FNCE 301, Financial Management H Guy Williams, 2006

|

|

|

- Primrose Wilkinson

- 8 years ago

- Views:

Transcription

1 REVIEW We ve used the DCF method to find present value. We also know shortcut methods to solve these problems such as perpetuity present value = C/r. These tools allow us to value any cash flow including stocks and bonds. Now we will examine how to value stocks and bonds. Bond Valuation The central questions for a financial manager: 1. What to invest in (valuation, Time Value of Money)? 2. How to finance the investment. Bond characteristics - A Bond is a contract between a borrower (issuer) and a lender (bondholder). The bondholder lends money to the issuer. The issuer, in turn, agrees to pay interest on this loan according to a set schedule, and to repay the loan principal at a stated maturity date. One party wants money, the other wants to lend money. Not easy for the two parties to find each other so there has been a market created to facilitate trading. The barrower issues a bond to the market, the lender has the opportunity to purchase the bond. Bond Terms: what is the interest rate and the payment schedule. - Face value (principal) of the bond is the amount to be repaid at maturity. Usually the face value is equal to $1,000. Face value is also known as PAR Value and Principle. If the bond is sold before maturity the new owner receives the face value payment at the end of the bond term. The face value is fixed, constant over the life of the bond, this is part of the bond agreement (covenant). - Market value is the price at which you could buy or sell a bond. The market value of a bond can change from day to day. The market value is determined by market forces. MARKET VALUE IS NOT THE SAME AS FACE VALUE! FNCE301 Class 3 Page 1

2 - Coupon rate is the interest rate to be paid on the face value of a bond. The coupon rate specifies the coupon payment. - Coupon payment is the periodic interest payment paid by the issuer to the bondholder. It is typically paid every six months. Coupon Payment = Face Value x Coupon Rate - Zero-coupon bond (pure discount bond) is a bond which does not pay any interest. No coupon payments. In this case we use the discount rate to value the bond. - Perpetuity bond (consol) is a bond that lasts forever and pays only interest. Same payment amount forever. Only need to know coupon rate, face value, and frequency. (PV = C/r, in this case we would be interested in C). Bond conditions (covenant) include interest rate, term, and payment schedule. From this we know when the bond loan will be repaid. Must be very careful about how the Bonds are typically issued at face value of $1,000. interest rate is stated. Here they say 6% semi-annual, so it s not 6%/2=3% Example every 6 months, it s 6% every 6 months. FV = $1,000 T = 3 years Coupon Rate = 6% semi-annual payments 0 $60 $ $60 $60 $60 $60 $1,000 We need face value, coupon rate, frequency, and maturity to estimate the bonds future cash flows and estimate it s value. The zero-coupon bond would require less values to solve. FNCE301 Class 3 Page 2

is a bond that lasts forever and pays only interest. Same payment amount forever.")

3 Bond Characteristics - Yield to Maturity, also called the Internal Rate of Return, is the average rate of return an investor will receive from a bond if purchased at the current market price and held to maturity (YTM always expressed in annual terms). Example: $1,000 Zero-Coupon Bond pays $1,200 after 1 year. What is the YTM? 1200 We do not know r but we can solve for r because we 1000 = r = 20% 1+ r know the market value is $1,000. So YTM = r = 20%. The credit rating of a company (such as Moody s), say AAA, AA, A, BBB, BB,, speaks to the companies strength, the likelihood that the firm will continue to meet it s obligations. But it does not speak to the longevity of the company, it does not indicate that the company is likely to be around 30 years to repay it s long term bonds. Here we are comparing how much we pay to how much we ultimately make. This is a key concept of bonds, used to compare values. The coupon rate stays the same over the entire life of the bond but the yield to maturity changes constantly according to the market value. YTM IS THE DISCOUNT RATE WHICH MAKES THE BOND S MARKET VALUE EQUAL TO THE PRESENT VALUE OF ALL FUTURE PAYMENTS OF THE BOND. Say we are considering buying a bond. The first thing we need to do is estimate the future payments of this asset. Next we need to calculate the present value of all the future payments, for this we need the discount rate. Now we are asking ourselves what is the proper discount rate for these future payments? But in fact some other people have already calculated the present value of the future payments, these people are the investors in the market and the PV they calculate for all future payments is the market value of the bond because this is the fair price of the asset. So PV = Market Value of future payments. Now we ask ourselves what discount rate did they use? Can we find this discount rate? Yes we can by back solving the equation. This discount rate is the YIELD TO MATURITY. Called the implied discount rate because it is implied by comparing the market value to the future payments. YTM is the interest rate that is required by investors in the bond market (the market interest rate). The market value of the bond is always known, then solve for the discount rate, this is the YTM. FNCE301 Class 3 Page 3

, say AAA, AA, A, BBB, BB,, speaks to the companies strength, the likelihood that the firm will continue to meet it s obligations.")

4 YTM is the IMPLIED DISCOUNT RATE of the bond also known as the Market Interest Rate. - Current yield is the ratio of the interest payment to the current market value of the bond (similar to YTM). Ratio of Coupon Payment to current Market Value. Current Yield measures the IMMEDIATE RETURN we will make from the bond, not the average return. NEXT PAYMENT CURRENT YIELD = MARKET VALUE Bond Issuers 0 $ Next payment with current market value = $ Bonds are issued by either corporations (corporate bonds) or the government (government bonds). - The main difference between corporate bonds and government bonds is that the corporate issuer may default. Risk is the difference, government bonds are guaranteed. The cash flow of a firm involves risk! The firm may default, go out of business, file for bankruptcy. But even in bankruptcy bond holders are repaid first (although maybe not all of their money). Risk is the difference here. Government bonds are guaranteed but the cash flow of a firm involves risk. A firm may default but failing to make it s bond payments usually means the firm is in bankruptcy. If the firm does go into bankruptcy the bond holders are the first to be repaid. - Bonds are the senior securities of a firm. The law requires bankrupt firms to pay off their bondholders before their equity holders. - Government bonds are the most reliable fixed income securities, and are considered to be risk-free. FNCE301 Class 3 Page 4

. - The main difference between corporate bonds and government bonds is that the corporate issuer may default. Risk is the difference, government bonds are guaranteed.")

5 U.S. Treasury securities (securities issued by the government) - Treasury bills (T-bills) Pure discount (zero-coupon) bonds. Issued with 3 months, 6 months, or 1 year to maturity in $10,000 denominations. Typically issued in $10,000 denominations. - Treasury notes and bonds T-Notes issued with between 1 and 10 years to maturity T-Bonds issued with 10 to 30 years to maturity These bonds have coupon payments. (30-year T-bonds are not currently issued by the Treasury or may have been reinstated) - Treasury Strips Long-term zero-coupon bonds (order of 30 years) The Treasury does not issue or sell strips directly to investors. Strips can be purchased and held only through financial institutions and government securities brokers and dealers. Usually held by institutions. Called this because the coupon payment has been stripped. Not popular with individual investors. - Inflation indexed securities Principal and coupon payments are adjusted to inflation (principal is adjusted only in certain types of issues) Guarantying a real return These can be issued by a firm as well. Coupon payments are adjusted to the inflation rate, protect investor against inflation. Principle is adjusted only in certain instances, certain types of issues. Example: FV = $1,000 T = 2 years Coupon Rate = 5% Annual Payments Coupon Payment = 1,000 *.05 = 50 In this example the inflation rates are 1.5% first year and 2.3% second year. Cash flows before inflation: Cash flows with inflation protection: $50 $ $65.75 $90.26 Payment 1: ( ) Payment 2: ( ) Note that in the second payment both periods are adjusted for inflation. In this example we did not show a principle adjustment, some issues have that, some don t. 2 We multiply the inflation rate by the coupon rate. FNCE301 Class 3 Page 5

- Treasury Strips Long-term zero-coupon bonds (order of 30 years) The Treasury does not issue or sell strips")

6 Bond Pricing - Value of financial securities = PV of expected future cash flows - Zero coupon bond, no coupon payments, only the principle payment with interest at maturity. Bond Price = Present Value = B = F (1+r) - Example: What is the price of a corporate zero-coupon bond that matures in 15 years if the market interest rate is 7%? The face value is $1,000 B = 1000 $ (1.07) 15 - Perpetuity bond, interest payments only but they continue forever. B = C = PV r - Example: What is the price of a perpetuity bond that pays 7% coupon annually if the market interest rate is 8%? B = 1000*.07 $ Coupon bond, interest payments at a defined interval (frequency). F = Face Value (PAR value), C = coupon payment T C C C C C C F - Example: What is the price at the time of issuance of an 8-year bond with a 9% annual coupon rate? The market interest rate for an eight-year horizon is 7% C = 9% r = 7% B = (1 - ) + $1, (1+.07) (1+.07) FNCE301 Class 3 Page 6

7 Bond pricing - In the examples above, the focus was on pricing the bonds given the market s required return (the market interest rate). - Conversely, if the bond s price is known, we can determine the market s required return, or YTM. We can find the discount rate if we have the future payments and the bond price. Why interested in this type of calculation? At the bond market we have future payments, bond price. But we do not have the discount rate, it is not part of the bond agreement. So we want to know how to calculate the discount rate. This gives us the return we will make if we buy the bond (this is also the YTM). So let s look at how to calculate the YTM. - The YTM is the discount rate that equates the bond s market price to the PV of its payments. We solve for the discount rate so we can know the YTM at a given market price. - YTM is calculated by trial and error (calculating by hand can be very tedious use Excel or financial calculator) Example - Consider a bond with an 8% coupon rate that matures in 3 years. The market price is $1,053. What is the yield to maturity of the bond? C C C F = (1+r) (1+r) (1+r) (1+r) For this schedule YTM = r = 6.02% FNCE301 Class 3 Page 7

. So let s look at how to calculate the YTM.")

