Developing Effective Internal Controls Using the COSO Model

|

|

|

- Barnaby Wilcox

- 10 years ago

- Views:

Transcription

1 Developing Effective Internal Controls Using the COSO Model Office of State Controller Internal Controls in a COSO Environment Seminar Raleigh, North Carolina March 2007 Mark S. Beasley Director, ERM Initiative and Professor of Accounting North Carolina State University

2 Today s Objectives 1. Why all the buzz about COSO? 2. What do we mean by internal control? 3. What are the key components for effective internal control? Page 2

3 Who is COSO? Page 3

4 Why all the recent fuss over Internal Controls? Page 4

5 Fraud! Perception that effective internal controls help prevent and detect fraud. Page 5

6 Sarbanes-Oxley Section 404 Annual management assessments of IC over financial i reporting Section 302 Quarterly certifications by CEO and CFO that they have Controls that material information is disclosed to them Evaluated the effectiveness of IC within prior 90 days Page 6

7 PCAOB Auditing Std No. 2 Paragraph.13 Management is required to base its assessment on a suitable, recognized control framework established by a body of experts that t follow due process procedures Paragraph.14 In the United States, COSO s Internal Control-Integrated Framework provides a suitable and available framework for purposes of management s assessment Page 7

8 Why All the Focus on IC? Internal Internal Accident External Controls Audit Audit Source: KPMG Fraud Survey Page 8

9 Today s Objectives 2. What do we mean by internal control? Page 9

10 COSO s Definition Internal control is a process, effected by an entity s board of directors, management and other personnel, designed dto provide reasonable assurance regarding the achievement of objectives Page 10

11 COSO s View of IC Page 11

12 3 Categories of IC Objectives Operations Compliance Financial Reporting Page 12

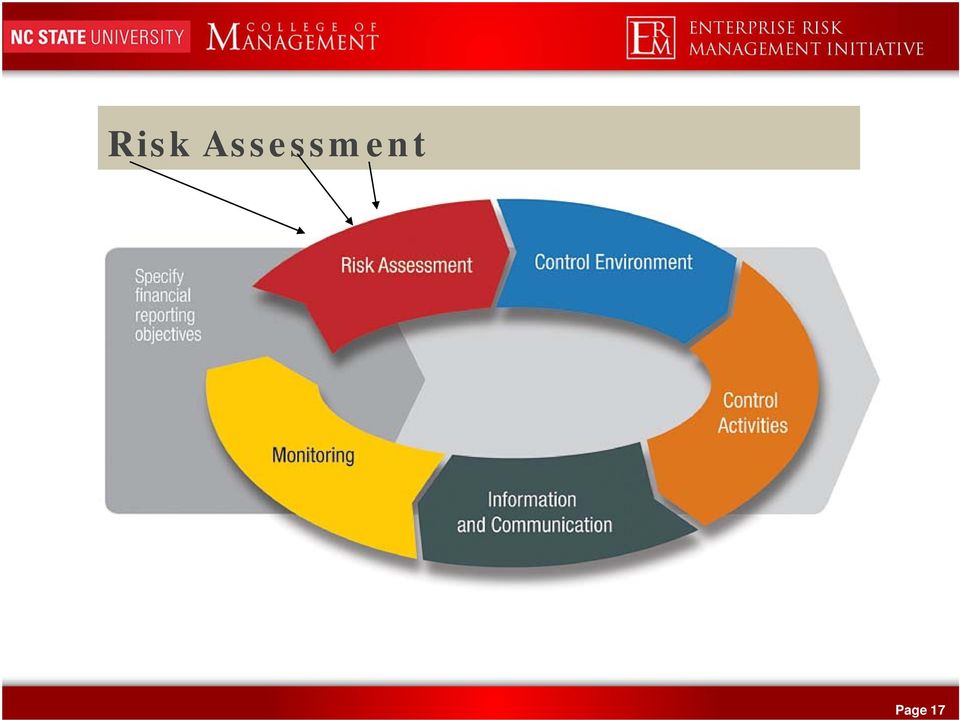

13 5 Components of IC Monitoring Information and Communication Control Activities Risk Assessment Control Environment Page 13

14 Internal Control as a Process Page 14

15 Key Concept 1. To identify the correct control, you must know what risks are present. 2. To know what risks are present, you need to understand what objectives are being sought. 3. Thus, Objectives Risks Controls Page 15

16 Today s Objectives 3. What are the key components for effective internal control? Page 16

17 Risk Assessment Page 17

18 Risk Assessment Precondition to controls is identifying risks Can t determine needed controls without knowing risks Every entity faces risks Risks constantly evolve Need a systematic process for risk management Focused on both likelihood and consequence Page 18

19 Drivers of Internal Controls Strategic Objectives Threats Threats Threats Business Processes Identified Risks Internal Control Page 19

20 Financial Reporting Objectives Safeguarding of Assets Emphasize reliable and relevant reporting Transparent - reflect economic reality Timely Meet GAAP minimum threshold Account and transaction level objectives 5 Financial Statement Assertions Page 20

21 A l i Ri k A i Fl Analyzing Risks Across T Transaction Flows Transactions Journals Cash disbursements Cash C h disbursements journal Payroll services and disbursements Payroll y journal Allocation and adjustments General journal Ledgers, Trial Balance, and Financial Statements General ledger g and subsidiary records General ledger trial balance Financial statements t t t Page 21

22 Control Environment Page 22

23 Control Environment Sets the tone at the top Board and Senior Management driven Influences control consciousness of its people Core to sound integrity it and ethical values Emphasis on competencies and authorities Foundation for all other components of IC Page 23

24 Relationship to Other Components Risk assessment Control activities Information and communication Monitoring Page 24

25 Core Themes Sound integrity and ethical values are critical to IC Code of Conduct Board and audit committee play a vital role Independence and financial expertise Mgt s philosophy and operating style support IC Actions consistent with Code of Conduct Entities must retain individuals with competencies Commitment to acquiring needed competencies Employees are assigned appropriate levels of authority Delegation is clear and accountable Human resource practices demonstrate commitment to integrity, it ethical behavior, and competence Screening done not just for employment, but also promotion Page 25

26 Subcomponents Control Environment Integrity Commitment Board Mgt Organ. Assignment Human & Ethical Values to Competence & Audit Comm. Philosophy & Operating Style Structure of Authority Respon. Resource Policies & Procedure Page 26

27 Control Activities Page 27

28 Control Activities Page 28

29 Control Activities Represent responses to identified risks Don t need a control if no corresponding risks Control activities are Actions taken to address risks of achieving objectives Occur at all levels l of an organization Company-wide controls Business process specific tasks Consists of 2 aspects: Policy of what should be done Procedures to accomplish policy Page 29

30 Example Revenues Assertions Exist/Occur Policies & Procedures That Ensure Recorded revenues actually earned Completeness Rights/Oblig Revenues earned are actually recorded Organization has rights to revenue receivables Valuation/Alloc Present/Discl Revenues recorded at correct amounts Revenue policies/terms disclosed properly Page 30

31 Categories of Control Activities 1. Adequate separation of duties 2. Proper authorization of transactions and activities 3Ad 3. Adequate documents and records 4. Physical control over assets and records 5. Independent checks on performance Page 31

