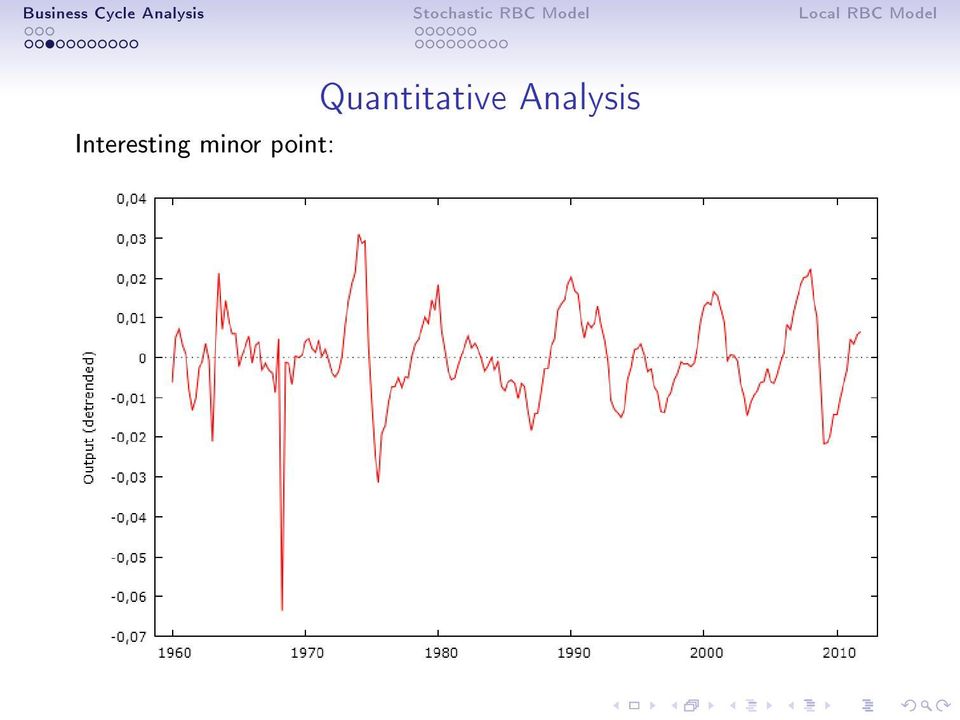

10 Interesting minor point: Quantitative Analysis

11 Quantitative Analysis Standard Deviations Variable Std.Dev Rel. Std.Dev Output Employment Priv. Consumption Priv. Investment Capital Table : Standard Deviations

12 Quantitative Analysis

13 Quantitative Analysis Leads and Lags Variable t 4 t 3 t 2 t 1 t 0 t 1 t 2 t 3 t 4 Output Employment Priv. Consumption Priv. Investment Capital Table : Lead and Lag Analysis

14 Output and Private Consumption Quantitative Analysis

15 Output and Private Investment Quantitative Analysis

16 Output and Capital Quantitative Analysis

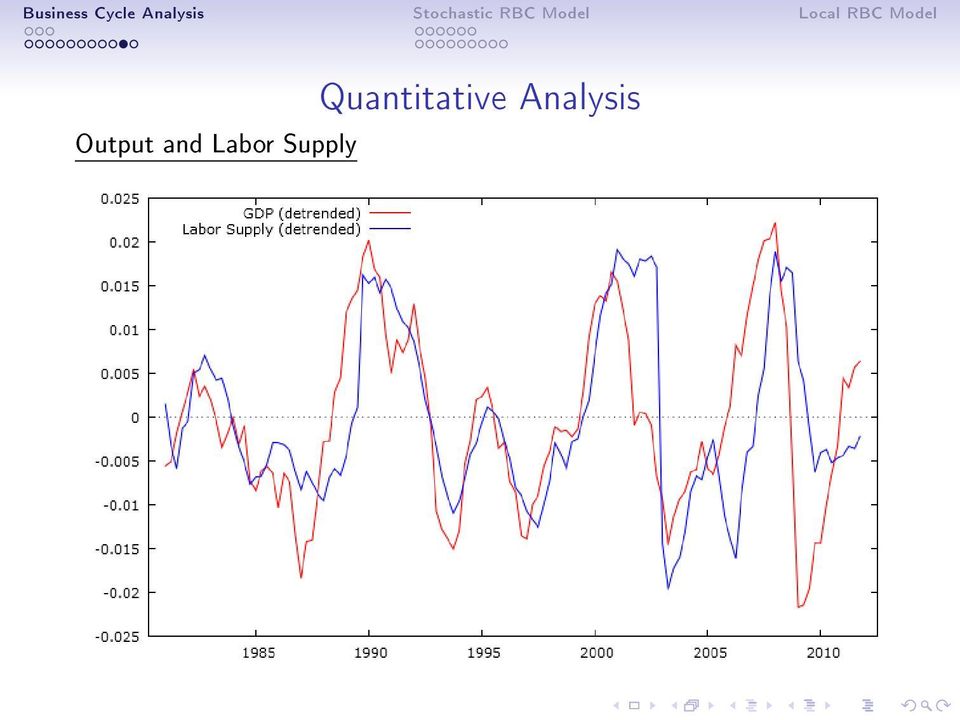

17 Output and Labor Supply Quantitative Analysis

18 Quantitative Analysis Autocorrelation Analysis Variable t 1 t 2 t 3 t 4 Output Employment Priv. Consumption Priv. Investment Capital Table : Coecient of Autocorrelation

19 Stochastic RBC Model TFP Calibration and Simulation

20 TFP 2 Production Functions: Y t = e At K t Y t = e At K t.36 N t.64 Solow Residuals A t = log ( A t = log ( Y t K t ) Y t K.36 t N.64 t ) linear regression of A t

Y t K.36 t N.")

21 TFP Linear Regressions: A t = t + u t ( ) (2.2443) A t = t + u t ( ) Negative relation between TFP and time in rst equation Positive relation between TFP and time in second equation

22 TFP Hypothesis Test for γ First production function: H 0 : γ = 0 against H 1 : γ < 0 we obtain the p-value=1 Φ( 1.13 ) = Second production function: H 0 : γ = 0 against H 1 : γ > 0 we obtain the p-value=1 Φ(12.14) 0 Reason?

23 TFP Reason Dierent production functions First production function: A t+1 Yt+1 Y t Kt+1 K t Second production function: A t+1 Yt+1 Y t 0.36 Kt+1 K t 0.64 Nt+1 N t

24 TFP Autoregressive Process First production function: Â t = ( ) Ât 1 + ɛ t ( ) Second production function: Â t = ( ) Ât 1 + ɛ t ( ) Testing Null H 0 : ρ A = 0 against H 1 > 0 for both cases gives a p-value 0

25 Calibration and Simulation Calibration 2 calibrations based on dierent assumptions concerning steady state same stochastic RBC model Simulation K t+1 = β ( (1 δ) K t + θ exp(ât)k t ) I t = βk t ( β 1 β + δ δβ β C t = θ exp(ât)k t I t Y t = θ exp(ât)k t ) + θ exp(ât)

26 Simulation Cases 1.TFP estimation based on Y t (K t, A t ) Calibration(β, δ, θ) = (0.99, 0.025, 0.035) 2.TFP estimation based on Y t (K t, A t, N t ) Calibration(β, δ, θ) = (0.99, 0.025, 0.035) 3.TFP estimation based on Y t (K t, A t ) Calibration(β, δ, θ) = (0.99, 0.073, 1 12 ) 4.TFP estimation based on Y t (K t, A t, N t ) Calibration(β, δ, θ) = (0.99, 0.073, 1 12 )