8 Bond market reporting The stock in red closed at % of it s Face Value, closed at a PREMIUM. The stock in blue closed at 89% of it s face value, at a DISCOUNT. The bottom stock closed at 100% of it s face value, PAR. In the quote ATT 8½ 22 the 8½ is the annual coupon rate (the rate is stated as annual, if the coupon is paid every 6 months the 6 month coupon rate will be 8.5/2=4.25%). The 22 is the year in which the bond matures. Current Yield is the YTM of the bond. Volume tells how many of that issue changed hands that day. Close is the last trading price of that day in percentage of face value. We know that MARKET PRICE = CLOSE PRICE (%) * FACE VALUE. The + or indicates if the direction of movement since that previous trading day. Net Change is the change in the bonds price in percent since that previous trading day. Note the AMF stock at the top, it s current yield is 25.3%. That is saying that the bond is VERY HIGH RISK. The high return is intended to compensate for that risk. In this table we see that for ATT the current yield (it s not YTM) is kind of increasing with maturity. Although we have different coupon rates we can still identify this pattern because for bonds that are paid in the future there is more risk that the firm will go bankrupt even though coming down from 99% to 97.75% (year 02 to 04) is not too much there is still some increase in the discount rate even for a firm like AT&T. The current yield also varies because the maturity is different. FNCE301 Class 3 Page 8

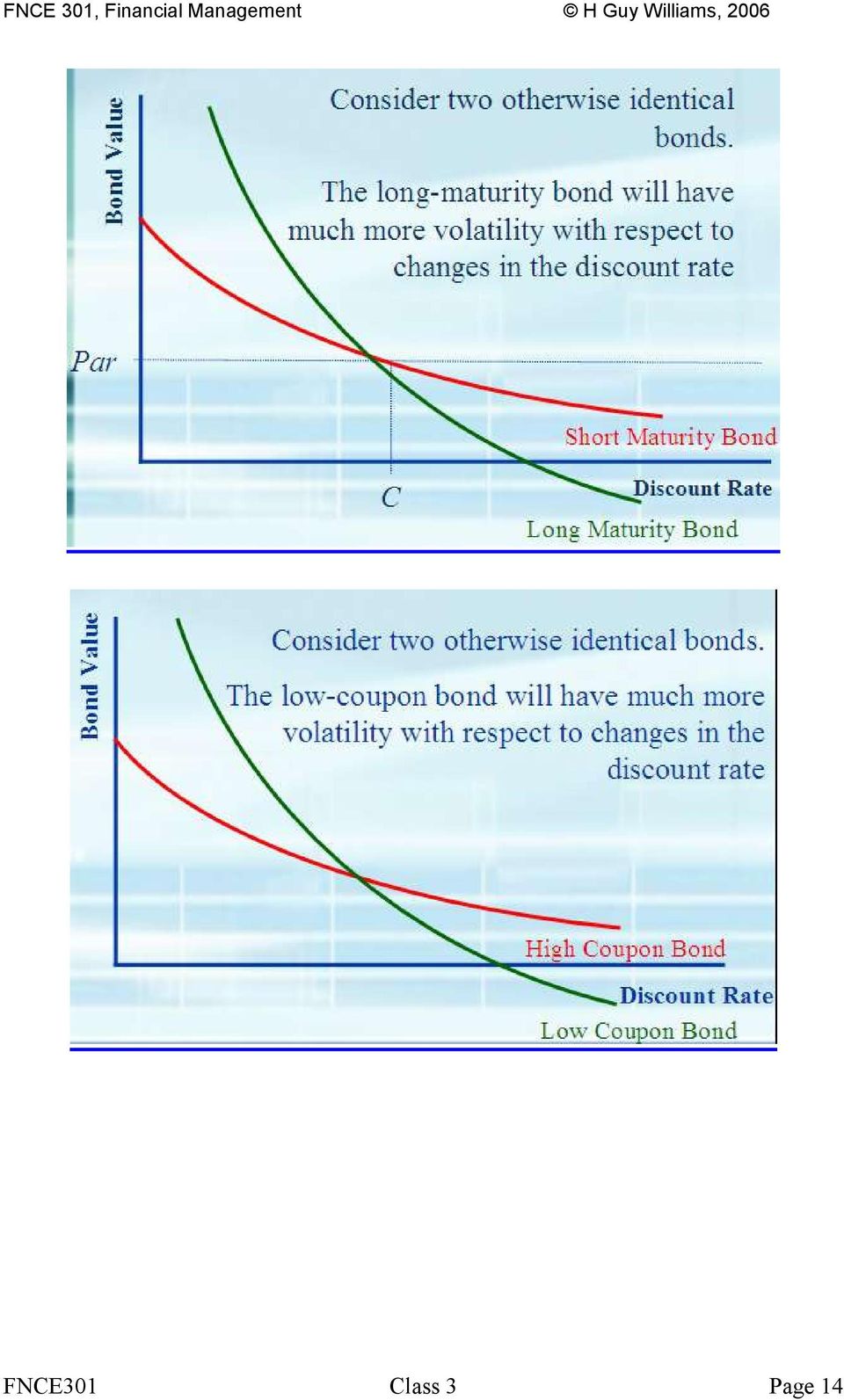

9 The relation between bond prices and interest rates - Fundamental fact: Bond prices move inversely to interest rates! One reason for this is opportunity cost. If your money is tied up in a bond you will loss the opportunity to make other investments. The discount rate relates to a similar investment available in the market. The investors must be compensated for this. If the current market interest rates are very high then the opportunity cost will be very high and the discount rate for investing in this bond will be high and this means that the market value of the bond will be LOW. So with increasing interest rates the bond prices are going down (to attract buyers). This does not mean that the magnitude of the change in every bonds price will be the same, in fact they will not be the same. For a given change in interest rates the change in bond price will vary greatly, some will change a little and some will change a lot. So what effects the magnitude of the change in the bond price for a given change in interest rate? What property of the bond effects the sensitivity of it s price to changes in interest rates. We examine an example. We have two zero-coupon bonds and the market interest rate changes from 9% to 12% (table below). Example: Determine the market value of a corporate bond with 20 years to maturity that has a 9% coupon rate, if the market interest rate is 7%, 9%, 11%. PREMIUM % : B = (1 ) = $1, % : B = (1 ) = $1, % : B = (1 ) + = $ DISCOUNT We see that the present value of the bond goes down as the interest rate increases! Also, when the coupon rate = market rate (discount rate) the face value equals the present value. This indicates that the money is growing at the same rate that we discounted it back to the present at. FNCE301 Class 3 Page 9

10 Although the discount rate and the coupon rate are different we can learn something by comparing them: - When coupon rate = Interest rate (YTM), the bond s price = face value (PAR bond) - When coupon rate > Interest rate (YTM), the bond s price > face value (Premium bond) - When coupon rate < Interest rate (YTM), the bond s price < face value (Discount bond) Back to our question: - What property of a bond affects the sensitivity of its price to the interest rate? For zero-coupon bonds the answer is MATURITY. (see example below) Example 1: The price of which of the following two zero-coupon bonds will be affected more if the interest rate increases from 9% to 12%? Bond A Bond B Face Value $1,000 $1,000 Time to Maturity 2 years 10 years Price (YTM = 9%) $ $ Price (YTM = 12%) $ $ As the interest rate changes the longer maturity bonds will feel the effect more, the rate change will have a longer time to act on the value. So in this example the long term bond losses more value as the interest rate increases. But what about the general case? Consider the example below: FNCE301 Class 3 Page 10

Example 1: The price of which of the following two zero-coupon bonds will be affected more if the interest rate increases from 9% to 12%?")

11 The relation between bond prices and interest rates Example 2: The price of which of the following bonds will be affected more if the interest rate increases from 9% to 12%? If we only consider the years to maturity we think the 12 year bond will be more sensitive. But one of these bonds has a coupon payment! How will this effect the bonds value? Bond A Bond B Face Value $1,000 $1,000 Coupon Rate 15% 0% Time to Maturity 12 years 10 years Price (YTM = 9%) $ (143%) $ (42.2%) Price (YTM = 12%) $ (118.6%) $ (32.2%) The form of the solution is: 9%: B A = (1 ) + $1, (1.09) (1+.09) If we have zero-coupon there is only one payment at the end, this is the entire value of the bond. But if we have many payments before maturity we get the value out closer to time zero, this helps offset the effect of a coupon rate which is lower than the market rate. In percentage terms bond B has suffered more. But maturity is not enough to establish a general rule. We see here that bond A had a longer maturity but the change was lower. What we see here suggest that we may want to look at the AVERAGE MATURITY FNCE301 Class 3 Page 11

The form of the solution is: 9%: B 150 1 1000 A = (1 ) + $1, 429.64 12 12.09 (1.09) (1+.09) If we have zero-coupon there is only one payment at the end, this is the entire value of the bond.")