32 Adequate Segregation of Duties Asset Accounting/ Authorization IT Custody Record keeping of Trans. Duties Page 32

33 Combinations of Control Activities Management uses a mix of Preventative controls Detective controls Combinations of Manual controls Automated controls Page 33

34 IT General and Application Controls Risk of unauthorized change to application software Risk of system crash Cash receipts application controls Sales Payroll applications application controls controls Other cycle application controls Risk of unauthorized master file update GENERAL CONTROLS Risk of unauthorized processing Page 34

35 Example of IT Controls General Controls Application Controls IT Organization Physical/Logical Security Access restriction to application Input data validation against master file Systems Development Range or Limit it Checks Change Management Sequence Checks Backup Planning Programmed edits logic tests Page 35

36 Cost Benefit Considerations Impact from Risks Costs of Implementing Controls Page 36

37 Information and Communication Page 37

38 Information and Communication Information is needed to carryout responsibilities Information From Management To Management Effective Communication is needed More than just information flow Key is understanding the messages Information & Communication needs to be controlled, too Page 38

39 Information Flow Key elements system must Identify Capture Process Distribute Information based on Internal and external sources Operational information used to develop financial information Information used to control activities that support objectives Page 39

40 Communication Has management developed Communications program to reinforce IC objectives? Communications strategy t to enable each employee to understand d IC responsibilities? Process to determine if information needed by employees is timely and accurate? Communication mechanism for employees to be aware of ethical and legal l requirements? Does the entity ty have fail-safe mechanisms s in case normal channels of communications are inoperative? Is the Board of Directors receiving needed information? Page 40

41 Monitoring Page 41

42 Monitoring Internal control systems need to be monitored a/k/a Monitoring of controls Focus assessing quality of system performance More than just information flow Key is understanding the messages Nature of Monitoring Ongoing Separate Evaluations Page 42

43 Ongoing Monitoring Built into operations Some automated Focus on deviations from norms Provide continual feedback on controls Should lead to investigations May lead to system changes Page 43

44 Separate Evaluations Evaluate effectiveness of ongoing monitoring Objective look from time to time Scope based on significance of risks Objective and competent evaluator Internal audit plays vital role Page 44

45 Monitoring of All Elements Page 45

46 Bringing it All Together 5 Components of Internal Control Must Work Together Can t have effective Internal Control if one component weak Page 46

47 The Big Picture Five COSO components work together: Note: Figure above is taken from COSO s Internal Control over Financial Reporting Guidance for Public Companies, Volume II: Guidance. Page 47

48 Risk Assessment Note: Figure above is taken from COSO s Internal Control over Financial Reporting Guidance for Public Companies, Volume II: Guidance. Page 48

49 Control Environment Note: Figure above is taken from COSO s Internal Control over Financial Reporting Guidance for Public Companies, Volume II: Guidance. Page 49

50 Control Activities Note: Figure above is taken from COSO s Internal Control over Financial Reporting Guidance for Public Companies, Volume II: Guidance. Page 50

51 Information and Communication Monitoring Note: Figure above is taken from COSO s Internal Control over Financial Reporting Guidance for Public Companies, Volume II: Guidance. Page 51

52 4 Points of Internal Control Failure 1. Focus on 4 Points of Failure - Assumption it s only the auditor s job Page 52

53 Failure # Points of Failure - Assumption it s only the auditor s job - Failure to link risks and controls Page 53

54 Failure # Points of Failure - Assumption it s only the auditor s job - Failure to link risks and controls - Inadequate monitoring of controls Page 54

55 Failure # Points of Failure - Assumption it s only the auditor s job - Failure to link risks and controls - Inadequate monitoring of controls - Ignoring reality risk of management override is always present Page 55

56 Guidance Volume I Provides a high level summary Summarizes recent developments, internal control challenges, and the costs and benefits associated with internal control Focuses on risk as a basis for developing internal control Introduces internal control as a process Page 56

57 Guidance Volume II Focuses on twenty fundamental principles These principles i are drawn from the original Internal Control Integrated Framework These principles assist smaller businesses in achieving internal control in a cost-effective manner Page 57

58 Guidance Volume II: Principles, Attributes, Approaches, and Examples Sound integrity and ethical values, particularly of Principle 1 top management, are developed and understood and set the standard of conduct for financial reporting. Three Attributes Three Approaches Articulates Values Monitors Adherence Addresses Deviation Articulating and Demonstrating Integrity and Ethics Informing Employees about Integrity and Ethics Demonstrating Commitment to Integrity and Ethics Six Examples Company Newsletter Reinforcing Integrity and Ethics Promoting Awareness of Ethical Behavior Etc Page 58

59 Guidance Volume III Contains illustrative tools to assist management in evaluating internal control Managers may use the illustrative tools in determining whether the company has effectively applied the principles It is expected that that other managers will use Volumes II and III as a reference source for guidance in those areas of particular need This volume is now also available in a Word format Page 59

60 A Look Back at Today s Objectives 1. Why all the buzz about COSO? Sarbanes-Oxley Good business sense 2. What do we mean by internal control? More than just checks and balances Responses to risks threatening objectives 3. What are the key components for effective internal control? Complex interactions of 5 core components Range from high-level actions to detailed processes Page 60

61 Internal Controls Provide Bridge to Success For Organizations Reduce exposures to risks threatening strategy For You Now an expected core competency of management Page 61

62 Reality: Internal control checklists must link to Risks Fraud risk is more than the auditor s responsibility Monitoring of controls must occur on an ongoing basis Management override is always present risk Mark Beasley Director ERM Initiative and Professor of Accounting NC State University

Guide to Internal Control Over Financial Reporting

Guide to Internal Control Over Financial Reporting The Center for Audit Quality prepared this Guide to provide an overview for the general public of internal control over financial reporting ( ICFR ).

Guide to Internal Control Over Financial Reporting The Center for Audit Quality prepared this Guide to provide an overview for the general public of internal control over financial reporting ( ICFR ).

Internal Control over Financial Reporting Guidance for Smaller Public Companies

Internal Control over Financial Reporting Guidance for Smaller Public Companies Frequently Asked Questions Internal Control over Financial Reporting Guidance for Smaller Public Companies Frequently Asked

Internal Control over Financial Reporting Guidance for Smaller Public Companies Frequently Asked Questions Internal Control over Financial Reporting Guidance for Smaller Public Companies Frequently Asked

University Audit and Compliance. Internal Controls Enterprise-Wide Risk Assessment

Internal Controls Enterprise-Wide Risk Assessment Balancing Risk and Controls In order to achieve goals and objectives, management needs to effectively balance risks and controls. Control procedures need

Internal Controls Enterprise-Wide Risk Assessment Balancing Risk and Controls In order to achieve goals and objectives, management needs to effectively balance risks and controls. Control procedures need

Communicating Internal Control Related Matters Identified in an Audit

Communicating Internal Control 1843 AU Section 325 Communicating Internal Control Related Matters Identified in an Audit (Supersedes SAS No. 112.) Source: SAS No. 115. Effective for audits of financial

Communicating Internal Control 1843 AU Section 325 Communicating Internal Control Related Matters Identified in an Audit (Supersedes SAS No. 112.) Source: SAS No. 115. Effective for audits of financial

AN AUDIT OF INTERNAL CONTROL OVER FINANCIAL REPORTING THAT IS INTEGRATED WITH AN AUDIT OF FINANCIAL STATEMENTS:

1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org STAFF VIEWS AN AUDIT OF INTERNAL CONTROL OVER FINANCIAL REPORTING THAT IS INTEGRATED WITH AN

1666 K Street, NW Washington, D.C. 20006 Telephone: (202) 207-9100 Facsimile: (202) 862-8430 www.pcaobus.org STAFF VIEWS AN AUDIT OF INTERNAL CONTROL OVER FINANCIAL REPORTING THAT IS INTEGRATED WITH AN

AUDIT OF READINESS FOR THE IMPLEMENTATION OF THE POLICY ON INTERNAL CONTROL

AUDIT OF READINESS FOR THE IMPLEMENTATION OF THE POLICY ON INTERNAL CONTROL AUDIT REPORT JUNE 2010 TABLE OF CONTENTS EXCUTIVE SUMMARY... 3 1 INTRODUCTION... 5 1.1 AUDIT OBJECTIVE. 5 1.2 SCOPE...5 1.3 SUMMARY

AUDIT OF READINESS FOR THE IMPLEMENTATION OF THE POLICY ON INTERNAL CONTROL AUDIT REPORT JUNE 2010 TABLE OF CONTENTS EXCUTIVE SUMMARY... 3 1 INTRODUCTION... 5 1.1 AUDIT OBJECTIVE. 5 1.2 SCOPE...5 1.3 SUMMARY

Risk Assessment Standards Toolkit. Practical Guidance in Implementing SFAS 104 111

Risk Assessment Standards Toolkit Practical Guidance in Implementing SFAS 104 111 Risk Assessment Standards Toolkit Practical Guidance in Implementing Statements on Auditing Standards 104 Through 111 About

Risk Assessment Standards Toolkit Practical Guidance in Implementing SFAS 104 111 Risk Assessment Standards Toolkit Practical Guidance in Implementing Statements on Auditing Standards 104 Through 111 About

[RELEASE NOS. 33-8810; 34-55929; FR-77; File No. S7-24-06]

![[RELEASE NOS. 33-8810; 34-55929; FR-77; File No. S7-24-06]](/thumbs/25/6464675.jpg "[RELEASE NOS. 33-8810; 34-55929; FR-77; File No. S7-24-06]") SECURITIES AND EXCHANGE COMMISSION 17 CFR PART 241 [RELEASE NOS. 33-8810; 34-55929; FR-77; File No. S7-24-06] Commission Guidance Regarding Management s Report on Internal Control Over Financial Reporting

SECURITIES AND EXCHANGE COMMISSION 17 CFR PART 241 [RELEASE NOS. 33-8810; 34-55929; FR-77; File No. S7-24-06] Commission Guidance Regarding Management s Report on Internal Control Over Financial Reporting

SARBANES-OXLEY SECTION 404: A Guide for Management by Internal Controls Practitioners

SARBANES-OXLEY SECTION 404: A Guide for Management by Internal Controls Practitioners SARBANES-OXLEY SECTION 404: A Guide for Management by Internal Controls Practitioners The Institute of Internal Auditors

SARBANES-OXLEY SECTION 404: A Guide for Management by Internal Controls Practitioners SARBANES-OXLEY SECTION 404: A Guide for Management by Internal Controls Practitioners The Institute of Internal Auditors

Internal Control Integrated Framework. May 2013

Internal Control Integrated Framework May 2013 0 Table of Contents COSO & Project Overview Internal Control-Integrated Framework Illustrative Documents Illustrative Tools for Assessing Effectiveness of

Internal Control Integrated Framework May 2013 0 Table of Contents COSO & Project Overview Internal Control-Integrated Framework Illustrative Documents Illustrative Tools for Assessing Effectiveness of

1 (a) Audit strategy document Section of document Purpose Example from B-Star

Audit strategy document Section of document Purpose Example from B-Star") Answers Fundamentals Level Skills Module, Paper F8 (IRL) Audit and Assurance (Irish) June 2009 Answers 1 (a) Audit strategy document Section of document Purpose Example from B-Star Understanding the entity

Answers Fundamentals Level Skills Module, Paper F8 (IRL) Audit and Assurance (Irish) June 2009 Answers 1 (a) Audit strategy document Section of document Purpose Example from B-Star Understanding the entity

A Risk-Based Audit Strategy November 2006 Internal Audit Department

Mental Health Mental Retardation Authority of Harris County ENTERPRISE RISK MANAGEMENT A Framework For Assessing, Evaluating And Measuring Our Agency s Risk A Risk-Based Audit Strategy November 2006 Internal

Mental Health Mental Retardation Authority of Harris County ENTERPRISE RISK MANAGEMENT A Framework For Assessing, Evaluating And Measuring Our Agency s Risk A Risk-Based Audit Strategy November 2006 Internal

Sarbanes-Oxley Section 404: Compliance Challenges for Foreign Private Issuers

Sarbanes-Oxley Section 404: Compliance s for Foreign Private Issuers Table of Contents Requirements of the Act.............................................................. 1 Accelerated Filer s...........................................................

Sarbanes-Oxley Section 404: Compliance s for Foreign Private Issuers Table of Contents Requirements of the Act.............................................................. 1 Accelerated Filer s...........................................................

Understanding the Entity and Its Environment and Assessing the Risks of Material Misstatement

Understanding the Entity and Its Environment 1667 AU Section 314 Understanding the Entity and Its Environment and Assessing the Risks of Material Misstatement (Supersedes SAS No. 55.) Source: SAS No. 109.

Understanding the Entity and Its Environment 1667 AU Section 314 Understanding the Entity and Its Environment and Assessing the Risks of Material Misstatement (Supersedes SAS No. 55.) Source: SAS No. 109.

Sarbanes-Oxley Control Transformation Through Automation

Sarbanes-Oxley Control Transformation Through Automation An Executive White Paper By BLUE LANCE, Inc. Where have we been? Where are we going? BLUE LANCE INC. www.bluelance.com 713.255.4800 [email protected]

Sarbanes-Oxley Control Transformation Through Automation An Executive White Paper By BLUE LANCE, Inc. Where have we been? Where are we going? BLUE LANCE INC. www.bluelance.com 713.255.4800 [email protected]

COSO Internal Control Integrated Framework (2013)

") COSO Internal Control Integrated Framework (2013) The Committee of Sponsoring Organizations of the Treadway Commission (COSO) released its updated Internal Control Integrated Framework (2013 Framework)

COSO Internal Control Integrated Framework (2013) The Committee of Sponsoring Organizations of the Treadway Commission (COSO) released its updated Internal Control Integrated Framework (2013 Framework)

February 2015. Sample audit committee charter

February 2015 Sample audit committee charter Sample audit committee charter This sample audit committee charter is based on observations of selected companies and the requirements of the SEC, the NYSE,

February 2015 Sample audit committee charter Sample audit committee charter This sample audit committee charter is based on observations of selected companies and the requirements of the SEC, the NYSE,

Guide to the Sarbanes-Oxley Act: IT Risks and Controls. Frequently Asked Questions

Guide to the Sarbanes-Oxley Act: IT Risks and Controls Frequently Asked Questions Table of Contents Page No. Introduction.......................................................................1 Overall

Guide to the Sarbanes-Oxley Act: IT Risks and Controls Frequently Asked Questions Table of Contents Page No. Introduction.......................................................................1 Overall

Performing Audit Procedures in Response to Assessed Risks and Evaluating the Audit Evidence Obtained

Performing Audit Procedures in Response to Assessed Risks 1781 AU Section 318 Performing Audit Procedures in Response to Assessed Risks and Evaluating the Audit Evidence Obtained (Supersedes SAS No. 55.)