27 Results Conditional on the calibration: Case 4 performed better than case 3 Case 2 performed better than case 1 Dued to dierent AR(1) process on detrended TFP Now: analyse dierent calibration performances

28 Comparison: Standard Deviations Variable Std.Dev Rel. Std.Dev Output Priv. Consumption Priv. Investment Capital Table : Standard Deviations Real Data Variable Std.Dev Rel. Std.Dev Output Priv. Consumption Priv. Investment Capital Table : Standard Deviations Case 2 Variable Std.Dev Rel. Std.Dev Output Priv. Consumption Priv. Investment Capital Table : Standard Deviations Case 4

29 Comparison: Standard Deviations Reason for dierent performance of cases? Idea dierent calibration of steady state conditional on same calibration: dierent AR(1) process on TFP Generate more or dierent random shocks two new cases: Case 4a four random shocks (±σ epsilon and ± 1.5 σ epsilon ) with probability 0.25 Case 4b higher random shocks (±2 σ epsilon ) with probability 0.5

30 Comparison: Standard Deviations Variable Std.Dev Rel. Std.Dev Output Priv. Consumption Priv. Investment Capital Table : Standard Deviations Real Data Variable Std.Dev Rel. Std.Dev Output Priv. Consumption Priv. Investment Capital Table : Standard Deviations Case 4a Variable Std.Dev Rel. Std.Dev Output Priv. Consumption Priv. Investment Capital Table : Standard Deviations Case 4b

31 Comparison: Leads and Lags Variable t 4 t 3 t 2 t 1 t 0 t 1 t 2 t 3 t 4 Output Priv. Consumption Priv. Investment Capital Table : Lead and Lag Analysis Real Data Variable t 4 t 3 t 2 t 1 t 0 t 1 t 2 t 3 t 4 Output Priv. Consumption Priv. Investment Capital Table : Lead and Lag Analysis Case 2 Variable t 4 t 3 t 2 t 1 t 0 t 1 t 2 t 3 t 4 Output Priv. Consumption Priv. Investment Capital Table : Lead and Lag Analysis Case 4

32 Comparison: Autocorrelation Variable t 1 t 2 t 3 t 4 Output Priv. Cons Priv. Inv Capital Table : Coe. of Autocorr. Real Data Variable t 1 t 2 t 3 t 4 Output Priv. Cons Priv. Inv Capital Table : Coe. of Autocorr. Case 2 Variable t 1 t 2 t 3 t 4 Output Priv. Cons Priv. Inv Capital Table : Coe. of Autocorr. Case 4

33 Sources for Improvement calibration of the steady state dierent series of random shocks cut initial observations of the simulated data of the RBC model more realistic assumptions concerning depretiation rates more realistic assumptions on production function include labor take into account diminishing marginal product of capital

34 Local RBC Model Procedure dierent assumption on production function Solve problem by optimization of log-linearized FOC Taylor Approximation Including growth in Steady State based on calibration by Campbell (quite the same as in Ex. 2) Solve the system Implement TFP shocks view summary statistics

35 Local RBC model System a t+1 = ρ a t + ɛ t+1 k t+1 = (b kk + b kc η ck ) k t + (b ka + b kc η ca ) a t c t = η ck k t + η ca a t y t = a t k t i t = Y I y t C I c t

36 Comparison: Standard Deviations Variable Std.Dev Rel. Std.Dev Output Priv. Consumption Priv. Investment Capital Table : Standard Deviations Real Data Variable Std.Dev Rel. Std.Dev Output Priv. Consumption Priv. Investment Capital Table : Standard Deviations Case 4 Variable Std.Dev Rel. Std.Dev Output Priv. Consumption Priv. Investment Capital Table : Standard Deviations Local RBC

37 Comparison: Leads and Lags Variable t 4 t 3 t 2 t 1 t 0 t 1 t 2 t 3 t 4 Output Priv. Consumption Priv. Investment Capital Table : Lead and Lag Analysis Real Data Variable t 4 t 3 t 2 t 1 t 0 t 1 t 2 t 3 t 4 Output Priv. Consumption Priv. Investment Capital Table : Lead and Lag Analysis Case 4 Variable t 4 t 3 t 2 t 1 t 0 t 1 t 2 t 3 t 4 Output Priv. Consumption Priv. Investment Capital Table : Lead and Lag Analysis Local RBC

38 Comparison: Autocorrelation Variable t 1 t 2 t 3 t 4 Output Priv. Cons Priv. Inv Capital Table : Coe. of Autocorr. Real Data Variable t 1 t 2 t 3 t 4 Output Priv. Cons Priv. Inv Capital Table : Coe. of Autocorr. Case 4 Variable t 1 t 2 t 3 t 4 Output Priv. Cons Priv. Inv Capital Table : Coe. of Autocorr. Local RBC

39 Summary and Criticism on RBC models Performance of RBC models improve with better assumptions on production function impressive results concerning analysed statistical moments BUT: what is the intuition behind TFP shocks? assumptions on depretiation rates are unrealistic no prices were taken into account no foreign markets are included

VI. Real Business Cycles Models

VI. Real Business Cycles Models Introduction Business cycle research studies the causes and consequences of the recurrent expansions and contractions in aggregate economic activity that occur in most industrialized

VI. Real Business Cycles Models Introduction Business cycle research studies the causes and consequences of the recurrent expansions and contractions in aggregate economic activity that occur in most industrialized

Real Business Cycle Models

Real Business Cycle Models Lecture 2 Nicola Viegi April 2015 Basic RBC Model Claim: Stochastic General Equlibrium Model Is Enough to Explain The Business cycle Behaviour of the Economy Money is of little

Real Business Cycle Models Lecture 2 Nicola Viegi April 2015 Basic RBC Model Claim: Stochastic General Equlibrium Model Is Enough to Explain The Business cycle Behaviour of the Economy Money is of little

Lecture 14 More on Real Business Cycles. Noah Williams

Lecture 14 More on Real Business Cycles Noah Williams University of Wisconsin - Madison Economics 312 Optimality Conditions Euler equation under uncertainty: u C (C t, 1 N t) = βe t [u C (C t+1, 1 N t+1)

Lecture 14 More on Real Business Cycles Noah Williams University of Wisconsin - Madison Economics 312 Optimality Conditions Euler equation under uncertainty: u C (C t, 1 N t) = βe t [u C (C t+1, 1 N t+1)

Topic 5: Stochastic Growth and Real Business Cycles

Topic 5: Stochastic Growth and Real Business Cycles Yulei Luo SEF of HKU October 1, 2015 Luo, Y. (SEF of HKU) Macro Theory October 1, 2015 1 / 45 Lag Operators The lag operator (L) is de ned as Similar

Topic 5: Stochastic Growth and Real Business Cycles Yulei Luo SEF of HKU October 1, 2015 Luo, Y. (SEF of HKU) Macro Theory October 1, 2015 1 / 45 Lag Operators The lag operator (L) is de ned as Similar

The RBC methodology also comes down to two principles:

Chapter 5 Real business cycles 5.1 Real business cycles The most well known paper in the Real Business Cycles (RBC) literature is Kydland and Prescott (1982). That paper introduces both a specific theory

Chapter 5 Real business cycles 5.1 Real business cycles The most well known paper in the Real Business Cycles (RBC) literature is Kydland and Prescott (1982). That paper introduces both a specific theory

Real Business Cycle Models

Phd Macro, 2007 (Karl Whelan) 1 Real Business Cycle Models The Real Business Cycle (RBC) model introduced in a famous 1982 paper by Finn Kydland and Edward Prescott is the original DSGE model. 1 The early

Phd Macro, 2007 (Karl Whelan) 1 Real Business Cycle Models The Real Business Cycle (RBC) model introduced in a famous 1982 paper by Finn Kydland and Edward Prescott is the original DSGE model. 1 The early

REAL BUSINESS CYCLE THEORY METHODOLOGY AND TOOLS

Jakub Gazda 42 Jakub Gazda, Real Business Cycle Theory Methodology and Tools, Economics & Sociology, Vol. 3, No 1, 2010, pp. 42-48. Jakub Gazda Department of Microeconomics Poznan University of Economics

Jakub Gazda 42 Jakub Gazda, Real Business Cycle Theory Methodology and Tools, Economics & Sociology, Vol. 3, No 1, 2010, pp. 42-48. Jakub Gazda Department of Microeconomics Poznan University of Economics

Why Does Consumption Lead the Business Cycle?