12 Duration - The duration of a bond is the PV-weighted average of the maturities of the individual bond s payments: This CT includes all the payments at time T, coupon and final. The duration measures the degree to which the market price of the bond is sensitive to changes in the market interest rate. To ultimately answer the question about sensitivity we need weighting factors valued according to the present value. This is called the Duration of the Bond. Example: Consider the average maturity of the following two bonds: $100 $100 $ AM = AM = On the left the dominant payment is year 1 because it is closest to time 0. Very different bonds but they have the same sensitivity. Example: Consider the average maturity of the following two bonds: $100 $100 $100 $100 $100 $200 AM = 51 AM = 51 The present value of A is more dependent on payment 1, not some payment 100 years from now! (The present value of some payment 100 years from now is going to very low, close to 0). Getting the money closer to time zero helps negate the effects of interest rate changes. The long term bond is always going to suffer more. To improve our estimating method we must include weights wrt time and PV. Time is what is having an effect on PV so we compensate for it. FNCE301 Class 3 Page 12

13 Example - What is the duration of a ($1,000) bond with 3 years to maturity that has a 9% coupon rate, if the interest rate is 8%? First find B: B = (1 ) + = $1, (1.08) (1.08) Now find D: D = [(1 ) + (2 ) + (3 ) + (3 )] = (1.08) (1.08) (1.08) (1.08) This is a 3 year bond but it s duration is only 2.76 years! Intuitively: we have a coupon rate which is HIGHER than our discount rate so we expect to make our money sooner, the duration will be less than the maturity. Duration Dominant Payment - A zero-coupon bond has a duration equal to its maturity (we can see this in the duration equation, get T*B/B) - Coupon bonds have durations shorter than their maturity (see example above, we get some PV before maturity so weighted average is lower) - Duration increases with maturity (holding everything else constant) - Duration is inversely related to the coupon Zero-Coupon has duration = Maturity. A Coupon bond has payments earlier (closer to present) so the average maturity will go earlier, closer to the present. - Duration is inversely related to the Yield To Maturity (In the formula we can see the YTM is in the denominator, so as it increases the duration decreases.) The higher the YTM the lower the bond price. The total effect will be lower duration. FNCE301 Class 3 Page 13

- Coupon bonds have durations shorter than their maturity")

14 FNCE301 Class 3 Page 14

15 Predicting bond price changes using duration Why do we need a measure like Duration? We can compare the effects of a change in interest rates between different bonds. Two bonds, A and B, how will each bond be effected by a change in the interest rates? Say interest rates go up, bond A has longer duration, which bonds price will increase more? Bond A: Duration = 4.2, Bond B: Duration = 1.7 Market interest rate goes up. The price of which bond will drop more? Bond A s price will drop more. It is going to be tying up our money in the market longer paying a discount rate lower than the market rate. It (bond A) must compensate the investor by lowering it s price. THE LONGER THE DURATION THE MORE SENSITIVE THE BOND IS TO CHANGES IN THE INTEREST RATE. - The approximate change in the price of a bond given the change in yield can be determined as follows: This denominator r is the original r before the price change. The sign of r indicates increase (+) or decrease (-) in interest rate. Using duration to measure the response of the bonds price to a change in interest rates. Notice the effect on bond price due to interest rate change is the same for a zero-coupon bond as it is for a coupon bond. The formula above is dealing with duration which is the weighted average of the maturities. Example: Consider an 8% bond with 25 years to maturity. Assume that the interest rate is 6%. The duration of this bond is How much will the bond s price change if the market interest rate decreases by two basis points to 5.98%? D = r = = B = (1 - ) + = 1256 B = (-13.55) (.0002) = Positive change for decreasing interest rate due to inverse relationship between bond prices and interest rates.d represents the weighted average of the maturities. In the above example: D = (... + ) = $ Duration creates a measure which is valid for coupon and non-coupon bonds. FNCE301 Class 3 Page 15

must compensate the investor by lowering it s price.")

16 APR and bond equivalent yield - The YTM on T-bonds and T-notes is calculated as a semi-annual rate because the coupons are paid semiannually YTM calculated in semi-annual terms but then doubled to get annual. - The financial press multiplies this number by two, and reports the Annualized Percentage Rate (APR) (easier to compare in annual terms). So APR is a nominal rate because it does not take into account compounding. - The APR is also called the Bond Equivalent Yield. Two bonds: Bond A: 5% semi-annual (has 10% APR) Bond B: 10% annual Bond A has the greater return due to compounding. Nominal and Effective Interest Rates (EAR) - Effective Annual Interest Rate (EAR) is the actual rate generated by the investment. It results from adjusting the nominal annual interest rate to compounding during the year where m is the number of compound intervals per year - Given a constant nominal rate, the effective rate increases with m (number of compounding periods per year) - If m becomes very large (infinite), then Continuous compounding MUST KNOW e VALUE FOR EXAM FNCE301 Class 3 Page 16

Bond B: 10% annual Bond A has the greater return due to compounding.")

17 Effective Annual Yield - The Effective Annual Yield adjusts the APR for the effects of compounding. (We adjust the APR to the number of payments every year.) - With semi-annual compounding: APR general form: EAY = (1+ ) # payments per yr # payments per yr [These types of rate adjustments are used to calculate investment income but not used in PV calculations? Is this because of the units of the equation? Time base?] Example: If a bond has a semi-annual YTM of 3%, then After 1 year, each dollar invested grows to (APR = 2 * 3% = 6%) 6% In this case APR = 6% and EAY = (1 + ) - 1 = 6.09% 2 bond returns 6.09% every year. - Thus, the APR is 6%, but the Effective Annual Yield is 6.09% per year. Effectively this The term structure of interest rates - So far we assumed that the interest rate is the same for all maturities (the yield curve is flat) (we ve assumed the interest rate is constant for every period). - However, in reality, at any point in time, bonds with different times to maturity will have different yields to maturity - The pattern of interest rates for bonds with different maturities at a given point in time is called the Term Structure of Interest Rates. There is no single risk free rate in the market. Each term/period/maturity has it s own rate. The interest rate of a bond is a function of maturity called the Term Structure of Interest Rates. If someone ask What is the current risk free rate in the market? the answer will not be a single number, would be a rate and it s FNCE301 Class 3 Page 17

6% In this case APR = 6% and EAY = (1 + ) - 1 = 6.09% 2 bond returns 6.")

18 time period. Interest rate is a function of maturity called the TSIR. Term Structure of Interest Rates Curve (Yield Curve): YTM Rate TIME Typically we will see the rate increase with time to compensate for opportunity loss. In this example we see the short term rates dipped between 3 months and 5 years. One explanation could be that demand for long term (30 yr) bonds fell off while demand for short term bonds increased. The increased demand would have the effect of lowering the rate of return. The demand for longer maturity bonds (such as 30 years) is much lower than that for short term bonds. So the return on these longer term bonds must be higher. Practice questions FNCE301 Class 3 Page 18

bonds fell off while demand for short term bonds increased.")

How To Value Bonds

Chapter 6 Interest Rates And Bond Valuation Learning Goals 1. Describe interest rate fundamentals, the term structure of interest rates, and risk premiums. 2. Review the legal aspects of bond financing

Chapter 6 Interest Rates And Bond Valuation Learning Goals 1. Describe interest rate fundamentals, the term structure of interest rates, and risk premiums. 2. Review the legal aspects of bond financing

Chapter 9 Bonds and Their Valuation ANSWERS TO SELECTED END-OF-CHAPTER QUESTIONS

Chapter 9 Bonds and Their Valuation ANSWERS TO SELECTED END-OF-CHAPTER QUESTIONS 9-1 a. A bond is a promissory note issued by a business or a governmental unit. Treasury bonds, sometimes referred to as

Chapter 9 Bonds and Their Valuation ANSWERS TO SELECTED END-OF-CHAPTER QUESTIONS 9-1 a. A bond is a promissory note issued by a business or a governmental unit. Treasury bonds, sometimes referred to as

Interest Rates and Bond Valuation

and Bond Valuation 1 Bonds Debt Instrument Bondholders are lending the corporation money for some stated period of time. Liquid Asset Corporate Bonds can be traded in the secondary market. Price at which

and Bond Valuation 1 Bonds Debt Instrument Bondholders are lending the corporation money for some stated period of time. Liquid Asset Corporate Bonds can be traded in the secondary market. Price at which

Bond Valuation. FINANCE 350 Global Financial Management. Professor Alon Brav Fuqua School of Business Duke University. Bond Valuation: An Overview

Bond Valuation FINANCE 350 Global Financial Management Professor Alon Brav Fuqua School of Business Duke University 1 Bond Valuation: An Overview Bond Markets What are they? How big? How important? Valuation

Bond Valuation FINANCE 350 Global Financial Management Professor Alon Brav Fuqua School of Business Duke University 1 Bond Valuation: An Overview Bond Markets What are they? How big? How important? Valuation

Bond Valuation. Capital Budgeting and Corporate Objectives

Bond Valuation Capital Budgeting and Corporate Objectives Professor Ron Kaniel Simon School of Business University of Rochester 1 Bond Valuation An Overview Introduction to bonds and bond markets» What

Bond Valuation Capital Budgeting and Corporate Objectives Professor Ron Kaniel Simon School of Business University of Rochester 1 Bond Valuation An Overview Introduction to bonds and bond markets» What

LOS 56.a: Explain steps in the bond valuation process.

