MSME & Asset Based Finance

|

|

|

- Stephany Greer

- 8 years ago

- Views:

Transcription

1 MSME & Asset Based Finance Creating Jobs & Competitiveness Through Finance 5 th Regional Competitiveness Event Sarajevo USAID RCI PFS Michael Gold, Managing Director, Crimson Capital May 19, 2010

2 Background Over 1.3 billion people live on < $1/day Another 1.6 billion people live on < $2/day Poverty and social unrest are increasing, not decreasing Most people in the world are workers and not entrepreneurs Most poor & MSMEs do not have urban real estate to use as collateral MSMEs account for the majority of companies and employment in most countries To dramatically increase employment and decrease poverty, innovative and effective ways to support MSMEs and their growth are needed

3 MSME Access to Finance: Obstacles Financial Institutions (FIs) view MSMEs as more risky, especially rural & agricultural businesses FIs view MSME lending as more costly FIs often depend on urban real estate collateral and historical financial statements in credit assessment Therefore MSMEs and high growth potential enterprises have difficulty obtaining finance from FIs Lending, if available at all, is often mismatched in purpose, type, tenor and required collateral Ironically, once MSMEs obtain finance from FIs, further growth is often impeded, putting them in a straightjacket

4 MSME Access to Finance: Objectives Innovatively finance MSMEs by filling gaps in the market Increase sales and profitability Increase equity through retained earnings Create new employment, maintain employment and increase incomes Support farmers and other small suppliers Support women, minorities and entrepreneurs Increase local production and manufacturing, thereby improving the trade balance Support all sectors including agriculture and all regions Improve quality, competitiveness and sustainability

5 Types of Finance for MSMEs Traditional bank lending Capital markets Asset-based finance

6 Traditional Bank Lending Overdraft financing: short term financing (< 1 year) Overdrafts Lines of credit Term loans/installment loans: medium to long term financing (> 1 year) The underwriting of traditional bank lending often makes it beyond the reach of many farmers and MSMEs but it is the main source of liquidity. Liquidity is usually not the main impediment to increased lending. How can we unleash this liquidity to catalyze growth?

7 Capital Markets Public capital markets: securities (mainly stocks/equities and bonds) offered to the investing public. Private capital markets: securities issued in private markets Venture Capital/Private Equity Strategic Investment Buy-outs Capital market instruments are usually more expensive to develop and labor intensive to manage, and require stronger legal and enforcement regimes for protecting investors. Careful consideration needed for the exit strategy.

8 Asset-based Finance Asset-based finance provides structured working capital and term loans secured by a specific asset. It can open financing for MSMEs that either cannot qualify for traditional bank/mfi loans or whose lending needs exceed what they can obtain from traditional products at a given point in time. Purchase Order Finance (POF) Accounts Receivable (A/R) Financing Factoring Leasing Warehouse Receipts (WHR) Documentary Credit / Guarantees

9 Purchase Order Finance (POF) Short term working capital finance to fill orders Pre-shipment / pre-export Transaction linked (not general line of credit or loan) POF does not require real estate/mortgage as collateral, leaving long term assets as security for long term lending Loan amount typically from 10, ,000 for MSMEs Tenor of days Extremely efficient instrument to create sales and jobs Effective throughout the value chain (from input and equipment suppliers, to producers, processors, distributors, traders, wholesalers, and retailers. It is a powerful tool for unlocking the value-chain s potential) The Places They Go When Banks Say No r.html?pagewanted=1&th&emc=th

The Places They Go When Banks Say No http://www.nytimes.com/2010/01/31/business/smallbusiness/31orde r.html?")

10 Crimson Capital Corp. 2010, all rights reserved. POF Structure

11 Accounts Receivable - A/R What it is: Accounts Receivable (A/R) financing is a revolving line of credit advanced against the A/R, with the amount of credit based on the A/R collection history. Usually offered by banks. Requires: efficient lien registration and bankruptcy systems, economies of scale and verifiable sales relationships between producers and buyers. Applicability: Usually more suited to large, corporate enterprises with large volumes of A/R than to MSMEs.

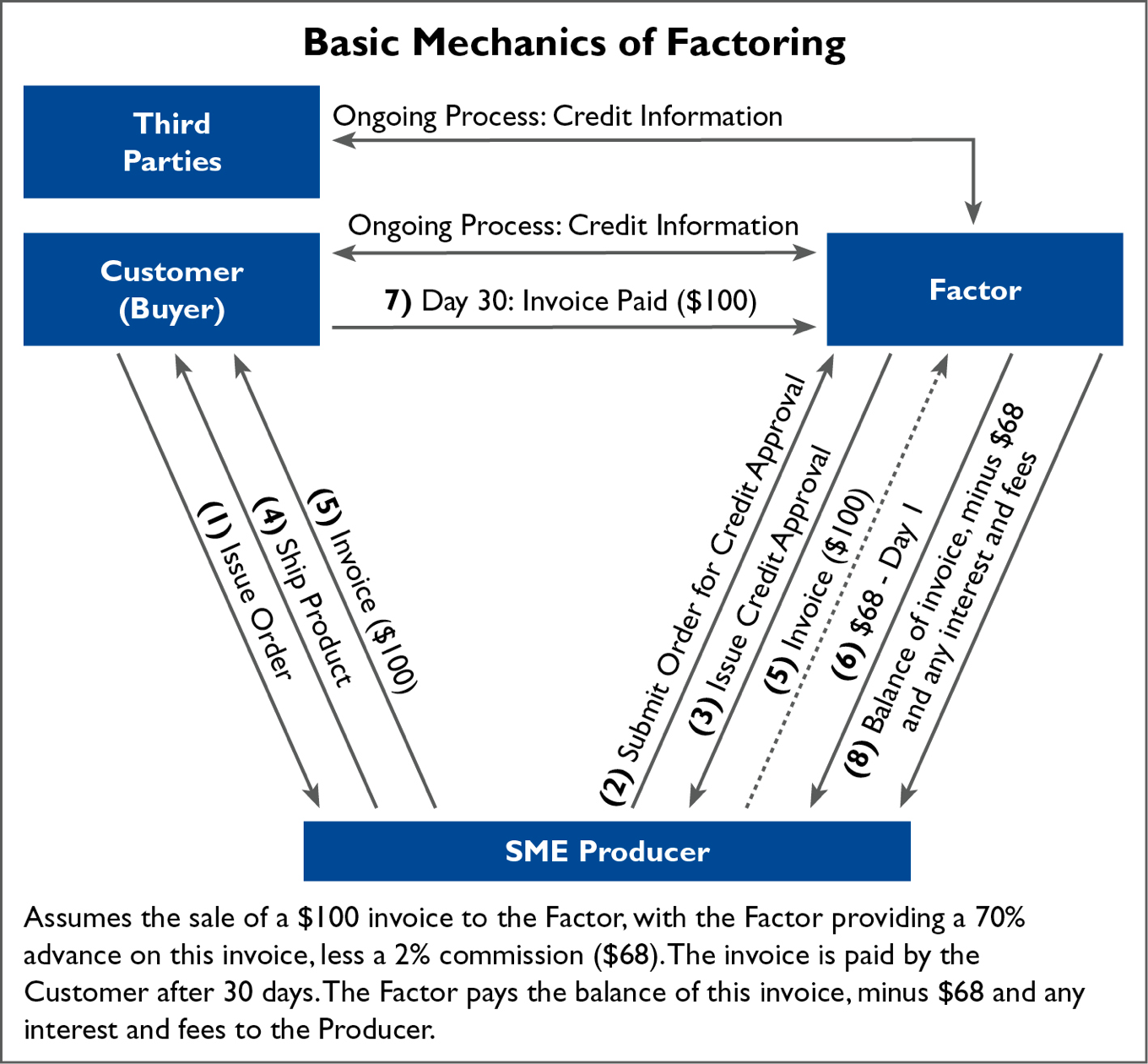

12 Factoring What it is: Factoring provides financing post-shipment, and basically accelerates payment. The enterprise sells its invoice(s) to the financier (called the factor ). The factor then pays the enterprise a percentage of the invoice face value and takes over responsibility for collection. Usually offered by specialized finance companies, not banks. Requires: Some economies of scale to be profitable Access to reliable credit information Applicability: Can be applied with weaker insolvency regimes, but requires excellent access to reliable credit information and certain economies of scale. Generally can be profitably applied to larger enterprises.