Performing Audit Procedures in Response to Assessed Risks 1781 AU Section 318 Performing Audit Procedures in Response to Assessed Risks and Evaluating the Audit Evidence Obtained (Supersedes SAS No. 55.)

Module 6 Documenting Processes and Controls

A logical place to begin any comprehensive evaluation of internal controls is at the top entity-level controls that might have a pervasive effect on the organization. This includes a consideration of factors

A logical place to begin any comprehensive evaluation of internal controls is at the top entity-level controls that might have a pervasive effect on the organization. This includes a consideration of factors

RISK BASED AUDITING: A VALUE ADD PROPOSITION. Participant Guide

RISK BASED AUDITING: A VALUE ADD PROPOSITION Participant Guide About This Course About This Course Adding Value for Risk-based Auditing Seminar Description In this seminar, we will focus on: The foundation

RISK BASED AUDITING: A VALUE ADD PROPOSITION Participant Guide About This Course About This Course Adding Value for Risk-based Auditing Seminar Description In this seminar, we will focus on: The foundation

ACCA P1 Internal Control. incorporated into Combined code, it was last revised in 2005 and still present as a standalone document.

Internal Control ACCA P1 Internal Control Turnbull Report 1999 provided guidance for creating strong internal control system and later incorporated into Combined code, it was last revised in 2005 and still

Internal Control ACCA P1 Internal Control Turnbull Report 1999 provided guidance for creating strong internal control system and later incorporated into Combined code, it was last revised in 2005 and still

INFORMATION TECHNOLOGY CONTROLS

CHAPTER 14 INFORMATION TECHNOLOGY CONTROLS SCOPE This chapter addresses requirements common to all financial accounting systems and is not limited to the statewide financial accounting system, ENCOMPASS,

CHAPTER 14 INFORMATION TECHNOLOGY CONTROLS SCOPE This chapter addresses requirements common to all financial accounting systems and is not limited to the statewide financial accounting system, ENCOMPASS,

The Committee of Sponsoring Organizations of the Treadway Commission

The Committee of Sponsoring Organizations of the Treadway Commission Request for Proposal to Develop Additional Application Guidance on Monitoring, Including Tools and Techniques October 17, 2006 The Committee

The Committee of Sponsoring Organizations of the Treadway Commission Request for Proposal to Develop Additional Application Guidance on Monitoring, Including Tools and Techniques October 17, 2006 The Committee

MEMORANDUM INTERNAL CONTROL REQUIREMENTS FOR NON-PROFITS

DIVISION OF CHILD CARE AND EARLY CHILDHOOD EDUCATION HEALTH AND NUTRITION UNIT P O BOX 1437, SLOT S 155 501-320-8982 FAX: 501-682-2334 TDD: 501-682-1550 TO: NON-PROFIT INSTITUTIONS FROM: HEALTH AND NUTRITION

DIVISION OF CHILD CARE AND EARLY CHILDHOOD EDUCATION HEALTH AND NUTRITION UNIT P O BOX 1437, SLOT S 155 501-320-8982 FAX: 501-682-2334 TDD: 501-682-1550 TO: NON-PROFIT INSTITUTIONS FROM: HEALTH AND NUTRITION

[300] Accounting and internal control systems and audit risk assessments

![[300] Accounting and internal control systems and audit risk assessments](/thumbs/25/6464424.jpg "[300] Accounting and internal control systems and audit risk assessments") [300] Accounting and internal control systems and audit risk assessments (Issued March 1995) Contents Paragraphs Introduction 1 12 Inherent risk 13 15 Accounting system and control environment 16 23 Internal

[300] Accounting and internal control systems and audit risk assessments (Issued March 1995) Contents Paragraphs Introduction 1 12 Inherent risk 13 15 Accounting system and control environment 16 23 Internal

Sarbanes-Oxley Section 404: Management s Assessment Process

Sarbanes-Oxley Section 404: Management s Assessment Process Frequently Asked Questions ADVISORY Contents 1 Introduction 2 Providing a Road Map for Management 3 Questions and Answers 3 Section I. Planning

Sarbanes-Oxley Section 404: Management s Assessment Process Frequently Asked Questions ADVISORY Contents 1 Introduction 2 Providing a Road Map for Management 3 Questions and Answers 3 Section I. Planning

How to set up a people based. accounting system that makes your. small business work for you. Thomas G. Post. Certified Public Accountant 281-351-2688

How to set up a people based accounting system that makes your small business work for you. By Thomas G. Post Certified Public Accountant 281-351-2688 www.texastaxman.com 1 Title How to set up a people

How to set up a people based accounting system that makes your small business work for you. By Thomas G. Post Certified Public Accountant 281-351-2688 www.texastaxman.com 1 Title How to set up a people

COSO 2013: WHAT HAS CHANGED & STEPS TO TAKE TO ENSURE COMPLIANCE

COSO 2013: WHAT HAS CHANGED & STEPS TO TAKE TO ENSURE COMPLIANCE COMMITTEE OF SPONSORING ORGANIZATIONS (COSO) 2013 The Committee of Sponsoring Organizations (COSO) Internal Controls Integrated Framework,

COSO 2013: WHAT HAS CHANGED & STEPS TO TAKE TO ENSURE COMPLIANCE COMMITTEE OF SPONSORING ORGANIZATIONS (COSO) 2013 The Committee of Sponsoring Organizations (COSO) Internal Controls Integrated Framework,

Hand IN Hand: Balanced Scorecards

ANNUAL CONFERENCE T O P I C Risk Management WORKING Hand IN Hand: Balanced Scorecards AND Enterprise Risk Management B Y M ARK B EASLEY, CPA; A L C HEN; K AREN N UNEZ, CMA; AND L ORRAINE W RIGHT Recent

ANNUAL CONFERENCE T O P I C Risk Management WORKING Hand IN Hand: Balanced Scorecards AND Enterprise Risk Management B Y M ARK B EASLEY, CPA; A L C HEN; K AREN N UNEZ, CMA; AND L ORRAINE W RIGHT Recent

Fraud Control Theory

13 Fraud Control Theory Using a variation of a saying from the 1960s, fraud happens. Like all costs of doing business, fraud must be managed. Management must recognize that people commit fraudulent acts

13 Fraud Control Theory Using a variation of a saying from the 1960s, fraud happens. Like all costs of doing business, fraud must be managed. Management must recognize that people commit fraudulent acts

CYBER SUPPLY INC. (Exact name of registrant as specified in its charter)

") UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K/A-1 [X] ANNUAL REPORT UNDER TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended February

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K/A-1 [X] ANNUAL REPORT UNDER TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended February

INTERNATIONAL STANDARDS FOR THE PROFESSIONAL PRACTICE OF INTERNAL AUDITING (STANDARDS)

") INTERNATIONAL STANDARDS FOR THE PROFESSIONAL PRACTICE OF INTERNAL AUDITING (STANDARDS) Revised: October 2012 i Table of contents Attribute Standards... 3 1000 Purpose, Authority, and Responsibility...

INTERNATIONAL STANDARDS FOR THE PROFESSIONAL PRACTICE OF INTERNAL AUDITING (STANDARDS) Revised: October 2012 i Table of contents Attribute Standards... 3 1000 Purpose, Authority, and Responsibility...