The following is a review of the Analysis of Fixed Income Investments principles designed to address the learning outcome statements set forth by CFA Institute. This topic is also covered in: Introduction

The following is a review of the Analysis of Fixed Income Investments principles designed to address the learning outcome statements set forth by CFA Institute. This topic is also covered in: Introduction

Chapter 8. Step 2: Find prices of the bonds today: n i PV FV PMT Result Coupon = 4% 29.5 5? 100 4 84.74 Zero coupon 29.5 5? 100 0 23.

Chapter 8 Bond Valuation with a Flat Term Structure 1. Suppose you want to know the price of a 10-year 7% coupon Treasury bond that pays interest annually. a. You have been told that the yield to maturity

Chapter 8 Bond Valuation with a Flat Term Structure 1. Suppose you want to know the price of a 10-year 7% coupon Treasury bond that pays interest annually. a. You have been told that the yield to maturity

You just paid $350,000 for a policy that will pay you and your heirs $12,000 a year forever. What rate of return are you earning on this policy?

1 You estimate that you will have $24,500 in student loans by the time you graduate. The interest rate is 6.5%. If you want to have this debt paid in full within five years, how much must you pay each

1 You estimate that you will have $24,500 in student loans by the time you graduate. The interest rate is 6.5%. If you want to have this debt paid in full within five years, how much must you pay each

Chapter 5: Valuing Bonds

FIN 302 Class Notes Chapter 5: Valuing Bonds What is a bond? A long-term debt instrument A contract where a borrower agrees to make interest and principal payments on specific dates Corporate Bond Quotations

FIN 302 Class Notes Chapter 5: Valuing Bonds What is a bond? A long-term debt instrument A contract where a borrower agrees to make interest and principal payments on specific dates Corporate Bond Quotations

Topics in Chapter. Key features of bonds Bond valuation Measuring yield Assessing risk

Bond Valuation 1 Topics in Chapter Key features of bonds Bond valuation Measuring yield Assessing risk 2 Determinants of Intrinsic Value: The Cost of Debt Net operating profit after taxes Free cash flow

Bond Valuation 1 Topics in Chapter Key features of bonds Bond valuation Measuring yield Assessing risk 2 Determinants of Intrinsic Value: The Cost of Debt Net operating profit after taxes Free cash flow

Answers to Review Questions

Answers to Review Questions 1. The real rate of interest is the rate that creates an equilibrium between the supply of savings and demand for investment funds. The nominal rate of interest is the actual

Answers to Review Questions 1. The real rate of interest is the rate that creates an equilibrium between the supply of savings and demand for investment funds. The nominal rate of interest is the actual

CHAPTER 8 INTEREST RATES AND BOND VALUATION

CHAPTER 8 INTEREST RATES AND BOND VALUATION Answers to Concept Questions 1. No. As interest rates fluctuate, the value of a Treasury security will fluctuate. Long-term Treasury securities have substantial

CHAPTER 8 INTEREST RATES AND BOND VALUATION Answers to Concept Questions 1. No. As interest rates fluctuate, the value of a Treasury security will fluctuate. Long-term Treasury securities have substantial

Bonds and Yield to Maturity

Bonds and Yield to Maturity Bonds A bond is a debt instrument requiring the issuer to repay to the lender/investor the amount borrowed (par or face value) plus interest over a specified period of time.

Bonds and Yield to Maturity Bonds A bond is a debt instrument requiring the issuer to repay to the lender/investor the amount borrowed (par or face value) plus interest over a specified period of time.

Interest Rates and Bond Valuation

Interest Rates and Bond Valuation Chapter 6 Key Concepts and Skills Know the important bond features and bond types Understand bond values and why they fluctuate Understand bond ratings and what they mean

Interest Rates and Bond Valuation Chapter 6 Key Concepts and Skills Know the important bond features and bond types Understand bond values and why they fluctuate Understand bond ratings and what they mean

Chapter 3 Fixed Income Securities

Chapter 3 Fixed Income Securities Road Map Part A Introduction to finance. Part B Valuation of assets, given discount rates. Fixed-income securities. Stocks. Real assets (capital budgeting). Part C Determination

Chapter 3 Fixed Income Securities Road Map Part A Introduction to finance. Part B Valuation of assets, given discount rates. Fixed-income securities. Stocks. Real assets (capital budgeting). Part C Determination

I. Readings and Suggested Practice Problems. II. Risks Associated with Default-Free Bonds

Prof. Alex Shapiro Lecture Notes 13 Bond Portfolio Management I. Readings and Suggested Practice Problems II. Risks Associated with Default-Free Bonds III. Duration: Details and Examples IV. Immunization

Prof. Alex Shapiro Lecture Notes 13 Bond Portfolio Management I. Readings and Suggested Practice Problems II. Risks Associated with Default-Free Bonds III. Duration: Details and Examples IV. Immunization

Understanding Fixed Income

Understanding Fixed Income 2014 AMP Capital Investors Limited ABN 59 001 777 591 AFSL 232497 Understanding Fixed Income About fixed income at AMP Capital Our global presence helps us deliver outstanding

Understanding Fixed Income 2014 AMP Capital Investors Limited ABN 59 001 777 591 AFSL 232497 Understanding Fixed Income About fixed income at AMP Capital Our global presence helps us deliver outstanding

Bond valuation. Present value of a bond = present value of interest payments + present value of maturity value

Bond valuation A reading prepared by Pamela Peterson Drake O U T L I N E 1. Valuation of long-term debt securities 2. Issues 3. Summary 1. Valuation of long-term debt securities Debt securities are obligations

Bond valuation A reading prepared by Pamela Peterson Drake O U T L I N E 1. Valuation of long-term debt securities 2. Issues 3. Summary 1. Valuation of long-term debt securities Debt securities are obligations

CHAPTER 15: THE TERM STRUCTURE OF INTEREST RATES

CHAPTER : THE TERM STRUCTURE OF INTEREST RATES CHAPTER : THE TERM STRUCTURE OF INTEREST RATES PROBLEM SETS.. In general, the forward rate can be viewed as the sum of the market s expectation of the future

CHAPTER : THE TERM STRUCTURE OF INTEREST RATES CHAPTER : THE TERM STRUCTURE OF INTEREST RATES PROBLEM SETS.. In general, the forward rate can be viewed as the sum of the market s expectation of the future

CHAPTER 5. Interest Rates. Chapter Synopsis

CHAPTER 5 Interest Rates Chapter Synopsis 5.1 Interest Rate Quotes and Adjustments Interest rates can compound more than once per year, such as monthly or semiannually. An annual percentage rate (APR)

CHAPTER 5 Interest Rates Chapter Synopsis 5.1 Interest Rate Quotes and Adjustments Interest rates can compound more than once per year, such as monthly or semiannually. An annual percentage rate (APR)

BOND - Security that obligates the issuer to make specified payments to the bondholder.

Bond Valuation BOND - Security that obligates the issuer to make specified payments to the bondholder. COUPON - The interest payments paid to the bondholder. FACE VALUE - Payment at the maturity of the

Bond Valuation BOND - Security that obligates the issuer to make specified payments to the bondholder. COUPON - The interest payments paid to the bondholder. FACE VALUE - Payment at the maturity of the

Analysis of Deterministic Cash Flows and the Term Structure of Interest Rates

Analysis of Deterministic Cash Flows and the Term Structure of Interest Rates Cash Flow Financial transactions and investment opportunities are described by cash flows they generate. Cash flow: payment

Analysis of Deterministic Cash Flows and the Term Structure of Interest Rates Cash Flow Financial transactions and investment opportunities are described by cash flows they generate. Cash flow: payment

Chapter. Bond Prices and Yields. McGraw-Hill/Irwin. Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved.