13 Factoring

14 Reverse Factoring A variant of factoring known as reverse factoring has been effective in broadening MSME access to finance. In ordinary factoring, because the factor purchases many invoice from a limited number of MSMEs, it must collect credit information and calculate credit risk for a large number of buyers. In reverse factoring, the factor pools and purchases receivables payable from only a few high-quality and/or international buyers and it needs to collect credit information and calculate the credit risk for only a few large, transparent, well-rated firms.

15 Leasing What it is: A contract where the provider (the lessor) owns the asset and grants the client (the lessee) the use of the equipment in exchange for periodic payments. financial leasing: the lease period extends for the asset s useful economic life, and the lessor recovers the full asset value plus interest/fees through regular lease payments. operating leasing: the term of the lease is shorter than the economic life of the asset and only a percentage of the asset s value is recovered over the lease term. More complicated/risky than financial leasing. Applicability: Excellent instrument for financing equipment. Lower risk than term/installment loans. Proper tax treatment important.

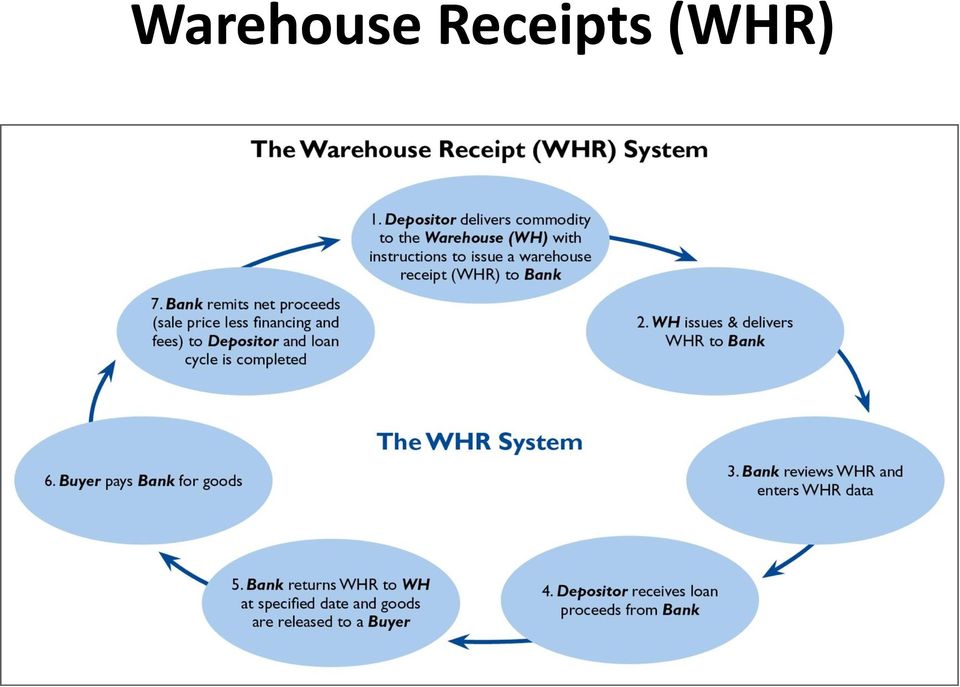

16 Warehouse Receipts (WHR) What it is: A warehouse receipt (WHR) is a document certifying the ownership, existence and availability of a particular quantity, type and quality of commodity in a designated facility, such as a bonded warehouse. Requires: (1) Reasonably well-developed banking system that recognizes the WHR certificate as collateral; (2) System of warehouses with adequate regulation and commodity protection that is trusted by banks; and (3) Accessible, accurate market information. Applicability: Difficult for small-scale producers and MSMEs to access. Capital investment and operating costs require economies of scale.

Accessible, accurate market information.")

17 Warehouse Receipts (WHR)

18 Documentary Credit Letters of Credit (L/C): An obligation taken on by a bank to make a payment for a specific commodity on a customer s behalf once specific conditions are met. Letters of Guarantee (L/G): A letter from a bank guaranteeing a sum of money to a specific beneficiary (the seller) if the opposing party (the buyer) does not meet specified conditions under the contract. Documentary Collections (D/Cs): the exporter (seller) provides his bank with the shipping and collection documents for a specific commodity. The importer s (buyer s) bank then presents the seller s the bank with shipping and title documents in exchange for payment (note that in the case of D/Cs neither the buyer s nor the seller s bank is guaranteeing payment).

bank then presents the seller s the bank with shipping and title documents in exchange for payment (note that in the case of D/Cs neither the buyer s nor the")

19 Guarantees A financial guarantee is an assurance given by an outside party to compensate a financier, in whole or in part, if a borrower does not fulfill contractual obligations under a credit agreement. USAID offers four core types of credit guarantees through the Development Credit Authority (DCA), but loan portfolio guarantees (LPGs) are the most common form for expanding finance to MSMEs. All DCA guarantees are legally binding commitments backed by the full faith of the US Government to share in up to 50 percent of a private lender s realized losses. DCA guarantees help alleviate market imperfections by reducing the perceived risk of lending to targeted sectors and borrowers, including farmers, agribusinesses and MSMEs.

20 Examples of MSME Finance Several illustrative examples of MSME and Asset Based Finance programs in developing countries are highlighted in the following slides.

21 Macedonia SME Finance Fund SME Finance Fund founded in 2003 to finance underserved MSMEs in Macedonia. USAID and Crimson Capital provided the original operational and lending capital. The Fund is structured as a Macedonian foundation. Norfund subsequently provided a long term loan for on-lending. Primary instrument is POF. Fund will introduce A/R financing and leasing. Over $17 million lent to MSMEs in 233 loans, and more than 2,095 new permanent jobs created, of which 1,039 are for women and 268 for minorities. This does not include the thousands of farmers and MSME suppliers that are also beneficiaries. Almost 50% of the loans are to women and minority owned firms, over 30% of the loans are to agriculture/agribusiness, and 7 startups have been financed Created over $62 million in new exports The Fund is self-sustaining from interest and fee income The Fund is a large generator of new employment per dollar

22 Kosovo SME Finance Fund SME Finance Fund founded in 2008 to finance underserved MSMEs in Kosovo. The Norwegian Ministry of Foreign Affairs and Crimson Capital provided startup and initial operational support. Norfund and USAID provided lending capital. The Fund is structured as a Limited Liability Company (LLC). Primary instrument is POF. Fund will introduce A/R financing and leasing. Non-bank Financial Institution (NBFI), registered, licensed and supervised by the Central Bank of Kosovo. In first 16 months of operation over $3 million in loans to MSMEs, stimulating more that $31 million in sales. Lent out USAID funds 2.27x in 16 months. 227 direct new jobs created, several hundreds of small farmers and suppliers supported. Created 54 jobs for women and minorities and 7 loans to women and minority owned firms. All funds continuously lent out. 0% defaults (for banks and MFIs, bad loans = 4.3% in 2009). Fund is now self-sustaining on interest and fee income from its lending operations

23 Azerbaijan: Examples of MSME Finance USAID Private Sector Competitiveness Enhancement Program (PSCEP). Introduced POF to 6 banks, expanding the use of Letters of Credit, Letters of Guarantee and Documentary Collection, and expanding the use and availability of leasing. Generated over $26 million in new MSME financing, including POF, in one year. USAID Trade and Investment Reform Support Program (TIRSP). Improving the enabling environment for leasing and making recommendations for banks/leasing companies to increase utilization of leasing. Bolivia: USAID Bolivia Rural Competitiveness Activity (ARCo). Assisted the micro-finance institution FIE to open 5 full service branches in the rural coca-growing regions of Yungas and Chapare and to develop and introduce MSME lending products, including POF (first introduction of POF to Bolivia). With total technical assistance funds of just $0.5 million, this innovative program resulted in over $18.5 million in loans to more than 6,500 clients. In addition, rural clients opened more than 9,400 savings accounts with deposits totaling over $4.7 million. Project won the USAID 2009 Award for Innovations in Value Chain Finance.

24 Examples of MSME Finance Kosovo: USAID Cluster and Business Support (KCBS). Developed documentation for a USAID DCA Loan Portfolio Guarantee (LPG) and implemented a series of training programs in agricultural lending to build the capacity of the partner bank s loan officers. The partner bank made 914 loans to farmers and agribusinesses, fully utilizing the DCA LPG for $10 million in lending in just two years. The partner bank also added agricultural loans to its core product profile. Peru: USAID Promoting Integrated Development (PDA). Assisting nine financial institutions to introduce a savings-linked credit product which helps rural agricultural producers obtain much needed access to finance in the rural, alternative development regions of Peru. Over $5.9 million in credit has been extended to more than 2,600 agricultural producers in the target areas. More than 2,400 savings accounts have been opened, totaling over $2.7 million.