COSO Framework 2013 & SOX Compliance. Roxanne L. Halverson, CISM, CGEIT Atlanta ISACA Geek Week August 19, 2013

COSO Framework 2013 & SOX Compliance Roxanne L. Halverson, CISM, CGEIT Atlanta ISACA Geek Week August 19, 2013 What s Happened On May 14, 2013, after a little more than 20 years the Committee of Sponsoring

COSO Framework 2013 & SOX Compliance Roxanne L. Halverson, CISM, CGEIT Atlanta ISACA Geek Week August 19, 2013 What s Happened On May 14, 2013, after a little more than 20 years the Committee of Sponsoring

GUIDANCE NOTE FOR DEPOSIT-TAKERS. Operational Risk Management. March 2012

GUIDANCE NOTE FOR DEPOSIT-TAKERS Operational Risk Management March 2012 Version 1.0 Contents Page No 1 Introduction 2 2 Overview 3 Operational risk - fundamental principles and governance 3 Fundamental

GUIDANCE NOTE FOR DEPOSIT-TAKERS Operational Risk Management March 2012 Version 1.0 Contents Page No 1 Introduction 2 2 Overview 3 Operational risk - fundamental principles and governance 3 Fundamental

Chapter 15 Auditing the Expenditure Cycle

Chapter 15 Auditing the Expenditure Cycle Expenditure cycle consists of activities related to the acquisition of and payment for plant assets and goods and services. Two major transaction classes: 1 purchases

Chapter 15 Auditing the Expenditure Cycle Expenditure cycle consists of activities related to the acquisition of and payment for plant assets and goods and services. Two major transaction classes: 1 purchases

Executive - Salary Guide

Salary Guide Executive - Salary Guide Chief Financial Officer $138,000 to $250,000+ Highest ranking financially-oriented position within a company. Responsibilities include overall financial control and

Salary Guide Executive - Salary Guide Chief Financial Officer $138,000 to $250,000+ Highest ranking financially-oriented position within a company. Responsibilities include overall financial control and

On the Setting of the Standards and Practice Standards for. Management Assessment and Audit concerning Internal

(Provisional translation) On the Setting of the Standards and Practice Standards for Management Assessment and Audit concerning Internal Control Over Financial Reporting (Council Opinions) Released on

(Provisional translation) On the Setting of the Standards and Practice Standards for Management Assessment and Audit concerning Internal Control Over Financial Reporting (Council Opinions) Released on

1. FPO. Guide to the Sarbanes-Oxley Act: IT Risks and Controls. Second Edition

1. FPO Guide to the Sarbanes-Oxley Act: IT Risks and Controls Second Edition Table of Contents Introduction... 1 Overall IT Risk and Control Approach and Considerations When Complying with Sarbanes-Oxley...

1. FPO Guide to the Sarbanes-Oxley Act: IT Risks and Controls Second Edition Table of Contents Introduction... 1 Overall IT Risk and Control Approach and Considerations When Complying with Sarbanes-Oxley...

COSO 2013 Internal Control Integrated Framework FRED J. PETERSON, PARTNER MOSS ADAMS LLP

COSO 2013 Internal Control Integrated Framework FRED J. PETERSON, PARTNER MOSS ADAMS LLP Disclaimer The material appearing in this presentation is for informational purposes only and should not be construed

COSO 2013 Internal Control Integrated Framework FRED J. PETERSON, PARTNER MOSS ADAMS LLP Disclaimer The material appearing in this presentation is for informational purposes only and should not be construed

How To Understand The Role Of An Internal Audit

Top Ten Issues facing Internal Auditing in the Future The IIA Dallas Chapter April 6, 2006 Presented by: David A. Richards, CIA, CPA President The Institute of Internal Auditors [email protected] 1

Top Ten Issues facing Internal Auditing in the Future The IIA Dallas Chapter April 6, 2006 Presented by: David A. Richards, CIA, CPA President The Institute of Internal Auditors [email protected] 1

An Examination of an Entity s Internal Control Over Financial Reporting That Is Integrated With an Audit of Its Financial Statements

Examination of an Entity s Internal Control 1403 AT Section 501 An Examination of an Entity s Internal Control Over Financial Reporting That Is Integrated With an Audit of Its Financial Statements Source:

Examination of an Entity s Internal Control 1403 AT Section 501 An Examination of an Entity s Internal Control Over Financial Reporting That Is Integrated With an Audit of Its Financial Statements Source:

The Importance of IT Controls to Sarbanes-Oxley Compliance

Hosted by Deloitte, PricewaterhouseCoopers and ISACA/ITGI The Importance of IT Controls to Sarbanes-Oxley Compliance 15 December 2003 1 Presenters Chris Fox, CA Sr. Manager, Internal Audit Services PricewaterhouseCoopers

Hosted by Deloitte, PricewaterhouseCoopers and ISACA/ITGI The Importance of IT Controls to Sarbanes-Oxley Compliance 15 December 2003 1 Presenters Chris Fox, CA Sr. Manager, Internal Audit Services PricewaterhouseCoopers

P L A N A D V I S O R Y. The Importance of Internal Controls in Financial Reporting and Safeguarding Plan Assets

P L A N A D V I S O R Y The Importance of Internal Controls in Financial Reporting and Safeguarding Plan Assets P L A N A D V I S O R Y Table of Contents Introduction 3 Why Internal Control Is Important

P L A N A D V I S O R Y The Importance of Internal Controls in Financial Reporting and Safeguarding Plan Assets P L A N A D V I S O R Y Table of Contents Introduction 3 Why Internal Control Is Important

6/8/2016 OVERVIEW. Page 1 of 9

OVERVIEW Attachment Supervisory Guidance for Assessing Risk Management at Supervised Institutions with Total Consolidated Assets Less than $50 Billion [Fotnote1 6/8/2016 Managing risks is fundamental to

OVERVIEW Attachment Supervisory Guidance for Assessing Risk Management at Supervised Institutions with Total Consolidated Assets Less than $50 Billion [Fotnote1 6/8/2016 Managing risks is fundamental to

GAO. Standards for Internal Control in the Federal Government. Internal Control. United States General Accounting Office.

GAO United States General Accounting Office Internal Control November 1999 Standards for Internal Control in the Federal Government GAO/AIMD-00-21.3.1 Foreword Federal policymakers and program managers

GAO United States General Accounting Office Internal Control November 1999 Standards for Internal Control in the Federal Government GAO/AIMD-00-21.3.1 Foreword Federal policymakers and program managers

Implementing Internal Controls over Executive Compensation Creating a Sustainable Compensation Control Environment

NASPP Implementing Internal Controls over Executive Compensation Creating a Sustainable Compensation Control Environment Michael S. Kesner, Principal Sustainable Compensation Control Environment Tone At

NASPP Implementing Internal Controls over Executive Compensation Creating a Sustainable Compensation Control Environment Michael S. Kesner, Principal Sustainable Compensation Control Environment Tone At

Guide to Public Company Auditing

Guide to Public Company Auditing The Center for Audit Quality (CAQ) prepared this Guide to Public Company Auditing to provide an introduction to and overview of the key processes, participants and issues

Guide to Public Company Auditing The Center for Audit Quality (CAQ) prepared this Guide to Public Company Auditing to provide an introduction to and overview of the key processes, participants and issues