Chapter Bond Prices and Yields McGraw-Hill/Irwin Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Bond Prices and Yields Our goal in this chapter is to understand the relationship

Chapter Bond Prices and Yields McGraw-Hill/Irwin Copyright 2008 by The McGraw-Hill Companies, Inc. All rights reserved. Bond Prices and Yields Our goal in this chapter is to understand the relationship

Chapter 6 Interest rates and Bond Valuation. 2012 Pearson Prentice Hall. All rights reserved. 4-1

Chapter 6 Interest rates and Bond Valuation 2012 Pearson Prentice Hall. All rights reserved. 4-1 Interest Rates and Required Returns: Interest Rate Fundamentals The interest rate is usually applied to

Chapter 6 Interest rates and Bond Valuation 2012 Pearson Prentice Hall. All rights reserved. 4-1 Interest Rates and Required Returns: Interest Rate Fundamentals The interest rate is usually applied to

- Short term notes (bonds) Maturities of 1-4 years - Medium-term notes/bonds Maturities of 5-10 years - Long-term bonds Maturities of 10-30 years

Maturities of 1-4 years - Medium-term notes/bonds Maturities of 5-10 years - Long-term bonds Maturities of 10-30 years") Contents 1. What Is A Bond? 2. Who Issues Bonds? Government Bonds Corporate Bonds 3. Basic Terms of Bonds Maturity Types of Coupon (Fixed, Floating, Zero Coupon) Redemption Seniority Price Yield The Relation

Contents 1. What Is A Bond? 2. Who Issues Bonds? Government Bonds Corporate Bonds 3. Basic Terms of Bonds Maturity Types of Coupon (Fixed, Floating, Zero Coupon) Redemption Seniority Price Yield The Relation

Bonds and preferred stock. Basic definitions. Preferred(?) stock. Investing in fixed income securities

stock. Investing in fixed income securities") Bonds and preferred stock Investing in fixed income securities Basic definitions Stock: share of ownership Stockholders are the owners of the firm Two types of stock: preferred and common Preferred stock:

Bonds and preferred stock Investing in fixed income securities Basic definitions Stock: share of ownership Stockholders are the owners of the firm Two types of stock: preferred and common Preferred stock:

Fixed Income: Practice Problems with Solutions

Fixed Income: Practice Problems with Solutions Directions: Unless otherwise stated, assume semi-annual payment on bonds.. A 6.0 percent bond matures in exactly 8 years and has a par value of 000 dollars.

Fixed Income: Practice Problems with Solutions Directions: Unless otherwise stated, assume semi-annual payment on bonds.. A 6.0 percent bond matures in exactly 8 years and has a par value of 000 dollars.

Practice Set #1 and Solutions.

Bo Sjö 14-05-03 Practice Set #1 and Solutions. What to do with this practice set? Practice sets are handed out to help students master the material of the course and prepare for the final exam. These sets

Bo Sjö 14-05-03 Practice Set #1 and Solutions. What to do with this practice set? Practice sets are handed out to help students master the material of the course and prepare for the final exam. These sets

ANALYSIS OF FIXED INCOME SECURITIES

ANALYSIS OF FIXED INCOME SECURITIES Valuation of Fixed Income Securities Page 1 VALUATION Valuation is the process of determining the fair value of a financial asset. The fair value of an asset is its

ANALYSIS OF FIXED INCOME SECURITIES Valuation of Fixed Income Securities Page 1 VALUATION Valuation is the process of determining the fair value of a financial asset. The fair value of an asset is its

Chapter 11. Stocks and Bonds. How does this distribution work? An example. What form do the distributions to common shareholders take?

Chapter 11. Stocks and Bonds Chapter Objectives To identify basic shareholder rights and the means by which corporations make distributions to shareholders To recognize the investment opportunities in

Chapter 11. Stocks and Bonds Chapter Objectives To identify basic shareholder rights and the means by which corporations make distributions to shareholders To recognize the investment opportunities in

CHAPTER 15: THE TERM STRUCTURE OF INTEREST RATES

Chapter - The Term Structure of Interest Rates CHAPTER : THE TERM STRUCTURE OF INTEREST RATES PROBLEM SETS.. In general, the forward rate can be viewed as the sum of the market s expectation of the future

Chapter - The Term Structure of Interest Rates CHAPTER : THE TERM STRUCTURE OF INTEREST RATES PROBLEM SETS.. In general, the forward rate can be viewed as the sum of the market s expectation of the future

NATIONAL STOCK EXCHANGE OF INDIA LIMITED

NATIONAL STOCK EXCHANGE OF INDIA LIMITED Capital Market FAQ on Corporate Bond Date : September 29, 2011 1. What are securities? Securities are financial instruments that represent a creditor relationship

NATIONAL STOCK EXCHANGE OF INDIA LIMITED Capital Market FAQ on Corporate Bond Date : September 29, 2011 1. What are securities? Securities are financial instruments that represent a creditor relationship

Exam 1 Morning Session

91. A high yield bond fund states that through active management, the fund s return has outperformed an index of Treasury securities by 4% on average over the past five years. As a performance benchmark

91. A high yield bond fund states that through active management, the fund s return has outperformed an index of Treasury securities by 4% on average over the past five years. As a performance benchmark

Chapter 6. Discounted Cash Flow Valuation. Key Concepts and Skills. Multiple Cash Flows Future Value Example 6.1. Answer 6.1

Chapter 6 Key Concepts and Skills Be able to compute: the future value of multiple cash flows the present value of multiple cash flows the future and present value of annuities Discounted Cash Flow Valuation

Chapter 6 Key Concepts and Skills Be able to compute: the future value of multiple cash flows the present value of multiple cash flows the future and present value of annuities Discounted Cash Flow Valuation

Chapter 4 Bonds and Their Valuation ANSWERS TO END-OF-CHAPTER QUESTIONS

Chapter 4 Bonds and Their Valuation ANSWERS TO END-OF-CHAPTER QUESTIONS 4-1 a. A bond is a promissory note issued by a business or a governmental unit. Treasury bonds, sometimes referred to as government

Chapter 4 Bonds and Their Valuation ANSWERS TO END-OF-CHAPTER QUESTIONS 4-1 a. A bond is a promissory note issued by a business or a governmental unit. Treasury bonds, sometimes referred to as government

CHAPTER 9 DEBT SECURITIES. by Lee M. Dunham, PhD, CFA, and Vijay Singal, PhD, CFA

CHAPTER 9 DEBT SECURITIES by Lee M. Dunham, PhD, CFA, and Vijay Singal, PhD, CFA LEARNING OUTCOMES After completing this chapter, you should be able to do the following: a Identify issuers of debt securities;

CHAPTER 9 DEBT SECURITIES by Lee M. Dunham, PhD, CFA, and Vijay Singal, PhD, CFA LEARNING OUTCOMES After completing this chapter, you should be able to do the following: a Identify issuers of debt securities;

Lesson 6 Save and Invest: Bonds Lending Your Money

Lesson 6 Save and Invest: Bonds Lending Your Money Lesson Description This lesson introduces bonds as an investment option. Using a series of classroom visuals, students will identify the three main parts

Lesson 6 Save and Invest: Bonds Lending Your Money Lesson Description This lesson introduces bonds as an investment option. Using a series of classroom visuals, students will identify the three main parts

How To Calculate Bond Price And Yield To Maturity

CHAPTER 10 Bond Prices and Yields Interest rates go up and bond prices go down. But which bonds go up the most and which go up the least? Interest rates go down and bond prices go up. But which bonds go

CHAPTER 10 Bond Prices and Yields Interest rates go up and bond prices go down. But which bonds go up the most and which go up the least? Interest rates go down and bond prices go up. But which bonds go

CHAPTER 15: THE TERM STRUCTURE OF INTEREST RATES

CHAPTER 15: THE TERM STRUCTURE OF INTEREST RATES 1. Expectations hypothesis. The yields on long-term bonds are geometric averages of present and expected future short rates. An upward sloping curve is

CHAPTER 15: THE TERM STRUCTURE OF INTEREST RATES 1. Expectations hypothesis. The yields on long-term bonds are geometric averages of present and expected future short rates. An upward sloping curve is

CHAPTER 14: BOND PRICES AND YIELDS

CHAPTER 14: BOND PRICES AND YIELDS PROBLEM SETS 1. The bond callable at 105 should sell at a lower price because the call provision is more valuable to the firm. Therefore, its yield to maturity should

CHAPTER 14: BOND PRICES AND YIELDS PROBLEM SETS 1. The bond callable at 105 should sell at a lower price because the call provision is more valuable to the firm. Therefore, its yield to maturity should

Chapter 4: Common Stocks. Chapter 5: Forwards and Futures

15.401 Part B Valuation Chapter 3: Fixed Income Securities Chapter 4: Common Stocks Chapter 5: Forwards and Futures Chapter 6: Options Lecture Notes Introduction 15.401 Part B Valuation We have learned

15.401 Part B Valuation Chapter 3: Fixed Income Securities Chapter 4: Common Stocks Chapter 5: Forwards and Futures Chapter 6: Options Lecture Notes Introduction 15.401 Part B Valuation We have learned

January 2008. Bonds. An introduction to bond basics

January 2008 Bonds An introduction to bond basics The information contained in this publication is for general information purposes only and is not intended by the Investment Industry Association of Canada

January 2008 Bonds An introduction to bond basics The information contained in this publication is for general information purposes only and is not intended by the Investment Industry Association of Canada

INTERACTIVE BROKERS DISCLOSURE STATEMENT FOR BOND TRADING

INTERACTIVE BROKERS DISCLOSURE STATEMENT FOR BOND TRADING THIS DISCLOSURE STATEMENT DISCUSSES THE CHARACTERISTICS AND RISKS OF TRADING BONDS THROUGH INTERACTIVE BROKERS (IB). BEFORE TRADING BONDS YOU SHOULD

INTERACTIVE BROKERS DISCLOSURE STATEMENT FOR BOND TRADING THIS DISCLOSURE STATEMENT DISCUSSES THE CHARACTERISTICS AND RISKS OF TRADING BONDS THROUGH INTERACTIVE BROKERS (IB). BEFORE TRADING BONDS YOU SHOULD

Practice Set #2 and Solutions.