25 Examples of MSME Finance Moldova: USAID Competitive Enhancement and Enterprise Development (CEED). Introduced POF to five partner banks. To date, the five partner banks have made loans totaling over $5.5 million to Moldovan MSMEs, enabling more than $12 million in new sales. Expanded the utilization of leasing. Armenia: USAID FS Share Financial Sector Stability Pilot (FSSP). Introducing POF to two partner banks to provide finance to MSMEs in agriculture, food processing, information & communications technology (ICT), energy, pharmaceuticals, and tourism. First POF loan made -- $15,000 to assist a pharmaceutical company produce eye drops for export to Russia -- just three months into the program. Analyzing the potential use of hedging mechanisms in SME lending to overcome the currency mismatch (dollarization of deposits need for lending liquidity in drams).

26 Examples of MSME Finance Macedonia: USAID Agribusiness Activity (AgBiz). Helping Macedonian agribusinesses source capital to enable them to expand and improve production as well as to increase sales. Assisted agribusinesses to access over $14.5 million in financing to expand their operations and complete trade deals. Also working with fresh fruit producers and marketers to install more efficient drip irrigation systems, upgrade storage facilities and enhance their export marketing capabilities. South Africa: USAID Financial Sector Project (FSP). Assisted a major commercial bank to introduce two new loan products -- Invoice Clearing and Vendor Finance -- designed specifically for the SME market. These products are analogous to factoring and POF respectively. Also supported capacity building of the National Credit Registry (NCR), which is responsible for monitoring the availability of credit, pricing and market conditions, trends in access to credit and indebtedness, and market conduct and competition.

27 Summary Access to finance for MSMEs can be increased by: Introduction/adaptation/utilization of appropriate financial instruments at existing FIs, including asset based lending products and guarantees. Creation of special purpose companies or funds to lend to/invest in MSMEs Technical assistance and training to FIs particularly on the use of specific financial instruments with live MSME borrowers on real transactions Technical assistance and training to SMEs to increase their capacity to qualify for loans and manage their finances Improvements in the legal, regulatory, and policy framework and capacity of institutions (registries, bureaus, supervisory agencies, etc.) Some additional information on MSME & Asset Based Financing:

PURCHASE ORDER FINANCE IN BOLIVIA

PURCHASE ORDER FINANCE IN BOLIVIA INNOVATIONS IN FINANCING VALUE CHAINS microreport #151 APRIL 2009 This publication was produced for review by the United States Agency for International Development. It

PURCHASE ORDER FINANCE IN BOLIVIA INNOVATIONS IN FINANCING VALUE CHAINS microreport #151 APRIL 2009 This publication was produced for review by the United States Agency for International Development. It

ANALYSIS OF THE POTENTIAL FOR DEVELOPMENT OF SME PURCHASE ORDER FINANCE PRODUCTS

ANALYSIS OF THE POTENTIAL FOR DEVELOPMENT OF SME PURCHASE ORDER FINANCE PRODUCTS 31 March 2007 This publication was produced for review by the United States Agency for International Development. It was

ANALYSIS OF THE POTENTIAL FOR DEVELOPMENT OF SME PURCHASE ORDER FINANCE PRODUCTS 31 March 2007 This publication was produced for review by the United States Agency for International Development. It was

Liberia Leasing Investment Forum

Finance Leasing in Liberia: Unlocking Accelerated Market and Business Development Adopting Best Practice Models to Make Leasing Work in Liberia Minerva Kotei Monrovia, A 40 Year Commitment to Leasing A

Finance Leasing in Liberia: Unlocking Accelerated Market and Business Development Adopting Best Practice Models to Make Leasing Work in Liberia Minerva Kotei Monrovia, A 40 Year Commitment to Leasing A

Your Logo Here Creative Ways to Finance Your Working Capital Needs. February 22, 2012 2/24/2012

Your Logo Here Creative Ways to Finance Your Working Capital Needs February 22, 2012 1 Trade Finance Tools Classic Trade Products: Letters Of Credit, Collections, Open Account Enhanced Trade Products:

Your Logo Here Creative Ways to Finance Your Working Capital Needs February 22, 2012 1 Trade Finance Tools Classic Trade Products: Letters Of Credit, Collections, Open Account Enhanced Trade Products:

ACCESS TO FINANCE FOR AGRICULTURAL ENTERPRISES. Presented by Farouk Kurawa Agricultural Finance Specialist, USAID MARKETS II

ACCESS TO FINANCE FOR AGRICULTURAL ENTERPRISES Presented by Farouk Kurawa Agricultural Finance Specialist, USAID MARKETS II AGRICULTURE IN NIGERIA It is a wide spread activity practiced across all regions

ACCESS TO FINANCE FOR AGRICULTURAL ENTERPRISES Presented by Farouk Kurawa Agricultural Finance Specialist, USAID MARKETS II AGRICULTURE IN NIGERIA It is a wide spread activity practiced across all regions

Export Transactions. Finance and Risk

Export Transactions Finance and Risk Table of Contents Export Finance Export Finance Methods Pre-Export Export Finance Methods Post-Export Structured Commodity Finance Export Risk Forms of Export Risk

Export Transactions Finance and Risk Table of Contents Export Finance Export Finance Methods Pre-Export Export Finance Methods Post-Export Structured Commodity Finance Export Risk Forms of Export Risk

SECTOR ASSESSMENT (SUMMARY): MICRO, SMALL AND MEDIUM-SIZED ENTERPRISE DEVELOPMENT 1 Sector Road Map 1. Sector Performance, Problems, and Opportunities

: MICRO, SMALL AND MEDIUM-SIZED ENTERPRISE DEVELOPMENT 1 Sector Road Map 1. Sector Performance, Problems, and Opportunities") Small Business and Entrepreneurship Development Project (RRP UZB 42007-014) SECTOR ASSESSMENT (SUMMARY): MICRO, SMALL AND MEDIUM-SIZED ENTERPRISE DEVELOPMENT 1 Sector Road Map 1. Sector Performance, Problems,

Small Business and Entrepreneurship Development Project (RRP UZB 42007-014) SECTOR ASSESSMENT (SUMMARY): MICRO, SMALL AND MEDIUM-SIZED ENTERPRISE DEVELOPMENT 1 Sector Road Map 1. Sector Performance, Problems,

SECTOR ASSESSMENT (SUMMARY): MICRO, SMALL, AND MEDIUM-SIZED ENTERPRISE DEVELOPMENT

: MICRO, SMALL, AND MEDIUM-SIZED ENTERPRISE DEVELOPMENT") Women s Entrepreneurship Support Sector Development Program (RRP ARM 45230) SECTOR ASSESSMENT (SUMMARY): MICRO, SMALL, AND MEDIUM-SIZED ENTERPRISE DEVELOPMENT A. Overview 1. Significance of micro, small,

Women s Entrepreneurship Support Sector Development Program (RRP ARM 45230) SECTOR ASSESSMENT (SUMMARY): MICRO, SMALL, AND MEDIUM-SIZED ENTERPRISE DEVELOPMENT A. Overview 1. Significance of micro, small,

Ethiopian Institute of Financial Studies (EIFS) PROJECT FINANCE

PROJECT FINANCE") PROJECT FINANCE With the growth in the economy and the revival in the industrial sector coupled with the increasing role of private players in the field of infrastructure, more and more Ethiopian banks

PROJECT FINANCE With the growth in the economy and the revival in the industrial sector coupled with the increasing role of private players in the field of infrastructure, more and more Ethiopian banks

How To Finance A Value Chain

Using the Value Chain in Financing Agriculture Rural and Agricultural Finance Conference Marrakech, Morocco Calvin Miller FAO Agribusiness and Finance Senior Officer Rome, Italy Presentation Applying Agri

Using the Value Chain in Financing Agriculture Rural and Agricultural Finance Conference Marrakech, Morocco Calvin Miller FAO Agribusiness and Finance Senior Officer Rome, Italy Presentation Applying Agri

Facilitating Remittances to Help Families and Small Businesses

G8 ACTION PLAN: APPLYING THE POWER OF ENTREPRENEURSHIP TO THE ERADICATION OF POVERTY The UN Commission on the Private Sector and Development has stressed that poverty alleviation requires a strong private