Why Does Consumption Lead the Business Cycle? Yi Wen Department of Economics Cornell University, Ithaca, N.Y. yw57@cornell.edu Abstract Consumption in the US leads output at the business cycle frequency.

Why Does Consumption Lead the Business Cycle? Yi Wen Department of Economics Cornell University, Ithaca, N.Y. yw57@cornell.edu Abstract Consumption in the US leads output at the business cycle frequency.

Real Business Cycles. Federal Reserve Bank of Minneapolis Research Department Staff Report 370. February 2006. Ellen R. McGrattan

Federal Reserve Bank of Minneapolis Research Department Staff Report 370 February 2006 Real Business Cycles Ellen R. McGrattan Federal Reserve Bank of Minneapolis and University of Minnesota Abstract:

Federal Reserve Bank of Minneapolis Research Department Staff Report 370 February 2006 Real Business Cycles Ellen R. McGrattan Federal Reserve Bank of Minneapolis and University of Minnesota Abstract:

Real Business Cycle Theory

Real Business Cycle Theory Guido Ascari University of Pavia () Real Business Cycle Theory 1 / 50 Outline Introduction: Lucas methodological proposal The application to the analysis of business cycle uctuations:

Real Business Cycle Theory Guido Ascari University of Pavia () Real Business Cycle Theory 1 / 50 Outline Introduction: Lucas methodological proposal The application to the analysis of business cycle uctuations:

MA Advanced Macroeconomics: 7. The Real Business Cycle Model

MA Advanced Macroeconomics: 7. The Real Business Cycle Model Karl Whelan School of Economics, UCD Spring 2015 Karl Whelan (UCD) Real Business Cycles Spring 2015 1 / 38 Working Through A DSGE Model We have

MA Advanced Macroeconomics: 7. The Real Business Cycle Model Karl Whelan School of Economics, UCD Spring 2015 Karl Whelan (UCD) Real Business Cycles Spring 2015 1 / 38 Working Through A DSGE Model We have

2. Real Business Cycle Theory (June 25, 2013)

") Prof. Dr. Thomas Steger Advanced Macroeconomics II Lecture SS 13 2. Real Business Cycle Theory (June 25, 2013) Introduction Simplistic RBC Model Simple stochastic growth model Baseline RBC model Introduction

Prof. Dr. Thomas Steger Advanced Macroeconomics II Lecture SS 13 2. Real Business Cycle Theory (June 25, 2013) Introduction Simplistic RBC Model Simple stochastic growth model Baseline RBC model Introduction

The Real Business Cycle Model

The Real Business Cycle Model Ester Faia Goethe University Frankfurt Nov 2015 Ester Faia (Goethe University Frankfurt) RBC Nov 2015 1 / 27 Introduction The RBC model explains the co-movements in the uctuations

The Real Business Cycle Model Ester Faia Goethe University Frankfurt Nov 2015 Ester Faia (Goethe University Frankfurt) RBC Nov 2015 1 / 27 Introduction The RBC model explains the co-movements in the uctuations

Econometric Modelling for Revenue Projections

Econometric Modelling for Revenue Projections Annex E 1. An econometric modelling exercise has been undertaken to calibrate the quantitative relationship between the five major items of government revenue

Econometric Modelling for Revenue Projections Annex E 1. An econometric modelling exercise has been undertaken to calibrate the quantitative relationship between the five major items of government revenue

Sales forecasting # 2

Sales forecasting # 2 Arthur Charpentier arthur.charpentier@univ-rennes1.fr 1 Agenda Qualitative and quantitative methods, a very general introduction Series decomposition Short versus long term forecasting

Sales forecasting # 2 Arthur Charpentier arthur.charpentier@univ-rennes1.fr 1 Agenda Qualitative and quantitative methods, a very general introduction Series decomposition Short versus long term forecasting

Real Business Cycle Theory. Marco Di Pietro Advanced () Monetary Economics and Policy 1 / 35

Monetary Economics and Policy 1 / 35") Real Business Cycle Theory Marco Di Pietro Advanced () Monetary Economics and Policy 1 / 35 Introduction to DSGE models Dynamic Stochastic General Equilibrium (DSGE) models have become the main tool for

Real Business Cycle Theory Marco Di Pietro Advanced () Monetary Economics and Policy 1 / 35 Introduction to DSGE models Dynamic Stochastic General Equilibrium (DSGE) models have become the main tool for

3 The Standard Real Business Cycle (RBC) Model. Optimal growth model + Labor decisions

Model. Optimal growth model + Labor decisions") Franck Portier TSE Macro II 29-21 Chapter 3 Real Business Cycles 36 3 The Standard Real Business Cycle (RBC) Model Perfectly competitive economy Optimal growth model + Labor decisions 2 types of agents

Franck Portier TSE Macro II 29-21 Chapter 3 Real Business Cycles 36 3 The Standard Real Business Cycle (RBC) Model Perfectly competitive economy Optimal growth model + Labor decisions 2 types of agents

16 : Demand Forecasting

16 : Demand Forecasting 1 Session Outline Demand Forecasting Subjective methods can be used only when past data is not available. When past data is available, it is advisable that firms should use statistical

16 : Demand Forecasting 1 Session Outline Demand Forecasting Subjective methods can be used only when past data is not available. When past data is available, it is advisable that firms should use statistical

Graduate Macroeconomics 2

Graduate Macroeconomics 2 Lecture 1 - Introduction to Real Business Cycles Zsófia L. Bárány Sciences Po 2014 January About the course I. 2-hour lecture every week, Tuesdays from 10:15-12:15 2 big topics

Graduate Macroeconomics 2 Lecture 1 - Introduction to Real Business Cycles Zsófia L. Bárány Sciences Po 2014 January About the course I. 2-hour lecture every week, Tuesdays from 10:15-12:15 2 big topics

The Real Business Cycle model

The Real Business Cycle model Spring 2013 1 Historical introduction Modern business cycle theory really got started with Great Depression Keynes: The General Theory of Employment, Interest and Money Keynesian

The Real Business Cycle model Spring 2013 1 Historical introduction Modern business cycle theory really got started with Great Depression Keynes: The General Theory of Employment, Interest and Money Keynesian

Advanced Macroeconomics (2)

") Advanced Macroeconomics (2) Real-Business-Cycle Theory Alessio Moneta Institute of Economics Scuola Superiore Sant Anna, Pisa amoneta@sssup.it March-April 2015 LM in Economics Scuola Superiore Sant Anna

Advanced Macroeconomics (2) Real-Business-Cycle Theory Alessio Moneta Institute of Economics Scuola Superiore Sant Anna, Pisa amoneta@sssup.it March-April 2015 LM in Economics Scuola Superiore Sant Anna

A Review of the Literature of Real Business Cycle theory. By Student E XXXXXXX

A Review of the Literature of Real Business Cycle theory By Student E XXXXXXX Abstract: The following paper reviews five articles concerning Real Business Cycle theory. First, the review compares the various