FIN-672 Securities Analysis & Portfolio Management Professor Michel A. Robe Practice Set #2 and Solutions. What to do with this practice set? To help MBA students prepare for the assignment and the exams,

FIN-672 Securities Analysis & Portfolio Management Professor Michel A. Robe Practice Set #2 and Solutions. What to do with this practice set? To help MBA students prepare for the assignment and the exams,

Bonds and the Term Structure of Interest Rates: Pricing, Yields, and (No) Arbitrage

Arbitrage") Prof. Alex Shapiro Lecture Notes 12 Bonds and the Term Structure of Interest Rates: Pricing, Yields, and (No) Arbitrage I. Readings and Suggested Practice Problems II. Bonds Prices and Yields (Revisited)

Prof. Alex Shapiro Lecture Notes 12 Bonds and the Term Structure of Interest Rates: Pricing, Yields, and (No) Arbitrage I. Readings and Suggested Practice Problems II. Bonds Prices and Yields (Revisited)

Finding the Payment $20,000 = C[1 1 / 1.0066667 48 ] /.0066667 C = $488.26

![Finding the Payment $20,000 = C[1 1 / 1.0066667 48 ] /.0066667 C = $488.26](/thumbs/17/134163.jpg "Finding the Payment $20,000 = C[1 1 / 1.0066667 48 ] /.0066667 C = $488.26") Quick Quiz: Part 2 You know the payment amount for a loan and you want to know how much was borrowed. Do you compute a present value or a future value? You want to receive $5,000 per month in retirement.

Quick Quiz: Part 2 You know the payment amount for a loan and you want to know how much was borrowed. Do you compute a present value or a future value? You want to receive $5,000 per month in retirement.

CHAPTER 8 INTEREST RATES AND BOND VALUATION

CHAPTER 8 INTEREST RATES AND BOND VALUATION Solutions to Questions and Problems 1. The price of a pure discount (zero coupon) bond is the present value of the par value. Remember, even though there are

CHAPTER 8 INTEREST RATES AND BOND VALUATION Solutions to Questions and Problems 1. The price of a pure discount (zero coupon) bond is the present value of the par value. Remember, even though there are

CHAPTER 14: BOND PRICES AND YIELDS

CHAPTER 14: BOND PRICES AND YIELDS 1. a. Effective annual rate on 3-month T-bill: ( 100,000 97,645 )4 1 = 1.02412 4 1 =.10 or 10% b. Effective annual interest rate on coupon bond paying 5% semiannually:

CHAPTER 14: BOND PRICES AND YIELDS 1. a. Effective annual rate on 3-month T-bill: ( 100,000 97,645 )4 1 = 1.02412 4 1 =.10 or 10% b. Effective annual interest rate on coupon bond paying 5% semiannually:

U.S. Treasury Securities

U.S. Treasury Securities U.S. Treasury Securities 4.6 Nonmarketable To help finance its operations, the U.S. government from time to time borrows money by selling investors a variety of debt securities

U.S. Treasury Securities U.S. Treasury Securities 4.6 Nonmarketable To help finance its operations, the U.S. government from time to time borrows money by selling investors a variety of debt securities

Chapter 6 APPENDIX B. The Yield Curve and the Law of One Price. Valuing a Coupon Bond with Zero-Coupon Prices

196 Part Interest Rates and Valuing Cash Flows Chapter 6 APPENDIX B The Yield Curve and the Law of One Price Thus far, we have focused on the relationship between the price of an individual bond and its

196 Part Interest Rates and Valuing Cash Flows Chapter 6 APPENDIX B The Yield Curve and the Law of One Price Thus far, we have focused on the relationship between the price of an individual bond and its

Click Here to Buy the Tutorial

FIN 534 Week 4 Quiz 3 (Str) Click Here to Buy the Tutorial http://www.tutorialoutlet.com/fin-534/fin-534-week-4-quiz-3- str/ For more course tutorials visit www.tutorialoutlet.com Which of the following

FIN 534 Week 4 Quiz 3 (Str) Click Here to Buy the Tutorial http://www.tutorialoutlet.com/fin-534/fin-534-week-4-quiz-3- str/ For more course tutorials visit www.tutorialoutlet.com Which of the following

http://www.investopedia.com/university/bonds/ Thanks very much for downloading the printable version of this tutorial.

Bond Basics Tutorial http://www.investopedia.com/university/bonds/ Thanks very much for downloading the printable version of this tutorial. As always, we welcome any feedback or suggestions. http://www.investopedia.com/contact.aspx

Bond Basics Tutorial http://www.investopedia.com/university/bonds/ Thanks very much for downloading the printable version of this tutorial. As always, we welcome any feedback or suggestions. http://www.investopedia.com/contact.aspx

Chapter 11. Bond Pricing - 1. Bond Valuation: Part I. Several Assumptions: To simplify the analysis, we make the following assumptions.

Bond Pricing - 1 Chapter 11 Several Assumptions: To simplify the analysis, we make the following assumptions. 1. The coupon payments are made every six months. 2. The next coupon payment for the bond is

Bond Pricing - 1 Chapter 11 Several Assumptions: To simplify the analysis, we make the following assumptions. 1. The coupon payments are made every six months. 2. The next coupon payment for the bond is

Bond Valuation. What is a bond?

Lecture: III 1 What is a bond? Bond Valuation When a corporation wishes to borrow money from the public on a long-term basis, it usually does so by issuing or selling debt securities called bonds. A bond

Lecture: III 1 What is a bond? Bond Valuation When a corporation wishes to borrow money from the public on a long-term basis, it usually does so by issuing or selling debt securities called bonds. A bond

Global Financial Management

Global Financial Management Bond Valuation Copyright 999 by Alon Brav, Campbell R. Harvey, Stephen Gray and Ernst Maug. All rights reserved. No part of this lecture may be reproduced without the permission

Global Financial Management Bond Valuation Copyright 999 by Alon Brav, Campbell R. Harvey, Stephen Gray and Ernst Maug. All rights reserved. No part of this lecture may be reproduced without the permission

Bond Valuation. Chapter 7. Example (coupon rate = r d ) Bonds, Bond Valuation, and Interest Rates. Valuing the cash flows

Bonds, Bond Valuation, and Interest Rates. Valuing the cash flows") Bond Valuation Chapter 7 Bonds, Bond Valuation, and Interest Rates Valuing the cash flows (1) coupon payment (interest payment) = (coupon rate * principal) usually paid every 6 months (2) maturity value

Bond Valuation Chapter 7 Bonds, Bond Valuation, and Interest Rates Valuing the cash flows (1) coupon payment (interest payment) = (coupon rate * principal) usually paid every 6 months (2) maturity value

Discounted Cash Flow Valuation

Discounted Cash Flow Valuation Chapter 5 Key Concepts and Skills Be able to compute the future value of multiple cash flows Be able to compute the present value of multiple cash flows Be able to compute

Discounted Cash Flow Valuation Chapter 5 Key Concepts and Skills Be able to compute the future value of multiple cash flows Be able to compute the present value of multiple cash flows Be able to compute

Lecture 11 Fixed-Income Securities: An Overview

1 Lecture 11 Fixed-Income Securities: An Overview Alexander K. Koch Department of Economics, Royal Holloway, University of London January 11, 2008 In addition to learning the material covered in the reading

1 Lecture 11 Fixed-Income Securities: An Overview Alexander K. Koch Department of Economics, Royal Holloway, University of London January 11, 2008 In addition to learning the material covered in the reading

5. Time value of money

1 Simple interest 2 5. Time value of money With simple interest, the amount earned each period is always the same: i = rp o We will review some tools for discounting cash flows. where i = interest earned

1 Simple interest 2 5. Time value of money With simple interest, the amount earned each period is always the same: i = rp o We will review some tools for discounting cash flows. where i = interest earned

Econ 330 Exam 1 Name ID Section Number

Econ 330 Exam 1 Name ID Section Number MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) If during the past decade the average rate of monetary growth

Econ 330 Exam 1 Name ID Section Number MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) If during the past decade the average rate of monetary growth

YIELD CURVE GENERATION

1 YIELD CURVE GENERATION Dr Philip Symes Agenda 2 I. INTRODUCTION II. YIELD CURVES III. TYPES OF YIELD CURVES IV. USES OF YIELD CURVES V. YIELD TO MATURITY VI. BOND PRICING & VALUATION Introduction 3 A

1 YIELD CURVE GENERATION Dr Philip Symes Agenda 2 I. INTRODUCTION II. YIELD CURVES III. TYPES OF YIELD CURVES IV. USES OF YIELD CURVES V. YIELD TO MATURITY VI. BOND PRICING & VALUATION Introduction 3 A