G8 ACTION PLAN: APPLYING THE POWER OF ENTREPRENEURSHIP TO THE ERADICATION OF POVERTY The UN Commission on the Private Sector and Development has stressed that poverty alleviation requires a strong private

UNNExT workshop on Paperless trade facilitation for Small and Medium-sized Enterprises

UNNExT workshop on Paperless trade facilitation for Small and Medium-sized Enterprises 2-4 February 2015 United Nations Conference Center (UNCC) Bangkok, Thailand Innovative financing and ITC solutions

UNNExT workshop on Paperless trade facilitation for Small and Medium-sized Enterprises 2-4 February 2015 United Nations Conference Center (UNCC) Bangkok, Thailand Innovative financing and ITC solutions

Secured Transactions and Collateral Registries Program

Secured Transactions and Collateral Registries Program Access to Finance, IFC Amman, Jordan, June 25, 2013 Alejandro Alvarez de la Campa Global Product Leader STCR OUTLINE 1. Definition of Secured Transactions

Secured Transactions and Collateral Registries Program Access to Finance, IFC Amman, Jordan, June 25, 2013 Alejandro Alvarez de la Campa Global Product Leader STCR OUTLINE 1. Definition of Secured Transactions

ABL Step 1 An Introduction. How SIPPA can change the Lending Environment and Access to Credit

ABL Step 1 An Introduction How SIPPA can change the Lending Environment and Access to Credit Traditional Bank vs ABL Bank Focused on Credit Status Over reliance on Real Estate Vulnerable to Economic Cycles

ABL Step 1 An Introduction How SIPPA can change the Lending Environment and Access to Credit Traditional Bank vs ABL Bank Focused on Credit Status Over reliance on Real Estate Vulnerable to Economic Cycles

Small and Medium Enterprises

Small and Medium Enterprises YOUR LOANS Small and Medium Enterprises Financing Products for Your Business A consumer education programme by: contents 1 Introduction 2 The right product for the right purpose

Small and Medium Enterprises YOUR LOANS Small and Medium Enterprises Financing Products for Your Business A consumer education programme by: contents 1 Introduction 2 The right product for the right purpose

University meets Microfinance. Do our clients grow? - Microfinance vs. SME Finance

University meets Microfinance Do our clients grow? - Microfinance vs. SME Finance July 2012 Definition(s) of MSME Definitions vary greatly between countries, financial regulators and financial institutions.

University meets Microfinance Do our clients grow? - Microfinance vs. SME Finance July 2012 Definition(s) of MSME Definitions vary greatly between countries, financial regulators and financial institutions.

First Industries Fund

First Industries Fund First Industries is one of 19 programs in the June 2004 economic stimulus package. It provides $100 million for agriculture, and $50 million for tourism. Final guidelines were approved

First Industries Fund First Industries is one of 19 programs in the June 2004 economic stimulus package. It provides $100 million for agriculture, and $50 million for tourism. Final guidelines were approved

Warehouse Receipt System From Banks Perspective

Warehouse Receipt System From Banks Perspective July 2011 By: Andrew K Bwalya- Director/Head Agribusiness Commodity Value Chain and Key Players Value chain Input Supply Agricultural Production Storage

Warehouse Receipt System From Banks Perspective July 2011 By: Andrew K Bwalya- Director/Head Agribusiness Commodity Value Chain and Key Players Value chain Input Supply Agricultural Production Storage

IFC and Agri-Finance. Creating Opportunity Where It s Needed Most

IFC and Creating Opportunity Where It s Needed Most Agriculture remains an important activity in emerging markets IMPORTANCE OF AGRICULTURE as major source of livelihood 75% of poor people in developing

IFC and Creating Opportunity Where It s Needed Most Agriculture remains an important activity in emerging markets IMPORTANCE OF AGRICULTURE as major source of livelihood 75% of poor people in developing

Key learning points I

Key learning points I What do banks do? Banks provide three core banking services Deposit collection Payment arrangement Underwrite loans Banks may also offer financial services such as cash, asset, and

Key learning points I What do banks do? Banks provide three core banking services Deposit collection Payment arrangement Underwrite loans Banks may also offer financial services such as cash, asset, and

RURAL AND AGRICULTURE FINANCE Prof. Puneetha Palakurthi School of Community Economic Development Sothern New Hampshire University

RURAL AND AGRICULTURE FINANCE Prof. Puneetha Palakurthi School of Community Economic Development Sothern New Hampshire University DRIVERS OF RURAL DEVELOPMENT High overall economic growth Effective land

RURAL AND AGRICULTURE FINANCE Prof. Puneetha Palakurthi School of Community Economic Development Sothern New Hampshire University DRIVERS OF RURAL DEVELOPMENT High overall economic growth Effective land

Opportunities for Financing the Agricultural Sector in Turkey

Opportunities for Financing the Agricultural Sector in Turkey Financing Agriculture in Turkey Conference Istanbul, Turkey 18 April, 2012 Calvin Miller Agribusiness and Finance Group Leader FAO, Rome, Italy

Opportunities for Financing the Agricultural Sector in Turkey Financing Agriculture in Turkey Conference Istanbul, Turkey 18 April, 2012 Calvin Miller Agribusiness and Finance Group Leader FAO, Rome, Italy

5.3.2015 г. OC = AAI + ACP

D. Dimov Working capital (or short-term financial) management is the management of current assets and current liabilities: Current assets include inventory, accounts receivable, marketable securities,

D. Dimov Working capital (or short-term financial) management is the management of current assets and current liabilities: Current assets include inventory, accounts receivable, marketable securities,

Ghana s Legal Framework for Secured Transactions

Ghana s Legal Framework for Secured Transactions M A R E K D U B O V E C M D U B O V E C @ N A T L A W.C O M Organization of the Presentation 1) Current Substantive Legal Framework 2) Assessment against

Ghana s Legal Framework for Secured Transactions M A R E K D U B O V E C M D U B O V E C @ N A T L A W.C O M Organization of the Presentation 1) Current Substantive Legal Framework 2) Assessment against

Medium-term or Intermediate Term Financing

Medium-term or Intermediate Term Financing Medium term finance [loan] is usually provided from three to ten years; Such finance is Obtained for meeting the cost of maintenance, repair, improvement and

Medium-term or Intermediate Term Financing Medium term finance [loan] is usually provided from three to ten years; Such finance is Obtained for meeting the cost of maintenance, repair, improvement and

Asia Pacific Trade Facilitation Forum 2014. 24 25 September 2014, BITEC Bangkok, Thailand

Asia Pacific Trade Facilitation Forum 2014 24 25 September 2014, BITEC Bangkok, Thailand Innovative trade financing initiatives for SMEs Asia Pacific Trade Facilitation Forum September 2014, Bangkok, Thailand

Asia Pacific Trade Facilitation Forum 2014 24 25 September 2014, BITEC Bangkok, Thailand Innovative trade financing initiatives for SMEs Asia Pacific Trade Facilitation Forum September 2014, Bangkok, Thailand

Small Business Initiative. Investing in small businesses, building big economies

Small Business Initiative Investing in small businesses, building big economies Impact: This contributes to creating a vibrant small and medium-sized enterprise (SME) sector, a vital ingredient for a healthy

Small Business Initiative Investing in small businesses, building big economies Impact: This contributes to creating a vibrant small and medium-sized enterprise (SME) sector, a vital ingredient for a healthy

Trade Finance : SMEs Emerging Needs

ASIA-PACIFIC TRADE FACILITATION FORUM 2013 [Session 2: Integrating SMEs into international supply chains through trade finance] Beijing, China, 10-11 September 2013 Trade Finance : SMEs Emerging Needs

ASIA-PACIFIC TRADE FACILITATION FORUM 2013 [Session 2: Integrating SMEs into international supply chains through trade finance] Beijing, China, 10-11 September 2013 Trade Finance : SMEs Emerging Needs

IFC Secured Transactions Advisory Project in China

IFC Secured Transactions Advisory Project in China 1 Background In 2004, the People s Bank of China (PBOC) recognized wide spread financing difficulties among small and medium enterprises (SMEs) and requested

IFC Secured Transactions Advisory Project in China 1 Background In 2004, the People s Bank of China (PBOC) recognized wide spread financing difficulties among small and medium enterprises (SMEs) and requested

Commonwealth Caribbean Regional Conference. Investing in Youth Exploring Strategies for Sustainable Employment. Financing and Financial Mechanisms

Commonwealth Caribbean Regional Conference Investing in Youth Exploring Strategies for Sustainable Employment Financing and Financial Mechanisms Presented by Ian Chinapoo May 25 th, 2011 Outline: Background