A Review of the Literature of Real Business Cycle theory By Student E XXXXXXX Abstract: The following paper reviews five articles concerning Real Business Cycle theory. First, the review compares the various

Macroeconomic Effects of Financial Shocks Online Appendix

Macroeconomic Effects of Financial Shocks Online Appendix By Urban Jermann and Vincenzo Quadrini Data sources Financial data is from the Flow of Funds Accounts of the Federal Reserve Board. We report the

Macroeconomic Effects of Financial Shocks Online Appendix By Urban Jermann and Vincenzo Quadrini Data sources Financial data is from the Flow of Funds Accounts of the Federal Reserve Board. We report the

Real Business Cycle Theory

Chapter 4 Real Business Cycle Theory This section of the textbook focuses on explaining the behavior of the business cycle. The terms business cycle, short-run macroeconomics, and economic fluctuations

Chapter 4 Real Business Cycle Theory This section of the textbook focuses on explaining the behavior of the business cycle. The terms business cycle, short-run macroeconomics, and economic fluctuations

Sovereign Defaults. Iskander Karibzhanov. October 14, 2014

Sovereign Defaults Iskander Karibzhanov October 14, 214 1 Motivation Two recent papers advance frontiers of sovereign default modeling. First, Aguiar and Gopinath (26) highlight the importance of fluctuations

Sovereign Defaults Iskander Karibzhanov October 14, 214 1 Motivation Two recent papers advance frontiers of sovereign default modeling. First, Aguiar and Gopinath (26) highlight the importance of fluctuations

Chapter 1. Vector autoregressions. 1.1 VARs and the identi cation problem

Chapter Vector autoregressions We begin by taking a look at the data of macroeconomics. A way to summarize the dynamics of macroeconomic data is to make use of vector autoregressions. VAR models have become

Chapter Vector autoregressions We begin by taking a look at the data of macroeconomics. A way to summarize the dynamics of macroeconomic data is to make use of vector autoregressions. VAR models have become

GDP: The market value of final goods and services, newly produced WITHIN a nation during a fixed period.

GDP: The market value of final goods and services, newly produced WITHIN a nation during a fixed period. Value added: Value of output (market value) purchased inputs (e.g. intermediate goods) GDP is a

GDP: The market value of final goods and services, newly produced WITHIN a nation during a fixed period. Value added: Value of output (market value) purchased inputs (e.g. intermediate goods) GDP is a

Towards a Structuralist Interpretation of Saving, Investment and Current Account in Turkey

Towards a Structuralist Interpretation of Saving, Investment and Current Account in Turkey MURAT ÜNGÖR Central Bank of the Republic of Turkey http://www.muratungor.com/ April 2012 We live in the age of

Towards a Structuralist Interpretation of Saving, Investment and Current Account in Turkey MURAT ÜNGÖR Central Bank of the Republic of Turkey http://www.muratungor.com/ April 2012 We live in the age of

4. Simple regression. QBUS6840 Predictive Analytics. https://www.otexts.org/fpp/4

4. Simple regression QBUS6840 Predictive Analytics https://www.otexts.org/fpp/4 Outline The simple linear model Least squares estimation Forecasting with regression Non-linear functional forms Regression

4. Simple regression QBUS6840 Predictive Analytics https://www.otexts.org/fpp/4 Outline The simple linear model Least squares estimation Forecasting with regression Non-linear functional forms Regression

Optimization of technical trading strategies and the profitability in security markets

Economics Letters 59 (1998) 249 254 Optimization of technical trading strategies and the profitability in security markets Ramazan Gençay 1, * University of Windsor, Department of Economics, 401 Sunset,

Economics Letters 59 (1998) 249 254 Optimization of technical trading strategies and the profitability in security markets Ramazan Gençay 1, * University of Windsor, Department of Economics, 401 Sunset,

Predicting Indian GDP. And its relation with FMCG Sales

Predicting Indian GDP And its relation with FMCG Sales GDP A Broad Measure of Economic Activity Definition The monetary value of all the finished goods and services produced within a country's borders

Predicting Indian GDP And its relation with FMCG Sales GDP A Broad Measure of Economic Activity Definition The monetary value of all the finished goods and services produced within a country's borders

PITFALLS IN TIME SERIES ANALYSIS. Cliff Hurvich Stern School, NYU

PITFALLS IN TIME SERIES ANALYSIS Cliff Hurvich Stern School, NYU The t -Test If x 1,..., x n are independent and identically distributed with mean 0, and n is not too small, then t = x 0 s n has a standard

PITFALLS IN TIME SERIES ANALYSIS Cliff Hurvich Stern School, NYU The t -Test If x 1,..., x n are independent and identically distributed with mean 0, and n is not too small, then t = x 0 s n has a standard

Current Accounts in Open Economies Obstfeld and Rogoff, Chapter 2

Current Accounts in Open Economies Obstfeld and Rogoff, Chapter 2 1 Consumption with many periods 1.1 Finite horizon of T Optimization problem maximize U t = u (c t ) + β (c t+1 ) + β 2 u (c t+2 ) +...

Current Accounts in Open Economies Obstfeld and Rogoff, Chapter 2 1 Consumption with many periods 1.1 Finite horizon of T Optimization problem maximize U t = u (c t ) + β (c t+1 ) + β 2 u (c t+2 ) +...

Advanced Macroeconomics (ECON 402) Lecture 8 Real Business Cycle Theory

Lecture 8 Real Business Cycle Theory") Advanced Macroeconomics (ECON 402) Lecture 8 Real Business Cycle Theory Teng Wah Leo Some Stylized Facts Regarding Economic Fluctuations Having now understood various growth models, we will now delve into

Advanced Macroeconomics (ECON 402) Lecture 8 Real Business Cycle Theory Teng Wah Leo Some Stylized Facts Regarding Economic Fluctuations Having now understood various growth models, we will now delve into

19 : Theory of Production

19 : Theory of Production 1 Recap from last session Long Run Production Analysis Return to Scale Isoquants, Isocost Choice of input combination Expansion path Economic Region of Production Session Outline

19 : Theory of Production 1 Recap from last session Long Run Production Analysis Return to Scale Isoquants, Isocost Choice of input combination Expansion path Economic Region of Production Session Outline

What Drives International Equity Correlations? Volatility or Market Direction? *

Working Paper 9-41 Departamento de Economía Economic Series (22) Universidad Carlos III de Madrid June 29 Calle Madrid, 126 2893 Getafe (Spain) Fax (34) 916249875 What Drives International Equity Correlations?

Working Paper 9-41 Departamento de Economía Economic Series (22) Universidad Carlos III de Madrid June 29 Calle Madrid, 126 2893 Getafe (Spain) Fax (34) 916249875 What Drives International Equity Correlations?