Solutions 2. 1. For the benchmark maturity sectors in the United States Treasury bill markets,

FIN 472 Professor Robert Hauswald Fixed-Income Securities Kogod School of Business, AU Solutions 2 1. For the benchmark maturity sectors in the United States Treasury bill markets, Bloomberg reported the

FIN 472 Professor Robert Hauswald Fixed-Income Securities Kogod School of Business, AU Solutions 2 1. For the benchmark maturity sectors in the United States Treasury bill markets, Bloomberg reported the

Chapter 5 Bonds, Bond Valuation, and Interest Rates ANSWERS TO END-OF-CHAPTER QUESTIONS

Chapter 5 Bonds, Bond Valuation, and Interest Rates ANSWERS TO END-OF-CHAPTER QUESTIONS 5-1 a. A bond is a promissory note issued by a business or a governmental unit. Treasury bonds, sometimes referred

Chapter 5 Bonds, Bond Valuation, and Interest Rates ANSWERS TO END-OF-CHAPTER QUESTIONS 5-1 a. A bond is a promissory note issued by a business or a governmental unit. Treasury bonds, sometimes referred

FNCE 301, Financial Management H Guy Williams, 2006

Review In the first class we looked at the value today of future payments (introduction), how to value projects and investments. Present Value = Future Payment * 1 Discount Factor. The discount factor

Review In the first class we looked at the value today of future payments (introduction), how to value projects and investments. Present Value = Future Payment * 1 Discount Factor. The discount factor

Bonds. Describe Bonds. Define Key Words. Created 2007 By Michael Worthington Elizabeth City State University

Bonds OBJECTIVES Describe bonds Define key words Explain why bond prices fluctuate Compute interest payments Calculate the price of bonds Created 2007 By Michael Worthington Elizabeth City State University

Bonds OBJECTIVES Describe bonds Define key words Explain why bond prices fluctuate Compute interest payments Calculate the price of bonds Created 2007 By Michael Worthington Elizabeth City State University

Chapter 6 Interest Rates and Bond Valuation

Chapter 6 Interest Rates and Bond Valuation Solutions to Problems P6-1. P6-2. LG 1: Interest Rate Fundamentals: The Real Rate of Return Basic Real rate of return = 5.5% 2.0% = 3.5% LG 1: Real Rate of Interest

Chapter 6 Interest Rates and Bond Valuation Solutions to Problems P6-1. P6-2. LG 1: Interest Rate Fundamentals: The Real Rate of Return Basic Real rate of return = 5.5% 2.0% = 3.5% LG 1: Real Rate of Interest

Fin 3312 Sample Exam 1 Questions

Fin 3312 Sample Exam 1 Questions Here are some representative type questions. This review is intended to give you an idea of the types of questions that may appear on the exam, and how the questions might

Fin 3312 Sample Exam 1 Questions Here are some representative type questions. This review is intended to give you an idea of the types of questions that may appear on the exam, and how the questions might

Review for Exam 1. Instructions: Please read carefully

Review for Exam 1 Instructions: Please read carefully The exam will have 20 multiple choice questions and 5 work problems. Questions in the multiple choice section will be either concept or calculation

Review for Exam 1 Instructions: Please read carefully The exam will have 20 multiple choice questions and 5 work problems. Questions in the multiple choice section will be either concept or calculation

CHAPTER 4. The Time Value of Money. Chapter Synopsis

CHAPTER 4 The Time Value of Money Chapter Synopsis Many financial problems require the valuation of cash flows occurring at different times. However, money received in the future is worth less than money

CHAPTER 4 The Time Value of Money Chapter Synopsis Many financial problems require the valuation of cash flows occurring at different times. However, money received in the future is worth less than money

CHAPTER 5 HOW TO VALUE STOCKS AND BONDS

CHAPTER 5 HOW TO VALUE STOCKS AND BONDS Answers to Concepts Review and Critical Thinking Questions 1. Bond issuers look at outstanding bonds of similar maturity and risk. The yields on such bonds are used

CHAPTER 5 HOW TO VALUE STOCKS AND BONDS Answers to Concepts Review and Critical Thinking Questions 1. Bond issuers look at outstanding bonds of similar maturity and risk. The yields on such bonds are used

Chapter 4 Valuing Bonds

Chapter 4 Valuing Bonds MULTIPLE CHOICE 1. A 15 year, 8%, $1000 face value bond is currently trading at $958. The yield to maturity of this bond must be a. less than 8%. b. equal to 8%. c. greater than

Chapter 4 Valuing Bonds MULTIPLE CHOICE 1. A 15 year, 8%, $1000 face value bond is currently trading at $958. The yield to maturity of this bond must be a. less than 8%. b. equal to 8%. c. greater than

Bonds are IOUs. Just like shares you can buy bonds on the world s stock exchanges.

Investing in bonds Despite their names, ShareScope and SharePad are not just all about shares. They can help you with other investments as well. In this article I m going to tell you how you can use the

Investing in bonds Despite their names, ShareScope and SharePad are not just all about shares. They can help you with other investments as well. In this article I m going to tell you how you can use the

Bond Price Arithmetic

1 Bond Price Arithmetic The purpose of this chapter is: To review the basics of the time value of money. This involves reviewing discounting guaranteed future cash flows at annual, semiannual and continuously

1 Bond Price Arithmetic The purpose of this chapter is: To review the basics of the time value of money. This involves reviewing discounting guaranteed future cash flows at annual, semiannual and continuously

MBA Finance Part-Time Present Value

MBA Finance Part-Time Present Value Professor Hugues Pirotte Spéder Solvay Business School Université Libre de Bruxelles Fall 2002 1 1 Present Value Objectives for this session : 1. Introduce present value

MBA Finance Part-Time Present Value Professor Hugues Pirotte Spéder Solvay Business School Université Libre de Bruxelles Fall 2002 1 1 Present Value Objectives for this session : 1. Introduce present value

2. Determine the appropriate discount rate based on the risk of the security

Fixed Income Instruments III Intro to the Valuation of Debt Securities LOS 64.a Explain the steps in the bond valuation process 1. Estimate the cash flows coupons and return of principal 2. Determine the

Fixed Income Instruments III Intro to the Valuation of Debt Securities LOS 64.a Explain the steps in the bond valuation process 1. Estimate the cash flows coupons and return of principal 2. Determine the

Investing in Bonds - An Introduction

Investing in Bonds - An Introduction By: Scott A. Bishop, CPA, CFP, and Director of Financial Planning What are bonds? Bonds, sometimes called debt instruments or fixed-income securities, are essentially

Investing in Bonds - An Introduction By: Scott A. Bishop, CPA, CFP, and Director of Financial Planning What are bonds? Bonds, sometimes called debt instruments or fixed-income securities, are essentially

Chapter. Investing in Bonds. 13.1 Evaluating Bonds 13.2 Buying and Selling Bonds. 2010 South-Western, Cengage Learning

Chapter 13 Investing in Bonds 13.1 Evaluating Bonds 13.2 Buying and Selling Bonds 2010 South-Western, Cengage Learning Standards Standard 4.0 Investigate opportunities available for saving and investing.

Chapter 13 Investing in Bonds 13.1 Evaluating Bonds 13.2 Buying and Selling Bonds 2010 South-Western, Cengage Learning Standards Standard 4.0 Investigate opportunities available for saving and investing.

How To Invest In Stocks And Bonds

Review for Exam 1 Instructions: Please read carefully The exam will have 21 multiple choice questions and 5 work problems. Questions in the multiple choice section will be either concept or calculation

Review for Exam 1 Instructions: Please read carefully The exam will have 21 multiple choice questions and 5 work problems. Questions in the multiple choice section will be either concept or calculation

Prepared by: Dalia A. Marafi Version 2.0

Kuwait University College of Business Administration Department of Finance and Financial Institutions Using )Casio FC-200V( for Fundamentals of Financial Management (220) Prepared by: Dalia A. Marafi Version

Kuwait University College of Business Administration Department of Finance and Financial Institutions Using )Casio FC-200V( for Fundamentals of Financial Management (220) Prepared by: Dalia A. Marafi Version

Chapter 6 Valuing Bonds. (1) coupon payment - interest payment (coupon rate * principal) - usually paid every 6 months.

coupon payment - interest payment (coupon rate * principal) - usually paid every 6 months.") Chapter 6 Valuing Bonds Bond Valuation - value the cash flows (1) coupon payment - interest payment (coupon rate * principal) - usually paid every 6 months. (2) maturity value = principal or par value

Chapter 6 Valuing Bonds Bond Valuation - value the cash flows (1) coupon payment - interest payment (coupon rate * principal) - usually paid every 6 months. (2) maturity value = principal or par value

Bonds, in the most generic sense, are issued with three essential components.