Commonwealth Caribbean Regional Conference Investing in Youth Exploring Strategies for Sustainable Employment Financing and Financial Mechanisms Presented by Ian Chinapoo May 25 th, 2011 Outline: Background

Section A: Introduction

Section A: Introduction A1 Was this business a subsidiary of another business in 2014? Yes No A2 If you are a subsidiary, what is the name of your current parent business? A3 Did your business generate

Section A: Introduction A1 Was this business a subsidiary of another business in 2014? Yes No A2 If you are a subsidiary, what is the name of your current parent business? A3 Did your business generate

IFC Financial Institutions Group

IFC Financial Institutions Group Supply Chain Finance for SMEs Qamar Saleem Senior Banking Specialist, EMENA October 22 2nd 2014 There exists $2.1-2.6 Trillion global SME credit gap, formal & informal

IFC Financial Institutions Group Supply Chain Finance for SMEs Qamar Saleem Senior Banking Specialist, EMENA October 22 2nd 2014 There exists $2.1-2.6 Trillion global SME credit gap, formal & informal

CHAPTER 9: BANKING DOING BUSINESS IN GREATER PHOENIX, U.S.A. 9.1: THE U.S. BANKING SYSTEM 9.2: ESTABLISHING A U.S. BANK ACCOUNT

CHAPTER 9: BANKING 9.1: THE U.S. BANKING SYSTEM Unlike banks in many countries, U.S. banks are not government-owned and managed. They provide deposit facilities for the general public, provide loans for

CHAPTER 9: BANKING 9.1: THE U.S. BANKING SYSTEM Unlike banks in many countries, U.S. banks are not government-owned and managed. They provide deposit facilities for the general public, provide loans for

Mitigation of Investment Risk

1of 37 F A O P o l i c y L e a r n i n g P r o g r a m m e Module 3: Investment and Resource Mobilization Mitigation of Investment Risk 2of 38 Mitigation of Investment Risk By Calvin Miller, Senior Officer,

1of 37 F A O P o l i c y L e a r n i n g P r o g r a m m e Module 3: Investment and Resource Mobilization Mitigation of Investment Risk 2of 38 Mitigation of Investment Risk By Calvin Miller, Senior Officer,

Disclosure 17 OffV (Credit Risk Mitigation Techniques)

") Disclosure 17 OffV (Credit Risk Mitigation Techniques) The Austrian Financial Market Authority (FMA) and the Oesterreichsiche Nationalbank (OeNB) have assessed UniCredit Bank Austria AG for the use of

Disclosure 17 OffV (Credit Risk Mitigation Techniques) The Austrian Financial Market Authority (FMA) and the Oesterreichsiche Nationalbank (OeNB) have assessed UniCredit Bank Austria AG for the use of

Secured Transactions and Collateral Registries Program

Secured Transactions and Collateral Registries Program Access to Finance, IFC San Jose, Costa Rica, 18 septiembre, 2013 Alejandro Alvarez de la Campa Global Product Leader STCR OUTLINE 1. Definition of

Secured Transactions and Collateral Registries Program Access to Finance, IFC San Jose, Costa Rica, 18 septiembre, 2013 Alejandro Alvarez de la Campa Global Product Leader STCR OUTLINE 1. Definition of

Division 9 Specific requirements for certain portfolios of exposures

L. S. NO. 2 TO GAZETTE NO. 43/2006 L.N. 228 of 2006 B3157 Division 9 Specific requirements for certain portfolios of exposures 197. Purchased receivables An authorized institution shall classify its purchased

L. S. NO. 2 TO GAZETTE NO. 43/2006 L.N. 228 of 2006 B3157 Division 9 Specific requirements for certain portfolios of exposures 197. Purchased receivables An authorized institution shall classify its purchased

Export Credit and Finance Essentials For Successful Exporters

International Trade Leadership Certificate Series Export Credit and Finance Essentials For Successful Exporters July 17, 2015 1 Alabama Small Business Development Center Network An affiliate of America

International Trade Leadership Certificate Series Export Credit and Finance Essentials For Successful Exporters July 17, 2015 1 Alabama Small Business Development Center Network An affiliate of America

Two trillion and counting

Two trillion and counting Assessing the credit gap for micro, small, and medium-size enterprises in the developing world OCTOBER 2010 Peer Stein International Finance Corporation Tony Goland McKinsey &

Two trillion and counting Assessing the credit gap for micro, small, and medium-size enterprises in the developing world OCTOBER 2010 Peer Stein International Finance Corporation Tony Goland McKinsey &

Public consultation on Building a Capital Markets Union

Case Id: 6793f8c7-c6ef-45dd-8987-665fe5775337 Date: 13/05/2015 23:30:38 Public consultation on Building a Capital Markets Union Fields marked with * are mandatory. Introduction The purpose of the Green

Case Id: 6793f8c7-c6ef-45dd-8987-665fe5775337 Date: 13/05/2015 23:30:38 Public consultation on Building a Capital Markets Union Fields marked with * are mandatory. Introduction The purpose of the Green

How To Get A Working Capital Loan From The Ex-Im Bank

How to Finance Export Receivables By Michael D. Farstad Export Finance Lender Table of Contents New Products Working Capital Supply Chain Finance Guarantee Program Global Credit Express Loan Guarantee

How to Finance Export Receivables By Michael D. Farstad Export Finance Lender Table of Contents New Products Working Capital Supply Chain Finance Guarantee Program Global Credit Express Loan Guarantee

FOR FINANCE LEASING INSTITUTIONS

OPERATING GUIDELINES FOR FINANCE LEASING INSTITUTIONS BANKING SUPERVISION DEPARTMENT BANK OF SIERRA LEONE FREETOWN JANUARY 2011 Table of Content No. Heading Page 1 Authority 1 2 Definition 1 3 Application

OPERATING GUIDELINES FOR FINANCE LEASING INSTITUTIONS BANKING SUPERVISION DEPARTMENT BANK OF SIERRA LEONE FREETOWN JANUARY 2011 Table of Content No. Heading Page 1 Authority 1 2 Definition 1 3 Application

Short Term Loans and Lines of Credit

Short Term Loans and Lines of Credit Disadvantaged Business Enterprise (DBE) Supportive Services Program The contents of this training course reflect the views of the author who is responsible for the

Short Term Loans and Lines of Credit Disadvantaged Business Enterprise (DBE) Supportive Services Program The contents of this training course reflect the views of the author who is responsible for the

POTENTIAL RESEARCH OPPORTUNITY FOR SECURED TRANSACIONS REFORM IN COLOMBIA

POTENTIAL RESEARCH OPPORTUNITY FOR SECURED TRANSACIONS REFORM IN COLOMBIA Alejandro Alvarez de la Campa, IFC Boston, September 16, 2011 OUTLINE 1) SECURED TRANSACTIONS: WHAT, WHY, HOW? 2) POTENTIAL IMPACT

POTENTIAL RESEARCH OPPORTUNITY FOR SECURED TRANSACIONS REFORM IN COLOMBIA Alejandro Alvarez de la Campa, IFC Boston, September 16, 2011 OUTLINE 1) SECURED TRANSACTIONS: WHAT, WHY, HOW? 2) POTENTIAL IMPACT

Overview of Financial Solutions

Overview of Financial Solutions The Etra Advisory Group provides solutions to businesses for growth, expansion, cash flow, refinance and acquisition. We cover the world of business financing that banks

Overview of Financial Solutions The Etra Advisory Group provides solutions to businesses for growth, expansion, cash flow, refinance and acquisition. We cover the world of business financing that banks

Schemes for Financing Micro, Small and Medium Enterprises

Schemes for Financing Micro, Small and Medium Enterprises Background The Small Scale Industries Sector, redefined since 2006 as the Micro Small and Medium Enterprises Sector has played a seminal role in

Schemes for Financing Micro, Small and Medium Enterprises Background The Small Scale Industries Sector, redefined since 2006 as the Micro Small and Medium Enterprises Sector has played a seminal role in

1 Regional Bank Regional banks specialize in consumer and commercial products within one region of a country, such as a state or within a group of states. A regional bank is smaller than a bank that operates

1 Regional Bank Regional banks specialize in consumer and commercial products within one region of a country, such as a state or within a group of states. A regional bank is smaller than a bank that operates

EXIM Bank EXIM Bank Trade Financing Solutions for Export Success!