Conditional guidance as a response to supply uncertainty

1 Conditional guidance as a response to supply uncertainty Appendix to the speech given by Ben Broadbent, External Member of the Monetary Policy Committee, Bank of England At the London Business School,

1 Conditional guidance as a response to supply uncertainty Appendix to the speech given by Ben Broadbent, External Member of the Monetary Policy Committee, Bank of England At the London Business School,

Integrated Resource Plan

Integrated Resource Plan March 19, 2004 PREPARED FOR KAUA I ISLAND UTILITY COOPERATIVE LCG Consulting 4962 El Camino Real, Suite 112 Los Altos, CA 94022 650-962-9670 1 IRP 1 ELECTRIC LOAD FORECASTING 1.1

Integrated Resource Plan March 19, 2004 PREPARED FOR KAUA I ISLAND UTILITY COOPERATIVE LCG Consulting 4962 El Camino Real, Suite 112 Los Altos, CA 94022 650-962-9670 1 IRP 1 ELECTRIC LOAD FORECASTING 1.1

Preparation course MSc Business&Econonomics: Economic Growth

Preparation course MSc Business&Econonomics: Economic Growth Tom-Reiel Heggedal Economics Department 2014 TRH (Institute) Solow model 2014 1 / 27 Theory and models Objective of this lecture: learn Solow

Preparation course MSc Business&Econonomics: Economic Growth Tom-Reiel Heggedal Economics Department 2014 TRH (Institute) Solow model 2014 1 / 27 Theory and models Objective of this lecture: learn Solow

1 National Income and Product Accounts

Espen Henriksen econ249 UCSB 1 National Income and Product Accounts 11 Gross Domestic Product (GDP) Can be measured in three different but equivalent ways: 1 Production Approach 2 Expenditure Approach

Espen Henriksen econ249 UCSB 1 National Income and Product Accounts 11 Gross Domestic Product (GDP) Can be measured in three different but equivalent ways: 1 Production Approach 2 Expenditure Approach

Week TSX Index 1 8480 2 8470 3 8475 4 8510 5 8500 6 8480

1) The S & P/TSX Composite Index is based on common stock prices of a group of Canadian stocks. The weekly close level of the TSX for 6 weeks are shown: Week TSX Index 1 8480 2 8470 3 8475 4 8510 5 8500

1) The S & P/TSX Composite Index is based on common stock prices of a group of Canadian stocks. The weekly close level of the TSX for 6 weeks are shown: Week TSX Index 1 8480 2 8470 3 8475 4 8510 5 8500

Chapter 9: Univariate Time Series Analysis

Chapter 9: Univariate Time Series Analysis In the last chapter we discussed models with only lags of explanatory variables. These can be misleading if: 1. The dependent variable Y t depends on lags of

Chapter 9: Univariate Time Series Analysis In the last chapter we discussed models with only lags of explanatory variables. These can be misleading if: 1. The dependent variable Y t depends on lags of

The VAR models discussed so fare are appropriate for modeling I(0) data, like asset returns or growth rates of macroeconomic time series.

data, like asset returns or growth rates of macroeconomic time series.") Cointegration The VAR models discussed so fare are appropriate for modeling I(0) data, like asset returns or growth rates of macroeconomic time series. Economic theory, however, often implies equilibrium

Cointegration The VAR models discussed so fare are appropriate for modeling I(0) data, like asset returns or growth rates of macroeconomic time series. Economic theory, however, often implies equilibrium

Financial Shocks, Cyclicality of Labor Productivity and the Great Moderation

Financial Shocks, Cyclicality of Labor Productivity and the Great Moderation October 28, 2014 Abstract The nature of the business cycle has sharply changed since the onset of great moderation with decline

Financial Shocks, Cyclicality of Labor Productivity and the Great Moderation October 28, 2014 Abstract The nature of the business cycle has sharply changed since the onset of great moderation with decline

IT Productivity and Aggregation using Income Accounting

IT Productivity and Aggregation using Income Accounting Dennis Kundisch, Neeraj Mittal and Barrie R. Nault 1 WISE 2009 Research-in-Progress Submission: September 15, 2009 Introduction We examine the relationship

IT Productivity and Aggregation using Income Accounting Dennis Kundisch, Neeraj Mittal and Barrie R. Nault 1 WISE 2009 Research-in-Progress Submission: September 15, 2009 Introduction We examine the relationship

The Japanese Saving Rate

The Japanese Saving Rate By KAIJI CHEN, AYŞE İMROHOROĞLU, AND SELAHATTIN İMROHOROĞLU* * Chen: Department of Economics, University of Oslo, Blindern, N-0317 Oslo, Norway (e-mail: kaijic@econ. uio.no); A.

The Japanese Saving Rate By KAIJI CHEN, AYŞE İMROHOROĞLU, AND SELAHATTIN İMROHOROĞLU* * Chen: Department of Economics, University of Oslo, Blindern, N-0317 Oslo, Norway (e-mail: kaijic@econ. uio.no); A.

Real Business Cycle Theory

Real Business Cycle Theory Barbara Annicchiarico Università degli Studi di Roma "Tor Vergata" April 202 General Features I Theory of uctuations (persistence, output does not show a strong tendency to return

Real Business Cycle Theory Barbara Annicchiarico Università degli Studi di Roma "Tor Vergata" April 202 General Features I Theory of uctuations (persistence, output does not show a strong tendency to return

Some useful concepts in univariate time series analysis

Some useful concepts in univariate time series analysis Autoregressive moving average models Autocorrelation functions Model Estimation Diagnostic measure Model selection Forecasting Assumptions: 1. Non-seasonal

Some useful concepts in univariate time series analysis Autoregressive moving average models Autocorrelation functions Model Estimation Diagnostic measure Model selection Forecasting Assumptions: 1. Non-seasonal

Modelling Electricity Spot Prices A Regime-Switching Approach

Modelling Electricity Spot Prices A Regime-Switching Approach Dr. Gero Schindlmayr EnBW Trading GmbH Financial Modelling Workshop Ulm September 2005 Energie braucht Impulse Agenda Model Overview Daily

Modelling Electricity Spot Prices A Regime-Switching Approach Dr. Gero Schindlmayr EnBW Trading GmbH Financial Modelling Workshop Ulm September 2005 Energie braucht Impulse Agenda Model Overview Daily

New Estimates of the Fraction of People Who Consume Current Income

New Estimates of the Fraction of People Who Consume Current Income Mark Senia Joe McGarrity Abstract: Using data from 1953-1986, Campbell and Mankiw (1989) estimate the fraction of consumers who consume

New Estimates of the Fraction of People Who Consume Current Income Mark Senia Joe McGarrity Abstract: Using data from 1953-1986, Campbell and Mankiw (1989) estimate the fraction of consumers who consume

2. What is the general linear model to be used to model linear trend? (Write out the model) = + + + or

= + + + or") Simple and Multiple Regression Analysis Example: Explore the relationships among Month, Adv.$ and Sales $: 1. Prepare a scatter plot of these data. The scatter plots for Adv.$ versus Sales, and Month versus

Simple and Multiple Regression Analysis Example: Explore the relationships among Month, Adv.$ and Sales $: 1. Prepare a scatter plot of these data. The scatter plots for Adv.$ versus Sales, and Month versus

The real business cycle theory

Chapter 29 The real business cycle theory Since the middle of the 1970s two quite different approaches to the explanation of business cycle fluctuations have been pursued. We may broadly classify them

Chapter 29 The real business cycle theory Since the middle of the 1970s two quite different approaches to the explanation of business cycle fluctuations have been pursued. We may broadly classify them

7 STOCHASTIC GROWTH MODELS AND REAL BUSINESS CYCLES

Economics 314 Coursebook, 2010 Jeffrey Parker 7 STOCHASTIC GROWTH MODELS AND REAL BUSINESS CYCLES Chapter 7 Contents A. Topics and Tools... 1 B. Walrasian vs. Keynesian Explanations of Business Cycles...

Economics 314 Coursebook, 2010 Jeffrey Parker 7 STOCHASTIC GROWTH MODELS AND REAL BUSINESS CYCLES Chapter 7 Contents A. Topics and Tools... 1 B. Walrasian vs. Keynesian Explanations of Business Cycles...