Impact of New Internal Control Frameworks

Impact of New Internal Control Frameworks Webcast: Tuesday, February 25, 2014 CPE Credit: 1 0 With You Today Bob Jacobson Principal, Risk Advisory Services Consulting Leader West Region [email protected]

Impact of New Internal Control Frameworks Webcast: Tuesday, February 25, 2014 CPE Credit: 1 0 With You Today Bob Jacobson Principal, Risk Advisory Services Consulting Leader West Region [email protected]

Control Environment Questionnaire

Control Environment Questionnaire Internal Control Questionnaire Question Yes No N/A Remarks INTEGRITY AND ETHICAL VALUES Management must convey the message that integrity and ethical values cannot be

Control Environment Questionnaire Internal Control Questionnaire Question Yes No N/A Remarks INTEGRITY AND ETHICAL VALUES Management must convey the message that integrity and ethical values cannot be

AUDITING AND ITS ROLE IN CORPORATE GOVERNANCE

AUDITING AND ITS ROLE IN CORPORATE GOVERNANCE Bank for International Settlements FSI Seminar on Corporate Governance for Banks 20 June 2006 Derek Broadley Deloitte Touche Tohmatsu, Hong Kong 1 Corporate

AUDITING AND ITS ROLE IN CORPORATE GOVERNANCE Bank for International Settlements FSI Seminar on Corporate Governance for Banks 20 June 2006 Derek Broadley Deloitte Touche Tohmatsu, Hong Kong 1 Corporate

CHAPTER 11 COMPUTER SYSTEMS INFORMATION TECHNOLOGY SERVICES CONTROLS

11-1 CHAPTER 11 COMPUTER SYSTEMS INFORMATION TECHNOLOGY SERVICES CONTROLS INTRODUCTION The State Board of Accounts, in accordance with State statutes and the Statements on Auditing Standards Numbers 78

11-1 CHAPTER 11 COMPUTER SYSTEMS INFORMATION TECHNOLOGY SERVICES CONTROLS INTRODUCTION The State Board of Accounts, in accordance with State statutes and the Statements on Auditing Standards Numbers 78

Communicating Internal Control Related Matters Identified in an Audit

Communicating Internal Control Related Matters 227 AU-C Section 265 Communicating Internal Control Related Matters Identified in an Audit Source: SAS No. 122; SAS No. 125; SAS No. 128. See section 9265

Communicating Internal Control Related Matters 227 AU-C Section 265 Communicating Internal Control Related Matters Identified in an Audit Source: SAS No. 122; SAS No. 125; SAS No. 128. See section 9265

February 2015. Audit committee performance evaluation

February 2015 Audit committee performance evaluation Audit committee performance evaluation The following questionnaire is based on emerging and leading practices to assist in the self-assessment of an

February 2015 Audit committee performance evaluation Audit committee performance evaluation The following questionnaire is based on emerging and leading practices to assist in the self-assessment of an

Integrated Approach Model of Risk, Control and Auditing of Accounting Information Systems

Informatica Economică vol. 17, no. 4/2013 87 Integrated Approach Model of Risk, Control and Auditing of Accounting Information Systems Claudiu BRANDAS, Dan STIRBU, Otniel DIDRAGA West University of Timisoara,

Informatica Economică vol. 17, no. 4/2013 87 Integrated Approach Model of Risk, Control and Auditing of Accounting Information Systems Claudiu BRANDAS, Dan STIRBU, Otniel DIDRAGA West University of Timisoara,

A Sarbanes-Oxley Roadmap to Business Continuity

A Sarbanes-Oxley Roadmap to Business Continuity NEDRIX Conference June 23, 2004 Dr. Eric Schmidt [email protected] Control Solutions International TECHNOLOGY ADVISORY, ASSURANCE & RISK MANAGEMENT

A Sarbanes-Oxley Roadmap to Business Continuity NEDRIX Conference June 23, 2004 Dr. Eric Schmidt [email protected] Control Solutions International TECHNOLOGY ADVISORY, ASSURANCE & RISK MANAGEMENT

Best Practices for Nonprofits Internal Control Self-Assessment

Advances in Management & Applied Economics, vol. 4, no.1, 2014, 41-87 ISSN: 1792-7544 (print version), 1792-7552(online) Scienpress Ltd, 2014 Best Practices for Nonprofits Internal Control Self-Assessment

Advances in Management & Applied Economics, vol. 4, no.1, 2014, 41-87 ISSN: 1792-7544 (print version), 1792-7552(online) Scienpress Ltd, 2014 Best Practices for Nonprofits Internal Control Self-Assessment

Corporate Governance and Enterprise Risk Management Derek Jackson, Senior Manager 5 September 2005

Corporate Governance and Enterprise Risk Management Derek Jackson, Senior Manager 5 September 2005 Corporate Governance Services 0 Overview Hong Kong Code on Corporate Governance Practices Corporate Governance

Corporate Governance and Enterprise Risk Management Derek Jackson, Senior Manager 5 September 2005 Corporate Governance Services 0 Overview Hong Kong Code on Corporate Governance Practices Corporate Governance

Sarbanes-Oxley Compliance Workbook. From Zero to SOX. Sarbanes-Oxley Compliance Workbook. sensiba san filippo www.ssfllp.com sox@ssfllp.

From Zero to SOX Zero to SOX An Overview The goals of a program to meet SOX 404 requirements go far beyond compliance. The process of building a sustainable, comprehensive internal control environment

From Zero to SOX Zero to SOX An Overview The goals of a program to meet SOX 404 requirements go far beyond compliance. The process of building a sustainable, comprehensive internal control environment

KANSAS CITY, MISSOURI RESPONSES TO THE FISCAL YEAR 2013 AUDIT MANAGEMENT LETTER

KANSAS CITY, MISSOURI RESPONSES TO THE FISCAL YEAR 2013 AUDIT MANAGEMENT LETTER Material Weaknesses (0) No material weaknesses were reported for FY 2013. Significant Deficiencies (1) Grant Receivable Accounting

KANSAS CITY, MISSOURI RESPONSES TO THE FISCAL YEAR 2013 AUDIT MANAGEMENT LETTER Material Weaknesses (0) No material weaknesses were reported for FY 2013. Significant Deficiencies (1) Grant Receivable Accounting

Internal Control - Integrated Framework

Internal Control - Integrated Framework Executive Summary Senior executives have long sought ways to better control the enterprises they run. Internal controls are put in place to keep the company on course

Internal Control - Integrated Framework Executive Summary Senior executives have long sought ways to better control the enterprises they run. Internal controls are put in place to keep the company on course

Audit of the Policy on Internal Control Implementation

Audit of the Policy on Internal Control Implementation Natural Sciences and Engineering Research Council of Canada Social Sciences and Humanities Research Council of Canada February 18, 2013 1 TABLE OF

Audit of the Policy on Internal Control Implementation Natural Sciences and Engineering Research Council of Canada Social Sciences and Humanities Research Council of Canada February 18, 2013 1 TABLE OF

UNITED STATES DEPARTMENT OF EDUCATION OFFICE OF INSPECTOR GENERAL

UNITED STATES DEPARTMENT OF EDUCATION OFFICE OF INSPECTOR GENERAL Evaluation and Inspection Services Memorandum May 5, 2009 TO: FROM: SUBJECT: James Manning Acting Chief Operating Officer Federal Student