EXIM Bank EXIM Bank Trade Financing Solutions for Export Success! Products: Risk Protection International sales are challenging enough without the added risk of not receiving payment for your goods or

EXIM Bank EXIM Bank Trade Financing Solutions for Export Success! Products: Risk Protection International sales are challenging enough without the added risk of not receiving payment for your goods or

A GUIDE ON FINANCIAL LEASING I. INTRODUCTION

NATIONAL BANK OF SERBIA A GUIDE ON FINANCIAL LEASING I. INTRODUCTION The purpose of this Guide is to provide basic information on financial leasing as a way to finance purchase of equipment and other fixed

NATIONAL BANK OF SERBIA A GUIDE ON FINANCIAL LEASING I. INTRODUCTION The purpose of this Guide is to provide basic information on financial leasing as a way to finance purchase of equipment and other fixed

Financing a Home in the United States

Financing a Home in the United States PHH Home Loans relocation service guides you through the United States home financing process and we will work with you and your company s relocation department to

Financing a Home in the United States PHH Home Loans relocation service guides you through the United States home financing process and we will work with you and your company s relocation department to

Syndicated Revenue Loans. Secured Lines of Credit

Syndicated Revenue Loans. Syndicated Revenue Loans are Revenue loans grouped together through a syndicate. Typically these loans are given while a revenue loan is still outstanding, but the business owner

Syndicated Revenue Loans. Syndicated Revenue Loans are Revenue loans grouped together through a syndicate. Typically these loans are given while a revenue loan is still outstanding, but the business owner

SECTOR ASSESSMENT (SUMMARY): FINANCE 1. 1. Sector Performance, Problems, and Opportunities

: FINANCE 1. 1. Sector Performance, Problems, and Opportunities") Country Partnership Strategy: Bangladesh, 2011 2015 SECTOR ASSESSMENT (SUMMARY): FINANCE 1 Sector Road Map 1. Sector Performance, Problems, and Opportunities 1. The finance sector in Bangladesh is diverse,

Country Partnership Strategy: Bangladesh, 2011 2015 SECTOR ASSESSMENT (SUMMARY): FINANCE 1 Sector Road Map 1. Sector Performance, Problems, and Opportunities 1. The finance sector in Bangladesh is diverse,

Accounts Receivable and Inventory Financing

Accounts Receivable and Inventory Financing Glossary Accounts Payable - A current liability representing the amount owed by an individual or a business to a creditor for merchandise or services purchased

Accounts Receivable and Inventory Financing Glossary Accounts Payable - A current liability representing the amount owed by an individual or a business to a creditor for merchandise or services purchased

11.437 Financing Community Economic Development Class 6: Fixed Asset Financing

11.437 Financing Community Economic Development Class 6: Fixed Asset Financing I. Purpose of asset financing Fixed asset financing refers to the financing for real estate and equipment needs of a business.

11.437 Financing Community Economic Development Class 6: Fixed Asset Financing I. Purpose of asset financing Fixed asset financing refers to the financing for real estate and equipment needs of a business.

Challenges and opportunities in reaching SME through Leasing Egypt Experience

Challenges and opportunities in reaching SME through Leasing Egypt Experience Presented by: Mohamed Amiri C.P.A., M.B.A., Dipl. Vice president International Co. for Leasing INCOLEASE Historical Background:

Challenges and opportunities in reaching SME through Leasing Egypt Experience Presented by: Mohamed Amiri C.P.A., M.B.A., Dipl. Vice president International Co. for Leasing INCOLEASE Historical Background:

The big Small and Medium story - A commentary on SME Financing

The big Small and Medium story - A commentary on SME Financing Mr. Rakesh Singh CEO Limited Key Fundamentals update Developments since Mar 14 Apr Dec 13 Nov 14 New Government Equity Fed tapering / US Recovery

The big Small and Medium story - A commentary on SME Financing Mr. Rakesh Singh CEO Limited Key Fundamentals update Developments since Mar 14 Apr Dec 13 Nov 14 New Government Equity Fed tapering / US Recovery

C&I LOAN EVALUATION UNDERWRITING GUIDELINES. A Whitepaper

C&I LOAN EVALUATION & UNDERWRITING A Whitepaper C&I Lending Commercial and Industrial, or C&I Lending, has long been a cornerstone product for many successful banking institutions. Also known as working

C&I LOAN EVALUATION & UNDERWRITING A Whitepaper C&I Lending Commercial and Industrial, or C&I Lending, has long been a cornerstone product for many successful banking institutions. Also known as working

Liberia Leasing Investment Forum

Finance Leasing in Liberia: Unlocking Accelerated Market and Business Development GROWING COMPETITIVE AND EFFECTIVE LEASING MARKETS Collins David-Ikpe Past chairman, Equipment Leasing Association of Nigeria

Finance Leasing in Liberia: Unlocking Accelerated Market and Business Development GROWING COMPETITIVE AND EFFECTIVE LEASING MARKETS Collins David-Ikpe Past chairman, Equipment Leasing Association of Nigeria

Ipx!up!hfu!uif Dsfeju!zpv!Eftfswf

Ipx!up!hfu!uif Dsfeju!zpv!Eftfswf Credit is the lifeblood of South Louisiana business, especially for the smaller firm. It helps the small business owner get started, obtain equipment, build inventory,

Ipx!up!hfu!uif Dsfeju!zpv!Eftfswf Credit is the lifeblood of South Louisiana business, especially for the smaller firm. It helps the small business owner get started, obtain equipment, build inventory,

How To Help A Leasing Enterprise

i FS Series #7: Enhancing the Leasing Enabling Environment FS SERIES #7: ENHANCING THE LEASING ENABLING ENVIRONMENT MODEL SCOPE OF WORK The author s views expressed in this publication do not necessarily

i FS Series #7: Enhancing the Leasing Enabling Environment FS SERIES #7: ENHANCING THE LEASING ENABLING ENVIRONMENT MODEL SCOPE OF WORK The author s views expressed in this publication do not necessarily

Trade finance in Nigeria: Structured commodity financing as an instrument for mitigating risk

Trade finance in Nigeria: Structured commodity financing as an instrument for mitigating risk By Olutola Bella, Banwo & Ighodalo The buoyancy of international trade and access to trade finance are key

Trade finance in Nigeria: Structured commodity financing as an instrument for mitigating risk By Olutola Bella, Banwo & Ighodalo The buoyancy of international trade and access to trade finance are key

International Accounting Standard 39 Financial Instruments: Recognition and Measurement

EC staff consolidated version as of 18 February 2011 FOR INFORMATION PURPOSES ONLY International Accounting Standard 39 Financial Instruments: Recognition and Measurement Objective 1 The objective of this

EC staff consolidated version as of 18 February 2011 FOR INFORMATION PURPOSES ONLY International Accounting Standard 39 Financial Instruments: Recognition and Measurement Objective 1 The objective of this

MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

ECON 4110: Sample Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Economists define risk as A) the difference between the return on common

ECON 4110: Sample Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Economists define risk as A) the difference between the return on common

Business Activities Definitions

Business Activities s Mortgage First mortgage brokering Second mortgage brokering First mortgage lending Second mortgage lending First mortgage servicing Third party first mortgage servicing Subordinate

Business Activities s Mortgage First mortgage brokering Second mortgage brokering First mortgage lending Second mortgage lending First mortgage servicing Third party first mortgage servicing Subordinate

HSBC Mutual Funds. Simplified Prospectus June 8, 2015

HSBC Mutual Funds Simplified Prospectus June 8, 2015 Offering Investor Series, Advisor Series, Premium Series, Manager Series and Institutional Series units of the following Funds: HSBC Global Corporate

HSBC Mutual Funds Simplified Prospectus June 8, 2015 Offering Investor Series, Advisor Series, Premium Series, Manager Series and Institutional Series units of the following Funds: HSBC Global Corporate

Commodity Futures Trading Commission Office of Public Affairs Three Lafayette Centre 1155 21st Street, NW Washington, DC 20581 www.cftc.