Threshold Autoregressive Models in Finance: A Comparative Approach

University of Wollongong Research Online Applied Statistics Education and Research Collaboration (ASEARC) - Conference Papers Faculty of Informatics 2011 Threshold Autoregressive Models in Finance: A Comparative

University of Wollongong Research Online Applied Statistics Education and Research Collaboration (ASEARC) - Conference Papers Faculty of Informatics 2011 Threshold Autoregressive Models in Finance: A Comparative

A STOCHASTIC DAILY MEAN TEMPERATURE MODEL FOR WEATHER DERIVATIVES

A STOCHASTIC DAILY MEAN TEMPERATURE MODEL FOR WEATHER DERIVATIVES Jeffrey Viel 1, 2, Thomas Connor 3 1 National Weather Center Research Experiences for Undergraduates Program and 2 Plymouth State University

A STOCHASTIC DAILY MEAN TEMPERATURE MODEL FOR WEATHER DERIVATIVES Jeffrey Viel 1, 2, Thomas Connor 3 1 National Weather Center Research Experiences for Undergraduates Program and 2 Plymouth State University

The Intertemporal Approach to the Current Account and Currency Crises

Darwin College Research Report DCRR-005 The Intertemporal Approach to the Current Account and Currency Crises Sergejs Saksonovs June 2006 Darwin College Cambridge University United Kingdom CB3 9EU www.dar.cam.ac.uk/dcrr

Darwin College Research Report DCRR-005 The Intertemporal Approach to the Current Account and Currency Crises Sergejs Saksonovs June 2006 Darwin College Cambridge University United Kingdom CB3 9EU www.dar.cam.ac.uk/dcrr

Topic 2. Incorporating Financial Frictions in DSGE Models

Topic 2 Incorporating Financial Frictions in DSGE Models Mark Gertler NYU April 2009 0 Overview Conventional Model with Perfect Capital Markets: 1. Arbitrage between return to capital and riskless rate

Topic 2 Incorporating Financial Frictions in DSGE Models Mark Gertler NYU April 2009 0 Overview Conventional Model with Perfect Capital Markets: 1. Arbitrage between return to capital and riskless rate

Forecasting the US Dollar / Euro Exchange rate Using ARMA Models

Forecasting the US Dollar / Euro Exchange rate Using ARMA Models LIUWEI (9906360) - 1 - ABSTRACT...3 1. INTRODUCTION...4 2. DATA ANALYSIS...5 2.1 Stationary estimation...5 2.2 Dickey-Fuller Test...6 3.

Forecasting the US Dollar / Euro Exchange rate Using ARMA Models LIUWEI (9906360) - 1 - ABSTRACT...3 1. INTRODUCTION...4 2. DATA ANALYSIS...5 2.1 Stationary estimation...5 2.2 Dickey-Fuller Test...6 3.

Simple Linear Regression Inference

Simple Linear Regression Inference 1 Inference requirements The Normality assumption of the stochastic term e is needed for inference even if it is not a OLS requirement. Therefore we have: Interpretation

Simple Linear Regression Inference 1 Inference requirements The Normality assumption of the stochastic term e is needed for inference even if it is not a OLS requirement. Therefore we have: Interpretation

Intermediate Macroeconomics: The Real Business Cycle Model

Intermediate Macroeconomics: The Real Business Cycle Model Eric Sims University of Notre Dame Fall 2012 1 Introduction Having developed an operational model of the economy, we want to ask ourselves the

Intermediate Macroeconomics: The Real Business Cycle Model Eric Sims University of Notre Dame Fall 2012 1 Introduction Having developed an operational model of the economy, we want to ask ourselves the

UNIVERSITY OF OSLO DEPARTMENT OF ECONOMICS

UNIVERSITY OF OSLO DEPARTMENT OF ECONOMICS Exam: ECON4310 Intertemporal macroeconomics Date of exam: Thursday, November 27, 2008 Grades are given: December 19, 2008 Time for exam: 09:00 a.m. 12:00 noon

UNIVERSITY OF OSLO DEPARTMENT OF ECONOMICS Exam: ECON4310 Intertemporal macroeconomics Date of exam: Thursday, November 27, 2008 Grades are given: December 19, 2008 Time for exam: 09:00 a.m. 12:00 noon

The Real Business Cycle Model for Lesotho

The Real Business Cycle Model for Lesotho Tanka Tlelima University of Cape Town, South Africa October 27, 29 Abstract This paper modi es Hansen s model of indivisible labour, to include labour exports,

The Real Business Cycle Model for Lesotho Tanka Tlelima University of Cape Town, South Africa October 27, 29 Abstract This paper modi es Hansen s model of indivisible labour, to include labour exports,

Random Walk Expectations and the Forward Discount Puzzle

Random Walk Expectations and the Forward Discount Puzzle Philippe Bacchetta and Eric van Wincoop* Two well-known, but seemingly contradictory, features of exchange rates are that they are close to a random

Random Walk Expectations and the Forward Discount Puzzle Philippe Bacchetta and Eric van Wincoop* Two well-known, but seemingly contradictory, features of exchange rates are that they are close to a random

Advanced Forecasting Techniques and Models: ARIMA

Advanced Forecasting Techniques and Models: ARIMA Short Examples Series using Risk Simulator For more information please visit: www.realoptionsvaluation.com or contact us at: admin@realoptionsvaluation.com

Advanced Forecasting Techniques and Models: ARIMA Short Examples Series using Risk Simulator For more information please visit: www.realoptionsvaluation.com or contact us at: admin@realoptionsvaluation.com

4. In the Solow model with technological progress, the steady state growth rate of total output is: A) 0. B) g. C) n. D) n + g.

0. B) g. C) n. D) n + g.") 1. The rate of labor augmenting technological progress (g) is the growth rate of: A) labor. B) the efficiency of labor. C) capital. D) output. 2. In the Solow growth model with population growth and technological

1. The rate of labor augmenting technological progress (g) is the growth rate of: A) labor. B) the efficiency of labor. C) capital. D) output. 2. In the Solow growth model with population growth and technological

Cash in advance model

Chapter 4 Cash in advance model 4.1 Motivation In this lecture we will look at ways of introducing money into a neoclassical model and how these methods can be developed in an effort to try and explain

Chapter 4 Cash in advance model 4.1 Motivation In this lecture we will look at ways of introducing money into a neoclassical model and how these methods can be developed in an effort to try and explain

Graduate Macro Theory II: Notes on Using Dynare

Graduate Macro Theory II: Notes on Using Dynare Eric Sims University of Notre Dame Spring 011 1 Introduction This document will present some simple examples of how to solve, simulate, and estimate DSGE

Graduate Macro Theory II: Notes on Using Dynare Eric Sims University of Notre Dame Spring 011 1 Introduction This document will present some simple examples of how to solve, simulate, and estimate DSGE

Forecasting of Economic Quantities using Fuzzy Autoregressive Model and Fuzzy Neural Network

Forecasting of Economic Quantities using Fuzzy Autoregressive Model and Fuzzy Neural Network Dušan Marček 1 Abstract Most models for the time series of stock prices have centered on autoregressive (AR)

Forecasting of Economic Quantities using Fuzzy Autoregressive Model and Fuzzy Neural Network Dušan Marček 1 Abstract Most models for the time series of stock prices have centered on autoregressive (AR)

A model to predict client s phone calls to Iberdrola Call Centre

A model to predict client s phone calls to Iberdrola Call Centre Participants: Cazallas Piqueras, Rosa Gil Franco, Dolores M Gouveia de Miranda, Vinicius Herrera de la Cruz, Jorge Inoñan Valdera, Danny

A model to predict client s phone calls to Iberdrola Call Centre Participants: Cazallas Piqueras, Rosa Gil Franco, Dolores M Gouveia de Miranda, Vinicius Herrera de la Cruz, Jorge Inoñan Valdera, Danny

Business Cycle Models - A Review of the Published Works Paper, Part 1

DEPARTMENT OF ECONOMICS WORKING PAPER SERIES 2008-02 McMASTER UNIVERSITY Department of Economics Kenneth Taylor Hall 426 1280 Main Street West Hamilton, Ontario, Canada L8S 4M4 http://www.mcmaster.ca/economics/

DEPARTMENT OF ECONOMICS WORKING PAPER SERIES 2008-02 McMASTER UNIVERSITY Department of Economics Kenneth Taylor Hall 426 1280 Main Street West Hamilton, Ontario, Canada L8S 4M4 http://www.mcmaster.ca/economics/

ECON20310 LECTURE SYNOPSIS REAL BUSINESS CYCLE

ECON20310 LECTURE SYNOPSIS REAL BUSINESS CYCLE YUAN TIAN This synopsis is designed merely for keep a record of the materials covered in lectures. Please refer to your own lecture notes for all proofs.