UNITED STATES DEPARTMENT OF EDUCATION OFFICE OF INSPECTOR GENERAL Evaluation and Inspection Services Memorandum May 5, 2009 TO: FROM: SUBJECT: James Manning Acting Chief Operating Officer Federal Student

Enterprise Risk Management

Enterprise Risk Management Topic Gateway Series No. 49 1 Prepared by Jasmin Harvey and Technical Information Service July 2008 About Topic Gateways Topic Gateways are intended as a refresher or introduction

Enterprise Risk Management Topic Gateway Series No. 49 1 Prepared by Jasmin Harvey and Technical Information Service July 2008 About Topic Gateways Topic Gateways are intended as a refresher or introduction

How To Audit A Financial Statement

INTERNATIONAL STANDARD ON 400 RISK ASSESSMENTS AND INTERNAL CONTROL (This Standard is effective, but will be withdrawn when ISA 315 and 330 become effective) * CONTENTS Paragraph Introduction... 1-10 Inherent

INTERNATIONAL STANDARD ON 400 RISK ASSESSMENTS AND INTERNAL CONTROL (This Standard is effective, but will be withdrawn when ISA 315 and 330 become effective) * CONTENTS Paragraph Introduction... 1-10 Inherent

THE SOUTH AFRICAN HERITAGE RESOURCES AGENCY ENTERPRISE RISK MANAGEMENT FRAMEWORK

THE SOUTH AFRICAN HERITAGE RESOURCES AGENCY ENTERPRISE RISK MANAGEMENT FRAMEWORK ACCOUNTABLE SIGNATURE AUTHORISED for implementation SIGNATURE On behalf of Chief Executive Officer SAHRA Council Date Date

THE SOUTH AFRICAN HERITAGE RESOURCES AGENCY ENTERPRISE RISK MANAGEMENT FRAMEWORK ACCOUNTABLE SIGNATURE AUTHORISED for implementation SIGNATURE On behalf of Chief Executive Officer SAHRA Council Date Date

INTERNAL ROUTINE AND CONTROLS Section 4.2

INTRODUCTION... 2 INTERNAL CONTROL SYSTEMS... 2 Key Control System Components... 2 Control Environment... 2 Risk Assessments... 2 Control Activities... 3 Information and Communication... 3 Monitoring...

INTRODUCTION... 2 INTERNAL CONTROL SYSTEMS... 2 Key Control System Components... 2 Control Environment... 2 Risk Assessments... 2 Control Activities... 3 Information and Communication... 3 Monitoring...

The Role of the Board in Enterprise Risk Management

Enterprise Risk The Role of the Board in Enterprise Risk Management The board of directors plays an essential role in ensuring that an effective ERM program is in place. Governance, policy, and assurance

Enterprise Risk The Role of the Board in Enterprise Risk Management The board of directors plays an essential role in ensuring that an effective ERM program is in place. Governance, policy, and assurance

Successfully identifying, assessing and managing risks for stakeholders

Introduction Names like Enron, Worldcom, Barings Bank and Menu Foods are household names but unfortunately as examples of what can go wrong. With these recent high profile business failures, people have

Introduction Names like Enron, Worldcom, Barings Bank and Menu Foods are household names but unfortunately as examples of what can go wrong. With these recent high profile business failures, people have

APPLICATION OF THE KING III REPORT ON CORPORATE GOVERNANCE PRINCIPLES

APPLICATION OF THE KING III REPORT ON CORPORATE GOVERNANCE PRINCIPLES Ethical Leadership and Corporate Citizenship The board should provide effective leadership based on ethical foundation. that the company

APPLICATION OF THE KING III REPORT ON CORPORATE GOVERNANCE PRINCIPLES Ethical Leadership and Corporate Citizenship The board should provide effective leadership based on ethical foundation. that the company

Employee Performance Review

Employee Performance Review Source: Learn to Read, Inc. Review Date: Date of Last Review: Employment Date: Name: Title: Reports to: Expectation Basis Leadership Readily assumes responsibility for projects

Employee Performance Review Source: Learn to Read, Inc. Review Date: Date of Last Review: Employment Date: Name: Title: Reports to: Expectation Basis Leadership Readily assumes responsibility for projects

Internal/External Audits

Internal/External Audits Joint World Bank/Federal Reserve System Seminar for Senior Bank Supervisors Arthur Lindo Federal Reserve Board Presentation Topics ❿Internal Audit, Corporate Governance and Controls

Internal/External Audits Joint World Bank/Federal Reserve System Seminar for Senior Bank Supervisors Arthur Lindo Federal Reserve Board Presentation Topics ❿Internal Audit, Corporate Governance and Controls

PART 10 COMPUTER SYSTEMS

PART 10 COMPUTER SYSTEMS 10-1 PART 10 COMPUTER SYSTEMS The following is a general outline of steps to follow when contemplating the purchase of data processing hardware and/or software. The State Board

PART 10 COMPUTER SYSTEMS 10-1 PART 10 COMPUTER SYSTEMS The following is a general outline of steps to follow when contemplating the purchase of data processing hardware and/or software. The State Board

Ten Steps to SOX Compliance for Smaller Public Companies

Presented by: Bob Benoit Lord & Benoit, LLC One West Boylston St. Worcester, MA 01605 (508) 853-6404 Ten Steps to SOX Compliance for Smaller Public Companies Team IT Controls Timeline Effectiveness Of

Presented by: Bob Benoit Lord & Benoit, LLC One West Boylston St. Worcester, MA 01605 (508) 853-6404 Ten Steps to SOX Compliance for Smaller Public Companies Team IT Controls Timeline Effectiveness Of

Transmittal Letter... 1. Objectives and Scope... 2. Approach... 3-7. Financial System... 8. Permitting Application... 9

Internal Audit Committee of Information Technology Risk Assessment Public Report Prepared By: Internal Auditors of Brevard County September 30, 2009 Table of Contents Transmittal Letter... 1 Objectives

Internal Audit Committee of Information Technology Risk Assessment Public Report Prepared By: Internal Auditors of Brevard County September 30, 2009 Table of Contents Transmittal Letter... 1 Objectives

ETHICS, FRAUD, AND INTERNAL CONTROL

CHAPTER ETHICS, FRAUD, AND INTERNAL CONTROL The three topics of this chapter are closely related. Ethics is a hallmark of the accounting profession. The principles which guide a manager s decision making

CHAPTER ETHICS, FRAUD, AND INTERNAL CONTROL The three topics of this chapter are closely related. Ethics is a hallmark of the accounting profession. The principles which guide a manager s decision making

Using COBiT For Sarbanes Oxley. Japan November 18 th 2006 Gary A Bannister

Using COBiT For Sarbanes Oxley Japan November 18 th 2006 Gary A Bannister Who Am I? Who am I & What I Do? I am an accountant with 28 years experience working in various International Control & IT roles.

Using COBiT For Sarbanes Oxley Japan November 18 th 2006 Gary A Bannister Who Am I? Who am I & What I Do? I am an accountant with 28 years experience working in various International Control & IT roles.