Page 1 of 5 Bond Basics Often considered to be one of the most conservative of all investments, bonds actually provide benefits to both conservative and more aggressive investors alike. The variety of

Page 1 of 5 Bond Basics Often considered to be one of the most conservative of all investments, bonds actually provide benefits to both conservative and more aggressive investors alike. The variety of

Chapter Review and Self-Test Problems. Answers to Chapter Review and Self-Test Problems

236 PART THREE Valuation of Future Cash Flows Chapter Review and Self-Test Problems 7.1 Bond Values A Microgates Industries bond has a 10 percent coupon rate and a $1,000 face value. Interest is paid semiannually,

236 PART THREE Valuation of Future Cash Flows Chapter Review and Self-Test Problems 7.1 Bond Values A Microgates Industries bond has a 10 percent coupon rate and a $1,000 face value. Interest is paid semiannually,

Chapter 4: Time Value of Money

FIN 301 Homework Solution Ch4 Chapter 4: Time Value of Money 1. a. 10,000/(1.10) 10 = 3,855.43 b. 10,000/(1.10) 20 = 1,486.44 c. 10,000/(1.05) 10 = 6,139.13 d. 10,000/(1.05) 20 = 3,768.89 2. a. $100 (1.10)

FIN 301 Homework Solution Ch4 Chapter 4: Time Value of Money 1. a. 10,000/(1.10) 10 = 3,855.43 b. 10,000/(1.10) 20 = 1,486.44 c. 10,000/(1.05) 10 = 6,139.13 d. 10,000/(1.05) 20 = 3,768.89 2. a. $100 (1.10)

Fixed Income Portfolio Management. Interest rate sensitivity, duration, and convexity

Fixed Income ortfolio Management Interest rate sensitivity, duration, and convexity assive bond portfolio management Active bond portfolio management Interest rate swaps 1 Interest rate sensitivity, duration,

Fixed Income ortfolio Management Interest rate sensitivity, duration, and convexity assive bond portfolio management Active bond portfolio management Interest rate swaps 1 Interest rate sensitivity, duration,

CHAPTER 5 INTRODUCTION TO VALUATION: THE TIME VALUE OF MONEY

CHAPTER 5 INTRODUCTION TO VALUATION: THE TIME VALUE OF MONEY Answers to Concepts Review and Critical Thinking Questions 1. The four parts are the present value (PV), the future value (FV), the discount

CHAPTER 5 INTRODUCTION TO VALUATION: THE TIME VALUE OF MONEY Answers to Concepts Review and Critical Thinking Questions 1. The four parts are the present value (PV), the future value (FV), the discount

Investments Analysis

Investments Analysis Last 2 Lectures: Fixed Income Securities Bond Prices and Yields Term Structure of Interest Rates This Lecture (#7): Fixed Income Securities Term Structure of Interest Rates Interest

Investments Analysis Last 2 Lectures: Fixed Income Securities Bond Prices and Yields Term Structure of Interest Rates This Lecture (#7): Fixed Income Securities Term Structure of Interest Rates Interest

Practice Questions for Midterm II

Finance 333 Investments Practice Questions for Midterm II Winter 2004 Professor Yan 1. The market portfolio has a beta of a. 0. *b. 1. c. -1. d. 0.5. By definition, the beta of the market portfolio is

Finance 333 Investments Practice Questions for Midterm II Winter 2004 Professor Yan 1. The market portfolio has a beta of a. 0. *b. 1. c. -1. d. 0.5. By definition, the beta of the market portfolio is

Review for Exam 1. Instructions: Please read carefully

Review for Exam 1 Instructions: Please read carefully The exam will have 25 multiple choice questions and 5 work problems covering chapter 1, 2, 3, 4, 14, 16. Questions in the multiple choice section will

Review for Exam 1 Instructions: Please read carefully The exam will have 25 multiple choice questions and 5 work problems covering chapter 1, 2, 3, 4, 14, 16. Questions in the multiple choice section will

Maturity The date where the issuer must return the principal or the face value to the investor.

PRODUCT INFORMATION SHEET - BONDS 1. WHAT ARE BONDS? A bond is a debt instrument issued by a borrowing entity (issuer) to investors (lenders) in return for lending their money to the issuer. The issuer

PRODUCT INFORMATION SHEET - BONDS 1. WHAT ARE BONDS? A bond is a debt instrument issued by a borrowing entity (issuer) to investors (lenders) in return for lending their money to the issuer. The issuer

Bond valuation and bond yields

RELEVANT TO ACCA QUALIFICATION PAPER P4 AND PERFORMANCE OBJECTIVES 15 AND 16 Bond valuation and bond yields Bonds and their variants such as loan notes, debentures and loan stock, are IOUs issued by governments

RELEVANT TO ACCA QUALIFICATION PAPER P4 AND PERFORMANCE OBJECTIVES 15 AND 16 Bond valuation and bond yields Bonds and their variants such as loan notes, debentures and loan stock, are IOUs issued by governments

FinQuiz Notes 2 0 1 4

Reading 5 The Time Value of Money Money has a time value because a unit of money received today is worth more than a unit of money to be received tomorrow. Interest rates can be interpreted in three ways.

Reading 5 The Time Value of Money Money has a time value because a unit of money received today is worth more than a unit of money to be received tomorrow. Interest rates can be interpreted in three ways.

Financial-Institutions Management. Solutions 1. 6. A financial institution has the following market value balance sheet structure:

FIN 683 Professor Robert Hauswald Financial-Institutions Management Kogod School of Business, AU Solutions 1 Chapter 7: Bank Risks - Interest Rate Risks 6. A financial institution has the following market

FIN 683 Professor Robert Hauswald Financial-Institutions Management Kogod School of Business, AU Solutions 1 Chapter 7: Bank Risks - Interest Rate Risks 6. A financial institution has the following market

CHAPTER 7: FIXED-INCOME SECURITIES: PRICING AND TRADING

CHAPTER 7: FIXED-INCOME SECURITIES: PRICING AND TRADING Topic One: Bond Pricing Principles 1. Present Value. A. The present-value calculation is used to estimate how much an investor should pay for a bond;

CHAPTER 7: FIXED-INCOME SECURITIES: PRICING AND TRADING Topic One: Bond Pricing Principles 1. Present Value. A. The present-value calculation is used to estimate how much an investor should pay for a bond;

CHAPTER 11 INTRODUCTION TO SECURITY VALUATION TRUE/FALSE QUESTIONS

1 CHAPTER 11 INTRODUCTION TO SECURITY VALUATION TRUE/FALSE QUESTIONS (f) 1 The three step valuation process consists of 1) analysis of alternative economies and markets, 2) analysis of alternative industries

1 CHAPTER 11 INTRODUCTION TO SECURITY VALUATION TRUE/FALSE QUESTIONS (f) 1 The three step valuation process consists of 1) analysis of alternative economies and markets, 2) analysis of alternative industries

Time Value Conepts & Applications. Prof. Raad Jassim

Time Value Conepts & Applications Prof. Raad Jassim Chapter Outline Introduction to Valuation: The Time Value of Money 1 2 3 4 5 6 7 8 Future Value and Compounding Present Value and Discounting More on

Time Value Conepts & Applications Prof. Raad Jassim Chapter Outline Introduction to Valuation: The Time Value of Money 1 2 3 4 5 6 7 8 Future Value and Compounding Present Value and Discounting More on

How to calculate present values

How to calculate present values Back to the future Chapter 3 Discounted Cash Flow Analysis (Time Value of Money) Discounted Cash Flow (DCF) analysis is the foundation of valuation in corporate finance

How to calculate present values Back to the future Chapter 3 Discounted Cash Flow Analysis (Time Value of Money) Discounted Cash Flow (DCF) analysis is the foundation of valuation in corporate finance

Pricing of Financial Instruments

CHAPTER 2 Pricing of Financial Instruments 1. Introduction In this chapter, we will introduce and explain the use of financial instruments involved in investing, lending, and borrowing money. In particular,

CHAPTER 2 Pricing of Financial Instruments 1. Introduction In this chapter, we will introduce and explain the use of financial instruments involved in investing, lending, and borrowing money. In particular,

Key Concepts and Skills. Multiple Cash Flows Future Value Example 6.1. Chapter Outline. Multiple Cash Flows Example 2 Continued

6 Calculators Discounted Cash Flow Valuation Key Concepts and Skills Be able to compute the future value of multiple cash flows Be able to compute the present value of multiple cash flows Be able to compute

6 Calculators Discounted Cash Flow Valuation Key Concepts and Skills Be able to compute the future value of multiple cash flows Be able to compute the present value of multiple cash flows Be able to compute

Investors Chronicle Roadshow 2011. Trading Bonds on the London Stock Exchange

Investors Chronicle Roadshow 2011 Trading Bonds on the London Stock Exchange Agenda How do bonds work? Risks associated with bonds Order book for Retail Bonds London Stock Exchange Website Tools 2 How

Investors Chronicle Roadshow 2011 Trading Bonds on the London Stock Exchange Agenda How do bonds work? Risks associated with bonds Order book for Retail Bonds London Stock Exchange Website Tools 2 How

The Time Value of Money

The following is a review of the Quantitative Methods: Basic Concepts principles designed to address the learning outcome statements set forth by CFA Institute. This topic is also covered in: The Time

The following is a review of the Quantitative Methods: Basic Concepts principles designed to address the learning outcome statements set forth by CFA Institute. This topic is also covered in: The Time