Commodity Futures Trading Commission Office of Public Affairs Three Lafayette Centre 1155 21st Street, NW Washington, DC 20581 www.cftc.gov Final Rules Regarding Further Defining Swap Dealer, Major Swap

Commodity Futures Trading Commission Office of Public Affairs Three Lafayette Centre 1155 21st Street, NW Washington, DC 20581 www.cftc.gov Final Rules Regarding Further Defining Swap Dealer, Major Swap

Liberia Leasing Investment Forum

Finance Leasing in Liberia: Unlocking Accelerated Market and Business Development Long Term Financing for Leasing The Venture Capital Option. Dr. Anthony O. Oboh Ph.d Managing Director/CEO, UVC and Fund

Finance Leasing in Liberia: Unlocking Accelerated Market and Business Development Long Term Financing for Leasing The Venture Capital Option. Dr. Anthony O. Oboh Ph.d Managing Director/CEO, UVC and Fund

UNNExT workshop on Paperless trade facilitation for Small and Medium-sized Enterprises

UNNExT workshop on Paperless trade facilitation for Small and Medium-sized Enterprises 2-4 February 2015 United Nations Conference Center (UNCC) Bangkok, Thailand Secured Transactions & Collateral Registry

UNNExT workshop on Paperless trade facilitation for Small and Medium-sized Enterprises 2-4 February 2015 United Nations Conference Center (UNCC) Bangkok, Thailand Secured Transactions & Collateral Registry

Leasing and Factoring for SME Finance

Leasing and Factoring for SME Finance ADBI Seminar on SME Finance May 2006 Yasuo IZUMI 1 The v iews expressed in this paper are the v iews of the author and do not necessarily reflect the views or policies

Leasing and Factoring for SME Finance ADBI Seminar on SME Finance May 2006 Yasuo IZUMI 1 The v iews expressed in this paper are the v iews of the author and do not necessarily reflect the views or policies

9 ACCESS TO CAPITAL FOR YORK REGION SMALL BUSINESSES

9 ACCESS TO CAPITAL FOR YORK REGION SMALL BUSINESSES The Planning and Economic Development Committee recommends the adoption of the recommendation contained in the following report dated May 19, 2009,

9 ACCESS TO CAPITAL FOR YORK REGION SMALL BUSINESSES The Planning and Economic Development Committee recommends the adoption of the recommendation contained in the following report dated May 19, 2009,

FINANCING SMALL AND MICRO ENTERPRISES IN AFRICA 2. THE CHARACTERISTICS OF MICROFINANCE ARRANGEMENTS IN AFRICA

FINANCING SMALL AND MICRO ENTERPRISES IN AFRICA 1. THE ISSUES There is the perception that the demand for finance by small enterprises far exceeds the supply, but recent research in 4 countries shows that

FINANCING SMALL AND MICRO ENTERPRISES IN AFRICA 1. THE ISSUES There is the perception that the demand for finance by small enterprises far exceeds the supply, but recent research in 4 countries shows that

DBN. A presentation on the DBN s MSME Support & Strategy-Emphasis on Innovation Fund Occasion:NBIC Entrepreneurs Circle

DBN A presentation on the DBN s MSME Support & Strategy-Emphasis on Innovation Fund Occasion:NBIC Entrepreneurs Circle MICHAEL HUMAVINDU, Research Department 28 February 2011 Contents 1. Introduction to

DBN A presentation on the DBN s MSME Support & Strategy-Emphasis on Innovation Fund Occasion:NBIC Entrepreneurs Circle MICHAEL HUMAVINDU, Research Department 28 February 2011 Contents 1. Introduction to

Movables Finance: Concepts, Key Elements, and Structuring

Movables Finance: Concepts, Key Elements, and Structuring Jinchang Lai Principal Operations Officer, and Lead for Financial Infrastructure, Finance & Markets, World Bank Group Rabat, September 25, 2014

Movables Finance: Concepts, Key Elements, and Structuring Jinchang Lai Principal Operations Officer, and Lead for Financial Infrastructure, Finance & Markets, World Bank Group Rabat, September 25, 2014

U.S. SMALL BUSINESS ADMINISTRATION. Craig Jordan. Lead Lender Relations Specialist

U.S. SMALL BUSINESS ADMINISTRATION Craig Jordan Lead Lender Relations Specialist James Pipper International Trade Officer GUARANTEED LENDING PROGRAMS UPDATE U.S. Government Export Financing Programs How

U.S. SMALL BUSINESS ADMINISTRATION Craig Jordan Lead Lender Relations Specialist James Pipper International Trade Officer GUARANTEED LENDING PROGRAMS UPDATE U.S. Government Export Financing Programs How

½ a mark for rounding up (6 marks) (b) There are a number of costs to the business associated with holding inventory:

(b) There are a number of costs to the business associated with holding inventory:") EDI LCCI IQ ON DEMAND AWARD IN BUSINESS FINANCE AND BANKING OPERATIONS SAMPLE LEVEL 4 MARKING SCHEME DISTINCTION MARK 75% CREDIT MARK 60% PASS MARK 50% TOTAL 100 MARKS QUESTION 1 (a) Inventory days Receivable

EDI LCCI IQ ON DEMAND AWARD IN BUSINESS FINANCE AND BANKING OPERATIONS SAMPLE LEVEL 4 MARKING SCHEME DISTINCTION MARK 75% CREDIT MARK 60% PASS MARK 50% TOTAL 100 MARKS QUESTION 1 (a) Inventory days Receivable

CHAPTER 16 Current Asset Management and Financing

Copyright 2008 by the Foundation of the American College of Healthcare Executives 6/13/07 Version 16-1 CHAPTER 16 Current Asset Management and Financing Investment and financing policies Cash and marketable

Copyright 2008 by the Foundation of the American College of Healthcare Executives 6/13/07 Version 16-1 CHAPTER 16 Current Asset Management and Financing Investment and financing policies Cash and marketable

Commercial Financial Services: Industry Specialization and Solutions for Working Capital Issues. October 6 th, 2014

Commercial Financial Services: Industry Specialization and Solutions for Working Capital Issues October 6 th, 2014 Who we are: Vision Always earning the right to be our clients' first choice. Strategic

Commercial Financial Services: Industry Specialization and Solutions for Working Capital Issues October 6 th, 2014 Who we are: Vision Always earning the right to be our clients' first choice. Strategic

ASSET-BASED FINANCE WHITE PAPER #1

ASSET-BASED FINANCE WHITE PAPER #1 CONTENTS Acronyms... i Introduction... ii Executive Summary... iii A. Asset-Based Finance...1 A1. Background...1 A2. Instruments and Applications...1 A2a. Accounts Receivables

ASSET-BASED FINANCE WHITE PAPER #1 CONTENTS Acronyms... i Introduction... ii Executive Summary... iii A. Asset-Based Finance...1 A1. Background...1 A2. Instruments and Applications...1 A2a. Accounts Receivables

Central Banks and the Development Agenda The CBN Experience Sadiq Usman 1 Presentation Outline 2 Slide Introduction Brief on Nigeria The recent Banking Crisis CBN Developmental Activities CBN Interventions

Central Banks and the Development Agenda The CBN Experience Sadiq Usman 1 Presentation Outline 2 Slide Introduction Brief on Nigeria The recent Banking Crisis CBN Developmental Activities CBN Interventions

Apple Capital Group, Inc.

COMMERCIAL FINANCE Commercial finance typical revolves around what are considered the assets of your business and are often called "asset based loans". The assets of your business are things such as your

COMMERCIAL FINANCE Commercial finance typical revolves around what are considered the assets of your business and are often called "asset based loans". The assets of your business are things such as your

FINANCE for the POOR Equipment Leasing and Lending: A Guide for Microfinance 1

FINANCE for the POOR Equipment Leasing and Lending: A Guide for Microfinance 1 GLENN D. WESTLEY Senior Advisor, Micro, Small and Medium Enterprise Division Inter-American Development Bank As microfinance

FINANCE for the POOR Equipment Leasing and Lending: A Guide for Microfinance 1 GLENN D. WESTLEY Senior Advisor, Micro, Small and Medium Enterprise Division Inter-American Development Bank As microfinance

Legislative Fiscal Bureau One East Main, Suite 301 Madison, WI 53703 (608) 266-3847 Fax: (608) 267-6873

266-3847 Fax: (608) 267-6873") Legislative Fiscal Bureau One East Main, Suite 301 Madison, WI 53703 (608) 266-3847 Fax: (608) 267-6873 May 5, 2005 Joint Committee on Finance Paper #144 Rural Business Enterprise Loans (Agriculture, Trade

Legislative Fiscal Bureau One East Main, Suite 301 Madison, WI 53703 (608) 266-3847 Fax: (608) 267-6873 May 5, 2005 Joint Committee on Finance Paper #144 Rural Business Enterprise Loans (Agriculture, Trade

A Simple Approach to Business Loans and Cash Management

A Simple Approach to Business Loans and Cash Management Christine Ho Vice President SME Banking 11 February 2009 Operating Cycle Liquidity Liquidity Management Management Working Capital Working Capital

A Simple Approach to Business Loans and Cash Management Christine Ho Vice President SME Banking 11 February 2009 Operating Cycle Liquidity Liquidity Management Management Working Capital Working Capital

Invoice Factoring, Debtors Discounting and Trade Finance are bridging facilities using your debtors, stock or movable assets to raise cash.