ECON20310 LECTURE SYNOPSIS REAL BUSINESS CYCLE YUAN TIAN This synopsis is designed merely for keep a record of the materials covered in lectures. Please refer to your own lecture notes for all proofs.

Section A. Index. Section A. Planning, Budgeting and Forecasting Section A.2 Forecasting techniques... 1. Page 1 of 11. EduPristine CMA - Part I

Index Section A. Planning, Budgeting and Forecasting Section A.2 Forecasting techniques... 1 EduPristine CMA - Part I Page 1 of 11 Section A. Planning, Budgeting and Forecasting Section A.2 Forecasting

Index Section A. Planning, Budgeting and Forecasting Section A.2 Forecasting techniques... 1 EduPristine CMA - Part I Page 1 of 11 Section A. Planning, Budgeting and Forecasting Section A.2 Forecasting

Deflation and the International Great Depression: A Productivity Puzzle

Federal Reserve Bank of Minneapolis Research Department Staff Report 356 February 2005 Deflation and the International Great Depression: A Productivity Puzzle Harold L. Cole University of California, Los

Federal Reserve Bank of Minneapolis Research Department Staff Report 356 February 2005 Deflation and the International Great Depression: A Productivity Puzzle Harold L. Cole University of California, Los

In ation Tax and In ation Subsidies: Working Capital in a Cash-in-advance model

In ation Tax and In ation Subsidies: Working Capital in a Cash-in-advance model George T. McCandless March 3, 006 Abstract This paper studies the nature of monetary policy with nancial intermediaries that

In ation Tax and In ation Subsidies: Working Capital in a Cash-in-advance model George T. McCandless March 3, 006 Abstract This paper studies the nature of monetary policy with nancial intermediaries that

Module 5: Multiple Regression Analysis

Using Statistical Data Using to Make Statistical Decisions: Data Multiple to Make Regression Decisions Analysis Page 1 Module 5: Multiple Regression Analysis Tom Ilvento, University of Delaware, College

Using Statistical Data Using to Make Statistical Decisions: Data Multiple to Make Regression Decisions Analysis Page 1 Module 5: Multiple Regression Analysis Tom Ilvento, University of Delaware, College

Why do emerging economies accumulate debt and reserves?

Why do emerging economies accumulate debt and reserves? Juliana Salomao June, 2013 University of Minnesota Abstract Reserve accumulation has the benet of decreasing external vulnerability but it comes

Why do emerging economies accumulate debt and reserves? Juliana Salomao June, 2013 University of Minnesota Abstract Reserve accumulation has the benet of decreasing external vulnerability but it comes

1 A simple two period model

A QUICK REVIEW TO INTERTEMPORAL MAXIMIZATION PROBLEMS 1 A simple two period model 1.1 The intertemporal problem The intertemporal consumption decision can be analyzed in a way very similar to an atemporal

A QUICK REVIEW TO INTERTEMPORAL MAXIMIZATION PROBLEMS 1 A simple two period model 1.1 The intertemporal problem The intertemporal consumption decision can be analyzed in a way very similar to an atemporal

Teaching modern general equilibrium macroeconomics to undergraduates: using the same t. advanced research. Gillman (Cardi Business School)

") Teaching modern general equilibrium macroeconomics to undergraduates: using the same theory required for advanced research Max Gillman Cardi Business School pments in Economics Education (DEE) Conference

Teaching modern general equilibrium macroeconomics to undergraduates: using the same theory required for advanced research Max Gillman Cardi Business School pments in Economics Education (DEE) Conference

Human Capital Risk, Contract Enforcement, and the Macroeconomy

Human Capital Risk, Contract Enforcement, and the Macroeconomy Tom Krebs University of Mannheim Moritz Kuhn University of Bonn Mark Wright UCLA and Chicago Fed General Issue: For many households (the young),

Human Capital Risk, Contract Enforcement, and the Macroeconomy Tom Krebs University of Mannheim Moritz Kuhn University of Bonn Mark Wright UCLA and Chicago Fed General Issue: For many households (the young),

A Primer on Forecasting Business Performance

A Primer on Forecasting Business Performance There are two common approaches to forecasting: qualitative and quantitative. Qualitative forecasting methods are important when historical data is not available.

A Primer on Forecasting Business Performance There are two common approaches to forecasting: qualitative and quantitative. Qualitative forecasting methods are important when historical data is not available.

Learning objectives. The Theory of Real Business Cycles

Learning objectives This chapter presents an overview of recent work in two areas: Real Business Cycle theory New Keynesian economics Advances in Business Cycle Theory slide 1 The Theory of Real Business

Learning objectives This chapter presents an overview of recent work in two areas: Real Business Cycle theory New Keynesian economics Advances in Business Cycle Theory slide 1 The Theory of Real Business

Modeling a Foreign Exchange Rate

Modeling a foreign exchange rate using moving average of Yen-Dollar market data Takayuki Mizuno 1, Misako Takayasu 1, Hideki Takayasu 2 1 Department of Computational Intelligence and Systems Science, Interdisciplinary

Modeling a foreign exchange rate using moving average of Yen-Dollar market data Takayuki Mizuno 1, Misako Takayasu 1, Hideki Takayasu 2 1 Department of Computational Intelligence and Systems Science, Interdisciplinary

Indeterminacy, Aggregate Demand, and the Real Business Cycle

Indeterminacy, Aggregate Demand, and the Real Business Cycle Jess Benhabib Department of Economics New York University jess.benhabib@nyu.edu Yi Wen Department of Economics Cornell University Yw57@cornell.edu

Indeterminacy, Aggregate Demand, and the Real Business Cycle Jess Benhabib Department of Economics New York University jess.benhabib@nyu.edu Yi Wen Department of Economics Cornell University Yw57@cornell.edu

Government Debt Management: the Long and the Short of it

Government Debt Management: the Long and the Short of it E. Faraglia (U. of Cambridge and CEPR) A. Marcet (IAE, UAB, ICREA, BGSE, MOVE and CEPR), R. Oikonomou (U.C. Louvain) A. Scott (LBS and CEPR) ()

Government Debt Management: the Long and the Short of it E. Faraglia (U. of Cambridge and CEPR) A. Marcet (IAE, UAB, ICREA, BGSE, MOVE and CEPR), R. Oikonomou (U.C. Louvain) A. Scott (LBS and CEPR) ()

Non-Stationary Time Series andunitroottests

Econometrics 2 Fall 2005 Non-Stationary Time Series andunitroottests Heino Bohn Nielsen 1of25 Introduction Many economic time series are trending. Important to distinguish between two important cases:

Econometrics 2 Fall 2005 Non-Stationary Time Series andunitroottests Heino Bohn Nielsen 1of25 Introduction Many economic time series are trending. Important to distinguish between two important cases:

Practical. I conometrics. data collection, analysis, and application. Christiana E. Hilmer. Michael J. Hilmer San Diego State University

Practical I conometrics data collection, analysis, and application Christiana E. Hilmer Michael J. Hilmer San Diego State University Mi Table of Contents PART ONE THE BASICS 1 Chapter 1 An Introduction

Practical I conometrics data collection, analysis, and application Christiana E. Hilmer Michael J. Hilmer San Diego State University Mi Table of Contents PART ONE THE BASICS 1 Chapter 1 An Introduction

Real-Business-Cycle Models and the Forecastable Movements in Output, Hours, and Consumption

Real-Business-Cycle Models and the Forecastable Movements in Output, Hours, and Consumption Julio J. Rotemberg; Michael Woodford The American Economic Review, Vol. 86, No. 1. (Mar., 1996), pp. 71-89. http://links.jstor.org/sici?sici=0002-8282%28199603%2986%3a1%3c71%3armatfm%3e2.0.co%3b2-y

Real-Business-Cycle Models and the Forecastable Movements in Output, Hours, and Consumption Julio J. Rotemberg; Michael Woodford The American Economic Review, Vol. 86, No. 1. (Mar., 1996), pp. 71-89. http://links.jstor.org/sici?sici=0002-8282%28199603%2986%3a1%3c71%3armatfm%3e2.0.co%3b2-y

Endogenous Technology Choices and the Dynamics of Wage Inequality

Endogenous Technology Choices and the Dynamics of Wage Inequality Empirical and Theoretical Evidence Jan Department of Economics European University Institute Fondazione Eni Enrico Mattei, February 2013

Endogenous Technology Choices and the Dynamics of Wage Inequality Empirical and Theoretical Evidence Jan Department of Economics European University Institute Fondazione Eni Enrico Mattei, February 2013

Not Your Dad s Magic Eight Ball

Not Your Dad s Magic Eight Ball Prepared for the NCSL Fiscal Analysts Seminar, October 21, 2014 Jim Landers, Office of Fiscal and Management Analysis, Indiana Legislative Services Agency Actual Forecast

Not Your Dad s Magic Eight Ball Prepared for the NCSL Fiscal Analysts Seminar, October 21, 2014 Jim Landers, Office of Fiscal and Management Analysis, Indiana Legislative Services Agency Actual Forecast

Asymmetries in Business Cycles and the Role of Oil Prices

Asymmetries in Business Cycles and the Role of Oil Prices Betty C. Daniel 1, Christian M. Hafner 2, Hans Manner 3, and Léopold Simar 2 1 Department of Economics, The University at Albany 2 Institute of

Asymmetries in Business Cycles and the Role of Oil Prices Betty C. Daniel 1, Christian M. Hafner 2, Hans Manner 3, and Léopold Simar 2 1 Department of Economics, The University at Albany 2 Institute of

NBER WORKING PAPER SERIES REAL BUSINESS CYCLE MODELS. Bennett T. McCallum. Working Paper No. 2480

NBER WORKING PAPER SERIES REAL BUSINESS CYCLE MODELS Bennett T. McCallum Working Paper No. 2480 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts Avenue Cambridge, MA 02138 January 1988 This paper

NBER WORKING PAPER SERIES REAL BUSINESS CYCLE MODELS Bennett T. McCallum Working Paper No. 2480 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts Avenue Cambridge, MA 02138 January 1988 This paper

Online Appendices to the Corporate Propensity to Save

Online Appendices to the Corporate Propensity to Save Appendix A: Monte Carlo Experiments In order to allay skepticism of empirical results that have been produced by unusual estimators on fairly small

Online Appendices to the Corporate Propensity to Save Appendix A: Monte Carlo Experiments In order to allay skepticism of empirical results that have been produced by unusual estimators on fairly small

Dynamic Macroeconomics I Introduction to Real Business Cycle Theory

Dynamic Macroeconomics I Introduction to Real Business Cycle Theory Lorenza Rossi University of Pavia these slides are based on my Course of Advanced Macroeconomics II held at UPF and bene t of the work

Dynamic Macroeconomics I Introduction to Real Business Cycle Theory Lorenza Rossi University of Pavia these slides are based on my Course of Advanced Macroeconomics II held at UPF and bene t of the work

Trade in Commodities and Emerging Market Business Cycles 1

Trade in Commodities and Emerging Market Business Cycles 1 David Kohn Universidad Torcuato Di Tella Fernando Leibovici York University Håkon Tretvoll BI Norwegian Business School September 215 Abstract

Trade in Commodities and Emerging Market Business Cycles 1 David Kohn Universidad Torcuato Di Tella Fernando Leibovici York University Håkon Tretvoll BI Norwegian Business School September 215 Abstract

Regression and Time Series Analysis of Petroleum Product Sales in Masters. Energy oil and Gas

Regression and Time Series Analysis of Petroleum Product Sales in Masters Energy oil and Gas 1 Ezeliora Chukwuemeka Daniel 1 Department of Industrial and Production Engineering, Nnamdi Azikiwe University

Regression and Time Series Analysis of Petroleum Product Sales in Masters Energy oil and Gas 1 Ezeliora Chukwuemeka Daniel 1 Department of Industrial and Production Engineering, Nnamdi Azikiwe University

Working Capital Requirement and the Unemployment Volatility Puzzle

Working Capital Requirement and the Unemployment Volatility Puzzle Tsu-ting Tim Lin Gettysburg College July, 3 Abstract Shimer (5) argues that a search-and-matching model of the labor market in which wage

Working Capital Requirement and the Unemployment Volatility Puzzle Tsu-ting Tim Lin Gettysburg College July, 3 Abstract Shimer (5) argues that a search-and-matching model of the labor market in which wage

Oil Price Uncertainty in a Small Open Economy

Oil Price Uncertainty in a Small Open Economy Yusuf Soner Başkaya Timur Hülagü Hande Küçük March 3, 22 Abstract In this paper, we present a dynamic general equilibrium model for an oil-importing small

Oil Price Uncertainty in a Small Open Economy Yusuf Soner Başkaya Timur Hülagü Hande Küçük March 3, 22 Abstract In this paper, we present a dynamic general equilibrium model for an oil-importing small

Should Central Banks Respond to Movements in Asset Prices? By Ben S. Bernanke and Mark Gertler *

Should Central Banks Respond to Movements in Asset Prices? By Ben S. Bernanke and Mark Gertler * In recent decades, asset booms and busts have been important factors in macroeconomic fluctuations in both

Should Central Banks Respond to Movements in Asset Prices? By Ben S. Bernanke and Mark Gertler * In recent decades, asset booms and busts have been important factors in macroeconomic fluctuations in both

7. Real business cycle

7. Real business cycle We have argued that a change in fundamentals, modifies the long-run solution of the system, while a temporary change not permanently affecting fundamentals leads to a short-run dynamics

7. Real business cycle We have argued that a change in fundamentals, modifies the long-run solution of the system, while a temporary change not permanently affecting fundamentals leads to a short-run dynamics

DECONSTRUCTING THE SUCCESS OF REAL BUSINESS CYCLES

DECONSTRUCTING THE SUCCESS OF REAL BUSINESS CYCLES EMI NAKAMURA* The empirical success of Real Business Cycle (RBC) models is often judged by their ability to explain the behavior of a multitude of real

DECONSTRUCTING THE SUCCESS OF REAL BUSINESS CYCLES EMI NAKAMURA* The empirical success of Real Business Cycle (RBC) models is often judged by their ability to explain the behavior of a multitude of real