AMPLIFY SNACK BRANDS, INC. AUDIT COMMITTEE CHARTER. Adopted June 25, 2015

AMPLIFY SNACK BRANDS, INC. AUDIT COMMITTEE CHARTER Adopted June 25, 2015 I. General Statement of Purpose The purposes of the Audit Committee of the Board of Directors (the Audit Committee ) of Amplify

AMPLIFY SNACK BRANDS, INC. AUDIT COMMITTEE CHARTER Adopted June 25, 2015 I. General Statement of Purpose The purposes of the Audit Committee of the Board of Directors (the Audit Committee ) of Amplify

CHARTER OF THE AUDIT COMMITTEE OF THE BOARD OF DIRECTORS OF SERVICEMASTER GLOBAL HOLDINGS, INC.

CHARTER OF THE AUDIT COMMITTEE OF THE BOARD OF DIRECTORS OF SERVICEMASTER GLOBAL HOLDINGS, INC. Adopted by the Board of Directors on July 24, 2007; and as amended June 13, 2014. Pursuant to duly adopted

CHARTER OF THE AUDIT COMMITTEE OF THE BOARD OF DIRECTORS OF SERVICEMASTER GLOBAL HOLDINGS, INC. Adopted by the Board of Directors on July 24, 2007; and as amended June 13, 2014. Pursuant to duly adopted

Advisory Guidelines of the Financial Supervisory Authority. Requirements regarding the arrangement of operational risk management

Advisory Guidelines of the Financial Supervisory Authority Requirements regarding the arrangement of operational risk management These Advisory Guidelines have established by resolution no. 63 of the Management

Advisory Guidelines of the Financial Supervisory Authority Requirements regarding the arrangement of operational risk management These Advisory Guidelines have established by resolution no. 63 of the Management

INTERNATIONAL STANDARDS FOR THE PROFESSIONAL PRACTICE OF INTERNAL AUDITING (STANDARDS)

") INTERNATIONAL STANDARDS FOR THE PROFESSIONAL PRACTICE OF INTERNAL AUDITING (STANDARDS) Introduction to the International Standards Internal auditing is conducted in diverse legal and cultural environments;

INTERNATIONAL STANDARDS FOR THE PROFESSIONAL PRACTICE OF INTERNAL AUDITING (STANDARDS) Introduction to the International Standards Internal auditing is conducted in diverse legal and cultural environments;

How To Ensure Internal Control Of Financial Reporting In India

PROTIVITI FLASH REPORT New Internal Control Requirements for Companies with Operations in India November 9, 2015 In the aftermath of major global financial frauds, several countries enacted legislation

PROTIVITI FLASH REPORT New Internal Control Requirements for Companies with Operations in India November 9, 2015 In the aftermath of major global financial frauds, several countries enacted legislation

Escrow Accounting and Internal Controls

Escrow Accounting and Internal Controls Nicole Thomas Deloitte & Touche, LLP 2012 Ohio TIPS Seminar November 12, 2012 Agenda Deloitte at a glance Importance of internal controls Escrow/trust accounting

Escrow Accounting and Internal Controls Nicole Thomas Deloitte & Touche, LLP 2012 Ohio TIPS Seminar November 12, 2012 Agenda Deloitte at a glance Importance of internal controls Escrow/trust accounting

The Updated COSO Internal Control Framework

The Updated COSO Internal Control Framework Frequently Asked Questions Second Edition Introduction The Committee of Sponsoring Organizations of the Treadway Commission (COSO) an organization providing

The Updated COSO Internal Control Framework Frequently Asked Questions Second Edition Introduction The Committee of Sponsoring Organizations of the Treadway Commission (COSO) an organization providing

UCLA Policy 360: Internal Control Guidelines for Campus Departments

UCLA Policy 360: Internal Control Guidelines for Campus Departments Issuing Officer: Assistant Vice Chancellor, Corporate Financial Services Responsible Dept: Financial Management Programs Effective Date:

UCLA Policy 360: Internal Control Guidelines for Campus Departments Issuing Officer: Assistant Vice Chancellor, Corporate Financial Services Responsible Dept: Financial Management Programs Effective Date:

Introduction to Enterprise Risk Management at UVM DRAFT

Introduction to Enterprise Management at UVM 1 Enterprise What is Enterprise Management? Enterprise risk management is a structured, consistent, and continuous process across the whole organization for

Introduction to Enterprise Management at UVM 1 Enterprise What is Enterprise Management? Enterprise risk management is a structured, consistent, and continuous process across the whole organization for

BAKER HUGHES INCORPORATED. CHARTER OF THE AUDIT/ETHICS COMMITTEE OF THE BOARD OF DIRECTORS (as amended and restated October 24, 2012)

") BAKER HUGHES INCORPORATED CHARTER OF THE AUDIT/ETHICS COMMITTEE OF THE BOARD OF DIRECTORS (as amended and restated October 24, 2012) The Board of Directors of Baker Hughes Incorporated (the Company ) has

BAKER HUGHES INCORPORATED CHARTER OF THE AUDIT/ETHICS COMMITTEE OF THE BOARD OF DIRECTORS (as amended and restated October 24, 2012) The Board of Directors of Baker Hughes Incorporated (the Company ) has

Integrated Risk Management:

Integrated Risk Management: A Framework for Fraser Health For further information contact: Integrated Risk Management Fraser Health Corporate Office 300, 10334 152A Street Surrey, BC V3R 8T4 Phone: (604)

Integrated Risk Management: A Framework for Fraser Health For further information contact: Integrated Risk Management Fraser Health Corporate Office 300, 10334 152A Street Surrey, BC V3R 8T4 Phone: (604)

Internal Control Systems and Maintenance of Accounting and Other Records for Interactive Gaming & Interactive Wagering Corporations (IGIWC)

") Internal Control Systems and Maintenance of Accounting and Other Records for Interactive Gaming & Interactive Wagering Corporations (IGIWC) 1 Introduction 1.1 Section 316 (4) of the International Business

Internal Control Systems and Maintenance of Accounting and Other Records for Interactive Gaming & Interactive Wagering Corporations (IGIWC) 1 Introduction 1.1 Section 316 (4) of the International Business

Internal Control Systems

Business and Information Process Rules, Risks, and Controls Internal Control Systems Internal controls encompass a set of rules, policies, and procedures an organization implements to provide reasonable

Business and Information Process Rules, Risks, and Controls Internal Control Systems Internal controls encompass a set of rules, policies, and procedures an organization implements to provide reasonable

Chapter 9 The Study of Internal Control and Assessment of Control Risk

Review Questions Chapter 9 The Study of Internal Control and Assessment of Control Risk 9-1 There are seven parts of the planning phase of audits: preplan, obtain background information, obtain information

Review Questions Chapter 9 The Study of Internal Control and Assessment of Control Risk 9-1 There are seven parts of the planning phase of audits: preplan, obtain background information, obtain information

Domain 5 Information Security Governance and Risk Management

Domain 5 Information Security Governance and Risk Management Security Frameworks CobiT (Control Objectives for Information and related Technology), developed by Information Systems Audit and Control Association

Domain 5 Information Security Governance and Risk Management Security Frameworks CobiT (Control Objectives for Information and related Technology), developed by Information Systems Audit and Control Association

Developing an Effective Enterprise Risk Management Program

Developing an Effective Enterprise Risk Management Program Jay Brietz, CPA and CIA Senior Manager This material was used by Elliott Davis Decosimo during an oral presentation; it is not a complete record

Developing an Effective Enterprise Risk Management Program Jay Brietz, CPA and CIA Senior Manager This material was used by Elliott Davis Decosimo during an oral presentation; it is not a complete record