Dear Sir / Madam, Re Bridging Facilities Invoice Factoring, Debtors Discounting and Trade Finance are bridging facilities using your debtors, stock or movable assets to raise cash. A key element is that

Dear Sir / Madam, Re Bridging Facilities Invoice Factoring, Debtors Discounting and Trade Finance are bridging facilities using your debtors, stock or movable assets to raise cash. A key element is that

Sources of Funds: Equity and Debt

Sources of Funds: Equity and Debt The Secrets to Successful Financing 1. Choosing the right sources of capital is a decision that will influence a company for a lifetime. 2. The money is out there; the

Sources of Funds: Equity and Debt The Secrets to Successful Financing 1. Choosing the right sources of capital is a decision that will influence a company for a lifetime. 2. The money is out there; the

SMALL BUSINESS LENDING OPPORTUNITIES FOR CREDIT UNIONS

SMALL BUSINESS LENDING OPPORTUNITIES FOR CREDIT UNIONS February 14, 2012 Terrence K. McHugh President Commercial Alliance 1 Business Lending in Credit Unions 1998 regulation limits business lending in

SMALL BUSINESS LENDING OPPORTUNITIES FOR CREDIT UNIONS February 14, 2012 Terrence K. McHugh President Commercial Alliance 1 Business Lending in Credit Unions 1998 regulation limits business lending in

SME Finance Policy - harnessing technology and innovation - G20 SME Workshop Riyadh, March 11, 2014

SME Finance Policy - harnessing technology and innovation - G20 SME Workshop Riyadh, March 11, 2014 Douglas Pearce 1 SME FINANCE CONSTRAINTS AND RESPONSES 2 INNOVATIVE APPROACHES CAN EASE CONSTRAINTS 3

SME Finance Policy - harnessing technology and innovation - G20 SME Workshop Riyadh, March 11, 2014 Douglas Pearce 1 SME FINANCE CONSTRAINTS AND RESPONSES 2 INNOVATIVE APPROACHES CAN EASE CONSTRAINTS 3

Electronic Finance: A New Approach to Financial Sector Development?

Geneva, Palais des Nations, 22-24 October 2001 UNCTAD Expert Meeting Electronic Finance: A New Approach to Financial Sector Development? Stijn Claessens (University of Amsterdam), Thomas Glaessner (World

Geneva, Palais des Nations, 22-24 October 2001 UNCTAD Expert Meeting Electronic Finance: A New Approach to Financial Sector Development? Stijn Claessens (University of Amsterdam), Thomas Glaessner (World

Secured Transactions Reform in China. August 2015

Secured Transactions Reform in China August 2015 Reform 2 Secured Transactions Reform ~ 2003 ~ 2007 ~ 2015 Before the Reform Only 4% of outstanding loans were fully secured by movables (PBOC/IFC) Restrictive

Secured Transactions Reform in China August 2015 Reform 2 Secured Transactions Reform ~ 2003 ~ 2007 ~ 2015 Before the Reform Only 4% of outstanding loans were fully secured by movables (PBOC/IFC) Restrictive

Liberia Leasing Investment Forum

Liberia Leasing Investment Forum Finance Leasing in Liberia: June 13-14, 2012 Monrovia, Liberia Leasing is both a source of affordable capital for small and medium-sized businesses and a catalyst for socio-economic

Liberia Leasing Investment Forum Finance Leasing in Liberia: June 13-14, 2012 Monrovia, Liberia Leasing is both a source of affordable capital for small and medium-sized businesses and a catalyst for socio-economic

How To Invest In A Farm Business

Impact Investment AFI Summit Discussion August 18, 2015 Catalyzing Investments Over Time Impact Investing S SCALE OF OUTREACH c a l e Institution Building Governance Project-based TA SUSTAINABILITY Why

Impact Investment AFI Summit Discussion August 18, 2015 Catalyzing Investments Over Time Impact Investing S SCALE OF OUTREACH c a l e Institution Building Governance Project-based TA SUSTAINABILITY Why

Export Import Bank Financing Programs

Export Import Bank Financing Programs The Export Import Bank of the United States (Ex Im Bank) is the official export credit agency of the United States. Ex Im Bank assists in financing the export of U.S.

Export Import Bank Financing Programs The Export Import Bank of the United States (Ex Im Bank) is the official export credit agency of the United States. Ex Im Bank assists in financing the export of U.S.

Working capital: Keep the ball rolling

Working capital: Keep the ball rolling Author : Michael Byrne Date : March 9, 2011 Working capital is considered the life line of any company, allowing the company to grow, expand operations, and weather

Working capital: Keep the ball rolling Author : Michael Byrne Date : March 9, 2011 Working capital is considered the life line of any company, allowing the company to grow, expand operations, and weather

THE MULTILATERAL INVESTMENT FUND DEPLOYING VALUE CHAINS FOR DEVELOPMENT. Nancy Lee General Manager MULTILATERAL INVESTMENT FUND

THE MULTILATERAL INVESTMENT FUND DEPLOYING VALUE CHAINS FOR DEVELOPMENT Nancy Lee General Manager MULTILATERAL INVESTMENT FUND 2. TABLE OF CONTENTS Introduction to the Multilateral Investment Fund Evolution

THE MULTILATERAL INVESTMENT FUND DEPLOYING VALUE CHAINS FOR DEVELOPMENT Nancy Lee General Manager MULTILATERAL INVESTMENT FUND 2. TABLE OF CONTENTS Introduction to the Multilateral Investment Fund Evolution

Loan guarantee funds. Inclusive rural financial services. Introduction

Loan guarantee funds Inclusive rural financial services Introduction For more than seven decades, loan guarantee funds (LGFs) have been used extensively internationally in different market segments and

Loan guarantee funds Inclusive rural financial services Introduction For more than seven decades, loan guarantee funds (LGFs) have been used extensively internationally in different market segments and

ISO20022 Trade Services Dashboard Description of business processes. ISO20022 - Trade Services Description of Business Processes

ISO20022 Trade Services Dashboard Description of business processes 1 Trade Services Description of Procurement: Sub-Functions Tendering Ordering Delivering Invoicing Process for buyer to contact potential

ISO20022 Trade Services Dashboard Description of business processes 1 Trade Services Description of Procurement: Sub-Functions Tendering Ordering Delivering Invoicing Process for buyer to contact potential

micronote #23 Leasing: A Potential Solution for SME Expansion and Rural Financial Sector Deepening

micronote #23 Leasing: A Potential Solution for SME Expansion and Rural Financial Sector Deepening A Case Study of Russia An animal fodder production company leases equipment (photo above) outside Krasnodar,

micronote #23 Leasing: A Potential Solution for SME Expansion and Rural Financial Sector Deepening A Case Study of Russia An animal fodder production company leases equipment (photo above) outside Krasnodar,

Financial Instruments: Recognition and Measurement

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 39 Financial Instruments: Recognition and Measurement This version of the Statutory Board Financial Reporting Standard does not include amendments that

STATUTORY BOARD FINANCIAL REPORTING STANDARD SB-FRS 39 Financial Instruments: Recognition and Measurement This version of the Statutory Board Financial Reporting Standard does not include amendments that

Non-Bank Debt Finance providers operating in Ireland

Non-Bank Debt Finance providers operating in Ireland Presented by: Tom Early Enterprise Ireland Date: Tuesday 10 th February 2015 Understand the Banks Perspective Banks are concerned with REPAYMENT CAPACITY

Non-Bank Debt Finance providers operating in Ireland Presented by: Tom Early Enterprise Ireland Date: Tuesday 10 th February 2015 Understand the Banks Perspective Banks are concerned with REPAYMENT CAPACITY

CORPORATE MEMBERS OF LIMITED LIABILITY PARTNERSHIPS

1. INTRODUCTION CORPORATE MEMBERS OF LIMITED LIABILITY PARTNERSHIPS 1.1 This note, prepared on behalf of the Company Law Committee of the City of London Law Society ( CLLS ), relates to BIS request for

1. INTRODUCTION CORPORATE MEMBERS OF LIMITED LIABILITY PARTNERSHIPS 1.1 This note, prepared on behalf of the Company Law Committee of the City of London Law Society ( CLLS ), relates to BIS request for